On the optimality of the refraction–reflection strategies for Lévy processes

Kei Noba

Abstract

In this paper, we study de Finetti’s optimal dividend problem with capital injection under the assumption that

the dividend strategies are absolutely continuous.

In many previous studies, the process before being controlled was assumed to be a spectrally one-sided Lévy process, however in this paper we use a Lévy process that may have both positive and negative jumps.

In the main theorem, we show that a refraction–reflection strategy is an optimal strategy.

We also mention the existence and uniqueness of solutions of the stochastic differential equations that define refracted Lévy processes.

AMS 2020 Subject Classifications: Primary 60G51; Secondary 93E20, 60J99

Keywords: Lévy process, stochastic control, optimal dividend problem

1 Introduction

We consider the situation in which a company pays dividends to its shareholders when the company has more than enough capital. In this situation, the company wants to pay more dividends before bankruptcy. The problem of finding a strategy for maximizing the expected net present value (NPV) of the dividend payments is called de Finetti’s optimal dividend problem. In this paper, in addition to the above situation, we assume that the shareholders provide capital injection to the company to prevent bankruptcy. In this situation, the company wants to pay more dividends and receive less capital injection. Our purpose in this paper is to find a strategy that maximizes the expected NPV of the dividend payments minus the cost of capital injection. Such a strategy is called an optimal strategy. We deal with this problem under the assumption that the cumulative amount of the dividends is absolutely continuous with respect to the Lebesgue measure about time and the density is bounded by the value .

Let be the surplus process of the company before dividends are deducted and capital injections are added. When is a Lévy process, many previous studies have shown the optimality of refraction strategies or refraction–reflection strategies in de Finetti’s optimal dividend problem or its capital injection version, respectively. A refraction strategy is a strategy in which the company continues to pay a certain amount of dividends only when the surplus exceeds a certain threshold. Additionally, a refraction–reflection strategy is a strategy in which the company pays dividends according to a refraction strategy when the surplus is non-negative, and the shareholders immediately provide capital injection of only the absolute value of the surplus when the surplus is negative. In de Finetti’s optimal dividend problem, the optimality of the refraction strategies was proved by [6], [1], and [2] when is a Brownian motion with a drift, by [4] when is a Crámer–Lundberg process with exponential jumps, by [10] when is a spectrally negative Lévy process, and by [20] when is a spectrally positive Lévy process. On the other hand, in the capital injection version, the optimality of the refraction–reflection strategies was proved by [13] when is a spectrally positive Lévy process and by [15] when is a spectrally negative Lévy process. In addition, the optimality of the refraction strategies was proved by [5] in another problem of stochastic control when is a spectrally negative Lévy process. However, de Finetti’s optimal dividend problems in the above situations for the general Lévy processes, which may have both positive and negative jumps, are the open problems. In this paper, we deal with de Finetti’s optimal problem with capital injection for general Lévy processes and prove the optimality of refraction–reflection strategies.

In addition to dealing with the general Lévy processes, this paper makes a new attempt at strategies about the refraction. In previous studies, it has been assumed that the drift coefficient of is not contained in when has bounded variation paths. (In this paper, we refer to the case in which has bounded variation paths and the drift coefficient of is included in as Case , and we refer to the other cases as Case ; see, Section 2.2.) In this paper, we introduce new refraction–reflection strategies and prove their optimality in Case .

Before proving the optimality of the refraction–reflection strategies, their existence is an important problem. The resulting processes of the refraction–reflection strategies are refracted–reflected processes, which were introduced by [14]. The construction of the refracted–reflected Lévy processes involves the following two steps.

-

(i)

We define the refracted Lévy processes using stochastic differential equations under non-Lipschitz conditions.

-

(ii)

We inductively define the refracted–reflected Lévy processes by reflecting the refracted Lévy processes at using the infimum.

For the existence of the refraction–reflection strategies, we must prove that the stochastic differential equations that define the refracted Lévy processes have unique strong solutions. The existence and uniqueness of the strong solutions of these stochastic differential equations were proved by [18] when has a positive Gaussian coefficient and by [9] when is a spectrally one-sided Lévy process in Case . In addition, the existence and uniqueness of the strong solutions of the extended stochastic differential equations that define level-dependent Lévy processes were proved by [3] when is a spectrally one-sided Lévy process. In this paper, we describe the existence and uniqueness of the strong solutions when general Lévy process has bounded variation paths or has unbounded variation paths with a finite number of jumps on one side on a compact interval. Especially in Case , we must introduce new refracted Lévy processes, so we use a new idea for proving the existence of refracted Lévy processes. The uniqueness can be proved as in the case of spectrally one-sided Lévy processes, or can be proved by [19, Theorem 5.1].

We take the following steps to prove the optimality of the refraction–reflection strategies.

-

(i)

From previous studies, we can predict the optimal threshold . We obtain a good representation of the density of the expected NPV of dividends and capital injections when we take the refraction–reflection strategy at .

-

(ii)

We give the verification lemma, which gives the sufficient condition for being an optimal strategy. Using the result in Step (i), we prove that the function satisfies the conditions that are given in the verification lemma. From this argument, we can see the optimality of the refraction–reflection strategy at .

In the spectrally one-sided cases, the theory of the scale functions of spectrally one-sided Lévy processes was at the core of the proof. However, there are no corresponding scale functions in the general Lévy processes, and thus we cannot use the same proof. On the other hand, in recent years, [11] and [12] have proved the optimality of the strategies for the problems of stochastic control using the general Lévy processes. [11] proved the optimality of the double barrier strategies for de Finetti’s optimal dividend problem with capital injection (there, the absolute continuity of the cumulative amount of the dividends was not assumed), and [12] proved the optimality of the barrier strategies for the singular control problem. In those papers, we investigated the properties of the expected NPV of some values in some strategies by observing the differences in the behavior of two slightly staggered sample paths, and we proved the optimality of the strategies. We use the same method for Step (i) of the proofs in this paper. The difficulty in the setting of this paper lies in the fact that the variation of the differences in the behavior of two slightly staggered sample paths is much more complicated in the case of the strategies about refraction than in the case of the strategies about only reflection. An important aspect of this paper is that this difficult part is solved and Step (i) of the proof is completed. The proofs used in this paper are expected to be applied to prove the optimality of various strategies about refraction for many problems of stochastic control using the Lévy processes.

