The Limits of Optimal Pricing in the Dark††thanks: This work is supported by a Google Faculty Research Award and an NSF grant CCF-2132506.

Abstract

A ubiquitous learning problem in today’s digital market is, during repeated interactions between a seller and a buyer, how a seller can gradually learn optimal pricing decisions based on the buyer’s past purchase responses. A fundamental challenge of learning in such a strategic setup is that the buyer will naturally have incentives to manipulate his responses in order to induce more favorable learning outcomes for him. To understand the limits of the seller’s learning when facing such a strategic and possibly manipulative buyer, we study a natural yet powerful buyer manipulation strategy. That is, before the pricing game starts, the buyer simply commits to “imitate” a different value function by pretending to always react optimally according to this imitative value function.

We fully characterize the optimal imitative value function that the buyer should imitate as well as the resultant seller revenue and buyer surplus under this optimal buyer manipulation. Our characterizations reveal many useful insights about what happens at equilibrium. For example, a seller with concave production cost will obtain essentially revenue at equilibrium whereas the revenue for a seller with convex production cost is the Bregman divergence of her cost function between no production and certain production. Finally, and importantly, we show that a more powerful class of pricing schemes does not necessarily increase, in fact, may be harmful to, the seller’s revenue. Our results not only lead to an effective prescriptive way for buyers to manipulate learning algorithms but also shed lights on the limits of what a seller can really achieve when pricing in the dark.

1 Introduction

Pricing is a basic question in microeconomics [24] as well as a ubiquitous problem in today’s digital markets [16]. In its textbook style setup, there are two agents: a buyer (he) and a seller (she). The seller produces types of divisible goods for sale and has production cost for producing bundle of the goods. Using a standard linear pricing scheme with unit price for goods , the seller charges the buyer when he purchases bundle under price vector . Naturally, the buyer’s optimal bundle for purchase depends on his value function about the products. We assume that, given price vector , the rational buyer will always pick the optimal bundle that maximizes his quasilinear utility . The key question of interest is how the seller can compute the revenue-maximizing optimal prices assuming rational buyer purchase behaviors.

The above basic problem can be easily solved if the seller has access to the buyer’s value function . However, in practice, this value function is usually private and unknown to the seller. To address this challenge, there has been a rich line of recent research which looks to design the optimal pricing scheme against an unknown buyer. Some of these work have adopted learning-based approaches that aim to compute the profit maximizing price by interacting with the buyer and gleaning information about the buyer’s utility function [3; 33; 32]. These are motivated by the wide spread of e-commerce today where the seller can repeatedly interact with the same buyer or buyers from the same population with similar preferences. For example, in online advertising, ad exchange platforms learn to price advertisers from past behaviors; in online retailing, retailers learn to price customers from their past purchase history; and in crowdsourcing, platforms learn to reward workers’ efforts. Another line of works look to design dynamic pricing mechanisms that dynamically adjusts the price based on the observed past buyer purchase behaviors with the objective of maximizing the aggregated total revenue [4; 5; 26; 27; 38].

A key challenge of pricing against such unknown buyers, regardless through learning or dynamic pricing, is that the buyer may manipulate his responses in order to mislead the seller’s algorithm and induce more favorable outcomes for themselves. This is a fundamental issue when learning from strategic data sources, and is particularly relevant in this pricing setup due to the strategic nature of the problem. In this case, the buyer controls the information content to the seller, therefore he naturally has incentives to utilize this advantage to gain more payoff by strategically misleading the seller’s algorithms. Indeed, as observed in previous studies, online advertisers may strategically respond to an ad exchange platform’s prices in order to induce a lower future price [22]; Consumers strategically time their purchases in order to obtain lower prices at online retailing platforms [23].

To understand the limits of the seller’s optimal pricing against such a strategic and possibly manipulative buyer, we put forward a natural model which augments the above basic pricing problem with only one additional step — i.e., we assume that the game starts with the buyer committing to a different value functions, coined the imitative value function, after which the seller will compute the optimal pricing scheme against this imitative buyer value function. The buyer’s commitment to an imitative value function captures a simple yet powerful buyer manipulation strategy that can be used against any seller learning algorithms — that is, the buyer simply behaves consistently according to this imitative value function during the entire interaction process. Intuitively, the motivation of such commitment assumption comes directly from the fact that the seller has no information about the buyer and has to optimize pricing “in the dark”. Consequently, if the buyer consistently behaves according to some different imitative value function, the seller is not able to distinguish this buyer from another buyer who truly has the value function (see more justifications of the commitment assumption in Section 3). Moreover, such an imitation strategy is also easy to execute in practice by the buyer regardless whether the seller is learning from him or is adopting dynamic pricing schemes. In fact, the buyer could even just report his imitative value function to the buyer directly at the beginning of any interaction. In this situation, no learning or dynamic pricing will be needed as the buyer will indeed always behave according to the imitative value function. Therefore, all the seller can do is to directly apply the optimal pricing scheme for the buyer’s imitative value function.

We remark that such imitation-based manipulation strategy has attracted much interest in recent works, with similar motivations as us — i.e., trying to understand how to manipulate learning algorithm or conversely, how to design strategy-aware learning algorithms to mitigate such manipulation. However, most of these works have focused on the general Stackelberg game model [19; 10] as well as the Stackelberg security games [18; 30; 29]. Our optimal pricing problem is also a Stackelberg model and thus a natural fit for the study. The crucial difference between our work and previous studies is that both agents in our model have continuous utility functions whereas all these previous works [19; 18; 30; 10] have discrete agent utility functions. Therefore, our model leads to a functional analysis and optimization problem, which is more involved. Fortunately, we show that the optimal functional solution can still be characterized by leveraging the structure of the pricing problem.

1.1 Our Results and Implications

Given the effectiveness and easy applicability of the buyer’s imitative strategy described above, this paper studies what the optimal buyer imitative value function is and how it would affect buyer’s surplus and the seller’s revenue. Our main result provides a full characterization about the optimal buyer imitative value function. We show that the optimal buyer imitative value function features a specific bundle of products that is most desirable to the buyer. Interestingly, it turns out that is a Leontief-type piece-wise linear concave value function [2] such that the buyer would only proportionally value a fraction of the desired bundle and nothing else. Moreover, we also characterize the seller revenue and buyer surplus at equilibrium as well as necessary and sufficient conditions under which the seller obtains strictly positive revenue.

The optimal buyer imitative value function turns out to depend crucially on the seller’s production cost function. When the cost function is concave, we show that the optimal buyer imitative value function will “squeeze” the seller revenue essentially to . The fortunate news for the seller, however, is that finding out the turns out to be an NP-hard task for the buyer. In fact, we prove that it is NP-hard to find the that can guarantee a polynomial faction of the optimal buyer surplus. For the widely adopted convex production cost, we show that the equilibrium seller revenue is the Bregman divergence between production and the bundle mentioned above. This illustrates an interesting message that convex production costs are “better” at handling buyer’s strategic manipulations. Note that production costs are indeed more often believed to be convex since economic models typically assume that marginal costs increase as quantity goes up [35; 34].

