Boosted CVaR Classification

Abstract

Many modern machine learning tasks require models with high tail performance, i.e. high performance over the worst-off samples in the dataset. This problem has been widely studied in fields such as algorithmic fairness, class imbalance, and risk-sensitive decision making. A popular approach to maximize the model’s tail performance is to minimize the CVaR (Conditional Value at Risk) loss, which computes the average risk over the tails of the loss. However, for classification tasks where models are evaluated by the loss, we show that if the classifiers are deterministic, then the minimizer of the average loss also minimizes the CVaR loss, suggesting that CVaR loss minimization is not helpful without additional assumptions. We circumvent this negative result by minimizing the CVaR loss over randomized classifiers, for which the minimizers of the average loss and the CVaR loss are no longer the same, so minimizing the latter can lead to better tail performance. To learn such randomized classifiers, we propose the Boosted CVaR Classification framework which is motivated by a direct relationship between CVaR and a classical boosting algorithm called LPBoost. Based on this framework, we design an algorithm called -AdaLPBoost. We empirically evaluate our proposed algorithm on four benchmark datasets and show that it achieves higher tail performance than deterministic model training methods.

1 Introduction

As machine learning continues to find broader usage, there is an increasing understanding of the importance of tail performance of models, in addition to their average performance. For instance, in datasets with highly imbalanced classes, the tail performance is the accuracy over the minority classes which have much fewer samples than the others. In the field of algorithmic fairness, where a dataset contains several demographic groups, the tail performance is the accuracy over certain underrepresented groups that normal machine learning models often neglect. In all these examples, it is crucial to design models with good tail performance that perform well across all parts/groups of the data domain, instead of just performing well on average.

Owing to its importance, several recent works have designed techniques to learn models with high tail performance HSNL (18); SKHL (20); SRKL (20). Maximizing the tail performance is sometimes referred to as learning under subpopulation shift, in the sense that the testing distribution could consist of just a subpopulation of the training distribution. Most of the works on subpopulation shift fall into two categories. In the first, also referred to as the domain-aware setting, the dataset is divided into several predefined groups, and the goal is to maximize the worst-group performance, i.e. the minimum performance over all the groups. Many methods, such as importance weighting Shi (00) and Group DRO SKHL (20); SRKL (20), have been proposed for domain-aware subpopulation shift. However, the domain-aware setting is not always applicable, either because the groups can be hard to define, or because the group labels are not available. Thus, in the second category of work on subpopulation shift, also referred to as the domain-oblivious setting, there are no pre-defined groups, and the goal is to maximize the model’s performance over the worst-off samples in the dataset. Most previous work on domain-oblivious subpopulation shift HSNL (18); DN (18); HNSS (18); LBC+ (20); MHN (21) measure the tail performance using the Distributionally Robust Optimization (DRO) loss, which is defined as the model’s maximum loss over all distributions within a divergence ball around the training distribution. A popular instance is the -CVaR loss, defined as the model’s average loss over the worst fraction of the samples incurring the highest losses in the dataset.

Naturally one might think of maximizing a model’s tail performance by directly minimizing the DRO loss or the -CVaR loss, as proposed by many previous work HSNL (18); DN (18); XDKR (20). However, HNSS (18) proved the negative result that for classification tasks where models are evaluated by the zero-one loss, empirical risk minimization (ERM) achieves the lowest possible DRO loss given that the model is deterministic and the DRO loss is defined by some -divergence function. We extend their result to the -CVaR loss which can be written as the limit of Rényi-divergence DRO losses (with a more direct and simpler proof due to the specialized case of CVaR). This is a very pessimistic result since it entails that there is no hope to get a better classifier than ERM so long as models are evaluated by a DRO (or CVaR) loss. So some previous work HNSS (18); LBC+ (20); MHN (21) proposed to avoid this issue by making extra assumptions on the testing distribution (specifically, that the testing subpopulation can be represented by a parametric model), and changing the evaluation metric correspondingly to something other than a -divergence DRO loss.

In this work, we take a different approach and show that no extra assumption is needed provided that we use randomized models. While the case of general DRO is more complicated, the reason why ERM achieves the lowest possible CVaR zero-one loss in the deterministic case is very simple: there is a linear relationship between the CVaR zero-one loss and the average zero-one loss, so the former is non-decreasing with the latter. For randomized models, however, such a monotonic relationship no longer exists. Note that for any single test sample, the zero-one loss of the deterministic model is either 0 or 1, while the expected zero-one loss of the randomized model is a real number in , so that the randomized model can typically achieve lower -CVaR loss than the deterministic model. In fact, we can prove that if the two models have the same average accuracy, then the -CVaR zero-one loss of the randomized model is consistently lower than the deterministic one.

Motivated by the above analysis, we propose the framework of Boosted CVaR Classification to train ensemble models via Boosting. The key observation we make is that minimizing the -CVaR loss is equivalent to maximizing the objective of -LPBoost, a subpopulation-performance counterpart of a classical boosting variant known as LPBoost DBST (02). Thus training with respect to the -CVaR loss can be related to a goal of boosting an unfair learner, which always produces a model with low average loss on any reweighting of the training set, to obtain a fair ensemble classifier with low -CVaR loss for a fixed . Note that this is in contrast to the classical boosting, which boosts a weak learner to produce an ensemble model with better average performance. We can thus show that -CVaR training is equivalent to a sequential min-max game between a Boosting algorithm and an unfair learner, in which the Boosting algorithm provides the sample weights and the unfair learner provides base models with low average loss with respect to these weights. After all base models are trained, we compute the optimal model weights. At inference time, we first randomly sample a base model according to the model weights, and then predict with the model. Thus, the final ensemble model is a linear combination of all the base models.

This paper is organized as follows: In Section 2, we provide the necessary background of subpopulation shift and CVaR, and show that ERM achieves the lowest CVaR zero-one loss in classification tasks with deterministic classifiers. In Section 3 we show how to boost an unfair learner: we first show that minimizing the CVaR loss is equivalent to maximizing the LPBoost objective in Section 3.1; based on this observation, we propose the Boosted CVaR Classification framework and implement an algorithm that uses LPBoost for CVaR classification in Section 3.2; Then, to improve computation efficiency, we implement another algorithm called -AdaLPBoost in Section 3.3. Finally, in Section 4 we empirically evaluate the proposed method on popular benchmark datasets.

