Coresets for Time Series Clustering

Abstract

We study the problem of constructing coresets for clustering problems with time series data. This problem has gained importance across many fields including biology, medicine, and economics due to the proliferation of sensors for real-time measurement and rapid drop in storage costs. In particular, we consider the setting where the time series data on entities is generated from a Gaussian mixture model with autocorrelations over clusters in . Our main contribution is an algorithm to construct coresets for the maximum likelihood objective for this mixture model. Our algorithm is efficient, and, under a mild assumption on the covariance matrices of the Gaussians, the size of the coreset is independent of the number of entities and the number of observations for each entity, and depends only polynomially on , and , where is the error parameter. We empirically assess the performance of our coresets with synthetic data.

1 Introduction

A multivariate time series dataset, represented as , where is the number of entities, is the number of time periods corresponding to entity and is the number of features, tracks features of a cross-section of entities longitudinally over time. Such data is also referred to as panel data [8] and has seen rapid growth due to proliferation of sensors, IOT and wearables that facilitate real time measurement of various features associated with entities and the rapid drop in storage costs. Specific examples of time series data include biomedical measurements (e.g., blood pressure and electrocardiogram), epidemiology and diffusion through social networks, weather, consumer search, content browsing and purchase behaviors, mobility through cell phone and GPS locations, stock prices and exchange rates in finance [2].

Computational problems of interest with time series data include pattern discovery [49], regression/prediction [39], forecasting [9], and clustering [47, 31, 2] which arises in applications such as anomaly detection [46]. Though clustering is a central and well-studied problem in unsupervised learning, most standard treatments of clustering tend to be on static data with one observation per entity [35, 11]. Time series clustering introduces a number of additional challenges and is an active area of research, with many types of clustering methods proposed [15]; direct methods on raw data, indirect methods based on features generated from the raw data, and model based clustering where the data are assumed to be generated from a model. For surveys of time series clustering, see [47, 2].

We focus on model-based time series clustering using a likelihood framework that naturally extends clustering with static data [11] to time series data [47], where each multivariate time series is generated by one of different parametrically specified models. For a survey of the importance of this sub-literature and its various real-world applications, see [30]. A prevalent approach is to assume a finite mixture of data generating models, with Gaussian mixture models being a common specification [50, 53]. Roughly, the problem is to partition probabilistically into clusters, grouping those series generated by the same time series model into one cluster. Generically, the model-based -clustering problem can be formulated as: , where is the probability of a time series belonging to cluster and is the likelihood of the data of entity , given that the data is generated from model (with parameters ). Temporal relationships in time series are commonly modeled as autocorrelations (AR)/moving averages (MA) [20, 61] that account for correlations across observations, and hidden Markov models (HMM) where the underlying data generating process is allowed to switch periodically [21, 62]. This paper focuses on the case when the data generation model for each segment is a multivariate Gaussian with autocorrelations. More formally, the generative model for each cluster is from a Gaussian mixture: , where , where captures the mixture of Gaussian distributions from which entity level observations are drawn, and captures the correlation between two successive observations through an AR(1) process [32, 44]. Overall, this model can be represented with cluster level model parameters and cluster probability .

Time series datasets are also much larger than static datasets [47]. For instance, as noted in [42], ECG (electrocardiogram) data requires 1 GB/hour, a typical weblog requires 5 GB/week. Such large sizes lead to high storage costs and also make it necessary to work with a subset of the data to conduct the clustering analysis to be computationally practical. Further, long time series data on entities also entails significant data security and privacy risks around the entity as it requires longer histories of entity behaviors to be stored and maintained [25, 41]. Thus, there is significant value for techniques that can produce approximately similar clustering results with smaller samples as with complete data.

Coresets have emerged as an effective tool to both speed up and reduce data storage by taking into account the objective and carefully sampling from the full dataset in a way that any algorithm run on the sampled set returns an approximate solution for the original objective with guaranteed bounds on approximation error [34]. Coresets have been developed for both unsupervised clustering (e.g., -means, Gaussian mixture models) and supervised machine learning (e.g., regression) methods for static data; for surveys on coresets for static data, see [7, 22]. A natural question is whether coresets can be also useful for addressing the time series clustering problem. Recently, there is evidence that small coresets can be efficiently constructed for time series data, albeit for regressions with time series (panel) data [37]. However, as we explain in Section 2, there are challenges in extending coresets for static data clustering and time series (panel) data regressions for time series clustering.

Our contributions.

We study coresets for a general class of time series clustering in which all entities are drawn from Gaussian mixtures with autocorrelations (as described above; see Problem 1). We first present a definition of coresets for the log-likelihood -clustering objective for this mixture model. One issue is that this objective cannot be decomposed into a summation of entity-time objectives due to the interaction of the term from log-likelihood and the term from Gaussians (Problem 1). To estimate this objective using a coreset, we introduce an analogous clustering objective on a subset of data (Definition 3.2). Our main result is an algorithm to construct coresets for this objective for the aforementioned mixture model (Theorem 4.2). Our algorithm is efficient (linear on both and ) and, assuming that the condition number of the covariance matrices of the Gaussians () are bounded and the eigenvalues of the autocorrelation matrices () are bounded away from (Assumption 1), the size of our coreset is independent of the number of entities and the number of observations s; it only polynomially depends on , and , where is the error parameter (Theorem 4.2).

Our coreset construction (Algorithm 1) leverages the Feldman-Langberg (FL) framework [27]. Due to multiple observations for each entity and associated autocorrelations, the objective is non-convex and quite complicated in contrast to the static setting where the objective only contains one observation drawn from Gaussian mixtures for each entity. Thus, bounding the “sensitivity” (Lemma 4.5) of each entity, which is a key step in coreset construction using the FL-framework, becomes challenging. We handle this technical difficulty by 1) upper-bounding the maximum effect of covariances and autocorrelations by using the observation that the gap between the clustering objectives with and without and is always constant, and 2) reducing the Gaussian mixture time series clustering problem to a certain -means clustering problem whose total sensitivity is upper bounded.

Empirically, we assess the performance of our coreset on synthetic data for a three cluster problem (Section 5), and compare the performance with two benchmarks: uniform sampling and a static coreset benchmark (LFKF [48]) in which we do not consider autocorrelations and regard time series data as static. We find that our coreset performs better relative to uniform sampling and LFKF on both data storage and computation speed for a range of accuracy guarantees: To achieve a similar fit with the full data, our coreset needs fewer entity-time observations (<40%); the computation time for a given level of accuracy reduces by a 3x-22x factor when compared to uniform sampling and LFKF. Moreover, our coreset speeds up the computation time relative to the full data by 14x-171x. We note that the performance advantage of our coreset is greater when there is more time series data relative to entities ().

