Merging Two Cultures: Deep and Statistical Learning

This Draft: Oct 12, 2021 )

Abstract

Merging the two cultures of deep and statistical learning provides insights into structured high-dimensional data. Traditional statistical modeling is still a dominant strategy for structured tabular data. Deep learning can be viewed through the lens of generalized linear models (GLMs) with composite link functions. Sufficient dimensionality reduction (SDR) and sparsity performs nonlinear feature engineering. We show that prediction, interpolation and uncertainty quantification can be achieved using probabilistic methods at the output layer of the model. Thus a general framework for machine learning arises that first generates nonlinear features (a.k.a factors) via sparse regularization and stochastic gradient optimisation and second uses a stochastic output layer for predictive uncertainty. Rather than using shallow additive architectures as in many statistical models, deep learning uses layers of semi affine input transformations to provide a predictive rule. Applying these layers of transformations leads to a set of attributes (a.k.a features) to which predictive statistical methods can be applied. Thus we achieve the best of both worlds: scalability and fast predictive rule construction together with uncertainty quantification. Sparse regularisation with un-supervised or supervised learning finds the features. We clarify the duality between shallow and wide models such as PCA, PPR, RRR and deep but skinny architectures such as autoencoders, MLPs, CNN, and LSTM. The connection with data transformations is of practical importance for finding good network architectures. By incorporating probabilistic components at the output level we allow for predictive uncertainty. For interpolation we use deep Gaussian process and ReLU trees for classification. We provide applications to regression, classification and interpolation. Finally, we conclude with directions for future research.

Keywords: Deep Learning, Machine Learning, Gaussian Process, Uncertainty Quantification, Bayesian, Regularization, Trees, Random Forests, TensorFlow, PyTorch

1 Introduction

Model specification is one of the most challenging parts of statistical modeling as originally discussed in Fisher’s seminal paper [Fisher, 1922]. Breiman [Breiman, 2001] highlighted the contrast between an algorithmic approach and traditional statistical modeling for 21st century data analytics. Algorithmic approaches focus their effort on understanding high-dimensional data structure. Deep learning is an algorithmic modeling approach which has changed the landscape for text [Devlin et al., 2018] and image analysis [Litjens et al., 2017] and many other areas of applications [Bhadra et al., 2019, Heaton et al., 2017, Dixon et al., 2019]. Our goal is to show that deep learning has wide applicability to traditional statistical areas for tabular data structures including categorical, spatial and time series analysis. Until now, traditional statistical models have relied heavily on additive functions with low approximation capacity based on shallow architectures. From a statistical viewpoint, much attention has been paid to stochastic models that combine with the deterministic part of a statistical model.

Deep Learners are based on superposition of univariate affine functions [Polson and Sokolov, 2017] and are universal approximators. Whilst Gaussian Process [Gramacy and Lee, 2008, Higdon et al., 2008] are also universal approximators and can capture relations of high complexity, they typically fail to work in high dimensional settings. Tree methods can be very effective in high dimensional problems. Hierarchical models are flexible stochastic models but require high-dimensional integration and MCMC simulation. Deep learning, on the other hand, is based on scalable fast gradient learning algorithms such as Stochastic Gradient Descent (SGD) and its variants. Modern computational techniques such as automated differentiation (AD) and accelerated linear algebra (XLA) are available to perform stochastic gradient descent (SGD) at scale within TensorFlow or PyTorch, thus avoids the curse of dimensionality by simply pattern matching and using interpolation to predict in other regions of the input space. The algorithmic culture has achieved much success in high dimensional problems. DL assumes a very flexible class of predictors, , and directly train this predictor using a predictive mean squared error loss. Such classes of functions include decision trees and neural networks. The goal is simple to find a predictor rule. Can we find a good predictor (a.k.a. algorithm) to evaluate on to predict output ? The caveat with an algorithmic approach is that it lacks uncertainty quantification.

The statistical modeling approach makes uncertainty quantification paramount and, following Breiman, we write

The limitations of statistical modeling are clear as model specification and validation is hard particularly in high dimensions.

Interpolation

Gaussian Process and piece-wise polynomial functions [Wahba, 1990] are popular approaches to interpolate and require specifying smoothness parameters or learning those using MLE or Bayesian inference. For example, often Gaussian Process models are used to quantify uncertainty of complex scientific simulators Higdon et al. [2008], Gramacy and Lee [2008] or complex geo-spacial processes Kim et al. [2005]. We show how they can be merged with deep learning.

Neal [2012] has shown that a function space defined by Bayesian neural network with Gaussian weights approximates is a Gaussian process as the number of neurons goes to infinity. Later MacKay [1998] has argued that Gaussian process models should be preferred since they do not require specifying architecture and only priors for hyperparameters of correlation functions need to be defined. On the other hand, modeling non-stationary and non-isotropic data is hard to model with Gaussian process, while neural networks can handle those types of relations. Thus, the fact that an architecture with specific distribution over weights approaches Gaussian process does not necessarily mean that GP is to be preferred. Several approaches were proposed to address the problem of modeling non-stationary and non-isotropic data with GP. Gramacy and Lee [2008] proposes using decision trees to partition the data so that each partition constrains a stationary subset and then a separate GP model is used for each subset. Fadikar et al. [2018] use several Gaussian Process models for different quartiles of the time series data to model non-stationary epidemic data. Srivastava et al. [2014] is a regularization technique that sets weights to randomly to zero.

Our approach then adds to traditional deep learning by incorporating probabilistic components at the output level, given learned data filters, which then allow for predictive uncertainty.. We illustrate the merging of the two cultures using deep Gaussian process and high dimensional classification using ReLU trees which provide an alternative to random forests. Finally, we outline directions for future research.

Uncertainty Quantification.

Statistical models are capable of representing uncertainty in predictions and parameters. When input-output relations are modeled using deterministic functions, such as ridge or neural network, this property is lost. Understanding uncertainty is key in many science and engineering applications. Neural networks are essentially a nonparametric regression which uses sparse or skinny representation [Olshausen and Field, 1996]. Bishop [1995] considers neural networks from statistical modeling p oint of view and presents neural networks as an extension to more traditional functions used in statistical modeling.

Ripley [2007] presents feed forward neural network as a way to project input into lower dimensional space within which the approximation can be preferred and compares is to projection pursuit regression. Bengio [2009] also presents a neural network as a way to generate representation of the data in a different subspace. Each layer is a representation.

The rest of the paper is outlined as follows. Section 2 merges the two cultures of statistical modeling and deep learning and describes classes of deep learners. To do this, we first describe how to perform unsupervised and supervised dimension reduction of the input space. Hand-crafted as well as learned transformations are discussed. Our approach differs from traditional deep learning by using probabilistic model as the last output layer. This allows us to use traditional statistical uncertainty quantification methods such as in logistic regression [Polson et al., 2013] or Gaussian Process [Gramacy and Lee, 2008]. Section 3 discusses the problem of model selection. Section 4 provides applications in regression, classification and interpolation. We provide a deep learning alternative to treed models. Finally, Section 5 concludes with directions for future research.

1.1 General latent feature model

Given a training dataset of input-output pairs the goal is to find a prediction rule for a new output given a new input . Let denote latent hidden features that are to be hand-coded or learned from the data and our nonlinear latent feature predictive model takes the form

| (1) | ||||

| (2) |

where is a data transformation, that is allows for relations between latent features and to be modeled by a well understood probabilistic model . Typically will perform dimension reduction or dimension expansion and can be learned from data. The top level of our model is stochastic. This gives a full representation of the predictive uncertainty in predicting new . In many cases, our predictor is simply the conditional mean .