This paper is organized as follows. In Section 2, we describe the notation and give some assumptions about Lévy processes, and we recall refracted and refracted–reflected Lévy processes. In Section 3, we give a mathematical setting for de Finetti’s optimal dividend problem with capital injection that we deal with in this paper, and we recall the definition of refraction–reflection strategies and confirm that they are admissible. In Section 4, we compute the densities of the expected NPVs of dividends and capital injections when we take an optimal refraction–reflection strategy at . In Section 5, we give the verification lemma and prove the optimality of a refraction–reflection strategy at using the results in Section 4 and the verification lemma; the main result is in this section. In Section 6, we give numerical results from Monte Carlo simulation, confirming numerically the correctness of our main results. In Section 7, we prove that the expected NPV of an optimal dividend payments and capital injections in this paper converges to that in [11] as . In Appendix A, we represent the infimum of the bounded variation functions using the stagnation time at of the function reflected at and the jumps; the result in this section is used in the proofs of results in Appendix B and Appendix C. In Appendix B, we give the existence of the solution of an ordinary differential equation; the results obtained in this section are used to prove the existence of the refracted Lévy processes in the case of bounded variation. (The uniqueness of the solution can be proved in the same way as the previous studies, thus we omit it.) In Appendix C, we prove that the resulting processes of refraction–reflection strategies are refracted–reflected Lévy processes. In Appendix D, we investigate the behavior of two paths of refracted–reflected Lévy processes with slightly offset starting positions; the results in this section are used to obtain the densities of the expected NPVs of dividends and capital injections of the refraction–reflection strategy at in Section 4. In Appendix E, we give a lemma for the continuity of hitting times; this lemma is also used to compute the densities of the expected NPVs of dividends and capital injections and to prove an inequality that appears in the verification lemma. In Appendix F, we give an example that satisfies the assumptions of the Lévy processes with unbounded variation paths to which our main results can be applied. In Appendix G, we give the proof of the verification lemma. In Appendix H, we give the proofs of two lemmas in Section 7.

2 Preliminaries

2.1 Lévy processes

We let be a Lévy process that is defined on a probability space . For all , we write for the law of when it starts at . We write for the characteristic exponent of , which is the function satisfying

| (2.1) |

The characteristic exponent has the form

| (2.2) |

where , , and is a Lévy measure on satisfying

| (2.3) |

It is known that the process has bounded variation paths if and only if and the Lévy measure satisfies . When this holds, we denote

| (2.4) |

where

| (2.5) |

We write for the natural filtration generated by . For , we define the hitting times of by

| (2.6) |

Here, we assume that . We fix the value throughout this paper. We define the process as

| (2.7) |

For , we define a hitting time of by

| (2.8) |

The following assumption is necessary for strategies to be admissible (see Remark 3.2).

Assumption 2.1.

We assume that the Lévy measure satisfies

| (2.9) |

2.2 Refracted Lévy processes

The Lévy process has the following two cases.

-

Case

has unbounded variation paths or has bounded variation paths with .

-

Case

has bounded variation paths and .

In each case, for , we define the process as the solution of the stochastic differential equation

| (2.10) |

where

| (2.11) |

The process is called a refracted Lévy process at . We give the following assumption for .

Assumption 2.2.

The stochastic differential equation (2.10) has a unique strong solution.

Remark 2.3.

It is known that satisfies Assumption 2.2 in the following cases.

-

(i)

If the process is a spectrally negative Lévy process, which is a Lévy process with no positive jumps and no monotone paths, and satisfies the condition in Case , then (2.10) has a unique strong solution by [9, Theorem 1]. By the same argument as that of the proof of [9, Theorem 1], it is easy to check that if the process is a spectrally positive Lévy process, which is a Lévy process with no negative jumps and no monotone paths, then (2.10) has a unique strong solution.

- (ii)

In addition to Remark 2.3, we give the following.

Corollary 2.4.

When has unbounded variation paths and satisfies or , the stochastic differential equation (2.10) has a unique strong solution.

If has unbounded variation paths and , by using Remark 2.3 (i) again each time a negative jump of appears, a unique strong solution of (2.10) can be constructed inductively. The same is true for the case in which has unbounded variation paths and . Thus, Corollary 2.4 can be proved soon by Remark 2.3 (i). We omit the detail of the proof.

Theorem 2.5.

When has bounded variation paths, the stochastic differential equation (2.10) has a unique strong solution.

When has bounded variation paths, (2.10) is an ordinary differential equation for fixed . Therefore, by using Theorem B.1 for each path, Theorem 2.5 can be proved directly.

For and , we write

| (2.12) |

2.3 Refracted–reflected Lévy processes

In this section, we recall the refracted–reflected Lévy processes that are defined in [14, Section 2.2]. For a Lévy process satisfying Assumption 2.2, we define the refracted–reflected process at as follows.

-

Step

Set and . If , go to Step . If , go to Step .

-

Step

Let be the refracted Lévy process at that satisfies

(2.13) We redefine . We set for . Go to Step .

-

Step

Let be the process that satisfies

(2.14) We redefine . We set for . Go to Step .

From the definition above, it is easy to check that satisfies

| (2.15) |

We define the refracted–reflected Lévy process at as

| (2.16) |

Remark 2.6.

By [9, Remark 3], the refracted Lévy process constructed from the spectrally negative Lévy process in Case has the strong Markov property with respect to . By the same argument as [9, Remark 3], we can check that the refracted Lévy processes and the refracted–reflected Lévy processes defined in this paper have the strong Markov property.

3 Optimal dividend problem with capital injection

In this section, we describe the problem in this paper and recall the refracted–reflected strategies.

3.1 Setting of the problem

We fix the cost per unit injected capital and the discount rate . In this paper, a strategy is a set of the processes and satisfying the following conditions.

-

(i)

There exists the process that is progressively measurable with respect to and satisfies

(3.1) -

(ii)

The process is -adapted, non-decreasing, right-continuous, and satisfies

(3.2)

Then, the resulting process of the strategy satisfies

| (3.3) |

The expected NPV of the dividend payments minus the cost of capital injections when we use the strategy is written as

| (3.4) |

Let be the set of all strategies that satisfy

| (3.5) |

The purpose of this study is to find a strategy that meets the following condition:

| (3.6) |

The strategy satisfying (3.6) is called an optimal strategy.

Remark 3.1.

Since all strategies satisfy (3.1), we have

| (3.7) |

Remark 3.2.

If does not satisfy (2.9), then for all strategies , we have

| (3.8) |

and is an empty set. To demonstrate, we assume that does not satisfy (2.9) and fix a strategy and a value . It is sufficient to prove to show (3.8). Since satisfies (3.2), we have

| (3.9) |

We define the stopping time as

| (3.10) |

By the definition of , there exists the value that satisfies

| (3.11) |

where

| (3.12) |

Since has the distribution and is independent from and , we have

| (3.13) | ||||

| (3.14) |

where in the last equality we used the fact that does not satisfy (2.9). By (3.9) and (3.14), we obtain .

3.2 Refraction–reflection strategies

The refraction–reflection strategy at is defined as

| (3.15) |

Then, the resulting process with corresponds to by (2.15). In addition, we confirm that the process corresponds to the process in Appendix C. Thus, the refraction–reflection strategy is a strategy such that the company pays dividends of or when the surplus process exceeds or equals and receives a capital injection when it falls below . From this fact, the refraction–reflection strategies exist.

Lemma 3.3.

The refraction–reflection strategy at belongs to .

Proof.

For simplicity, we write for for .

4 Some properties of the function

In this section, we define the optimal barrier and compute the derivative of . This section is necessary to prove the optimality of the refracted–reflected strategies in Section 5.

We define the value by

| (4.1) |

where with .

Remark 4.1.

The value is finite since .

Remark 4.2.

If is regular for for , then . In addition, it is easy to check that is right-continuous at . Thus, .

Remark 4.3.

Let we define

| (4.2) |

Thereafter we will show that the refraction–reflection strategy at is an optimal strategy, but we can prove the optimality of the refraction–reflection strategy at by the same argument.

