Regime Switching Optimal Growth Model with Risk Sensitive Preferences

Abstract.

We consider a risk-sensitive optimization of consumption-utility on infinite time horizon where the one-period investment gain depends on an underlying economic state whose evolution over time is assumed to be described by a discrete-time, finite-state, Markov chain. We suppose that the production function also depends on a sequence of i.i.d. random shocks. For the sake of generality, the utility and the production functions are allowed to be unbounded from above. Under the Markov regime-switching model, it is shown that the value function of optimization problem satisfies an optimality equation and that the optimality equation has a unique solution in a particular class of functions. Furthermore, we show that an optimal policy exists in the class of stationary policies. We also derive the Euler equation of optimal consumption. Furthermore, the existence of the unique joint stationary distribution of the optimal growth process and the underlying regime process is examined. Finally, we present a numerical solution by considering power utility and some hypothetical values of parameters in a regime switching extension of Cobb–Douglas production rate function.

Key words: Regime switching models, Growth models, Risk sensitive Preferences, Optimal consumption, Euler equation

AMSC: 91B62, 91B55, 91B70, 60J10, 90C40

1. Introduction

Stochastic optimal growth model pioneered by [Brock and Mirman (1972)], has received considerable attention in the economics or related literature. We consider, in this paper, a regime switching optimal growth model for a single sector in the discrete time settings where the agent has risk sensitive preferences. Markov regime-switching models have important applications in economics and econometrics (see, for example, [Hamilton (1989), Hamilton (2016)]). It is assumed that at the beginning of a trading day an economic agent can access to information about the income from the previous investment and the current economic state. Given this information, the agent invests a portion of the previous income in the production technology and consumes the rest. Depending on the investment and the economic state, the next random income is realized at the beginning of the next day. The next market state is also observed simultaneously. This cycle goes on. The agent’s objective is to maximize the discounted risk sensitive non-expected utility of consumption in the infinite time horizon.

A similar problem has been studied in [Bäuerle and Jaśkiewicz (2018)] assuming absence of transitions in the economic state. In other words the productivity shocks have been assumed to be i.i.d., instead of following Markovian dynamics. We extend the results of [Bäuerle and Jaśkiewicz (2018)] to include the regime switching scenarios, since many state of the art macroeconomic models consider Markov shocks in productivity rate. For example, [Mendoza (1991)] considered a real business cycles (RBC) model, where technological disturbances including interest-rate and productivity shocks were assumed to be governed by two-state Markov chain, (see Page 802 therein). [Stadler (1994)] discussed a RBC theory in which productivity shocks were supposed to follow a stationary Markov process, (see Page 1754 therein). [Van Nieuwerburgh and Veldkamp (2006)] assumed that the technology shock follows a two-state Markov switching process when discussing asymmetries in a RBC model. [Heutel (2012)] adopts a Markov process for modelling persistency in productivity shocks when investigating optimal environmental policies responding to business cycles. [Azzimonti and Talbert (2014)] supposed that an aggregate productivity shock was governed by a first-order Markov process when studying polarized business cycles. The Markov regime-switching model for optimal growth considered here can capture an important aspect of economic growth, namely the impacts of transitions in different phases of business cycles such as expansion and recession on the growth in an unified setting. Specifically, the model may provide theoretical insights into making investment-consumption decisions with the objective of achieving sustainability in the economic growth in the presence of changing economic regimes. We describe probabilistic transitions in economic regimes using a discrete-time, finite-state, Markov chain whose probability laws are given. To the best of our knowledge, this problem has not been studied in the literature.

For the sake of generality, in this paper, the production function and the utility function are allowed to be unbounded from above. We refer to [Bäuerle and Jaśkiewicz (2018)], [Durán(2003)], [Kamihigashi (2007)] and [Wessels (1977)] and references therein for similar considerations. We follow the weighted supremum norm approach for studying the optimization problem. As in [Hansen and Sargent (1995)] and [Bäuerle and Jaśkiewicz (2018)] the finite horizon objective function has been defined recursively. Its limiting value is then shown to exist which gives rise to the non-expected discounted utility in the infinite time horizon. We then study the corresponding optimality equation using the Banach fixed point theorem. To show that the dynamic programming operator maps a space of certain functions into itself, we consider the class of concave, non-decreasing and non-negative functions with weighted supremum norm as in [Bäuerle and Jaśkiewicz (2018)]. In [Bäuerle and Jaśkiewicz (2018)] the contraction property of the operator has been established by applying Chebyshev’s association inequality of random variables. We have first extended that association inequality to the regime switching case (see Lemma 4.4) and then applied the inequality for establishing the contraction mapping. Furthermore, it is shown that the optimal investment policy exists in the class of stationary policies.

The Euler equation for optimal consumption is also considered. An Euler equation generally states that the average gain in utility for saving now and then consuming in future, instead of immediate consumption should, after discounting, be equal to the utility gain of consuming now. The readers can find the study of Euler equation in [Brock and Mirman (1972)] and [Kamihigashi (2007)]. It is interesting to note that under the present settings for a nonzero risk aversion parameter, the Euler equation involves an expectation with respect to a probability measure different from the standard equilibrium market measure. Specifically, under an optimal consumption policy, the measure depends on the value function. Consequently, higher (lower) probabilities are assigned to the scenarios corresponding to smaller (larger) values of the value function. In view of this, such measures are also referred to as the worst-case measure (see [Hansen and Sargent (2007)]).

In addition to the above results, we have also established that, under additional assumptions, the joint process consisting the optimal income and the underlying economic state has a non-trivial joint stationary distribution. This is accomplished as an application of a result from [Meyn and Tweedie (2009)]. To facilitate the application of this result, we prove that the stochastic kernel of the joint process is Feller and bounded in probability.

Numerical results based on hypothetical parameter values in a parametric model with three regimes of the production rate are provided to illustrate the impacts of changes in the production rate regime on the optimal investment-income ratio and the value function. To this end, a regime switching extension of the Cobb–Douglas production function and the power utility is considered. The numerical results are presented graphically along with some insightful economical interpretations. In this connection a fair comparison is added between this and the fixed regime counter part examined in [Bäuerle and Jaśkiewicz (2018), Example 1]. Prior to choosing specific numerical values for computation, we identify the range of parameter values for which all the theoretical assumptions in this paper are fulfilled.

