Leveraging Population Outcomes to Improve

the Generalization of Experimental Results111The authors would like to thank Nicole Pashley, Dustin Tingley, Tara Slough, the Miratrix CARES Lab, and the UCLA Causal Inference reading group. Melody Huang is supported by the National Science Foundation Graduate Research Fellowship under Grant No. 2146752. Any opinion, findings, and conclusions or recommendations expressed in this material are those of the authors(s) and do not necessarily reflect the views of the National Science Foundation.

Abstract

Generalizing causal estimates in randomized experiments to a broader target population is essential for guiding decisions by policymakers and practitioners in the social and biomedical sciences. While recent papers developed various weighting estimators for the population average treatment effect (PATE), many of these methods result in large variance because the experimental sample often differs substantially from the target population, and estimated sampling weights are extreme. To improve efficiency in practice, we propose post-residualized weighting in which we use the outcome measured in the observational population data to build a flexible predictive model (e.g., machine learning methods) and residualize the outcome in the experimental data before using conventional weighting methods. We show that the proposed PATE estimator is consistent under the same assumptions required for existing weighting methods, importantly without assuming the correct specification of the predictive model. We demonstrate the efficiency gains from this approach through simulations and our application based on a set of job training experiments.

1 Introduction

The “credibility revolution” has elevated the role of randomized, controlled trials (RCTs), which are praised for their strong internal validity [4, 19, 3]. Control over the design of the RCT allows researchers to draw causal inferences about treatment effects, within the experimental sample, while imposing minimal assumptions. This focus on credibility is not without controversy though, with some arguing that the emphasis on causality has led researchers to narrow the scope of their inquiry [24, 14]. This debate has revealed a pressing need for methods that allow researchers to generalize the causal impact of treatments, and resulting policy implications, beyond the experimental setting.

In light of this need, a robust literature on methods for generalizing experimental results to broader populations of interest has emerged. Often, in practice, the cost of a controlled environment is that the experiment cannot be conducted on a representative sample of the target population of interest. Recent work has outlined the necessary assumptions for generalizing an experiment to identify the population average treatment effect (PATE), i.e., the effect of the experimental treatment in a clearly defined target population that differs from the experimental sample [11, 23, 5]. In practice, the most common approach first models the experimental sample inclusion probability, with the PATE then estimated using inverse probability weighted estimators [44, 46, 8]. Alternative estimators focus on modeling treatment effect heterogeneity [28, 33] or doubly robust estimation [13].

Despite these theoretical advances in methods for estimating the PATE, in practice, weighted estimators are often imprecise, especially when the experimental sample differs substantially from the target population. This makes it difficult for policymakers and practitioners to draw conclusions about the impact of treatment in the target population to guide their policy recommendations. Indeed, researchers empirically find that weighted estimators often increase the mean squared error for the PATE compared to an estimator ignoring sampling weights because inverse probability weighting estimators have much larger standard errors, even though they have smaller bias [31]. More generally, considering the bias-variance tradeoff, the cost of large precision loss associated with the conventional weighting methods makes it unclear if it is “worth weighting” and questions the applicability of these weighting methods commonly used by empirical researchers.

In practice, these weighting methods often leave a valuable resource on the table — outcome data measured in the population. While inverse probability weighting methods leverage population data about pre-treatment covariates when modeling the sampling weights, use of outcome data has primarily been limited to use in placebo tests [11, 23]. Recently, the data fusion literature proposed using experimental data to help aid the estimation of causal effects in observational studies (e.g., see [1, 2, 26]). Our proposed approach aims to incorporate observational population data to reduce noise in generalizing experimental results. Population data often have larger sample sizes and therefore provide an opportunity to model covariate-outcome relationships with more flexible modeling approaches. It is this opportunity — to incorporate large population data sets that contain outcome data to improve precision — that serves as the foundation of our method.

We propose post-residualized weighting to leverage outcome data measured in the population to improve precision in estimation of the PATE. We begin by constructing a predictive model of the outcome using the population data. We then use this to residualize the experimental outcome data, and these residuals replace the experimental outcome in the standard inverse probability weighting estimators used for generalization. Identification of the PATE proceeds under the same assumptions required for existing inverse probability weighting methods, namely that the sampling weights are correctly specified. We show that this estimator is consistent, regardless of the residualizing model constructed in the population data. Therefore, we can safely use machine learning methods to build a predictive model. We then establish under what conditions the proposed post-residualized weighting estimator is more efficient than existing methods.

We also extend our estimator to the weighted least squares framework, which has three advantages: (1) it incorporates the well-known benefits of stabilized weighting estimators (i.e. Hàjek estimators), (2) it allows for additional precision gains from prognostic variables measured only within the experiment, and (3) it addresses concerns about scaling differences between the outcomes measured in the experiment and the population data. Importantly, we provide a diagnostic that allows researchers to assess when the post-residualized weighting method is likely to result in efficiency gains.

The paper proceeds by introducing our empirical application evaluating generalizability of site-specific results for trials conducted under the Job Training Partnership Act, described below. We then introduce notation and existing methods for estimating the population average treatment effect from experimental data in Section 2. In Section 3 we introduce post-residualized weighting, prove its statistical properties, and introduce a diagnostic to assess whether researchers should expect efficiency gains in their applications. We extend these results to weighted least squares estimation in Section 4, and discuss a special case in which we include the predicted outcome as a covariate in Section 5. Finally, we provide simulation evidence supporting the performance of post-residualized weighting estimators and diagnostic tools in Section 6 and apply them to an empirical application evaluating the Job Training Partnership Act in Section 7.

1.1 Background and Data

To motivate our method, we re-evaluate a foundational experiment that assessed the impact of a job training program. The Job Training Partnership Act (JTPA) was introduced by the U.S. Congress in 1982 to help provide employment and training programs to economically disadvantaged adults and youths. To assess its effectiveness, the national JTPA study evaluated the impact of the program across a diverse set of 16 experimental sites between 1987 and 1989. The experimental units were individuals who were interviewed and deemed eligible to receive JTPA services. Individuals assigned to treatment were given access to the JTPA services, while those assigned to control were told that the services were not available. The treatment to control ratio was set at 2:1. A follow-up survey 18 months later was then conducted to measure outcomes, such as earnings and employment [6].

We use the same 16 experimental sites from the national JTPA study as the basis for our analysis. While the original study focused on four target groups: adult women and men (categorized formally as ages 22 and older), and female and male out-of-school youths (ages 16-21), we focus our analysis on adult women, the largest target group within the JTPA study.222The estimated impact of JTPA for the other target groups were not found to be statistically significant in the original study. We consider two different outcomes: employment status (binary outcome) and total earnings (zero-inflated, continuous outcome). Across the 16 sites, the average effect on earnings was $1240 and employment was 1.63%, but point estimates across sites ranged from -$5210 in Butte, MT to $3030 in Providence, RI for earnings and -7% in Butte, MT and Marion, OH to 7% in Heartland, FL and Providence, RI. Had a policymaker only run their experiment in Providence, RI, they may have concluded that the treatment was effective, but not so in Butte, MT. Weighted estimators can adjust for demographic differences across sites, but many of the sites, such as Butte, MT, contain few units, emphasizing the need for precise estimators when generalizing results to other populations.

Unlike the original study, which evaluated the overall effectiveness, our focus is on generalizing the effect. The multisite design of this experiment serves as an ideal test bed for our method. We generalize the results of each site individually to a target population defined by the units in the other 15 sites, allowing us to benchmark our estimator against the experimentally identified causal estimate of the excluded sites and evaluate precision gains from post-residualized weighting. Ultimately, we find between a 5% and 21% reduction in variance where our methods are applicable. A summary of the JTPA experimental set up is provided in Supplementary Materials Table A5.

