Representation of probability distributions with implied volatility and biological rationale

Department of Mathematics

Bar Ilan University

Ramat-Gan, Israel

Abstract

Economic and financial theories and practice essentially deal with uncertain future. Humans encounter uncertainty in different kinds of activity, from sensory-motor control to dynamics in financial markets, what has been subject of extensive studies. Representation of uncertainty with normal or lognormal distribution is a common feature of many of those studies. For example, proposed Bayessian integration of Gaussian multisensory input in the brain or log-normal distribution of future asset price in renowned Black-Scholes-Merton (BSM) model for pricing contingent claims.

Standard deviation of log(future asset price) scaled by square root of time in the BSM model is called implied volatility. Actually, log(future asset price) is not normally distributed and traders account for that to avoid losses. Nevertheless the BSM formula derived under the assumption of constant volatility remains a major uniform framework for pricing options in financial markets. I propose that one of the reasons for such a high popularity of the BSM formula could be its ability to translate uncertainty measured with implied volatility into price in a way that is compatible with human intuition for measuring uncertainty.

The present study deals with mathematical relationship between uncertainty and the BSM implied volatility. Examples for a number of common probability distributions are presented. Overall, this work proposes that representation of various probability distributions in terms of the BSM implied volatility profile may be meaningful in both biological and financial worlds. Necessary background from financial mathematics is provided in the text.

1 Background and introduction

1.1 Vanilla options

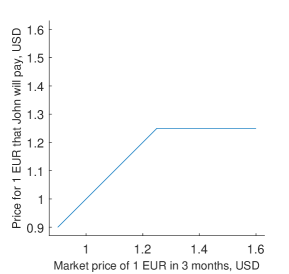

Example 1

Today €1 costs $1.25. John wants to buy €100,000 in 3 months from today. John does not want to bear a risk that the price of Euro will go up, on the other hand he wants to benefit in case the price of Euro will go down. To allow this, John buys a 3 months European call option with strike $1.25. If in 3 months €1 costs $1.20, John will pay $120,000 for his €100,000, less than $125,000 that he would pay today. If in 3 months €1 costs $1.30, John will exercise his option and buy €100,000 for $125,000 instead of $130,000. The graph with the amount John will pay for €1 depending on future €/$ exchange rate is depicted in Figure 1. If €/$ exchange rate is above the strike at option’s 3 months expiry John can simply benefit from the difference instead of taking a position in €111Say, 1€will cost 1.35$ in 3 months. Then John will be able to benefit ..

As demonstrated in Example 1, European call option provides an insurance against price increase at option’s expiry above a strike price defined in option’s contract. Option holder has a right to benefit from certain market moves and at the same time bears no obligations. Therefore, option is not free and has to be purchased as any insurance. If John from Example 1 needs to sell an asset at certain future date he could use an insurance against price decrease in the form of European put option. Holder of European put option has a right but not obligation to sell an asset at the strike price at option’s expiry. Both European call and European put are referred to as vanilla options.

Vanilla option prices for many assets222Like exchange rates, equities, commodities, interest rates, etc. are cited in the market. Vanilla option prices are commonly cited in terms of a notion called implied volatility. The renowned Black-Scholes-Merton (BSM) formula for vanilla option price establishes a relationship between option price and corresponding value of implied volatility [5]:

| (1) |

| (2) |

with

| (3) |

| (4) |

| (5) |

The following notation is used in formulae (1) - (5):

-

•

- price of vanilla call option

-

•

- price of vanilla put option

-

•

- today’s asset price

-

•

- strike price of the asset in option’s contract

-

•

- time to option’s expiry, i.e. when asset’s price is compared to the strike

-

•

, - local (of the currency that measures the asset price) and foreign interest333Intuitively, say one deposits in a bank $1,000 and get $1,050 in 1 year. In this case one earns 5% interest, in other words the interest rate of the deposit is 5%. respectively. In case of the option from Example 1 USD is local currency and EUR is foreign currency

-

•

- implied volatility; when is fixed and value of is the same for any strike , is equal to the standard deviation of annualized continuous returns444Standard deviation of , where is unknown asset’s price at future time . of

Here parameters and are defined in option’s contract, , and are cited in the market. Values of , depend on 555One may deposits $1,000 for 1 year and get 5% yearly interest, she may deposit $1,000 for 2 years and get a higher 6% yearly interest (receive ) in 2 years.. For the same , both call and put will imply the same value of implied volatility ; otherwise situation will create an arbitrage opportunity in the market and arbitrage will be realized pretty fast.

