Noise inference for ergodic Lévy driven SDE

Abstract.

We study inference for the driving Lévy noise of an ergodic stochastic differential equation (SDE) model, when the process is observed at high-frequency and long time and when the drift and scale coefficients contain finite-dimensional unknown parameters. By making use of the Gaussian quasi-likelihood function for the coefficients, we derive a stochastic expansion for functionals of the unit-time residuals, which clarifies some quantitative effect of plugging in the estimators of the coefficients, thereby enabling us to take several inference procedures for the driving-noise characteristics into account. We also present new classes and methods available in YUIMA for the simulation and the estimation of a Lévy SDE model. We highlight the flexibility of these new advances in YUIMA using simulated and real data.

1. Introduction

We consider the following univariate Markovian stochastic differential equation (SDE):

| (1) |

where:

-

•

The coefficients and are smooth enough with being non-degenerate, and known except for an unknown parameter

for bounded convex domains and ();

-

•

The driving noise is a standardized non-Gaussian Lévy process with finite moments, whose distribution depends on an unknown parameter , a domain in , and where is independent of .

We write in the sequel. We suppose that there are true values and which induce the true image measure of , and that we observe a discrete-time sample , where , with the sampling stepsize satisfying that

| (2) |

the so-called rapidly increasing experimental design.

Our objective is to estimate the value under the ergodicity. We remark the parameter may not completely characterize the distribution , so that the problem is not necessarily parametric; for example, is just a skewness or kurtosis, which may or may not completely determine .

For the estimation of the coefficient parameter , from the statistical point of view it is important what kind of distributional is used to approximate the conditional distribution of given . Previously, [12] and [18] considered estimation of based on the Gaussian quasi-likelihood (GQL), and proved the asymptotic normality and the tail probability estimates of the Gaussian quasi-maximum likelihood estimator (GQMLE). At the expense of efficiency, the GQL based method has the robustness against misspecification of the driving-noise distribution, which may be crucial in the context of time-series models, see [17, Section 6.2]. Further, concerned with estimation of a Lévy-measure functional of the form , with denoting the Lévy measure of , the previous study [13] proposed a moment-matching based estimator and proved its asymptotic normality at rate . However, the procedure imposed some stringent conditions on the behavior of around the origin [13, Assumption 2.7], and was not quite suitable if we want to estimate directly; in general, estimation of the distribution and that of the corresponding Lévy measure can be of technically rather different matters.

In this paper, we will propose yet another strategy for estimating based on the unit-time approximation, which goes as follows:

-

(1)

First we construct the GQMLE and the residual

(3) -

(2)

We then estimate the -i.i.d. sequence ()

by adding up the finer increments over the th unit-time interval :

(4) where, for each ,

and then measure the discrepancy between a functional of and that of through a stochastic expansion.

-

(3)

For an appropriate function , we estimate by

The rest of this paper is organized as follows. We briefly summarize some prerequisites in Section 2, and then presents theoretical results in Section 3. Section 4 introduces new classes and methods in YUIMA R package ([2] and [7]) for the estimation procedure proposed in the previous sections. Some numerical examples based on simulated and real data are given in Section 5.

2. Preliminaries

2.1. Notations and conventions

Here are some basic notations and conventions used in this paper.

-

•

For any vector variable , we write .

-

•

denotes a universal positive constant which may vary at each appearance.

-

•

stands for the transpose operator, and for any matrix .

-

•

For a matrix and vector , we will write . In particular, when , it stands for the dot product of two vectors. We will also write for two square matrices and of the same order.

-

•

The convergences in probability and in distribution are denoted by and , respectively, and all limits appearing below are taken for unless otherwise mentioned.

-

•

For two nonnegative real sequences and , we write if .

-

•

For any , denotes the maximum integer which does not exceed .

-

•

Given a function and a signed measure on a one-dimensional Borel space, we write

2.2. Basic assumptions

Denote by the underlying complete filtered probability space; every processes are adapted to the filtration . We will write for the expectation operator associated with .

Assumption 2.1.

The Lévy process has moments of any order with , , and , for any .

Assumption 2.2.

-

(1)

The drift coefficient and scale coefficient are Lipschitz continuous, and for every .

-

(2)

For each and , the following conditions hold:

-

•

The coefficients and admit the partial derivatives and for and , all of which have continuous extensions as elements in .

-

•

There exists nonnegative constant satisfying

(5)

-

•

Then

Assumption 2.3.

-

(1)

There exists a probability measure such that for every , we can find constants and for which

(6) for any where .

-

(2)

For any , we have

(7)

We introduce a block-diagonal -matrix

whose components are defined by:

Assumption 2.4.

is positive definite.

We define real valued functions and on and by

| (8) | |||

| (9) |

We assume the following identifiability condition for and :

Assumption 2.5.

, and there exist positive constants and such that for all ,

| (10) | |||

| (11) |

2.3. Examples

Although Assumption 2.1 imposes a strong restriction on the mean and variance structure of , there is still room for statistical modeling of with respect to, for example, its skewness and jump activity. In this section, with the parameter constraints for Assumption 2.1, we give concrete Lévy processes induced from subordinators (i.e. non-decreasing Lévy processes) by the following two procedures: For given two independent subordinators and , one can easily construct a possibly skewed Lévy process of finite variation by taking its bilateral version: . Another way to deliver a new Lévy process is to take a normal mean variance mixture of a subordinator: for , a subordinator , and a standard normal random variable being independent of , the normal mean variance mixture of at time is given by

By their construction, and hold as long as the -th moment of and exists. It is worth noting that having a generator of and in hand, we can directly obtain that of and . All of the following induced Lévy processes can be generated by the functions setLaw and simulate in YUIMA package.

Example 2.6.

(Bilateral gamma [9]) For , the bilateral gamma process is defined by the difference of two independent gamma subordinators and whose Lévy densities are expressed as: for each ,

We write the law of as and it is straightforward from the form of that . Since the density function of is the convolution of two gamma density, it satisfies the symmetry relation

and on the positive real line, its form is given by

where denotes the Whittaker function. By using the independence between and , the parameter constraints for Assumption 2.1 are written as follows:

Example 2.7.

