Optimal bailout strategies resulting from the drift controlled supercooled Stefan problem

Abstract

We consider the problem faced by a central bank which bails out distressed financial institutions that pose systemic risk to the banking sector. In a structural default model with mutual obligations, the central agent seeks to inject a minimum amount of cash in order to limit defaults to a given proportion of entities. We prove that the value of the central agent’s control problem converges as the number of defaultable institutions goes to infinity, and that it satisfies a drift controlled version of the supercooled Stefan problem. We compute optimal strategies in feedback form by solving numerically a regularized version of the corresponding mean field control problem using a policy gradient method. Our simulations show that the central agent’s optimal strategy is to subsidise banks whose equity values lie in a non-trivial time-dependent region.

Keywords: Systemic risk, Mean field control, Supercooled Stefan problem,

Propagation of chaos, Bail-outs

1 Introduction

In this paper, we analyse a simple mathematical model for a central bank that optimally injects cash into a banking system with interbank lending in order to prevent systemic default events. By way of introduction, we first review known results on the dynamics without intervention and its relation to the supercooled Stefan problem. We then describe the optimisation problem faced by the central agent and discuss its setting within the literature on Mean Field Control (MFC) problems together with this paper’s contributions.

1.1 Interbank lending and the supercooled Stefan problem

We study a market with financial institutions and their equity value process for with finite time horizon and . We interpret in the spirit of structural credit risk models as the value of assets minus liabilities. Hence, we consider an institution to be defaulted if its equity value hits 0. We refer the reader to [49] for the classical treatment as well as to [40] and the references therein for a discussion of such models in the present multivariate context with mutual obligations.

We consider specifically a stylised model of interbank lending where all firms are exchangeable, their equity values are driven by Brownian motion, and where the default of one firm leads to a uniform downward jump in the equity value of the surviving entities. The latter effect is the crucial mechanism for credit contagion in our model as it describes how the default of one firm affects the balance sheet of others. Here, we follow [37, 50, 48]) to assume that the satisfy

| (1) |

where , are non-negative i.i.d. random variables, is an -dimensional standard Brownian motion, independent of , and is a given parameter measuring the interconnectedness in the banking system. The initial condition reflects the current state of the banking system. This might include minimal capital requirements prescribed by the regulator as conditions to enter the banking system, but we do not consider this question explicitly.

Even this highly stylised simple system produces complex behaviour for large pools of firms, including systemic events where cascades of defaults caused by interbank lending instantaneously wipe out significant proportions of the firm pool (see [37, 50, 30]).

One way of analysing this is to pass to the mean-field limit for . It is known (see, e.g., [29]) that the interaction (contagion) term in (1) converges (in an appropriate sense) to a deterministic function as , i.e.,

Moreover, the are asymptotically independent with the same law as a process which together with satisfies a probabilisitic version of the supercooled Stefan problem, namely

| (2) |

where is subject to the constraint

| (3) |

Here, is a standard Brownian motion independent of the random variable , which has the same law as all . We refer to [30] for a discussion on how this probabilistic formulation relates to the classical PDE version of the supercooled Stefan problem.

From a large pool perspective (see [37, 50]), may be viewed as the equity value of a representative bank and as its default time, while describes the interaction with other institutions under the assumption of uniform lending and exchangeable dynamics. In particular, can be interpreted as the fraction of defaulted banks at time and consequently as the loss that the default of these entities has caused for the survivors.

It is known that solutions to (2), (3) are not unique in general (see [29, 27]), which explains the need to single out so-called physical solutions that are meaningful from an economic and physical perspective. Under appropriate conditions on , these physical solutions are characterised by open intervals with smooth , separated by points at which this dependence may only be Hölder continuous or even exhibit a discontinuity, an event frequently referred to as blow-up (see [30]). If the mean of the initial values is close enough to zero relative to the interaction parameter , a jump necessarily happens (see [37]).

In case a discontinuity does occur at some , the following restriction on the jump size defines such a physical solution:

| (4) |

with and . By the results of [30], the above condition on the jumps of uniquely defines a solution to (2) and (3) under some restrictions on the initial condition . For future reference, we also introduce the concept of minimal solutions, which we know to be physical whenever the initial condition is integrable (see [27]). We call a solution minimal, if for any other that satisfies (2) with loss process given by (3), we have that

| (5) |

Note that by combining the results of [27] and [30] the minimal solution is the unique physical one, and thus ecnomoically meaningful one, if the initial condition satisfies the assumptions of [30].

1.2 The central agent’s optimisation problem

The purpose of this paper is to analyse strategies that a central bank (central agent) can take to limit the number of defaults. They achieve this by controlling the rate of capital injected to distressed institutions. That is to say, rather than bailing out firms which are already defaulted, the central agent intervenes already ahead of the time their equity values become critical. This rate of capital111 As we are working in continuous time, we also assume that the central agent is able to inject money continuously. At first sight this is a bold approximation of reality but allows us to work without an a-priori fixed time grid determining when the central agent reacts. received by bank is determined by processes and added to (1). In the finite dimensional situation, the then satisfy

| (6) |

A mathematically similar problem has been studied in [58]. There the question of finding an optimal drift in order to maximize the number of Brownian particles that stay above is treated, however without the singular interaction term appearing in (6).

In anticipation of a propagation of chaos result (proved in Section 2), we therefore consider an extension of (2) and (3) with a drift process , i.e.,

| (7) | ||||

| (8) |

Throughout the paper we will consider a constraint , which amounts to the assumption that at any point in time the central agent has limited resources for the capital injections. We will specify further technical conditions on later, which allow us to show that indeed the finite system converges in a suitable sense to this McKean–Vlasov equation.

We now consider a central agent who injects capital into a representative bank at rate at time in order to keep

that is the number of defaults that occur before222We consider rather than in the constraint because may have a jump discontinuity precisely at , which would considerably complicate the analysis. However, by [46, Corollary 2.3], we know that solutions to (1) cannot have discontinuities after time . We can derive an analogous result for the controlled case using Girsanov’s theorem if, in addition to the pointwise bound on , we assume a bound on the total cost over the infinite horizon, i.e. for some . In this setting, by choosing sufficiently large, we then do not need to distinguish between and . a given time , below a specified threshold , while minimising the expected total cost

We therefore consider the following constrained optimisation problem: For given , the central agent solves

| (9) |

Define now for the Lagrange function and use it to express the constrained optimization problem as an unconstrained one, namely , which holds true since

Assuming the absence a duality gap333Proving the absence a duality gap seems difficult as standard minimax theorems cannot be easily applied. Moreover, our numerical experiments suggest that at least for certain values of it might fail to hold true. (or equivalently the existence of a saddlepoint of , i.e. for all ), then we can interchange the and and solve the dual problem .

For these reasons we shall from now on consider the inner optimisation problem for fixed (which can – due to the complementary slackness condition – only hold if the constraint is binding, i.e. ). If there is no duality gap, the optimal for a prespecified threshold can in turn be determined by solving the outer optimisation problem, i.e. where .

Writing for the solution process associated with the minimal solution , analogously defined as in (5) but now for (7), we thus minimise the following objective function

| (10) | |||||

where is the absorbed minimal solution process and the default time. Note that the only difference between and is the constant , which however does not play a role in the optimisation over . By varying , we can therefore trace out pairs of costs and losses which are solutions to (9) for different . The Lagrange multiplier (as a function of ) can then be interpreted as shadow price of preventing further defaults. Indeed, as for usual constrained optimization problems, the optimal cost seen as a function of the loss level satisfies under certain technical conditions

As we show numerically in Section 3, the optimal loss as a function of is monotone decreasing, so that for large enough (and ), the threshold becomes small enough to avoid systemic events.

Note that, by the arguments at the end of Section 1.1, using the minimal solution in the optimisation task is the only economically meaningful concept because non-physical solutions (with a potential higher probability of default) cannot be realistically justified, in particular when seen as limits of particle systems. We refer to [29, Section 3.1] for examples of such non-physical solutions.

Both from a theoretical and numerical perspective, we shall analyse the objective function (10) together with the dynamics (7), which is a non-standard MFC problem with a singular interaction through hitting the boundary. As we show in Section 2, in particular Theorem 2.8, optimisation of the McKean–Vlasov equation (7) yields the same result as first optimising in the -particle system and then passing to the limit. In particular, by Theorem 2.10, optimizers of the McKean–Vlasov equation (7) are -optimal for the -particle system. This then justifies our numerical implementation described in Section 3 where we deal directly with the MFC problem.

1.3 Relation to the literature

Theory of MFC problems and applications to systemic risk

Due to the big amount of literature on MFC problems we focus here on relatively recent works and mostly on MFC and not on the related concept of Mean Field Games (MFG) as introduced in [43] and [39]. We refer to [21, 20, 25] for definitions of the MFC and MFG optima in general set-ups and discussions on the differences. As we here deal with a central agent our optimization problem corresponds to a Pareto optimum where all the agents cooperate to minimize the costs. Therefore MFC is the appropriate concept. Note that instead of MFC the terminology McKean–Vlasov control is often also used.

Similarly as for classical optimal control, dynamic programing principles have also been derived for MFC problems and can be found in [53, 31]. We also refer to [54, 14, 3, 44], where in diffusion set-ups formulations using a Hamilton-Jacobi Bellman (HJB) equation on the space of probability measures for closed-loop controls (also called feedback controls) are deduced. In the recent work [36] this has been generalized to jump diffusion processes. For a dynamic programming principle for open-loop controls we refer to [13], and to [20, 1] for a characterisation by a stochastic maximum principle.

