Regression Markets and Application to Energy Forecasting

Abstract

Energy forecasting has attracted enormous attention over the last few decades, with novel proposals related to the use of heterogeneous data sources, probabilistic forecasting, online learning, etc. A key aspect that emerged is that learning and forecasting may highly benefit from distributed data, though not only in the geographical sense. That is, various agents collect and own data that may be useful to others. In contrast to recent proposals that look into distributed and privacy-preserving learning (incentive-free), we explore here a framework called regression markets. There, agents aiming to improve their forecasts post a regression task, for which other agents may contribute by sharing their data for their features and get monetarily rewarded for it. The market design is for regression models that are linear in their parameters, and possibly separable, with estimation performed based on either batch or online learning. Both in-sample and out-of-sample aspects are considered, with markets for fitting models in-sample, and then for improving genuine forecasts out-of-sample. Such regression markets rely on recent concepts within interpretability of machine learning approaches and cooperative game theory, with Shapley additive explanations. Besides introducing the market design and proving its desirable properties, application results are shown based on simulation studies (to highlight the salient features of the proposal) and with real-world case studies.

Keywords: energy forecasting, data markets, mechanism design, regression, estimation

1 Introduction

Renewable energy forecasting has evolved tremendously over the last 10-20 years, with a strong evolution towards probabilistic forecasting, cutting-edge statistical and machine learning approaches, the use of large amounts of heterogeneous and distributed data, etc. For a recent and compact review of the state of the art withing energy forecasting, the reader is referred to Hong et al. (2020). Especially when it comes to the use of heterogeneous and distributed data sources, numerous works support the idea that forecasting quality may be substantially improved, see Andrade and Bessa (2017), Cavalcante et al. (2017) and Messner and Pinson (2019) among others. These works have shown that improvements may be obtained by using offsite information (e.g., power and meteorological measurements) as well as weather forecasts over neighboring grid points, for areas covering tens to a few hundreds of kilometers. Improvements are observed for forecasts in the form of conditional expectations, but also for probabilistic forecasts, e.g., quantiles, intervals and predictive densities. When using the term distributed, we here mean both in the geographical and ownership sense, i.e., the data potentially valuable to a given agent of the energy system is actually collected and owned by other agents. Therefore, some have pushed forward proposals towards distributed and privacy-preserving learning (Zhang and Wang; 2018, Sommer et al.; 2021), as a way to get the benefits from such distributed data, without revealing the private information of the agents involved. Beyond energy applications, this approach is generally known as federated learning (Li et al.; 2020), with substantial developments over the last few years. The alternative that we propose to explore here is that of data monetization within a collaborative and market-based analytics framework. In the frame of the paper, it is assumed that if remunerated, agents are willing to share their actual data with an analytics platform. Privacy-related aspects are hence not readily considered, since data is shared with the platform but not with other agents. If privacy was to be additionally accommodated in that collaborative and market-based analytics framework, alternative approaches relying on distributed computing, differential privacy, etc. could be employed. As a representative example, Goncalves et al. (2021) analyzed some of these alternative approaches in a collaborative forecasting context.

Concepts of information sharing have been prevalent in some parts of the economics and game-theory focused literature, going as far back as the 1980s (Gal-Or; 1985). Data monetization and data markets have been increasingly discussed over the last 5-10 years, with a number of proposals towards algorithmic solutions (Agarwal et al.; 2019), as well as fundamental aspects of pricing and privacy-preservation (Acemoglou et al.; 2019), more generally also with consideration of bilateral exchange of data vs. monetization of data (Rasouli and Jordan; 2021). For a recent review of the state of the art related to data markets, see Bergemann and Bonatti (2019) and Liang et al. (2018). Approaches that would be suitable for renewable energy forecasting and energy applications more broadly are scarse though, with the notable recent example of Goncalves et al. (2020), who adapt and apply an approach in line with the proposal of Agarwal et al. (2019), restricted to batch learning and in-sample assessment of the value of data and features provided. Renewable energy forecasting appears to be an ideal playground to develop, apply and assess data markets, in view of the known value of distributed data, the liberalization of energy markets, and potential resulting impact. In addition, such data markets can then be developed along the lines of cutting-edge forecasting frameworks, where forecasts are thought of within a probabilistic framework, the environment is seen as nonstationary, etc. As of today, there does not exist such data markets that would jointly look at in-sample and out-of-sample value of data for forecasting, as well as both batch and online learning in underlying regression models. Consequently here, our aim is to describe and to analyze a theoretically sound and practical proposal for data monetization within a collaborative and market-based analytics framework, which is readily suitable for energy-related forecasting applications and these aforementioned characteristics. We restrict ourselves to a market with a single buyer and multiple sellers. This corresponds to the case where an agent that would like to improve the solving of a regression task posts this task on an analytics platform, where other agents can come and propose their features and own data. Many tasks could be posted in parallel, but buyers or tasks would not compete for the features and data to be supplied. However, several tasks could be posted and handled in parallel (as in our case-study application) based on the idea that buying the data does not bring exclusivity. Exclusivity is here defined as the fact that if data is sold to an agent, it cannot be sold to another agent in parallel. In contrast, if aiming for exclusivity, other setups exist for feature allocation among multiple buyers and sellers with the aim of maximizing social welfare, as for the example case of Cao et al. (2017).

Within energy forecasting applications, one most often finds a regression model and a learning process used to fit model parameters. Therefore, we place our focus on so-called regression markets. These markets readily build on the seminal work of Dekel et al. (2010), who were the first to look at mechanism design aspects for a regression setting where agents may be strategic in the way they share private information. Here, regression markets are considered in both batch and online versions, since modern learning and forecasting techniques mostly rely on these two approaches. We restrict ourselves to a certain class of regression problems (linear in parameters), which allows us to obtain certain market properties. It was already shown and discussed by Dekel et al. (2010) that certain properties, especially truthfulness (also referred to as incentive compatibility) is difficult to obtain in a more general regression setting. Extensions to privacy-constrained truthful regression, limited to a linear setting, were also recently discussed (Cummings et al.; 2015). The quality of the model fitting is assessed by a negatively-oriented convex loss function (lower is better), which may be quadratic in the case of Least-Squares (LS) fitting, a smooth quantile loss in the case of quantile regression, a Maximum Likelihood (ML) score for more general probabilistic models, etc. That convex loss function is at the core of our proposal, since the main idea is that an agent may be able to decrease the loss by using data from other agents. These agents should be monetarily compensated in a fair and efficient way, i.e., in line with their individual and marginal contribution to improvements in . For that purpose, we use some recent concepts related to interpretability in machine learning, following the original proposal of Lundberg and Lee (2017) and the wealth of subsequent proposals, which directly connect to a cooperative game-theoretical framework as in Agarwal et al. (2019). Finally, a particular aspect of our contribution is that we consider both in-sample (i.e., model fitting based on past data) and out-of-sample (i.e., use of those models for forecasting based on new data) since, in actual energy forecasting application, both need to be considered in order to improve model fitting, but also genuine forecast quality.

The document is structured as following: firstly, Section 2 describes the agents and preliminaries regarding regression tasks. Subsequently, Section 3 introduces our original proposal for regression market mechanisms, where agents are monetarily rewarded for their contribution to improving the solving of a given regression task, in the sense of lowering the convex loss function . The overall concept is presented for both batch and online setups, also with a description of feature valuation and allocation policies. The extension to the out-of-sample regression and forecasting case is also covered. The properties of our regression market mechanisms are finally presented and proven. The approach is illustrated based on a set of simulation studies, which are gathered in Section 4, for a broad range of models and cases. Section 5 then describes and discusses an application to real-world forecasting case-studies, with both mean and quantile forecasting problems, as well as batch and online learning. Finally, Section 6 gathers a set of conclusions and perspectives for future work.

2 Setup, regression and estimation

2.1 Central and support agents

Consider a set of agents . Out of this set of agents, one of the agents is referred to as central agent, in the sense that this agent has an analytics task at hand, in the form of a regression problem for an eventual forecasting application. We refer to the other agents , as support agents, since they may be supporting the central agent with the analytics task at hand. The central agent has a target variable , seen as a stochastic process, i.e., a succession of random variables indexed over time, with the time index. Eventually, a time-series is observed, which consists of realizations from , one per time index value. For simplicity, we consider that realizations of can take any value in , even though in practice, it is also fine if restricted to a subset of it (positive values only, or within the unit interval , for instance).

The central agent aims at obtaining a model that can describe some given characteristics of , e.g., its mean or a specific quantile with nominal level . This description relies on a set of input features (also referred to as explanatory variables). These features and their observations are distributed among all agents. We denote by the observation of feature at time . As for the target variable, we consider for simplicity that , though in practice these may also be restricted to a subset of .

All features and target variable are observed at successive time instants, , such that we eventually have time-series of those. Let us write the vector of values for the feature , the vector of values for all features at time , while gathers all target variable observations, over the time steps. In the case only a subset of features is used, the vector of feature values at time is denoted by . In practice such features may be observations (meteorological, power measurements, etc.) or forecasts (e.g., for weather variables). We write the design matrix, the row of which is .

