Spectrahedral Regression

Abstract

Convex regression is the problem of fitting a convex function to a data set consisting of input-output pairs. We present a new approach to this problem called spectrahedral regression, in which we fit a spectrahedral function to the data, i.e. a function that is the maximum eigenvalue of an affine matrix expression of the input. This method represents a significant generalization of polyhedral (also called max-affine) regression, in which a polyhedral function (a maximum of a fixed number of affine functions) is fit to the data. We prove bounds on how well spectrahedral functions can approximate arbitrary convex functions via statistical risk analysis. We also analyze an alternating minimization algorithm for the non-convex optimization problem of fitting the best spectrahedral function to a given data set. We show that this algorithm converges geometrically with high probability to a small ball around the optimal parameter given a good initialization. Finally, we demonstrate the utility of our approach with experiments on synthetic data sets as well as real data arising in applications such as economics and engineering design.

Keywords: convex regression, support function estimation, semidefinite programming, approximation of convex bodies.

1 Introduction

The problem of identifying a function that approximates a given dataset of input-output pairs is a central one in data science. In this paper we consider the problem of fitting a convex function to such input-output pairs, a task known as convex regression. Concretely, given data , our objective is to identify a convex function such that for each . In some applications, one seeks an estimate that is convex and positively homogenous; in such cases, the problem may equivalently be viewed as one of identifying a convex set given (possibly noisy) support function evaluations. Convex reconstructions in such problems are of interest for several reasons. First, prior domain information in the context of a particular application might naturally lead a practitioner to seek convex approximations. One prominent example arises in economics in which the theory of marginal utility implies an underlying convexity relationship. Another important example arises in computed tomography applications in which one has access to support function evaluations of some underlying set, and the goal is to reconstruct the set; here, due to the nature of the data acquisition mechanism, the set may be assumed to be convex without loss of generality. A second reason for preferring a convex reconstruction is computational – in some applications the goal is to subsequently use as an objective or constraint within an optimization formulation. For example, in aircraft design problems, the precise relationship between various attributes of an aircraft is often not known in closed-form, but input-output data are available from simulations; in such cases, identifying a good convex approximation for the input-output relationship is useful for subsequent aircraft design using convex optimization.

A natural first estimator one might write down is:

| (1) |

There always exists a polyhedral function that attains the minimum in (1), and this function may be computed efficiently via convex quadratic programming [19, 20, 22]. However, this choice suffers from a number of drawbacks. For a large sample size, the quality of the resulting estimate suffers from over-fitting as the complexity of the reconstruction grows with the number of data points. For small sample sizes, the quality of the resulting estimate is often poor due to noise. From a statistical perspective, the estimator may also be suboptimal [15, 16]. For these reasons, it is of interest to regularize the estimator by considering a suitably constrained class of convex functions.

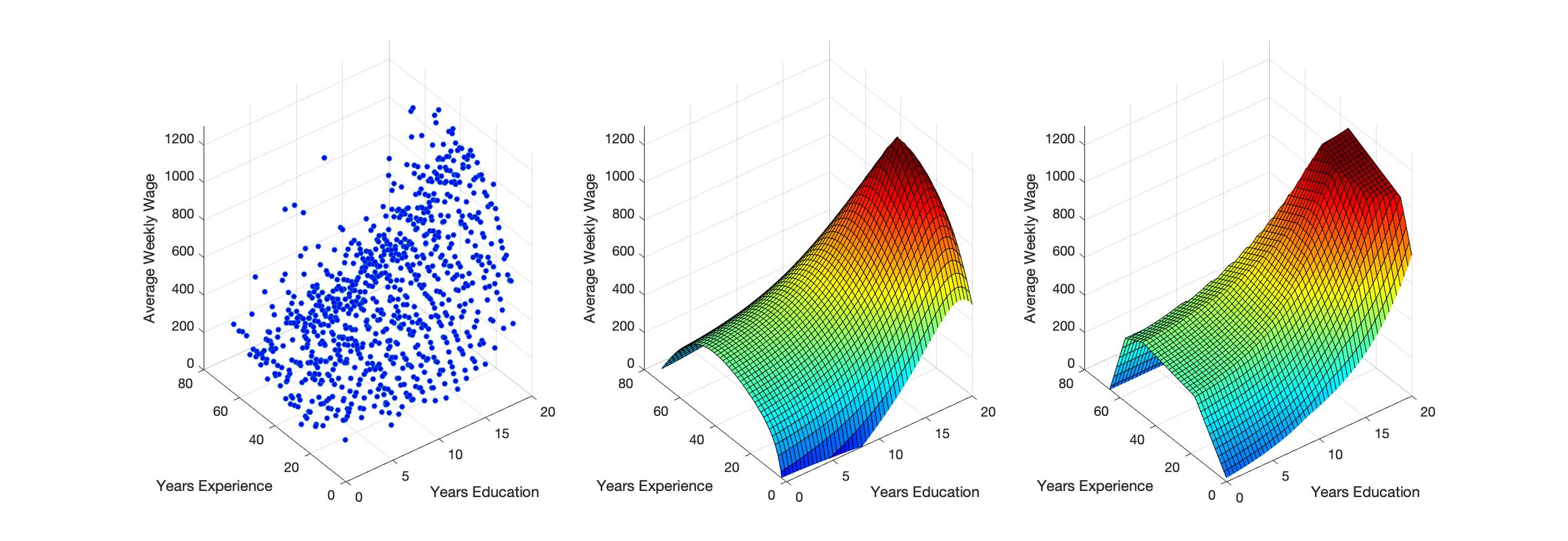

The most popular approach in the literature to penalize the complexity of the reconstruction in (1) is to fit a polyhedral function that is representable as the maximum of at most affine functions (for a user-specified choice of ) to the given data [9, 10, 12, 18, 25], which is based on the observation that convex functions are suprema of affine functions. However, this approach is inherently restrictive in situations in which the underlying phenomenon is better modeled by a non-polyhedral convex function, which may not be well-approximated by -polyhedral functions. Further, in settings in which the estimated function is subsequently used within an optimization formulation, the above approach constrains one to using linear-programming (LP) representable functions. See Figure 1 for a demonstration with economic data.

To overcome these limitations, we consider fitting spectrahedral functions to data. To define this model class, let denote the set of real symmetric matrices that are block diagonal with blocks of size at most , with dividing .

Definition 1.

Fix positive integers such that divides . A function is called -spectrahedral if it can be expressed as follows:

where . Here is the largest eigenvalue of a matrix.