2 Existing Estimators for Generalization

2.1 Setup

We begin by defining the target population as an infinite super-population with probability distribution and probability density , for which we wish to infer the effectiveness of treatment. Following [8], suppose we observe units as the “experimental sample,” but, as with most experiments in practice, the selection into the experiment from the target population is biased . Let represent the random set of indices for the units in the experimental sample.

Let be the binary treatment variable, where for units assigned to treatment, and for control. Using the potential outcomes framework [32, 39], we define to be the potential outcome of unit that would realize if unit receives the treatment , where . For each unit in the experiment, only one of the potential outcome variables can be observed, and the realized outcome variable for unit is denoted by We also observe pre-treatment covariates for units in the experiment. We use to represent the sampling distribution for the experimental sample, i.e., with density . Because we consider settings where the selection into the experiment from the target population is biased,

We assume that the treatment assignment is randomized within the experiment.

Assumption 1 (Randomization within Experiment).

| (1) |

Under this assumption, it is well known that the sample average treatment effect (SATE) can be estimated without bias using a difference-in-means estimator:

| (2) |

This within-experiment estimand, the SATE, is important for evaluating the effectiveness of treatment. However, researchers often want to know to what extent the findings are externally valid to the target population [11, 31, 17]. This population level estimand, the population average treatment effect (PATE), is our primary causal quantity of interest and is formally defined as:

| (3) |

where the expectation is taken over the target population distribution . When the experimental sample is randomly drawn from the target population , can be used as an unbiased estimator for . However, in most settings, experimental units are not randomly drawn from the target population with equal probability.

To estimate the PATE, we also assume we observe an sample of units from the target super-population as the “population data,” which is separate from the experimental sample. This design is most common in the social sciences, and is called the non-nested design in that the experimental sample is not a subset of the population data [12].333While we focus on the non-nested design in this paper, the same proposed approach is useful for the nested design where the experimental sample is a subset of the population data. The main difference arises in the analytical expressions of the efficiency gain from our proposed approach. Typically, the size of the population data is much larger than the experimental data, i.e., . In the conventional setup, researchers only observe pre-treatment covariates for each unit in the population data. In the next subsection, we review assumptions and estimators for the PATE under this conventional setup. In Section 3, we then consider our setting in which researchers also observe an outcome measure in addition to pre-treatment covariates in the population data. Importantly, because the treatment is not randomized in the population data, we cannot identify the PATE just using the population data.

2.2 Assumptions

We make the standard assumptions of no interference and that treatments are identically administered across all units (i.e., SUTVA, defined in [40]). In order to identify the PATE using experimental data, we require additional assumptions about sampling of the experimental units. First, we assume that, conditional on a set of pre-treatment covariates , the sample selection mechanism is ignorable. More formally,

Assumption 2 (Ignorability of Sampling and Potential Outcomes).

| (4) |

Assumption 2 states that, conditional on , the distribution of the potential outcomes is the same across the experimental sample and the target population [44, 35, 28].444For identification of the PATE, a weaker assumption of conditional ignorability of sampling and treatment effect heterogeneity may be invoked instead. However, the variance derivations rely on the conditional ignorability of sampling and potential outcomes. We also assume that given the pre-treatment covariates , there is a positive probability of being included in the experimental sample [47].

Assumption 3 (Positivity).

For all with we have

| (5) |

2.3 Estimation of PATE

There is a robust, and growing, literature on methods for estimating the PATE. The most common approach is the inverse probability weighting estimator (IPW) [11]. The IPW estimator relies on sampling weights usually defined as an inverse of the probability of being sampled into the experiment. In our case, given the infinite superpopulation defined by , we first define a relative density as follows.

| (6) |

Sampling weights are proportional to the inverse of this relative density. For each unit ,

Weights are typically estimated using a binary outcome model, such as logistic regression [44, 34, 8] by exploiting the fact that weights are proportional to the relative probability of being in the observed population data to the probability of being in the experimental sample, conditional on being in either set:

where takes on a value of if the unit belongs to the experimental sample, and if the unit belongs to the observed population data. Researchers can estimate and using a binary outcome model where we model with by stacking the experimental data and population data [44, 8, 18]. Alternatively, researchers can use balancing methods, such as entropy balancing, which estimates weights such that weighted moments (e.g., means of each pre-treatment covariate ) of the experimental data is equal to moments of the observed population data [15, 22, 23].

Once researchers have estimated the sampling weights, the PATE can be estimated using a weighted estimator, also known as the Hàjek estimator:

| (7) |

This weighted estimator can be computed using a weighted least squares regression of the outcome on an intercept and the treatment indicator, with the estimated weights . The weighted estimator is equivalent to the estimated coefficient of the treatment indicator.

Under Assumption 1–3 and the consistent estimation of the sampling weights, the weighted estimator is a consistent estimator of the PATE [8]. However, in practice, weighted estimators can suffer from large variance due to extreme weights. This problem has been highlighted in the observational causal inference literature with respect to inverse propensity score weighted estimators, in which large imbalances between treatment and control groups can result in extreme weights [27, 43]. This issue is often exacerbated in the generalization setting, where imbalances between a convenience experimental sample and target population can be relatively large. As a result, losses in precision from weighting can be challenging to overcome when generalizing from the SATE to the PATE [31].

3 Post-Residualized Weighting

Existing methods, such as the weighted estimator described above, require pre-treatment covariate data, measured in both the experimental sample and target population, for estimating the sampling weights. However, researchers often have access to an outcome variable in the observational population data as well. Our proposed method, post-residualized weighting, aims to improve precision in the estimation of the PATE by leveraging this outcome variable measured in the observational population data.

3.1 Setup

In contrast to the conventional setup, we consider settings where researchers observe an outcome variable in addition to pre-treatment covariates in the population data. See Figure 1 for a visualization of the difference in settings from conventional methods. Below we describe two canonical social science examples that motivate the data settings that underpin our method and to which we return. We also come back to our benchmark analysis of the JTPA data in Section 7.

Example: Get-Out-the-Vote (GOTV) Experiments

Political scientists have conducted a number of field experiments to evaluate the impact of canvassing efforts, including door-to-door, phone, and mail, on voter turnout. Such GOTV experiments typically rely on administrative data to measure the outcome, namely voter turnout data from the Secretary of State. These experiments are often conducted in a small geographic region (e.g., New Haven, Connecticut in [21]), but scholars are often interested in generalizing the effect to broader populations, such as for a statewide election. Importantly, when considering generalization, the outcome variable of voter turnout is available not only for the experimental data but also for the broader target population of interest. In our framework, we use this information about voter turnout measured in the observational population data to improve precision in the estimation of the PATE.

Example: Education Experiments

Education research also relies on experiments to evaluate the performance of classroom interventions, such as the impact of smaller class size on curriculum-based and standardized tests [48, e.g.,]. These experiments are often done in partnership with school systems. For example, the Tennessee STAR experiment was conducted in classrooms across Tennessee. However, researchers are interested in the broader impact of such interventions. For example, a researcher may ask what the long term impact of small class sizes in primary school is on standardized test scores, such as the SAT, for all public schools in the United States. To estimate the PATE, existing methods use demographic variables from a random sample of public school students to construct sampling weights. In our framework, we can additionally use SAT scores measured for a random sample of public school students, which improves estimation accuracy.

Remark

For simplicity of exposition, this section focuses on settings where we observe the same outcome measure in the experimental and population data. The outcomes measured in the population may be a mix of treatment and control outcomes. However, our proposed method can also accommodate scenarios in which we only observe a proxy outcome variable (rather than the same outcome measure) in the population data. We consider this case in Section 5. ∎

3.2 Post-residualized Weighted Estimators

Our proposed post-residualized weighting approach exploits the outcome measured in the population data to improve precision in the estimation of the PATE. The key idea is that we estimate a predictive model with the outcome measured in the population data and then use this estimated predictive model to residualize outcomes in the experimental data, before using conventional weighting estimators for the PATE.

