Scaling Blockchains: Can Committee-based Consensus Help?

Abstract

In the high-stakes race to develop more scalable blockchains, some platforms (Binance, Cosmos, EOS, TRON, etc.) have adopted committee-based consensus (CBC) protocols, whereby the blockchain’s record-keeping rights are entrusted to a committee of elected block producers. In theory, the smaller the committee, the faster the blockchain can reach consensus and the more it can scale. What’s less clear, is whether such protocols ensure that honest committees can be consistently elected, given blockchain users typically have limited information on who to vote for. We show that the approval voting mechanism underlying most CBC protocols is complex and can lead to intractable optimal voting strategies. We empirically characterize some simpler intuitive voting strategies that users tend to resort to in practice and prove that these nonetheless converge to optimality exponentially quickly in the number of voters. Exponential convergence ensures that despite its complexity, CBC exhibits robustness and has some efficiency advantages over more popular staked-weighted lottery protocols currently underlying many prominent blockchains such as Ethereum.

Keywords: Approval Voting, Blockchain Consensus Protocols, Blockchain Economics, Token Voting, Committee-Based Consensus, Delegated Proof of Stake, DPoS, Stake-Weighted Voting.

1 Introduction

Permissionless blockchains face a challenging problem: How can anonymous/untrusted decentralized agents all agree on a sequence of events, e.g., transactions, or more general state updates? The Bitcoin Whitepaper (Nakamoto 2008) introduced “Nakamoto Consensus”, a novel consensus protocol that allowed participants to reach agreement on the state of a distributed database in the absence of trust and stable identities, paving the way to a new form of decentralized money. Once Bitcoin’s success highlighted the value of blockchain technology, a high-stakes race ensued to design improved consensus mechanisms that could shore-up Bitcoin’s flaws – most notably low throughput/scalability, high economic and environmental costs, and delayed transaction finality (we expand on these in §A).

One suggested alternative with the potential to address the above is “Committee-based consensus”, whereby participants can delegate the chain’s record-keeping rights to a relatively small committee. The core idea is that smaller committees can reach consensus more efficiently, albeit, at the cost of less decentralization. Currently, several prominent blockchains including the Binance Smart Chain (BSC), Cosmos-based chains111Including the Cosmos Hub, crypto.com’s chain Cronos, Thorchain, Axelar, Osmosis, Secret and the defunct Terra blockchain among many others., Algorand, EOS, and TRON use this approach,222Note, blockchains like EOS, who raised a record-breaking $4 billion in its Initial Coin Offering in 2017, and Tron, define themselves as “Delegated Proof of Stake” systems, but this branding has become tarnished by the criticisms of their technical design (The Interchain Foundation 2017, Xu et al. 2018) and some of their business behavior (Copeland 2020, Rubin 2021, Hui 2020). It is important to note that these criticisms do not undermine the core ideas of committee-based consensus, as evidenced by the fact that more prominent blockchains (like Cosmos) rely on it as well. though, importantly, they differ in how the committee members are chosen.

Despite the prevalence of committee-based consensus protocols in practice, they have received relatively little attention in the academic literature so far. In particular, the question of how participants of blockchain systems, who typically have limited and dispersed information, can optimally choose/elect effective and trustworthy committees to maintain the state of the chain is of critical importance, and is not well understood. This work seeks to shed some light on this issue.

Before diving into further details, we first provide a brief overview of some common consensus protocols, comparing single-leader vs. committee-based approaches.

Single-leader vs. committee-based consensus protocols

Bitcoin’s implementation of Nakamoto consensus relies on single-leader consensus protocol termed “Proof of Work” (PoW). In PoW, blockchain users can compete with each other by engaging in “wasteful” computations, for the chance of being selected “block leader.” If selected, they have the right to append a block of transactions to the blockchain, and reap any rewards that come with it. The more computing (hash) power participants have, the higher their odds of selection. This incentive structure, in turn, has lead to an arms race to invest in specialized computing hardware (ASICs), which have little value outside of PoW mining.

One desirable feature of PoW’s wasteful computation is that it affords Sybil resistance333A Sybil attack involves creating a large number of pseudonymous accounts in an attempt to seize control of the network. by imposing a cost to enter the block-producer “lottery.” However, less wasteful alternatives exist: Nakamoto consensus can also be implemented using Proof-of-Stake (PoS), and early PoS protocols like Nxt (Nxt Community 2016) were essentially PoS-based versions of Nakamoto consensus, where the chance of being selected as block leader is proportional to one’s token stake, rather than one’s computing power.

Blockchain platforms are increasingly gravitating towards PoS-based consensus as this mechanism is generally believed to be more scalable and less wasteful than PoW (John et al. 2020). Nonetheless, the way PoS is currently implemented on many blockchains maintains the single-leader design philosophy of Bitcoin’s original PoW, and it is therefore prone to some of the very same shortcommings. In addition to questions surrounding bandwidth limitations, single-leader protocols generally suffer from lack of “instant finality”: transactions aren’t considered “final” until several successive blocks have been appended to the chain, meaning, their internal states can only reach eventual consistency. In practice, these chains can and do “fork” unpredictably, creating conflicting versions of message history, for instance, when two producers independently produce blocks at around the same time, or when a malicious producer purposely produces multiple conflicting blocks.444It should be noted that forking frequency on PoW and PoS can be quite different in practice. For instance, Ethereum (PoS) sees hundreds of (short-term) forks every day (Etherscan 2022). By contrast, Bitcoin (PoW) sees fewer than one fork per month (Lovejoy 2020).

Committee-based consensus protocols have the potential to address some of the issues raised by replacing the “single-block-producer” leader model in Nakamoto consensus, with one that relies on the formation of dynamic committees who write blocks with near-instant finality (assuming consensus is reached quickly within the committee itself).555 When the committee is static, the blockchain is said to be “permissioned.” In this work, we focus solely on the permissionless setting, where the committee changes dynamically. At its core, (elected) committee-based consensus is rather simple: users continuously vote to elect their preferred block producers to the committee. Keeping the committee size small improves efficiency: increasing throughput, decreasing latency and allowing for member specialization. Unfortunately, a small number of malicious committee members can also undermine the security of the entire blockchain, thus there is a fundamental tension between performance and robustness – a small committee is extremely efficient but is more centralized, and may compromise security.

Committee-based consensus designs in practice

There is some variation in the design of committee-based consensus protocols in practice, and in particular, on the question of how committee members should be optimally chosen. We outline below three of the most popular implemented designs in prominent blockchains:

-

•

Lottery: Algorand committees are not elected by users, but rather chosen randomly via a stake-weighted lottery.

-

•

Single-choice voting: Most Cosmos-based chains, including the Cosmos Hub, Cronos, Thorchain, Axelar, Osmosis and Secret, use single-choice elections to elect a committee, i.e., each user can only vote for a single candidate. As do Tron and the Binance Smart Chain.

-

•

Approval voting: EOS (which raised a record breaking $4 Billion in its ICO in 2017) as well as its forks like Telos use a more general voting mechanism termed “approval voting” where voters can approve a collection of candidates rather than focusing their voting power on a single one.

All of these blockchains (Algorand, BSC, Cosmos, EOS, Tron etc) may differ widely in their features – they have different tokenomics, different virtual machines and their committees run different consensus algorithms. Nonetheless, the method for selecting committees can be largely divorced from the other features of the system, making it amenable to independent study. Of the three designs above, approval voting is the most general. In fact, we later argue that the other two designs can be thought of special (simple) cases of approval voting. We therefore focus the bulk of our attention in this paper on studying approval voting for electing committees in committee-based consensus protocols.

Research Questions

Several interrelated questions follow: First, how should agents vote for their preferred candidates given they only have partial information? Second, how small can the committee be without undermining security? Third, how does committee-based consensus with approval voting compare to the other two common protocols mentioned above?

Summary of Model

To answer these questions, we develop an approval voting model under partial information. Block producers can be one of two types, either “honest” or “dishonest,” and the vote succeeds if a fraction of the elected committee is honest. This is in line with the analysis of most consensus protocols (like those used in Cosmos, Algorand and EOS) where participants are either honest or “byzantine,” and the consensus protocol exhibits a strict phase transition when the number of byzantine participants exceeds a given threshold — usually rds.

Token holders are tasked to elect block producers into a committee, but the voters have limited information about the candidates: they receive private signals about the type of each candidate block producer and vote strategically to try and maximize the probability of electing an honest committee. The election process is based on a variation of approval voting, whereby voters approve of a collection of candidates, and the candidates with the most approvals are elected to the committee (Brams and Fishburn 2007). As we will discuss later, this is fundamentally different from traditional voting schemes, where voting for more than one candidate means splitting your vote.

