Robust Generalized Method of Moments:

A Finite Sample Viewpoint

Abstract

For many inference problems in statistics and econometrics, the unknown parameter is identified by a set of moment conditions. A generic method of solving moment conditions is the Generalized Method of Moments (GMM). However, classical GMM estimation is potentially very sensitive to outliers. Robustified GMM estimators have been developed in the past, but suffer from several drawbacks: computational intractability, poor dimension-dependence, and no quantitative recovery guarantees in the presence of a constant fraction of outliers. In this work, we develop the first computationally efficient GMM estimator (under intuitive assumptions) that can tolerate a constant fraction of adversarially corrupted samples, and that has an recovery guarantee of . To achieve this, we draw upon and extend a recent line of work on algorithmic robust statistics for related but simpler problems such as mean estimation, linear regression and stochastic optimization. As two examples of the generality of our algorithm, we show how our estimation algorithm and assumptions apply to instrumental variables linear and logistic regression. Moreover, we experimentally validate that our estimator outperforms classical IV regression and two-stage Huber regression on synthetic and semi-synthetic datasets with corruption.

1 Introduction

Econometric and causal inference methodologies are increasingly being incorporated in automated large scale decision systems. Inevitably these systems need to deal with the plethora of practical issues that arise from automation. One important aspect is being able to deal with corrupted or irregular data, either due to poor data collection, the presence of outliers, or adversarial attacks by malicious agents. Even more classical applications of econometric methods in social science studies, can greatly benefit from robust inference so as not to draw conclusions solely driven by a handful of samples, as was recently highlighted in [3].

Recent work in statistical machine learning has enabled robust estimation for regression problems and more generally estimation problems that reduce to the minimization of a stochastic loss. However, many estimation methods in causal inference and econometrics do not fall under this umbrella. A more general statistical framework that encompasses the most widely used estimation techniques in econometrics and causal inference is the framework of estimating models defined via moment conditions. In this paper we offer a robust estimation algorithm that extends prior recent work in robust statistics to this more general estimation setting.

For a family of distributions , identifying the parameter is often equivalent to solving

| (1) |

for an appropriate problem-specific vector-valued function . This formalism encompasses such problems as linear regression (with covariates , response , and moment ) and instrumental variables linear regression (with covariates , response , instruments , and moment ).

Under simple identifiability assumptions, moment conditions are statistically tractable, and can be solved by the Generalized Method of Moments (GMM) [13]. Given independent observations , the GMM estimator is

for a positive-definite weight matrix . Of course, for general functions , finding (the global minimizer of a potentially non-convex function) may be computationally intractable. Under stronger assumptions, all approximate local minima of the above function are near the true parameter, in which case the GMM estimator is efficiently approximable. For instrumental variables (IV) linear regression, these assumptions follow from standard non-degeneracy assumptions.

Due to its flexibility, the GMM estimator is widely used in practice (or heuristic variants, in models where it is computationally intractable). Unfortunately, like most other classical estimators in statistics, the GMM estimator suffers from a lack of robustness: a single outlier in the observations can arbitrarily corrupt the estimate.

Robust statistics

Initiated by Tukey and Huber in the 1960s, robust statistics is a broad field studying estimators which have provable guarantees even in the presence of outliers [15]. Outliers can be modelled as samples from a heavy-tailed distribution, or even as adversarially and arbitrarily corrupted data. Classically, robustness of an estimator against arbitrary outliers is measured by breakdown point (the fraction of outliers which can be tolerated without causing the estimator to become unbounded [11]) and influence (the maximum change in the estimator under an infinitesimal fraction of outliers [12]). These metrics have spurred development and study of numerous statistical estimators which are often used in practice to mitigate the effect of outliers (e.g. Huber loss for mean estimation, linear regression, and other problems [14]).

Unfortunately, classical robust statistics suffers from a number of limitations due to emphasis on statistical efficiency and low-dimensional statistical problems. In particular, until the last few years, most high-dimensional statistical problems lacked robust estimators satisfying the following basic properties (see e.g. [5] for discussion in the setting of learning Gaussians and mixtures of Gaussians):

-

1.

Computational tractability (i.e. evading the curse of dimensionality)

-

2.

Robustness to a constant fraction of arbitrary outliers

-

3.

Quantitative error guarantees without dimension dependence.

In a revival of robust statistics within the field of theoretical computer science, estimators with the above properties have been developed for various fundamental problems in high-dimensional statistics, including mean and covariance estimation [5, 7], linear regression [8, 2], and stochastic optimization [6]. However, practitioners in econometrics and applied statistics often employ more sophisticated inference methods such as GMM and IV regression, for which computationally and statistically efficient robust estimators are still lacking.

Our contribution

In this work, we address the aforementioned lack. Extending the Sever algorithm for robust stochastic optimization [6], we develop a computationally efficient and provably robust GMM estimator under intuitive deterministic assumptions about the uncorrupted data. We instantiate this estimator for two special cases of GMM—instrumental variables linear regression and instrumental variables logistic regression—under distributional assumptions about the covariates, instruments, and responses (and in fact our algorithm also applies to the IV generalized linear model under certain conditions on the link function).

