Spiked Covariance Estimation from Modulo-Reduced Measurements

Elad Romanov Or Ordentlich

Hebrew University of Jerusalem Hebrew University of Jerusalem

Abstract

Consider the rank-1 spiked model: , where is the spike intensity, is an unknown direction and . Motivated by recent advances in analog-to-digital conversion, we study the problem of recovering from i.i.d. modulo-reduced measurements , focusing on the high-dimensional regime (). We develop and analyze an algorithm that, for most directions and , estimates to high accuracy using measurements, provided that . Up to constants, our algorithm accurately estimates at the smallest possible that allows (in an information-theoretic sense) to recover from . A key step in our analysis involves estimating the probability that a line segment of length in a random direction passes near a point in the lattice . Numerical experiments show that the developed algorithm performs well even in a non-asymptotic setting.

1 Introduction

We consider the problem of estimating a spiked covariance matrix from Gaussian modulo-folded measurements. Let be an unknown direction, and be the signal-to-noise (SNR) ratio. Consider the spiked covariance matrix

| (1) |

and denote . Equivalently, one may write

| (2) |

where have entries; the one dimensional component is often thought of as the “signal”, whereas is thought of as “noise”. In this paper, we consider the problem of estimating from independent and modulo-reduced measurements of . Let be the dynamic range, and for , denote the modulo operation by

| (3) |

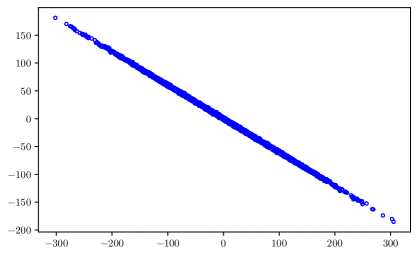

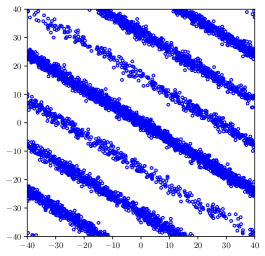

so that is the unique number in the half-open interval such that . For a vector , is defined by modulo-reducing each coordinate separately. In the setup we consider, one is given independent copies of , denoted by , and wishes to estimate the unknown direction . Throughout, we denote by independent copies of , such that . See Figure 1 for a graphical illustration, in dimensions.

Motivation.

Our motivation for considering this problem is driven by recent developments in signal processing. Analog-to-digital converters (ADCs), devices that convert analog (continuous) signals into digital (discrete, e.g. bits) signals, are an essential component in virtually all modern communication devices. From a mathematical perspective, ADCs are set out to solve essentially the following problem: Given a vector-valued random variable , find a quantizer (binning scheme), , with a finite range, ( being the allowable representation length in bits), so as to minimize the quantization error: . Quantization is an extensively studied problem, and its fundamentals limits (in information theory: “rate-distortion theory”), under setups of varying generality, are largely understood; see, e.g., [Cover and Thomas, 2012, Gersho and Gray, 2012].

Optimal vector quantizers (that achieve the fundamental limits) typically involve rather complicated constructions, that depend intricately on the exact statistics of . Since ADCs are implemented in mixed analog-digital circuits, sophisticated vector quantizers are prohibitive and the design is often restricted to architectures of a scalar product form: where . Perhaps the simplest – and most popular – architecture in practice is a uniform scalar quantizer, determined by its dynamic range and bit-rate . The quantizer divides the interval into intervals of equal size , so that the scalar quantizer maps to its closest interval center. Note that for this scheme to attain quantization error that vanishes as the quantization rate increases, the dynamic range must be .111If falls inside , then . For the expected error to be of the same order, the probability of a saturation, namely , has to be small.

Although simple to implement, the uniform quantizer can be pronouncedly sub-optimal for vector-valued signals, as it cannot leverage the cross-coordinate correlations that often occur in real-world applications. An important use-case in digital communications is Massive MIMO, where typically the number of users is much smaller than the number of receive antennas; this results in signals that have strong cross-entry correlations.222A multi-user MIMO channel is modeled by , where the number of receive antennas, is the number of transmitting users, each equipped with a single antenna, and is the channel matrix ( represents the channel gains from transmitter to the receiver). The vector represents the transmissions of the users, and is white noise. The “signal” part, , lives inside an -dimensional subspace in , where typically . One example, among many, for the extreme case of rank MIMO (corresponding to model (2) exactly), is in low-earth orbit (LEO) communications, where a phased array receiver is used to track a rapidly moving satellite. Thus, a quantization scheme that can exploit these statistical inter-dependencies, while retaining the simplicity of the uniform quantizer, is highly desired.

A recently proposed architecture, “modulo-ADCs” [Ordentlich et al., 2018], attempts to address these issues. Their idea is rather simple: do not truncate onto , as the uniform quantizer does; instead, apply modulo-reduction and then quantize as before. For this idea to work, one clearly need some means of “unwrapping” from (with high probability). When the coordinates of are independent and unimodal, with the mode at (for example, a centered Gaussian), it is easy to see that the best estimator for from (in the sense of error probability) is just . Thus, a coordinate cannot be recovered once it saturates the ADC dynamic range, ; so to consistently undo the modulo, one needs , and the scheme has no advantage over the standard uniform quantizer. It turns out, however, that when has strong correlations, it is often possible to consistently unwrap at substantially smaller values of ; see next section.

