Variation of Gini and Kolkata Indices with Saving Propensity in the Kinetic Exchange Model of Wealth Distribution: An Analytical Study

Abstract

We study analytically the change in the wealth () distribution against saving propensity in a closed economy, using the Kinetic theory. We estimate the Gini () and Kolkata ( indices by deriving (using ) the Lorenz function , giving the cumulative fraction of wealth possessed by fraction of the people ordered in ascending order of wealth. First, using the exact result for when we derive , and from there the index values and . We then proceed with an approximate gamma distribution form of for non-zero values of . Then we derive the results for and at and as . We note that for the wealth distribution becomes a Dirac -function. Using this and assuming that form for larger values of we proceed for an approximate estimate for centered around the most probable wealth (a function of ). We utilize this approximate form to evaluate , and using this along with the known analytical expression for , we derive an analytical expression for . These analytical results for and at different are compared with numerical (Monte Carlo) results from the study of the Chakraborti-Chakrabarti model. Next we derive analytically a relation between and . From the analytical expressions of and , we proceed for a thermodynamic mapping to show that the former corresponds to entropy and the latter corresponds to the inverse temperature.

I Introduction

The economic and financial systems exhibit emerging complex properties of many-body systems and, therefore inevitably, have caught the attention of physicists. Physicists have been studying complex systems for a very long time and have developed several successful models for them. The Kinetic theory, being the oldest and most successful theory of many-body systems, has been developed extensively in the context of income and wealth distribution in societies and applied to markets as a first step [1, 2].

In the Kinetic Exchange (KE) model with a uniform saving propensity of the agents, called the Chakraborti-Chakrabarti (CC) model [3, 2], we take a closed and conserved economic system with agents having a total amount of wealth, (here we have taken that ). These agents are allowed to interact with each other by exchanging their wealth, , through a two-agent money-conserving random stochastic trade process. Here, we have only considered the case where, at a any time , both the agents taking part in any of the binary interactions (trades) are chosen randomly from , and in addition to this, the agents save a constant fraction (saving propensity) of their wealth, during each exchange (CC model [3]). In any trade at time , the exchange of wealth of the th with that of the th agent can be expressed as

| (1) |

where is a stochastic fraction varying in every time () or interaction (trade). We intend to study how the resulting steady-state wealth distribution changes with the saving propensity . The inequality in the wealth distribution can be measured using the Lorenz function [4] , which gives the cumulative fraction of wealth possessed by fraction of the people ordered in ascending order of wealth (explained with greater detail in section II). Using , we can calculate two inequality measures or indices — Gini () [5] and Kolkata () [6, 7] (also explained with greater detail in section II). Numerical studies have been conducted to determine how the values of indices and vary with . In ref. [8], a numerical analysis shows that as increases, and decrease (for = 0 the index value for and , and for the index value for and ).

Patriarca, Chakraborti, and Kaski [9] assumed that the steady-state wealth distribution in the CC model could be represented well by a Gamma function and compared that with the Monte Carlo (MC) results. There have been extensive studies and also applications of this Gamma form for the income or wealth distribution in the KE models of markets (see for example [10, 11] for important recent applications and discussion on the approximation). In [12], a general expression for corresponding to this Gamma approximation of is given, but the -index still lacks an analytical expression.

In this paper, we study analytically the variation of the and indices against the saving propensity () of the agents, using the Gamma distribution form for the wealth distribution in the CC model. In section II, we introduce the basic quantities we study here. In section III, we derive the exact values for the and indices corresponding to and further, we make use of the Gamma function approximation to analytically calculate the values of the inequality measures corresponding to and . In section IV, using the results from [9] we make an assumption that for larger values of the wealth distribution remains as a Dirac -function and we proceed for an approximate estimate for centered around the most probable wealth (a function of ). This leads to an analytic form of and, consequently, of and for large values of . These analytical results for and at different values of are compared with the MC results for the CC model. Finally, in this section, we show that initial variation of with is linear. In section V, by integrating over , we expand the Gini index in powers of and compare it with the Landau expansion of the free energy functional in terms of the order parameter (see e.g., [13]). We use this to show that is equivalent to entropy and is equivalent to the inverse temperature. Finally in section VI, we summarize our work and end with some discussions.