All our characterizations so far focus on the standard linear pricing scheme. Our last result examines the possibility of using a more general class of pricing schemes to address the buyer’s strategic manipulation. Surprisingly, we show that for the strictly more general class of concave pricing functions (i.e., the seller is allowed to use any concave function as a pricing function), the equilibrium will remain the same as described above. Therefore, the more general pricing schemes do not necessarily help to address buyer’s manipulation behavior. In fact, we show that there exist examples where strictly broader class of pricing functions leads to strictly worse seller revenue. This is because more general pricing schemes may “overfit” buyer’s incentives, which renders it easier to manipulate. This illustrates an interesting phenomenon in learning from strategic data sources and shares similar spirit to overfitting in standard machine learning tasks.

1.2 Additional Related Works

Due to space limit, here we only briefly discuss the most related works while refer readers to Appendix A.1 for more detailed discussions and comparisons. Closely related to ours is a recent study by Tang and Zeng [36]. They study the bidders’ problem of committing to “imitate” a fake value distribution in auctions and acting consistently as if the bidder’s value were from the fake distribution. This is similar in spirit to our buyer’s commitment to an imitative value function. However, there is significant difference betweens our setting and that of [36], which leads to very different conclusions as well. Specifically, the seller in [36] auctions a single indivisible item with no production costs whereas our seller sells multiple divisible items with production costs. Another recent work [28] also studies buyer’s strategic manipulation against seller’s pricing algorithms, but in a single-item multi-buyer situation. Moreover, they assume a fixed seller learning strategy (thus not adaptive to buyer’s strategy) with separated exploration-exploitation phases motivated by [4]. Another very relevant literature is learning the optimal prices or optimizing aggregated total revenue by repeatedly interacting with a single buyer [4; 5; 26; 27; 38]. These works all focus on designing learning algorithms that can learn from strategically buyer responses. Our work complements this literature by studying the limits of what learning algorithms can achieve. Moreover, the setups of these previous works are also different from us – they either assume buyer values are drawn from distributions [4; 5; 27] or the seller sells a single indivisible good with discrete agent utilities. Thus, their results are not comparable to us.

There have also been studies on learning the optimal prices from truthful revealed preferences, i.e., assuming the buyer will honestly best respond to seller prices [8; 39; 6; 42; 3; 33; 32]. Our works try to understand if the assumption of truthful revealed preferences does not hold and if the buyer will strategically respond to the seller’s learning, what learning outcome could be expected when the buyer simply imitates a different value function that is optimally chosen. From this perspective, these works serve as a key motivation for the present paper. More generally, our work subscribes to the general line of research on learning from strategic data sources. Most works in this space has focused on classification [11; 20; 43; 17; 25; 21; 12], regression problems [31; 15; 13] and distinguishing distributions [40; 41]. Our work however focuses on learning the optimal pricing scheme.

2 Preliminaries

Basic Setup of the Optimal Pricing Problem.

A seller (she) would like to sell different types of divisible goods to a buyer (he). It costs her to produce bundle of these goods. Let denote the set of all feasible bundles that the seller can produce. We assume is convex, closed and has positive measure. As a standard assumption [24; 33; 8; 6; 39], the buyer has a concave value function for any goods bundle . We do not make any assumption about the seller’s production cost , except that it is monotone non-decreasing. For normalization, we assume and .

The seller aims to find a revenue-maximizing pricing scheme assuming rational buyer behaviors. A seller pricing scheme is a function that specifies the sale price for any bundle . By convention, always. Let the set denote the set of all pricing functions that are allowed to use by the buyer. The majority of this paper will focus on the textbook-style linear pricing scheme [24]. A linear pricing scheme is parameterized by a price vector (to be designed) such that where ’th entry is interpreted as the unit price for goods . Let set

denote the set of all linear pricing functions. In Section 6 we will also study the broader classes of concave pricing schemes where the set consists of all monotone non-decreasing concave functions.

For any price function , a rational buyer looks to purchase bundle that maximizes his utility; That is, . Ties are broken in favor of the seller.111This is usually without loss of generality since the seller can always induce desirable tie breaking by providing a negligible additional incentive to the buyer. The buyer’s best response can thus be viewed as a function of the seller’s price function . Knowing that the buyer will best respond, the seller would like to pick the pricing function to maximize her revenue. Formally, is the solution to the following bi-level optimization:

| (1) |

The optimal solution to such a bi-level optimization problem forms an equilibrium of this pricing game. More formally, this is often called the optimal Stackelberg equilibrium or strong Stackelberg equilibrium [14; 33]. We call the equilibrium pricing function and the equilibrium bundle. Note that this is a challenging functional optimization problem since the seller is picking a function , while not a vector variable. However, when is the set of linear pricing scheme, the above problem becomes a bi-level variable optimization problem since any can be fully characterized by a price vector .

Terminologies from Convex Analysis. We defer basic definitions like convex/concave functions and super/sub-gradients to Appendix B, and only mention two useful notations here: (1) the set of super/sub-gradient for concave/convex function is denoted as ; (2) The Bregman divergence of a function is defined as . is an important distance notion and is strictly positive for strictly convex functions when .

3 A Model of Pricing Against a Deceptive Buyer in the Dark ()

As mentioned in related work section 1.2, the literature of algorithms to learn pricing schemes from unknown buyers is massive. This work, however, takes a different perspective and seeks to understand how a buyer can strategically deceive the seller, through a simple yet effective class of manipulation strategies. Our model naturally captures a buyer’s strategic responses to seller’s pricing algorithms when the seller has no prior knowledge about the buyer, i.e., pricing “in the dark”.

Thus, we study a buyer manipulation strategy that is oblivious to any pricing algorithm. That is, the buyer simply imitates a different value function by consistently responding to any seller acts according to . Consequently, whatever the seller learns will be with respect to this imitative value function . Alternatively, one can think of the buyer as committing to always behave according to value function . Nevertheless, the buyer’s objective is still to maximize his true utility by carefully crafting an imitative value function to commit to. Given the buye’s commitment to value function , the best pricing scheme for the seller is to use the optimal pricing function against buyer value function . Similar to , the imitative value functions is assumed to be concave and monotone non-decreasing as well. Let set denote the set of all such functions. These resulted in the following model of Pricing Against a Deceptive buyer in the Dark ():

-

•

The buyer with true value function (unknown to seller) commits to react optimally according to an imitative value function .

-

•

The seller learns the buyer’s imitative value function and compute the optimal pricing function by solving bi-level Optimization Problem (1) w.r.t. .

-

•

The buyer observes the seller’s pricing function , and then follows his commitment to react optimally w.r.t. to by purchasing bundle .

We remark that such commitment to a fake value function is not uncommon in the literature; similar assumptions have been adopted in many recent works in, e.g., auctions [36], general Stackelberg games [19; 10] and security games [18; 30; 29]. The buyer’s ability of making such a commitment fundamentally comes from the fact that the seller has no prior knowledge about the buyer’s true value function , i.e., has to “price in the dark”. We refer curious reader to Appendix A.2 for a more detailed discussion about this assumption.