An -spectrahedral function is convex as it is a composition of a convex function with an affine map. For the case , the matrices are all diagonal and we recover the case of -polyhedral functions. The case corresponds to second-order-cone-programming (SOCP) representable functions, and the case utilizes the expressive power of semidefinite programming (SDP). In analogy to the enhanced modeling power of SOCP and SDP in comparison to LP, the class of -spectrahedral functions is much richer than the set of -polyhedral functions for general . For instance, when this class contains the function . For estimates that are -spectrahedral, subsequently emplying them within optimization formulations yields optimization problems that can be solved via SOCP and SDP.

An -spectrahedral function that is positively homogenous (i.e., in the definition above) is the support function of a convex set that is expressible as the linear image of an -spectraplex defined, for positive integers and such that divides , by

| (2) |

We refer to the collection of linear images of as -spectratopes. Again, the case corresponds to the -simplex, and the corresponding linear images are -polytopes. Thus, in the positively homogenous case, our proposal is to identify a linear image of an -spectraplex to fit a given set of support function evaluations. We note that the case was recently considered in [24], and we comment in more detail on the comparison between the present paper and [24] in Section 1.2.

1.1 Our Contributions

We consider the following constrained analog of (1):

| (3) |

Here the parameters are specified by the user.

First, we investigate in Section 2 the expressive power of -spectrahedral functions. Our approach to addressing this question is statistical in nature and it proceeds in two steps. We begin by deriving upper bounds on the error of the constrained estimator (3) (under suitable assumptions on the data supplied to the estimator (3)), which entails computing pseudo-dimension of a set that captures the complexity of the class of spectrahedral functions. As is standard in statistical learning theory, this error decomposes into an estimation error (due to finite sample size) and an approximation error (due to constraining the estimator (3) to a proper subclass of convex functions). We then compare these to known minimax lower bounds on the error of any procedure for identifying a convex function [9, 25]. Combined together, for the case of fixed (as a function of ) we obtain tight lower bounds on how well an -spectrahedral function can approximate a Lipschitz convex function over a compact convex domain, and on how well a linear image of an -spectraplex can approximate an arbitrary convex body (see Theorem 8). To the best of our knowledge, such bounds have only been obtained previously in the literature for the case , e.g., how well -polytopes can approximate arbitrary convex bodies [3, 5].

Second, we investigate in Section 3 the performance of an alternating minimization procedure to solve (3) for a user-specified . This method is a natural generalization of a widely-used approach for fitting -polyhedral functions, and it was first described in [24] for the case of positively homogenous convex regression with . We investigate the convergence properties of this algorithm under the following problem setup. Consider an -spectrahedral function . Assuming that the covariates are i.i.d. Gaussian and each for i.i.d. Gaussian noise , we show in Theorem 10 that the alternating minimization algorithm is locally linearly convergent with high probability given sufficiently large . A key feature of this analysis is that the requirements on the sample size and the assumptions on the quality of the initial guess are functions of a ‘condition number’ type quantity associated to , which (roughly speaking) measures how changes if the parameters that describe it are perturbed.

1.2 Related Work

There are three broad topics with which our work has a number of connections, and we describe these in detail next.

First, we consider our results in the context of the recent literature in optimization on lift-and-project methods (see the recent survey [6] and the references therein). This body of work has studied the question of the most compact description of a convex body as a linear image of an affine section of a cone, and has provided lower bounds on the sizes of such descriptions for prominent families of cone programs such as LP, SOCP, and SDP. This literature has primarily considered exact descriptions, and there is relatively little work on lower bounds for approximate descriptions (with the exception of the case of polyhedral descriptions). The present paper may be viewed as an approximation-theoretic complement to this body of work, and we obtain tight lower bounds on the expressive power of -spectrahedral functions (and on linear images of the -spectraplex) for bounded .

Second, recent results provide algorithmic guarantees for the widely used alternating minimization procedure for fitting -polyhedral functions [7, 8]; this work gives both a local convergence analysis as well as a dimension reduction strategy to restrict the space over which one needs to consider random initializations. In comparison, our results provide only a local convergence analysis, although we do so for a more general alternating minimization procedure that is suitable for fitting general -spectrahedral functions. We defer the study of a suitable initialization strategy to future work (see Section 5).

Finally, we note that there is prior work on fitting non-polyhedral functions in the convex regression problem. Specifically, [13] suggests various heuristics to fit a log-sum-exp type function, which may be viewed as a ‘soft-max’ function. However, these methods do not come with any approximation-theoretic or algorithmic guarantees. In recent work, [24] considered the problem of fitting a convex body given support function evaluations, i.e., the case of positively homogenous convex regression, and proposed reconstructions that are linear images of an -spectraplex; in this context, [24] provided an asymptotic statistical analysis of the associated estimator and first described an alternating minimization procedure that generalized the -polyhedral case, but with no algorithmic guarantees. In comparison to [24], the present paper considers the more general setting of convex regression and also allows for the spectrahedral function to have additional block-diagonal structure, i.e., general -spectrahedral reconstructions. Further, we provide algorithmic guarantees in the form of local convergence analysis of the alternating minimization procedure and we provide approximation-theoretic guarantees associated to -spectrahedral functions (which rely on finite sample rather than asymptotic statistical analysis).

1.3 Notation

For , we define for the linear pencil . The usual vector norm is denoted and the sup norm by . The matrix Frobenius norm is denoted by , and the matrix operator norm by . We denote by the ball in centered at with radius .

2 Expressiveness of spectrahedral functions via statistical risk bounds

In this section, we first obtain upper bounds on the risk of the -spectrahedral estimator in (3) decomposed into the approximation error and estimation error. We then compare this upper bound with known minimax lower bounds on the risk for certain classes of convex functions. This provides lower bounds on the approximation error of -spectrahderal functions to these functions classes.

2.1 General Upper Bound on the Risk

To obtain an upper bound on the risk of the estimator (3), we use the general bound obtained in [10, Section 4.1]. To give the statement, consider first the following general framework. Let be observations satisfying

| (4) |

for a function contained in some function class . We assume the errors are i.i.d. mean zero Gaussians with variance . Now, let be a collection of function classes of growing complexity with . For each , define the constrained least squares estimator

We consider the risk of this estimator in the random design setting111One can also consider the risk in the fixed design setting, where one assumes the covariates are fixed, and risk bounds proved in [10] include this case. The results in this work can be directly extended to this case as well by applying the corresponding results., where we assume are i.i.d. random vectors in with distribution . The risk is then defined by

Additionally, assume that both and are uniformly bounded by a positive and finite constant .

