Testing macroecological theories in cryptocurrency market: neutral models can not describe diversity patterns and their variation

Abstract

We develop an analysis of the cryptocurrency market borrowing methods and concepts from ecology. This approach makes it possible to identify specific diversity patterns and their variation, in close analogy with ecological systems, and to characterize the cryptocurrency market in an effective way. At the same time, it shows how non-biological systems can have an important role in contrasting different ecological theories and in testing the use of neutral models. The study of the cryptocurrencies abundance distribution and the evolution of the community structure strongly indicates that these statistical patterns are not consistent with neutrality. In particular, the necessity to increase the temporal change in community composition when the number of cryptocurrencies grows, suggests that their interactions are not necessarily weak. The analysis of the intraspecific and interspecific interdependency supports this fact and demonstrates the presence of a market sector influenced by mutualistic relations. These latest findings challenge the hypothesis of weakly interacting symmetric species, the postulate at the heart of neutral models.

1 Introduction

Since the appearance of Bitcoin, the first peer-to-peer digital currency, introduced by a paper authored under the pseudonym of Satoshi Nakamoto in 2008 [1], the cryptocurrency market has known a spectacular growth in terms of capitalization and the number of different cryptocurrencies. This success arouses economists’ interest, engaged in exploring if these digital currencies could perform all the three functions of money (medium of exchange, unit of account, and store of value) [2] and worried about the effects that this trend could produce on traditional monetary or governmental authorities.

As most cryptocurrencies are used more like a portfolio speculative asset than as a currency,

they attracted the attention of traders and institutional investors.

This trend has been reflected in academic studies, that generally have focused

on Bitcoin and its price dynamics [3, 4, 5].

More recently, some studies have

tried to describe the overall market [6], looking at the dynamics

of all the cryptocurrencies actively traded [7, 8].

Among these last works, El Bahrawy et al. [7]

introduced an interesting perspective

looking at the cryptocurrencies market as an ecological system.

Based on this frame of mind, they described several typical distributions. The use of this parallelism is not new and follows a stream of works

where non-biological [9, 10], synthetic systems [11, 12, 13]

or artificial-life type simulations [14] have been described in terms of ecological systems and

used for testing ecological and evolutive theories.

In this work, we will focus on these aspects, developing an in-depth analysis

of the cryptocurrencies market either

for describing some of its fundamental aspects

or for comparing and evaluating

ecological models.

In the last two decades, two contrasting ecological theories generated an important debate around the principal mechanisms that shape ecological communities. Niche theories [15, 16] state that the most relevant factors that determine communities are defined by the selection produced by the interactions among the individuals, the species, and the environment. In contrast, neutral theories [17, 18] consider that the dominant factors are the stochastic processes present in populations dynamics, which determine their random drift.

In its more successful implementation, the neutral theory of biodiversity models the organisms of a community with identical per-capita birth, death, immigration and speciation rates [17]. There are no differences among the species, which are considered demographically and ecologically identical. These hypotheses imply, from a theoretical perspective, the assumption of functional equivalence: on the same trophic level species are characterized by identical rates of vital events. From a model perspective, they lead to the symmetry postulate: the dynamics of the community is not influenced by interchanging the species labels of individuals [19].

In this work we will consider only neutral models which describe populations at the level of individuals, not of species, allowing the direct estimation of species abundances. Among these models, we consider very general Markovian models, usually described through a master equation [18] or a Langevin equation [29]. These approaches generate predictions at stationarity. For this reason, we will focus our attention on data that can be considered closed to stationarity.

These ecologically neutral models generate statistical neutral distributions of different macroecological patterns. In general, to test these theories with empirical data it is determined, using a statistical selection, if such distributions are compatible with the empirical ones. Strictly speaking, this statistical neutrality (the adherence between the model and data distribution) is a necessary but not sufficient condition for claiming neutrality [20]. Even if this is the most pragmatic way for testing neutrality, the analysis of the form of interactions and if species satisfy the assumption of functional equivalence could produce more enlightening and definitive results.

Based on these considerations, the principal aim of our study will be the analysis and characterization of different macroecological patterns converted to the specific case of

the cryptocurrency market.

Furthermore, we will focus our attention on the examination of the interdependence and correlations present among cryptocurrencies.

In the section on Methods, we will present in detail which patterns and how these analyses

can be carried out.

In brief, the construction of an analogy between the cryptocurrency market and ecological system will better elucidate the community structure of the cryptocurrency market shedding light on the existing relationships between cryptocurrencies. Despite its importance, the theoretical description of structure and interactions in markets is limited and new concepts and approaches are required. Ecology is capable of introducing new and powerful ideas, previously debated and tested. In this work, we will describe specific dynamics, determine new stylized facts and patterns and compare them with a testable theory. This analysis will bring new insights and comprehension of the considered market, highlighting important elements which could be useful for assisting in hedging risks. The natural limitation of an analogy-based approach could be overcome in the future by introducing specific features for correcting inaccuracies and building new models.

2 Data

We collected the cryptocurrencies data from the website Coin Market Cap [21], which extracts from the exchange market platforms the price expressed in US dollars (exchange rate), the volume of trading in the preceding 24 h and the market capitalization of the different cryptocurrencies. Market capitalization is the product of the price for the circulating supply, which can not account for dormant or destroyed coins. Traded cryptocurrencies can disappear from the website list to reappear later on. In fact, capitalization of cryptocurrencies not traded in the 6 h preceding the weekly report is not included in the dataset and cryptocurrencies inactive for 7 days are not included in the list. For this reason, we filled these lacunae by introducing the average between the values available at the extremes of each gap. Finally, we cleared the dataset by correcting some mismatches or typos present in the names or symbols of the cryptocurrencies.

We considered weekly data from 28 April 2013 to 2 February 2020, which correspond to a series of 354 time steps. The dataset contains a total of 3588 cryptocurrencies.

3 Methods

To construct the parallelism between ecological systems and the cryptocurrency market we consider that each cryptocurrency represents a species and its capitalization its abundance. In this way, the wealth invested in a cryptocurrency replaces the population size of a species.

The first macroecological pattern that we analyze is the Species Abundance Distribution (SAD), a classical biodiversity descriptor that characterizes static features of ecosystem diversity. This distribution represents the probability that a species presents a given population size. By using a very general stochastic Markovian model for neutral ecological communities, Volkov et al. showed that, at stationarity, the SAD follows an analytic zero-sum multinomial distribution for local communities and, for the metacommunity, the celebrated Fisher’s distribution [18, 22], as already predicted by Hubbell’s neutral model [17]. Note that, as the model is nonspatial the term metacommunity represents a single, permanent large community where migration is absent. In contrast, local communities present dynamics defined by immigration from a permanent source of species (the metacommunity). In this sense, our data must be considered as collected from the metacommunity and, based on the results of Volkov et al., they should be described by a Fisher’s distribution: [23]. A classical alternative to the distribution produced by the neutral theory is the log-normal one: , which is equivalent to a normal distribution if the variable is chosen. This distribution has a long tradition of use in the ecological literature [24] and it is a reasonable and parsimonious null hypothesis for the SAD [25], which can be obtained from pure statistical non-biological arguments, based on the central limit theorem [26], or can be generated by niche or demographic differences among species in population models [27]. To sum up, a description of the SAD with a Fisher’s distribution would support the idea of Neutral dynamics. In contrast, a log-normal distribution would suggest the presence of other types of population dynamics or pure statistical mechanisms.