(Normal (exponentially) tempered stable) The normal (exponentially) tempered stable law is defined by the law of the normal mean variance mixture of the positive exponentially tempered stable random variable whose Lévy density is given by

and its law is denoted by ; especially inverse Gaussian law corresponds to . From [15, Theorem 30.1], the Lévy density of is explicitly expressed as:

where stands for the modified Bessel function of the third kind with index . From the expression of the Lévy density, the associated positive exponentially tempered stable subordinator satisfies and thus the corresponding normal (exponentially) tempered stable process also does . Since as for , the Blumenthal-Getoor index of is . The parameter constraints for Assumption 2.1 are written as follows:

Especially in the simple case where (that is, is a time-changed Brownian motion), the above constraints are reduced to

2.4. Stepwise Gaussian quasi-likelihood estimation

Here and in what follows, for any process we will denote by the -th increment

and for a measurable function on . Building on the discrete time formal Gaussian approximation, we define the stepwise GQL functions and as follows [18]:

where is any maximizer of over . We then define the associated stepwise GQMLE where is any maximizer of over . Formally, the first-stage corresponds to the quasi log-likelihoods associated with the (fake) approximation for , and also the second-stage does to the one associated with .

Let denote the (true) Lévy measure of , and

Under the aforementioned Assumptions 2.1 to 2.5, both and exist and are finite (and , where denotes the Gaussian variance of , possibly ). We can deduce the asymptotic normality and the uniform tail-probability estimate:

Theorem 2.8.

We note that , and are asymptotically independent if , hence if in particular is symmetric. We refer to [12] and [18] for technical details of the proof of Theorem 2.8; although the two cited papers used a -estimator type identifiability condition, which is seemingly different from Assumption 2.5 (-estimator type), it is trivial that we can follow the same line without any essential change.

To appreciate the difficulty of relaxing the standing condition in (2), let us first mention the case of diffusions: let be a standard Wiener process, and consider the following one-dimensional diffusion process

defined on the stochastic bases . Write the infinitesimal generator of as . By repeatedly applying Itô’s formula, it follows that for , , and a sufficiently smooth function , we have

Thus, under suitable integrability conditions, we obtain the expansion of :

| (13) |

In particular, the first-order approximation of the conditional expectation and conditional variance are given by

respectively, which are used for constructing the GQL for diffusions. Relaxation of the condition to for is then possible by taking large enough according to the value of : the associated GQMLE has the consistency and asymptotic normality under . We refer to [8] for details. At this point, we should remark that the GQL based on the first term on the right-hand side of (13) (with and ) is fully explicit whatever is.

On the other hand, although similar Itô-Taylor expansions to and can be easily derived in our Lévy driven case (1), the corresponding infinitesimal generator contains not only the differential operator but also the integral operator with respect to the Lévy measure of the driving Lévy noise. Specifically, its infinitesimal generator is given by

for a suitable function . Consequently, the modified GQL based on the higher-order Itô-Taylor expansion (13) contains the unknown parameter in addition to the drift and scale parameters. It is not clear that the simultaneous estimation of and by the modified GQL has a nice theoretical property. Even if it does, the entailed numerical optimization involved would be quite heavy and unstable since, for each , we need to repeatedly compute several integrals with respect to inside of the modified GQL. For this reason, it is difficult to remove the condition in the present general non-linear-SDE setting, as long as we use the GQL based on the stochastic expansion (13).

3. Theoretical results

3.1. Stochastic expansion of residual functional

Having the GQMLE in hand, we now turn to approximating , the the unit-time distribution of , based on the residuals

where

Write and , and let

From now on we will mostly omit “” from notation. In particular, for a measurable function we will abbreviate as .

Theorem 3.1.

Theorem 3.1 reveals the quantitative effect of plugging in . The second term on the right-hand side of (14) is not but , which implies that the asymptotic distribution of is indeed subject to influence of the proposed unit-time approximation; this is natural and expected, for we are using the -consistent (generally sub-optimal) estimator of .

To prove Theorem 3.1, we begin with a preliminary estimate.

Proof.

We will abbreviate as and so on; with a slight abuse of notation, we will write for . Write ; then,

for a suitable random point . Decompose as follows:

where

Before proceeding, let us note that by Theorem 2.8 the sequence is -bounded for each :

| (16) |

where we implicitly assume that when using this notation.

First we will deduce

| (17) |

Since the parameter space is supposed to be bounded and convex, the Sobolev inequality is in force (see [1] for details): for a random field and , we have

Noting the identities

valid for each and , we can apply Sobolev’s and Jensen’s inequalities to conclude that, for ,

Let denote the indicator function of the interval .

To proceed, we recall Burkholder’s inequality for stochastic integrals with respect to a centered Lévy process: under the moment conditions on , for any predictable process and we have

where is a positive constant depending only on , and for (see [14, Theorem IV 48]).

Turning to , we note the standard moment estimate: for any real ,

With this and the Lipschitz property of , analogous arguments as in handling yield that for each

| (19) |

Proof of Theorem 3.1.

Mimicking the estimates for (17), for each we obtain

Combined with (15) and (16), it follows from Hölder’s inequality that for each ,

| (21) |

and hence as well. We use the expression

for a (random) . By means of Schwarz’s inequality and (15),

By the moment estimates in the proof of Lemma 3.2, Hölder’s inequality, and (21), and also recalling (2), we see that for ,

This completes the proof. ∎

3.2. -estimation of noise parameter

We keep Assumptions 2.1 to 2.5 in force. Having Theorem 3.1 in hand, we proceed with estimation of based on the unit-time residual sequence . Let

and consider an -estimator

| (22) |

Among others, this includes the (quasi) maximum-likelihood for , where is a model for the unit-time noise distribution . We need to impose several conditions on the function , all of which are standard in the general theory of -estimation.

Assumption 3.3.

-

(1)

and for some .

-

(2)

, the -matrix is positive definite, and

The consistency of can be easily seen from Theorem 3.1 and Lemma 3.2: we have the continuous random function

where by Jensen’s inequality with if and only if , and moreover, the convergence is uniform in since . Hence the consistency follows.

We turn to the asymptotic normality of . Let . In the sequel, for any measurable function we will simply write for .

Proof.

Corollary 3.4 suggests that the effect of plugging in the GQMLE does remain in the limit. Therefore, in order to construct confidence interval and hypothesis testing for , we need to verify the joint asymptotic distribution of with some invertible matrix . We additionally introduce the following condition.

Assumption 3.5.

There exist -matrix and -matrix such that

| (24) | |||

| (25) |

Furthermore, the -matrix

is invertible.

From now on, we will write for the conditional expectation .

Remark 3.6.

Let

We also introduce the -matrix

where the ingredients are defined as follows:

Now we are ready to state the main result.