The features are distributed among all agents in as following: the central agent owns a set (of cardinal ) of features, , as well as the target variable ; the support agents, gathered in the set , own the other input features, which could be of relevance to the central agent for that regression task. Each agent has a set with features, , such that . We write the set that contains the features of support agents only, .

2.2 Regression framework

2.2.1 Regression models that are linear in their parameters

Generally speaking, based on temporally index data, collected at regular time intervals, a regression problem aims at describing the mapping between a set of explanatory variables, and the target variable , i.e.,

| (1) |

In principle may be linear or nonlinear, and a wealth of approaches can be considered for its modeling. We restrict ourselves to the case of parametric regression in the sense that

| (2) |

Consequently, given a structural choice for , the regression may be fully and uniquely described by the set of parameters , . In the linear regression case, , while for nonlinear regression. We additionally restrict ourselves to the case of regression models that can be expressed as linear in their parameters , since if using convex loss functions the resulting estimation problem is convex too. That class of regression problems is not limited to linear regression only though, since also covering nonlinear regression problems such as polynomial regression, local polynomial regression, additive models with splines, etc. This therefore means the model in (2) can be expressed as

| (3) |

where is the observation at time of the augmented feature vector . For instance if having features and and considering polynomial regression of order 2, the augmented feature vector at that time can written as . The vector of parameters hence has dimension .

In the following, to place ourselves in the most generic framework, we focus on the regression problems as in (3), as they also encompass basic linear regression when . We write the design matrix, the row of which is .

2.2.2 Separable and non-separable regression problems

Consider the general case for which a linear regression model uses features within a set as input (so, possibly from both central and support agents), to describe a characteristic of . Linear regression relies on the following model for ,

| (4) |

where is a centred noise with finite variance. This readily translates to

| (5) |

For instance, if is the expectation of , this means that this expectation is modeled as a linear function of the input feature values at time .

In the special case where only the features of the central agent are used, one has

| (6) |

i.e., only considering the features owned by the central agent, . The ’s are hence the coefficients in the linear model corresponding to the features owned by the central agent. In contrast, if the features of all support agents were also considered, the corresponding linear model would be

| (7) |

where the ’s (related to ) are the coefficients in the linear model corresponding to the features owned by the all support agents. In principle, could be taken aside since not relating to a feature owned by neither central nor support agents. For simplicity in the following, we consider that the central agent also has a unit feature, that hence corresponds to that intercept. As can be seen from (7), such linear regression models are separable, in the sense that we can separate blocks of terms that relate to the individual features of each agent. Similarly, additive models with splines are separable, since these may be written as

| (8) |

where

| (9) |

In the above, the ’s denotes the basis functions, while is the spline basis expansion relying on basis functions. In addition, is the number of degrees of freedom, being itself a function of spline type and the number of knots. By combining (8) and (9), one sees that additive models with a spline basis take the form of the generic parametric regression model (3), and that these are separable.

In contrast, if using polynomial regression (as well as local polynomial regression) with degree greater than 1, the regression models are not separable, since interaction terms in the form of direct multiplication of features owned by different agents will be present. Consequently, one cannot have this separation in blocks as for linear regression and additive models with splines. To illustrate those situations, two examples are gathered below.

Example 2.1 (ARX model for the mean)

The central agent may want to learn an Auto-Regressive with eXogenous input (ARX) model, to describe the mean of , based on lagged values of the target variable (say, one lag only), as well as lagged input features from the support agents. A first support agent owns feature while a second support agent owns feature . This yields

| (10) |

Example 2.2 (Polynomial quantile regression of order 2)

In a quantile regression problem, for a given nominal level (say, for instance, ), to describe the quantile of , the central agent owns feature . In parallel, two support agents own two relevant features and . Those are overall considered within the following polynomial quantile regression problem or order 2:

| (11) | ||||

2.3 Estimation problems

For the regression problems in the above, one eventually has to estimate the parameter vector based on available data. We differentiate two cases: batch and online, which are further described in the following.

2.3.1 Residuals and loss functions

Eventually, based on those collected data, one aims at finding the “best” mapping that describes the relationship between the input features and the target variable. Given a chosen regression model for (within our restricted class of regression models), this is done by minimizing a chosen loss function of the residuals in expectation, to obtain the optimal set of parameters , i.e.,

| (12) |

Common loss functions include the quadratic loss for mean regression, the absolute loss for median regression and more generally the quantile loss for quantile regression. In all cases, is a negatively-oriented proper scoring rule, with minimum value at . It is negatively oriented since lower values are preferred (in other words, the model more accurately describes the data at hand in the sense of ). It is a strictly proper scoring rule since the best score value is only given to the best outcome (in principle, ) (Gneiting and Raftery; 2007). In the following, we will use the notation instead, since given the explanatory and response variable data, the loss actually is a direct function of the vector of coefficients only.

The quadratic loss function readily allows for both batch and online estimation approaches, though the online case is not straightforward if considering absolute and quantile loss functions. Indeed, to use the type of gradient-based approach described hereafter, the following assumption is necessary.

Assumption 1

Loss functions are twice differentiable everywhere and continuous, .

Absolute and quantile loss functions do not satisfy Assumption 1. However, one can use the smooth quantile loss introduced by Zheng (2011) instead (also covering the absolute case for ). The smooth quantile loss function is defined as

| (13) |

where is the nominal level of the quantile of interest, , while is a smoothing parameter. A number of interesting properties of such loss functions, as well as relevant simulation studies, are gathered in Zheng (2011).

2.3.2 Batch estimation

In the batch estimation case, the parameters of the regression model (3) are estimated once for all based on observations gathered for times . Given a choice of a regression model based on a set of features , we write the vector of parameters corresponding to the potentially augmented vector of features . Given a loss function , the vector of parameters can be obtained as

| (14) |

where is an in-sample estimator for , defined as

| (15) |

and where is the augmented feature vector value at time . We denote by the value of the loss function estimate at the estimated , . Interesting special cases then include the estimation of , i.e., using the features of the central agent only with loss function value estimate , as well as the case for which all features are considered (from both central and support agents) yielding the estimated coefficients and loss function value estimate . The overall added value of employing features from support agents can then be quantified as . One may intuitively expect that all potential features contribute to lowering the loss function estimate from to . However, such features will contribute to a varied extent, with possibly some that provide a negative contribution, i.e., in practice, they make the loss function estimate worse. It is a general problem in statistical learning and forecasting to select the right features to lower the loss function at hand.

An important property of the batch estimation problems, with model types and loss functions we consider, is described in the following proposition.

Proposition 1

We do not give a formal proof of Proposition 1 here, as it is a straightforward and key result of convex optimization: the optimization problem in (14), based on convex loss functions (as used in regression model estimation, e.g., quadratic, quantile, etc.), relies on a continuous and strictly convex function . Hence, its solution exists and is unique.

Depending on the loss function and its in-sample estimate , the estimation problem in (14) may have a closed-form solution (as for the quadratic loss case), or may require the use of numerical methods (i.e., for absolute and quantile loss functions, possibly Huber loss (Huber; 1964) and more general convex loss functions).

2.3.3 Online estimation

So far, it was assumed that the regression model parameters do not change with time. However, due to nonstationarity in the data and underlying processes, and possibly to lighten the computation burden, it may be relevant to consider that these model parameters vary in time. In that case, we also use a time index subscript for . The estimation of in a recursive and adaptive manner is referred to as online learning. For a thorough recent coverage of approaches to online learning, the reader is referred to Orabona (2020).

In the online learning setup, recursivity translates to the idea that the model parameter estimates at a given time can be obtained based on the previous model parameter estimates (hence, at time ) and the new available information at time . That newly available information at time typically is a function of the latest residual, i.e., the difference between the latest regression output (for time , based on model parameters from time ) and the observation at time . In parallel, adaptivity is linked to the use of a forgetting scheme, so that higher weight is given to the most recent information. The most usual approach is exponential forgetting, where the importance given past information decreases exponentially. It uses a forgetting factor , with values close to 1. Past information is then weighted by where denotes the age of information compared to current time . Eventually, the optimization related to the estimation of model parameters at time can be be formulated as

| (16) |

where

| (17) |

In the above, , and is the effective window size, . It is a scaling parameter for the loss function estimate similar to the number of observations in the case of the batch estimator. is to be seen as a time-varying estimator of the loss function at time .

As a proxy to solving (16), one can use a fairly straightforward trick for recursive updates of all quantities involved. Given that Assumption 1 is satisfied, recursive updates can be obtained based on a Newton-Raphson step. Considering a model based on the set of features , and with loss function (and estimator ), that Newton-Raphson step forms the basis for the update of model parameters from time to time , with

| (18) |

In practice, this means that, if having the set of optimal model parameters at time , one can use the above update to obtain the optimal model parameters at time . Obviously, there may be a tracking error involved, which is today commonly studied in terms of regret – see Orabona (2020) for instance.