1.1 Related work

We start with very brief background on the spiked model, Eq. (2). In the high-dimensional statistics (, ) literature, the spiked model was popularized by [Johnstone, 2001], who studied the largest eigenvalue of the sample covariance matrix . Subsequent advances in random matrix theory [Baik et al., 2005, Paul, 2007] characterized the behavior of PCA (namely, the relation between the principal components of and its empirical counterpart ) rather precisely. Since then, a vast literature on the spiked model (and variations thereof) has emerged – which we make no pretense to survey here; as an entry point, geared towards statisticians, see [Wainwright, 2019, Chapter 8]. We cite the following minimax lower bound for the spike estimation problem (without modulo-reduction) [Wainwright, 2019, Example 15.19]:

| (4) |

In the regime , this rate is attained, up to prefactors, by PCA ( taken to be the largest eigenvector of ), see [Wainwright, 2019, Corollary 8.7].

Moving on, there has recently been a great deal of activity in the signal processing community around recovery from modulo-reduced measurements [Bhandari et al., 2017, Ordentlich et al., 2018, Bhandari et al., 2018, Graf et al., 2019, Romanov and Ordentlich, 2019, Bhandari and Krahmer, 2019, Bhandari et al., 2020, Bhandari et al., 2021, Weiss et al., 2021]. Most relevant to this paper is a line of works dealing with recovery from modulo-reduced measurements, and motivated by the modulo-ADC architecture described before [Ordentlich and Erez, 2017, Ordentlich et al., 2018]. The setting is this: the source is Gaussian , with some covariance matrix (not necessarily spiked); one observes modulo-reduced measurements , and wishes to recover itself (with high probability). How large should be so that consistent recovery is possible, in an information-theoretic sense? When it is possible, how could one do so practically? (Assuming is known? And when it is not?) The answers, it turns out, depend rather intricately on the diophantine properties of the matrix .

Let us start with the fundamental limits. A simple observation is that when ( being the variance of the -th coordinate), one has with high probability, so that consistent recovery is straightforward. It is easy to see that when is white, in other words , this requirement is in fact tight. For general , one may readily show that the maximum a posteriori probability (MAP) estimator for given is

| (5) |

that is, one needs to minimize a quadratic form over the coset of . Searching over the coset directly (and consequently, computing exactly) is not computationally tractable, in all but the simplest cases; nonetheless, since is optimal in the sense of error probability, its performance characterizes the information-theoretic limits of the problem. The latter has a rather elegant geometric interpretation. Let be the lattice generated by , and let be the Voronoi cell of . Then [Romanov and Ordentlich, 2021] the success probabililty of (5) is the Gaussian measure of :

As a corollary, it is not hard to show that333 denotes the determinant of . implies that ; see also Proposition 2. When the lattice is a uniformly random lattice, sampled, up to normalization, from the Haar measure over (also called Haar-Siegel measure), one can show that is with high probability “sufficiently ball-like”, so that is also a sufficient condition. Random lattices have played a prominent role in the lattice coding literature [Zamir, 2014], which is closely related to the present line of work. An important point is that “natural” random matrix ensembles, such as the spiked ensemble (1) with , do not correspond to the Siegel-Haar measure on the space of lattices. In [Domanovitz and Erez, 2017] the authors demonstrate that certain orthogonally-invariant ensembles, that arise in channel coding theory, indeed allow for consistent recovery with not much larger than . In particular, for the spiked ensemble (1), they show that with high probability over , the error probability is small whenever , where grows exponentially fast in , but does not depend on the SNR .

As for practical recovery algorithms, let us start by assuming is known. As already mentioned, computing the MAP estimator directly is intractable; instead [Ordentlich and Erez, 2017] proposed to use a sub-optimal estimator, the so-called Integer Forcing (IF) decoder. The idea is to find an invertible integer matrix so as to minimize the maximal variance:

| (6) |

The corresponding maximal deviation, , is called the th successive minimum of the lattice . Since , one can reliably recover from , using , whenever . Of course, to compute the IF decoder, Eq. (6), one clearly needs to know .444An important caveat is that Eq.(6) is actually a computationally hard problem, and may only be solved exactly for very small . In practice, one usually solves this approximately, using a lattice reduction algorithm, like the Lenstra-Lenstra-Lovász (LLL) algorithm [Lenstra et al., 1982]. Observe that if one a priori restricts the minimization to , then Eq. (6) is equivalent to finding a shortest basis for the lattice . In some applications, for example in wireless communications (where depends on the channel matrix, which rapidly changes over time) [Tse and Viswanath, 2005], this is not a reasonable assumption. In [Romanov and Ordentlich, 2021], the authors propose a blind unwrapping algorithm, that does not know beforehand, in a setting where one needs to simultaneously unwrap many i.i.d. signals . A natural step towards that end is to estimate from the (modulo-reduced) data, from which the integer-forcing decoder (6) could be computed. Alas, directly computing the maximum likelihood estimator (MLE) of from modulo-reduced measurements is not computationally feasible. Instead, they propose an algorithm which iteratively alternates between 1) A covariance estimation step, where a certain “proxy” of is estimated; 2) An integer forcing decoder, computed from that proxy; the idea is to gradually “whiten” the entire dataset, effectively computing the IF decoder “in small steps”. They prove a result of the following form: when the error of the informed IF decoder (Eq. (6)) is small enough, then the error of the adaptive algorithm is essentially comparable to it, up to dimension-dependent prefactors. However, their algorithm is only suited to rather modest , as seen both in the analysis (the prefactors are exponential in ) and the numerical experiments. The problem lies with their covariance estimation procedure, whose performance breaks down rapidly as the dimension increases. This is the starting point for the present paper.

Our contributions.

We propose a computationally tractable algorithm to estimate the spike from modulo-reduced measurements, under the spiked covariance model Eq. (1) and in high dimension . We show that for most directions (formally: with high probability over ), estimation is possible with samples, under essentially the smallest (up to constants) that allows for consistent unwrapping. Thus, in this setting, we provably overcome the curse of dimensionality suffered by the algorithm of [Romanov and Ordentlich, 2021]. While we do not directly tackle the unwrapping problem, note that in applications where the SNR is approximately known, the algorithm readily yields an estimate for , from whence one could compute the IF decoder (6). Our numerical experiments below show that this method attains an unwrapping error probability that is not far from that of the informed IF decoder.

Notation.

For sequences we use the following standard notation: , . By we mean that for some universal constant ; we write whenever both and . We also use big-O notation; if is a parameter, we use to signify that the constants might depend on . For a vector , denotes its (Euclidean) norm.

2 Proposed method

An observation.

Our algorithm is based on the following observation: the eigen-structure of the covariance matrix of is preserved when truncated onto a ball. Set a truncation radius. For , let be its spherically-truncated version: for ,

Observe that , since is symmetric. Denote the covariance by .

Proposition 1

Let be any covariance matrix, with (orthonormal) eigenvectors and corresponding eigenvalues . Then

-

1.

The basis diagonalizes . Denote ; the respective eigenvalues are:

(7) -

2.

The ordering is preserved: .

Proposition 1 is not new by any means. It has appeared before in [Palombi et al., 2012], which considered covariance estimation from spherically-truncated Gaussian measurements (see also discussion later in this section). The proof of Item 1 is rather trivial; for completeness, we provide a short proof (Appendix A). Item 2 is considerably less so; we refer to [Palombi et al., 2012, Proposition 3.3] for the details.

The algorithm.

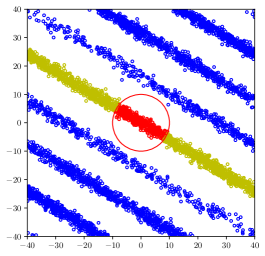

We draw inspiration from Figure 1. For “most” directions , the points are arranged, essentially, in parallel and separated stripes. The central stripe (that crosses the origin) consists of points that have not undergone folding, . Picking only points inside a small enough ball , we therefore obtain, approximately, an i.i.d. sample from . By Proposition 1, the leading eigenvector of is , and therefore PCA with should yield a consistent estimator (as ). See Figure 2 for a graphical illustration; and Algorithm 1 for a formal description.

The truncation radius.

In spite of its seeming simplicity, the behavior of Algorithm 1 depends drastically on the truncation radius . Its choice should balance between two opposing effects. On the one hand, the algorithm uses effectively measurements for estimation (where , so cannot be too small; on the other hand, we need to take only (or mostly) points from the central stripe, so cannot be too large. Let us start with an observation: when , is exponentially small in , so the algorithm requires measurements. Consequently, to (potentially) overcome the curse of dimensionality one must set . In that case, (Lemma 2), so that for a large spike, , ; therefore, we shall henceforth restrict our attention to . As we have said, cannot be chosen too large, and in general there is a rather delicate tradeoff between the parameters and the direction itself. Our main result, Theorem 1, says, roughly, the following: there is a choice such that for most directions, if and , then Algorithm 1 estimates with small error from only measurements.

On estimating .

In this paper, we restrict our attention to estimating only the direction (and not ). We mention two potential strategies for estimating , not pursued here further due to space constraints:

-

•

[Palombi et al., 2012] studies covariance estimation from spherically-truncated Gaussian measurements. Relying on Proposition 1, they prove that the mapping between the true and truncated eigenvalues is invertible, and propose a fixed point iteration to recover from (given exactly, without noise). Our proposed algorithm computes an estimate of ; computing error bounds for the method of [Palombi et al., 2012], applied to , is potentially challenging, especially in the regime where , where the mapping is necessarily badly conditioned.

-

•

Since only one eigenvalue of is unknown, a more natural approach is to invert (numerically) the mapping , which is strictly decreasing.