In total, post-residualized weighting has four steps. The first step is to estimate sampling weights , which is the same as the conventional weighting approach. In the second step, we fit a flexible model in the population data to predict the outcome variable using pre-treatment . We refer to this predictive model fitted in the population data as a residualizing model, and formally denote it as : where is the support of . In the third step, we use the estimated residualizing model to predict outcomes in the experimental data, which is separate from the population data used to estimate the residualizing model. In the fourth and final step, we apply the weighted estimator (equation (7)) using the residuals from this prediction, (denoted by ) as outcomes (instead of used in the conventional weighting approach).

We summarize our proposed approach in Table 1. In the following section, we directly extend the weighted estimator discussed in Section 2. We then consider how post-residualizing can improve a more general weighted least squares estimator that includes further covariate adjustment in Section 4.

| Post-residualized Weighting for the PATE estimation: | |

|---|---|

| Step 1: | Estimate sampling weights, , for units in the experimental sample. |

| Step 2: | Choose a residualizing model : , where is the support of . Using the population data, estimate that predict the population outcomes using pre-treatment covariates . |

| Step 3: | Predict for each unit in the experimental data, and compute residual for units in the experimental sample. |

| Step 4: | Estimate the PATE using residuals and estimated sampling weights . |

| No covariate adjustment within the experimental data (Section 3) | |

| See post-residualized weighted estimator (Definition 1). | |

| With covariate adjustment within the experimental data (Section 4) | |

| See post-residualized weighted least squares estimator (Definition 2). | |

Definition 1 (Post-residualized Weighted Estimator).

Let be estimated sampling weights. Define to be residuals from the residualizing model prediction (i.e., ). The post-residualized weighted estimator is defined as:

| (8) |

We summarize several key aspects of the post-residualized weighted estimator here and formally discuss each point in the subsequent sections. First, the identification of the PATE is obtained under the same assumptions required for existing weighted estimators, and we do not make any additional assumptions (Section 3.3). Most importantly, our proposed estimator is consistent for the PATE, regardless of the choice of the residualizing model. That is, we do not require the correct specification of the residualizing model to guarantee consistency of the proposed estimator. Therefore, akin with [38] and [42], the residualizing model can be seen as an “algorithmic model” in that the goal is to predict outcomes, rather than substantively explain an underlying probabilistic process.

Second, the proposed post-residualized weighted estimator, , can achieve significant improvements in precision over the traditional weighted estimator (equation (7)) when the residualizing model can predict outcomes in the experiment well (Section 3.4). We will show in Section 3.4 that while we maintain consistency regardless, how much efficiency gain we achieve depends on the predictive performance of the fitted residualizing model . As such, researchers should, when possible, use not only simple models, such as ordinary least squares, but also more flexible machine learning models, such as random forests or other ensemble learning methods [7, 36] as the residualizing models to improve precision of the PATE estimation.

Finally, we derive a diagnostic measure that researchers can use to determine whether residualizing will likely lead to precision gains when estimating the PATE (Section 3.5). As emphasized in the second point above, when the residualizing model can predict outcomes in the experiment well, we can expect efficiency gains. However, when the residualizing model fails to predict outcome measures in the experimental data, it is possible for post-residualizing to increase uncertainty of the PATE estimation. Our diagnostic measure helps researchers to estimate the expected efficiency gain, thereby deciding whether residualizing is beneficial in their applications.

Remark

Our proposed post-residualized weighting estimator is closely connected to the augmented inverse probability weighted estimators (AIPW) [37] developed for the PATE [13] in that both estimators combine weighting and outcome-modeling. The process of estimating weights for both the post-residualized weighting estimators and AIPW is the same. However, the key difference between two approaches is that the AIPW estimates the outcome model using only the experimental data, thereby not exploiting the outcome variable available in the population data. In contrast, our post-residualized weighting estimator explicitly uses the outcome information available in the population data to estimate the residualizing model and improve precision. Furthermore, post-residualized weighting does not attempt to model both the treatment and control outcomes separately, and therefore, does not have the double robustness that the AIPW has. ∎

3.3 Consistency

In this section, we show that the post-residualized weighted estimator is a consistent estimator of the PATE regardless of the choice of the residualizing model . This emphasizes the point that need not be a correct specification of the underlying data generating process, but merely a function that predicts outcomes measured in the population.

Theorem 1 (Consistency of Post-residualized Weighted Estimators).

Assume that sampling weights are consistently estimated and Assumptions 1–3 hold with pre-treatment covariates . Then, the post-residualized weighted estimator, using any residualizing model built on the population data, is a consistent estimator for the PATE:

where denotes the convergence in probability.

The proof of Theorem 1 can be found in Supplementary Materials A. This property allows for a large degree of flexibility in building the residualizing model, since consistency is guaranteed regardless of model specification or performance of . We can obtain the consistency even for a misspecified residualizing model because the predicted experimental outcome is only a function of the pre-treatment covariates , and thus, with randomized treatments (Assumption 1), its distribution is the same across treatment and control units on average for any sample size. As such, residualizing preserves the consistency of the original weighted estimator without requiring any additional assumptions.

While consistency is guaranteed, efficiency gains from residualizing do depend on the ability of the residualizing model to predict outcome measures in the experimental data. Theorem 1 allows for researchers to leverage complex, “black box” approaches (such as ensemble methods) to maximize the predictive accuracy, as interpretability of the residualizing model is secondary to being able to fit the data well. In the next section, we will formalize the criteria for variance reduction from residualizing.

3.4 Efficiency Gains

The post-residualized weighted estimator allows researchers to include information from the observational population data about the relationship between the pre-treatment covariates and the population outcomes into the estimation process. Whether or not we obtain precision gains, and the magnitude of these precision gains, will depend on the nature of the residualizing model. In general, the better researchers are able to explain the outcomes measured in the experiment using the residualizing model, the greater the efficiency gains.

To make these gains more explicit, we first define the weighted variance and weighted covariance as follows.

| (9) | |||||

| (10) |

where and . The efficiency gain for the post-residualized weighted estimator is formalized as follows.

Theorem 2 (Efficiency Gain for Post-residualized Weighted Estimators).

The difference between the asymptotic variance of and that of is:

| (11) |

where denotes the scaled asymptotic variance of random variable over the sampling distribution , i.e., is the probability of being treated within the experiment, i.e.,

The proof of Theorem 2 can be found in Supplementary Materials A. Theorem 2 decomposes the efficiency gain from post-residualized weighting into two components: (1) the variance of the predicted experimental outcomes , and (2) how related the predicted outcomes are to the actual outcomes in the experimental samples (represented by and ). If the covariance between the predicted outcomes and actual outcomes in the experimental sample is greater than the variance of the predicted outcomes, we expect precision gains. In other words, the gains to precision from residualizing depend on how well outcome measures in the experiment are explained by the residualizing model fitted to the population data.555We note that the efficiency gain expression does not include uncertainty associated with estimating the residualizing model. This is because the chosen is a dimension reducing function of the fixed pre-treatment covariates. As such, researchers should leverage the large amounts of data available at the population level to apply flexible modeling strategies in order to maximize the variation explained by the residualizing model.

In the following subsection, we will describe a diagnostic measure that can help researchers determine whether or not they should expect precision gains from residualizing.

3.5 Diagnostics

As discussed above, while post-residualized weighting stands to greatly improve precision in estimation of the PATE, this is not guaranteed. To address this concern, we derive a diagnostic that evaluates when researchers should expect precision gains from residualizing.

We define a pseudo- measure as:

| (12) |

where we define for

can be interpreted as the weighted goodness-of-fit of the residualizing model for the potential outcomes under control for units in the experiment. Researchers can estimate using the estimated residuals across the control units in the experiment. When , we expect an improvement in precision across the control units from residualizing.

