-functions and the topology of superlevel sets of stochastic processes

Abstract

We describe the topology of superlevel sets of (-stable) Lévy processes X by introducing so-called stochastic -functions, which are defined in terms of the widely used -functional in the theory of persistence modules. The latter share many of the properties commonly attributed to -functions in analytic number theory, among others, we show that for -stable processes, these (tail) -functions always admit a meromorphic extension to the entire complex plane with a single pole at , of known residue and that the analytic properties of these -functions are related to the asymptotic expansion of a dual variable, which counts the number of variations of X of size . Finally, using these results, we devise a new statistical parameter test using the topology of these superlevel sets. We further develop an analogous theory, whereby we consider the dual variable to be the number of points in the persistence diagram inside the rectangle .

Index terms— Dirichlet series; zeta functions; stochastic processes; topology of superlevel sets; persistent homology; self-similar processes; Lévy processes

MSC2020 Classification— 60D05, 62F03, 30B50, 55N31, 60G18

1 Introduction

The problem of the characterization of the topology of superlevel sets of random functions has been a long studied topic in the theory of random fields. While a complete description has been thus far unknown, partial descriptors of the topology of superlevel sets, such as their Euler characteristic, have been described for certain classes of random processes [2, 3, 4, 37, 13, 32]. Thus far, the study of the homology of superlevel sets of random functions in dimension one has focused on either smooth random (Gaussian) fields [2, 3], or irregular processes which are in some sense canonical, such as Brownian motion [13, 37, 4]. In this paper, following the universality reasoning detailed in [36, §3], we will adopt the second point of view while enlarging the category of processes considered to objects acting as universal limits of random processes in 1D.

This work is another stage in a program started in [35] and later continued in [36], which aimed to characterize the barcodes of random functions as completely as possible (in dimension one). To do this, we adopted the tree formalism originally developped by Le Gall [19, 20], which brings benefits in the probabilistic setting. This formalism allowed us to partially study the case of Markov or self-similar processes, and to processes admitting the two latter as limits [36]. In this paper, we further develop the theory to describe almost completely the case of (-stable) Lévy processes.

The understanding of so-called topological noise is an active area of research in Topological Data Analysis (TDA) (cf. section 2.3 for a quick introduction, or [12, 34] for a more comprehensive one). This topological noise is characterized by the behaviour of the small bars of the barcode of a function and its role is particularly difficult to grasp. Nonetheless, topological noise has proved useful in a variety of different applications, which seem to exploit the information contained therein, sometimes directly, or indirectly through the use of Wasserstein metrics on the space or functionals such as [15, 31, 43, 17, 10], despite the absence of general stability results. The program described above is based around the intuition that while it might be hopeless to find a general stability theorem, there should be a form of statistical stability of barcodes.

By statistical stability we mean that any two samples drawn from the same probability distribution should have “close” or “similar” behaviour of its topological noise. For example, this paper shows that, at least in the simple setting of 1D and for a fairly wide range of distributions, this topological noise does indeed exhibit the robustness sought. More precisely, we show that the number of bars of length , , is a dual to , and that it exhibits the statistical robustness required, such as an almost sure asymptotic behaviour as .

If this notion of statistical stability is a good one, a natural subsequent question is whether it is possible to differentiate stochastic processes given their topological signature. In this paper, we partially answer this question positively through the development of a statistical test constructed with the functional , which can differentiate -stable processes for different values of . In dimension one, while interesting, this development is unlikely to do better than wavelet analysis or other known techniques (cf. [16] and the references therein). However, further developments in this direction could eventually lead to “topological statistics”, i.e. robust statistical tests for random fields, for which all known techniques do not generalize, but for which barcodes are easily computable.

This discussion and the results of this paper hint at the fact that statistical stability is a correct notion of stability to consider, and there are many open questions to be tackled, some of these questions are:

-

•

Dimensionality: are the statistical stability results of this paper particular to dimension one, or do they generalize in some way to higher dimensional random fields?

-

•

Signal vs. noise problem: Given the regular structure of topological noise shown in this paper, does this allow us to detect the presence of an underlying topological signal?

-

•

Statistical robustness of topological noise: What can we say, quantitatively, about the variation of topological noise induced by perturbations of the distribution of the noise (for instance in some Wasserstein metric)?

-

•

Best proxys for topological signatures: much of this paper was inspired by what is used in practice, namely Wasserstein metrics and the functional and its dual . However, there is no guarantee this yields the best possible proxys to answer the two previous problems. In this regard, is it possible to prove or disprove which proxys do best in what context?

From a more probabilistic point of view, this paper introduces so-called -functions associated to a stochastic process, constructed using the functional we previously discussed. The main, and perhaps most important, departure from the conventional TDA theory is that we will consider this quantity for complex for reasons which will become evident throughout this paper, but which are analogous to the ones behind the complexification of the Riemann -function in analytic number theory. There are some similarities to the results of Pitman, Yor and Biane in [39, 6, 38] regarding the probabilistic interpretation of the -function and more generally -functions based on connections with some families of infinitely divisible distributions connected to Brownian motion. However, the -functions herein are of different nature to those considered by Pitman, Yor and Biane, as they stem from a different construction. For Brownian motion, we fall back on one of the infinitely divisible distributions considered by these authors. Renewal theory [23] intervenes at many different steps in this paper and combined with the results of Pitman, Yor and Biane, it is a posteriori perhaps not surprising that the -functions hereby introduced share some of the analycity properties of the Riemann -function.

1.1 Our contribution

More precisely, our contribution can be split along the following lines:

-

1.

We establish a duality relation with respect to the Mellin transform between the study of and the number of leaves of a -trimmed tree , (cf. section 2.5). With the help of a correct notion of integration on trees developped in [37], it is possible to prove an interpolation theorem for (proposition 2.18);

-

2.

We introduce -functions for stochastic processes and for persistent measures (cf. section 2.6 and section 2.7 respectively). We show an interpolation theorem for Wasserstein -distances between diagrams (proposition 2.41) and a characterization of convergence between diagrams in these Wasserstein distances in terms of the -functions introduced (theorem 2.45).

-

3.

We show that in the context of -stable Lévy processes, the associated (tail) -functions always admit a meromorphic extension to the entire complex plane, with a unique pole at with known residue (theorem 3.25). By duality, this meromorphic extension implies the existence of an asymptotic series for as , which we explicitly calculate up to superpolynomial (i.e. smaller than any polynomial) corrections (theorem 3.15). An explicit form of the meromorphic continuation of is shown to be related to the superpolynomial corrections to the asymptotic expansion of theorem 3.15 (cf. section 2.1.1). We also define a generating function for the length of the th longest bar (cf. section 3.3.2);

-

4.

We give an almost sure result detailing the asymptotics of for any continuous semimartingale (proposition 3.1), which turns out to be related to the quadratic variation of the process, providing further evidence for the link between regularity and hinted at in [37, 40]. We conclude from this that the -functions associated to continuous semimartingales always have a simple pole at ;

-

5.

We apply the theory above to different stochastic processes, such as Brownian motion, reflected Brownian motion. We derive explicit formulæ for the respective -functions of these processes and infer the associated asymptotic expansions of (theorems 4.2, 4.14 propositions 4.4 and 4.15) and in the case of Brownian motion, the explicit distribution of the length of the th longest bar (cf. section 4.1.2).

-

6.

We design a statistical test for the parameter of -stable Lévy processes by using the theory previously described (cf. section 3.3.3);

-

7.

We study local trees and introduce local -functions (cf. section 2.6) and deduce formulæ for the number of points contained in the rectangle of the persistence diagram, , by introducing the notion of propagators, which, for Markov processes, reduces the problem of the study of to the study of hitting times of the process (cf. section 3.4), in particular, we link the regularity of these propagators with meromorphic extensions of the local -functions of the process (proposition 3.40);

-

8.

Finally, we apply the theory above to different stochastic processes, such as Brownian motion, reflected Brownian motion, Brownian motion with drift and the Ornstein-Uhlenbeck process for which explicit computations are possible. We derive explicit formulæ for the respective (local, global) -functions of these processes and infer the associated asymptotic expansions of (theorems 4.6, 4.14 propositions 4.13 and 4.15 and section 4.3). We also infer formulæ regarding the Ornstein-Uhlenbeck process, in particular concerning its local time (cf. section 4.4).

2 Generalities

2.1 The Mellin transform

Definition 2.1.

Let be a locally integrable function over the ray . The Mellin transform of is

Note that is the Haar measure of . The Mellin transform reflects the Pontryagin duality with respect to this locally compact abelian group. Its theory is analogous to that of the bilateral Laplace transform, as the map induces an isomorphism of abelian groups.

Notation 2.2.

For convenience, we will also employ the shorthand notation .

Definition 2.3.

The fundamental strip of , is the maximal set

where is well defined.

The Mellin transform can be inverted by virtue of the following theorem, which follows from the Laplace inversion theorem.

Theorem 2.4 (Mellin inversion,[18, 33]).

Let have fundamental strip and let . Then

-

1.

If is integrable and is integrable, then for almost every

If is continuous, the equality holds everywhere.

-

2.