II Basic Quantities

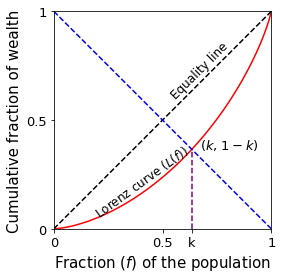

Inequality in society, in terms of wealth (also of income, votes, citations etc), is ubiquitous. We can measure the inequality in using the Lorenz function [4]

| (2) |

The equality line in Fig. 1 is formed by , when the wealth is distributed equally among all the agents. Using , we can calculate two inequality measures or indices — Gini () [5] and Kolkata () [6, 7]. The value of the index is given by the area between the Lorenz curve and the equality line, normalised by the area () under the equality line:

| (3) |

The index is given by the ordinate value of the intersecting point of the Lorenz curve and the diagonal perpendicular to the equality line. Since each point on the diagonal perpendicular to the equality line will have an abscissa value (say, ) equal to the compliment of the ordinate value (correspondingly, ), the point where this diagonal crosses the Lorenz curve, giving the -index value (see Fig. 1), has the self-consistent property

| (4) |

Defining the complimentary Lorenz function one can view the -index as its fixed point: . We can see from Fig. 1 that fraction of wealth is possessed by fraction of the richer population. The values , corresponds to equality and , corresponds to extreme inequality.

III Analytical results from the Gamma function approximation

In this section we will use the Gamma distribution model to derive the analytical results for and the inequality indices, corresponding to (), () and the limit ().

When , Patriarca et al. [9] gives us the following normalized Gamma function representation of :

| (5) |

with

and

| (6) |

III.1 Case ()

For a vanishing saving propensity (), as a consequence of the conservation of money, relaxes towards an exponential or Gibbs distribution in the steady-state [3, 14]. By putting into eqn. (5)

| (7) |

To calculate the , we first find the fraction of the population having money up to :

using and we get

Next we calculate the cumulative wealth of the population with maximum wealth up to :

giving finally (expressing in terms of )

| (8) |

From eqn. (3), for ), we get , giving and from eqn. (4), we get . From the numerical solution of this self-consistent equation, we get for the same case ( or ).

As may be seen from Fig. 2, using the MC simulation of the CC model with , we get and as compared to the analytical estimates here, and for ().

III.2 Case ()

Starting with eqn. (5), we consider the case of or and , giving

| (9) |

Next, we find the fraction of the population of people having wealth up to ;

Here denotes the Lambert -function (see [15, 16]) and by convention only two branches of , that is (known as the principle branch) and , are real valued. However, only for the value of lies between and and therefore we use . We then find the cumulative fraction of wealth of people having maximum wealth ;

In the above equation, when , and for , . Replacing in terms of we get the Lorenz function

| (10) |

Using thus Lorenz function in eqn 3 we get, , and from eqn 4 we get,

The numerical solution of this self-consistent equation gives .

As may be seen from Fig. 2, using MC simulation of the CC model with , we get and as compared to the analytical estimates here, and for ().

III.3 Case ()

For both the KE distribution and its Gamma approximation (with ) becomes Dirac function with . The fraction of the population having wealth up to is given by

Next we calculate , the cumulative wealth of the population with maximum wealth up to :

giving

| (11) |

For or , we get from eqn. (3). For deriving the -index value we use eqn 3 and we get , giving for the same case ( or ).

As may be seen from Fig. 2, using the MC simulation of the CC model with , we get and as compared to the analytical estimates here, and for ().