There is one-to-one (and of course monotonous) correspondence between vanilla option prices (, ) and values of implied volatility (). Consider an ideal and non-realistic case: for some predefined and for an arbitrary the same values of implied volatility are implied from option prices cited in the market, then the uncertainty of is described by normal distribution with standard deviation and expectation . Equivalently, the distribution of the future asset price is lognormal with the probability density function

| (6) |

The book by J. Hull "Options, futures and other derivatives" is among many different references with more detailed exposition of the basics of financial mathematics.

1.2 Vanilla price and implied probability density function

Let , , be option’s strike, time to expiry and today’s spot respectively. Let us write the formula for a call price in the form

| (7) |

where denotes implied666The word “implied” will sometimes be omitted further in text. Computations of volatility smiles in this work are related exclusively to implied probabilities. probability density of asset price at option’s expiry and denotes corresponding cumulative probability. Consequently,

| (8) |

Hence

| (9) |

In the ideal case when distribution of the future asset price is lognormal, formula (7) becomes [5]:

with ; , being respectively the mean and standard deviation of . For lognormal formula (7) is equivalent to formula (1) [5].

The formula for the put option price is:

| (10) |

The put-call parity states the following relationship between the prices of put and call with the same strike:

| (11) |

1.3 Biological motivation for representing uncertainty with log-normal implied volatility

According to Weber-Fechner law, the subjective perception/sensation is proportional to the logarithm of the stimulus intensity [3]:

| (12) |

is perception, is stimulus intensity and is constant. In other words, the relationship between stimulus and perception is logarithmic. Correspondingly, it is reasonable to propose that normal uncertainty in the stimulus would result in log-normal uncertainty in perception of the stimulus. It has been shown that the population distribution of the intrinsic excitability or gain of a neuron is a heavy tail distribution, more precisely a log-normal shape [4].

Different empirical works provided evidence that the brain both represents probability distributions and performs probabilistic inference, see for example review [7]. A study of uncertainty learning and integration in sensorimotor learning showed that subjects internally represent statistical distribution of task’s uncertainty () and subject’s uncertainty about true value of the sensed input (); the authors concluded that the central nervous system employs probabilistic models during sensorimotor learning [6]. The study employed bayesian integration of normally distributed uncertainties. Based on Weber-Fechner law [3], it could be proposed that normally distributed uncertainty of what is sensed/produced leads to log-normal type of uncertainty about the outer world within the internal representation.

For different kinds of assets, for example FX exchange rates, traders mostly measure option prices in terms of log-normal implied volatility instead of price measured in terms of currency. That is traders and financial institutions naturally prefer to use implied volatility as alternative measure for pricing uncertainty of the future asset price. Market’s estimates for uncertainty of future asset prices deviate from log-normal as vanilla options with different strikes have different implied volatilities. Nevertheless, the uncertainty is measured in a sense as a deviation from log-normal distribution whose implied volatility is constant. The relationship between implied volatility and option’s strike is called volatility smile.

2 Results

Any probability distribution defined by the density function whose integral (7) exists for any can be represented with implied volatility smile. Below a process for obtaining representation of probability distribution with implied volatility smile is demonstrated for a number of commonly used distributions with graphical examples of volatility smiles. In general the algorithm is as follows:

2.1 Implied volatility for different probability distributions

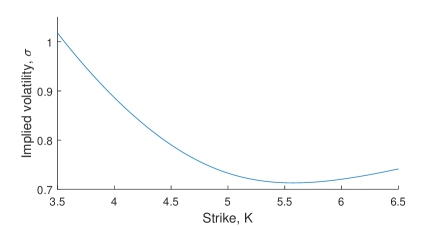

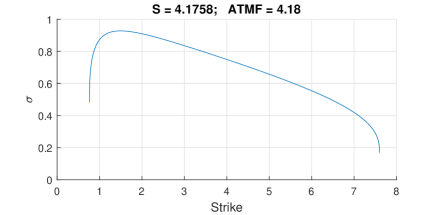

An example of implied volatility profile as a function of strike is demonstrated in Figure 2. The implied volatility in the figure is not flat and so the risk-neutral probability density for the future asset price is not log-normal. The graph of volatility smile shows that the distribution has fatter tails777The higher is implied volatility the greater is uncertainty and consequently vanilla option is more expensive. on both sides (especially on the left side) compared to log-normal distribution with equal to minimal (on the graph) value of implied volatility.