Assuming the block producer committee uses a traditional consensus protocol to certify blocks, such as Practical Byzantine Fault Tolerance (Castro and Liskov 1999), this imposes a strict threshold effect on the committee: if fewer than rd of the committee members are dishonest ( in our terminology), they cannot disrupt the consensus protocol, but once more than rd of the committee members are dishonest, they can completely subvert the committee (which can result in halting transactions, or executing double-spend attacks).

We seek to characterize agent optimal voting strategies under these conditions. Further, guided by some stylized facts emerging from our basic empirical observations, we also consider a restriction of the voting strategy space to two simple and intuitive classes: “threshold voting,” where voters vote for all candidates whose (conditional) probability of being honest is above a certain threshold (Definition 5), and “cardinal voting,” where voters vote for their top candidates (Definition 6).

Summary of Results

Even with this relatively simple model, computing the probability of electing an honest committee turns out to be challenging. In Theorem 2, we derive this probability in the most general terms, allowing for specialization to various voting strategy classes. We then proceed to examine the success probabilities for the two, intuitive, voting strategy classes we consider.

We first analyze a special case where there is only a single voter, and show that it is (mathematically) equivalent to a setting in which all voters can credibly (and costlessly) pool their information. Pooling of information is often regarded as a pure hypothetical exercise, but it is worth studying in our setting because voter incentives are aligned, and there is no obvious downside to sharing one’s information with others. Under these conditions, we show that the cardinal voting strategy is in fact the optimal strategy (Proposition 2). But this result breaks down when there is more than one voter, if signals cannot be shared (Proposition 5).

Proposition 1 gives a closed-form solution for the the probability of electing an honest committee when voters follow the threshold strategy. But threshold voting can be suboptimal even when there is just a single voter Proposition 3).

Despite the general suboptimality of these simple strategies (other than in the special signal pooling case), we show that the system is surprisingly asymptotically stable. More specifically, regardless of the strategy considered, and under relatively weak assumptions, the probability of electing an honest committee tends to one, exponentially fast, as the number of voters increases (Theorem 3). Thus, although the optimal voting strategy may be too complex to be realistically achievable, simple, intuitive voting strategies, that token holders tend to use in practice, exhibit very strong robustness.

Finally, to address the aforementioned tradeoff between efficiency and blockchain security, we compare the approval-voting mechanism for committee selection to two other popular mechanisms: single-choice voting, and lottery selection. We find that approval voting typically requires much smaller committee sizes (1 to 2 orders of magnitude) to attain the same levels of security (defined as failure tolerance).

Overall, our results suggest that for most practical purposes, committee-based consensus is efficient and robust to the complexity it introduces on the agent strategy space, as long as enough voters are participating in the system. Some limitations are discussed in Section 7.

In the appendix, Section A, we discuss in more depth, some of the basics of blockchain consensus protocols and the approval voting mechanism that we model. Readers already familiar with these concepts can skip the section, or its relevant parts, without loss.

2 Literature Review

Committee-based consensus is widely used in the blockchain space (Kogias et al. 2016, Meng et al. 2018, Gleehokie et al. 2018, TRON 2018, Cosmos 2021), but the academic literature is arguably still lagging behind. Of the few studies we could find, Meng et al. (2018), Yang et al. (2019), Hu et al. (2021) examine related topics, but they focus mostly on hypothetical tweaks that could be added to improve existing systems. In contrast, we seek to formally analyze and understand whether the existing systems themselves are robust and efficient, given voters have limited information.

Approval voting was introduced into the blockchain space in Delegated Proof of Stake (DPoS), and the first literature on DPoS started with practitioners, where it was often asserted that DPoS consensus is a more efficient and democratic version of the standard PoS mechanism (Binance 2020, Cryptopedia 2021). The approval voting mechanism underlying DPoS is described in the original whitepaper, Bitshares (2021), but there is little attempt to assess potential agent voting behavior and what could go wrong with it.

Approval voting has been widely studied in the context of political elections (Brams and Fishburn 2007), and we highlight here some facts about the known dynamics of approval voting in general. In a -winner election system, it is desirable to have the property that if a candidate is ranked first by at least of the voters, then that candidate should be elected to the committee. Unfortunately, this property does not hold under approval voting (Elkind et al. 2017).

Similarly, an approval voting scheme can end up electing candidates that would lose a majority of pairwise contests against the other candidates, i.e., an approval voting scheme may elect a “Condorcet loser” (Niemi 1984).

One of the most interesting features of approval voting schemes is that voters typically have multiple honest strategies (Niemi 1984). For example, consider an up-to-, -winner system with two voters (), and four candidates (), . If the two voters’ preference orders are for voter and for voter then the candidate will be in the elected committee for any , so both and cannot be in the elected committee. Should voter vote for only, or and ? These are both honest strategies, and thus even honest players must think strategically. This feature makes the analysis of approval voting systems complex.

Committee-based consensus mechanisms that use approval voting inherit these aforementioned properties, but differ from traditional approval voting in several ways that we describe in the model section. The most significant departure is perhaps that extant studies (outside of the blockchain literature) assume voters have competing interests, and usually have perfect information about the candidates themselves. By contrast, in the blockchain protocol setting, voter interests can be more aligned. All voters wish to elect an honest committee, but they have limited information about the candidates. This completely changes the nature of the analysis.

Though we are not aware of any studies considering strategic agent voting behavior in committee-based protocols, numerous studies have looked at strategic agent behavior in other Blockchain protocols. Saleh (2021), Roşu and Saleh (2021), Fanti et al. (2019) are some of the first studies looking at the economics of PoS systems. Leonardos et al. (2020) study weighted voting in validator committees in PoS protocols. There is also a relatively large computer science literature blending strategic considerations and technical design elements of PoS, such as Gaži et al. (2019), Chen and Micali (2016), Bentov et al. (2016), Kiayias et al. (2017).

Beyond PoS, Alsabah and Capponi (2020), Biais et al. (2019), Cong et al. (2021a), Garratt and van Oordt (2020) focus on the economics of PoW, and the underlying mining mechanism. Several other studies focus more specifically on Bitcoin, such as Nakamoto (2008), Easley et al. (2019), Huberman et al. (2021), Pagnotta (2021), Prat and Walter (2021).

Other works have considered consensus in the presence of three types of participants byzantine, altruistic and rational Aiyer et al. (2005), or just byzantine and rational Amoussou-Guenou et al. (2020). In the byzantine-rational model of consensus Amoussou-Guenou et al. (2020), there are still two types of participants, and there is still a phase transition when the number of byzantine participants exceeds a certain threshold, thus our analyses applies almost equally in this setting as well.

Finally, on a broader note, our work is related to the literature studying security guarantees for different types of blockchain protocols, e.g., Lewis-Pye and Roughgarden (2020, 2021), though we are not aware of any prior work focused specifically on committee-based consensus. More generally, our work also has implications for the literature studying the economics of token systems, see e.g., Cong et al. (2021b), Tsoukalas and Falk (2020), Gan et al. (2021a, b).

To the best of our knowledge, ours is the first paper to analyze the efficiency of committee elections in committee-based consensus protocols, with private information and strategic voters.

3 Preliminaries and Empirical Observations

3.1 Definitions

Approval voting is a system where each voter may select (“approve”) any number of candidates, and the winners are the candidates approved by the largest number of voters (see Kilgour (2010) for a survey on approval voting). Formally:

Definition 1 (-winner Approval Voting).

A set of voters votes on a set of candidates, . Let , and . Voter chooses a subset of candidates they wish to vote for. For each candidate , the score of candidate , that is, the number of votes the candidate receives, is defined to be

| (1) |

The elected committee is determined to be the candidates with the highest scores.

In blockchain settings, stake-holders typically vote for a set of “block-producers” modifying the k-winner Approval Voting system to include a cap on the number of candidates. Formally:

Definition 2 (up-to--vote, -winner Approval Voting).

With notation as in definition 1, we limit the maximum number of candidates each voter can vote for, so that voter chooses a subset of candidates restricted to . As before, the elected committee is determined to be the candidates with the highest scores.

We will assume throughout that there are at least candidates, . In general, there may be less than candidates in the elected committee if less than candidates received any votes. Alternatively, there may be more than candidates if there are ties. We specify how we handle these cases in Definition 3.

3.2 Empirical Observations: Approval Voting on EOS

Block Producers on EOS are elected by token holders according to a up-to--vote, -winner approval voting system (see Definition 2, with and ). The winning candidates form the block producer committee. Elections are held continuously, and each committee of block producers remains in control of the chain for 126 seconds (EOS 2018).

EOS voters are not directly rewarded for staking (although this has been proposed as in NY (2019)), instead voters are assumed to benefit indirectly from the stability and performance of the platform. In EOS and other DPoS systems, votes are weighted by stake, and voters are allowed to “proxy” their votes, i.e., delegate their voting power to a different voter.