2.1 Main results

The following is our main result. It shows that for most directions , the error attained by Algorithm 1 can be made quite small, with reasonably controlled, and assuming only . To make the presentation lighter, we focus exclusively on the regime where the spike is not small, (which is also practically more interesting). Below, denotes the largest eigenvector of , with the sign ambiguity resolved by assuming that .

Theorem 1

Fix a constant , and set as in (11). There is a universal constant and a set with

such that whenever and , the following error bounds hold (depending on the magnitude of ), with probability :

-

1.

Assume that and . Then

(8) -

2.

Assume that . Then

(9)

Discussion.

Let us start with the small-spike regime, . The first term in Eq. (8) is, up to prefactors, the error rate for PCA without modulo-folding, see e.g. [Wainwright, 2019, Chapter 8]; in particular, when , it matches the minimax lower bound Eq. (4). The second term corresponds to error incurred by erroneously taking “bad” points , that do not belong on the central stripe. By taking large enough, this term can be made to decay arbitrarily (polynomially) fast as . We note that in this regime, the consequences of Theorem 1 are, in fact, rather unsurprising: if , then with high probability, . Since , the cube contains a segment of length ; consequently, a large fraction of are actually themselves already inside the cube, since the “typical length” of the projection along , , is (the standard deviation).

The “interesting” regime is . Note that unlike in the small-spike regime, here the error, Eq. (9), increases as grows. Moreover, the magnitude of has to be constrained by : (the constant is itself not particularly important, and can be improved). Thus, to retain the scaling , has to grow at most polynomially with ; in that case, note that the term in the bound for is always negligible. Furthermore, note that has to scale at least as , which anyhow precludes the practically of the algorithm when is super-polynomial, regardless of the third term.

Let us try to get some intuition for the particular form of the bounds (8), (9), by considering a simplified setting, where one had direct access to all the measurements that lie inside the ball , and used them to perform PCA. There are roughly (Lemmas 1, 2)

such measurements. By Proposition 1, the population covariance is spiked, and one can show (Lemma 7) that the effective spike is

(Note that lies inside , and consequently ). In particular, note that when , decreases with but cannot grow further to compensate for this; this is the reason why the error in Eq. (9) degrades with . Now, assuming that is large enough (this point is a little subtle, since we let grow as well), the error is bounded like

using “standard” bounds for PCA (e.g. [Wainwright, 2019, Chapter 8]). Plugging in the above estimates for recovers the first terms in Eqs. (8), (9). The challenging part of the analysis (and our main technical contribution) is to control the last term: namely, show that for most directions , when , the contribution of the erroneously picked (“bad”) points is indeed very small with high probability.

Experiments.

We demonstrate the validity and relevance of our results through numerical experiments:

-

•

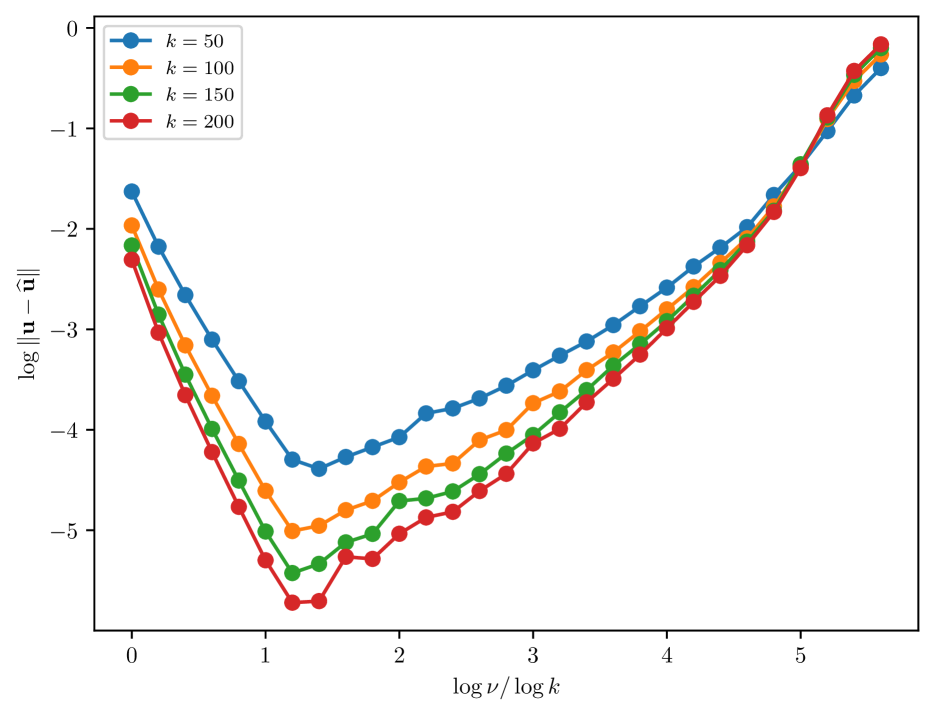

In Figure 3(a) we study the behavior of the error, , as the spike magnitude changes. For several values, , we have set , and varied for an exponent ; each point on the graph is the average error across repetition. We observe that as increases, scaling indeed suffices for estimation. Moreover, we see that for small spikes, , the error decreases as increases, whereas when the error increases; this is consistent with Theorem 1.

