Cubature Method for Stochastic Volterra Integral Equations

Abstract

In this paper, we introduce the cubature formula for Stochastic Volterra Integral Equations. We first derive the stochastic Taylor expansion in this setting, by utilizing a functional Itô formula, and provide its tail estimates. We then introduce the cubature measure for such equations, and construct it explicitly in some special cases, including a long memory stochastic volatility model. We shall provide the error estimate rigorously. Our numerical examples show that the cubature method is much more efficient than the Euler scheme, provided certain conditions are satisfied.

MSC2020. 60H20, 65C30, 91G60

Keywords. Stochastic Volterra integral equations, cubature formula, stochastic Taylor expansion, fractional stochastic volatility model, rough volatility model

1 Introduction

Consider a stock price in a Brownian setting under risk neutral measure :

| (1.1) |

In the Black-Scholes model, the volatility process is a constant. There is a large literature on stochastic volatility models where is also a diffusion process, see e.g. Fouque-Papanicolaou-Sircar-Solna [19]. Strongly supported by empirical studies, the fractional stochastic volatility models and rough volatility models have received very strong attention in recent years, where satisfies the following Stochastic Volterra Integral Equation (SVIE):

| (1.2) |

Here is another Brownian motion possibly correlated with , ’s are appropriate deterministic functions, and the deterministic two time variable function has a Hurst parameter in the sense that and when is small. Such a model was first proposed by Comte-Renault [10] for , to model the long memory property of the volatility process. Another notable work is Gatheral-Jaisson-Rosenbaum [23], which finds market evidence that volatility’s high-frequency behavior could be modeled as a rough path with . We remark that one special case of (1.2) is the fractional Brownian motion, where and , see, e.g. Nualart [44].

Our goal of this paper is to understand and more importantly to numerically compute the option price in this market: assuming zero interest rate for simplicity,

| (1.3) |

Note that the volatility process in (1.2) is in general neither a Markov process nor a semimartingale111When , is actually a semimartingale, see e.g. [51]. However, it is still highly non-Markovian, so the numerical challenge remains in this case.. Consequently, is highly non-Markovian, in the sense that one cannot Markovianize it by adding finitely many extra states, and correspondingly the option price is characterized as a path dependent PDE (PPDE, for short), see Viens-Zhang [51]. This imposes significant challenges, both theoretically and numerically. Indeed, compared to the huge literature on numerical methods for PDEs, there are very few works on efficient numerical methods for such PPDEs. Besides the standard Euler scheme Zhang [55], we refer to Wen-Zhang [53] for an improved rectangular method; Jacquier-Oumgari [31] and Ruan-Zhang [50] on numerical methods for high dimensional (nonlinear) PPDEs driven by SVIEs; Richard-Tan-Yang [48, 49] on discrete-time simulation schemes, including the Euler and Milstein schemes, and the corresponding Multi-Level Monte-Carlo method; Ma-Yang-Cui [41] by using Markov chain approximation; and Alfonsi-Kebaier [1], Bayer-Breneis [3], and Harms [29] by using Laplace transform for singular kernel functions. In recent years, there has also been a growing interest on the convergence analysis and error estimates for stochastic Volterra integral equations, see, e.g. Bayer-Fukasawa-Nakahara [4], Bayer-Hall-Tempone [5], Bonesini-Jacquier-Pannier [8], Friz-Salkeld-Wagenhofer [20], Fukasawa-Ugai [21], Gassiat [22], Li-Huang-Hu [35], and Nualart-Saikia [45]. In this paper, we propose the cubature method for the above option price (1.3). This is a deterministic method, and our numerical examples show that, under certain conditions, it is much more efficient than the simulation methods such as the Euler scheme.

The cubature method was first introduced by the seminal works Lyons-Victoir [40] and Litterer-Lyons [37] for diffusion processes, see also Gyurkó-Lyons [26], Litterer-Lyons [38], Ninomiya-Shinozaki [42], and Ninomiya-Victoir [43] for its extensive numerical implementations. The method builds upon the stochastic Taylor expansion for smooth :

| (1.4) |

see, e.g. Kloeden-Platen [34], where is a linear combination of multiple integrals against the Brownian motion (typically in Stratonovich form), called the signatures of , and is the remainder term. The main idea is to introduce a discrete measure to match the expectations of the signatures: recalling that is the expectation under ,

| (1.5) |

Then we will have an approximation . Since is discrete and it is easy to compute the exact value of (without involving simulations), the algorithm is very efficient, provided sufficient technical conditions to make the approximation error small enough.

In this paper we shall consider the general SVIE, see (2.1) below, and our goal is to approximate . To introduce the cubature method for , our first step is to derive the stochastic Taylor expansion in this setting. Note that (1.4) relies heavily on the Itô formula, but the solution to the SVIE is not a semimartinagle, which prohibits us from applying the Itô formula directly. To overcome this difficulty, we utilize an auxiliary two time variable process introduced by Wang [52] and Viens-Zhang [51], see (2.6) below. This process satisfies and enjoys the desired semimartingale property: for fixed , the process is a semimartingale. In particular, [51] established a functional Itô formula, which enables us to derive the desired stochastic Taylor expansion, with more involved signatures for the SVIEs than the diffusion case. We then introduce a discrete cubature measure for , in the pirit of (1.4) and (1.5), and prove the following error estimate: for some constant which depends on the regularity of the coefficients,

| (1.6) |

The above result is desirable only when is small. For general , we follow the idea of [40, Theorem 3.3] and utilize the flow property of the path dependent value function established in [51]. To be precise, we consider a uniform partition of : , and construct a cubature measure on each subinterval . Let be the independent composition of , we then have the following estimate:

| (1.7) |

where is independent of . The above estimate clearly converges to as .

We remark that, while our stochastic Taylor expansion can be developed for any kernel with Hurst parameter , the cubature formula becomes much more subtle when . In this paper we restrict to the case , and leave the case to future study. For applications, we refer to Comte-Renault [10] for the long memory model with , Gulisashvili-Viens-Zhang [24] for the integrated variance model with , and El Omari [15] for the mixed fractional Brownian motion model with more general . We also refer to Beran [6, Section 4.2] for applications in hydrology, Loussot-Harba-Jacquet-Benhamou-Lespesailles-Julien [39] for applications in image processing, Gupta-Singh-Karlekar [25] for applications in signal classification, Blu-Unser [7] for fractional spline estimators, and Perrin-Harba-Berzin Joseph-Iribarren-Bonami [47] for the theory of higher order fractional Brownian motions with general . However, we should point out that our result does not cover the rough volatility models in Gatheral-Jaisson-Rosenbaum [23] with . Moreover, the estimates (1.6) and (1.7) require the coefficients to be sufficiently smooth, as we will specify in the paper. In particular, the constant will depend on such regularity.

The efficiency of our cubature method comes down to the construction of the cubature measure in (1.7), which will involve deterministic paths for some constant . When the dimension of is large, or when is large, the will be large; and when is large, in light of (1.7) we will require to be large. We refer to §7.5 for more precise comments on the efficiency issue. When all the conditions are satisfied so that is at a reasonable level, our numerical examples show that the cubature method is much more efficient than the Euler scheme.