The rest of this paper is organized as below. In Section 2 we present the regime switching investment-consumption model for a single sector. The optimization problem is formulated in Section 3. In Section 4 the optimality equation of the value function is obtained. Moreover, the existence of the optimal stationary policy is also established. The Euler equation for optimal consumption is derived in Section 5. The establishment of the existence of the joint stationary distribution for the optimal income process and the underlying economic state is presented in Section 6. The numerical results and their interpretations for a natural regime switching extension of a model with Cobb–Douglas production function, coupled with a power utility are discussed in Section 7. We conclude the paper in Section 8 which contains some directions of future investigations. For the sake of self-containedness some results with proofs have been added at the end in the Appendix section.

2. Multiperiod Growth and Consumption Model

In this section, a Markov regime-switching extension to the stochastic optimal growth model with risk sensitive preferences in [Bäuerle and Jaśkiewicz (2018)] is provided. Firstly, some notations are defined. denote the set of positive integers. A complete probability space is considered on which all the random processes are defined. It is supposed that at each time epoch , an economic agent has an income of the amount and wishes to allocate the income between consumption and investment. Let and denote the consumption and investment at the time epoch , respectively. Assume that the investment is used as an input for production and that this input is a key factor influencing the output at the next time epoch , which gives rise to the income of the agent . Furthermore, it is supposed that the output is also influenced by the observable market regime at the time epoch , which is described by . To take account of random perturbation, it is assumed that the income dynamics are governed by the following regime dependent production equation:

Here is a sequence of independent and identically distributed (i.i.d.) random variables taking their values in with common distribution . Note that represents the random shock at the time epoch . is a discrete-time time-homogeneous Markov chain with a finite state space . The probability laws of the chain are described by a given transition probability matrix . The initial wealth is assumed to be drawn from a given distribution on . and

is a Markov regime-switching production function. We assume that the regime-switching production function possesses the following property.

-

(F1)

For every and for each the function is non-decreasing, continuous, concave, and for every the function is Borel measurable.

Note that the above assumption on the production function is reasonable because the non-decreasing property of the production function is due to the fact that the output does not decrease as the input increases; the concavity property of the production function is due to the diminishing marginal productivity; the Borel measurability of the production function is a technical property so that the expectation of the production function with respect to the random shock is well-defined.

Let denote the following closed lower triangle

Then the history process of the income-regime-investment till time is given by

where for all . The last constraint is due to the fact that every time, only the income is invested after subtracting a non-negative amount for consumption. Hence, the production input at the time epoch is constrained by the income at that time epoch. Let the set denote the set of all feasible histories till time . The Borel sigma field on be denoted by . An investment policy is a sequence where for each is a -measurable mapping so that . The collection of all investment policies is denoted by . A policy is said to be Markov if there exists a sequence of Borel measurable maps in

such that for every . A Markov policy is said to be stationary if there exists a fixed , so that for all .

Conventionally, we identify a stationary policy with the mapping . Thus the set of all stationary investment policies is also denoted by .

The utility function is assumed to be

-

(U1)

strictly concave, increasing, continuous at zero and

In addition to above, we assume that there exists a continuous function which is non-decreasing in the first variable for each such that,

-

(U2)

for a fixed constant

-

(F2)

for a fixed constant ,

where denotes the one-period discounting factor.

Remark 2.1.

If is a bounded utility, then (U2) and (F2) are trivially true with a constant function , and . However, for unbounded utility, (F2) puts a constraint on . For illustrating the feasibility of (U2)-(F2) in the unbounded utility case, we consider the following toy example. Let , and for all . Then (U2)-(F2) hold with , and for any .

Before ending this section we introduce few more notations which are essential for the subsequent sections. Often we write instead of , given in (U2)-(F2) for notational convenience. We define for each , using , the following space of functions

Thus for every , there exists a constant such that

The -norm of a Borel measurable function is defined as

| (2.1) |

Then, is a Banach space (see Proposition 7.2.1 in [Hernández-Lerma and Lasserre (1999)]), where

We further consider a closed subset of by

Clearly, is a complete convex metric space. As in [Bäuerle and Jaśkiewicz (2018)] we study maximization of the agent’s non-expected utility defined via the entropic risk measure in the infinite time horizon case. The objective function will be presented in the following section.

3. The Optimization Problem

For each and , let the map be given by

| (3.1) |

Some important properties of are listed below whose proofs are deferred to the Appendix.

Theorem 3.1.

Let . For each and ,

-

(i)

if , where is the zero function, i.e., for any and any ;

-

(ii)

is monotonic, i.e., if , then ;

-

(iii)

;

-

(iv)

is concave, i.e., for any ;

-

(v)

under (F2), for some constant ;

-

(vi)

As in [Hansen and Sargent (1995)] and [Bäuerle and Jaśkiewicz (2018)] we model the objectives of an economic agent recursively. In other words, we introduce the objective function using a sequence of operators given by

where as described in (F2) and .

Lemma 3.2.

Assume that the conditions (U2) and (F2) hold. Then

(i) is well defined, and

(ii) is monotone.

Proof.

The fact that the range of is indeed in can be verified in the following manner. Assuming (U2) and (F2) and using Theorem 3.1(v), we get for every and any , that

| (3.2) |

as is non-decreasing. Thus, the map

is well defined. Moreover, by Theorem 3.1 (ii) and using under (F2), we directly get that for and , i.e., is monotone. ∎

For any initial income , state and we define -stage total discounted utility

| (3.3) |

where for all . In particular .

Theorem 3.3 below generalizes some results for performance functionals in Section 2 of [Bäuerle and Jaśkiewicz (2018)] to a Markov regime-switching situation, where the performance functionals depend on the modulating Markov chain.

Theorem 3.3.

For every , and ,

(i) the sequence is non-decreasing and is non-negative;

(ii) and for each

(iii) exists for every , and

Proof.

The objective function , defined as compositions of , is non-negative due to the non-negativity of . Using Theorem 3.1(i) and the non-negativity of , clearly . Now by applying on both sides and using the monotonic property Lemma 3.2(ii), we get . That is . Thus (i) is true.

Since and , using (U2) and the non-decreasing property of the utility function we have

| (3.4) |

Since is monotonic (Lemma 3.2(ii)), we get an inequality by applying on both sides of (3.4). Then using (3.2) with , , and of course , we obtain

| (3.5) |

Recall that . Continuing this procedure, we finally derive that

| (3.6) |

From (i) and (ii), is non-decreasing and bounded from above and hence exists for every , and .