Finding Predictions.

The key is to find a good data tranformation, e.g. deep learning architecture, that predicts well. Essentially DL solves two problems. First it finds the latent features . Second, it interpolates/predict a new output for a new input . This latter property is governed by predictive cross-validation. Predictive uncertainty is also required, which is provided by our probabilistic model at the top layer .

2 Merging Deep and Statistical Learning

The main role of feature selection is to find the data transformation so that the relations between input and output can be captured by one of the statistical models. For example we often apply log-transformations so that a linear model can be used. In this section we discuss several approaches to data transformation that enable usage of simple predictive rules for the transformed data. There are two forms of data transformations, first dimension expansion and second dimension reduction.

2.1 Dimensionality Expansion

First, we review dimensionality expansion data transformation that transforms input vector into higher dimensional vector . One approach is to use hand-coded predictors. This expanded set can include terms such as interactions, dummy variables or nonlinear functional of the original predictors. The goal is to model the joint distribution of outputs and inputs, namely , where we allow or stochastic predictors.

The joint distribution is characterized by its two conditionals distributions

-

•

. This performs prediction via and uncertainty quantification using its probabilistic structure.

-

•

. This conditional is very dimensional and we need to perform dimension reduction and find an efficient set of nonlinear features to be used as predictors in step 1. Selection using sparsity and deep learners will be the methods used.

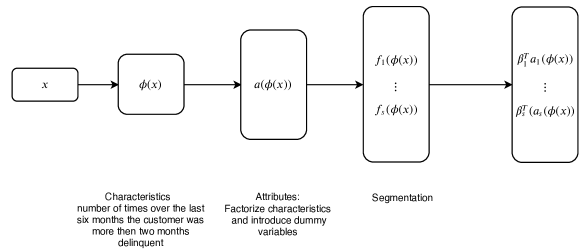

As an example of this approach, we describe a predictive model used by Fair, Isaac to predict credit worthiness [Hoadley, 2001]. Today this indicator is known as FICO score. The overall architecture of the FICO model is shown in Figure 1.

In the Fair, Isaac architecture, first the variable (monthly bills and payments over the last 12 months) was transformed into many interpretable variables, e.g. months delinquent and then calculate the characteristics vector from those interpretable variables. For example, the number of times in the last six months that the customer was more than two months delinquent. Than the data was segmented and a separate predictive model developed for each of the segments. Each segment-specific predictive model was a variant of the logistic regression.

Kernel Expansion

The idea is to enlarge the feature space via basis expansion. The basis is expanded using nonlinear transformations of the original inputs so that linear regression or generalized linear model can be used to model the input-output relations. Kernel trick increase dimensionality, and allows hyperplane separation. The transformation is specified via a kernel function which calculates the dot product of feature mappings

By choosing feature map , we implicitly choose a kernel function. For example, when , choosing is equivalent to expanding the basis to .

Tree Expansion

Similar to kernels we can think of trees as a technique for expanding a feature space. Each region in the input space defined by a terminating node of a tree correspond to a new feature. Then predictive rule becomes very simple, identify in which region the new input is and use average across observations from this region to calculate the prediction.

Deep Learning Expansions

Similar to a tree model that finds features (a.k.a tree leaves) by splitting the input space into rectangular regions, the deep learning model finds the regions by using hyperplanes at the first layer and combinations of hyperplanes in the further layers. The prediction rule is embedded into a parameterized deep learner, a composite of univariate semi-affine functions, denoted by where represents the weights of each layer of the network. A deep learner takes the form of a composition of link functions

where is a univariate link function. Specifically, let denote the -th layer, and so . The final output is the response , which can be numeric or categorical. A deep prediction rule is then

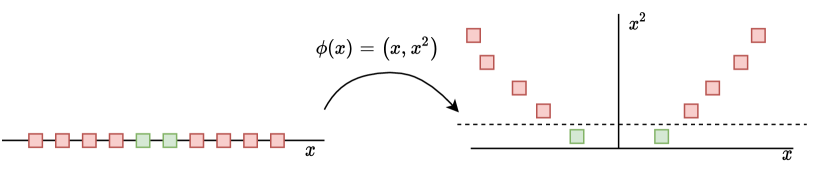

We demonstrate the similarity between a tree model and a layer of a deep learning model by showing how a DL model classifies observations form a simulated daugnat dataset shown in Figure 3(a). It is clear that a linear separator will no work in this case, however, we can use four lines to split the data into nine regions as shown in Figure 3(b).

|

|

| (a) Dataset | (b) Hyperplanes and probability heat map for classification based on the four hyper-planes |

Given this split, it is easy to design a predictive rule for classifying the red and green dots. If a point is on the left of lines 2, 4 and on the right of lines 4, 1, then classify as red and classify as green otherwise. The four lines are given by the linear system

Finally, we perform classification by a logistic regression

Figure 3(b) shows the heat plot of the with red being 1 and white being 0.

We can also visualize the deep learning model using a tree-like diagram to highlight the similarity between two approaches.

It is often beneficial to replace the original input with the features of lower dimensionality when developing a predictive model for . It was shown, for example, in the context of regressions, that a lower variance prediction rule can be obtained in lowe dimensional space [Adragni and Cook, 2009] . For fully Bayesian discussion see Lindley [1968].

To achieve good generalisability we need to be able to perform nonlinear dimension reduction and to find a suitable set of features/factors. Deep learners together with sparse optimization provides such a framework. From a probabilistic view point, it is natural to view input-output paris as being generated from some distribution

We are interested in two conditional distributions

-

•

the probabilistic quantification of uncertainty about the output at a new input . One of the key assumptions— an equivalent to sufficient data reduction in a statistical context– is to assume that

Here is a dimension increasing set of characteristics set, e.g. the inclusion of dummy variables (one hot encodings), interaction terms, and is dimension reducing deep learning model, trained from input-output pairs.

Typically is constructed as a combination of hand-crafted and learned transformation from deep learning. This provides the efficient data reduction necessary to provide high dimensional prediction.

-

•

the conditional distribution of inputs, given the outputs which can be used to perform supervised learning of data transformations comprising the deep learner . In the unsupervised case, one simply used the marginal distribution .

Figure XXX shows how the data transformations work to construct the nonlinear deep learners. DL simply uses a composition/superposition of semi-affine filters (a.k.a. link functions).

This leads to the following framework for high-dimensional modeling.

Given a training data , we first use to uncover structure in the predictors relevant for modeling the output . The learned factors are denoted by and are constructed as a sequence of input filters. Finally, the predictive model is given by a probabilistic model of the form . Here initially expands the dimension of the input space by including terms such as interactions, dummy variables (a.k.a. one hot encodings) and other nonlinear features of the input space deemed relevant. Then reduce dimension by deep learning by projecting back with univariate activation function (a.k.a. link) into an affine space (a.k.a regression)

Deep learning can then be viewed as a feature engineering solution and one of finding nonlinear factors via supervised dimension reduction. A composition of hand-coded characteristics–dimension expanding— with supervised learning of data filters–dimension reduction Advances in computation allow for massive data and gradients of high dimensional nonlinear filters Neural networks can be viewed from two perspectives. Either as a flexible link function in a GLM model McCullagh [2019] or a method to achieve dimensionality reduction, similar to sliced inverse regression Li [1991] or sufficient dimensionality reduction Cook and Forzani [2009].