2 Related work

Time series or panel data analysis are important in many fields– biological [18], engineering [3], economics [51] and the social sciences [59]. Clustering has been a central problem in unsupervised learning and also has a long history of use across many fields; for a historical overview of applications across fields, see [12]. While most standard treatments of clustering in machine learning tend to be on static data [35, 11], there is by now a significant and rapidly growing literature on time series clustering; recent surveys include [47, 2]. While there are many coresets for algorithms on static data (including for clustering), there has been little work on coresets on time series data (see below).

Coresets for clustering.

Coresets for various clustering objectives on static data have been well studied, including -median [34, 17, 55, 38, 19], -means [34, 17, 28, 13, 10, 55, 38, 19], and -center [1, 33]. For surveys of static coresets, see [52, 23]. [48, 26] present coreset constructions for clustering problems on static data generated using Gaussian mixture models. [48] constructs a coreset of size under the same boundedness assumption as ours. [26] remove this assumption and construct a coreset whose size additionally depends on , but require another assumption that all s are integral and in a bounded range. In contrast, we consider a generalized problem where each entity has multiple observations over time and accounts for autocorrelations across successive observations. The new idea is to reduce the GMM time series clustering problem (Problem 1) to a -means clustering problem whose points are linear combinations of those in (Lemma 6.12), and show that the effect of autocorrelation parameters on the entity objectives can be upper bounded (Lemma 6.11).

Regression with time series data.

[37] construct coresets for a regression problem, called GLSEk, for time-series data including autocorrelations and a -partition of entities. This is a supervised learning task that includes an additional label for each entity-time pair. It aims to find a -partition of entities and additional regression vectors for each partition such that a certain linear combination of terms is minimized. In contrast, our problem is an unsupervised learning task, estimates points by Gaussian means instead of , and includes covariances between different features. The definitions of coresets in [37] and ours consist of entity-time pairs but our coresets need to include multiple weight functions ( for entities and for time periods of selected entity ; see Definition 3.2) instead of one weight function as in the regression problem. This is to deal with the interaction of the term from the log-likelihood and the term from the Gaussians. [37]’s result relies on an assumption that the regression objective of each entity is in a bounded range over the parameter space. This may not be satisfied in our setting since the clustering objective of an entity may be unbounded when all Gaussian means are far away from observations of this entity. To bypass this, we reduce our problem to a -means clustering problem (Definition 4.1), whose total sensitivity is provably (Lemma 6.12), by upper bounding the affect of covariance and autocorrelation parameters on the clustering objectives of entities (Lemma 6.11) under the assumption that the condition number of covariance matrix is bounded (Assumption 1), which provides an upper bound for the total sensitivity of entities on our problem (Lemma 4.5).

Another related direction is to consider coreset construction for -segmentation with time series data [54, 29], which aims to estimate the trace of an entity by a -piecewise linear function (-segment). Note that the case of is equivalent to the linear regression problem. [54, 29] proposed efficient coreset construction algorithms which accelerate the computation time of the -segmentation problem. The main difference from our setting is that they consider a single entity observed at multiple time periods, and the objective is an additive function on all time periods. This enables them to relate the -segmentation problem to the static setting. It is interesting to investigate coreset construction for more optimization problems with time series data.

3 Clustering model and coreset definition

Given , we first model a general class of time series clustering problems. Then we specify our setting with Gaussian mixture time series data (Problem 1), and define coresets accordingly (Definition 3.2).

Clustering with time series data.

Given an integer , let denote a probability simplex satisfying that for any , we have for and . Let denote a parameter space where each represents a specific generative model of time series data. For each entity and model , define to be the average likelihood/realized probability of from model . The ratio is used to normalize the contribution to the objective of entity due to different lengths . The time series clustering problem is to compute and that minimizes the negative log-likelihood, i.e., Here, for each , represents the probability that each time series is generated from model . Note that the clustering objective depends on the choice of model family . In this paper, we consider the following specific model family that each time series is generated from Gaussian mixtures.

GMM clustering with time series data.

Let be a given probability vector. Let denote the collection of all symmetric positive definite matrices in . For each , with probability (), let for each where represents a Gaussian mean and represents the error vector drawn from the following normal distribution: , where is an AR(1) autocorrelation matrix and is the covariance matrix of a multivariate Gaussian distribution. Now we let and note that each Gaussian generative model can be represented by a tuple . Moreover, we have that the realized probability of each entity is

| (1) |

where is the determinant of and with

We note that each sub-function contains at most two entity-time pairs: and . Our Gaussian mixture time series model gives rise in the following clustering problem.

Problem 1 (Clustering with GMM time series data).

Given a time series dataset and integer , the GMM time series clustering problem is to compute and that minimize

From Equation (1) it follows that the coefficient of each Gaussian before the operation is , whose summation is not a fixed value and depends on s. To remove this dependence on the coefficients, we define to be the normalized coefficient for , define offset function to be , and define whose summation of coefficients before the operations is 1. This idea of introducing also appears in [24, 26], which is useful for coreset construction. This leads to the following observation.

Observation 3.1.

For any and ,

Our coreset definition.

The clustering objective can only be decomposed into the summation of s instead of sub-functions w.r.t. entity-time pairs. A simple idea is to select a collection of weighted entities as a coreset. However, in doing so, the coreset size will depend on s and fail to be independent of both and s. To address this problem, we define our coreset as a collection of weighted entity-time pairs, which is similar to [37]. Let denote the collection of indices of all . Given , we let denote the collection of entities that appear in . Moreover, for each , we let denote the collection of observations for entity in .

Definition 3.2 (Coresets for GMM time series clustering).

Given a time series dataset , constant , integer , and parameter space , an -coreset for GMM time series clustering is a weighted set together with weight functions and for such that for any and ,

Combining the above definition with Observation 3.1, we note that for any and ,

| (2) |

As tends to 0, converges to . Moreover, given such a coreset , if we additionally have that , we can minimize to solve Problem 1. Thus, if , we conclude that . Note that we introduce multiple weight functions ( for entities and for time periods of selected entity ) in Definition 3.2 unlike the coreset for time series regression in [37] which uses only one weight function. This is because contains and operators instead of linear combinations of ; it is unclear how to use a single weight function to capture both the entity and time levels.

