Estimation and Inference of Extremal Quantile Treatment Effects for Heavy-Tailed Distributions

Abstract

Causal inference for extreme events has many potential applications in fields such as climate science, medicine and economics. We study the extremal quantile treatment effect of a binary treatment on a continuous, heavy-tailed outcome. Existing methods are limited to the case where the quantile of interest is within the range of the observations. For applications in risk assessment, however, the most relevant cases relate to extremal quantiles that go beyond the data range. We introduce an estimator of the extremal quantile treatment effect that relies on asymptotic tail approximation, and use a new causal Hill estimator for the extreme value indices of potential outcome distributions. We establish asymptotic normality of the estimators and propose a consistent variance estimator to achieve valid statistical inference. We illustrate the performance of our method in simulation studies, and apply it to a real data set to estimate the extremal quantile treatment effect of college education on wage.

1 Introduction

Quantifying causal effects of binary treatments on extreme events is an important problem in many fields of research. Examples include the effect of anthropogenic forcing on extreme precipitation, the effect of smoking on low birth weights, and the effect of education on high wages (e.g., Madakumbura et al.,, 2021; Dessì et al.,, 2018; Heckman et al.,, 2018). The quantile treatment effect (QTE) (e.g., Doksum,, 1974; Lehmann and D’Abrera,, 1975), which is based on the potential outcome framework, quantifies such causal effects.

Formally, for a binary treatment and an outcome , let and denote the potential outcomes of under treatment and respectively. The fundamental problem of causal inference is that for each sample unit, only one of the outcomes can be observed, namely the one under the given treatment. The observed response is (i.e., we make the stable unit treatment value assumption). Causal effects of on can be defined in various ways according to different targets of interest. An example is the often used average treatment effect, which is defined as . In this paper, the causal effect at extremely high/low quantiles is our main interest. Let the -QTE be defined as

| (1) |

where and denotes the -quantile of the potential outcome , and denotes its distribution function. We will treat the case where is very close to or .

The QTE is generally not identifiable from observational data without making additional assumptions. A commonly made assumption, called the unconfoundedness assumption (e.g., Rosenbaum and Rubin,, 1983), is that for some set of observed covariates . Under this assumption, the propensity score defined as can be used to adjust for confounding in the binary treatment setting, and the QTE is identifiable.

Along these lines, Firpo, (2007) introduced an adjusted quantile estimator (see (6)), defined as the minimizer of the inverse propensity score weighted empirical quantile loss, to estimate the -QTE in (1) for a fixed quantile level . He also established the asymptotic normality of this estimator, allowing statistical inference.

For extreme events, the interest lies in the -QTE for close to or . Considering the lower tail, we allow the quantile to converge to zero as the sample size tends to infinity. In particular, we distinguish between three cases based on different rates of , and we call them: (a) intermediate: if and ; (b) moderately extreme: if and ; and (c) extreme: if and . Here is the effective sample size or the expected number of observations below the -quantile in a sample of size . We note that the cases and are sometimes referred to as “extreme” and “very extreme” (Chernozhukov,, 2005; Chernozhukov et al.,, 2016; Zhang,, 2018).

The asymptotic results of with fixed in Firpo, (2007) no longer hold in the framework of changing levels , and Zhang, (2018) first established the asymptotic theory for this estimator in this framework. Specifically, in the intermediate case, Zhang, (2018) showed that the estimator is asymptotically normal and suggested a valid full-sample bootstrap confidence interval. For the moderately extreme case, he showed that the limiting distribution of the estimator is no longer Gaussian, and proposed a out of bootstrap for valid inference.

For many applications, the most relevant quantiles are often those that go beyond the range of the data. For instance, in attribution studies, climate scientists investigate the causal effect of anthropogenic influences on climate extremes such as heavy precipitation. The quantiles of interest for such extreme events typically go far beyond the range of historical recordings and therefore extreme value extrapolation is required (e.g., Easterling et al.,, 2016; van Oldenborgh et al.,, 2017). Formally this corresponds to the case of extreme (rather than intermediate or moderately extreme) -QTE where .

From now on, we use the notation to denote levels where and , which includes the extreme case, and we use to denote only the intermediate levels where and . To the best of our knowledge, there is no existing method for the estimation and inference of the -QTE where . In particular, since the effective sample size below the -quantile tends to zero, the estimators based on empirical quantile loss are no longer applicable.

In this paper, we focus on heavy-tailed distributions, which have polynomially decaying tail probabilities and are thus heavier than Gaussian. Heavy tails are often encountered in risk analysis applications and many works therefore study this distribution class (e.g., Matthys et al.,, 2004; Wang et al.,, 2012; Athey et al.,, 2021; Xu et al.,, 2022). We propose a new quantile estimator for based on parametric tail approximations from extreme value theory (de Haan and Ferreira,, 2007), which enables us to extrapolate from intermediate to extreme quantiles. Indeed, based on the theory of regular variation, we have

| (2) |

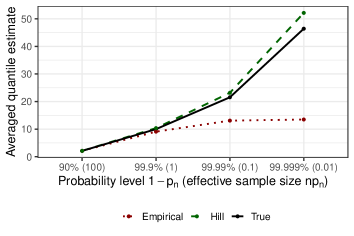

where is the extreme value index of the potential outcome . Figure 1 in Section 2.1 illustrates the advantage of using extrapolation as in (2) for estimation of extreme quantiles compared to empirical estimates.

Our proposed estimator (see (8) in Section 3) is obtained by plugging in the estimator (see (6)) from Firpo, (2007) for intermediate quantiles and a newly proposed causal Hill estimator (see (7)) for the extreme value index based on inverse propensity score weighting. We use the Hill type instead of the Pickands type estimator for the extreme value index because the latter is known to suffer from high variance in the heavy-tailed case, but we would also like to note that the Hill type estimator is not invariant to location shift while the Pickands estimator is. The final -QTE estimator is , which we call the extremal QTE estimator. Beyond point estimation, we establish the asymptotic normality of this estimator. In particular, inspired by Zhang, (2018) and Chernozhukov and Fernández-Val, (2011), we propose a new normalizing factor for the extrapolation quantile estimators of two treatment groups, to deal with the problem that they may have different convergence rates.

The asymptotic variance of the extremal QTE estimator is unknown, and we propose a technically tractable variance estimator. We prove that this estimator is consistent under an additional assumption (Assumption 6). Even when this assumption does not hold, this estimator is conservative, in the sense that it is still consistent to some quantity that is larger than the true variance. Thus it can be used to construct asymptotically honest confidence intervals for the extremal QTE.

The extremal QTE estimator can be used for estimation and inference of moderately extreme and extreme quantiles for heavy-tailed distributions. It thus provides an alternative to Zhang, (2018) for moderately extreme QTEs, and a first method for extreme QTEs.

Our approach requires additional assumptions when compared to Zhang, (2018), including most importantly the second-order regular variation, which is fairly standard in extreme value theory (e.g., de Haan and Ferreira,, 2007). It is the price we need to pay in order to go to more extreme quantiles than Zhang, (2018).

The topic of causality for extreme events is receiving increasing interest. The line of work by Gissibl and Klüppelberg, (2018); Gissibl et al., (2018); Gnecco et al., (2021) and Mhalla et al., (2020) define structural causal models and investigate causal relationships in the setting where several variables are simultaneously extreme, and they focus on learning the unknown causal structure. In climate science, there is a large body of literature on attribution studies where the effect of climate change on weather extremes is analyzed (e.g., Hannart et al.,, 2016; Easterling et al.,, 2016; van Oldenborgh et al.,, 2017; Naveau et al.,, 2018, 2020). These methods focus on model-based data where interventions on, say, carbon dioxide emissions, are possible, and no adjustment for confounding is required. Jana et al., (2021) propose a method to quantify the causal effect of London cycling superhighways on extreme traffic congestion, but no theoretical analysis of this method is done. Our method adds to this growing literature and provides a theoretically justified approach for estimation and inference of extremal QTEs in the presence of confounding variables.

The paper is structured as follows. In Section 2, we review some key concepts from extreme value theory and the -QTE estimator. In Section 3, we propose the causal Hill extreme value index estimator and the extremal QTE estimator, and show their asymptotic normality. Furthermore, we propose a variance estimator and prove that it is consistent under an additional assumption, and that it is conservative otherwise. In Section 4, we present the finite sample behavior of our proposed extremal QTE estimator in different simulation settings, and compare it to existing methods. We apply our methodology to a real data set about college education and wage in Section 5. All proofs, more technical details and additional simulations can be found in the Supplementary Material. Any equations, theorems, etc., from the Supplementary Material are referred to starting with a letter A–F corresponding to the respective section in that document.

To be in line with the literature on extreme value theory, we focus on extremal QTEs in the upper tail, that is, . Results for the lower tail can be derived similarly.

2 Preliminaries

2.1 Extreme Value Theory

We are interested in extreme quantiles with level where . Empirical estimates of extreme quantiles with become highly biased and classical asymptotic theory no longer applies (see Figure 1). Extreme value theory studies methods for quantile extrapolation that result in more accurate estimates of extremal quantiles (e.g., de Haan and Ferreira,, 2007). This theory relies on the following mild assumption on a distribution that guarantees that the tail can be well approximated in a parametric way. Let the random variable have distribution and quantile function , where is the left-continuous inverse of a non-decreasing function .

Definition 1.

(cf. de Haan and Ferreira, (2007)) The distribution is in the max-domain of attraction of a generalized extreme value distribution if there exist and sequences of constants and , , such that

| (3) |

for all such that . For , the right hand side is interpreted as . The parameter is called the extreme value index (EVI).

This condition is mild as it is satisfied for most standard distributions, for example, the normal, Student- and beta distributions. For a complete characterization of the max-domain of attraction of the three regimes (, , ), we refer to Resnick, (2008) and Embrechts et al., (1997). We focus on the heavy-tailed case where , that is, distributions with regularly varying tails , where is a slowly varying function at . The regular variation of the tail of can be equivalently expressed in terms of the tail quantile function . The max-domain of attraction condition (3) for is equivalent to

| (4) |

Relation (4) and the fact that the quantile function can be expressed as for , imply that for large enough ,

| (5) |

where is a sequence such that and . By using an intermediate sequence , relation (5) allows us to extrapolate from intermediate to extreme quantiles. We illustrate the benefit of using the extreme value extrapolation (5) in Figure 1. It can be seen that the empirical estimates are strongly biased for extreme quantiles when the effective sample size , while the extrapolation allows for approximately unbiased estimates.

To analyze the asymptotic distribution of the extrapolated quantiles, usually a second-order condition is assumed.

Definition 2.

(cf. de Haan and Ferreira, (2007)) The function is of second-order regular variation with first-order parameter and second-order parameter if there exists a positive or negative function with such that for all

The function is called the second-order auxiliary function. For , is defined as .