As is standard in the theory of empirical processes, the rate is determined by the complexity of the class , which in this case is determined by the pseudo-dimension of the set

| (5) |

Recall that the pseudo-dimension of subset , denoted by Pdim(), is defined as the maximum cardinality of a subset for which there exists such that for every , one can find with for and for .

Theorem 4.2 in [10], stated below, provide an upper bound on the risk of split into approximation error and estimation error.

Theorem 2.

Let . Suppose there is a constant such that . Then, there exists an absolute constants such that

| (6) |

The -spectrahedral estimator (3) is a special case of the estimator when is the class of convex functions and is the class of -spectrahedral functions as in Definition 1, denoted by . Since the class is parameterized by matrices in , we define for each and ,

| (7) |

and define the -spectrahedral estimator of by

We also define the estimator when is the class of support functions of convex bodies (compact and convex subsets) in , denoted by , and is the subclass consisting of positively homogeneous -spectrahedral functions, or equivalently, support functions of -spectratopes. This corresponds to the case when the offset matrix . In this setting, we assume we are given observations satisfying

where , , is the support function of a set . We denote the class of -spectratopes, or linear images of in by . To define the -spectratope estimator, let

and define

For support function estimation, we notate the risk in terms of the convex bodies. Letting denote the probability distribution on of , we define the risk

In the following lemma, we prove an upper bound on the pseudo-dimension of the relevant set (5) needed to apply Theorem 2 for the estimators and .

Lemma 3.

For such that divides , define for ,

and for ,

Then, there exists absolute constant such that

To prove the lemma, we need the following known result (see for instance, Lemma 2.1 in [1]):

Proposition 4.

Let be fixed polynomials of degree at most in variables for . The number of distinct sign vectors that can be obtained by varying is at most .

Proof.

(of Lemma 3) Assume that the pseudo-dimension of is . By the definition of pseudo-dimension, the size of the collection of sign vectors

must be at most . For each ,

where is the determinant of the principal submatrix of . Indeed, if and only if all of these determinants are non-negative. Thus, the size of is the same size of

where for each , is a piecewise polynomial in . To bound the size of , we use the idea from [1]. We can partition into at most regions over which the vector is coordinate-wise a fixed polynomial. Then we apply Proposition 4.

We have polynomials of degree at most in up to variables, i.e. the number of degrees of freedom of -block matrices. Thus, the number of distinct sign vectors in satisfies . This implies that , and hence

The second claim follows similarly, where instead . ∎

We can now obtain an upper bound on the risk of the estimators and . Recall that we assume and functions in are uniformly bounded by some , and for support function estimation we assume and elements of are contained in .

Theorem 5.

-

(i)

For any convex function , there exist absolute constants and such that

-

(ii)

For any convex body in ,

2.2 Minimax Rates

The minimax risk for estimating a function in the class from in the random design setting is defined by

In Table 1 we summarize known rates as of this minimax risk for certain sub-classes of convex functions. First consider the class of functions in with compact and convex domain . In this case, the approximation error in the risk bound is zero and the rate of convergence is . This is the best rate we can achieve when the domain satisfies a certain smoothness assumption (see [10, Theorem 2.6]) and also appealing to the fact that . Otherwise, the best lower bound we have is using standard arguments for parametric estimation.

Additionally we consider two non-parametric sub-classes of convex functions. First is Lipschitz convex regression, where we assume the true function belongs to the class of -Lipschitz convex functions with convex and compact full-dimensional support . Second is support function estimation, where we assume the true function is the support function of a set belonging to the collection of convex and compact subsets of contained in the ball for some finite . In both settings, the usual LSE over the whole class is minimax sub-optimal [15, 16], necessitating a regularized LSE to obtain the minimax rate.

2.3 Approximation Rates

For Lipschitz convex regression, Lemma 4.1 in [25] implies the following: for ,

| (8) |

For support function estimation, let denote the Hausdorff distance between any and in . A classical result of Bronshtein (see Section 4.1 in [3]) implies that

| (9) |

This result is also the core of the proof of (8).

We first show that inserting (8) and (9) into Theorem 5 and optimizing over gives general upper bounds on the risk for our -spectrahedral estimators. These rates match the minimax rate up to logarithmic factors for fixed , and even when is allowed to depend logarithmically on .

Corollary 6.

Suppose for a non-decreasing and differentiable function .

-

(a)

(Lipschitz convex regression) Suppose and define the function

Then, for ,

(10) -

(b)

(Support function estimation) Suppose and define the function

Then, for ,

(11)

We now provide two specific examples for particular functions :

-

(i)

If for fixed and , then

and

-

(ii)

If , then , and

and

Indeedn, the inverse of is , where is the Lambert W function. The bound then follows from the fact that satisfies and as , .

Remark 7.

Proof.

As stated previously, an important observation from Corollary 6 is that when is a fixed constant that does not depend on , the risk bounds for an optimal choice match (up to logarithmic factors) the minimax lower bounds of the classes and . This indicates that the approximation error for the classes and for fixed cannot be improved from what was used in the proof. Indeed, this statistical risk analysis provides the following main result of this section: approximation rate lower bounds for the parametric classes and .

Theorem 8.

Suppose there exists an absolute constant and such that for all large enough. Let . For all , for all large enough,

Also, let . For all , for all large enough,

Remark 9.

Proof.

We argue by contradiction. Suppose that for all ,

for some constant (that may depend on and ) and fixed . Then by Theorem 5, there exist constants , such that

The infimum on the right side is achieved at , and thus

For this inequality to hold for all , it must be that , a contradiction. The second statement is proved similarly. ∎

3 Computational Guarantees

3.1 Alternating Minimization Algorithm

We now describe an alternating minimization algorithm to solve the non-convex optimization problem (3). Let for each and let be the true underlying parameters. That is, for each , we observe

We assume the ’s are i.i.d. mean zero Gaussian noise with variance .

One step of the algorithm starts with a fixed parameter . Then, compute the maximizing eigenvector , , such that for , . With the ’s fixed, update by solving the linear least squares problem:

| (12) |

where .

Input: Collection of inputs and outputs ; initialization

Algorithm: Repeat until convergence

Step 1: Update optimal eigenvector

Step 2: Update by solving (12). , where .

Output: Final iterate

3.2 Convergence Guarantee

The following result shows that under certain conditions, this alternating minimization procedure converges geometrically to a small ball around the true parameters given a good initialization. To state the initialization condition in the result, we define for the similarity transformation for an orthogonal matrix . Note that the eigenvalues of for are invariant under any . In the following we only consider the setting where , and denote .