If is locally integrable and of bounded variation in a neighbourhood of , then

A sufficient condition for the Mellin transform to be well-defined on is that the function is such that

In fact, Mellin transforms are a good tool to study asymptotic expansions as suggested by the following theorem.

Theorem 2.5 (Fundamental correspondence, [21]).

Let be a continuous function with non-empty fundamental strip . Then,

-

•

Assume that admits a meromorphic continuation to the strip for , that it has only a finite amount of poles there and that it is analytic on . Assume also that there exists such that along a denumerable set of horizontal segments with where ,

Indexing the poles on by their location and by their order and denoting the th coefficient in the Laurent expansion around of , we have an asymptotic expansion of around

-

•

Conversely, if the function has such an asymptotic expansion around , then has a meromorphic continuation to the strip .

Furthermore, an analogous statement holds true for asymptotic expansions around and meromorphic continuations beyond .

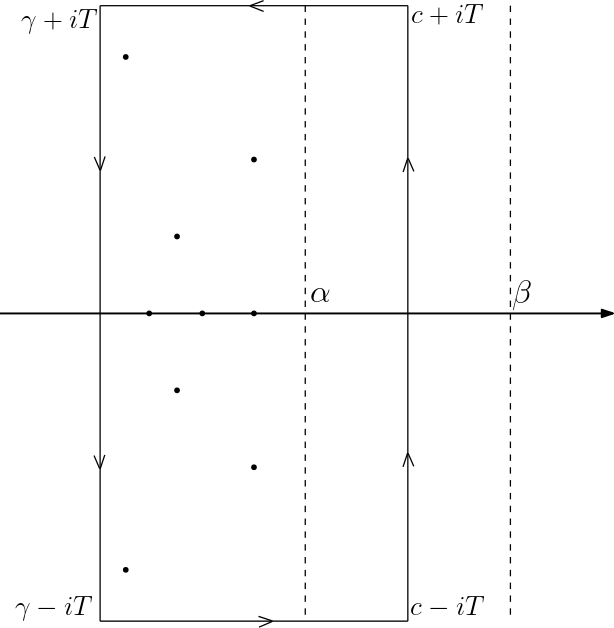

Sketch of proof.

It suffices to perform contour integration using the contour of figure 1. The estimates of the theorem allow us to discard the top and bottom integrals and to state that the integral of the path along is . Conversely, consider

for some . It follows that

which is well-defined on the strip . ∎

2.1.1 Analytic continuation

As stated by the fundamental correspondence (theorem 2.5), the existence of an asymptotic expansion around of entails a meromorphic continuation of to a larger strip. If admits a converging Laurent series (with finite singular part) on some open disk around the origin, then this extension is in fact valid over all of , and the residues of the poles of will be related to the Laurent coefficients of . It turns out that in this context, one can even write an explicit integral representation for the extension of .

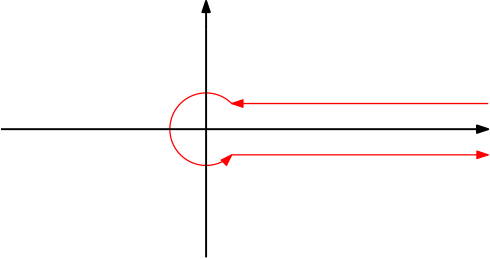

Lemma 2.6 (Integral representation of ).

Let be a meromorphic function admitting a Laurent series at , with singular part of degree , holomorphic on a neighbourhood of and integrable over the Hankel contour (cf. figure 2). Suppose further that its fundamental strip is non-empty. Then, the function admits a meromorphic continuation on given by

where denotes the Hankel contour.

Proof.

We start by splitting the Hankel contour into three pieces.

-

1.

A segment from to ;

-

2.

A circle around the origin of radius ;

-

3.

A segment from to .

For , is holomorphic everywhere on this contour, so that we may take according to Cauchy’s theorem. Notice also that

It follows that for

as desired. The integral over the complex contour converges for all . Finally, the second expression for is obtained through Euler’s reflection formula, namely

which after some simplification yields the desired expression. ∎

Remark 2.7.

If has fundamental strip , then the extension given by this procedure holds over .

Furthermore, if posseses a meromorphic continuation to (i.e. we admit the possibility of a branch cut on the positive real axis), then we can find a more explicit formulation for the Hankel representation of .

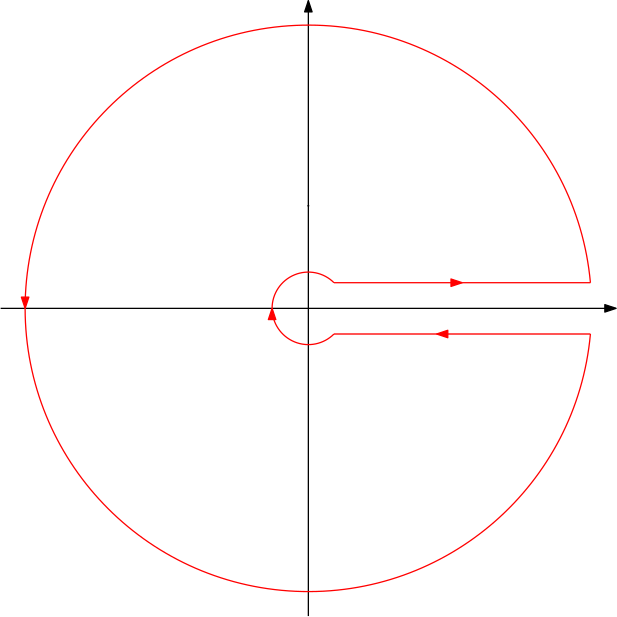

Lemma 2.8 (Functional equation of ).

Suppose posseses a meromorphic continuation to and denote the set of poles of not including . Suppose further that has the following decay condition : for all and for some monotone increasing sequence of radii as ,

where is the circle of radius minus a small (symmetric) arc of length around the positive real axis (cf. figure 3). Then,

Proof.

The proof relies on the use of the residue theorem by completing the Hankel contour into a Pac-Man (cf. figure 3), whose circular contribution is going to zero, due to the assumption of the lemma.

By the residue theorem, we then have

as desired. ∎

2.2 Connected components of superlevel sets of stochastic processes

Let us briefly recall the construction of a tree from a continuous function . For a more complete description of this, the reader is welcome to consult [19, 35].

Definition/Proposition 2.9 ([19]).

Let , the function

is a pseudo-distance on and the quotient metric space

with distance is a rooted -tree, whose root coincides with the image in of the point in at which achieves its infimum.

The tree has the particularity that its branches correspond to connected components of the superlevel sets of , as illustrated by figure 4. Let us now introduce the so-called -simplified or -trimmed tree of . This object is obtained by “giving a haircut” of length to . More precisely, if we define a function which to a point associates the distance from to the highest leaf above with respect to the filtration on induced by , then

Definition 2.10.

Let . An -trimming or -simplification of is the metric subspace of defined by

Notation 2.11.

Let us denote the number of leaves of .

2.3 A crashcourse in persistent homology

Throughout this section, we will detail and give the ideas behind persistent homology. A proper introduction to this is out of the scope of this paper, so we encourage the reader to consult the following classical references about this topic [24, 30, 12, 34]. This section aims nonetheless to give a brief introduction compiling the main results and intuition behind this field. To do so, it is convenient to break down the topic along its title. First, we will briefly recall what homology is and how it can be defined, and then we will explain the persistent aspect of persistent homology. It goes without saying that a reader familiar with these concepts may skip this section entirely.

2.3.1 Homology

In general, the motivation behind the introduction of objects in algebraic topology such as homology is to study topological spaces through algebra. That is, to attach an algebraic object (such as a module, a group, etc.) to a topological space, in such a way that, loosely speaking, this algebraic object remains invariant for any two homeomorphic topological spaces. Furthermore, we would like this invariant to behave well with respect to continuous maps. Namely, if we have a continuous map between two topological spaces , we would like to have an induced morphism at the level of the two invariants we attached to and . The most famous such invariant for topological spaces is the fundamental group first introduced by Poincaré. Some useful references for further reading are [24, 30].

In the terms of category theory, the above discussion is equivalent to saying that we use functors between the category of topological spaces, Top, and a category of algebraic objects, such as the category of groups, Grp, or that of modules over some ring , . In this sense, homology is nothing other than a functor . For our purposes, it is sufficient to consider the ring to be a field , so that we are really working over the category of vector spaces over this field . We will not detail the precise definitions of these objects, as we will not really need them, but a good reference as an introduction to category theory is given by Mac Lane in [27].

Recall that finding such a functor entails attaching a vector space to a topological space, in such a way that continuous maps between topological spaces induce linear maps at the level of vector spaces. To render this practical, let us first focus on triangulable spaces. Namely, spaces which are homeomorphic to a simplicial complex (a set of oriented simplices glued to one-another along edges, -faces or points). Given a simplicial complex , we can define a so-called chain complex, which is nothing other than a sequence of vector spaces, denoted , called the space of chains (the star denotes an index, which we call the degree), where is the free -vector space generated by the set of -faces in the simplicial complex. For the sake of notational simplicity, whenever the simplicial complex we are talking about and the field over which we are working on is clear, we may drop and and denote .