IV Results for and by expanding Lorenz function around the most probable value of wealth

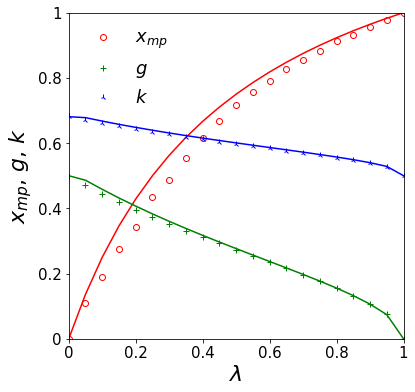

In this section, we derive analytically the inequality measure and for large values. We know [3] that as (at , the dynamics in the CC model stops) becomes a Dirac -function. Here, we assume that for , where , remains a Dirac -function centered at , where is maximum (i.e, where ). From eqn. (5) we can find as follows (using for )

This gives

Then the wealth distribution for , is given by

| (12) |

To calculate the , we first find the fraction of the population having money up to :

Next we calculate , the cumulative wealth of the population with maximum wealth up to :

giving

However, here has only a linear term in . To have minimal non-linearity required for and to satisfy the requirements and we write,

| (13) |

Now that we have , we can find . Since,

Hence we get,

| (14) |

For estimating we use eqn. (4) giving,

| (15) |

It may be interesting to note that, for eqn. (15) becomes , giving the value equal to (inverse of the Golden Ratio).

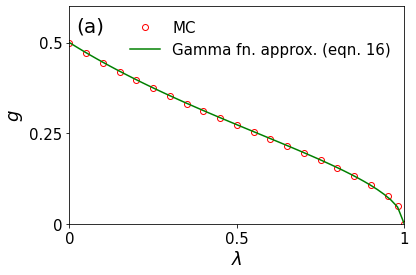

McDonald and Jensen [12] presented an analytic expression for from Gamma function (5) form of :

| (16) |

Here is given by the eqn. (6). In Fig. 3 (a), we have compared this analytical result with the MC result. From eqn. (14) we know that,

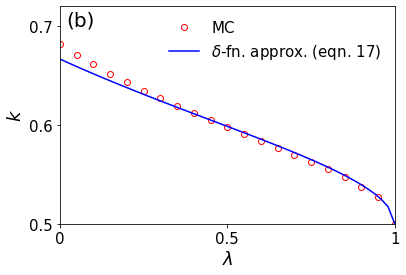

By substituting this and eqn (16) in eqn. (15), we obtain a general analytical expression for as

| (17) |

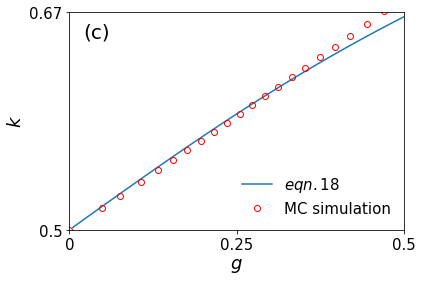

Here , a function of , is given by eqn. (6). In Fig. 3 (b), we can see how well this new result agrees with that obtained from the MC simulation.

In addition to this, by using eqn. (15) and , we derive a relationship between and

| (18) |

We can simplify this non-linear relationship by expanding the square root and neglecting the higher order terms of . This leads to a linear relationship

| (19) |

for the initial variations of with . We can see the same in Fig. 3, where the curve appears to be a straight line for smaller values of and this region has a slope of .

V Thermodynamic mapping of and indices

The -function approximation of the Gamma distribution in the CC model discussed in the earlier section can help us to map the and indices of the society to the entropy () and inverse of temperature () respectively (also the ordered population fraction , starting from the poorest, as the equivalent order parameter) of an equivalent thermodynamic system.

As we discussed in the earlier section IV, the Lorenz function in the limit can be approximated (see eqn.(13)) as,

| (20) |

with , giving and as required. From Fig. 1, one can express the in the Landau free energy (entropy) form (cf. [13]):

| (21) |

with indefinite integral over (arbitrary fluctuation in the order parameter) . We can now compare with the Landau free energy functional with order parameter (see for e.g. [13]). It may be noted that as is positive definite, the term in as the highest order term in (21) is enough to represent even the continuous (second order) transition in the effective Landau theory for the CC model.