∎

The problem statement. For an initial income , state and policy the non-expected discounted utility in the infinite time horizon is given by

| (3.7) |

The aim of the economic agent is to find an optimal value (the so-called value function) of the non-expected discounted utility in the infinite time horizon and a policy for which

We conclude this section by the following remarks.

Remark 3.4.

If , then there exists such that for all . Consequently

Similarly we can prove that for every and

| (3.8) |

The above recursion generalizes the recursion for the performance functionals in Eq. (12) of [Bäuerle and Jaśkiewicz (2018)] to a Markov-regime-switching environment.

Remark 3.5.

The fact that the objective function is non-expected utility can be illustrated by further computation of . To this end we introduce the notation to denote the distribution of where for all . Let denote the expectation w.r.t. . Using these notations, we write below

Clearly for , the above expression cannot be written as a conditional expectation of an utility function.

4. Value Function and Optimal Stationary Policy

This section is dedicated for establishing the following theorem. This asserts that the non-expected discounted utility in the infinite time horizon (as defined in earlier section) can be maximized by a stationary investment policy. Moreover, the optimal utility value function and the optimal stationary policy can be obtained by solving a Bellman equation.

Theorem 4.1.

Assume (U1)-(U2) and (F1)-(F2). Then, the following statements are true.

-

(a)

There exists a unique function such that

(4.1) for each and . Moreover, is strictly concave for each .

-

(b)

Let be as in (4.1), then , given by

(4.2) is strictly concave, continuous and non-decreasing. There exists a unique such that

(4.3) Moreover, the functions and are continuous and non-decreasing for each .

-

(c)

for all and for all , i.e. there exists an optimal stationary policy .

Throughout this section we assume that (U1)-(U2) and (F1)-(F2) are satisfied. We start with a result that we shall use in many places. Before giving a proof for Theorem 4.1, several results are presented in the following lemmas and their proofs are provided.

Lemma 4.2.

Let and . Then, the function

is continuous, concave, non-decreasing and non-negative. Additionally if is strictly concave, is also strictly concave.

Proof.

Let us fix and . By (F1), for every , we have . Since, for each , is non-negative and non-decreasing,

Consequently, since , where is the Borel -field on is a probability space,

This implies that as involves composition of negative log function of an average of the above expression.

Furthermore, since by (F1), for every , the function is non-decreasing and, by definition of , is non-decreasing, for every , the composition is non-decreasing. Again as is decreasing, is an average of a family of decreasing functions. Finally as is also decreasing, , the composition of the two above decreasing functions is non-decreasing.

Since composition of continuous functions is continuous, by virtue of (F1), is continuous for every and . In addition to that . Hence, the dominated convergence theorem implies that is continuous.

In order to show the concavity of w.r.t. , let where . By (F1) for each and

holds. Since, is non-decreasing and concave in its first argument for each , we obtain, for each , and

Applying properties (ii) and (iv) in Theorem 3.1 respectively gives

| (4.4) |

Hence is concave in its first argument for each . Again, if is strictly concave, the inequality above (4) is also strict, implying the strict concavity of . ∎

Lemma 4.3.

Assume that is a non-decreasing function in its first argument for each such that is also non-decreasing for each . Then, for any the function is non-decreasing and continuous.

Proof.

First we note that is Lipschitz continuous uniformly in with a common constant 1. Indeed, as is non-decreasing, for ,

Next, since is non-decreasing, for ,

Thus . Hence is Lipschitz continuous with constant for all .

Lemma 4.4.

For each , let , be non-decreasing in . Furthermore, assume that one of and is constant w.r.t. . Then

Proof.

We fix and set , and where and are random variables on and with distributions and respectively. From their definitions, the aforementioned and functions are non-increasing in . Hence, we can invoke Proposition A.1 in the Appendix using the conditional expectation given . That gives

Moreover, and are independent as one of and is constant in . Consequently, by the tower property of conditional expectations, we get

Thus by summarising the above two inequalities

Hence, by taking on both sides we get the desired inequality. ∎

For any we define the operator as follows

| (4.5) |

for all and .

Lemma 4.5.

The operator maps into itself and is a contraction.

Proof.

We first show that for each . Indeed, by (U2), we obtain

| (4.6) |

By following the similar steps as in the proof of property (iii) in Theorem 3.1 we arrive at the following

| (4.7) |

Therefore using the above inequality (4)

Here in the last step we have used (F2). Hence by substituting the above into (4) and using the definition of -norm we obtain

Moreover, by (U1) and Lemma 4.2, for each , we have that is non-negative.

By (U1) and Lemma 4.2, the function is continuous. Moreover, the constrained correspondence set given by is compact valued, where is the power set of . Therefore, is continuous as a consequence of the Maximum Theorem [Sundaram (1996), pg. 235] provided is hemicontinuous. To show that the correspondence is hemicontinuous, we need to show that it is both upper and lower hemicontinuous. For showing the upper hemicontinuity let be an open neighbourhood of Then there exists such that

Select the neighborhood of . Then for all , and consequently

Thus the correspondence is upper hemicontinuous. To prove the lower hemicontinuity let and be an open set such that This implies that there exists such that . By selecting , observe that , and also for all , . Therefore,

As , for all . Hence is lower hemicontinuous. Consequently, is hemicontinuous. Next, since is increasing by (U1), we observe that for we have

for each . So is non-decreasing. We now show the concavity of . From (4.5) we get

| (4.8) |

for any . Let us fix , where and . Also let and denote the maximizer in (4.5), which exists due to the continuity of . Again, say) is in . Hence, by (U1) we obtain

| (4.9) |

Now combining (4.8) with (4.9) and (4) and utilizing the fact that are maximizers, in and respectively, we finally obtain

| (4.10) |

Hence we have proved that maps into itself. Now we prove that is a contraction on . Assume that Then, for every and ,

which follows from property (ii) in Theorem 3.1. Using the fact that and are non-decreasing in first variable and is constant in we apply Lemma 4.4 to assert that the above is less than or equal to

by (iii) in Theorem 3.1. By (F2) above is not greater than . By changing the roles of with we finally obtain

Again, from (F2), , and so . Consequently, is a contraction. This completes the proof. ∎

Proof of Theorem 4.1.