We note that Definition 2 is stronger than Definition 1: if is of second-order regular variation with first-order parameter , then satisfies the max-domain of attraction condition with extreme value index . Second-order regular variation is satisfied by many popular distributions, and it is often possible to derive the function and the value of explicitly; see Alves et al., (2007) for details and examples.

2.2 Estimation of the -QTE

The estimation of -QTE from Firpo, (2007) relies on the propensity score , which is used to adjust for confounding in the binary treatment setting. In particular, Firpo, (2007, Corollary 1) shows that the QTE is identifiable under the following assumptions.

Assumption 1.

-

i)

.

-

ii)

has compact support and there exists such that for all .

Assumption 1 is the unconfoundedness condition and Assumption 1 is called the common support assumption. Both assumptions are fairly standard in causal inference literature, and we impose them throughout this paper.

The propensity score is generally unknown in practice and needs to be estimated. For independent copies of , we follow Hirano et al., (2003), Firpo, (2007) and Zhang, (2018) and use the nonparametric sieve method to obtain an estimate (see Section A in the Supplementary Material for more details). Based on inverse propensity score weighting, Firpo, (2007) proposed the following estimators for the quantiles of the potential outcomes and :

| (6) | ||||

The -QTE is then estimated by .

Under Assumption 2 below and the two regularity Assumptions 7 and 8 in Section B of the Supplementary Material, Zhang, (Theorem 3.1 2018) showed that for the intermediate quantile index (i.e., , ), the -QTE estimator is asymptotic normal. For the moderately extreme case (i.e., and ), however, Zhang, (2018) showed that the limiting distribution is no longer Gaussian.

Assumption 2.

(Regularity conditions on the potential outcome distributions)

For :

-

i)

and are continuously distributed with densities and , respectively.

-

ii)

The density of is monotone in its upper tail.

-

iii)

The distribution function of belongs to the max-domain of attraction of a generalized extreme value distribution with extreme value index (see Definition 1).

3 Extremal Quantile Treatment Effect Estimation for Heavy-Tailed Models

We now go beyond the intermediate and moderately extreme cases and propose an extremal QTE estimator based on quantile extrapolation, that can be used in moderately extreme and extreme cases (i.e., , ). We also derive its asymptotic normality and propose an asymptotic variance estimator which enables us to construct a confidence interval for the extremal QTE.

3.1 Extremal QTE Estimator

Our extremal QTE estimator is based on the quantile extrapolation approach (see approximation (5)), so estimators for the EVIs of the potential outcome distributions are required. In the classical setting, the Hill estimator introduced by Hill, (1975) is a common choice for heavy-tailed cases. In the potential outcome setting, however, the classical Hill estimator is not appropriate due to confounding. Therefore, we propose the following causal Hill estimators that adjust for confounding via the estimated propensity score (see (15)):

| (7) | ||||

Zhang, (2018) also proposed two EVI estimators for short-tailed distributions in his supplementary material, one is the Pickands type estimator and one is the Hill type estimator. Rather than extrapolation, his goal of using the EVI estimator is to estimate the -th QTE, that is, the lower endpoint of the distribution. His Hill type estimator is moment-based, which also uses inverse propensity score weighting, but with the true propensity score. In the simulations in Section 4, we implement the quantile extrapolation approach with his Pickands type estimator and compare it to our proposed estimator (7).

Building on the causal Hill estimators in (7) and the intermediate quantile estimator in (6), we propose the following quantile extrapolation estimator

| (8) |

for , and the final extremal QTE estimator is defined as the difference of the extrapolated quantiles:

| (9) |

For simplicity, we use the same intermediate level for both extrapolation estimators and in this paper, but in principle, one can use different intermediate levels for each potential outcome. The latter might be advantageous if the potential outcome distributions have very different tail behaviors, or if there is a severe imbalance between treated and non-treated samples.

To obtain the extremal QTE estimator (9), the intermediate level (or if we consider ) needs to be chosen. The optimal choice of the depends on the underlying data distribution and is difficult in practice, and there is a bias-variance trade-off. Specifically, if is too small, then the effective sample size is small and this will lead to high variance. On the other hand, if is too large, then the assumptions of extreme value theory may not hold because we are no longer in the tail of the distribution, and this will lead to high bias. In practice, there are some commonly used approaches for choosing . The simplest one is to set to some reasonable fixed value based on the background knowledge of the concrete problem. One can also plot the estimates depending on different and then select in the first stable region of the plot (e.g., Resnick,, 2007). There are also adaptive methods to approximate the optimal (e.g., Drees and Kaufmann,, 1998; Boucheron and Thomas,, 2015).

3.2 Asymptotic Properties

The main theoretical result in this subsection is Theorem 3, which shows the asymptotic normality of the extremal QTE estimator . The major steps to prove this theorem are the following: (1) showing that the asymptotic behavior of the quantile extrapolation estimator depends only on the asymptotic distribution of the causal Hill estimator (see Lemma 2); (2) deriving the asymptotic distribution of (see Theorem 2), which builds on an asymptotic linearity result (see Theorem 1); (3) introducing a new normalizing factor (see formula (10)) when deriving the asymptotic distribution of to account for the issue that and may have different convergence rates.

3.2.1 Asymptotic Properties of the Causal Hill Estimator

We first present a result showing that under the same conditions as the Theorem 3.1 of Zhang, (2018), our proposed causal Hill estimator is consistent.

Lemma 1.

To obtain asymptotic normality of the causal Hill estimator, we require Assumption 3 below, which is a second-order regular variation assumption. This assumption is standard to obtain asymptotic normality results for heavy-tailed distributions, and it is satisfied by most heavy-tailed distributions such as the Student- and the Fréchet distribution (e.g., de Haan and Ferreira,, 2007).

Assumption 3.

For , the tail function of is of second-order regular variation (see Definition 2) with extreme value index , second-order auxiliary function and second-order parameter .

To guarantee that the estimated propensity score is compatible with the causal Hill estimator, we also require Assumption 4 below, which is a regularity assumption on the sieve estimator. This assumption is of similar type as Assumption 7 which is used in the Theorem 3.1 of Zhang, (2018).

Assumption 4.

For , is -times continuously differentiable in with all derivatives bounded by some uniformly over . Here as , where is the number of sieve bases and is the dimension of .

Before showing asymptotic normality of the causal Hill estimator, we show an important asymptotic linearity result under the above two extra assumptions.

Theorem 1.

Remark 1.

is the influence function for the intermediate quantile estimator which also appears in Zhang, (2018) (see also Theorem 5), and is the new influence function appearing in our result, which has a similar form as . The factors and in the influence functions correspond to the information gain from the nonparametric estimation of the propensity score. Zhang, (2018) made the observation that since is of order , the term with factor in is negligible under suitable integrability conditions. The same holds for the information gain term in because is also of order (see Lemma 9). We discuss this in more detail when considering variance estimation in Section 3.3.

Given the asymptotic linearity result in Theorem 1 and the fact that the influence functions depend on the sample size , we will use a triangular array central limit theorem to obtain asymptotic normality. This requires that the covariance matrix of the random vectors converge (see Assumptions 8 and 9). The extra Assumption 9 is of similar flavor as Assumption 8 used in Theorem 3.1 of Zhang, (2018). In fact, we can show that the sequence is bounded by using similar arguments as in the proof of Theorem 2. Its convergence is therefore mostly a technical condition.

We now give the asymptotic normality result of the causal Hill estimator.

3.2.2 Asymptotic Properties of the Extremal QTE Estimator

We now study the asymptotic properties of the quantile extrapolation estimator in (8). We first give the following lemma which shows that the asymptotic behavior of only depends on the asymptotic distribution of the EVI estimator.

Lemma 2.

Lemma 2 (and the main result Theorem 3) allows that , but it cannot converge to zero arbitrarily fast as . This is reasonable since it means that there are limitations on how far the extrapolation can be pushed. The other rate condition is also natural since we are interested in the case where converges to much faster than . These rate conditions are standard (see, e.g., de Haan and Ferreira,, 2007).

We already know from Theorem 1 that the causal Hill estimator is asymptotically normal. Thus, to show asymptotic normality of the extremal QTE estimator in (9), the only remaining difficulty is that and can have different normalizing factors and convergence rates. This is problematic if the ratio of the normalizing factors oscillates. Zhang, (2018) encountered the same issue, and he followed the idea from Chernozhukov and Fernández-Val, (2011) to construct a feasible normalizing factor under the assumption that the ratio of normalizing factors converges. We proceed similarly. Specifically, based on Lemma 2, we introduce the following normalizing factor

| (10) |

and make the following assumption.

Assumption 5.

Assumption 5 states that the tails of the potential outcome distributions are either comparable or that one of them is heavier than the other. This is a fairly standard assumption satisfied by many models.

Using the normalizing factor (10), we can show asymptotic normality of the extremal QTE estimator.

Theorem 3.

Due to the asymptotic bias of (see Theorem 2), there is also an asymptotic bias of the extremal QTE estimator , which affects the validity of our later proposed confidence interval (see (12)). This asymptotic bias equals if . Recall that by the second-order regular variation assumption (see Assumption 3), so holds if grows not too fast. The rate at which tends to zero is unknown, and we therefore advise being conservative in the sense that one should choose (or equivalently, ) rather small in practice to ensure that , and hence the asymptotic bias is negligible.

3.3 Variance Estimation and Confidence Intervals

In order to conduct statistical inference based on Theorem 3, a consistent estimator of the asymptotic variance is needed. The main difficulty in estimating lies in estimating the corresponding matrix , which is the limit of the covariance matrices of the influence functions. Recall from Remark 1 that these influence functions contain terms describing the information gain from nonparametric estimation of the propensity score. Firpo, (2007) encountered a similar issue and he proposed a nonparametric regression approach to estimate the contribution of the information gain to the variance. In this paper, however, we will not go in this direction. Instead, we show that under suitable assumptions, the information gain for the proposed extremal QTE estimator is actually negligible, which can simplify the covariance matrix needed to be estimated, and thus a simpler and computational cheaper method can be proposed. Specifically, we require the following assumption:

Assumption 6.

For

where

Lemma 9 in the Supplementary Material shows that both and are of order . Hence Assumption 6 holds under suitable integrability conditions, and Section C in the Supplementary Material presents a concrete example where it is satisfied. We propose the following variance estimator

| (11) |

where

and is defined in (24) and its entries are estimated using inverse propensity score weighting; see Section D of the Supplementary Material for the for details. The following result shows that this estimator is consistent.

Theorem 4.

Based on Theorem 3 and the variance estimator (11), we propose the following approximate confidence interval of the extremal QTE:

| (12) |

where is the normalization constant in (10) and is the -quantile of the standard normal distribution.