By Theorem 3.7, we have

based on which we can construct an approximate confidence set for , and also perform a Wald-type test. Also trivially, we can recover the asymptotic distribution of :

It is difficult to obtain and in explicit easy-to-handle forms even if the coefficients and are simple. However, by an application of Cauchy-Schwartz inequality and the estimates in the proof of Theorem 3.8, we can observe that at least, the left-hand-sides in (24) and (25) are tight. Moreover, we can formally write their limit by means of the representation theorem ([10, Proposition 3]): there exists a predictable process such that

| (26) |

From Itô’s formula and some calculations, we have

To sum up, we obtain the following expression:

By applying the central limit theorem for the stochastic integral with respect to a Poisson random measure (cf. [19, Lemma A.2]), the isometry property of the stochastic integral yield that under suitable moment and regularity conditions,

where and are given by the limits in probability:

and the other ingredients are the same as our previous works (cf. Theorem 2.8). However, since the explicit form of cannot be obtained in general, it is difficult to check the above convergence.

Finally, we would like to add that Theorem 3.7 and the resulting Wald-type test are valid without Assumption 3.5 if the minimum eigenvalue of is positive uniformly in . Such a condition for eigenvalues is often assumed in the context of (non-)linear regression.

Proof of Theorem 3.7.

By the Cramér-Wold device, we may and do assume that without loss of generality. It is straightforward to deduce that from Theorem 2.8, Theorem 3.1, Lemma 3.2, and the estimates we have seen in the previous proofs. Hence, by means of Slutsky’s theorem, it suffices to show that

| (27) |

From [18, Proof of Theorem 3.4], we have

This together with (23) and the definition of leads to

| (28) |

where

By (24), (25), and the arguments in the proof of Corollary 3.4, the martingale central limit theorem concludes (27) if we have the following convergences:

| (29) | |||

| (30) | |||

| (31) | |||

| (32) | |||

| (33) |

Trivially forms a martingale difference array with respect to , since we have for each ; this immediately ensures (29). By the arguments in Remark 3.6, we can replace (30), (31), and (32) by

respectively. Noting that for any under Assumption 2.1, we can deduce the last three convergences from [3, Lemma 9] and the ergodic theorem.

It remains to show (33). It follows from Itô’s formula and Assumption 2.1 that for any ,

where is the compensated Poisson random measure of ; recall that we are assuming that . Then, we can rewrite and as

Taking a similar route to the estimate (18), we have

Since under Assumptions 2.1 and 3.3, we obtain the desired result. ∎

3.3. Further remarks

3.3.1. Dimension of the processes

For the asymptotics of the GQMLE, we could consider multivariate without any essential change [18]; we will conduct related simulations in Section 5.2. Moreover, the estimator of may not be necessarily the GQMLE and could be any measurable mappings for which we have an asymptotically linear representation as in (28).

3.3.2. Model selection for

Residual based on information criterion (IC) formulation after estimation should be possible (both AIC and BIC types). We can infer the structure of as in the i.i.d case, yet should be careful in making possibly necessary corrections stemming from the stochastic expansion (14). For example, for the AIC statistics to be theoretically in effect, among other conditions it is required that the random sequence is -bounded for some . It could be verified by means of the uniform tail-probability estimate for through the random function ; indeed, we could make use of the same machinery to deduce Theorem 2.8(2).

3.3.3. Setting of noise inference

Although we have set a finite-dimensional above, we could consider infinite-dimensional , most generally itself: once has been constructed, it is also possible to take into account conventional nonparametric procedures, such as the kernel density estimation, and also goodness-of-fit tests; see Section 5.3 for an illustration.

4. Implementation

In this section, we discuss the new classes and the new methods in the YUIMA R package that gives us the possibility to deal with an SDE driven by a Lévy process completely specified by the user. To construct an object of YUIMA class, that is a mathematical description of an SDE driven by a pure Lévy jump process, three steps are necessary:

-

(1)

Definition of an object that contains all the information about the structure of the pure Lévy jump. In this step, the user can specify a random number generator, a density function, a cumulative distribution function, a quantile function, a characteristic function, and the number of components for the underlying Lévy process.

-

(2)

Definition of the structure of the SDE where the driving noise is determined from the object constructed in Step 1.

-

(3)

Construction of an object that belongs to the YUIMA class whose slots are reported in Figure 1. The slot model is filled with the object built in Step 2. This new object can be used to simulate a sample path by overwriting the slot sampling with the structure of the time grid. Alternatively, we can use this object to estimate the SDE defined in Step 2. In this case, we can store the observed data in the slot data.

4.1. yuima.law: A New Class for a Mathematical Description of the Lévy process

In this section, we describe the structure of a yuima.law-object and its constructor setLaw. The main advantage of this new class is the possibility of connecting YUIMA with any CRAN package that provides functions for a specific random variable. Figure 2 reports the slots that constitute an object of yuima.law class.

The first five slots contain R user-defined functions. In particular, the first two slots contain the random number generator and the density function respectively. Although it is not necessary to specify these functions to construct an object of yuima.law class, the definition of a random number generator is necessary to run the YUIMA simulate method while the density function is used internally by the YUIMA qmleLevy method. The template of these two functions is listed below:

# User specified random number generatorR> user.rng <- function(n, eta, t){+ ... ... ... # Body of the function+ }# User specified density functionR> user.density <- function(x, eta, t){+ ... ... ... # Body of the function+ } where the input eta is a vector containing the names of the Lévy noise parameters and the input t refers to the label of the time variable.

An object of yuima.law class is built using setLaw constructor.

R> setLaw(rng = function(n, ...){ NULL }, density = function(x, ...){ NULL },+ cdf = function(q, ...){ NULL }, quant = function(p, ...){ NULL },+ characteristic = function(u, ...){ NULL }, time.var = "t",+ dim = NA ) The first five inputs in the function fill the corresponding slots in the yuima.law object. Figure 3 describes the steps required for the construction of the yuima.law-object.