Probability distribution is defined by the shape of the volatility smile , spot , time to maturity , interest rates and . Values of , , , can be used to compute expectation of the future asset price equal to ATMF and to put a constraint on parameters of probability density function. Below I use vanilla call prices to compute implied volatility profiles that correspond to a number of implied probability density functions listed in Table 1.

| Distribution | Density function | Expected value (= ATMF = ) | Call price |

|---|---|---|---|

| Lognormal | formula (1) | ||

| Gamma | formula (14) | ||

| Normal | formula (27) | ||

| Translated Student | formula (39) | ||

| Uniform | formula (43) | ||

| Log uniform | formula (47) |

2.2 Gamma distribution of asset price at expiry

The probability density function of gamma distribution depends on two parameters, and :

| (13) |

Now compute the price of a call option when the risk neutral probability density follows gamma distribution. The computation will use the definition (7) of a call price:

| (14) | |||||

Here is the cumulative probability density function of gamma distribution (13). Correspondingly, the at the money forward (ATMF) of the asset would be the expected value of risk neutral probability density and for gamma distribution the ATMF is:

| (15) | |||||

By using the formula for the call price (14) and the put-call parity (11) get the price of the put option:

| (16) |

Formula (15) will be useful for constraining parameters of the risk-neutral probability density function given that

| (17) |

So the spot value now satisfies the following equality:

| (18) |

Equivalently, or

| (19) | |||||

| (20) |

So, for gamma distribution

| mean | (21) | ||||

| variance | (22) | ||||

| (23) | |||||

| (24) |

2.3 Normal distribution

The case of normal implied probability of the asset price in future time corresponds to Bachelier’s model of arithmetic Brownian motion [1]. The price of the call option according to Bachelier’s formula is computed as follows [2]:

| (27) | |||||

| (28) |

where is implied normal volatility888Equal to the standard deviation of the future asset price normalized by the square root of time in case the future asset price is normally distributed, is the forward value of the asset (strike with this value nullifies the forward contract), and is probability density of the standard normal distribution.

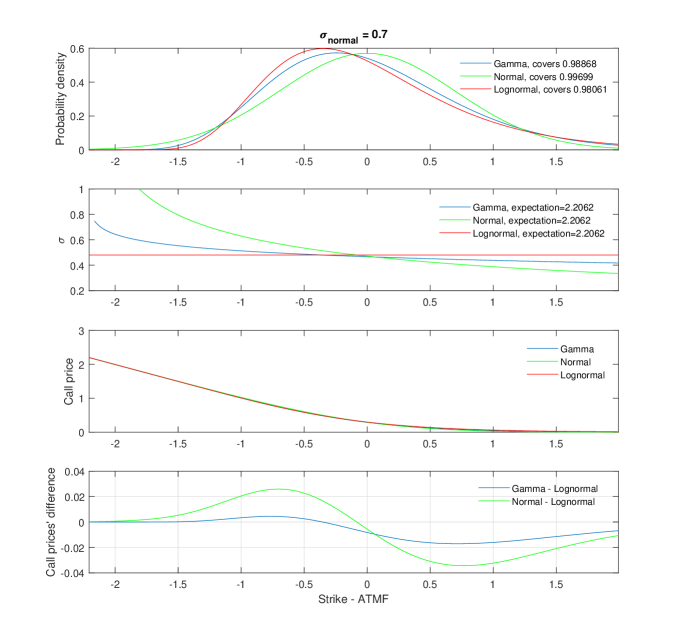

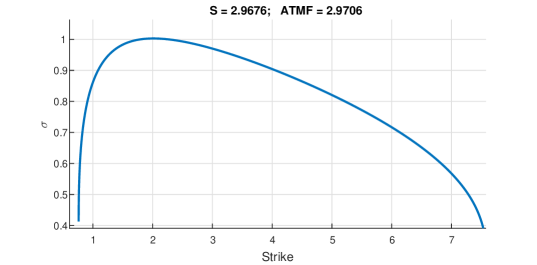

Examples of probability density, volatility smile and call option prices for gamma, normal and lognormal risk-neutral probability densities are demonstrated in Figure 3.