Since Assumption 6 only affects the information gain terms in the covariance matrix and these terms reduce the variance, even Assumption 6 does not hold, the variance estimator is conservative, in the sense that it is still consistent to some quantity (see (22) and the proof of Theorem 4) that is larger than the true variance ; see Lemma 3 below. Therefore, even if Assumption 6 does not hold, it is safe to use our estimator .

4 Simulations

We conducted simulations to examine the finite sample behavior of our proposed extremal QTE estimator (9) and the related confidence interval (12), and to compare them to other methods. All simulations were carried out in R and the code is available at Github.

4.1 Simulation Set-up

Throughout the simulation study, we consider univariate covariate as Zhang, (2018). Specifically, let and be uniformly distributed random variables on and assign the treatment by with propensity score . We generate the outcomes from the following three models:

where follows a Student-t distribution with degrees of freedom, is Fréchet distributed with shape parameter , location and scale , and is Pareto distributed with shape parameter and scale .

The EVIs of the potential outcome distributions are for model and and for model . For model , a small calculation yields . Models and are more heavy-tailed than .

We consider data sets with sample size and aim to estimate the -QTE with . Throughout, the target coverage for the confidence intervals is (i.e., ). For all bootstrap based methods, we use bootstrapped data sets. The empirical squared error and coverage are calculated based on sampled data sets.

4.2 Implemented Methods

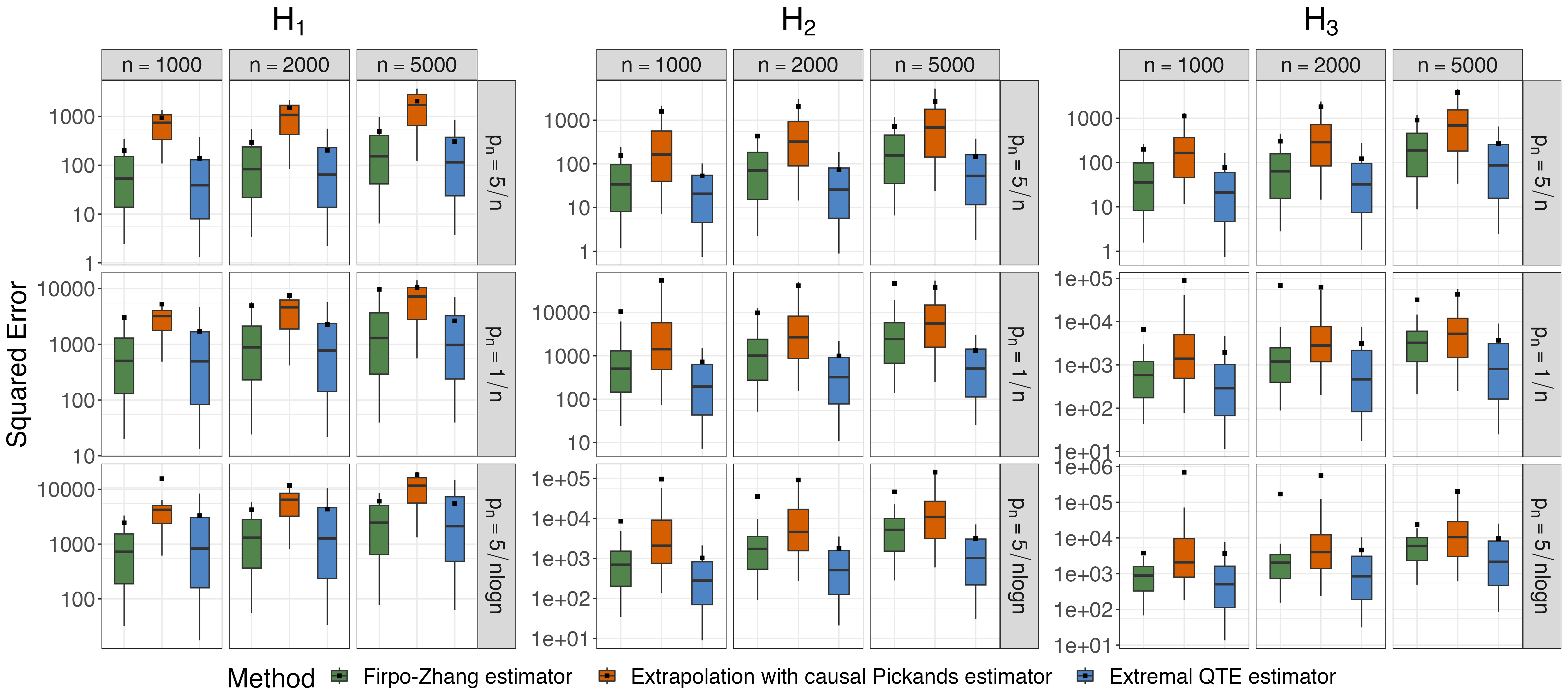

For point estimation of the extremal QTE, we compare the squared errors of three methods:

- •

-

•

Extrapolation with a causal Pickands estimator:

(13) where

This estimator is based on quantile extrapolation with the causal Pickands EVI estimator proposed in the supplementary materials of Zhang, (2018).

-

•

Extremal QTE estimator (see (9)): our proposed estimator based on quantile extrapolation with the causal Hill EVI estimator.

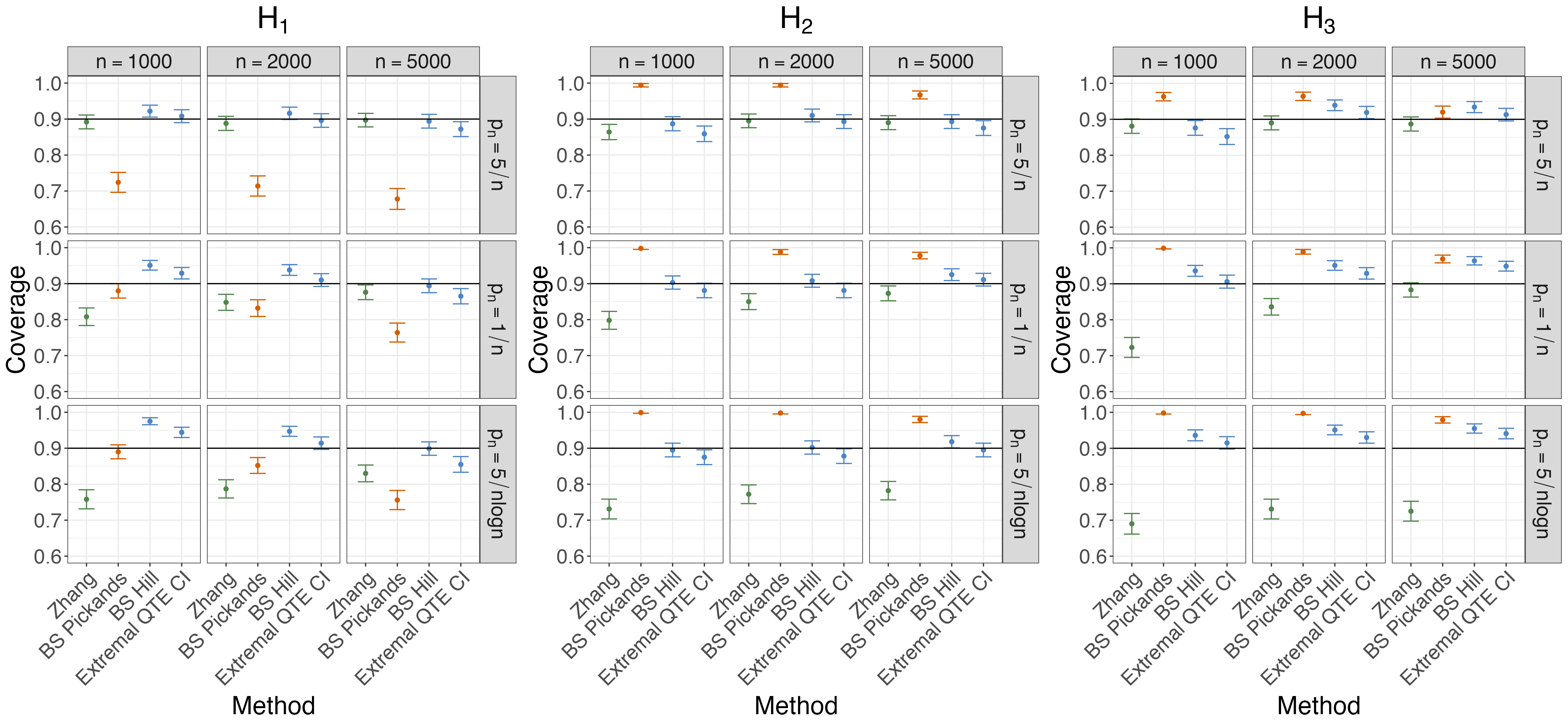

For the confidence interval of the extremal QTE, we compare the empirical coverages of the following four methods:

- •

-

•

BS Pickands: a bootstrap based method with the bootstrap confidence interval

(14) where is the point estimate (13) of the extremal QTE based on the full sample and is the estimated standard deviation of this estimate via the non-parametric bootstrap.

- •

-

•

Extremal QTE CI: our proposed confidence interval (12).

For the intermediate quantile level of the extrapolation based methods, we use . This value guarantees that all rate assumptions about and in Theorems 3 and 4 are satisfied. An additional sensitivity analysis can be found in Section E.3 of the Supplementary Material. We note that may not be optimal in all settings, and we use it in our simulations mostly for convenience. Choosing the optimal data-dependent is a difficult problem in extreme value theory. In practice, we recommend choosing it by plotting the estimates using different and selecting the in the first stable region of the plot (e.g., Resnick 2007). Please also see the real data application in Section 5 for an illustration of this approach.

For the size of sieve basis functions in the propensity score estimation, we use . Note that this choice is only for the case of univariate , and please see Section B of the Supplementary Material for some justifications about this choice. Specifically, we have and . In practice, people may choose the sieve basis functions according to their specific problem and use model selection methods such as cross-validation. Please see the real data application in Section 5 for an illustration.