We corroborate the theory with experiments solving IV linear regression on corrupted synthetic and semi-synthetic data, which demonstrate that our algorithm outperforms non-robust IV as well as Huberized IV.

Techniques and Relation to [DKKLSS19]

Our robust GMM algorithm builds upon the Sever algorithm and framework introduced in [6] for stochastic optimization. In this section, we briefly outline the relation. The Sever algorithm robustly finds an approximate critical point for the empirical mean of input functions , i.e. for convex functions, approximately and robustly solves

The approach is to alternate between (a) finding an approximate critical point of the current sample set, and (b) filtering the sample set by , until convergence (i.e. when no samples are filtered out). Filtering ensures that at convergence, the mean of over the current sample set (which is small by criticality) is near the mean over the uncorrupted samples, so is an approximate critical point for the uncorrupted samples, as desired.

Any moment condition which is the gradient of some function can be interpreted as a critical-point finding problem, and solved in the above way. An example is linear regression, where the moment is the gradient of the squared-loss . However, is not a gradient, so IV linear regression cannot directly be solved by Sever. In general, we need a way to robustly find an approximate solution to

Our approach is to alternate approximately minimizing

where is the current sample set, with a filtering step. However, it is not sufficient to filter by , because the minimization step does not necessarily output for which is small (unlike for Sever, where , and so an approximate zero of can always be found, for an arbitrary set of functions ).

To fix this, we introduce a second filtering step based on . Under an identifiability condition for the uncorrupted samples (which is needed even in the absence of corruption), we show that the above situation, where is large, can be detected by the gradient filtering step, so that at convergence the empirical moment is in fact small.

Further related work

The generalized method of moments and instrumental variables regression have indeed been studied in the context of robust statistics [1, 10, 17, 18]. However, the resulting estimators face the same nearly ubiquitous issues described above. For instance, [1] presents a variant of two-stage least squares which uses least absolute deviations. The resulting estimator performs well under the metric of bounded influence, but an arbitrary outlier can still cause arbitrary changes in the estimator. The estimator proposed by [10] modifies the closed-form solution to IV linear regression using robust mean and covariance estimators. These have attractive theoretical properties but are computationally intractable, and the heuristics by which they are implemented in practice have no associated theoretical guarantees. The robust GMM estimator presented in [18] has bounded influence but is not robust to a constant fraction of outliers.

2 Preliminaries

For random variables indexed by a set , we use the notation for the sample expectation . Similarly, if are scalars, then we define the sample variance . If are vectors then we define the sample covariance matrix . A random vector is -hypercontractive if for all vectors .

Definition 2.1.

For a closed set , a function , and , a -approximate critical point of (in ) is some such that for any vector with for arbitrarily small , it holds that .

Definition 2.2.

For a closed set , a -approximate learner is an algorithm which, given a differentiable function returns a -approximate critical point of .

Definition 2.3.

The (unscaled) logistic function is defined by .

Outline

In Section 3, we describe the robust GMM problem, and we describe deterministic assumptions on a set of corrupted sample moments, under which we’ll be able to efficiently estimate the parameter which makes the uncorrupted moments small. In Section 4, we describe a key subroutine of our robust GMM algorithm, which is commonly known in the literature as filtering. In Section 5, we describe the robust GMM algorithm and prove a recovery guarantee under the assumptions from Section 3. In Section 6, we apply this algorithm to instrumental variable linear and logistic regression, proving that under reasonable stochastic assumptions on the uncorrupted data, arbitrarily -corrupted moments from these models satisfy the desired deterministic assumptions with high probability. Finally, in Section 7, we evaluate the performance of our algorithm on two corrupted datasets.

3 Robust GMM Model

In this section, we formalize the model in which we will provide a robust GMM algorithm. Classically, the goal of GMM estimation is to identify given data , using the moment condition . We consider the added challenge of the -strong contamination model, in which an adversary is allowed to inspect the data and replace samples with arbitrary data, before the algorithm is allowed to see the data. This corruption model encompasses most reasonable sources of outliers.

For our main theorem, we do not make stochastic assumptions about . Instead, we make deterministic assumptions (strong identifiability, boundedness, and so forth) about the moments of the corrupted data (for IV linear and logistic regression, we will prove that the assumptions hold with high probability under reasonable distributional assumptions).

Concretely, since only samples were corrupted, there is a set of uncorrupted samples. This set is unknown, but all we need is that it exists. More specifically, we assume that there exists a large subset of the data, of size at least , which satisfies finite-sample analogues of various distributional identifiability and boundedness conditions.

Assumption 3.1.

Given differentiable moments , a corruption parameter , well-conditionedness parameters and , a Lipschitzness parameter , and a noise level parameter , there is a set with (the “uncorrupted samples”), a vector (the “true parameter”), and a radius with the following properties:

-

•

Strong identifiability.

-

•

Bounded-variance gradient. for all unit-vectors ,

-

•

Bounded-variance noise. for all unit vectors

-

•

Well-specification.

-

•

Lipschitz gradient. for all

-

•

Stability of gradient. .

