On Parameter Estimation in Unobserved Components Models subject to Linear Inequality Constraints

Abstract

We propose a new quadratic programming-based method of approximating a nonstandard density using a multivariate Gaussian density. Such nonstandard densities usually arise while developing posterior samplers for unobserved components models involving inequality constraints on the parameters. For instance, Chan et al., (2016) provided a new model of trend inflation with linear inequality constraints on the stochastic trend. We implemented the proposed quadratic programming-based method for this model and compared it to the existing approximation. We observed that the proposed method works as well as the existing approximation in terms of the final trend estimates while achieving gains in terms of sample efficiency.

1 Introduction

Consider the following unobserved components model.

where the initial condition is treated as a parameter.

Suppose we wish to restrict the trend to be in the interval where and are constants. Linear inequality constraints like these occur quite naturally in many economic applications. For instance, Chan et al., (2016) discussed such situations in the context of modeling trend inflation. The problem of interest is to efficiently estimate the parameters involved in an unobserved components model under such restrictions. By efficiency, we mean the run time and the sample efficiency.

1.1 Motivation

In the presence of the aforementioned inequality constraints, the conditional distribution of given the other parameters, i.e. is nonstandard and thus conventional methods of inference in state-space models cannot be used. Chan and Strachan, (2012) suggest an approach for estimation in such non-linear state-space models where the key element is to approximate using a multivariate Gaussian density. The Gaussian approximation is then used as a proposal density for an acceptance-rejection Metropolis-Hastings algorithm (Chan et al., (2016)).

We propose a new quadratic programming-based approach to approximating the nonstandard density using a Gaussian density. In general, the idea is to efficiently solve the following quadratic programming problem.

| subject to |

The above quadratic program maximizes the kernel of a multivariate Gaussian density for for general linear inequality constraints. In general, we can say the following about the time complexity of solving a quadratic program like the one mentioned above.

As our problem has more structure like . We may be able to further improve on the empirical run time if not the asymptotic polynomial time complexity.

1.2 Investigating Run-Time of the Quadratic Program

We know the following.

where , , and is given as follows.

We set , , and . We use quadprogram available in MATLAB to solve the following quadratic programming problem.

| subject to |

We can write it equivalently as follows.

| subject to |

We use the US quarterly CPI data from 1947Q1 to 2015Q4. Specifically, given the quarterly CPI figures , we compute and use it as the inflation rate. We take subsets of and to investigate the run times for different values of .

The run times in solving the above quadratic programming problem for different values of are reported in Table 1.

| Elapsed Time (in seconds) | |

|---|---|

| 50 | 0.0058 |

| 100 | 0.0076 |

| 150 | 0.0140 |

| 200 | 0.0149 |

| 250 | 0.0172 |

| 300 | 0.0185 |

| 350 | 0.0208 |

| 400 | 0.0264 |

| 450 | 0.0241 |

| 500 | 0.0304 |

| 550 | 0.0309 |

Comment. We observed that the empirical run times are quite small. This suggests that the idea is promising and we should explore it further. The solution to the discussed quadratic program is bound to lie within the constraints. Hence, for Bayesian computations, it is a better candidate for the mean of the distribution which the parameter is getting generated from. The idea is to improve the estimation and avoid any approximations due to the linear constraints and also expect that the sample efficiency will improve. The estimation performed using this idea will be termed QuadProg henceforth.

2 QuadProg for the Trend Inflation Model discussed in Chan et al., (2016)

2.1 Model Description

Chan et al., (2016) discuss a new model of trend inflation with inequality constraints. The model is discussed in great detail is the original paper. Let is an observed measure of inflation at time , then the measurement and state equations of the model are given as follows.

where and . The linear inequality constraints on the behavior of an are imposed by considering the following.

where denotes the Gaussian distribution with mean and variance truncated to the interval .

Furthermore, the model considers the following.

where and are known constants.

Following are the priors for the unknown parameters.

2.2 The Proposed Modification

Chan et al., (2016) discusses given an initial value of the CPI inflation rate, use the measurement equation to generate the CPI inflation rate data, , and develop a Markov chain Monte Carlo (MCMC) algorithm for generating from the posterior densities for the above model. Due to the presence of the inequality constraints, and are nonstandard and thus conventional methods of inference in state-space models cannot be used. Instead, they use an approach developed in Chan and Strachan, (2012) for posterior sampling in nonlinear state-space models. An essential element of this algorithm is a Gaussian approximation to the conditional density . This uses a precision-based algorithm that builds upon results derived for the linear Gaussian state-space model by Chan and Jeliazkov, (2009). The Gaussian approximation is then used as a proposal density for an ARMH step. They also use this algorithm to draw from and .