2.4 Translated Student’s -distribution

Probability density function for translated Student’s -distribution is defined as follows:

| (29) |

We consider the case when . The translated distribution is obtained from Student’s -distribution by translating the expected value of the distribution from zero to .

It is known that for the cumulative probability is as follows:

| (30) |

and for , using symmetry with respect to ,

| (31) |

where

| (32) |

and is regularized incomplete beta function:

| (33) |

is the beta function

and

is the incomplete beta function.

Now compute call option price for translated Student’s -distribution using formula (7) and assuming .

| (34) |

Denote

| (35) | |||||

| (36) |

Sign “+” in notation in formula (35) is used to emphasize that .

Now use derivations that lead to formula (34) in order to compute the call price for the case :

| (37) |

| (38) |

Due to symmetry, .

Now use (34) - (38) to write the formula for the call price when risk-neutral probability density function is translated Student’s -distribution:

Noting from (32) that we finally get the pricing formula for the call option:

| (39) |

Using put-call parity (11), the price for the put option is:

| (40) |

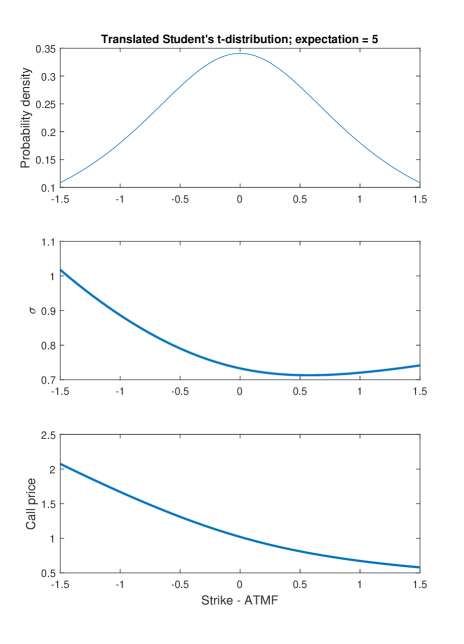

An example of volatility smile and call prices corresponding to some Student’s t-distribution is demonstrated in Figure 4.

2.5 Uniform distribution of the asset price at expiry

Probability density function for uniform distribution on an interval , , is defined as follows:

| (41) |

Using equation (7), the corresponding call price can be written as:

| (42) |

The case when is not interesting (the price of a call option would be zero) and so assume now that , then the price of the option is

| (43) |

The expected value is equal to ATMF strike999Otherwise arbitrage opportunity is created. and is computed as follows:

| (44) |

Using put-call parity (11), the price for the put option is:

| (45) |

An example of volatility smile corresponding to uniform risk-neutral probability density is depicted in Figure 5.

2.6 Log uniform distribution

Probability density function for log uniform distribution on an interval , , is defined as follows:

| (46) |

and corresponds to uniform distribution of . Using equation (7), the corresponding call price can be written as:

The case when is not interesting (the price of a call option would be zero) and so assume now that , then the price of a call option is

| (47) |

The expected value corresponding to ATMF strike is computed as follows:

| (48) |

An example of volatility smile corresponding to log-uniform risk-neutral probability density is depicted in Figure 6.

2.7 Mixture of log-normal distributions

All distributions considered above but uniform have probability density concentrated mostly near their single maximum. Now consider a different case of a probability distribution whose density may have several points of local maximum.

Mixture of log-normal distributions is defined on the same basis as the mixture of normal distributions. Let be normally distributed independent random variables with expectation and standard deviation respectively. Given non-negative numbers that sum up to 1, , the mixture of log-normal distributions is known to be:

| (49) |

Denote expectation of each log-normal distribution as follows: . Direct computations lead to the values of the expectation and variance of :

| (50) |

Noting that the random variables are also independent,

| (51) | |||||

Now use formula (7) for computing the price of the call option

| (52) | |||||

where corresponds to call option whose underlying at time is distributed according to .

3 Discussion

This work demonstrated examples of how probability distributions can be represented in terms of their corresponding implied volatilities. Of course, only distributions whose integral (7) exists are relevant. I propose the following advantages of representing probability distribution with corresponding volatility smile over probability density function:

-

1.