Part (a). Clearly, a solution of (4.1), if exists, is a fixed point of (as in (4.5)) and vice versa. The latter exists uniquely from Lemma 4.5 and the Banach fixed point theorem

applied to the operator .

Hence, (4.1) has a unique solution . In addition, note that (4) has strict inequality making strictly concave. Since and are identical, is strictly concave too.

Part (b). Due to the strict concavity of (Part (a)), , which is given by (4.2) is also strictly concave, continuous and non-decreasing by invoking an application of Lemma 4.2. Due to the strictly concavity, for each and ,

the set of maximizers on the right-hand side of (4.1) is a singleton. Hence, the multifunction becomes a unique function (say) that maximizes the right side of (4.1). Consequently (4.3) is true.

We now show to be continuous. To this end we first recall the applicability of Maximum Theorem which has been asserted in the proof of Lemma 4.5. As a further consequence of the Maximum Theorem the map , which gives the set of maximizers of , is compact valued and upper hemicontinuous.

As a singleton valued upper hemicontinuous function is continuous, is also a continuous function. Therefore, the optimal consumption strategy is also continuous in .

We fix two points Suppose there exists a such that . Then, using , which is true for every due to the strict concavity of , we get

By adding on both sides and rearranging

Using (4.1) and (4.3), clearly the left side is greater or equal to and the right side is less than or equal to . This leads to a contradiction. Hence we have proved by contradiction that for all and every .

Furthermore, observe that (4.1) can be re-written as follows

Recall that . Using (U1), the strict concavity of and arguments similar to the above, one gets that the optimal consumption strategy is also non-decreasing in for all .

Part (c). From (4.1) it follows that

| (4.11) |

for all , and . Let us set, for each , given by

Note that . In view of this, by letting be any investment policy, for any history (4.11) implies that

| (4.12) |

Consequently, since is monotone we get,

| (4.13) |

for . Since and is monotone for every we obtain

for any , and . Here the last equality follows from (3.3). Since the above is true for every , by (3.7), we get for any , and . Hence,

| (4.14) |

We next aim to establish the reverse inequality. Let be as in (4.3). We set such that for all . For convenience of notation we set and for any non-negative function , we define:

Then the right-hand side of (4.3) can be re-written as

for . Consequently, the equality (4.3) can be rewritten as follows:

| (4.15) |

Hence, by iterating the last equality times we get that

| (4.16) |

where denotes the -th composition of the operator with itself. Thus, (4.16) with property (ii) in Theorem 3.1 followed by (4) together with the Assumption (F2) yield that

| (4.17) | |||||

for and . Now by putting in Lemma 4.4, we have that

| (4.18) | |||||

where the second inequality is due to (4) and the Assumption (F2). Next combining the inequalities (26) and (27) gives:

| (4.19) | |||||

Now we repeat the above procedure as follows: from Lemma 4.3 (see also (3.8)) the function

is non-decreasing. Hence, making use again of Lemma 4.4 ( ), (4) and (F2) we get

| (4.20) |

By combining (4.19) and (4) we obtain that

Repeating this procedure, i.e., making use of Lemma 4.4 for the functions (by Lemma 4.3 it is non-decreasing) and for we finally deduce

| (4.21) |

Thus, letting in (4.21) and by noting that it follows that

| (4.22) |

5. Euler Equation for Consumption

The relation between the gain of utility of present consumption and the discounted expected value of that of the future consumption is expressed in Euler equation. The equation generally states that the gain in utility for saving now and then consuming in future, instead of immediate consumption should not, after discounting, be less or more than the utility gain of consuming now. This section is devoted to establish the Euler equation for optimal consumption. We impose additional conditions that guarantee differentiability of functions which are required in formulating the model.

-

(U3)

The function is continuously differentiable on

-

(U4)

where is the right-hand derivative of at .

-

(F3)

The function is continuously differentiable on , for each .

-

(F4)

for all and .

-

(F5)

For almost every w.r.t. , there is an investment such that for all where

Assumption (F5) together with concavity (F1) imply that -a.s. for every . This also implies, in view of (F4), for all for almost every w.r.t. .

Theorem 5.1.

Assume (U1)-(U4) and (F1)-(F5). Then, we have the following.

- (a)

-

(b)

For each , the functions and are increasing.

It is important to note that the above Euler equation for consumption involves the value function . This is not the case when the objective is to maximize the standard expected utility. It is evident that setting in ((a)) removes the dependence, and coincides with the well-known Euler equation for the model with the expected utility. We also note that for a nonzero , the right side involves an expectation w.r.t. a different probability measure that depends on the value function. In the subsequent lemmas we shall assume that the conditions (U1)-(U4) and (F1)-(F5) hold true.

Lemma 5.2.

Proof.

Let us fix . To prove (5.2), take any sequence as By Assumptions (F4) and (U1) and the fact that , we get from (4.3) that and hence from (4.2). Again, from (4.11), using non-negativity of , and Theorem 3.1(i), we get by setting . Consequently, by (ii) and (vi) of Theorem 3.1 and (4.2) we have

| (5.3) |

for all . Recall that from (U1), and that from (F4), . Then for any ,

Letting on both sides of above equality, we obtain that

| (5.4) |

Since and are concave and is increasing, the composition is concave and thus Lemma A.2 is applicable to as . As a result, the sequence in (5.4) is monotone increasing. As the integrands in (5) are uniformly bounded by 1, and is a finite measure, the integrals converge using the convergence of (5.4). To be more precise

| (5.5) |

It is evident from Assumption (F5) that there is a such that for all . Now due to the concavity of in , i.e., for all and , we get for all and . Thus . Hence by (U4) almost everywhere w.r.t. for each . Then the right side of (5.5) is positive infinity. Therefore exists as infinity. ∎

We recall that the optimal policy (as in (4.3)) is in for each . We show in the following lemma that for each , the optimal investment is neither zero nor complete . The proof is motivated from [Kamihigashi (2007), Lemma A.5].

Lemma 5.3.

Let be as in (4.3). Then, for any and .

Proof.

We define, for each , and

Then, since is an optimal policy, we have

| (5.6) |

Let if possible for a given , and . Then for , (5.6) gives

Letting yields . That is , a contradiction to Lemma 5.2. Thus for every and .