We are here interested in feedback controls and would therefore need to solve the corresponding HJB equation (as e.g. in [54]), i.e. an infinite dimensional fully nonlinear partial differential equatios (PDE) of second order in the Wassertein space of probability measures. Solving such an equation is challenging, since it involves computing measure derivatives, which is numerically intractable. In our context the situation is even more intricate due to the singular interactions through the boundary. Indeed, even under the (usually not satisfied) assumption that is , the problem is far beyond a standard MFC framework. In this case, in (7) can be replaced by , thus a time derivative of the measure component, which makes the problem ‘non-Markovian’. Moreover, we deal with subprobability measures describing the marginal distributions of the absorbed process which governs the underlying dynamics. Note also that the total mass of these subprobability measures as well as itself can exhibit jumps if is discontinuous, and that these jumps emerge endogenously from the feedback mechanism.

This is in contrast to some other recent papers where jumps are exogenously given. For instance, the recent articles [36, 6] consider the control of (conditional) McKean–Vlasov dynamics with jumps and associated HJB-PIDEs, while in [7] a stochastic maximum principle is derived to analyse a mean-field game with random jump time penalty.

In the context of systemic risk and contagion via singular interactions through hitting times the paper [51] is especially relevant. There a game in which the banks determine their (inhomogeneous) connections strategically is analysed. It turns out that by a reduction of lending to critical institutions in equilibrium systemic events can be avoided. A model involving singular interaction through hitting the boundary is also considered in [32]. There, an optimization component is incorporated via a quadratic functional that allows the institutions to control parts of their dynamics in order to minimize their expected risk, which then leads to a MFG problem. The quadratic cost functional is inspired by the earlier work [22], which also treats the mean-field game limit of a system of banks who control their borrowing from, and lending to, a central bank, and where the interaction comes from interbank lending. Let us finally mention the very recent article [8] which applies reinforcement learning to a model that can be considered as an extension of [22] adding a cooperative game component within certain groups of banks.

In the wider context of interaction through boundary absorption, a few works on mean-field games have also appeared recently. In [17], the players’ dynamics depends on the empirical measure representing players who have not exited a domain. This is extended to smooth dependence on boundary losses prior to the present time in [18], and to the presence of common noise in [16]. The economic motivation for these models are, among others, systemic risk and bank runs.

Numerics for MFC and MFG problems

Among the numerical methods proposed for MFC and MFG problems, we refer to [23] for a policy gradient-type method where feedback controls are approximated by neural networks and optimised for a given objective function; to [34] and again to [23] for a mean-field FBSDE method, generalising the deep BSDE method to mean-field dependence and in the former case to delayed effects; and to [5] for a survey of methods for the coupled PDE systems, mainly in the spirit of the seminal works [2, 4]; see also a related semi-Lagrangian scheme in [19] and a gradient method and penalisation approach in [52].

Beside these works on PDE systems, a lot of research has recently been conducted on how to apply (deep) reinforcement or Q-learning to solve MFC and MFG problems or combinations thereof (see e.g., [35, 11, 10, 9] and the references therein). We also refer to two recent survey articles [38, 45] on machine learning tools for optimal control and games. The first article focuses on methods that try to solve the problems by relying on exact computations of gradients exploiting the full knowledge of the model, while the second one presents learning tools that aim at solving MFC and MFG problems in a model-free fashion.

In our modeling and numerical approach we have full knowledge of the model, but what distinguishes it from the existing literature is the particular singular interaction through the boundary absorption. This means that all the discussed numerical schemes and methods need to be adapted to accommodate the current special situation. We opted for an adaptation of the policy gradient-type method considered in [55], since it shares the same computational complexity as the gradient-based algorithms in e.g. [12, 41, 52], but enjoys an accelerated convergence rate and can handle general convex nonsmooth costs (including constraints), which allows to incorporate the current objective function. It exploits a forward-backward splitting approach and iteratively refines the approximate controls based on the gradient of the cost, evaluated through a coupled system of nonlocal linear PDEs. The precise algorithm is outlined in Section 3.

1.4 Contributions and findings

As already mentioned, our model differs in a number of fundamental points from the existing literature: first, while [22, 17, 18, 51, 32, 16] study mean-field game solutions and equilibria of -player games, where each player maximises their own objective, we study the problem of a central planner who specifically seeks to control the number of defaults. Second, in contrast to [18], where the coefficients of the players’ processes may depend on the loss process and to [16], which further includes a driver which is a smoothed version of (hence modeling delayed effects of hitting the boundary), we consider the firm values driven by directly, resulting in an instantaneous effect of defaults and the emergence of systemic events. Third, the techniques we use are also entirely different from those in these preceding works. Instead of relying on techniques for martingale problems used e.g. in [42] to derive a limit theory for controlled McKean–Vlasov dynamics, we extend the method from [27] to show the convergence of the finite system to the mean-field limit.

Moreover, we provide a numerical solution adapting the approach of [55] to the current setting. This means first of all to express in the dynamics (7) and in the loss function explicitly in terms of the distribution of , which can be (formally) achieved through , i.e. the spatial derivative of its density at (assuming it exists). To cast the absorbed process formally into a (more) standard McKean–Vlasov framework, instead of (7), we write the dynamics in a form where the drift and diffusion coefficients are multiplied with the Heaviside function (in the state). Both the computation of and the presence of the Heaviside function need some regularization, which is treated in Section 3.1. This regularized version then allows to apply the policy gradient descent method of [55] where we compute the gradient via a coupled forward-backward PDE system (instead of a particle method as in [55]). In particular, the forward problem is given by a smoothed version of the Stefan problem with a drift term determined by the feedback control, while the backward problem determines a decoupling field of the adjoint process.

From an economic point of view, our findings indicate a high sensitivity on the parameter in (7). As shown in Figure 7(b), for a certain value of and in a regime where triggers jump discontinuities in the uncontrolled regime, the optimal control strategy switches from not avoiding a jump to avoiding a jump. Moreover, our numerical experiments suggest that it is not possible to vary the capital injection to control the size of the jump continuously, since the possible jump size is restricted by the physical jump constraint (4). Viewed differently, a large systemic event can happen if the central agent withdraws a small amount of capital from a scenario without jumps.

Summarizing, the main contributions of the present paper are as follows:

-

•

We show convergence of the system with agents to the mean-field limit (see Section 2), including well-posedness of the central agent’s optimisation problem, i.e. the existence of unique minimal solutions to the Stefan problem as given by (7)-(8) for any suitably regular control process and the existence of an optimal control which minimises (10).

-

•

We propose a numerical scheme (see Section 3) based on policy gradient iteration, where the gradient is computed via coupled forward and backward PDEs satisfied by the density of a regularized version of the equity value process and a decoupling field corresponding to an adjoint process, respectively.

-

•

We analyse by way of detailed numerical studies the structure of the central agent’s optimal strategy in different market environments, and the minimal losses that are attained under optimal strategies with varying cost (see also Section 3).

2 Convergence to a mean-field limit

In this section, we show the existence of a minimising strategy for the central agent’s objective function in the mean-field limit, as well as convergence of the -agent control problem.

2.1 The model setup

We fix a measure and define a reference probability space to be a tuple such that supports a Brownian motion that is adapted to and there is a -measurable random variable with . Note that with this definition, is independent of by construction. We endow the space

| (11) |

with the topology of weak convergence in . Since is bounded in the -norm and weakly closed, is a compact Polish space. We then define the space of admissible controls

| (12) |

Note that the space of admissible controls as well as the objective functional as defined in (10) depend implicitly on the choice of stochastic basis . We will sometimes write or when we wish to emphasize this dependence. To be able to guarantee existence of optimizers and to make the optimization problem independent of the choice of stochastic basis , we will consider the relaxed optimization problem

| (13) |

as is standard in the stochastic optimal control literature (see e.g. [33]). We say that solve problem (7)-(8) on if is a reference probability space with Brownian motion and initial condition such that and (7)-(8) holds -almost surely.

Note that it is not clear a priori that the process given in (7) is well-defined. Indeed, it is known that the McKean–Vlasov problem (2) and (3) may admit more than one solution, and it is not known that physical solutions exist for general , although it is known for of the special form , where is Lipschitz (see e.g. [29, 46]). To pin down a meaningful solution concept, we therefore rely on the notion of minimal solutions as defined in (5). By the results of [27], we know that minimal solutions of the uncontrolled system are physical whenever the initial condition is integrable.

Throughout the following sections always denotes the set of probability measures on a Polish space which we endow with the Lévy-Prokhorov metric, i.e., convergence of probability measures is to be understood in the (probabilistic) weak sense. For function spaces etc. we apply rather standard notation and refer to Section A.1 for more details.

2.2 Well-posedness of minimal solutions for general drift

We fix the reference probability space and show that minimal solutions exist for any . Define the operator for a càdlàg function and as

| (14) |

Note here that solves (7) if and only if is a fixed-point of . We next introduce a function space that is mapped to itself by : Set

| (15) |

where is the extended real line. Note that for , defines a cumulative distribution function of a probability measure on . Therefore, equipping with the topology of weak convergence, i.e., we have that in if and only if for all that are continuity points of , we obtain that is a compact Polish space. As in the uncontrolled case, is continuous on .

2.3 Existence of an optimal control

A key step in proving existence of an optimizer is to show that sequences of solutions to (7)-(8) are compact in a certain sense and that their cluster points are solutions of (7)-(8). This is the content of the next theorem.

Theorem 2.2.

Proof.

See Section A.2 in the Appendix. ∎

Remark 2.3.

Note that in Theorem 2.2, we do not assume that either the or are minimal solutions. At this point, we do not know how to prove that is minimal if all are minimal. Stability of the minimal solution is an open question (cf. [27, Conjecture 6.10]). For the proof of the subsequent theorem where we prove existence of an optimizer to (13), formulated with the minimal solution, this however does not matter.

Next, we prove that the infinite-dimensional problem (13) admits an optimizer.

Theorem 2.4.

There is an optimizer of (13), i.e., there is a stochastic basis and such that

Proof.

Let be solutions to (7)-(8) on such that . By Theorem 2.2, after passing to subsequences if necessary, there is a reference probability space such that solves (7)-(8) on and holds in as well as in .

2.4 Properties of the controlled -particle system

We describe the controlled -particle system mentioned in the introduction in more detail. We consider a stochastic basis supporting certain exchangeable random variables, defined as follows.