We should remark that the above efficiency issue was already present for the cubature method in the standard Brownian setting. There have been great efforts in the literature to overcome this difficulty and to apply the idea of the cubature method to more general models, see, e.g., Crisan-Manolarakis [11, 12], Crisan-McMurray [13], Raynal-Trillos [14], Filipović-Larsson-Pulido [16], Foster-Lyons-Oberhauser [17], Foster-Reis-Strange [18], and Hayakawa-Oberhauser-Lyons [30]. It will be very interesting to explore if these ideas can help to improve the cubature method in the Volterra framework. We would also like to mention the very interesting connection between the signature, the kernel method, and machine learning, see Chevyrev-Oberhauser [9], Kidger-Bonnier-Arribas-Salvi-Lyons [32], Kiraly-Oberhauser [33], Liao-Lyons-Yang-Ni [36], and the references therein.

Finally, we note that, while sharing many properties, the SVIE (1.2) is different from the following SDE driven by a fractional Brownian motion :

| (1.8) |

We refer to Baudoin-Coutin [2] and Passeggeri [46] for some works on signatures for fractional Brownian motions, and Harang-Tindel [27, 28] on signatures defined for “ Volterra path”. We shall remark that, unlike our signature which is directly for the solution to the SVIE (1.2) (instead of for the driving Brownian motion ), these signatures are for the driving fractional Brownian motion or “Volterra path” which has much simpler structure. In particular, their signatures do not lead to the desired stochastic Taylor expansion which is crucial for the cubature method.

The rest of the paper is organized as follows. In §2 we derive the stochastic Taylor expansions for the general SVIEs and prove the tail estimate. In §3 we introduce the cubature formula when is small, and in §4 we modify the cubature formula when is decomposed into parts. We construct the cubature measure explicitly for a one dimensional SVIE in §5 , and for the -dimensional fractional stochastic volatility model in §6. In §7 we present various numerical examples and compare its efficiency with the Euler scheme. Finally, we present some technical proofs in Appendix.

2 Stochastic Taylor expansions

Throughout this paper, let be a filtered probability space, , and a -dimensional Brownian motion. Let be a fixed terminal time. We consider -dimensional state process solving the following SVIE under Stratonovich integration : given ,

| (2.1) |

and we are interested in the efficient numerical computation of

| (2.2) |

Throughout the paper, the following hypotheses will always be enforced: for some which will be specified in contexts,

(H0) Each is infinitely smooth on , and either or has Hurst parameter , that is, and when is small.

(HN) The functions with all the derivatives up to the order bounded.

For later purpose, we will also need the following stronger version of (H0).

(H0-N) Each is infinitely smooth on , and either or has Hurst parameter , in the sense that when is small, for all integers such that .

Remark 2.1.

(i) When has Hurst parameter , is Hölder- continuous in for any small . This implies that for any smooth function , where denotes the Itô integral, and they coincide with the Young’s pathwise integral. On the other hand, when , is clearly a semimartingale. So, letting denote the set of such that , we may rewrite (2.1) in Itô’s form, and in particular they are wellposeded under (H0) and (H2):

| (2.3) |

(ii) Consider a special case: , , , for . Then we can easily see that . So the system (2.1) actually covers the case that the coefficients depends on the time variable .

Remark 2.2.

(i) In fractional stochastic volatility models, where is interpreted as the volatility (or variance) process of certain underlying asset price, the assumption implies that the volatility has “long memory”, see Comte-Renault [10]. We also refer to [6, 7, 15, 24, 25, 39, 47] for applications and theory when .

(ii) The case , supported by the empirical studies in Gatheral-Jaisson-Rosenbaum [23], has received very strong attention in the mathematical finance literature in recent years. The singularity of in this case will make the theory much more involved, for example one may need to consider the weak solution to (2.1), and consequently the numerical algorithms will be less efficient. We shall leave this important and challenging case to future study.

2.1 The functional Itô formula

Note that is not a semimartingale when , which prohibits us from applying many stochastic analysis tools such as the Itô formula directly. To get around of this difficulty, in this subsection we introduce a functional Itô formula, which is established in Viens-Zhang [51] but tailored for the purpose of this paper.

Denote for each , equipped with the uniform norm. For each and , let denote the Fréchet derivative of . That is, is a linear mapping satisfying:

| (2.4) |

Similarly we may define the second order derivate as a bilinear mapping on :

| (2.5) |

We may continue to define higher order derivatives in an obvious manner, and let denote the set of continuous functions which has uniformly continuous derivatives up to order . Moreover, as in [51] (see also an earlier work [52]), we introduce a two time variable process for :

| (2.6) |

This process enjoys the following nice properties:

-

•

For fixed , the process is an -progressively measurable semimartingale;

-

•

For fixed , the process is -measurable, continuous on , infinitely smooth on , and with “initial” condition . In particular, , a.s.

Then we have the following functional Itô formula, which is essentially the same as [51, Theorem 3.10], but in Stratonovic form instead of Itô form.

Proposition 2.3.

Let (H0) and (H2) hold and for some . Then

| (2.7) |

Here and denote the paths , , respectively.

We now turn to the problem (2.2). For any and , introduce

| (2.8) |

Since is differentiable, by Remark 2.1 (i) it is clear that the above Volterra SDE is wellposed. Moreover,

and we have the following simple result, whose proof is postponed to Appendix.

Proposition 2.4.

Under (H0) and (HN), we have for any . Moreover, all the involved derivatives are bounded by , where depends only on the parameters in (H0) and (HN).

2.2 The stochastic Taylor expansion

Fix , and set , , where . In this subsection we fix and consider the stochastic Taylor expansion of at . We first introduce some notation: for any and ,

| (2.9) |

Assume is sufficiently smooth, by (2.7) we have

| (2.10) | |||

where we used the fact that . Now fix , note that is a semimartingale, and is in . Then

Apply Itô’s formula and plug these into (2.10), we obtain

| (2.11) | |||

The formulae (2.10) and (2.2) are the first order and second order expansions of . For higher order expansions, we introduce the following notation. For any , denote with elements , with elements , and introduce a set of mappings for the indices:

Given , , , and , , denote

| (2.19) |

Note that and here actually depend on , but we omit this dependence for notational simplicity. We then have the following expansion, whose proof is postponed to Appendix.

Proposition 2.5.

For any , under (H0) and (H(N+3)), we have

| (2.20) | |||||

2.3 The remainder estimate

In this subsection we estimate the remainder term in Taylor expansion, which will provide guideline for our numerical algorithm later. For an appropriate function and , denote

| (2.21) |

Moreover, for , , and , denote

| (2.22) |

We first have the following simple but crucial lemma, whose proof is postponed to Appendix.

Lemma 2.6.

Fix , , and let be bounded, jointly measurable in all variables, and, for each , is -measurable in . There exists a universal constant such that, for any ,

| (2.26) | |||

| (2.30) |

Note that and contribute differently in (2.26) and (2.30). Alternatively, we note that is Lipschitz continuous, but is Hölder- continuous for . To provide a more coherent error estimate, we shall modify (2.20) slightly. For any and , denote

| (2.33) |

We then have the following tail estimate, whose proof is postponed to Appendix.

Theorem 2.7.

Let (H0) and (H(N+3)) hold, and be determined by

| (2.36) |

Then there exists a constant , which depends only on and , such that

| (2.37) |

Remark 2.8.

Clearly, for fixed , the error in (2.37) will be smaller when is smaller, when and are smoother (so that is smoother), and when the dimensions and are smaller (so that is smaller). This is consistent with our numerical results later.

3 The cubature formula: the one period case

Note that (2.37) is effective when is small. In this section we consider the case that is small. Then we may simply set and thus . We shall apply the results in §2 with . In particular, in this case . For notational simplicity, in this section we shall omit the superscript 0, e.g. , , and .