This framework also sheds light on how to build deep (skinny) architectures. Given data points, we split into regions [Harding, 1967] so that there is a ”fixed” sample size within each bin. To summarize

-

•

Transform into many interpretable characteristics. First generate several time series from raw inputs, e.g. months delinquent. Then extract futures from those time series, e.g. number of times over the last six months the customer was more then two months delinquent. This process leads to thousands of characteristics that are screened to be included into the predictive models

-

•

Then population is segmented based on the screened characteristics. This process was manual. Similar to the CART algorithm.

-

•

A separate function (scorecard) was developed for each segment. Each characteristic was binned into sets called attributes. A scorecard is linear function of the attribute indicators (dummy) variables.

Increase of dimensionality is the key! 24 inputs led to thousand of characteristics and hundreds after screening. After discrediting input about 10 attributes per characteristics and after introducing 10 segments, we get tens of thousands of features. Essentially it is a generalized additive models (GAM) with bin smoothing.

One advantage of “depth” is that the hierarchical mixture allows the width of a given layer to be manageable. With a single layer (e.g., kernel PCA/SVM) we need exponentially many more basis functions in that layer. Consider kernel PCA with say RBF kernels: technically there are infinitely many basis functions, but it cannot handle that many input dimensions. Presumably a deep neural network allows a richer class of covariances that allows anisotropy, nonstationarity etc. In the end, this is reflected in the function realizations from a DNN. To see this, consider the deep GP models, which are infinite width limits of DNNs (ref). There is a recursive formula connecting the covariance of layer to that of layer , but no closed form. The covariance function of the final hidden layer is probably very complicated and capable of expressing a lot of features, even if the covariances in each layer may be simple. The increase in dimensionality happens through the hierarchical mixture rather than trying to do it all in one layer.

From a statistical viewpoint, this is similar to the liner shallow wide projections introduced Wold (1955) and the sufficient dimension reduction framework of Cook (2007).

In an unsupervised learning context we simply use information in the marginal distribution, , of the input space as opposed to the conditional distribution, . PCA, PCR, RRR, PPR all fall into this category. PLS, SIR are examples of supervised learning of features, See [Polson and Sokolov, 2017] for further discussion.

The joint distribution is characterized by its two conditionals and . We first embed into which can be very high dimensional— including dummies, interactions etc. Then we need to model and this requires dimension reduction. We will perform this using a deep learner where indexes the weights in each affine layer.

Estimate and hence find the nonlinear feature extraction using stochastic gradient descent. inverse conditional distribution . Data reduction techniques

2.2 PCA, PCR and SVD Algorithm

Given inputs and outputs and associated observed data and . The goal is to find data transformations so that modeling the transformed data becomes an easier task. In this paper we consider several types of transformations and model non-linear relations.

We start by reviewing widely used singular value decomposition (SVD) which allows to find linear transformations to identify lower dimensional representation of , the technique is known as principle component analysis (PCA) or both and , known as partial least squares (PLS).

First, start with the SVD decomposition of the input matrix: . If then of full rank. Here nonzero ordered singular values. Then is the matrix of eigenvectors for . We can then transform the original first layer to an orthogonal regression, namely with corresponding OLS estimator .

PLS and SVD Algorithm

PCR has a long history in statistics. This is an unsupervised approach to dimension reduction (no ’s). Specifically, we first center and standardize .

Then, we provide an SVD decomposition of

This find the eigen-values and eigenvectors arranged in descending order, so we can write

This leads to a sequence of regression models with being the overall mean and

Therefore, PLS finds “features” .

PCA and multivariate output

PCA emulation requires us to compute a reduction of multivariate output using singular value decomposition of by finding eigenvectors of . Then, we assume that the output is a linear combination of the singular vectors

where the weights follow a Gaussian Process.

Hence the method can be highly non-linear. This method is typically used when input variables come from a design of experiment. If interpretability of factors is not important, and from a purely predictive point of view, PLS will lead to improved performance.

One can view deep learning models as non-stochastic hierarchical data transformations. THe advantage is that we can learn deterministic data transformations before applying a stochastic model. That allows us to establish the connection between the Brillinger result and use of deep learning models and to develop a unified framework for modeling complex high-dimensional data sets. The prediction rule can be viewed as interpolation.

In high-dimensional spaces you can mix-and-match the deterministic and stochastic data transformation rules.

Model selection (a.k.a. dimension reduction)

The goal of PCR is to minimize predictive MSE

The choice of is determined via predictive cross-validation. The th model is simple regression of on . Mallows [1973] and provide the relationship between shrinkage and model selection.

Dropout

This is a model selection technique designed to avoid over-fitting in deep learning. This is done by removing input dimensions in randomly with a given probability . For example, suppose that we wish to minimize MSE, , then, when marginalizing over the randomness, we have a new objective

This is equivalent to, with ,

Hence, this is equivalent to a Bayesian ridge regression with a -prior as an objective function and reduces the likelihood of over-reliance on small sets of input data in training.

PLS provides three diagnostic plots: scree plot for dimensionality selection, by-plot and the correlation plot. The by-plot and the correlation plot allows the modeler to see how the output and input variables weight on hidden features.

2.3 Partial Least Squares

(PLS) transforms where are the scores and are the scores respectively. By construction the loadings and that correspond to regressions of on and on are designed so that and have maximum correlation. So the prediction rule will have the lowest possible in-sample MSE fit. THis contrasts with PCA which simply looks for variations of maximum explanation in the space without regard of the predictive ability of . PLS, therefore, provides the optimal patten matching data transformation methods111There is no logical reason why the output variable needs to be closely related to the principal components, see Ehrenberg [1968], Polson and Scott [2012]. Moreover, Cook [2007] warned of pitfalls of using for identifying dimensionality reduction transformations of , in his analysis of agricultural field trials, the predictions should be chosen without output (the crop yield), thus making PLS inappropriate. Note, that requirement of being stochastic is not always satisfied. An important example is when is a result of design of experiment. PLS also has a number of other advantages, which are specific to high dimensional problems. First, it handles multi-collinearity (as opposed to OLS). Second, it allows to handle multivariate .

dimension reduction of depends on , the supervised learning reduction is more efficient. The alternative non-linear un-supervised approach is to use an autoencoder. Polson et al. [2021] show that one can avoid the linear assumption of PLS by combining with other non-linear techniques and improve the predictive power of a model.

Ng [2015] provides a simple summary of PLS and shows that are singular vectors of

Partial Least Squares (PLS) uses both and to calculate the projection, further it simultaneously finds projections for both input and output , it make it applicable to the problems with high-dimensional output vector as well as input vector. Let be matrix of observed outputs and be an input matrix. PLS finds a projection directions that maximize covariance between and , the resulting projections and for and , respectively are called score matrices, and the projection matrices and are called loadings. The -score matrix , has columns, one for each “feature” and is chosen via cross-validation. The key principle is that is a good predictor of , the -scores. This relations are summarized by the equations below

Here and are orthogonal projection (loading) matrices and and are are projections of and respectively.

Originally PLS was developed to deal with the problem of collinearity in observed inputs. Although, principal component regression also addresses the problem of collinearity, it is often not clear which components to choose. The components that correspond to the larges singular values (explain the most variance in ) are not necessarily the best ones in the predictive settings. Also ridge regression addresses this problem and was criticized by [Fearn, 1983]. Further ridge regression does not naturally provide projected representations of inputs and outputs that would make it possible to combine it with other models as we propose in this paper. Thus, PLS seem to be the right method for high-dimensional problems when the goal is to model non-linear relations using another model.