4.3 Simulation Results

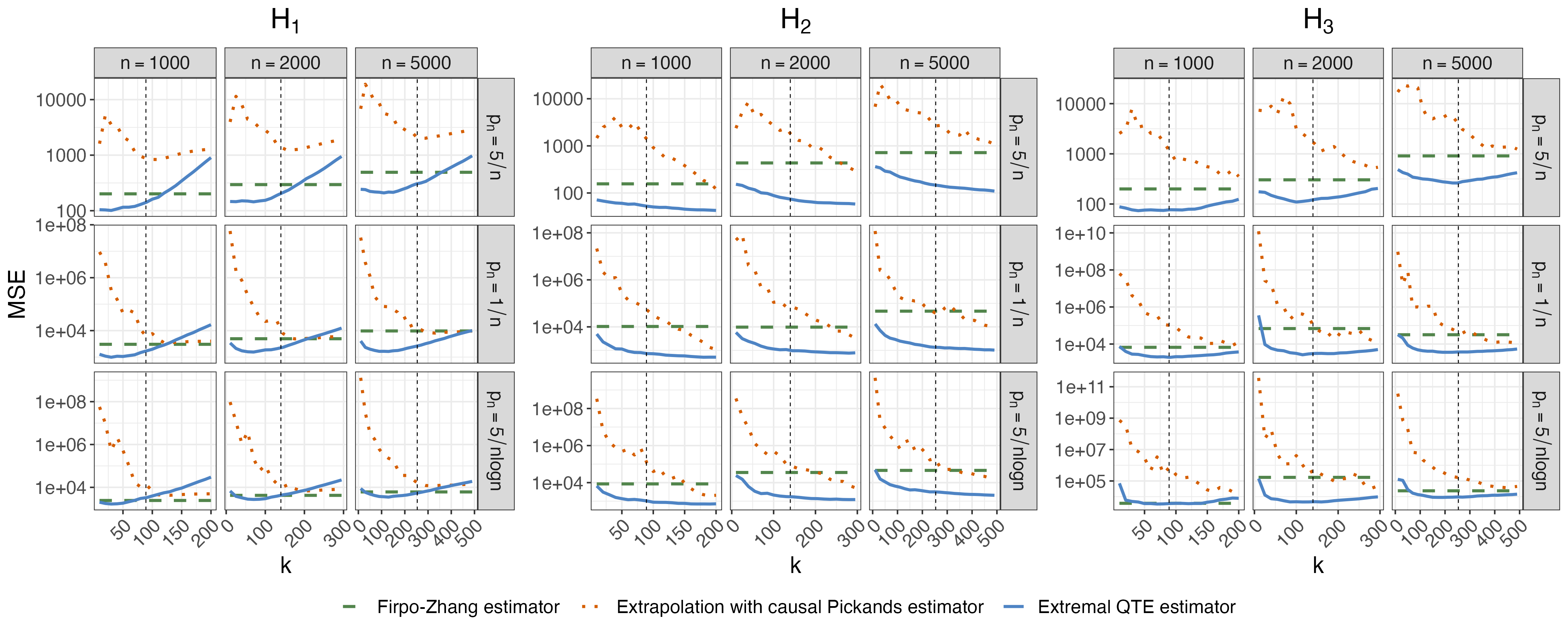

The squared errors of the point estimates are shown in Figure 2. We see that our proposed extremal QTE estimator generally performs better than the other two methods. In particular, it exhibits the lowest mean squared error (MSE) over almost all settings. This is especially true for the more heavy-tailed models and , in which our method greatly outperforms the others. The extrapolation based method using the Pickands EVI estimator has the worst performance, which is not surprising as the Pickands estimator is known to suffer from high variance in heavy-tailed settings. This also indicates that choosing a suitable EVI estimator is crucial for the extrapolation based method.

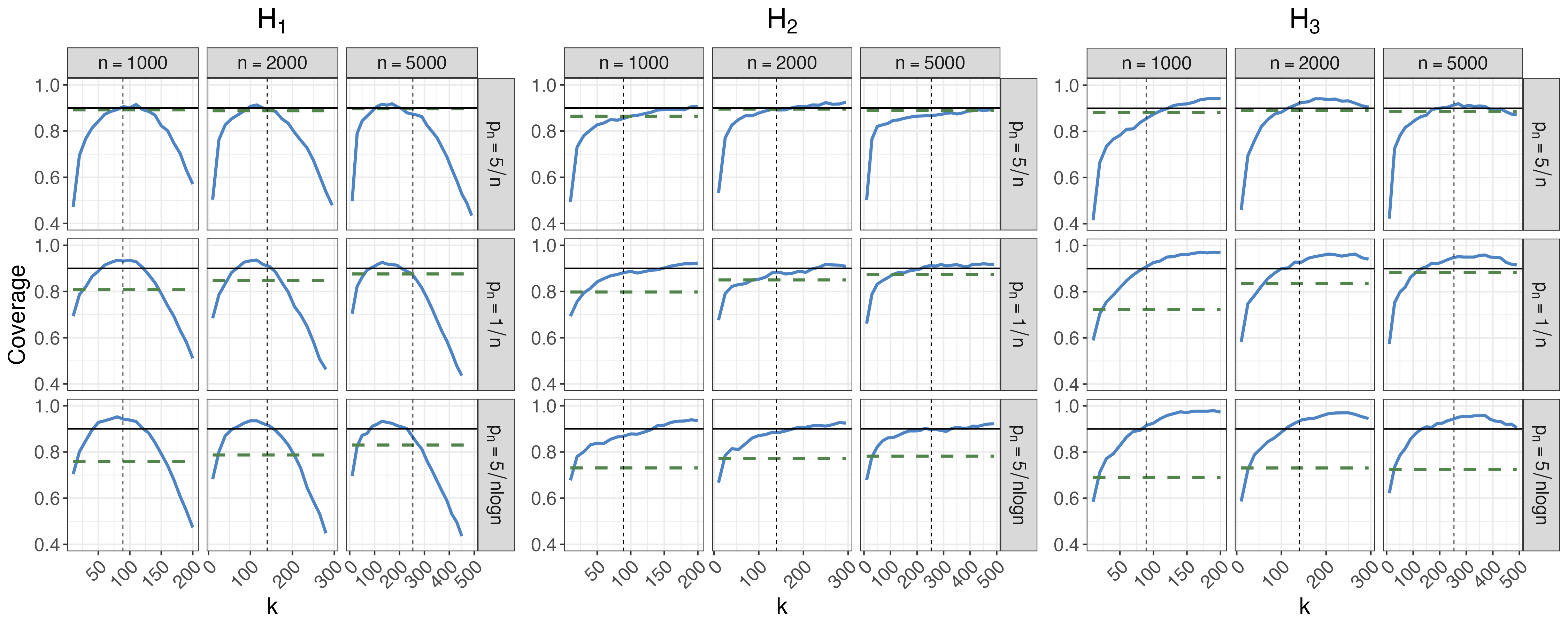

Figure 3 compares the empirical coverage of the different confidence intervals. We see that “Zhang” performs quite well for the not so extreme quantile level , but that it can undercover largely when the quantile index becomes more extreme. Such results were expected as this method is designed for the moderately extreme case where , and not for the extreme case where . The bias of the Firpo–Zhang estimator in the extreme case could be a reason for this undercoverage. We see that “BS Pickands” may suffer from both undercoverage (e.g., setting of ) and overcoverage (e.g., setting of ). In comparison, “BS Hill” and our proposed confidence interval “Extremal QTE CI” perform better, with empirical coverage close to the nominal level. The performance of “BS Hill” shows that the bootstrap based method may be valid, and it would be interesting to formalize this in future research. Compared to “BS Hill”, “Extremal QTE CI” has computational advantage, as it does not require bootstrapping the data.