1.1 Related Work

Caveats of DRO. DRO was first applied to domain-oblivious subpopulation shift tasks in HSNL (18), in which the authors proved that the DRO loss is an upper bound of the worst-case loss over groups (group CVaR) for fairness problems. DN (18) analyzed the convergence rate of DRO for the Cressie-Read family of -divergence. However, HNSS (18) showed that minimizing -divergence DRO over deterministic function classes, with respect to the zero-one classification loss, yields the same minimizer as that of ERM, provided that the former has loss less than one. SKHL (20) further showed that for highly flexible classifiers (such as many modern neural models) that achieve zero error on each training sample, both empirical average risks and DRO risks are zero, so that the model is not specifically focusing on population DRO objective. SRKL (20) made the related point that the Group DRO objective with respect to the zero one loss is prone to overfit.

Boosting. Boosting is a classic algorithm in machine learning dating back to AdaBoost proposed in Sch (90). See Sch (03) for a survey of the early works. Motivated by the success of AdaBoost, many later works proposed variants of Boosting, such as AdaBoost RWST (05), AdaBoostSL (09), LPBoost DBST (02), SoftBoost RWG (07) and entropy regularized LPBoost WGV (08). There are some previous works that apply ensemble methods to tasks related to subpopulation shift: see GFB+ (11) for a survey of Bagging, Boosting and hybrid methods for the class imbalance problem, while IN (19); BHL (19) used AdaBoost to improve algorithmic fairness.

2 Preliminaries

In this section we provide the necessary background on subpopulation shift, DRO and CVaR, in the context of classification, which is the focus of the paper. Particularly, we will demonstrate that in classification tasks, ERM achieves the lowest CVaR loss, so there is no gain in using CVaR compared to ERM. Then, we show that using randomized models can circumvent this problem.

Denote the input space by , the label space by , and the data domain by . We are given a dataset that i.i.d. sampled from some underlying data distribution. We assume that any input has only one true label , i.e. for any there exists such that . Given a family of classifiers , the goal of a subpopulation shift task is to train a classifier with high tail performance. Given a loss function , the standard training algorithm is empirical risk minimization (ERM) which minimizes the empirical risk defined as

| (1) |

Denote the set of minimizers of the empirical risk by . For classification tasks, the model performance is evaluated by the zero-one loss . Although we can use different surrogate loss functions during training, at test time we always use the zero-one loss because we care about the accuracy, and the zero-one loss is equal to one minus the accuracy.

To quantitatively measure the tail performance of model , we can use the -CVaR (Conditional Value at Risk) loss. For a fixed , the -CVaR loss is defined as

| (2) |

where is the unit simplex in . The -CVaR loss measures how well a model performs over the worst fraction of the dataset. For instance, if is an integer, then the -CVaR loss is the average loss over the samples that incur the highest losses. We use CVaR classification to refer to classification tasks where models are evaluated by the CVaR loss. Denote the set of minimizers of the -CVaR loss by .

The CVaR loss can be written as the limit of DRO (Distributional Robust Optimization) losses. For some divergence function between distributions, the DRO loss measures the model’s performance over the worst-case distribution 111 is absolute continuous to (i.e. ) if for any event , . within a ball w.r.t. divergence around the training distribution . Formally, the DRO loss of model is defined as

| (3) |

If we denote the Rényi-divergence by , then the -CVAR loss is equal to the limit of as (see Example 3 in DN (18)). Many previous works proposed to train a model with high tail performance by minimizing the CVaR loss or the DRO loss. However, the following result shows that for classification tasks, any model in is also the minimizer of the CVaR loss if only contains deterministic models, i.e. every is a deterministic mapping (all proofs can be found in Appendix A):

Proposition 1.

If only contains deterministic models, then for any model and any , we have . Moreover, if , then we have .

HNSS (18) showed that a counterpart of the above result holds for any -divergence DRO loss. As noted earlier, we can write the -CVaR loss as the limit of the Rényi family of -divergence DRO losses. However our proof is much more direct and simple, and proceeds by showing the following simple monotonic relationship between the average zero-one loss and the -CVaR zero-one loss: , so the -CVaR loss is non-decreasing with the ERM loss. This is a very pessimistic result, since it entails that there is no hope to obtain a better model than ERM no matter what learning algorithm we use for CVaR classification.

For the DRO context, some previous papers HNSS (18); LBC+ (20); MHN (21) propose to avoid this issue by making extra assumptions on the testing distribution, so as to change the evaluation metric to some function other than the -divergence DRO loss. In this work, however, we take a completely different approach: we show that the above difficulty can be circumvented without any extra assumptions by using randomized models222If is a randomized model, then for any , is a random variable over , i.e. for any , is a real number in instead of binary.. For a randomized model , its empirical risk and -CVaR loss is defined as the expectation of (1) and (2), where the expectation is taken over the randomness of . For randomized models, the monotonic relationship in Proposition 1 does not exist, and they can achieve lower -CVaR zero-one loss than deterministic models. For example, if we have a deterministic model with average accuracy 90%, then the 10%-CVaR zero-one loss of this model is 1. However, if we have 5 deterministic models with average accuracy 90%, such that each sample is classified correctly by at least 4 of the 5 models, then the 10%-CVaR zero-one loss of the average of the 5 models is only 0.2, though its average accuracy is still 90%. Furthermore, we can prove that:

Proposition 2.

Let be a deterministic model, and be any randomized model whose average zero-one loss is the same as that of . Then, for any , .

This result implies that the tail performance of a randomized model is consistently higher than a deterministic model with the same average performance. In a nutshell, we have proved that for CVaR classification, ERM is the best deterministic model learning algorithm, and randomized models can achieve higher performance than deterministic models.