The second macroecological pattern is the Species Population Relation (SPR).

It describes the scaling of the number of species with the total number of individuals .

When the different

species of a total population follow the Fisher’s

distribution,

the expected number of species for a given population is given by:

[23].

Ecological studies usually measure the relationship between

the number of species and the area sampled, which can be easily obtained assuming

a linear relation between and the area.

An alternative characterization of this relation commonly found in the literature is based on empirical curves showing a power-law behavior, with exponents presenting typical values between 0 and 1 [28].

So far we have focused on static macroecological patterns which can be related to results generated by neutral theories at the steady-state. However, stationarity is just an approximation, and not necessarily a good one, for systems characterized by a state of flux in species, abundance and composition. For this reason, we look at the temporal behavior of our system and characterize time-dependent patterns.

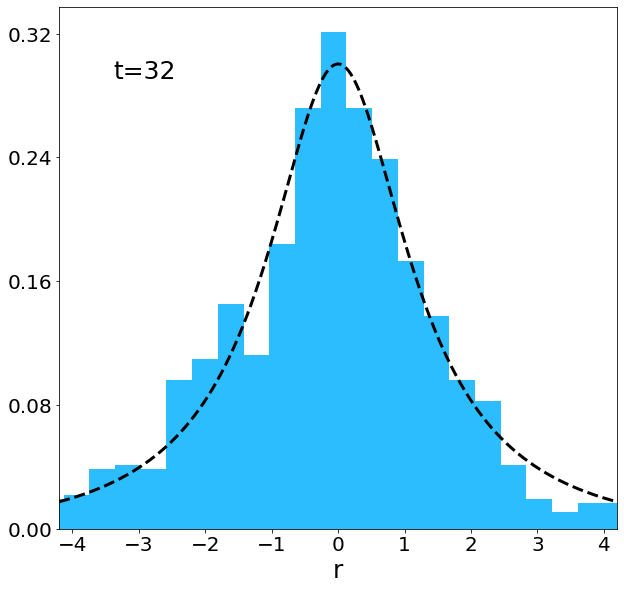

The intertwined history of different species along their evolution generates complex communities characterized by non-trivial structures. New species continuously replace old ones producing an intricate overlap where the turnover can be characterized employing the species turnover distribution (STD). This distribution is defined as the probability that the ratio of the population of a species separated by a time interval , , is equal to . Under stationary conditions, Azaele et al. [29] introduced a neutral model that can forecast the STD. Within this framework, an analytic expression for this distribution is obtained:

| (1) |

where and are parameters and is a renormalization constant equal to .

The community composition of cryptocurrencies presents a coherent structure that evolves over time. This structure can be quantified by analyzing how the capitalization of each coin changes. A variety of different indices has been used in ecology studies for tracking modifications in community composition through a similarity measure [31, 32]. Here, we adopt a simple and well-known one that presents a straightforward interpretation of its values [33]. Given the capitalization of a given species , we consider (1 is added in order to avoid the log of ), where is a given month. Note that the log-transformation is a natural approach for quantities which can be roughly described by a log-normal distribution. The next step is the estimation of the Pearson’s correlation of the log-transformed data: , where the correlation is calculated over the index . This method is well known [34, 33] and easily supports tests of significance: 0 represents complete randomness and is the null hypothesis for significance tests. To conclude, we characterize the mode of the community similarity evolution by looking at the functional form of the temporal decay of , which describes the transformation from perfectly correlated structures towards totally uncorrelated ones.

We compare the results obtained from this empirical analysis of the community composition with the ones generated by a neutral model introduced in [30, 29], which is constituted by a system of stochastic discrete differential equations. The model describes an ecological community with a fixed number of species, where the total number of individuals in the community is set to . In the large population limit, these constraints can be relaxed and similar results are obtained [30]. If represents the population of the i-th species at time , its evolution follows this equation:

| (2) |

The parameter controls the population size near the extinction threshold,

taking into account the total effect of immigration, extinctions and speciations.

and are the mean value and the standard deviation of the distribution

which describes the per capita birth rate.

Based on the principle of neutrality, we assume that and are

the same for all individuals. Finally, is

an uncorrelated Gaussian noise term, with zero mean and unit variance.

By taking the continuum limit, this stochastic discrete model can be approximated by a

Langevin and the associated Fokker-Plank equation.

Its analytical solution shows that, in the limit of large ,

a Gamma distribution describes the SAD for this model.

Such distribution can well describe various experimental SAD data and

approaches the Fisher’s distribution for [30, 29]. These results can be connected with the classical outcomes of the neutral theory

as formulated by Volkov et al. [18] for a particular choice of

the birth and death coefficients.

Our last analysis looks at the characterization of the interdependence among cryptocurrencies. This inspection will help in exploring if in a community of cryptocurrencies the symmetric species postulate is well supported and if interactions between species can be considered weak in relation to stochastic effects, as expected for neutral dynamics. As capitalizations present a growing trend, we do not study directly their correlations. In contrast, we consider the log-variation of the capitalization of a given species : . As a dependence measure, we consider the Pearson’s correlation between the synchronous time evolution of of a pair of cryptocurrencies and : . The interdependencies among the log-variations in the capitalization are addressed looking at the corresponding correlation matrix.