3.1 Simplification of the stochastic Taylor expansion

In this case we have: denoting ,

| (3.5) |

Thus (2.36) becomes

| (3.6) |

Moreover, by abusing the notation we may modify and define as follows:

| (3.7) |

Remark 3.1.

Motivated from the Taylor expansion (3.6), the step-N Volterra signature should have the following form in the space :

| (3.8) |

where denotes the canonical basis of . Below, we shall focus on the expectation of the Volterra signature at any step.

To facilitate the cubature method in the next subsection, we shall rewrite (3.6) further slightly. Note that, for fixed , the mapping (as a function of ) is not one to one, so we may combine the terms with the same . That is, we may rewrite (3.6) as:

| (3.12) |

Since it requires rather complicated notations to characterize precisely in the general case, we leave it to the special cases we will actually compute numerically.

3.2 The cubature formula

We now extend the cubature formula for Brownian motion in [40] to the Volterra setting, especially for the Taylor expansion (3.12). From now on, we set the canonical space, the canonical process, and thus is the Wiener measure so that is a -Brownian motion. For some , , we introduce a discrete probability measure on : for some constants , , ,

| (3.16) |

Here, the second line implies that is symmetric, since Brownian motion is symmetric. Also, it is ok to consider non-uniform partition . Recall (2.19), for each piecewise linear as in (3.16), , and , denote

| (3.17) |

Then we have

| (3.18) |

Definition 3.2.

Let , . We say defined in (3.16) is an N-Volterra cubature formula on if, recalling ,

| (3.19) |

We now have the main result of this section, whose proof is postponed to Appendix.

3.3 A simplification of the cubature formula

Due to the symmetric properties of Brownian motion and , we may simplify the requirement (3.19). Recall (2.19) and abuse the notation, for we denote

| (3.26) |

Lemma 3.4.

Let (H0) hold and be such that is odd for some , in particular if is odd, then

| (3.27) |

Proof One may easily derive the first equality from (2.26) by induction on . The second equality follows directly from the symmetric properties of .

Note further that, when , we have . This, together with Lemma 3.4, implies the following result immediately.

Theorem 3.5.

When is odd, note that , so we will get the cubature formula for free at the -th order. Therefore, we shall always consider odd .

Example 3.6.

(i) In the case , obviously we have

| (3.33) |

(ii) In the case , we have:

| (3.36) |

4 The cubature formula: the multiple period case

In this case we consider general , and we use the setting in §2, in particular .

4.1 The cubature formula on each subinterval

Recall (2.36). Note that in (3.6) and are separated and the cubature measure is determined only by . In (2.36), however,

and we are not able to move the term outside of the stochastic integral, which prohibits us from constructing a desirable to match the conditional expectations of : . In light of (2.37), we shall instead content ourselves with

| (4.1) |

We shall remark though, in general conditional expectations are only defined in a.s. sense, which requires specifying the probability on . However, here we will construct only on the paths on . For this purpose, we interpret the conditional expectations in a pathwise sense, as we explain in the remark below, so that (4.1) could make sense.

Remark 4.1.

Under our conditions, one can easily see that , for a deterministic function . Similarly, for the we are going to construct, we will interpret it as a regular conditional probability distribution and thus we also have the structure for a deterministic function . Then by (4.1) we actually mean a stronger result:

| (4.2) |

We refer to [54, Chapter 9] for more details of the pathwise stochastic analysis. In this paper, since our main focus is the approximation, to avoid introducing further complicated notations, we abuse the notation slightly and write them as conditional expectations.

From now on, we shall assume is sufficiently smooth in . Then, recalling (2.6), the mapping is smooth: for any ,

| (4.3) |

Then the mapping is also smooth. Our idea is to introduce further the Taylor expansion of at . For any with , denote and . Then by the standard Taylor expansion formula we have, for any ,

| (4.6) |

We now extend Theorem 2.7. Recall Lemma 3.4 and Theorem 3.5.

Theorem 4.2.

Let be odd and (H0-), (H(N+3)) hold. Let be determined by:

| (4.7) | |||

Then, there exists a constant , which depends on , , and the upper bounds of and their derivatives up to the order , such that

| (4.8) |

Proof For each , noting that is even and is odd, set . Using the notations in (4.6), one can see that involves the derivatives of and up to the order , and the derivatives of up to the order . Note that , then

Recall Proposition 2.4 for the bounds of the derivatives of . Now following the arguments in Theorem 2.7, one can easily see that, for some appropriate constant depending on the parameters specified in this theorem,

This implies (4.8) immediately.

Definition 4.3.

Let be odd and fix . We say defined in (4.12) is a modified -Volterra cubature formula on if, for all , , and ,

| (4.13) |

Remark 4.4.

(i) The equations in (4.13) corresponding to exactly characterize the cubature measures for Brownian motions. That is, our modified -Volterra cubature formula is a cubature formula for the standard one, but not vice versa in general. In the case , however, as we will see in Example 4.6 (i) below, the two are equivalent.

(ii) The kernel in (4.13) is rescalable in the sense of (3.25). Then by the same arguments as in Theorem 3.3, is independent of (or ). Indeed, as in (8.16) below, is a modified N-Volterra cubature formula on if and only if the following is a modified N-Volterra cubature formula on :

| (4.17) |

We emphasize that is universal in the sense that it depends only on , the dimensions, and our construction of the cubature measure, but does not depend on or even . In particular, is independent of , , or , and .

Theorem 4.5.

This proof is also postponed to Appendix.

4.2 The cubature formula on the whole interval

Recall is defined on . We shall now compose all the :

| (4.29) |

Here refers to independent composition. Then is a probability measure on . Similarly let denote the Wiener measure on , then . The following result extends [40, Theorem 3.3] to our setting.

Theorem 4.7.

Let be odd and (H0-), (H(N+4)) hold, and is defined by (4.29) with each as in Definition 4.3. Then, for the in Theorem 4.5 and in Remark 4.4, we have

| (4.32) |

Moreover, for a possibly larger which may depend on the bounds of the derivatives of up to the order , and the , but not on , we have222 The constant below is due to the estimate for the derivatives of in Proposition 2.4. If one can improve this estimate, under certain technical conditions, then one can replace with the new bound for the derivatives of up to the order . This comment is valid for the estimates in (4.8) , (4.20), (4.32) as well.

| (4.33) |

which converges to as .

Proof Note that, recalling (2.8).

Recall Remark 4.1 and note that , then by (4.2) we see that (4.32) follows directly from (4.20). Finally, by (2.19), (2.33), and Proposition 2.4 we obtain (4.33).

Remark 4.8.

(i) Compared to Theorem 3.3, the above Theorem 4.7 allows us to deal with large . Moreover, compared with the in (3.32), it is easier to construct the cubature measure in (4.13) and the in (4.29). The price to pay, however, is that (4.13) requires higher regularity of in order to have the desired convergence rate.

(ii) Provided sufficient regularity (H0-) on and (H(N+4)) on and , we have the convergence and its rate in (4.33) as , which is very desirable in theory. However, by (4.12) and (4.29), we see that each will involve paths, and thus the independent composition will involve paths. Therefore, practically we still don’t want to make too large, which in turn means that cannot be too large. We note that the same difficulty arises in the Brownian setting, and there have been various ideas on improving the efficiency, for example the recombination schemes in [30, 38]. It will be very interesting to explore these ideas and see if they can be extended to the Volterra setting.