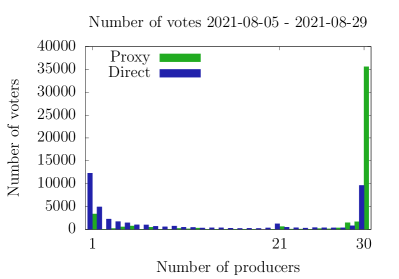

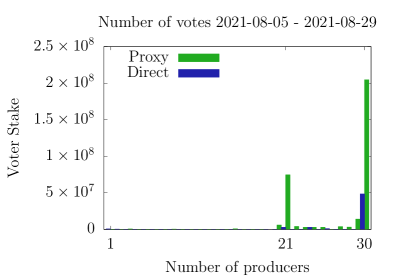

To understand the actual voting strategies employed by users, we extracted voting data from EOS. As the EOS blockchain is extremely large (over 8TB) and the majority of transactions are unrelated to voting, we gathered daily voting snapshots from EOS Authority (a block producer) and we used these to analyze voter behavior during the period 2021-08-05 - 2021-08-29 (the findings are consistent and exhibit relatively little variability, over different/longer time windows). Each snapshot contained the current votes of the nearly 1 million accounts that have ever voted.

Figure 1 shows the number of votes cast by individual voters (left panel), and stake-weighted votes (right panel), on a typical day.

The key observation is that most voters follow a “cardinal voting strategy” where they vote for a fixed number of block producers, either 1, 21 or 30. A formal definition of “cardinal voting” is given in Definition 6.

4 Model

4.1 Approval Voting with Limited Information

We lay out a simple model, where the blockchain’s token holders vote according to an up-to-, -winner approval voting system (Definition 2), to elect a committee of block producers. There is a pool of candidates to choose from, , and strategic voters on the platform, . Every producer has an unknown type, either “honest”, , or “malicious”, . The goal of each voter is to maximize the probability that a supermajority (e.g. a -majority) of the elected committee is honest. We discuss some possible alternative objectives in Appendix E.

Definition 3 (Honest Committee).

Suppose the producers with highest number of votes are elected to be on the block-producer committee, . If there are less than candidates with non-zero score, then the committee is filled adversarially (i.e., in a worst-case fashion), and if there are ties between the candidates such that there are more than producers with highest score, then they are broken adversarially (between the ones with least score). Since most Byzantine Agreement protocols require at least honest members, we say the committee is honest, , if at least of the elected block producers are honest.

Suppose the a priori probability that producer is honest is . Also, suppose voter receives a private noisy signal vector, about producer’s honesty,

| (2) |

where is a normally distributed noise term with and , i.e., ,. It follows that signals are normally distributed with if producer is honest, and if producer is malicious.

We assume that , are publicly visible, but voters cannot observe others’ private signals.

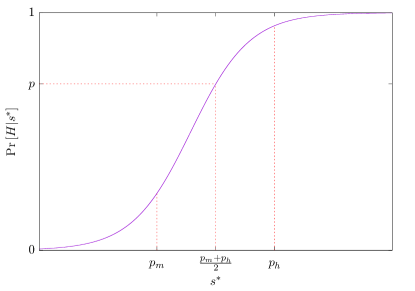

When voter receives a signal, , regarding producer , the voter can compute the posterior probability that producer is honest conditioned on :

| (3) |

The map is a bijective function, and we calculate it explicitly in Lemma 2 in Appendix B.1. The result is given below in (4).

| (4) |

After observing their private signal, voters simultaneously submit their “votes” ; we consider any voting strategy in the class of voting strategies, represented by the letter .

Voter ’s payoff is given by if the elected committee is honest () and otherwise. We assume voting has some unit cost, (the opportunity cost of staking one unit of capital).

Voter ’s objective is to maximize their utility given by

| (5) |

With exogenous and , this objective simplifies to maximizing the success probability — the probability that the elected committee is honest, conditioned on the private signal vector a user receives, , given the platform voting system in Definition 2. Formally:

| (6) |

Definition 4 (Voting Strategy).

A voting strategy is an algorithm used by voters, that takes as input the parameters the voter has access to and outputs a subset of candidates the voter wishes to vote for . We denote the committee elected by exerting algorithm as .

With Definition 4, we can interchangeably talk about the voters maximizing the success probability by exerting a voting algorithm and rewrite Equation 6 as:

| (7) |

We say that a strategy is optimal if it maximizes the success probability - the probability of electing an honest committee, Equation 6 or 7. Table 1 summarizes the notation.

| Number of (candidate) block producers | |

|---|---|

| Number of voters | |

| A priori probability block producer candidate is honest | |

| The base signal for a malicious candidate producer | |

| The base signal for an honest candidate producer | |

| Standard deviation of the noise, for voter , and producer | |

| Elected Committee size | |

| Voter ’s raw signal about producer | |

| Producer ’s posterior probability of being honest, conditioned on . |

While voters’ optimization problem is well-defined, computing the objective function is challenging. As a first step, we need to define the types of voting strategies that are accessible to agents. This is the objective of the next section.

4.2 Class of Voting Strategies

In principle, any function is a possible voting strategy. It seems clear, however, that any reasonable strategy should be coordinate-wise non-decreasing, i.e., if and , and if then . In other words, if one candidate’s signal increases (while the other signals remain the same) this cannot cause the voter to switch their vote away from the candidate. We refer to this class as the “general class” of voting strategies (previously referred to as class ).

Within this this general class, we also consider in our analysis two particularly simple and intuitive strategies related to our empirical observations: threshold voting (Definition 5) and cardinal voting (Definition 6).

Definition 5 (Threshold Voting).

Voter is said to follow the “threshold” voting strategy if they choose a threshold and vote for all producers , with posterior probability higher than this threshold, formally: .

If we define , then is the probability that voter votes for producer (assuming voter is following the threshold voting strategy). Summing over all voters, the number of votes received by producer is distributed as the sum of Bernoulli random variables with parameters . If , then the number of votes received by producer is a binomial random variable. When the are distinct, then the number of votes received by producer is a Poisson Binomial Random Variable. See Appendix C for a review of useful properties of the Poisson Binomial Distribution.

This characterization of the distribution of votes when voters follow the threshold voting strategy will be important as we study the dynamics of this strategy in Section 5.

Definition 6 (Cardinal Voting).

Voter is said to follow the “cardinal” voting strategy if they choose to vote for the top producers with the highest posterior probabilities of being honest .

When voters follow the cardinal voting strategy, the number of votes received by each producer is still distributed as a Poisson Binomial random variable, but now the parameters (the probability that voter votes for candidate ) are much more challenging to compute, as we will discuss in the analysis.

5 Analysis

We begin our analysis by characterizing the probability of electing an honest committee in the most general terms possible (Section 5.1) and unveiling some associated complexities (Section 5.2). We then examine outcomes in a simplified single-voter/signal pooling setting which helps build intuition (Section 5.3), before looking at the general multi-voter case (Section 5.4). The preliminary results obtained hint at possible asymptotic optimality, which is formally analyzed in Section 5.5. Finally, we compare approval voting committee-based consensus to other PoS-based mechanisms (Section 6).

5.1 The Probability of Electing an Honest Committee

The voters’ goal is to vote in such a way that the probability of electing an honest committee (Definition 4) is maximized. Before we can maximize this probability, however, we must calculate the probability of electing an honest committee for a fixed set of strategies. Computing this probability is quite complex, and we break it down into a series of manageable steps. For exposition, we also focus primarily in the text on threshold voting, and leave the cardinal voting analysis for the Appendix.

-

1.

Section 5.1.1: Probability that a user votes for an honest candidate: First, we calculate the probability that an honest candidate receives a vote from voter . Proposition 3 calculates this probability when voters follow the threshold voting strategy, and Proposition 6 calculates this probability when voters follow the cardinal voting strategy.

- 2.

-

3.

Section 5.1.3: (Aggregate) Probability of selecting an honest committee: Once we have the density function of votes for both honest and dishonest producers, we can calculate the probability that a -fraction of the elected committee is honest. Theorem 2 calculates this probability in closed-form, when voters follow the threshold voting strategy. In Appendix G, we outline how to adapt Theorem 2 to the cardinal-voting setting.

Remark 1 (Voter precision).

Throughout this section, we assume that producers are indistinguishable except for their type, meaning, the variance of the noise , for in Equation 2. This implies there is a single pdf, that denotes the probability an honest producer receives votes. This simplification is done purely for expositional purposes; to obtain the result for the more general case, one would need to replace Theorem 9 (used in the proof of Theorem 2) by the more general Bapat-Beg Theorem (Bapat and Beg 1989). The resulting expression remains closed-form, but is too cumbersome for display.