3 Boosted CVaR Classification

In this section, we propose the framework of Boosted CVaR Classification, which learns ensemble models with high tail performance via Boosting. An ensemble model consists of base models and a distribution over the models. is called the model weight vector. At inference time, we first sample a model according to , and then predict with the model. Denote the zero-one loss of base model over sample by . Then, the -CVaR zero-one loss of the ensemble model is333The notion means that the ensemble model consists of base models and model weight vector .

| (4) |

The motivation of this framework comes from a direct relationship between the CVaR loss and the objective of a variant of Boosting we call -LPBoost, which shows that training with respect to the -CVaR loss can be related to the goal of boosting an unfair learner (Section 3.1). Thus in Section 3.2, we present the Boosted CVaR Classification framework which formulates the training process as a sequential game between the training algorithm and the unfair learner, and implement an algorithm that uses (Regularized) LPBoost for CVaR classification. Finally, in Section 3.3 we implement another algorithm which we name -AdaLPBoost that is computationally more efficient.

3.1 -LPBoost

Suppose we have already obtained base models , and the -th function incurs losses on the samples . Consider the following primal/dual linear programs:

Dual:

| (5) | ||||

| s.t. | ||||

Primal:

| (6) | ||||

| s.t. |

where . Note that the primal problem can be written as a linear program by introducing slack variables . See the full derivation of this primal-dual linear program in Appendix A.3. Let us denote the optimal dual objective by and the optimal primal objective by . For this linear program, strong duality holds, i.e. . We refer to these primal/dual linear programs as -LPBoost, since it can be seen as subpopulation-performance counterpart of a classical variant of Boosting called LPBoost DBST (02).

Intuitively, the dual problem computes a such that every has a high weighted average loss w.r.t. . One might wonder what the primal problem is doing. The magical thing is that the primal problem is in fact searching for the model weight vector that minimizes the -CVaR zero-one loss of the ensemble model consisting of , as shown by the following proposition:

Proposition 3.

For any , we have the following relationship between the -LPBoost objective and the -CVaR zero-one loss:

| (7) |

and the optimal solution of the primal problem achieves the minimum in (7).

This result also shows a direct relationship between CVaR and LPBoost: minimizing the -CVaR loss is equivalent to maximizing the -LPBoost objective. Thus, the problem now becomes how to maximize . Note that we can rewrite the first constraint of the dual problem as for all , so is the accuracy of the best . Therefore, we can increase by training a new model whose weighted average loss with respect to , i.e. , is small. We can repeat this process until we have obtained sufficient base models so that there is no such that makes small. Then, we can obtain the optimal model weight vector by solving the primal problem of -LPBoost.

3.2 The Boosted CVaR Classification Framework

Motivated by the above analysis, we design the Boosted CVaR Classification framework that formulates the training process outlined in the previous section as a sequential game between a boosting algorithm and an unfair learner . We make the following assumption on :

Assumption 1.

We have access to an unfair learner that takes any sample weight vector as input, and always outputs a base model whose weighted average zero-one loss with respect to is at most . is called the guarantee of the learner .

In each round, the boosting algorithm picks a sample weight vector and feeds it to the learner which outputs a base model whose average loss w.r.t. is at most . The boosting algorithm goes as the following:

-

•

For ,

-

–

Pick a sample weight vector and feed it to

-

–

Receive a base model from such that

-

–

-

•

At the end of training, pick a model weight vector and return

To study the worst-case performance of the boosting algorithm, we can view as an adversary: The boosting algorithm picks and in order to minimize (4), while picks under the constraint in order to maximize (4).

Based on this framework, we implement Algorithm 1, which uses LPBoost to pick sample weights and model weights. For solving linear programs, there are a number of convex optimization solvers available. Now we prove a convergence rate theorem for this algorithm. To show that Algorithm 1 converges, we need to prove that with a sufficiently large , the worst-case -CVaR loss of the ensemble model can be as close to as we want444The -CVaR loss is lower bounded by , because can always output a model whose average loss over the uniform distribution of is at least , so that the average loss is at least g.. Ideally we would like to be in the order of . However, RWG (07) presented a counterexample in its Theorem 1 where -LPBoost requires base models to converge. To make logarithmic in , WGV (08) proposed (Entropy) Regularized -LPBoost, which adds regularization to the dual problem. At each iteration it solves the following convex problem for some regularization coefficient to pick :

| (8) | ||||

| s.t. |

where is the entropy function. With the regularization, we can prove the following theorem:

Theorem 4 (Theorem 1 in WGV (08)).

For any , if we run Regularized -LPBoost with , then we have with base models where

| (9) |

Connection to AdaBoost.

3.3 -AdaLPBoost

We have proved that the -CVaR loss achieved by Regularized -LPBoost can be arbitrarily close to with . However, one disadvantage of Algorithm 1 is that it needs to train a different set of base models for each . On the other hand, since controls the trade-off between fairness and average performance, in practice we might want to change from time to time. For example, we might want to tune down to make the model fairer. Thus, it would be more efficient if we could train only one set of base models for all , and by adjusting the model weight vector for different we could still achieve tail performance comparable to Regularized -LPBoost.

To this end, we first use the classical Regularized LPBoost (with ) to pick to train the base models, since the resulting base models would also be suitable for more general . Following SL (09), we solve this step using a variant of AdaBoost. We then pick the model weights by solving the -LPBoost primal problem after all base models are trained. The method, which we denote by -AdaLPBoost, is listed in Algorithm 2. The difference between Algorithm 2 and the original AdaBoost is that AdaBoost picks where and is the weighted average loss, whereas Algorithm 2 picks for a constant , which we find achieves better performance than AdaBoost in our experiments.

The advantage of using our two-step approach is that when changes, we only need to adjust the model weight vector without training an entirely new set of base models. We next show that the two-step approach is not just intuitively reasonable, but comes with strong theoretical guarantees. To begin with, we consider a mixed algorithm called “AdaBoost + Average”, where we train the based models with AdaBoost (as in Algorithm 2) and output the average of the base models (such that ). For AdaBoost + Average, we have the following result:

Theorem 5.