After the construction of an object that belongs to the yiuma.law class, by using the standard constructor setModel where an yuima.law object is passed to setModel through the argument measure, the user can specify completely a SDE driven by a pure Lévy jump as shown in the following command line:

R> setModel(drift = "User.Defined_drift", jump.coeff = "User.Defined_jump.coef",+ measure.type = "code", measure = list(df = User.Defined_yuima.law)) We remark that an object of yuima.law class can be also used to specify the Lévy noise in the Continuous Time ARMA model [4] and in the COGARCH process [5, 6]. In the first case, the model is built using the constructor setCarma:

R> setCarma(p, q, measure.type = "code", measure = list(df = User.Defined_yuima.law)) where and are two integers indicating the order of the autoregressive and the moving average parameters. The COGARCH(p,q) process can be defined in YUIMA using the function setCogarch as follows:

R> setCogarch(p, q, measure.type = "code", measure = list(df = User.Defined_yuima.law))

Figure 4 shows how to use an object of yuima.law class in the definition of models that can be constructed using YUIMA.

4.2. yuima.qmleLevy.incr: Estimation of an SDE driven by a Lévy pure jump process in yuima

In this section, we discuss how to estimate an SDE driven by a Lévy pure jump process in YUIMA. In particular, we describe the features of the new class yuima.qmleLevy.incr and explain the usage of the new method qmleLevy. The yuima.qmleLevy.incr class is the extension of the classical yuima.qmle class because we have additional slots associated with the filtered Lévy increments obtained using the procedure described in Section 3. As a child class, yuima.qmleLevy.incr class inherits all the YUIMA methods developed for the yuima.qmle class. Figure 5 reports the new slots. The most relevant for our study is the slot Incr.Lev where we can find the estimated Lévy increments.

An object of yuima.qmleLevy.incr class can not be directly constructed by the user but it is a possible output of the function qmleLevy that performs the estimation approach discussed in Section 2. The syntax of this function is as follows:

R> qmleLevy(yuima, start, lower, upper, joint = FALSE, third = FALSE,+ Est.Incr = "NoIncr", aggregation = TRUE) The first argument is an object of yuima class where the slot data contains the observed dataset, while the slot model is a mathematical description of the SDE driven by the pure Lévy jump process. The arguments start, lower and upper are used in the optimization routine to identify the initial guesses and box-constraints. The arguments joint and third are technical arguments related to the procedure of the GQMLE; we refer to [7] for a specific documentation of their meaning. The most important arguments for the estimation of the Lévy increments are Est.Incr and aggregation. The argument Est.Incr assumes three values: NoIncr, Incr and IncrPar. In the first case, the function returns an object of yuima.qmle class that contains only the SDE parameters. The function qmleLevy internally runs only the GQMLE procedure. Setting Est.Incr = "Incr" or Est.Incr = "IncrPar", qmleLevy returns an object of yuima.qmleLevy.incr class. In the first case the object contains the estimated increments while, in the second case, we also obtain the estimated parameters of the Lévy measure. The last argument aggregation is a logical variable. If aggregation = TRUE, the estimated Lévy increments are (4) associated to the unit-time intervals while, if aggregation = FALSE, the function returns the -time Lévy increments, see (3).

5. Numerical Examples

5.1. Univariate Lévy SDE model

In this section, we show how to use YUIMA in the simulation and estimation of an univariate SDE driven by a pure jump Lévy process defined by the user through an object of yuima.law class. The model, that we consider, is defined by the following SDE:

| (34) |

where is a real parameter while and are positive parameters, and where is a symmetric Variance Gamma process with parameter .

In this example we use an object of yuima.law class to construct a link between YUIMA and the VarianceGamma package [16] available in CRAN. We use two functions available in the package VaranceGamma respectively rvg for the random number generation and dvg to construct the density function. The parametrization in VarianceGamma package was introduced in [11] where the symmetric Variance Gamma random variable is defined as a normal variance mean mixture with a gamma subordinator. Specifically, we set

for the characteristic function of . Setting and , we identify the distribution of the increments for the symmetric Variance Gamma Lévy process used in (34).

Following the structure presented in Section 4, we define an object of yuima.law class that contains all the information on the underlying process . We run all examples using version yuima.1.15.4 available on R-Forge.

R> library(VarianceGamma)#### Definition of a yuima.law object ####R> myrng <- function(n, eta, t){+ rvg(n, vgC = 0, sigma = sqrt(t), theta = 0, nu = 1/(eta*t))+ }R> mydens <- function(x, eta, t){+ dvg(x, vgC = 0, sigma = sqrt(t), theta = 0, nu = 1/(eta*t))+ }R> mylaw <- setLaw(rng = myrng, density = mydens, dim = 1)R> class(mylaw)

[1] "yuima.law"attr(,"package")[1] "yuima"

R> slotNames(mylaw)

[1] "rng" "density" "cdf" "quantile"[5] "characteristic" "param.measure" "time.var" "dim"

Using the constructor setLaw we are able to build an object of yuima.law class where the first two slots contain the random number generator (myrng) and the density function (mydens) that we will use for the simulation and the estimation of the distribution of in the model (34). The next step is to build an object of yuima.model class using the standard constructor setModel:

#### Definition of an object of yuima.model class ####R> yuima1 <- setModel(drift = "alpha1*(alpha2-X)", jump.coeff = "gamma",+ jump.variable = "J", solve.variable = c("X"), state.variable = c("X"),+ measure.type = "code", measure = list(df = mylaw))

It is worth noticing that the slot measure of the object yuima1 contains the object mylaw constructed previously.

R> print(yuima1@measure[[1]])

An object of class "yuima.law"Slot "rng":function(n, eta, t){ rvg(n, vgC = 0, sigma = sqrt(t), theta = 0, nu = 1/(eta*t))}Slot "density":function(x, eta, t){ dvg(x, vgC = 0, sigma = sqrt(t), theta = 0, nu = 1/(eta*t))}Slot "cdf":function(q,...){NULL}<environment: 0x000001e202715cf0>Slot "quantile":function(p,...){NULL}<environment: 0x000001e202715cf0>Slot "characteristic":function(u,...){NULL}<environment: 0x000001e202715cf0>Slot "param.measure":[1] "eta"Slot "time.var":[1] "t"Slot "dim":[1] NA

We can generate a sample path using the simulate method in YUIMA that we report in Figure 7. The simulation scheme in YUIMA is based on the Euler discretization, and the small-time increments of the noise therein are generated by the random number generator stored in mylaw object.

#### real parameters ####R> alpha1 <- 0.4; alpha2 <- 0.25; gamma<- 0.25; eta <- 1#### Sample grid ####R> n <- 50000R> Time <- 1000R> sam <- setSampling(Terminal = Time, n = n)#### Simulation ####R> yuima2 <- setYuima(model = yuima1, sampling = sam)R> true <- list(alpha1 = alpha1, alpha2 = alpha2, gamma = gamma, eta = eta)R> set.seed(123)R> yuima3 <- simulate(yuima2, true.parameter = true, sampling = sam)#### plot sample path ####R> plot(yuima3)

To assess numerically the effectiveness of the three-step estimation procedure discussed in Section 2 and Section 3 we re-estimate the model in (34) using the data stored in the object yuima3.

