School of Computing

\universityNewcastle University

\crest![[Uncaptioned image]](/html/2111.00987/assets/University_Crest.png) \degreetitleDoctor of Philosophy

\subjectLaTeX

\degreetitleDoctor of Philosophy

\subjectLaTeX

Modelling the transition to a low-carbon energy supply

Abstract

A transition to a low-carbon electricity supply is crucial to limit the impacts of climate change. Reducing carbon emissions could help prevent the world from reaching a tipping point, where runaway emissions are likely. Runaway emissions could lead to extremes in weather conditions around the world - especially in problematic regions unable to cope with these conditions.

However, the movement to a low-carbon energy supply can not happen instantaneously due to the existing fossil-fuel infrastructure and the requirement to maintain a reliable energy supply. Therefore, a low-carbon transition is required, however, the decisions various stakeholders should make over the coming decades to reduce these carbon emissions are not obvious. This is due to many long-term uncertainties, such as electricity, fuel and generation costs, human behaviour and the size of electricity demand. A well choreographed low-carbon transition is, therefore, required between all of the heterogenous actors in the system, as opposed to changing the behaviour of a single, centralised actor.

The objective of this thesis is to create a novel, open-source agent-based model to better understand the manner in which the whole electricity market reacts to different factors using state-of-the-art machine learning and artificial intelligence methods. In contrast to other works, this thesis looks at both the long-term and short-term impact that different behaviours have on the electricity market by using these state-of-the-art methods.

Specifically, we investigate the following applications:

-

1.

Predictions are made to predict electricity demand in the short-term. We model the impact that poor predictions have on investments in electricity generators and utilisation over the long-term. We find that poor short-term predictions lead to a higher proportion of coal, gas, and nuclear power plants.

-

2.

We devise a long-term carbon tax for the United Kingdom using a genetic algorithm approach. We find multiple strategies that can minimise both long-term carbon emissions and electricity cost.

-

3.

Oligopolies can have a detrimental effect on an electricity market by raising electricity prices without an increase in benefit to users. Reinforcement learning can be used to devise intelligent bidding strategies which are based upon forecasts and predictions of other agent behaviour to maximise revenues. These behaviours can not be modelled through traditional rule-based algorithms. We use reinforcement learning to model strategic bidding into the electricity market, and find ways to limit the impact of this strategic bidding through a market cap. We find that introducing a market cap can significantly reduce the ability for oligopolies to manipulate the market.

These studies require a number of core challenges to be addressed to ensure our agent-based model, ElecSim, is fit for purpose. These are:

-

1.

Development of the ElecSim model, where the replication of the pertinent features of the electricity market was required. For example, generation company investment behaviour, electricity market design and temporal granularity. We find that the temporal granularity of the model has a large impact on accuracy of the model, but with suitably chosen representative days calibration is possible to accurately model a time period.

-

2.

The complexity of a model increases with the replication of increasing market features. Therefore, optimisation of the code was required to maintain computational tractability, to allow for multiple scenario runs. This enabled us to run multiple iterations to train different machine learning techniques.

-

3.

Once the model has been developed, its long-term behaviour must be verified to ensure accuracy. In this work, cross-validation was used to both validate and calibrate ElecSim. We are able to accurately model a historic period observed in the real-world with this approach

-

4.

To ensure that the salient parameters are found, a sensitivity analysis was run. In addition, various example scenarios were generated to show the behaviour of the model. We find that the input parameters, such as the cost of capital have a disproportionate effect on the long-term electricity mix.

The findings outlined previously demonstrate the ability for artificial intelligence, machine learning and agent-based models to perform complex analyses in an uncertain system. We find that solely focusing on the accuracy of machine learning techniques, for instance, misses out on a significant amount research potential. We instead argue, that by further developing these research themes, we are able to better understand the electricity market system of the United Kingdom.

keywords:

LaTeX PhD Thesis Engineering University of CambridgeI would like to dedicate this thesis to my family and my loving parents…

I hereby declare that except where specific reference is made to the work of others, the contents of this dissertation are original and have not been submitted in whole or in part for consideration for any other degree or qualification in this, or any other university. This dissertation is my own work and contains nothing which is the outcome of work done in collaboration with others, except as specified in the text and Acknowledgements. This dissertation contains fewer than 65,000 words including appendices, bibliography, footnotes, tables and equations and has fewer than 150 figures.

Acknowledgements.

First, I would like to express my gratitude to my supervisors Dr Matthew Forshaw and Dr Stephen McGough. Who, without their support, guidance and insight I would have been unable to develop my skills in an academic context. Through their help and encouragements I have been able to exceed my own expectations. Secondly, I would like to thank my parents and brother for supporting me during this time. Especially my father who has proved a guiding light during the most challenging parts. For example, inspiring my work on how disruption could be modelled with computational methods and pushing me to go further. Thirdly I would like to thank Sumiré Moncholi for putting up with me during these years and providing daily support and care. Since joining Newcastle University I have been helped and inspired by the vast range of problems and applications tackled within the School of Computing and the School of Mathematics, Statistics and Physics. In particular Junyang Wang, George Stamatiadis, Adam Cattermole, Kathryn Garside, Alexander Brown, Michael Dunne-Willows, Ashleigh McLean, Lauren Roberts, Thomas Cooper, Shane Halloran, Jonny Law, Peter Michalák, Saleh Mohamad and Mario Parreno. I would also like to thank all my friends outside of the department during this time, especially Thomas Smith, Clement Venard, Sam Major, Marta Fernandez, Wenijan Yang, Alessandro Boussalem, Lars Eriksson, Tom Brunt, Owen Jones, Marianne Amor, Kevin Amor and Connor Scott. Finally, I would like to thank my colleagues at the University of Cambridge’s Centre for Science and Policy, for providing a challenging and stimulating environment to undertake an internship: Nicola Buckley, Katie Cohen, Rob Doubleday, Su Ford, Kate McNeil, Lauren Milden, Jackie Ouchikh, Erica Pramauro and Laura Sayer.Glossary

- Artificial neural network

- A machine learning algorithm that is modelled on the brain and made up of multiple layers of neurons and weights

- Dispatched

- A power plant can be dispatched if the time and amount of electricity that can be controlled by a human operator. Examples are gas, coal and oil power plants.

- Generation company

- A company which owns power plants and sells electricity to the grid

- Market power

- Market power refers to the ability of a firm, or group of firms, to raise and maintain prices above the level that would prevail under competition

- Net present value

- The difference between the present value of cash inflows and the present value of cash outflows over a period of time

- Online learning

- Online learning is a machine learning or statistical method which data which is made available in sequential order is used to update the predictor for future data at each step

- Peaker plant

- A peaker power plant is one which which is used in times of high demand and low supply. Due to their expense they are only used when necessary and can not compete with other sources of energy during the majority of market operation

- Smart meter

- A small digital meter which records electricity consumption within a household or business premises

- Short run marginal cost

- The cost it takes to produce an additional MWh of electricity, excluding capital costs

- Weighted average cost of capital

- The rate at which a company is expected to pay on average for its loans and in stock dividends/buybacks

Acronyms

- ABM

- Agent Based Model

- ABMs

- Agent Based Models

- ANN

- Artificial Neural Network

- ARIMA

- Auto Regressive Integrated Moving Average

- BEIS

- UK Government Department for Business, Energy and Industrial Strategy

- CCGT

- Combined Cycle Gas Turbine

- CE

- Correlation

- DDPG

- Deep Deterministic Policy Gradient

- GA

- Genetic Algorithm

- GenCos

- Generation Companies

- IRES

- Intermittent Renewable Energy Sources

- LCOE

- Levelised Cost of Electricity

- LDC

- Load Duration Curve

- LSTM

- Long Short Term Memory Neural Network

- MAE

- Mean Absolute Error

- MAPE

- Mean Absolute Percentage Error

- MARS

- Multivariate Adaptive Regression Spline

- MASE

- Mean Absolute Squared Error

- MDP

- Markov Decision Process

- MLP

- Multilayer Perceptron

- NPV

- Net Present Value

- NRMSE

- Normalised Root Mean Squared Error

- PDC

- Price Duration Curve

- PPDC

- Predicted Price Duration Curve

- RBF

- Radial Basis Function

- REE

- Relative Energy Error

- RL

- Reinforcement Learning

- RMSE

- Root Mean Squared Error

- SOM

- Self-Organizing Maps

- SVR

- Support Vector Regression

- WACC

- Weighted Average Cost of Capital

Chapter 1 Introduction

1.1 Motivation

The impacts of global warming on the earth may have profound effects on land and ocean ecosystems IPCC2018. The release of carbon emissions into the atmosphere increases the likelihood of the most severe impacts and increases the likelihood that tipping points are reached, where runaway carbon emissions and average temperature rises are likely.

Therefore a transition to a low-carbon energy supply is required to prevent the impacts of climate change. A low-carbon electricity supply is one which releases a lower amount of carbon dioxide over its lifetime than the current, fossil-fuel based system.

However, such a transition is complex and contains multiple uncertainties. For instance, what carbon tax should the UK government set over the next 30 years? Are poor short-term electricity demand forecasts locking us in to higher emissions over the long-term? Can we limit the market power of generator companies? And can we rely on these models to make decisions of such importance?

Whilst much work has been carried out investigating energy models in different electricity and energy markets, these models are not often fully validated against real-world data. This thesis seeks to validate a novel agent-based model, ElecSim, by calibrating with real-world data. Through this calibration, confidence can be gained in the underlying dynamics of the model and provide policy makers with the opportunity to better understand the system with which they are dealing with.

Secondly, much work has been undertaken to understand certain aspects of electricity markets using agent-based models and machine learning. However, this work, often, does not place these findings into a wider context. For instance, whilst a high degree of focus is placed on the ability of reinforcement learning to bid strategically within an agent-based setting, how to limit this behaviour has not been investigated to the same extent.

Similarly, machine learning has been used to predict electricity demand at various time intervals. However, the effect that different prediction methods have on the long-term electricity market has not been explored. Finally, machine learning and simulation has the ability to optimise an entire system. However, this ability received much research attention, instead the focus has been on smaller scale changes to models. In this thesis we aim to fill this research gap by first calibrating our model, and secondly reducing electricity price and carbon emissions from the United Kingdom’s electricity mix by optimising carbon tax strategies.

1.2 Research questions

The central question of this thesis is: how can artificial intelligence (AI) and machine learning (ML) answer fundamental questions of the energy transition using an agent-based model of the electricity system?

This thesis aims to go beyond small-scale improvements to agent-based models and answering scope-limited questions by understanding first: what challenges can AI and ML tackle, and secondly: how do these methods relate back to the wider energy system?

By taking this approach, we answer multiple subquestions, which are explored below:

-

1.

Can a simulation model an electrcity market over the long-term? Traditional electricity market models mimic the behaviour of centralised actors with perfect foresight and information. Other models which model actors as having imperfect foresight and information lack the ability to model multiple time-steps over a long time horizon. In Chapter 3, a novel open-source agent-based model called ElecSim is presented which challenges these issues. We show that it is possible to create an electricity model which can simulate multiple time-steps over a long-time horizon and generate realistic electricity mixes as model outputs.

-

2.

Is it possible to model the variability of an electricity system? Intermittent renewable energy can produce electricity at both maximum capacity and at zero capacity in short time intervals. It, therefore, becomes important to model these variations in power output over a long-term horizon. Otherwise, the model may overestimate the production of energy from renewables and underestimate the variability of such technologies. This is achieved in Chapter 3 by showing that with representative days, we are able to accurately model an entire year with a reduced computational burden. Without this additional feature, an overestimation of intermittent renewable energy and underestimation of dispatchable generation is observed.

-

3.

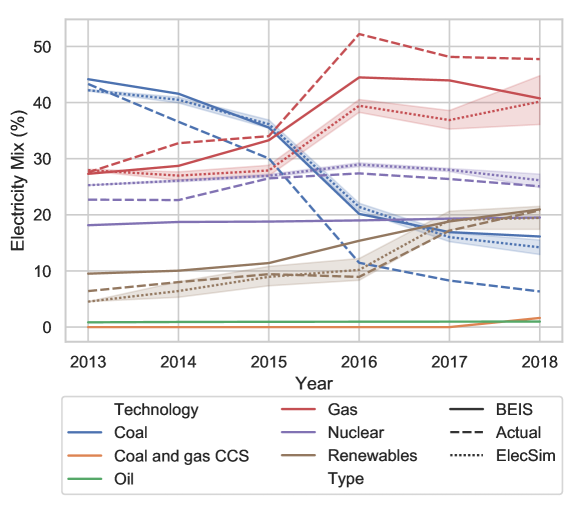

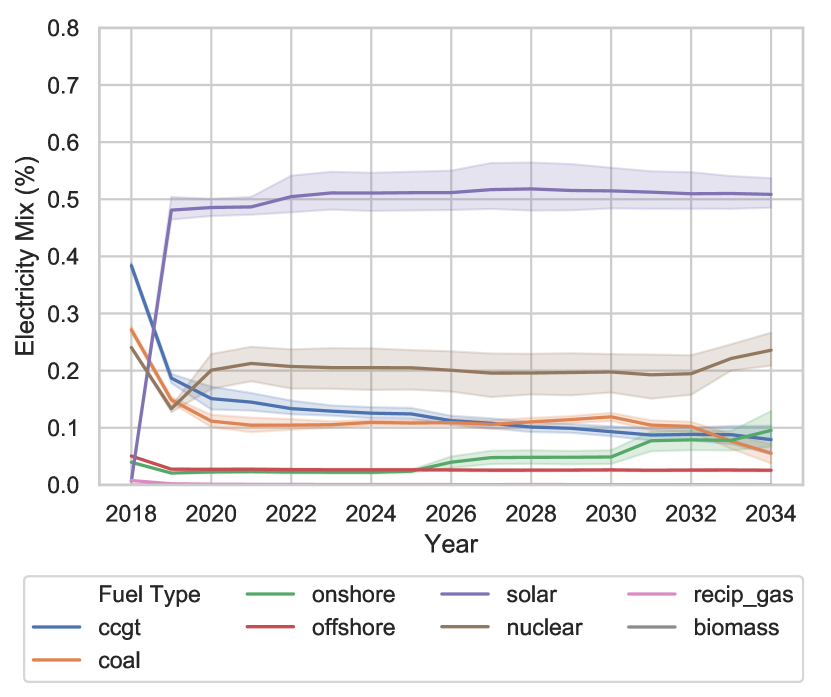

Can we trust an electricity model’s outputs? Whilst long-term energy models can provide quantitative advice to experts, policymakers and stakeholders, the veracity of these models are rarely validated. The validation of long-term electricity models can highlight problems with the dynamics of the model, important components, and provide confidence in the outputs. Here, an approach is presented to provide confidence in such outputs in Chapter 3. We achieve this through the use of a distributed genetic algorithm optimisation algorithm to calibrate our model. Through such a calibration we are able to observe a real-world transition of the UK’s electricity market from coal to gas over a 5-year period.