5.1.1 Probability of voting for an honest candidate

When voters follow the threshold or cardinal voting strategy, we can compute the probability (resp. ) which is the probability that an honest (reps. malicious) candidate receives a vote from voter . Proposition 1 gives the probabilities when voters follow the threshold voting strategy.

Proposition 1 (Threshold voting).

For a producer , let (resp. ) denote the probability that voter casts a vote for producer conditioned on producer being honest (resp. dishonest).

5.1.2 Distribution of votes

Propositions 1 and 6 give the probabilities and that voter votes for honest, or dishonest candidates.

Note that for a given candidate, , once we condition on the candidate’s type (either honest or dishonest), the events that voter and voter vote for candidate become independent. This means that the number of votes received by each type of candidate is distributed according as a Poisson Binomial Random variable. Theorem 1 gives the general form of the distribution of votes () received by honest and dishonest producers in terms of the probabilities (, that voter casts a vote for producer .

Theorem 1 (Distribution of Votes).

For a producer, , let (resp. ) denote the probability that voter casts a vote for producer conditioned on producer being honest (resp. dishonest). Then the probability distribution of the number of votes received for honest and dishonest producers is given by

| (10) | ||||

| (11) |

where is the set of all subsets of integers that can be selected from .

5.1.3 Probability of electing an honest committee

The final step in this analysis is to compute the probability that a -fraction of the committee is honest. Notice that when voters follow the threshold voting strategy, for a given voter, , and distinct candidates and , the probability that votes for and are independent events. This allows us to prove Theorem 2, which gives an analytic representation of the probability of electing an honest committee in the threshold voting setting.

Theorem 2 (Success Probability (threshold voting)).

Suppose there are producers, and each producer is honest independently with probability . If the number of votes received by each candidate are independent random variables then the probability that there are at least honest producers in a committee of size , is given by:

| (12) |

where are the PDF and CDF of the number of votes received by an honest producer, and are the PDF and CDF of the number of votes received by a dishonest producer.

In the cardinal voting setting, it is possible to prove an analog of Theorem 2. The exact formula is significantly more complicated, however, because the events that voter votes for candidate and candidate are no longer independent (they are now negatively correlated). In Appendix G, we outline how to adapt Theorem 2 to the cardinal-voting setting.

5.2 The Complexity of Approval Voting

We focus here (without loss) on threshold voting. Similar results hold in case of cardinal voting.

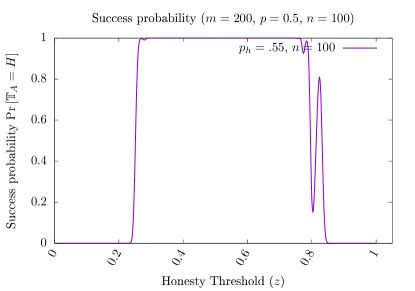

Finding the optimal voting strategy requires maximizing the objective function given by Theorem 2. Unfortunately, this objective function is complex, and this makes the voters’ general optimization problem in (7) challenging. To understand the origin of this complexity, we visualize in Figure 2 the objective function, that is, the probability of electing an honest committee.

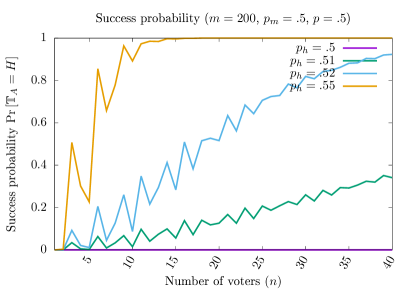

Suppose for now that all voters follow a threshold voting strategy, with some common threshold, . In this setting, we can calculate the exact probability of success as a function of the threshold chosen. Figure 2 shows the success probability under threshold voting, for small numbers of voters ( to ). Although, in practice, systems have many more voters, these graphs highlight some of the complex dynamics of approval voting.

The optimal thresholds tend to hover around , meaning that with these parameters, voters should vote for any candidate, , whose posterior probability, , is above this threshold and not vote for any candidate below this threshold. The thinness of the peaks, however, indicates that even small deviations from the optimal strategy can drastically reduce the success probability. In addition, the number of local optima appears to increase with . These properties make the general optimization problem intractable at relatively low or medium values of (with the exception of , for which the objective is unimodal).

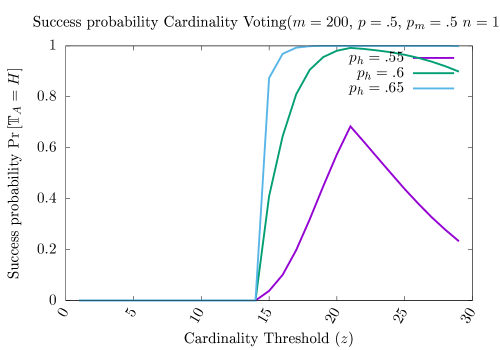

Next, we examine the situation for a large number of voters , in Figure 3.

Figure 3 shows that for large , the previous issues fade: the local optima tend to merge, and almost any reasonable threshold has a close to 100% probability of success.

Combining insights from Figures 2 and 3, we conclude that the voters’ problem behaves drastically differently depending on low vs. high-number of voters, and hints that asymptotic analysis may offer more tractable results.

Next, we analytically characterize (to the extent possible) the optimality of voting strategies, separating the case from the general case.

5.3 Special Case: Equivalence between & with Signal Pooling

In this section we consider the special case of a single voter (). Beyond letting us build intuition, we show that the general case, collapses to when voters are allowed to credibly (and costlessly) share their signals. This is more than a mere hypothetical exercise. Signal pooling has no obvious downside in our setting given voter incentives are aligned, and thus could be plausible in practice.

Single Voter

Before presenting the result, we introduce one intermediate technical lemma that will be useful throughout the analysis.

Lemma 1.

Suppose is a Poisson Binomial random variable with trials and let with denote the Poisson Binomial with parameters . Let , and be positive integers, such that then .

To understand the implication of Lemma 1, consider a -winner approval voting system in which candidates have posterior probabilities of being honest . Suppose the subset of candidates elected to the committee is so that their posterior probabilities are . If we think about the realization of honesty of each candidate as a trial with probability then the number of honest candidates on the committee is a Poisson Binomial with parameters . The success probability, e.g. the probability of an honest committee is the probability that the number of honest candidates on the committee is at least . Lemma 1 implies that the success probability is maximized when each of the posterior probabilities of the different candidates is as high as it can be.

Proposition 2 (Optimality of Cardinal voting when ).

Consider a -winner approval voting system with voter and candidates, then the globally optimal strategy is the cardinal strategy with .

Proposition 2 follows from the fact that if there is only a single voter, that voter possesses all relevant information about each producer’s type, and the voter can unilaterally decide the committee. Thus the optimal strategy is to form the committee from the candidates that have the highest (posterior) probability of being honest. In other words, the voter should vote for the top candidates (when sorted accorded to their posterior probability of being honest), and this strategy is optimal across all possible strategies, not just cardinal or threshold voting.

Proposition 3 (Suboptimality of Threshold voting when ).

Consider a -winner approval voting system with voter and candidates, then any threshold strategy is not optimal.

More specifically, when we say a strategy is not optimal we mean that there is a non-zero probability event (realization of signals) in which the non-optimal strategy achieves a success probability that is strictly smaller than would be achieved using a different strategy .

| (13) |

In particular, in the proof of Proposition 3 we show Equation (13) is true for and . In other words, we show that for the threshold strategy gives a strictly lower success probability than the cardinal strategy.

Signal Pooling

If voters could credibly (and costlessly) share their private signals, then it is straightforward to show that they effectively act as a single voter.

As in the private signal setting, each voter can calculate the probability that a given producer is honest, conditioned on the received signals. But now, we assume voters can condition on all the signals. We calculate the resulting posterior probability in Lemma 3 in Appendix B.1.

Proposition 4 shows that when voters share their signal, the optimal strategy (out of all possible strategies) is to follow the cardinal voting strategy with threshold .

Proposition 4 (Optimality of Cardinal Voting with Shared Signals).

Consider a -winner approval voting system with voters, candidates and such that voters’ private signals are credibly shared. Then the globally optimal strategy is the cardinal voting strategy with where each voter is ranking based on the shared instead of their private .

A natural question that follows is, whether cardinal voting persists to be the optimal strategy in the general multi-voter case. We examine this in the next section.

5.4 General Case: Multiple Voters

Given we show in the previous Section 5.3 that the threshold strategy is already suboptimal for , while the cardinal strategy is in fact optimal for , we focus our attention here on the latter.

In the multi-voter setting (), the optimal cardinal strategy becomes extremely complex and even computing the exact success probability for a fixed strategy is difficult. Despite this, we can formally show that the cardinal strategy that was always optimal with may become suboptimal with .