#### starting point ####R> set.seed(123)R> start <- list(alpha1 = runif(1, 0.01, 2), alpha2 = runif(1, 0.01, 2),+ gamma = runif(1, 0.01, 2), eta = runif(1, 0.5, 1.5))#### upper and lower bounds ####R> upper <- list(alpha1 = 2, alpha2 = 2, gamma = 2, eta = 1.5)R> lower <- list(alpha1 = 0.01, alpha2 = 0.01, gamma = 0.01, eta = .5)#### GQMLE procedure ####R> res.VG <- qmleLevy(yuima3, start = start, lower = lower,+ upper = upper, Est.Incr = "IncrPar", aggregation = TRUE,+ joint = FALSE)

The function qmleLevy returns an object of yuima.qmleLevy.incr class that extends the standard class yuima.qmle.

R> class(res.VG)

[1] "yuima.qmleLevy.incr"attr(,"package")[1] "yuima"

R> slotNames(res.VG)

[1] "Incr.Lev" "logL.Incr" "minusloglLevy" "Levydetails" "Data" "model" [7] "call" "coef" "fullcoef" "fixed" "vcov" "min"[13] "details" "minuslogl" "nobs" "method"

The slot Incr.Lev is filled with an object of yuima.data class that contains the estimated unit-time Lévy increments.

R> str(res.VG@Incr.Lev, 2)

Formal class ’yuima.data’ [package "yuima"] with 2 slots ..@ original.data:’zooreg’ series from 1 to 1000 Data: num [1:1000, 1] 0.141 0.249 -1.219 1.336 0.106 ... .. ..- attr(*, "dimnames")=List of 2 Index: num [1:1000] 1 2 3 4 5 6 7 8 9 10 ... Frequency: 1 ..@ zoo.data :List of 1

Figure 8 reports the trajectory of the estimated unit-time Lévy increments.

#### Visualization of the estimated unit-time increments ####R> plot(res.VG@Incr.Lev)

5.2. Multivariate Lévy SDE model

In this section, we simulate and estimate a bivariate SDE model driven by two independent symmetric Variance Gamma processes. As done in the previous section we construct the random number generator and the joint density function of the underlying bivariate Lévy process using the function developed in the VarianceGamma package. We report below the code for simulating and estimating the process that satisfies the following system of SDEs:

| (35) |

where is a bivariate Lévy process where the components are two independent symmetric Variance Gamma processes.

The first step is to construct an object of yuima.law class that contains a random number generator and the joint density of the bivariate Lévy process . As done for the model in (34) we use the functions available in the R package VarianceGamma. The random number generator of the increments can be defined using the following command lines:

#### Construction of a bivariate rng function ####R> myrng2 <- function(n, eta1, eta2, t){+ res0 <- rvg(n, vgC = 0, sigma = sqrt(t), theta = 0, nu = 1 / (eta1 * t))+ cbind(res0, rvg(n, vgC = 0, sigma = sqrt(t), theta = 0, nu = 1 / (eta2 * t)))+ } Compared with the random number generator used in the univariate case, the result of the function rng is a two-column matrix where each column contains increments generated from a symmetric Variance Gamma random variable. Exploiting the independence assumption we construct the joint density of the process as a product of two univariate symmetric Variance Gamma densities using the following R function:

#### Construction of the joint density ####R> mydens2 <- function(x, eta1, eta2, t){+ dvg(x[,1], vgC = 0, sigma = sqrt(t), theta = 0, nu = 1/(eta1 * t)) *+ dvg(x[,2], vgC = 0, sigma = sqrt(t), theta = 0, nu = 1/(eta2 * t))+ } Using the constructor setLaw, we build an object of yuima.law that contains information for simulating the noise and for estimating the parameters in (35).

R> mylaw2 <- setLaw(rng = myrng2, density = mydens2, dim = 2) We simulate a trajectory of the model in (35) using the standard syntax in YUIMA as follows:

#### Model Definition ####R> yuima2 <- setModel(drift = c("alpha11*(alpha12-X1-0.2*X2)","alpha21*(alpha22-X2)"),+ jump.coeff = matrix(c("gamma1", 0, 0, ""gamma2"), 2, 2), solve.variable = c("X1", "X2"),+ state.variable = c("X1", "X2"), measure.type = c("code", "code"),+ measure = list(df = mylaw2), jump.variable = "J")#### Choosing model parameters ####R> alpha11 = 0.4; alpha12 = 0.25; gamma1 = 0.2; eta1 = 1R> alpha21 = 0.3; alpha22 = 0.3; gamma2 = 0.1; eta2 = 1R> true2 <- list(alpha11 = alpha11, alpha12 = alpha12, gamma1 = gamma1, eta1 = eta1,+ alpha21 = alpha21, alpha22 = alpha22, gamma2 = gamma2, eta2 = eta2)#### Setting the sample grid ####R> n2 <- 50000R> Time2 <- 1000R> sam2 <- setSampling(Terminal = Time2, n = n2)#### Simulation ####R> yuima2 <- setYuima(model = yuima2, sampling = sam2)R> set.seed(123)R> yuima2 <- simulate(yuima2, true.parameter = true2, sampling = sam2) Figure 9 reports the simulated trajectory of each member in the process

R> plot(yuima2)

Now we execute the three-step estimation procedure using, as a dataset, the simulated trajectory stored in the slot data of the object yuima2. As done in the univariate case, we select randomly a starting point and we fix upper and lower bounds for each parameter. We select the inputs of the function qmleLevy to get an object of yuima.qmleLevy.incr class that contains the estimated unit-time increments of the noise and the Lévy measure parameters of the bivariate symmetric Variance Gamma process .