Now consider (without any loss of generality) the expression for (in eqn. (21)) up to the quadratic term in and compare with that for Landau free energy [13] (as temperature approaches the transition temperature ) up to the term quadratic in the arbitrary fluctuation of the order parameter (, of which the equilibrium value in the range to will be determined by the minimization of ) as . This suggests , giving

| (22) |

This indicates that Gini index , where denotes entropy (see e.g. [17, 18]) in the CC model and that the Kolkata index , given by , or , or for large . Thus corresponds to the inverse temperature (see e.g., [19]). It may also be noted from eqn. (22) that since , the transition point occurs in the CC model when the saving propensity becomes . This is because the fluctuations in the order parameter here in the CC model is maximum (so are in and ) at and the fluctuations decrease continuously as increases, and they vanishes as approaches unity (where vanish and becomes corresponding to the equality line in Fig. 1).

VI Summary and Discussion

To summarize, we have studied analytically the variation of the Gini index () and the Kolkata index () against the saving propensity () of the agents, using Gamma distribution [9] ( form (5) with from (6)) for the wealth distribution in the Kinetic Exchange Chakraborti-Chakrabarti model [3]. The notion of wealth in this paper is a generalised one depending on the social context; it is a broad phrase that can be used for money (see e.g., [2] for application of CC model to money exchanges), social opinion formation and vote share (see the CC model application to social opinion formation where saving parameter is used as voters’ conviction parameter in [20, 21]), citations (see e.g., [22, 23] for the observed value of the initial slope for vs relationship for citation statistics, derived here analytically in sec. IV, eqn. (19) where the slope becomes ), and so on, and hence the results we obtained can be observed in all of these social contexts.

We start by deriving the exact results for and indices corresponding to and , as well as for in sections III and IV. This is achieved by assuming the wealth distribution in the CC model to be a Gamma distribution and using the -function approximation of it in the limit, and for other values of the derivation gets involved and requires the use of the generalized Lambert -function [16]. To avoid this, we concentrate on higher values of () and we assume (in section IV) the steady wealth distribution to be represented by a -function centred around the most probable income () and we find an approximate representation (13) for the Lorenz function . Using this expression for , we get the analytical results (14) and (15) for () and (). Using eqn. (16), we obtained the pre-factor , and then compared the MC results for and with those from the analytical results (14) and (15) in Fig. 3. Using this method, we were not only able to derive a general expression for , but we also derived a relationship between and , from which we were able to arrive at the conclusion that the initial variations of vs is a linear one with slope . This result (initial slope ) was also already observed in [22, 23] from analysis of various datasets, including income distributions of different countries, citation distributions of individual scientists, movie income distribution, votes share distribution among the candidates, etc. It may also be noted from eqn. (19) that for the case of extreme competition (when , see e.g., [7, 19]) one gets , corresponding to the rule of Pareto (see e.g., [2]).

Further, in section V, using this -function representation of the Gamma distribution (5) for , we obtained and compared the Gini function in (21) with the Landau free energy functional form . We then conclude that the Gini index () corresponds to free energy () or entropy (cf. [17, 18]) and the Kolkata index () corresponds to the inverse temperature of an equivalent thermodynamic system.

The Kinetic exchange model, where the agents have saving propensity (as in the CC model [3]), has been widely studied (see e.g., [10, 11] for recent discussions) and applied with some success in several realistic trade situations. The Gamma function representation [9] of the wealth distribution in the model allows us analytic formulation of the inequality indices like and for general values of , as discussed in sections III, and IV. The analytical expressions (14) and (15), for and respectively, allowed us to get their thermodynamic analogs (discussed in section V). As we have discussed earlier, many of our results here are already observed in Monte Carlo simulations (for example in [8]) as well as in data analysis (for example in [17, 18, 19, 22, 23]) reported elsewhere.

Acknowledgments

We are grateful to Suchismita Banerjee for her comments on the manuscript. We are extremely thankful to an anonymous referee for bringing the reference [12] to our notice. BJ is grateful to the Saha Institute of Nuclear Physics for the award of their Undergraduate Associateship. BKC is thankful to the Indian National Science Academy for their Senior Scientist Research Grant.

References

- [1] V. M. Yakovenko and J. Barkley Rosser, Colloquium: Statistical mechanics of money, wealth, and income, Rev. Mod. Phys. 81, 1703 (2009).