-

4.

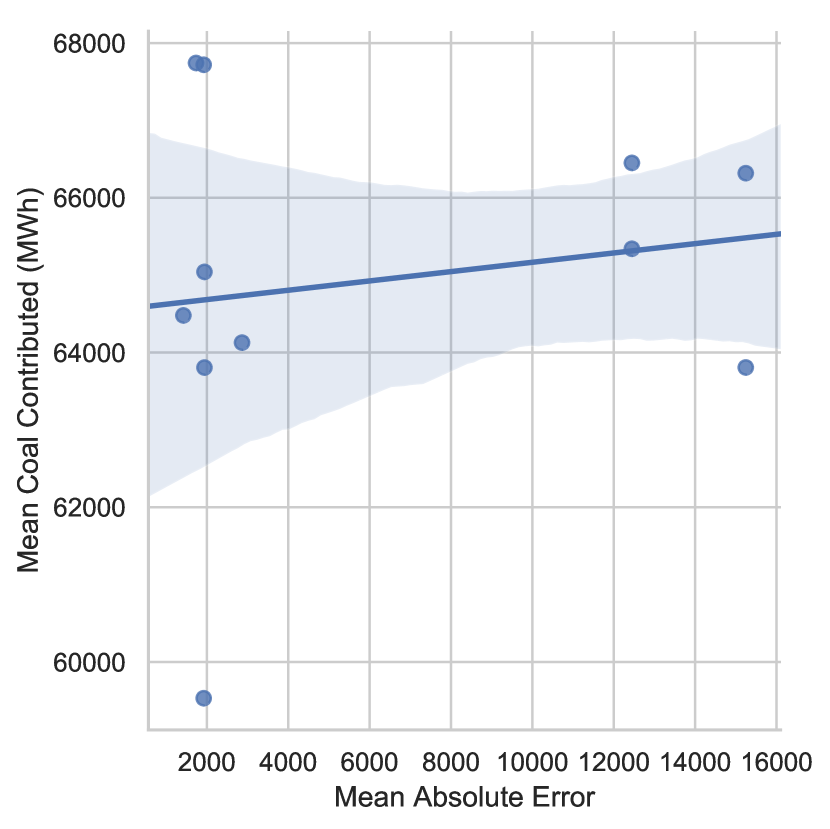

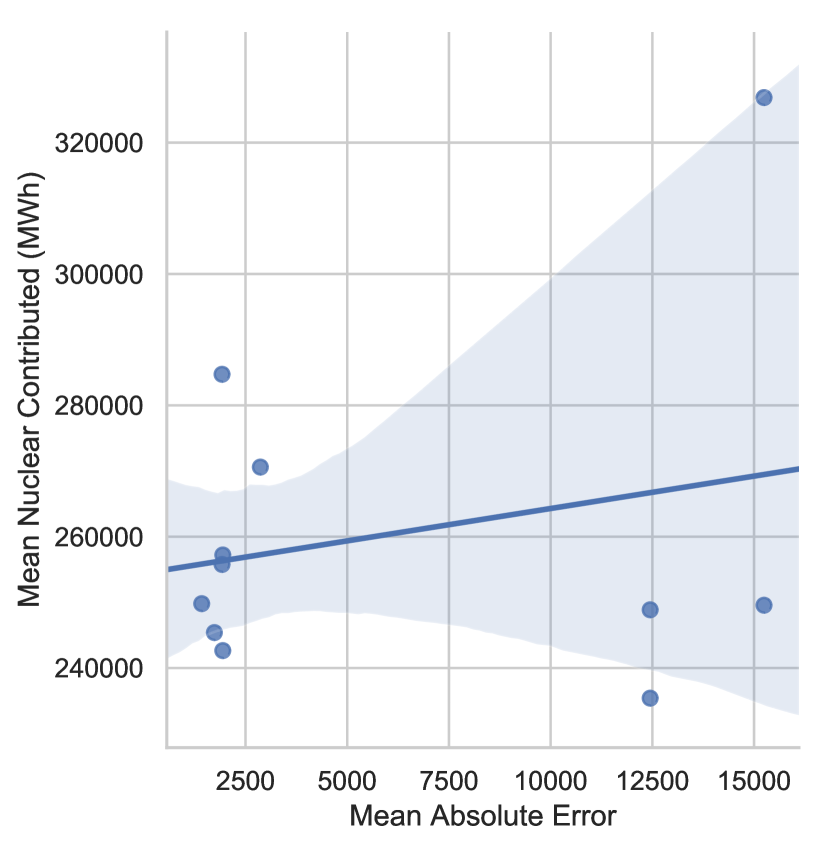

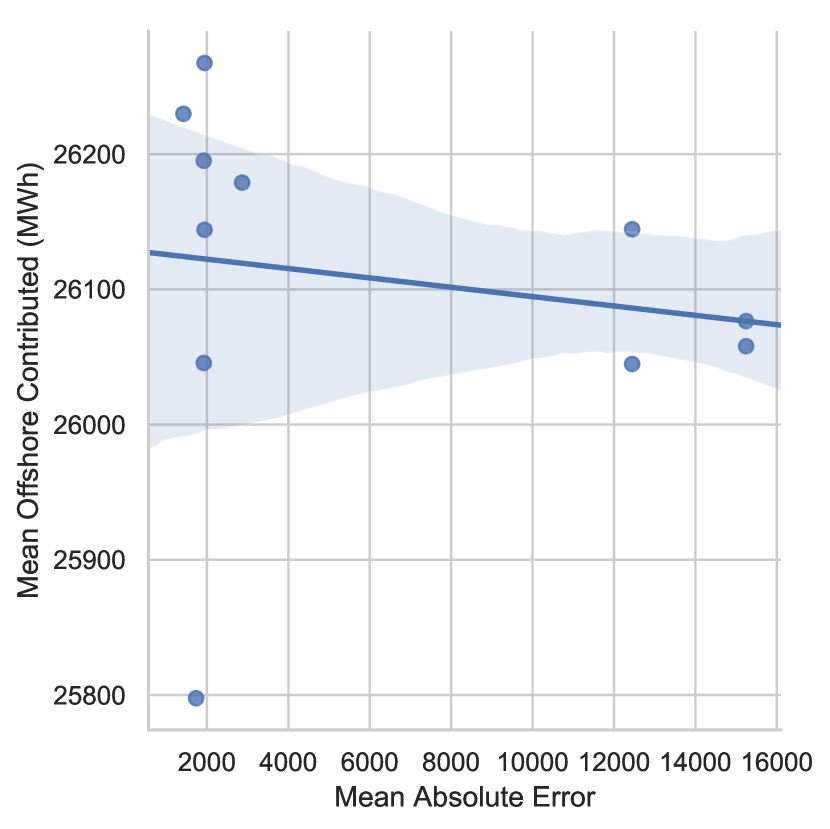

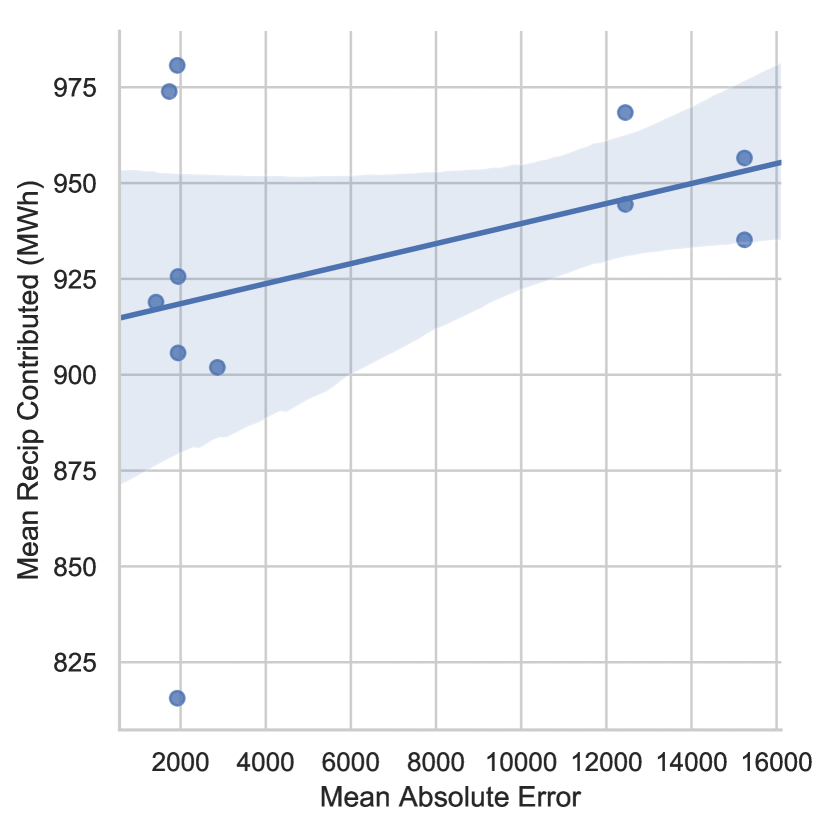

Do poor short-term forecasts of electricity demand have a long-term impact? Forecasting of electricity demand within electricity markets is critical. The settlement of markets occurs prior to the time in which the demand must be supplied. However, the long-term effect on the markets of poor forecasts has not been investigated. In Chapter 4 we investigate the long-term impact of poor short-term predictions. We find that poor short-term demand forecasts leads to increased investments in coal, gas and nuclear power, with a reduction in both onshore and offshore wind.

-

5.