We use the quadratic-programming-based approximation of the Gaussian density (QuadProg) as proposed and discussed in this report for modifying the posterior sampling procedure in Chan et al., (2016) for and as follows.

Instead of generating from the proposal density of the form , we can use the quadratic program solver to obtain and then draw a candidate to be accepted or rejected via an acceptance-rejection Metropolis-Hasting (ARMH) step.

3 Empirical Results

We used the US quarterly CPI data from 1947Q1 to 2011Q3. Specifically, given the quarterly CPI figures , we computed and used it as the inflation rate. As suggested and discussed in Chan et al., (2016), we set the hyperparameters as follows.

-

1.

.

-

2.

and .

-

3.

.

-

4.

, and .

We used 10,000 Monte-Carlo simulations with 1000 as the burn-in time.

We used the following two estimation methods.

We used Matlab for the purpose of implementation.

3.1 Trend Estimation

We estimated the trend for the US quarterly CPI data using AR-Trend-Bound and Quad-Prog methods.

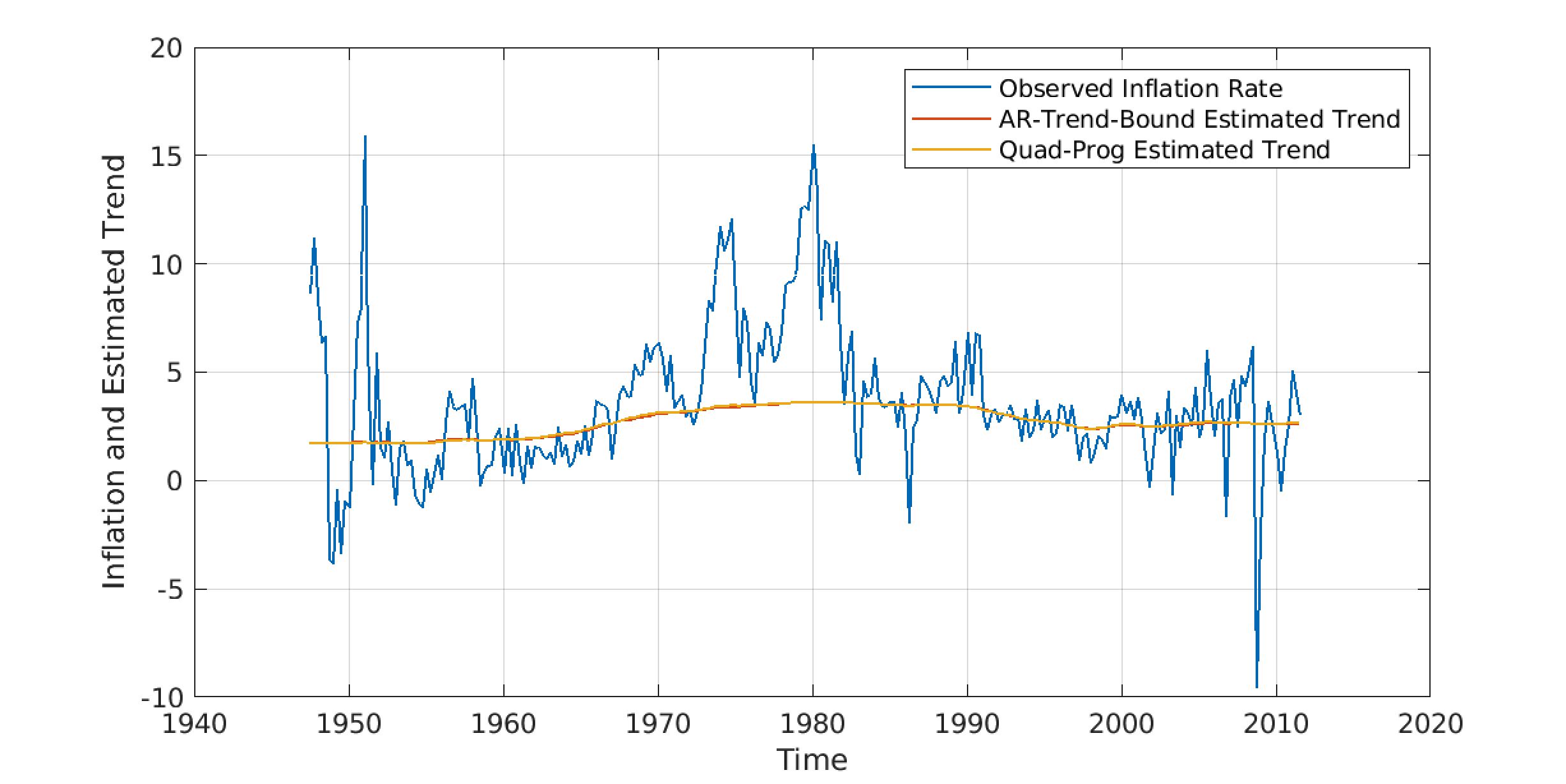

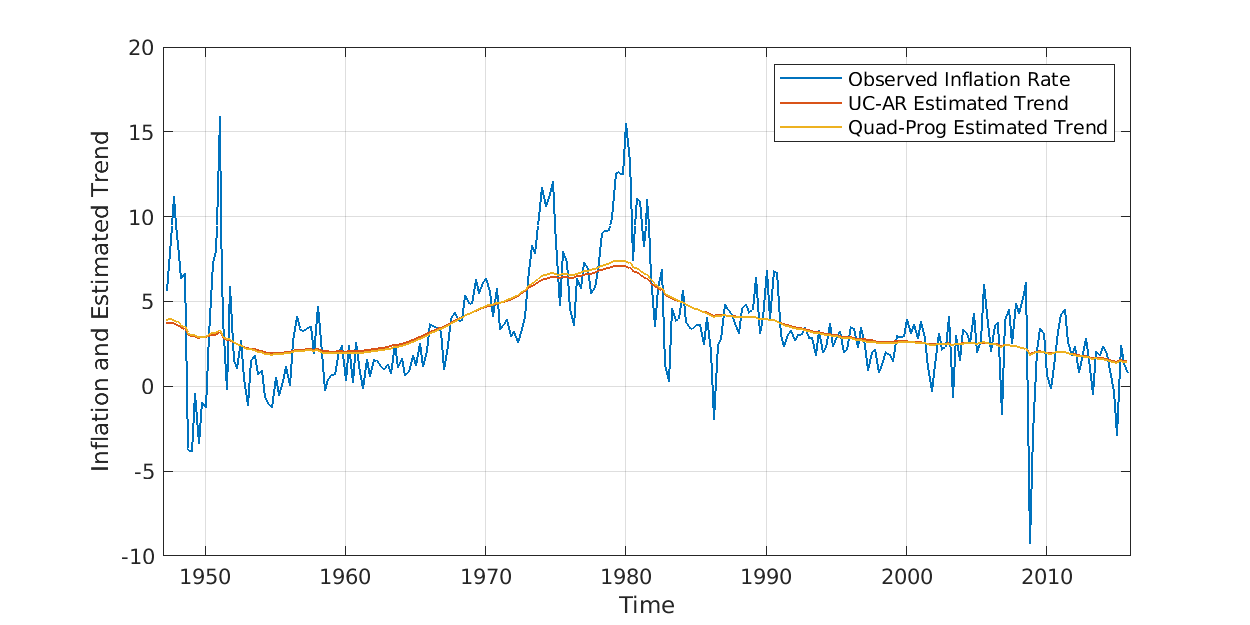

Figure 1 shows the observed rate of inflation, trend estimated using AR-Trend-Bound, and trend estimated using Quad-Prog. We observe that the trend estimates using the two different methods are quite close to each other confirming that the the proposed modification indeed does good estimation.

3.2 Sample Efficiency

One of the limitations of Monte Carlo methods is that different draws are seemingly/pseudo-random, i.e. there may exist a significant autocorrelation in the draws generated over different time points. We are interested in understanding how does the proposed method compares to the existing approach in terms of presence of such autocorrelation. A common diagnostic of sample efficiency is the inefficiency factor, defined as follows.

where is the sample autocorrelation at lag length and is chosen large enough so that the autocorrelation tapers off. Note that purely random/independent draws would give an inefficiency factor of 1. Inefficiency factors indicate how many extra draws need to be taken to give results equivalent to independent draws. For instance, if we take 5000 draws of a parameter and find an inefficiency factor of 10, then these draws are equivalent to 500 independent draws from a given distribution.