- [2] B. K. Chakrabarti, A. Chakraborti, S. R. Chakravarty, and A. Chatterjee, Econophysics of Income and Wealth Distributions (Cambridge University Press, 2013).

- [3] A. Chakraborti and B. K. Chakrabarti, Statistical mechanics of money: how saving propensity affects its distribution, The European Physical Journal B - Condensed Matter and Complex Systems 17, 167 (2000).

- [4] M. O. Lorenz, Methods of measuring the concentration of wealth, Publications of the American Statistical Association 9, 209 (1905).

- [5] C. Gini, Measurement of inequality of incomes, The Economic Journal 31, 124 (1921).

- [6] A. Ghosh, N. Chattopadhyay, and B. K. Chakrabarti, Inequality in societies, academic institutions and science journals: Gini and k-indices, Physica A: Statistical Mechanics and its Applications 410, 30 (2014).

- [7] S. Banerjee, B. K. Chakrabarti, M. Mitra, and S. Mutuswami, Inequality measures: The kolkata index in comparison with other measures, Frontiers in Physics 8, 540 (2020).

- [8] S. Paul, S. Mukherjee, B. Joseph, A. Ghosh, and B. K. Chakrabarti, Kinetic exchange income distribution models with saving propensities: Inequality indices and self-organised poverty lines, Phil. Trans. R. Soc. A. (accepted for publication; 2021), DOI: 10.1098/rsta.2021.0163.

- [9] M. Patriarca, A. Chakraborti, and K. Kaski, Statistical model with a standard distribution, Phys. Rev. E 70, 016104 (2004).

- [10] D. S. Quevedo and C. J. Quimbay, Non-conservative kinetic model of wealth exchange with saving of production, The European Physical Journal B 93, 186 (2020).

- [11] M. B. Ribeiro, Income Distribution Dynamics of Economic Systems: An Econophysical Approach (Cambridge University Press, 2020).

- [12] J. B. McDonald, and B. C. Jensen, An Analysis of Some Properties of Alternative Measures of Income Inequality Based on the Gamma Distribution Function, Journal of the American Statistical Association, 74, 368, (1979).

- [13] L. D. Landau and E. M. Lifshitz, Statistical Physics (Pergamon Press, 1958).

- [14] Dragulescu, A. and Yakovenko, V. M., Statistical mechanics of money, Eur. Phys. J. B 17, 723 (2000)

- [15] R. M. Corless, G. H. Gonnet, D. E. G. Hare, D. J. Jeffrey, and D. E. Knuth, On the lambert function, Advances in Computational Mathematics 5, 329 (1996).

- [16] I. Mező and Á. Baricz, On the generalization of the lambert function, Transactions of the American Mathematical Society 369, 7917 (2017).

- [17] T. S. Biró and Z. Néda, Gintropy: Gini index based generalization of entropy, Entropy 22, 879 (2020).

- [18] D. Koutsoyiannis and G. Sargentis, Entropy and wealth, Entropy 23, 1356 (2021).

- [19] A. Ghosh and B. K. Chakrabarti, Limiting value of the kolkata index for social inequality and a possible social constant, Physica A: Statistical Mechanics and its Applications 573, 125944 (2021).

- [20] M. Lallouache, A. S. Chakrabarti, A. Chakraborti, and B. K. Chakrabarti, Opinion formation in kinetic exchange models: Spontaneous symmetry-breaking transition, Phys. Rev. E 82, 056112, (2010).

- [21] P. Sen and B. K. Chakrabarti, Sociophysics: An Introduction, (Oxford University Press; 2021)

- [22] A. Chatterjee, A. Ghosh and B. K. Chakrabarti, Socio-economic inequality: Relationship between Gini and Kolkata indices, Physica A: Statistical Mechanics and its Applications, 466, (2016).

- [23] S. Banerjee, S. Biswas, B. K. Chakrabarti, A. Ghosh, R. Maiti, M. Mitra and D. R. S. Ram, Evolutionary Dynamics of Social Inequality and Coincidence of Gini and Kolkata indices under Unrestricted Competition, (2021), arXiv:2111.07516[physics.soc-ph]