Proposition 5 (Suboptimality of Cardinal voting when ).

Consider a -winner Approval Voting system with voter and candidates, then the cardinal strategy can be suboptimal.

Intuitively, this result occurs because a vote for a candidate can actually bump other candidates out of the committee. To dig deeper, consider a situation with two voters (voter and voter ), where voter has better information than voter , (i.e., for all ). Even if is large, voter ’s signals convey information (a single voter who had access to the signals and would do better than one with access to alone). The problem is that voter 1 can only convey information about their signal through discrete votes, and a vote for candidate may be too strong an endorsement for that candidate given that the signal is only weakly informative.

As an extreme case, consider a situation where voter is perfectly informed (i.e., voter can differentiate between honest and dishonest producers with probability 1), and voter is perfectly uninformed (i.e., from voter ’s perspective, each candidate is honest independently with probability , in other words for all ). In this case, it should be clear that voter should not cast any votes, while voter should cast votes.

The suboptimality of the cardinal voting strategy persists even if both voters have the same information (i.e., for ). This is because the realized signals can convey different amounts of information. For example, suppose voter ’s sorted signals are and voter ’s sorted signals are . Suppose as well that , but . In this case, voter has high confidence that the committee should consist of the candidates , but voter is essentially indifferent between candidates . The cardinality strategy with threshold would force voter 1 to vote for and , but not , and this vote (based on little information) could displace committee members who would have been elected by voter (whose signals were very informative).

5.5 Asymptotic Optimality (Main Result)

So far, we have established via Proposition 3, that the threshold strategy is suboptimal, and via Proposition 5, that the cardinality strategy may be suboptimal. However, our basic numerical study in Section 5.2 suggests that as the number of voters increases, the optimality gap may decrease.

Theorem 3 (Exponential Convergence (Main Result)).

Let denote the set of dishonest producers, and suppose there exists a set of honest producers, , with , and a such that where denotes the probability that voter votes for producer . Then the probability of electing an honest committee is bounded from below and tends to 1 as increases, in particular, we have

| (14) |

Theorem 3 shows that as the number of voters, , tends to infinity, then the probability of electing an honest committee tends to 1, exponentially quickly, as long as the signals are not completely uninformative, that is, as long as there exists an arbitrarily small gap s.t. when is honest and is dishonest. The lower bound on the success probability decreases quadratically in the number of block producer candidates , because if there are too many block producers relative to the number of voters, no single block producer can amass enough votes to make it onto the committee with high probability. As long as there are not too many candidates, however, the exponential dependence on the number of voters dominates the quadratic dependence on the number of producer candidates. Importantly, this result holds across all voting strategy classes, and this leads to the following two corollaries.

Corollary 1.

If , and , then the probability of an honest committee when all voters follow the Threshold strategy converges to as (assuming ).

Corollary 2.

If , and , then the probability of an honest committee when all voters follow the Cardinality strategy converges to as (assuming ).

Remark 2.

Since is the number of producers, and is the a priori probability a candidate is honest, the number of honest candidates is distributed as , and the expected number of honest candidates is . If the number of honest candidates is less than , then there is no way to elect honest producers. The assumption that ensures that the probability there are fewer than honest candidates is small.

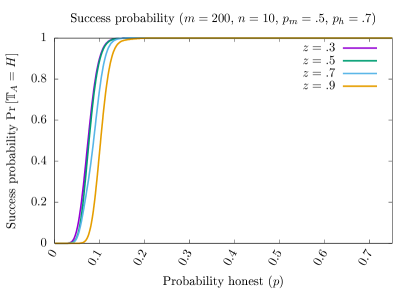

Figure 5 illustrates the exponential convergence result, assuming each voter follows a (generally suboptimal) Threshold Voting strategy (Definition 5) with . The figure shows that even with relatively weak signals, the probability of success rapidly converges to 100%.

Note, convergence to optimality also holds (more trivially) for other asymptotics of interest, such as if the signal informativeness or if the prior . See Appendix F for an illustration.

6 Efficiency vs .Security: Comparison of Consensus Protocols

In this section, we compare the approval voting mechanism analyzed in §5, to two other popular mechanisms implemented in practice: single-choice voting (e.g., Cosmos and Binance Smart Chain), and lottery based (e.g., Algorand).

6.1 Single-Choice Voting (e.g., Cosmos, Binance, etc.)

Most blockchains built on the Cosmos SDK employ single-choice committee-based election, and the elected committee runs the Tendermint consensus protocol (which requires a fraction of honest participants). This is the voting mechanism used by the Cosmos Hub, crypto.org, Osmosis, Secret, Oasis, Binance Chain etc. It is also the mechanism used by Tron and the Binance Smart Chain.

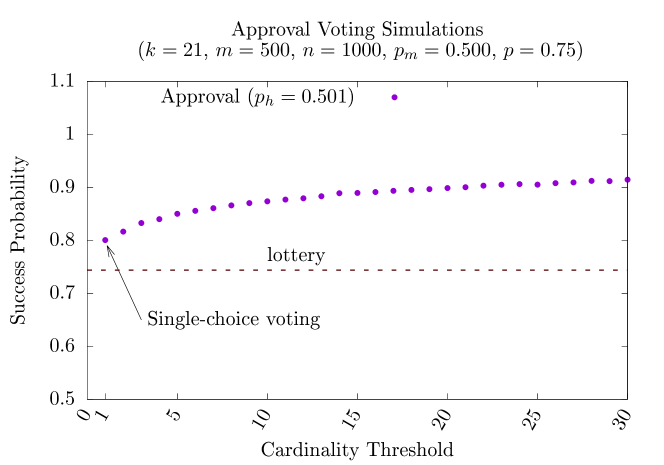

Mathematically, the single-choice setting is equivalent to our cardinal voting setting where voters would be required to set their cardinality threshold . In this case, each voter’s optimal strategy is intuitive: vote for the candidate that is most likely to be honest, i.e., voter votes for candidate where is maximized. Despite this, one cannot directly apply Theorem 2 to recover the closed-form aggregate success probability, because the number of votes received by each candidate are not independent variables (if voter votes for candidate , voter does not vote for candidate ). We therefore analyze this protocol numerically focusing on the following question: how does the restriction affect the protocol’s success probability (compared to setting a different global threshold )?

Figure 6 shows how the probability of electing an honest committee differs when voters follow a cardinal voting strategies with different thresholds, . The key observation is that when voters vote for only a single voter, , the success probability is minimized, that is, the single-choice restriction constitutes the worst possible cardinal voting strategy.

By contrast, in more general approval voting systems (e.g. EOS, Telos), even if voters choose their threshold suboptimally, they are essentially guaranteed to have higher success probabilities than in the single-choice setting.

The lottery protocol which bypasses voting in favor of random selection (e.g., Ethereum) is represented by the dashed line. We assume (i.e., each candidate has a 75% chance of being honest) and the committee size is 21.

6.2 Lottery-based committees (e.g., Algorand)

Algorand employs committee-based consensus, but uses a randomly selected committee to certify each block. In order to ensure that the Algorand protocol never forks, the protocol must never elect a dishonest committee.

The analysis of the Algorand protocol proceeds as follows. Suppose some fraction, , of the tokens are held by honest participants (i.e., , an elected committee member is honest with probability ) then if a committee of size is randomly selected, then the probability the committee is at least rds honest is

| (15) |

A Chernoff bound (e.g. Dubhashi and Panconesi (2009)[Exercise 1.2]) then shows

| (16) |

which decays exponentially as the committee size, , increases (as long as ). In particular, we can make the failure probability arbitrarily small by choosing the committee size to be large enough.

Remark 3.

A key drawback of the lottery-based election method is that the success probability only converges to 1 as the committee size () increases. By contrast, Theorem 3 shows that for approval voting, the success probability converges to 1 as the number of voters increases. This is the key reason why voting-based systems can have much smaller committee sizes than lottery-based systems.

For example, Algorand suggests a target committee size of about , instead of 21 for EOS (Chen and Micali 2016)[Section 5.1]. If we assume that (at most) of the tokens are ever held by malicious participants, a Chernoff bound gives that the probability of electing a dishonest committee (i.e., a committee with more than dishonest members), is bounded by .

The probability that a dishonest committee is ever elected can then be bounded by taking a union bound over all potential elections (e.g. if there is an election every four seconds for the next twenty five years, there will be approximately million elections). Taking a union bound over the elections held in the text 25 years, we have the probability of a fork in the next 25 years is at most .