For any given parameter vector of length , there are inefficiency factors (one for each ). As and each is of length , we have total number of inefficiency factors corresponding each approach of estimation. We used to calculate the inefficiency factors. For reporting, we construct a box plot of inefficiency factors for each parameter. We compare the box plots for each parameter across different methods of estimation.

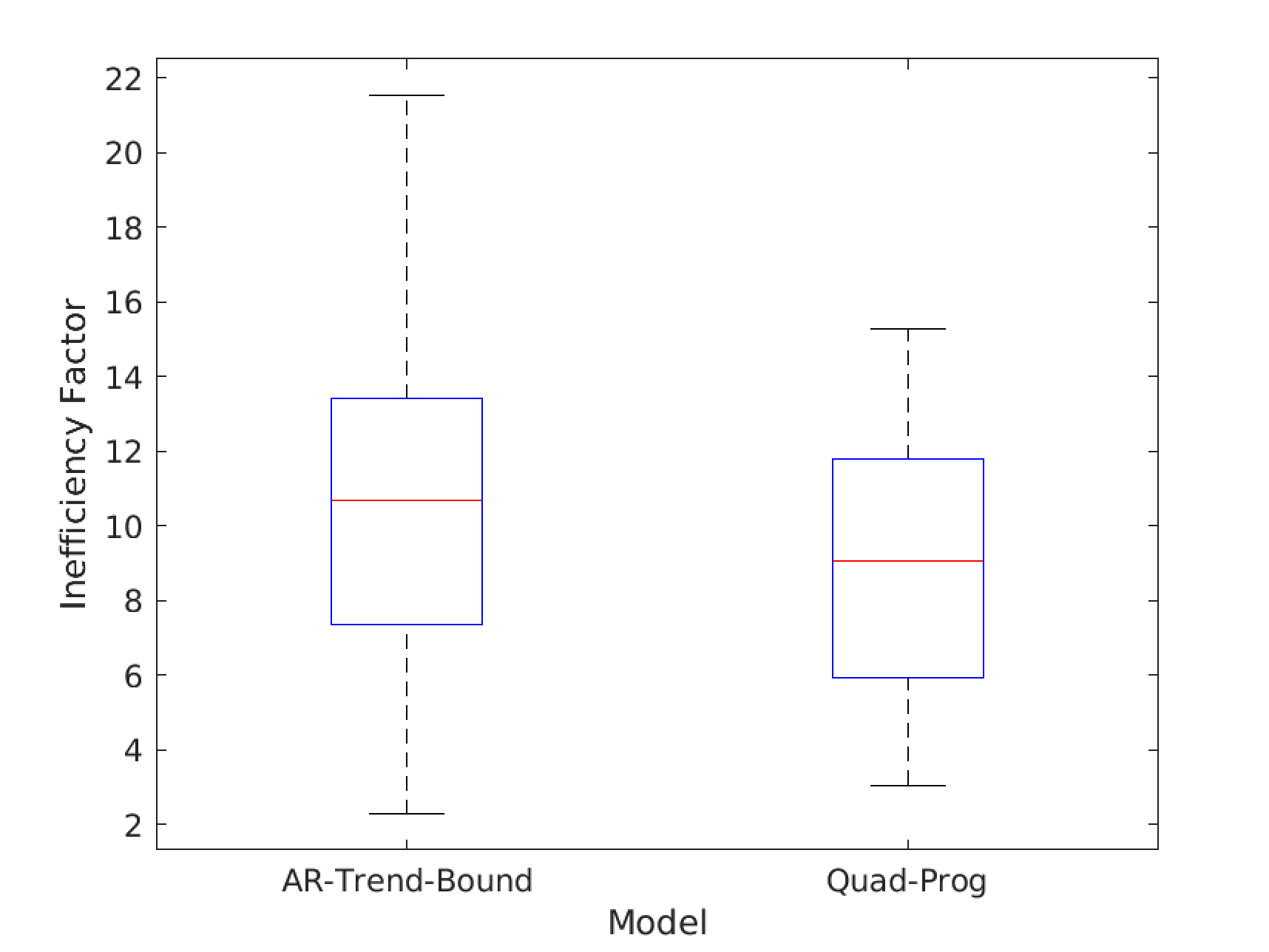

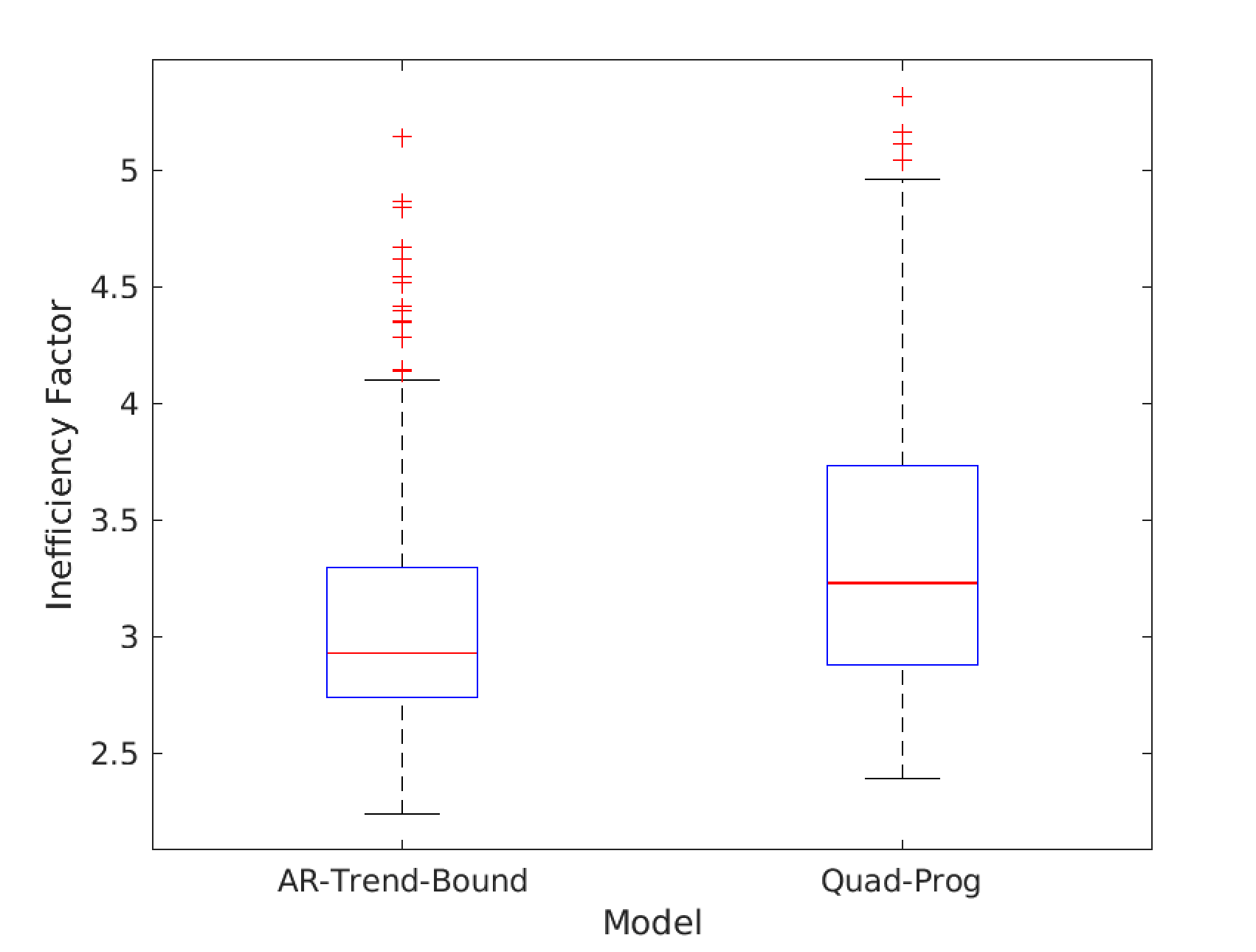

Figure 2 shows the box plots of inefficiency factors for sampling using AR-Trend-Bound and Quad-Prog methods. We observe that Quad-Prog leads to a lower average and maximum sample inefficiency as compared to AR-Trend-Bound.