4 Results

4.1 General dynamics

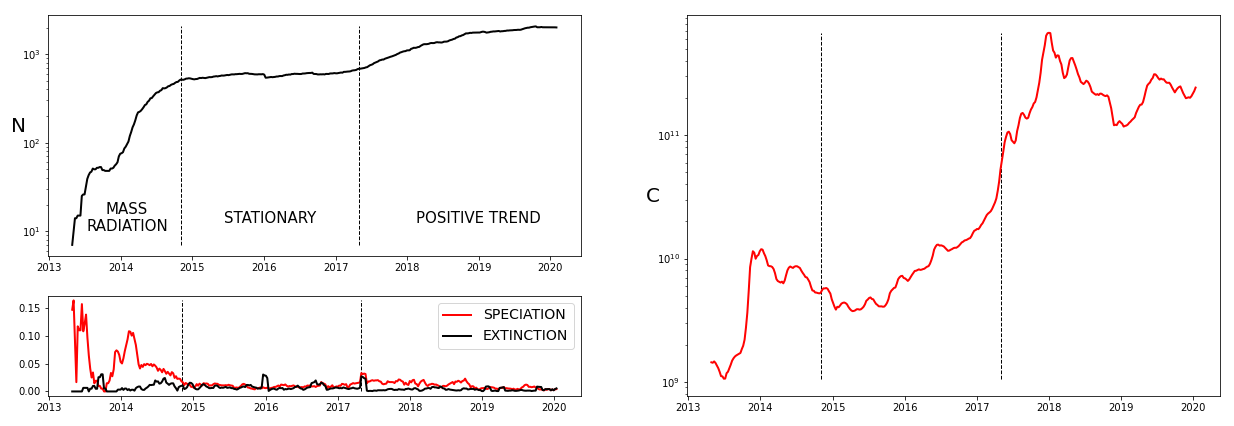

We consider the time series which collect the number of active cryptocurrencies at a given time () and we evaluate the corresponding speciation and extinction rates (see Figure 1), measured as the number of cryptocurrencies entering (respectively, leaving) the market on a given week, normalized over the number of active cryptocurrencies at that time. By looking at the number of active cryptocurrencies and at the speciation and extinction rates, it is possible to qualitatively discriminate between 3 different regimes: before 2014-06-01 a mass radiation phase, characterized by a spectacular increase in the number of cryptocurrencies, caused by a very high number of speciation events. This phase is characterized by significant fluctuations. Between 2014-11-02 and 2017-04-30 we can highlight a stationary phase, with comparable values of speciation and extinction rates. Starting from 2017-05-07, a positive trend characterizes a new regime where the number of cryptocurrencies grows slightly in a gradual and regular fashion. Also, this regime presents higher values of speciation rates in relation to the extinction ones. In general, extinction rates fluctuate around a typical value, except for some sparse and sudden extinction bursts. In contrast, speciation rates present different behaviors which determine the modes of the three considered regimes.

The total market capitalization in general presents important positive trends. In the regime where the number of active cryptocurrencies is stationary, intervals of exponential growth can be detected; in the regime with important radiation of new currencies, stages with super-exponential behaviors can be identified.

4.2 Species Abundance Distribution

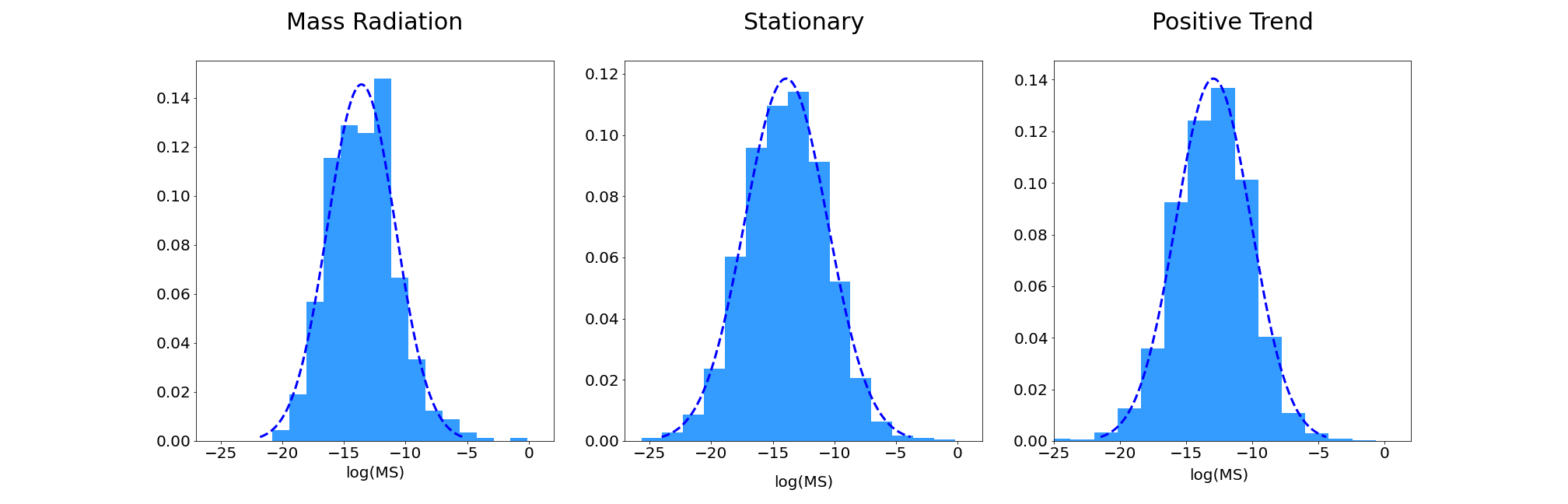

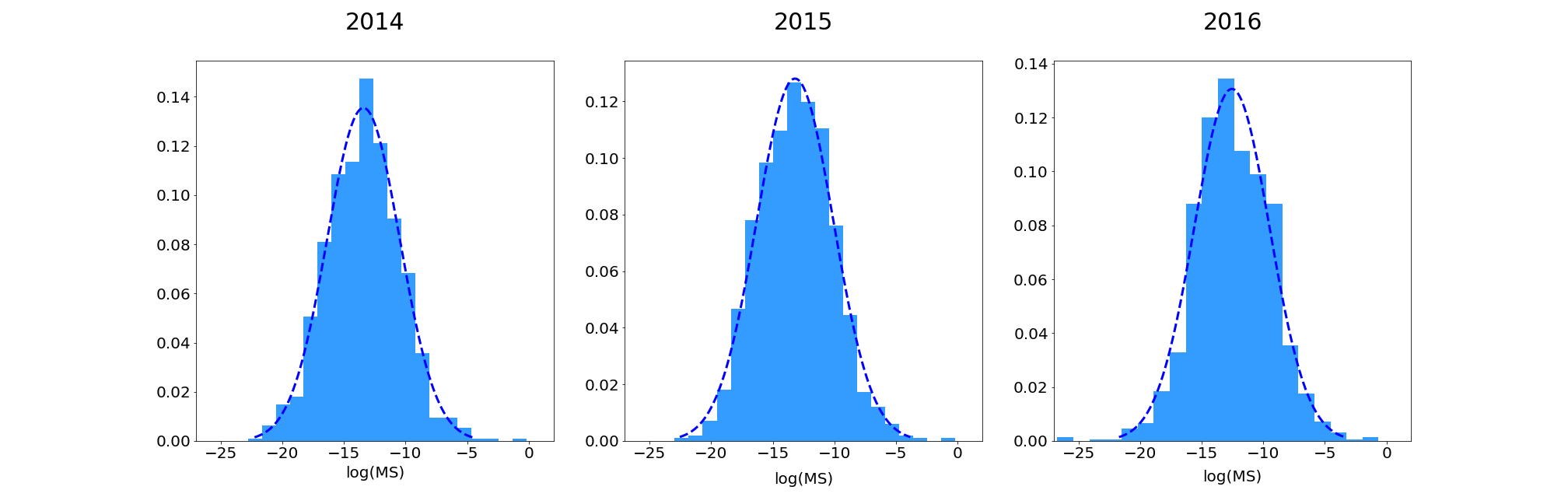

Figure 2 shows the SADs considering different periods and time scales. We present data aggregated along a year or more, considering all the stationary and non-stationary periods. For each cryptocurrency, we measure the corresponding market share for overcoming the problem of the non-stationarity of the capitalization. Comparable results can be obtained for shorter time scales, corresponding to a month or even a week. For testing the neutral theory we must focus on the stationary period, where we can consider the dynamics in the number of active cryptocurrencies as stationary and we can compare the empirical data to the theoretical predictions, which are obtained at stationarity. It is important to note that, in ecology, the situation of incompletely censused regions is frequent. This condition usually produces an under-sampling of rare species. In this situation, it is common to consider to fit only the portion of the distribution which encompasses the most common species. In contrast, in our case, we can consider having access to a fully sampled community, an assumption supported by the regularity of the shape of the left tail of the distribution, which does not suffer from strong statistical fluctuations. Just by looking at the full shape of our distributions, which always present an evident internal mode, we can firmly discard the hypothesis that Fisher’s distribution can give a good description of our dataset. In fact, Fisher’s distribution is monotonic and does not present internal modes. In contrast, we can perform a high-quality fitting using the log-normal distribution. In particular, by using a Kolmogorov-Smirnov test of our observations against the fitted log-normal distributions, we cannot reject the hypothesis that the data come from the fitted distribution since p-values are very high in all the considered cases (see Fig. 2).