For any , and for , the training -CVaR zero-one loss of the ensemble model given by AdaBoost + Average is at most if we set .

The theorem guarantees that AdaBoost + Average can achieve low -CVaR zero-one loss. Next, note that the -CVaR zero-one loss of -AdaLPBoost is upper bounded by the minimum of those of ERM and AdaBoost + Average, because -LPBoost ensures that the it picks achieves the lowest -CVaR zero-one loss, while ERM corresponds to and AdaBoost + Average corresponds to . In other words, the theorem ensures that the tail performance of AdaBoost + Average is high, and -AdaLPBoost achieves a tail performance no lower than that.

3.4 Discussion

Generalization Bound for the CVaR Loss.

In our analysis, we only provide theoretical guarantees on the training -CVaR zero-one loss for the methods we propose. One might be curious about the generalization capability of boosting with respect to the CVaR loss. A recent work KLPR (20) proved a generalization bound for the CVaR loss under the assumption that the hypothesis set has a finite VC-dimension, and it is well-known that if has a finite VC-dimension, then the set of ensemble models based upon also has a finite VC-dimension (see e.g. Section 6.3.1 in MRT (18)). However, in the VC-dimension-based analysis, the generalization error increases with , while in practice it usually decreases with . Thus, people use the margin-based analysis to obtain a tighter bound. We leave the margin-based analysis of Boosted CVaR Classification to future work.

Sensitivity to Outliers.

An algorithm that maximizes the tail performance of a model can be very sensitive to outliers. This is because such an algorithm puts more weight on samples on which the model has high losses, while intuitively outliers tend to incur high losses. Consequently, the algorithm puts more weight on outliers. A recent work ZDKR (21) proposed to solve this problem with an algorithm called DORO, which ignores a fraction of the samples with the highest losses within the minibatch for each iteration. DORO can also be combined with our Boosting algorithms.

Connection to (Domain-Aware) Group DRO.

Our algorithm has a strong connection to Group DRO proposed in SKHL (20) for domain-aware subpopulation tasks. Group DRO assumes that the dataset is divided into groups and minimizes the model’s maximum loss over the groups with AdaBoost. We can obtain Group DRO from AdaBoost + Average by choosing , and defining as the loss of model over group . Our algorithm suggests that we can improve Group DRO if we choose the model weights with LPBoost.

4 Experiments

4.1 Setup

Datasets.

We conduct our experiments on four datasets: COMPAS LMKA (16), CelebA LLWT (15), CIFAR-10 and CIFAR-100 KH+ (09). The first, COMPAS, is a tabular recidivism dataset widely used in fairness research. The second, CelebA, with the target label as whether a person’s hair is blond or not, was used in SKHL (20) to evaluate their proposed Group DRO algorithm. And finally, CIFAR-10 and CIFAR-100 are two widely used image datasets. Both COMPAS and CelebA are binary classification tasks, while CIFAR-10 is 10-class and CIFAR-100 is 100-class classification. On COMPAS we use the training set as the validation set because the dataset is very small. CelebA has its official train-validation split. On CIFAR-10 and CIFAR-100 we take out 10% of the training samples and use them for validation. Our selection of datasets covers different types, complexity, and both binary and multi-class classification.

Learner .

We implement the unfair learner as follows: given a sample weight vector , for each iteration we sample a minibatch with replacement according to the probability distribution , and then update the model parameters with ERM over the minibatch (by minimizing the cross-entropy loss). The learner stops and returns the model after a fixed number of iterations, with the learning rate decayed twice during training. See our code for training details.

Training.

We use a three-layer feed-forward neural network with ReLU activations on COMPAS, a ResNet-18 HZRS (16) on CelebA, a WRN-28-1 ZK (16) on CIFAR-10 and a WRN-28-10 on CIFAR-100. On each dataset, we first warmup the model with a few epochs of ERM, and then train base models on COMPAS and CIFAR-10, and base models on CelebA and CIFAR-100 from the warmup model with the sample weights given by the boosting algorithms. We train our models with CPU on COMPAS and with one NVIDIA GTX 1080ti GPU on other datasets. We solve linear programs with the CVXPY package DB (16); AVDB (18), which at its core invokes MOSEK ApS (21) and ECOS DCB (13) for optimization.555Please refer to their official websites for license information.

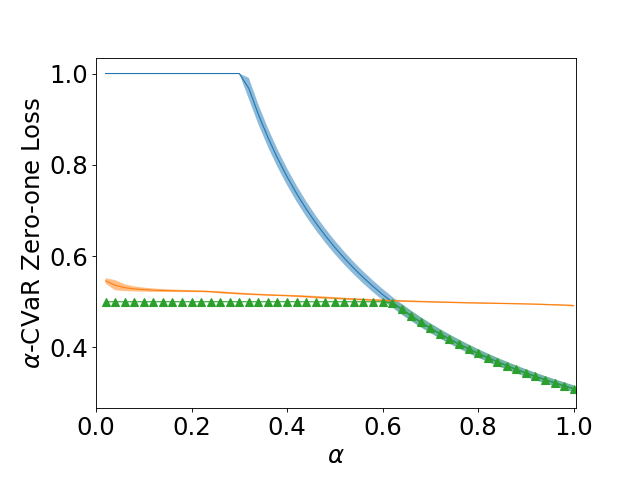

On each dataset, we run ERM and -AdaLPBoost with different values of . Here ERM refers to the deterministic version, in which a single base model is trained and used as the final model. For -AdaLPBoost, we choose on all datasets which is close to the theoretical optimal value . We also compare -AdaLPBoost with AdaBoost + Average in order to demonstrate the effectiveness of selecting with LPBoost. To simultaneously compare the performances under different , we plot the -CVaR zero-one loss vs curve for each method on every dataset.