-

•

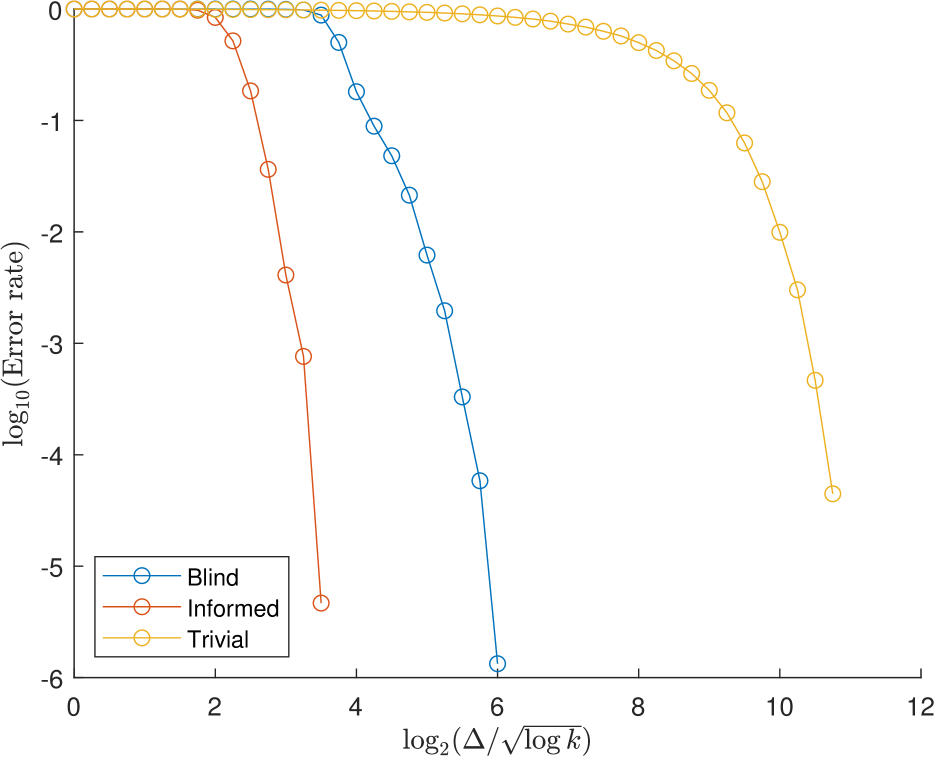

In Figure 3(b) we apply our algorithm as an intermediate step for blind unwrapping. We set , , and vary . At every working point, we compute the error rate, namely the fraction of erroneously recovered samples , of the informed IF decoder (Eq. (6)), the blind IF decoder (computed from ), and the trivial decoder . For each method, is increased in jumps of , until the point where ; each point on the graph is the average of repetitions (so, overall, single recovery trials). We see, for this particular setup, a gap of around bits between the the informed and blind decoders, and of about bits between the blind and trivial decoders. To put things in context, a hypothetical quantization scheme based around modulo-folding and the blind decoder could save up to bits per coordinate (so bits overall) compared to the uniform quantizer (both designed so that the probability of a saturation is ).

By Theorem 1, when , the condition ensure that one can estimate most directions with measurements. Recall that the present problem was motivated by the modulo-unfolding problem (which is a harder problem). It turns out that for the latter, the condition is actually necessary. Thus, if one’s goal is to solve the unwrapping problem (e.g. for implementing modulo-ADCs), and to that end estimates the covariance as an intermediate step, then our algorithm succeeds with essentially the smallest allowable dynamic range. We show the following (see Appendix B for the proof):

Proposition 2

Suppose that there exists , with . Then .

We remark in passing that, once we have obtained an estimate for , and consequently for , using Algorithm 1, we may use it to unwrap the measurements (using, e.g., the IF decoder). Having unwrapped the samples, we can use standard methods (e.g., PCA) to get an improved estimate of . We do not pursue this option here for two reasons: 1) The performance of such an algorithm depends on the unwrapping error probability, which is difficult to analyze. In particular, unwrapping errors could have a disastrous effect on the estimation error; 2) Our primary motivation for estimating in the first place was to perform unwrapping. To that end, once we obtain an estimate of with accuracy sufficient for unwrapping, further improvements are of limited interest.

3 Analysis

In this section, we give a proof outline for our main result, Theorem 1. In the interest of space, the proofs of most technical lemmas are relegated to the Appendix.

Going forward, we fix a truncation radius:

| (11) |

This particular choice is rather arbitrary. One could carry out the analysis with any for ; this would only change the constants in the bounds.