We can define a linear map called the boundary map, which is defined degree-by-degree as follows. The boundary map sends the generator of an -face (an element of ) to the (signed) sum of the generators of its boundary (which are elements of ), where the sign in front of each generator is determined by the compatibility of its orientation with the orientation of the -face. With this definition , which reflects the fact that the boundary of a boundary is always empty. So, we can see a chain complex as some graded vector space along with the map . Looking at the restriction of to each degree of , we can write as a chain of morphisms

with the property that . This property implies in particular that . We call the space of cycles, reflecting the fact that elements of tend to be “loops” or “cycles” of -chains. Homology quantifies exactly which cycles are not boundaries. More precisely, fixing a degree , we can define the th homology group over the field as

where denotes the restriction of to . In some sense, this gives a definition of what we mean by an -dimensional hole. All of this discussion is best illustrated by an example. In order to avoid sign problems, it is often practical to work over , so as to simplify calculations. In general, this is restrictive, but it is enough for our purposes and let us fix the simplicial complex of figure 5.

In this case, we see that and with all of the higher chains being . Furthermore, the boundary operator sends

with all other generators being sent to zero. From this, it is clear that , which represents the cycle which loops around the simplicial complex and . It follows that , so that we indeed detect a hole inside the complex. If we now fill that hole with a cell which fills the triangle (let us note it ), we now have , and its boundary , so that by filling this “hole”, we have effectively killed the . As for , it always quantifies the number of connected components, as (finite) simplicial complexes are connected if and only if they are path connected, so these paths constitute cycles which map any two elements of to each other. In particular, if we suppose that is path connected, then is always generated by all the sums of pairs of vertices in , so we get one generator of for every connected component.

At this point, given some triangulable space , the reader might be worried whether this definition depends on the triangulation we chose for , but it is a theorem that this is a well-defined invariant of topological spaces, cf. [24] for details. In fact, we have adopted a rather restrictive point of view throughout this discussion, as in reality we can make sense on how homology can be defined in more general settings [30].

2.3.2 Persistent homology

Now that we have roughly sketched out what homology is, let us introduce the idea behind persistent homology. Once again, we refer the reader to consult the following references if he or she desires a more detailed description of the theory [12, 34]. In this case, instead of dealing with a simple chain complex , we induce a filtration on this complex, which is typically done by giving a function on the underlying topological space . For example, if is a differentiable manifold and is a smooth function, then we can filter the complex by considering the subsets and considering . We call this filtration of the complex the superlevel filtration (an analogous definition can be given for sublevel filtrations). Of course, we may then compute the homology of for every , which gives us a family of vector spaces indexed by . However, by the functorial nature of , the fact that we have a (continuous) inclusion for every yields a linear map between the vector spaces .

These morphisms are of interest to us, as they tell us about how the homology changes as we vary the level . This motivates the study of the so-called persistent homology, which is nothing other than the family of vector spaces and the family of morphisms . This is more comfortably expressed in the language of category theory : persistent homology is a functor , where is seen as a small category (the objects are elements of and there is a morphism between if and only if ) defined by and .

If the function is nice enough, for instance and is compact, the persistent homology induced by the superlevel filtrations of can be decomposed into so-called interval modules. The latter are themselves functors defined as follows. Fixing a field and if is an interval of , then

The decomposition theorem states the following (cf. Oudot’s book [34] for a more complete description).

Theorem 2.12 (Decomposition theorem, Auslander, Ringel, Tachikawa, Gabriel, Azumaya).

Under some conditions for and , if denotes the persistent homology with values in , then it is isomorphic to a (possibly infinite) direct sum of interval modules. Moreover, this decomposition is unique up to isomorphism and permutation of the terms.

This theorem entails that if the filtration function and the space are nice enough, the persistent homology functor in fact decomposes as a direct sum of interval modules, more precisely, fixing a degree in homology we have

where the are intervals of . Notice then that this means that the information contained in the persistence module can be encoded by these intervals . This collection of intervals is what we call the barcode associated to a function , typically denoted . Another way of representing this information is by keeping track of the endpoints of the interval. In this way, we may represent the intervals as a collection of points in the half-plane

This collection of points is called the persistence diagram associated to , and is typically denoted .

This is not exactly the full story, as there are some technical caveats to this. Indeed, the theorem requires “nice enough” and . Throughout this paper we will be dealing with funtions (or in , up to a finite number of discontinuities), for which these spaces could be of infinite dimension. Crucially, however, if is compact and is , the rank of the maps is always finite. Under this condition, the decomposition theorem above applies so we may consider our modules to be decomposable (cf. [11, 34] for details).

Specializing all of this to amounts to talking about connected components of superlevel sets. In this sense, is exactly equal to the number of connected components of . The rank of corresponds to the number of connected components of which contain all of . The decomposition theorem can also be easily understood in this setting : bars in the barcode (or equivalently points in the persistence diagram) indicate when a connected component was “born” and when it gets absorbed by another one, with the rule that the “eldest” connected component is the one which always “survives”.

2.3.3 Persistent homology as a measure

There is one last point to be discussed, which will come in useful in section 2.7. That is, it can be useful to consider persistence diagrams as measures over the upper half-plane of . For q-tame modules, we can define such a measure as follows : if , then

This turns out to be a measure, once we have ironed out some details, as done in [12]. As an example, if the module is decomposable, then the persistence measure is nothing other than the sum of Dirac masses at every point of the persistence diagram. As we will see, considering persistent diagrams as measures has considerable advantages. The reason for this is because the space of measures is a linear space, so that we can operate on the space of diagrams with greater ease than in the algebraic context. This injection onto a linear space yields some desirable properties for persistence diagrams : for example, the ability to define Fréchet means [43], or a notion of mean and expectation. This suggests that this injection is crucial in simplifying the study of persistence diagrams in a probabilistic setting.

Furthermore, the fact that it is a space of measures allows us to use tools, such as optimal transport. In particular, there are natural notions of distances – so-called Wasserstein distances – which stem from this point of view. This approach has been explored in [17], to which we refer the reader for further details. The idea is to use the diagonal as a source of infinite mass, and study the optimal transport distances between diagrams (now seen as measures), where the distance on the base space (the upper-half plane) is the -distance on the plane, namely

Definition 2.13 (Wasserstein distances for diagrams).

If are two persistent measures (to which we have added the diagonal as a source of infinite mass), then the Wasserstein distance between two diagrams is given by

where denotes the set of all measures on whose marginals are and .

If we take the -norm, which is exactly the so-called bottleneck distance referred to in [34, 12], which we may define as follows, for any two persistent measures ,

An important result testifying of why persistent homology is interesting is that it is a stable construct in the following sense.

Theorem 2.14 (Stability theorem, [12]).

Let be a compact, triangulable metric space and let , then if we see and as persistence measures, then

Fixing a smaller functional space, it is possible to prove a stability theorem for as well.

Theorem 2.15 (Wasserstein stability, [42]).

Let be a compact, triangulable metric space of dimension and let denote the space of real valued -Lipschitz functions on . Then if , for every

where denotes the persistence measure associated to the persistent homology in degree of , .