It is easy to check that is right-continuous and may not be left-continuous. In this case, may be less than . Only when , we may need to define the value as follows. If only the case is required, then one can go to Lemma 4.6 directly.

We define

| (4.3) |

and for , we define the independent random variable as

| (4.6) |

In addition, we define

| (4.7) |

Note that , and if , then we have and thus

| (4.8) |

In addition, if , then -a.s. and thus we have (4.8). Therefore, we have the following lemma.

Lemma 4.4.

We assume that and satisfies one of the following.

-

(i)

;

-

(ii)

and is regular for itself for .

Then, there exists satisfying

| (4.9) |

Remark 4.5.

When satisfies or and is irregular for itself for , we assume that . Thus (4.9) holds when satisfies condition (i) or (ii) in Lemma 4.4.

Lemma 4.6.

We assume that satisfies condition (i) or (ii) in Lemma 4.4. The function is concave, and the function

| (4.12) |

is its density with respect to the Lebesgue measure.

Proof of Lemma 4.6.

For , we write and . In addition, we write and for the cumulative amounts of dividends and capital injections, respectively, when we impose the refraction–reflection strategy at on and write . Note that behaves as a refracted–reflected Lévy process. We write “” and “” for “” and “” of .

For , we have

| (4.13) |

Note that for sufficiently small , by Lemmas D.1 and D.3, the Stieltjes integrals using processes and , which are monotone processes, are well-defined.

(i) We want to give bounds of (4.13) to compute the right derivative of . We fix and . We inductively define stopping times , and values as

| (4.14) |

| (4.15) |

where . From Lemmas D.1 (3) and D.3, we have

| (4.16) |

and may increases only on , thus we have

| (4.17) |

Note that, by Lemmas D.1 (2), (4) and D.3, the values and are non-negative, thus by Lemmas D.1 (1) and D.3, we have . In addition, since and takes non-negative values and by Lemmas D.1 (2) and D.3, we have

| (4.18) |

From Lemma D.1 (3), (4) and D.3, the processes and are non-decreasing, thus by (4.18) and Lemmas D.1 (1) and D.3,

| (4.19) |

From (4.16), (4.17) and (4.19)we have

| (4.20) | ||||

| (4.21) |

Since satisfies (3.15), may start to increase at time . In addition, it does not increase after time by (4.19). Furthermore, we have , which holds with “” on , thus we have

| (4.22) | ||||

| (4.23) |

Using the strong Markov property at , and since does not increase after time , we have

| (4.24) |

Using the strong Markov property at , we have

| (4.25) | ||||

| (4.26) | ||||

| (4.27) |

Using (4.24) and (4.27), we have

| (4.28) |

and

| (4.29) | |||

| (4.30) | |||

| (4.31) |

From (4.13), (4.21), (4.23), (4.28), and (4.31), we have, for ,

| (4.32) |

(ii) We prove that for and ,

| (4.33) |

By Fubini’s theorem, we have

| (4.34) | |||

| (4.35) |

where . In fact, from the definitions of , , , and , we have

| (4.36) |

and thus, for ,

| (4.37) |

By (4.37), the term in absolute value of the left-hand side of (4.37) is integrable for , and we could use Fubini’s theorem at (4.35). Since the right-hand side of (4.37) is integrable with respect to the measure , we can apply Fatou’s lemma to (4.35) regardless of the plus or minus of the term in the integral, and we have

| (4.38) | |||

| (4.39) |

We fix such that is càdlàg and the differential equation (2.10) has a unique solution (almost surely satisfies these conditions), and we prove that

| (4.40) |

almost everywhere (a.e.) with respect to . Since for fixed there is only one where does not equal to in the summation and by

| (4.41) |

it is sufficient for (4.40) to prove that

| (4.42) |

a.e. with respect to . We assume that does not jump at ( does not have jumps a.e. with respect to ) and assume . Then, for sufficiently small , we have for , and thus, by the definitions of and , we have for all . Therefore, we have (4.42). We assume that . Since the function is non-increasing and since when , we have

| (4.43) |

We need to consider the following three cases.

-

(ii-a)

We assume that . Then, for sufficiently small , and thus

(4.44) where in the equality we used (4.9).

- (ii-b)

-

(ii-c)

We assume that and is irregular for for . Then, takes the value for a while after hitting , and after that, jumps away from . Thus for sufficiently small . Therefore, we have (4.45).

From the arguments above, we have (4.40) a.e. with respect to . From (i), (4.39), and (4.40), we have (4.33).

(iii) We prove that for and ,

| (4.46) |

From the definition of , we have

| (4.47) |

We replace “” by “”, “” by “”, “” by “” and “” by “” from all the equations in (ii) except for (4.33). In addition, we replace “” by “” from (4.39), (4.40), (4.42), (4.43) and (4.44). We can then confirm that these equations in (ii) except for (4.33) are correct by the same arguments as that in (ii). From (i) and (4.47), and (4.39) and (4.40) with the symbols replaced as above, we have (4.46).

(iv) From (4.33) and (4.46), the function is right-continuous on . Similarly, from (4.33) and (4.46) with changed to , the function is left-continuous on . In addition, we have, for and ,

| (4.48) |

By (4.48), the function is mid-point concave and thus concave on . From (4.33) and (4.46), we have

| (4.49) |

Since the function is non-increasing, this function is continuous a.e. with respect to the Lebesgue measure and by (4.49) and [17, Proposition 3.1 in Appendix], the right derivative and the left derivative of is equal to the function a.e. with respect to the Lebesgue measure. Furthermore, by [17, Proposition 3.2 in Appendix], the left-derivative of is the density of , thus (4.12) is the density of . The proof is complete. ∎

Lemma 4.8.

We assume that and is irregular for itself for . The function is concave and the function is its density with respect to the Lebesgue measure.

Proof.

Hereinafter, we assume that the function , which usually symbolizes for the derivative, represents the function .

5 Verification

In this section, we prove the optimality of the refraction–reflection strategy using the verification lemma and results in Section 4. Before giving the main theorem, we give an assumption.

Assumption 5.1.

When has unbounded variation paths, for , the function

| (5.1) |

has a locally bounded density on with respect to the Lebesgue measure. The function is continuous a.e. on with respect to the Lebesgue measure.

This assumption is necessary to prove that the function belongs to , which is a class of functions that will appear in the proof of the main theorem, and to prove Lemma 5.5 when has unbounded variation paths. We give examples of the processes with unbounded variation paths satisfying Assumption 5.1 in Appendix F.

Theorem 5.2.

The refracted–reflected strategy is an optimal strategy.

Before giving its proof, we give classes of functions and an operator that are almost the same as those defined in [11, Section 2].

Let be the set of functions satisfying the following conditions.

-

(i)

The function satisfies

(5.2) for some .

-

(ii)

The function has the locally bounded density with respect to the Lebesgue measure on , i.e., there exists a locally bounded measurable function on such that

(5.3)

Let be the set of functions such that is continuously differentiable on and the derivative has the locally bounded density with respect to the Lebesgue measure on . Let be the operator applied to (resp. ) with a fixed density (resp. a fixed density of the derivative ) for the case in which has bounded (resp. unbounded) variation paths with

| (5.4) |

This operator is well defined by [11, Remark 2.4].