3.1 High level view

Divide the pairs into groups. Denote by

respectively the points that were picked by Algorithm 1, and those for which . Note that, conditioned on , ; hence is an i.i.d. sample from . Observe also that , since . We denote by the subset of measurements for which , in other words, such that to begin with. The measurements in , will be called bad. We have

Now, the sample covariance,

| (12) |

is a consistent (as ) estimator for , whose largest eigenvector is (Proposition 1). Consequently, PCA yields a consistent estimator for the unknown direction. Alas, the set is not directly observable, so the algorithm uses instead:555Note that we have normalized by , which is unknown. This is done for the sake of convenience in the analysis; the eigenvectors, of course, are not affected.

| (13) |

This injects additional error into the covariance estimation process, in two ways. First, the covariance is computed using the -s instead of the -s (the latter are unknown); we have only for , which may be a strict subset of . Second, we use additional samples, on top of : the points in necessarily come from the wrong distribution. Set

so that . A bound on this operator norm yields, by standard eigenvector perturbation results, a bound on . Note: is simply the statistical estimation error in estimating from i.i.d. measurements; the other term, , is the error induced through picking erroneous measurements. We shall bound each error term separately.

3.2 The covariance estimation error

We start with ; the argument is quite standard. First, we show that with high probability, is reasonably large. Denote

| (14) |

so that . Controlling is straightforward using, e.g., Chernoff’s inequality (Appendix H, Lemma 19):

Lemma 1

For any , for universal ,

Next is an (tight, for large ) estimate for ; the (short) proof is relegated to Appendix G.1:

Lemma 2

where, recall, the error function is defined by

| (15) |

Note that Lemma 2 implies that when , whereas when ; in other words, .

Error bounds for covariance estimation rely on the concentration properties of the data. Thus, we need to show that “inherits” the favorable properties of the underlying Gaussian vector . We start with a general Lemma, whose proof appears in Appendix G.2:

Lemma 3

For every convex function ,

The proof of Lemma 3 relies on the Gaussian correlation inequality. As an important corollary, it allows us to control the sub-Gaussian and sub-exponential norms of ; see Appendix C, Lemma 9.

Recall that by Proposition 1, is a spiked covariance matrix with largest eigenvector :

so that applying Lemma 3 (with ),

The rest of the analysis proceeds along rather standard lines, as in e.g. [Wainwright, 2019, Section 8.2.2]; the full details are given in Appendix C. We prove:

Lemma 4

Suppose that . Then, with probability ,

3.3 The sample picking error

Decompose

so that

| (16) |

Above, we used: for ; for ; and .

The next Lemma is one of our main technical results. It states that for most directions , the probabiliy that a pair is bad, meaning that but , is overwhelmingly small provided that :

Lemma 5

Fix a constant . There is a universal and a subset with

such that if , then for all ,

The proof appears in Appendix D. The key idea is to reduce the problem into a question in geometric probability: whether a randomly rotated line segment is far away from all non-zero lattice points.

Lemma 6

Assume the setup of Lemma 5, with , , . Suppose that . With probability :

3.4 Concluding the analysis

So far, we have shown that is small with high probability. To deduce that their largest eigenvectors are close as well (using eigenvector perturbation results), we first need to show that the spectral gap of is large. We prove the following in Appendix E:

Lemma 7

There are universal such that for ,

Consequently, .

Acknowledgements

This work was supported in part by ISF under Grant 1791/17 and in part by the GENESIS Consortium via the Israel Ministry of Economy and Industry. The work of Elad Romanov was supported in part by an Einstein-Kaye fellowship from the Hebrew University of Jerusalem.

References

- [Artstein-Avidan et al., 2015] Artstein-Avidan, S., Giannopoulos, A., and Milman, V. D. (2015). Asymptotic geometric analysis, Part I, volume 202. American Mathematical Soc.

- [Baik et al., 2005] Baik, J., Arous, G. B., and Péché, S. (2005). Phase transition of the largest eigenvalue for nonnull complex sample covariance matrices. The Annals of Probability, 33(5):1643–1697.

- [Bhandari and Krahmer, 2019] Bhandari, A. and Krahmer, F. (2019). On identifiability in unlimited sampling. In 2019 13th International conference on Sampling Theory and Applications (SampTA), pages 1–4.

- [Bhandari et al., 2021] Bhandari, A., Krahmer, F., and Poskitt, T. (2021). Unlimited sampling from theory to practice: Fourier-prony recovery and prototype adc. arXiv preprint arXiv:2105.05818.

- [Bhandari et al., 2017] Bhandari, A., Krahmer, F., and Raskar, R. (2017). On unlimited sampling. In 2017 International Conference on Sampling Theory and Applications (SampTA), pages 31–35. IEEE.

- [Bhandari et al., 2018] Bhandari, A., Krahmer, F., and Raskar, R. (2018). Unlimited sampling of sparse sinusoidal mixtures. In 2018 IEEE International Symposium on Information Theory (ISIT), pages 336–340.

- [Bhandari et al., 2020] Bhandari, A., Krahmer, F., and Raskar, R. (2020). On unlimited sampling and reconstruction. IEEE Transactions on Signal Processing.

- [Boucheron et al., 2013] Boucheron, S., Lugosi, G., and Massart, P. (2013). Concentration inequalities: A nonasymptotic theory of independence. Oxford university press.