4 Theoretical results

We present our coreset algorithm (Algorithm 1) and the main result on its performance (Theorem 4.2). Theorem 4.2 needs the following assumptions on covariance and autocorrelation parameters.

Assumption 1.

Assume (1) that there exists constant such that where represents the largest eigenvalue and represents the smallest eigenvalue, and (2) for , for some constant . Here is a collection of all diagonal matrix in whose diagonal elements are at most .

The first assumption requires that the condition number of each covariance matrix is upper-bounded, which also appears in [60, 45, 48] that consider Gaussian mixture models with static data. The second assumption, roughly, requires that there exist autocorrelations only between the same features. The upper bound for diagonal elements ensures that the autocorrelation degrades as time period increases, which is also assumed in [37]. Note that both the eigenvalues of and the positions of means s affect cost function s. For instance, consider the case that all eigenvalues are 1 and all autocorrelations are 0, i.e., for all , and . In this case, it is easy to see that , i.e., the value of is unbounded as changes. Differently, the component’s cost functions are bounded in [37] since s do not appear in [37] that consider regression problems.

Let denote the parameter space. For preparation, we propose the following -means clustering problem.

Definition 4.1 (-means clustering of entities).

Given an integer , the goal of the -means clustering problem of entities of is to find a set of centers that minimizes over all center sets . Let denote the optimal -means value of .

Note that there exists an time algorithm to compute a nearly optimal solution for both and [43]. Another widely used algorithm is called -means++ [6], which provides an -approximation in time but performs well in practice. We also observe that for any . This observation motivates us to consider a reduction from Problem 1 to Definition 4.1, which is useful for constructing .

4.1 Our coreset algorithm

We first give a summary of our algorithm (Algorithm 1). The input to Algorithm 1 is a time series dataset , an error parameter of coreset , an integer of clusters, (vector norm bound), and a covariance eigenvalue gap . We develop a two-staged importance sampling framework which first samples a subset of entities (Lines 1-8) and then samples a subset of time periods for each selected entity (Lines 9-14).

In the first stage, we first set as the number of selected entities (Line 1). Then we solve the -means clustering problem over entity means (Definition 4.1), e.g., by -means++ [6] (Lines 2-3), and obtain an (approximate) optimal clustering value , a -center set , and an offset value for each . Next, based on the distances of points to , we partition into clusters where entity belongs to cluster (Line 4). Based on , and , we compute an upper bound for the sensitivity w.r.t. entity (Lines 5-6). Finally, we sample a weighted subset of entities as our coreset for the entity level by importance sampling based on (Lines 7-8), which follows from the Feldman-Langberg framework (Theorem 6.6).

In the second stage, we first set as the number of time periods for each selected entity (Line 9). Then for each selected entity , we compute as the optimal -means clustering objective of s (Line 10). Next, we compute an upper bound for the sensitivity w.r.t. time period (Lines 11-12) based on and . Finally, we sample a weighted subset of time periods by importance sampling based on (Lines 13-14).

4.2 Our main theorem

Our main theorem is as follows, which indicates that Algorithm 1 provides an efficient coreset construction algorithm for GMM time series clustering.

Theorem 4.2 (Main result).

Note that the success probability in the theorem can be made for any at the expense of an additional factor in the coreset size. The coreset size guaranteed by Theorem 4.2 has a polynomial dependence on factors , and and, importantly, does not depend on or s. Compared to the clustering problem with GMM static data [48], the coreset has an additional dependence on due to autocorrelation parameters. Compared to the regression problem (GLSEk) with time series data [37, Theorem 5.2], the coreset does not contain the factor “” that upper bounds the gap between the maximum and the minimum entity objective. The construction time linearly depends on the total number of observations , which is efficient. The proof of Theorem 4.2 can be found in Section 8.

Proof overview of Theorem 4.2.

The proof consists of three parts: 1) Bounding the size of the coreset, 2) proving the approximation guarantee of the coreset, and 3) bounding the running time.

Parts 1 & 2: Coreset size and correctness guarantee of Theorem 4.2. We first note that the coreset size in Theorem 4.2 is . Here, is the number of sampled entities that guarantee that is a coreset for at the entity level (Lemma 4.3). is the number of sampled observations for each that guarantees that is a coreset for at the time level (Lemma 4.4).

Lemma 4.3 (The 1st stage outputs an entity-level coreset).

With probability at least , the output of Algorithm 1 with satisfies that for any and ,

Lemma 4.4 (The 2nd stage outputs time level coresets for each ).

With probability at least , for all , the output of Algorithm 1 with satisfies that for any ,

From Lemmas 4.3 and 4.4, we can conclude that is an -coreset for GMM time-series clustering, since the errors for the entity level and the time level are additively accumulated, and that the size of the coreset as claimed; see Section 8 for a complete proof.

Both lemmas rely on the Feldman-Langberg framework [27, 13] (Theorem 6.6). The key is to upper bound both the “pseudo-dimension” (Definition 6.5) that measures the complexity of the parameter space, and the total sensitivity (Definition 6.4) that measures the sum of maximum influences of all sub-functions ( for Lemma 4.3 and for Lemma 4.4). The coreset size guaranteed by the Feldman-Langberg framework then is .

For Lemma 4.4, we can upper bound the pseudo-dimension by (Lemma 7.1). For the total sensitivity, a key step is to verify that (Line 12) is a sensitivity function of . This step uses a similar idea as in [37] and leads to showing a bound for the total sensitivity (Lemma 7.2). Then we verify that is enough for Lemma 4.4 by the Feldman-Langberg framework (Theorem 6.6). The proof can be found in Section 7.

Proof sketch:

By [4, 58], the pseudo-dimension is determined by the number of parameters that is upper bounded by and the number of operations on parameters that is upper bounded by including exponential functions. Then we can upper bound the pseudo-dimension by (Lemma 6.9 in Section 6.2).

For the total sensitivity, the key is to verify that (Line 6) is a sensitivity function w.r.t. ; this is established by Lemma 4.5 below. Then the total sensitivity is at most . This completes the proof of Lemma 4.3 since is enough by the Feldman-Langberg framework (Theorem 6.6).

Lemma 4.5 ( is a sensitivity function w.r.t. ).