4.2 Results

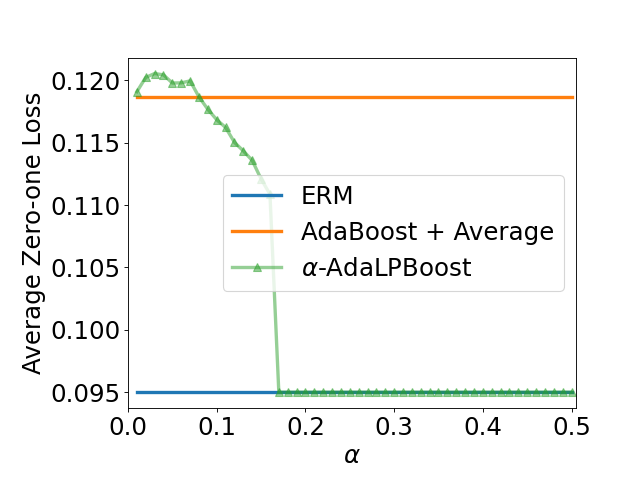

We plot the experimental results in Figure 1. Each experiment is repeated five times with different random seeds, and we plot the 95% confidence interval for each experiment. From the figure, we can see that the results are very consistent across different random seeds. It is also remarkable that on every dataset, the -CVaR loss curve of -AdaLPBoost almost overlaps with the minimum of ERM and AdaBoost + Average. From the plots we can make the following observations:

-

•

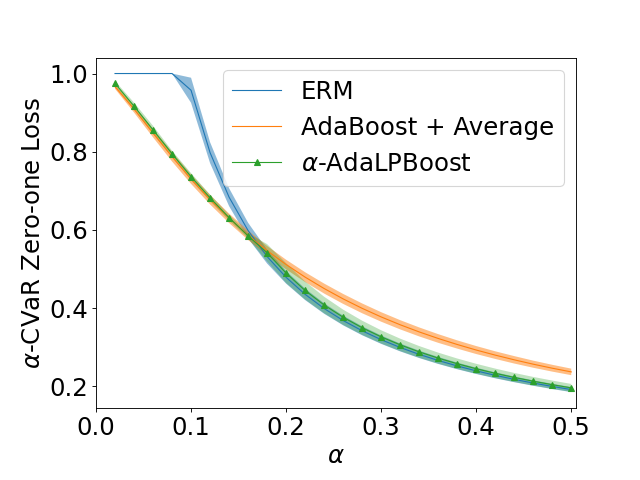

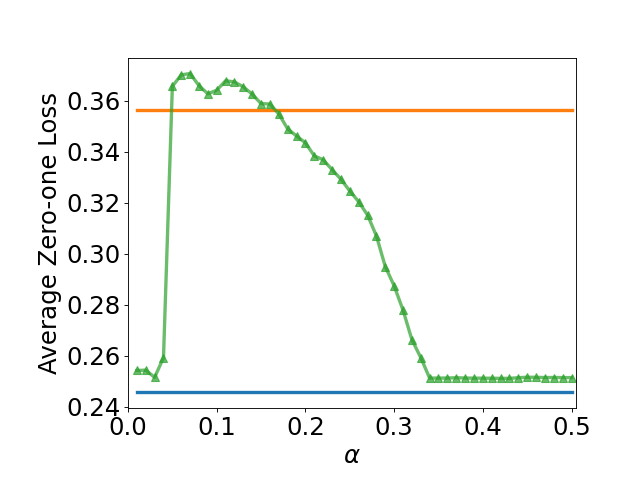

When is large, the -CVaR loss is close to the average loss, and we can see that the -CVaR loss of -AdaLPBoost is very close to that of ERM. We also plot the test average loss of the three methods on CIFAR-10 and CIFAR-100 in Figure 2, from which we can see that there is a gap between the ERM line and AdaBoost + Average line, and the average loss curve of -AdaLPBoost mostly lies between them.

-

•

When is small, the -CVaR loss of -AdaLPBoost is close to that of AdaBoost + Average, which is much lower than that of ERM. Recall our initial theoretical results on the equivalence of minimizers of the average loss and the CVaR loss for deterministic models, ERM achieves the lowest -CVaR loss among all deterministic models, so the results show that the ensemble model achieves higher tail performance than any deterministic model.

Overall, we find that -AdaLPBoost can automatically choose between high average performance (when is big) and high tail performance (when is small).

One might ask why -AdaLPBoost does not achieve lower average loss than ERM in our experiments, given that the model class of the ensemble models is larger than that of the deterministic models. The reason is that the model class we use for deterministic models (e.g. ResNet) is already very complex, so the average performance of ERM is high enough, and its loss mainly comes from the generalization gap instead of insufficient capacity of representation. In fact, we find that when is big, the model weight vector produced by LPBoost is very close to , i.e. almost all the weight is put on the first ERM model. That is why the -AdaLPBoost curve and the ERM curve overlap when is big.

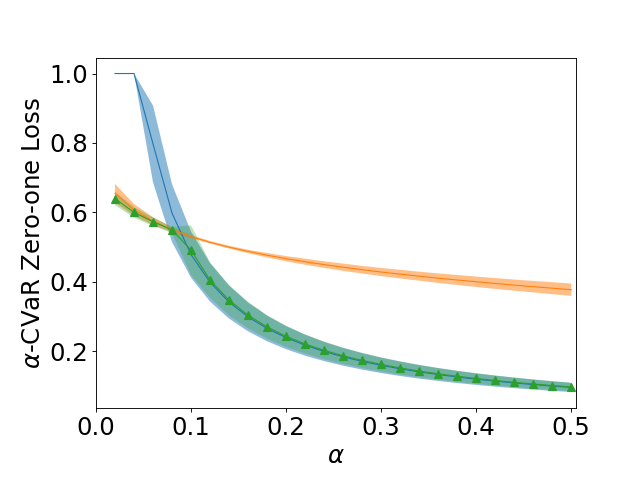

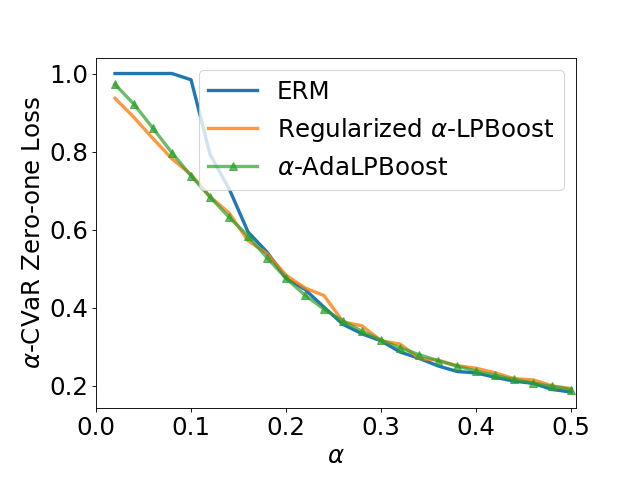

Comparison with Regularized LPBoost.