5 Extremal Quantile Treatment Effect of College Education on Wages

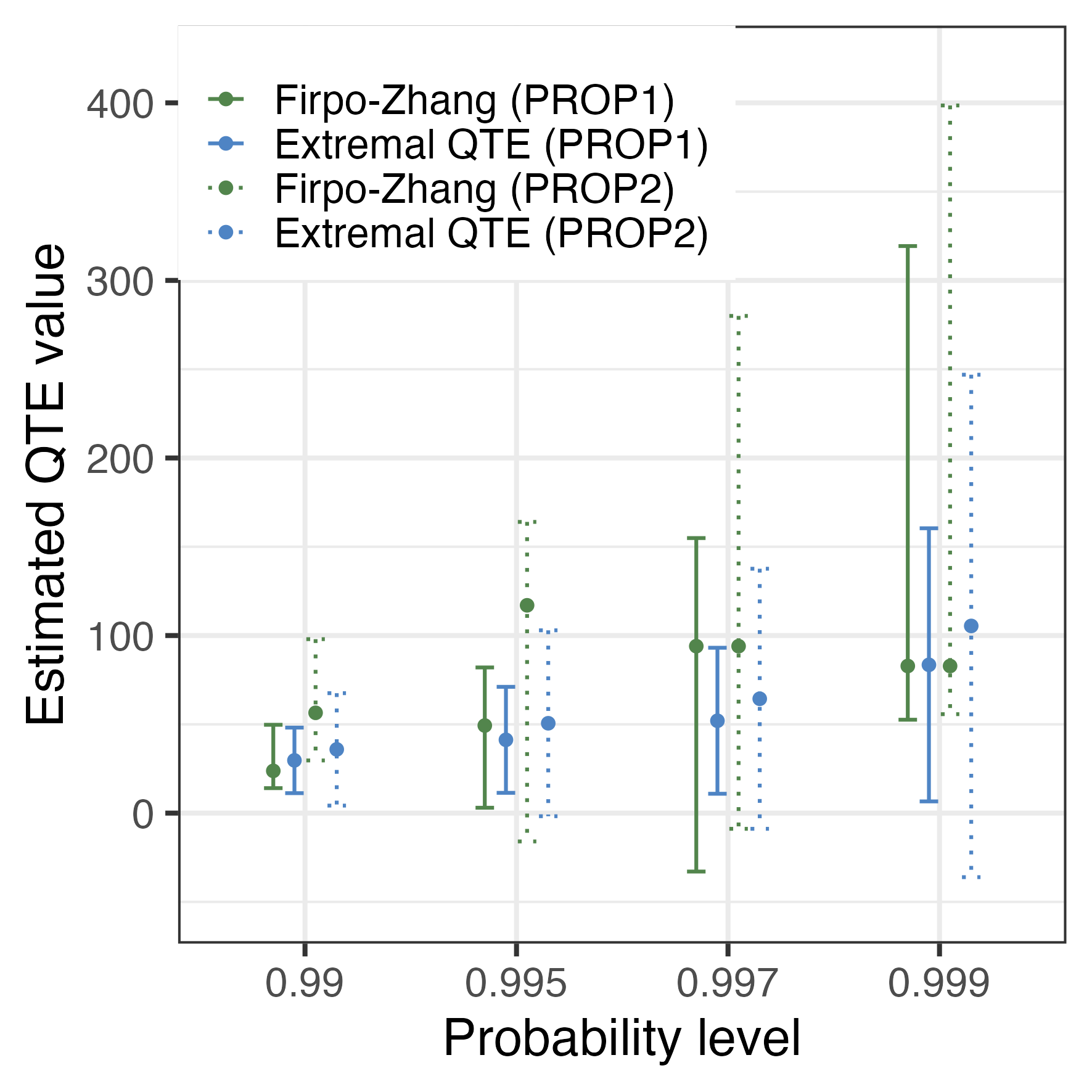

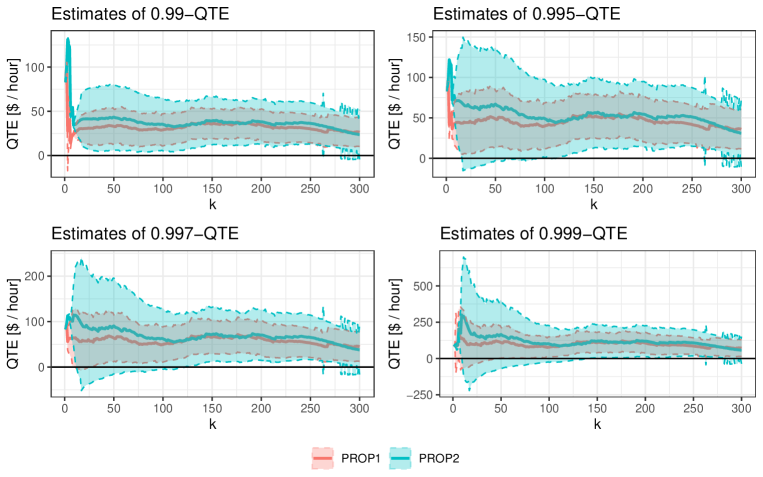

The causal effect of education on wage has been studied extensively in the literature (e.g., Card,, 1995; Heckman and Vytlacil,, 1998; Card,, 1999; Messinis,, 2013; Heckman et al.,, 2018). It is well-known that wage exhibits heavy-tailed behavior, and there can be considerable confounding between education and wage (e.g., Griliches,, 1977; Heckman et al.,, 2006). In this section, we apply our method to obtain point estimates and confidence intervals of the extremal QTE of college education on wage in the upper tail of the distribution, where we focus on the 0.99, 0.995, 0.997 and 0.999-QTEs. As comparison, we also implement the Firpo–Zhang estimator and the out of bootstrap confidence interval of Zhang, (2018).

We use data from the National Longitudinal Survey of Youth (NLSY79). It consists of a representative sample of young Americans who were between 14 and 21 years old at the time of the first interview in 1979, and contains a wide range of information about education, adult income, parental background, test scores and behavioral measures of the study participants. In particular, we use the NLSY79 data analyzed by Heckman et al., (2006, 2018), which is available from https://www.journals.uchicago.edu/doi/suppl/10.1086/698760. This data set consists of male participants who finished their education before the age of and were not in the military. We only consider participants that graduated from high school. The same (or similar) data set was also used in other literature (e.g., Brand and Xie,, 2010; Cheng et al.,, 2021; Zhou,, 2022).

The outcome is the hourly wage (in US dollar) at age , and the treatment equals if the person did not receive any college education, and otherwise. For the covariates used for propensity score estimation, we follow Heckman et al., (2018) and consider race, region of residence in 1979, urban status in 1979, broken home statue, age in 1979, number of siblings, family income in 1979, education (highest grade completed) of father and mother, scores from the Armed Services Vocational Aptitude Battery (ASVAB) test, and GPAs from 9th grade core subjects (language, math, science and social science). This leads to covariates in total as some of the variables are categorical. We omit samples with missing values, leading to a data set with samples, among which went to college. In this data set, the 0.99, 0.995, 0.997 and 0.999 quantiles of hourly wage are 50.47, 60.72, 85.50 and 154.73 US dollar, respectively.

For the propensity score estimation, considering that there are covariates and the sample size is , we refrain from using too many high-order terms in the sieve method to avoid overfitting. In particular, we consider two approaches. The first approach, which we refer to as PROP1, uses only linear terms, leading to sieve basis functions with . This approach is equivalent to logistic regression, which is widely used in practice for the propensity score estimation, and is the default option in many packages (Olmos and Govindasamy,, 2015). The second approach, which we refer to as PROP2, allows second-order terms and uses model selection to avoid overfitting. Specifically, we first apply a model selection procedure on the covariates. Then, we do another round of model selection, allowing only first- and second- order terms of all covariates that were selected in the first step. Both model selection steps are implemented using the R package glmulti (Calcagno and de Mazancourt,, 2010) with Akaike’s information criteria and a genetic search algorithm. The resulting model of PROP2 can be found in Section F.1 of the Supplementary Material. We use the same estimated propensity scores for all methods, and we mention that with a larger sample size, one may consider to use more higher-order terms in the sieve method for the propensity score estimation.

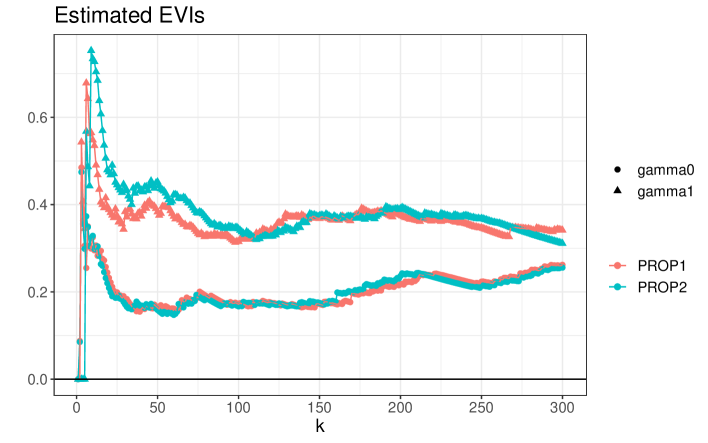

To select the tuning parameter for our method, here we use the approach of plotting the estimated EVI and QTE versus and then choose from the first stable region (e.g., Resnick,, 2007). The corresponding plots can be found in Section F.2 of the Supplementary Material. Based on these plots, we choose . Note that the choice used in Section 4 leads to , resulting in similar confidence intervals as using .

Figure 4 presents the results of the different methods. Considering the point estimate, we see that both Firpo–Zhang and our method give positive QTE estimates, but the corresponding values are quite different in some cases. In particular, the estimated values of Firpo–Zhang are not monotonically increasing when the quantile levels become more extreme, whereas ours are monotonic for these data. Such monotonicity implies that college education would have a stronger effect on wages for higher quantiles, which seems possible.

The confidence intervals of both methods mostly lie on the positive part, showing strong evidence that the QTEs are positive. The intervals of our method are considerably narrower than Zhang’s out of bootstrap intervals for the 0.997- and 0.999-QTEs, a clear advantage of our methodology. We also observe that the propensity scores estimated by the second approach lead to wider confidence intervals in all cases.

At last, we would like to note that the unconfoundedness assumption can not be verified in practice. For example, one may suspect that cognitive ability is not explicitly controlled for in this data example, so the unconfoundedness assumption may not hold. But since we have controlled for many important related covariates, we think that the unconfoundedness assumption is still a suitable approximation. For more discussion we refer to Brand and Xie, (2010).

6 Discussion

We propose a method to estimate the extremal QTE of a binary treatment on a continuous outcome for heavy-tailed distributions under the unconfoundedness assumption. Our method, which we call the extremal QTE estimator, builds on the quantile extrapolation approach from extreme value theory. We use the inverse propensity score weighted intermediate quantile estimates of Firpo, (2007) and our newly proposed causal Hill estimator to extrapolate to extreme quantiles. We show the asymptotic normality of the causal Hill estimator and the extremal QTE estimator. In particular, asymptotic normality of the extremal QTE estimator holds for extremal -QTEs, where may converge to . This is particularly important since it represents a common setting in risk assessment where the quantities of interest are beyond the range of the data. To the best of our knowledge, our approach is the first that achieves this. We also develop an estimator for the asymptotic variance which is consistent under suitable assumptions. This enables us to construct confidence intervals for the extremal QTEs. Simulations show that our method generally performs well.

As mentioned before, there is an asymptotic bias term of our proposed extremal QTE estimator (see Theorem 3), which is due to the asymptotic bias of the causal Hill estimator . In this paper, we suggest choosing a sufficiently small so that the asymptotic bias is negligible. It would be interesting and desired to formally propose bias-corrected versions of and in future research.

One potential issue of introducing inverse propensity score weighting to EVI estimators is that it complicates the estimation of the asymptotic variance, making statistical inference difficult. Bootstrap methods can be useful in practice for constructing confidence intervals for QTEs, as our simulation results suggest. It is important to study the theoretical validity of such bootstrap based methods in future research. In particular, it would be interesting to investigate whether the bootstrap based methods are valid even without Assumption 6.

The proposed method is just the first step towards the goal of doing causal inference for extremes. The considered causal inference setting is the most common and simplest one: binary treatment with assumed unconfoundedness. We believe that it is possible to extend it in many ways to fit a range of applications. For example, it would be interesting to generalize our method to categorical and continuous treatment settings by using the generalized propensity score (Imbens,, 2000). One may also consider extending our method to other causal inference settings, such as instrumental variable settings that allow for some types of confounding. At last, quantile extrapolation is not limited to heavy-tailed distributions, and it would be interesting to extend our proposed extremal QTE estimator to other settings where the potential outcome distributions may have lighter tails.

Acknowledgments

Sebastian Engelke was supported by an Eccellenza grant of the Swiss National Science Foundation.

References

- Alves et al., (2007) Alves, M. F., Gomes, M. I., De Haan, L., and Neves, C. (2007). A note on second order conditions in extreme value theory: linking general and heavy tail conditions. REVSTAT Statistical Journal, 5(3):285–304.

- Athey et al., (2021) Athey, S., Bickel, P. J., Chen, A., Imbens, G., and Pollmann, M. (2021). Semiparametric estimation of treatment effects in randomized experiments. Technical report, National Bureau of Economic Research.

- Boucheron and Thomas, (2015) Boucheron, S. and Thomas, M. (2015). Tail index estimation, concentration and adaptivity. Electronic Journal of Statistics, 9(2):2751–2792.

- Brand and Xie, (2010) Brand, J. E. and Xie, Y. (2010). Who benefits most from college? evidence for negative selection in heterogeneous economic returns to higher education. American sociological review, 75(2):273–302.

- Bubeck, (2015) Bubeck, S. (2015). Convex optimization: Algorithms and complexity. Foundations and Trends® in Machine Learning, 8(3-4):231–357.

- Calcagno and de Mazancourt, (2010) Calcagno, V. and de Mazancourt, C. (2010). glmulti: An r package for easy automated model selection with (generalized) linear models. Journal of Statistical Software, 34(12):1–29.

- Card, (1995) Card, D. (1995). Using geographic variation in college proximity to estimate the return to schooling. pages 201–222. In Aspects of Labour Market Behaviour: Essays in Honour of John Vanderkamp (Louis N. Christofides, E. Kenneth Grant and Robert Swidinsky, eds.).

- Card, (1999) Card, D. (1999). The causal effect of education on earnings. Handbook of Labor Economics, 3:1801–1863.