In the literature, there are two types of algorithms for finding the projections [Manne, 1987]. The original one proposed by Wold et al. [1984] which uses conjugate-gradient method [Golub and Van Loan, 2013] to invert matrices. The first PLS projection and is found by maximizing the covariance between the and scores

Then the corresponding scores are

We can see from the definition that the directions (loadings) for are the right singular vectors of and loadings for are the left singular vectors. The next step is to perform regression of on , namely . The next column of the projection matrix is found by calculating the singular vectors of the residual matrices . The final regression problem is solved . Thus the PLS estimate is

Helland [1990] showed that PLS estimator can be calculated as

where ,

Helland [1988] proposed an alternative algorithm to calculate the parameters For , set . Let be centered and standardized. Given and . For to do

2.4 DL-PLS

Partial least squares algorithm finds projections of the input and output vectors and in such a way that correlation between the projected input and output is maximized. Our DL-PLS model will introduce nonlinearity by assuming that is a deep learner of . From Brillinger’s result we see that linear PLS calculates and for arbitrary .

where is a deep learner. Here is inverted to as .

Although we use a composite model DL-PLS, our estimation procedure is two-step. We first estimate the score matrices and then estimate parameters of the deep learning function . This two step process is motivated by the Brillinger [2012]. The results of Brillinger guarantee that matrices are invariant (up to proportionality) to nonlinearity, even when the true relationship between -scores and -scores is nonlinear.

PLS-ReLU

For example, is a simple feed-forward ReLU neural network, for which sparse Bayesian priors are useful to improve the generalization (Polson and Ročková [2018]). and are matrices,

The weights and are to be learned.

PLS-CNN

Partial least squares can also be used as a layer at any stage of deep learning. For example, in a convolutional neural network,

where denotes the convolution over the region , with input image , weights and bias . Then we can add a PLS layer by regressing the output on and perform feature reduction, which results in a CNN-PLS model.

PLS-Autoencoder

As the input and output have the same dimensions, one can consider using an autoencoder network. We build on the architecture of Zhang et al. [2019].

where is a matrix which acts as a lower dimensional intermediate hidden layer and .

DL-RNN

The idea of using a sequence of transformations was also previously considered for the analysis of temporal data Wiener [1964], Singpurwalla et al. [2018], West [1981]. Work of Masreliez [1975] provides an equivalent decomposition of Brillinger for time series models.

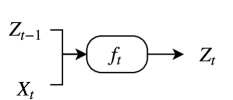

The deep learning analog is the recurrent architecture that uses autoregression in the latent feature space. Let denote the observed response and are hidden states, then the RNN model is:

where is an activation function such as . The time invariant weight matrices and are found through training the network. are external inputs up to lags, are the previous hidden states, and the hidden state is initialized to zero, .

The main difference between RNNs and feed-forward deep learning is the use of a hidden layer with an auto-regressive component, here . It leads to a network topology in which each layer represents a time step, indexed by , in order to highlight the temporal nature.

Additional depth can be added to create deep RNNs by stacking layers on top of each other, using the hidden state of the RNN as the input to the next layer. RNNs architectures are learned through the same mechanism described for feedforward architectures. One key difference between implementations of RNNs is that drop-out is not applied to the recurrent connections, only to the non-recurrent connections. In contrast, drop-out is applied to all connections in a feedforward architectures.

DL-PLS-GP

Given a new predictor matrix of size , the same projection produces the corresponding . We can use Gaussian process regression to predict from as follows

where ’s are the Gaussian process regression predictors.

where is , is , and is . is a kernel function. The conditional mean, , is given by

Then prediction of is

3 Finding Good Prediction Rules

There are two ways of finding good prediction rules in high dimensions. One is via shrinkage and the other is based on ensemble rules.

3.1 Shrinkage

We will rely heavily on the Bayesian shrinkage interpretation of PCR and PLS due to Frank and Friedman (1993). Polson and Scott [2010, 2012] provide a general theory of global-local shrinkage and, in particular, analyze -prior and horseshoe shrinkage. PLS behaves differently from standard shrinkage rules as it can shrink away from the origin for certain eigen-directions.

The corresponding shrinkage factors for RR and PCR are typically normalized so that they give the same overall shrinkage so that the length of solution vector are the same ().

This scale factors provide a diagnostic plot: . If any then one can expect supervised learning (a.k.a. PLS with ’s influence the scaling factors) will lead to different predictions than unsupervised learning (a.k.a. PCR with solely dependent on ). In this sense, PLS is an optimistic procedure in that the goal is to maximise the explained variability of the output in sample with the hope of generalizing well out-of-sample. For linear estimator, means that both the bias and the variance are increased. Frank and Friedman [1993] mention the possibility of improving the performance of PLS by modifying the scale factors as , although it’s not certain since PLS is not linear. The shrinkage factors of PLS are also discussed in Rosipal and Krämer [2005] and are closely related to the Ritz pairs.

The key insight is that all of the estimators are of the from

where are scale factors. denotes method (e.g. RR, PCR, PLS). is the rank of (number of nonzero ). For PCR, the scale factors are for top eigenvectors Frank and Friedman [1993]

The Bayesian paradigm provides novel insights into how to construct estimators with good predictive performance. The goal is simply to find a good predictive MSE, namely , where denotes a prediction value. Stein shrinkage (a.k.a regularization with an norm) in known to provide good mean squared error properties in estimation, namely . These gains translate into predictive performance (in an iid setting) for .

The main issue is how to tune the amount of regularization (a.k.a prior hyper-parameters). Stein’s unbiased estimator of risk provides a simple empirical rule to address this problem as does cross-validation. From a Bayes perspective, the marginal likelihood (and full marginal posterior) provides a natural method for hyper-parameter tuning. The issue is computational tractability and scalability. In the context of DL, the posterior for is extremely high dimensional and multimodal and posterior MAP provides good predictors .

3.2 Ensemble Predictors

Bayes conditional averaging performs well in high dimensional regression and classification problems. High dimensionality, however, brings with it the curse of dimensionality and it is instructive to understand why certain kernel can perform badly. Adaptive Kernel predictors (a.k.a. smart conditional averager) are of the form

Here is a deep predictor with its own trained parameters. For tree models, the kernel is a cylindrical region (open box set). Figure 6 illustrates the implied kernels for trees (cylindrical sets) and random forests. Not too many points will be neighbors in a high dimensional input space.

|

|

| (a) Tree Kernel | (b) Random Forest Kernel |

Constructing the regions to preform conditional averaging is fundamental to reduce the curse of dimensionality. Deep learning can improve on traditional methods by performing a sequence of GLM-like transformations. Effectively DL learns a distributed partition of the input space. For example, suppose that we have partitions and a DL predictor that takes the form of a weighted average or soft-max of the weighted average for classification. Given a new high dimensional input , many deep learners are then an average of learners obtained by our hyper-plane decomposition. Our predictor takes the form

where are the weights learned in region , and is an indicator of the region with appropriate weighting given the training data.

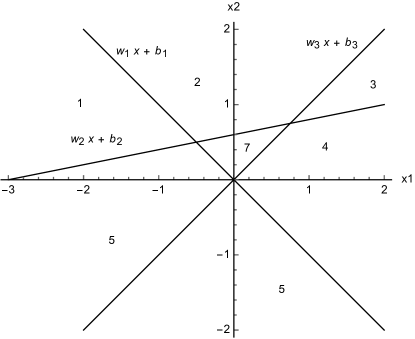

The partitioning of the input space by a deep learner is similar to the one performed by decision trees and partition-based models such as CART, MARS, RandomForests, BART, and Gaussian Processes. Each neuron in a deep learning model corresponds to a manifold that divides the input space. In the case of ReLU activation function the manifold is simply a hyperplane and the neuron gets activated when the new observation is on the “right” side of this hyperplane, the activation amount is equal to how far from the boundary the given point is. For example in two dimensions, three neurons with ReLU activation functions will divide the space into seven regions, as shown on Figure 7.