Definition 2.5.

Set , where the are random variables taking values in some space . We say that is -exchangeable, if

for any permutation of . We say that is -exchangeable if the vector is -exchangeable under .

The stochastic basis is supposed to support an -dimensional Brownian motion and an -exchangeable, -measurable random vector . The particles in the system then satisfy the dynamics

| (19) |

where is -exchangeable, and , where . In analogy to the infinite-dimensional case, we denote . We then consider the set of admissible controls

| (20) |

The same examples as in the uncontrolled case show that solutions to (19) are not unique in general (cf. Section 3.1.1 in [29]). Therefore, in [28], physical solutions are introduced. Similarly to the infinite dimensional case we can also consider minimal solutions. We call a solution to (19) minimal, if for every solution to (19)

holds almost surely. The same argument as in [27, Lemma 3.3] shows that the notions of physical and minimal solution are equivalent in the controlled -particle system. In analogy to the infinite-dimensional case, we introduce the operator

| (21) |

where is some càdlàg process adapted to the filtration generated by . We will often simply write instead of . The statements are then meant to hold for arbitrary, fixed . An important property is that is monotone in the sense that

We then readily see by straightforward induction arguments that

| (22) |

holds almost surely, where is any solution to the particle system and denotes the -th iterate of . A similar argument as for the system without drift in [27] shows that the iteration converges to the minimal solution after at most iterations.

Lemma 2.6.

For , let be defined as in (21). Then is the minimal solution to the particle system with drift and the error bound

| (23) |

holds almost surely.

Proof.

Analogous to the proof of Lemma 3.1 in [27]. ∎

Roughly speaking, the next result says that limit points (in distribution) of solutions to the controlled -particle system converge (along subsequences) to solutions of the controlled McKean–Vlasov equation (7)-(8). By we denote here the space of càdlàg paths on equipped with the -topology.

Theorem 2.7.

For , let be a solution to the particle system (19) on the stochastic basis and define . Suppose that for some measure we have

Then there is a subsequence (again denoted by ) such that in , where coincides almost surely with the law of a solution process to the McKean–Vlasov problem (7)-(8) satisfying .

Proof.

See Section A.4 ∎

The next theorem shows that when we optimize the policy in the particle system and then take the limit of the resulting optimal values, we obtain the same value that we find by optimizing the infinite-dimensional version of the problem.

Theorem 2.8.

For , define the value of a perturbed controlled -particle system as

where and is the minimal solution of the controlled -particle system with drift as introduced in Lemma 2.6 and perturbed initial condition for and all . Then it holds that

| (24) |

Proof.

Step 1: We show the inequality . To that end, choose and such that

Arguing as in the proof of Theorem 2.7, we see that is tight, and by Theorem 2.7 converges to a limit that is supported on the set of solutions to the McKean–Vlasov problem (7)-(8). By Skorokhod representation, we may assume that this happens almost surely on some stochastic basis . Since the map is bounded and lower semicontinuous on , Fatou’s Lemma and the Portmanteau theorem imply

Defining , let denote the canoncial process on . By the arguments in the proof of Theorem 2.7 we have that is Brownian motion under with respect to the filtration generated by , and we see that is an admissible reference space for almost every . Since corresponds to the law of a solution to the McKean–Vlasov problem (7)-(8), it follows that almost surely. We have therefore obtained

| (25) |

Step 2: We show that . Let be a probability space and be an optimizer attaining , whose existence was shown in Theorem 2.4. Let be the product space obtained by taking copies of , and consider the (random) cost functional

| (26) |

where is the supremum norm on . Let be the set of all -measurable random variables, defined on the stochastic basis , taking values in and consider the problem

| (27) |

Letting be the vector obtained by taking i.i.d. copies of , and choosing , which we abbreviate in the following with , we obtain

Noting that is the empirical cumulative distribution function of the i.i.d. random variables , and that , the same estimates as in Step 1 of the proof of Proposition 6.1 in [27] show that

We have therefore shown that

Now choose a sequence such that .

Define the sequence of events and set , where is the minimal solution on with drift . With this choice, is in and satisfies

Here we used that and . This implies

| (28) |

Since , the monotonicity of implies that

| (29) |

where is defined as in (21) with initial condition . Combining (29) with (28) and again using the monotonicity of , we obtain

A straightforward induction then shows that for all , and Lemma 2.6 then yields that we have

where corresponds to the loss process associated to the particle system with initial condition . This yields

Since we have already shown that , this shows , which concludes the proof. ∎

Remark 2.9.

We conjecture that the perturbation in the initial condition of the particle system in Theorem 2.8 is an artefact of our proof technique rather than a necessity.

Theorem 2.10.

Let be a probability space and be an optimizer attaining . Let be the product space obtained by taking copies of and let be the vector obtained by taking i.i.d. copies of . Then, is -optimal for the particle system, i.e., for every , it holds that

for sufficiently large.

Proof.

Let be given. Recall the notation introduced in Step 2 of the proof of Theorem 2.8. Consider the problem

| (30) |

Proceeding as in Step 2 of the proof of Theorem 2.8, it follows that . By Theorem 2.8, we have , and therefore for large enough. Arguing as in Step 2 of the proof of Theorem 2.8, we can find such that and holds. Choosing large enough such that , we obtain

∎

3 Numerical solution of the MFC problem

In this section, we present a numerical scheme for the central agent’s mean-field control problem. We directly compute the optimal feedback control by a policy gradient method (PGM; see Section 3.2 and 3.3) applied to a regularised version of the dynamics and the objective function (see Section 3.1). The gradient is approximated by finite difference schemes for the density of the forward process and a decoupling field for an adjoint process (see Section 3.4). This will allow us to conduct parameter studies of the optimal strategies as well as the resulting losses and costs in Section 3.5.

Recall from (10) and above the process corresponding to the minimal solution , and write the objective function as

| (31) |

where , and derivatives of are defined in a distributional sense if necessary.

In the case of regular solutions, the absorbed process associated with (7), , for the hitting time of 0, has a sub-probability density supported on and an atomic mass at . Similarly as in [30, Theorem 1.1], it satisfies the forward Kolmogorov equation

| (32) |

where

| (33) |

and where denotes the set of all where is differentiable. If , in particular in the event of a blow-up at , we have the following jump condition for the solution of (32), .

Assuming again regular enough solutions where we can take the derivative with respect to time of the equation , we find that

Moreover, we can rewrite the controlled dynamics of for as

| (34) |

Note that the current control problem lies outside the standard MFC context due to the following three main aspects: (i) the interaction through the boundary leads to a time derivative of the measure component, which makes the problem as written in (34) (without replacing by ) ‘non-Markovian’; (ii) the drift coefficient is non-Lipschitz in the measure component; (iii) the dynamics are defined by an absorbed process, which moreover has an irregular drift coefficient (as can be discontinuous in time). We will address these points by a regularisation in the next section, which will subsequently allow us to apply a policy gradient method, which is inspired by [56].

3.1 Regularisation

Denote by the law of corresponding to in the regular case where a density exists. For (small) , we approximate in terms of the measure by

where is a smooth approximation of the Dirac distribution with support in and where the bracket notation is used to denote the integral.

We then define a smooth function such that for and for , for some , and consider the dynamics

| (35) |

where

For completeness, we give the specific and used in our computations in Appendix B.1. There, we also show the graphs of and its first two derivatives for the value , which is frequently used in our tests below.

Under the dynamics (35), the process does not get absorbed at 0, but once it crosses 0 from above its diffusion and drift coefficients decay rapidly so that with high probability it remains in the interval (see Figure 4 for an illustration of the density of such a process).

The reason why we consider these modified dynamics is to cast the absorbed process into a standard McKean–Vlasov framework. The objective function can also be rewritten and becomes

| (36) |

A crucial point here is that both the coefficients in the dynamics and the objective can be written in terms of and alone, i.e. without any time (or spatial) derivatives of the measure flow . Note also that satisfy the differentiability assumptions made [1, Section 3], which we shall need for the Fréchet differentiability of the function defined in (40) below.

Once we have the optimal control in feedback form for , and the associated density of , we can compute the optimal loss and cost pair as

| (37) | |||||

| (38) |

3.2 Policy gradients

We follow here in spirit the approach of [56]. We consider first a slightly more general form of the MFC problem, written as a nonsmooth optimization problem over the Hilbert space of -valued square integrable, progressively measurable processes,

| (39) |

with the functionals and defined as follows: for all ,

| (40) |

where is defined in (36).

The splitting of the objective function into and allows for a separate treatment of the smooth component and a non-smooth component . We will use to incorporate the constraints on , specifically, for and outside. It is clear that is convex due to the convexity of .

Assuming that lies in the Wasserstein space of probability measures on with finite second moment, denoted by , we introduce the Hamiltonian by

| (41) |

with

| (42) |

Moreover, by [1, Lemma 3.1], is Fréchet differentiable and its derivative satisfies for all ,

| (43) |

-a.e. Here, is the state process controlled by , satisfying (35), and are square integrable adapted adjoint processes such that for all ,

| (44) | ||||

Above and hereafter, we use the tilde notation to denote an independent copy of a random variable as in [1].

We now consider controls in feedback form, namely , which determine as solution of

| (45) |

Then a sufficiently smooth decoupling field such that and satisfies

| (46) |

with terminal condition .

Computation of gradient by decoupling fields

In our application, we can express the right-hand side of (LABEL:decoupling_pde) more explicitly. For the Hamiltonian (41) with and defined by (35) and (36), respectively, we have, by [24, Section 5.2.2, Example 1]

Consequently, for the decoupling field , with ,

which can be re-written as

As , we obtain

| (47) |

where we will assume that has a density which satisfies

| (48) |

3.3 A proximal policy gradient method (PGM)

We now compute a sequence of approximations to the optimal control in feedback form, namely . Following [56], we will carry out proximal gradient steps with given, e.g. zero, and thereafter, for step size ,

| (49) | ||||

where is the proximal map of such that

For the considered , an indicator function, is simply the projection onto , i.e. .