- Cheng et al., (2021) Cheng, S., Brand, J. E., Zhou, X., Xie, Y., and Hout, M. (2021). Heterogeneous returns to college over the life course. Science advances, 7(51):eabg7641.

- Chernozhukov, (2005) Chernozhukov, V. (2005). Extremal quantile regression. The Annals of Statistics, 33(2):806–839.

- Chernozhukov and Fernández-Val, (2011) Chernozhukov, V. and Fernández-Val, I. (2011). Inference for extremal conditional quantile models, with an application to market and birthweight risks. The Review of Economic Studies, 78(2):559–589.

- Chernozhukov et al., (2016) Chernozhukov, V., Fernández-Val, I., and Kaji, T. (2016). Extremal quantile regression: An overview. In Handbook of Quantile Regression (R. Koenker, V. Chernozhukov, X. He, and L. Peng, eds.). Chapman and Hall.

- de Haan, (1970) de Haan, L. (1970). On Regular Variation and Its Application to the Weak Convergence of Sample Extremes. Number 63 in Mathematical Centre tracts. Mathematisch Centrum.

- de Haan and Ferreira, (2007) de Haan, L. and Ferreira, A. (2007). Extreme Value Theory: An Introduction. Springer Series in Operations Research and Financial Engineering. New York: Springer New York.

- Dessì et al., (2018) Dessì, A., Corona, L., Pintus, R., and Fanos, V. (2018). Exposure to tobacco smoke and low birth weight: from epidemiology to metabolomics. Expert Review of Proteomics, 15(8):647–656.

- Doksum, (1974) Doksum, K. (1974). Empirical probability plots and statistical inference for nonlinear models in the two-sample case. The Annals of Statistics, 2(2):267–277.

- Drees and Kaufmann, (1998) Drees, H. and Kaufmann, E. (1998). Selecting the optimal sample fraction in univariate extreme value estimation. Stochastic Processes and their Applications, 75(2):149–172.

- Durrett, (2013) Durrett, R. (2013). Probability: Theory and Examples, volume 4.1. Cambridge: Cambridge University Press.

- Easterling et al., (2016) Easterling, D. R., Kunkel, K. E., Wehner, M. F., and Sun, L. (2016). Detection and attribution of climate extremes in the observed record. Weather and Climate Extremes, 11:17–27. Observed and Projected (Longer-term) Changes in Weather and Climate Extremes.

- Embrechts et al., (1997) Embrechts, P., Klüppelberg, C., and Mikosch, T. (1997). Modelling Extremal Events: for Insurance and Finance. Springer, London.

- Firpo, (2007) Firpo, S. (2007). Efficient semiparametric estimation of quantile treatment effects. Econometrica, 75(1):259–276.

- Gissibl and Klüppelberg, (2018) Gissibl, N. and Klüppelberg, C. (2018). Max-linear models on directed acyclic graphs. Bernoulli, 24(4A):2693–2720.

- Gissibl et al., (2018) Gissibl, N., Klüppelberg, C., and Otto, M. (2018). Tail dependence of recursive max-linear models with regularly varying noise variables. Econometrics and Statistics, 6:149 – 167.

- Gnecco et al., (2021) Gnecco, N., Meinshausen, N., Peters, J., and Engelke, S. (2021). Causal discovery in heavy-tailed models. The Annals of Statistics, 49(3):1755–1778.

- Griliches, (1977) Griliches, Z. (1977). Estimating the returns to schooling: Some econometric problems. Econometrica: Journal of the Econometric Society, 45(1):1–22.

- Hannart et al., (2016) Hannart, A., Pearl, J., Otto, F. E. L., Naveau, P., and Ghil, M. (2016). Causal counterfactual theory for the attribution of weather and climate-related events. Bulletin of the American Meteorological Society, 97(1):99–110.

- Heckman and Vytlacil, (1998) Heckman, J. and Vytlacil, E. (1998). Instrumental variables methods for the correlated random coefficient model: Estimating the average rate of return to schooling when the return is correlated with schooling. Journal of Human Resources, 33(4):974–987.

- Heckman et al., (2018) Heckman, J. J., Humphries, J. E., and Veramendi, G. (2018). Returns to education: The causal effects of education on earnings, health, and smoking. Journal of Political Economy, 126(S1):S197–S246.

- Heckman et al., (2006) Heckman, J. J., Stixrud, J., and Urzua, S. (2006). The effects of cognitive and noncognitive abilities on labor market outcomes and social behavior. Journal of Labor economics, 24(3):411–482.

- Hill, (1975) Hill, B. M. (1975). A simple general approach to inference about the tail of a distribution. The Annals of Statistics, 3(5):1163–1174.

- Hirano et al., (2003) Hirano, K., Imbens, G. W., and Ridder, G. (2003). Efficient estimation of average treatment effects using the estimated propensity score. Econometrica, 71(4):1161–1189.

- Hua and Joe, (2011) Hua, L. and Joe, H. (2011). Second order regular variation and conditional tail expectation of multiple risks. Insurance: Mathematics and Economics, 49(3):537–546.

- Imbens, (2000) Imbens, G. W. (2000). The role of the propensity score in estimating dose-response functions. Biometrika, 87(3):706–710.

- Jana et al., (2021) Jana, K., Bhuyan, P., and McCoy, E. J. (2021). Causal analysis at extreme quantiles with application to london traffic flow data.

- Kosorok, (2007) Kosorok, M. R. (2007). Introduction to empirical processes and semiparametric inference. New York: Springer Science & Business Media.

- Lehmann and D’Abrera, (1975) Lehmann, E. L. and D’Abrera, H. J. (1975). Nonparametrics: statistical methods based on ranks. Toronto: Holden-Day.

- Lorentz, (1966) Lorentz, G. (1966). Approximation of functions. New York: Holt, Rinehart and Winston.

- Madakumbura et al., (2021) Madakumbura, G. D., Thackeray, C. W., Norris, J., Goldenson, N., and Hall, A. (2021). Anthropogenic influence on extreme precipitation over global land areas seen in multiple observational datasets. Nature Communications, 12(1):1–9.

- Matthys et al., (2004) Matthys, G., Delafosse, E., Guillou, A., and Beirlant, J. (2004). Estimating catastrophic quantile levels for heavy-tailed distributions. Insurance: Mathematics and Economics, 34(3):517–537.

- Messinis, (2013) Messinis, G. (2013). Returns to education and urban-migrant wage differentials in china: IV quantile treatment effects. China Economic Review, 26:39–55.

- Mhalla et al., (2020) Mhalla, L., Chavez-Demoulin, V., and Dupuis, D. J. (2020). Causal mechanism of extreme river discharges in the upper Danube basin network. Journal of the Royal Statistical Society: Series C (Applied Statistics), 69(4):741–764.

- Naveau et al., (2020) Naveau, P., Hannart, A., and Ribes, A. (2020). Statistical methods for extreme event attribution in climate science. Annual Review of Statistics and its Application, 7(1):89–110.

- Naveau et al., (2018) Naveau, P., Ribes, A., Zwiers, F., Hannart, A., Tuel, A., and Yiou, P. (2018). Revising return periods for record events in a climate event attribution context. Journal of Climate, 31(9):3411–3422.

- Newey, (1994) Newey, W. K. (1994). The asymptotic variance of semiparametric estimators. Econometrica: Journal of the Econometric Society, 62(6):1349–1382.

- Olmos and Govindasamy, (2015) Olmos, A. and Govindasamy, P. (2015). Propensity scores: a practical introduction using r. Journal of MultiDisciplinary Evaluation, 11(25):68–88.

- Resnick, (2007) Resnick, S. I. (2007). Heavy-tail phenomena: probabilistic and statistical modeling. New York: Springer Science & Business Media.

- Resnick, (2008) Resnick, S. I. (2008). Extreme Values, Regular Variation and Point Processes. Springer, New York.

- Rosenbaum and Rubin, (1983) Rosenbaum, P. R. and Rubin, D. B. (1983). The central role of the propensity score in observational studies for causal effects. Biometrika, 70(1):41–55.

- van Oldenborgh et al., (2017) van Oldenborgh, G. J., van der Wiel, K., Sebastian, A., Singh, R., Arrighi, J., Otto, F., Haustein, K., Li, S., Vecchi, G., and Cullen, H. (2017). Attribution of extreme rainfall from hurricane harvey, august 2017. Environmental Research Letters, 12(12):124009.

- Wang et al., (2012) Wang, H. J., Li, D., and He, X. (2012). Estimation of high conditional quantiles for heavy-tailed distributions. Journal of the American Statistical Association, 107(500):1453–1464.

- Xu et al., (2022) Xu, W., Wang, H. J., and Li, D. (2022). Extreme quantile estimation based on the tail single-index model. Statistica Sinica, 32:893–914.

- Zhang, (2018) Zhang, Y. (2018). Extremal quantile treatment effects. The Annals of Statistics, 46(6B):3707–3740.

- Zhou, (2022) Zhou, X. (2022). Attendance, completion, and heterogeneous returns to college: A causal mediation approach. Sociological Methods & Research, page 00491241221113876.

The supplementary material consists of the following seven sections.

- A

-

Details of the estimated propensity score using sieve method

- B

-

Regularity assumptions for sieve estimation and the central limit theorem

- C

-

Examples satisfying Assumption 6

- D

-

Details of Variance Estimation

- E

-

Supplementary material for simulations

- F

-

Supplementary material for real application

- G

-

Proofs

Appendix A Details of the estimated propensity score using sieve method

Suppose that we observe independent copies of . The main idea of the sieve method is to approximate the logit of the propensity score by a linear combination of sieve basis functions, and then estimate the propensity score by

| (15) |

where is a vector consisting of sieve basis functions, and

| (16) |

and is the sigmoid function.

Let be a vector consisting of sieve basis functions. Following Hirano et al., (2003) and Firpo, (2007), we use polynomials as the sieve basis functions in this paper. In particular, we require that and for all such that , the span of contains all polynomials up to order . For an illustration purpose, some possible examples for are or . The crucial point in sieve estimation is that the dimension of the sieve space grows to infinity at an appropriate speed with the sample size . In other words, with larger sample size, one may consider a more complex model for the estimation.

Appendix B Regularity assumptions for sieve estimation and the central limit theorem

For sieve estimation, we require certain regularity assumptions:

Assumption 7.

-

i)

is continuous and has density such that .

-

ii)

is -times continuously differentiable with all the derivatives bounded, where and denotes the dimension of .

-

iii)

is -times continuously differentiable in with all derivatives bounded by some uniformly over , where .

-

iv)

Let 111For any vector or matrix , the norm .. We assume , and .

In Assumption 7, i) and ii) are standard assumptions for sieve estimation. iii) and iv) were introduced by Zhang, (2018) for the intermediate quantile estimation, and we refer to Zhang, (2018) for more discussions about these two assumptions.