For each , we have Moreover, .

Proof sketch of Lemma 4.5. We first define for any , and define . Based on , we define another sensitivity function and want to reduce to . Note that , i.e., removes the covariance and autocorrelation parameters from . Due to this observation, we have that by upper bounding the affect of covariance parameters (controlled by factor ) and autocorrelation parameters (controlled by factor ), summarized as Lemma 6.11. Then to prove Lemma 4.5, it suffices to prove that which implies that the total sensitivity of is upper bounded by (Lemma 6.12), due to fact that (Lemma 6.13). Finally, the proof of Lemma 6.12 is based on a reduction from to the -means clustering problem of entities (Definition 4.1) by rewriting and then projecting each to its closest center in . The full proof of this lemma can be found in Section 6.3.

Part 3: Running time in Theorem 4.2. The first stage costs time. The dominating steps are 1) to compute in Line 2 which costs time; 2) to solve the -means clustering problem of entities (Line 3) which costs time. The second stage costs at most time. The dominating step is to compute for all in Line 10, where it costs time to compute each .

Remark 4.6 (Technical comparison with prior works).

Note that our entity coreset construction uses some ideas from [24, 48] and also develops novel technical ideas. A generalization of [24, 48] to time series data is to treat all observations independent and compute a sensitivity for each directly for importance sampling. However, this idea cannot capture the property that multiple observations are drawn from the same Gaussian model (certain ). To handle multiple observations, we show that although each consists of sub-functions , it can be approximated by a single function on the average observation , specifically, we have . This property enables us to "reduce" the representative complexity of , and motivate two key steps of our construction: 1) For the sensitivity function, we give a reduction to a certain -means clustering problem on average observations of entities (Definition 4.2) by upper bounding the maximum effect of covariances and autocorrelations and applying the fact that . 2) For the pseudo-dimension, we prove that there are only intristic operators in between parameters and observations , based on the reduction of the representative complexity of .

Generalizing our results in the same manner as [26] does over [24, 48] would be an interesting future direction since we may get rid of Assumption 1. Currently, it is unclear how to generalize the approach of [26] to time series data since [26] assumes that each point is an integral point within a bounded box, while we consider a continuous GMM generative model (1), and hence, each coordinate of an arbitrary observation is drawn from a certain continuous GMM distribution which is not integral with probability and can be unbounded.

Remark 4.7 (Discussion on lower bounds).

There is no provable lower bound result for our GMM coreset with time series data. We conjecture that without the first condition in Assumption 1, the coreset size should depend exponentially in and logarithmic in . The motivation is from a simple setting that all (GMM with static data), in which [26] reduces the problem to projective clustering whose coreset size depends exponentially in and logarithmic in . Moreover, [26] believes that these dependencies are unavoidable for GMM coreset.

5 Empirical results

We compare the performance of our coreset algorithm , with uniform sampling as a benchmark using synthetic data. The experiments are conducted with PyCharm IDE on a computer with 8-core CPU and 32 GB RAM.

Datasets.

We generate two sets of synthetic data all with 250K observations with different number of entities and observations per individual : (i) for all and (ii) , for all . As cross-entity variance is greater than within entity variance, this helps to assess coreset performance sensitivity when there are more entities (high ) vs. more frequent measurement/ longer measurement period (high ).

We fix , , and generate multiple datasets with model parameters randomly varied as follows: (i) Draw from a uniform distribution over . (ii) For each , draw from . (iii) Draw by first generating a random matrix and then let , and (iv) draw all diagonal elements of from a uniform distribution over [0, ]. Given these draws of parameters, we generate a GMM time-series dataset as follows: For each , draw given . Then, for all draw with covariance matrix and autocorrelation matrix and compute .

Baseline and metrics.

We use coresets based on uniform sampling (Uni) and based on [48] (LFKF) that constructs a coreset for Gaussian mixture model with static data as the baseline. Given an integer , uniformly sample a collection of entity-time pairs , let for each , and let for each ; and LFKF regard all entity-time pairs as independent points and sample a collection of entity-time pairs via importance sampling. For comparability, we set to be the same as our coreset size. The goal of selecting LFKF as a baseline is to see the effect of autocorrelations to the objective and show the difference between static clustering and time series clustering.

Let (negative log-likelihood) denote the objective of Problem 1 with full data. Given a weighted subset , we first compute as the maximum likelihood solution over .222We solve this optimization problem using an EM algorithm similar to [5]. The M step in each iteration is based on IRLS [40] and the E-step involves an individual level Bayesian update for . Then over the full dataset serves as a metric of model fit given model estimates from a weighted subset . We use the likelihood ratio, i.e., as a measure of the quality of [14]. The running time for GMM clustering with full data () and coreset () are and respectively. is the coreset construction time.

Empirical setup.

We vary . For each , we run and Uni to generate 5 coresets each. We estimate the model with the full dataset and the coresets and record , and the run times.

| size | (s) | (s) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Uni | LFKF | Uni | LFKF | Uni | LFKF | ||||||||

| Synthetic 1 | 0.1 | 2050 | 2058 | 2069 | 2041 | 22 | 34 | 56 | 1514 | 109 | 2416 | 1355 | 3436 |

| 0.2 | 2093 | 2210 | 2264 | 104 | 342 | 446 | 404 | 41 | 1054 | 652 | |||

| 0.3 | 2194 | 2398 | 2384 | 306 | 714 | 686 | 191 | 62 | 419 | 392 | |||

| 0.4 | 2335 | 3963 | 2705 | 588 | 3844 | 1328 | 93 | 38 | 621 | 260 | |||

| 0.5 | 2383 | 3304 | 3461 | 684 | 2526 | 2840 | 72 | 47 | 132 | 147 | |||

| Synthetic 2 | 0.1 | 811 | 825 | 841 | 812 | 2 | 26 | 58 | 1718 | 694 | 1859 | 1687 | 9787 |

| 0.2 | 824 | 895 | 871 | 24 | 166 | 118 | 447 | 139 | 1991 | 1484 | |||

| 0.3 | 864 | 958 | 994 | 104 | 292 | 364 | 199 | 51 | 527 | 832 | |||

| 0.4 | 860 | 1190 | 1114 | 96 | 756 | 604 | 98 | 43 | 408 | 450 | |||

| 0.5 | 910 | 1361 | 1284 | 196 | 1098 | 944 | 71 | 57 | 389 | 277 | |||

Results.