(iii) Note that the choice of is not unique. In particular, (4.13) involves certain number of equations. To make it solvable, we need to allow for sufficient number of parameters , , , . As mentioned in (ii), the complexity of our cubature algorithm increases dramatically for large , but is much less sensitive to the value of . So whenever possible, we would prefer a small while allowing for a reasonably large . We shall remark that, when the dimension is large, typically we need a large . This consideration is not serious for the one period case, which however requires to be small.

(iv) Clearly we have a better rate for a larger (again, provided sufficient regularity). However, a larger implies more equations in (4.13), which in turn requires larger values of and/or . In the meantime, a larger implies a larger in (4.33). So the algorithm may not be always more efficient for a larger .

5 A one dimensional model

In this section we focus on the following model with :

| (5.1) |

where the Brownian motion is one dimensional and the Hurst parameter . We investigate a few cases in details and compute the desired . We shall illustrate the efficiency of our algorithm in these cases by several numerical examples in §7 below.

Note that in this case , then there is no need to consider . So, for , by abusing the notation we may view , . We may omit , inside and in (2.19).

5.1 The multiple period case with order

We shall construct as in (4.12) for a fixed . In the numerical examples in §7, we may simply compose these independently as in (4.29).

In this case (4.21) consists of only one equation:

| (5.2) |

To construct , we set and in (4.12):

| (5.3) |

Then (5.2) becomes

Thus

| (5.4) |

We remark that the above computation does not involve , in fact, as we saw in Example 4.6 (i), the cubature measure in this case coincides with that of standard Brownian motion. However, in order to have the desired error estimate, by Theorem 4.5 we need .

5.2 The multiple period case with order

While we may apply (4.28) directly, in this one dimensional case actually we may simplify the problem further. Note that the corresponding term which requires the further expansion (4.6) or (4.7) is: recalling (2.2) and abusing the notation ,

For , we shall assume (H0-2), namely , then . Thus

Note that , then

This leads to the following expansion:

where satisfies the desired estimate. Consequently, we may merge the 2 equations in the second line of (4.28) into one equation, in the same spirit of (3.12), by considering only their sum. Therefore, in this case (4.28) reduces to three equations:

| (5.8) |

To construct , we set and in (4.12):

| (5.9) |

Note that, in light of Remark 4.8, we would prefer a small . However, if we set here, the cubature measure does not exist for any value . By straightforward calculation we see that (5.8) becomes

| (5.10) |

In particular, the first two equations coincide, and we obtain

| (5.11) |

This requires so that . Then for any , we would obtain a solution by (5.11). One particular solution is:

| (5.12) |

We remark that, in this case , so we actually have a total of three paths, instead of four paths: by abusing the notation ,

| (5.13) |

5.3 The one period case with order

Recall (3.31) and (3.33), in particular we shall only consider . Then one can verify straightforwardly that,

| (5.17) |

By (2.26), one can easily compute that

| (5.18) |

To construct , we set and in (3.16) :

| (5.19) |

For notational simplicity, we introduce

| (5.20) |

Then one may compute:

| (5.23) |

where

| (5.27) |

Combining (5.18) and (5.23), we obtain from (3.19) that

| (5.28) |

First by the second equation we obtain (we may use the other one as well):

| (5.29) |

Plug this into the first equation in (5.28) we obtain one solution:

| (5.30) |

Example 5.1.

5.4 The one period case with order

Recall (3.31) and (3.36), in particular we shall only consider and . Clearly , for the in (5.17). Moreover, again omitting ,

Recall (5.20) and the Gamma function , and denote by the -th derivative of . We then have the following result.

Lemma 5.2.

For the above model, we have , where

| (5.33) |

Moreover, denote , we have

| (5.36) |

Proof Note that ,

| (5.42) |

By (3.5) one can check that , , . Then, by (2.26),

Now the expectations in (5.36) follow from straightforward computation.

We next construct a desired . Note that (3.32) consists of equations for and equations for . To allow for sufficient flexibility, we set and in (3.16):

| (5.44) |

Similar to (5.23), the following result is obvious.

Lemma 5.3.

Theorem 5.4.

(3.19) is equivalent to the following equations:

| (5.58) |

We remark that (5.58) consists of equations, with unkowns: , , . Since these equations are nonlinear, in particular they involve -th order polynomials of , in general we are not able to derive explicit solutions as in (5.30). Indeed, even the existence of solutions is not automatically guaranteed, and in that case we can actually increase and/or in (5.44) to allow for more unknowns. Nevertheless, we can solve (5.58) numerically, and our numerical examples in the next section show that the numerical solutions of (5.58) serve for our purpose well.

6 A fractional stochastic volatility model

Consider a financial market where denotes the underlying asset price and is the volatility process:

| (6.3) |

Here are correlated Brownian motions with constant correlation , with Hurst parameter . Assume for simplicity the interest rate is , and our goal is to compute the option price .

Note that (6.3) involves the time variable , so we are in the situation with and in (2.1). Indeed, denote , then we have

| (6.6) |

Here, for notational simplicity, we use indices instead of for . We shall emphasize that, although are correlated here, the Taylor expansions (2.20) and (2.36) will remain the same, but the expectations in Lemma 2.6 need to be modified in an obvious way. In particular, (3.27) will hold true only when is odd. Therefore, in this section we modify the in (3.31): still denoted as by abusing the notation,

| (6.7) |

Then all the results in the previous sections remain true. Alternatively, we may express as linear combinations of independent Brownian motions. However, this will make more complicated and does not really simplify the analysis below.

6.1 The multiple period case with

By (6.7), we see that

Thus the cubature measure should satisfy: for ,

| (6.8) |

This is the same as the Brownian motion case. More precisely,

| (6.11) |

To construct , we set and in (4.12): noting that is -dimensional,

| (6.12) |

Plug these into (6.11), we have

| (6.13) |

One can easily solve the above equations:

| (6.16) |

6.2 The one period case with

We first note that, due to the multiple dimensionality here, the system corresponding to (3.32) will be pretty large, especially when in the next subsction. However, since are not of Volterra type, the system can be simplified significantly. Furthermore, we shall modify the cubature method slightly as follows.

Remark 6.1.

Recall that in (3.12) and (3.31) we group the terms with the same . Note that the mapping is also not one to one, and since , many terms do not appear in the Taylor expansion (or say the corresponding ). It turns out that it will be more convenient to group the terms based on for this model, as we will do in this and the next subsections. To be precise, let denote the terms with appearing in the Taylor expansion, and . We emphasize that, unlike in (3.12), the elements here are not . We then modify Definition 3.2 by replacing (3.19) with:

| (6.17) |

We remark that, if (as random variables), then automatically we have for all in (3.16).

Recall (6.7) that Lemma 3.4 remains true when is odd, we shall only find . Instead of applying the Taylor expansion (3.6) directly on (6.3), we first expand as in (3.6). Indeed, note that , where

| (6.18) |

Then, applying the chain rule we have: denoting and ,

| (6.21) |

Here is a generic term whose order is not equal to . Then, recalling Remark 6.1, by (6.6) we can easily obtain

| (6.26) |

We remark that this solution is independent of . In fact, numerical results (which are not reported in the paper) show that this does not provide a good approximation, even when is small. So we shall move to the order in the next subsection, although it becomes much more involved to find the cubature measure.

6.3 The one period case with

In this case, besides the in (6.26), we also need . For this purpose, we need the -nd order expansion of and the -rd order expansion of . These derivations are straightforward, but rather tedious. We thus postpone them to Appendix and turn to numerical examples first.

7 Numerical examples

7.1 The algorithm

Our numerical algorithm consists of the following five steps. We are illustrating only the algorithm in §5.4. The algorithms in the other subsections, especially those in §6, need to be modified slightly in the obvious manner.