The proof of the following result appears after the statement and it depends on multiple lemmas that we state and prove in the appendix.

Theorem 10.

Assume is a standard Gaussian random vector in and let . Also suppose that the true parameter satisfies the following spectral condition:

| (13) |

where and is the second largest eigenvalue. Let . There exist constants , such that if the initial parameter choice satisfies

for some similarity transformation and

then the error at iteration satisfies

with probability greater than .

Remark 11.

The assumption (13) is not always satisfied, but we provide some examples where it is. First, consider the case where , and are non-commutative matrices, and . Let . In this case the eigengap is

This follows from the computation of eigenvalues using the characteristic polynomial and the quadratic formula. We see that for any and such that , the eigengap is a strictly positive number. For example, if and , then

Another set of parameters that satisfy condition (13) is when . In fact, for any spectrahedral function that is differentiable for all , must necessarily satisfy (13).

Proof.

First, given assumption (13), we show that for large enough, for all parameters satisfying for some similarity transform ,

| (14) |

the parameter obtained after applying one iteration of the algorithm satisfies

| (15) |

with high probability.

Let be such that . The update then equals

where . Note that . Throughout the rest of the proof, we sometime abuse notation and consider the Kronecker product for and to be the vector .

By the invariance for all , without loss of generality we can assume in the following that for the transformation satisfying assumption (14). Let and be such that for ,

Also denote by the orthogonal projection matrix onto the span of the columns of . Then, we have the following deterministic upper bound:

Now, since ,

We also have the lower bound . Thus,

| (16) |

where .

Lemmas 12 and 13 then imply the following. For , there exist absolute constants such that if , then with probability greater than ,

| (17) |

for all satisfying assumption (14). Since is convex function, Jensen’s inequality implies

Then, by the definition of the Kronecker product,

Next note that , where , and . Then, by a variation of the Davis-Kahan Theorem (Corollary 3 in [28]),

Putting the bounds together and using assumption (14),

| (18) |

Plugging the bound (3.2) into (17) gives

| (19) |

Also by Lemmas 12 and 13 if , then with probability greater that ,

| (20) |

for all satisfying (14). We then have the following lower bound:

| (21) |

Plugging the bound (3.2) into (20) gives

| (22) |

and finally combining (19) and (22) with (3.2) implies

It remains to bound the error term. For this, we apply Lemma 14, which says that there exist constants such that

for all satisfying (14) with probability greater than .

This implies that for , with probability ,

We now show that given the above upper bound, also satisfies (14). Indeed, for

we have

and thus

The final conclusion follows from the fact that after iterations, applying the bound (15) times gives

and all bounds hold simultaneously with probability at least . ∎

4 Numerical Experiments

In this section, we empirically compare spectrahedral and polyhedral regression for estimating a convex function from data. More specifically, we compare -spectrahedral estimators to -polyhedral estimators, both of which have degrees of freedom per dimension. For each experiment, we apply the alternating minimzation algorithm with multiple random initializations, and the solution that minimizes the least squared error is selected. We adapted the code [23] for support function estimation used in [24] for spectrahedral regression.