Naturally, the buyer with true value function would like to find the optimal imitative value function to maximizes his utility. This results in the following equilibrium definition.

Definition 1 (Equilibrium of ).

The equilibrium of consists of the optimal imitative value function that the buyer commits to, the seller’s optimal pricing function against , and the buyer’s response bundle . Formally, is an equilibrium for a buyer with true value function to if

| where | (2) |

The equilibrium of gives rise to a challenging tri-level functional optimization problem.222Even for linear pricing where , this is still a functional optimization problem since the buyer’s imitative value function is an arbitrary function in . Note that, the dependence of the buyer’s objective on is indirectly through the two argmax problems afterwards. The buyer is assumed to know the production cost function , which is needed to compute his optimal . This can be easily justified in situations where the seller has been on the market for some time, therefore her production cost gradually becomes public knowledge.

4 The Equilibrium of under Linear Pricing, and Implications

In this section, we characterize the equilibrium of under linear pricing schemes, i.e., consists of all linear pricing functions. A linear pricing function is determined by a non-negative price vector . To distinguish functionals from vector variables, we will use to denote the set of all possible non-negative price vectors so that each uniquely corresponds to a linear pricing function in . Under linear pricing, the equilibrium in Def. 1 denoted by is characterized by Eq. (2) where .

Even with linear pricing, this is still a very challenging tri-level functional optimization problem since is a function chosen from the set of all possible functions from to , denoted by set . A first thought one might have is: why doesn’t the buyer simply imitate . We will see later that this is not — in fact far from being — optimal since it makes the game zero-sum and the seller will pick a price that guarantee 0 revenue, e.g., a price of . This leads the trade to happen at 0 production, which is clearly not optimal for the buyer. The optimal should provide some incentive for the seller to produce some amount that is in some sense the best for the buyer. We will provide two concrete examples in the next section in Figure 2.

The main result of this section is the following characterization for the equilibrium of . This general characterization does not depend on any specific property about function .

Theorem 1.

In the equilibrium of under linear pricing, the optimal buyer imitative value function can w.l.o.g. be written as the following concave function parameterized by production amount and a real value :

| (3) |

where

| (4) |

Moreover, under imitative value function ,

-

1.

For any vector in the -dimensional simplex, the linear pricing scheme with price vector is optimal for .

-

2.

In any of the above optimal linear pricing schemes, the buyer’s optimal bundle response is always and the buyer payment will always equal .

-

3.

At equilibrium, the buyer surplus is and the seller revenue is .

Note that the described by Equation (3) may not be the unique optimal buyer imitative value function, but it is one of the optimal ones. Moreover, any optimal imitative value function will result in the same buyer surplus and seller revenue.

Interpretation of Theorem 1. Before a formal proof, it is worthwhile to take a closer look at the characterization of the buyer’s optimal imitative value function characterized by Theorem 1 and the special pricing problem it ultimately induces. At a high level, the buyer has a desirable amount of products in mind, characterized by the first equation in (4). He would pretend that his value for equals . Moreover, the value of any production amount will linearly depend on the maximum possible coordinate-wise fraction of that contains, i.e., the term in .333Notably, the format of this value function appears to have interesting connections to the well-known Leontief production function [2] which has the format of . However, leontief functions are used to describe seller’s production quantities as a function of quantities of different factors with no substitutability. It is an expected surprise that similar type of value function turns out to be optimal for buyer’s strategic manipulation.

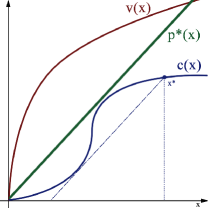

The is chosen as the largest possible slope of the segment between to among all possible (see Figure 1 for an illustration in one dimension about how is chosen based on the cost function ). This is certainly a very carefully chosen value. Note that

which implies non-negativity of the seller’s revenue . In fact, the seller can achieve strictly positive revenue if and only if the above is strict. Finally, the optimal buyer imitative value function leads to a special pricing problem for the seller. Since the buyer’s value is designed such that he is only interested in purchasing some fraction of , the seller’s optimal pricing will charge for the bundle and this total charge can be distributed arbitrarily over the products, e.g., by charging for product where . Overall, Theorem 1 fully characterized what the pricing problem is like at the equilibrium of .

Remark 1.

Theorem 1 only provides a structural characterization about the equilibrium but does not imply that the equilibrium can be computed efficiently since we still need to solve the optimization problem (4) to find the optimal . As we will show later, this turns out actually to be an NP-hard problem in general. This is an interesting situation where the result reveals useful structural insights despite its computational intractability.

Proof Sketch of Theorem 1..

The proof of Theorem 1 is somewhat involved. We give a sketch here and defer formal arguments to Appendix C. The most challenging part is to find the optimal function , which is a functional optimization problem. Standard optimization analysis only apply to programs with vector variables, while not functional variables. To overcome this challenge, our proof has two major steps. First, we argue that the concave functions of the specific format as in Equation (3) would suffice to help the buyer to achieve optimality. This effectively reduce the functional optimization problem to a variable optimization problem since any function of Format (3) can be characterized by variables. Second, we then analyze the variable optimization problem we get and prove characterization of its optimal solutions. The first step is the most involved part and uses a significant amount of convex analysis. Such complication comes from the reasoning over the tri-level optimization problem (2). Tri-level optimization is generally highly intractable [9] — indeed, as we will show later, computing the equilibrium is NP-hard in general. Nevertheless, our analysis was able to bypass the difficulty by leveraging the special structure of the pricing problem and leads to a clean and useful characterization for the structure of the equilibrium.

A crucial intermediate step is the following characterization for a slightly simpler version of the question. That is, fixing any bundle , which imitative value function will maximize the utility of the buyer with true value function , subject to that the optimal buyer purchase response under is ? Fortunately, this question indeed admits a succinct characterization as shown below.

Lemma 1.

For any bundle , the optimal buyer imitative value function , subject to that the resultant optimal buyer purchase response is bundle , can without loss of generality have the following piece-wise linear concave function format, parameterized by a real number :

| (5) |

where is the solution to the following linear program (LP):

∎

5 Explicit Characterizations for Convex and Concave Costs

In this section, we instantiate Theorem 1 to both convex and concave cost functions, arguably the most widely adopted two classes of cost functions. In both cases, we give more explicit characterizations of the equilibrium outcome, including the buyer’s optimal imitative value function as well as both agents’ payoffs.

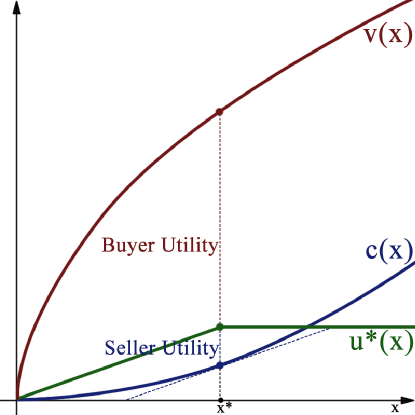

Convex production costs are widely adopted in many applications [7; 37]. When is convex and differentiable, we show the following explicit characterization about the equilibrium outcome. A graphical visualization for this theorem is depicted in the left panel of Figure 2.