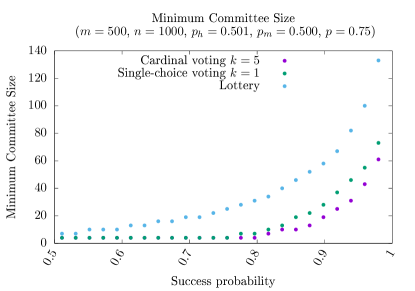

In Algorand, it is very easy to calculate the probability of a dishonest committee, for a given fraction of honest candidates (), and a given committee size (). Intuitively speaking, allowing users to vote should increase the probability of electing an honest committee, and thus reduce the size of the committee needed to ensure that it reaches the critical (rd) threshold of honest members.

In Figure 7, we plot the minimum committee size necessary to achieve a desired failure probability, when the committee is chosen by lottery (as in Algorand or Espresso) or according to an approval vote (as in DPoS). The key takeaway is that even when the voters have only minimal information and ), allowing users to vote for candidates drastically reduces the size of the committee necessary to achieve a specific failure bound. Since the committee executes a Byzantine Agreement protocol with communication cost that is quadratic in the committee size, , minimizing the committee size is critical for performance.

Note, Figure 7 was generated assuming the voters follow a cardinal voting strategy. When , this is single-choice voting, i.e., the case when each voter is only allowed to vote for one candidate (as in most Cosmos-based chains). When , this is the case when voters vote for their top 5 candidates. This is not the optimal cardinal voting strategy, but this plot shows that even when voters follow a simple, but suboptimal voting strategy, election-based committee selection can yield very small committees and outperform the other protocols. To summarize:

Result 1.

Approval voting outperforms both lottery-based, and single-choice voting consensus mechanisms, even when users are assumed to follow suboptimal cardinality thresholds.

7 Discussion and Conclusion

The paper analyzes committee-based consensus protocols and shows that even though elections based on approval voting lead to intractable optimal voting strategies, they nonetheless exhibit strong robustness to more intuitive (suboptimal) voting strategies that users resort to in practice, converging to optimality exponentially quickly in the number of voters. The paper also shows that committee-based consensus using approval voting has the potential to outperform other commonly employed mechanisms such as single-choice and lottery-based protocols (in terms of failure rates). We next discuss some of the limitations.

Stake-weighted voting: In our model, all voters votes have equal weight, whereas many platforms rely on stake-weighted voting. In this case, the Poisson Binomial Distributions become Generalized Poisson Binomials Zhang et al. (2018). In particular, Theorem 2 holds as is, but the distribution functions (defined in Theorem 1) become somewhat more involved. Importantly, the qualitative insights of the paper (e.g., asymptotic optimality) continue to hold.

Different objectives: Beyond optimizing to reduce failure rates, our model does not deal with other features that voters may care about. These are outside the scope of this work, but could be of interest for future work.

For instance, one drawback of electing committees as opposed to selecting random committees is that elections seems to lead to stagnation, especially early on in the blockchain life-cycle. EOS represents a rather extreme example: The first 89 million EOS blocks were mined by only 63 distinct producers Zheng et al. (2020b). By comparison, the first 655,000 Bitcoin blocks were mined by more than 275,000 distinct addresses, and the first 8 million Ethereum blocks were mined by over 5000 distinct addresses Zheng et al. (2020a).

A small, static set of block producers reduces decentralization – a core tenet of almost all cryptocurrencies. The idea that there should be a diversity of block producers is core to the open, democratic ideals that spawned much of the blockchain ecosystem, and the idea that there should be turnover in the set of block producers has been formalized in the notion of chain quality which is a measure of fairness. Chain quality is a measure of whether (in sufficiently long time windows) the fraction of blocks contributed by each participant is proportional to their hash power or stake Garay et al. (2015).

Chain quality is a different metric by which we could measure different election mechanisms, and this could be an interesting direction for future research. A discussion can be found in Appendix E.

Alternative voting schemes: In this work, we focused on lottery-based selection, single-vote mechanisms and approval voting because these are the systems that have currently been deployed for committee selection.

Other alternative voting systems exist, e.g. ranked-choice voting Nurmi and Palha (2021). Even though we were not able to find practical implementations, it could be interesting to analyze whether these can outperform approval voting in settings where voter incentives are aligned, but voters are (on the whole) poorly informed.

A separate question is vote weighting. All current Proof-of-Stake blockchains weight stake linearly, but there are alternative weighting mechanisms, the most common being Quadratic Voting Posner and Weyl (2014), Lalley and Weyl (2018). In Quadratic Voting, a voter’s vote weight is proportional the square-root of their stake, rather than being proportional to the stake itself. Quadratic Voting has been used in the blockchain context (e.g. Gitcoin Grants), but to the best of our knowledge, has not been used as a method for electing a consensus committee.

References

- Agarwal and Aggarwal (2018) Agarwal M, Aggarwal V (2018) Regret bounds for stochastic combinatorial multi-armed bandits with linear space complexity. arXiv preprint arXiv:1811.11925.

- Aiyer et al. (2005) Aiyer AS, Alvisi L, Clement A, Dahlin M, Martin JP, Porth C (2005) BAR fault tolerance for cooperative services. Proceedings of the twentieth ACM symposium on Operating systems principles, 45–58.

- Alsabah and Capponi (2020) Alsabah H, Capponi A (2020) Pitfalls of bitcoin’s proof-of-work: R&d arms race and mining centralization. Available at SSRN 3273982 .

- Amoussou-Guenou et al. (2020) Amoussou-Guenou Y, Biais B, Potop-Butucaru M, Piergiovanni ST (2020) Rational vs byzantine players in consensus-based blockchains. AAMAS, 43–51.

- Angelis et al. (2018) Angelis SD, Aniello L, Baldoni R, Lombardi F, Margheri A, Sassone V (2018) Pbft vs proof-of-authority: applying the cap theorem to permissioned blockchain. Italian Conference on Cyber Security (06/02/18), URL https://eprints.soton.ac.uk/415083/.

- Bapat and Beg (1989) Bapat R, Beg M (1989) Order statistics for nonidentically distributed variables and permanents. Sankhyā: The Indian Journal of Statistics, Series A 79–93.

- Bentov et al. (2016) Bentov I, Pass R, Shi E (2016) Snow white: Provably secure proofs of stake. IACR Cryptol. ePrint Arch. 2016(919).

- Biais et al. (2019) Biais B, Bisiere C, Bouvard M, Casamatta C (2019) The blockchain folk theorem. The Review of Financial Studies 32(5):1662–1715.

- Binance (2020) Binance (2020) Delegated proof of stake explained. URL https://academy.binance.com/en/articles/delegated-proof-of-stake-explained.

- Binance Academy (2021) Binance Academy (2021) https://academy.binance.com/en/glossary/transactions-per-second-tps.

- Bitcoin Wiki (2021) Bitcoin Wiki (2021) https://en.bitcoin.it/wiki/Confirmation.

- Bitshares (2021) Bitshares (2021) Delegated proof of stake (dpos). URL https://how.bitshares.works/en/master/technology/dpos.html.

- Brams and Fishburn (2007) Brams S, Fishburn PC (2007) Approval Voting (Springer), URL http://dx.doi.org/10.1007/978-0-387-49896-6.

- Buchman (2016) Buchman E (2016) Tendermint: Byzantine fault tolerance in the age of blockchains.

- Cambridge University (2021) Cambridge University (2021) Cambridge bitcoin electricty consumption index. URL https://cbeci.org/.

- Castro and Liskov (1999) Castro M, Liskov B (1999) Practical byzantine fault tolerance. Proceedings of the Third Symposium on Operating Systems Design and Implementation, 173–186 (USENIX Association).

- Cesa-Bianchi and Lugosi (2012) Cesa-Bianchi N, Lugosi G (2012) Combinatorial bandits. Journal of Computer and System Sciences 78(5):1404–1422.

- Chen and Micali (2016) Chen J, Micali S (2016) Algorand. ArXiv: abs/1607.01341.

- Chen et al. (2016) Chen W, Hu W, Li F, Li J, Liu Y, Lu P (2016) Combinatorial multi-armed bandit with general reward functions. Proceedings of the 30th International Conference on Neural Information Processing Systems, 1659–1667.

- Chen et al. (2013) Chen W, Wang Y, Yuan Y (2013) Combinatorial multi-armed bandit: General framework and applications. International Conference on Machine Learning, 151–159 (PMLR).

- Combes et al. (2015) Combes R, Talebi MS, Proutiere A, Lelarge M (2015) Combinatorial bandits revisited. arXiv preprint arXiv:1502.03475 .

- Cong et al. (2021a) Cong LW, He Z, Li J (2021a) Decentralized mining in centralized pools. The Review of Financial Studies 34(3):1191–1235.

- Cong et al. (2021b) Cong LW, Li Y, Wang N (2021b) Tokenomics: Dynamic adoption and valuation. The Review of Financial Studies 34(3):1105–1155.