2.4 Trees and barcodes

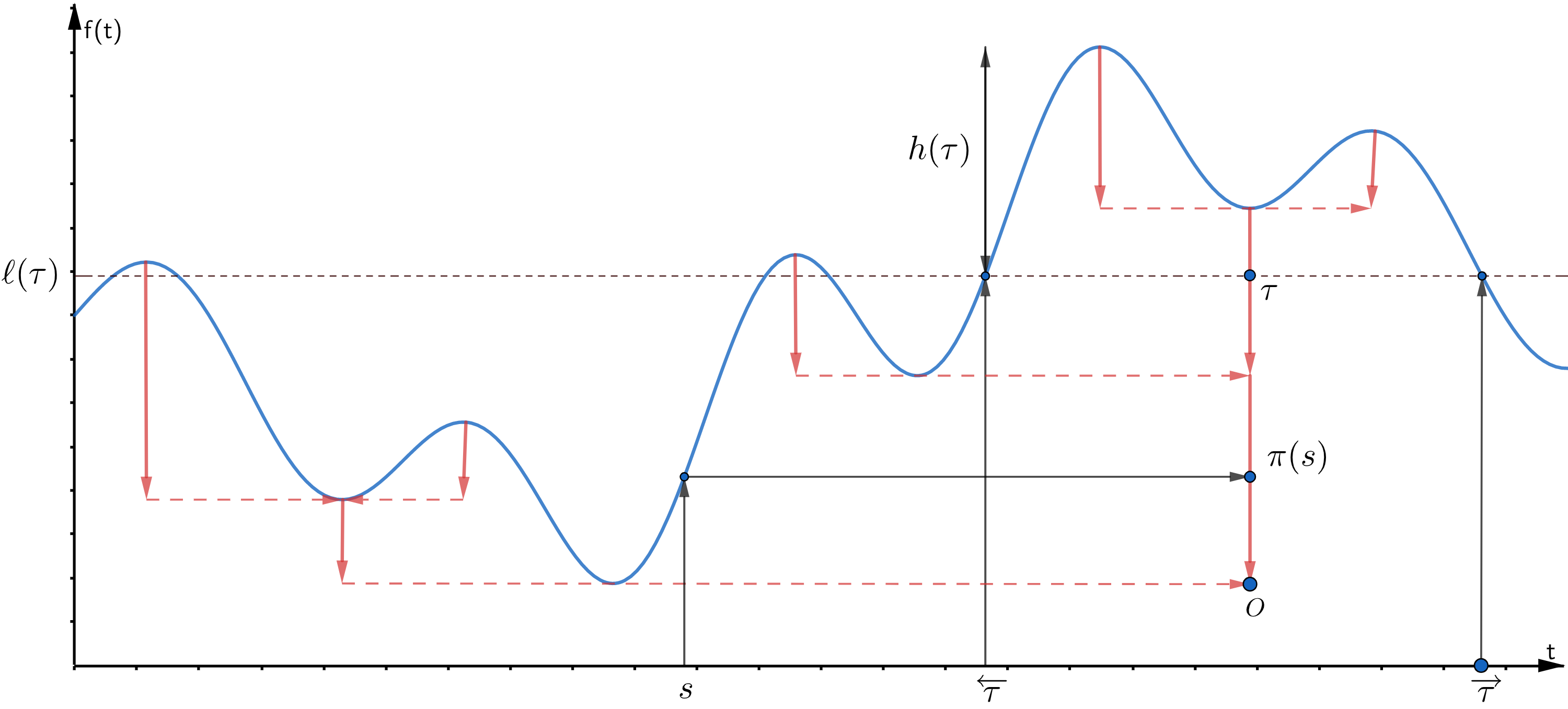

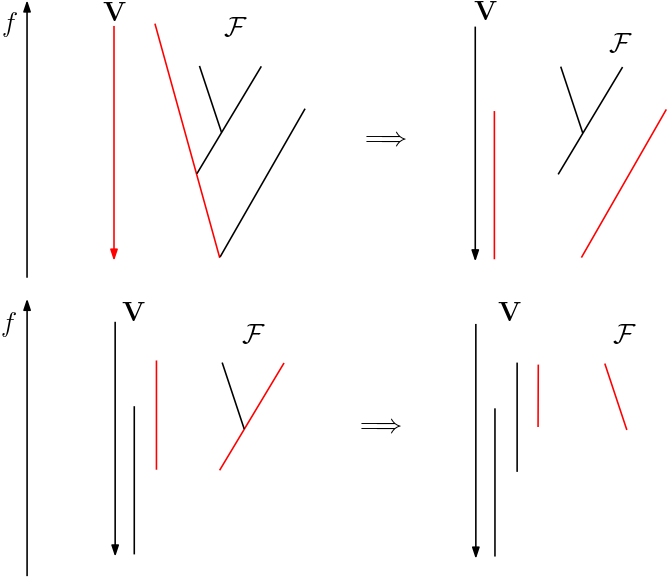

There is a correspondence between trees and barcodes described in full detail in [35]. Starting from , we can look at the longest branch (starting from the root) of . This branch corresponds to the longest bar of since branches of correspond to connected components of the superlevel sets of . Next, we erase this longest branch and, on the remaining (rooted) forest, look for the next longest branch. This will be the second longest bar of the barcode. Proceeding iteratively in this way, we retrieve . An illustration of this algorithm can be found in figure 6.

We can interpret geometrically as being equal to the number of leaves of . In terms of the barcode, the same counts the number of bars of length with the caveat that we count the infinite bar as having length equal to the range of . As we will see, reasoning in terms of trees has some major advantages, so in what will follow we will adopt the following convention

Convention 2.16.

The length of the infinite bar of will be set to .

2.5 Integration on trees and the duality between and

Let us recall the following simple remark made in [35]. On a tree , we can define a notion of integration by defining the unique atomless Borel measure which is characterized by the property that every geodesic segment on has measure equal to its length. Formally, we can express in two ways [37]

By using the second way of writing , the identity

is clear, as every sum in the second expression is finite for all and has terms. Of course, we could very well have written it using the first sum, but this poses the difficulty that if is infinite, so is the sum considered in this formal expression for at least some value of . However, the restricted sum

is finite for all and there are exactly terms in this sum. We thus obtain an alternative expression for

We deduce that more information is contained in than in (and by extension than in ). The calculation above provides the connection between Chazal and Divol and Baryshnikov’s functional and the functional detailed in this paper , since is nothing other than the derivative of .

The study of is in fact completely equivalent to the study of . Indeed,

where associating to the distance between and the highest leaf (with respect to the filtration of ) above in . We immediately recognize the above integral as being the Mellin transform of . Allowing for complex , this integral relation can be inverted by virtue of the Mellin inversion theorem, provided that the fundamental strip of is not empty. For compact intervals and continuous functions , this fundamental strip is never empty (provided ) and in fact is exactly equal to . Thus, for any real number ,

which estabilished the duality relation desired. Notice also that is a norm in the sense that

For any (deterministic) continuous function , is nothing other than a sum of the bars of the barcode to the power . An in depth explanation of this is provided in [35, §2.2], but let us briefly give some intuition for this. By the algorithm depicted in figure 6, if we denote any of the bars of the barcode, seen as embedded in the tree the length of the branch, , can be written as

The bars of the barcode partition the tree , so that the integration present in the definition of is nothing other than the sum of the ’s.

Remark 2.17.

This definition of coincides perfectly with a definition of typically used in persistent homology [15, 31, 43, 17, 10], as long as we consider that the infinite bar has the length of the range (i.e. the ) of the function . Of course, within this framework an equally valid definition for would have been to exclude the infinite bar from being counted all-together, and to consider only the bars of finite length. This approach turns out to give the correct definition for the -functional in the definition of tail -functions (cf. definition 3.24), which is necessary to study Lévy -stable processes for .

Additionally, by the usual inequalities of -spaces,

Proposition 2.18.

is almost -convex, i.e. let and and set , then,

Proof.

The statement follows directly from an application of Lyapunov’s inequality for -spaces. ∎

More generally, it is always true that one can express the -norm of a function as the Mellin transform of the repartition function of , .

2.5.1 Calculation of in dimension one

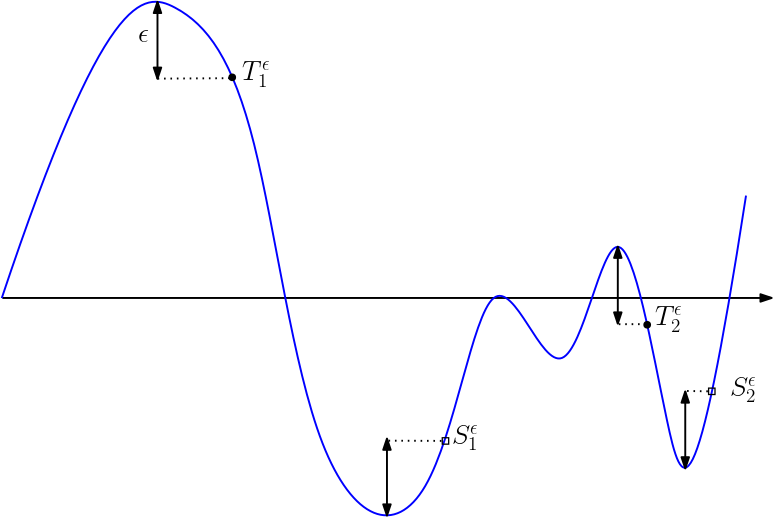

In dimension one, it is possible to use the total order of and count by counting the number of times we go up by at least from a local minimum and down by at least from a local maximum. This idea can be formalized by the following sequence, originally introduced by Neveu et al. [32].

Definition 2.19.

Setting , we define a sequence of times recursively

Counting the number of bars of length is thus exactly to count the number of up and downs we make. More precisely

| (2.1) |

by which we mean that it is the smallest such that the set over which or are defined as infima is empty.

Notation 2.20.

We denote the range of . Symbolically,

Moreoever, denote the number of the process restricted to the interval .

Intuitively, this calculation process hints at the fact that if is small, the number of bars should strongly depend on the regularity of the process, as ultimately counts the number of “oscillations” of size . In a very precise sense, regularity almost fully determines the asymptotics of in the regime. This intuition is corroborated by the following theorem.

Theorem 2.21 (Picard, §3[37] and [35]).

Given a continuous function ,

where denotes the upper-box dimension, ,

For the rest of this paper it is exactly the functional which shall occupy us.

Remark 2.22.

The functional is stable under perturbations of . However, it is unknown whether a similar stability result exists for .

2.6 -functions associated to stochastic processes

Definition 2.23.

Let be a stochastic process on some compact topological space . Its -function is defined by:

for .

This is reminiscent of the structure of the -function, but a priori not enough to draw any parallels. However, it turns out that this nomenclature turns out to have a meaning for stochastic processes. Similarly, we could consider the functional of , which denotes the forest

Remark 2.24.

In the tree setting the number is also the number of branches of length in the forest .

Following this analogy, it is natural to define

Definition 2.25.

The local -function associated to at , is defined as

Proposition 2.26.