Theorem 2.

When is convex and differentiable, the piece-wise linear concave value function defined by Equation (3), with and , is an optimal buyer imitative value function.

Under , the trade happens at bundle with payment . The seller revenue is precisely the Bregman divergence between and . The buyer surplus is .

and buyer utility .

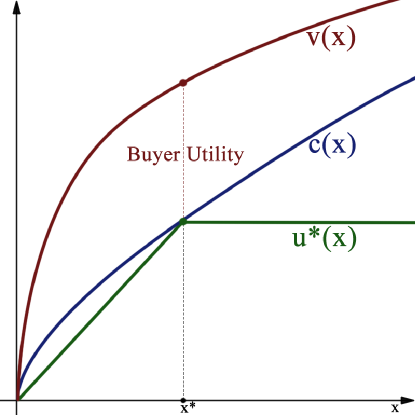

We now consider concave costs and prove the following characterization. A graphical visualization for the theorem is depicted in the right panel of Figure 2.

Theorem 3.

When is concave, the piece-wise linear concave value function defined by Equation (3), with and , is an optimal buyer imitative value function.

Under , the trade happens at bundle with payment . The seller revenue will be . The buyer extracts the maximum possible surplus .

Graphical visualizations for the above two theorems are depicted in Figure 2. Note that both examples in Figure 2 show the sub-optimality of imitating for the buyer. To see this, note makes the game zero-sum. To guarantee non-negative revenue, the seller must pick a price such that the line is always above . A buyer imitating will end up purchasing a amount in both cases, and thus are sub-optimal for him.

An important conceptual message from Theorem 3 is that when the seller production cost is concave and known to the buyer, the buyer can always come up with an imitative value function which squeeze the seller’s revenue to its extreme, i.e., .444In real practice, the buyer can slightly deviate from his value function to given a small amount of incentive for the seller to strictly prefer production. Under the seller’s optimal imitative value function, the trade will happen at his most favorable bundle amount and the seller pays just the cost function to the seller.

Theorem 3 is certainly bad news for the seller. However, it is a descriptive result and only shows it is possible for the buyer to achieve maximum possible surplus. Our next result brings somewhat good news to the seller. Specifically, we show it is NP-hard for the buyer to optimize, even approximately, his optimal surplus. The hardness holds even when the production cost function is concave, in which case the surplus is characterized by Theorem 3. This shows that even though in theory the buyer can derive large surplus from strategic manipulation, even approximately figuring out such an optimal manipulation is impossible in general, unless P = NP.

Theorem 4.

[Intractability of Equilibrium] It is NP-hard to approximate the buyer equilibrium surplus in games to be within ratio for any . This hardness result holds even when the production cost function is concave and the buyer’s true value function is simply the linear function .

Formal proofs for both equilibrium characterizations and the hardness of approximating the buyer equilibrium surplus can be found in Appendix D. We note that an intriguing open question is whether optimal imitative value function can be computed for convex production cost . In this case, the optimal bundle can be explicitly expressed as for any value function , however how to derive the optimal remains challenging.

6 The Risk of Over-exploiting Buyer’s Incentives

To counteract the buyer’s strategic manipulation, one of the most natural approaches is perhaps to use a richer or more powerful class of pricing schemes, as opposed to only using linear pricing. Such additional power of pricing will always increase the revenue when facing an honest buyer. Unfortunately, however, we show that it does not necessarily help in the presence of buyer manipulation — in fact, the seller may suffer the risk of over-exploiting the buyer’s incentives so that it becomes easier for the buyer to manipulate. This phenomenon is similar in spirit to the overfitting phenomenon in machine learning. That is, using a richer hypothesis class does not necessarily reduce the testing error, though it does reduce the training error. We believe that our findings in this section partially explain why simple pricing schemes like linear pricing are preferred in reality.

We first prove that the strictly more general class of concave pricing schemes can never do better for the seller than the (much) restricted class of linear pricing. In fact, surprisingly, the equilibrium of under concave pricing turns out to be exactly the same as the equilibrium under linear pricing. This time, our proof utilizes a crucial observation that under concave pricing, the tri-level optimization problem of can be reduced to solving a bi-level optimization problem (in particular, FOP (6)). Recall that the proof of Theorem 1 also reduces the tri-level FOP to a bi-level FOP through a characterization about the price and optimal buyer bundle in Lemma 3. However, Lemma 3 does not hold any more if the seller uses the richer class of concave pricing schemes. Therefore, the FOP (6) we obtain here is different from the core FOP (11) we solve in the proof of Theorem 1. Nevertheless, through careful convex analysis, we are able to show that the optimal solution to FOP (6) also admits an optimal solution of similar structure as characterized by Theorem 1.

Theorem 5.

The equilibrium of under concave pricing is exactly the same as the equilibrium under linear pricing as characterized by Theorem 1.

Proof Sketch of Theorem 5..

We start by examining how the use of concave pricing schemes may simplify FOP (2). Recall that both value functions and pricing functions are monotone non-decreasing and normalized to be at . For any concave buyer value function , it is easy to see that the optimal pricing function simply equals (i.e., charging buyer exactly his imitative value) and ask the buyer to break ties in favor of the seller by picking to maximize the seller’s revenue. Consequently, the use of concave pricing simplifies FOP 2 to the following bi-level functional optimization problem:

We fix a particular bundle and examine what buyer value function would maximize the buyer’s utility subject to that the trade will happen at bundle . This results in the following functional optimization problem (FOP) for the buyer with functional variable .

| (6) |

where the constraint means the seller’s optimal price for value function is and thus the buyer best response amount is indeed . The remaining proof relies primarily on the following lemma.

Lemma 2.

The following concave function is optimal to FOP (6):

| (7) |

Theorem 5 shows that more general class of pricing schemes may not help the seller to obtain more revenue. One might then wonder whether it at least never hurts since if that is the case, at least it would never be a worse choice. Unfortunately, our following example shows that a richer class of pricing schemes may bring strict harm to the seller and strict benefit to the seller.

Example 1 ( The Risk of Overexploiting Buyer Incentives).

There is a single type of divisible good to sell, i.e., . Let the seller’s production cost function be the convex function and let the buyer’s true value function be the following piece-wise linear concave function

Let denote the set of all concave pricing schemes. The following proposition completes Example 1 and its proof can be found in Appendix E.2.

Proposition 1.

For the instance in Example 1, there exists pricing scheme class with such that when the seller changes from linear pricing class to the richer class , the seller’s revenue strictly decreases and the buyer’s surplus strictly increases at the equilibrium of .

7 Conclusions

Motivated by optimal pricing against an unknown buyer, this paper put forwards a simple variant of the very basic pricing model by augmenting it with an additional stage of buyer commitment at the beginning. This motivation is driven by the seller’s ignorance of the buyer’s value function and thus have to price in the dark. We fully characterize the equilibrium of this new game model. The equilibrium reveals interesting insights about what the seller can learn, and how much seller revenue and buyer surplus it may result in. We also show that more general class of pricing schemes may overfit the buyer’s incentive and lead to a pricing game that is even easier for the buyer to manipulate.