4.3 Species Population Relation

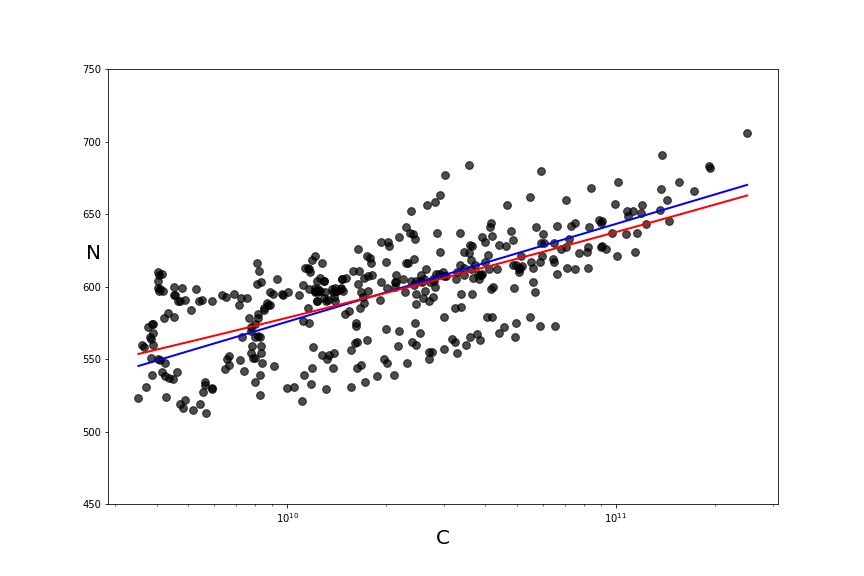

For studying the SPR, we analyze the stationary period and scan the corresponding dataset with different temporal intervals. We consider intervals between 1 and 10 weeks and, for each sample, we measure the value of capitalization and number of species. We plot the pairs of all these values in Figure 3, where we represent the fitting obtained by using the relation compared with a power-law. The dependence of on is very weak and it is not possible to affirm if the logarithmic or the power-law function better describes the data points.

4.4 Evolution of the Community Structure

We estimate the species turnover distribution using the cryptocurrencies

market share. We consider coins with located in the stationary period.

The fittings of the STD with the analytic expression of equation 1 present contrasting results, as can be appreciated in Figure 4.

For some values of the fitting is satisfactory, for others there is a small but systematic difference between fitted and empirical distributions. Empirical data present an asymmetry between left and right tails, with a greater propensity of developing negative values, which correspond to decreasing populations. The parameters obtained from the fitting of the STD

can be used to produce the SAD generated by the neutral model of [30, 29].

The fitted values of B () lead to SADs presenting a shape

far from the expected for neutral models describing a single community without migration.