#### Starting point generation ####R> set.seed(123)R> start2 <- list(alpha11 = runif(1, 0.01, 2), alpha12 = runif(1, 0.01, 2),+ gamma1 = runif(1, 0.01, 2), eta1 = runif(1, 0.5, 2), alpha21 = runif(1, 0.01, 2),+ alpha22 = runif(1, 0.01, 2), gamma2 = runif(1, 0.01, 2), eta2 = runif(1, 0.5, 2))#### Upper and lower bounds ####R> upper2 <- list(alpha11 = 2, alpha12 = 2, gamma1 = 2, eta1 = 2,+ alpha21 = 2, alpha22 = 2, gamma2 = 2, eta2 = 2)R> lower2 <- list(alpha11 = 0.01, alpha12 = 0.01, gamma1 = 0.01, eta1 = .5,+ alpha21 = 0.01, alpha22 = 0.01, gamma2 = 0.01, eta2 = .5) ## set lower bound#### Estimation ####R> res.VG2 <- qmleLevy(yuima2, start = start2, lower = lower2, upper = upper2,+ Est.Incr = "IncrPar", aggregation = TRUE, joint = FALSE) With the following command lines, we compare the initial values for the optimization routine, the fixed and estimated parameters.

#### Starting values ####unlist(start2)[names(coef(res.VG2))]

alpha11 alpha12 alpha21 alpha22 gamma1 gamma2 eta1 eta20.5822793 1.5787272 1.8815299 0.1006574 0.8238641 1.0609299 1.8245261 1.8386286

#### Real parameters ####unlist(true2)[names(coef(res.VG2))]

alpha11 alpha12 alpha21 alpha22 gamma1 gamma2 eta1 eta2 0.40 0.25 0.30 0.30 0.20 0.10 1.00 1.00

#### Estimated parameters ####coef(res.VG2)

alpha11 alpha12 alpha21 alpha22 gamma1 gamma2 eta1 eta20.3668973 0.2633624 0.2984875 0.3009404 0.2053790 0.1017661 0.9883838 0.9745951 The estimated parameters seem to be precise. The Euclidean norm of the difference between true2 and coef(res.VG2) is approximately 0.0457 while, applying the same distance between true2 and start2, it results to be 2.652 with a reduction of . We show the standard errors applying the function summary.

#### Summary ####summary(res.VG2)

summary(res.VG2)Quasi-Maximum likelihood estimationCall:qmleLevy(yuima = yuima2, start = start2, lower = lower2, upper = upper2, joint = FALSE, Est.Incr = "IncrPar", aggregation = TRUE)Coefficients: Estimate Std. Erroralpha11 0.3668973 0.005725729alpha12 0.2633624 0.002610983alpha21 0.2984875 0.028302434alpha22 0.3009404 0.017663594gamma1 0.2053790 0.023555954gamma2 0.1017661 0.010761713eta1 0.9883838 0.098752509eta2 0.9745951 0.094324105-2 log L: -494221.9 -494557.8 5335.13 The estimated time-unit increments of the bivariate Lévy noise are available in the slot Incr.Lev

R> summary(res.VG2@Incr.Lev)

Length1 Length2 Class Mode 1000 1000 yuima.data S4

R> plot(res.VG2@Incr.Lev, ylab = c(expression(paste(Delta, J[1, t])),+ expression(paste(Delta, J[2, t]))), xlab = "t")

5.3. Real Data

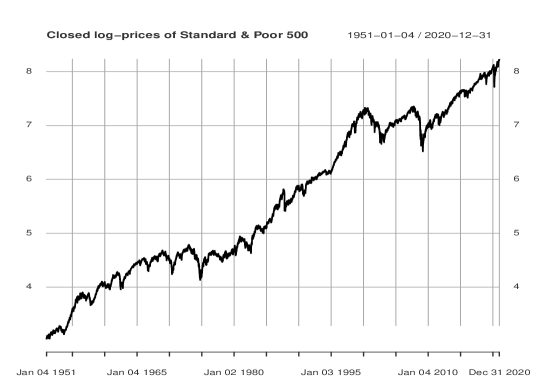

In this section, we discuss how to estimate a stochastic differential equation driven by a Lévy process using real data. Once the increments have been obtained, we show how to use them in the two different situations: noise selection and forecasting. We start with an example that shows how to combine the information stored in an object of yuima.qmleLevy.incr class with available R packages for selecting a Lévy measure. The data is downloaded from yahoo.finance using the R package quantmod that downloads time-series in an xts format. We get the closing log-prices of the S&P500 index ranging from 04 January 1951 to 04 January 2021 using the following command lines:

#### Download Dataset ####R> library(quantmod)R> getSymbols(Symbols = "^GSPC", from = "1951-01-04", to = "2021-01-04")R> logprice <- log(GSPC$GSPC.Close)R> plot(logprice, main = "Closed log-prices of Standard & Poor 500", main.cex = 0.8)

Figure 11 reports the time series used in our example. We describe the log-price by the following SDE:

| (36) |

where , , and . We construct an object of yuima class that contains the mathematical description of the SDE in (36) and the data.

#### Law Definition ####R> mylaw3 <- setLaw(dim = 1)R> #### Model and Data ####yuima3 <- setModel(drift = "alpha1+alpha2*X", jump.coeff = matrix(c("gamma1*X^gamma2")),+ measure.type = "code", measure = list(df = mylaw3), jump.variable = "J",+ solve.variable = c("X"), state.variable = c("X"))R> Data <- setData(logprice, delta = 1/30)R> yuima3 <- setYuima(data = Data, model = yuima3)R> print(Data)

Number of original time series: 1length = 17615, time range [1951-01-04 ; 2020-12-31]Number of zoo time series: 1 length time.min time.max deltaGSPC.Close 17615 0 587.133 0.03333333 From the structure of the object Data, we observe that the time is expressed in a monthly basis. Therefore, setting , we have and .

It is worth noting that the object mylaw does not require a formal specification for the random number generator and for the density function as done in the previous examples. Indeed, we do not assume any specific form of the Lévy measure of the process and the estimation of the unit-time increments described in Section 3 is completely model-free.