The key difference between tree-based architecture and neural network based models is the way hyper-planes are combined. Thus, the number of hyper-planes grow exponentially with the number of layers. The key property of an activation function (link) is and it has zero value in certain regions. For example, hinge or rectified learner box car (differences in Heaviside) functions are very common. As compared to a logistic regression, rather than using in deep learning is typically used for training, as .

Amit and Geman [1997] provide an interesting discussion of efficiency. Formally, a Bayesian probabilistic approach (if computationally feasible) optimally weights predictors via model averaging with

Such rules can achieve optimal out-of-sample performance. Amit et al. [2000] discusses the striking success of multiple randomized classifiers. Using a simple set of binary local features, one classification tree can achieve 5% error on the NIST data base with 100,000 training data points. On the other hand, 100 trees, trained under one hour, when aggregated, yield an error rate under 7%. This stems from the fact that a sample from a very rich and diverse set of classifiers produces, on average, weakly dependent classifiers conditional on class.

1/ Ensamble Rules

To further exploit this, consider the model of weak dependence, namely exchangeability. This often occurs in high dimensional spaces, where it is easy to find a prediction rule with high variance and the rule by a portfolio argument reduces the variance.

Suppose that we have exchangeable, , and stacked predictors

Suppose that we wish to find weights, , to attain where convex in the second argument;

where . Hence, the randomized multiple predictor with weights provides the optimal Bayes predictive performance.

3.3 Brillinger Estimation

Brillinger [2012] considers the single-index model with non-Gaussian regressors where are stochastic with conditional distribution

Here is the single features found by data reduction from high dimensional . Let denote the least squares estimator which solved . By Stein’s lemma,

Then is consistent as

Hence, estimator is proportional to . We can also non-parametrically estimate by plotting and smoothing values with near .

Hence, when the s are Gaussians and independent of the error, we have the relationship . This relationship follows from the weaker assumption

Hence, this approach can be applied to binary classification with and other models such as survival models.

If we substitute in equation 2 with to get , to minimize predictive MSE for future observations, we simply use the conditional mean . In terms of the loading matrix we are to have the predictive rule

The Brillinger result allows us to estimate the using PLS. Essentially, we have a multivariate index model. As long as we have stochastic regressions, we can identify the matrix. Surprisingly you can identify the weights and the latent variables that then determine the features using only OLS or PLS.

4 Applications

4.1 Identifying Nonlinear Systems

To illustrate our methodology, we start with multivariate observation and state identification problem. We start with a simple linear example to show how sequential steps of PLS is used to estimate the coefficient matrix .

where , and . is the matrix of i.i.d. noises drawn from normal distribution.

Since it is a simple linear system, the OLS directly identifies , however, it is instructive to see how the sequential PLS performs the same task.

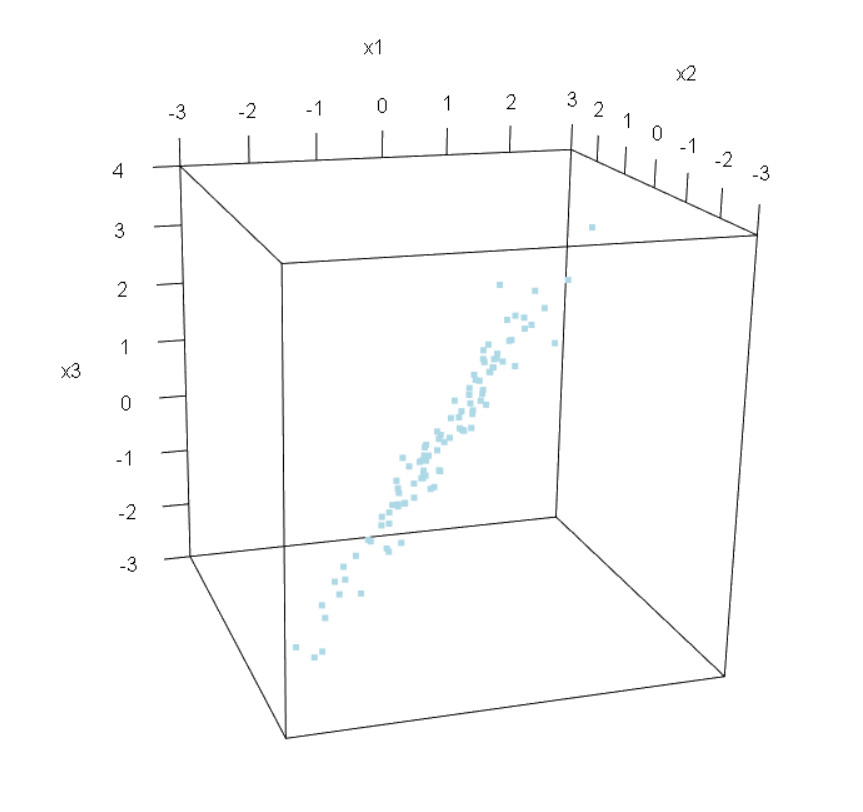

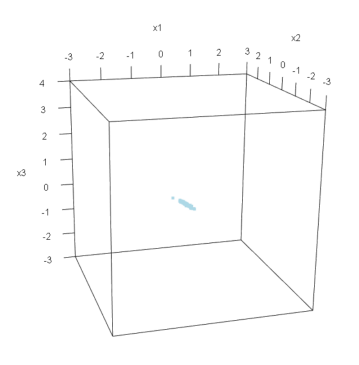

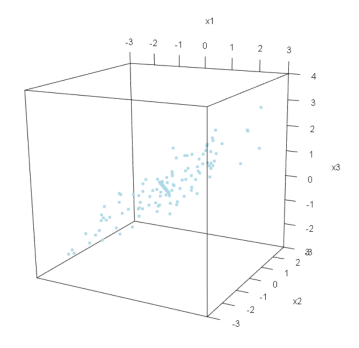

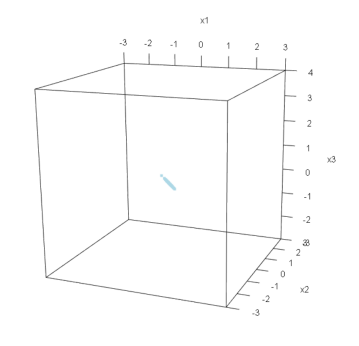

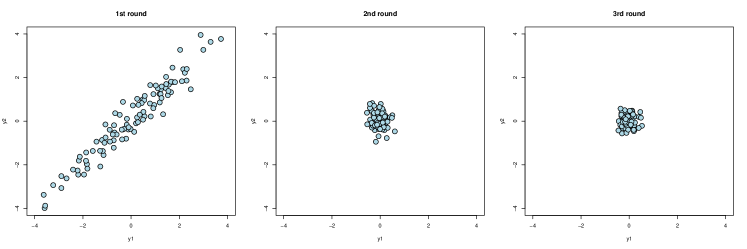

Figure 8 provides two rotational views of 2-dimensional variables and as we move from the left to right, the sequential implementation of the PLS algorithms to find the latent score features. Each iteration extracts one additional component of the data.