The stability of the gradient condition essentially states that the radius of the ball containing is sufficiently small that cannot change much in this ball. Note that if the gradient is constant in , as for IV linear regression, then the Lipschitz gradient assumption is satisfied with , and the stability assumption is vacuous. For non-linear moment problems, such as our logistic IV regression problem, this condition requires that the -norm of the parameters be sufficiently small, such that the logits do not approach the flat region of the logistic function, a condition that is natural to avoid loss of gradient information and extreme propensities.

Lemma 3.2.

Under Assumption 3.1, the following bounds hold for all :

-

•

for all unit vectors and

-

•

-

•

-

•

-

•

4 The Filter Algorithm

In many robust statistics algorithms, an important subroutine is a filtering algorithm for robust mean estimation. In this section we describe a filtering algorithm used in numerous prior works, including e.g. [6]. Given a set of vectors and a threshold , the algorithm returns a subset, by thresholding outliers in the direction of largest variance. Formally, see Algorithm 1.

This algorithm has two important properties. First, if it does not filter any samples, then the sample mean is provably stable, i.e. it cannot have been affected much by the corruptions, so long as the uncorrupted samples had bounded variance (proof in Appendix B.1).

Lemma 4.1.

Suppose that Filter does not filter out any samples. Then

for any and such that .

Second, if the threshold is chosen appropriately (based on the variance of the uncorrupted samples), then the filtering step always in expectation removes at least as many corrupted samples as uncorrupted samples. Equivalently, the size of the symmetric difference between the current sample set and the uncorrupted samples (i.e. the number of corrupted samples in the current set plus the number of uncorrupted samples which have been filtered out of the current set) always decreases in expectation (proof in Appendix B.1.1).

Lemma 4.2.

Consider an execution of Filter with sample set of size , and vectors , and bound . Let be the sample set after this iteration’s filtering. Let satisfy . Suppose that , then

where the expectation is over the random threshold.

5 The Iterated-Gmm-Sever Algorithm

In this section, we describe and analyze an algorithm Iterated-Gmm-Sever for robustly solving moment conditions under Assumption 3.1. The key subroutine is the algorithm Gmm-Sever, which given an initial estimate and a radius such that the true parameter is contained in , returns a refined estimate such that (with large probability) the radius bound can be decreased by a constant factor.

Like the algorithm Sever [6], our algorithm Gmm-Sever alternates (a) finding a critical point of a function associated to the current samples, and (b) filtering out “outlier” samples. Unlike Sever, the function we optimize is not simply an empirical mean over the samples, but rather the squared-norm of the sample moments. Moreover, we need two filtering steps: the moments as well as directional derivatives of the moments, in a carefully chosen direction. See Algorithm 2 for the complete description.

We will only prove a constant failure probability for Gmm-Sever. However, we will show that it can be amplified to an arbitrarily small failure probability . We call the resulting algorithm Amplified-Gmm-Sever; see Algorithm 3. The algorithm Iterated-Gmm-Sever then consists of iteratively calling Amplified-Gmm-Sever to refine the parameter estimate and bound the true parameter within successively smaller balls; see Algorithm 4.

We start by analyzing Gmm-Sever. In the next two lemmas, we show that if the algorithm does not filter out too many samples, then we can bound the distance from the output to . First, we show a first-order criticality condition (in the direction ) for the norm of the moments of the “good" samples. If there was no corruption, then we would have an inequality of the form

With -corruption, the algorithm is designed so that we can still show the following inequality, matching the above guarantee up to (proof in Appendix C.1):

Lemma 5.1.

Under Assumption 3.1, at algorithm termination, if , then the output of Gmm-Sever satisfies

Moreover, we can show that any point satisfying the first-order criticality condition must be close to , using the least singular value bound on the gradient (proof in Appendix C.2).

Lemma 5.2.

Putting the above lemmas together, we immediately get the following bound on .

Lemma 5.3.

Under Assumption 3.1, at algorithm termination, if , then the output of Gmm-Sever satisfies

It remains to bound the size of at termination. We follow the super-martingale argument from [6], which uses Lemma 4.2 (proof in Appendix C.3).

Theorem 5.4.

Suppose that the initial conditions and satisfy . Let be the output of Gmm-Sever. Then with probability at least , it holds that

The time complexity of Gmm-Sever is where is the time complexity of the -approximate learner . Moreover, for any the success probability can be amplified to by repeating Gmm-Sever times, or until at termination. We call this Amplified-Gmm-Sever, and it has time complexity .

With the above guarantee for Gmm-Sever and Amplified-Gmm-Sever, we can now analyze Iterated-Gmm-Sever (proof in Appendix C.4).

Theorem 5.5.

Suppose that the input to Iterated-Gmm-Sever consists of functions , a corruption parameter , well-conditionedness parameters and , a Lipschitzness parameter , a noise level parameter , a radius bound , and an optimization error parameter , such that Assumption 3.1 is satisfied for some unknown parameter , and . 111This constant may be improved; we focus in this paper on dependence on the parameters of the problem and do not optimize constants. Suppose that the algorithm is also given a failure probability parameter .

Then the output of Iterated-Gmm-Sever satisfies

with probability at least . Moreover, the algorithm has time complexity , where is the time complexity of a -approximate learner and .