Then a sufficiently smooth decoupling field such that satisfies

| (50) |

where for the density that satisfies

| (51) |

and where

Finally,

| (52) |

3.4 Numerical implementation

We pick regularisation parameters for and defined as above. Then in the -th iteration, we first solve numerically (51) for and then (LABEL:decoupling_pde) for , where is the measure with density . We use a semi-implicit finite difference scheme on a non-uniform mesh, as detailed below.

We define a numerical approximation on a time mesh , , for a positive integer .

We also define a non-uniform spatial mesh with , for , .

In the following, we drop the iteration index and use instead superscript to denote the timestep of any function defined on the space-time mesh and subscript its spatial index, in particular, for the numerical PDE solutions, , . We assume a feedback control is defined on this mesh.

Starting with the forward equation (51), for each and , we approximate the drift coefficient by

| (53) |

and set . Then define a finite difference scheme by , and for ,

This is an upwind scheme for the first order terms, taking the appearance of in explicit, but otherwise implicit. The form of the scheme is chosen to be consistent with (51) for non-uniform meshes, in particular where the mesh size is piecewise constant.

For the adjoint equation (3.2), with now given in addition to , we first define the right-hand side,

| (54) |

and then, with , we define for

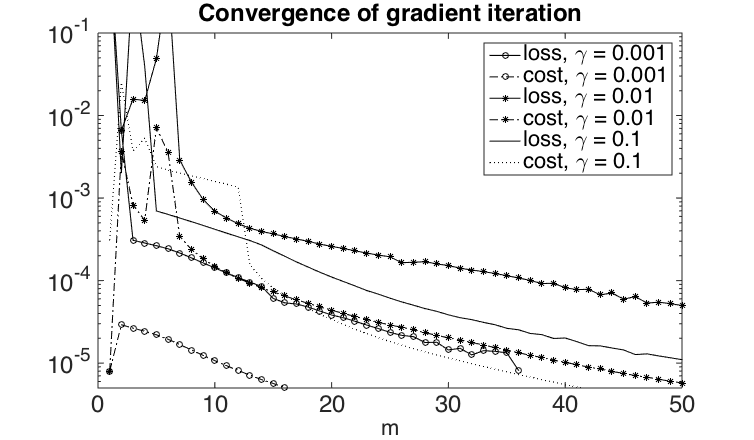

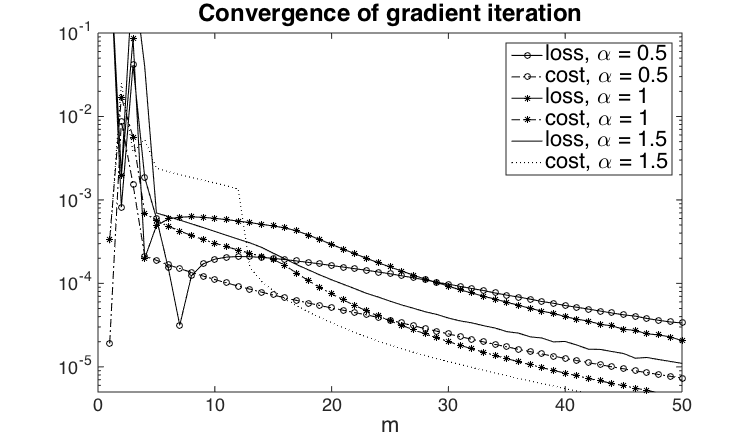

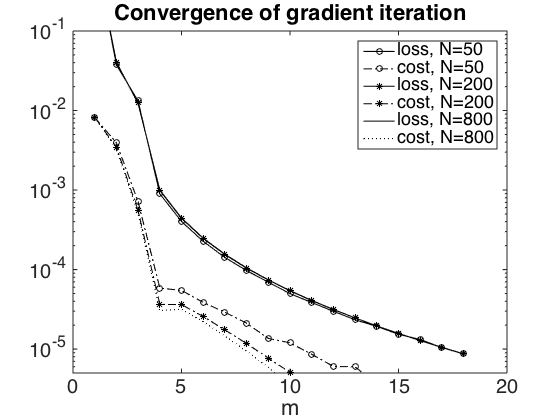

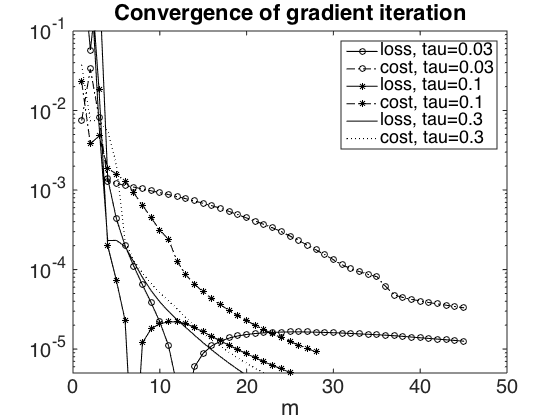

Let us remark that we do not have a convergence proof for this numerical scheme and it also seems out of reach due to the delicate interplay between the discretization and regularization parameters visible from Table 1. Nevertheless, for fixed and we can empirically show convergence of the gradient iterations (see Figure 1), which then allows us to compute approximate optimal policies. In this sense our numerical tests indicate at least qualitatively how the optimal policies look like. Note that a rigorous convergence proof of a similar policy gradient iteration method in the non-mean field regime has recently been provided in [57].

Set-up and model parameters

In the rest of the paper, we give illustrations of the model’s suggested strategies and resulting loss behaviour in different market scenarios, influenced by the interaction parameter , the risk aversion , the initial state , and maximum cash injection rate .

In all examples, we choose a gamma initial density,

| (56) |

The parameters of the initial distribution could be calibrated to CDS spreads if they are traded (see [15]). The default parameters we use are , , chosen to give a range of different behaviours by varying the other parameters. In this case, is differentiable with . This choice implies that there are smooth solutions for a short enough time interval (see [37, 30]). It also implies (see [37, Theorem 1.1]) that a blow-up (of the unregularised system) is guaranteed to happen at some time for . Conversely, it is known (see [47, Theorem 2.2 and the comment below it]) that the condition leads to the so-called weak feedback regime, where continuity of solutions always holds true.

A simple estimation of meaningful from typical asset volatilities, recovery rates, and mutual lending as proportion of overall debt is found in [48], suggesting possible values from 0.3 to possibly higher than 5. We shall conduct tests for . With , it is clear that a jump cannot occur for , but is guaranteed for as then . The terminal time is chosen as . We find empirically that the uncontrolled system does not jump in this interval for (although it may jump eventually), and does jump halfway through the interval for . We have intentionally chosen an initial distribution where blow-ups can happen at such relatively short time scales to illustrate the different effects. In our regularised version of the problem, this manifests in a smooth transition to high values of losses, around 60%, over a short period of time. We fix at first, and investigate the effect of larger values later on.

Mesh convergence

We first analyse the convergence of the finite difference approximations for fixed control. In particular, we first choose . The interaction parameter is .

The mesh is chosen uniformly in the intervals , , , such that approximately 5% of the points lie in the first interval, 45% in the second, and 50% in the third, and the total number of spatial mesh points is approximately . This has the effect that the average mesh size is roughly eight times the time step size, which turns out a reasonable ratio in our numerical tests.

It is of crucial importance to have enough mesh points in the intervals and to approximate the smoothed Heaviside function and the smoothed delta distribution with its first two derivatives. A strong local mesh refinement as above allows this while keeping the total computational complexity feasible. Notice for our choice above the local mesh size around zero is almost 100 times smaller than for larger .

In Table 1, we report for a varying number of time-steps (and proportionally chosen ) and smoothing parameter the computed loss (columns 5–10, rows 3–8). Let be the loss computed with time steps and parameter . Then from the table we conjecture convergence of as for fixed , but divergence as for fixed .

| CPU | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| (s) | ||||||||||

| 1.956 | -2.42 | 0.5643 | 0.6430 | 0.7137 | 0.8324 | 4.7756 | 0 | 0.44 | ||

| -0.806 | 1.31 | 0.5663 | 0.6260 | 0.6693 | 0.7268 | 0.8384 | 5.1210 | 1.2 | ||

| -0.614 | 1.82 | 0.5655 | 0.6164 | 0.6481 | 0.6778 | 0.8223 | 0.0336 | 4.2 | ||

| -0.337 | 1.94 | 0.5649 | 0.6118 | 0.6376 | 0.6589 | 0.6884 | 0.6096 | 17 | ||

| -0.173 | — | 0.5645 | 0.6096 | 0.6327 | 0.6486 | 0.6647 | 0.6893 | 83 | ||

| — | — | 0.5643 | 0.6085 | 0.6304 | 0.6440 | 0.6548 | 0.6680 | 427 | ||

| 4.414 | 2.192 | 1.354 | 1.084 | 1.322 | — | |||||

| 2.01 | 1.61 | 1.24 | 0.81 | — | — |

To investigate this more quantitatively, we report in the third and fourth columns and , where . The fact that, for fixed , the increments for successive mesh refinements decrease inversely proportional to is consistent with first order convergence in and . Conversely, we fix and examine and in the last two rows. The behaviour indicates a decrease of first order in as long as is small compared to , but divergence thereafter. Finally, the approximate computational times, reported in the last column, are approximately linear in and independent of .444Computations performed using Matlab on a 2.8 GHz Intel Core i7 with 16 GB 1600 MHz DDR3.

A similar behaviour is observed for the approximation of the cost and for different parameters, as shown in Appendix B.2.

Convergence of policy gradient iteration (PGM)

Next, we analyse the convergence of the policy gradient iteration. Here and thereafter, we will use a modification whereby (49) is evaluated for , while for . As the occupation time of is small, the effect of this choice has a negligible effect on the expected cost in all cases. We found that this modified iteration converged faster and more reliably in our numerical tests.