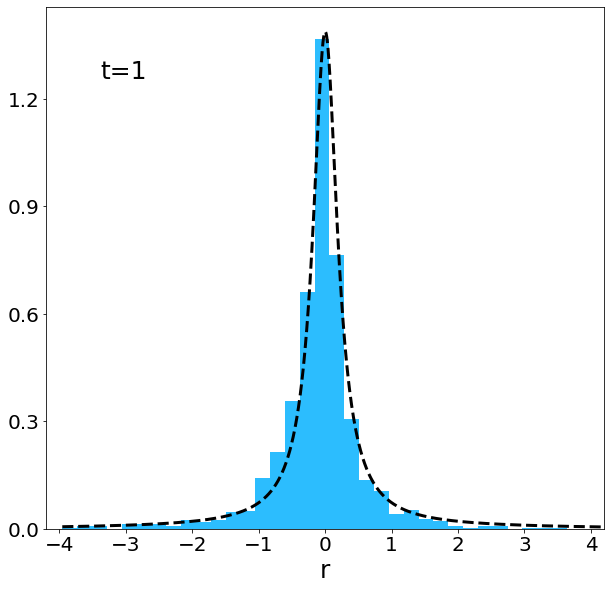

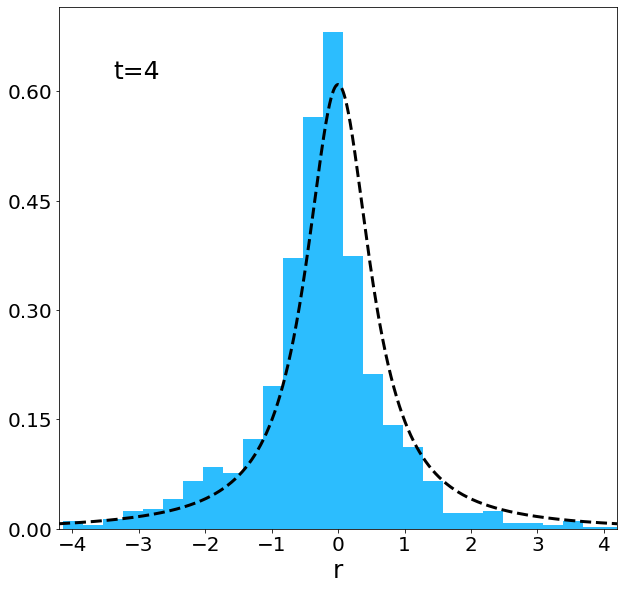

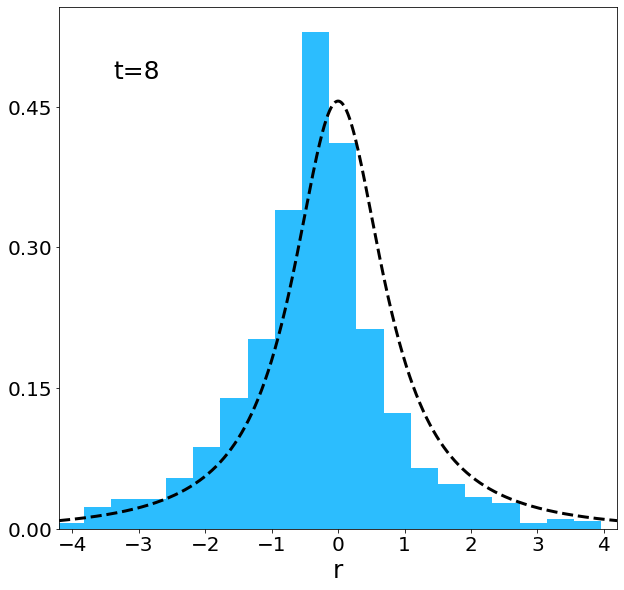

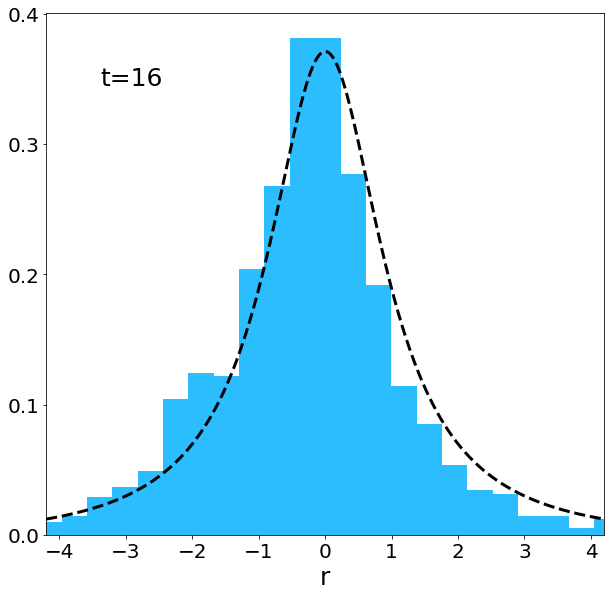

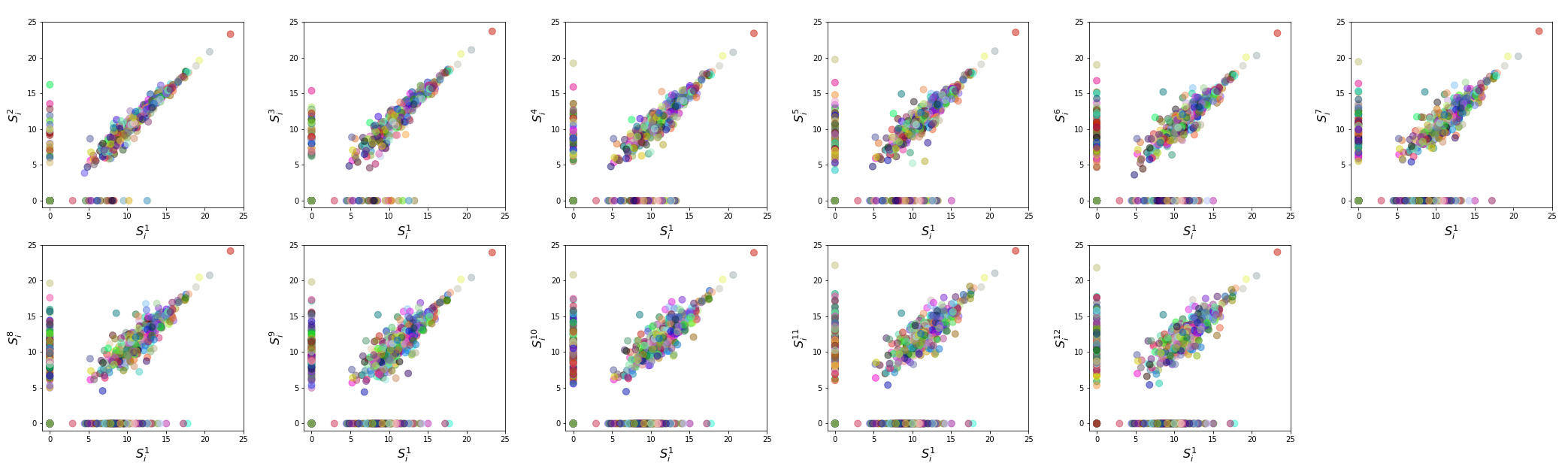

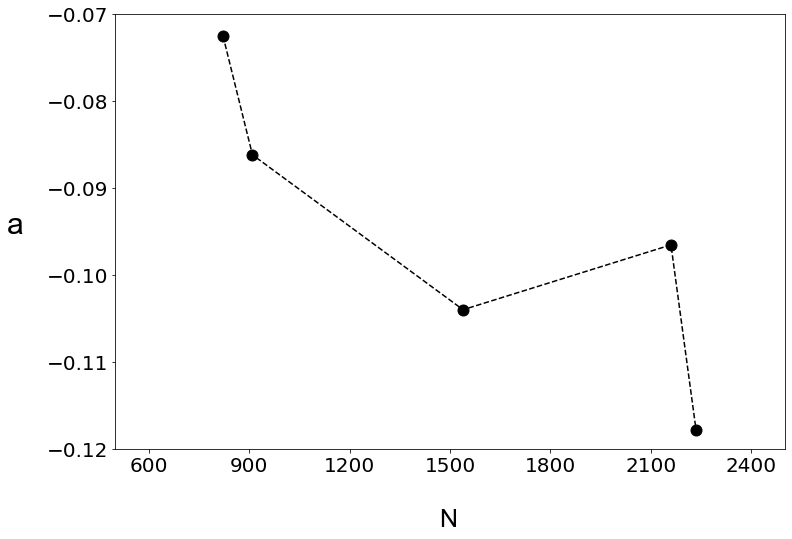

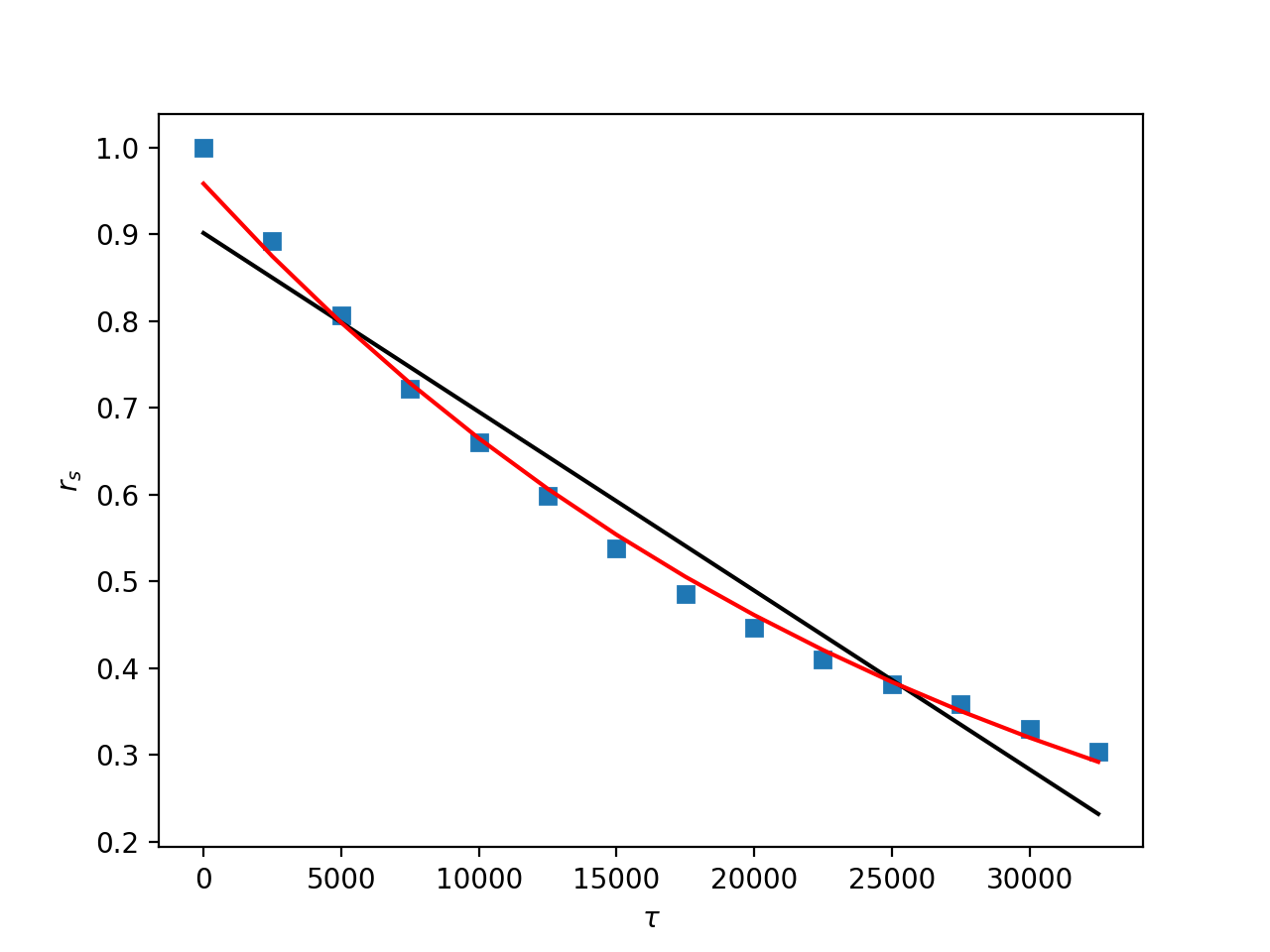

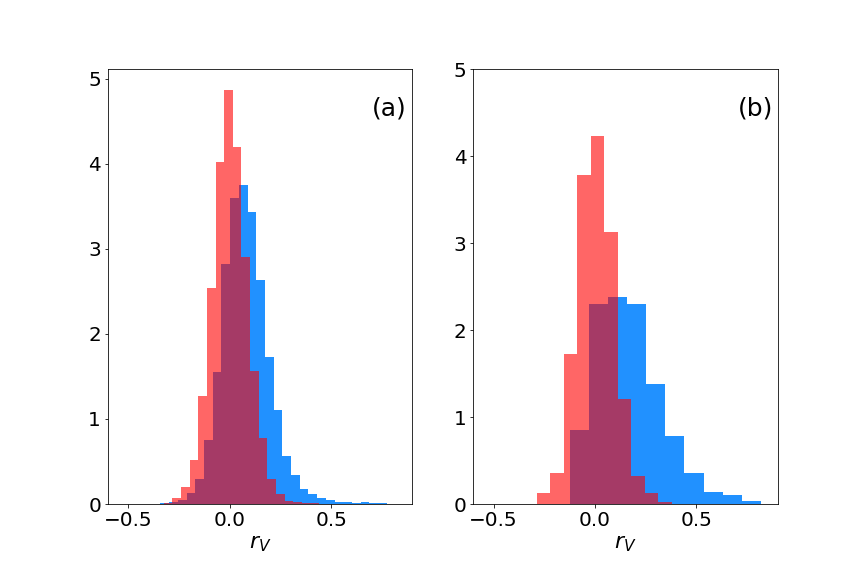

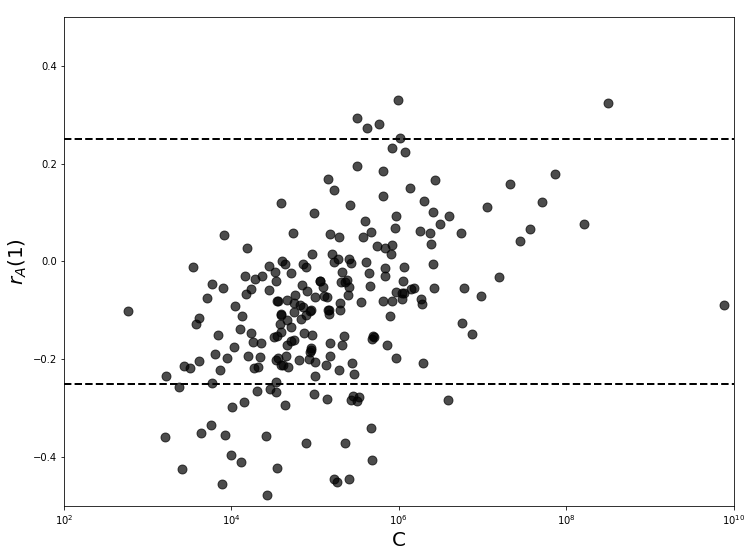

Figure 5 shows an example of the scattering plot of the log-abundances in the initial community versus abundances at the following specified time. For these different plots we evaluated the correlations and we examined their evolution along one year. We perform this analysis for all our data. In the period of mass radiation, we can observe an exponential behavior. In contrast, as the community enters the stationary regime, the decreases with time following a clear linear behavior and this mode is maintained until the end of our time series. The slope values of the linear fittings () decrease along the considered years. These slope values are an interesting parameter for quantifying what ecologists call temporal -diversity [32], which characterizes the change in the composition of a single community through time. More negative values represent a more intense variation in the community structure, which corresponds to a stronger temporal -diversity. In this framework, the relation between temporal -diversity, which characterizes the temporal variation of species in a single community, and temporal -diversity is particularly interesting. In Figure 6 we can appreciate a general trend of increasing temporal -diversity with increasing -diversity. -diversity is estimated using a simple count of the number of species (species richness) in the considered interval.

In addition, we analyze if a clear relationship exists between the abundance of the population of a given species and its lifetime. We estimated the abundance considering the mean value of the capitalization of a species estimated over its time series. The lifetime is obtained by measuring the occurrence of the fraction of weeks in which a cryptocurrency is active over all the considered weeks. By looking at the scattering plot of these quantities (Figure 6), we can see that cryptocurrencies with a capitalization smaller than present a reduced lifespan, with occurrences that hardly reach 0.5. However, we can perceive that these quantities display an unexpected rather weak dependence.

We conclude this analysis by comparing the behavior displayed during the stationary period with the outcome of the neutral model presented in equation 2. Simulations are run for a number of generations that allows reaching values close to the smallest one displayed by real data. We fix the number of species considering the mean number of species appearing in the dataset during the chosen periods and we select the ratio among values that are small enough for generating distributions close to the Fisher’s one. This purpose is reached by fixing and varying .