Now let if possible . Observe that, for , (5.6) gives

Letting yields , where is the left hand derivative of , which exists everywhere due to strict concavity of from Theorem 4.1(b). Utilizing , due to (U4). This gives , and this is a contradiction to the finiteness of which is implied by the strict concavity of from Theorem 4.1(b). Hence for every and . ∎

The proof of following Lemma is along the similar lines as the proofs of [Stachurski (2009), Proposition 12.1.18 and Corollary 12.1.19].

Lemma 5.4.

For each , the function is continuously differentiable on and for . Here .

Proof.

We first note that and exist by strict concavity of from part (a) of Theorem 4.1. Moreover, since is concave, for each , . Thus for proving differentiability, it is enough to show .

To this end we fix , . From Lemma 5.3 we have . Consequently, there exists an open neighborhood of zero with

Therefore, is defined where for all , is given by

as in the proof of Lemma 5.3. Since is optimal in Theorem 4.1 (c), we have for all . Then, it follows that,

| (5.7) |

By replacing by in (5), where is a sequence such that and , we obtain

Hence, by letting on the both sides of above inequality, and using the continuous differentiablility of , and continuity of in , we get . Next, by taking any sequence such that and , and using (5), we obtain

By taking limit on both sides of above inequality we get, as earlier, . Thus, as desired. Hence, the left and right derivatives are equal (implying differentiability of at ) to . Recall from Theorem 4.1 that gives the optimal consumption . This completes the proof. ∎

Proof of Theorem 5.1.

Note that by Theorem 4.1 (b), defined in Eq. (4.2) is strictly concave. Consequently, as in the proof of Lemma 5.4, the right-derivative and the left-derivative exist. Hence we are required to show their equality and the continuity of the derivative. To this end we set a new measure on the product space by

for each , and note that

Hence is a probability measure. Using the above and Theorem 3.1(iii) for any

Recall that, under the Assumptions (F1) and (F3), is concave, non-decreasing and continuously differentiable, in for each and . Furthermore, is concave and differentiable in by Lemma 5.4, for each . Hence using Mean Value Theorem we have

Thus, by combining above two inequalities, for each ,

Hence for and ,

| (5.8) |

Similarly for obtaining an estimate of the left-hand side derivative of we consider, for each ,

Hence, for and

| (5.9) |

Next, we claim that, for each , is continuous on . To see this, first we observe that the integrand is continuous in , thanks to Lemma 5.4, Assumptions (F1) and (F3). Again, due to the concavity of and (Assumption (F1) and part (a) of Theorem 4.1) and the non-decreasing property of in (Assumption (F1)), for all , where is an arbitrarily small positive number, and . Again, since,

we may apply the dominated convergence theorem to conclude that is continuous on . As is an arbitrary positive number, is continuous on .

Since is concave and (5.8) and (5.9) hold, then for such that , we obtain

| (5.10) |

Now letting in (5.10), continuity of yield that, for each , is continuously differentiable on and from the second statement of Lemma 5.4 we get

Hence is identical to the right side of ((a)). Again, as shown in Theorem 4.1, and Lemma 5.3 the policy is the maximizer of the map . Hence, the first-order condition with respect to gives that . Thus, by part (b) of Theorem 4.1, is also identical to the left side of ((a)).

This completes the proof of part (a).

In order to prove (b) suppose that We divide the proof in two sub-cases.

1) If then by Lemma 5.3 we have . Consequently, because , , where we have used the definition from Theorem 4.1(b). Hence part (b) holds for this sub-case.

2) We prove (b) for the sub-case by contradiction. Since on the right side of the Euler equation ((a)) the variable appears via only, we obtain , if we assume . But the equality cannot hold, since is strictly concave. Similarly, if then by the second statement of Lemma 5.4 we must have, for each , However, this equality contradicts the strict concavity of . Recall from Theorem 4.1(b) that the functions and are non-decreasing in , for each . Therefore, (b) holds true for every sub-case. ∎

6. Stationary Distributions

In this section, a dynamics of the growth is obtained when the economic agent follows a stationary policy. This along with the regime switching dynamics jointly become a discrete time Markov chain on product state space . Consider this Markov chain when the optimal stationary policy is followed by the economic agent. We recollect and redefine

| (6.3) |

where is independent of and i.i.d. random sequence, distributed as , a probability measure on .

Clearly, is a Markov chain with respect to the minimal sigma-field generated by . We also recall that due to (F5), for every , , and in , -a.e.. In addition to this, utilising the fact that for and , and the Assumption (F1) that is non-decreasing in for every and , we may confine ourselves to the study of the income process on .

In this section, we shall show the existence of at least one non-trivial stationary distribution of (6.3). To this end we first show that the system is globally stable under a set of assumptions. Next, following the approach of [Bäuerle and Jaśkiewicz (2018)] and references therein, we use the Euler equation ((a)) and the Foster-Lyapunov theory (see [Foster (1953), Meyn and Tweedie (2009)]) of Markov chains for showing the existence of a non-trivial stationary distribution.

We impose the following assumptions on the distribution of the random shock and the production function for pursuing the subsequent investigation.

-

(D1)

-

(D2)

There exist and such that

-

(D3)

The transition probability matrix is irreducible.

The term represents the production rate at when shock is and state is . This value is nonzero -a.e. due to (F5). Thus the integrand in Assumption (D1) is well defined. Clearly, (D1) precludes the situation where on an average the ratio of growth rates of ideal bank and the production is larger than one at every economic state. On the other hand, the role of Assumption (D2) is to preclude the situation where the average production rate is infinity. Moreover, since the state space is finite, (D3) ensures existence of a unique stationary distribution of the Markov chain , see [Serfozo (2009), Chapter 1].

Lemma 6.1.

Assume that (D1) holds. Then, for and , there exist and such that

Proof.

First note that is well-defined since by the Assumption (U1), the utility function is increasing. Next, by the Cauchy-Schwarz inequality, it follows that for each

| (6.4) |

Furthermore, substitution of ((a)) into (6) yields

| (6.5) |

as , and for each , due to (F1) and . Now from Assumption (D1) it follows that there exists and such that for every and . Again as , there is a such that . Hence

where is chosen as mentioned above. Since is non-decreasing (as due to Theorem 4.1(a)), for we have Consequently, by (6)

| (6.6) |

For and , since , the functions , , are non-decreasing, and , are non-increasing, we have for each

Using (6), the right side of above is bounded above by

| (6.7) |

The result follows from the estimates (6) and (6.7) combined together. ∎

Let us denote by the power set of . For a given , the measurable map , given by

| (6.8) |

Note that due to the Theorem 8.9 in [Stokey et al. (1989)] the above defined is the stochastic kernel of the Markov chain (6.3) on in our setting. In other words, the number is the probability that the economic system will move from state to some state in the set after one period of time. In the remaining part of this section we aim to show that is globally stable. To this end we need to establish some properties of this stochastic kernel. A stochastic kernel defines a linear operator from bounded measurable functions, on , to itself via the formula

The kernel is said to have the Feller property if, for each , is bounded and continuous whenever is, see [Chung and Walsh (2005)] for details. Since

due to the boundedness of and continuity of , direct application of dominated convergence theorem gives continuity of . Hence defined in (6) is Feller.