- [Cover and Thomas, 2012] Cover, T. M. and Thomas, J. A. (2012). Elements of Information Theory. John Wiley & Sons.

- [Domanovitz and Erez, 2017] Domanovitz, E. and Erez, U. (2017). Outage behavior of integer forcing with random unitary pre-processing. IEEE Transactions on Information Theory, 64(4):2774–2790.

- [Gersho and Gray, 2012] Gersho, A. and Gray, R. M. (2012). Vector quantization and signal compression, volume 159. Springer Science & Business Media.

- [Graf et al., 2019] Graf, O., Bhandari, A., and Krahmer, F. (2019). One-bit unlimited sampling. In ICASSP 2019 - 2019 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pages 5102–5106.

- [Johnstone, 2001] Johnstone, I. M. (2001). On the distribution of the largest eigenvalue in principal components analysis. Annals of statistics, pages 295–327.

- [Latała and Matlak, 2017] Latała, R. and Matlak, D. (2017). Royen’s proof of the gaussian correlation inequality. In Geometric aspects of functional analysis, pages 265–275. Springer.

- [Laurent and Massart, 2000] Laurent, B. and Massart, P. (2000). Adaptive estimation of a quadratic functional by model selection. Annals of Statistics, pages 1302–1338.

- [Lenstra et al., 1982] Lenstra, A. K., Lenstra, H. W., and Lovász, L. (1982). Factoring polynomials with rational coefficients. Mathematische annalen, 261(ARTICLE):515–534.

- [Ordentlich and Erez, 2017] Ordentlich, O. and Erez, U. (2017). Integer-forcing source coding. IEEE Transactions on Information Theory, 63(2):1253–1269.

- [Ordentlich et al., 2018] Ordentlich, O., Tabak, G., Hanumolu, P. K., Singer, A. C., and Wornell, G. W. (2018). A modulo-based architecture for analog-to-digital conversion. IEEE journal of selected topics in signal processing, 12(5):825–840.

- [Palombi et al., 2012] Palombi, F., Toti, S., and Filippini, R. (2012). Numerical reconstruction of the covariance matrix of a spherically truncated multinormal distribution. Journal of Probability and Statistics, 2017.

- [Paul, 2007] Paul, D. (2007). Asymptotics of sample eigenstructure for a large dimensional spiked covariance model. Statistica Sinica, pages 1617–1642.

- [Romanov and Ordentlich, 2019] Romanov, E. and Ordentlich, O. (2019). Above the Nyquist rate, modulo folding does not hurt. IEEE Signal Processing Letters, 26(8):1167–1171.

- [Romanov and Ordentlich, 2021] Romanov, E. and Ordentlich, O. (2021). Blind unwrapping of modulo reduced gaussian vectors: Recovering MSBs from LSBs. IEEE Transactions on Information Theory, 67(3):1897–1919.

- [Royen, 2014] Royen, T. (2014). A simple proof of the gaussian correlation conjecture extended to multivariate gamma distributions. Far East Journal of Theoretical Statistics, 48:139–145.

- [Tse and Viswanath, 2005] Tse, D. and Viswanath, P. (2005). Fundamentals of wireless communication. Cambridge university press.

- [Vershynin, 2018] Vershynin, R. (2018). High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press.

- [Wainwright, 2019] Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge University Press.

- [Weiss et al., 2021] Weiss, A., Huang, E., Ordentlich, O., and Wornell, G. W. (2021). Blind modulo analog-to-digital conversion. arXiv preprint arXiv:2108.08937.

- [Zamir, 2014] Zamir, R. (2014). Lattice Coding for Signals and Networks: A Structured Coding Approach to Quantization, Modulation, and Multiuser Information Theory. Cambridge University Press.

Appendix A Proof of Proposition 1, Item 1

Decompose along the principal components:

where . Then,

Now, observe that the cross terms, , are zero, since conditioning onto the ball preserves the symmetry . Thus,

and so the claim is proved.

Appendix B Proof of Proposition 2

For brevity, define

| (17) |

where is the MAP estimator of from ; in other words, is the success probability of the MAP estimator at SNR with spike direction . Recalling that the MAP estimator is optimal in the sense of error probability, it is clear that to prove Proposition 2, it suffices to show that implies that .

We start with a simple observation:

Lemma 8

The function is decreasing.

Proof. For any , denote and , and let be a deterministic function such that is the MAP estimator for . Fix any ; we shall now construct a suboptimal estimator for given , based on . The idea is simple: we generate known noise and set , which also equals . Note that . Considering the sub-optimal estimator for , we conclude,

Let us start by showing . By Lemma 8, the assumptions of Proposition 2 imply that . Now, it is easy to see that when , ; in this case, the problem simply decouples across the different coordinates. Thus,

and therefore for some universal . Clearly, then, for large , so by the standard estimate (for large ), we get hence .