The two -functions we have so far defined are related via the following formula

Proof.

Let us start by noticing that is nothing other than

where this derivative is defined and locally constant almost everywhere. From this and the fact that the derivative is also defined and locally constant almost everywhere and

Applying the Mellin transform to both sides and applying Tonelli’s theorem,

From the derivation functional property of the Mellin transform (cf. table 1) we get

Applying the expectation to both sides, multiplying times and applying Tonelli’s theorem once again, we have the desired result, namely,

∎

Remark 2.27.

If the process starts at , it is in general easy to compute for , but more challenging to do so for . In what will follow, we will always focus on .

Notation 2.28.

For the rest of this paper we will take the following conventions. First, we will sometimes omit the subscript of whenever convenient. The Laplace transform is always taken with respect to the variable and its conjugate variable will always be . Similarly, Mellin transforms will always be taken with respect to the variable and its conjugate variable will be .

Lemma 2.29.

Let such that the functions and are monotone in their arguments. Then, denoting the Laplace transform with respect to ,

Proof.

The monotonicity of in its arguments ensures that is a measurable, positive function. The statement holds by virtue of Tonnelli’s theorem. ∎

Remark 2.30.

Notice this last lemma is applicable to , , and other such quantities.

2.7 Average diagrams and characterizations of Wasserstein convergence of diagrams

Notation 2.31.

For the rest of this section, denote

which we equip with the metric -metric on recalled in equation 2.3.3. Let and denote an open tubular neighbourhood of radius around inside and denote its complement in by . Finally, denote

By looking at persistence diagrams of functions as measures (cf. section 2.3.3 for details), it is possible to define a notion of an average diagram of a stochastic process.

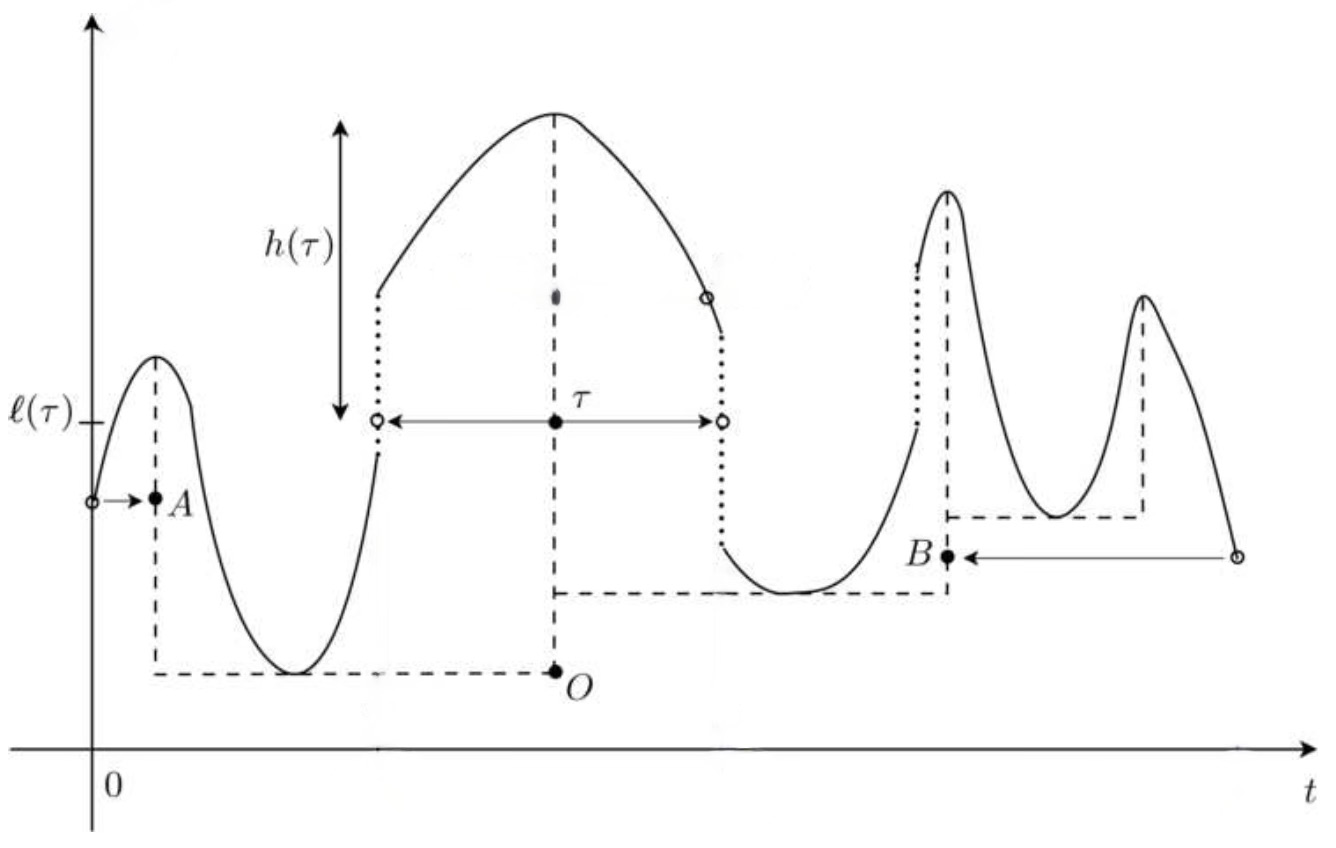

Definition 2.32.

Let be a compact, triangulable metric space, be a Polish metric space of (q-tame) functions on and let denote the space of measures on the upper half-plane . Let be the map taking , where is seen as a measure, and let be a stochastic process of law on . Then, the average diagram of is given by

Remark 2.33.

Note that is itself a measure. Whenever this measure is absolutely continuous with respect to the Lebesgue measure on , there exists such that for any test function

A sufficient condition to ensure the existence of is that exists (this is equivalent to requiring the existence of ). Instead of using birth-death coordinates, we may also express this density in terms of birth-persistence coordinates. In these coordinates, we will denote this density function by , somewhat abusing the notation.

Definition 2.34.

This allows us to define a -function for as follows.

Definition 2.35.

Let and suppose that for some

then define the -function associated to by

Remark 2.36.

A priori, is defined on the strip . This could have also been guaranteed by replacing the condition of decay of by requiring that .

As before, we may also define a local -function.

Definition 2.37.

The local -function associated to at is defined as

Remark 2.38.

These definitions are compatible with the notions of -functions defined for a stochastic process. Seeing as a measure on , (and the same holds for local -functions).

A characterization of the topology metrized by the distance is useful and has been investigated by Divol and Lacombe in [17]. The reader familiar with optimal transport will recognize this as an adaptation of the known characterization for probability measures of Wasserstein topology by vague convergence and convergence of th-moments. That this equivalence holds for measures of a priori infinite mass is, however, a non-trivial extension.

Lemma 2.39 (Characterization of the topology metrized by , [17]).

Let and . Then, the following equivalence holds

Remark 2.40.

Of course, given our choice of notation, if , we can rewrite as .

Furthermore, it is possible to show that

Proposition 2.41 (Interpolation for optimal transport).

Let and . Define by

Then, for

Consequently, if , then .

Remark 2.42.

For probability measures, Wasserstein interpolation follows trivially from an application of Jensen’s inequality. However, since diagrams are a priori of infinite mass, this interpolation result needs to be shown.

Proof.

Let be an optimal transport for . Applying Littlewood’s inequality,

where this equality holds everywhere on the support of . This can be shown by defining

This set either has null or positive measure. If it has positive measure, then we can modify the transport plan by sending the projections of to the diagonal, thereby producing a transport plan of strictly inferior cost to that of , which is a contradiction. Hence, is of null measure, so the equality holds over the support of the measure. Finally, this entails

If , since is an optimal transport between and and , itself must have compact support and the diameter of the support is bounded above by , so the inequality of the proposition follows. ∎

Lemma 2.43 (Sequential continuity of the inverse Mellin transform).

Let be a sequence of functions uniformly bounded by a function , whose Mellin transform is defined over some non-empty strip . Suppose further that there is a function such that and uniformly on every compact set of . Then, almost everywhere.

Proof.

For every , and so the sequence is bounded in a weighted space. Up to extraction of a subsequence, converges a.e. to some function , also bounded above by . By dominated convergence, along this subsequence, , which entails that a.e. since the Mellin transform is injective and identically on , since along any subsequence uniformly on every compact set of . It follows that the sequence has as its only accumulation point, finishing the proof. ∎

Remark 2.44.

It is sufficient to consider that for all , the sequence is absolutely uniformly integrable.

Both of these lemmas allow for a comprehensive characterization of the objects we have thus far been concerned with throughout this paper.

Theorem 2.45 ( characterization of Wasserstein -convergence).

Let be a sequence of q-tame measures and and suppose that the sequence can be uniformly bounded above by a function such that for as and on , as . Then, the following are equivalent:

-

1.

There exists such that .

-

2.

There exists such that and .

-

3.

For almost every and , and .

-

4.

For almost every , and uniformly on every compact of .

-

5.

For all , .

Proof.

Let us break down the proof in different steps.

-

•

by lemma 2.39.