Remark 5.3.

By the same argument as in [11, Remark 2.5], for (resp. ), the map

| (5.5) | ||||

| (5.6) |

is continuous on when has bounded (resp. unbounded) variation paths.

Using the operator , we can give the following verification lemma that gives the sufficient condition for being an optimal strategy.

Lemma 5.4.

Suppose that has bounded (resp. unbounded) variation paths. Let be a function belonging to (resp. ). We fix the density of (resp. the density of the derivative ) with respect to the Lebesgue measure and suppose the following.

| (5.7) | |||

| (5.8) | |||

| (5.9) |

Then for .

The proof of Lemma 5.4 is almost the same as the proof in the spectrally positive cases in [13, Appendix A]. However, unlike the spectrally positive cases, it uses a more general operator than the infinitesimal generator, and it is necessary to take the same precautions as in [11, Remark 5.9]. Thus, we give the proof of Lemma 5.4 in Appendix G.

For the optimality of the strategy , it is sufficient to prove that the function satisfies the conditions in Lemma 5.4.

We confirm that belongs to (resp. ) when has bounded (resp. unbounded) variation paths. From Remark 3.1 and since

| (5.10) |

the function satisfies (5.2). In addition, by Lemmas 4.6 and 4.8, the function belongs to . By Lemma 4.6 and Assumption 5.1, the function belongs to when has unbounded variation paths.

In the following, we prove that satisfies the other conditions in Lemma 5.4.

Lemma 5.5.

Proof.

(i) We prove (5.11) on . In addition, we prove (5.11) at when has unbounded variation paths. By the strong Markov property and by the definitions of and , we have

| (5.13) |

The process is a martingale for with . In fact, by Remark 3.1, the monotonicity of , the compensation formula of Poisson point processes, (5.10), and (2.9), we have, for and ,

| (5.14) | ||||

| (5.15) | ||||

| (5.16) | ||||

| (5.17) |

where is the Poisson random measure on associated with . In addition, we have, for and ,

| (5.18) | |||

| (5.19) | |||

| (5.20) | |||

| (5.21) | |||

| (5.22) | |||

| (5.23) |

where in the third equality, we used the strong Markov property and (5.13). By Remark 5.3, and since is continuous and is non-increasing by Lemma 4.6, the map is the sum of a continuous function and a monotone function on (resp. the sum of a continuous function on and , which can be taken to be continuous a.e. by Assumption 5.1) when has bounded (resp. unbounded) variation paths. Thus, by the same argument as that of the proof of [11, Lemma 5.7], we have (5.11) on when has bounded variation paths. In addition, we can take the density of the function to be continuous and satisfying (5.11) on .

(ii) We prove (5.12). Using the strong Markov property, we have, for ,

| (5.24) | ||||

| (5.25) |

where

| (5.26) |

By (5.25), the function has the density with respect to the Lebesgue measure, which is equal to . In addition, the function has a density which is locally bounded and continuous a.e. on when has unbounded variation paths by Lemma 4.6 and Assumption 5.1 and since the function has the same derivative as by (5.25). By the same argument as in (i), the process is a martingale for with . Thus, again by the same argument as in (i) (here, we may need to use Lemma 4.8 instead of Lemma 4.6 when and is irregular for itself for ), we have

| (5.27) |

when has bounded variation paths. In addition, we can take the density of the function to be continuous and satisfying (5.27) on . We put for , which is the density of with respect to the Lebesgue measure, when has unbounded variation paths. From (5.25) and (5.27), we obtain (5.12) in both cases of having bounded and unbounded variation paths.

(iii) We prove (5.11) at when has bounded variation paths and . We assume that . Then, is regular for for , and thus by the strong Markov property and (5.13), and since is non-increasing, we have

| (5.28) | ||||

| (5.29) | ||||

| (5.30) |

where

| (5.31) |

By (5.30) and since is non-increasing, we have , and thus the map is left-continuous at . From the above argument and (i), we have

| (5.32) |

We assume that which implies . Then, is regular for for , and thus by the strong Markov property and (5.25), and since is non-increasing, we have

| (5.33) | ||||

| (5.34) |

By (5.34) and since is non-increasing, we have , and thus the map is right-continuous at . From (4.9), the above argument, and (ii), we have

| (5.35) | ||||

| (5.36) |

By (5.32) and (5.36), we have (5.11) at when has bounded variation paths and .

From (i), (ii), and (iii), the proof is complete. ∎

Proof of Theorem 5.2.

We have already confirmed that belongs to (resp. under Assumption 5.1) when has bounded (resp. unbounded) variation paths. Thus, it is sufficient to prove that satisfies (5.7), (5.8), and (5.9) by Lemma 5.4.

From Lemmas 4.6 and 4.8, satisfies (5.8). In addition, since is non-decreasing and by Remark 3.1 and (3.5) with and , satisfies (5.9). For , we have by Lemma 4.6, the definition of , and (4.9), and thus we have

| (5.37) |

where in the last equality we used (5.11). For , we have by Lemmas 4.6, 4.8, and the definition of , and thus we have

| (5.38) |

where in the last equality we used (5.12). Therefore, the function satisfies (5.7). The proof is complete. ∎

6 Numerical results

In this section, we present numerical results for and via Monte Carlo simulation as in [12], and we confirm the correctness of our main theorem. Since the purpose of this study is not to think of better simulation methods, we use the classical Euler scheme.

For the simulation, we use the Lévy process that has the form

| (6.1) |

where is a standard Brownian motion, and are independent Poisson processes with arrival rate , is an independent and identically distributed (i.i.d.) sequence of continuous uniform random variables on , and is an i.i.d. sequence of Weibull random variables with shape parameter and scale parameter . In this section, we give simulations in two cases. In Cases and , we assume that and , respectively. Note that the Lévy process in Case has unbounded variation paths and we did not confirm that satisfies the conditions in Assumption 5.1. For the other parameters, we set , , and .

In our simulation, we truncate the time horizon at and discretize as equally spaced points with distance as in [12]. To approximate and , we prepare the set of sample paths that approximate starting from , and we represent these with

| (6.2) |

Then the approximated sample paths of and when starts from are

| (6.3) |

defined as follows, inductively: for , if , then

| (6.4) |

if , then

| (6.5) |

else

| (6.6) |

where and . Thus, we approximate by

| (6.7) |

where for and with . In addition, we approximate by

| (6.8) | ||||

| (6.9) |

By the strong Markov property at , the function with is approximated by

| (6.10) |

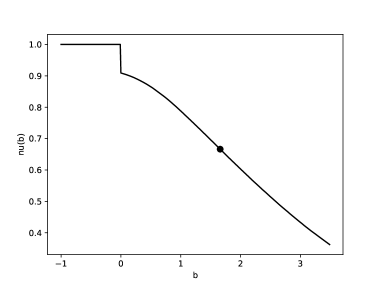

where . In the first step, we compute for in Case and for in Case , and make figures. Then, the function in Cases and is approximated by Figure 1.