Let us denote the space of measures on by . A sequence is called tight if, for all , there exists a compact set such that for all , refer [Billingsley (1999)] for details. For given and we set and for

| (6.9) |

A stochastic kernel is said to be bounded in probability if the sequence is tight for all , and .

Lemma 6.2.

For each and the sequence , as in (6.9), is bounded in probability.

Proof.

We first note that the map given by

is coercive where is defined in Lemma 6.1. Indeed,

As , , and , from above, . Next we show that for all ,

| (6.10) |

with and , where and are as in Lemma 6.1, and and are as in (D2) Indeed, since , using Lemma 6.1 and Assumption (D2),

Hence, using (6.10) we get

By applying the above inequality repeatedly, we get

Thus we have as . Now we apply Lemma D.5.3 of [Meyn and Tweedie (2009)] to conclude that is bounded in probability. ∎

Theorem 6.3.

Assume that (U1)-(U4), (F1)-(F5) and (D1)-(D3) hold. Then there exists a non-trivial stationary distribution for the Markov chain in (6.3).

Proof.

Due to (D3) the finite-state Markov chain has a unique stationary distribution , say. Let be sampled from . Then using Lemma 6.2 and the Feller property of , the theorem follows as a direct application of Theorem 12.0.1 of [Meyn and Tweedie (2009)]. ∎

7. Numerical Experiment

In this section we show that the natural regime switching extension of a model with Cobb–Douglas production function coupled with a power utility would satisfy the assumptions presented in Sections 3 - 6. Further, we provide numerical results to illustrate a numerical approximation to the value function in Eq. (4.1) under a parametric model to be considered in Section 7.1 below and the impacts of introducing regime switches on the (approximate) value function and the optimal investment ratio as the income varies. Specifically, the (approximate) value function and the optimal investment ratio will be compared with their counterparts under the non-regime-switching model studied in [Bäuerle and Jaśkiewicz (2018), Example 1].

7.1. A parametric model

We consider the following example of regime switching extension of a model which has Cobb–Douglas production function

where is a given function defined on a finite set taking values in . Thus, it is clear that (F1) holds. Note that the income process in this case evolves as

where is an irreducible Markov chain with state space and transition probability matrix . Hence (D3) is true. As in [Bäuerle and Jaśkiewicz (2018), Example 1], we consider the power utility, i.e., with . Therefore, (U1) holds. Assumption (U2) holds for for any constant whose more suitable range will be set later for satisfying other assumptions. Furthermore, the random shocks and their reciprocals are assumed to have finite mean, i.e., and . For example, lognormal distributions possess this.

Next we check Assumption (F2). Let us fix the discount factor and income of an agent to . Then, for , we have,

| (7.1) |

Here the first inequality follows from the Jensen inequality for concave function ( for each ). So, for given , by dividing to both sides we get

| (7.2) |

Since iff , we consider two cases. If , then the right side of (7.2) is bounded above by . Since , (F2) holds true for every whenever . In the second case we consider the complementary region of income , i.e., . Then

| (7.3) |

Hence, for given one can choose such that satisfies . Thus for this choice of and , (F2) holds for all . It is straightforward to see that the Assumptions (U3)-(U4) and (F3)-(F5) also hold true.

The only remaining Assumptions (D1) and (D2) are examined below. To establish (D1), w.l.o.g. we can assume that . Then, since and for ,

But, due to our assumption of the finiteness of the right side expression of the second inequality above is integrable w.r.t. . Hence, the Dominated Convergence Theorem is applicable to . Thus by noting that for each ,

Therefore, (D1) is true. Using the fact that for any , for all ,

Thus (D2) holds with and .

7.2. Numerical values of parameters

The hypothetical values of the parameters are specified in this subsection. Specifically, we set and the risk sensitivity parameter . The distribution of the random shock is assumed to be the probability distribution function of a standard Lognormal distribution. A three-state Markov chain is considered, and the state space of the chain is assumed to be . The transition probability matrix and the parameters are taken as

From the specified numerical values for in the three different states, the regimes and are associated with the low and high production rate regimes, respectively provided the investment value is not too small. The power parameter of utility is taken as .

7.3. Computation of optimal investment

A numerical approximation of the solution to (4.1) for the parametric model as described in Subsections 7.1 and 7.2 is presented below. The proposed numerical method relies on the fact that the solution of (4.1) is the fixed point of the contraction (as in (4.5)) which is also the limit of repeated application of the operator on a fixed function in the Banach space. Starting with the zero function, we stop after third step of iteration to obtain a numerical approximation of the value function. More specific details are described below.

Under the assumption of , the integral w.r.t. in (4.1), is simply

where is the cdf of the standard lognormal distribution. This can be rewritten as . This is numerically approximated using the composite trapezoidal rule by considering 18 equally spaced consecutive sub-intervals of . The supremum w.r.t. on is approximated by the maximum of values obtained for 30 equi-spaced values of in 000The running time of the code in online Matlab compiler is nearly two minutes..