-

•

. By the Portmanteau theorem, the vague convergence of to entails that for any continuity set of , . In particular, since the and are q-tame, is a continuity set of for almost every and , so and a.e..

-

•

. Since a.e., if we let , then

The domination conditions of the theorem on and guarantee that this quantity is integrable as soon as . By dominated convergence, on every compact of . We apply the same reasoning to the by noting that the measure of is always dominated by that of .

-

•

. Fix and take a compact set around contained in . It suffices thus to show that the convergence of these -functions entails vague convergence of the , which will show the result by lemma 2.39. Denoting , the boundedness condition of the theorem on entails that, by lemma 2.43, almost everywhere. Since the collection of and together forms a -system, so for every continuity set of , we have convergence of their measures to , and so by applying the Portmanteau theorem once again, vaguely, which shows the result.

-

•

trivially.

∎

Remark 2.46.

Of course, by interpolation, it is sufficient that for all and , be bounded to guarantee that for any , , if .

Remark 2.47.

Theorem 2.45 applies to average diagrams from any stochastic process satisfying the hypotheses of the theorem. This entails that if the -functions of a process converge on some open set , the underlying expected diagrams themselves converge in some Wasserstein distance.

3 -functions of Lévy processes and semimartingales

3.1 Semimartingales

A first important motivating result regarding -functions is the following.

Proposition 3.1.

Let be a continuous semimartingale on the interval such that for

Then, the (local) -function of is meromorphic on (resp. ) with a single simple pole at (resp. ). Furthermore, if is a continuous semimartingale (and some conditions) and , then in

Remark 3.2.

By quadratic variation, we mean the quadratic variation in the probabilistic sense, i.e. in the sense that we take the limit of the variation of the process as the mesh of the partition of the interval goes to zero, as opposed to the real quadratic variation, where the supremum over all partitions is considered.

Proof.

The statement holds by the almost sure existence of continuous modifications of local times for continuous semimartingales and the fact that uniformly in and , it is known [41, Ch. VI Thm. 1.10] that under the technical hypothesis of the theorem,

Recall the density occupation formula for the local times of a continuous semimartinglale [28, Cor. 9.7], which states that, almost surely, for every and any non-negative measurable function on

Taking to be the constant function , we get that in

But for small enough, by monotonicity of ,

so that in for every small enough,

Since can be taken to be arbitrarily small

in as desired. ∎

Remark 3.3.

If the continuous semimartingale is Brownian motion, the same arguments as well as a result regarding the representation by downcrossings of the local time by Itô [25, §2.4] show that this asymptotic relation holds in fact almost surely.

Corollary 3.4.

If is a continuous semimartingale, then in expectation admits a pole of order at of residue .

In [36], we have already studied the functional for Markov processes. Let us briefly recall some useful known facts about .

Proposition 3.5 (P, [36]).

Proof of proposition 3.5.

The only thing to prove is the result of equation 3.3, as the previous statements are all proved in [36]. Since we are dealing with processes which are not periodic in the sense of [36], then

since as soon as the hitting time is attained we have at least bars (due to the boundary of the interval). Using standard functional properties of the Laplace transform it is easy to see that

where denotes the probability density function of . However, the Laplace transform of this density function is nothing other than the moment generating function , since is a positive random variable. ∎

Remark 3.6.

If the process has the strong Markov property, we can write as the product of the Laplace transform of the distribution of its increments

The expression of is particularly simple as soon as these increments are independent and identically distributed.

Remark 3.7.

Ordering the bars of the barcode of a function by their length, and denoting the length of the th longest branch by , the following equivalence holds

The probability distribution of both of the events above are thus the same. Consequently, there is a one-to-one correspondence between the elements of the sums

whenever these quantities are defined. In particular, the distribution of each bar is in principle readily available, since is the Mellin transform of the distribution of . We will later see that in particular cases, we can gain access to the explicit distribution of bars in this way (cf. section 3.3.2).

3.2 Renewal theory

Throughout this section, we shall consider that the stopping times are such that the sequence is a sequence of i.i.d. atomless random variables, where

We shall adapt and enounce some theorems from renewal theory (cf. Allan Gut’s book [23] for a detailed account of this) Let us define by

Tautologically, for every , . In fact, adopting the convention that the infinite bar has length the range of the process, we can write, always under convention 2.16 that

Remark 3.8.

Notice that convention 2.16 for the infinite bar might not be the most natural or more convenient from this point of view. Indeed, if we had adopted the convention that the infinite bar always has length at least , then

and is a first passage time process defined by

Nonetheless, as previously stated, we will keep adopting convention 2.16 for the rest of this paper.

According to renewal theory, posses various desirable limit theorems which we shall briefly recall and refer the reader to [23] for complete proofs of the latter.

Theorem 3.9 (Strong Law of Counting Processes, Theorem 5.1 [23]).

Let , then

for all . If , then the limits are .

Theorem 3.10 (CLT for Counting Processes, Theorem 5.2 [23]).

Let and , then

Furthermore,

These results are in particular applicable for Lévy processes, where it is possible to show that the requirement that the sequence is i.i.d. is satisfied. In particular, the theorems above give the asymptotic long-time behaviour of the number of bars.

3.3 Lévy processes

For Lévy processes, the small scale asymptotics of can also be studied up to the following caveat : a wide range of Lévy processes have almost surely discontinuous paths (but nonetheless càdlàg), but our construction of trees (as done in [35]) is based on continuous functions. For this reason, it is necessary to define what tree we associate to a process when has almost surely discontinuous paths. Luckily, this caveat has been treated for càdlàg processes in [19, 37]. We will adopt the approach taken by Picard in [37], where the reader can find the details of the construction. Loosely speaking, Picard’s approach consists in “completing” the function at the discontinuity points by joining an imaginary line linking the points of discontinuity (cf. figure 8).

In any case, it has been shown that on some fixed interval , it is possible to obtain the behaviour of the number of bars of length as .

Proposition 3.11 (Picard, §3 [37]).

Let be a Lévy process and suppose that, almost surely has no interval on which it is monotone. Define

for

then as in probability. If for some , then the convergence is almost sure.

Remark 3.12.

The hypothesis on is satisfied if or is not the sum of a subordinator and a compound Poisson process, in which case is finite, so is bounded. Furthermore, the convergence is always almost sure for -stable processes for which is not a subordinator by the scaling property. In fact, in that case there exists a constant such that almost surely,

If we can quantify correction terms to this asymptotic relation in , this gives rise to a statistical test for by using the stability results discussed in [36], we will explore this in more detail in section 3.3.3. By the self-similarity of -stable process following the arguments of [37, §3], we can already at least conclude that

Notation 3.13.

In what will follow, we will denote by and two independent random variables distributed as the analogously denoted ones in proposition 3.11. Furthermore, define . In particular, if , abusing the notation we will denote .

Remark 3.14.

Henceforth, unless otherwise specified, we will always assume that almost surely has no interval on which it is monotone.

This result by Picard is exactly the Strong Law of Counting Processes (theorem 3.9) applied to the stopping times we previously considered. Self-similarity allows us to trade the limit by an limit. However, Picard’s result is more general that what could’ve been deduced with self-similarity, as it applies to Lévy processes which are not necessarily -stable. In this setting, one could ask whether it is possible to prove an analogous theorem to the CLT of Counting Processes (theorem 3.10).

Theorem 3.15.

Let be a Lévy process such that almost surely has no interval on which it is monotone, using the notation defined in 3.13,

for any , where denotes the radius of convergence of the Taylor series of around , which can be bounded below by , which is larger than for small enough. Furthermore, if is -stable, the formula above becomes

| (3.4) |

Let us stress that the main addition over the CLT of Counting Processes (theorem 3.10) is two-fold :

-

•

We have found a similar limit for a processes which is not self-similar, and so for which the limit was a priori not interchangeable with the limit.

-

•

We have further specified the rate of decay of the remainder in terms of , and this will turn out to be of importance;

To show the theorem, it is convenient to show first some technical lemmata, one of which is a slight refinement to a technical lemma proved in [37].

Lemma 3.16 (Picard, Proposition 3.14 [37]).

The variables and admit finite moments of order for all and the moment generating function is well defined on a neighborhood of zero. Furthermore, the radius of convergence of around , , then

if is -stable, then , for some constant (which might be infinite). Finally, there exists such that

Remark 3.17.

The bound on the constant in this lemma is not optimal. Notice also that this result entails as .

Lemma 3.18.

Lemma 3.19.

For every , there exists a constant such that

Furthermore, for real and ,

In particular,

Lemma 3.20.

For any , weakly in , for any

at a rate for any . Furthermore, for any

weakly at a rate and the convergence is strong as soon as .

Proof of lemma 3.16.

It is sufficient to show it for knowing that an analogous treatment is possible for . The points in are characterized by the fact that

In particular, the supremum over all ranging within of this quantity is also less than .

Consider now an interval , where and is an integer and let us slice this interval into segments of length . It is clear that the following inequality holds

since over each smaller interval we can have only smaller spread than over the entire interval. However, the right hand side is a supremum over i.i.d. random variables, so that

By the non-monotonicity of , . In particular, if we let , and denote , then:

as soon as . It follows that is well-defined for in some neighbourhood of zero and in particular all moments of are well-defined and finite. Finally, combining the above remark with an application of Markov’s inequality we get

Almost surely, , where is a geometric random variable. The moments of can easily be calculated, yielding the estimation in the lemma for the moments..