In line with Rubin’s “locked box” approach [41], we do not suggest estimating the analogous among treated units. However, if the variation in the control outcomes is greater than the overall treatment effect heterogeneity, then checking if is greater or less than zero is an effective diagnostic for whether or not we expect precision gains from residualizing. We formalize this in the following corollary, where we write the relative reduction from residualizing as a function of this proposed measure.

Corollary 1 (Relative Reduction from Residualizing).

With defined as in equation (12), define as the weighted goodness-of-fit of the residualizing model for the potential outcomes under treatment. Let , such that:

Furthermore, define the ratio . Then the relative reduction in variance from residualizing is given by:

Corollary 1, proof available in Supplementary Materials A, decomposes the overall relative reduction in variance of the weighted estimator from residualizing into two components: (1) our proposed diagnostic measure and (2) a factor, represented by , that measures the difference in prediction error between the experimental control and experimental treated potential outcomes. If the residualizing model explains similar amounts of variation across both the treated and control potential outcomes, then and . In that scenario, will be roughly indicative of the expected relative reduction. When takes on a negative value, this is a strong indication that residualizing is unlikely to result in precision gains, since it is unlikely the prediction error will be significantly lower for treated units.

To summarize, can diagnose when one should expect improvements in precision from residualizing. When takes on negative values, researchers should not proceed with residualizing, as it is likely to result in precision loss.

4 Post-residualized Weighting with Covariate Adjustment

In Section 3, we showed that the post-residualized weighted estimator is a consistent estimator of the PATE, regardless of the residualizing model that researchers use. However, researchers often rely on covariate adjustment to experimental data to improve precision in estimation. We now extend our post-residualized weighted estimator to include a standard covariate adjustment for the experimental data.

As with estimation of the SATE, including covariate adjustment when estimating the PATE can combat the precision loss associated with the weighted estimators. Additionally, while estimation of weights requires covariates to be measured across both the population and the experimental data, covariate adjustment can leverage covariates that are only measured in the experimental data, where researchers can measure prognostic variables [45]. The weighted least squares estimator for the PATE is estimated using a weighted regression, regressing the outcomes on the treatment indicator and pre-treatment covariates. More formally,

| (13) |

where are experimental pre-treatment covariates included in the covariate adjustment. Covariates can differ from the required for Assumptions 2–3. This weighted least squares estimator is consistent for the PATE under Assumptions 1–3 as long as the sampling weights is consistently estimated [13].

By extending the weighted least squares estimator (equation (13)), we formally define the post-residualized weighted least squares estimator as follows:

Definition 2 (Post-Residualized Weighted Least Squares Estimator).

Given a residualizing model estimated as , the

post-residualized weighted least squares estimator for the PATE is defined as,

| (14) |

where and are experimental pre-treatment covariates included in the covariate adjustment. We allow to differ from used to calculate .

In practice, the post-residualized weighted least squares estimator can be estimated by running a weighted regression, where the estimated residualized values is regressed on the treatment indicator and covariates , and using the sampling weights as the weights. The coefficient of the treatment indicator is the post-residualized weighted least squares estimate for the PATE. If no pre-treatment covariates are included, the post-residualized weighted least squares estimator is equivalent to the post-residualized weighted estimator (equation (8)) discussed in Section 3.

There are two advantages to the post-residualized weighted least squares estimator. First, it can leverage precision gains from pre-treatment covariates that are measured in the experimental data but not in the population data. That is, can include more covariates than . Second, provides additional robustness over the post-residualized weighted estimator . More specifically, without further covariate adjustment, residualizing can be sensitive to differences between the population and experimental units in the covariate-outcome relationships. As illustrated in Section 3.4, when this difference is large, residualizing can result in efficiency loss. However, by performing covariate adjustment on the residualized outcomes in the experimental data, we have an opportunity to correct for the difference in the covariate-outcome relationships between the experimental data and the population data. In other words, the post-residualized weighted least squares estimator, , gives researchers two opportunities to combat the precision loss of weighting: once from using the population data in the residualizing process, and a second from adjusting for covariates in the experimental data.

4.1 Consistency

We show that, much like the post-residualized weighted estimator , the post-residualized weighted least squares estimator is also a consistent estimator of the PATE, regardless of the chosen residualizing model and pre-treatment covariates that researchers adjust for in the weighted least squares estimator.

Theorem 3 (Consistency of Post-residualized Weighted Least Squares Estimators).

Assume that sampling weights are consistently estimated and Assumptions 1–3 hold with pre-treatment covariates . Then, the post-residualized weighted least squares estimator that adjusts for pre-treatment covariates equation (14) is a consistent estimator

with any residualizing model and any pre-treatment covariates .

This theorem follows closely from Theorem 1, with a proof available in Supplementary Materials A. As before, we highlight that no additional assumptions are needed to establish consistent estimation of the PATE.

A potential concern with covariate adjustment is that performing covariate adjustment within the experimental data can result in worsened asymptotic precision and invalid measures of uncertainty [20]. An alternative approach is to include interaction terms between the treatment indicator and covariates [51]. Regardless, we can compute valid standard errors with the Huber–White sandwich standard error estimator.

4.2 Efficiency Gain

In this section, we discuss the efficiency gains that can be obtained from residualizing. Like the weighted estimator case, we expect that when outcomes measured in the experiment are better predicted by the residualizing model , the efficiency gains from residualizing is larger. However, because there is an additional opportunity for covariate adjustment using covariates measured in the experiment , the residualizing model must explain variation in outcomes that cannot be explained using covariates in the weighted least squares regression. We formalize this below.

Theorem 4 (Efficiency Gain for Post-Residualized Weighted Least Squares Estimators).

The difference between the asymptotic variance of and that of is:

| (15) |

where and are the true coefficients666We define the true coefficients as the coefficients that would be estimated as the experimental sample size . See Supplementary Materials for more information. associated with the pre-treatment covariates, defined in the weighted least squares regression equation (13) and the post-residualized weighted least squares regression equation (14), respectively.

When we include covariate adjustment to the experimental data, the gains to precision depend on two factors. The first factor, , compares the explanatory power of the residualizing model with the linear regression. More specifically, if is able to explain more variation than the linear combination of , then we expect the first term to be positive. The second term, , represents the amount of variation in the residualized outcomes that can be explained by the pre-treatment covariates . Thus, the magnitude of the precision gain will depend on (1) how much variation the residualizing model can explain in outcomes across the experimental sample, and (2) how much of the variation the covariates are able to explain in the residualized outcomes .

A natural question is why not directly adjust for covariates within the experimental sample instead of using a residualizing model? One advantage to using the post-residualized weighting over directly adjusting for covariates within the experimental sample arises from the fact that there is typically a larger amount of data available in the population data (i.e. ). While researchers could choose to use a flexible model within the experimental data to perform covariate adjustment, there is a greater restriction with respect to degrees-of-freedom to what type of model can be fit. The availability of large amounts of population data can be leveraged in the residualizing process to better estimate covariate-outcome relationships. Additionally, by using population data to build and tune the residualizing model, we protect the fidelity of inferences using the experimental data since it is only used for estimation of the PATE.

When data generating processes are not identical in the experimental and population data, we see concerns similar to the weighted estimator case. When there are large differences between outcomes measured in the experiment and outcomes measured in the population data, there is a risk that we may lose precision from residualizing. However, in the context of weighted least squares, the additional step of covariate adjustment can help mitigate potential efficiency losses that arise from a residualizing model that poorly predicts outcomes measured in the experiment.