Considering both quadratic loss and smooth pinball loss functions, we have the following general results for online learning based on a Newton-Raphson step for regression models that are linear in their parameters. In both cases, online learning based on a Newton-Raphson step requires a memory in the form of a matrix , directly relating to the Hessian for the loss function considered, and at time .

Proposition 2

Given a loss function , , and a regression model as in (3), with a set of parameters, the Newton-Raphson step at time is given by

| (19a) | |||||

| (19b) | |||||

| (19c) | |||||

with, if is the quadratic loss,

| (20a) | |||||

| (20b) | |||||

and if is the smooth quantile loss, given the smoothing parameter and nominal level ,

| (21a) | |||||

| (21b) | |||||

There also, the proof of Proposition 2 is omitted, since only relying on calculating relevant derivatives and Hessian of loss functions, to be plugged in (18). Similar derivations can be performed for other types of loss functions that meet Assumption 1, as well as for special cases of loss functions that do not meet Assumption 1, e.g., the Huber loss. Similarly to the batch case, that approach enjoys the interesting property of existence and uniqueness of the Newton-Raphson step.

Proposition 3

The proof of Proposition (3) readily relies on Assumption 1, since for loss functions , both gradient and Hessian are always well-defined.

The recursive updates given in Proposition 2 are for a given time . However, it does not tell us how such an online learning scheme should be initialized. In practice, one generally uses batch estimation with a small sample of data (say, 50 to 100 time points) to obtain initial parameter estimates for the online learning scheme. Alternatively, all parameter estimates may be initialized to 0 (or any other relevant expert guess) and the online learning scheme applied from the start. In that case though, one would need to wait for some steps (again, say, 20 to 100 time points) before to inverse a matrix in (19c), as those may be (close to) singular.

2.4 Defining regression tasks

Let us close this section related to regression by defining regression tasks, in both batch and online versions. The reason why we need to define those tasks is that these will be the tasks that central agents may post on a collaborative analytics platform, within the market frame to be described in the following section. Another type of task is finally defined for the out-of-sample regression case, when the models and estimated parameters (from either batch or online learning stage) are to be used for out-of-sample genuine forecasting.

Definition 1 (Batch regression task)

Given the choice of regression model and loss function , as well as data collected for a set of input features and a target variable over a period with time steps, a batch regression task can be represented as

| (22) |

i.e., as a mapping from those data to a set of coefficients such that the loss function estimate is minimized (and with minimum value ).

Definition 2 (Online regression task)

At time , given a regression model , a loss function and a forgetting factor , as well as newly collected data at time for a set of input features and a target variable , the online regression task relies on the following mapping

| (23) |

where as input is the previous set of estimated model parameters (from time ), is the loss function estimate value at time , is the memory of the regression task, while and are the new data (for both input features and target variable) at time . Based on those, the regression task updates the memory to yield , the estimated model parameters to yield , as well as the loss function estimate .

Note that the choice of regression model for and a loss function leads to a unique mapping and for both batch and online regression tasks, based on Propositions 1 and 3, respectively. In a last stage, let us define in the following the out-of-sample regression task.

Definition 3 (Out-of-sample regression task)

At time , given a choice of regression model and estimated parameters available at that time (from either batch or online regression tasks, which we write ), as well as data collected for a set of input features , the out-of-sample regression task maps those to a -step ahead forecast for a characteristic of the target variable , i.e.,

| (24) |

There again, the mapping exists and is unique (unless the parameters are equal to 0), since dealing with regression models that are linear in their parameters.

3 Introducing regression markets

3.1 General considerations

Emphasis is placed on a market with a single buyer and multiple sellers. This market is hosted by an analytics platform, handling both the collaborative analytics and the market components. This is in line with other works that look at data markets with some form of collaborative analytics involved as for, e.g., Agarwal et al. (2019) and Goncalves et al. (2020).

On this platform, a central agent posts a regression task (either batch or online, as defined in the above), which therefore implies a choice for a regression model . This choice for is to be understood as choosing a class of potential regression models, e.g., plain linear regression or additive spline regression, based on features that may be provided. The central agent additionally declares a willingness to pay for improving model fitting, or forecast accuracy, in the sense of a loss function . The willingness to pay may be readily linked to the perceived cost of modeling and forecasting errors in some decision process, for instance if trading in electricity markets. is expressed in monetary terms (e.g., €, £ or $) per unit improvement in and per data point provided. If support agents were to provide relevant additional features, the loss function (or its estimate in practice) may be lowered, and the support agents remunerated based on the valuation of their features, relatively to others’ features and to the overall improvement in the loss function . Obviously, a general problem for any statistical and machine learning setup is to select features that are valuable, here within the class of regression models considered. Otherwise, the loss function will worsen. Consequently, those features have no value to the central agent, and the support agents should not be remunerated for features that are not valuable. Within the class of regression models chosen by the central agent, the analytics platform performs the necessary feature selection, based on cross-validation for instance. Consequently, we formulate the following crucial assumption.

Assumption 2

Within our regression markets, given that central agents have expressed a choice for a class of regression models, the analytics platform is entrusted with the feature selection process, for instance based on cross-validation, so that only valuable features (in the sense that using them lowers the loss function ) are considered.

It should be noted regression markets could endogenously perform the feature selection process, since, as will be described in the following, features that are not valuable will yield null or even negative payments. Hence, at this stage such features could be removed and the regression market run again without them. Alternatively, regression markets could rely on penalized regression problems, e.g., lasso (Tibshirani; 1996) and elastic nets (Zou and Hastie; 2005). This would have the advantage of endogenously selecting features, though decreasing overall benefits and potential distorting payments as the price to pay for that penalization.

All agents involved, i.e., both central and support agents, are to be seen as opportunistic. By this, we mean that they all hope to have a gain or a payment from participation in the regression market, although no gain or payment is guaranteed. In practice, the central agent cannot know in advance whether support agents may bring valuable features and data which would improve model fitting and improve forecast accuracy (in the sense of lowering a loss function ). Similarly, support agents cannot know in advance whether their data and features will be selected, and what potential payment they may receive. This aspect actually is in line with other proposals for data markets with a central analytic components, e.g., Agarwal et al. (2019) and Goncalves et al. (2020). There, the buyers place a bid and the payment to the support agents (referred to as data sellers) is readily linked to the market-clearing price. Then, if the price out of the market clearing is higher than the price offered by the buyer, the value of their input data is altered by adding a noise to it (the variance of which is proportional to the difference between the bid and actual market price). Importantly also, the market price in each trade is purely dependent on the value of the data in the previous trades, hence set before the current buyer enters the market with a specific analytics task. In the case where support agents would like to condition their participation to a minimum payment, one could also use the concept of “reservation to sell” placed within a lasso-based regression framework, as recently proposed by Han et al. (2021). More generally, minimum gain and payments for all agents involved could also be considered at the feature selection stage. This reservation to sell and minimum requested payment may reflect perceived privacy loss, a loss of a competitive advantage, the cost of acquiring and storing the data, etc.

In the following, we first consider the batch setup, which allows to introduce the relevant markets concepts and its desirable properties. It is then extended to the online case, for which the data is streaming. Hence, the regression model parameters, allocation policies and payments are updated each and every time , when new data becomes available. In both cases, these markets are for an in-sample assessment of the value of the features and data of the support agents. This in-sample assessment is only a proxy for what their value may be out-of-sample, when used for genuine forecasting. In practice, there may be substantial differences between in-sample and out-of-sample estimates for a chosen loss function , and this is why we consider here complementary regression markets for the in-sample and out-of-sample stages. However, it is clear that such out-of-sample forecasts can only be issued if the features and data of support agents has already been used to train relevant regression models. This is why, in our proposal for regression markets, one needs to combine an in-sample assessment of improvements in (based on the batch or online regression market) and an out-of-sample assessments of (based on an out-of-sample regression market). Our proposal for the definition of payments then rely on considerations related to quality, i.e., in-sample and out-of-sample reduction in a loss function , and volume since the payment will be proportional to the quantity of data being shared by the support agents. Especially in a data streaming and online environment, this volumetric side of the payment is important to ensure that the data is continuously being shared by support agents.

3.2 Batch regression market

In a batch regression market, the central agent has a willingness to pay for improving the value of the loss function , for instance expressed in € per time instant (or data point) and per unit decrease in . Obviously, is in practice replaced by its estimate . And, the process is based on a batch of data for the time instants between times 1 and . In principle, the support agents have a willingness to sell (), for instance expressed in € per data point shared, which may be a function of the cost of collected the data, privacy-related considerations, etc. However here, we consider that that their willingness to sell is , i.e., they are happy to receive any possible payment for their features and data.

The central agent communicates the loss function , regression model for , length of dataset (and the actual time period it corresponds to), owns set of features, as well as willingness to pay , to the analytics platform. The mapping is then well-defined within that analytics platform. In parallel, interested support agents share the data for their sets of features (so, data points per feature) with the analytics platform. Within that framework, let us formally define a batch regression market.