Case 1

Case 2

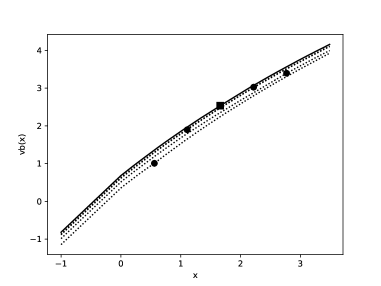

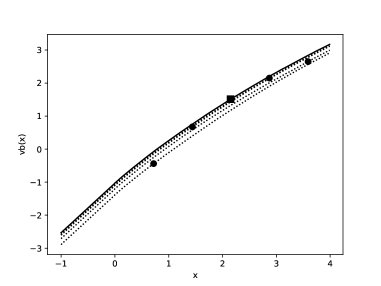

From this computation, is approximated by and in Cases and , respectively. In the second step, we compute for some and for in Case and in Case . Here, we compute for in Case and for in Case . Then the function with , , , , and in Cases and is approximated by Figure 2. In these figures, the function is represented by the solid line and the others are represented by the dotted line.

Case 1

Case 2

From Figure 2, we can see by visual inspection that is the optimal barrier. In particular, we have not confirmed that in Case satisfies the assumptions given in this paper, but we can expect that the main result is true for it.

7 Convergence result

In the previous sections we have shown the optimality of refraction–reflection strategies. On the other hand, in [11], I have proved the optimality of double barrier strategies under different conditions. In this section, we show that the expected NPV of the dividend payments and capital injections when taking the optimal refraction–reflection strategy converges to that when taking the optimal double barrier strategy under the condition of [11] by taking the limit of to .

In this section, we assume that Assumption 2.2 and Assumption 5.1 hold for all . In addition, we give [11, Assumption 2.1].

Remark 7.1.

[11, Assumption 2.1 (2.4)] is stronger than Assumption 2.1. If we only give Assumption 2.1, we can predict that the expected NPV of an optimal dividend payments and capital injections may go to infinity by taking the limit of to since the expected NPV of the dividend payments may become infinite when we take double barrier strategies (see, [11, Remark 3.4]). However, since I only considered cases with [11, Assumption 2.1 (2.4)] in [11], we give it in this section for simplicity.

We write for refracted Lévy process at with . Similarly, we write for reflected Lévy process at , i.e. for . In addition, we denote, for , and ,

| (7.1) | ||||

| (7.2) | ||||

| (7.3) |

For fixed , an optimal strategy of the problem in Section 3.1 is the refraction–reflection strategy at by Remark 4.3 and Theorem 5.2. Similarly, an optimal strategy of the problem in [11, Section 2.2] is the doubly barrier strategy at by [11, Theorem 5.1]. We write the expected NPVs of the dividend payments and capital injections as and when using the strategy and with , respectively. The purpose of this chapter is to prove that and converge and for as , respectively.

Lemma 7.2.

For , we have

| (7.4) |

for all such that does not have negative jumps at , -a.s..

From Lemma 7.2, the convergence (7.4) is true for a.e. , -a.s.. We give the proof of Lemma 7.2 in Appendix H.1.

Using Lemma 7.2, we can get the following corollary. The proof is easy, so we omit it.

Corollary 7.3.

For , we have as . In addition, we have as .

For fixed , we write for refracted–reflected Lévy process at . In addition, we write and for the cumulate amount of dividend payments and capital injections when we apply refraction–reflection strategy at . We represent the symbols about doubly barrier strategies by substituting for in the symbols above.

The following lemma is necessary to prove Theorem 7.5.

Lemma 7.4.

For , we have

| (7.5) |

for all such that does not have negative jumps at , -a.s.. In addition, the above is also true when and has bounded variation paths.

Theorem 7.5.

For , we have

| (7.6) |

This convergence is uniformly in on any compact set.

Proof.

For fixed , let be the set of all strategies that satisfies the conditions in Section 3.1. Similarly, be the set of all strategies that satisfies the conditions in [11, Section 2.2]. Then, by the definitions of and , we have, for with , , and thus, we have

| (7.7) |

Since is an optimal barrier, we have for and , thus by (7.7), we have

| (7.8) |

For and , we have

| (7.9) | |||

| (7.10) | |||

| (7.11) |

where in the first equality, we used integration by parts and in the last equality, we used Lemma 7.4 and the dominated convergence theorem with and

| (7.12) |

By the same argument as above, we have

| (7.13) |

By (7.7), (7.8), (7.11) and (7.13), we obtain (7.6). Uniform convergence on any compact set follows from Dini’s theorem. The proof is complete. ∎

Acknowledgments

I express my deepest gratitude to Prof. Kazutoshi Yamazaki and Prof. Kouji Yano for their comments on the structure of this paper. This work was supported by JSPS KAKENHI Grant Number 21K13807 and JSPS Open Partnership Joint Research Projects Grant Number JPJSBP120209921.

Appendix A Lemma for infimum

In this appendix, we give a lemma for the infimum, which is used to prove Theorem B.1 and in Appendix C.

Lemma A.1.

Let be the càdlàg function from to that has bounded variation and satisfies

| (A.1) |

for some . We define

| (A.2) |

Then we have, for ,

| (A.3) |

Remark A.2.

If the Lévy process has bounded variation paths and satisfies , then the paths of satisfy the conditions that are imposed for in Lemma A.1, almost surely.

Proof of Lemma A.1.

(i) In the first step, we assume that the function is non-increasing. We define

| (A.4) |

Since is non-increasing and by the definition of , we have

| (A.5) |

and thus

| (A.6) |

By (A.6) and the definition of , we have

| (A.7) |

and thus we have

| (A.8) |

By (A.5) and (A.8), (A.3) holds for . By (A.5), (A.1), and (A.6), we have, for ,

| (A.9) | |||

| (A.10) |

By (A.10) and since (A.3) holds for , we have (A.3) for . Thus, we obtain (A.3) on .

(ii) In the second step, we assume that the map has only a finite number of positive jumps on each compact interval in . Let be the -th positive jump time of . We consider the value for each interval with , where . Since is non-increasing on and by (i), we have (A.3) for . We fix . For , we have

| (A.11) |

where

| (A.12) |

Since the function is non-increasing on , we can apply (i) for and have, for ,

| (A.13) |

where

| (A.14) |

By (A.13) and (A.12), and since we have

| (A.15) |

we have, for ,

| (A.16) |

Since has a positive jump at , we have

| (A.17) |

By (A.11), (A.16), and (A.17), we have

| (A.18) |

Since (A.3) holds for and (A.18) holds for , we obtain (A.3) for .