This shows that the radius of convergence of the Taylor series is bounded below by , since Taylor series converge up to their nearest singularity. If is -stable, we can use the relation which tells us that, in distribution , so that by the ratio test,

This limit is equal to , since is analytic on a non-trivial disk around , by lemma 3.16 and usual properties of the Laplace transform.

whenever , which shows the desired result.

∎

Proof of lemma 3.18.

The statement in follows from the following observation.

by the arguments of lemma 3.16. This sum converges, since . As , , since is almost surely nowhere monotone, so that the entire sum tends to . The almost sure statement follows from the fact that is monotone, since both and are monotone functions of . Since convergence implies almost sure convergence along a subsequence , for by monotonicity of

so the convergence is almost sure. ∎

Proof of lemma 3.19.

The first inequality of the lemma relies on the fact that

since . Notice an analogous inequality holds for . By Markov’s inequality, we know that

from which the first inequality follows by lemma 3.18. The second and third inequalities follow from noticing that for any and

and applying Jensen’s inequality. ∎

Proof of lemma 3.20.

Consider a test function , then integrating by parts

| (3.5) |

By performing the change of variables , we see that the integral is weakly approaching , as is not supported at . Additionally, away from , the function

is a compactly supported -function, integrating by parts subsequent times equation 3.5 yields bounds of this integral by , where is a constant which depends on the test function and its support.

Let us now show that

Once again integrating by parts,

Applying the residue theorem to evaluate the complex integral we get, for ,

where is the circle of center and radius . By the estimation lemma, the contribution of this integral is bounded by . It follows that

thereby giving the speed of convergence desired. ∎

Proof of theorem 3.15.

Throughout this proof, we shall denote

The assumption of non-monotonicity of the Lévy process ensures that, almost surely, and both tend to as . Consider now the times and given in definition 3.36. Since is Lévy, and are independent from one another, and are both equal in distribution to and respectively.

By lemma 3.16, and admit finite moments for all and the function is well defined, so, by equation 3.3

| (3.6) |

If we denote the radius of convergence of the Taylor series at zero associated to , for ,

This radius of convergence can be bounded below with the results of lemma 3.16 by

which entails that as . We deduce from this series the Laurent series associated to , namely

where the remainder in is an analytic function of for . By the inequalities of lemma 3.19, the function doesn’t admit any poles on the half plane , so that the Taylor series above converges over the same disk as that of .

Observe now that for some small , the inverse Laplace transform of can be written as

| (3.7) |

Weakly, the integrals going off to infinity are of order for any , since for any test function , integrating by parts

But using lemma 3.19,

which entails that the integrals going to infinity in equation 3.7 converge weakly to at a rate for any . Thus, asymptotically as , for ,

for any . If the process is -stable, then in distribution for all , so that in distribution and

for all . As , for any , since

for any by Markov’s inequality. ∎

Remark 3.21.

A similar theorem can be proven in for -stable processes. For instance, if is -stable and one obtains that for every ,

Interestingly, there is a constant term appearing in this expansion, which can be understood as induced by the boundary. This interpretation comes from Picard’s analysis of the problem [37], in which the first term of this asymptotic series was also derived (cf. proposition 3.11).

If has almost surely discontinuous paths, exhibits macroscopic jumps. These will turn out to bring significative contributions, so much so that

Corollary 3.22.

If , the -function of any -stable Lévy process is ill-defined for any .

Proof.

The -function of a stochastic process can be written as

| (3.8) |

if is -stable, the first term can be written as

where we have momentarily taken . Since has a Lévy -stable distribution, taking now complex, is infinite as soon as , since does not admit any moments of order (of real part) larger than . Applying theorem 3.15, we know that the second term in the above decomposition of is only defined for , so the fundamental strip of is empty. ∎

In fact, it is possible to show that as . It turns out that the distribution of is dominated by the probability of having one large jump, which confirms our previous statement on the effect of the discontinuity of Lévy processes on the distribution of . This is the so-called single big jump principle.

Proposition 3.23 (Single big jump principle, Bertoin, [5]).

If is an -stable process (), there exists a constant such that

Loosely speaking, it is intuitive to think that a corrective asymptotic power series for of the form

should exist for the following reason. By the single big jump principle, the probability that the range exceeds for large is dominated by the probability of a single big jump. However, it is also possible to have large jumps of size where . The probability of each of these jumps happening is of order and by independence, the probability that jumps of size happen is . In general, we cannot expect these events to be disjoint from one another, so the coefficients of this sum may be negative. Finally, by the scaling invariance it is sufficient to show that this is so for . Corrective terms to the above asymptotic relation should thus in principle exist, but the explicit calculation of these terms is out of the scope of this paper.

By contrast, we will now show that is well-behaved. This motivates the following definition

Definition 3.24.

The tail -function of the stochastic process on is defined as

Theorem 3.25.

The tail -function associated to an -stable Lévy process is given by

| (3.9) |

which extends to a meromorphic function of to the entire complex plane (since is itself meromorphic), with a unique simple pole at of residue .

Proof of theorem 3.25.

To show that this quantity is well-defined, let us start by noticing that

which for goes to zero (uniformly in ) exponentially fast as , showing that does as well for by an application of Markov’s inequality. We can also compute the contribution of the second term of equation 3.8. First, notice that

Using the scaling property of the Mellin transform and inverting the Laplace transform

| (3.10) |

Finally, setting

the polynomial scaling property of the Mellin transform, yields the final result. ∎

Remark 3.26.

Alternate proof of theorem 3.15.

By lemma 3.16 and the analyticity of the expresion of with respect to , admits a Laurent series on some non-trivial annulus around zero with a single simple pole at . By the fundamental correspondence (theorem 2.5), the existence of this Laurent expansion guarantees that admits a meromorphic continuation to the whole complex plane with only simple poles at every for every and at . The poles at the negative integer multiples of are compensated exactly by those of the -function in the denominator of the expression of , leaving only a pole at . Now, recalling that

has a supplementary pole at . Admitting that has the decay condition to apply the fundamental correspondence by inverting the Mellin transform we get the asymptotic relation desired. ∎

3.3.1 Exponential corrections

The fundamental correspondence is limited in that it allows us only to describe asymptotically up to terms smaller than any polynomial. However, in accordance to the discussion of section 2.1.1, a finer study of the analytic properties of can yield the superpolynomial corrections to our estimate, assuming that admits a meromorphic extension to the whole complex plane. Using lemmata 2.6 and 2.8,

| (3.11) | |||

| (3.12) |

Recognizing that

we may formally invert the Mellin transform if all the ’s are simple poles to obtain the exponentially small corrections

Generally, the poles are not simple so the corrective terms to this series stem from residues of higher order poles (the corrections remain nonetheless superpolynomially small as ).

3.3.2 Distribution of the length of branches

The distribution of the length of the th branch (in the sense of figure 6) can be calculated. Recall that

For ,

If we suppose once again that is a Lévy -stable process, this can be simplified to yield

Taking the Mellin transform of a power is in general difficult. Inversion is also in general complicated due to the presence of the -function in the denominator of the above expression. To remediate the first problem, we can form the generating function yielding the distribution for the th bar,

which allows us to express

Proposition 3.27.

For , the distribution of the length of the th longest branch is characterized by its Mellin transform which is given by

Whenever convenient, the expression above can also be evaluated by considering a circular contour of small enough radius around the origin and evaluating

3.3.3 Statistical parameter testing for -stable processes and perspectives

What we will aim to do in this section is to illustrate by example why barcodes can be a robust statistical tools for parameter testing. Parameter testing is a widely studied subject, notably for self-similar processes, where the problem has been treated in dimension (a non-comprehensive list of references is [16] and the references therein). A variety of different methods, such as multi-scale wavelet analysis, have been used to produce these results (although other methods such as the ones of [16] have also been used), so our approach does not offer anything new in this respect. The interest of our method lies in possible applications to higher dimensional random fields, for which wavelet analysis is not an effective tool. A complete theoretical framework for this would require the study of the trees of higher dimensional random fields, which are out of the scope of this paper : instead, this section acts as a proof of concept for the use of topological estimators and their utility, by studying what happens in dimension 1.

In what follows, we will consider to be an -stable Lévy process, of which we will aim to estimate the parameter . From proposition 3.11 we know that almost surely

In particular, given some sample we may compute the sampled value of , which we will denote explicitly. A close inspection of the behaviour of the sample mean should thus yield an estimation for the parameter of the process .

Remark 3.28.

More precisely, given a sample, our test consists in performing the following steps.

-

1.

Sample paths of the stochastic process (for example at regular intervals of size for some ) ;

-

2.

Compute the barcode of the sampled paths. To do this, first construct a filtered simplicial complex (which is in this case nothing other than a chain with links) by taking each point to be a vertex of a complex and joining adjacent sampling points with an edge. The filtration on this complex is the value of the process at the edge (for an edge connecting vertex to vertex , the value of the filtration is ). Finally, the persistent homology of this complex can be computed with the gudhi package [1], which incidentally also offers a convenient implementation of filtered simplicial complexes due to Boissonnat and Maria [7].