Definition 4 (batch regression market)

Given a regression model , a loss function and a batch period with time steps, a batch regression market mechanism is a tuple (, , ) where is the space of the target variable, , is the space of the input features, , and is the vector of payout functions .

Based on all features provided, and based on the mapping , the analytics platform deduces the overall improvement in the loss function estimate as . This yields the payment of the central agent

| (25) |

which is a direct function of the quantity of data, improvement in loss function (as estimated over the data used for estimated the model parameters) and the willingness to pay of the central agent. As mentioned previously, the payment has a volumetric component, since one buys a quantity of data points at once, and a quality component, since the payment is conditioned by the decrease in the loss function estimate by using the features and data of the support agents.

In parallel, the batch regression market relies on allocation policies to define the payment for any feature of the support agents, . We write the allocation policy value for feature for the loss function , corresponding to its marginal contribution to the overall decrease of the loss function . We therefore intuitively expect the following desirable properties for allocation policies.

Property 1

Allocation policies are such that

-

(i)

-

(ii)

Those desirable properties for allocation policies are crucial for some of resulting inherent properties of the regression markets to be introduced and discussed later on. Eventually, the payment for feature is

| (26) |

so that, overall, the payment to agent is

| (27) |

The payment is both volumetric, since the quantity of data is accounted for and linearly influences the payment, as well as quality driven. On that last point, it is a function of the overall improvement in by considering the support agents’ features (i.e., ), and the marginal contribution of each and every feature to that improvement (through the allocation policy ).

The key question is then about how to value each and every feature from the support agents within the regression task at hand (and hence, for the central agent). This is the aim of the allocation policies in (26) and (27).

In the simplest case where the input features are independent, the regression model separable and linear, and a quadratic loss is considered, one may actually consider the coefficient of determination as a basis for determining the ’s. We refer to this approach as a “leave-one-out” policy.

Definition 5 (leave-one-out allocation policy)

For any feature , and loss function , the leave-one-out allocation policy can be estimated as

| (28) |

In the above, both estimators are scaled by the loss estimate improvement when going from the central agents features only () to the whole set of features . The difference between the two estimators is in the numerator. In the first case, is for the decrease in the loss estimate when going from the full set of features minus to the full set of features. And, in the second case, is for the decrease in the loss estimate when going from the set of features of the central agent only, to that set plus . This leave-one-out policy may be seen as a simple case of a Vickrey-Clarke-Grove (VCG) mechanism, and for instance considered by Agarwal et al. (2019) and Rasouli and Jordan (2021).

For the special case where is a quadratic loss function, one can take a variance-decomposition point of view to observe that

| (29) |

with the variance operator. Hence, readily translates to the share of the variance in the target variable explained by the feature . Consequently, both estimators are equivalent and one readily verifies that allocation policies fulfil Property 1.

Strictly speaking, the leave-one-out allocation policies do not meet the desirable properties expressed in Property 1, unless Assumption 2 is respected. It may not even be appropriate in the case where the features are not independent, when the regression model is non-separable and nonlinear, and if the loss function is not quadratic. In that more general case, a Shapley-based approach can be used instead. Shapley values and related allocation are well-known concepts in cooperative game theory with many desirable properties, while essentially providing a fair compensation for an agent’s contribution to collective value creation. For a compact introduction, the reader is referred to Winter (2002), while the application of Shapley value for data valuation is covered by Ghorbani and Zou (2019).

Allocation values are consequently defined by the marginal value of the various features in a Shapley sense, hence yielding the Shapley allocation policy.

Definition 6 (Shapley allocation policy)

For any feature , and loss function , the (original) Shapley allocation policy is given by

| (30) |

In the case where features are independent, considering a linear regression and a quadratic loss function, one has . Even in the linear case and with quadratic loss, if features are not independent, spurious allocation may be obtained when employing the leave-one-out strategy, as hinted by Agarwal et al. (2019). For instance, consider two features and being correlated perfectly, the marginal value of each feature as given by and would be 0 if using the first estimator in (28). In contrast if using the second estimator in (28), and would correctly reveal their marginal value, but one would eventually have (since considering twice the same marginal feature value in the overall picture), which does not respect the basic definition such that allocations should sum to 1. The reason why we introduce here those two types of allocations is that in practice, various allocations could be used alternatively, as long as allocation policies are positive and sum to 1. Despite the fact Shapley allocations should be seen as the most relevant one, these are notoriously computationally heavy to calculate as the number of features increases. This is general problem known and addressed by the computer science and algorithmic game theory communities, see e.g., Jia et al. (2019) for a recent example also related to data markets.

A more important issue with the Shapley allocation policy is that it may violate one of the desirable basic properties of allocation policies, i.e., such that . This is since, as indicated in Section 2.3.2, certain features may actually make the loss function estimate worse when they provide no (or very little, compared to the batch sample size) valuable information. For those features, readily using a Shapley allocation policy would yield negative values for . This problem was for instance recently identified and discussed by Liu (2020), who then proposed to use zero-Shapley and absolute-Shapley values instead.

Definition 7 (zero-Shapley and absolute-Shapley allocation policies)

For any feature , and loss function , the zero-Shapley allocation policy is given by

| (31) |

while the absolute-Shapley allocation policy is defined as

| (32) |

It is unclear today what approach to correcting Shapley allocation policies may be more appropriate when looking at data important and valuating in the context of regression markets. At least, both definitions ensure that the resulting allocation policies are positive – they may not sum to 1 though. In our case, by using Assumption 2, the original Shapley allocation policy can be readily employed, while meeting Property 1. The zero-Shapley and absolute-Shapley allocation policies may be useful instead for the out-of-sample regression markets, where the inherent value of the features and data provided by the support agents may not necessarily be positive.

Finally, let us compile here the important properties of the batch regression market mechanism introduced in the above, which we look at in a way that is fairly similar to the case of wagering markets as in Lambert et al. (2008) as well as data markets as in Agarwal et al. (2019).

Theorem 1

Batch regression markets, using the proposed regression framework and payout functions based on (original) Shapley allocation policies, yield the following desirable properties:

-

(i)

Budget balance – the sum of revenues is equal to the sum of payments

-

(ii)

Symmetry – the market outcomes are independent of the labelling of the support agents

-

(iii)

Truthfulness – support agents only receive their maximum potential revenues when reporting their true feature data

-

(iv)

Individual rationality – the revenue of the support agents is at least 0

-

(v)

Zero-element – a support agent that does not provide any feature, or provide a feature that has no value (in terms of improving the loss estimate ), gets a revenue of 0

-

(vi)

Linearity – for any two set of features and , the revenue obtained by sharing is equal to the sum of the revenues if having shared and separately

Note that Lambert et al. (2008) also mentions sybilproofness, normality and monotonicity, which are not seen as relevant here. Those properties may be investigated in the future though. Linearity is an interesting property which ensures that support agents will not be strategic in packaging their features since, whatever the way they submit features to the regression market (individually or as a bundle), the overall revenue obtained will be the same. Note also that, similarly to the case of Agarwal et al. (2019), the batch regression markets inherit the additive property from the additivity axiom defining Shapley values. The proofs are gathered in Appendix A. Truthfulness can only be ensured up to sampling uncertainty since, as discussed in the proof, it would strictly hold if having access to the actual loss – in practice, however, only an in-sample estimate is available. For the case of using leave-one-out allocation policies instead, the same properties are obtained for plain linear regression models, a quadratic loss, and independent features. This relies on the law of total variance, of which the variance decomposition of (28) is an example consequence. Truthfulness may not be verified in the more general case, though the other properties will hold. These properties are obviously interesting – still, they may not prevent some potential challenges with data duplication. For strategic behavior such as data replication, we have to use other payoff allocation mechanisms, such as the Shapley Approximation proposed by Agarwal et al. (2019), at the cost of loosing budget balance.

Finally, it should be noted that such a setup for batch regression market may be readily extended to the case of batch learning based on sliding windows, since payments would only be due for the new data points being used.

3.3 Online regression market

To adapt to the fact data is naturally streaming, and also that the analytics approaches may require to continuously learn from data in an online environment, we propose here an online version of the regression market introduced in the above. The base considerations are the same. The central agent has a willingness to pay for improving the value of the loss function (in € per time instant and per unit decrease in ). This agent communicates the loss function , regression model for , her own set of features, as well willingness to pay , to the analytics platform. Most likely, the central agent also needs to inform about the duration over which the process will be re-iterated, as it may not make sense to only try and learn at a single instant. On the other side, interested support agents share the data for their sets of features with the analytics platform, by delivering a new set of feature data at each and every time , as time passes. At each time , the mapping is well-defined within that analytics platform. Within that framework, let us formally define an online regression market.

Definition 8 (online regression market)

Given a regression model , a loss function and a given time , an online regression market mechanism is a tuple (, , ) where is the space of the target variable, , is the space of the input features, , and is the vector of payout functions .