Our results opens the possibilities for many other interesting questions. For example, given the risk of using a too general class of pricing schemes, what class of pricing schemes is a good compromise between extracting revenue and robust to buyer manipulations? Is linear pricing scheme the best such class or any other pricing scheme? Second, as the first study of our setup, we have chosen to focus on a simple setup where the seller has completely no knowledge about the buyer’s value function. An interesting question is, how the seller’s learning and resultant revenue may increase when the seller has some prior knowledge about the buyer’s values. In fact, one natural modeling question is how to model the seller’s prior knowledge about the buyer’s value function. Is the prior knowledge about which subclass the value functions are from or about what distribution the parameters of the value functions are from? Finally, our model assumes that the buyer has full knowledge about the seller. An ambitious though extremely intriguing question to ask is what if the buyer also has incomplete knowledge about the seller and how to analyze the equilibrium under the information asymmetry from both sides.

References

- [1] E. Akyol, C. Langbort, and T. Basar. Price of transparency in strategic machine learning. arXiv, pages arXiv–1610, 2016.

- [2] R. Allen. Macro-economic theory: a mathematical treatment. 1967.

- [3] K. Amin, R. Cummings, L. Dworkin, M. Kearns, and A. Roth. Online learning and profit maximization from revealed preferences. In Twenty-Ninth AAAI Conference on Artificial Intelligence, 2015.

- [4] K. Amin, A. Rostamizadeh, and U. Syed. Learning prices for repeated auctions with strategic buyers. In Advances in Neural Information Processing Systems, pages 1169–1177, 2013.

- [5] K. Amin, A. Rostamizadeh, and U. Syed. Repeated contextual auctions with strategic buyers. In Advances in Neural Information Processing Systems, pages 622–630, 2014.

- [6] M.-F. Balcan, A. Daniely, R. Mehta, R. Urner, and V. V. Vazirani. Learning economic parameters from revealed preferences. In International Conference on Web and Internet Economics, pages 338–353. Springer, 2014.

- [7] P. Beato and A. Mas-Colell. On marginal cost pricing with given tax-subsidy rules. Journal of Economic Theory, 37(2):356–365, 1985.

- [8] E. Beigman and R. Vohra. Learning from revealed preference. In Proceedings of the 7th ACM Conference on Electronic Commerce, pages 36–42, 2006.

- [9] O. Ben-Ayed and C. E. Blair. Computational difficulties of bilevel linear programming. Operations Research, 38(3):556–560, 1990.

- [10] G. Birmpas, J. Gan, A. Hollender, F. Marmolejo, N. Rajgopal, and A. Voudouris. Optimally deceiving a learning leader in stackelberg games. Advances in Neural Information Processing Systems, 33, 2020.

- [11] M. Brückner and T. Scheffer. Stackelberg games for adversarial prediction problems. In Proceedings of the 17th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 547–555, 2011.

- [12] Y. Chen, Y. Liu, and C. Podimata. Learning strategy-aware linear classifiers. Advances in Neural Information Processing Systems, 33, 2020.

- [13] Y. Chen, C. Podimata, A. D. Procaccia, and N. Shah. Strategyproof linear regression in high dimensions. In Proceedings of the 2018 ACM Conference on Economics and Computation, EC ’18, page 9–26, New York, NY, USA, 2018. Association for Computing Machinery.

- [14] V. Conitzer and T. Sandholm. Computing the optimal strategy to commit to. In Proceedings of the 7th ACM conference on Electronic commerce, pages 82–90, 2006.

- [15] O. Dekel, F. Fischer, and A. D. Procaccia. Incentive compatible regression learning. Journal of Computer and System Sciences, 76(8):759–777, 2010.

- [16] A. V. den Boer. Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science, 20(1):1–18, 2015.

- [17] J. Dong, A. Roth, Z. Schutzman, B. Waggoner, and Z. S. Wu. Strategic classification from revealed preferences. In Proceedings of the 2018 ACM Conference on Economics and Computation, EC ’18, page 55–70, New York, NY, USA, 2018. Association for Computing Machinery.

- [18] J. Gan, Q. Guo, L. Tran-Thanh, B. An, and M. Wooldridge. Manipulating a learning defender and ways to counteract. In Advances in Neural Information Processing Systems, pages 8272–8281, 2019.

- [19] J. Gan, H. Xu, Q. Guo, L. Tran-Thanh, Z. Rabinovich, and M. Wooldridge. Imitative follower deception in stackelberg games. In Proceedings of the 2019 ACM Conference on Economics and Computation, pages 639–657, 2019.

- [20] M. Hardt, N. Megiddo, C. Papadimitriou, and M. Wootters. Strategic classification. In Proceedings of the 2016 ACM Conference on Innovations in Theoretical Computer Science, ITCS ’16, page 111–122, New York, NY, USA, 2016. Association for Computing Machinery.

- [21] L. Hu, N. Immorlica, and J. W. Vaughan. The disparate effects of strategic manipulation. In Proceedings of the Conference on Fairness, Accountability, and Transparency, FAT* ’19, page 259–268, New York, NY, USA, 2019. Association for Computing Machinery.

- [22] N. Korula, V. Mirrokni, and H. Nazerzadeh. Optimizing display advertising markets: Challenges and directions. IEEE Internet Computing, 20(1):28–35, 2015.

- [23] J. Li, N. Granados, and S. Netessine. Are consumers strategic? structural estimation from the air-travel industry. Management Science, 60(9):2114–2137, 2014.

- [24] A. Mas-Colell, M. D. Whinston, J. R. Green, et al. Microeconomic theory, volume 1. Oxford university press New York, 1995.

- [25] S. Milli, J. Miller, A. D. Dragan, and M. Hardt. The social cost of strategic classification. In Proceedings of the Conference on Fairness, Accountability, and Transparency, FAT* ’19, page 230–239, New York, NY, USA, 2019. Association for Computing Machinery.

- [26] M. Mohri and A. Munoz. Optimal regret minimization in posted-price auctions with strategic buyers. In Advances in Neural Information Processing Systems, pages 1871–1879, 2014.

- [27] M. Mohri and A. Munoz. Revenue optimization against strategic buyers. In Advances in Neural Information Processing Systems, pages 2530–2538, 2015.

- [28] T. Nedelec, C. Calauzenes, V. Perchet, and N. El Karoui. Robust stackelberg buyers in repeated auctions. In International Conference on Artificial Intelligence and Statistics, pages 1342–1351. PMLR, 2020.

- [29] T. H. Nguyen, N. Vu, A. Yadav, and U. Nguyen. Decoding the imitation security game: Handling attacker imitative behavior deception. In 24th European Conference on Artificial Intelligence, ECAI 2020, including 10th Conference on Prestigious Applications of Artificial Intelligence, PAIS 2020, pages 179–186. IOS Press BV, 2020.

- [30] T. H. Nguyen and H. Xu. Imitative attacker deception in stackelberg security games. In Proceedings of the 28th International Joint Conference on Artificial Intelligence, pages 528–534. AAAI Press, 2019.