#### Estimation of time-unit increments ####R> set.seed(123)R> start3 <- list(alpha1 = runif(1, min = 10^(-10), max = 1),+ alpha2 = runif(1, min = -1, max = -10^(-10)), gamma1 = runif(1, min = 10^(-10), max = 1),+ gamma2 = runif(1, min = 0, max = 2))R> lower3 <- list(alpha1 = 10^(-10), alpha2 = -1, gamma1 = 10^(-10), gamma2 = 0)R> upper3 <- list(alpha1 = 1, alpha2 = 1, gamma1 = 1, gamma2 = 2)R> res3 <- qmleLevy(yuima3, start = start3, lower = lower3, upper = upper3,+ Est.Incr = "Incr", aggregation = TRUE, joint = FALSE)R> summary(res3)

Quasi-Maximum likelihood estimationCall:qmleLevy(yuima = yuima3, start = start3, lower = lower3, upper = upper3, joint = FALSE, Est.Incr = "Incr", aggregation = TRUE)Coefficients: Estimate Std. Errorgamma1 0.016267709 0.0007539279gamma2 0.694168099 0.0715834862alpha1 0.012156634 0.0081051421alpha2 -0.000635202 0.0015396235-2 log L: -113838.7 -113858.5 Applying logLik method to res3, we determine the value for the stepwise GQL function and the value of GQMLE with the following command lines:

R> T_n <- tail(index(Data@zoo.data[[1]]),1L)R> H_1 <- -1/T_n*logLik(res3)[1]R> GQMLE <-logLik(res3)[2]R> print(c(H_1, GQMLE)) [1] -96.94454 56929.23019

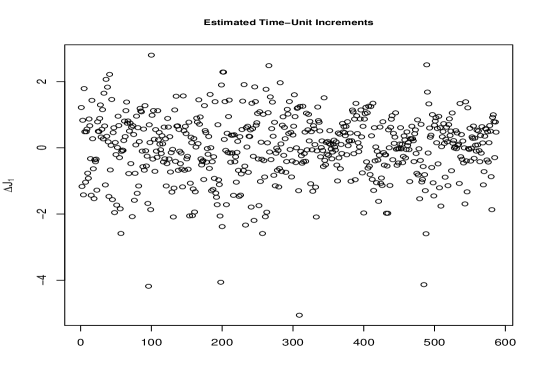

The unit-time increments are stored in the slot res3@Incr.Lev and they can be extrapolated using the following command lines:

#### Time-unit increments ####R> UnitaryIncr <- as.numeric(res3@Incr.Lev@original.data)R> plot(UnitaryIncr, ylab = expression(Delta*J[1]), xlab = " ",+ main = "Estimated Time-Unit Increments", cex.main = 0.8)

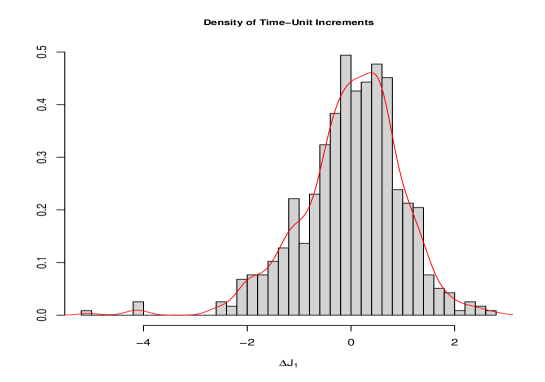

Figure 12 reports the estimated time-unit increments of the process . Due to the fact that the object UnitaryIncr belongs to the numeric class, we can apply any method available in R for any numeric object. Just for an illustration, in the following command lines, we show how to get the kernel density estimate based on the estimated increments, and compare it with the empirical histogram; a graphical comparison is reported in Figure 13.

#### Plot kernel density ####R> hist(UnitaryIncr, freq = F, nclass = 50, main = "Density of Time-Unit Increments",+ cex.main =0.8, xlab = expression(Delta*J[1]), ylab = " ")R> lines(density(UnitaryIncr), col = "red")

A model selection exercise can be done using the function stepAIC.ghyp available in the package ghyp that allows the user to compare a list of distributions widely applied in finance. In particular, based on the Akaike Information Criterion, this function identifies the best model between the Generalized Hyperbolic, the Hyperbolic, the Variance Gamma, the Normal Inverse Gaussian, the Student- and the Normal distribution.

#### Model selection ####R> library(ghyp)R> Comparison <- stepAIC.ghyp(UnitaryIncr)R> Comparison$best.model

Asymmetric Hyperbolic Distribution:Parameters: alpha.bar mu sigma gamma 1.8398103 0.5383745 0.9075450 -0.5337697log-likelihood:-793.7689Call:stepAIC.ghyp(data = UnitaryIncr) In our example, the function stepAIC.ghyp selects the Asymmetric Hyperbolic distribution as the best fitting model with the -parametrization for a generic Generalized Hyperbolic distribution. The latter is a normal variance mean mixture with a Generalized Inverse Gaussian subordinator and, as described in the package documentation [20], the -parametrization requires the characteristic function of to be:

where , and . The real parameters and control the position and the skewness while is a scale parameter for the Generalized Hyperbolic distribution. The Hyperbolic distribution is obtained by setting .

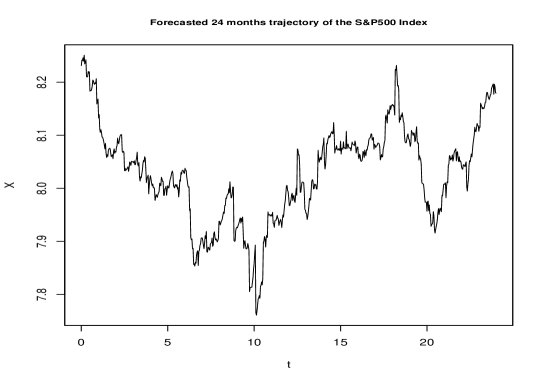

In the second example, we show how to use an object of yuima.law class to generate a new trajectory using the increments of the process . In this case, we need to estimate the increments associated with the interval of length (small model-time length). In this example, we use a shorter dataset composed of three years of observations of the S&P500 index ranging from 04 January 2018 to 04 January 2021. For the estimation of the increments, the chunk code is exactly the same used in the previous example with only one difference. Indeed, to obtain the increments we set the input aggregation as FALSE.