In the batch regression case, one has a single estimate of the loss over the batch period (with data points), hence allowing to define a payment (for example for a given feature in (26)) that combines the contribution to the loss improvement and the volume of data. In an online regression case, however, the loss estimator varies with time. It is hence not possible to define a single payment over a period with data points based on a single loss function value. Instead, one needs to track the loss estimates through time, and use the loss estimate at time to value the data points provided at that time. In a way, in the batch case, one could also consider that the payment to a support agent for data point at time for feature is

| (33) |

while the overall payment of the central agent at a given time is

| (34) |

These payments are the same for all , and by summing up over time (), one retrieves the payments defined in (25) and (26). Now, we will extend this idea of having payments at each and every time to the case of time-varying loss estimates.

In an online learning environment, it is the loss estimators that vary with time. They will impact the allocation policies and make them time-varying too. By first observing that (17) can be decomposed as

| (35) |

loss function estimates can be readily updated at each and every time . Consequently, at a given time , the payment of the central agent is

| (36) |

Compared to the batch case in (25), has disappeared since the payment is for a single time instant, while the loss estimates are specific to time . This represents a time-varying generalization of the payment for the batch case.

To obtain the payments to the support agents, the only aspect missing is to determine the allocation policies. In line with the online estimation in Section 2.3.3, which is recursive and time-adaptive, it would be ideal to have a recursive and simple approach to update allocation policies.

Proposition 4

At any given time , both leave-one-out and (original) Shapley allocation policies can be updated in a recursive fashion, with

| (37) |

This means that, for a given feature and both types of allocation policies, the allocation at time can be obtained based on the previous allocation at time and on the allocation specific to the loss for the new residual at time . Consequently, a payment (for feature ) is made at each and every time step based on the time-varying loss function estimates and allocation policies. This yields

| (38) |

Similar to the case of the model parameter estimates in online learning, a legitimate question is about how to initialize payments. Since the allocation policies and payments are readily obtained from the loss estimates (and hence model parameter estimates), the approach to model parameter initialization will drive the initialization of the payments.

Finally, online regression markets have the same properties as the batch ones.

Corollary 1

Online regression markets, using the proposed regression framework and payout functions based on Shapley allocation policies, yield the properties of (i) budget balance, (ii) symmetry, (iii) truthfulness, (iv) individual rationality, (v) zero-element, and (vi) linearity.

The proof for that corollary is omitted since similar to that for Theorem 1.

3.4 Extension to forecasting and out-of-sample loss function assessment

Both of the above markets, in batch and online versions, relate to a learning problem and the in-sample assessment of a loss function . In many practical cases, however, such models are then to be used out of sample, for forecasting purposes for instance. There may hence be a discrepancy between the in-sample loss estimate and the out-of-sample one. This is while, if forecasts are to be used as a basis for decision making, the actual perceived cost induced by the deviation between forecast and realization is represented by the out-of-sample loss, not the in-sample one.

Consequently, besides the batch and online regression markets that relate to the learning task, those should be complemented by out-of-sample payments. One can here make a direct comparison with the case of electricity markets, where one usually first has a forward (e.g., day-ahead) mechanism leading to resource allocation and payments, and then a balancing mechanism to update and correct the outcomes from the forward mechanism. In the present case, the learning process is first necessary to fit a regression model and assess the in-sample value of the features of support agents. Then, out of sample, the input features of those agents are used for genuine forecasting, and payments are to be based on the contribution to a decrease in the loss function and its out-of-sample estimate. Let us formally define the out-of-sample regression manner in the following.

Definition 9 (out-of-sample regression market)

Given a regression model and its parameters estimated through either batch or online regression markets, a loss function and a out-of-sample period with time steps, an out-of-sample regression market mechanism is a tuple (, , ) where is the space of the target variable, , is the space of the input features, , and is the vector of payout functions .

Consider being at a time , having to use some of the regression models trained based on a batch of past data, or online. The estimated parameters are here denoted by to indicate that they are those available at that time. In the batch case, these might be older since estimated once for all on older data, unless a sliding window approach is used. In the online case instead, those may be the most recent parameters available based on the latest updated at time . That model is used to issue a forecast for lead time for the target variable of interest, or possibly a nowcast (i.e., with ) in the case is not observed in real-time. We write the set of time instants over which forecasts are being issued. The out-of-sample loss estimate over is

| (39) |

Such an estimator is separable in time, i.e.,

| (40) |

Again, considering the linearity property of both leave-one-out and Shapley allocations, this translates to having over the out-of-sample period

| (41) |

where is an allocation based on the evaluation of the loss function at time only. Such time-dependent allocation are then directly linked to the idea of using Shapley additive explanation (Lundberg and Lee; 2017) for interpretability purposes. However here, such allocations aim at defining the contribution of the various features to the loss for a given forecast at time . Eventually, the payment for feature at time (and linked to the forecast for time ) is

| (42) |

Those payments can be summed over the out-of-sample period , i.e.,

| (43) |

On the central agent side, the payment at each time instant is

| (44) |

to them be summed over the period .

Finally, based on those concepts, the out-of-sample regression markets enjoy the same desirable properties as the batch and online regression markets.

Corollary 2

Out-of-sample regression markets, using the proposed regression framework and payout functions based on Shapley allocation policies, yield the properties of (i) budget balance, (ii) symmetry, (iii) truthfulness, (iv) individual rationality, (v) zero-element, and (vi) linearity.

The proof for that corollary is omitted since similar to that for Theorem 1.

4 Illustrative examples based on simulation studies

To illustrate the various regression markets, we first concentrate on a number of examples and related simulation studies. Obviously, these are simplified versions of what would be done with real-world applications, since for instance, the models of the central agent are well specified. In parallel, we focus on the batch and online regression markets only, since the use of out-of-sample markets will be more interesting and relevant when focusing on a forecasting application with real data later on.

4.1 Batch regression market case

In order to underline the broad applicability of the presented regression market approach, emphasis is placed on three alternative cases: plain linear regression with a quadratic loss, polynomial regression with a quadratic loss, and an autoregression with exogenous input with quantile loss.

4.1.1 Case 1: Plain linear regression and quadratic loss

Firstly, emphasis is placed on the simplest case of a plain linear regression problem, for which the central agent focuses on the mean of a target variable , while owning feature . A quadratic loss function is used. The willingness to pay of is € per time instant and per unit improvement in . In parallel, two support agents and own relevant features (for ), and (for ). The regression chosen by the central agent (which is well specified in view of the true data generation process) and posted on the analytics platform relies on a model of the form

| (45) |

where is a realization of a white noise process, centred on 0 and with finite variance.

Let us for instance consider a case where the true parameter values are . For all features, the values of the input features are sampled from a Gaussian distribution, , with . In addition, , with .

We simulate that process for 10 000 time steps and learn the model parameters based on that period. The in-sample loss function estimates considering the central agent features only (so, an intercept and ), and then with features from the additional support agents (, and ) are gathered in Table 1. For this specific run and example, the overall value of the support agents is (1.191-0.087) = 1.104.

| Agents | ||

|---|---|---|

| In-sample loss estimate | 1.191 | 0.087 |

Since in this simple setup, we use linear regression, have independent input features and a quadratic loss function, both leave-one-out and Shapley allocation policies are equivalent. Those are gathered in Table 2. This table also gathers the payments received by agents and for their features. The values for both allocation policies are the same, up to some rounding. The overall payment from the central to the support agents is of 1104€ (i.e., 10 000).

| Feature/Agent | |||||

|---|---|---|---|---|---|

| [%] | 22.7 | 73.4 | 3.9 | 22.7 | 77.3 |

| [%] | 22.7 | 73.4 | 3.9 | 22.7 | 77.3 |

| [€] | 250.7 | 810 | 43.3 | 250.7 | 853.3 |

| [€] | 250.7 | 810 | 43.3 | 250.7 | 853.3 |

Note that this is the only case where leave-one-out allocation policies are used, since this will not make sense for the other case studies which are more advanced, e.g., with non-separable and nonlinear regression models, and/or loss functions that are not quadratic.

4.1.2 Case 2: Polynomial regression (order 2) and quadratic loss

We generalize here to a polynomial regression of order 2, with the same number of agents, a quadratic loss and the same willingness to pay (€ per time instant and per unit improvement in ). The central agent focuses on a target variable , while owning feature . The two support agents and own relevant features (for ) and (for ). The regression chosen by the central agent and posted on the analytics platform relies on the following model:

| (46) | ||||

where is a realization of a white noise process, centred on 0 and with finite variance. It is well-specified and hence corresponds to the true data generation process. The true parameter values are . For all features, the values of the input features are sampled from a Gaussian distribution, , with . In addition, , with .

The process is simulated over 10 000 time steps to estimate the regression model parameters, as well as to compute Shapley allocation policies and payments. Following Assumption 2, feature selection is performed and only the relevant terms in the polynomial regression (i.e., those with non-zero parameters, and contributing to lowering loss function estimates) are retained. It should be noted that there is additional subtlety in the case of interaction terms, making that one should obtain Shapley allocation policies (and payments) at the feature level (so, here, , and ), and not based on individual components in the regression model. This is since these terms in the regression model may come as a bundle. For instance, if starting with a coalition with only, and aiming to assess the value from adding to that coalition, it brings 2 additional terms ( and ) at once. And, if starting from a coalition with only, and aiming to assess the value from adding to that coalition, it adds 2 additional terms and too. However, it also means that one should look at it the other way around, and recognize that contributes to the value brought by the term .