-

3.

For some range of small enough , and for some positive constant compute the quantity

Here, the notion of some range of small enough and the constant both depend on , with the limiting condition that as , the lower bound on the range of valid goes to zero.

Our claim is that the computed quantity is a valid estimation of the parameter (for fBM, the quantity obtained in this way is an estimate of ).

Lemma 3.29 (Convergence of the sample means).

The quotient

at a rate , for every where is a constant depending on and the th moment of . In particular,

at the same rate, where is a superpolynomially small function of .

Remark 3.30.

The at first seemingly convoluted expression for the estimator can be explained due to the results of theorem 3.15. The substraction present in the numerator and denominator is performed so that the constant terms of equation 3.4 vanish. Ignoring the superpolynomial contributions to this expression which remain small, we then have that the argument inside the of the estimator is roughly

With this in mind, let us now formally prove the statement of lemma 3.29.

Proof.

That the numerator and the denominator tend to the respective expected values holds by a simple application of the weak law of large numbers, since is a random variable in for . The rate of convergence of this limit can be obtained via a simple application of Markov’s inequality, by noting first that the summands in the denominator tend to their limits faster than those of the numerator, as the latter’s th moments are always larger than the former’s. From theorem 3.15, we see that the limit can be expressed as

where is a function tending to superpolynomially fast as , determined by the superpolynomial corrections to the results of theorem 3.15. The statement of the lemma ensues. ∎

Lemma 3.31 (Probable -distance of sampling).

Denote the trajectory samples of the -stable process at every interval of length . More precisely, somewhat abusing the notation we can write,

There exists a constant such that

Remark 3.32.

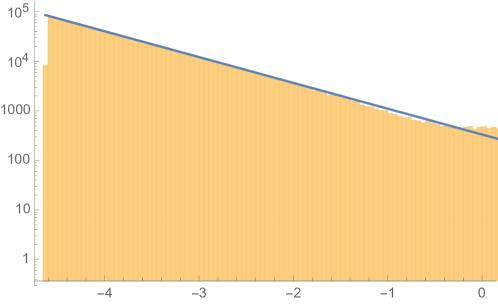

The asymptotic dependence above fixes admissible values of as a function of as holding whenever the asymptotic dependence above is valid (it must be valid between and ). Furthermore, the parameter we chose above is also further constrained by the requirement that the asymptotic relation of theorem 3.15 holds between and . More precisely, we fix and such that the superpolynomial contributions in the expansion of theorem 3.15 are negligible with respect to the term in and by imposing that is large enough so that the asymptotic relation of lemma 3.31 simultaneously holds within the range . In practice, we may fix and by looking at a log-log chart of , the regime of validity of and the value of become clear, as shown in figure 9.

Remark 3.33.

With respect to the barcode, linear interpolation between values of or the consideration of the process is equivalent.

Remark 3.34.

It is not a priori obvious that the event above is measurable. However, continuity in probability and the a.s. existence of a càdlàg modification of the process allows us to interpret this event to be a supremum over every , rendering the event measurable.

Proof.

It suffices to show the result over the interval . Noticing that the sampling coincides with the value of the path at every , it suffices to evaluate the probability that over intervals of length the real sampled path (notice the absence of a hat) strays away from the sampled path . Focusing on a single interval , the single big jump principle 3.23 states that there exists a constant such that this probability of straying away in this interval is

By independence, over such intervals

as desired. ∎

Now, let us recall the following theorem.

Theorem 3.35 (P, Theorem 3.1 [36]).

Let , then there exists a -matching between the barcodes of and . In particular, for any

Moreover, if is continuous with respect to , then

which at fixed quantitatively translates to

where is the modulus of continuity of on the interval . Finally, the following inequalities also hold

This statement can be specialized given our two lemmas above. The theorem provides bounds on provided that we know the value of , since if is small enough, has some almost sure asymptotic behaviour. On the other hand, by virtue of lemma 3.31 we have a probable estimate of , i.e. with probability , we may give a bound of , rendering the statement quantitative. The second part of the statement of theorem 3.35 provides bounds on the distance between and , provided that we know that is continuous. This happens to be the case for Brownian motion, as shown in [36]. Showing it in full generality for Lévy processes requires a closer study of the range of Lévy processes and the continuity of the inverse Mellin transform of . However, for the purposes of the construction of our statistical test, lemma 3.29 suffices, as it provides us with a quantitative guarantee that the parameter is well estimated by our estimator .

3.4 Propagators and local -functions

In dimension one, it is possible to use the total order of and count by counting the number of times we go up from to . This idea can be formalized by the following sequence of stopping times already introduced in the literature of classical probability theory (cf. for instance [41]).

Definition 3.36.

Setting , we define a sequence of times recursively

| (3.13) |

Counting the number of bars of length is thus exactly to count the number of up and downs we make. More precisely,

| (3.14) |

by which we mean that it is the smallest such that the set over which or are defined as infima is empty.

With the aforementioned, it is possible to define a Feynman-like formalism to perform the computation of .

Definition 3.37.

Let be a (strong Markov) stochastic process and let

be the hitting time of by . We define the propagator from to by

whenever this exists.

Remark 3.38.

Whenever convenient, we may take , and modify the subsequent expressions appropriately.

If the process has the strong Markov property and the increments between the stopping times and are identically distributed, we can once again apply renewal theory. In particular, the Laplace transform of the occupation numbers can be understood in terms of the propagators above. For ,

Similarly, all moments of the distribution can in principle be calculated

where denotes the polylogarithm.

Remark 3.39.

If in distribution, we can rewrite the above as,

If and admit an asymptotic expansion for small (alternatively, we can suppose that this function is a smooth enough function of ), then the Mellin transform of the expression above admits a meromorphic continuation. Furthermore,

so that the order of the divergence of is dictated exclusively by the order of the first correction in to the product above. In reality,

Corollary 3.40.

Suppose that the increments in the sequence of stopping times defined by are i.i.d. and that and have asymptotic expansions of the form of that of the fundamental correspondence (cf. theorem 2.5), then, the function has a meromorphic extension on the half plane for any .

Proof.

It’s a simple application of the fundamental correspondence. ∎

3.4.1 Itô diffusions

Computing the local -functions is sometimes easier than computing the -function associated with the process . This is because the computation of the distribution of might not always be straightforward. An example of this is the case of Itô diffusions, i.e. solutions to stochastic differential equations of the form

for some smooth functions and . These processes have the strong Markov property and the sequence of stopping times defined above are identically distributed as and do not depend explicitly on time. Furthermore, these processes have infinitesimal generator

We can use the theory of diffusion developped by Itô and McKean [25] to find explicit expressions for the propagators . The propagator is exactly the fundamental solution associated with the equation

The solution to the above boundary value problem has been shown to be of the form [25, p.130]

where if (resp. ) is (up to some constant) the unique increasing (resp. decreasing) positive solution of the equation

Noting the solution for and the solution for , for ,

| (3.15) |

These solutions and are smooth in , so that the (Laplace transform of the) local -function admits a meromorphic continuation to .

3.4.2 Obtention of the local time for continuous semimartingales

The obtention of an expression for the propagators of a semimartingale is in principle sufficient to obtain an expression for the Laplace transform (in time) of the local time. This is possible due to the following theorem.

Theorem 3.41 (Revuz,Yor, Ch. VI Theorem 1.10 [41]).

Let be a continuous semimartingale and let be its local time on the interval at level . Writing the Doob decomposition of , suppose that for

then in ,

in particular, this convergence holds in distribution as well.

Notation 3.42.

Whenever the underlying process is implicitly clear, we will denote the local time by .

This theorem entails in particular that for ,

Under the technical hypothesis that if for some , for every the function is bounded above by some integrable function of , the dominated convergence theorem entails that the Laplace transform of the limit and the limit of the Laplace transforms also coincide. Alternatively, we may also check whether is a monotone function of over some neighbourhood for small enough and apply the monotone convergence theorem. This allows us to conclude that

Finally, this has consequences for the distribution of since is exactly the Mellin transform of the distribution of the local time.

4 Examples of applications

4.1 Brownian motion

For the rest of this section, will denote a standard Brownian motion started at .

4.1.1 Associated -function and asymptotic expansions for

Let us start by remarking that, in distribution

The stopping times and of theorem 3.15 are identically distributed and are distributed as the hitting times of by a reflected Brownian motion. An application of Doob’s stopping theorem (cf. [8, p.641]) shows that

| (4.16) |

The term can also be computed by considering the fundamental solution of the corresponding heat equation with Dirichlet boundary conditions. We obtain [36]

Respectively, since Brownian motion is a -stable Lévy process, using equation 3.9 (here, ) we can write

| (4.17) |

Remark 4.1.

Putting everything together, we get

Theorem 4.2.

The -function of Brownian motion on the interval admits an meromorphic extension to the whole complex plane. Furthermore, it is exactly equal to

for all and has a unique simple pole at of residue .

Remark 4.3.