(iii) In the third step, we consider the general cases. For , we define the function on as

| (A.19) |

Here, we assume that implies . Note that for , the function satisfies the assumption in (ii). We define

| (A.20) |

By the definition of , for , the function

| (A.21) |

is non-decreasing and takes values in . For , we write

| (A.22) |

where . From (A.22), the left-continuity of , and the right-continuity of , for , there exist such that for , and thus we have, for ,

| (A.23) |

Since the function (A.21) is non-negative and by (A.23), we have, for ,

| (A.24) | ||||

| (A.25) |

By the definition of and , and have the same negative jumps at the same times. By the above fact and since the function (A.21) is non-decreasing, we have, for ,

| (A.26) | ||||

| (A.27) |

By (A.25), (A.27), and the definition of , we have, for ,

| (A.28) |

From (ii), we have, for ,

| (A.29) |

By the definition of and by (A.28), we have

| (A.30) |

uniformly on compact intervals as . In addition, since all for have the same negative jumps at the same times and by (A.30) and the dominated convergence theorem, we have

| (A.31) |

uniformly on compact intervals as . Note that we can use the dominated convergence theorem in (A.31) since we have, for and ,

| (A.32) |

and since has bounded variation paths which implies,

| (A.33) |

Since converges to non-decreasingly as for , we have

| (A.34) |

By (A.34) and the dominated convergence theorem, we have

| (A.35) |

as . By taking the limit of (A.29) as and by (A.30), (A.31), and (A.35), we obtain (A.3). The proof is complete. ∎

Remark A.3.

We consider the case where holds in the same situation as Lemma A.1. Then we have, for ,

| (A.36) |

It can be proved by first assuming that the map has only a finite number of negative jumps on each compact interval in , and then considering the approximation as in (iii) in the proof of Lemma A.1. The proof is similar to A but simpler and is therefore omitted.

Appendix B Existence and uniqueness of the solution of an ordinary differential equation

Let be the càdlàg function from to that has bounded variation and satisfies (A.1) for some . We define the function as

| (B.1) |

In this section, we prove the following theorem.

Theorem B.1.

For , there exists the unique function that satisfies

| (B.2) |

where

| (B.3) |

Using this theorem, we can prove Theorem 2.5 directly. After that, we give the proof of Theorem B.1.

The proof of the uniqueness is the same as the proof for spectrally negative cases in [8, pp. 287] but changing from to and from to . Thus, it is enough to prove the existence of a solution in the following.

B.1 Special cases

We assume that the function satisfies one of the following.

-

Case A

We have .

-

Case B

The function has only a finite number of negative jumps on each compact interval in and we have .

-

Case C

The function has only a finite number of positive jumps on each compact interval in and we have .

We prove that (B.2) has a solution when the function satisfies one of the conditions above. Here, we use the same idea as the proof of that in [8, Theorem 10.4].

- Case A

-

Case B

For , we define functions and times inductively as follows:

(B.4) where and . Note that takes values in and behaves as a reflected Lévy process at when is a path of Lévy process. Since has finitely many negative jumps on each compact interval, we have

(B.5) Thus, we can define the function on as

(B.6) We check that the process satisfies (B.2). We have, for ,

(B.7) Thus we have, for ,

(B.8) (B.9) In addition, by Lemma A.1, we have, for ,

(B.10) By the definition of and (B.10), we have, for ,

(B.11) (B.12) -

Case C

In Case B, the solution could be constructed by joining paths whose motion is reflected by when taking values above and whose drift is subtracted by when taking values below . Similarly in Case C, the solution can be constructed by joining paths that have the original motion when taking values above , and paths that have the motion reflected at with the drift subtracted by when taking values below . The proof is almost the same as in Case B and is therefore omitted.

The proof in special cases in Theorem B.1 is complete.

B.2 Other cases

We assume that . For , we define the function on as

| (B.13) |

Then, the function is a function that belongs to Case B in Section B.1 when and Case C in Section B.1 when and that converges to the function uniformly on compact intervals as since the function has bounded variation and by the definition of . In addition, the function satisfies

| (B.14) |

For , let the function on be the solution of (B.2) driven by the function . For with , we have

| (B.15) |

where

| (B.16) |

Since is non-decreasing, we have

| (B.17) |

We want to check that

| (B.18) |

To demonstrate, we assume that for some . Since the function does not have negative jumps and is continuous, there exist with such that

| (B.19) |

Since is non-decreasing and by (B.15), there exists such that

| (B.20) |

However, (B.19) and (B.20) contradict (B.17), and thus we have

| (B.21) |

By (B.21), is a non-decreasing process that takes only non-negative values. Therefore, we obtain (B.18).

From (B.18), the function is non-increasing on for , and thus we can define the function as

| (B.22) |

where in the last equality we used

| (B.23) |

which comes from (B.18) and for . We want to check that the function is a solution of (B.2) driven by the function . By the definition of and since for and , we have

| (B.24) |

Since we have and for and since the functions and satisfy (B.2) driven by the functions and , respectively, we have

| (B.25) |

From (B.24) and (B.25), we have

| (B.26) |

Since we have and for and the function satisfies (B.2) driven by the function for , and by (B.26), the function satisfies (B.2) driven by the function .

The proof of Theorem B.1 is complete.

Appendix C Behavior of

In this appendix, we confirm that the process , which is the resulting process of the refraction–reflection strategy at defined in Section 3.2, corresponds to the process .

We consider the proof in three cases.

(i) We assume that has unbounded variation paths or bounded variation paths with . When has unbounded variation paths, since is regular for for and by [8, Theorem 6.7], we have

| (C.1) |

When has bounded variation paths with , since is irregular for for , the process takes a value only a finite number of times in a finite time, and thus we have (C.1). From (3.15) and (C.1), we have

| (C.2) |

From (3.15) and (C.2), we have

| (C.3) |

From (C.2), (C.3), and (2.16), we have

| (C.4) |

(ii) We assume that has bounded variation paths with . From (3.15), we have

| (C.5) | |||

| (C.6) |

Note that the definition of depends on the value of since Case applies if holds and Case applies if holds. By comparing with (2.16), it is enough to show that

| (C.7) |

We fix . If for , we have

| (C.8) |

and thus (C.7) is true. We assume that for some and define

| (C.9) | ||||

| (C.10) |

By (C.10) and the same argument as that of the proof of (A.23), we have

| (C.11) |

Since exists, and by (2.16) with Lemma A.1, and (C.9), we have

| (C.12) |

Since the map

| (C.13) |

is non-increasing on , takes non-negative values, and , we have

| (C.14) | |||

| (C.15) |

where in the last equality we used (2.16) with Lemma A.1. From (C.11), (C.12), and (C.15), we obtain (C.7). The proof is complete.

Appendix D Behavior of two paths

In this appendix, we consider the behavior of two paths of refracted–reflected processes. Here, we use the same notation as in the proof of Lemma 4.6.

Lemma D.1.

We fix , , and with . Then, -a.s., we have the following.

-

(1)

We have

(D.1) -

(2)

The process is non-increasing and takes values in .

-

(3)

The process is non-decreasing and takes values in . The support of its Stieltjes measure is included in the closure of .

-

(4)

The process is non-increasing and takes values in . The support of its Stieltjes measure is included in the closure of .

Proof of Lemma D.1.

We define the stopping times and as follows: for ,

| (D.2) |

where . We assume that , , and for . Then, we can observe the behavior of sample paths, inductively, as follows.