Eventually here, the in-sample loss function estimates based on the central agent features only (so, the intercept and ) is of 0.72. With features from the additional support agents, it decreases to 0.09. The value of support agents is then of 0.63 in terms of the reduction of the loss function, though part of it also comes from the central agent’s feature through the interaction term. The Shapley allocation policy values for the various features are gathered in Table 3, as well as related payments. The contribution of feature comes from both and , while that of feature comes from the and terms. However, the sum of the Shapley allocation policies is not of 1 (it is of 0.65), since part of the overall improvement comes from the central agent’s feature through the interaction term . The overall payment from the central agent is of 520.42€. The payment would have been of 630€ if all improvements came from the feature and data of the support agents alone (hence, no interaction term).

| Feature (/Agent) | (/) | (/) |

|---|---|---|

| [%] | 44.36 | 20.59 |

| [€] | 355.44 | 164.98 |

4.1.3 Case 3: Quantile regression based on an ARX model

In the third case, the central agent wants to learn an Auto-Regressive with eXogenous input (ARX) model with a quantile loss function (with nominal level ), based on lagged values of the target variable (say, one lag only), as well as lagged input features from the support agents. The setup with agents and features is the same as for case 1. The willingness to pay is of =1€ per time instant and per unit improvement in the quantile loss function. The underlying model for the regression reads

| (47) |

where is a realization of a white noise process, centred on 0 and with finite variance.

The central agent is interested in 2 quantiles, with nominal levels 0.1 and 0.75, hence requiring 2 batch regression tasks models in parallel. Support agent features are sampled similarly as in case 1 (from a standard Normal), and the characteristics of the noise term are also the same. The true parameter values are .

We simulate that process for 10 000 time steps. The quantile loss estimates based on the central agent features only are of 0.086 and 0.152 for the 2 nominal levels of 0.1 and 0.75. In parallel, when using the support agent features, these decrease to 0.052 and 0.096, respectively. The improvements are hence of 0.034 and 0.056 for those 2 nominal levels. The Shapley allocation policy values and payments to the support agents are gathered in Table 4.

| Feature/Agent: | ||||||

|---|---|---|---|---|---|---|

| 0.1 | [%] | 66 | 6.7 | 27.3 | 66 | 34 |

| [€] | 218.14 | 22.17 | 90.2 | 218.17 | 112.37 | |

| 0.75 | [%] | 63.3 | 7.5 | 29.2 | 63.3 | 36.7 |

| [€] | 354.41 | 42.01 | 163.72 | 354.41 | 205.73 |

4.2 Online regression market case

4.2.1 Case 1: Recursive Least Squares with an ARX model

We use as a basis the same underlying model as in (47) and with the same agent setup. The central agent aims at using online learning with a quadratic loss for that ARX model and with a willingness to pay of =0.1€ per time instant and per unit improvement in the quadratic loss function. The major difference here is that the parameters vary in time, i.e.,

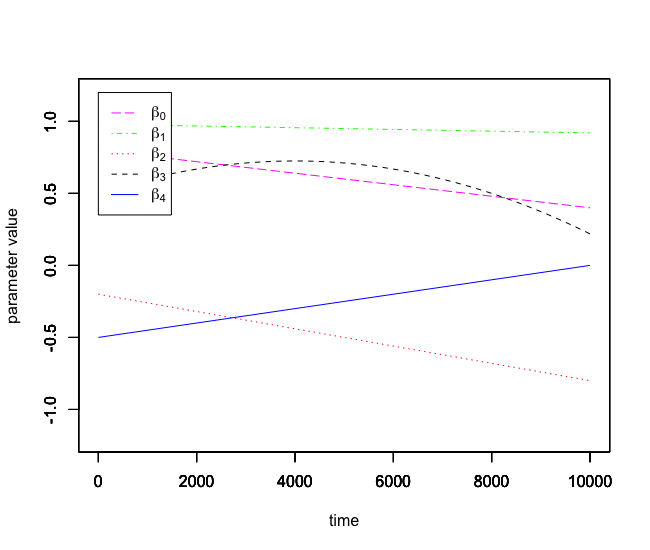

| (48) |

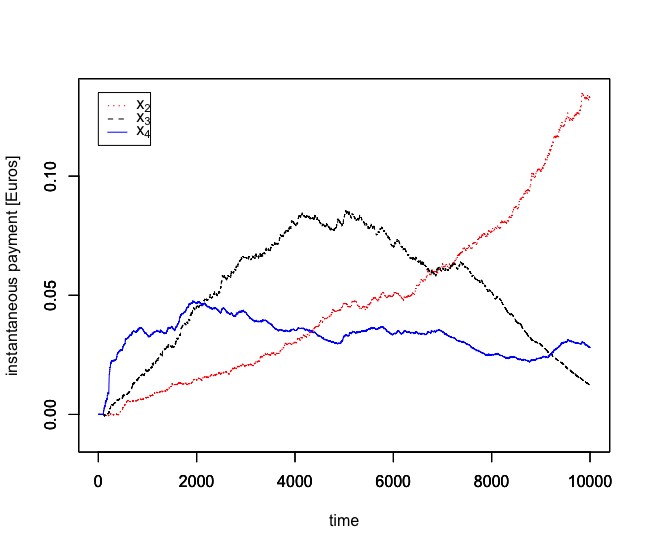

as illustrated in Figure 1(a).

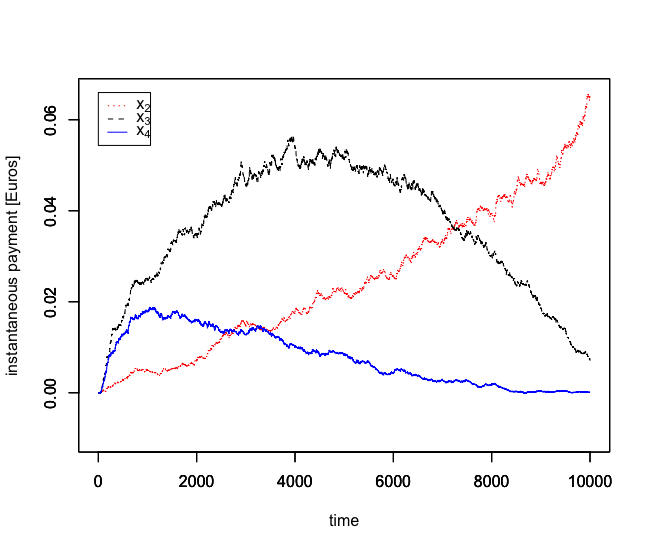

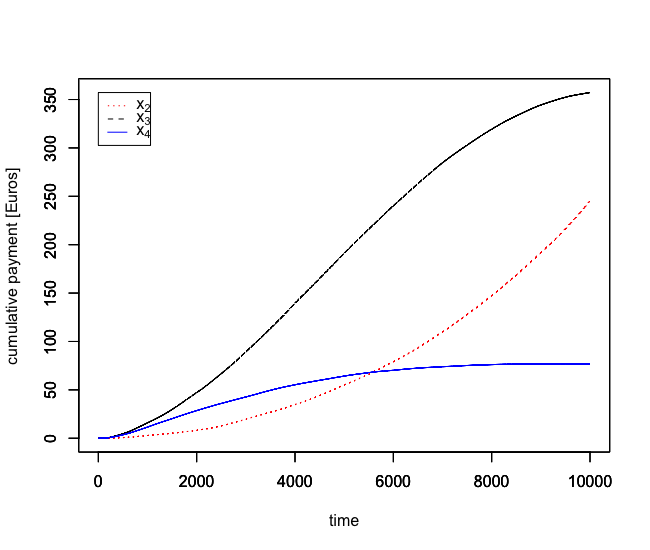

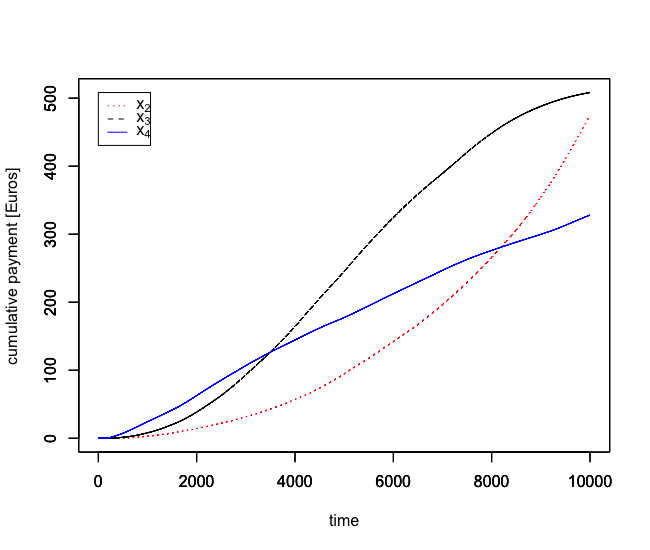

The central agent posts the task on the analytics platform, with online learning over a period of times steps, and defines a forgetting factor of 0.998. Since the online regression market relies on an online learning component, the parameters are tracked in time (see Figure 1(b)), and with the payments varying accordingly. Such online learning schemes are very efficient in tracking parameters in the types of regression models considered here, i.e., linear in their parameters and with parameters changing smoothly in time. The payments made for the 3 features of the support agents ( for , as well as and for ) are depicted in Figure 2, both in terms of instantaneous payments, and cumulative ones over the period. Since the model parameters (and their estimates) vary in time, the contributions of the various features to the improvement in the loss function also vary accordingly. This is reflected by the temporal evolution of the instantaneous payments. Here, for instance, since the estimated parameter is getting closer to 0 as time passes, its relative importance is decreasing. In contrast, the estimate is going up and down, and this yields a similar trajectory of the related instantaneous payments for the feature . Finally as the importance of grows with time (since, even if is negative, the contribution of to explaining the variance in the response variable increases), one observes a sharp rise in the corresponding instantaneous payment. Evidently, since cumulative in nature, the cumulative payments are non-decreasing with time (they can only increase or reach a plateau).