4.3 Diagnostic

We now extend the proposed diagnostic from Section 3.5 to the post-residualized weighted least squares estimator. More formally, we define as:

where we now include covariate adjustments from weighted least squares regression in our diagnostic. are the residuals that arise from regressing the residualized outcomes under control on the pre-treatment covariates in the weighted regression. Similarly, the quantity are the residuals from regressing the outcomes under control on the pre-treatment covariates. In this way, we are directly comparing the variance of the outcomes, following covariate adjustment, across the control units.

The interpretation of this value is identical to that of the pseudo- value in the weighted estimator case. A negative estimated indicates that residualizing may result in a loss in efficiency. When the estimated is positive, we expect there to be improvements.

5 Extension: Using the Predicted Outcomes as a Covariate

Thus far, we have discussed residualizing, or directly subtracting the predicted outcome values from the outcomes measured in the experimental sample. An alternative approach is to regress the outcomes measured in the experimental sample on the predicted outcomes from our residualizing model. In particular, consider including the as a covariate in a weighted linear regression:

We can extend this approach to also include pre-treatment covariates:

The residualizing methods we discussed in Sections 3 and 4 can be seen as special cases of these methods when we set .

Residualizing by directly including as a covariate in the weighted least squares has many advantages. The primary advantage is that this approach allows researchers to flexibly use proxy outcomes measured in the target population. When the outcome of interest is not measured at the population level, or if the outcomes are measured in different ways across the experimental sample and the observed population data, researchers can estimate the residualizing model using alternative proxy outcomes related to the outcome of interest. However, this can lead to scaling issues that limit the ability of the weighted and weighted least squares methods for post-residualizing to achieve efficiency gains. We show how including as a covariate addresses these concerns.

Additionally, as with our post-residualized estimators and discussed in Sections 3 and 4, both and are consistent estimators of the PATE (Section 5.2). Finally, including the predicted outcome as a covariate protects against efficiency loss, unlike and in the previous sections. This is true whether researchers rely on a proxy outcome , or if they build the residualizing model on .

5.1 Proxy Outcomes in the Population Data

There are many settings in which researchers may rely on a proxy outcome . First, an outcome measure used to estimate the residualizing model in the population data may differ from the outcome measure in the experiment. Second, even when the outcome measure used to estimate the residualizing model in the population data is in principle the same measure as the outcome of interest in the experimental data, there can be differences between and that may arise due to differences in how the outcomes are measured or operationalized across the experimental sample and the population, or when the potential outcomes depend on context. For example, this might occur if the population is a mix of both treatment and control conditions with non-random treatment selection.

Example: Get-Out-the-Vote (GOTV) Experiments

Consider Get-Out-the-Vote experiments, again, where we are interested in the causal effect of a randomized GOTV message on voter turnout, which is measured by administrative voter files in the United States [21, e.g.,]. Imagine, however, that we do not have administrative data available on our population, such as for all voters in the United States, but rather, we have a nationally representative survey. For many nationally representative surveys, it is infeasible to link administrative individual-level voting history data due to privacy issues and data constraints; as such, we do not have access to voter turnout. Instead, surveys often ask voters an “intent-to-vote” question, which can proxy for actual voter turnout. Our proposed method can use this “intent-to-vote” variable to build a residualizing model.

Example: Education Experiments

Imagine that researchers are primarily interested in the causal effect of small class sizes not on long term standardized outcomes such as the SAT, but rather a curriculum-based test score specific to a state collected during a given academic year. In this case, researchers may not have access to this curriculum-based measure in the state-level population data, but may have

access to related standardized testing scores. These standardized test scores may be used as a proxy to the curriculum-based test score of interest that is measured in the experimental data when constructing the residualizing model.

When using proxy outcomes to estimate the residualizing model, efficiency gain will be impacted by how similar the proxy outcomes are to the actual outcomes of interest. More formally, consider the following decomposition of the residuals :

| (16) |

where we define as the proxy outcome. Conceptually, represents the proxy outcome, had it been measured for the experimental data. For example, in the GOTV experiment, could represent the “intent-to-vote” variable, had it been measured for the experimental sample.

Equation (16) decomposes the residual term into two components. The second component (b) is the model prediction error. This is driven by how well the chosen residualizing model fits proxy outcomes measured in the population data. The first component (a) is how similar the proxy outcomes measured in the population data are to the outcome measures used in the experimental data. If the proxy outcomes differ substantially from the outcomes measured in the experimental data, while the post-residualized weighted estimators will still be consistent (see Theorem 1), there may be losses in efficiency from residualizing, regardless of how much we are able to minimize the prediction error in the second term (b).

5.2 Consistency

Like the previously proposed post-residualized weighted estimators and , both and will be consistent estimators of the PATE. This follows from the fact that is just a function of pre-treatment covariates . In this sense, we can think of and as extensions of the weighted least squares estimator, where is an additional pre-treatment covariate included in the weighted linear regression. Thus, as shown in Section 4, both and are consistent estimators of PATE.

5.3 Efficiency Gain and Diagnostics

There are two advantages to using as an additional covariate. First, because is treated as a covariate in a weighted regression, the estimated coefficient (i.e., ) can capture any potential scaling differences between the proxy outcomes and the actual outcomes of interest. For example, returning to the Get-Out-the-Vote experiments, intent-to vote is often measured on a Likert scale, while voter turnout is simply a binary variable of whether the individual voted or not. In such a scenario, residualizing directly on can lead to efficiency loss, despite the fact that intent-to-vote is correlated to voter turnout.

Second, treating as a covariate protects against precision loss when the proxy outcomes are significantly different from the outcomes of interest. At worst, is unrelated to , and we expect the coefficient in front of to be near zero. When this occurs, we expect the variance of the post-residualized weighted estimator when using as a covariate to be similar to the variance of a conventional estimator that does not include population-level outcome information. More formally:

Corollary 2.

The post-residualized weighted estimator using as a covariate will be at least as asymptotically efficient as the standard weighted estimator:

This result follows from from [49], who shows that the variance of an estimator that accounts for pre-treatment covariates will be asymptotically less than or equal to the variance of an estimator that does not account for pre-treatment covariates.

To account for whether or not the re-scaled predicted outcomes sufficiently explain enough of the variation in the experimental sample, we extend our previously proposed diagnostic measures to the proxy outcome setting. To do so, we propose using sample splitting across the control units in the experimental sample. We regress on the control outcomes across one subset of the sample. This allows us to estimate . Then using , we can estimate residuals, accounting for the scaling factor (i.e., ), across the held out sample, and calculate the and diagnostics from before. We finally conduct cross-fitting, i.e., repeating the same procedure by flipping the role of training and test data and then averaging diagnostics from both sample splitting.

5.4 When to worry about external validity

When diagnostic measures indicate that post-residualized weighting is unsuitable for the data at hand, it is important to understand why. In particular, Equation (16) shows that efficiency loss could occur from (1) the residualizing model’s prediction error, and (2) the difference between the outcomes in the population and the outcomes measured in the experimental sample. Low diagnostic values indicate that post-residualizing methods may not provide efficiency gains, however it may also be indicative of contextual differences in the potential outcomes, which affect the validity of the PATE estimate.

The residualizing model’s prediction error, from equation (16)-(b), can be estimated through cross validation using the population-level data. Researchers can hold out random subsets of the population-level data when estimating the residualizing model and calculate the prediction error across the held out sample. If the cross validated error is large, there will likely be little to no efficiency gains from using post-residualized weighting due to poor prediction, even if the true outcome is used to estimate . The difference between the outcomes and the proxy outcome , from equation (16)-(a), can be estimated when the proxy outcome is also measured in the experimental sample. For example, in the Get-Out-the-Vote experiments, researchers may have voters’ intent-to-vote in the experimental sample. Alternatively, in the education experiments, researchers could measure both the curriculum-based test score and the standardized test score in the experimental sample.