6 Applications

In this section, we apply Iterated-Gmm-Sever to solve linear and logistic instrumental variables regression in the strong contamination model.

Robust IV Linear Regression

Let be the vector of real-valued instruments, and let be the vector of real-valued covariates. Suppose that and are mean-zero. Suppose that the response can be described as for some fixed . The distributional assumptions we will make about , , and are described below.

Assumption 6.1.

Given a corruption parameter , well-conditionedness parameters and , hypercontractivity parameter , noise level parameter , and norm bound , we assume the following: (i) Valid instruments: , (ii) Bounded-variance noise: , (iii) Strong instruments: , (iv) Boundedness: , (v) Hypercontractivity: is -hypercontractive, (vi) Bounded 8th moments: and (vii) Bounded norm parameter: .

Define

for , and let be independent samples drawn according to . Let . We prove that under the above assumption, if is sufficiently large, then with high probability, for any -contamination of , the functions satisfy Assumption 3.1. Formally, we prove the following theorem (see Appendix D):

Theorem 6.2.

Let . Suppose that for a sufficiently small constant , and suppose that for a sufficiently large constant . Then with probability at least over the samples , the following holds: for any -corruption of the samples and any upper bound , Assumption 3.1 is satisfied. In that event, if , , , and are known, then there is a -time algorithm which produces an estimate satisfying, with probability at least :

Robust IV Logistic Regression

Let be a vector of real-valued instruments, and let be a vector of real-valued covariates. Suppose that and are mean-zero. Suppose that the response can be described as for some fixed , where is the (unscaled) logistic function. The proofs only use -Lipschitzness of and , and that is bounded away from .

As far as distributional assumptions, we assume in this section that Assumption 6.1 holds, and additionally assume that the norm bound satisfies for an appropriate constant , where , , and are as required for the Assumption. We obtain the following algorithmic result (proof in Appendix E):

Theorem 6.3.

Let . Suppose that for a sufficiently small constant , and suppose that for a sufficiently large constant . Suppose that . Then with probability at least over the samples , the following holds: for any -corruption of the samples, Assumption 3.1 is satisfied. In that event, if , , , , and are known, then there is a -time algorithm which produces an estimate satisfying, with probability at least :

7 Experiments

In this section we corroborate our theory by applying our algorithm Iterated-Gmm-Sever to several datasets for IV linear regression with heterogeneous treatment effects. This is a natural setting in which the instruments and covariates are high-dimensional, necessitating dimension-independent robust estimators.

IV Linear Regression with Heterogeneous Treatment Effects.

Consider a study in which each sample has a vector of characteristics, a scalar instrument , a scalar treatment , and a response . Assuming that the average treatment effect is linear in the characteristics with unknown coefficients, and that the response noise is independent of the instrument, we can write a moment condition

This can be interpreted as an IV linear regression, and therefore our algorithm applies to it.

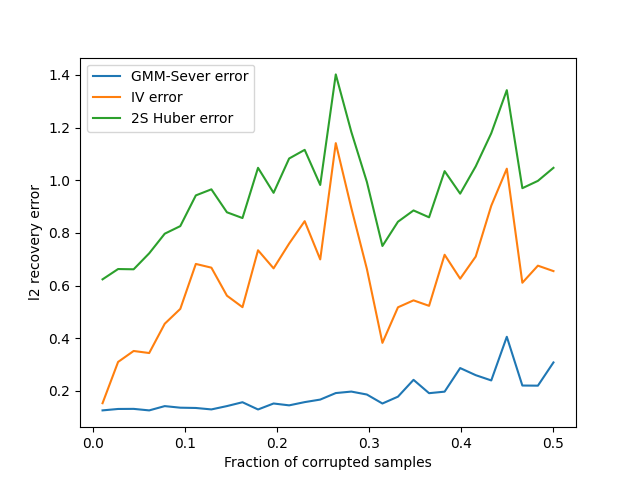

Synthetic experiment.

For our first experiment, we generate a unknown -dimensional parameter vector . We then generate independent samples each with a -dimensional characteristic vector drawn from . The instrument is drawn from an unbiased Bernoulli distribution, and the binary treatment is drawn from a Bernoulli- distribution with

where is a standard normal random variable and . Finally, the response is

The treated samples () with positive tend to have larger (and hence larger response), and the treated samples with negative tend to have smaller (and hence smaller response), so ordinary least-squares would tend to overestimate the treatment effect in the direction of the all-ones vector. However, is by construction independent of , so is a valid instrument. Indeed, in the absence of corruption, IV linear regression approximately recovers the true parameter .

We then corrupt an -fraction of the samples, by setting the characteristic vector equal to the all-ones vector (and leaving the instrument and response unchanged). We compute the recovery error of Iterated-Gmm-Sever, classical IV, and two-stage Huber regression for varying between and . For each choice of , we repeat the experiment times and average the recovery errors for each algorithm. See Figure 1(a) for the results.