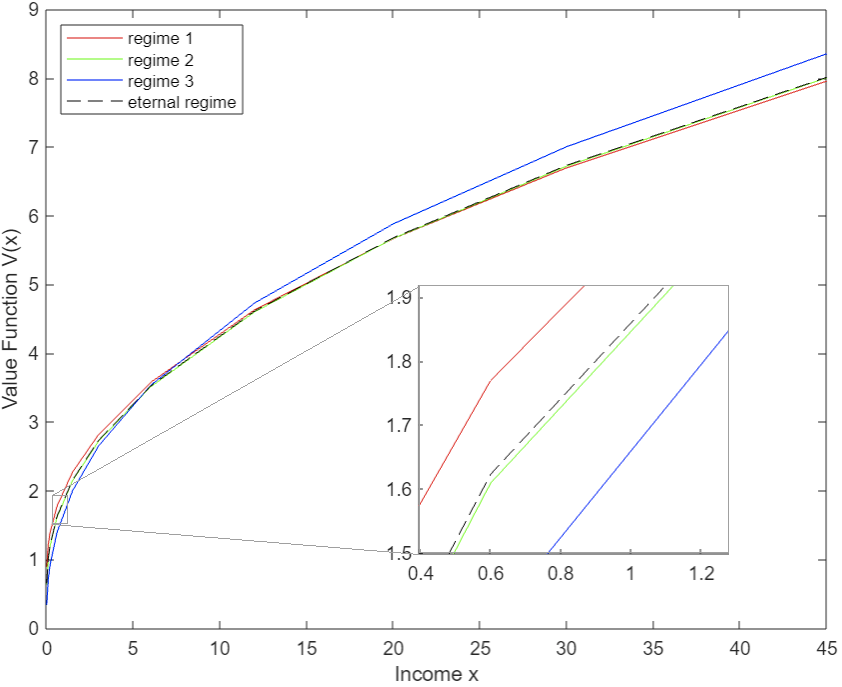

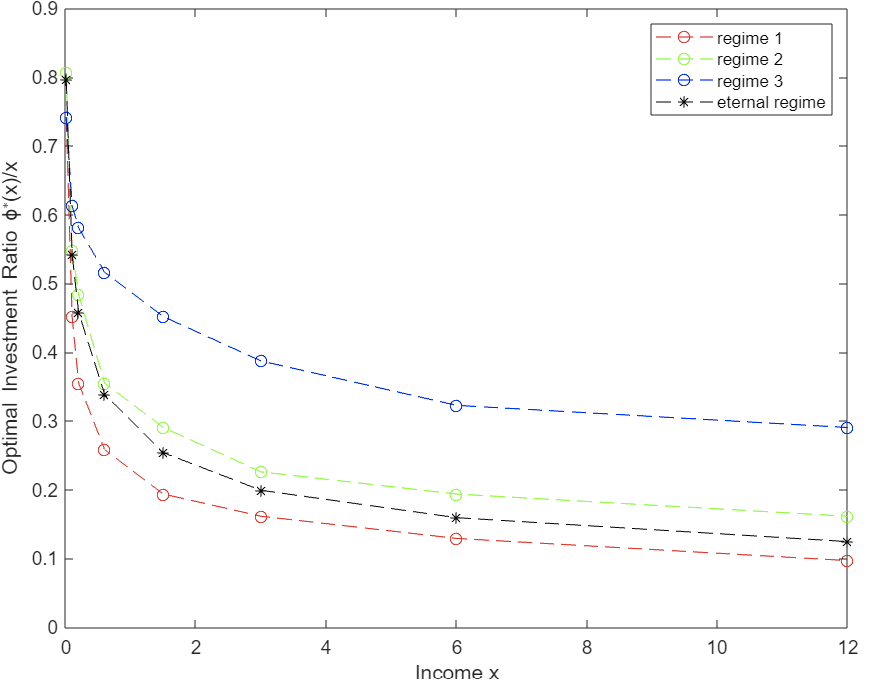

In Figure 1 the approximate value function is plotted along vertical axis against some specific values along horizontal axis for each value of . The line plots for , and are in red, green and blue colors respectively. The black broken line plot corresponds to the value function of a single-regime model with parameter values identical to those of regime 2. Similar color scheme is adopted in Figure 2, where the ratio of optimal investment and income (i.e., ) is plotted against income for each regime and eternal middle regime cases. The Matlab code, used in this paper, can be accessed from https://github.com/agiiser/Regime-Switching-Optimal-Growth-Model.

7.4. Interpretation

Figure 2, where the optimal investment ratios are plotted, illustrates an intuitive phenomena, namely, the investment ratios depend on the production rates. Specifically, from Figure 2, it can be seen that the optimal investment ratio curve shifts up when increases from 1 to 3 through 2, (i.e., the production rate increases from the lowest to the highest). This is consistent with the intuition that it may be optimal to invest more when the production rate is higher. It is also noted that for each fixed production rate regime , the optimal investment ratio decreases as the income increases. This reflects that the ratio of optimal consumption and income increases with hike of income. These are common features observed in the fixed/eternal regime models too. Now we discuss some other features which are specific to regime switches in the production rate only.

We first note that the stationary distribution of the regime switching dynamics in the numerical example is . This represents a typical scenario where the middle state is more likely than the extreme states on both sides. Furthermore, the transition to low or high production from the middle state is equally likely. Despite this symmetry in transition, influence of an extreme regime on the middle regime can be considered in the following scenario. In principle, if the production function parameters in low and high regimes are not similarly far from the middle regime, the one which is more extreme, should influence the investment decision at the middle regime too. This is verified with the numerical example under consideration. We note that the difference of the values of and is much larger than the difference of the values of and . As a result the influence of a higher production rate regime should also be observed in the middle production rate regime. This is indeed observed in Figure 2. The green line, for middle regime is found above the black line, which corresponds to the eternal middle regime with no chance of switching. Such influence is also seen in Figure 1. The value function at the middle regime deviates from that for eternal middle regime and moves towards the value function at third regime. The value function plots also exhibit standard features like monotonicity and concavity w.r.t. income. Also, for significantly large incomes, the value function shifts up when the production rate increases from the lowest regime to the highest regime. However, due to the very defining formula, such association of production function is reversed when investment is sufficiently small, which is the case when income is low. This explains the visible inflection of ordering of value function w.r.t. the regime order.

8. Conclusion

One can perhaps imagine a formulation of regime switching dynamics, that is different from ours, where

denotes the history at th time unit. In this case, the state of the market is only observed on the next day. This would also imply that the production function depends on two different sources of randomness, one described by i.i.d. () and another auto-correlated (). However, a stationary strategy in this setting depends solely on the income of the day as in [Bäuerle and Jaśkiewicz (2018)].

In yet another formulation, the market states may be unobserved but influences the production, and the scope of the policies are restricted to be those which are insensitive to the past market states. Then the past realizations of do not appear in the history process. This one appears as a minor generalization of the literature, where independent noise is replaced by a correlated noise only and rest are identical.