Figure 9 shows the effect of the PLS data transformations on the output variable. To identify the system the goal is to transform the output variable until it looks like white nose. As you see in Figure 9 it occurs in one step and our dimensionality reduction is performed. The second step provides a marginal improvement.

Correspondingly, when we regress the the multivariate output on scores, we recover the loadings matrix . Moreover, we can generalize it to a non-linear system using Brillinger result. We can use either OLS or PLS to identify the system.

where and . Using OLS or PLS, we can estimate the coefficient and successfully recover the nonlinear absolute function.

4.2 Simulated Examples

4.2.1 Dimension Reduction

First, we consider how deep learning can be used as a sufficient dimensionality reduction technique to identify lower dimensional features that can be later used as inputs to statistical models. We start with a synthetic example that demonstrates an application of one layer neural network to find a piece-wise linear structure in the data. Consider real-valued function ,

We generate input-output pairs , where , and . There is one-dimensional structure in the input-output relations which is represented by a ridge function . We use neural network to identify this one dimensional structure. We introduce a one-dimensional bottleneck in our neural network. The overall architecture is as follows , where , and . Both and are single layer neural networks.

![[Uncaptioned image]](/html/2110.11561/assets/x16.png) |

![[Uncaptioned image]](/html/2110.11561/assets/x17.png) |

| vs | vs |

4.3 MARTHE

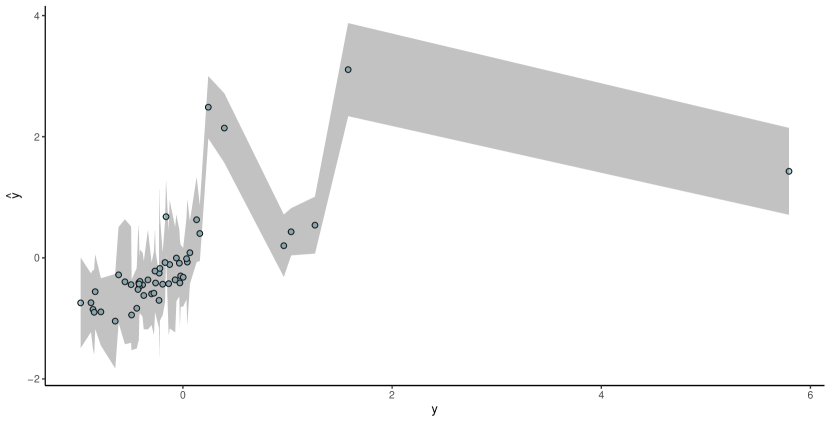

The MARTHE dataset [Surjanovic and Bingham, ] consists of input-output pairs where outputs are realizations of the numerical simulation of Strontium-90 transport in the upper aquifer of the RRC “Kurchatov Institute” radwaste disposal site in Moscow, Russia [Volkova et al., 2008]. The input vector has components describing physical properties of the aquifer, such as hydraulic conductivity, porosity and transversal dispersivity. The outputs are contaminant concentrations at 10 wells, To illustrate our methodology, we use the output at one well, well number eight.

Gaussian Processes (GPs) have been used to provide an output map together with uncertainty bands. Figure 11 shows the scatter plot of the predicted values with 95% confidence band of the GP model and the actual observations .

We use a Gaussian Process with zero mean and separable anisotropic Gaussian covariance function which is the sum of inverse exponentiated squared difference plus the nugget

The lengthscale parameters of the covariance function and the nugget parameter were estimated by maximizing the Bayesian integrated log likelihood Gramacy [2016, 2020].

Our merging of two cultures leads to an improved fit and predictive map as follows. First, we use partial least squares (PLS) [Polson et al., 2021] to provide feature selection. Remember that the learned features depend on both the input and output pairs leading to an optimal mean squared error in-sample fit. Moreover, PLS provides a dimension reduction, that helps in the GP model at the top level. Dimensionality reduction is crucial in many applications. For example in the problems of sequential design of experiment, when lower dimensionality allows for more efficient exportation of the input space [MacKay, 1992, Fedorov and Hackl, 1997].

We can view our model as a hierarchical latent feature model, where we use the stochastic GP model to provide a predictive distribution at the top level.

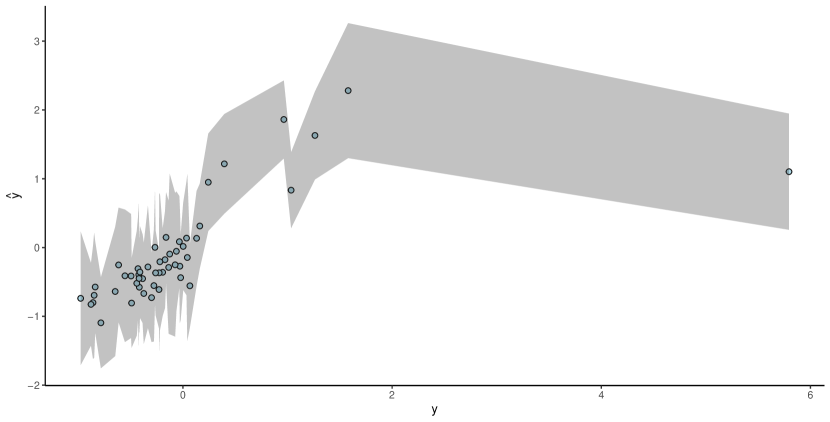

4.4 PLS-GP

Given a new predictor matrix of size we wish to find a predictor of the output . First, we use the same projection produces the corresponding input scores . These can be interpreted as the hidden latent features. Then Gaussian process regression finds the predictor of the output scores , component-by-component, using the features as follows

where ’s are the Gaussian process regression predictors.

where is , is , and is . is a kernel function. The conditional mean, from the GP model is given by

Then prediction of then takes the form .

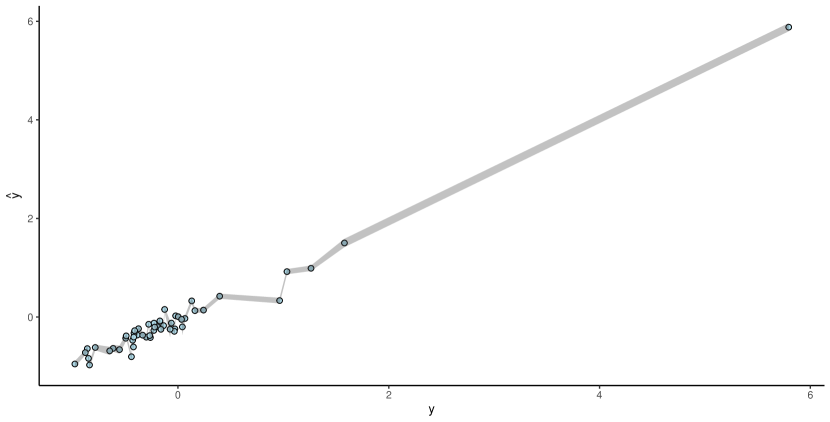

Figure 12 shows the comparison of the predicted and actual values along with uncertainty bounds

For the PLS dimensionality reduction we used cross-validation to select the number of components.