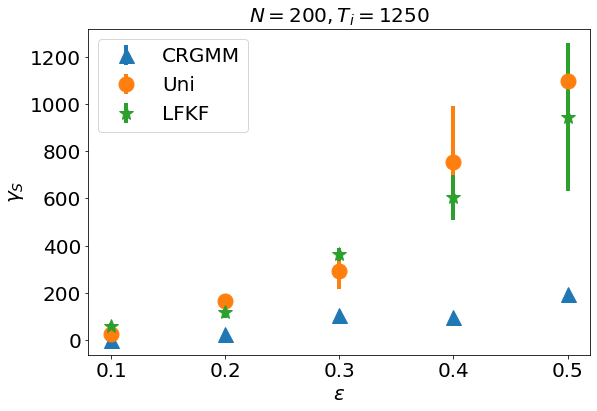

Table 1 summarizes the quality-size-time trade-offs of our coresets for different error guarantees . The achieved by our coreset is always close to the optimal value and is always smaller than that of Uni and LFKF. We next assess coreset size. For the case, the coreset achieves a likelihood ratio with only 72 entity-time pairs (0.03%), but Uni/LFKF achieves the closest (but worse) likelihood ratio of , with 191 entity-time pairs (0.08%). Thus, our coreset achieves a better likelihood than uniform and LFKF with less than 40% of observations. Further, from Figure 1, we see that not only is the quality of our coreset () superior, it has lower standard deviations suggesting lower variance in performance. In terms of total computation time relative to the full data (), our coresets speed up by 14x-171x. Also, the computation time () of Uni and LFKF is always larger than that of our coreset (3x-22x).333A possible explanation is that our coreset selects of entities that are more representative that Uni, and hence, achieves a better convergence speed. Finally, is lower for Synthetic 2 given that there are fewer entities and cross-entity variance is greater than within entity variance. From Figure 1, we also see that both the fit and std in performance for coresets is much lower for Synthetic 2. Thus, overall our coreset performs better when there is more time series data relative to entities ()—a feature of sensor based measurement that motivates this paper.

6 Proof of Lemma 4.3: The first stage of Algorithm 1 outputs an entity-level coreset

For preparation, we first introduce an importance sampling framework for coreset construction, called the Feldman-Langberg framework [27, 13].

6.1 The Feldman-Langberg framework

We first give the definition of query space and the corresponding coresets.

Definition 6.1 (Query space [27, 13]).

Let be a finite set together with a weight function . Let be a set called queries, and be a given loss function w.r.t. . The total cost of with respect to a query is The tuple is called a query space. Specifically, if for all , we use for simplicity.

Intuitively, represents a linear combination of weighted functions indexed by , and represents the ground set of . Due to the separability of , we have the following coreset definition.

Definition 6.2 (Coresets of a query space [27, 13]).

Let be a query space and be an error parameter. An -coreset of is a weighted set together with a weight function such that for any ,

Remark 6.3.

For instance, we set , , and in the GMM time-series clustering problem. Then by Definition 6.2, Lemma 4.3 represents that is an -coreset for the query space .

Another example is to set , , and . Then Lemma 4.4 represents that is an -coreset for the query space .

Now we are ready to give the Feldman-Langberg framework.

The Feldman-Langberg framework.

Feldman and Langberg [27] show how to construct coresets by importance sampling and the coreset size has been improved by [13]. For preparation, we first give the notion of sensitivity which measures the maximum influence for each point .

Definition 6.4 (Sensitivity [27, 13]).

Given a query space , the sensitivity of a point is The total sensitivity of the query space is .

We also introduce a notion which measures the combinatorial complexity of a query space.

Definition 6.5 (Pseudo-dimension [27, 13]).

For a query space , we define for every and . The (pseudo-)dimension of is the largest integer such that there exists a subset of size satisfying that

Pseudo-dimension plays the same role as VC-dimension [56]. Specifically, if the range of is and , pseudo-dimension can be regarded as a generalization of VC-dimension to function spaces. Now we are ready to describe the Feldman-Langberg framework.

Theorem 6.6 (Feldman-Langberg framework [27, 13]).

Let be a given query space and . Let be an upper bound of the pseudo-dimension of every query space over . Suppose is a function satisfying that for any , and define to be the total sensitivity. Let be constructed by taking samples, where each sample is selected with probability and has weight . Then, with probability at least , is an -coreset of .

6.2 Bounding the pseudo-dimension of

Our proof idea is similar to that in [48]. For preparation, we need the following lemma which is proposed to bound the pseudo-dimension of feed-forward neural networks.

Lemma 6.7 (Restatement of Theorem 8.14 of [4]).

Let be a given query space where for any and , and . Suppose that can be computed by an algorithm that takes as input the pair and returns after no more than of the following operations:

-

•

the exponent function on real numbers.

-

•

the arithmetic operations , and on real numbers.

-

•

jumps conditioned on , and comparisons of real numbers, and

-

•

output 0,1.

If the operations include no more than in which the exponential function is evaluated, then the pseudo-dimension of is at most .

Note that the above lemma requires that the range of functions is . We have the following lemma which can help extend this range to .

Lemma 6.8 (Restatement of Lemma 4.1 of [58]).

Let be a given query space. Let be the indicator function satisfying that for any , and ,

Then the pseudo-dimension of is precisely the pseudo-dimension of the query space .

Now we are ready to prove bound the pseudo-dimension of by the following lemma.

Lemma 6.9 (Pseudo-dimension of ).

The pseudo-dimension of over weight functions is at most .

Proof:

Our argument is similar to that in [37, Lemma 5.9]. Fix a weight function . We only need to consider the following indicator function where for any , and ,

Note that the parameter space is which consists of at most parameters. For any , function can be represented as a multivariate polynomial that consists of terms where , and . Thus, consists of arithmetic operations, exponential functions, and jumps. By Lemmas 6.7 and 6.8, we complete the proof.

6.3 Bounding the total sensitivity of

Next, we prove that function (Line 6 of Algorithm 1) is a sensitivity function w.r.t. ; summarized as follows.

Lemma 6.10 ( is a sensitivity function w.r.t. ).

For each , we have

Moreover, .

To prove the lemma, we will use a reduction from general to and from to (without both covariances and autocorrelations), which upper bounds the affect of the covariance matrix and autocorrelation matrices. We define to be

| (3) |

for any , and define to be

for any and . Compared to , we note that does not contain covariance and autocorrelation matrices.