Apart from the above mentioned settings, the formulation of an incomplete information setting is also interesting where, is partially observed only via the realization of production function, and the optimization is not restricted to the state-insensitive policies.

Acknowledgement: We would like to sincerely thank Professor John Stachurski for insightful and valuable comments.

Appendix A

Proof of Theorem 3.1.

We note that the constant zero function belongs to . Furthermore, . Using monotonicity of expectation and reverse monotonicity of and , the first and second properties follow. Since is concave, using Jensen’s inequality

Hence the third property holds. For proving the fourth property we do the following. For each and , set

where is as in (U2) (F2). Then by the definition of the spaces and , for each , the map is in for each , . Let be given by

where is a probability mass function (pmf) on , and . We wish to establish concavity of the above function using the second order Fréchet derivative which is a map from to the space of all bilinear forms on .

By a direct calculation, along a pair of directions is given by

for any . Hence using the Cauchy-Schwartz inequality we get for every

for all . Thus is concave on . Moreover, for each , and , , where the pmf is . Hence is concave too. This completes the proof of (iv). The inequality in (v) follows from Theorem 3.1(iii) and (F2). Indeed, since and , we have

for any and Lastly, for , the assertion (vi) follows by taking and in assertion (iv) and then using (i). To prove the case we first apply the assertion (ii) with and , to get for each . Since, given a , , we get . Or . ∎

The following result can be found in [Devroye et al. (1996)] (Theorem A.19). We provide the proof here for making this self-contained.

Proposition A.1.

Let be a real-valued random variable defined on and let and be non-increasing real-valued measurable functions. Then,

provided that all expectations exist and are finite.

Proof.

As both and are non-increasing . Using this we obtain the following using two independent and identically distributed random variables and

Hence the proposition is true. ∎

The proof of the next result is a slight modification of [Kamihigashi (2007), Lemma 3.1] or [Stachurski (2009), Corollary 11.2.10].

Lemma A.2.

Let be a concave function such that . For every , we have

Proof.

Let such that . Then due to concavity of ,

∎

References

- [Azzimonti and Talbert (2014)] Azzimonti, M. and Talbert, M., Polarized business cycles, Journal of Monetary Economics 67 (2014), 47-61.

- [Bäuerle and Jaśkiewicz (2018)] Bäuerle, N. and Jaśkiewicz, A., Stochastic optimal growth model with risk sensitive preferences, J. Econ. Theory 173 (2018), 181-200.

- [Billingsley (1999)] Billingsley, P., Convergence of probability measures. Second edition. Second edition. A Wiley-Interscience Publication. John Wiley & Sons, Inc., New York, 1999.

- [Brock and Mirman (1972)] Brock, W.A. and Mirman, L., Optimal economic growth and uncertainty: the discounted case, J. Econ. Theory 4 (1972), 479-513.

- [Chung and Walsh (2005)] Chung, K.L. and Walsh, J. B., Markov Processes, Brownian Motion, and Time Symmetry. Springer, New York, 2005.

- [Devroye et al. (1996)] Devroye, L., Györfi, L. and Lugosi, G., A Probabilistic Theory of Pattern Recognition. Springer-Verlag, New York, 1996.

- [Durán(2003)] Durán, J., Discounting long-run average growth in stochastic dynamic programs, Econ. Theory 22 (2003), 395-413.

- [Foster (1953)] Foster, F. G., On the stochastic matrices associated with certain queueing processes, Ann. Math. Statistics 24 (1953), 355-360.

- [Hamilton (1989)] Hamilton, J. D., A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle, Econometrica. Econometrica 57 (1989), 357-384.

- [Hamilton (2016)] Hamilton, J. D., Macroeconomic Regimes and Regime Shifts. In Handbook of Macroeconomics, Volume 2A, Uhlig, H. and Taylor, J. (eds.), pp. 163-201. Amsterdam: Elsevier, 2016.

- [Hansen and Sargent (1995)] Hansen, L.P. and Sargent, T. J., Discounted linear exponential quadratic Gaussian control, IEEE Trans. Autom. Control 40 (1995), 968-971.

- [Hansen and Sargent (2007)] Hansen, L. P. and Sargent, T. J., Recursive robust estimation and control without commitment, J. Econ. Theory 136 (2007), 1–27.

- [Hernández-Lerma and Lasserre (1999)] Hernández-Lerma, O. and Lasserre, J. B., Further Topics on Discrete-Time Markov Control Processes. Springer-Verlag, New York, 1999.

- [Heutel (2012)] Heutel, G., How should environmental policy respond to business cycles? Optimal policy under persistent productivity shocks, Review of Economic Dynamics 15 (2012), 244-264.

- [Jaśkiewicz and Nowak (2011b)] Jaśkiewicz, A. and Nowak, A. S., Stochastic games with unbounded payoffs: applications to robust control in economics, Dyn. Games Appl. 1 (2011b), 253-279.

- [Kamihigashi (2007)] Kamihigashi, T., Stochastic optimal growth with bounded or unbounded utility and with bounded or unbounded shocks, J. Math. Econ. 43 (2007), 477-500.

- [Mendoza (1991)] Mendoza, E. G., Real business cycles in a small open economy, The American Economic Review 81 (1991), 797-818.

- [Meyn and Tweedie (2009)] Meyn, S. and Tweedie, R.L., Markov Chains and Stochastic Stability, Cambridge University Press, 2009.

- [Stadler (1994)] Wessels, J., Real business cycles, Journal of Economic Literature 32 (1994), 1750-1783.

- [Serfozo (2009)] Serfozo, R., Basics of applied stochastic processes. Springer-Verlag, Berlin, 2009.

- [Sundaram (1996)] Sundaram, Rangarajan. K., A first course in optimization theory. Cambridge University Press, 1996.

- [Stachurski (2009)] Stachurski, J., Economic Dynamics: Theory and Computation. MIT Press, 2009.

- [Stokey et al. (1989)] Stokey, N.L., Lucas, R.E. and Prescott, E., Recursive Methods in Economic Dynamics. Harvard University Press, Cambridge, MA, 1989.

- [Van Nieuwerburgh and Veldkamp (2006)] Van Nieuwerburgh, S. and Veldkamp, L., Learning asymmetries in real business cycles, Journal of Monetary Economics 53 (2006), 753-772.

- [Wessels (1977)] Wessels, J., Markov programming by successive approximations with respect to weighted supremum norms, J. Math. Anal. Appl. 58 (1977), 326-335.