4.1 Synthetic Regression Problems

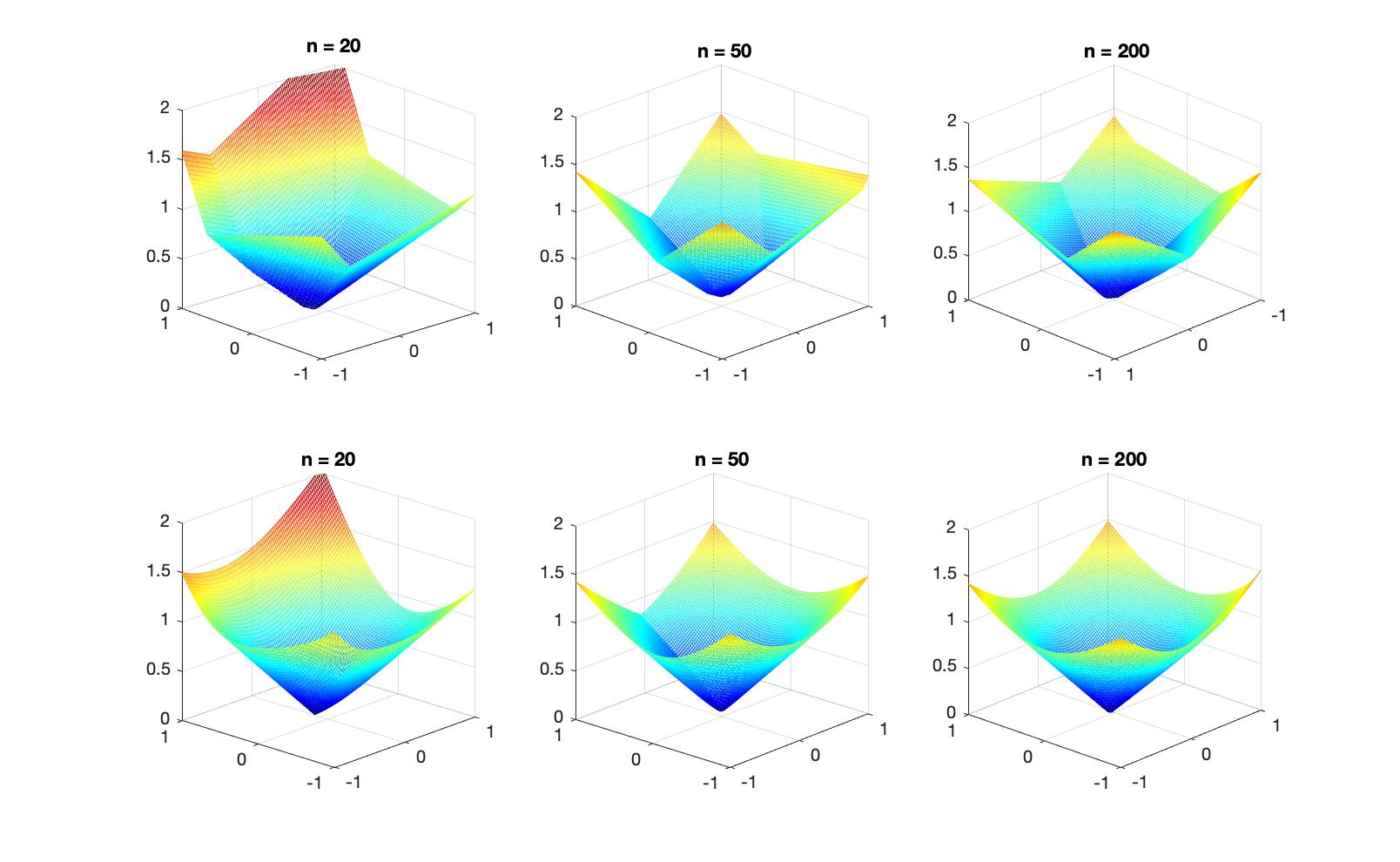

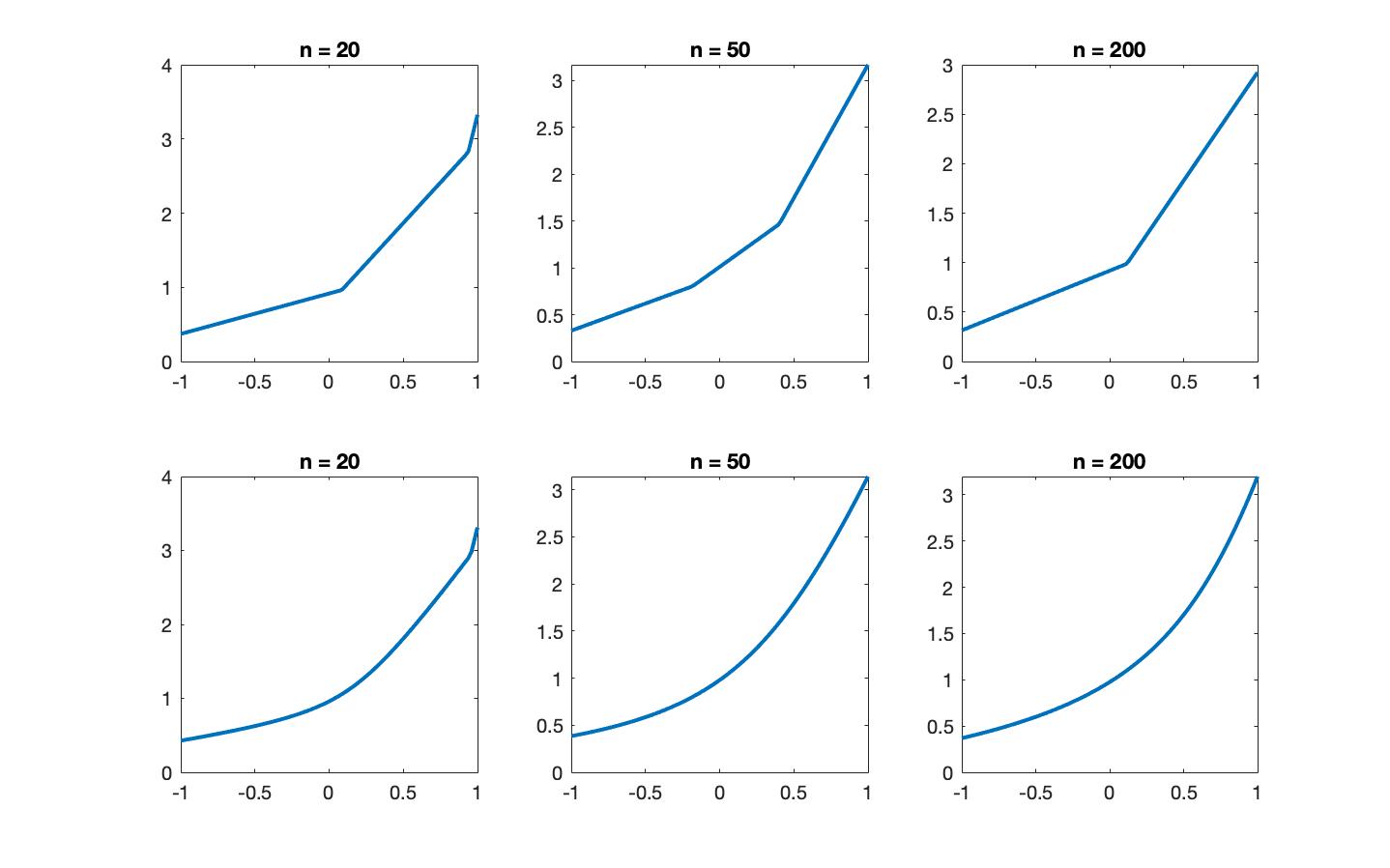

The first experiments use synthetically generated data from a known convex function, one from a spectrahedral function and another from a convex function that is neither polyhedral nor spectrahedral. In both problems below, the root-mean-squared error (RMSE) is obtained by first obtaining estimators form 200 noisy training data points and then evaluating the RMSE of the estimators on 200 test points generated from the true function. We ran the alternating minimization algorithm with 50 random initializations for 200 steps or until convergence, and chose the best estimator.

First, we consider i.i.d. data points distributed as , where is uniformly distributed in , and

| (23) |

where . In Figure 2, we have plotted polyhedral and spectrahedral estimators obtained from and data points. The RMSE for both models is given in Table 2. The function is a spectrahedral function, and the spectrahedral estimator performs better than the polyhedral estimator as expected.

Second, we consider i.i.d. data points generated as , where and

| (24) |

where and . The underlying convex function is neither polyhedral nor spectrahedral, but the spectrahedral estimator better captures the smoothness of the function as illustrated in Figure 3. The spectrahedral estimator also outperforms the polyhedral estimator with respect to the RMSE when comparing the model fitted to the training data set to the test data set, see Table 2.

4.2 Predicting Average Weekly Wages

The first experiment we perform on real data is predicting average weekly wages based on years of education and experience. This data set is also studied in [12]. The data set is from the 1988 Current Population Survey (CPS) and can be obtained as the data set ex1029 in the Sleuth2 package in R. It consists of 25,361 records of weekly wages for full-time, adult, male workers for 1987, along with years experience and years of education. It is reasonable to expect that wages are concave with respect the years experience. Indeed, at first wages increase with more experience, but with a decreasing return each year until a peak of earnings is reached, and then they begin to decline. Wages are also expected to increase as the number of years of education increases, but not in a concave way. However, as in [12], we use the transformation to obtain a concave relationship. We used polyhedral and spectrahedral regression to fit convex functions to this data set, as illustrated in Figure 1. We also estimated the RMSE for different values of (the degrees of freedom per dimension) through hold-out validation with 20% of the data points, see Table 3. This generalization error is smaller for the spectrahedral estimator than the polyhedral estimator in each case.