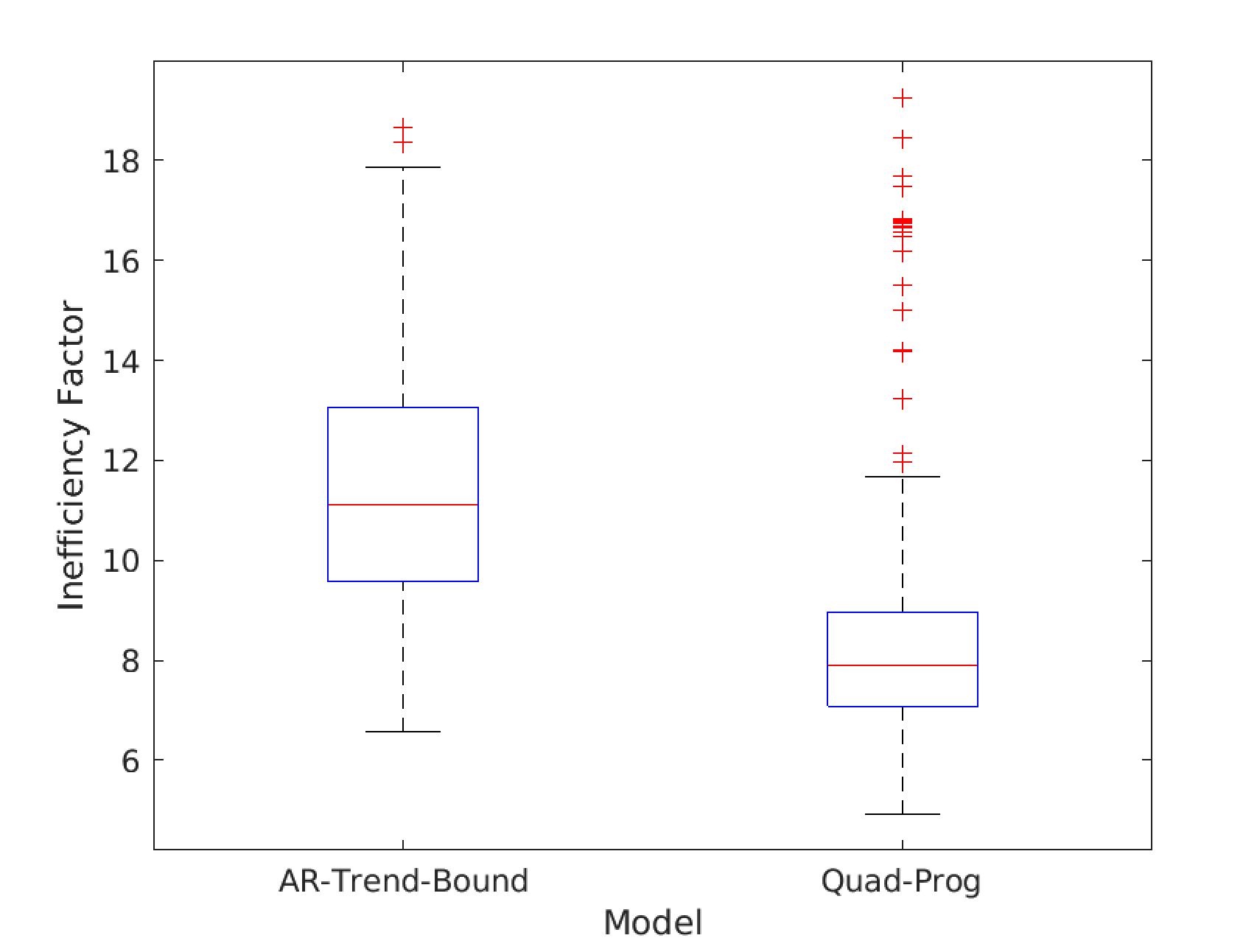

Figure 3 shows the box plots of inefficiency factors for sampling using AR-Trend-Bound and Quad-Prog methods. We observe that Quad-Prog leads to a lower average and maximum sample inefficiency as compared to AR-Trend-Bound.

Figure 4 shows the box plots of inefficiency factors for sampling using AR-Trend-Bound and Quad-Prog methods. We observe that Quad-Prog AR-Trend-Bound perform very similar in terms of average and maximum sample efficiency.

References

- Chan and Jeliazkov, (2009) Chan, J. C. and Jeliazkov, I. (2009). Efficient simulation and integrated likelihood estimation in state space models. International Journal of Mathematical Modelling and Numerical Optimisation, 1(1-2):101–120.

- Chan et al., (2016) Chan, J. C., Koop, G., and Potter, S. M. (2016). A bounded model of time variation in trend inflation, nairu and the phillips curve. Journal of Applied Econometrics, 31(3):551–565.