Step 3. Establish the equations (3.32) with unknowns , , , from (3.16), then solve these equations to obtain a desired . We may in general use numerical methods to solve these (polynomial) equations, when explicit solutions are not available, see Remark 7.1 below.

Step 4. For each obtained in Step 3, solve the (deterministic) ODE (3.21), by discretizing equally into pieces. That is, denoting and ,

| (7.1) |

For convenience, we typically set as a multiple of for the in (3.19).

Step 5. We obtain the approximation by (3.20): .

We note that, provided the conditions in Remark 2.8, our algorithm is deterministic and is much more efficient than the probabilistic methods, e.g. the Euler scheme in Zhang [55].

Remark 7.1.

(i) In Subsections 5.1, 5.2, 5.3, 6.1, 6.2, we have obtained the cubature paths, then we can move to Step 4 directly.

(ii) We remark that Steps 1-3 depend only on the model, more specifically only on , but not on the specific forms of or . So, given the model, we may compute the desired offline, and then for each and , we only need to complete Steps 4 and 5.

(iii) To illustrate the idea for Step 3, we consider the equations in (5.58). We shall use the steepest decent method to minimize the following weighted sum:

where , and , are some appropriate weights.

(iv) For (iii) above, we may replace it with any efficient solver for equations (5.58).

Remark 7.2.

In this paper we focus on the impacts of and , but do not analyze rigorously the impact of (or ) in Step 4, which can be chosen much larger than . We shall only comment on it heuristically in this remark.

(i) First, by (7.1) and in particular due to the path dependence, it is clear the running time of the algorithm grows quadratically (rather than linearly) in .

(ii) By standard arguments, under mild regularity conditions one can easily show that

So there is a balance between the quadratic running cost and this error estimate. Theoretically, given an error level , we shall choose the parameters , and which satisfy and minimize the computational cost. Since the algorithm is much more sensitive to than to , we content ourselves in this paper to choose a reasonably large and we identify with to emphasize the dependence on . Indeed, our numerical results show that the total error is not sensitive to , see Example 7.7 below.

In the rest of this section, all the numerics are based on the use of Python 3.7.6 under Quad-Core Intel Core i5 CPU (3.4 GHz). For the running time, we use and to denote second and millisecond, respectively.

7.2 An illustrative one dimensional linear model

In this subsection we present a one dimensional numerical example:

| (7.2) |

In this case, Normal, so essentially we can compute the true value of :

| (7.3) |

We use , , and to denote the values computed by using the one period cubature formula, the multiple period cubature formula with periods, and the Euler scheme, respectively. We shall compare our numerical results with this true value. In particular, since the cubature method is deterministic, while is random, we shall explain how we compare the numerical results of the cubature methods with .

Our first example shows that, when is small, the one period method in (3.32) is more efficient than the multiple period method in (4.13) with , especially when is small. We remark that, although , (3.32) and (4.13) have different kernels and thus have different cubature paths.

Example 7.3.

Consider (7.2) with and . Then, with order ,

| (7.4) |

We see that the last error is small when is small or is large. However, it is still larger than the error of which is in this case.

Proof First, by (7.3) it is clear that .

However, for the multiple period cubature method with and , by (5.3) and (5.4) we have: by abusing the notations ,

Our next example shows that, when is large, the one period algorithm fails, but the multiple period algorithm does converge when becomes large, as we expect.

Example 7.4.

Consider (7.2) with , , , . We compute the value from the one period model with and from the multiple period model with and from to . The cubature paths are constructed as in Example 7.3, with in Step 4. Numerical results are reported in Table 1.

We remark that, here the function is not as smooth as required in Theorems 3.3 and 4.7. Nevertheless we see from the numerical results that the cubature method still works well.

We now present an example to compare the accuracy between and .

Example 7.5.

We note that, although we have a better rate of convergence in Theorem 4.7 when , the numerical results in this example do not show such improvement. One explanation is that the constant in (4.33) becomes larger when we increase , see Remark 4.8 (iv). The numerical results for the one period cubature method does not show significant improvement either when we increase the order from to . However, for the fractional stochastic volatility model (6.3), as we saw in §6.2, the one period cubature method with does not depend on at all, and thus it is clearly not as good as the one period cubature method with .

Our next example compares the one period cubature method with the Euler scheme. More examples concerning this comparison will be presented in the next two subsections.

Example 7.6.

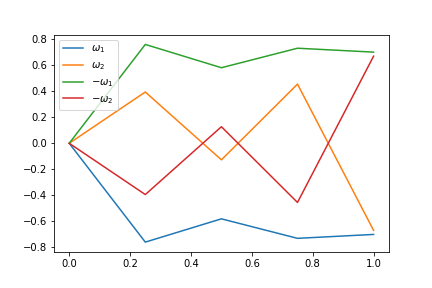

We now explain the numerical results in Table 3. First, in this case . Next, by solving (7.1) numerically, we report the approximate solution of (5.58) in Table 4, see also Figure 1 for the plot of the four approximate cubature paths (after rescaling to ). We then obtain . In Table 3, the cubature error . The reported running time is for Steps 4 and 5 only, since Steps 1-3 can be completed offline once for all.

| (cubature time) | (ms) | (ms) | (ms) |

| (Euler time) | (ms) | 0.00156 (ms) | (ms) |

| (percentile) | 0.0026 () | 0.00119 () | 0.00081 () |

For the Euler scheme, we also set time discretization step . Let denote the sample size in Euler scheme, namely the number of simulated paths of the Brownian motion. Clearly both the approximate value and the running time depend on , in particular, the latter is proportional to . Note that is random. We repeat the Euler scheme times, each with sample size , and obtain and the corresponding Euler scheme errors , . We shall use the sample median of to measure the accuracy of the Euler scheme. We can then compare and , and to have a more precise comparison, we will actually compute the percentile of the cubature error among the Euler scheme errors : -percentile means about of are smaller than . So roughly means and the two methods have the same accuracy; while means that and the cubature method has better accuracy: the smaller is, the better the cubature method outperforms. Moreover, since are i.i.d., we may use the Normal approximation to compute the percentile. We will report their mean and standard deviation , and then the percentile , where is the cdf of the standard normal.

For the above example, we test three cases: , and the numerical results are reported in Table 3. As we see, when , the Euler schemes takes milliseconds (for each run, not for runs), which is about times slower than the milliseconds used for the cubature method, and the percentile of the cubature method is . So the cubature method outperforms the Euler scheme both in running time and in accuracy. When we increase the sample size to , the percentile increases to , so the cubature method still outperforms in accuracy. In this case the running time of the Euler scheme increases to milliseconds, which is about times slower than the cubature method. On the other hand, if we decrease the sample size to , the running time of the Euler scheme drops to milliseconds, which is still times slower than the cubature method, but the accuracy deteriorates further with a percentile . So in all three cases, the cubature method outperforms the Euler scheme significantly both in running time and in accuracy.

We conclude this subsection with an example concerning the impact of .

Example 7.7.

Consider the same setting as in Example 7.6, but we try three different ’s. The numerical results are shown in Table 5.333The running time for the Euler scheme grows quadratically in , as expected. However, the running time for the cubature method grows slower than quadratically, especially when is not that large. This is possibly because in our code, for the sake of readability, there is a relatively time consuming step whose cost grows linearly in . The efficiency of our cubature method could be improved slightly further, when is small, if we write the code in a more straightforward way.

| (cubature time) | (ms) | (ms) | (ms) |

| (time, ) | (ms) | (ms) | (s) |

| (time, ) | (ms) | (s) | (s) |

| (time, ) | (ms) | (s) | (s) |

As we can see, the cubature method is not sensitive to . The Euler scheme does rely on our choices of and . However, in all the above choices, the cubature method outperforms both in running time and in accuracy.