In settings where is not measured in the experimental data, researchers can still use the proposed diagnostic measures to determine if there are concerns about generalizability. For example, if the cross validated prediction error is low, but the diagnostics indicate that post-residualized weighting will not improve efficiency, then this indicates that the residualizing model predicts the population outcomes well, but does not predict outcomes measured in the experiment well. This could be due to two problems. First, if the population outcome is a proxy measure of the outcome measured in the experimental sample, then it could be that the measure used in the population data is not a good proxy for the experimental outcome. Alternatively, if researchers believe that the experimental and population outcomes are measured in the same way, then a low or negative measure, in conjunction with low cross validated prediction error, would indicate that the outcome-covariate relationships in the population are considerably different from the outcome-covariate relationships in the experimental sample. In this case, there may be limited external validity of the experiment due to a failure of the consistency of parallel studies assumption, since the potential outcomes may depend on context (see [17] for more discussion).

6 Simulation

We now run a series of simulations to empirically examine the proposed post-residualizing method. In total, we consider four different data-generating scenarios, based on the following model for the potential outcomes under control:

where are observed pre-treatment covariates, and is a binary indicator variable, taking the value of one when unit is in the experimental data, and taking the value of zero when unit is in the population data. controls for differences between the experimental sample and population data outcomes, and the terms dictate the nonlinearity of the data generating processes.

We then define the treatment effect model as follows:

where is an observed pre-treatment covariate that governs treatment effect heterogeneity. Therefore, the observed outcomes take on the following form: . We provide additional details, including the sampling model and distributions of observed covariates in Supplementary Materials C.

The first two scenarios test the method when the outcome measures for both the experimental sample and the population data are drawn from the same underlying data generating process, to explore a setting where the outcome is measured identically across the experiment and target population (i.e., ). The third and fourth scenarios use different data generating processes to simulate the experimental sample and population data outcome measures (i.e., ). This mimics the setting in which researchers use a proxy outcome. For both of these settings, we consider a version of the data generating processes that is linear in the included covariates, and a second version that contains nonlinearities. Table 2 provides a summary of the different scenarios.

| Proxy and Experimental Sample Outcomes | DGP Type | |

|---|---|---|

| Scenario 1 | Identical DGP () | Linear () |

| Scenario 2 | Identical DGP () | Nonlinear () |

| Scenario 3 | Different DGP () | Linear () |

| Scenario 4 | Different DGP () | Nonlinear () |

We compare conventional and post-residualized versions of two sets of estimators in each simulation. We perform post-residualizing in two different ways: the first directly residualizes the outcomes in the experimental sample by subtracting the predicted outcomes, and the second treats the predicted outcomes as a covariate in a weighted regression. Therefore, we compare a total of six different estimators: (1) the weighted estimators , , , and (2) weighted least squares (wLS) , , and . The difference-in-means estimator (DiM) is also provided as a baseline with no weighting adjustment.

The underlying sampling process is governed by a logit model. At each iteration of the simulation we draw both a biased experimental sample and a random sample of a larger target population, the population data. The population data is used to estimate the residualizing model and sampling weights. We use entropy balancing to estimate the sampling weights for each simulation. Our residualizing model is a regression that contains all the pair-wise interactions of the included covariates. The weighted least squares regression includes covariates additively without any interactions.777It is possible in practice to include nonlinear transformation of pre-treatment covariates in the regression adjustment step. However, we have omitted it to illustrate the efficiency gains that can be obtained from accounting for nonlinearities through the residualizing step. This mimics how, in practice, we are able to fit more complex models to more data.

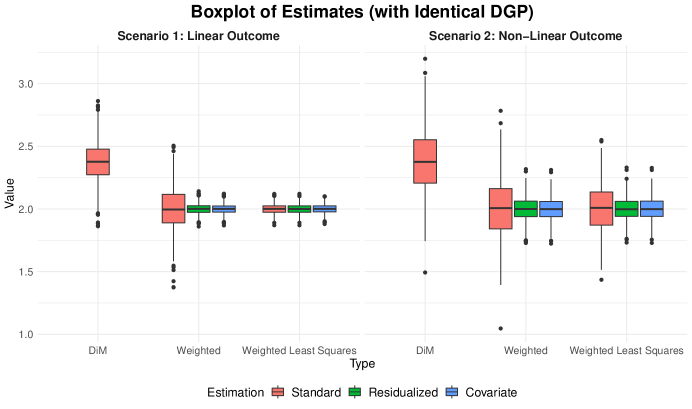

Overall, we find that when the underlying outcome model is complex and contains nonlinear terms, our post-residualizing method exhibits large precision gains compared to conventional methods. When there is no difference between the population-level outcomes and the outcomes in the experimental sample, seen in Figure 2, direct residualizing and including as a covariate performs identically.

Scenario 1

When we consider a linear DGP, residualizing results in substantial precision gains for the weighted estimator. However, for the weighted least squares estimator, residualizing does not result in precision gains, because the covariate adjustment taking place in the weighted regression already includes the linear terms in the data generating process, and thus, the residualizing step does not model anything in the outcomes that is not already accounted for in the wLS regression.

Scenario 2

When we include nonlinear terms into the data generating process, residualizing results in precision gains for all of the estimators, because the residualizing model is able to account for some of the nonlinearities that the wLS regression does not account for. It is worth noting that the estimated residualizing model is not a correct specification of the underlying outcome model for the population data. However, because we have included the pairwise interactions between the covariates, the residualizing model is able to significantly reduce the variance for both estimators, even without accounting for all of the nonlinear terms in the underlying data generating process.

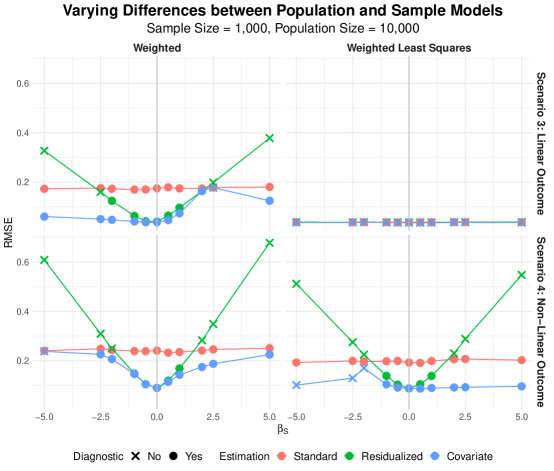

Scenarios 3 and 4

Next we consider a difference in the underlying data generating process between the experimental and population outcomes, presented in Figure 3. We operationalize this by including an interaction between treatment, the sampling indicator, and covariates. The degree to which the two processes differ is varied across different simulations using a single parameter, . When the difference is relatively small (i.e. small ), the two methods used to residualize the experimental sample outcomes perform identically. This is evident by a lower RMSE when for the post-residualized weighted estimators. When the difference in the DGP are large (i.e., ), residualizing by directly subtracting the outcomes from the predicted outcomes results in precision loss, evident by a larger RMSE for the post-residualized weighted estimator , and for the post-residualized weighted least square estimator when the true DGP is nonlinear. However, treating the predicted outcomes as a covariate in a weighted linear regression and allows for precision gain, even in these settings. We see that at worst, the covariate-based residualizing approach performs equivalently to the conventional estimators.

It is important to highlight that regardless of the degree of divergence between the population and experimental sample DGP’s, post-residualized weighting is able to maintain nominal coverage. Furthermore, our proposed diagnostic measures adequately capture when we expect to gain or lose precision from residualizing. We provide coverage results and a summary of the diagnostic performance in the Supplementary Materials C.