4.2.2 Case 2: Online learning in a quantile regression model

For this last simulation case, let us consider a linear quantile regression model, hence with a central agent aiming to perform online learning with a smooth quantile loss function. The underlying model for the process is such that

| (49) |

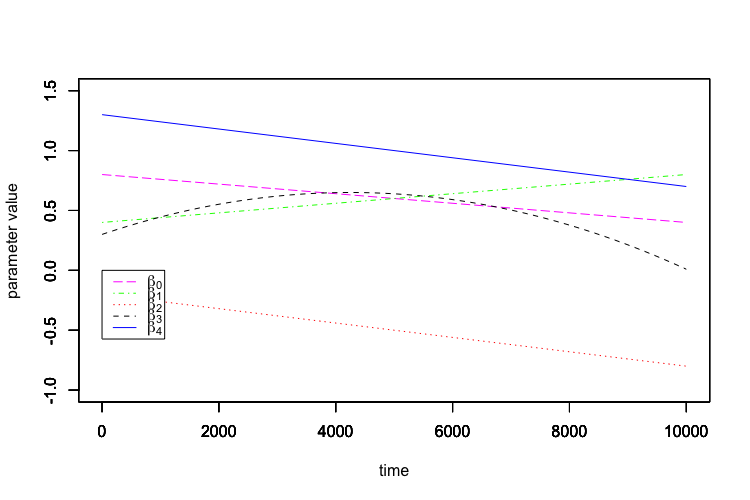

where , and are sampled from a standard Gaussian , is sampled from and the noise term is sampled from . It should be noted that the standard deviation of the noise is then scaled by . Thinking about the distribution of , that means that , and are important features to model its mean (or median), while will have an increased importance when aiming to model quantiles that are further away from the median (i.e., with nominal levels going towards 0 and 1). The temporal variation of the true model parameters are depicted in Figure 3.

The central agent posts the task on the analytics platform, with online learning over a period of time steps, and defines a forgetting factor of 0.999. The parameter of the smooth quantile loss function is set to . The payments made for the 3 features of the support agents ( for , as well as and for ) are depicted in Figure 4, both in terms of instantaneous payments, and cumulative ones over the period. These are for a choice of a nominal level of for the quantile of interest.

To illustrate the previous points made such that the relative value of the various features may depend on the nominal level , Table 5 gathers the payments obtained per feature and per agent in the cases of focusing on quantiles with nominal levels 0.1, 0.25, 0.5, 0.75 and 0.9. Particularly one retrieves the fact that the payment for feature is 0 when looking at the median. This is in line with the definition of the data generation process, for which is only supposed to have value to model and predict quantiles away from the median.

| 0.1 | 712.82 | 705.71 | 332.78 | 712.82 | 1038.49 |

|---|---|---|---|---|---|

| 0.25 | 751.19 | 748.03 | 112.81 | 751.19 | 860.84 |

| 0.5 | 747.63 | 749.59 | 0 | 747.63 | 749.59 |

| 0.75 | 658.78 | 666.06 | 150.21 | 658.78 | 816.27 |

| 0.9 | 519.37 | 531.04 | 341.72 | 519.37 | 872.76 |

5 Application to real-world forecasting problems

The regression market approach we proposed is originally developed with energy forecasting applications in mind. Besides the simulation-based case studies considered in the above to illustrate the workings and applicability of regression markets, we focus here on real-world applications using data from South Carolina (USA). Regression models are used as a basis for forecasting, hence with a learning stage (batch and online) and an out-of-sample stage (for genuine forecasting). We restrict ourselves to a fairly simple setup with 1-hour ahead forecasting, though other lead times could be similarly considered (possibly requiring different input data and regression models). The aim is certainly not to develop a forecasting approach which is to be better than the state-of-art, but to show how our regression market mechanism (i) incentivizes data sharing, (ii) yields improved forecasts, and (iii) appropriately compensates support agents for their contribution to improvement in the loss function (and the forecasts) of the central agent.

5.1 Data description and modeling setup

To ensure that the application to real-world data can be reproduced and comprises a good starting point for others, we use a dataset from an open database for renewable energy data in the USA. The wind power generation data for a set of 9 wind farms in South Carolina (USA) was extracted from the Wind Integration National Dataset (WIND) Toolkit described in Draxl et al. (2015). The data is hence not completely real, but still very realistic in capturing the local and spatio-temporal dynamics of wind power generation within an area of interest. It is owing to such spatio-temporal dynamics that one expects to see benefits in using others’ data to improve power forecasts – see Cavalcante et al. (2017) and Messner and Pinson (2019) for instance. An overview of the wind farms and of their characteristics is given in Table 6. These are all within 150 kms of each other. Wind power measurements are available for a period of 7 years, from 2007 to 2013, with an hourly resolution. For the purpose of the regression and forecasting tasks, all power measurements are normalized and hence take values in . An advantage of this type of data is that there is no missing and no suspicious data point to be analyzed and possibly to be removed. In this setup, each wind farm may be seen as an agent. We therefore have 9 agents who can take the role of either central or support agent. Let us write the power measurement of agent at time , which is a realization of the random variable .

| Agent | id | C [%] | P [MW] | Lat./Long. | County | Elevation [m] |

|---|---|---|---|---|---|---|

| 4456 | 34.11 | 1.75 | 34.248/-79.75 | Florence | 36.17 | |

| 4754 | 35.75 | 2.96 | 34.02/-79.537 | Florence | 17.5 | |

| 4934 | 36.21 | 3.38 | 33.925/-79.958 | Florence | 36.2 | |

| 4090 | 26.6 | 16.11 | 34.732/-82.122 | Laurens | 219.73 | |

| 4341 | 28.47 | 37.98 | 34.556/-81.889 | Laurens | 182.31 | |

| 4715 | 27.37 | 30.06 | 34.334/-82.133 | Laurens | 164.07 | |

| 5730 | 34.23 | 2.53 | 33.136/-80.857 | Colleton | 42.75 | |

| 5733 | 34.41 | 2.6 | 33.112/-80.665 | Colleton | 27.0 | |

| 5947 | 34.67 | 1.24 | 32.641/-80.504 | Colleton | 5.4 |

Emphasis is placed on very short-term forecasting (i.e., 1 hour ahead) as a basis for illustration of regression markets for a real-world setup. This allows us to use fairly simple time-series modeling and forecasting approaches. Those may readily extended to the case of further lead time, possibly using additional input features, e.g., from remote sensing and weather forecasts. More advanced modeling approaches could additionally be employed, e.g., if aiming to account for the nonlinearity and double-bounded nature of wind power generation (Pinson; 2012).

For a given central agent and support agents , the basic underlying model considered for the regression markets writes

| (50) |

which is simply an ARX model with maximum lag . In principle, one would run a data analysis exercise to pick the number of lags, or alternatively cross-validation. We assume here that expert knowledge, or such an analysis, allowed to conclude for the use of 2 lags for the central agent, and 1 lag only for the support agents.

For both cases in the following, we place ourselves within a simplified electricity market setup, where it is assumed that wind farms have to commit to a scheduled power generation 1-hour ahead. They then get a set price per MWh scheduled (e.g., 40$), though with a penalization afterwards for deviation from schedule. This penalization is proportional to a chosen loss function. In the first case, for the batch and out-of-sample regression markets, a quadratic loss function is used. This translates to the agents assessing their forecasts in terms of Mean Square Error (MSE) and aiming to reduce it. In the second case, we envision an asymmetric loss as in European electricity markets (with 2-price imbalance settlement), where agents then aim to reduce a quantile loss, with the nominal level of the quantile being a direct function of the asymmetry between penalties for over- and under-production (Morales et al.; 2014). In both cases, agents could perform an analysis to assess the value of forecasts in those markets, as well as their willingness to pay to improve either quadratic of quantile loss. Here, we consider that all agents have valued their willingness to pay, denoted and expressed in $ per percent point improvement in their loss function and per data point, to be shared between in-sample (batch or online) and out-of-sample regression markets. We use percent point improvement as those loss functions are normalized.