7.3 A one dimensional nonlinear model

We now consider the following nonlinear model, but still in -dimensional setting:

| (7.5) |

We shall use one period cubature method with when is small, and multiple period cubature method with and appropriate when is large. Our main purpose is to compare the efficiency of the cubature method with that of the Euler scheme.

We first note that, by Remark 7.1 (ii), the cubature paths for (7.5) is the same as those for (7.2). In particular, for the one period method with , we may continue to use the paths in Table 4. For comparison purpose, we will use the same for the cubature method and the Euler scheme. For the in Euler scheme, there is an obvious tradeoff between the running time and the accuracy. While one may try to find an “optimal” for a given , such an analysis relies on a precise idea on the constants involved in the error estimates, as in Remark 7.2 (ii). Since our main focus is the cubature method and since our examples show that the cubature method outperforms significantly (under our strong conditions), we do not go through that analysis. Instead, unless stated otherwise, for simplicity in the rest of this section we shall always set

each time with simulation paths. We use and to compute and . However, in this case we are not able to compute the exact value of as in (7.3). Since the convergence of the Euler scheme approximations is well understood, for comparison purpose we shall set the true value as the sample mean of the Euler scheme approximations:

| (7.6) |

In the first example we show the impact of the regularity of .

Example 7.8.

Consider (7.5) with , , and we consider three different ’s with corresponding . We choose , and compare the one period cubature method with with the Euler scheme. The numerical results are reported in Table 6.

| / | / 1 | / 1 | / 0.56 |

|---|---|---|---|

| 0.5401 | 1.00073 | 0.0617 | |

| 0.5402 | 1.00041 | 0.0601 | |

| (time) | 0.0001(1.75ms) | 0.00032(1.66ms) | 0.0016 (1.63ms) |

| (time) | 0.0008(80.4ms) | 0.00200(82ms ) | 0.00147(75ms) |

| (percentile) | 0.00064(18%) | 0.00149(20.1%) | 0.0011(54.3%) |

As we can see, the cubature method outperforms the Euler scheme in all these three cases. However, when becomes less smooth, the advantage of the cubature method fades away, which is consistent with the theoretical observation in Remark 2.8.

The next example illustrates the impact of .

Example 7.9.

| 0.2 | 0.5 | 0.8 | |

|---|---|---|---|

| 1.00073 | 1.0109 | 1.045 | |

| 1.00041 | 1.0056 | 1.022 | |

| (time) | 0.00032(1.66ms) | 0.0054(5.25ms) | 0.0234(11ms) |

| (time) | 0.00200 (82ms) | 0.0332(445ms) | 0.0152(1.16s) |

| (percentile) | 0.00149(20.1%) | 0.0098(57.4%) | 0.0115(69.4%) |

Again consistent with our theoretical result, the performance of the cubature method decays when gets large. In the above example, the cubature method obviously outperforms the Euler scheme when , and still works better when , but in the case , there is a tradeoff between the speed and the accuracy and it is hard to claim the cubature method is more efficient. In the last case, we shall use the multiple period cubature method, as we do in the next example, and we can easily see that the cubature method outperforms the Euler scheme again.

Example 7.10.

Consider (7.5) with , , and three different ’s with corresponding . We choose , and compare the multiple period cubature method with and with the Euler scheme. The numerical results are reported in Table 8.

| / | / 1 | / 1 | / 0.56 |

| (time) | |||

| (time) | 0.0074(4.2s) | 0.023 (s) | 0.011 (s) |

| (percentile) | (37.37%) | () | () |

7.4 A fractional stochastic volatility model

In this section we consider the following special case of (6.3) with and :

| (7.9) |

Again we will use one period cubature method with when is small, multiple period cubature method with and appropriate when is large, and we shall compare the efficiency between the cubature method and the Euler scheme.

Example 7.11.

| / | / 1 | / 1 | / 0.56 |

| (time) | |||

| (time) | 0.0063 (273ms) | 0.0157(283ms) | 0.0037(272ms) |

| (percentile) | (21.3%) | () | () |

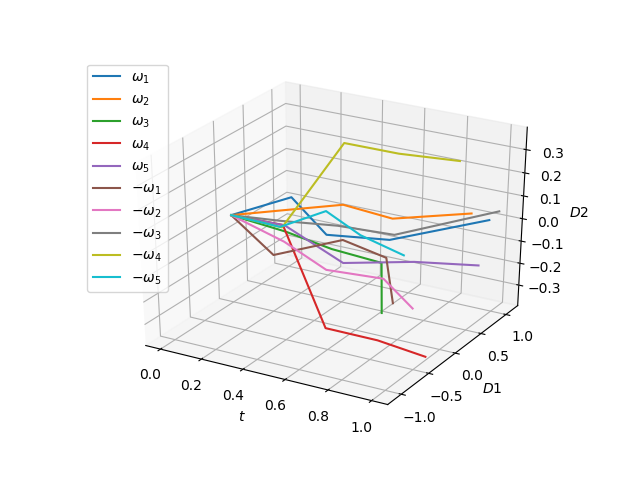

For the cubature method, we first compute the cubature paths following the same idea as in Remark 7.1. By §8.1 below we choose and . Then we obtain

and the paths are plotted in Figure 2 (after rescaling to ).

Example 7.12.

| / | / 1 | / 1 | / 0.56 |

| 0.37897 | 1.4932 | 0.17098 | |

| 0.3698 | 1.4887 | 0.17797 | |

| (time) | |||

| (time) | 0.0119(306ms) | 0.0361(311ms) | 0.007(304ms) |

| (percentile) | 0.0092(40.8%) | 0.0270(19.1%) | 0.0052(50%) |

Example 7.13.

Consider (7.9) with , , , , , and consider three different . We shall compare the efficiency of the multiple period cubature method with , and the Euler scheme. We set . Recalling , for the cubature method we use and in (6.16). We repeat the Euler scheme times (instead of times). The numerical results are reported in Table 11.

| (time) | |||

| (time) | 0.033 (15.8s) | 0.036(15.8s) | 0.037(15.5s) |

| (percentile) | (81.1%) | () | () |

We see that the cubature method outperforms the Euler scheme when and , especially in the latter case, but does not seem to work well when . This is consistent with our theoretical result.

7.5 Some concluding remarks

We first note that, our theoretical convergence analysis for the cubature method, namely Theorems 3.3 and 4.7, is complete, provided sufficient regularities on and (corresponding to ). In particular, it holds true for arbitrary dimensions and arbitrarily large (for Theorem 4.7).

For the numerical efficiency, in its realm, the cubature method has clear advantages over the Euler scheme. In light of Remark 4.8, the cubature method requires the following three conditions though: (i) sufficient regularity, so as to obtain the desired error estimate; (ii) low dimension (and relatively small ), so that can be relatively small; and (iii) not too large , so that can be relatively small. We remark that the standard cubature method in [40] for diffusions also requires these conditions. However, the constraints are more severe in the Volterra setting here, for example, the constant in (4.33) is larger here, and for given dimensions and , there are more equations required in (4.13) and hence we may need a larger . When the number of cubature paths is large (recalling again Remark 4.8 (ii)), it will be interesting to explore if the approach in [11, 12] could help reduce the complexity, which we shall leave for future research. The less smooth case, especially when , requires novel idea to extend our approach.