Newey, (1994) showed that if consists of orthonormal polynomials, then . In this case, if for some positive constants , Assumption 7 is equivalent to , , and . In particular, since and , this assumption holds if we have and sufficient smoothness.

Below we present the regularity assumptions for the central limit theorem.

Assumption 8.

There exist real numbers such that

Assumption 9.

There exist real numbers and such that

where

Appendix C Examples satisfying Assumption 6

Example 1.

Let be a random vector and let , , be functions satisfying almost surely for some real numbers such that . Let be random variables independent of and let potential outcome

Let be the distribution function of . Suppose that satisfies the second-order regular variation condition with extreme value index and second-order parameter . Then satisfies the second-order regular variation condition with the same parameters , , and Assumption 6 is met.

We give two concrete examples for the distribution of in Example 1.

Example 2.

The first example is the Student -distribution. Let be the CDF of the Student -distribution with degrees of freedom. It is known that satisfies the second-order regular-variation condition with first-order parameter and second-order parameter (see e.g. Example 3 in Hua and Joe, (2011)). Therefore, by Theorem 2.3.9 in de Haan and Ferreira, (2007), is of second-order regular variation with extreme value index and second-order parameter . One special case is the Cauchy distribution for .

Example 3.

Another example is the Fréchet model for . It is known that satisfies the second-order regular variation condition with first order parameter and second-order parameter (see e.g. Example 4.2 in Alves et al., (2007)). Thus, by Theorem 2.3.9 in de Haan and Ferreira, (2007), is of second-order regular variation with extreme value index and second-order parameter .

Lemma 4.

Let be a random vector and let be a function satisfying almost surely for some real numbers such that . Let be a random variable such that and let . Denote the CDFs of and by and , respectively. Suppose that is of second-order regular variation with extreme value index and second-order parameter . Then, is of second-order regular variation with extreme value index and second-order parameter . In addition, for , we have

| (17) |

and

| (18) |

Proof of Lemma 4.

First, since replacing by does not change the CDF of or on , we can assume without loss of generality that .

By Theorem 2.3.9 in de Haan and Ferreira, (2007), being second-order regular variation with extreme value index and second-order parameter is equivalent to being second-order regular variation with first-order parameter and second-order parameter . Therefore, equation (25) in Hua and Joe, (2011) implies that is of second-order regular variation with parameters and , given the condition that there exists such that , The required condition holds in our case because for all . Theorem 2.3.9 in de Haan and Ferreira, (2007) then implies that is second-order regularly varying with parameters and .

Now we prove claim (17).

First, since , we have , and thus for all ,

and

Because is of second-order regular variation with first-order parameter , we have

which implies

| (19) |

Since , we have that for ,

Now we prove claim (18).

We have that almost surely,

| (20) | ||||

For the first term, since is uniformly distributed, we have that follows a standard exponential distribution. Thus

Based on (19), we have that is of order , and thus

For the second term, we have

Since is of second-order regular variation, we have that , and it follows that

Combining this with (19) yields

Appendix D Details of Variance Estimation

The true variance in Theorem 3 is , where we denote the true covariance matrix

| (21) |

where are defined according to Assumption 8. and , , , , are defined according to Assumption 9.

Let

| (22) |

with the simplified covariance matrix

| (23) |

where the entries are defined as the following limits:

Appendix E Supplementary material for simulations

E.1 Tuning parameters of Zhang’s out of bootstrap

For the tuning parameters of the out of bootstrap of Zhang, (2018), we use the same values as suggested in the paper. Specifically, for the subsample size , we follow the formula suggested in Section 5.5 of Zhang, (2018):

where . For sample sizes , we obtain .

For the spacing parameter and in the feasible normalizing factor, we use the formulas described in Section 5.5 of Zhang, (2018):

E.2 Q-Q plots

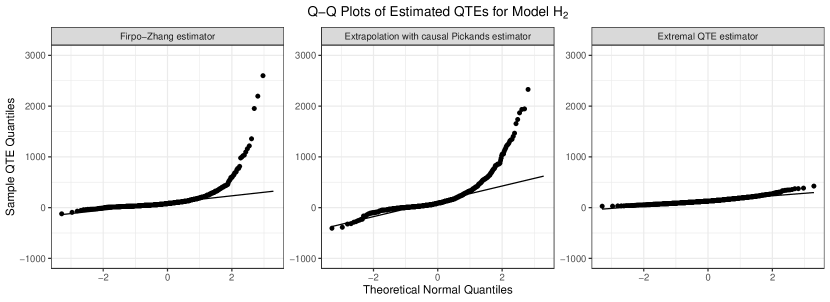

To empirically verify the asymptotic normality result of our extremal QTE estimator in Theorem 3, we show in Figure 5 its related normal Q-Q plot. As comparison, we also present the normal Q-Q plots for the extrapolation estimator with the causal Pickands estimator and the Firpo–Zhang estimator. The Q-Q plots of all settings are similar, thus we only present those of model with and as an example. From the plot, our proposed extremal QTE estimator is approximately normal, which empirically verifies Theorem 3. The other two estimators, however, appear not to be asymptotically normal. This is expected for the Firpo–Zhang estimator because Zhang, (2018) showed that this estimator is not asymptotically normal in the extreme case.

E.3 Dependency on

We implement simulations to investigate how the choice of the tuning parameter affects the MSE and the coverage of the extrapolation based extremal QTE estimators. We also present the result of the Firpo-Zhang estimator for MSE and Zhang’s out of bootstrap for coverage as comparison. The considered models , and are the same as in Section 4.

Figure 6 shows the simulation results about MSE. The MSE of the Firpo-Zhang estimator is a line because it does not depend on . From this figure, we can see that the value of has a big influence on the MSE of our extremal QTE estimator and the quantile extrapolation method with the causal Pickands estimator. In particular, a clear bias-variance trade-off with respect to is shown in the plots related to and . We also note that for the more heavy-tailed models and , our proposed method with the causal Hill estimator outperforms the Firpo-Zhang estimator for a wide range of values of .

Figure 7 shows the simulation results about coverage. The coverage of the Zhang’s out of bootstrap method is a line because it does not depend on . We can see that there is always a range of where our proposed confidence interval (12) has good coverage. The particular range, however, depends on the respective model. We also note that our method works well in terms of coverage for a wide range of for models .

The above observations generally agree with the observation from classical quantile extrapolation setting, see e.g. de Haan and Ferreira, (2007).

Appendix F Supplementary material for real application

F.1 The resulting model of PROP2

The resulting model of PROP2 is:

“college1+race+region+age80+mhgcmi+fhgcmi+

sasvab5+sasvab6+sgr9scoscigpa+sasvab2:mhgcmi+sasvab5:age80+sasvab5:sasvab2+

sasvab6:sasvab2+sgr9langgpa:age80+sgr9langgpa:mhgcmi+sgr9scoscigpa:age80+

race:age80+race:mhgcmi+region:age80+region:fhgcmi+region:sgr9scoscigpa”.

F.2 Plots of the estimated EVIs and QTEs with different

Figure 8 and 9 shows the plots of the estimated EVIs and QTEs versus the tuning parameter for the real data analyzed in Section 5, respectively. For Figure 8, and are denoted by triangular and circle, respectively. In both figures, the red and blue colors correspond to the results with the estimated propensity scores using PROP1 and PROP2 (see Section 5 for the details of these two approaches), respectively.

Appendix G Proofs

We mention again that unless otherwise stated, denotes the intermediate quantile which satisfies and . We will use notations and interchangeably for convenience.

G.1 Proof of Lemma 1

To prove Lemma 1, we first introduce Theorem 5, Lemma 5, Lemma 6, Lemma 7 and Lemma 8. Theorem 5 is a special case of Theorem 3.1 in Zhang, (2018), so we omit its proof.

Theorem 5.

Lemma 5 shows that for a CDF with positive extreme value index, the normalization sequence can be replaced by a simpler expression.

Lemma 5.

For , suppose Assumption 2 is met and has an extreme value index . Then

Proof of Lemma 5.

Lemma 6 is a classical result in causal inference literature, and we omit its proof.

Lemma 6.

Let be a measurable function such that and are finite. Suppose and there exists such that almost surely. Then we have

Lemma 7 gives the convergence rate of the estimated propensity score by using the sieve method.

Proof of Lemma 7.

By Assumption 7 , we have since . Therefore, we can apply Lemma 1 and 2 in Hirano et al., (2003) to obtain

The condition implies , and the Assumption 7 implies as . In addition, and implies . Combining the above rates, we have

In particular, we have The second part of the lemma then follows from the assumption that is continuous and bounded away from zero, which allows us to apply the continuous mapping theorem (see Theorem 7.25 in Kosorok, (2007)).

∎

Lemma 8 shows that the following two terms converge to zero in probability. This lemma will be used many times in the remaining proofs, so we prove it here.

Proof of Lemma 8.

We show the first part of the lemma, and the second part follows analogously. For simplicity of notation, we denote . So

| (26) | ||||

| (27) | ||||

| (28) |

by the triangle inequality. Now we show that both terms (27) and (28) converge to zero in probability, which then proves the original claim.

For the first term (27), we need the subgradient condition for (defined by (6)). Specifically, since

is convex, a necessary condition for is that where denotes the set of subgradients of at (for details see e.g. Bubeck, (2015)).

Because is a continuous random variable for , there exists at most one almost surely. In the first case where for all , the subgradient condition implies

In the second case where there exists some such that , we have

where is an interval and the set addition is understood elementwise. The subgradient condition then implies that there exists some such that

Hence

since .

Combining the above two cases, we have that almost surely

By Assumption 1, we have that . So by Lemma 7 we have

| (29) |

Because , we have

For the second term (28), the proof of Theorem 3.1 in Zhang, (2018) showed that the term

converges in distribution to a normal random variable (in particular, Zhang, (2018) proved the corresponding result for lower quantiles, but the same holds for upper quantiles). Hence, we have

∎

Now we give the proof of Lemma 1.

Proof of Lemma 1.

We show the claim for , and the case of can be proved analogously. First, we expand (defined by (7)) as

where

In the following, we will show that and that converge to zero in probability, which then proves the original claim.

Now we prove that . This part of the proof is similar to the proof of Theorem 3.2.2 in de Haan and Ferreira, (2007), which shows the consistency of the classical Hill estimator. First, we have

because .