4.5 Deep Learning Gaussian Process

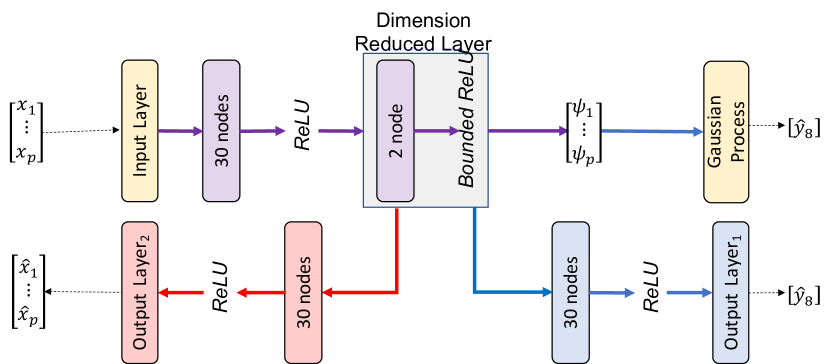

Both PLS and DL learn a low dimensional representation of the input vector. We build a combined DL-GP model. The goal of the DL model is to find , which is a reduced dimensionality representation of input vector . Then to use a Gaussian Process to model relations between low dimensional inputs and the output . Our architecture is shown in Figure 13.

Figure 14 shows the predicted and actual scattershot.

| Plain GP | PLS + GP | DL + GP | |

|---|---|---|---|

| RMSE | 4.5 | 1.6 | 0.89 |

| MAPE | 0.8 | 0.73 | 0.16 |

5 Discussion

The goal of statistics is to build predictive models along with uncertainty and to develop understanding about the data generating mechanism. Data models are well studied in statistical literature but often do not provide enough flexibility to learn the input-output relations. Black box predictive rules such as trees and neural networks, are more flexible learners but do not provide predictive uncertainties or ability for probabilistic modeling.

Data can be though of as generated by black box on which a vector of input variables is mapped to an output (or response vector ). One goal is prediction to be able to assign a response variable to a new (unseen before) input . Two cultures have emerged: stochastic methods with parameters or black box predictions rules. What makes a good statistical model? What makes a good prediction rule? Given a model (and computation) leads to an optimal prediction rule. However, in high dimensional problems finding good models is challenging. One needs a good a priori distribution that gets updated in the light of evidence.

Our methodology provides a merging of these two cultures. We show that deterministic black box rule can be used as transformation of high dimensional inpour and outputs. In the transformed space lead to hidden features that are empirically learned as supposed to theoretically specified. Statistical modeling then provides uncertainty assessment via traditional Bayesian updating methods.

References

- Adragni and Cook [2009] Kofi P. Adragni and R. Dennis Cook. Sufficient dimension reduction and prediction in regression. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 367(1906):4385–4405, 2009. doi: 10.1098/rsta.2009.0110. URL https://royalsocietypublishing.org/doi/abs/10.1098/rsta.2009.0110.

- Amit and Geman [1997] Y. Amit and D. Geman. Shape Quantization and Recognition with Randomized Trees. Neural Computation, 9(7):1545–1588, July 1997.

- Amit et al. [2000] Yali Amit, Gilles Blanchard, and Kenneth Wilder. Multiple randomized classifiers: Mrcl. 2000.

- Bengio [2009] Yoshua Bengio. Learning deep architectures for ai. Foundations and trends® in Machine Learning, 2(1):1–127, 2009.

- Bhadra et al. [2019] Anindya Bhadra, Jyotishka Datta, Yunfan Li, and Nicholas G Polson. Horseshoe regularization for machine learning in complex and deep models. arXiv preprint arXiv:1904.10939, 2019.

- Bishop [1995] Christopher M Bishop. Neural networks for pattern recognition. Oxford university press, 1995.

- Breiman [2001] Leo Breiman. Statistical modeling: The two cultures (with comments and a rejoinder by the author). Statistical science, 16(3):199–231, 2001.

- Brillinger [2012] David R. Brillinger. A Generalized Linear Model With “Gaussian” Regressor Variables. In Peter Guttorp and David Brillinger, editors, Selected Works of David Brillinger, Selected Works in Probability and Statistics, pages 589–606. Springer, New York, NY, 2012. ISBN 978-1-4614-1344-8. doi: 10.1007/978-1-4614-1344-8˙34. URL https://doi.org/10.1007/978-1-4614-1344-8_34.

- Cook [2007] R Dennis Cook. Fisher lecture: Dimension reduction in regression. Statistical Science, 22(1):1–26, 2007.

- Cook and Forzani [2009] R Dennis Cook and Liliana Forzani. Likelihood-based sufficient dimension reduction. Journal of the American Statistical Association, 104(485):197–208, 2009.

- Devlin et al. [2018] Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. Bert: Pre-training of deep bidirectional transformers for language understanding. arXiv preprint arXiv:1810.04805, 2018.

- Dixon et al. [2019] Matthew F. Dixon, Nicholas G. Polson, and Vadim O. Sokolov. Deep learning for spatio-temporal modeling: Dynamic traffic flows and high frequency trading. Applied Stochastic Models in Business and Industry, 35(3):788–807, 2019. doi: https://doi.org/10.1002/asmb.2399. URL https://onlinelibrary.wiley.com/doi/abs/10.1002/asmb.2399.

- Ehrenberg [1968] A. S. C. Ehrenberg. The elements of lawlike relationships. Journal of the Royal Statistical Society. Series A (General), 131(3):280–302, 1968. ISSN 00359238. URL http://www.jstor.org/stable/2343524.

- Fadikar et al. [2018] Arindam Fadikar, Dave Higdon, Jiangzhuo Chen, Bryan Lewis, Srinivasan Venkatramanan, and Madhav Marathe. Calibrating a stochastic, agent-based model using quantile-based emulation. SIAM/ASA Journal on Uncertainty Quantification, 6(4):1685–1706, 2018.

- Fearn [1983] T. Fearn. A Misuse of Ridge Regression in the Calibration of a Near Infrared Reflectance Instrument. Journal of the Royal Statistical Society: Series C (Applied Statistics), 32(1):73–79, 1983. ISSN 1467-9876.

- Fedorov and Hackl [1997] Valerii V Fedorov and Peter Hackl. Model-oriented design of experiments, volume 125. Springer Science & Business Media, 1997.

- Fisher [1922] Ronald A Fisher. On the mathematical foundations of theoretical statistics. Philosophical Transactions of the Royal Society of London. Series A, Containing Papers of a Mathematical or Physical Character, 222(594-604):309–368, 1922.

- Frank and Friedman [1993] Ildiko E. Frank and Jerome H. Friedman. A Statistical View of Some Chemometrics Regression Tools. Technometrics, 35(2):109–135, 1993. ISSN 0040-1706. doi: 10.2307/1269656. URL https://www.jstor.org/stable/1269656.

- Golub and Van Loan [2013] Gene H Golub and Charles F Van Loan. Matrix computations. JHU press, 2013.

- Gramacy [2016] Robert B Gramacy. lagp: large-scale spatial modeling via local approximate gaussian processes in r. Journal of Statistical Software, 72(1):1–46, 2016.

- Gramacy [2020] Robert B Gramacy. Surrogates: Gaussian process modeling, design, and optimization for the applied sciences. Chapman and Hall/CRC, 2020.

- Gramacy and Lee [2008] Robert B Gramacy and Herbert K H Lee. Bayesian treed gaussian process models with an application to computer modeling. Journal of the American Statistical Association, 103(483):1119–1130, 2008.

- Harding [1967] Edward Frank Harding. The number of partitions of a set of n points in k dimensions induced by hyperplanes. Proceedings of the Edinburgh mathematical society, 15(4):285–289, 1967.

- Heaton et al. [2017] JB Heaton, NG Polson, and Jan Hendrik Witte. Deep learning for finance: deep portfolios. Applied Stochastic Models in Business and Industry, 33(1):3–12, 2017.