Clustering cost of entities.

By the definition of , we have that for any ,

| (4) |

Next, we introduce another function as a sensitivity function w.r.t. , i.e., for any ,

Define to be the total sensitivity w.r.t. . We first have the following lemma.

Lemma 6.11 (Relation between sensitivities w.r.t. and ).

For each , we have

Proof:

It is easy to verify since

For the other side, we have the following claim that for any and ,

| (5) |

Then for any and , letting and , we have

Consequently, we have , which completes the proof.

Proof of Claim (5).

It remains to prove Claim (5). For any and , we have

Hence, it suffices to prove that

Since , we suppose . Then we have

On one hand, we have

On the other hand, we have

This completes the proof.

By the definition of and the above lemma, it suffices to prove the following lemma that provides an upper bound for .

Lemma 6.12 (Sensitivities w.r.t. ).

The following holds:

-

1.

For each , we have

-

2.

.

For preparation, we introduce some notations related to the clustering problem (Definition 4.1). For any , we define

and for any ,

where . Let . Then similarly, we can prove that (Line 5 of Algorithm 1) is a sensitivity function w.r.t. ; summarized as follows.

Lemma 6.13 ( is a sensitivity function w.r.t. ).

For each ,

Moreover, .

Proof:

This lemma is a direct corollary by the fact that there are only different centers , which implies that there are at most different functions accordingly. We partition into at most groups where each element satisfies that . Then we observe that if . Then for any ,

which implies the lemma.

To prove Lemma 6.12, the main idea is to relate to . The idea is similar to [48]. For preparation, we also need the following key observation.

Lemma 6.14 (Upper bounding the projection cost).

For a fixed number and a fixed and a fixed value , define as

Then, for every it holds that

Proof:

Use the relaxed triangle inequality for -norm, we have

Recall that . Now we are ready to prove Lemma 6.12.

Proof:

[Proof of Lemma 6.12] For each and , letting , we have

| (6) |

Let . We have that

| (7) |

Hence, we have

The second property is a direct conclusion.

Now we are ready to prove Lemma 6.10.

Proof:

7 Proof of Lemma 4.4: The second stage of Algorithm 1 outputs a time-level coreset

The proof idea is similar to that in Lemma 4.3, i.e., to bound the pseudo-dimension and the total sensitivity for the query space .

7.1 Bounding the pseudo-dimension of

We have the following lemma.

Lemma 7.1 (Pseudo-dimension of ).

The pseudo-dimension of over weight functions is at most .

Proof:

7.2 Bounding the total sensitivity of

Next, we again focus on proving (Line 12 of Algorithm 1) is a sensitivity function w.r.t. ; summarized as follows.

Lemma 7.2 ( is a sensitivity function for ).

For each , we have that for each

Moreover, .

Similar to Section 6, we introduce another function as a sensitivity function w.r.t. , i.e., for any ,

Define to be the total sensitivity w.r.t. . We first have the following lemma, whose proof idea is simply from Lemma 6.11 and [37, Lemma 4.4].

Lemma 7.3 (Relation between sensitivities w.r.t. and ).

For each , we have

Proof:

By the same argument as in Lemma 6.11, we have that

By a similar argument as in [37, Lemma 4.4], we have that

Combining the above two inequalities, we complete the proof.

Then we have the following lemma that relates and (Line 11 of Algorithm 1), whose proof follows from [57, Theorem 7] for the case that .

Lemma 7.4 (Sensitivities w.r.t. ).

For each , the following holds:

-

1.

For each , we have

-

2.

.

8 Proof of Theorem 4.2

Proof:

Note that the coreset size matches the bound in Theorem 4.2. We first prove the correctness. For any , we have

Symmetrically, we can also verify that

Consequently, we have

| (8) |

Combining with Lemma 4.3, we have that

By replacing with , we prove the correctness.

For the computation time, the computation in Line 2 costs time since each and can be computed in time, and can be computed in time. In Line 3, it costs time to solve the -means clustering problem by -means++. Line 4 costs time since each costs time to compute. Lines 5-6 cost time for computing sensitivity function . Lines 7-8 cost time for constructing . Overall, it costs at the first stage. Line 10 costs at most time to compute . Lines 11-12 cost time to compute . Lines 13-14 cost time to construct . Since , we have that it costs at most time at the second stage. We complete the proof.

9 Limitations, conclusion, and future work

In this paper, we study the problem of constructing coresets for clustering problems with time series data; in particular, we address the problem of constructing coresets for time series data generated from Gaussian mixture models with auto-correlations across time. Our coreset construction algorithm is efficient under a mild boundedness assumption on the covariance matrices of the underlying Gaussians, and the size of the coreset is independent of the number of entities and the number of observations and depends only polynomially on the number of clusters, the number of variables and an error parameter. Through empirical analysis on synthetic data, we demonstrate that the coreset sampling is superior to uniform sampling in computation time and accuracy.

Our work leaves several interesting directions for future work on time series clustering. While our current specification with autocorrelations assumes a stable time series pattern over time, future work should extend it to a hidden Markov process, where the time series process may switch over time. Further, while our focus here is on model-based clustering, it would be useful to consider how coresets should be constructed for other clustering methods such as direct clustering of raw data and indirect clustering of features.

Overall, we hope the paper stimulates more research on coreset construction for time series data on a variety of unsupervised and supervised machine learning algorithms. The savings in storage and computational cost without sacrificing accuracy is not only financially valuable, but also can have sustainability benefits through reduced energy consumption. Finally, recent research has shown that summaries (such as coresets) for static data need to include fairness constraints to avoid biased outcomes for under-represented groups based on gender and race when using the summary [16, 36]; future research needs to extend such techniques for time series coresets.

Acknowledgments

This research was supported in part by an NSF CCF-1908347 grant.

References

- [1] Pankaj K Agarwal and Cecilia Magdalena Procopiuc. Exact and approximation algorithms for clustering. Algorithmica, 33(2):201–226, 2002.

- [2] Saeed Aghabozorgi, Ali Seyed Shirkhorshidi, and Teh Ying Wah. Time-series clustering–a decade review. Information Systems, 53:16–38, 2015.

- [3] Hirotugu Akaike and Genshiro Kitagawa. The practice of time series analysis. Springer Science & Business Media, 2012.