(i) We observe the behavior for . Note that by (ii) on or the definition of for . From the definitions of the processes and , they behave as the reflected Lévy processes of at , respectively, and so we have

| (D.3) | |||

| (D.4) | |||

| (D.5) | |||

| (D.6) |

Thus the behavior of is non-increasing and takes values in . In fact, we define

| (D.7) |

then we have, for ,

| (D.8) |

for ,

| (D.9) |

and for ,

| (D.10) | |||

| (D.11) | |||

| (D.12) |

In addition, the support of its Stieltjes measure is included in the closure of since the map

| (D.13) |

may decrease on by the same argument as that after (C.9). Since and take values in for , the process is a constant process satisfying

| (D.14) |

From the above and (D.1), the process is non-increasing (decreases only when decreases) and satisfies

| (D.15) | ||||

| . | (D.16) |

(ii) We observe the behavior for . From the definitions of the processes and , they behave as the refracted Lévy processes of and at , respectively. From the definition of refracted Lévy processes, we have

| (D.17) |

where

| (D.18) |

for . From (D.17) and since by (i) and is non-decreasing, changes continuously, is non-increasing until the value reaches and the rate of change over time is no more than . Thus, if takes values below , is takes value before doing so. We confirm that does not take values below . Assume that at time . Then, by the uniqueness of the strong solution of the stochastic differential equation (2.10), for . In conclusion, the process is non-increasing and takes values in . In addition, the support of its Stieltjes measure is included in the closure of by (D.17). From (3.15), we have

| (D.19) |

which is non-decreasing. From the above arguments and by (D.1), the process is a constant process satisfying

| (D.20) |

By inductively repeating (i) and (ii) for , the proof is complete. ∎

Lemma D.3.

We assume that belongs to Case . We fix , , and with . Then, -a.s., we have the same statements as (1)–(4) in Lemma D.1.

Proof.

By (2.16), we have

| (D.21) | ||||

| (D.22) |

and thus we have (2) in Lemma D.1. By (3.15) and (D.22), we have

| (D.23) | ||||

| (D.24) |

which is non-decreasing. Since behaves as and by (3.15) and (A.2), we have, for ,

| (D.25) | ||||

| (D.26) | ||||

| (D.27) |

By (D.27), we have

| (D.28) |

which is non-increasing (may decrease only when and thus ). By (2), (D.24), (D.28), and (D.1), we have (3) and (4) in Lemma D.1.

The proof is complete. ∎

Lemma D.4.

We assume that is irregular for itself for . We fix , , and with . Then, -a.s., we have (1), (2), (4) in Lemma D.1. In addition, we have

| (D.29) |

Proof.

Since is irregular for for , the process takes a value only a finite number of times in a finite time. Thus, by (3.15), we have (D.29). Since (D.22) holds, we have (2). By (D.1) and (D.29), we have

| (D.30) |

and by the same argument as in (i) in the proof of Lemma D.1, we have (4). The proof is complete. ∎

Appendix E A property of the Laplace transform of a hitting time

In this appendix, we give a lemma for the continuity of the function .

Lemma E.1.

We assume that is regular for for . Then, the function is right-continuous at . In addition, if then the function is left-continuous at .

Proof.

Note that the limits and exist since the function is non-increasing.

(i) We prove that

| (E.1) |

We assume that is regular for for . By the strong Markov property and since the function is non-increasing on , we have, for ,

| (E.2) |

Thus, by taking the limit as , we have (E.1). We assume that is irregular for for . Then, for the process , is irregular for and thus is regular for by the hypothesis. In addition, is irregular for for since does not take a value less than or equal to for a while after taking a value greater than . By the strong Markov property and since the function is non-increasing on , we have, for ,

| (E.3) | ||||

| (E.4) |

Thus, by taking the limit as , we have (E.1).

(ii) We assume that and prove that

| (E.5) |

We assume that is regular for for . By the same argument as in the proof of (E.4), we have, for ,

| (E.6) | ||||

| (E.7) |

Thus, by taking the limit as , we have (E.5). We assume that is irregular for for . Then, for the process , is irregular for and thus is regular for by the hypothesis. By the strong Markov property and since the function is non-increasing on , we have, for ,

| (E.8) |

Thus, by taking the limit as , we have (E.5).

Appendix F An example satisfying Assumption 5.1

In this appendix, we prove that hyper-exponential Lévy processes with unbounded variation paths satisfies the assumptions that are necessary to apply our main result.

We assume that the Lévy measure is absolutely continuous with respect to the Lebesgue measure and has a density

| (F.1) |

where , and , , , and are sets of positive values satisfying

| (F.2) |

Then is called a hyper-exponential Lévy process. In addition, we assume that . Then has unbounded variation paths.

We have

| (F.3) |

and thus satisfies Assumption 2.1. By Corollary 2.4, satisfies Assumption 2.2. By [7, Remark 1, Theorem 1, 3 and 5], we have, for and a non-negative bounded measurable function ,

| (F.4) | ||||

| (F.5) | ||||

| (F.6) |

where , , and are values in , , , , , and are real values for , and

| (F.7) | ||||

| (F.8) |

Here, we assume that . By the strong Markov property at and , and from (F.4) and (F.6), we have

| (F.9) |

where

| (F.10) |

From the above equation and since the function is continuous on by the same proof as that of Lemma E.1, the function has the following density on with respect to the Lebesgue measure:

| (F.11) |

Thus, satisfies Assumption 5.1. Therefore, we can apply Theorem 5.2 for the hyper-exponential Lévy processes with unbounded variation paths.

Appendix G Proof of Lemma 5.4

We write , , and for . Then, the function belongs to (resp. ) when has bounded (resp. unbounded) variation paths and satisfies

| (G.1) | |||

| (G.2) | |||

| (G.3) |

We fix a strategy . Using the Meyer–Itô formula (see, e.g., [16, Theorem IV.70] (resp. [16, Theorem IV.71]) when has bounded (resp. unbounded) variation paths) for the process , we have, -a.s. with ,

| (G.4) | |||

| (G.5) | |||

| (G.6) |

where , is the standard Brownian motion, is the Poisson random measure on associated with ,

| (G.7) | ||||

| (G.8) |

and

| (G.9) |

Note that the process is a local martingale. By (G.1) and (G.2), we have, for ,

| (G.10) |

From (G.6) and (G.10), we have, -a.s. with ,

| (G.11) | ||||

| (G.12) | ||||

| (G.13) |

We take a localizing sequence of stopping times for . By taking the expectation using with at time and by (G.3) and (G.13), we have

| (G.14) | ||||

| (G.15) |

By taking the limit as and , we have

| (G.16) |

Since (G.16) is true for all , , and , by taking the limit as , the proof is complete.

Appendix H The proofs of the lemmas in Section 7

H.1 The proof of Lemma 7.2

We fix and such that , is càdlàg and the differential equation (2.10) has a unique solution for .

(i) We take with and prove that

| (H.1) |

We assume that . Then, we have

| (H.2) |

where

| (H.3) |

Thus, the map changes continuously. If for , then we have , where for , and for . Thus, we have for and

| (H.4) | ||||

| (H.5) |

which contradicts . Therefore, the inequality (H.1) is true.

We assume that . If for some , then we have for , and thus . By the definition of , on , it behaves as the Lévy process . Thus, the map is non-decreasing on , and we have and . However, since all negative jumps of and occur at the same time and have the same size, the above situation does not occur. Therefore, the inequality (H.1) is true.

(ii) We prove (7.4) when does not have positive jumps at . For , we have for . Below, we consider the convergence (7.4) after .