- [31] J. Perote and J. Perote-Peña. Strategy-proof estimators for simple regression. Math. Soc. Sci., 47:153–176, 2004.

- [32] A. Roth, A. Slivkins, J. Ullman, and Z. S. Wu. Multidimensional dynamic pricing for welfare maximization. ACM Transactions on Economics and Computation (TEAC), 8(1):1–35, 2020.

- [33] A. Roth, J. Ullman, and Z. S. Wu. Watch and learn: Optimizing from revealed preferences feedback. In Proceedings of the forty-eighth annual ACM symposium on Theory of Computing, pages 949–962, 2016.

- [34] P. Samuelson and W. Nordhaus. Microeconomics. Irwin/McGraw-Hill, 1998.

- [35] R. W. Shephard and R. Färe. The law of diminishing returns. Zeitschrift für Nationalökonomie, 34(1-2):69–90, 1974.

- [36] P. Tang and Y. Zeng. The price of prior dependence in auctions. In Proceedings of the 2018 ACM Conference on Economics and Computation, pages 485–502, 2018.

- [37] R. Turvey. Marginal cost. The Economic Journal, 79(314):282–299, 1969.

- [38] A. Vanunts and A. Drutsa. Optimal pricing in repeated posted-price auctions with different patience of the seller and the buyer. In Advances in Neural Information Processing Systems, pages 939–951, 2019.

- [39] M. Zadimoghaddam and A. Roth. Efficiently learning from revealed preference. In International Workshop on Internet and Network Economics, pages 114–127. Springer, 2012.

- [40] H. Zhang, Y. Cheng, and V. Conitzer. Distinguishing distributions when samples are strategically transformed. In Advances in Neural Information Processing Systems, pages 3193–3201, 2019.

- [41] H. Zhang, Y. Cheng, and V. Conitzer. When samples are strategically selected. In International Conference on Machine Learning, pages 7345–7353, 2019.

- [42] H. Zhang and V. Conitzer. Learning the valuations of a -demand agent. In H. D. III and A. Singh, editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 11066–11075. PMLR, 13–18 Jul 2020.

- [43] H. Zhang and V. Conitzer. Incentive-aware pac learning. AAAI 2021, 2021.

Appendix A Additional Discussions

A.1 Additional Discussions on Related Works

Our work is related to a recent study by Tang and Zeng [36] who study the bidders’ problem of committing to a fake type distribution in auctions and acting consistently as if the bidder’s type were from the fake type distribution. This is similar in spirit to our buyer’s commitment to an imitative value function. However, there are two key differences between our work and [36]. First, the seller in our model (realistically) has production cost where as the auction setting of [36] does not have production cost. This is an important difference because with production cost, the optimal manipulation in our case is trivial, i.e. the buyer will imitate a value function of 0. However, this trivial solution does not arise in the model of [36] because in their setup there are multiple buyers (bidders) and the competition among bidders increases the auctioneer’s revenue despite bidders’ imitative or faking behaviors. This is the second key difference between our work and [36]. Therefore, our work illustrates how the production cost can affect the buyer’s strategic manipulation and the seller’s revenue whereas the work of Tang and Zeng [36] sheds light on how the bidders’ competition affect the auctioneer’s mechanism design and ultimate revenue. Though these two aspects are not comparable, we believe they are both interesting for a deep understanding.

Another very relevant literature is learning the optimal prices or optimizing aggregated total revenue by repeatedly interacting with a single buyer [4, 5, 26, 27, 38]. Similar to us, they also consider the buyer’s strategic behavior that potentially tricks the seller’s learning algorithm. However, these previous works all focus on designing learning algorithms that can handle strategic data sources. Our work can be viewed as a complement to this literature. Instead of proposing new algorithms, we focus on understanding the limits of what learning algorithms can achieve by analyzing a basic model which is a variant of the textbook-style optimal pricing model. Moreover, the setups of these previous works are also different from us, which make them not comparable to us. For example, some of these models [4, 5, 27] assume that the buyer’s values for goods are drawn from distributions (a.k.a., demand distribution) and consequently his best responses to seller prices are stochastic with randomness inherited from his value distribution. However, our model assumes that the buyer has an unknown but fixed value function that drives his purchase responses. Such a response is the solution to buyer’s optimization problem while not from a random distribution. There have also been models that consider unknown but fixed buyer values like us [26, 38]. However, these works have focused on a single indivisible good with discrete agent utilities whereas our model has multiple divisible goods with continuous agent utilities.

There have also been studies on learning the optimal prices from truthful revealed preferences, i.e., assuming the buyer will honestly best respond to seller prices [8, 39, 6, 42, 3, 33, 32]. Our works try to understand if the assumption of truthful revealed preferences does not hold and if the buyer will strategically respond to the seller’s learning, what learning outcome could be expected when the buyer simply imitates a different value function that is optimally chosen. From this perspective, these works serve as a key motivation for the present paper.

More generally, our work subscribes to the general line of research on learning from strategic data sources. Strategic classification has been studied in other different settings or domains or for different purposes, including spam filtering [11], classification under incentive-compatibility constraints [43], online learning [17, 12], and understanding the social implications [1, 25, 21]. Finally, going beyond classification, strategic behaviors in machine learning has received significant recent attentions, including in regression problems [31, 15, 13], distinguishing distributions [40, 41].

A.2 Additional Discussion on Buyer’s Commitment

The buyer’s ability of making such a commitment fundamentally comes from the fact that the seller has no prior knowledge about the buyer’s true value function , i.e., has to “price in the dark”.555By convention, all value functions are assumed to be concave. This can be equivalently viewed as a restriction to the buyer’s manipulation imposed by the seller’s (very limited) prior knowledge about concavity of buyer values. Later, we will also briefly discuss how the absence of this prior knowledge may lead to worst seller revenue. To find a good pricing scheme, the seller may interact with the buyer to learn the his value function [39, 8, 6], or learn the optimal pricing scheme [33], or directly optimize the aggregated revenue during repeated interactions [4, 5, 26, 27, 38]. However, regardless what algorithm the seller may adopt, the buyer can always choose to consistently behave according to a carefully crafted different value function , i.e., the commitment. For example, suppose the seller tries to apply any machine learning algorithm, the buyer may respond by directly announcing his imitative value function even before the learning starts and then behave consistently. In such scenarios, learning is even not needed since the best a seller can do is to respond with the optimal pricing against . Similarly, if the seller adopts any dynamic pricing mechanism, the buyer may respond similarly by announcing her value function . Since the seller lacks knowledge about the buyer’s value, such imitative buyer behavior makes him indistinguishable from a buyer who truly has value function . Therefore, our equilibrium characterization in later sections will help to understand what the optimal imitative value function for the buyer is and what revenue the seller can possibly achieve when pricing against such a strategic buyer in the dark, i.e., without any prior knowledge.