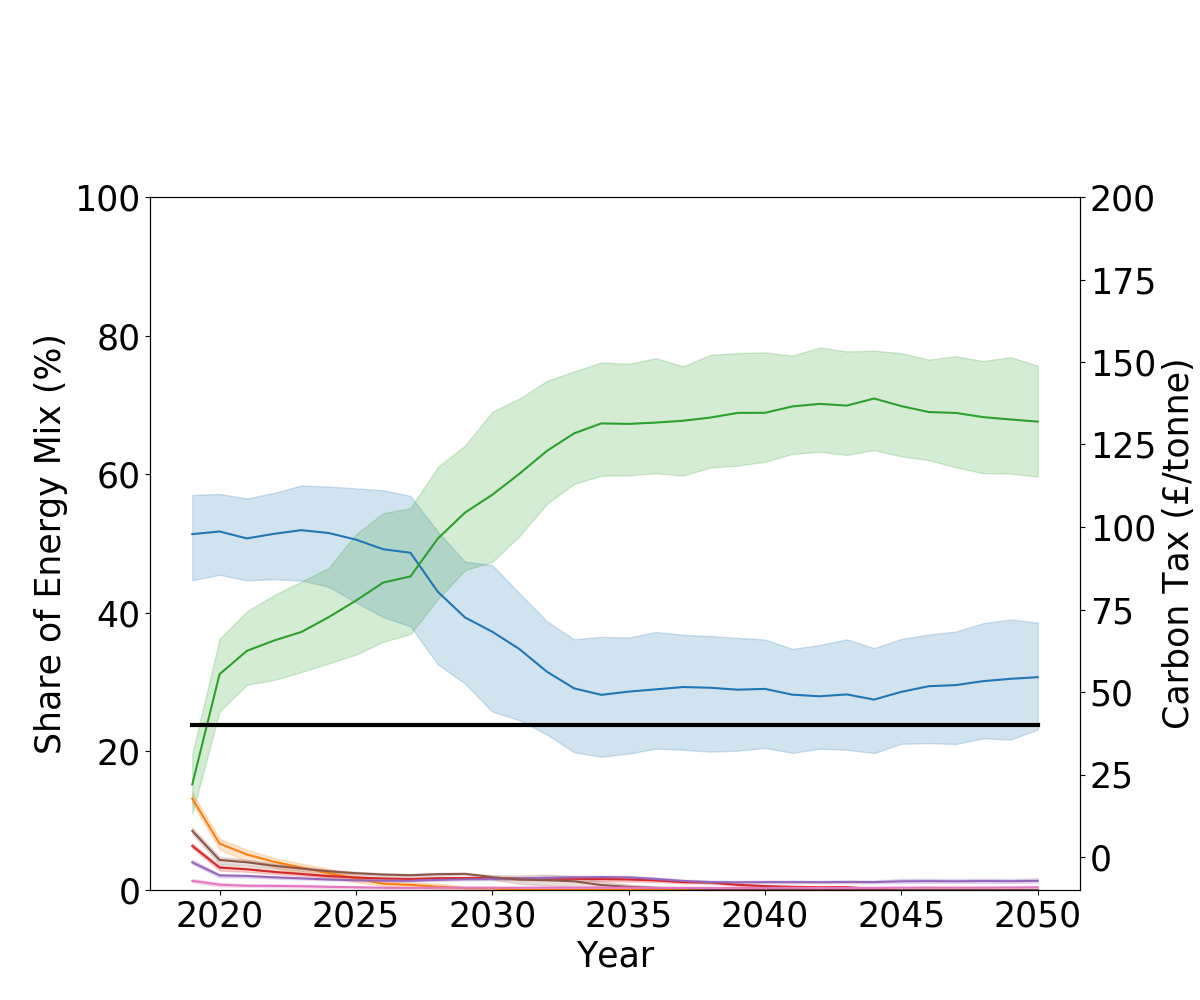

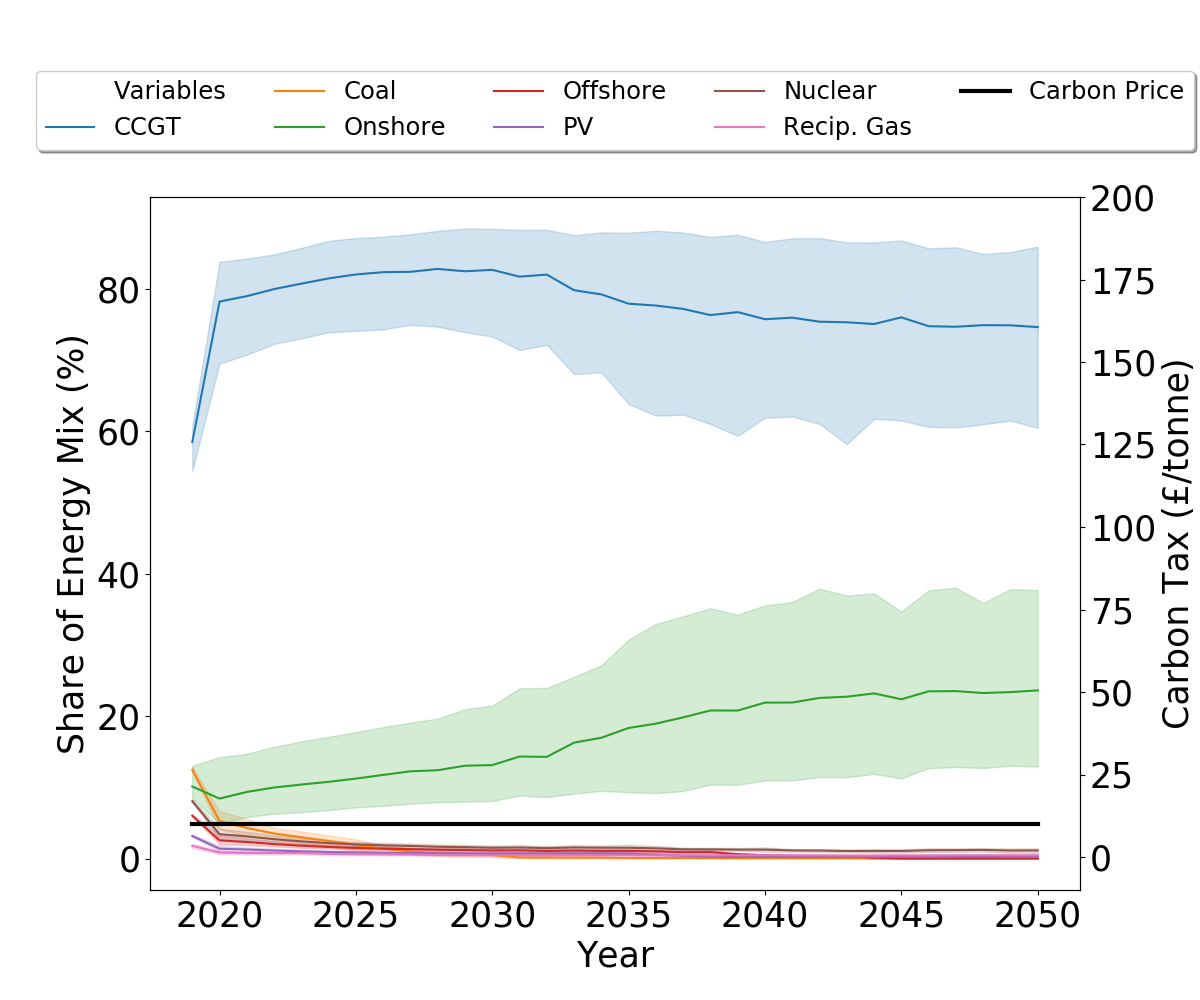

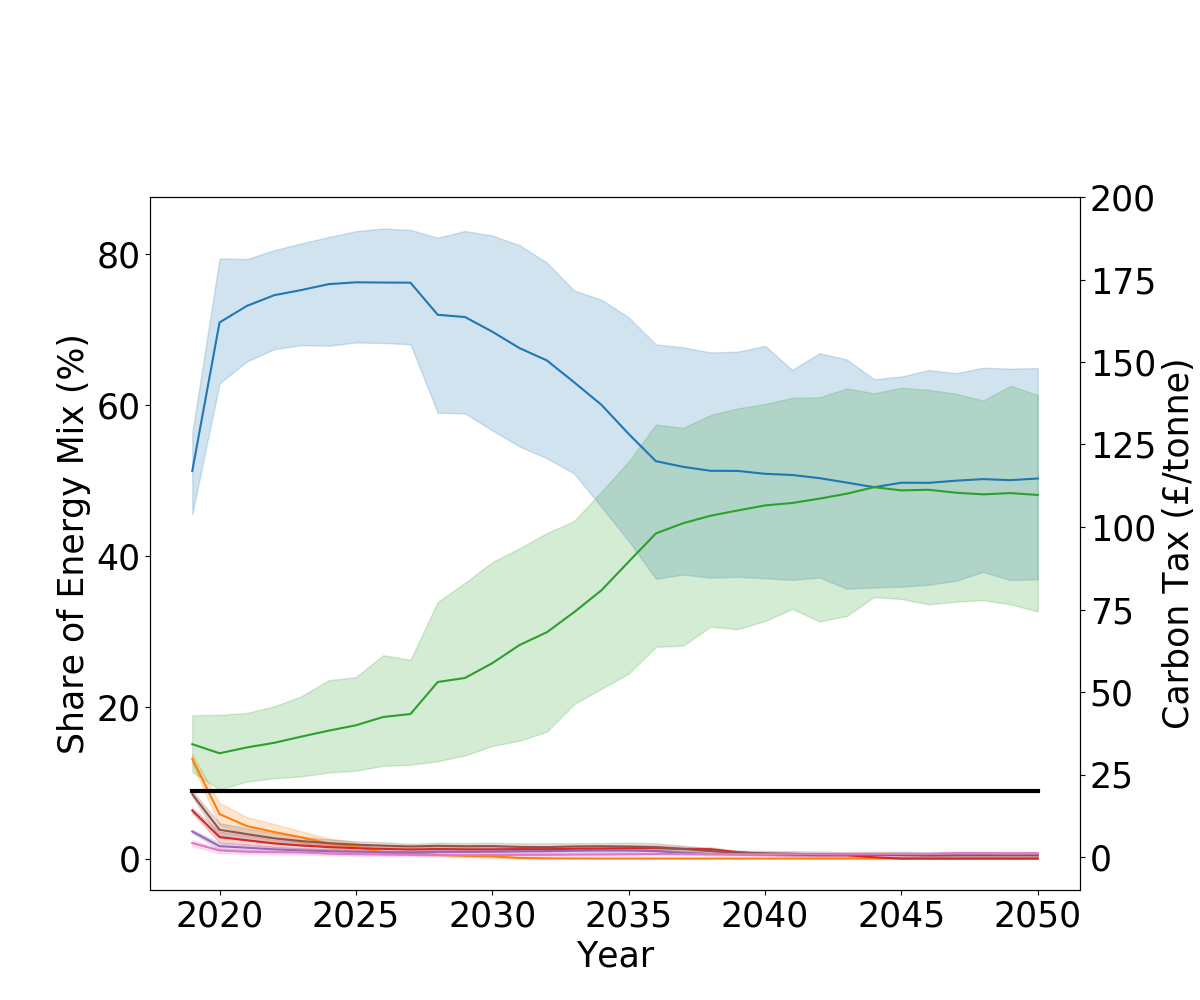

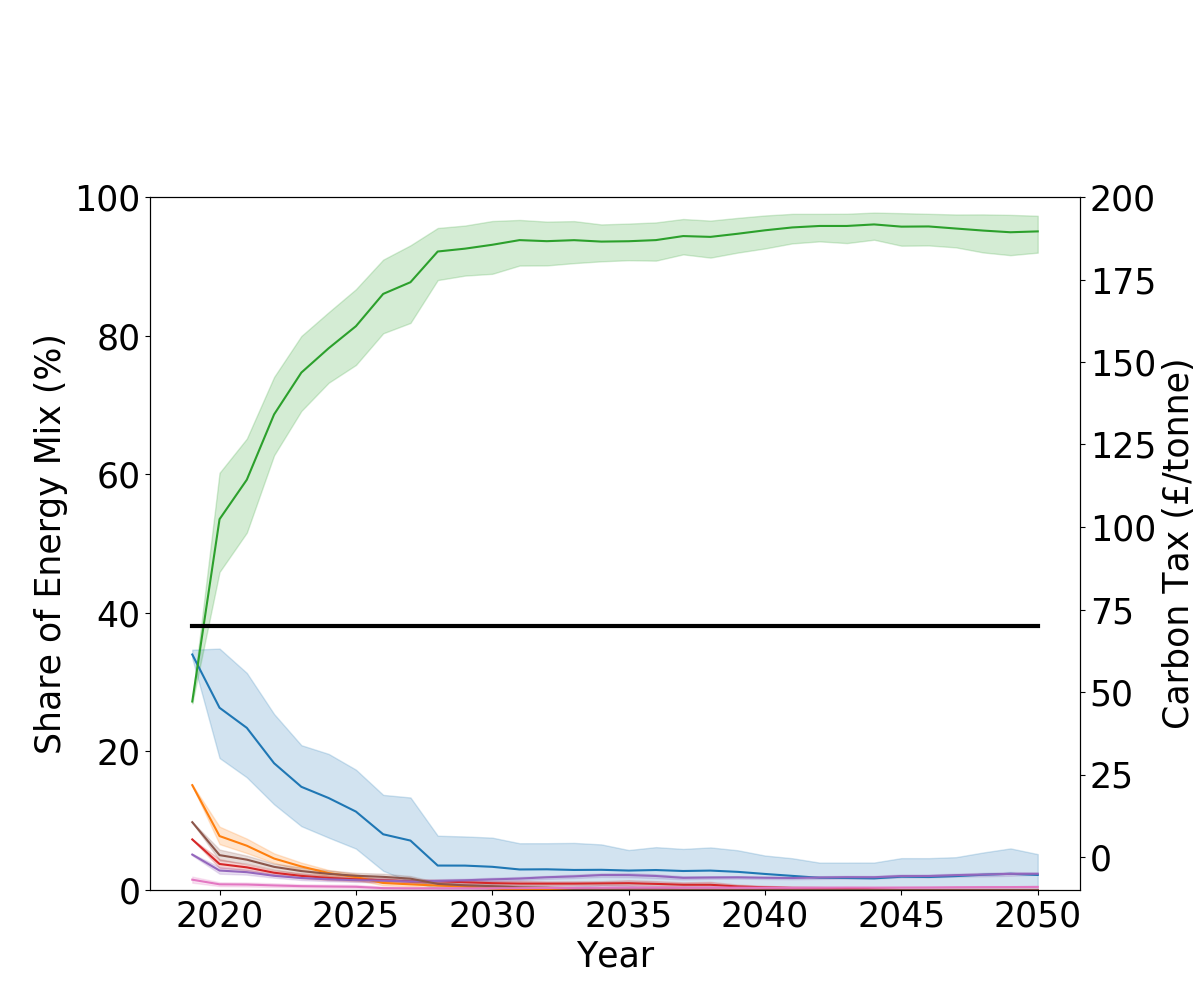

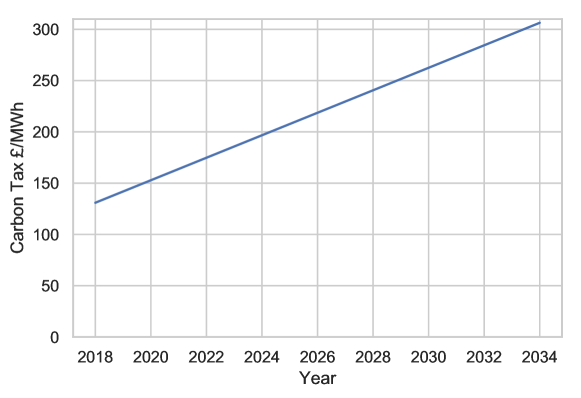

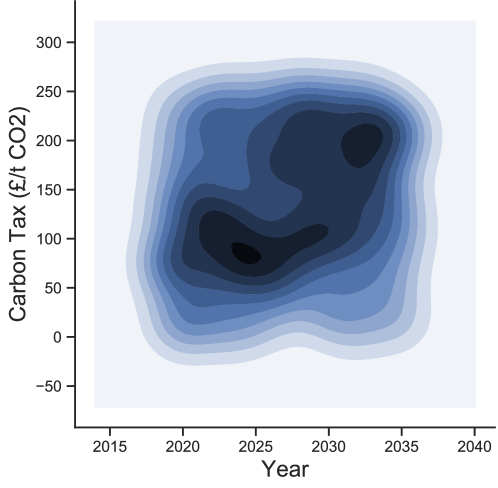

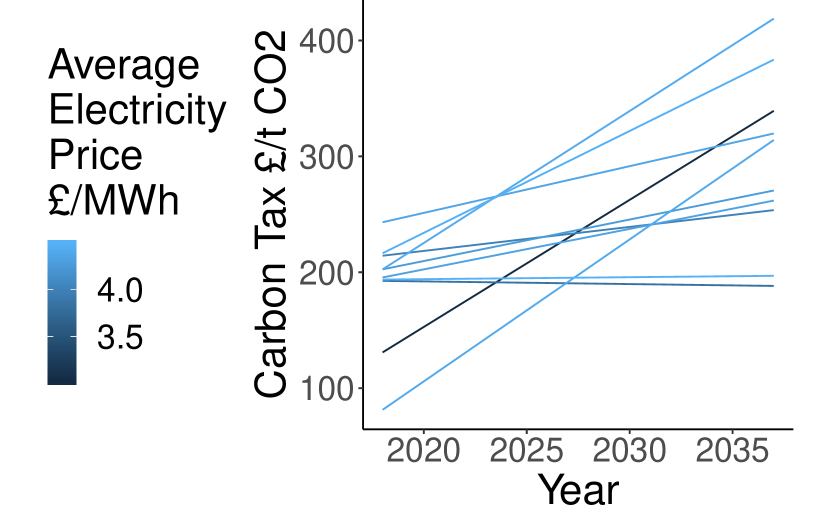

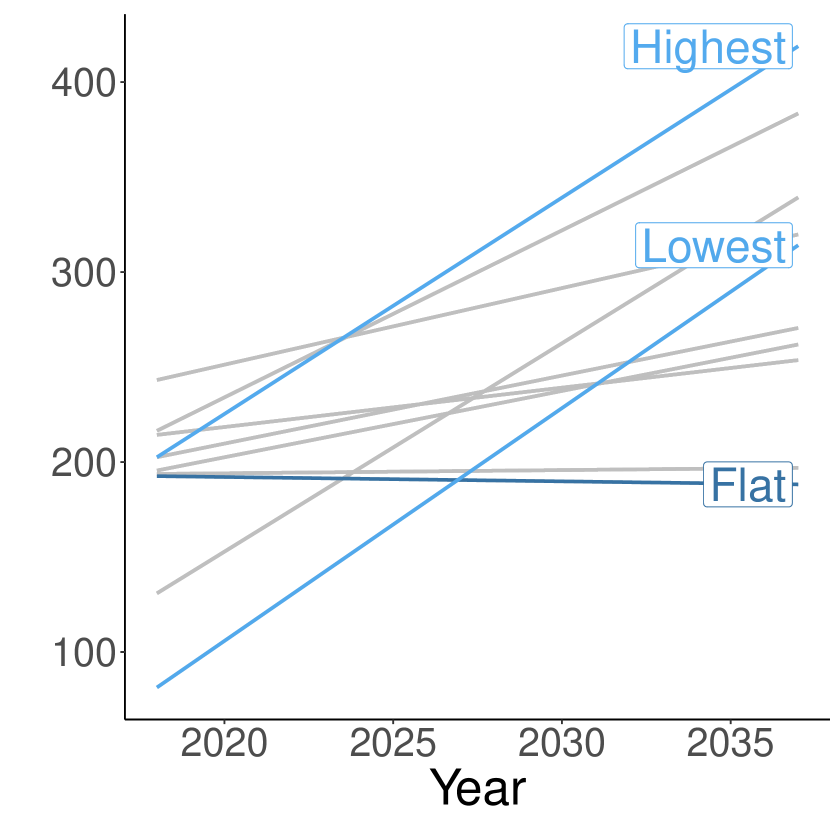

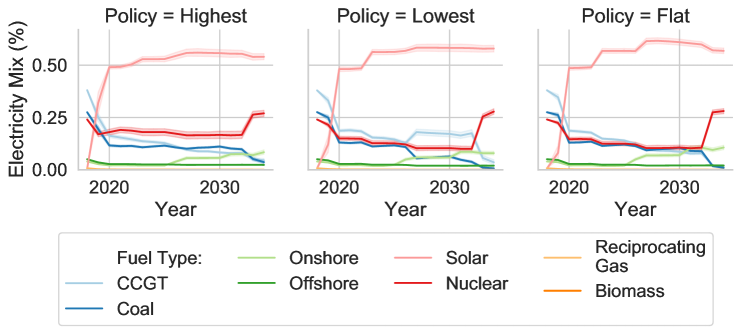

Is it possible to use an algorithm to set carbon policy? Setting carbon taxes has been proposed as a solution to reduce our reliance on fossil fuels. However, the impact of such carbon taxes are unknown, as are the optimal strategies from different perspectives. Such a problem can be solved using optimisation based techniques. Here, a solution to finding optimal strategies from the perspective of a benevolent government is presented in Chapter 5. We find that it is possible to find a variety of different carbon tax strategies to minimise both electricity price and carbon emissions, as long as a high carbon price is set (around £200).

-

6.

Is it possible to limit the power of large generator companies? It is known that oligopolies have a negative effect on markets for consumers. However, what has been explored to a lesser degree, is the proportion of capacity that generation company must own before they have market power. In addition, what would the effect be of a market cap on such electricity markets? Would a market cap reduce the ability for Generation Companies (GenCos)to inflate electricity prices artificially? Chapter 6 investigates this issue. We find that if a generator company, or group of colluding generator companies own over 11% of the total generation capacity, electricity prices start to increase. However, the impact of this market power can be limited through the setting of a market cap. In the case of the UK, a market cap of £190/MWh suffices.

Through these questions we not only answer whether AI and ML methods can be used with electricity market agent-based models, but also what is the wider impact of the behaviours on the market.

1.3 Methodology

Primarily, in this work, simulation is used as a tool to better understand and make projections for electricity markets. Specifically, in this thesis, the agent-based modelling paradigm is used. This enables us to model generator companies as individual agents, with heterogeneous strategies and characteristics. These agents have access to imperfect information and imperfect foresight. This methodology differentiates this work from the traditional centralised optimisation approach. Agent-based models are critical to model the behaviour of individual actors within an electricity system. Without this distinction, the system must be modelled as a homogenous system, which does not accurately reflect the real world. Through this approach, we hope to learn that it is possible to accurately model the UK’s national electricity system with an agent-based approach.

Machine learning and statistical techniques are used to make short-term forecasts of electricity demand. We use both deep learning, offline learning and online learning to further improve our methods. Online learning is a machine learning approach which utilises new data to update model weights, and does not require the model to be completely retrained, which is the case for offline learning. In comparison, deep learning utilises neural networks with many different layers. We utilise these methods due to their data-driven approach and strong ability to forecast time-series data. Online learning is used as over the time-periods with which we are forecasting, the underlying time-series changes in structure. Online learning is able to continually use new data points to retrain the model. Deep learning, on the other hand, uses many layers to learn more complex patterns from the training set. Through taking this approach, we hope to learn that it is possible to improve predictions for energy demand data when compared to the traditional machine learning methods.

Once our simulation model is built, we are able to answer different questions using several approaches. For example, we perturb the exogenous electricity demand by the error distribution generated by the aforementioned electricity demand forecasting methods. This provides an insight into how small errors can have large impacts on long-term electricity markets in terms of both investments made and generator utilisation. This approach was taken due to its ability to mimic the behaviour of generator companies in a simple manner. We hope to learn what the impact of short-term decisions are on the long-term market.

Multi-objective genetic algorithms are used to explore carbon tax policies which will reduce both carbon emissions and average electricity price. We find that we are able to achieve both of these goals by setting a median carbon tax of £200 per tonne of carbon dioxide. This methodology is chosen due to the genetic algorithm’s distributed nature. We are able to run the algorithm in parallel and reduce training time significantly. From this, we hope to learn that there is an automatic method to reduce the search space for policy makers when coming up with complex policy in a high parameter space.

Finally, we explore the ability for deep reinforcement learning (DRL) to make strategic bidding decisions within a day-ahead electricity market. This work enables us to see the proportion of capacity that must be controlled to artificially inflate the electricity price in the market using market power. Deep reinforcement learning was chosen due to its ability to quickly form a policy on the expected environment. The bidding environment with multiple competing agents is highly complex and difficult to solve through a rule-based approach, and so DRL is chosen to simplify the approach of forming a policy. Through this, we hope to learn the parameters which allow for the manipulation of the market, such as the size of generator companies and total capacity controlled, and how to reduce this impact of it occurs.

1.4 Contributions