#### Download dataset ####R> getSymbols(Symbols = "^GSPC", from = "2018-01-04", to = "2021-01-04")R> logprice2 <- log(GSPC$GSPC.Close)#### Model and data ####R> mylaw4 <- setLaw(dim = 1)R> yuima4 <- setModel(drift = "alpha1+alpha2*X", jump.coeff = matrix(c("gamma1*X^gamma2")),+ measure.type = "code", measure = list(df = mylaw4), jump.variable = "J",+ solve.variable = c("X"), state.variable = c("X"))R> Data <- setData(logprice, delta = 1/30)R> yuima4 <- setYuima(data = Data, model = yuima4)#### Estimation delta t increments ####R> set.seed(123)R> start4 <- list(alpha1 = runif(1, min = 10^(-10), max = 5),+ alpha2 = runif(1, min = -1, max = -10^(-10)), gamma1 = runif(1, min = 10^(-10), max = 1),+ gamma2 = runif(1, min = 0, max = 2))R> lower4 <- list(alpha1 = 10^(-10), alpha2 = -1, gamma1 = 10^(-10), gamma2 = 0)R> upper4 <- list(alpha1 = 5, alpha2 = -10^(-10), gamma1 = 1, gamma2 = 2)R> res4 <- qmleLevy(yuima4, start = start4, lower = lower4, upper = upper4,+ Est.Incr = "Incr", aggregation = FALSE, joint = FALSE)R> summary(res4)

Quasi-Maximum likelihood estimationCall:qmleLevy(yuima = yuima4, start = start4, lower = lower4, upper = upper4, joint = FALSE, Est.Incr = "Incr", aggregation = FALSE)Coefficients: Estimate Std. Errorgamma1 0.08111166 0.005677789gamma2 0.00000000 0.065495083alpha1 2.01137182 1.367347271alpha2 -0.25019063 0.171158938-2 log L: -4207.318 -4210.077

Using the estimated increments in the slot res4@Incr.Lev we can build an object of yuima.law class that internally uses a random number generator that samples from the data in res4@Incr.Lev.

#### yuima.law Definition ####R> mydata <- as.numeric(res4@Incr.Lev@original.data)R> myrndEmp <- function(n, mydata){+ sample(mydata, size = n)+ }R> mylaw5 <- setLaw(rng = myrndEmp)

The object mylaw contains a random number generator that uses the R function sample, however, the user can apply more advanced sampling methods from packages available from CRAN. We can simulate one-year trajectory of the S&P500 log prices in YUIMA. Figure 14 reports the simulated sample path.

#### Generation 1 year trajectory ####R> yuima5 <- setModel(drift = "alpha1+alpha2*X", jump.coeff = matrix(c("gamma1*X^gamma2")),+ measure.type = "code", measure = list(df = mylaw5), jump.variable = "J",+ solve.variable = c("X"), state.variable = c("X")+ xinit = as.numeric(tail(logprice2, 1L)))R> samp5 <- setSampling(Initial = 0, Terminal = 24, n = 24*30)R> yuima5 <- setYuima(model = yuima5, sampling = samp5)R> true5 <- as.list(coef(res4))R> true5$mydata <- mydataR> set.seed(123)R> yuima5 <- simulate(yuima5, true.parameter = true5, sampling = samp5)R> plot(yuima5, main = "Forecasted 24 months trajectory of the S&P500 Index",+ cex.main = 0.8)

In Figure 14, the 24 months trajectory displays an oscillatory behavior. It fluctuates around the long term mean that can be estimated using the ratio .

Acknowledgement

We thank the anonymous reviewers for their valuable comments. This work was partly supported by JST CREST Grant Number JPMJCR14D7, Japan.

References

- [1] R. A. Adams. Some integral inequalities with applications to the imbedding of Sobolev spaces defined over irregular domains. Trans. Amer. Math. Soc., 178:401–429, 1973.

- [2] A. Brouste, M. Fukasawa, H. Hino, S. M. Iacus, K. Kamatani, Y. Koike, H. Masuda, R. Nomura, T. Ogihara, Y. Shimizu, M. Uchida, and N. Yoshida. The yuima project: A computational framework for simulation and inference of stochastic differential equations. Journal of Statistical Software, 57(4):1–51, 2014.

- [3] V. Genon-Catalot and J. Jacod. On the estimation of the diffusion coefficient for multi-dimensional diffusion processes. Ann. Inst. H. Poincaré Probab. Statist., 29(1):119–151, 1993.

- [4] S. M. Iacus and L. Mercuri. Implementation of lévy carma model in yuima package. Comp. Stat., 30(4):1111–1141, 2015.

- [5] S. M. Iacus, L. Mercuri, and E. Rroji. Cogarch (p, q): Simulation and inference with the yuima package. J. Stat. Softw., 80(1):1–49, 2017.

- [6] S. M. Iacus, L. Mercuri, and E. Rroji. Discrete-time approximation of a cogarch (p, q) model and its estimation. J. Time Ser. Anal., 39(5):787–809, 2018.

- [7] S. M. Iacus and N. Yoshida. Simulation and inference for stochastic processes with yuima. A comprehensive R framework for SDEs and other stochastic processes. Use R, 2018.

- [8] M. Kessler. Estimation of an ergodic diffusion from discrete observations. Scandinavian Journal of Statistics 24(2): 211–229, 1997.

- [9] U. Küchler and S. Tappe. Bilateral gamma distributions and processes in financial mathematics. Stochastic Process. Appl., 118(2):261–283, 2008.

- [10] A. Løkka. Martingale representation of functionals of Lévy processes. Stochastic Process. Appl., 22(4): 867–892, 2004.

- [11] D. B. Madan and E. Seneta. The variance gamma (v.g.) model for share market returns. J. Bus., 63(4):511–524, 1990.

- [12] H. Masuda. Convergence of Gaussian quasi-likelihood random fields for ergodic Lévy driven SDE observed at high frequency. Ann. Statist., 41(3):1593–1641, 2013.

- [13] H. Masuda and Y. Uehara. Two-step estimation of ergodic Lévy driven SDE. Stat. Inference Stoch. Process., 20(1):105–137, 2017.

- [14] P. E. Protter, Stochastic Integration and Differential Equations, second edition, Springer-Verlag, Berlin.

- [15] K.-i. Sato. Lévy processes and infinitely divisible distributions. Cambridge university press, 1999.

- [16] D. Scott and C. Y. Dong. VarianceGamma: The Variance Gamma Distribution, 2018. R package version 0.4-0.

- [17] D. Straumann. Estimation in conditionally heteroscedastic time series models, volume 181 of Lecture Notes in Statistics. Springer-Verlag, Berlin, 2005.

- [18] Y. Uehara and H. Masuda. Stepwise estimation of a Lévy driven stochastic differential equation. Proc. Inst. Statist. Math. (Japanese), 65(1):21–38, 2017.

- [19] Y. Uehara, Statistical inference for misspecified ergodic Lévy driven stochastic differential equation models. Stochastic Process. Appl., 129(10): 4051–4081, 2019.

- [20] M. Weibel, D. Luethi, and W. Breymann. ghyp: Generalized Hyperbolic Distribution and Its Special Cases, 2020. R package version 1.6.1.