We monitor in each iteration the loss at time computed as in (53), and the expected cost, computed as in (55). For and the terminal loss and total expected cost at the -th iteration, respectively, we plot in Figure 1 the steps and . In these tests, the iteration terminates if either both of these quantities are smaller than or 50 iterations are reached.

The left-hand plot in Figure 1(a) shows the convergence for different values of . The intermediate value of has the largest absolute error, while the smallest leads to the smallest one. In the latter case, the cost is very small due to the very small penalty of losses. The asymptotic rate of convergence appears similar for all parameters considered.

In Figure 1(b), we analyse the effect of on the convergence. The error is largest for the smallest of , while the error is smallest for , which is the case where a jump occurs in an uncontrolled setting and losses are the largest.

Further parameter studies are given in the Appendix, where Figure 10(a) establishes robustness of the convergence under mesh refinement and Figure 10(b) illustrates the effect of the step size.

In most situations, the number of iterations required for reasonable accuracy, i.e. a relative error below around was between 10 and 30, so that for the chosen discretisation (with timesteps and mesh as chosen above) the computing time to solve the MFC problem was between 3 and 10 minutes on the laptop as specified earlier.

3.5 Computational analysis of central agent’s strategy

We now move to an analysis of the optimal strategies, and the achievable pairs of costs and losses under the optimal and other strategies.

Analysis of the optimal strategy

The policy gradient method produces directly an approximation to the optimal feedback control . We found that an initialisation of the iteration with a function of the form for and 0 elsewhere, for some large enough so that the support of covers the support of , produces more regular controls for small iteration numbers than a zero initialisation. The following plots were produced with and a tolerance in the loss and cost (compare Figure 1(a)).

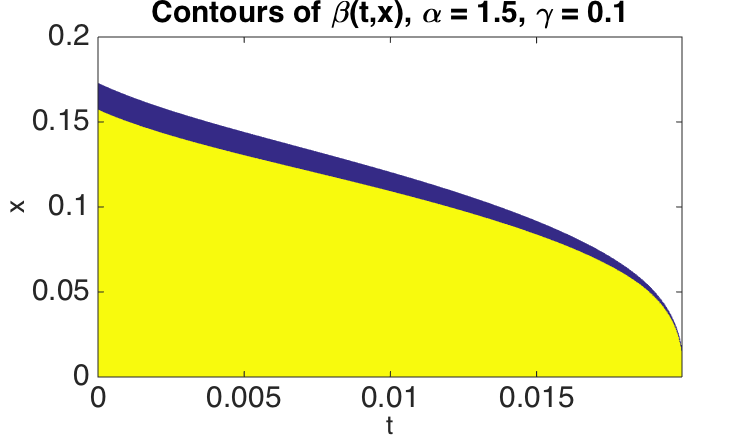

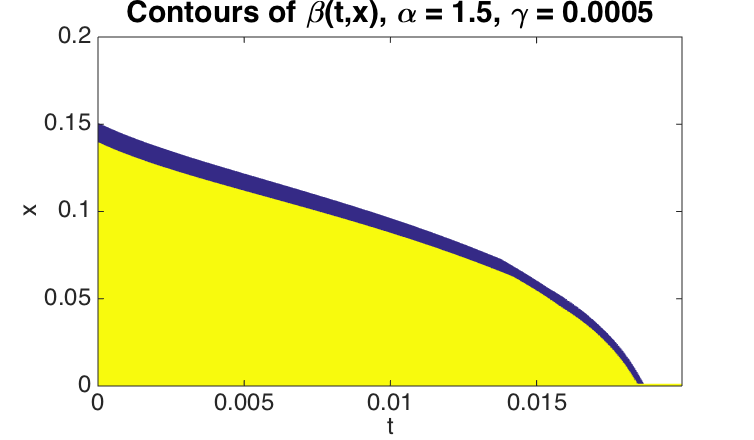

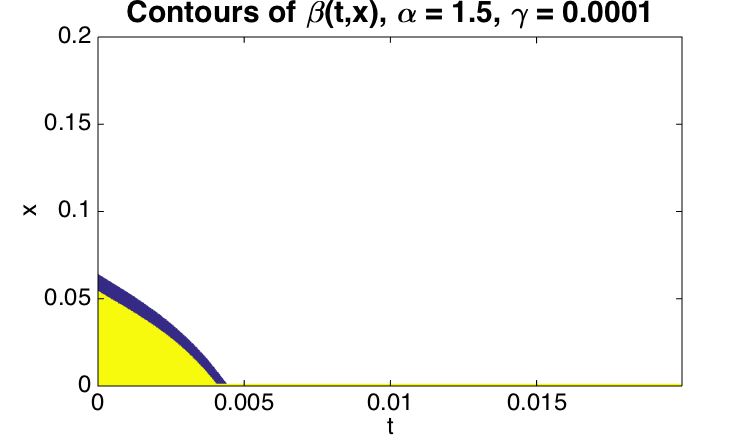

We depict in Figure 2 contours of the optimal feedback control for different . As expected from the form of the Hamilton-Jacobi-Bellmann equation, the control is close to a ‘bang-bang’ structure, i.e. a piecewise constant function where the control always takes one of the two extreme values,i.e. either or . The two regions are separated by a narrow strip where the control transitions continuously. We conjecture this to be an effect of the numerical procedure, which is designed for Lipschitz continuous feedback controls.

The (yellow) shaded region closest to is where , i.e. the central agent subsidises firms closest to default at or close to the maximum rate. The white region furthest from is where , i.e. the central agent does not subsidise firms with high reserves.

For larger , here exemplified by in Figure 2(a), the contribution of the loss to the objective is large enough for the central agent to act for all , for values in up to a decreasing curve in . Close to the chosen end point, the effect of the control on the overall losses becomes negligible and does not justify the associated cost. In a sense this behaviour is an artifact of the finite observation interval.

For smaller , in Figures 2(b) and 2(c), the agent only acts (for sufficiently small states) up to a certain point in time and then does nothing. Combining this with the plots of the resulting loss curves in Figure 3, a possible interpretation is that the agent seeks to delay the onset of the strongly contagious phase until it is no longer viable to do with a certain cost budget, depending on . In particular, as visible from Figure 3, under the current optimization criterion the jump is not avoided for . We discuss at the end of the next subsection other strategies for avoiding jumps – for the current optimisation criterion such a strategy is however not necessarily optimal.

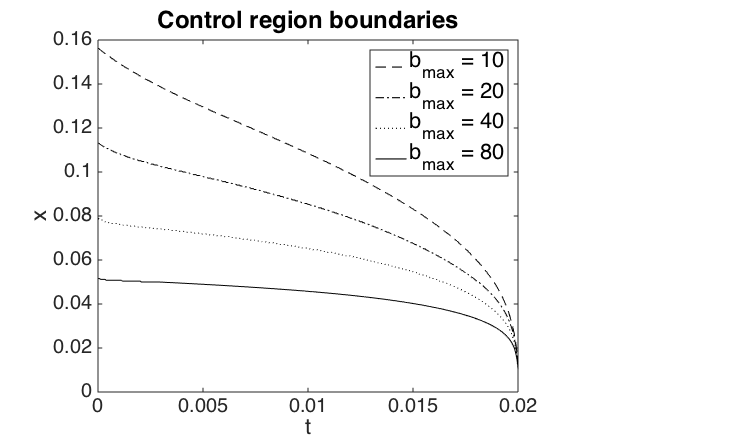

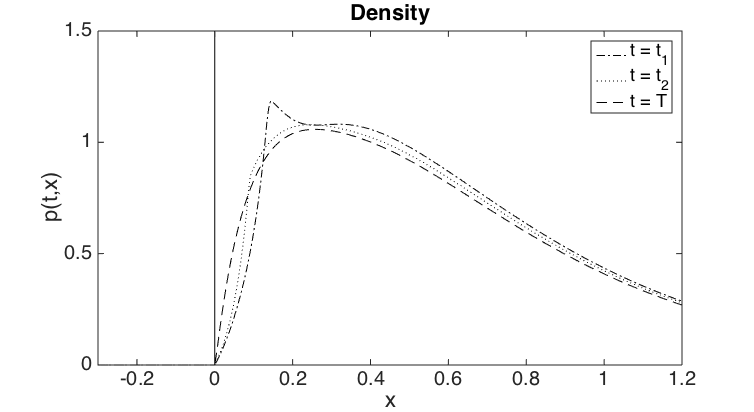

Next, we analyse the impact the upper bound of on the control strategy. We show only the level set for clarity in Figure 4, for different . The region under this curve indicates where the agent controls at (or close to) the maximum rate. The region shrinks as increases, meaning that the agent is able to control the banks’ equity process more effectively whenever it gets close to zero.

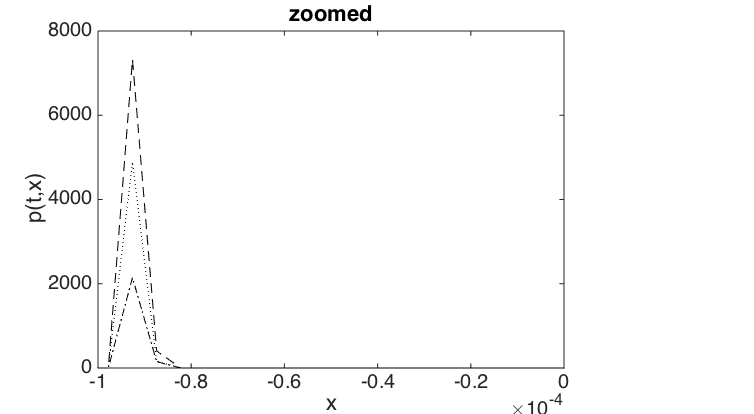

Lastly in this section, we analyse the behaviour of the PDE solutions and at different times and on different scales in around 0. Figure 5 shows in the left panel the accumulation of probability mass in the interval due to the smooth truncation of the SDE coefficients, approximating the absorption at . As can be deduced from the right plot in Figure 5, the area under the density for positive is thus reduced, but only by a small amount in the current parameter setting (see Figure 3 for the corresponding loss function with ).