The work in this thesis makes a number of key contributions:

-

1.

Development of the open-source, generalised long-term agent-based model for decentralised electricity markets, ElecSim Kell. This can be accessed at: https://github.com/alexanderkell/elecsim. This model is parametrised to the UK electricity market, and contains the major pertinent features to model this market. This answers research question 1 by modelling an electricity market over the long-term.

-

2.

Validation of the aforementioned model through the use of cross-validation through five years and comparison with the established UK Government model until 2035 Kell2020. Through this validation we are able to answer research questions 2 and 3 by modelling the inter-year variability and verify the outputs of the model.

-

3.

Forecasting of electricity demand using machine learning models and exploration of the impact of the prediction errors on the long-term electricity market Kell2018a. This contribution answers research question 4 by showing that short-term errors do have a large impact on the final electricity mix.

-

4.

Optimisation of a carbon tax policy to reduce electricity cost and carbon emissions for the UK electricity market using a multi-objective genetic algorithm, from the perspective of a benevolent government Kell2020a. This answers research question 5 by showing that it is possible to come up with an optimal strategy for setting a carbon price to reduce carbon emissions and electricity price.

-

5.

Exploration of the long-term impact of strategic bidding and collusion on decentralised electricity markets Kell2020d. This answers research question 6 by showing that if generator companies control a large part of the market, market power occurs. However, it is possible to limit these market powers significantly by setting a market cap on electricity price.

This work directly addresses the aim of the research. We use AI and ML to answer fundamental questions of the energy transition through the use of an agent-based model of the electricity system. With the development of a novel agent-based model, we are able to answer targeted questions on how the electricity system behaves under different pressures. We do not simply stop at validating the ability of an algorithm to perform a specific task, but rather relate this back to the wider market.

1.5 Thesis organisation and structure

-

Chapter 1

describes the motivations behind this thesis and highlights the main contributions of the research. Finally, the peer-reviewed publications produced during this PhD are presented.

-

Chapter 2

describes the technical background material that relates to the rest of this work and investigates the different types of solutions that have been used in the current literature and differentiate this from this work.

-

Chapter 3

introduces the simulation framework developed within this work. This includes the technical details of the simulation tool, how this simulation is validated and the difficulties of validating such simulation models. Finally, a sensitivity analysis to show the impact of various variables is displayed, and some example future scenarios are produced. This chapter contains contributions 1 and 2.

-

Chapter 4

explores the literature on electricity demand forecasting, how this can be improved with online learning, and what the long-term impact of errors are on decentralised electricity markets. This chapter contains contribution 3.

-

Chapter 5

demonstrates the ability for the model to come up with optimal strategies and scenarios through the use of machine learning techniques. Specifically, a carbon tax strategy between 2018 and 2035 is optimised to reduce both electricity cost and carbon emissions. This chapter contains contribution 4.

-

Chapter 6

demonstrates the ability for large or colluding generator companies to influence the price of electricity in their favour using deep reinforcement learning, as well as an approach to prevent this from occurring through the use of price caps. This chapter contains contribution 5.

-

Chapter 7

summarises the conclusions of the work and motivates future directions for work in this area.

1.6 Related publications

During the course of my PhD I have authored the following peer-reviewed publications:

-

Kell

Kell, A., Forshaw, M., & McGough, A. S. (2019). ElecSim : Monte-Carlo Open-Source Agent-Based Model to Inform Policy for Long-Term Electricity Planning. The Tenth ACM International Conference on Future Energy Systems (ACM e-Energy 2019), 556–565.

This work introduces the agent-based model, ElecSim. The current state-of-the-art of agent-based models is reviewed, and the technical foundations of how ElecSim works is detailed. An initial validation method of comparing the price duration curve of the model to that observed in real life is displayed. Finally, some example scenarios are presented. This work forms the basis for Chapter 3.

-

Kell2019a

Kell, A., Forshaw, M., & McGough, A. S. (2019). Modelling carbon tax in the UK electricity market using an agent-based model. E-Energy 2019 - Proceedings of the 10th ACM International Conference on Future Energy Systems, 425–427.

In this paper, further scenarios are explored by varying the carbon tax level. The effect of carbon tax on investments is demonstrated in the electricity market. This work augments the work done in Chapter 3.

-

Kell2020

Kell, A. J. M., Forshaw, M., & McGough, A. S. (2020). Long-Term Electricity Market Agent Based Model Validation using Genetic Algorithm based Optimisation. The Eleventh ACM International Conference on Future Energy Systems (e-Energy’20).

In this paper, further improvements are made to the ElecSim model. Through the addition of representative days, the model is validated between 2013 through 2018 by optimising for long-term predicted electricity price. The results are compared to those of the UK Government, for both a long-term and short-term validation. The results are comparable to those of the UK Government. This work further extends Chapter 3.