We collect the species abundances and take into account the extinction/speciation events. These events are calculated when the term crosses a zero value. From these artificial data, we can obtain the values. We run a large amount of simulations for different values of , and for . For this range of parameters values, the model generates only exponential decays. Figure 7 shows a typical example for specific parameters.

4.5 Correlations

We studied the sub-set of 225 cryptocurrencies that are active during the entire stationary period. The correlation matrix for pairs of cryptocurrencies is reported in Fig. 8. A qualitative observation of the correlation values shows a clear deviation from the values of the randomized sample and the matrix presents a clear structure. For the cryptocurrencies with higher capitalization, correlations have larger values, which are statistically significant and positive. This result can be clearly appreciated by looking at the behavior of the largest 25 cryptocurrencies.

Finally, we look at the temporal autocorrelation for a single cryptocurrency: . We focus on , as for autocorrelation values are in general indistinguishable from the ones of a random series. As shown in Figure 8, there is a clear dependence of on the capitalization of the considered cryptocurrencies. For smaller capitalizations, some cryptocurrencies present a significant anticorrelation, for larger capitalizations only a few cryptocurrencies show a significant, but small, positive correlation. In particular, among the largest 25 currencies only two present significant correlation values.

5 Discussion

The shape of the SADs lends strong support to alternatives to the neutral theory. In fact, neutral models without migration, which describe the distribution at the metacommunity scale, predict a Fisher’s distribution. In contrast, tests of fit quality show that the log-normal approximates the observed species abundance data very well. This means that looking at the log-scale, the SAD shows a strong central tendency and relatively few rare or abundant species. In contrast, neutral dynamics would generate more rare species and truly dominant ones would be improbable.

The analysis of the SPR gives no definitive answers that would allow the selection of one of the two alternative models. In fact, a dependence between species and population exists, but it is very weak and it is not possible to distinguish between a logarithmic or a power-law dependence.

The STD fitting with the distribution generated by a neutral model

does not allow a straightforward interpretation.

Even if the fitting, for some values of , is promising, we must

stress that the same distribution fits equally well turnover data

generated by very different community populations, corresponding to

distinct SADs, which can

describe situations with or without central modes.

For this reason, it is important to look at what SAD is produced by

a given STD fitting. In our case, the STD fittings generate

SADs presenting a shape far from the expected for neutral models

describing a single community without migration.

For this reason, we think that this result is not supporting the neutral theory.

This specific example shows how curve-fitting is a valuable approach

to test a model, but it is not necessarily conclusive. In particular, this is the case when the fitting distributions are flexible enough for

describing very different situations.

The evolution of the community structure correlations shows a very interesting mode. In fact, after the radiation phase, it displays a characteristic linear decay. Neutral models describing a single community without migration can not generate this linear behavior. The absence of an exponential behavior suggests that the dynamics of the change in the community structure is very far from being random, with a quite slow drift in the relative abundances of moderately abundant species. The system is apparently endowed with a mechanism, not present in the neutral model, which allows relative rare and moderately abundant coins to persist over time. This conjecture is supported by the performance of the cryptocurrencies persistence in relation to their abundance: only very rare coins effectively go systematically extinct. Persistence and abundance display a weak dependence and, in contrast with the results of neutral models (see [29]), it is not evident that the less abundant species are clearly more prone to extinction.

The relation of the pace of change in the community structure with its species richness shows how the presence of more cryptocurrencies tends to accelerate the reorganization of the composition of the community over time. If a considerable amount of new species enter the system, the market must accommodate via a faster temporal reorganization which can generate a finer temporal subdivision of the wealth injected in the market. The fact that an increase in -diversity has a direct effect on temporal -diversity, may suggest that interspecific competition among cryptocurrencies is not so weak.

These original results demonstrate the particular advantage of

using non-biological data for testing and improving

ecological theories and methodologies in the quantification

of temporal behaviors, where ecological datasets are generally scarce or must rely on fragmented paleontological data.

The analysis of the correlation matrix for pairs of cryptocurrencies quantifies the dependence of the increase/decrease of a species on the increase/decrease of a species . Results clearly show the presence of a group of coins, included among the higher capitalized cryptocurrencies, presenting a cohesive response in the variation of their capitalization. This important result shows a coherent behavior in a sector of the market. The positive and statistical relevant correlations suggest the presence of mutualism: cryptocurrencies that belong to this sector benefit from an increase in the capitalization of the other cryptocurrencies which belong to the same sector. This effect can be determined either by endogenous factors either by the eventual contribution of exogenous common cause drivers. We can distinguish between two classes of cryptocurrencies: a minor one where the variation of the capitalization presents clear positive correlations, and a larger one, where this variation is uncorrelated. At the considered time scale, there is no switch between these classes and we can label species as belonging or not to a given class. Cryptocurrencies are not symmetric in relation to this behavior and the symmetric species postulate seems not to be satisfied, implying that the system is not neutral. In neutral models, common species are treated simply as rare species, but here the behavior of the correlations suggests that different mechanisms are shaping these two classes of cryptocurrencies and should be taken into account. Coins with larger capitalization can not be treated simply as rare coins writ large [35]. We remember that, in ecologically neutral models, the correlation in the abundances of a pair of species is the same as the correlation in the abundances of any other pair of species [20]. Thus, a distribution with equal correlation coefficients can stand in as a proxy for measuring statistical neutrality. A similar role can be assumed by the correlations between pairs of .

Finally, we can shed a light on the relevance of the interactions between species,

and if they are effectively weak compared to the stochastic drivers of the dynamics,

by contrasting the values of the correlation among pairs of cryptocurrencies with the autocorrelation

of each cryptocurrency.

The pair correlations can be seen as a proxy for between-species interdependency (interspecific) and the autocorrelations as a within-species temporal interdependency (intraspecific).

We can note how for the largest capitalizations, when the interspecific correlations are relevant and positive, the intraspecific ones are generally much smaller and statistically not significant.

In this case, interspecific correlations are not weak in comparison with intraspecific ones

and could be generated by some constraints on the community dynamics

not generated by neutral dynamics.

To sum up, we have developed an analysis of the cryptocurrency market borrowing methods and concepts from ecology. This approach allows for identifying specific diversity patterns and their variation, in close analogy with ecological systems, and to describe them effectively. At the same time, we can contrast different ecological theories, testing the validity of using neutral models. The behavior of the SAD and the evolution of the community structure strongly suggest that these statistical patterns are not consistent with neutrality. In particular, the necessity to increase the community composition change when species richness increases suggests that the interactions among cryptocurrencies are not necessarily weak. This fact is supported by the analysis of intraspecific and interspecific interdependency, which also demonstrates that a market sector influenced by mutualistic relations can be outlined. All these outcomes challenge the hypothesis of weakly interacting symmetric species.