- [4] Martin Anthony and Peter L Bartlett. Neural network learning: Theoretical foundations. Cambridge University press, 2009.

- [5] Peter Arcidiacono and John Bailey Jones. Finite mixture distributions, sequential likelihood and the EM algorithm. Econometrica, 71(3):933–946, 2003.

- [6] David Arthur and Sergei Vassilvitskii. -means++: the advantages of careful seeding. In Nikhil Bansal, Kirk Pruhs, and Clifford Stein, editors, Proceedings of the Eighteenth Annual ACM-SIAM Symposium on Discrete Algorithms, SODA 2007, New Orleans, Louisiana, USA, January 7-9, 2007, pages 1027–1035. SIAM, 2007.

- [7] Olivier Bachem, Mario Lucic, and Andreas Krause. Practical coreset constructions for machine learning. arXiv preprint arXiv:1703.06476, 2017.

- [8] Badi Baltagi. Econometric analysis of panel data. John Wiley & Sons, 2008.

- [9] Kasun Bandara, Christoph Bergmeir, and Slawek Smyl. Forecasting across time series databases using recurrent neural networks on groups of similar series: A clustering approach. Expert systems with applications, 140:112896, 2020.

- [10] Luca Becchetti, Marc Bury, Vincent Cohen-Addad, Fabrizio Grandoni, and Chris Schwiegelshohn. Oblivious dimension reduction for -means: beyond subspaces and the Johnson-Lindenstrauss lemma. In Proceedings of the 51st Annual ACM SIGACT Symposium on Theory of Computing, pages 1039–1050. ACM, 2019.

- [11] Avrim Blum, John Hopcroft, and Ravindran Kannan. Foundations of data science. Cambridge University Press, 2020.

- [12] Hans-Hermann Bock. Clustering methods: a history of -means algorithms. Selected contributions in data analysis and classification, pages 161–172, 2007.

- [13] Vladimir Braverman, Dan Feldman, and Harry Lang. New frameworks for offline and streaming coreset constructions. CoRR, abs/1612.00889, 2016.

- [14] Adolf Buse. The likelihood ratio, wald, and lagrange multiplier tests: An expository note. The American Statistician, 36(3a):153–157, 1982.

- [15] Jorge Caiado, Elizabeth A Maharaj, and Pierpaolo D’Urso. Time series clustering. Handbook of cluster analysis, pages 241–263, 2015.

- [16] L. Elisa Celis, Vijay Keswani, Damian Straszak, Amit Deshpande, Tarun Kathuria, and Nisheeth K. Vishnoi. Fair and diverse dpp-based data summarization. In Jennifer G. Dy and Andreas Krause, editors, Proceedings of the 35th International Conference on Machine Learning, ICML 2018, Stockholmsmässan, Stockholm, Sweden, July 10-15, 2018, volume 80 of Proceedings of Machine Learning Research, pages 715–724. PMLR, 2018.

- [17] Ke Chen. On coresets for -median and -means clustering in metric and Euclidean spaces and their applications. SIAM J. Comput., 39(3):923–947, August 2009.

- [18] Mike X Cohen. Analyzing neural time series data: theory and practice. MIT press, 2014.

- [19] Vincent Cohen-Addad, David Saulpic, and Chris Schwiegelshohn. A new coreset framework for clustering. pages 169–182, 2021.

- [20] Pierpaolo D’Urso and Elizabeth Ann Maharaj. Autocorrelation-based fuzzy clustering of time series. Fuzzy Sets and Systems, 160(24):3565–3589, 2009.

- [21] Jason Ernst, Gerard J Nau, and Ziv Bar-Joseph. Clustering short time series gene expression data. Bioinformatics, 21(suppl_1):i159–i168, 2005.

- [22] Dan Feldman. Core-sets: Updated survey. Sampling Techniques for Supervised or Unsupervised Tasks, pages 23–44, 2020.

- [23] Dan Feldman. Introduction to core-sets: an updated survey. CoRR, abs/2011.09384, 2020.

- [24] Dan Feldman, Matthew Faulkner, and Andreas Krause. Scalable training of mixture models via coresets. In Advances in Neural Information Processing Systems 24: 25th Annual Conference on Neural Information Processing Systems 2011. Proceedings of a meeting held 12-14 December 2011, Granada, Spain, pages 2142–2150, 2011.

- [25] Dan Feldman, Amos Fiat, Haim Kaplan, and Kobbi Nissim. Private coresets. In Proceedings of the forty-first annual ACM symposium on Theory of computing, pages 361–370, 2009.

- [26] Dan Feldman, Zahi Kfir, and Xuan Wu. Coresets for Gaussian mixture models of any shape. arXiv preprint arXiv:1906.04895, 2019.

- [27] Dan Feldman and Michael Langberg. A unified framework for approximating and clustering data. In Proceedings of the forty-third annual ACM symposium on Theory of computing, pages 569–578. ACM, 2011. https://arxiv.org/abs/1106.1379.

- [28] Dan Feldman, Melanie Schmidt, and Christian Sohler. Turning big data into tiny data: Constant-size coresets for -means, PCA and projective clustering. In Proceedings of the Twenty-Fourth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1434–1453. SIAM, 2013.

- [29] Dan Feldman, Cynthia R. Sung, Andrew Sugaya, and Daniela Rus. idiary: From GPS signals to a text- searchable diary. ACM Trans. Sens. Networks, 11(4):60:1–60:41, 2015.

- [30] Sylvia Frühwirth-Schnatter. Panel data analysis: a survey on model-based clustering of time series. Adv. Data Anal. Classif., 5(4):251–280, 2011.

- [31] Tak-chung Fu. A review on time series data mining. Engineering Applications of Artificial Intelligence, 24(1):164–181, 2011.

- [32] John N Haddad. A simple method for computing the covariance matrix and its inverse of a stationary autoregressive process. Communications in Statistics-Simulation and Computation, 27(3):617–623, 1998.

- [33] Sariel Har-Peled. Clustering motion. Discrete & Computational Geometry, 31(4):545–565, 2004.

- [34] Sariel Har-Peled and Soham Mazumdar. On coresets for -means and -median clustering. In 36th Annual ACM Symposium on Theory of Computing,, pages 291–300, 2004.

- [35] Christian Hennig, Marina Meila, Fionn Murtagh, and Roberto Rocci. Handbook of cluster analysis. CRC Press, 2015.