5.2 Batch and out-of-sample regression markets

In the batch and out-of-sample case, the first 10 000 time instants (so, a bit more than a year) are used to train the regression models within the batch regression market, while the following 10 000 time instants are for the out-of sample forecasting period, hence for the out-of-sample regression market.

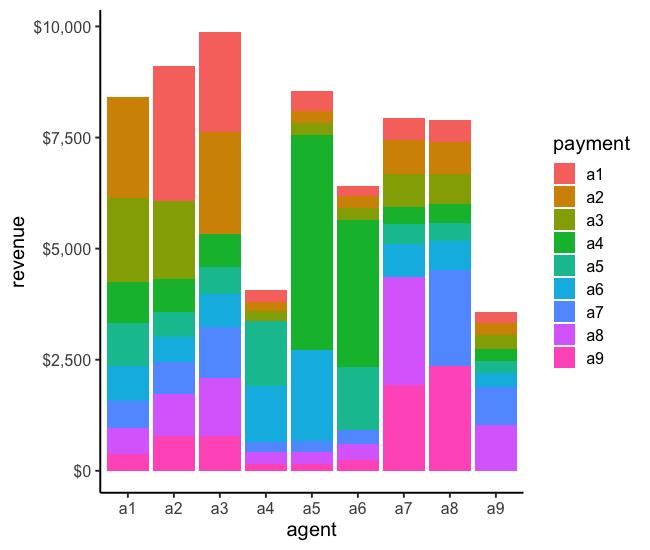

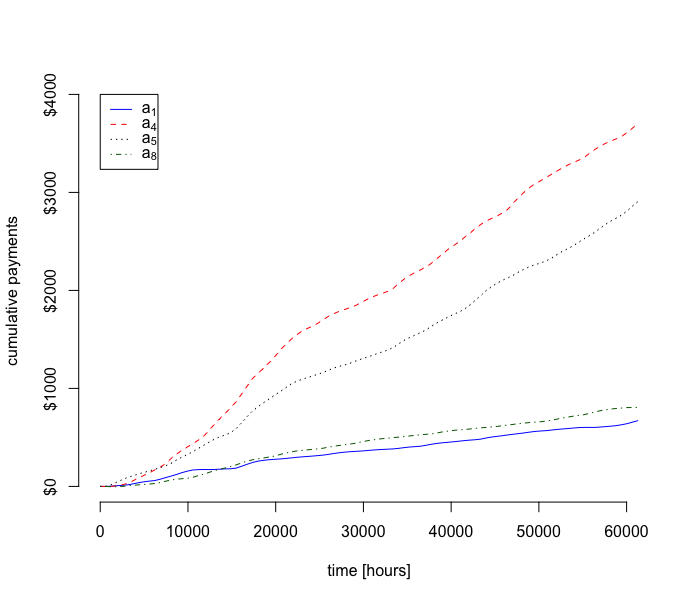

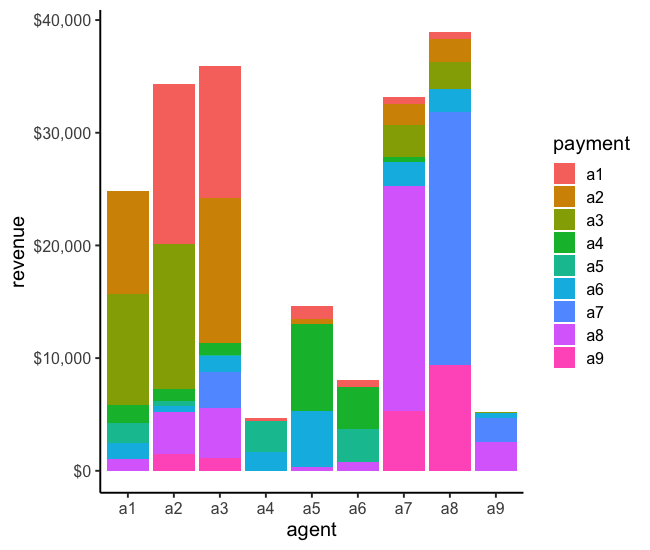

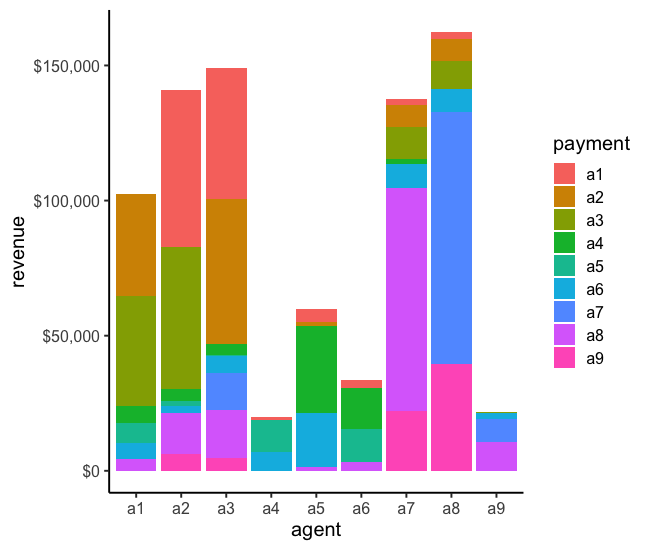

Let us first zoom in on the case of agent , splitting her willingness to pay as 0.5$ per percent point improvement in quadratic loss and per data point within the batch regression market, and 1.5$ for the out-of-sample regression market. In that case, in-sample through the batch regression market, the quadratic loss is reduced from 2.82% of nominal capacity to 2.32% thanks to the data of the support agents. And, out-of-sample, that loss decreases from 3.09% to 2.53% when relying on the support agents. The allocation policies as well as payments are gathered in Table 7. The overall payment of central agent for the two markets is of 10 855.98$. As mentioned when introducing regression markets, there may obviously be disparities between the value of features and data of support agents at the batch and out-of-sample stages. It is clear here for instance if looking at the Shapley allocation for support agent , where the in-sample allocation is of 32.35% and then dropping to 22.27% out-of-sample. For all other support agents, the Shapley allocation values increase when going from batch to out-of-sample regression markets, somewhat compensating for the substantial change observed for .

| Market | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| batch | [%] | 23.17 | 32.35 | 9.75 | 8.24 | 7.92 | 6.36 | 6.84 | 3.81 |

| [$] | 574.29 | 801.72 | 241.52 | 204.12 | 196.19 | 157.71 | 169.42 | 94.38 | |

| out-of-sample | [%] | 26.96 | 22.27 | 10.74 | 11.47 | 9.33 | 7.15 | 7.07 | 4.34 |

| [$] | 2284.52 | 1887.31 | 909.83 | 972.02 | 790.49 | 605.65 | 599.15 | 367.66 | |

| Total payment [$] | 2858.81 | 2689.03 | 1151.35 | 1176.14 | 986.68 | 763.36 | 768.57 | 462.04 | |

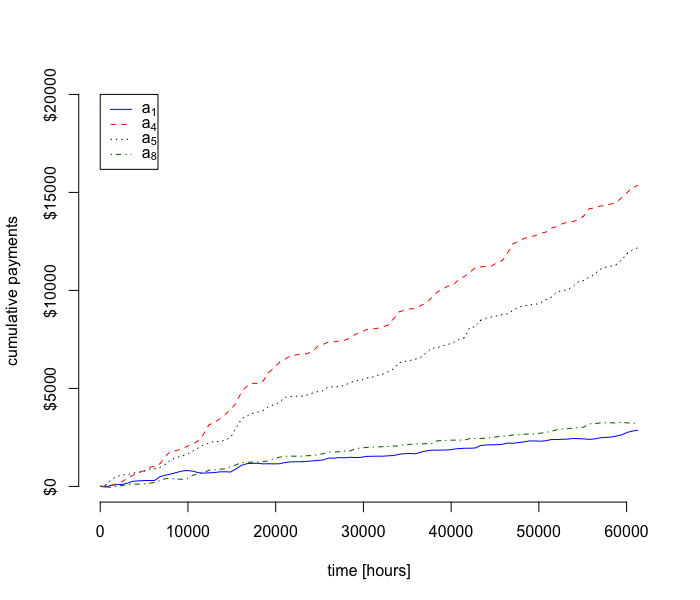

First of all, agents and provide the features that make the strongest contribution towards lowering the quadratic loss, both in-sample in the batch regression market and for genuine forecasting through the out-of-sample regression market. However, one of them () has higher Shapley allocation policy values in-sample, and the other one () out-of-sample. It is then reflected by the payments. Eventually, from the perspective of the support agents, those total payments should be divided by 20 000, to reflect the unit value of each data point provided for their features. For instance, the value of an individual data point of is of 14¢, and of only 2.3¢ for .