Now we empirically show that -AdaLPBoost can achieve performance comparable to Regularized LPBoost. In Figure 3 we plot the -CVaR loss of ERM, -AdaLPBoost and Regularized LPBoost () on CIFAR-10. The plot clearly shows that there is almost no gap between the performance of -AdaLPBoost and Regularized LPBoost, so we can safely replace the latter with the former for computational efficiency.

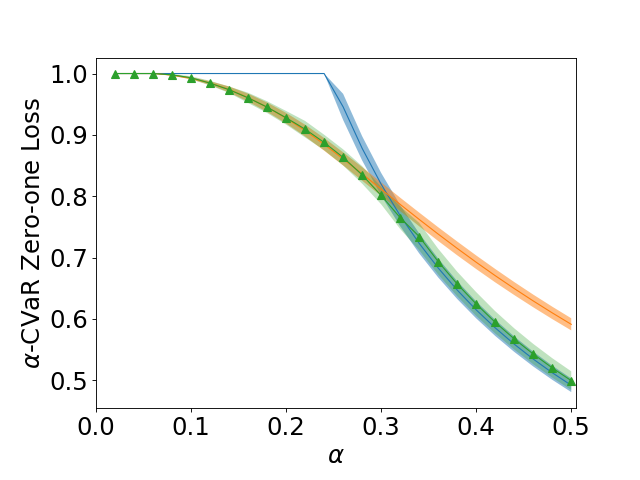

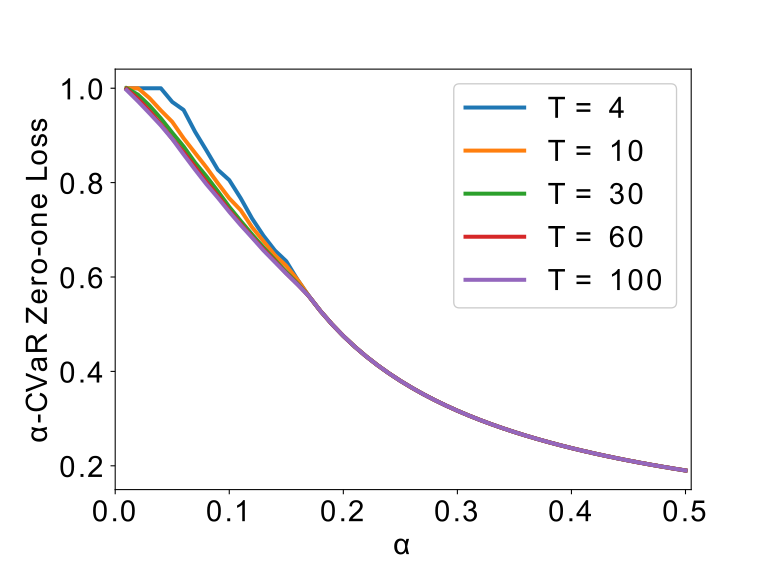

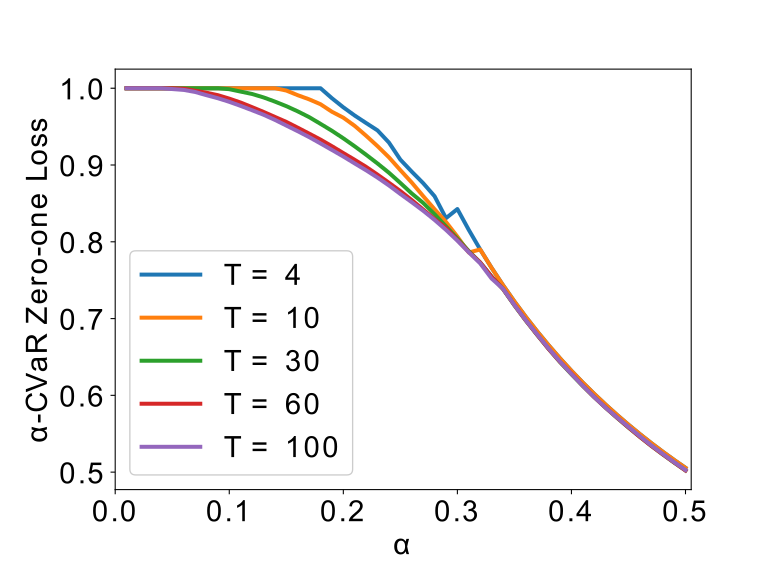

Convergence.

Finally, we empirically examine the convergence rate of -AdaLPBoost by studying how the -CVaR loss changes with . In Figure 4 we plot the results on CIFAR-10 and CIFAR-100, which show that AdaLPBoost converges slowly after . Theoretically, for a dataset with samples, in order to acheive in Theorem 5, we need to be at least 500, which would take a huge amount of time. Note that does not mean that the training time is 30 times more, because we can train each base model for fewer iterations since it is initialized from a warmup model and only needs finetune. In our experiments, the training time of AdaBoost is 3-6 times the training time of ERM if .

5 Conclusion

In this work, we addressed an issue raised by previous work that no deterministic model learning algorithm could be better than ERM for DRO classification (which we show formally also extends to CVaR) by learning randomized models. Specifically we proposed the Boosted CVaR Classification framework which is motivated by the direct relationship between -CVaR and -LPBoost, which is a sub-population variant of the classical LPBoost algorithm for classification. To further improve the computational efficiency, we implemented the -AdaLPBoost algorithm. In our experiments, we showed that the ensemble models produced by -AdaLPBoost achieved higher tail performance than deterministic models, and the algorithm could automatically choose between high average performance and high tail performance under different values of .