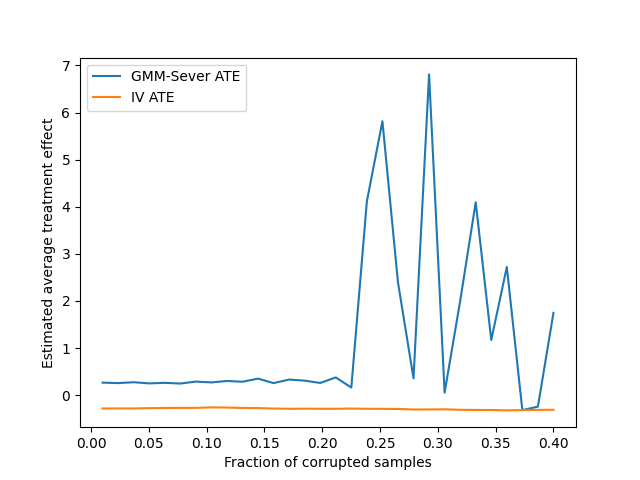

Semi-synthetic experiment.

In this experiment, we use the data of Card [4] from the National Longitudinal Survey of Young Men for estimating the average treatment effect (ATE) of education on wages. The data consists of samples with years of education as the treatment, log wages as the response, and proximity to a -year college as the instrument, along with covariates (e.g. geographic and demographic indicator variables). For simplicity, we restrict the model to only two covariates (years and squared years of labor force experience). We find that the ATE estimated by Iterated-Gmm-Sever is close to the positive ATE estimated by classical IV, suggesting that Card’s inference may be robust. Next, we corrupt an -fraction of the data. Specifically, we solve the IV regression on the uncorrupted data, and we alter the responses of a random -fraction of the data in a way such that the parameter which satisfies the moment conditions is exactly negated (for not too small, this can be done by solving an underdetermined linear system). This in particular negates the ATE inferred by classical IV regression.

In Figure 1(b), we plot the ATE inferred by IV and the ATE inferred by Iterated-Gmm-Sever as is varied from to (the Iterated-Gmm-Sever breaks down on this data for larger levels of corruption). We see that Iterated-Gmm-Sever approximately recovers the correct (positive) ATE of the uncorrupted data, for up to around . For larger , the estimate becomes unstable. This is due to the algorithm removing some but not all of the outliers, which are very large norm. We expect that an additional norm thresholding procedure could help remedy this instability, but further investigation may be required.

References

- [1] Takeshi Amemiya. Two stage least absolute deviations estimators. Econometrica: Journal of the Econometric Society, pages 689–711, 1982.

- [2] Ainesh Bakshi and Adarsh Prasad. Robust linear regression: Optimal rates in polynomial time. In Proceedings of the 53rd Annual ACM SIGACT Symposium on Theory of Computing, pages 102–115, 2021.

- [3] Tamara Broderick, Ryan Giordano, and Rachael Meager. An automatic finite-sample robustness metric: Can dropping a little data change conclusions?, 2021.

- [4] David Card. Using geographic variation in college proximity to estimate the return to schooling, 1993.

- [5] Ilias Diakonikolas, Gautam Kamath, Daniel Kane, Jerry Li, Ankur Moitra, and Alistair Stewart. Robust estimators in high-dimensions without the computational intractability. SIAM Journal on Computing, 48(2):742–864, 2019.

- [6] Ilias Diakonikolas, Gautam Kamath, Daniel Kane, Jerry Li, Jacob Steinhardt, and Alistair Stewart. Sever: A robust meta-algorithm for stochastic optimization. In International Conference on Machine Learning, pages 1596–1606. PMLR, 2019.

- [7] Ilias Diakonikolas, Gautam Kamath, Daniel M Kane, Jerry Li, Ankur Moitra, and Alistair Stewart. Being robust (in high dimensions) can be practical. In International Conference on Machine Learning, pages 999–1008. PMLR, 2017.

- [8] Ilias Diakonikolas, Weihao Kong, and Alistair Stewart. Efficient algorithms and lower bounds for robust linear regression. In Proceedings of the Thirtieth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 2745–2754. SIAM, 2019.

- [9] Rick Durrett. Probability: theory and examples, volume 49. Cambridge university press, 2019.

- [10] Gabriela V Cohen Freue, Hernan Ortiz-Molina, and Ruben H Zamar. A natural robustification of the ordinary instrumental variables estimator. Biometrics, 69(3):641–650, 2013.

- [11] Frank R Hampel. A general qualitative definition of robustness. The Annals of Mathematical Statistics, 42(6):1887–1896, 1971.

- [12] Frank R Hampel. The influence curve and its role in robust estimation. Journal of the american statistical association, 69(346):383–393, 1974.

- [13] Lars Peter Hansen. Large sample properties of generalized method of moments estimators. Econometrica: Journal of the econometric society, pages 1029–1054, 1982.

- [14] Peter J Huber. Robust estimation of a location parameter. In Breakthroughs in statistics, pages 492–518. Springer, 1992.

- [15] Peter J Huber. Robust statistics, volume 523. John Wiley & Sons, 2004.

- [16] Arun Jambulapati, Jerry Li, Tselil Schramm, and Kevin Tian. Robust regression revisited: Acceleration and improved estimation rates. arXiv preprint arXiv:2106.11938, 2021.

- [17] William S Krasker. Two-stage bounded-lnfluence estimators for simultaneous-equations models. Journal of Business & Economic Statistics, 4(4):437–444, 1986.