7 Empirical Evaluation: Job Training Partnership Act

To evaluate and benchmark how our proposed post-residualizing method may work in practice, we now turn to an empirical application. Recall that, while the original study evaluated the overall impact of JTPA, our focus is on generalizing the effect of each site individually to the other 15 sites. More specifically, in our leave-one-out analysis for each site, we define the PATE as the average treatment effect among units in the remaining 15 sites. We then generalize the experimental results from one site to the population defined by the pooled remaining sites. This allows us to benchmark our method’s performance by comparing our PATE estimators to the pooled experimental benchmark in the remaining sites. We evaluate generalizability for two outcomes: employment status (binary outcome) and total earnings (zero-inflated, continuous outcome).

7.1 Post-Residualized Weighting

7.1.1 Residualizing model

We include baseline covariates measured in the interview stage of the JTPA study. The covariates include measures of age, previous earnings, marital status, household composition, public assistance history, education and employment history, access to transportation, and ethnicity. More details about the pre-treatment covariates can be found in Supplementary Materials D.

We construct our residualizing model using an ensemble method, the SuperLearner [29]. The ensemble model contains the Random Forest, with varying hyperparameters, and the LASSO, with hyperparameters chosen using cross validation. This allows us to capture nonlinearities in the data through the Random Forest, as well as linear relationships using the LASSO [29]. We build separate models for the probability of employment and total earnings. We fit our residualizing model on the control units from the target population. Details can be found in Supplementary Materials D.

7.1.2 Estimators

We estimate the PATE using two different estimators: the weighted estimator and the weighted least squares estimator (wLS). For each estimator, we consider the conventional estimators ( and ), the post-residualized estimators directly subtracting the predicted outcomes from the outcomes in the experimental sample ( and ), and the post-residualized estimators using the predicted outcomes as a covariate ( and ). Sampling weights are estimated using entropy balancing in which we match main margins for age, education, previous earnings, race, and marital status [22]. Our weighted least squares (wLS) estimators include age, education level, and marital status as controls. Standard errors are estimated using heteroskedastic-consistent standard errors (HC2).

7.1.3 Diagnostics

For each site, we compute the pseudo- diagnostics. This can be done directly for the post-residualized weighted and weighted least squares estimators. When treating as a covariate, we use sample splitting to estimate the pseudo- values. Because some of the experimental sites comprise of relative few units (i.e., the experimental site of Montana contains only 38 units total), we perform repeated sample splitting, taking the average of the diagnostic across the repeated splits [50, 10].

7.2 Results

7.2.1 Bias

Because the conventional estimators and our proposed approach rely on the same identification assumptions, we first want to verify that the overall bias in the PATE estimation is not affected by the post-residualized weighting step. Across all 16 sites, the point estimates from post-residualized weighting do not change substantially from standard estimation approaches. Even in experimental sites in which it may not be advantageous to perform post-residualized weighting for efficiency gains, point estimates from post-residualized weighting methods are close to those from the conventional weighting estimators. We report the mean absolute error for all 16 sites in Supplementary Materials Table A7.

7.2.2 Diagnostics

To evaluate whether the post-residualized weighting estimators provide efficiency gains over conventional approaches, we estimate our diagnostics. Supplementary Materials Table A9 summarizes the performance of the diagnostic measures across all 16 sites for both earnings and employment.

On average, we see that the proposed diagnostic measures are able to adequately capture when researchers should expect precision gains from residualizing. The diagnostic has a high true positive rate for both directly residualizing and using as a covariate. As such, when the diagnostic measures indicate that researchers should residualize, residualizing results in precision gains. In the case when we are directly residualizing, the diagnostic measure also has a relatively high true negative rate, which implies that when , there is a loss in precision from directly residualizing. In the case of including as a covariate, there is a greater false negative rate, as the diagnostic tends to be more conservative in this setting. This is especially noticeable when employment is the outcome. Many of the false negatives here correspond to estimated values that are negative, but very close to zero.

7.2.3 Efficiency Gain

Results on the efficiency gains to post-residualized weighting are summarized in Table 3, and graphically displayed in Figure 4. Restricting our attention to the sites for which the values are greater than zero, there is a large reduction in variance overall from residualizing. When directly residualizing, for earnings, residualizing results in a 21% reduction in estimated variance for the weighted estimator and a 12% reduction for the weighted least squares estimator. For employment, directly residualizing leads to a 10% reduction in estimated variance for the weighted estimator and a 5% reduction for the weighted least squares estimator.

Summary of Standard Errors across Experimental Sites Subset by Diagnostic

Earnings

Employment

Number

of Sites

Conventional

Post-Resid.

Weighting

Number

of Sites

Conventional

Post-Resid.

Weighting

Weighted

Direct Residualizing

10

2.42

2.13

11

8.33

7.81

as Covariate

7

2.17

1.86

1

5.58

5.01

Weighted Least Squares

Direct Residualizing

12

2.71

2.56

11

7.88

7.64

as Covariate

7

1.87

1.71

1

5.56

5.45

When using as a covariate, we see that including the predicted outcomes as a covariate results in a 25% reduction in variance for the weighted estimator and 16% reduction for weighted least squares when earnings is the outcome. For employment, adjusting for the predicted outcomes results in a 9% reduction in variance for the weighted estimator, and a 4% reduction for the weighted least squares.

There are several takeaways to highlight. First, we see that directly residualizing the outcomes can result in significant precision gain. In particular, the reduction in variance in the post-residualized weighted least squares demonstrates the advantage residualizing has over just using regression adjustment. Second, the larger reduction in variance from using as a covariate underscores the value of being able to capture the scaled relationships between the outcomes in the population data and in the experimental sample.

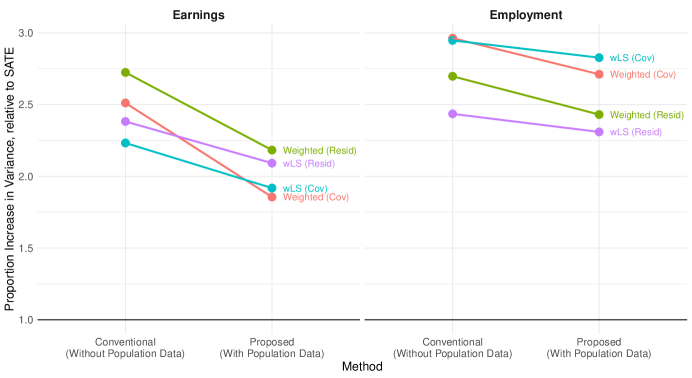

Figure 4 shows the relative variance of the PATE estimators to the unweighted SATE. It is well known that PATE estimators typically have higher variance than the SATE [31], however we see that with the post-residualized method, some of the precision loss incurred from the weighted PATE estimators can be offset. Table 3 provides a summary of the standard errors of the PATE estimators, relative to the difference-in-means estimators.

8 Conclusion

Ever since researchers raised concerns over external validity of experiments [9], researchers have also worked on how to estimate population causal effects with weighting estimators [11, 8, 23, 13]. These estimators, while unbiased under Assumptions 1 – 3, typically have high variance, especially if some sampling weights are extreme [31], making it difficult for policymakers and practitioners to draw conclusions about the impact of treatment in the target population.

In this paper we introduce post-residualized weighting, which solves an important problem for practitioners by improving precision in estimation of population treatment effects. To do this, we leverage outcome data measured in the target population, valuable information not incorporated by current methods. Our proposed method first builds a flexible model using population outcome and covariate data, which is then used to residualize the experimental outcome data. We show that post-residualized weighting estimators, which rely on residualized outcomes, are consistent for the PATE under the same identifying assumptions as current methods. However, by utilizing residualized outcomes, the post-residualized weighting estimators can obtain large precision gains over conventional approaches. We propose three classes of post-residualized weighting estimators: a weighting estimator using the residualized experimental outcomes; a weighted least squares estimator based on the residualized experimental outcomes; and an extension of weighted least squares in which the predicted values of the residualizing model are included as a covariate.