4.3 Convex Approximation in Engineering Applications

In the following two examples, we consider applications of convex regression in engineering applications where the goal is to subsequently use the convex estimator as an objective or constraint in an optimization problem. Polyhedral regression returns a convex function compatible with a linear program, and using spectrahedral regression provides an estimator compatible with semidefinite programming.

4.3.1 Aircraft Data

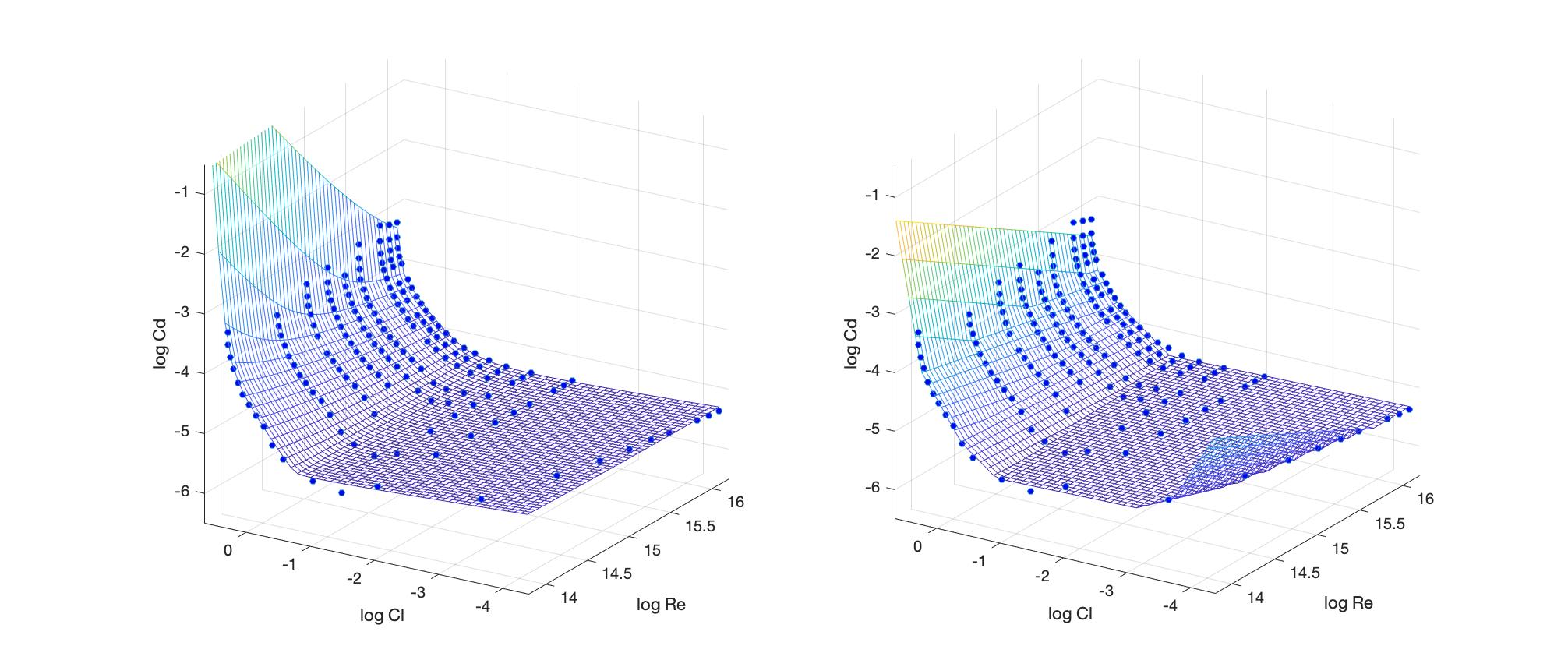

In this experiment, we consider the XFOIL aircraft design problem studied in [13]. The profile drag on an airplane wing is described by a coefficient CD that is a function of the Reynolds number (Re), wing thickness ratio (), and lift coefficient (CL). There is not an analytical expression for this relationship, but it can be simulated using XFOIL [4]. For a fixed , after a logarithmic transformation, the data set can be approximated well by a convex function. We fit both spectrahedral and polyhedral functions to this data set, and the best fits for the whole data set appears in Figure 4 for models with 6 degrees for freedom per dimension. Then, we performed hold-out validation, training on 80% of the data and testing on the remaining 20%. The RMSE is given in Table 3, where we observe that the spectrahedral estimator achieves a smaller error than polyhedral regression.

4.3.2 Power Modeling For Circuit Design

A circuit is an interconnected collection of electrical components including batteries, resistors, inductors, capacitors, logical gates, and transistors. In circuit design, the goal is to optimize over variables such as devices, gates, threshold, and power supply voltages in order to minimize circuit delay or physical area. The power dissipated, , is a function of gate supply and threshold voltages . The following model, see [13] and [11], can be used to study this relationship:

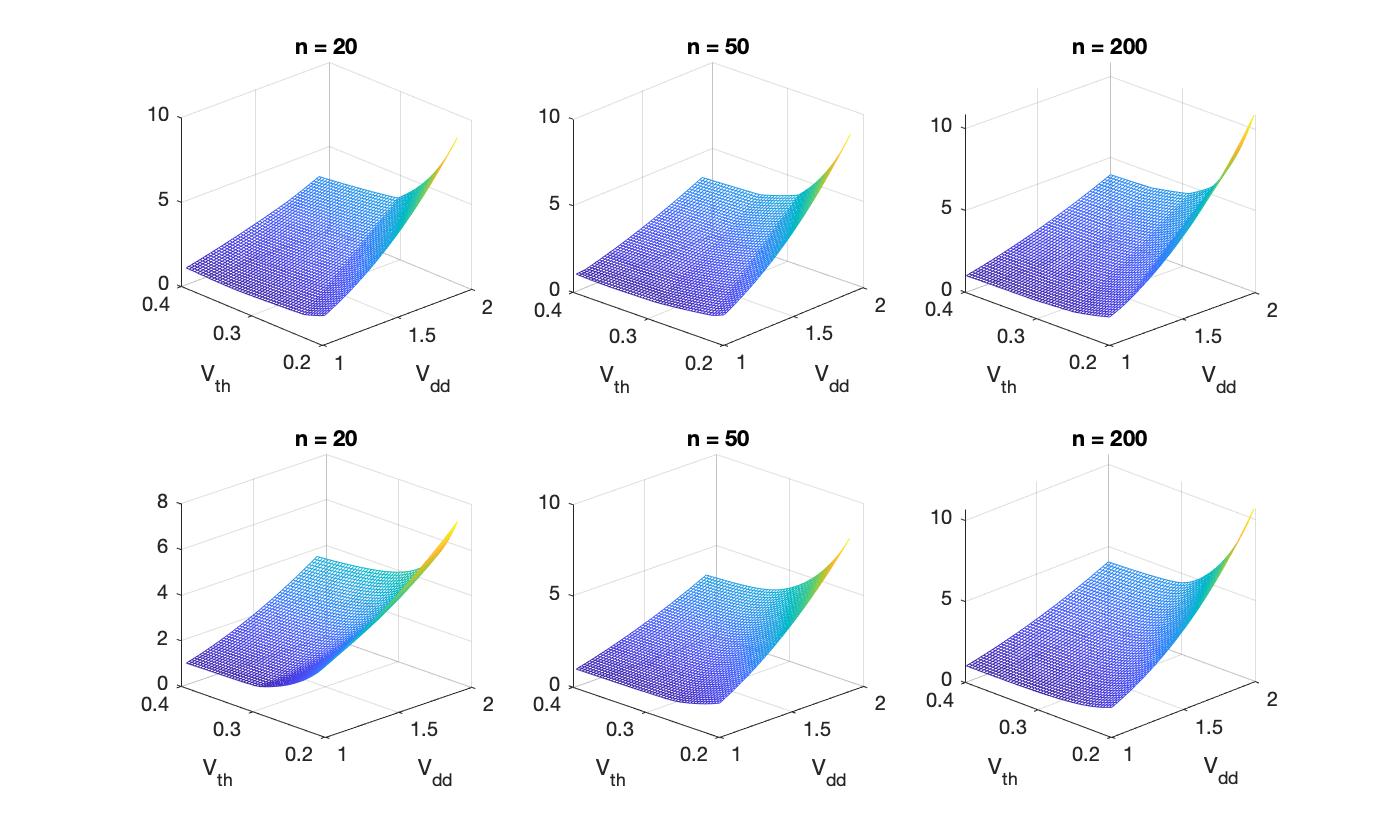

We generate i.i.d. data points as in [11] as follows. For each input-output pair, first sample uniformly over the domain and and compute . Then, apply the transformation . We fit this collection of transformed data points using polyhedral and spectrahedral regression, and the estimators for , and are illustrated in Figure 5. We also perform hold-out validation with 20% of the data for the case and the RMSE appears in in Table 3. By this measure, the spectrahedral estimator performs much better than the polyhedral estimator in this application.

| Application | Spectrahedral | Polyhedral | |

| Average Weekly Wages | 3 | 142.1166 | 145.5803 |

| 6 | 140.1173 | 141.4989 | |

| 10 | 140.0352 | 141.9851 | |

| Aircraft Profile Drag | 3 | 0.086 | 0.0895 |

| 6 | 0.0576 | 0.0709 | |

| 10 | 0.0452 | 0.0515 | |

| Circuit Design | 3 | 0.0085 | 0.02 |

| 6 | 0.0072 | 0.012 | |

| 10 | 0.0072 | 0.0088 |

5 Discussion and Future Work

In this work, we have introduced spectrahedral regression as a new method for estimating a convex function from noisy measurements. Spectrahedral estimators are appealing from a qualitative and quantitative perspective and we have shown they hold advantages over the usual LSE methods as well as polyhedral estimators when the underlying convex function is non-polyhedral. Our theoretical results and numerical experiments call for further study of the expressivity of this model class and its computational advantages. We now describe a few directions of future research.

An interesting open question is to obtain the approximation rate for -spectrahedral functions to the class of Lipschitz convex functions and - spectratopes to the class of convex bodies for general . There is extensive literature on this approximation question for polytopes (see, for instance, [3, 5]), and we have obtained matching bounds (up to logarithmic factors) for fixed . For depending on , and in particular in the case , the literature is more limited, one example is [2]. Progress in this direction would complete our understanding of the expressive power of the model presented here and have important consequences for how well semidefinite programming can approximate a general convex program.

We have also proved computational guarantees for a natural alternating minimization algorithm for spectrahedral regression. However, this convergence guarantee depends on a good initialization. In practice, running the algorithm with multiple random initializations and taking the estimator with the smallest error works well, but it would be very interesting to extend the results on initialization in [7] to the spectrahedral case. Another line of future work is to extend other methods to solve the non-convex optimization (3) in the max-affine case such as the adaptive partitioning method in [12] and the method proposed in [25]. These algorithms also lack theoretical guarantees and it would be interesting to obtain conditions under which these methods obtain good estimates of the true parameter.

Acknowledgments

E. O. was supported by NSF MSPRF Award 2002255 with additional funding from ONR Award N00014-18-1-2363. V. C. was supported in part by National Science Foundation grant CCF-1637598, in part by National Science Foundation grant DMS-2113724, and in part by AFOSR grant FA9550-20-1-0320.

References

- [1] P. L. Bartlett, V. Maiorov, and R. Meir, Almost linear VC-dimension bounds for piecewise polynomial networks, Neural Computation, 10 (1998), pp. 2159–2173.

- [2] A. I. Barvinok, Approximations of convex bodies by polytopes and by projections of spectrahedra, arXiv:1204.0471, (2012).

- [3] E. M. Bronshtein, Approximation of convex sets by polytopes, Journal of Mathematical Sciences, 153 (2008).

- [4] M. Drela, Xfoil subsonic airfoil development system. Open source software available at http://web.mit.edu/drela/Public/web/xfoil/, 2000.

- [5] R. M. Dudley, Metric entropy of some classes of sets with differentiable boundaries, Journal of Approximation Theory, 10 (1974), pp. 227–236.

- [6] H. Fawzi, J. Gouveia, P. A. Parrilo, J. Saunderson, and R. R. Thomas, Lifting for simplicity: Concise descriptions of convex sets, arXiv:2002.09788, (2020).

- [7] A. Ghosh, A. Guntuboyina, A. Pananjady, and K. Ramchandran, Max-affine regression I: Parameter estimation for Gaussian designs. https://tinyurl.com/spyjmgv, 2019.

- [8] A. Ghosh, A. Pananjady, A. Guntuboyina, and K. Ramchandran, Max-affine regression with universal parameter estimation for small-ball designs, in 2020 IEEE International Symposium on Information Theory (ISIT), 2020, pp. 2706–2710.

- [9] A. Guntuboyina, Optimal rates of convergence for convex set estimation from support functions, The Annals of Statistics, 40 (2012), pp. 385–411.