We remark that though the imitative strategy may not always be the absolutely best possible strategy for the buyer, but it enjoys many advantages. First of all, as we will prove later, this strategy does lead to significant improvement to the buyer’s utility666It is never worse since the buyer can always at least behave truthfully by letting . and, in fact, is provably the best possible (among all possible strategic behaviors that the buyer may adopt) in certain circumstances, e.g., when the seller’s production cost function is concave. Second, this imitative strategy is easy to adopt in practice and requires no knowledge about the seller pricing scheme. For example, this imitative strategy works equally well for any price learning algorithm so long as it can effectively learn the optimal price from the buyer. Third, it also has good long term effect since the seller cannot distinguish whether the buyer truly has value function or not, and may just have to use the same learned price for future purchases from this buyer. However, we show later that any buyer behavior that is not consistently imitating a value function can be easily identified by the seller. In such situations, even though the seller ended up with some prices, she knows that it is not the truly optimal price for this buyer and may take this into account in future interactions.

Appendix B Technical Background: Concave/Convex Functions and Super/Sub-Gradients

Let be any function where is the domain of . A vector is called a super-gradient for at if for any we have . Function is called concave if for any and any we have . Super-gradients do not always exist. However, a concave function has at least one super-gradient at any . For a differentiable concave function , its gradient is the only super-gradient at for any . If is concave but not differentiable, it may have multiple super-gradients at some . In this case, we use to denote the set of all super-gradients of at . Among all super-gradients in , of our particular interest is the following one: . This is the super-gradient that maximize linear function . When is differentiable, is the (only) super-gradient.

Function is called convex if is concave. For convenience of stating our results, we will mostly work with differentiable convex functions in this paper. A useful distance notion for differentiable convex function is the Bregman divergence:

is always non-negative for convex functions and strictly positive for strictly convex functions when . However, Bregman divergence is asymmetric among variables, i.e., in general.

Appendix C Proof of Theorem 1

See 1

We start with a useful lemma that characterizes the relation between optimal seller price and optimal buyer bundle for any concave buyer utility function . A similar result has been proved in [33]. The only difference here is that we allow any concave buyer utility function whereas the buyer utility function in [33] is assumed to be strictly concave and differentiable. Nevertheless, the proof remains similar and thus is omitted due to space limit.

Lemma 3.

For any concave buyer value function reported by the buyer, let be the optimal price vector for the seller and be the resultant buyer optimal bundle for purchase, then the following relation holds:

| (8) |

where .777The “” comes from the fact that the seller will pick the profit-maximizing price if multiple prices result in the same optimal buyer purchase.

A crucial intermediate step in our proof is the following characterization for a slightly simpler version of the question. That is, fixing any bundle , which imitative value function will maximize the utility of the buyer with true value function , subject to that the optimal buyer purchase response under is ? If we can find a succinct characterization for this simpler question, what remains is just to search for the best bundle . That will be a (variable) optimization problem, which is suitable for standard optimization techniques to solve. Fortunately, the above question does admit a succinct characterization.

Lemma 4.

[Lemma 1 restated] For any bundle , the optimal buyer imitative value function , subject to that the resultant optimal buyer purchase response is bundle , can without loss of generality have the following piece-wise linear concave function format, parameterized by a real number :

| (9) |

where is the solution to the following linear program (LP):

| (10) |

Moreover, under imitative value function , we have

-

1.

For any convex coefficients , the linear pricing scheme with unit price vector will be optimal.

-

2.

In any of the above optimal linear pricing schemes, the buyer’s optimal bundle response will always be and the buyer payment will equal .

Proof of Lemma 4.

From the buyer’s perspective, with a fixed bundle in mind, his problem is to come up with an imitative value function such that its corresponding price as from Lemma 3 maximizes his revenue at bundle . This results in the following functional optimization problem (FOP) for the buyer with functional variable .

| (11) |

where the first constraint means the seller’s optimal price for value function is and thus the buyer best response bundle is indeed .

The lemma states that the defined in Equation (9) is an optimal solution to FOP (11). To analyze FOP (11), we first simplify the class of concave function that we need to consider. In particular, we claim that there always exists an optimal solution to FOP (11) such that has the following form:

| (12) |

where the only parameter is the coefficient vector. To prove this, let be any optimal solution to FOP (11). Construct another concave value function as follows:

| (13) |

Note that is precisely the payment for a buyer with value function when his optimal bundle amount is . We show that this new value function will result in the same optimal buyer bundle and payment . It thus does not change either of the agent’s utilities and remains optimal for the buyer.

First, we argue that the constructed is still feasible to FOP (11). Concavity of is evident since it is the minimum of a set of linear functions. By Lemma 3, we have if is element-wise strictly greater than . Otherwise, let ,888If there are multiple that all minimize , the proof is valid by picking any of them. we have which is the ’th element of , while all the other gradient entries of are . Therefore, we have . Specifically, which equals precisely the buyer payment under utility .

We now verify that the constraints in FOP (11) still holds for . We start from verifying for special s where there exists such that . In this case, we have

| (since ) | ||||

| (by feasibility of ) | ||||

| (by concavity of ) | ||||

| (since and ) | ||||

| (by definition of and ) |

Specifically, the second inequality holds because is the directional derivative of at in the direction of , which is non-increasing with respect to due to the concavity of . The above argument also implies by instantiating .

Next, we consider the case when for . There will be two possible situations to consider:

-

1.

If is element-wise greater than , then . Thus, we have .

-

2.

If is not element-wise greater than , let and . Then we have which is the ’th element of , while all the other elements of are . In addition, denote . Note that for , we have . However, we have because is element-wise less than or equal to . Thus, we have by monotonicity of . Our previous derivation for the special case with implies . These together imply

As a result, the constructed is feasible to FOP (11) because for any .

Next, we argue that achieves the same buyer utility, and thus must also be optimal. This is simply because the feasibility of implies that the optimal buyer bundle will still be and payment will still be . As a result, buyer achieves the same utility when using and , yielding the optimality of .

So far we showed that there always exists an optimal of Form (9). Therefore, to solve FOP (11), we can without loss of generality focus on functions of the Form (9), which is parameterized . By plugging in Form (9) into FOP (11), we obtain the following LP with variable .

| (14) |

We now further simplify the above LP to become LP (10). That is, we argue that only the first constraint is needed and thus the other constraints can be omitted. When the first constraint is instantiated with , it implies . This immediately implies the second and the last constraint. By the proof above, we know that for any and is not element-wise greater than either, there must exist such that . Therefore, the third constraint is guaranteed to be satisfied as long as the first constraint is satisfied. As a result, the above LP can be further simplified to LP (10).

The constraint of LP (10) guarantee that the seller will maximize revenue at bundle . Since at , any will minimize the term . Lemma 3 then implies the optimal prices at can be any convex combination of pricing vectors . The total payment will always be under any of these optimal pricing schemes. This completes the proof. ∎

Theorem (1) then follows from Lemma 4. We first observe that constraint in linear program (10) can be re-written as for (the constraint is trivial for ). Since the objective of LP (10) is equivalent to minimizing , we thus have the optimal equals .

We have now characterized the optimal imitative value function for any fixed . To compute the globally optimal imitative value function , we only need to pick the that maximizes the buyer’s surplus. By viewing as a variable , we obtain the desired form of as in Equation (3). Finally, the buyer surplus and seller revenue follow directly from the fact that purchase happens at bundle with payment . These conclude the proof of Theorem 1.