- [18] Elvezio Ronchetti and Fabio Trojani. Robust inference with gmm estimators. Journal of econometrics, 101(1):37–69, 2001.

- [19] Joel A Tropp. An introduction to matrix concentration inequalities. arXiv preprint arXiv:1501.01571, 2015.

Appendix A Omitted proofs from Section 3

A.1 Proof of Lemma 3.2

Proof.

First claim.

Note that

where the first inequality expands as and applies Cauchy-Schwarz to the resulting second term; the second inequality applies the Lipschitz gradient assumption and bounded-variance gradient assumption at ; the third inequality applies the stability of gradient assumption; and the fourth inequality uses that . It follows that

as claimed.

Second claim.

Observe that for any unit vector ,

The first term is at most by the bounded-variance noise assumption. The second term can be written and bounded as

by the first claim. This proves the second claim.

Third claim.

We have for any that , so

as claimed, where the second inequality uses the strong identifiability assumption and Lipschitz gradient assumption, and the third inequality uses the stability of gradient assumption.

Fourth claim.

We note that

The expectation of the gradient has operator norm at most by bounded-variance and Lipschitzness of the gradient, and this is at most by stability of the gradient and the inequality . As a result,

so together with well-specification it follows that as claimed.

Fifth claim.

This follows immediately from the first claim. Indeed, for any and unit vectors and ,

Taking the supremum over all we get that as claimed. ∎

Appendix B Omitted proofs from Section 4

B.1 Proof of Lemma 4.1

Proof.

If the algorithm does not remove any samples, then it holds that

The claim then follows from application of Lemma F.1 to sets and , since the total variation distance between the uniform distribution on and the uniform distribution on is at most . ∎

B.1.1 Proof of Lemma 4.2

Proof.

If no elements are filtered out, then the inequality trivially holds. Suppose otherwise. The difference is precisely the number of good elements (i.e. ) filtered out in this iteration minus the number of bad elements filtered out in this iteration. Due to the random thresholding, the expectation of the former is , and the expectation of the latter is . Thus, we need to show that .

Define and . Let be the largest eigenvector of . We have that

where the first inequality uses the fact that variance is the smallest second moment obtainable by shifting; the second inequality uses that and ; and the third inequality is by the lemma’s assumption.

On the other hand, since the algorithm doesn’t terminate, it holds that

Defining , , and , it follows that

There are two cases to consider:

-

1.

If . Then

Thus,

-

2.

If . By the above calculation,

On the other hand,

But . As a result,

But .

In either case, the desired claim holds. ∎

Appendix C Omitted proofs from Section 5

C.1 Proof of Lemma 5.1

Proof.

By the termination conditions of Gmm-Sever, no samples are filtered out in the last iteration. Thus, by Lemma 4.1 and the bounds , since no samples are filtered out on Step 3, it holds that

where the last inequality uses the guarantee of Lemma 3.2 that for unit vectors .

In the second filter operation, since no samples are filtered out, Lemma 4.1 implies that

where the last inequality uses that by Lemma 3.2. Next, since by Lemma 3.2, it follows that

Together with the first inequality, we get that

By assumption, . Therefore assuming that . Substituting this bound, we get

Now recall that is a -critical point of in the region . Since , the line segment between and is also contained in , so by definition of a -critical point, it holds that

So by the triangle inequality, and rounding up the above constants to integers,

as claimed. ∎

C.2 Proof of Lemma 5.2

Proof.

Expanding as an integral, we have that

Now, the first term is precisely . We bound the absolute value of the second term by Cauchy-Schwarz and the Lipschitzness of the gradient; it is at most

As a result,

Suppose that . Then by assumption that , it follows that . Thus , which contradicts the assumptions that and . We conclude that in fact , so that

However, by Assumption 3.1 and Lemma 3.2,

So together with the lemma’s assumption,

As a result,

so that by the least singular value bound in Lemma 3.2, as claimed. ∎

C.3 Proof of Theorem 5.4

Proof.

For let be the algorithm’s sample set at the beginning of the -th iteration, so that . Define a “sticky" stochastic process based on :

By soundness of the filtering algorithm (Lemma 4.2), we know that is a super-martingale. By Ville’s maximal inequality [9] and since , it holds with probability at least that . In this event, for all , so , and therefore . In particular, , where is the terminal sample set. Then by Lemma 5.3, it follows that

where is the output of GMM-Sever. Since this bound holds deterministically whenever , the failure probability can be decreased to by repeating GMM-Sever until either , or repetitions have occurred.

The time complexity bound follows from observing that the Filter algorithm runs in polynomial time, and in each repetition at least one sample is removed from , so the algorithm terminates after at most repetitions. ∎

C.4 Proof of Theorem 5.5

Proof.

Formally, Iterated-Gmm-Sever does the following procedure:

-

1.

Initialize , , , , and

-

2.

Compute

-

3.

Set

-

4.

If , then terminate and return . Otherwise, set , , and return to step (2).

First, note that by induction and the termination condition, is halved in every iteration, so it holds for all that .

Runtime.