One caveat of using a randomized model is that one might be able to game the model via repeatedly using it. For example, when applying for a credit card, one can submit the application repeatedly until it gets approved if the decision is given by a randomized model. It is important to study how to improve the tail performance in this scenario where the model can be used repeatedly, which we leave as an open question.

One future direction is the application of ensemble methods to the fairness without demographics problem, in which the dataset is divided into several groups which are unknown during training, and the goal is to minimize the model’s worst-group loss, i.e. its maximum loss over all the groups. The worst-group loss can be upper bounded by the CVaR loss or certain families of DRO loss, but the bound is loose, and the model with the lowest CVaR loss is not guaranteed to achieve the lowest worst-group loss. Due to the difficulty of the problem, some recent works considered the scenario where a small set of samples with group labels is provided after training and before testing. Ensemble methods can be useful in this scenario: we can train base models, and then solve a linear program to obtain the optimal model weight vector with the provided validation set with no need of training new models. We leave the design of such algorithms to future work.

Social Impact.

Subpopulation shift has been widely studied to improve the fairness of machine learning, which is of great social importance. Models with high tail performance are considered fair because they perform well on all parts of the data domain. In this work we show how to improve the tail performance by learning ensemble models, which is a great contribution to the area of fair machine learning. However, we also observe that ensemble methods improve the tail performance by lowering the accuracy over samples in the majority group. Such trade-offs are nonetheless inevitable under the assumption that the average accuracy does not increase. It is an interesting sociological question to what extent it is just to improve fairness by sacrificing the majority group.

Code.

Codes for this paper can be found at: https://github.com/RuntianZ/boosted_cvar.

Acknowledgments and Disclosure of Funding

This research is supported by DARPA Guaranteeing AI Robustness against Deception (GARD) under the cooperative agreement number HR00112020006 and the official title "Provably Robust Deep Learning".

References

- ApS [21] MOSEK ApS. MOSEK Optimizer API for Python. Version 9.2.44, 2021.

- AVDB [18] Akshay Agrawal, Robin Verschueren, Steven Diamond, and Stephen Boyd. A rewriting system for convex optimization problems. Journal of Control and Decision, 5(1):42–60, 2018.

- BHL [19] Dheeraj Bhaskaruni, Hui Hu, and Chao Lan. Improving prediction fairness via model ensemble. In 2019 IEEE 31st International Conference on Tools with Artificial Intelligence (ICTAI), pages 1810–1814, 2019.

- CBL [06] Nicolo Cesa-Bianchi and Gábor Lugosi. Prediction, learning, and games. Cambridge university press, 2006.

- DB [16] Steven Diamond and Stephen Boyd. CVXPY: A Python-embedded modeling language for convex optimization. Journal of Machine Learning Research, 17(83):1–5, 2016.

- DBST [02] Ayhan Demiriz, Kristin P Bennett, and John Shawe-Taylor. Linear programming boosting via column generation. Machine Learning, 46(1):225–254, 2002.

- DCB [13] A. Domahidi, E. Chu, and S. Boyd. ECOS: An SOCP solver for embedded systems. In European Control Conference (ECC), pages 3071–3076, 2013.

- DN [18] John Duchi and Hongseok Namkoong. Learning models with uniform performance via distributionally robust optimization. arXiv preprint arXiv:1810.08750, 2018.

- FS [97] Yoav Freund and Robert E Schapire. A decision-theoretic generalization of on-line learning and an application to boosting. Journal of computer and system sciences, 55(1):119–139, 1997.

- GFB+ [11] Mikel Galar, Alberto Fernandez, Edurne Barrenechea, Humberto Bustince, and Francisco Herrera. A review on ensembles for the class imbalance problem: bagging-, boosting-, and hybrid-based approaches. IEEE Transactions on Systems, Man, and Cybernetics, Part C (Applications and Reviews), 42(4):463–484, 2011.

- HNSS [18] Weihua Hu, Gang Niu, Issei Sato, and Masashi Sugiyama. Does distributionally robust supervised learning give robust classifiers? In International Conference on Machine Learning, pages 2029–2037. PMLR, 2018.

- HSNL [18] Tatsunori Hashimoto, Megha Srivastava, Hongseok Namkoong, and Percy Liang. Fairness without demographics in repeated loss minimization. In Jennifer Dy and Andreas Krause, editors, International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 1929–1938, Stockholmsmässan, Stockholm Sweden, 10–15 Jul 2018.

- HZRS [16] Kaiming He, Xiangyu Zhang, Shaoqing Ren, and Jian Sun. Deep residual learning for image recognition. In Proceedings of the IEEE conference on computer vision and pattern recognition, pages 770–778, 2016.

- IN [19] Vasileios Iosifidis and Eirini Ntoutsi. Adafair: Cumulative fairness adaptive boosting. CoRR, abs/1909.08982, 2019.

- KH+ [09] Alex Krizhevsky, Geoffrey Hinton, et al. Learning multiple layers of features from tiny images. 2009.

- KLPR [20] Justin Khim, Liu Leqi, Adarsh Prasad, and Pradeep Ravikumar. Uniform convergence of rank-weighted learning. In International Conference on Machine Learning, pages 5254–5263. PMLR, 2020.

- LBC+ [20] Preethi Lahoti, Alex Beutel, Jilin Chen, Kang Lee, Flavien Prost, Nithum Thain, Xuezhi Wang, and Ed Chi. Fairness without demographics through adversarially reweighted learning. Advances in Neural Information Processing Systems, 33, 2020.

- LLWT [15] Ziwei Liu, Ping Luo, Xiaogang Wang, and Xiaoou Tang. Deep learning face attributes in the wild. In Proceedings of the IEEE international conference on computer vision, pages 3730–3738, 2015.

- LMKA [16] Jeff Larson, Surya Mattu, Lauren Kirchner, and Julia Angwin. How we analyzed the compas recidivism algorithm. ProPublica (5 2016), 9(1), 2016.