Appendix D Omitted Proofs in Section 5

D.1 Proof of Theorem 2

See 2

Proof.

Suppose is convex and differentiable. Fix any . Consider the function with variable . This is a one-dimensional convex non-decreasing function. Due to convexity, the supremum of over equals precisely the derivative of at , which is . To find the that maximizes the buyer’s revenue, the buyer will pick . Given the above characterization, the theorem conclusion follows from Theorem 1. ∎

D.2 Proof of Theorem 3

See 3

Proof.

Suppose is concave and differentiable. Fix any . Consider the function with variable . This is a one-dimensional concave non-decreasing function. Due to concavity, the supremum of over is achieved at . The supremum thus equals precisely . To find the that maximizes the buyer’s revenue, the buyer will pick . Given the above characterization, the theorem conclusion follows from Theorem 1. Specifically, the buyer payment , leading to seller revenue . ∎

D.3 Proof of Theorem 4

See 4

Proof.

As stated in the theorem, we consider the case where the buyer’s true value function is and the seller’s production cost function is a concave function that we will construct. Theorem 3 shows in this case, the buyer’s optimal surplus is

Next, we show that this optimization problem is NP-hard to be approximated within any meaningful ratio, as described by the theorem. Our reduction is from the independent set problem. For any connected graph with nodes, let node set . A set is an independent set of if and only if any are not adjacent in . The problem of finding the largest independent set problem is NP-hard, and cannot be approximated within ratio for any constant .

Given any instance graph of the Independent set problem, we construct the following concave production cost function:

Moreover, the set of feasible bundles is . Note that is a concave function because the minimum of two linear functions is concave and the sum of concave functions remains concave. Moreover, is monotone non-decreasing and . So is indeed a valid cost function for our setting. Under this construction, the maximum possible buyer surplus is the optimal objective of the following optimization problem (OP):

| (15) |

We now show via a reduction from the largest independent set problem that it is NP-hard to approximate OP (15) to be within ratio for any . Let be the maximum independent set. We claim that the optimal objective value of the above optimization problem equals precisely , the size of the maximum independent set. For convenience, let term and thus . Note that for any .

First, we show that the optimal objective value of OP (15) is at least . To see this, consider such that if and if . We argue that for any , . This is because for any — for any , we must have as the two nodes are both in the independent set and thus cannot have an edge between them (i.e., ). Therefore, and thus . As a consequence, for any , and thus the objective of (15) at is at least .

Next, we show the reverse direction, i.e., is at most . Note that is a convex function. So it must achieve the maximum at some vertex of the feasible region, which is a binary vector. Let denote the set of the indexes of non-zero values in . First of all, for any , . Second, for any , if there exists such that is an edge, then and thus . This implies . Similarly, as well. Finally, for any without any neighbor included in , it is easy to see that . To sum up, only the node that does not have any neighbor included in can have whereas any other node has . Therefore, is at most the size of the number of independent nodes in , which is at most the size of the maximum independent set for , as desired.

So far we have shown that the optimal objective value of OP (15) equals precisely the size of the maximum independent set of . However, we are not done yet to prove the inapproximability of maximizing . This is because takes fractional variables as input. The fact that it is hard to find an independent set to approximate the size of the maximum independent set does not imply the hardness of finding a fractional variable to approximate .

To prove the inapproximability of the continuous OP (15), we show that any -approximation to OP (15) can be efficiently turned into an -approximation to the largest independent set problem, using ideas from de-randomization. Since it is NP-hard to approximate the largest independent set problem to be within for any , this will conclude the proof of the proposition.

Specifically, let be any -approximation to OP (15). We construct a random binary vector as follows: and for each independently. By convexity of , we have . In other words, if we pick the random solution , the expected objective is at least . By a standard de-randomization procedure (up to an additive difference due to Monte-Carlo sampling),999Specifically, for each . To de-randomize, we simply calculate and through Monte-Carlo sampling, and then pick the larger one. we can efficiently find a binary vector whose value is also at least . By a similar argument above, we know that all the independent nodes in form an independent set whose size is at least , as desired. ∎

Appendix E Omitted Proofs in Section 6

E.1 Proof of Lemma 2

See 2

Proof of Lemma 2.

We first prove the a function of the following format, parameterized by variable , is optimal to FOP (6):

| (16) |

To prove this, let be any optimal solution to (6). We now construct another concave value function as follows:

| (17) |

Next, we first argue that the constructed is still feasible to FOP (6). First, for any where , we have

| (by definition of ) | (18) | ||||

| (by feasibility of ) | (19) | ||||

| (By concavity of , and ) | (20) | ||||

| (by definition of ) | (21) |

Note the last inequality is by concavity of , we have where we have . Thus, we have .

Then we consider the case . There will be two possible situations if :

-

1.

If is element-wise greater than , then . Thus, we have by the monotonicity of .

-

2.

If is not element-wise greater than , let and . Then we have . In addition, denote . Note that for , we also have . However, we have because is element-wise less than or equal to . Thus, we have by monotonicity of . By equations (18)-(21), we have . On the other hand, for any which is not element-wise greater than , there must exist a where such that .

As a result, the constructed is feasible to FOP (6) because for any .

Next, we argue that achieves the same buyer utility, and thus must also be optimal. This is because: (1) the feasiblity of implies that the optimal price will be ; (2) the optimal buyer amount will then be by breaking ties rule. As a result, buyer achieves the same utility when using and , yielding the optimality of .

So far we showed that there always exists an optimal of Form (16), which is parameterized . We then return to the situation of linear pricing since a linear pricing scheme with unit price where is optimal for such a among all concave pricing schemes. The characterization then follows from Theorem 1. ∎

E.2 Proof of Proposition 1

See 1

Proof.

We first analyze the situation of linear pricing. By the characterization in Theorem 2, we know that the optimal purchase bundle satisfies . Given and in Example 1, this solves for in the linear pricing setting. Furthermore, this gives and optimal imitative value function . The seller revenue in this case is .

Next, we show that the seller’s revenue will strictly decrease at equilibrium when using pricing class that augments linear pricing class with the following additional choice of a concave pricing function

where is a small constant.

Consider the imitative value function and a particular linear pricing response . In this case, the buyer will purchase an amount , implying . Solving for gives . Now, we solve for the linear pricing response that maximizes the seller revenue.

Thus, the optimal linear pricing response to is . The buyer will purchase , giving the seller a revenue of . Finally, consider the pricing function for the buyer’s imitative value function . We observe that , meaning . Thus, the buyer can purchase and the seller will get revenue . This is strictly larger than the seller’s revenue from the optimal linear pricing scheme. Thus the seller’s optimal pricing scheme from is .

Finally, note that , meaning the optimal bundle for the buyer to purchase when the seller responds with is . In this case the buyer surplus is , meaning the optimal true buyer surplus given pricing function is greater than the optimal true buyer surplus given any linear pricing response. Thus, is an optimal imitative function under pricing class and the seller revenue of is strictly lower than the seller revenue of under linear pricing class . ∎