The termination condition is deterministic. In particular, the algorithm will terminate once

This holds if . Since halves in every iteration and , the algorithm will therefore terminate after at most iterations. By the runtime bound on Amplified-Gmm-Sever, it follows that Iterated-Gmm-Sever has time complexity .

Correctness.

Next, we claim by induction that after the -th call to Amplified-Gmm-Sever, it holds with probability at least that . For , this follows from Theorem 5.4 and the assumption that (which implies that ).

Now fix any for which the algorithm has not yet terminated, and condition on . Then by the triangle inequality,

As a result, . In this event, by Theorem 5.4, it holds with probability at least that . By the induction hypothesis, the event we conditioned on occurs with probability at least , so by a union bound, it holds that with probability at least , completing the induction.

Now consider the final iteration . Restating the termination condition, we have

By assumption that , it follows that

Thus, with probability at least , the output of Iterated-Gmm-Sever satisfies

By the choice of , this bound is . By the iteration bound and choice of , the overall failure probability is at most . ∎

Appendix D Proof of Theorem 6.2

We need to prove that the contaminated samples satisfy Assumption 3.1 with some set of size . To this end, it suffices to prove that with high probability over the original samples , there is a subset of these original samples, with , such that for any subset of size at least , the conditions of Assumption 3.1 are satisfied. In this event, the intersection of with the uncontaminated samples certifies the assumption.

In the subsequent lemmas, we verify one by one that each condition of Assumption 3.1 is satisfied with high probability for all subsets of size at least of a set of size at least ; we then take the intersection of the sets to yield a set witnessing Assumption 3.1.

Lemma D.1.

Let be sufficiently small. If then with probability at least , there is a subset of size such that for every subset with , it holds that

As a consequence, if is less than a sufficiently small constant, then

Proof.

The first statement follows from Corollary F.4, -hypercontractivity of , and the covariance upper bound on . Let . It follows from the first statement, that for any ,

By assumption that , it follows that . The second statement follows. ∎

Lemma D.2.

Let and suppose that for an appropriate constant . Then with probability , there is a set with such that for all unit vectors and .

Proof.

By hypercontractivity, we have

for any vector , and similarly for . Moreover, we have assumed that the coordinates of and have th moments bounded by . Thus, we can apply Lemma F.6 to and to get sets each of size at least , that with probability satisfy

and

for all unit vectors and . Let . Then , and the above bounds hold over as well up to a constant factor loss. Thus,

The lemma follows. ∎

Lemma D.3.

Let and suppose that . Then with probability , there is a set with such that for every unit vector .

Proof.

Since , observe that for every unit vector . The claim follows from Corollary F.4. ∎

Lemma D.4.

Let , and suppose that . With probability , there is a subset with such that for every with , it holds that

Proof.

Observe that and by assumption. The claim follows from Lemma F.5. ∎

Corollary D.5.

Let . Suppose that for a sufficiently small constant , and suppose that for a sufficiently large constant . Then with probability at least , there is a set with such that for every subset with , the following hold:

-

•

-

•

for all unit vectors and all

-

•

for all unit vectors

-

•

-

•

is constant in .

Proof.

Let be the sets guaranteed by Lemma D.1 (with parameter ), Lemma D.2 (with parameter ), Lemma D.3 (with parameter ), and D.4 (with parameter ), which satisfy the claims of the respective lemmas with probability at least . Let . We have that , so is a subset of each of of size at least . Let have . By Lemma D.1 and since , it holds that . By Lemma D.2 and since , it holds that . By Lemma D.3 we have , and by Lemma D.4 we have . Finally, is clearly constant in . ∎

The above corollary validates Assumption 3.1 for linear instrumental variables. Since is constant in , the Assumption holds for any bound on the norm of the true solution . Formally, we can instantiate Theorem 5.5 to get a provably robust estimator for instrumental variables linear regression, as stated in Theorem 6.2.

Remark 1.

Although Theorem 6.2 is stated with a constant probability of failure, this is only for simplicity of presentation; in fact, the probabilities of failure all decay exponentially with , once exceeds the sample complexity stated in the theorem.

Appendix E Proof of Theorem 6.3

Let be independent samples drawn according to . Let . We prove that under the above assumptions, if is sufficiently large, then with high probability, for any -contamination of , the functions satisfy Assumption 3.1. The proof is similar to the previous section, with slight complications introduced by the non-linearity of the non-linear function .

Lemma E.1.

Let . Suppose that for an appropriate constant . Then with probability at least , there is a set with such that for every with , it holds that

Proof.

Let be the set guaranteed by Lemma D.2 with parameter , and let be the set guaranteed by applying Corollary F.4 to with parameter . Take , so that . Let with . By Cauchy-Schwarz, we have that

First, by the guarantee of Lemma D.2, we have

Second, by the guarantee of Corollary F.4 and Lipschitzness of , we have

Together,

as claimed. ∎

Lemma E.2.

Let and suppose that for an appropriate constant . Then with probability , there is a set with such that

for all and unit vectors .

Proof.

Let be the set guaranteed by Lemma D.2. Simply note that since is -Lipschitz,

for all unit vectors . ∎

Lemma E.3.

Let . Suppose that for an appropriate constant . There is a set with such that for every with , it holds that

Proof.