- MHN [21] Paul Michel, Tatsunori Hashimoto, and Graham Neubig. Modeling the second player in distributionally robust optimization. In International Conference on Learning Representations, 2021.

- MRT [18] Mehryar Mohri, Afshin Rostamizadeh, and Ameet Talwalkar. Foundations of machine learning. MIT press, 2018.

- RWG [07] Gunnar Rätsch, Manfred K Warmuth, and Karen A Glocer. Boosting algorithms for maximizing the soft margin. Advances in neural information processing systems, 20:1585–1592, 2007.

- RWST [05] Gunnar Rätsch, Manfred K Warmuth, and John Shawe-Taylor. Efficient margin maximizing with boosting. Journal of Machine Learning Research, 6(12), 2005.

- Sch [90] Robert E Schapire. The strength of weak learnability. Machine learning, 5(2):197–227, 1990.

- Sch [03] Robert E Schapire. The boosting approach to machine learning: An overview. Nonlinear estimation and classification, pages 149–171, 2003.

- Shi [00] Hidetoshi Shimodaira. Improving predictive inference under covariate shift by weighting the log-likelihood function. Journal of statistical planning and inference, 90(2):227–244, 2000.

- SKHL [20] Shiori Sagawa, Pang Wei Koh, Tatsunori B. Hashimoto, and Percy Liang. Distributionally robust neural networks for group shifts: On the importance of regularization for worst-case generalization. In International Conference on Learning Representations, 2020.

- SL [09] Chunhua Shen and Hanxi Li. A duality view of boosting algorithms. CoRR, abs/0901.3590, 2009.

- SRKL [20] Shiori Sagawa, Aditi Raghunathan, Pang Wei Koh, and Percy Liang. An investigation of why overparameterization exacerbates spurious correlations. In Hal Daumé III and Aarti Singh, editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 8346–8356. PMLR, 13–18 Jul 2020.

- WGV [08] Manfred K Warmuth, Karen A Glocer, and SVN Vishwanathan. Entropy regularized lpboost. In International Conference on Algorithmic Learning Theory, pages 256–271. Springer, 2008.

- XDKR [20] Ziyu Xu, Chen Dan, Justin Khim, and Pradeep Ravikumar. Class-weighted classification: Trade-offs and robust approaches. In Hal Daumé III and Aarti Singh, editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 10544–10554. PMLR, 13–18 Jul 2020.

- ZDKR [21] Runtian Zhai, Chen Dan, Zico Kolter, and Pradeep Ravikumar. Doro: Distributional and outlier robust optimization. In Marina Meila and Tong Zhang, editors, Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pages 12345–12355. PMLR, 18–24 Jul 2021.

- ZK [16] Sergey Zagoruyko and Nikos Komodakis. Wide residual networks. arXiv preprint arXiv:1605.07146, 2016.

Appendix A Proofs

A.1 Proof of Proposition 1

We have the following relationship: . Thus, because , so .

If , then for all , we have . Thus, . ∎

A.2 Proof of Proposition 2

For a deterministic model , we have . For a randomized model such that , we have and

| (10) | ||||

Thus, . ∎

A.3 Derivation of the Primal-Dual Formulation of -LPBoost

The primal problem of -LPBoost is

| (11) | ||||

| s.t. |

Introducing slack variables , the primal problem can be written as a linear program:

| (12) | ||||

| s.t. | ||||

The Lagrangian of this problem is

| (13) | ||||

The dual problem is . In order to ensure that , we need

| (14) |

Under these conditions, we have . Let , then the dual problem becomes

| (15) | ||||

| s.t. | ||||

which is equivalent to (5).

Connection to Original LPBoost.

The original soft-margin LPBoost formulation (Eqn. (4) and (5) in [6]) is:

Dual:

| (16) | ||||

| s.t. | ||||

Primal:

| (17) | ||||

| s.t. | ||||

A.4 Proof of Proposition 3

The proof is based on the following dual formulation of CVaR (see Example 3 in [8]):

| (18) |

So we have

| (19) | ||||

since is defined as the zero-one loss of model over . And since the primal problem finds the that maximizes , achieves the maximum above. ∎

A.5 Proof of Theorem 5

Consider an expert problem where there are experts such that the loss of expert at round is (e.g. let the prediction of expert at round be , and let the loss function be ). A weighted average forecaster randomly samples an expert according to the weights at round , and its average loss is . Then Algorithm 2 satisfies for all , so by Theorem 2.2 in [4] we have

| (20) |

By assumption, for all we have . With , we have

| (21) |

Let , then . Finally, note that the -CVaR zero-one loss of the ensemble model is upper bounded by . ∎

Appendix B Experiment Details

On the COMPAS dataset, we use a three-layer feed-forward neural network activated by ReLU as the classification model. For optimization we use momentum SGD with learning rate 0.01 and momentum 0.9. The batch size is 128. We warmup the model for 3 epochs, and each base model is trained for 500 iterations, with the learning rate 10x decayed at iteration 400.

On the CelebA dataset, we use a ResNet18 as the classification model. For optimization we use momentum SGD with learning rate 0.001, momentum 0.9 and weight decay 0.001. The batch size is 400. We warmup the model for 5 epochs, and each base model is trained for 4000 iterations, with learning rate 10x decayed at iteration 2000 and 3000.

On each of the Cifar-10/Cifar-100 dataset, we take out 5000 samples from the training set and make them the validation set. The remaining 45000 training samples consist the training set. We use a WRN-28-1 on Cifar-10 and a WRN-28-10 on Cifar-100. For optimization we use momentum SGD with learning rate 0.1, momentum 0.9 and weight decay 0.0005. The batch size is 128. For Cifar-10, we warmup the model for 20 epochs, and each base model is trained for 5000 iterations, with the learning rate 10x decayed at iteration 2000 and 4000. For Cifar-100, we warmup the model for 40 epochs, and each base model is trained for 10000 iterations, with the learning rate 10x decayed at iteration 4000 and 8000.

On all datasets and for all , we use for -AdaLPBoost.