-

Kell2018a

Kell, A., McGough, A. S., & Forshaw, M. (2018). Segmenting residential smart meter data for short-Term load forecasting. e-Energy 2018 - Proceedings of the 9th ACM International Conference on Future Energy Systems.

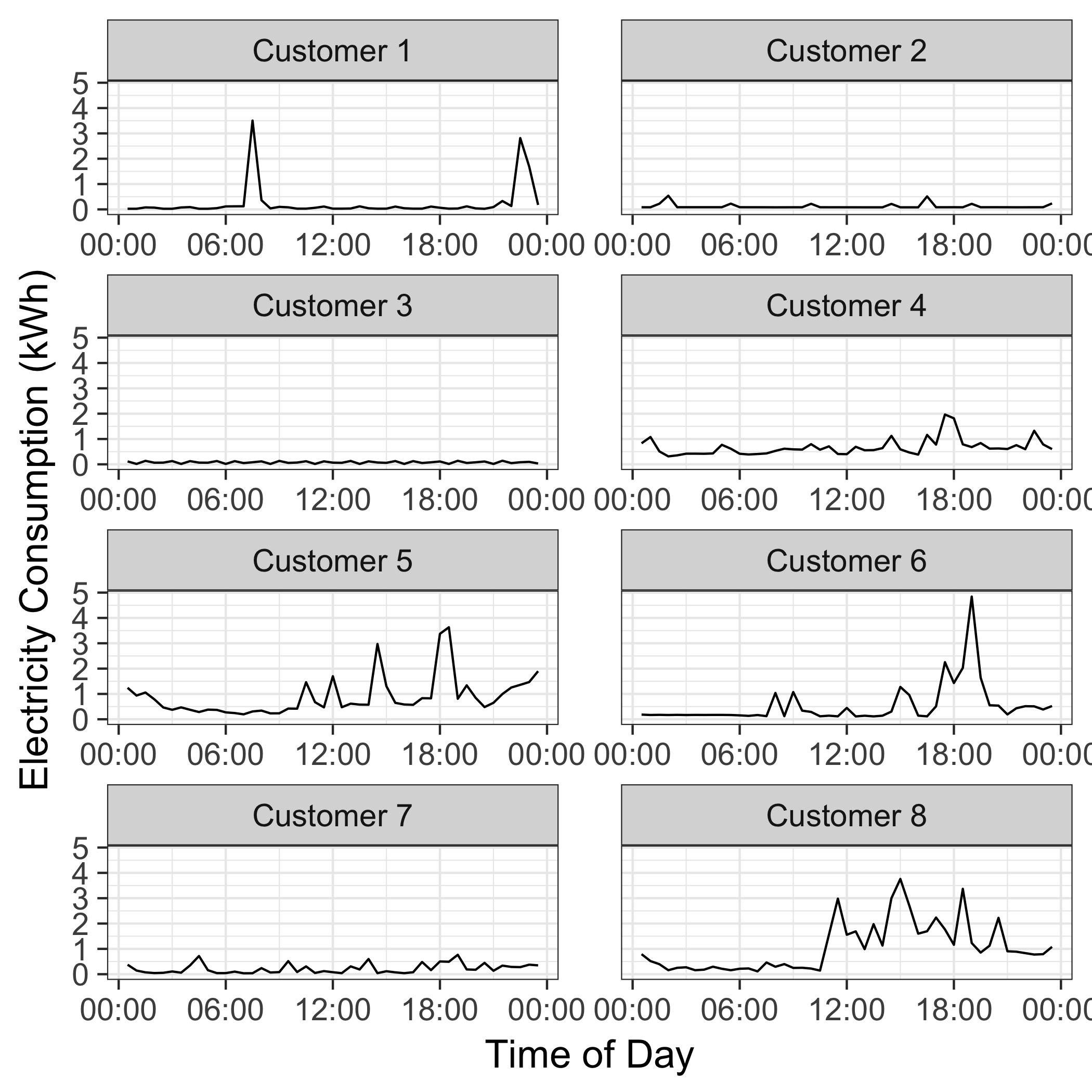

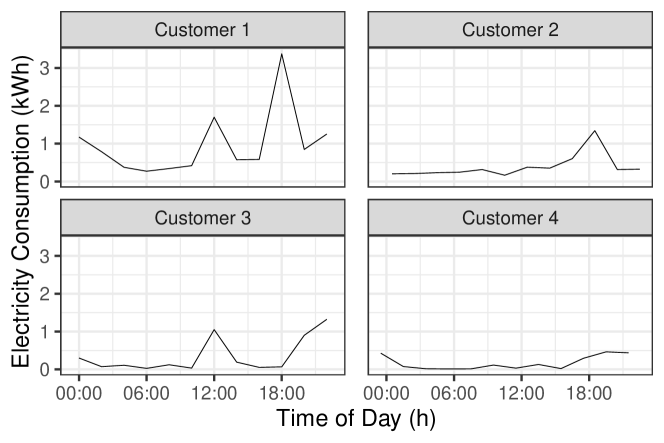

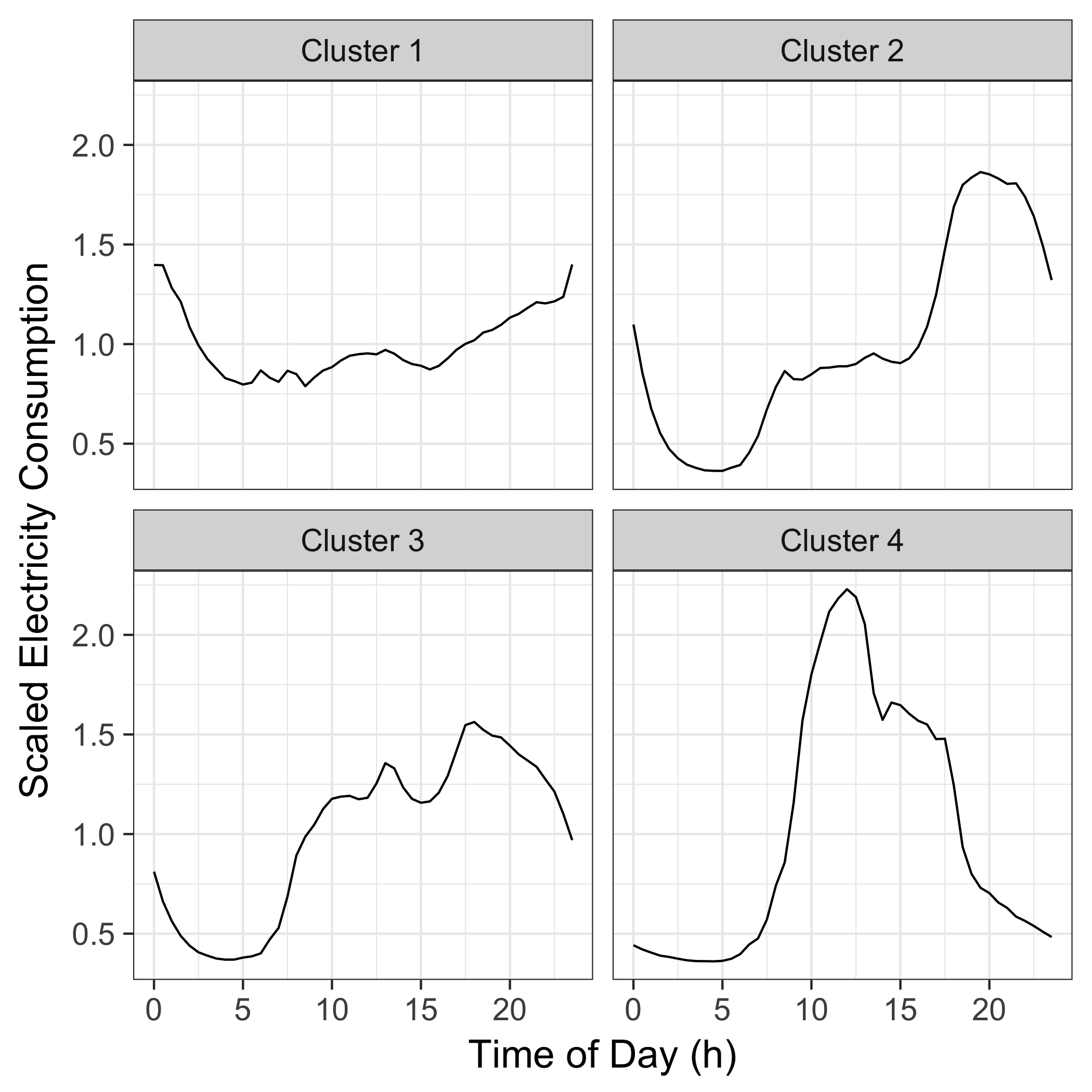

In this work, various machine learning and deep learning techniques are used to predict electricity demand 30 minutes ahead using smart meter data. Various households are clustered using a k-means clustering technique to further improve the accuracy. This paper forms the basis for Chapter 4.

-

Kell2020c

Kell, A. J. M., McGough, A. S., & Forshaw, M. (2020). The impact of online machine-learning methods on long-term investment decisions and generator utilization in electricity markets. 11th International Green and Sustainable Computing Conference, IGSC 2020.

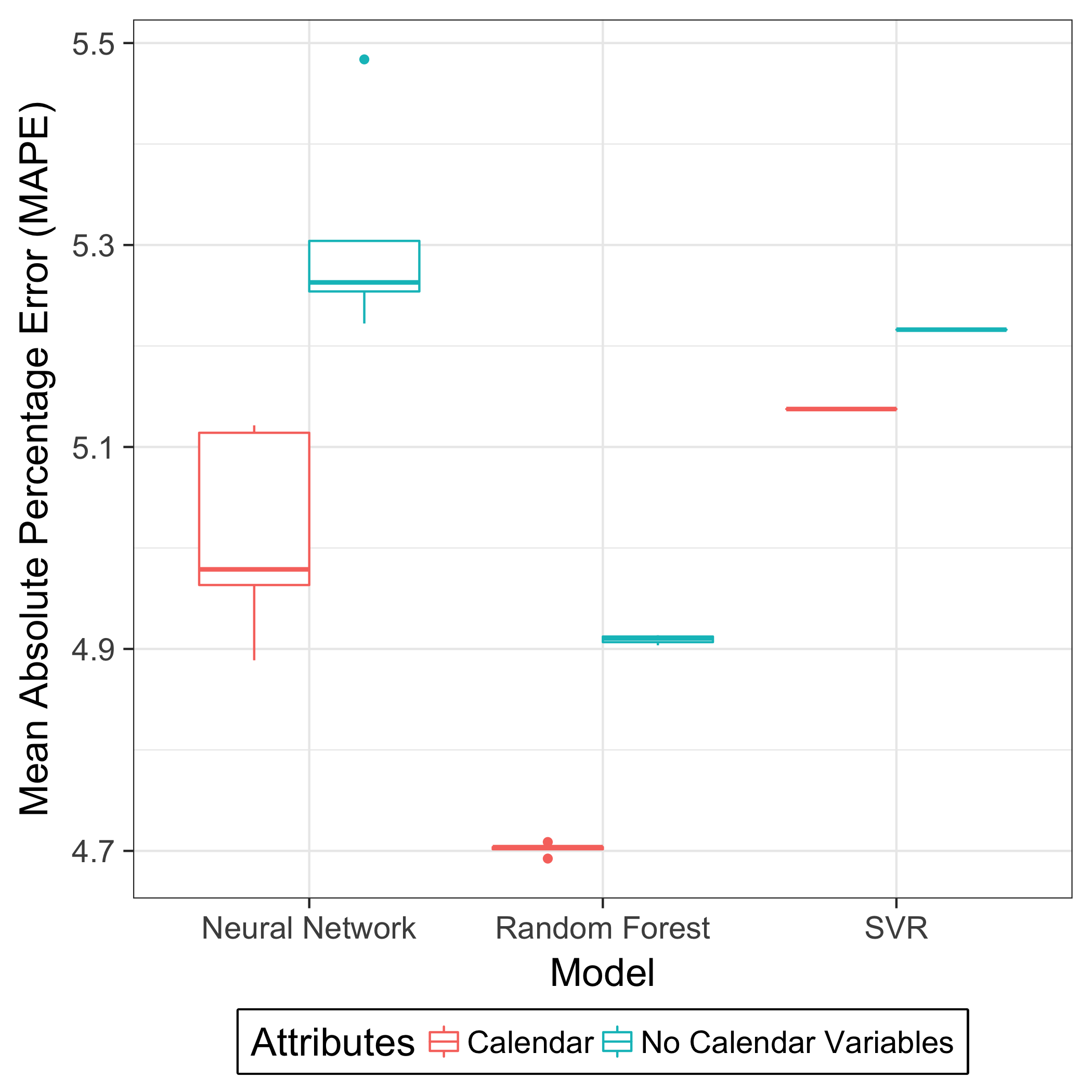

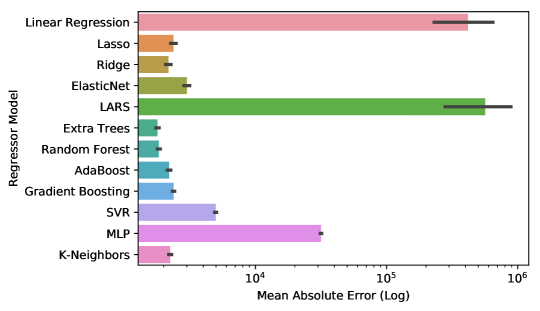

This paper expands on the work carried out in Kell2018a. However, instead of predicting 30 minutes ahead, electricity demand over the next day is predicted, over a 24-hour horizon. To improve results, online learning is used, which is able to update the parameters of the models as new data points become available. The results are significantly improved using this method. Finally, the errors of these predictions are taken and the long-term effects of these are shown on the electricity market using the ElecSim models, both in terms of generator utilisation and long-term investment decisions.