- Copeland (2020) Copeland T (2020) Steem vs tron: The rebellion against a cryptocurrency empire. Decrypt .

- Cosmos (2021) Cosmos (2021) Validator FAQ. https://hub.cosmos.network/main/validators/validator-faq.html.

- Cryptopedia (2021) Cryptopedia (2021) What are proof of stake (PoS) and delegated proof of stake (DPoS)? URL https://www.gemini.com/cryptopedia/proof-of-stake-delegated-pos-dpos#section-delegated-proof-of-stake.

- Daian et al. (2020) Daian P, Goldfeder S, Kell T, Li Y, Zhao X, Bentov I, Breidenbach L, Juels A (2020) Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability. 2020 IEEE Symposium on Security and Privacy (SP), 910–927 (IEEE).

- Dubhashi and Panconesi (2009) Dubhashi DP, Panconesi A (2009) Concentration of measure for the analysis of randomized algorithms (Cambridge University Press).

- Easley et al. (2019) Easley D, O’Hara M, Basu S (2019) From mining to markets: The evolution of bitcoin transaction fees. Journal of Financial Economics 134(1):91–109.

- Elkind et al. (2017) Elkind E, Faliszewski P, Skowron P, Slinko A (2017) Properties of multiwinner voting rules. Social Choice and Welfare 48(3):599–632.

- EOS (2018) EOS A (2018) EOS voting guide. https://medium.com/@auroraeos/eos-voting-guide-3bf4e0be251b.

- Etherscan (2022) Etherscan (2022) Ethereum uncle count and rewards chart. https://etherscan.io/chart/uncles.

- Fanti et al. (2019) Fanti G, Kogan L, Viswanath P (2019) Economics of proof-of-stake payment systems. Technical report, Working paper.

- Fernández and Williams (2010) Fernández M, Williams S (2010) Closed-form expression for the poisson-binomial probability density function. IEEE Transactions on Aerospace and Electronic Systems 46(2):803–817.

- Flashbots (2021) Flashbots (2021) https://explore.flashbots.net/.

- Gan et al. (2021a) Gan J, Tsoukalas G, Netessine S (2021a) Initial coin offerings, speculation, and asset tokenization. Management Science 67(2):914–931.

- Gan et al. (2021b) Gan R, Tsoukalas G, Netessine S (2021b) To infinity and beyond: Financing platforms with uncapped crypto tokens. Available at SSRN 3776411 .

- Garay et al. (2015) Garay J, Kiayias A, Leonardos N (2015) The Bitcoin backbone protocol: Analysis and applications. EUROCRYPT, 281–310 (Springer).

- Garratt and van Oordt (2020) Garratt R, van Oordt MR (2020) Why fixed costs matter for proof-of-work based cryptocurrencies. Available at SSRN 3572400 .

- Gaži et al. (2019) Gaži P, Kiayias A, Zindros D (2019) Proof-of-stake sidechains. 2019 IEEE Symposium on Security and Privacy (SP), 139–156 (IEEE).

- Gleehokie et al. (2018) Gleehokie, 1337micro, Chanryma, testzcrypto, hkshwa, bytemaster, nathanhourt (2018) EOS.IO technical white paper v2. URL https://github.com/EOSIO/Documentation/blob/master/TechnicalWhitePaper.md.

- Glueck et al. (2008) Glueck DH, Karimpour-Fard A, Mandel J, Hunter L, Muller KE (2008) Fast computation by block permanents of cumulative distribution functions of order statistics from several populations. Communications in Statistics - Theory and Methods 37(18):2815–2824.

- Hu et al. (2021) Hu Q, Yan B, Han Y, Yu J (2021) An improved delegated proof of stake consensus algorithm. Procedia Computer Science 187:341–346.

- Huberman et al. (2021) Huberman G, Leshno JD, Moallemi C (2021) Monopoly without a monopolist: An economic analysis of the bitcoin payment system. The Review of Economic Studies ISSN 0034-6527, URL http://dx.doi.org/10.1093/restud/rdab014, rdab014.

- Hui (2020) Hui A (2020) Arbitration challenged in hostile work environment lawsuit. https://www.coindesk.com/markets/2020/07/09/tron-arbitration-challenged-in-hostile-work-environment-lawsuit/.

- InsideTheSimulation (2021) InsideTheSimulation (2021) https://ethmerge.com/.

- John et al. (2020) John K, Rivera TJ, Saleh F (2020) Economic implications of scaling blockchains: Why the consensus protocol matters. Available at SSRN .

- Kiayias et al. (2017) Kiayias A, Russell A, David B, Oliynykov R (2017) Ouroboros: A provably secure proof-of-stake blockchain protocol. Annual International Cryptology Conference, 357–388 (Springer).

- Kilgour (2010) Kilgour D (2010) Approval balloting for multi-winner elections. Handbook on Approval Voting (Springer, Berlin, Heidelberg).

- Kogias et al. (2016) Kogias EK, Jovanovic P, Gailly N, Khoffi I, Gasser L, Ford B (2016) Enhancing Bitcoin security and performance with strong consistency via collective signing. USENIX, 279–296.

- Lalley and Weyl (2018) Lalley SP, Weyl EG (2018) Quadratic voting: How mechanism design can radicalize democracy. AEA Papers and Proceedings, volume 108, 33–37.

- Lamport et al. (1982) Lamport L, Shostak R, Pease M (1982) The Byzantine generals problem. ACM Transactions on Programming Languages and Systems 4(3):382–401.

- Leonardos et al. (2020) Leonardos S, Reijsbergen D, Piliouras G (2020) Weighted voting on the blockchain: Improving consensus in proof of stake protocols. International Journal of Network Management 30(5):e2093.

- Lewis-Pye and Roughgarden (2020) Lewis-Pye A, Roughgarden T (2020) A general framework for the security analysis of blockchain protocols. arXiv preprint arXiv:2009.09480 .

- Lewis-Pye and Roughgarden (2021) Lewis-Pye A, Roughgarden T (2021) How does blockchain security dictate blockchain implementation? arXiv preprint arXiv:2109.04848 .

- Lovejoy (2020) Lovejoy JPT (2020) An empirical analysis of chain reorganizations and double-spend attacks on proof-of-work cryptocurrencies. Master’s thesis, Massachusetts Institute of Technology.

- Meng et al. (2018) Meng Y, Cao Z, Qu D (2018) A committee-based byzantine consensus protocol for blockchain. 2018 IEEE 9th International Conference on Software Engineering and Service Science (ICSESS), 1–6 (IEEE).

- Nakamoto (2008) Nakamoto S (2008) Bitcoin: A peer-to-peer electronic cash system. Decentralized Business Review 21260.

- Niemi (1984) Niemi RG (1984) The problem of strategic behavior under approval voting. The American Political Science Review 78(4):952–958, ISSN 00030554, 15375943, URL http://www.jstor.org/stable/1955800.

- Nurmi and Palha (2021) Nurmi H, Palha RP (2021) A theoretical examination of the ranked choice voting procedure. Transactions on Computational Collective Intelligence XXXVI, 1–16 (Springer).

- Nxt Community (2016) Nxt Community (2016) Nxt whitepaper. https://nxtdocs.jelurida.com/Nxt_Whitepaper.

- NY (2019) NY E (2019) The missing piece to the EOS incentive model: Part 1. %****␣main.bbl␣Line␣300␣****https://medium.com/eos-new-york/the-missing-piece-to-the-eos-incentive-model-bd39977d243f.

- Pagnotta (2021) Pagnotta ES (2021) Decentralizing money: Bitcoin prices and blockchain security. The Review of Financial Studies ISSN 0893-9454, URL http://dx.doi.org/10.1093/rfs/hhaa149, hhaa149.

- Pham and Tran (1982) Pham TD, Tran LT (1982) On functions of order statistics in the non IID case. Sankhyā: The Indian Journal of Statistics, Series A 251–261.

- Posner and Weyl (2014) Posner EA, Weyl EG (2014) Quadratic voting as efficient corporate governance. The University of Chicago Law Review 81(1):251–272.

- Prat and Walter (2021) Prat J, Walter B (2021) An equilibrium model of the market for bitcoin mining. Journal of Political Economy 129(8):000–000.

- Rejwan and Mansour (2020) Rejwan I, Mansour Y (2020) Top- combinatorial bandits with full-bandit feedback. Algorithmic Learning Theory, 752–776 (PMLR).

- Roşu and Saleh (2021) Roşu I, Saleh F (2021) Evolution of shares in a proof-of-stake cryptocurrency. Management Science 67(2):661–672.

- Rubin (2021) Rubin J (2021) Block.one pays $27.5m to settle class-action lawsuit. Coindesk .

- Saleh (2021) Saleh F (2021) Blockchain without waste: Proof-of-stake. The Review of financial studies 34(3):1156–1190.