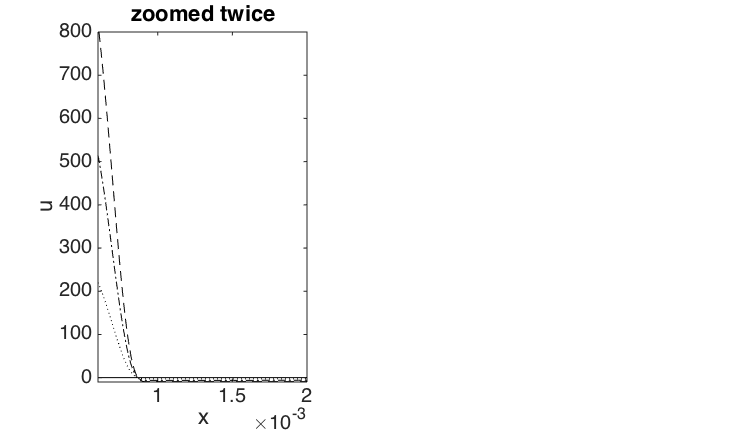

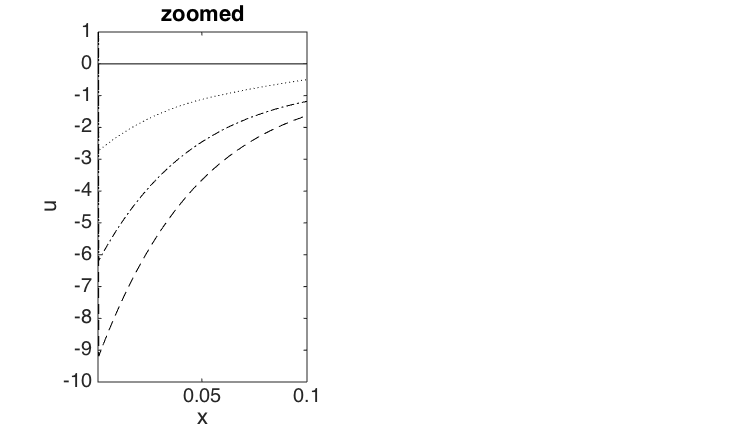

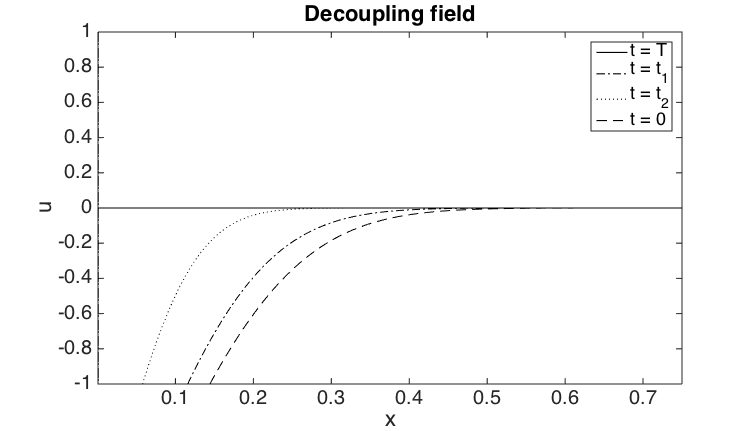

In Figure 6 we illustrate the behaviour of on different scales in . The left-most plot shows the range , where attains large positive values; in the middle plot, over , has moderate negative values; the right-most plot is truncated below by , this being the threshold which determines where the control is active. This can be seen from (52) in conjunction with (49): for , the gradient is , so for a converged control we have where and where . From this the bang-bang structure of the control becomes also clear.

Analysis of optimal cost-loss pairs

Finally, we examine the pairs of costs and losses that are obtained under the optimal policy and other heuristic strategies.

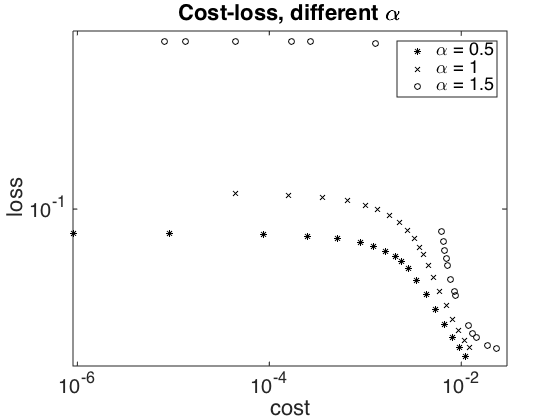

In Figure 7(a), we vary to trace out the curve , where and are the costs and losses given by (37) and (38) for the chosen . For a given cost, the graph gives the loss achievable under the optimal strategy. To achieve a smaller loss, a higher cost is generally incurred.

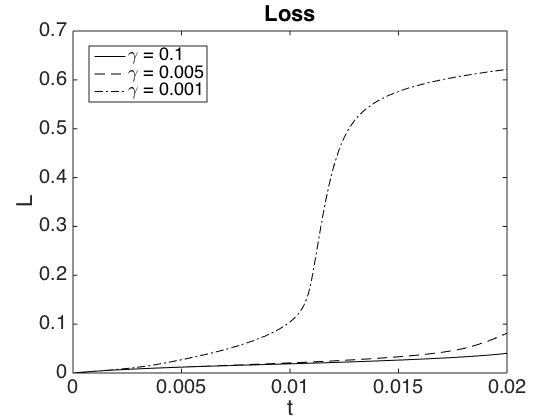

We focus first on the data for and . In these cases, the uncontrolled system exhibits no jumps and cash injection simply reduces the losses. For small , minimising the cost is the priority and the losses approach those of the uncontrolled system. For growing , it becomes favourable to increase the cash injection and a significant reduction of losses can be achieved. This levels off for large as the cap on the cash injection rate limits the overall effect of bail-outs.

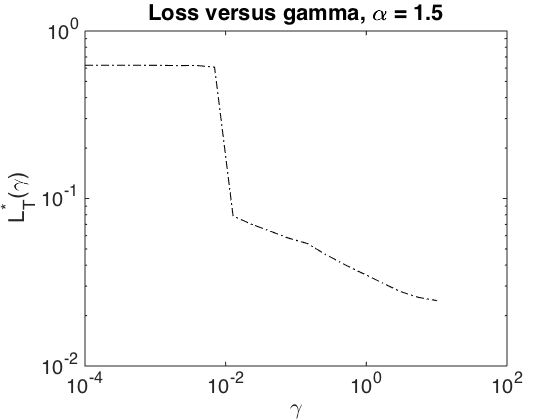

For strong interaction, here exemplified by , we observe a discontinuity, which is further analysed in Figure 7(b). For around 0.01, the optimal strategy switches from not preventing a jump to preventing a jump. This is manifested in Figure 7(b) by an downward discontinuity in the number of losses. The optimal value of the central agent’s control problem is also discontinuous in at this point. In other words, it is not possible to vary the capital injection to control the size of the jump continuously. Rather, the possible jump size is restricted by the constraint (4) on physical solutions. Conversely, withdrawal of a small amount of cash by the central agent from a scenario with low losses can trigger a large systemic event.

Note that Figure 7(b) also allows to deduce the relation between and the threshold by looking for such that , as explained in the introduction. Indeed, this corresponds to solving the outer optimization problem where with denoting the Lagrange function. Under the assumption of no duality gap and a unique optimizer , is necessarily determined via . As we observe a jump discontinuity of , this suggests that there is a duality gap at least for certain values of .

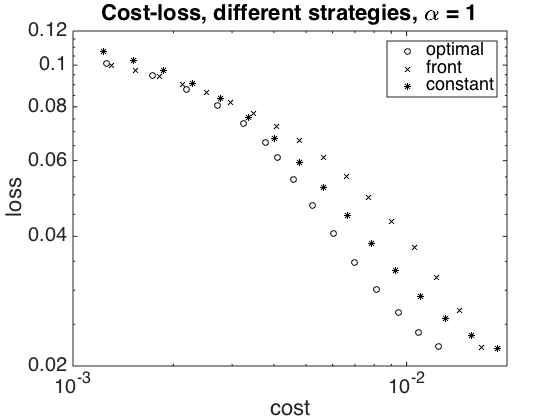

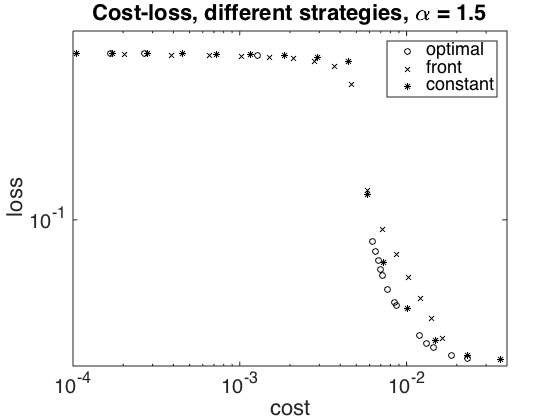

We proceed by comparing the costs and losses under the optimal strategy with some other heuristic strategies. As first benchmark, we consider a uniform strategy by which the central agent injects cash at a constant rate whenever an agent’s value for a constant , which we vary, resulting in pairs . The total cost here can be computed as , where is the density of the regularised process with such uniform (in time) control.

We also consider a ‘front loaded’ strategy whereby at the outset, for some chosen ‘floor’ , the central agent injects a lump sum of into all players with , hence lifting their reserves up to . Again, we vary to obtain a parametrised curve . The total cost in this case is found as .

The pairs of cost and loss are shown in Figure 8. In particular, Figure 8(a) illustrates the case without jump for , whereas in the situation of 8(b) with there is a jump in the uncontrolled system, which can be avoided with sufficiently large control.