-

Kell2020a

Kell, A. J. M., McGough, A. S., & Forshaw, M. (2020). Optimising carbon tax for decentralised electricity markets using an agent-based model. The Eleventh ACM International Conference on Future Energy Systems (e-Energy’20), 454–460.

In this paper, different carbon tax strategies are trialled using a multi-objective genetic algorithm. With the aim to minimise both the electricity price and carbon emissions. It is found that it is possible to achieve both of these goals through different carbon tax strategies. This work builds on Kell2019 by using a similar multi-objective genetic algorithm optimisation approach.

-

Kell2020d

Kell, A. J. M., Forshaw, M., & McGough, A. S. (2020). Exploring market power using deep reinforcement learning for intelligent bidding strategies. The 4th IEEE International Workshop on Big Data for Financial News and Data at 2020 IEEE International Conference on Big Data (IEEE BigData 2020).

This paper uses reinforcement learning to control the bidding behaviour of a single GenCo, or a group of colluding GenCos in the day-ahead market. It is found that if the other agents bid using their short run marginal costs, the GenCos which use the reinforcement learning algorithm are able to artificially inflate the market price using their market power. The work in this paper forms the work done in Chapter 6.

Papers not forming part of this thesis

-

Kell2019

Kell, A. J. M., Forshaw, M., & McGough, A. S., (2019). Optimising energy and overhead for large parameter space simulations. 2019 10th International Green and Sustainable Computing Conference, IGSC 2019.

In this work, a multi-objective genetic algorithm is used to reduce both overhead and energy consumption of a cluster of computers at Newcastle University. This is achieved by varying different parameters of a reinforcement learning algorithm. The methods used in this paper influence much of the work presented in Chapters 3, 4 and 6.

-

KellA.J.M.McGoughA.S.ForshawM.MercureJ.F.Salas2020

Kell, A. J. M., McGough A. S., Forshaw, M., Mercure, J. F., Salas, P. (2020). Deep Reinforcement Learning to Minimize Long-Term Carbon Emissions and Cost in the Investment of Electricity Generation. 34th NeurIPS 2020, Workshop on Tackling Climate Change with Machine Learning.

This paper modifies the FTT:Power model by using reinforcement learning as the electricity generator investment algorithm Mercure2012. FTT:Power is a global power model which uses logistic differential equations to simulate competition between different electricity generating technologies. These logistic differential equations are replaced with the deep deterministic policy gradient reinforcement learning method. It is found find that, if the goal is to reduce both carbon emissions and electricity price, a transition to renewables occurs.

Chapter 2 Background and Literature Review

Summary

This chapter provides an overview of the relevant material which motivates and underpins the work carried out in this thesis and places the work in context with a literature review. Section 2.1.1, introduces electricity markets and how they are regulated. In Section 2.1.2, an introduction into how electricity markets are modelled is presented. We provide an introduction in Section 2.1.3 to simulation and in Section 2.1.4 to machine learning. Finally, we conclude this chapter in Section 2.1.

We also review the literature by giving an introduction to the relevant energy models and provide a systematic review on how AI has been applied to agent-based models. Section 2.2.1 gives an introduction to the field of energy modelling. In Section 2.2.2 we present different types of energy models, as well as a detailed view on agent-based models, the focus of this thesis. We present a table in Section 2.2.4, which displays a high-level overview of the major models in the literature. Section 2.2.9 details a systematic review on how AI has been utilised with agent-based models in the electricity sector. We conclude this chapter in Section 2.2.18, where we discuss the limitations and benefits of modelling types and how AI can be integrated into agent-based models in the future.

2.1 Background and Introduction

2.1.1 Electricity Markets

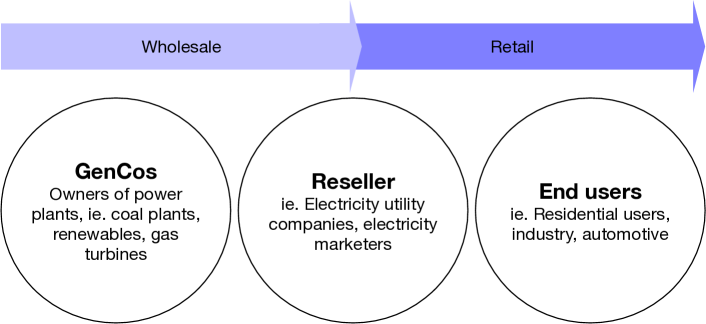

Electricity markets are complex. One of the principal reasons for this is the expense and difficulty of storing electricity. This is because electricity must be consumed the moment it is generated. Additionally, as electricity travels over high voltage transmission lines, electricity doesn’t always follow simple or unique paths, especially when the transmission lines become congested. In addition there is power loss during transmission. Finally, electricity markets require technical overseers to ensure that the entire transmission system operates safely and reliably.

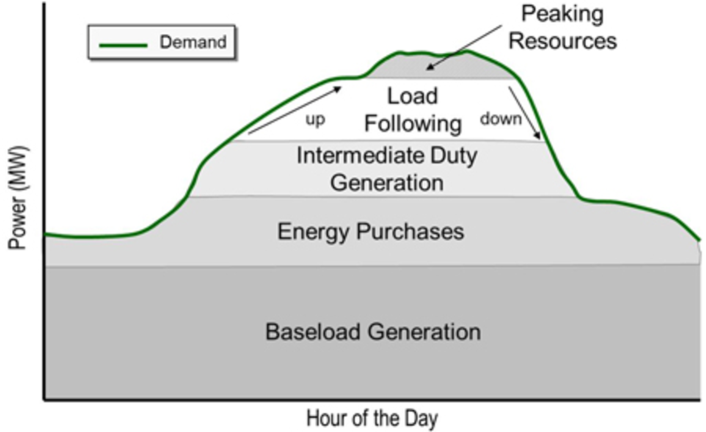

Another aspect to consider is the fact that electricity is homogeneous. A single unit of electricity produced by a wind turbine is equivalent to a unit of electricity produced by a gas turbine. However, the functioning of different electricity producers, or generators, are not homogenous. Coal, gas and oil power plants can be dispatched at the will of a human operator. Their ramp rates are well understood, as is the amount of fuel that is available. Where the ramp rate is defined as the increase or decrease in output per minute and is usually expressed as megawatts per minute (MW/min). Intermittent Renewable Energy Sources (IRES), however, such as solar, wind and tidal are dependent on the supply of solar irradiance, wind speed and the tide at any moment. Whilst these can be predicted, predictions are often wrong, and perfect knowledge is impossible. Therefore, at times where there is too much supply from Intermittent Renewable Energy Sources (IRES) generators must be curtailed if all regulator generators are already offline or can not be shut down or ramped down. In the opposite case, where there is too little supply from IRES, supply must be made up from other sources, such as coal, gas or hydro.

The environmental impact from different electricity generators differs significantly. Whilst gas and coal can be dispatched at a time convenient to the grid operators, they emit \ceCO2 along with other toxic substances. In this context, dispatched refers to electricity that can be generated on demand at the request of power grid operators, according to market needs. Wind and solar do not dispatch such gases and substances, and therefore can not be controlled as easily. Storage technologies can be used to fill these gaps; however, large-scale storage depends on large pumped reservoirs that can move water to a higher position when demand for electricity is low, and supply is high. Not all geographies have access to such reservoirs, and therefore would rely on battery technology made from chemicals. However, reaching such high storage capabilities are expensive and are yet to have been done in the real world cole2019cost. Another option is converting electricity to hydrogen. However, this technology is also expensive and uncompetitive with traditional fossil fuels such as coal, gas and oil. Currently, peaker plant are used to fill these gaps. Peaker plants are plants which are used in times of high demand and low supply. However, these plants are expensive to operate, highly polluting and use fossil fuels lin2011energy. It is expected that these peaker plant s will be used increasingly due to the intermittent nature of renewable technologies lin2011energy.

The electricity grid must match supply with demand at all times. Failure to do so results in an imbalance of supply and demand, and affects the frequency of the electricity network. Large differences between supply and demand can lead to blackouts or oversupply and may damage equipment. A number of different markets exist to regulate the supply and demand, running from within seconds, to days-ahead and bilateral contracts which settle electricity for years ahead conejo2010electricity.

There are a number of different market mechanisms that can be used to balance the supply and demand of electricity. Largely these can be divided between ancillary services and wholesale transactions. Wholesale transactions can occur as bilateral trades or on a day-ahead market conejo2010electricity. Bilateral trades can occur between two electricity suppliers and those that have an electricity demand conejo2010electricity. In this case, suppliers and customers create contracts for electricity in advance. Typically, these agents must let the market operator know of their trades conejo2010electricity. In a day-ahead market, the system price is, in principle, determined by matching offers from generators to bids from consumers at each node to develop a supply and demand equilibrium price conejo2010electricity.

Ancillary markets, on the other hand, provide a method to facilitate and support the continuous flow of electricity so that supply continually meets demand conejo2010electricity. These include markets to regulate power and voltage control as well as frequency control. These markets make use of increasing supply or reducing demand at the times where this is required conejo2010electricity.

There exist many markets to better regulate the supply and demand at different time intervals. For example the intra-day market, capacity market. These markets ensure that electricity supply continues to meet demand as more intermittent renewable energy comes online. The intra-day market is able to dynamically meet fluctuations in supply and demand which were not matched using the day-ahead and bilateral markets. Whereas, the capacity market pays participants a per MW rate for the capacity they offer to the market.

Other mechanisms exist, such as the contracts for difference and the carbon price floor to transform the UK’s electricity system. Contracts for difference pays a fixed price to generators irrespective of the market price. The carbon price floor places a minimum tax on carbon.

An imbalanced system can also be resolved through the means of demand response (the reduction of electricity demand), interconnection with other countries, and through storage for example with vehicle to grid or by other means. In this thesis, however, we focus primarily on the day-ahead market and carbon price floor due to these markets having the largest impact on the macro-scale of the electricity market.

2.1.2 Introduction to Electricity Market Modelling

Energy models are useful tools for insight into the functioning of electricity markets. For example, modellers and analysts can develop an intuition of how such a system works, and through modelling, they can challenge untested hypothesise. The argument that these models are used for insight and not just informational data is as old as the models themselves Huntington1982; Pfenninger2014, and is true for models in many different disciplines Geoffrion1976. We argue that energy models should not be taken as truth, because as previously mentioned, no model can perfectly model the real world. However, the intuition that can be learned can prove to be a valuable resource.

Energy modelling and energy policy as a distinct field began after the oil crisis in the 1970s, where long-term planning was deemed as important in the electricity field Craig2002. Models which make use of optimisation techniques have been used since these times for diverse applications, from the global energy market to small off-grid systems. Optimisation techniques are models in which a central actor invests in the cost-optimal (cheapest) energy system over a multi-year time period.

The utilisation of energy models has lately been redirected to ensuring that there exists a security of supply, the resilience of the energy system, affordability and that there is a transition to a low-carbon supply. These models can also be used to investigate the impact that different technologies have on investments made in the future.

However, since the traditional models have been established, various changes in the energy industry have occurred. Originally, electricity systems were built upon large-scale centralised electricity production based on fossil fuels foxon2010developing. Since then there has been a transition towards decentralised, distributed, intermittent renewable energy sources, such as solar and wind IEA2015a. In addition, there has been an advent in flexible demand driven by new technologies such as smart meters avancini2019energy. This paradigm shift requires models which can work with higher temporal and spatial detail to account for fluctuations in demand, supply and distributed electricity generators.

Modelling electricity markets is a complex task. There exist many variables, actors, services and behaviours within electricity markets which make it impossible to perfectly model the system. Often simplifications must be made, where models are designed for a specific task Pfenninger2014. Large established models exist which model every possible detail; however, with the increase in temporal and spatial resolution required, the computational tractability of these models can be negatively impacted. Many of the large models used today have existed for a long time, before the advent of the Internet Pfenninger2014. Therefore, these models and modellers risk becoming outdated, as their models are not updated.

Energy and electricity models generally follow two approaches: bottom-up or a top-down approach Ringkjob2018. Bottom-up models are often referred to as the engineering approach and are based on detailed technological representations of the energy system. Top-down models, on the other hand, follow an economic approach and consider the long-term changes and macroeconomic relationships Mai2013. It is possible to combine both the technological properties and long-term changes by creating a hybrid approach Fortes2014.

2.1.3 Introduction to Simulation

A computer simulation is a virtual model of a real-world system which is programmed into computer software. These models can be used to study how such a system works. One is able to change parameters in the system and make predictions as to how a system might behave. These simulations are particularly beneficial when the system one is analysing is difficult to experiment with fishman1978principles. For example, the system exhibits a high financial costs of experimentation, or negative consequences may have large impacts mitrani1982simulation. Additionally, for systems that operate on long timescales, such as energy markets, one may not have the ability to repeat experiments in a controlled environment.

Digital twins are a particular instance of a simulation. Digital twins have often been instantiated to a particular system, as opposed to a general system. For example, a digital twin can be made of the UK electricity market, whilst a simulation can be generalised to any decentralised market. By having a digital twin of a particular system, we are able to remove the risks associated with interacting with a system and iterate many experiments within a short time to find an optimal set of parameters. In addition, a digital twin is able to behave more like the system in question.