Lemma E.4.

Let and suppose that . Then with probability , there is a set with such that

for all unit vectors .

Proof.

By assumption, . So we can apply Corollary F.4 to conclude. ∎

Lemma E.5.

Let , and suppose that . With probability , there is a subset with such that for every with , it holds that

Proof.

Observe that and by assumption. The claim follows from Lemma F.5. ∎

As a result of the above lemmas, we get the following corollary, just as in the previous section.

Corollary E.6.

Let . Suppose that for a sufficiently small constant , and suppose that for a sufficiently large constant . Suppose that . Then with probability at least , there is a set with such that for every subset with , the following hold:

-

•

-

•

for all unit vectors and all

-

•

for all unit vectors

-

•

-

•

for all

Appendix F Technical lemmas

In this section we collect technical lemmas that are needed for our proof. Most of these results are standard in the robust statistics literature (see, e.g., [16]).

The following fact is key to the filtering algorithm and various other bounds.

Lemma F.1.

Let be distributions on . Let and suppose that and . Then if and , it holds that

where .

Proof.

Since there is some coupling under which . As a result,

Thus we have that:

Let be a unit vector. Bounding the means of and by second moments around , we have that

By law of total probability,

Similarly,

As a result, we get that:

We conclude that

Re-arranging we get the desired inequality. ∎

The above lemma implies that if an adversary is allowed to corrupt an -fraction of data, and the original distribution has variance no more than in any direction, then the corrupted mean must be within of the original mean, unless the corrupted distribution has significantly larger variance.

Lemma F.2.

Let . Suppose that are independent and identically distributed with . Suppose that . Then with probability there is a subset with such that

and as a consequence

Proof.

Since , we have that . Define . By a Chernoff bound, we have with probability . Fix a unit vector and define

for . We have that , and also are independent and uniformly bounded by . Thus, Hoeffding’s inequality implies that

Define

For any fixed unit vector we’ve shown that with probability . Let be a net of the unit ball in with resolution and cardinality at most . By a union bound, it holds that for all with probability . But now

for any vectors . Define

Then

Taking , we get that . So long as for a large enough constant , it holds with probablity at least that

and moreover . By the latter inequality it also follows that

as claimed. ∎

Lemma F.3.

Let . Suppose that are independent and identically distributed with . Suppose that for all . Suppose that for an appropriate absolute constant . Then with probability , there is a subset with such that for any with it holds that

Proof.

Let be the subset guaranteed by Lemma F.2, with the properties that and .

Fix a unit vector . Let be such that . Define . By a Chernoff bound, it holds with probability that . Thus the size of the set is at most . As a result, any with , must either contain all elements from the set or elements from its complement, whose values dominate the value of any element in . More formally: note that . Since every element in has value larger than any element in , we thus have: . Thus, it holds that

Next, note that is bounded by . Since

we have that . Therefore by Bernstein’s inequality, with probability

we have that

But now

Thus, with probability , for all with , we have that

Assume moreover that . Define . Then for any vectors , we have by Cauchy-Schwarz that

Since we have that . So

Fix a net on the unit sphere in , with resolution and cardinality . Then with probability the lower bound holds for all in the net and all of size . As a result, for any unit vector and any such , it holds that

We conclude that

So long as for a sufficiently large constant , this holds with probability at least as claimed. ∎

Corollary F.4.

Let be sufficiently small. Suppose that are independent and identically distributed -dimensional random vectors, with positive-definite covariance . Suppose that for all . Suppose that for a large constant . Then with probability there is a subset with such that for every subset with , it holds that

Proof.

Lemma F.5.

Let . Let be i.i.d. -dimensional random vectors with and . If for a sufficiently large constant , then with probability at least , there is a subset with such that for every with , it holds that .

Proof.

Since , we have that . Define . By a Chernoff bound, we have with probability . Now

and the random variables are independent and bounded in operator norm by . Thus, we can apply the Matrix Chernoff bound [19] to get

| (2) |

so long as for a sufficiently large constant . Moreover, for any unit vector ,

Since is bounded in norm by , a Bernstein bound implies that for any unit vector ,

Take a net over unit vectors in of granularity and cardinality . Then the above inequality holds for all in the net, with probability , which is at least if for an appropriate constant .

Let denote the aforementioned net of the unit ball in . We have that in the aforementioned event:

Re-arranging yields:

Lemma F.6.

Let . Let be independent and identically distributed -dimensional random vectors with for all and coordinate-wise bounded -th moments, i.e. . Suppose that for a sufficiently large constant . With probability at least , there is a set with such that

for all and an absolute constant .

Proof.

Since (since for any unit vector ), we have that

By a Chernoff bound, we have that with probability at least . Now fix a unit vector and define

for . We have that

and also are independent and uniformly bounded by . Thus, the Bernstein bound implies that

for some universal constant . Note that:

Thus:

Take . For any fixed unit vector , it holds that with probability . Take . We can union bound over a -net of the unit ball in , which has cardinality at most , and note that

so in fact it holds that

for all unit vectors , with probability

since for a sufficiently large constant . Finally, it also holds that with probability . It therefore holds with probability at least that for all unit vectors ,

as claimed. ∎