- The Block (2021) The Block (2021) https://www.theblockcrypto.com/data/on-chain-metrics/ethereum.

- The Interchain Foundation (2017) The Interchain Foundation (2017) https://blog.cosmos.network/consensus-compare-tendermint-bft-vs-eos-dpos-46c5bca7204b.

- TRON (2018) TRON (2018) TRON whitepaper version 2.0. https://tron.network/static/doc/white_paper_v_2_0.pdf.

- Tsoukalas and Falk (2020) Tsoukalas G, Falk BH (2020) Token-weighted crowdsourcing. Management Science 66(9):3843–3859.

- Xu et al. (2018) Xu B, Luthra D, Cole Z, Blakely N (2018) EOS: An architectural, performance, and economic analysis. Retrieved June 11:2019.

- Yang et al. (2019) Yang F, Zhou W, Wu Q, Long R, Xiong NN, Zhou M (2019) Delegated proof of stake with downgrade: A secure and efficient blockchain consensus algorithm with downgrade mechanism. IEEE Access 7:118541–118555.

- Zhang et al. (2018) Zhang M, Hong Y, Balakrishnan N (2018) The generalized poisson-binomial distribution and the computation of its distribution function. Journal of Statistical Computation and Simulation 88(8):1515–1527.

- Zheng et al. (2020a) Zheng P, Zheng Z, Wu J, Dai HN (2020a) Xblock-ETH: Extracting and exploring blockchain data from Ethereum. IEEE Open Journal of the Computer Society 1:95–106.

- Zheng et al. (2020b) Zheng W, Zheng Z, Dai HN, Chen X, Zheng P (2020b) Xblock-EOS: Extracting and exploring blockchain data from EOSIO. arXiv preprint arXiv:2003.11967.

Appendix

Appendix A A Primer on Blockchain Consensus Protocols & Committee Elections

Herein we provide a primer on single-leader and committee-based consensus protocols. Readers familiar with their basic operational features can skip this section without loss.

As mentioned in the introduction, the core problem facing all cryptocurrencies (and decentralized databases of all kinds), is how to provide a single, universally accepted ordering of transactions (or state updates). Most modern cryptocurrencies are based on the notion of a hash chain, where blocks of data are chained together using cryptographic hash functions. Hash chains are an append-only data structure, meaning that new blocks (containing transactions) can be appended to the end of the chain, while internal blocks of the chain cannot be modified or re-ordered (without modifying all subsequent blocks). Since anyone can easily append new blocks to the end of a hash chain, decentralized systems need a method for deciding how and when new blocks can be added to the chain.

Most cryptocurrencies use a form of leader election, where a leader is elected at regular intervals. This leader, or “block producer,” is given the right to produce a single block. There is an inherent value in becoming a block producer, as block producers have the power to insert, re-order and censor transactions (Daian et al. 2020).666The value that can be extracted by inserting, re-ordering and censoring transactions is termed “Maximum Extractable Value” (MEV), and is worth hundreds of millions of dollars on blockchains like Ethereum (Flashbots 2021). In addition, most cryptocurrencies provide direct incentives for block production in the form of transaction fees and block rewards. Transaction fees are paid by the users to incentivize the block producer to include specific transactions in a block. Block rewards are new coins that are minted and paid directly to block producers. For example, in Bitcoin, block rewards are currently set to BTC. In many cryptocurrencies, block rewards are the only mechanism by which new coins are generated. For reference, in July 2021, Ethereum miners received about 18% of their direct compensation from transaction fees and 82% from block rewards (The Block 2021).

Block producers also have the ability to harm the platform itself. Block producers can censor transactions within the block they produce. Lazy or inept block producers can reduce the total transaction throughput of the system by failing to include enough transactions in a block or failing to produce a block altogether. Malicious block producers can “fork” the chain by appending two blocks at the same block height. This type of behavior can lead to “double-spending attacks” and can destabilize the entire blockchain.

Block producers’ power to harm the ecosystem, means that the selection mechanism must ensure that only “honest” producers are elected. When block producer candidates have stable identities, classical consensus protocols (e.g. Lamport et al. (1982), Castro and Liskov (1999)) provide efficient and robust mechanisms for leader election. In a permissionless setting, however, where the set of block producer candidates is anonymous and dynamic, classical consensus protocols fail, and other methods must be devised.

Proof of Work (PoW)

As mentioned earlier, the Bitcoin whitepaper Nakamoto (2008) introduced a novel single-leader protocol whereby block-producing candidates (“miners”) expend effort in the form of computing cryptographic hashes on random values, and their chance of becoming block leader is proportional to the amount of effort they exert. This Proof of Work consensus, is used by many of the leading cryptocurrencies (by market cap), including Bitcoin, Ethereum, Dogecoin and Litecoin.

Although PoW-based consensus has proven stable and secure, it has several drawbacks, most notably its societal cost, and its low transaction throughput. Currently, block producer candidates on Bitcoin expend about as much electricity as the country of Finland in an effort to be chosen as block producers (Cambridge University 2021).

Proof-of-Work based consensus, also has limitations on how frequently block producers can be chosen, and this directly affects the blockchain’s transaction throughput. Currently, the leading PoW-based blockchains, Bitcoin and Ethereum, can handle less than tens of transactions per second. By contrast Visa handles thousands of transactions per second (Binance Academy 2021).

Proof of Stake (PoS)

The aforementioned drawbacks of PoW have pushed the blockchain community to explore alternatives, and in this quest, Proof of Stake (PoS) has arguably emerged as the current frontrunner. The Ethereum blockchain, for instance, which supports the world’s second largest cryptocurrency ETH, originally launched with a PoW protocol but has been gradually trying to transition to a form of PoS for several years (InsideTheSimulation 2021).

In PoS, block producers are elected in proportion to their token balance (“stake”) on the blockchain, rather than their computational effort. Similar to PoW systems, where candidates signal their support of the platform by expending computing resources, in PoS systems, candidates signal their support of the system by acquiring and holding native tokens on the blockchain.

There are many variants of the PoS protocol, but a common feature of almost all PoS systems is that block producers are elected with probability proportional to their “staked” tokens (as in Ethereum 2.0) or their passive token balances (as in Algorand).

Committee-based Consensus

Although under PoS, block producers can earn significant returns, being an efficient block producer usually requires powerful computing equipment, a dedicated internet connection, and a robust software configuration. In some blockchains, a nontrivial minimum amount of tokens is also required to be eligible to participate. Many regular token holders are thus ineligible (or simply unwilling) to take on this type of role. To address this problem, most PoS systems support some type of delegation mechanism, whereby token holders can delegate their stake to professional block producers (usually in exchange for some sort of profit sharing).

Committee-based consensus takes this separation between token holders and block producers to the extreme. In most traditional PoW systems, block producers are selected in a lottery-like procedure according to their (proportional) hash power. Several PoS systems (e.g. Tezos, Algorand, Cardano) adapted this idea to elect leaders randomly with probability equal to their proportional token stake.777In fact, the core technical contribution in systems like Algorand and Cardano is a decentralized, verifiable lottery mechanism. As an alternative to this lottery-based leader election, several blockchains allow users to cast (stake-weighted) votes for block producers and the ones with the highest number of votes become producers for some fixed duration of time.

In platforms using committee-based consensus, a small committee ( in the Cosmos Hub, in EOS or in TRON) of block producers is elected by a stake-weighted vote, and is responsible for producing and validating blocks.888Although almost all PoS systems support some form of delegation, the term “Delegated Proof of Stake” is usually reserved for the specific type of committee-based consensus protocols used by systems like EOS and TRON.

Some Advantages of Committee-based Consensus

Committee-based consensus has several perceived advantages over other commonly used consensus protocols. First, the committee can check each other’s actions and prevent malicious behavior. For example, in most classical consensus protocols up to a -fraction999Most consensus protocols can tolerate . of the participants can behave maliciously without adversely affecting the system.

Second, the voting process takes a nonzero amount of time, so electing a batch of producers at once increases efficiency in contrast two Nakamoto consensus, where a single block producer is selected at each step.

Third, it allows the chain to achieve instant finality – when the committee certifies a block, that block is immediately finalized. This is in contrast to PoW blockchains that only achieve eventual finality. Bitcoin wallets, for instance, typically wait until a transaction is buried 6 blocks deep in the chain before considering it “finalized” (Bitcoin Wiki 2021). Blockchains that rely on committee-based-consensus can achieve instant finality in the following sense. If the system never elects a committee with more than a -fraction of malicious members, then as soon as a committee certifies a block, that block can be considered final, and will never be forked away. Thus committee-based consensus protocols need to ensure that the probability a malicious committee is elected is so small, that even if the chain runs for years, there will never be a committee with more than a -fraction of malicious members.