- [10] Q. Han and J. A. Wellner, Multivariate convex regression: global risk bounds and adaptation., arXiv:1601.06844, (2016).

- [11] L. A. Hannah and D. B. Dunson, Ensemble methods for convex regression with applications to geometric programming based circuit design, Proceedings of the 29th International Conference on Machine Learning, (2012).

- [12] L. A. Hannah and D. B. Dunson, Multivariate convex regression with adaptive partitioning, Journal of Machine Learning Research, 14 (2013), pp. 3261–3294.

- [13] W. W. Hoburg, P. G. Kirschen, and P. Abbeel, Fitting geometric programming models to data, Optimization and Engineering, (2015).

- [14] Y. Klochkov and N. Zhivotovskiy, Uniform Hanson-Wright type concentration inequalities for unbounded entries via the entropy method, Electronic Journal of Probability, 25 (2020), pp. 1–30.

- [15] G. Kur, F. Gao, A. Guntuboyina, and B. Sen, Convex regression in multidimensions: Suboptimality of least squares estimators, arXiv:2006.02044, (2020).

- [16] G. Kur, A. Rakhlin, and A. Guntuboyina, On suboptimality of least squares with application to estimation of convex bodies, in Proceedings of Thirty Third Conference on Learning Theory, J. Abernethy and S. Agarwal, eds., vol. 125 of Proceedings of Machine Learning Research, PMLR, July 2020, pp. 2406–2424.

- [17] M. Ledoux and M. Talagrand, Probability in Banach Spaces: Isoperimetry and Processes., Springer-Verlag Berlin Heidelberg, 2013.

- [18] A. Magnani and S. P. Boyd, Convex piecewise-linear fitting, Optimization and Engineering volume, 10 (2009), p. 1–17.

- [19] J. Prince and A. Willsky, Reconstructing convex sets from support line measurements, IEEE Transactions on Pattern Analysis and Machine Intelligence, 12 (1990), pp. 377–389.

- [20] J. Prince and A. Willsky, Convex set reconstruction using shape information, CVGIP: Graphical Models and Image Processing, 53 (1991), pp. 413–427.

- [21] M. Rudelson and R. Vershynin, Hanson-Wright inequality and sub-gaussian concentration, Electronic Communications in Probability, 18 (2013), pp. 1 – 9.

- [22] E. Seijo and B. Sen, Nonparametric least squares estimation of a multivariate convex regression function, The Annals of Statistics, 39 (2011), pp. 1633 – 1657.

- [23] Y. S. Soh, Code for “Fitting tractable convex sets to support function evaluations”. https://github.com/yssoh/cvxreg, 2019.

- [24] Y. S. Soh and V. Chandrasekaran, Fitting tractable convex sets to support function evaluations, Discrete & Computational Geometry, (2021), pp. 1–42.

- [25] G. B. A. G. C. Szepesvári, Near-optimal max-affine estimators for convex regression, Proceedings of the 18th International Conference on Artificial Intelligence and Statistics, 38 (2015).

- [26] R. Vershynin, Introduction to the non-asymptotic analysis of random matrices, in Compressed Sensing, Cambridge University Press, 2012, pp. 210–268.

- [27] R. Vershynin, High-Dimensional Probability: An Introduction with Applications in Data Science, Cambridge University Press, 2020.

- [28] T. W. Y. Yu and R. J. Samworth, A useful variant of the Davis—Kahan theorem for statisticians, Biometrika, 102 (2015), pp. 315–323.

Appendix A Lemmas for the Proof of Theorem 10

We first give a few definitions that are needed in following lemmas. A random vector is sub-Gaussian with parameter if and for each , . The sub-Gaussian norm of a random variable , denoted by , is defined as

For , the sub-Gaussian norm is defined as . The sub-exponential norm of , denoted by , is defined as

and the sub-exponential norm of a vector is defined similarly.

We also recall that the covering number of a Euclidean ball satisfies

| (25) |

for by a standard volume argument.

The proofs rely on uniform spectral concentration bounds of a sample covariance matrix, which follow from Bernstein’s inequality and Dudley’s inequality. A general reference for the ideas in the lemmas below is [27].

Lemma 12.

Let be an -sub-Gaussian r.v. in and be such that

Define the set . For each , define to be the rank one matrix such that

Then, and for all ,

Proof.

For the first claim, recall that is sub-Gaussian if is sub-Gaussian for every . Indeed, we first see that for ,

where . Then, by the triangle inequality,

For the second claim, first note that for all , Weyl’s inequality implies

Then, observe that , where , and . By a variation of the Davis-Kahan Theorem (Corollary 3 in [28]),

This implies that

∎

Lemma 13.

Define for and . Let be stochastic process in such that

-

(i)

;

-

(ii)

for all , , .

Define to be the matrix with i.i.d. rows in distributed as , and let . Fix . Then, there exist absolute constants such that if ,

This implies that with probability greater than ,

Proof.

First suppose that for all , , i.e. that is is isotropic. For the general case, since is isotropic, the conclusion follows from the fact that .

We first show that for any , the stochastic process has sub-Gaussian increments .

Case 1: . We first see that

| (26) |

Then, note that

and by Lemma 2.7.7 in [27],

Each term in the sum also has zero mean. Indeed,

Applying Bernstein’s inequality (Corollary 2.8.3 in [27]) gives for all ,

For the second tail probability in (A), Theorem 3.1.1 in [27] implies

where we have used that is isotropic. Thus, since and ,

Case 2: . By the triangle inequality,

where for the second to last inequality we have used that

and the last inequality follows from the lower bound on and the fact that . By Bernstein’s inequality again (Corollary 2.8.3 in [27]) and the lower bound on ,

Proposition 2.5.2 in [27] then implies that for all ,

Lemma 14.

Consider the setting of Theorem 10. Let and define . Then, there exist absolute constants , , and such that for ,

Proof.

First, note that for all , and

| (28) |

Then,

Now, recall that for an absolute constant [17]. Applying Theorem 1.1 in [14] to the family of matrices gives: For ,

| (29) |

Also by (28), and thus,

Letting for a constant large enough,

| (30) | ||||

We now upper bound . For ,

Define the stochastic process . Then, for and in ,

By a variant of the Davis-Kahan Theorem (Corollary 3 in [28]) and (13),

Then, , and by the Hanson-Wright Inequality [21, Theorem 2.1], since is independent of the ’s, there is a constant such that

Thus, has sub-gaussian increments and there is a constant such that

Then, by Theorem 8.1.6 in [27] and (25),

Combining this bound with (30) gives

Taking completes the proof. ∎