We assume that does not have positive jumps at and prove that

| (H.6) |

Here, note that exists by (i). If for some , then (H.6) is obvious by (i), so we only check cases where for all . We fix and , then there exists such that

| (H.7) |

There exists and such that . In fact, if it does not exist, then we have, by (H.1), (H.7) and the definition of ,

| (H.8) |

which contradicts that for . Thus, we have

| (H.9) |

where in the second inequality, we used (H.7). The inequalities (H.9) are true for , we have (H.6).

We assume that with , then we can define . If does not have negative jumps at , then we have , and for there exists such that and does not have jump at . Thus, we have

| (H.10) |

Since (H.10) is true for and by (i), we have (7.4). If has a negative jump at , then , and for there exists such that and does not have jump at . Thus, we have

| (H.11) |

The proof is complete.

H.2 The proof of Lemma 7.4

We fix and such that , is càdlàg and the differential equation (2.10) has a unique solution for .

(i) We assume that and prove that, for with ,

| (H.12) |

We define the stopping times and as follows: for ,

| (H.13) |

where . We prove (H.12) on and for , inductively. We assume that , , .

We assume that (H.12) is true for and prove that (H.12) on . On , behaves as the reflected Lévy process since it takes values in . Thus, we can regard as behaving the refracted–reflected Lévy process at with on . Therefore, by Lemma D.1 and D.3 and Remark D.2, we have , and for . Thus, we have and for Therefore, (H.12) is true on .

We assume that (H.12) is true for and prove that (H.12) on . After time , behaves as refracted Lévy process at with until it takes value . On the other hand, behaves as refracted Lévy process at with when and as reflected Lévy process at when until it takes value . By the above facts together with Lemma D.1 (2) and D.3, Remark D.2 and Lemma 7.2, we have , where is the refracted–reflected Lévy process at with satisfying , and thus for . In addition, by (3.3) and the above, we have, for ,

| (H.14) |

Therefore, (H.12) is true on .

We assume that (7.5) is true at when . Since behaves as on and by Lemma D.1 and D.3 and Remark D.2, we have, for and

| (H.15) | ||||

| (H.16) |

Only in this place we assume that . From the above and (3.3), the convergence (7.5) is true on . Since and by the same argument as that of (ii) of the proof of Lemma 7.2, we have for when does not have positive jumps at . In addition, and do not increases on . Thus, by (3.3), we have for when does not have positive jumps at . We also have by the same argument as above and since does not have positive jumps at , so we have and

| (H.17) | ||||

| (H.18) |

Therefore, by (3.3) and the above, we have and (7.5) is true on when does not have positive jumps.

(iii) We assume that and has bounded variation paths and non-negative drift. Under the condition above, we prove (H.12) for with .

If , we have for by [11, Section 3]. On the other hand, if , we have for by (2.16) and the facts that

| (H.19) |

By (2.16), (3.15), Lemma A.1, Remark A.3 and [11, Section 3], we have, for ,

| (H.20) | ||||

| (H.21) |

(iv) We give the same assumption as (iii) and prove (7.5) for a.e. . We can prove when does not have jump at by the similar argument as that of the proof of (H.6), thus we omit it. By (2.16), (3.15), Lemma A.1, Remark A.3, the monotone convergence theorem and [11, Section 3], we have, for ,

| (H.22) | ||||

| (H.23) |

Therefore, by (3.3), we have and also (7.5) when does not have positive jumps at .

The proof is complete.

References

- [1] S. Asmussen and M. Taksar. Controlled diffusion models for optimal dividend pay-out. Insurance Math. Econom., Vol. 20, No. 1, pp. 1–15, 1997.

- [2] E. V. Boguslavskaya. Optimization problems in financial mathematics: explicit solutions for diffusion models. Ph.D. Thesis, University of Amsterdam, 2006.

- [3] I. Czarna, J. L. Pérez, T. Rolski, and K. Yamazaki. Fluctuation theory for level-dependent Lévy risk processes. Stochastic Process. Appl., Vol. 129, No. 12, pp. 5406–5449, 2019.

- [4] H. U. Gerber and E. S. W. Shiu. On optimal dividend strategies in the compound Poisson model. N. Am. Actuar. J., Vol. 10, No. 3, p. 84, 2006.

- [5] D. Hernández-Hernández, J. L. Pérez, and K. Yamazaki. Optimality of refraction strategies for spectrally negative Lévy processes. SIAM J. Control Optim., Vol. 54, No. 3, pp. 1126–1156, 2016.

- [6] M. Jeanblanc-Picqué and A. N. Shiryaev. Optimization of the flow of dividends. Uspekhi Mat. Nauk, Vol. 50, No. 2(302), pp. 25–46, 1995.

- [7] A. Kuznetsov, A. E. Kyprianou, and J. C. Pardo. Meromorphic Lévy processes and their fluctuation identities. Ann. Appl. Probab., Vol. 22, No. 3, pp. 1101–1135, 2012.

- [8] A. E. Kyprianou. Fluctuations of Lévy processes with applications. Universitext. Springer, Heidelberg, second edition, 2014. Introductory lectures.

- [9] A. E. Kyprianou and R. L. Loeffen. Refracted Lévy processes. Ann. Inst. Henri Poincaré Probab. Stat., Vol. 46, No. 1, pp. 24–44, 2010.

- [10] A. E. Kyprianou, R. Loeffen, and J. L. Pérez. Optimal control with absolutely continuous strategies for spectrally negative Lévy processes. J. Appl. Probab., Vol. 49, No. 1, pp. 150–166, 2012.

- [11] K. Noba. On the optimality of double barrier strategies for Lévy processes. Stochastic Process. Appl., Vol. 131, pp. 73–102, 2021.

- [12] K. Noba and K. Yamazaki. On singular control for Lévy processes. Math. Oper. Res., Published Online, 2022.

- [13] J. L. Pérez and K. Yamazaki. Refraction-reflection strategies in the dual model. Astin Bull., Vol. 47, No. 1, pp. 199–238, 2017.

- [14] J. L. Pérez and K. Yamazaki. On the refracted-reflected spectrally negative Lévy processes. Stochastic Process. Appl., Vol. 128, No. 1, pp. 306–331, 2018.

- [15] J. L. Pérez, K. Yamazaki, and X. Yu. On the bail-out optimal dividend problem. J. Optim. Theory Appl., Vol. 179, No. 2, pp. 553–568, 2018.

- [16] P. E. Protter. Stochastic integration and differential equations, Vol. 21 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2005. Second edition. Version 2.1, Corrected third printing.

- [17] D. Revuz and M. Yor. Continuous martingales and Brownian motion, Vol. 293 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, third edition, 1999.

- [18] R. Situ. Theory of stochastic differential equations with jumps and applications. Mathematical and Analytical Techniques with Applications to Engineering. Springer, New York, 2005. Mathematical and analytical techniques with applications to engineering.

- [19] H. Tsukada. Pathwise uniqueness of stochastic differential equations driven by brownian motions and finite variation Lévy processes. Stochastics, pp. 1–20, 2021.

- [20] C. Yin, Y. Wen, and Y. Zhao. On the optimal dividend problem for a spectrally positive Lévy process. Astin Bull., Vol. 44, No. 3, pp. 635–651, 2014.