Our proposed framework has many advantages. As discussed in Section 3.2, the residualizing model, , is an “algorithmic model,” which merely needs to adequately predict the outcomes measured in the experiment, but does not need to be correctly specified. This allows researchers a great deal of flexibility in constructing it. In Section 5 we discuss how researchers can leverage proxy outcomes that are correlated with, but different from, the outcome measured in the experimental setting. Finally, we provide diagnostic measures, based on the outcomes measured among experimental controls, that allow researchers to determine whether post-residualized weighting will likely improve precision in estimating the PATE.

We evaluate our three post-residualized estimators through simulation studies and an empirical application. Our simulations show significant precision gains from post-residualized weighting, and confirm the performance of the diagnostic measure to differentiate when researchers should expect precision gains from post-residualized weighting. We also find that including the predicted outcomes as a covariate ensures that post-residualized weighting does not hurt precision.

In our re-evaluation of the impact of the Job Training Partnership Act (JTPA), we use the multi-site nature of the experiment to benchmark the performance of our estimators relative to common methods using a within study comparison approach. We evaluate two outcomes, employment and earnings. We find that the post-residualized methods result in a 5-25% average reduction in variance, and that confidence intervals maintain nominal coverage. In particular, we achieve the most significant gains from including the predicted outcomes as a covariate, underscoring the value of this method when scaling issues may be present in the relationship between the outcomes in the population data and in the experimental sample. Finally, our diagnostic measures accurately capture when the post-residualized estimators result in precision gains in estimation of the PATE.

References

- [1] Susan Athey, Raj Chetty and Guido Imbens “Combining experimental and observational data to estimate treatment effects on long term outcomes” In arXiv preprint arXiv:2006.09676, 2020

- [2] Susan Athey, Raj Chetty, Guido W Imbens and Hyunseung Kang “The surrogate index: Combining short-term proxies to estimate long-term treatment effects more rapidly and precisely”, 2019

- [3] Delia Baldassarri and Maria Abascal “Field experiments across the social sciences” In Annual Review of Sociology 43 Annual Reviews, 2017, pp. 41–73

- [4] Abhijit V Banerjee and Esther Duflo “The experimental approach to development economics” In Annu. Rev. Econ. 1.1 Annual Reviews, 2009, pp. 151–178

- [5] Elias Bareinboim and Judea Pearl “Causal Inference and the Data-Fusion Problem” In Proceedings of the National Academy of Sciences 113.27 National Acad Sciences, 2016, pp. 7345–7352

- [6] Howard S Bloom “The National JTPA Study. Title II-A Impacts on Earnings and Employment at 18 Months.” ERIC, 1993

- [7] Leo Breiman “Random forests” In Machine learning 45.1 Springer, 2001, pp. 5–32

- [8] Ashley L Buchanan et al. “Generalizing Evidence From Randomized Trials Using Inverse Probability of Sampling Weights” In Journal of the Royal Statistical Society: Series A (Statistics in Society) 181.4 Wiley Online Library, 2018, pp. 1193–1209

- [9] Donald T Campbell and Julian C Stanley “Experimental and quasi-experimental designs for research” Houghton Mifflin Company, 1963

- [10] Victor Chernozhukov, Mert Demirer, Esther Duflo and Ivan Fernandez-Val “Generic Machine Learning Inference on Heterogeneous Treatment Effects in Randomized Experiments, with an Application to Immunization in India”, 2018

- [11] Stephen R Cole and Elizabeth A Stuart “Generalizing evidence from randomized clinical trials to target populations: The ACTG 320 trial” In American journal of epidemiology 172.1 Oxford University Press, 2010, pp. 107–115

- [12] Bénédicte Colnet et al. “Causal Inference Methods for Combining Randomized Trials and Observational Studies: A Review” In arXiv preprint arXiv:2011.08047, 2020

- [13] Issa J Dahabreh et al. “Generalizing Causal Inferences from Individuals in Randomized Trials to All Trial-Eligible Individuals” In Biometrics 75.2 Wiley Online Library, 2019, pp. 685–694

- [14] Angus Deaton and Nancy Cartwright “Understanding and misunderstanding randomized controlled trials” In Social Science & Medicine 210 Elsevier, 2018, pp. 2–21

- [15] Jean-Claude Deville and Carl-Erik Särndal “Calibration Estimators in Survey Sampling” In Journal of the American Statistical Association 87.418 Taylor & Francis, 1992, pp. 376–382

- [16] Peng Ding “Two seemingly paradoxical results in linear models: the variance inflation factor and the analysis of covariance” In Journal of Causal Inference 9.1, 2021, pp. 1–8 DOI: doi:10.1515/jci-2019-0023

- [17] Naoki Egami and Erin Hartman “Elements of External Validity: Framework, Design, and Analysis”, Available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3775158, 2020

- [18] Naoki Egami and Erin Hartman “Covariate Selection for Generalizing Experimental Results: Application to Large-Scale Development Program in Uganda” In Journal of the Royal Statistical Society, Series A, 2021

- [19] Armin Falk and James J Heckman “Lab experiments are a major source of knowledge in the social sciences” In science 326.5952 American Association for the Advancement of Science, 2009, pp. 535–538

- [20] David A. Freedman “On regression adjustments in experiments with several treatments” In Ann. Appl. Stat. 2.1 The Institute of Mathematical Statistics, 2008, pp. 176–196 DOI: 10.1214/07-AOAS143

- [21] Alan S. Gerber and Donald P. Green “The Effects of Canvassing, Telephone Calls, and Direct Mail on Voter Turnout: A Field Experiment” In The American Political Science Review 94.3 [American Political Science Association, Cambridge University Press], 2000, pp. 653–663 URL: http://www.jstor.org/stable/2585837

- [22] Jens Hainmueller “Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies” In Political analysis JSTOR, 2012, pp. 25–46

- [23] Erin Hartman, Richard Grieve, Roland Ramsahai and Jasjeet S Sekhon “From sample average treatment effect to population average treatment effect on the treated: combining experimental with observational studies to estimate population treatment effects” In Journal of the Royal Statistical Society: Series A (Statistics in Society) 178.3 Wiley Online Library, 2015, pp. 757–778

- [24] John Huber “Is theory getting lost in the “identification revolution”?” In The Monkey Cage, 2013 URL: https://themonkeycage.org/2013/06/is-theory-getting-lost-in-the-identification-revolution/

- [25] Daniel Jacob “Cross-fitting and averaging for machine learning estimation of heterogeneous treatment effects” In arXiv preprint arXiv:2007.02852, 2020

- [26] Nathan Kallus and Xiaojie Mao “On the role of surrogates in the efficient estimation of treatment effects with limited outcome data” In arXiv preprint arXiv:2003.12408, 2020

- [27] Joseph DY Kang and Joseph L Schafer “Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data” In Statistical science 22.4 Institute of Mathematical Statistics, 2007, pp. 523–539

- [28] Holger L Kern, Elizabeth A Stuart, Jennifer Hill and Donald P Green “Assessing methods for generalizing experimental impact estimates to target populations” In Journal of research on educational effectiveness 9.1 Taylor & Francis, 2016, pp. 103–127

- [29] Mark J Laan, Eric C Polley and Alan E Hubbard “Super Learner” In Statistical Applications in Genetics and Molecular Biology 6.1 De Gruyter, 2007

- [30] Winston Lin “Agnostic Notes on Regression Adjustments to Experimental Data: Reexamining Freedman’s Critique” In Annals of Applied Statistics 7.1 The Institute of Mathematical Statistics, 2013, pp. 295–318 DOI: 10.1214/12-AOAS583

- [31] Luke W. Miratrix, Jasjeet S. Sekhon, Alexander G. Theodoridis and Luis F. Campos “Worth Weighting? How to Think About and Use Weights in Survey Experiments” In Political Analysis 26.3 Cambridge University Press, 2018, pp. 275–291 DOI: 10.1017/pan.2018.1