Whilst simulations must be built with expert knowledge, and through a thorough understanding of the system that one would like to model, machine learning is a data-driven approach. Data-driven approaches need not require an understanding of the system in which they are trying to model. Rather, they infer properties of the system entirely from data. These models are desirable in cases where a system is too complicated to have a full understanding of how the system works. These models have been shown to generate accurate results in many different disciplines Covington2016; WarrenLiao2005; Wiens2009.

Simulations can be used to learn how a system may evolve, find optimal input parameters, learn the key features of a system and to extract data from the system. Another key use of simulations is to interact with a physical system. This list is non-exhaustive, as there exist many different uses for simulations.

2.1.4 Introduction to Machine Learning

Machine learning (ML) is the study of computer algorithms that improve automatically with the use of data. By using training data, these algorithms are trained to make predictions or decisions without being explicitly programmed to do so.

Machine learning methods can be split into three different categories: (1) supervised learning, (2) unsupervised learning and (3) reinforcement learning. Each of these methods can be used in the following cases:

-

1.

Supervised learning is used where the data used has labelled data. Labelled data is where the true value that one is trying to predict is available in the data.

-

2.

Unsupervised learning is where there are no labels associated with the data. The model must, therefore infer from distinct clusters in the data where the divides in the values may lie.

-

3.

Reinforcement learning is concerned with how software agents must take actions in an environment in order to maximise a cumulative reward.

In addition to the aforementioned machine learning methods, there exists an additional paradigm: optimisation methods. These methods explore a mathematical or software function to find a minimum or maximum value of an objective. These can be used to minimise an expected error, minimise total cost or maximise total return from a system, for example.

In the following sections we explore an overview of the different machine learning techniques that are applicable to the problems addressed in this thesis:

Supervised Learning

Supervised learning uses training data, which contains both the inputs and desired outputs, to predict the output associated with new inputs. A functioning supervised learning model, will therefore be able to correctly determine the output for inputs that were not part of the original training data. Supervised learning can be used for both regression and classification. Regression is where a continuous output is returned, whereas classification is where a discrete value is returned.

The model widely used supervised learning algorithms are:

-

•

Support vector machines

-

•

Linear regression

-

•

Logistic regression

-

•

Decision trees

-

•

Neural networks

Support vector machines, neural networks and decision trees can be used for both regression and classification, whereas linear regression and logistic regression are used for regression and classification respectively. Therefore, decisions must be made when choosing the appropriate algorithm for the respective task.

Once a decision has been made with respect to whether classification or regression is required, it is often the case that a number of different algorithms are trialled to see which yield the best results.

However, these algorithms have different characteristics which should be taken into account. For instance, neural networks and support vector machines are able to learn complex patterns in data to a higher level than linear regression and so are often chosen for more complex datasets and problems.

Secondly decision trees are interpretable, in that, one is able to graphically visualise why a specific output has been returned by the model through a series of decision criteria. This is a feature which is lacking in neural networks, which can often yield good results, but remain a black-box.

Linear and logistic regression can be used to understand the most important variables to influence the output variables. So whilst, they are unable to model complex problems as well as neural networks or support vector machines, they can be used for better model interpretation.

In this thesis, we use a variety of different supervised learning techniques for specific problems, as previously discussed.

Unsupervised Learning

As previously mentioned, unsupervised learning learns patterns from unlabelled data. Unsupervised learning can therefore exhibit self-organisation that can capture patterns in data that were previously unknown.

Some of the most common algorithms include:

-

•

Hierarchical clustering

-

•

k-means clustering

-

•

Self-organizing maps

Hierarchical clustering, similar to decision trees, can be graphically visualised to observe the decisions made by the algorithm. This can be useful, particularly when it is required to see which groups are more similar to one another, and different parent groupings.

k-means partitions observations into k clusters, in which each observation belongs to each cluster. k-means provides a cluster centre, which serves as a prototype of the cluster, and provides useful information about the mean of the cluster.

A self-organising map produces a low-dimensional representation of higher dimensional data while preserving the topological structure of the data. This can make high dimension data easier to visualise. Self-organising maps are a type of neural network.

Reinforcement Learning

Reinforcement learning (RL) is an algorithm which allows intelligent agents to take actions in an environment in order to maximise a cumulative reward. Reinforcement learning does not require labelled input/output data. The basis of RL is to find a balance between exploration and exploitation.

A large amount of research has been dedicated in recent times to improving the performance of reinforcement learning algorithms Arulkumaran2017; Hunt2016a. Various different methodologies have been tried and tested, from the use of neural networks in deep reinforcement learning to updating a lookup table.

Some of the algorithms used in the literature are:

-

•

Q-learning

-

•

Deep Deterministic Policy Gradient (DDPG)

-

•

Deep Q Network (DQN)

A major difference between the algorithms presented are the action and state spaces. For example, Q-learning requires both a discrete action and state space. Whereas, DDPG and DQN operate with a continuous action and state space. Q-learning updates a look-up table to map observations to actions, whereas DDPG and DQN use deep neural networks to learn a policy.

The type of algorithm chosen can therefore be dependent on the different features required. Due to Q-learning working with a look-up table, they are more interpretable than DDPG and DQNs, as one is able to simply look at the lookup table to see which action is taken with different observations. However, due to the discrete nature of the action and state space, this methodology is less useful if one would like to have more precise actions.

It is possible to discretise the action and state space of Q-learning, but the speed and efficiency of the algorithm is greatly reduced with increasing discretised steps. Deep reinforcement learning techniques, similar to neural networks, are able to learn complex patterns within data, which can lead to better results. Care must therefore be taken when making decisions on the type of algorithm used.

Conclusion

In this section, we have introduced key concepts that have been used as part of this thesis: electricity markets and their modelling, simulation and digital twins, machine learning methods such as supervised learning and reinforcement learning as well as optimisation techniques. All of the mentioned methods have been used in this thesis for the purpose of increasing our understanding of electricity markets over both a long, and short time periods.

We have motivated the need for novel approaches to be used when understanding and modelling energy systems due to the fundamental changes that have occurred since the 1970s. From a system with a centralised actor and power stations which run on fossil fuels to one built on decentralised generation capacity and many heterogeneous actors.

Additionally, we have discussed the complexity of modelling a system such as electricity markets. However, the insight that can be gained is invaluable and can provide further understanding to those who need to make decisions under large uncertainties. The ramifications of such decisions go far beyond the energy sector, and therefore any help that can be given to decision-makers is of utmost importance. Further details presented in this chapter will be presented in future chapters.

2.2 Literature Review

2.2.1 Energy Modelling

Energy modelling is a broad field, so there have been multiple reviews that attempt to separate these models into different classifications Ringkjob2018; Savvidis2019a; Sensfub2007. Examples of the metrics for classification are the mathematical underpinning, the underlying methodology, analytical approach or data requirements. This thesis focuses specifically on agent-based models and AI applied to electricity markets and not the wider literature of energy models. We, therefore, refer the reader to the papers presented in Table 2.1 for a more thorough investigation of this broader field.

| Publication | Focus |

|---|---|

| The gap between energy policy challenges and model capabilities Savvidis2019a | Assesses the ability of energy systems models to answer major energy policy questions. |

| Agent-based simulation of electricity markets: a literature review Sensfub2007 | An overview of the work applying agent-based models to the analysis of electricity markets. |

| A review of modelling tools for energy and electricity systems with large shares of variable renewables Ringkjob2018 | An aid for modellers to choose an appropriate model which can cater for large shares of variable renewables. |

| Energy systems modeling for twenty-first century energy challenges Pfenninger2014 | The issues of using existing models for twenty-first century challenges in energy. |

| A review of energy systems models in the UK: Prevalent usage and categorisation Hall2016 | Provide a classification schema for energy models. |

| A survey of stochastic modelling approaches for liberalised electricity markets Most2010 | Overview and classification of stochastic models dealing with price risks in electricity markets. |

2.2.2 Model types

Large, detailed bottom-up optimisation models have long been used for energy system modelling. These optimisation models are typically based upon a detailed description of the technical components of the energy system.

The ultimate goal of optimisation models is to optimise a given quantity, for example, the minimisation of cost or the maximisation of welfare. In this context, welfare can be designed as the material and physical well-being of people Keles2017. However, these models do not state how likely each of these scenarios is to develop.

There are limitations to optimisation based models: traditional centralised optimisation models are not designed to describe a system that is out of equilibrium. Optimisation models assume perfect foresight and risk-neutral investments with no regulatory uncertainty Pfenninger2014. The core dynamics which emerge from equilibrium remain a black-box. For example, the model assumes a target will be reached and does not provide information when this is not the case. Reasons for this could be investment cycles which move the model away from equilibrium Chappin2017.

Equilibrium models take an economic approach. They model the energy sector as a part of the whole economy and study how it relates to the rest of the economy Ringkjob2018. POLES Soria2012 is a global detailed econometric model developed by the European Commission. E3MG is an econometric simulation developed by Cambridge Econometrics Dagoumas2010. MARKAL-MACRO is a hybrid model. Where MARKAL is bottom-up, and MACRO is top-down.

Simulation models simulate an energy system based upon specified equations, characteristics and rules. These are often bottom-up models, and are designed with a high level of technological description Ringkjob2018. Agent-based models are a specific case of simulation models, where actors are modelled explicitly as agents with heterogeneous strategies and behaviours.

Additionally, there exist a set of power system models which can help with decisions such as investment planning or decisions about generator dispatch. An example of a large power systems model is WASP jenkins1974wein.

2.2.3 Agent-based models

In this subsection, we outline current agent-based models available and motivate why the model, ElecSim, is required. Part of the literature review outlined here has been previously published in Kell.

Electricity market liberalisation in many western democracies has changed the framework conditions Praca2003. Centralised, monopolistic, decision making entities have given way to multiple heterogeneous agents acting for their own best interest Most2010. Policy options must, therefore, be used to encourage changes to attain a desired outcome. It has been proposed that these complex agents are modelled using agent-based models (ABMs) due to their non-deterministic nature Kell.

A number of ABM tools have emerged over the years to model electricity markets: SEPIA Harp2000, EMCAS Conzelmann, NEMSIM Batten2006, AMES Sun2007, GAPEX Cincotti2013, PowerACE Rothengatter2007, EMLab Chappin2017 and MACSEM Praca2003. Table 2.2 shows, however, that these do not suit the needs of an open source, long-term market model.

Table 2.2 contains five columns: tool name, whether the tool is open source or not, whether they model long-term investment in electricity infrastructure and the markets they model and we determine how the stochasticity of real life is modelled.

We chose these columns to compare the models due to their importance in the application of understanding long-term electricity market scenarios. Firstly, an open-source tool enables independent users to verify the code developed for these models. It is important that this can be achieved, so that the outputs are not obfuscated by a closed system. Long-term investment allows for the endogenous propagation of an electricity market.

We believe that a model which models both day-ahead and futures markets is of importance. This is because these markets are interlinked and correlated. If we did not take into account the day-ahead market, we would not be able to determine the economic success of the GenCos, where profitable GenCos are able to invest further, and those which are less successful invest less. The futures market enables GenCos to invest for the long-term, which determines the trajectory of a scenario. Other aspects, such as intra-day markets are important for the short-term, but less important for the long-term.

In addition, the ability to model stochasticity is of importance, due to the non-deterministic nature of the real-world. For instance, the price paid by GenCos is non-deterministic and can vary at any point in time between GenCos. In reality, a large number of features are stochastic, but we discuss those that, we believe, are most pertinent to long-term electricity markets.

There have been several recent studies using ABMs which focus on electricity markets. However, they often utilise ad-hoc tools designed for a particular application hadar2019; Kunzel2018; Saxena2019. In our work, we develop the model ElecSim, which has been built for re-use and reproducibility. The survey Weidlich2008 cites that many of these tools do not release source code or parameters, which is a problem that ElecSim seeks to address by being open source and releasing parameters.

SEPIA Harp2000 is a discrete event ABM. SEPIA models plants as being always on. SEPIA does not model a spot market, instead focusing on bilateral contracts. As opposed to this, ElecSim has been designed with a merit-order, spot market in mind. As shown in Table 2.2, SEPIA does not include a long-term investment mechanism.

EMCAS Conzelmann is a closed source ABM. EMCAS investigates the interactions between physical infrastructures and economic behaviour of agents. However, ElecSim focuses on the dynamics of the market, and provides a simplified, transparent model of market operation, whilst maintaining the robustness of results.

NEMSIM Grozev2005 is an ABM that represents Australia’s National Electricity Market (NEM). Participants are able to grow and change over time using learning algorithms. NEMSIM is non-generalisable to other electricity markets, unlike ElecSim.

AMES Sun2007 is an ABM specific to the US Wholesale Power Market Platform. GAPEX Cincotti2013 is an ABM framework for modelling and simulating power exchanges. However, neither of these model the long-term dynamics for which ElecSim is designed.

PowerACE Rothengatter2007 is a closed source ABM of electricity markets that integrates short-term daily electricity trading and long-term investment decisions. PowerACE models the spot market, forward market and a carbon market. Similarly to ElecSim, PowerACE initialises GenCos with each of their power plants. However, as shown in Table 2.2, unlike ElecSim, PowerACE does not consider stochasticity of price risks in electricity markets Most2010.

EMLab Chappin2017 is an open-source ABM toolkit for the electricity market. Like PowerACE, EMLab models an endogenous carbon market; however, they both differ from ElecSim by not taking into account stochasticity in outages and operating costs.

MACSEM Praca2003 has been used to probe the effects of market rules and conditions by testing different bidding strategies. MACSEM does not model long term investments or stochastic inputs.