- [36] Lingxiao Huang, Shaofeng H.-C. Jiang, and Nisheeth K. Vishnoi. Coresets for clustering with fairness constraints. In Hanna M. Wallach, Hugo Larochelle, Alina Beygelzimer, Florence d’Alché-Buc, Emily B. Fox, and Roman Garnett, editors, Advances in Neural Information Processing Systems 32: Annual Conference on Neural Information Processing Systems 2019, NeurIPS 2019, December 8-14, 2019, Vancouver, BC, Canada, pages 7587–7598, 2019.

- [37] Lingxiao Huang, K. Sudhir, and Nisheeth K. Vishnoi. Coresets for regressions with panel data. In Hugo Larochelle, Marc’Aurelio Ranzato, Raia Hadsell, Maria-Florina Balcan, and Hsuan-Tien Lin, editors, Advances in Neural Information Processing Systems 33: Annual Conference on Neural Information Processing Systems 2020, NeurIPS 2020, December 6-12, 2020, virtual, 2020.

- [38] Lingxiao Huang and Nisheeth K. Vishnoi. Coresets for clustering in Euclidean spaces: Importance sampling is nearly optimal. In Konstantin Makarychev, Yury Makarychev, Madhur Tulsiani, Gautam Kamath, and Julia Chuzhoy, editors, Proccedings of the 52nd Annual ACM SIGACT Symposium on Theory of Computing, STOC 2020, Chicago, IL, USA, June 22-26, 2020, pages 1416–1429. ACM, 2020.

- [39] Jui-Long Hung, Morgan C Wang, Shuyan Wang, Maha Abdelrasoul, Yaohang Li, and Wu He. Identifying at-risk students for early interventions—a time-series clustering approach. IEEE Transactions on Emerging Topics in Computing, 5(1):45–55, 2015.

- [40] Murray Jorgensen. Iteratively reweighted least squares. Encyclopedia of Environmetrics, 3, 2006.

- [41] T Tony Ke and K Sudhir. Privacy rights and data security: GDPR and personal data driven markets. Available at SSRN 3643979, 2020.

- [42] Eamonn Keogh. A decade of progress in indexing and mining large time series databases. In Proceedings of the 32nd international conference on Very large data bases, pages 1268–1268, 2006.

- [43] Amit Kumar, Yogish Sabharwal, and Sandeep Sen. A simple linear time (1+)-approximation algorithm for -means clustering in any dimensions. In 45th Symposium on Foundations of Computer Science (FOCS 2004), 17-19 October 2004, Rome, Italy, Proceedings, pages 454–462. IEEE Computer Society, 2004.

- [44] James P LeSage. The theory and practice of spatial econometrics. University of Toledo. Toledo, Ohio, 28(11), 1999.

- [45] Jiao-fen Li, Wen Li, and Seak-Weng Vong. Efficient algorithms for solving condition number-constrained matrix minimization problems. Linear Algebra and its Applications, accepted, 08 2020.

- [46] Jinbo Li, Hesam Izakian, Witold Pedrycz, and Iqbal Jamal. Clustering-based anomaly detection in multivariate time series data. Applied Soft Computing, 100:106919, 2021.

- [47] T Warren Liao. Clustering of time series data—a survey. Pattern recognition, 38(11):1857–1874, 2005.

- [48] Mario Lucic, Matthew Faulkner, Andreas Krause, and Dan Feldman. Training Gaussian mixture models at scale via coresets. The Journal of Machine Learning Research, 18(1):5885–5909, 2017.

- [49] Benjamin M Marlin, David C Kale, Robinder G Khemani, and Randall C Wetzel. Unsupervised pattern discovery in electronic health care data using probabilistic clustering models. In Proceedings of the 2nd ACM SIGHIT international health informatics symposium, pages 389–398, 2012.

- [50] Ming Ouyang, William J Welsh, and Panos Georgopoulos. Gaussian mixture clustering and imputation of microarray data. Bioinformatics, 20(6):917–923, 2004.

- [51] M Hashem Pesaran. Time series and panel data econometrics. Oxford University Press, 2015.

- [52] Jeff M. Phillips. Coresets and sketches. CoRR, abs/1601.00617, 2016.

- [53] Aarthi Reddy, Meredith Ordway-West, Melissa Lee, Matt Dugan, Joshua Whitney, Ronen Kahana, Brad Ford, Johan Muedsam, Austin Henslee, and Max Rao. Using gaussian mixture models to detect outliers in seasonal univariate network traffic. In 2017 IEEE Security and Privacy Workshops (SPW), pages 229–234. IEEE, 2017.

- [54] Guy Rosman, Mikhail Volkov, Dan Feldman, John W. Fisher III, and Daniela Rus. Coresets for k-segmentation of streaming data. In Zoubin Ghahramani, Max Welling, Corinna Cortes, Neil D. Lawrence, and Kilian Q. Weinberger, editors, Advances in Neural Information Processing Systems 27: Annual Conference on Neural Information Processing Systems 2014, December 8-13 2014, Montreal, Quebec, Canada, pages 559–567, 2014.

- [55] Christian Sohler and David P. Woodruff. Strong coresets for -median and subspace approximation: Goodbye dimension. In FOCS, pages 802–813. IEEE Computer Society, 2018.

- [56] VN Vapnik and A Ya Chervonenkis. On the uniform convergence of relative frequencies of events to their probabilities. Theory of Probability and its Applications, 16(2):264, 1971.

- [57] Kasturi Varadarajan and Xin Xiao. On the sensitivity of shape fitting problems. In 32nd International Conference on Foundations of Software Technology and Theoretical Computer Science, page 486, 2012.

- [58] Mathukumalli Vidyasagar. A theory of learning and generalization. Springer-Verlag, 2002.

- [59] William WS Wei. Time series analysis. In The Oxford Handbook of Quantitative Methods in Psychology: Vol. 2. 2006.

- [60] Joong-Ho Won, Johan Lim, Seung-Jean Kim, and Bala Rajaratnam. Condition-number-regularized covariance estimation. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 75(3):427–450, 2013.

- [61] Yimin Xiong and Dit-Yan Yeung. Time series clustering with ARMA mixtures. Pattern Recognition, 37(8):1675–1689, 2004.

- [62] Yun Yang and Jianmin Jiang. Hmm-based hybrid meta-clustering ensemble for temporal data. Knowledge-Based Systems, 56:299–310, 2014.