- Chan and Strachan, (2012) Chan, J. C. and Strachan, R. W. (2012). Estimation in non-linear non-gaussian state space models with precision-based methods. Available at SSRN 2025754.

- Kozlov et al., (1980) Kozlov, M. K., Tarasov, S. P., and Khachiyan, L. G. (1980). The polynomial solvability of convex quadratic programming. USSR Computational Mathematics and Mathematical Physics, 20(5):223–228.

- Sahni, (1974) Sahni, S. (1974). Computationally related problems. SIAM Journal on computing, 3(4):262–279.

Appendix A Implementing QuadProg for Trend Estimation in a Simple Unobserved Components Model (UC-AR)

As an initial test for the proof-of-concept, we tried the same idea of quadratic programming-based approximation of a multivariate Gaussian density for a relatively simple unobserved components model discussed as follows.

Let be some observed measure at time , then the measurement and state equations of the model are given as follows.

where , , , and is an unknown parameter.

Following are the priors for the unknown parameters.

For the above model, we have an explicit and no approximation posterior sampler, i.e. approximation using a multivariate Gaussian density is not required. However, just to make sure that the proposed idea works well in terms of estimation and sample efficiency, we implemented Quad-Prog for this model.

A.1 Empirical Results

We used the US quarterly CPI data from 1947Q1 to 2015Q4. Specifically, given the quarterly CPI figures , we computed and used it as the inflation rate. As suggested and discussed in Chan et al., (2016), we set the hyperparameters as follows.

-

1.

and .

-

2.

and

-

3.

and

We used 10,000 Monte-Carlo simulations with 1000 as the burn-in time.

We used the following two estimation methods.

-

1.

UC-AR: The explicit and no approximation method.

-

2.

Quad-Prog: Modifying the explicit method using the idea proposed in this report.

We used Matlab for the purpose of implementation.

A.1.1 Trend Estimation

We estimated the trend for the US quarterly CPI data using UC-AR and Quad-Prog methods.

Figure 5 shows the observed rate of inflation, trend estimated using UC-AR, and trend estimated using Quad-Prog. We observe that the trend estimates using the two different methods are quite close to each other confirming that the proposed modification indeed does good estimation.

A.1.2 Sample Efficiency

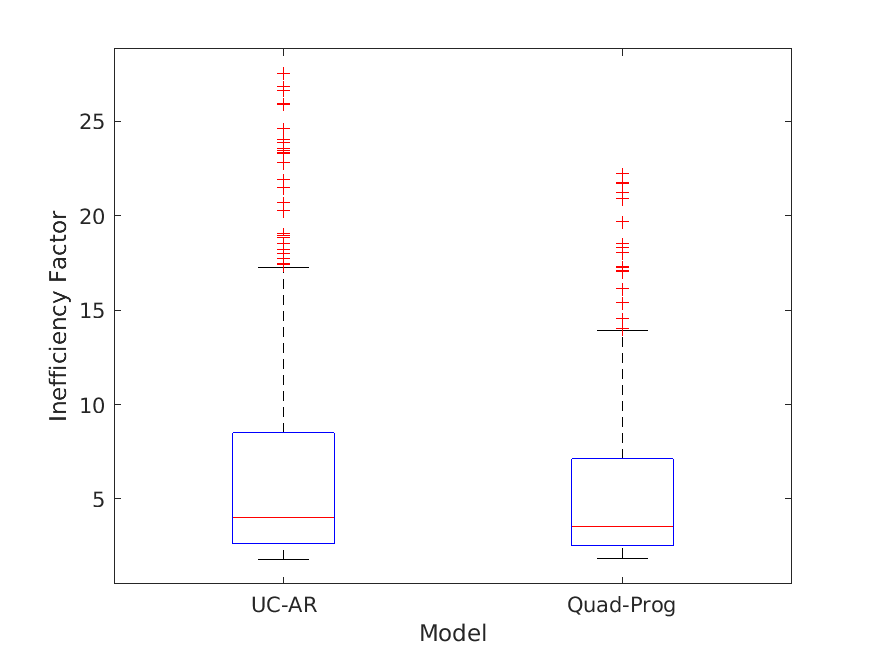

Figure 6 shows the box plots of inefficiency factors for sampling using AR-Trend-Bound and Quad-Prog methods. We observe that Quad-Prog and UC-AR perform similarly in terms of average sample efficiency. However, Quad-Prog leads to a slightly lower maximum sample inefficiency as compared to UC-AR which is most likely attributed to chance.