- Helland [1988] Inge S. Helland. On the structure of partial least squares regression. Communications in Statistics - Simulation and Computation, 17(2):581–607, 1988. ISSN 0361-0918. doi: 10.1080/03610918808812681. URL https://doi.org/10.1080/03610918808812681.

- Helland [1990] Inge S. Helland. Partial Least Squares Regression and Statistical Models. Scandinavian Journal of Statistics, 17(2):97–114, 1990.

- Higdon et al. [2008] Dave Higdon, James Gattiker, Brian Williams, and Maria Rightley. Computer model calibration using high-dimensional output. Journal of the American Statistical Association, 103(482):570–583, 2008.

- Hoadley [2001] Bruce Hoadley. Statistical Modeling: The Two Cultures: Comment. Statistical Science, 16(3):220–224, 2001. ISSN 08834237. URL http://www.jstor.org/stable/2676684.

- Kim et al. [2005] Hyoung-Moon Kim, Bani K Mallick, and CC Holmes. Analyzing nonstationary spatial data using piecewise gaussian processes. Journal of the American Statistical Association, 100(470):653–668, 2005.

- Li [1991] Ker-Chau Li. Sliced inverse regression for dimension reduction. Journal of the American Statistical Association, 86(414):316–327, 1991.

- Lindley [1968] D. V. Lindley. The choice of variables in multiple regression. Journal of the Royal Statistical Society. Series B (Methodological), 30(1):31–66, 1968. ISSN 00359246. URL http://www.jstor.org/stable/2984458.

- Litjens et al. [2017] Geert Litjens, Thijs Kooi, Babak Ehteshami Bejnordi, Arnaud Arindra Adiyoso Setio, Francesco Ciompi, Mohsen Ghafoorian, Jeroen Awm Van Der Laak, Bram Van Ginneken, and Clara I Sánchez. A survey on deep learning in medical image analysis. Medical image analysis, 42:60–88, 2017.

- MacKay [1992] David JC MacKay. Information-based objective functions for active data selection. Neural computation, 4(4):590–604, 1992.

- MacKay [1998] David JC MacKay. Introduction to Gaussian Processes. NATO ASI series F computer and systems sciences, 168:133–166, 1998.

- Mallows [1973] C. L. Mallows. Some Comments on CP. Technometrics, 15(4):661–675, 1973. ISSN 0040-1706. doi: 10.2307/1267380. URL https://www.jstor.org/stable/1267380. Publisher: [Taylor & Francis, Ltd., American Statistical Association, American Society for Quality].

- Manne [1987] Rolf Manne. Analysis of two partial-least-squares algorithms for multivariate calibration. Chemometrics and Intelligent Laboratory Systems, 2(1):187–197, 1987.

- Masreliez [1975] C Masreliez. Approximate non-gaussian filtering with linear state and observation relations. IEEE Transactions on Automatic Control, 20(1):107–110, 1975.

- McCullagh [2019] Peter McCullagh. Generalized linear models. Routledge, 2019.

- Neal [2012] Radford M Neal. Bayesian learning for neural networks, volume 118. Springer Science & Business Media, 2012.

- Ng [2015] Kee Siong Ng. A simple explanation of partial least squares. 2015.

- Olshausen and Field [1996] Bruno A Olshausen and David J Field. Emergence of simple-cell receptive field properties by learning a sparse code for natural images. Nature, 381(6583):607, 1996.

- Polson et al. [2021] Nicholas Polson, Vadim Sokolov, and Jianeng Xu. Deep Learning Partial Least Squares. arXiv preprint arXiv:2106.14085, 2021.

- Polson and Ročková [2018] Nicholas G Polson and Veronika Ročková. Posterior concentration for sparse deep learning. Advances in Neural Information Processing Systems, 31, 2018. URL https://proceedings.neurips.cc/paper/2018/file/59b90e1005a220e2ebc542eb9d950b1e-Paper.pdf.

- Polson and Scott [2010] Nicholas G. Polson and James G. Scott. Shrink Globally, Act Locally: Sparse Bayesian Regularization and Prediction, volume 105. Oxford University Press, 2010. Bayesian Statistics 9.

- Polson and Scott [2012] Nicholas G. Polson and James G. Scott. Local shrinkage rules, Lévy processes and regularized regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 74(2):287–311, 2012. doi: https://doi.org/10.1111/j.1467-9868.2011.01015.x. URL https://rss.onlinelibrary.wiley.com/doi/abs/10.1111/j.1467-9868.2011.01015.x.

- Polson and Sokolov [2017] Nicholas G. Polson and Vadim Sokolov. Deep Learning: A Bayesian Perspective. Bayesian Analysis, 12(4):1275–1304, 2017. ISSN 1936-0975, 1931-6690. doi: 10.1214/17-BA1082. URL https://projecteuclid.org/journals/bayesian-analysis/volume-12/issue-4/Deep-Learning-A-Bayesian-Perspective/10.1214/17-BA1082.full.

- Polson et al. [2013] Nicholas G Polson, James G Scott, and Jesse Windle. Bayesian inference for logistic models using pólya–gamma latent variables. Journal of the American statistical Association, 108(504):1339–1349, 2013.

- Ripley [2007] Brian D Ripley. Pattern recognition and neural networks. Cambridge university press, 2007.

- Rosipal and Krämer [2005] Roman Rosipal and Nicole Krämer. Overview and recent advances in partial least squares. In International Statistical and Optimization Perspectives Workshop” Subspace, Latent Structure and Feature Selection”, pages 34–51. Springer, 2005.

- Singpurwalla et al. [2018] Nozer D Singpurwalla, Nicholas G Polson, and Refik Soyer. From least squares to signal processing and particle filtering. Technometrics, 60(2):146–160, 2018.

- Srivastava et al. [2014] Nitish Srivastava, Geoffrey Hinton, Alex Krizhevsky, Ilya Sutskever, and Ruslan Salakhutdinov. Dropout: a simple way to prevent neural networks from overfitting. The journal of machine learning research, 15(1):1929–1958, 2014.

- [52] S. Surjanovic and D. Bingham. Virtual library of simulation experiments: Test functions and datasets. Retrieved December 20, 2019, from http://www.sfu.ca/~ssurjano.

- Volkova et al. [2008] E Volkova, B Iooss, and F Van Dorpe. Global sensitivity analysis for a numerical model of radionuclide migration from the rrc “Kurchatov Institute” radwaste disposal site. Stochastic Environmental Research and Risk Assessment, 22(1):17–31, 2008.

- Wahba [1990] Grace Wahba. Spline models for observational data, volume 59. Siam, 1990.

- West [1981] Mike West. Robust sequential approximate bayesian estimation. Journal of the Royal Statistical Society: Series B (Methodological), 43(2):157–166, 1981.

- Wiener [1964] Norbert Wiener. Extrapolation, interpolation, and smoothing of stationary time series: with engineering applications. MIT press Cambridge, MA, 1964.

- Wold et al. [1984] S. Wold, A. Ruhe, H. Wold, and W. J. Dunn, III. The Collinearity Problem in Linear Regression. The Partial Least Squares (PLS) Approach to Generalized Inverses. SIAM Journal on Scientific and Statistical Computing, 5(3):735–743, 1984. ISSN 0196-5204. doi: 10.1137/0905052. URL https://doi.org/10.1137/0905052.

- Zhang et al. [2019] Chu Zhang, Tian Peng, Jianzhong Zhou, Jie Ji, and Xiaolu Wang. An improved autoencoder and partial least squares regression-based extreme learning machine model for pump turbine characteristics. Applied Sciences, 9(19):3987, 2019.