In both cases, the optimal strategy gives lower losses than the heuristic strategies for the same fixed cost. Conversely, less cash injection is required for a given loss tolerance.555Note that the strategy with upfront payments is not in the class of Lipschitz feedback controls for which the policy gradient method is designed.

We observe that we cannot enforce the sufficient condition for avoiding jumps, i.e., , for any of these strategies. It is clear that the strategy where the initial capital of all banks is raised to a certain minimum level satisfies and hence the necessary condition for avoiding jumps, , holds for . However, the sufficient condition can be violated even when all banks have a high initial capital. What would work to enforce the sufficient condition is to set for some , and the uniform distribution on .

Considering the physical jump condition (4), for a jump to occur it matters how much of the surviving mass can be concentrated around zero at any given point. Intuitively, starting with a higher initial condition, the Brownian motion will diffuse the mass sufficiently and make large concentrations at zero less likely, hence preventing a jump. Similarly, sufficiently large for small and should transport mass away from zero and prevent a jump as long as the initial density satisfies (which rules out an instantaneous jump). Therefore, both the constant and optimal strategies should be able to prevent jumps for large enough . A rigorous analysis, however, goes beyond the scope of this paper.

Appendix A Proofs

A.1 Notation

Throughout the paper, denotes the space of càdlàg functions on endowed with the -topology, denotes the space of continuous functions on endowed with the topology of compact convergence, i.e., in if and only if uniformly for every compact . If is a Polish space, we denote the space of probability measures on by and endow it with the topology of weak convergece, i.e., we say that in iff for all . If and , we denote the integral of with respect to also with brackets, i.e., we write . Furthermore, if is the pushforward of the measure with respect to the map , we denote this by .

A.2 Existence of minimal solutions and optimizers

Lemma A.1.

For any , define the process

| (57) |

Then, the process satisfies the extended crossing property, i.e.,

| (58) |

for any stopping time with respect to , the natural filtration generated by .

Proof.

Let be a stopping time. Since is almost surely bounded, by Novikov’s condition and Girsanov’s theorem we may find an equivalent probability measure such that is a -Brownian motion under . The strong Markov property of Brownian motion then yields

and by the equivalence of and the claim follows. ∎

A.3 Existence of solutions

Lemma A.2.

Suppose that in . Then, uniformly in on any compact subset of .

Proof.

Let . By weak -convergence, we have for any . Let and choose with such that

| (59) |

Choose large enough such that for all . We obtain, for ,

which yields the claim. ∎

Proof of Theorem 2.2.

. Step 1: We construct the reference probability space .

Since the sequence is constant and the space (endowed with the product topology of Euclidean and uniform topology) is Polish, the sequence is tight on . Since is compact, the sequence is tight on . By Prokhorov’s theorem, after passing to a subsequence if necessary, we may assume that in . By the Skorokhod representation theorem, we may without loss of generality assume that holds almost surely on some probability space, which we denote by . Note that this is possible since the property of solving (7)-(8) only depends on the (joint) law of . We then define to be for . Since is measurable and -adapted, it admits a progressively measurable modification, which we again denote by , and we see that . We next show that is a -Brownian motion: by the continuous mapping theorem and the continuity of the coordinate projections, it follows that is the Wiener measure. Let and let and and set , then we have by dominated convergence

Since the Borel -algebra on is generated by the evaluation mappings, we obtain that is independent of for , and therefore is an -Brownian motion. We have shown that is an admissible reference space.

Step 2: Since is compact, after passing to subsequences if necessary, we may assume that in . We now show that solves (7)-(8) on . Let be endowed with the product topology and define and analogously as . By Lemma A.2, it follows that in almost surely. Since is deterministic, it follows that in distribution on . We introduce some notation: define for and as

| (60) |

For and , define the path functionals and . Then, is a solution to (7)-(8) on if and only if . We may write this condition equivalently on the canonical path space as for . Note that with the notational conventions explained in Section A.1, denotes the pushforward of the measure by the map and denotes the integral of the functional with respect to . Since satisfies the extended crossing property by Lemma A.1, satisfies the crossing property (cf the proof of Lemma 5.5 in [27]). Lemma 5.3 in [27] and Step 1 imply that

| (61) |

in . ∎

A.4 Proof of Theorem 2.7

Proof.

The proof is to a large extent analogous to the proof of Proposition 5.6 in [27]. Define

Since is a random probability measure on and the spaces and are compact, is tight by the same reasoning as in Corollary 4.5 in [27]. Therefore, after passing to a subsequence if necessary, we may assume that for some random probability measure on By Skorokhod representation, we may assume without loss of generality that the convergence happens almost surely on the same probability space . Arguing in the same fashion as in the proof of Lemma 5.4 in [27], we see that for almost every , if , then is a Brownian motion with respect to the filtration generated by . For , set , where is defined as in (60). By Lemma A.2, the map is continuous from to , and therefore also as a map from to . Theorem 4.2 in [27] together with Corollary 12.7.4 in [59] then shows that is continuous. Since , the continuous mapping theorem implies that . Applying the continuous mapping theorem to , we see that holds almost surely. It remains to check that if , then for holds -almost surely for almost every . This can be checked as in Step 1 of the proof of Proposition 5.6 in [27], making use of Lemma A.1 to show that satisfies the crossing property (almost surely). ∎

Appendix B Further numerical details and tests

We here report further details and tests of our numerical procedure.

B.1 Smoothing

Let us start by precisely specifying the smoothing functions and used in the regularization procedure of the objective function and the dynamics. We choose , where,

| (64) |

where normalises the integral (close) to 1. The function and its first two derivatives are shown in Figure 9 for . Note in particular the large positive and negative values of .

We also choose for some , , where , , and 0 else, with the standard normal CDF.

B.2 Mesh convergence

Here, we demonstrate the convergence of the finite difference approximation in two more settings. In Table 2 for the cost, for , and in Table 2 again for the losses, but now for . The notation with , and is analogous as before.

| -1.650 | 1.86 | 1.2548 | 1.1449 | 1.0225 | 0.8010 | 0.0526 | 0.5638 | ||

| -0.887 | 0.83 | 1.2383 | 1.1115 | 1.0085 | 0.9004 | 0.6965 | 0.0343 | ||

| -1.066 | 1.99 | 1.2294 | 1.0970 | 0.9939 | 0.9246 | 0.6131 | 0.4506 | ||

| -0.534 | 2.00 | 1.2187 | 1.0846 | 0.9839 | 0.9126 | 0.8484 | 1.0968 | ||

| -0.267 | — | 1.2134 | 1.0784 | 0.9790 | 0.9126 | 0.8644 | 0.8199 | ||

| — | — | 1.2107 | 1.0753 | 0.9764 | 0.9123 | 0.8701 | 0.8365 | ||

| -1.354 | -0.989 | -0.641 | -0.422 | -0.335 | — | ||||

| 1.37 | 1.54 | 1.51 | 1.25 | — | — |

| 3.802 | 1.99 | 7.3549 | 7.4198 | 7.6336 | 8.7134 | 735.42 | 0 | ||

| 1.910 | 2.03 | 7.3929 | 7.4573 | 7.4919 | 7.6925 | 8.7711 | 735.91 | ||

| 0.941 | 2.00 | 7.4120 | 7.4771 | 7.5103 | 7.4765 | 9.5999 | -4.196 | ||

| 0.470 | 2.00 | 7.4214 | 7.4868 | 7.5203 | 7.5373 | 7.5867 | 6.2291 | ||

| 0.235 | — | 7.4261 | 7.4916 | 7.5251 | 7.5421 | 7.5504 | 7.5550 | ||

| — | — | 7.4285 | 7.4939 | 7.5275 | 7.5445 | 7.5531 | 7.5571 | ||

| 0.6547 | 0.3353 | 0.1701 | 0.0860 | 0.0398 | — | ||||

| 1.95 | 1.97 | 1.97 | 2.15 | — | — |

In these settings, the behaviour in is somewhat better than in Table 1 (losses for , i.e. with jump in the uncontrolled case), but as there, a good approximation is only achieved if the mesh size is sufficiently small in comparison with .

B.3 Gradient iteration

Finally we conducted further tests in view of the mesh refinement and the role of the step size in the gradient iteration.

Figure 10(a), left, illustrates that the convergence is robust with respect to mesh refinement, i.e., the number of iterations required for a prescribed accuracy does not increase significantly as the number of time steps and mesh points increases simultaneously.

In Figure 10(b) we investigate the effect of the step size . Choosing small leads to poor convergence, while is optimal among the values presented here. Picking even larger step sizes can lead to divergence.

Declaration

Funding: The authors gratefully acknowledge financial support by the Vienna Science and Technology Fund (WWTF) under grant MA16-021 and by the Austrian Science Fund (FWF) through grant Y 1235 of the START-program.

References

- [1] B. Acciaio, J. Backhoff-Veraguas, and R. Carmona, Extended mean field control problems: stochastic maximum principle and transport perspective, SIAM J. Control Optim. 57 (2019), no. 6, 3666–3693.

- [2] Y. Achdou and I. Capuzzo-Dolcetta, Mean field games: numerical methods, SIAM J. Numer. Anal. 48 (2010), no. 3, 1136–1162.

- [3] Y. Achdou and M. Laurière, On the system of partial differential equations arising in mean field type control, Discr. Contin. Dyn. Sys. 35 (2015), no. 9, 3879–3900.

- [4] , Mean field type control with congestion (II): An augmented Lagrangian method, Appl. Math. Optim. 74 (2016), no. 3, 535–578.

- [5] , Mean field games and applications: Numerical aspects, Mean Field Games (2020), 249–307.

- [6] N. Agram and B. Øksendal, Fokker–Planck PIDE for McKean–Vlasov diffusions with jumps and applications to HJB equations and mean-field games, arXiv:2110.02193 (2021).