Such representation shows deviation of tails of the probability distribution from log-normal distribution and could visually provide information about fatness of tails versus log-normal distribution.

-

2.

When empirical data are fitted with probability density function from prescribed family (e.g. gamma, normal, lognormal) the fit cannot be precise. The deviation could be described by the geometric form of the volatility smile, although such process would require development of a suitable numerical procedure.

-

3.

It is more natural for humans performing repeatable creative processes that involve “creative” measuring of uncertainty, like options’ trading.

The above list is, probably, incomplete and further study would contribute to it.

Among different assets, interest rates may take negative values. Log-normal distribution is supported only for positive arguments though. In case of possible negative values of an asset, pricing formula (27) with normal implied volatility is used. It could be interesting to see how different probability distributions are represented with normal implied volatility what is left for future analysis.

Appendix A Delta of a call option when future asset price follows gamma distribution

Differentiate equation (14) with respect to spot in order to get formula for a delta of a call option. First of all find derivative of the gamma probability density function (13) with respect to parameter .

| (53) | |||||

Therefore, noting that cumulative distribution results from integrating the probability density with respect to , , differentiation of with respect to is identical to differentiation of in formula (53) because the integral has “nice” convergence properties.

Computations of call’s delta will use either of the two assumptions and each assumption will underlie a different value of .

-

1.

The parameter that defines the shape of the probability density function is constant while only is influenced by the changes in spot .

-

2.

Variance of the distribution is constant and both and are influenced by the changes in spot .

A.1 under the assumption of constant

The following property is satisfied when .

| (54) |

Now use formulae (53) and (54) to differentiate cumulative gamma probability with respect to spot :

| (55) | |||||

Here is an arbitrary parameter of the probability function while from (15) corresponds to the risk-neutral probability density of the future asset price. Now use formula (55) to differentiate the call price (26) with respect to .

| (56) | |||||

formula (15) was used in the equality one before the last.

A.2 under the assumption of constant variance

Use formulae (23, 24) to compute derivatives and under the assumption of constant variance:

| (57) | |||||

| (58) |

Now find the partial derivative

| (59) |

is the digamma function. There is no functional form that relates the integral of the right hand side of (59) over to cumulative probability function due to the factor , in contrary to the partial derivative of with respect to in (53). For this reason functional expression of for the case of constant variance is not derived. Numeric computation of can be based on numerical differentiation of the expression

Appendix B Delta of a call option when future asset price follows translated Student distribution

Differentiate equation (39) with respect to spot in order to get formula for a delta of a call option. First of all note the expression for derivative of the regularized incomplete beta function from (33) with respect to :

| (61) |

So, for from (32)

| (62) |

Correspondingly, from (62)

| (63) |

So, using formula (63), the formula for delta of the call option (39) is:

| (64) |

Appendix C Delta of a call option when future asset price follows uniform distribution

Use (44) to obtain . So,

| (65) |

Assume at the moment that and substitute (65) into (42) to get

| (66) |

Now compute :

| (67) | |||||

Equations (67) and (65) imply:

| (68) | |||||

So finally, the formula for of the call option when asset price is uniformly distributed is as follows.

| (70) |

Correspondingly, for ,

| (71) |

References

- [1] Louis Bachelier. Théorie de la spéculation. Annales scientifiques de l’École Normale Supérieure, 3e série, 17:21–86, 1900.

- [2] Paul Dawson, David Blake, Andrew J G Cairns, and Kevin Dowd. Options on normal underlyings. CRIS Discussion Paper Series, 2007.

- [3] Gustav Theoder Fechner. Elemente der Psychophysik [Elements of psychophysics]. Breitkopf und Härtel, Leipzig, 1860.

- [4] Scheler Gabriele. Logarithmic distributions prove that intrinsic learning is hebbian. F1000Research, 6, 2017.

- [5] J. Hull. Options, Futures and Other Derivatives. Options, Futures and Other Derivatives. Pearson/Prentice Hall, 2006.

- [6] Konrad P. Kording and Daniel M. Wolpert. Bayesian integration in sensorimotor learning. Nature, 427:244–247, 2004.

- [7] Alexandre Pouget, Jeffrey M Beck, Wei Ji Ma, and Peter E Latham. Probabilistic brains: knowns and unknowns. Nat Neurosci., 6(9):1170–1178, 2013.