As shown in Table 2.2, none of the tools fill each of the characteristics that we require. We therefore propose ElecSim to contribute an open-source, long-term, stochastic investment model. For this work, we decided that a novel agent-based simulation was required to fill all of these categories, as the use-cases developed for our work is specific towards the requirements of our model. Whilst it is true that no other model meets each of our defined characteristics, however, it is not the case that these models are not useful. In fact, they are useful for their own specific purposes.

Tool name Open Source Long-Term Investment Market Stochastic Inputs SEPIA Harp2000 ✓ ✓ Demand EMCAS Conzelmann ✓ ✓ Outages NEMSIM Batten2006 ? ✓ ✓ AMES Sun2007 ✓ Day-ahead GAPEX Cincotti2013 ? Day-ahead PowerACE Rothengatter2007 ✓ ✓ Outages Demand EMLab Chappin2017 ✓ ✓ Futures Fuel prices MACSEM Praca2003 ? ✓ ElecSim Kell ✓ ✓ Futures ✓

2.2.4 Energy models classification

In this section, we present a high-level overview of the various models that are in existence in a table format: Table 2.3. These models fall into various categories. However, for simplification we classify these as either agent-based models (ABM) or non-ABM. The time horizon details what the main purpose of the model is, is it a long-term model. Finally, the time-step column details the time resolution granularity.

| Model | Underlying methodology | Time horizon | Time step |

|---|---|---|---|

| E3MG | Non-ABM | 2100 | Annually until 2030 and then each decade until 2100 |

| LEAP | Non-ABM | Medium and long-term | Annual |

| MARKAL | Non-ABM | Medium and long-term | User-defined |

| MARKAL-MACRO | Non-ABM | Medium and long-term | User-defined |

| NEMS | Hybrid | Medium (25 years) | Yearly |

| OSeMOSYS | Non-ABM | Medium and long-term (2010-2050) | 5-year |

| PRIMES | ABM | Medium to long-term | Yearly |

| POLES | Non-ABM | Long-term (up to 2050) | Yearly |

| TIMES | Non-ABM | Medium and long-term | User-chosen time-slices |

| WASP | Non-ABM | Medium and long-term | 12 load duration curves per year |

| MESSAGE | Non-ABM | Short, medium and long-term | User-defined (Multiple of number of years) |

| PLEXOS | Non-ABM | Short-term | 1-minute |

| ELMOD | Non-ABM | Short-term | Hourly |

| ElecSim | ABM | Short, medium and long-term | Hourly |

2.2.5 Validation

This subsection covers the difficulties inherent in validating energy models and the approaches taken in the literature to validate these models.

2.2.6 Limits of Validating Energy Models

Beckman et al. state that questions frequently arise as to how much faith one can put in energy model results. This is due to the fact that the performance of these models as a whole are rarely checked against historical outcomes Beckman2011.

Under the definition by Hodges et al. Hodges long-range energy forecasts are not validatable Craig2002. Under this definition, validatable models must be observable, exhibit constancy of structure in time, exhibit constancy across variations in conditions not specified in the model and it must be possible to collect ample data Hodges.

Whilst it is possible to collect data for energy models, the data covering important characteristics of energy markets are not always measured. Furthermore, the behaviour of the human population and innovation are neither constant nor entirely predictable. This leads to the fact that static models cannot keep pace with long-term global evolution. Assumptions made by the modeller may be challenged in the form of unpredictable events, such as the oil shock of 1973 Craig2002.

This, however, does not mean that energy-modelling is not useful for providing advice in the present. A model may fail at predicting the long-term future because it has forecast an undesirable event, which led to a pre-emptive change in human behaviour—thus avoiding the original scenario that was predicted. This could, therefore, be viewed as a success of the model.

Schurr et al. argued against predicting too far ahead in energy modelling due to the uncertainties involved Schurr_1961. However, they specify that long-term energy forecasting is useful to provide basic information on energy consumption and availability, which is helpful in public debate and in guiding policymakers.

Ascher concurs with this view and states that the most significant factor in model accuracy is the time horizon of the forecast; the more distant the forecast target, the less accurate the model. This can be due to unforeseen changes in society as a whole gillespie_1979.

It is for these reasons that we focus on a shorter-term (5-year) horizon window when calibrating our model for validation. This enables us to have increased confidence that the dynamics of the model work without external shocks and can provide descriptive advice to stakeholders. However, it must be noted that the UK electricity market exhibited a fundamental transition from natural gas to coal electricity generation during this period, meaning that a simple data-driven modelling approach would not work.

In addition to this short-term cross-validation, we compare our long-term projections to those of BEIS from 2018 to 2035. It is possible that our projections and those of BEIS could be wrong. However, this allows us to thoroughly test a particular scenario with different modelling approaches, and allow for the possibility to identify potential flaws in the models.

2.2.7 Validation Examples

In this Section, we explore a variety of approaches used in the literature for energy model validation.

The model OSeMOSYS Howells2011 is validated against the similar model MARKAL/TIMES through the use of a case study named UTOPIA. UTOPIA is a simple test energy system bundled with ANSWER Hunter2013, a graphical user interface packaged with the MARKAL model generator Noble2004. Hunter et al. use the same case study to validate their model Temoa Hunter2013. In these cases, MARKAL/TIMES is seen as the "gold standard". In this work, however, we argue that the ultimate gold standard should be real-world observations, as opposed to a hypothetical scenario.

The model PowerACE demonstrates that realistic prices are achieved by their modelling approach. However, they do not indicate success in modelling GenCo investment over a prolonged time period Ringler2012.

Barazza et al. validate their model, BRAIN-Energy, by comparing their results with a few years of historical data; however, they do not compare the simulated and observed electricity mix Barazza2020. This reduces the confidence that one may have in the results of the produced electricity mix.

Work by Koomey et al. expresses the importance of conducting retrospective studies to help improve models Koomey2003. In this case, a model can be rerun using historical data in order to determine how much of the error in the original forecast resulted from structural problems in the model itself, or how much of the error was due to incorrect specification of the fundamental drivers of the forecast Koomey2003.

A retrospective study published in 2002 by Craig et al. focused on the ability of forecasters to accurately predict electricity demand from the 1970s Craig2002. They found that actual energy usage in 2000 was at the very lowest end of the forecasts, with only a single exception. They found that these forecasts underestimated unmodelled shocks such as the oil crises which led to an increase in energy efficiency.

Hoffman et al. also developed a retrospective validation of a predecessor of the current MARKAL/TIMES model, named Reference Energy System Hoffman_1973, and the Brookhaven Energy System Optimization Model ERDA_48. These were studies applied in the 70s and 80s to develop projections to the year 2000. This study found that the models had the ability to be descriptive but were not entirely accurate in terms of predictive ability. They found that emergent behaviours in response to policy had a strong impact on forecasting accuracy. The study concluded that forecasts must be expressed in highly conditioned terms Hoffman2011.

2.2.8 Modelling Conclusion

In this section, we have introduced various electricity market models and the categories that they fall into. However, it can prove to be challenging to place models within a clear boundary, as many models fall within a continuous spectrum. We introduced the concept that traditional models may not have the ability to detail every single component of an electricity market without losing tractability.

The need for a new paradigm in which decentralised agents act within an environment was discussed. So was the need for a model with high temporal resolution to more accurately model the intermittency of renewable energy. Traditional optimisation models work in a normative, prescriptive way. However, it is not possible to describe a system which is out of equilibrium. Another limitation of the traditional optimisation models is that they assume perfect foresight, with risk-neutral investments and no regulatory uncertainty. It assumes that certain scenarios are possible, but does not highlight the way a target may not be reached.

It is for these reasons that in this thesis, we focus on agent-based models, which move away from the traditional optimisation approach, and allow for a more dynamic solution without rigid mathematical expressions.

Additionally, we found that there was a gap in the literature for an open-source agent-based model that could model long-term investments, was generalisable to many countries and modelled stochastic inputs. It is for this reason that we developed the model ElecSim.

2.2.9 Machine Learning and Agent-Based Models

In this section, we review the literature that investigates how artificial intelligence and machine learning can be integrated into agent-based models for the electricity sector. To select the related articles to review, we conduct a systematic analysis of relevant research in the field. We limited our search to literature published in the five most recent years (2016-2021). As a result of this, we provide a comprehensive status of the applications of ML and AI in agent-based models for the electricity sector. For this purpose we used the Elsevier Scopus database. To find the articles, we used the following set of search terms to select our articles:

-

1.

Machine Learning, Artificial Intelligence, Deep Learning, Neural Networks, Decision Tree, Support Vector Machine, Clustering, Bayesian Networks, Reinforcement Learning, Genetic Algorithm, Online Learning, Linear regression.

-

2.

Agent-based modelling.

-

3.

Electricity.

We searched using each of the keywords in each of the bullet points. For instance, the first keyword search was: Machine Learning, Agent-Based Modelling and Electricity. The second was: Artificial Intelligence, Agent-based modelling and Electricity. We selected these search terms to focus this review on agent-based models applied to the electricity sector and machine learning, which is the focus of this thesis.

These search terms resulted in 149 research articles. However, not all of these were related to our research focus. For instance, a number of electric vehicle, buildings and biological papers were returned. After a further manual review, these 149 papers were reduced to 55 papers which were specifically related to agent-based modelling, electricity, artificial intelligence and machine learning.

Figure 2.1 shows the amount of articles published each year between 2016 and the present date. Whilst the number of articles published in this field has increased per year since 2018 to 2020, the number of papers published in 2017 was lower when compared to the other years, with a large number published in 2016. We reviewed these 55 papers systematically in the following sections.

2.2.10 Market Type

In this literature review, we make three different market type distinctions: international/national energy market, local energy market and a microgrid. The international/national energy market typically considers a country, multiple countries or the world. A local energy market is a smaller region than the international/national energy market, for instance, a city or region. Whereas a microgrid serves a discrete geographic footprint, such as a university campus, business centre or neighbourhood. Whilst there is some cross-over between a local energy market and microgrid, a microgrid can be disconnected from the traditional grid and operate autonomously.

Tables 2.4, 2.5 and 2.6, 2.7 and 2.8 categorise each of the market types respectively. The papers have been displayed in chronological order and categorise the market type, machine learning (ML) type used, the application in which it was used and the algorithm used. These different criteria are explored in the following subsections.

2.2.11 Machine Learning Types

Within this work, we have covered five different type of artificial intelligence paradigms. These are: supervised learning, unsupervised learning, reinforcement learning, optimisation and game theory

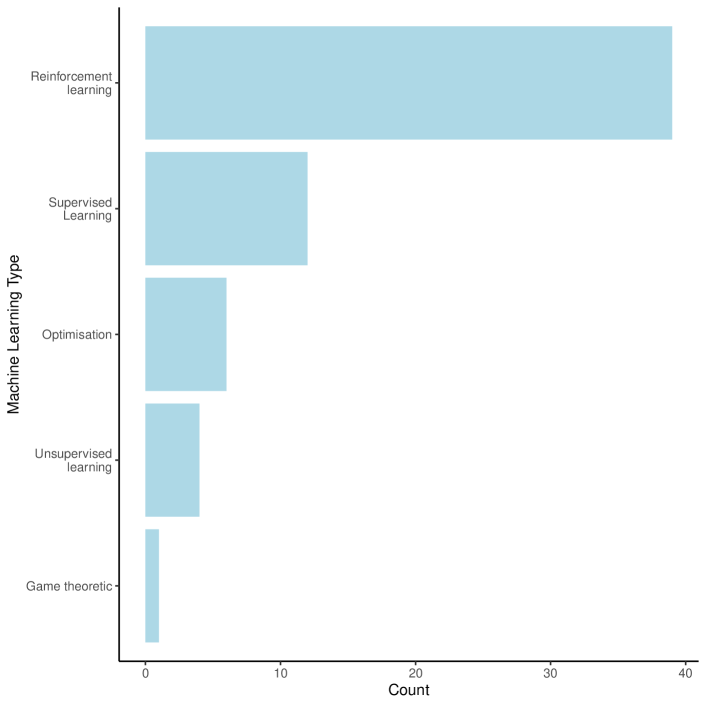

Each of these techniques have been utilised in the papers surveyed. However, a particular focus has been placed on reinforcement learning within the research community. As shown by Figure 2.2, 37 out of the 55 papers used a reinforcement learning algorithm. This greatly outweighs the other machine learning types. The second most used machine learning type was supervised learning, used by eight papers. The fact that reinforcement learning has been used so extensively within the agent-based modelling community for electricity highlights the usefulness of this technique within this field.

Within each of the different machine learning types there exist many algorithms. The algorithms used in the papers surveyed are now presented. Within reinforcement learning the deep deterministic policy gradient (DDPG), Deterministic Policy Gradient (DPG) Deep Q-Network (DQN), Deep Q-Learning, Fitted Q-iteration (FQI), long short-term memory neural network (LSTM), Multi-Agent Deep Deterministic Policy Gradient (MADDPG), Markov Decision Process (MDP), Novel WoLF-PHC, Policy Iteration (PI), Probe and Adjust, Q-Learning, Roth-Erev, SARIMAX and Variant Roth-Erev are used.

Within supervised learning, the following algorithms were used: Artificial Neural Network (ANN), Bayesian networks, Classification trees, Extreme Machine Learning, Lasso regression, Linear regression and Support Vector Machine (SVM) were used. Fewer algorithms were used for both unsupervised learning and optimisation. For supervised learning, the following algorithms were used: Bayesian classifier, K-Means Clustering, Naive Bayes classifier. For optimisation the following algorithms were trialled: Bi-level coordination optimisation, Genetic Algorithm, Iterative algorithm and Particle Swarm Optimisation. For the game theory method, a game theoretic algorithm was used.

2.2.12 Applications