- [7] Clémence Alasseur, Luciano Campi, Roxana Dumitrescu, and Jia Zeng, MFG model with a long-lived penalty at random jump times: application to demand side management for electricity contracts, arXiv:2101.06031 (2021).

- [8] Andrea Angiuli, Nils Detering, Jean-Pierre Fouque, Mathieu Laurière, and Jimin Lin, Reinforcement learning for intra-and-inter-bank borrowing and lending mean field control game, arXiv preprint arXiv:2207.03449 (2022).

- [9] Andrea Angiuli, Nils Detering, Jean-Pierre Fouque, and Jimin Lin, Reinforcement learning algorithm for mixed mean field control games, arXiv preprint arXiv:2205.02330 (2022).

- [10] Andrea Angiuli, Jean-Pierre Fouque, and Mathieu Lauriere, Reinforcement learning for mean field games, with applications to economics, arXiv preprint arXiv:2106.13755 (2021).

- [11] Andrea Angiuli, Jean-Pierre Fouque, and Mathieu Laurière, Unified reinforcement q-learning for mean field game and control problems, Mathematics of Control, Signals, and Systems (2022), 1–55.

- [12] Richard Archibald, Feng Bao, Jiongmin Yong, and Tao Zhou, An efficient numerical algorithm for solving data driven feedback control problems, Journal of Scientific Computing 85 (2020), no. 2, 1–27.

- [13] E. Bayraktar, A. Cosso, and H. Pham, Randomized dynamic programming principle and Feynman–Kac representation for optimal control of McKean–Vlasov dynamics, Transactions Amer. Math. Soc. 370 (2018), no. 3, 2115–2160.

- [14] Alain Bensoussan, Jens Frehse, and Sheung Chi Phillip Yam, The master equation in mean field theory, Journal de Mathématiques Pures et Appliquées 103 (2015), no. 6, 1441–1474.

- [15] K. Bujok and C. Reisinger, Numerical valuation of basket credit derivatives in structural jump-diffusion models, J. Comp. Finance 15 (2012), no. 4, 115.

- [16] M. Burzoni and L. Campi, Mean field games with absorption and common noise with a model of bank run, arXiv:2107.00603 (2021).

- [17] L. Campi and M. Fischer, -player games and mean-field games with absorption, Ann. Appl. Probab. 28 (2018), no. 4, 2188–2242.

- [18] L. Campi, M. Ghio, and G. Livieri, -player games and mean-field games with smooth dependence on past absorptions, Available at SSRN 3329456 (2019).

- [19] E. Carlini and F. J. Silva, A semi-Lagrangian scheme for a degenerate second order mean field game system, Discr. Contin. Dyn. Sys. 35 (2015), no. 9, 4269–4292.

- [20] R. Carmona and F. Delarue, Forward–backward stochastic differential equations and controlled McKean–Vlasov dynamics, Ann. Probab. 43 (2015), no. 5, 2647–2700.

- [21] R. Carmona, F. Delarue, and A. Lachapelle, Control of McKean–Vlasov dynamics versus mean field games, Math. Financ. Econ. 7 (2013), no. 2, 131–166.

- [22] R. Carmona, J.-P. Fouque, and L. H. Sun, Mean field games and systemic risk, Comm. Math. Sci. 13 (2015), no. 4, 911–933.

- [23] R. Carmona and M. Laurière, Convergence analysis of machine learning algorithms for the numerical solution of mean field control and games: II – the finite horizon case, arXiv:1908.01613 (2019).

- [24] René Carmona and François Delarue, Probabilistic Theory of Mean Field Games with Applications I, Springer, 2018.

- [25] René Carmona and Mathieu Laurière, Deep learning for mean field games and mean field control with applications to finance, arXiv preprint arXiv:2107.04568 (2021).

- [26] C. Cuchiero, C. Reisinger, and S. Rigger, Implicit and fully discrete approximation of the supercooled Stefan problem in the presence of blow-ups, arXiv:2206.14641 (2022).

- [27] C. Cuchiero, S. Rigger, and S. Svaluto-Ferro, Propagation of minimality in the supercooled Stefan problem, Ann. Appl. Probab., to appear.

- [28] F. Delarue, J. Inglis, S. Rubenthaler, and E. Tanré, Global solvability of a networked integrate-and-fire model of McKean-Vlasov type, Ann. Appl. Probab. 25 (2015), no. 4, 2096–2133. MR 3349003

- [29] , Particle systems with a singular mean-field self-excitation. Application to neuronal networks, Stoch. Proc. Appl. 125 (2015), no. 6, 2451–2492.

- [30] F. Delarue, S. Nadtochiy, and M. Shkolnikov, Global solutions to the supercooled Stefan problem with blow-ups: regularity and uniqueness, Probab. Math. Phys. 3 (2022), no. 2, 171–213.

- [31] M. Djete, D. Possamaï, and X. Tan, McKean–Vlasov optimal control: the dynamic programming principle, arXiv:1907.08860 (2019).

- [32] Romuald Elie, Tomoyuki Ichiba, and Mathieu Laurière, Large banking systems with default and recovery: A mean field game model, arXiv preprint arXiv:2001.10206 (2020).

- [33] W. H. Fleming and H. M. Soner, Controlled Markov processes and viscosity solutions, vol. 25, Springer, 2006.

- [34] J.-P. Fouque and Z. Zhang, Deep learning methods for mean field control problems with delay, Frontiers Appl. Math. Stat. 6 (2020), 11.

- [35] Xin Guo, Anran Hu, Renyuan Xu, and Junzi Zhang, Learning mean-field games, Advances in Neural Information Processing Systems 32 (2019).

- [36] Xin Guo, Huyên Pham, and Xiaoli Wei, Itô’s formula for flow of measures on semimartingales, arXiv preprint arXiv:2010.05288 (2020).

- [37] B. Hambly, S. Ledger, and A. Søjmark, A McKean–Vlasov equation with positive feedback and blow-ups, Ann. Appl. Probab. 29 (2019), no. 4, 2338–2373.

- [38] Ruimeng Hu and Mathieu Lauriere, Recent developments in machine learning methods for stochastic control and games, Recent Developments in Machine Learning Methods for Stochastic Control and Games (May 13, 2022) (2022).

- [39] M. Huang, R. P. Malhamé, and P. E. Caines, Large population stochastic dynamic games: closed-loop McKean–Vlasov systems and the nash certainty equivalence principle, Comm. Info. Sys. 6 (2006), no. 3, 221–252.

- [40] A. Itkin and A. Lipton, Structural default model with mutual obligations, Rev. Deriv. Res. 20 (2017), no. 1, 15–46.

- [41] Bekzhan Kerimkulov, David Šiška, and Lukasz Szpruch, A modified MSA for stochastic control problems, Applied Mathematics & Optimization 84 (2021), no. 3, 3417–3436.

- [42] Daniel Lacker, Limit theory for controlled McKean–Vlasov dynamics, SIAM Journal on Control and Optimization 55 (2017), no. 3, 1641–1672.

- [43] J.-M. Lasry and P.-L. Lions, Mean field games, Japanese J. Math. 2 (2007), no. 1, 229–260.

- [44] M. Laurière and O. Pironneau, Dynamic programming for mean-field type control, Comptes Rendus Mathematique 352 (2014), no. 9, 707–713.

- [45] Mathieu Laurière, Sarah Perrin, Matthieu Geist, and Olivier Pietquin, Learning mean field games: A survey, arXiv preprint arXiv:2205.12944 (2022).

- [46] S. Ledger and A. Søjmark, At the mercy of the common noise: blow-ups in a conditional McKean–Vlasov Problem, Electr. J. Probab. 26 (2021), no. none, 1 – 39.

- [47] Sean Ledger and Andreas Søjmark, Uniqueness for contagious McKean–Vlasov systems in the weak feedback regime, Bulletin of the London Mathematical Society 52 (2020), no. 3, 448–463.

- [48] A. Lipton, V. Kaushansky, and C. Reisinger, Semi-analytical solution of a McKean–Vlasov equation with feedback through hitting a boundary, Europ. J. Appl. Math. (2019), 1–34.

- [49] R. C. Merton, On the pricing of corporate debt: The risk structure of interest rates, J. Finance 29 (1974), no. 2, 449–470.

- [50] S. Nadtochiy and M. Shkolnikov, Particle systems with singular interaction through hitting times: application in systemic risk modeling, Ann. Appl. Probab. 29 (2019), no. 1, 89–129. MR 3910001

- [51] , Mean field systems on networks, with singular interaction through hitting times, Ann. Probab. 48 (2020), no. 3, 1520–1556.

- [52] L. Pfeiffer, Numerical methods for mean-field-type optimal control problems, Pure Appl. Funct. Anal. 1 (2016), no. 4, 629–655.

- [53] H. Pham and X. Wei, Dynamic programming for optimal control of stochastic McKean–Vlasov dynamics, SIAM Journal on Control and Optimization 55 (2017), no. 2, 1069–1101.

- [54] , Bellman equation and viscosity solutions for mean-field stochastic control problem, ESAIM: Contr. Optim. Calculus. Var. 24 (2018), no. 1, 437–461.

- [55] C. Reisinger, W. Stockinger, and Y. Zhang, A fast iterative PDE-based algorithm for feedback controls of nonsmooth mean-field control problems, arXiv preprint arXiv:2108.06740 (2021).

- [56] , A fast iterative PDE-based algorithm for feedback controls of nonsmooth mean-field control problems, arXiv preprint (2021).

- [57] Christoph Reisinger, Wolfgang Stockinger, and Yufei Zhang, Linear convergence of a policy gradient method for finite horizon continuous time stochastic control problems, arXiv preprint arXiv:2203.11758 (2022).

- [58] W. Tang and L. Tsai, Optimal surviving strategy for drifted Brownian motions with absorption, The Annals of Probability 46 (2018), no. 3, 1597–1650.

- [59] W. Whitt, Stochastic-process limits, Springer Series in Operations Research, Springer-Verlag, New York, 2002, An introduction to stochastic-process limits and their application to queues. MR 1876437