Our results show that the community structure of the cryptocurrency market can be effectively described by using an ecological perspective. Our analysis, besides static distributions, highlights specific patterns of a rich temporal dynamics. These data were compared directly with neutral models. Even if falsified, these models offer a reference point for parsimonious description, acting as a useful null model. Our study introduces interesting new strategies for describing dynamical patterns that are novel even for ecological studies. The accessibility to the whole data set of the cryptocurrency market, without limitations derived from sampling, makes possible the exploration of these tools. For these reasons, these results have an interesting impact either in the characterization of the cryptocurrency market, either on the relevance that non-biological systems can have in testing ecological theories. Finally, the new set of empirical regularities and general tendencies displayed by the cryptocurrencies market could introduce interesting elements of exploration for the exciting and emerging field of market ecology [36, 37].

Acknowledgments

EAAM received partial financial support from the PIBIC program of Universidade Federal do Rio de Janeiro. We thank Prof. Marcus Vinícius Vieira, from the Graduate Program in Ecology - UFRJ, for useful comments and suggestions and Prof. Jorge Simões de Sá Martins for revising the manuscript.

References

References

- [1] S. Nakamoto, Bitcoin: A Peer-to-Peer Electronic Cash System. (2009). https://bitcoin.org/ bitcoin.pdf

- [2] S. Ammous, Can cryptocurrencies fulfill the functions of money? Q. Rev. Econ. Finance, 70, 38 (2018).

- [3] A. Urquhart, The inefficiency of Bitcoin. Econ. Lett. 148, 80 (2016).

- [4] V. Dimitrova, M. Fernández-Martínez, M.A. Sánchez-Granero, J.E. Trinidad Segovia, Some comments on Bitcoin market (in)efficiency. Plos One 14, e0219243 (2019).

- [5] De Sousa Filho F. N. M., Silva J. N., Bertella M. A., Brigatti E. The Leverage Effect and Other Stylized Facts Displayed by Bitcoin Returns. Braz. J. Phys., 51, 576 (2021).

- [6] S. Drożdż et al. Competition of noise and collectivity in global cryptocurrency trading: Route to a self-contained market. Chaos, 30, 023122 (2020).

- [7] El Bahrawy A et al. Evolutionary dynamics of the cryptocurrency market. R. Soc. open sci. 4, 170623 (2017).

- [8] Wu K, Wheatley S, Sornette D. Classification of cryptocurrency coins and tokens by the dynamics of their market capitalizations. R. Soc. open sci. 5, 180381 (2018).

- [9] Gaston, K. J. et al. Comparing animals and automobiles: a vehicle for understanding body size and abundance relationships in species assemblages? Oikos 66, 172 (1993).

- [10] Blonder, B. et al. Separating macroecological pattern and process: comparing ecological, economic, and geological systems. PLoS One 9, e112850 (2014).

- [11] P. Keil et al. Macroecological and macroevolutionary patterns emerge in the universe of GNU/Linux operating systems. Ecography 41, 1788 (2018).

- [12] Valverde, S. and Sole, R. V. Punctuated equilibrium in the large-scale evolution of programming languages. J. R. Soc. Interface 12, 20150249 (2015).

- [13] A. Buchanan, N.H. Packard, and M.A. Bedau. Measuring the Drivers of Technological Innovation in the Patent Record. Artificial Life 17, 109 (2011).

- [14] S.S. Chow, C.O. Wilke, C. Ofria, R.E. Lenski, C. Adami, Adaptive radiation from resource competition in digital organisms. Science 305, 84 (2004).

- [15] Grinnell, J. The niche-relationships of the California Thrasher. The Auk, 34, 427 (1917).

- [16] MacArthur, R. H. On the relative abundance of bird species. Proc. Natl. Acad. Sci. USA 43, 293 (1957).

- [17] S. P. Hubbell, The Unified Neutral Theory of Biodiversity and Biogeography (MPB-32), Princeton Univ. Press, (2001).

- [18] Volkov, I., J. R. Banavar, S. P. Hubbell, and A. Maritan. Neutral theory and relative species abundance in ecology. Nature 424, 1035 (2003).

- [19] C. Borile et al. Spontaneously Broken Neutral Symmetry in an Ecological System. Phys. Rev. Lett. 109, 038102 (2012).

- [20] Fisher C. K., Mehta P. Niche-to-neutral transition in ecology Proceedings of the National Academy of Sciences. 111, 13111 (2014).

- [21] Total Market Capitalization. https://coinmarketcap.com/all/views/all/.

- [22] B. J. McGill, B.A. Maurer, M.D. Weiser Empirical evaluation of neutral theory. Ecology, 87, 1411 (2006).

- [23] R. A. Fisher, A. S. Corbet, C. B. Williams, The relation between the number of species and the number of individuals in a random sample of an animal population. J. Anim. Ecol. 12, 42 (1943).

- [24] Preston, F. W., The Commonness, And Rarity, of Species. Ecology 29, 254 (1948).

- [25] B.J. McGill, A test of the unified neutral theory of biodiversity. Nature, 422, 881 (2003).

- [26] May, R. M. in Ecology and Evolution of Communities (eds Cody, M. L. & Diamond, J. M.) pg.81-120 Belknap, Harvard Univ. Press, Cambridge, Massachusetts, (1975).

- [27] S.R. Connolly et al., Commonness and rarity in the marine biosphere. Proceedings of the National Academy of Sciences, 111, 8524 (2014).

- [28] Sandro Azaele, Samir Suweis, Jacopo Grilli, Igor Volkov, Jayanth R. Banavar, and Amos Maritan, Statistical mechanics of ecological systems: Neutral theory and beyond. Rev. Mod. Phys. 88, 035003 (2016).

- [29] Azaele S., Pigolotti S., Banavar J. and Maritan A. Dynamical evolution of ecosystems. Nature 444, 926 (2006).

- [30] S. Pigolotti, A. Flammini, A. Maritan, Stochastic model for the species abundance problem in an ecological community. Phys. Rev. E 70, 011916 (2004).

- [31] M. Dornelas, N. J. Gotelli, B. McGill, H. Shimadzu, F. Moyes, C. Sievers, A. E. Magurran, Assemblage Time Series Reveal Biodiversity Change but Not Systematic Loss. Science 344, 296 (2014).

- [32] Magurran AE, Dornelas M, Moyes F, Henderson PA. Temporal diversity - A macroecological perspective. Global Ecol Biogeogr. 28, 1949 (2019).

- [33] B.J. McGill, E. A. Hadly, B. A. Maurer, Community inertia of Quaternary small mammal assemblages in North America. Proceedings of the National Academy of Sciences, 102, 16701 (2005).

- [34] Engen, S., Lande, R., Walla, T., DeVries, P. J., Analyzing spatial structure of communities using the two-dimensional poisson lognormal species abundance model. Am. Nat. 160, 60 (2002).

- [35] K.J. Gaston, Common Ecology, BioScience, 61, 354 (2011).

- [36] J. D. Farmer, Market force, ecology and evolution. Ind. Corp. Change, 11, 895 (2002).

- [37] M. P. Scholl, A. Calinescu, J. D. Farmer, How market ecology explains market malfunction. Proceedings of the National Academy of Sciences, 118, e2015574118 (2021).