We shall also remark that the parameters in the cubature method cannot be too big. For the Euler scheme, by increasing the sample size gradually one may improve the accuracy “continuously” at the price of sacrificing the speed. For the cubature method we have only limited choices on and thus lose the flexibility of improving its accuracy “continuously”. Consequently, the cubature method is more appropriate in the situations where one has strong requirement on the speed but is less stringent on the accuracy.

8 Appendix

Proof of Proposition 2.4. Recall (2.8). Following rather standard arguments, we see that exists and has the following representation:

| (8.3) |

We note that at above we need the second derivative of exists so that the Stratonovich integration makes sense. Then we see immediately . By similar arguments we can prove the results for higher order derivatives. In particular, we note that the -th derivative of would involve the -th derivative of .

Proof of Proposition 2.5. We first note that, by Proposition 2.4 , so the right side of (2.20) makes sense.

When , one may verify easily that (2.20) reduces to (2.10), (2.2), respectively. Assume (2.20) holds for . For , , , , we have

Note that, for , by Itô’s formula and Proposition 2.3 we have

| (8.7) |

Then, by Itô’s formula we have, for given , , ,

| (8.8) | |||

Thus, since (2.20) holds for by induction assumption, we have

Then it suffices to show that,

| (8.9) |

Proof of Lemma 2.6. Recall that , the case is obvious. We now assume . Fix and denote

Then, when , we have

coinciding with the Ito integral, and when ,

Proof of Theorem 2.7. First, similar to (2.2) and (2.20), one can verify that

| (8.12) |

Fix , , , and denote for . By (2.30) and (2.33) we may prove by induction that, for , , and for some constant which may depend on ,

In particular, by setting we have

| (8.13) | |||

By (2.33) we have . Moreover, fix . When , we have

Then

When , recalling (2.19) and by (8.7) we have: denoting ,

where, similarly to (8), the last equality can be verified straightforwardly. Then

Thus

So in all the cases, by (8.13) we have

Then, by (8.12) we obtain

This implies (2.37) immediately.

Proof of Theorem 3.3. It is clear that the functional Itô formula (2.7) holds true under as well, then (3.12) and (8.12) also hold true under . Thus, by (3.19),

Therefore, by Theorem 2.7, it suffices to show that

| (8.14) |

Now for each and , as in (8.12), note that

where denotes the time derivative of . Then

| (8.15) |

If , we have . Denote , then , and

If , , then . Denote , then , and

Plug these into (8), we obtain (8.14) immediately, and hence (3.24) holds true.

Finally, when (3.25) holds true, by (3.19) one can easily see that in (3.16) is an N-Volterra cubature formula on if and only if the following rescaled one is an N-Volterra cubature formula on :

| (8.16) |

In particular, this implies that is independent of ,

Proof of Theorem 4.5. Note that

Then, following the same arguments as in Theorem 3.3, it suffices to provide desired estimate for . Similar to Lemma 3.4, by the desired symmetric properties, for any we have

Then, by (4.13) we have

The estimate for is implied by (4.8). Moreover, for each and , again set as in the proof of Theorem 4.2. Then, by (4.6) and similar to (8),

Thus, since ,

Recall , this is the desired estimate.

8.1 The one period cubature formula for (6.3) with

Denote

| (8.17) |

First, similar to (3.6) we have

We remark that , however, thanks to the new convention in Remark 6.1, we do not need to consider and separately. Then we can easily see that the terms in derived from consist of the following stochastic integrals:

| (8.21) |

Note that, for ,

| (8.26) |

Similarly, we may have the expansion of as in (8.1):

| (8.27) | |||

where the terms presented above involve , and contains the terms without :

| (8.28) | |||

Then we see that the terms in derived from are:

| (8.32) |

and

| (8.38) |

where

Note that, for and with , and , we have: recalling (8.17),

| (8.53) |

We note that, by (6.26), (8.21), and (8.32)-(8.38),

| (8.54) |

We now construct a desired as in (3.16). Recall , and . We remark that, the correlation between affects only the expectations in (8.26) and (8.53), but the expectations under in (3.18) remain the same. The integrals against corresponding to the stochastic integrals in (6.26), (8.21), and (8.32)-(8.38) are: for each and for appropriate functions ,

| (8.61) |

For , by (8.54), together with the constraint on , there will be in total equations. In our example (7.9), however, the coefficients are homogeneous, i.e. independent of . Then in (8.1) the terms and thus the two terms , , in (8.32) are not needed (the terms are stilled needed, even though in (8.1), because they appear in the last line of (8.1) as well when ). Therefore, we have a total of equations. We thus set and . Since each -dimensional path involves parameters, plus the parameters , there will be unknowns. For each , by (6.21), (8.1), (8.1), (8.1), one can easily derive from (8.61) the right side of (6.17), as -nd order or -th order polynomials of . This, together with (6.26), (8.26), (8.53), as well as , leads to the required equations, in exactly the same manner as in (5.58). Again, we are not able to solve these equations explicitly, so we will solve them numerically.

References

- [1] A. Alfonsi, and A. Kebaier. Approximation of Stochastic Volterra Equations with kernels of completely monotone type. arXiv preprint arXiv:2102.13505 (2021).

- [2] F. Baudoin and L. Coutin. Operators associated with a stochastic differential equation driven by fractional brownian motions. Stochastic Processes and their Applications, 117(5):550–574, 2007.

- [3] C. Bayer, and S. Breneis. Markovian approximations of stochastic Volterra equations with the fractional kernel. Quantitative Finance 23.1 (2023): 53-70.

- [4] C. Bayer, M. Fukasawa, and S. Nakahara. On the weak convergence rate in the discretization of rough volatility models. SIAM Journal on Financial Mathematics, 13 (2022), pp. 66-73.

- [5] C. Bayer, E. J. Hall, and R. Tempone. Weak error rates for option pricing under the rough Bergomi model. International Journal of Theoretical and Applied Finance, Vol. 25, No. 07n08, 2250029 (2022).

- [6] J. Beran. Statistics for Long-Memory Processes. London, U.K.: Chapman Hall, 1994.

- [7] T. Blu and M. Unser. Self-similarity: Part II–Optimal estimation of fractal processes. IEEE Trans. Signal Process., 55(4):1364–1378, 2007.

- [8] O. Bonesini, A. Jacquier, and A. Pannier. Rough volatility, path-dependent PDEs and weak rates of convergence. arXiv preprint arXiv:2304.03042 (2023).

- [9] I. Chevyrev and H. Oberhauser. Signature moments to characterize laws of stochastic processes. Journal of Machine Learning Research, 23, 1–42, 2022.

- [10] F. Comte and E. Renault. Long memory in continuous-time stochastic volatility models. Mathematical finance, 8(4):291–323, 1998.

- [11] D. Crisan and K. Manolarakis. Solving backward stochastic differential equations using the cubature method: application to nonlinear pricing. SIAM Journal on Financial Mathematics, 3(1):534–571, 2012.

- [12] D. Crisan, K. Manolarakis. Second order discretization of backward SDEs and simulation with the cubature method. The Annals of Applied Probability, 24(2):652–678, 2014.

- [13] D. Crisan, E. McMurray. Cubature on wiener space for McKean–Vlasov SDEs with smooth scalar interaction. The Annals of Applied Probability, 29(1):130–177, 2019.

- [14] P. C. de Raynal and C. G. Trillos. A cubature based algorithm to solve decoupled mckean–vlasov forward–backward stochastic differential equations. Stochastic Processes and their Applications, 125(6):2206–2255, 2015.