Since is the CDF of , is uniformly distributed on . Let , so its CDF is for , which then implies that has a standard exponential distribution. Let be the tail function of . Then we have that and almost surely. Since , we have that almost surely

By Assumption 2 , satisfies the max-domain of attraction condition with extreme value index , so by Theorem 1.1.6 and Corollary 1.2.10 in de Haan and Ferreira, (2007), we have that for all ,

Then, by the statement 5 of the Proposition B.1.9 in de Haan and Ferreira, (2007), we have that for any such that , there exists some such that for , ,

which is equivalent to

For large enough and for such that , we can set and to obtain

Multiplying by on both sides of the above inequality and summing up all with gives us that almost surely, lies in the interval with

Since and can be arbitrarily small, to prove , it is enough to show

For (i), let and . We have

where at the second last equality we used Lemma 6, and

Thus, by the weak law for triangular array (see Theorem 2.2.4 in Durrett, (2013)), we have

or equivalently,

| (30) |

For (ii), let and . By the fact that has a standard exponential distribution, we have

Similarly, we have

Thus, by the weak law for triangular array, we have

| (31) |

This concludes that .

Now we prove that converge to zero in probability. For , let

so

Given the previous results (30) and the fact that almost surely, it is sufficient to show that . Consider

where is defined in Theorem 5. By Lemma 5, we have

and Theorem 5 implies that

Therefore,

and consequently

By the continuous mapping theorem,

| (32) |

Thus .

For , note that

thus

The last equality follows from Lemma 8 and the result (32) that . Since , we have .

∎

G.2 Proof of Theorem 1

Lemma 9.

Proof of Lemma 9.

We have already seen in the proof of Lemma 1 that follows a standard exponential distribution. Therefore, for , we have

Thus the first claim follows. Note that for positive , thus the second claim follows from the Markov inequality. ∎

Now we prove Theorem 1.

Proof of Theorem 1.

We show the claim for , and the case can be proved analogously. As in the proof of Lemma 1, we expend

where

In the following, we will show that

which then implies the original claim that

For , we proceed similarly as in the proof of Theorem 3.2.5 in de Haan and Ferreira, (2007). As shown in the proof of Lemma 1, we have that almost surely,

where and . By Assumption 3, we have for all ,

with , and . Equivalently, we have

By the proof of Theorem 3.2.5 in de Haan and Ferreira, (2007), there exists a function such that and for any , there exists such that for all , ,

For large enough and for such that , we can set and . Multiplying by on both sides of the above inequality and summing up all with gives us that almost surely,

| (33) |

where

Let . We first show that converge in probability to some constant. Since by assumption and , it is enough to show that

converge in probability to some constant.

Let and . By the fact that has probability density function on , we can calculate

and

Thus, by the weak law for triangular array, we have

which implies

Because can be arbitrarily close to zero, by inequality (33), we have that almost surely,

Similarly, by using the weak law for triangular array, one can obtain that

Hence, we conclude that almost surely,

| (34) |

For , similarly as in the proof of Lemma 1, we have

where and are defined as in Theorem 5, and we applied Theorem 5 to obtain the last equality. By applying the delta method, we have

| (35) |

Combining with result (30), we obtain

| (36) |

Note that by Theorem 5, we have .

For , similarly as in the proof of Lemma 1, we have

Theorem 5 and the result (35) then imply that

Thus, by Lemma 8 we have

| (37) |

For , we expand

For the second term, we have

by that fact that (see the comment below (36)) and Lemma 7. Hence, we obtain

Denote

then we have

where for the second last equality we used that

which can be shown by using a similar argument as on page 43. Thus, we have

where .

In order to derive the influence function which arises from using the estimated propensity score, we follow similar steps as in the proof of Theorem 3.1 of Zhang, (2018). First, we rewrite with

For , note that , so we have

where in the second inequality we used Assumption 1 and , and in the second last equality we used Lemma 7, result (29) and which can be obtained by the Markov inequality and Lemma 9. Thus .

For , we expand where

and denotes the CDF of .

First, we show . For this we consider

and the pseudo true propensity score , where is the vector consisting of sieve basis functions and is the sigmoid function (see Section B for more details). We rewrite with

and we show that both terms converge to in probability. For , note that

and thus . We also have

where for the last equality we applied Lemma 9 which gives and the Lemma 1 of Hirano et al., (2003) which gives with under Assumption 7. The convergence to can be obtained because Assumption 7 implies as . Therefore we have .

For , we use the Taylor expansion to get

with

where is random, lies on the line between and , and depends on resp. . For , we have

where the first inequality holds because the summands of are i.i.d. and with mean , the second inequality holds because , and , and for the last equality we used Lemma 9. Thus .

Note that the summands of and are no longer independent because of . Therefore, for and , we apply the triangle inequality to obtain

where we used similar arguments as for and the fact that . By the Markov inequality, we have

Under the Assumption 7, we have by the Lemma 2 in Hirano et al., (2003) that . Hence, by the Cauchy–Schwarz inequality, we have

By Assumption 7 iv) , we have and , thus , which concludes that .

At this point, we have . For , we proceed in a similar manner as for . First, we decompose with

For , we have

where the second last equality holds because and , and the last equality holds because Assumption 7 implies .

Hence, we have . For , we use the mean value theorem for to get

where lies on the line between and . Since is the solution of the optimization problem (16), the first order condition

can be derived by differentiation of the objective function. Extending

and applying the mean value theorem for leads to

where

We define

which allows us to write

Now we show that both terms and are .

For , using the mean value theorem for and the fact that , we have

where in the last equality we used and . In addition, Hirano et al., (2003) showed in the proof of their Theorem 1 that and , and the last result implies that by the Markov inequality. Therefore, by the submultiplicativity of Frobenius norm we have

where the last equality is implied by Assumption 7 .

For , we rewrite . From the proof of Theorem 3.1 in Zhang, (2018), we know that In addition, we have . Therefore,

where the last equality is implied by Assumption 7 .

Now we have . Let

we rewrite

where

Now we show that both terms and are .

For , from previous proofs we know that . In addition, Hirano et al., (2003) showed in the proof of their Theorem 1 that . Together with the fact that , we have . Since is bounded away from 0 and 1 by Assumption 1, using the mean value theorem and the triangular inequality give us

where the last equality follows from Assumption 7 .

For , first note that we can view as the least squares approximation of using the approximation functions . By Assumption 4 that is -times continuously differentiable with all derivatives bounded by on . Thus, similarly as the Lemma 1 in Hirano et al., (2003) which follows from the Theorem 8 on page 90 in Lorentz, (1966), it holds that

Hence, by the triangular inequality we have

where the last equality follows from Assumption 4 .

Therefore, we have

and consequently

| (38) |

G.3 Proof of Theorem 2

Proof of Theorem 2.

Let and let be its covariance matrix. For , we write with

We will apply the multidimensional Lindeberg CLT to prove the claim. We first show that the expectation of is a zero vector. For , we have

and

where the second equality follows from Lemma 6 and the last equality holds as which can be seen from the proof of Lemma 9. Thus we have . Analogously, one can show that .

Now we show that the covariance matrix converge to via showing entry-wise convergence. We first compute

where the second last equality is obtained by applying the law of iterated expectation and the last equality follows from Lemma 9. Similarly, we have

Thus

Analogously, we have

For the intersection terms between two potential outcome distributions, we have

Thus

At last, we have

Therefore, under Assumption 9 and 8, we have

The above results implies that

Now we verify the Lindeberg condition, that is, for any ,

Since on we have , we can bound

Thus, it is enough to show the Lyapunov type condition .

Recall that and . For any , we know from Lemma 9 that

In addition, it is easy to see that

Hence, for any , by the Cauchy-Schwarz inequality we have

Similar inequalities hold for all combinations of , , and .

Since is bounded away from and by Assumption 1, for

we can see by expanding all above terms that its rate is of order

which shows that the Lyapunov type condition hold.

Therefore, we can apply the multidimensional Lindeberg CLT to obtain

where is a -dimensional Gaussian vector with mean zero and covariance matrix . The claim then follows from applying the continuous mapping theorem.

∎

G.4 Proof of Lemma 2

Proof of Lemma 2.

The proof is similar to the proof of Theorem 4.3.8 in de Haan and Ferreira, (2007). Denote , we have by the assumption that . Using , we can expand

By using the same arguments as in the proof of Lemma 1, we have

By applying the Theorem 2.3.9 in de Haan and Ferreira, (2007), we have

which then implies

as . By assumption that , we have

Note that

so

| (39) |

Since for all , we have

thus

By Theorem 2 and the fact that , we have

thus

Combing the equality (39) and the fact that , we have

which implies

Combining the above results, we conclude that

which implies

as .

∎

G.5 Proof of Theorem 3

G.6 Proof of Theorem 4

We first introduce Lemma 10 which shows that under Assumption 6, the covariance matrix simplifies to . In particular, the components , and become zero, which implies that the extrapolated quantiles and are asymptotically independent.

Proof of Lemma 10.

Now we give the proof of Theorem 4.

Proof of Theorem 4.

Recall that , where

with are defined in equation (25). By Lemma 1, we have for . By Lemma 2 and Assumption 5, we have . By Lemma 10, only the covariance terms , , and in are nonzero. Therefore, to prove the consistency of the estimated variance , it is suffice to show that for ,

where are defined as in Assumption 9 and as in Assumption 8. We only show the result for , the case of can be shown analogously. We proceed in a similar manner as in the proof of Lemma 1.

For (i), we expand

with

We will show that and that converge to zero in probability.

For , we have

Note that

by a similar proof as the proof of Lemma 7 and

by the fact that and the Markov inequality, we have .

For , note that the terms have the same signs for all . Thus

We have seen in (29) that , together with Lemma 8 we conclude that . Combining the above results we have .

For (ii), we expand

with

where . We will show that and that converge to zero in probability.

For , let . As in the proof of Lemma 1, we have almost surely. Because , we have that almost surely

Since satisfies the max-domain of attraction condition with a positive extreme value index , we can apply the Corollary 1.2.10 and the statement 5 of the Proposition B.1.9 in de Haan and Ferreira, (2007) to obtain that for any such that and , there exists such that for any and , we have

Since and can be arbitrary small, we can take them small enough such that . Hence, we can first take logarithm and then take square on the above inequality to obtain

For large enough and for such that , we can set and . Multiplying by on both sides of the above inequality and summing up all with gives us that almost surely, lies in the interval with

We have that

by Assumption 1 ii) and the result (30), and

by Assumption 1 ii) and the result (31). Hence, since and can be arbitrarily small, to prove , it is enough to show that

We have

by Lemma 10, and

where we apply Lemma 6 in the second last equality and apply Lemma 9 in the last equality. This shows that

and therefore we can conclude that .

For , we have

where the inequality follows from the Assumption 1 ii), and the last result follows from results (30), (32), and the result that

as we proved that in the proof of Lemma 1.

For , since the terms have the same signs for all . Thus

For , similarly as in the proof of Lemma 1, we have

We have shown that and , so follows from Lemma 7. Combining all the previous results we can conclude that .

For (iii), we expand

with

where . The next step is to show that and that converge to zero in probability, which is enough to prove . The remaining proof is similar to the one for , so we omit it. ∎

G.7 Proof of Lemma 3

Proof of Lemma 3.