- [15] M. El Omari. Mixtures of higher-order fractional Brownian motions. Communications in Statistics - Theory and Methods, 52(12):4200–4215, 2023.

- [16] D. Filipović, M. Larsson, and S. Pulido. Markov cubature rules for polynomial processes. Stochastic Processes and their Applications, 130(4):1947–1971, 2020.

- [17] J. Foster, T. Lyons, and H. Oberhauser. An optimal polynomial approximation of Brownian motion. SIAM Journal on Numerical Analysis, 58(3):1393–1421, 2020.

- [18] J. Foster, G. dos Reis and C. Strange. High order splitting methods for SDEs satisfying a commutativity condition. arXiv preprint, arxiv:2210.17543, 2022.

- [19] J.-P. Fouque, G. Papanicolaou, R. Sircar, and K. Solna. Multiscale stochastic volatility for equity, interest rate, and credit derivatives. Cambridge University Press, Cambridge, 2011.

- [20] P. K. Friz, W. Salkeld, and T. Wagenhofer. Weak error estimates for rough volatility models. arXiv preprint arXiv:2212.01591, (2022)

- [21] M. Fukasawa, and T. Ugai. Limit distributions for the discretization error of stochastic Volterra equations. arXiv preprint arXiv:2112.06471, (2021).

- [22] P. Gassiat. Weak error rates of numerical schemes for rough volatility. SIAM Journal on Financial Mathematics, Vol. 14, No. 2, pp.475-496, (2023).

- [23] J. Gatheral, T. Jaisson, and M. Rosenbaum. Volatility is rough. Quantitative Finance, 18(6):933–949, 2018.

- [24] A. Gulisashvili, F. Viens, and X. Zhang. Extreme-strike asymptotics for general Gaussian stochastic volatility models. Annals of Finance, 15(1):59–101, 2019.

- [25] A. Gupta, P. Singh, and M. Karlekar. A novel signal modeling approach for classification of seizure and seizure-free EEG signals. IEEE Transactions on Neural Systems and Rehabilitation Engineering, 26(5):925–935, 2018.

- [26] L. G. Gyurkó and T. J. Lyons. Efficient and practical implementations of cubature on wiener space. In Stochastic analysis 2010, pages 73–111. Springer, 2011.

- [27] F. A. Harang and S. Tindel. Volterra equations driven by rough signals. Stochastic Processes and their Applications, 142, 34–78, 2021.

- [28] F. A. Harang, S. Tindel, and X. Wang. Volterra equations driven by rough signals 2: higher order expansions. Stochastics and Dynamics, DOI: 10.1142/S0219493723500028, 2023.

- [29] P. Harms. Strong convergence rates for Markovian representations of fractional processes. Discrete and Continuous Dynamical Systems - B, 2021, 26(10): 5567-5579.

- [30] S. Hayakawa, H. Oberhauser, and T. Lyons. Hypercontractivity meets random convex hulls: analysis of randomized multivariate cubatures. Proceedings of the Royal Society A 479.2273 (2023): 20220725.

- [31] A. J. Jacquier and M. Oumgari. Deep PPDEs for rough local stochastic volatility. Available at SSRN 3400035, 2019.

- [32] P. Kidger, P. Bonnier, I. P. Arribas, C. Salvi, and T. Lyons. Deep signature transforms. In Advances in Neural Information Processing Systems, pages 3105–3115, 2019.

- [33] F. J. Király and H. Oberhauser. Kernels for sequentially ordered data. Journal of Machine Learning Research, 20(31):1–45, 2019.

- [34] P. E. Kloeden and E. Platen. Numerical solution of stochastic differential equations, volume 23. Springer, 1992.

- [35] M. Li, C. Huang, and Y. Hu. Numerical methods for stochastic Volterra integral equations with weakly singular kernels. IMA Journal of Numerical Analysis 42.3 (2022): 2656-2683.

- [36] S. Liao, T. Lyons, W. Yang, and H. Ni. Learning stochastic differential equations using rnn with log signature features. preprint, arXiv:1908.08286, 2019.

- [37] C. Litterer and T. Lyons. Cubature on wiener space continued. In Stochastic Processes and Applications to Mathematical Finance, pages 197–217. World Scientific, 2007.

- [38] C. Litterer and T. Lyons. High order recombination and an application to cubature on wiener space. The Annals of Applied Probability, 22(4):1301–1327, 2012.

- [39] T. Loussot, R. Harba, G. Jacquet, C. L. Benhamou, E. Lespesailles, and A. Julien. An oriented fractal analysis for the characterization of texture: Application to bone radiographs. EUSIPCO Signal Process., 1, 371–374, 1996.

- [40] T. Lyons and N. Victoir. Cubature on wiener space. Proceedings of the Royal Society of London. Series A: Mathematical, Physical and Engineering Sciences, 460(2041):169–198, 2004.

- [41] J. Ma, W. Yang, and Z. Cui. Semimartingale and continuous-time Markov chain approximation for rough stochastic local volatility models. preprint, arXiv:2110.08320, 2021.

- [42] S. Ninomiya, and Y. Shinozaki. On implementation of high-order recombination and its application to weak approximations of stochastic differential equations. Proceedings of the NFA 29th Annual Conference, 2021.

- [43] S. Ninomiya, and N. Victoir. Weak approximation of stochastic differential equations and application to derivative pricing. Applied Mathematical Finance, vol. 15, no. 2, pp. 107-121 , 2008.

- [44] D. Nualart. Malliavin calculus and related topics. 2nd ed., Springer, Berlin, 2006.

- [45] D. Nualart, and B. Saikia. Error distribution of the Euler approximation scheme for stochastic Volterra equations. Journal of Theoretical Probability (2022): 1-48.

- [46] R. Passeggeri. On the signature and cubature of the fractional Brownian motion for H1/2. Stochastic Processes and their Applications, 130(3), 1226-1257, 2020.

- [47] E. Perrin, R. Harba, C. Berzin-Joseph, I. Iribarren, and A. Bonami. nth-order fractional Brownian motion and fractional Gaussian noises. IEEE Transactions on Signal Processing, 49(5):1049–1059, 2001.

- [48] A. Richard, X. Tan, and F. Yang Discrete-time Simulation of Stochastic Volterra Equations. Stochastic Processes and their Applications, 141, 109–138, 2021.

- [49] A. Richard,X. Tan, and F. Yang On the discrete-time simulation of the rough Heston model. SIAM Journal on Financial Mathematics, 14(1): 223–249, 2023.

- [50] J. Ruan and J. Zhang. Numerical methods for high dimensional path-dependent PDEs driven by stochastic Volterra integral equations. Working paper, 2022.

- [51] F. Viens and J. Zhang. A martingale approach for fractional brownian motions and related path dependent PDEs. The Annals of Applied Probability, 29, 3489-3540, 2019.

- [52] T. Wang. Linear quadratic control problem of stochastic Volterra integral equations, ESAIM:COCV (2018) 1849-1879.

- [53] C. Wen and T. Zhang. Improved rectangular method on stochastic Volterra equations. Journal of Computational and Applied Mathematics, 235(8):2492–2501, 2011.

- [54] J. Zhang. Backward Stochastic Differential Equations: From Linear to Fully Nonlinear Theory. Probability Theory and Stochastic Modelling 86. Springer, New York, 2017.

- [55] X. Zhang. Euler schemes and large deviations for stochastic Volterra equations with singular kernels. Journal of Differential Equations. 244(9):2226-2250, 2008.