It remains to show . To that end, we will use a simple geometric characterization of the MAP estimator, following [Romanov and Ordentlich, 2021]. Let

be the lattice generated by the matrix , and denote by the Voronoi cell of (that is, all points whose closest lattice point is ). By [Romanov and Ordentlich, 2021, Section III, Eq. (38)], the success probability of the MAP estimator is

Now, it is a well-known fact that is a convex symmetric set, with . Let be the effective radius of , defined by

( denotes the volume of the Euclidean unit ball). Recall that among all convex bodies with a given (finite) volume, a ball has the largest Gaussian measure. Thus,

Note that , which concentrates around with “typical” deviations of order (see, e.g., Lemma 17). This gives , so

where the last inequality follows from Stirling’s approximation: , and therefore .

Appendix C Proof of Lemma 4

Decompose along the principal components:

where is the projection along and is the orthogonal complement. Note that, while and are uncorrelated, they are not independent (as was the case without truncation, for a Gaussian vector) since we condition on . Also, recalling the “spiky” structure of ,

| (18) |

Condition on , and denote for convenience , so that are i.i.d. measurements from . Write

| (19) |

so that the error can be decomposed as , with

| (20) |

We first show that inherits the sub-Gaussian concentration properties of . We denote, respectively, the sub-Gaussian and sub-exponential norms by and . For a quick reminder on these norm (and Orlicz norms in general), see Definition 1 and Lemma 20.

Lemma 9

We have

and

Proof. Let be convex and increasing, and let be such that is convex. Observe that is convex, and consequently, by Lemma 3, , where is the Orlicz -norm (see Definition 1). Consequently,

Furthermore, using Lemma 20, Items 1 and 5,

This proves the first two bound. As for the last one,

where follows from Lemma 20, Item 2, and follows from Lemma 20, Item 1, and the first part of this proof.

We now bound the errors , again conditioned on :

Lemma 10

Assume that . Then, with probability ,

Proof. By the centralization Lemma (Lemma 20, Item 3) and Lemma 9,

By Bernstein’s inequality (Lemma 21),

Set . Then whenever , the probability is .

Lemma 11

With probability ,

Proof. Set , and observe that , since and are uncorrelated. We want to bound with high probability; to that end, we use a standard -net argument, executed in detail for the sake of completeness. Using [Vershynin, 2018, Corollary 4.2.13], fix a -net of of size . Let be a member of the net, such that . Now,

which implies . Consequently, , so it suffices to bound the latter. Recalling, by Lemma 9, that , by Bernstein’s inequality and a union bound over the net,

Set

so that the probability is bounded by .

Lemma 12

With probability ,

Proof of Lemma 4.

Appendix D Proof of Lemma 5

The core of the argument is this: we reduce the question of whether is large to a geometric question; specifically, whether a randomly rotated line segment is close to any non-zero lattice point. The details proceed as follow.

Recall: the pair is bad when but . Our goal is to show that for most directions , the probability that is bad is small, specifically,

We start by constraining ourselves to a set of “typical” vectors . As in Eq. (2), write, , for independent , . Let be a confidence parameter (we shall set later), and consider the event

| (21) |

where is such that , and are as in Eq. (10). Clearly, .

Operating under , let us bound the event by another, larger, event. To start, note that implies that for some non-zero lattice vector . Consequently, when , implies that . Decomposing , this further implies that

| (22) |

As for the condition , equivalently , it follows from the triangle inequality that

| (23) |

Let be the set of incoherent directions,

| (24) |

with a universal constant such that for (see Lemma 18). Now, under , and assuming that , Eqs. (22) and (23) imply that

| (25) |

where we set

| (26) |

Henceforth, we shall assume to be large enough so that . Consider the line segment, ,

| (27) |

Observe that under , the occurrence of the event in Eq. (25) implies, in particular, that

Note that given , this is a deterministic geometric condition. Set

| (28) |

and

| (29) |

Summarizing the preceding discussion, we have argued that whenever , the event already implies that are good. Thus, for ,

| (30) |

The proof of Lemma 5 will follow from the following auxiliary result:

Lemma 13

Fix a constant and set . There is a universal constant , such that if then, for ,

Lemma 13 is purely a result in geometric probability. It states the following: take the 1D line segment , and rotate it uniformly in space (apply a random rotation ). Then with high probability, the rotated segment will end up far away from all non-zero lattice points. The remainder of this section is devoted to proving Lemma 13.

Let us discretize the interval into disjoint sub-intervals of maximal length, such that the length of a sub-interval is ; let be the corresponding end-points, and note that we may take . Clearly, any point in must be -close to some point in . In particular, implies that for some . Consequently,

| (31) |

Since , each term of Eq. (31) is, by definition,

where denotes the surface area. Note that, one the one hand,

where denotes the boundary of a set, and follows from the well-known fact that for convex bodies , ; see, e.g., [Artstein-Avidan et al., 2015, Theorem B.1.14]. On the other hand, clearly, whenever . Setting

| (32) |

we conclude that

| (33) |

Lemma 14

We have

where is the volume of the -dimensional unit ball.

Proof. This is an essentially standard packing argument, made slightly more complicated (when is large) since we are considering intersections against a sphere rather than a ball. For radii , denote the (closed) annulus by

Observe that implies666 denotes the positive part of , namely, . , so

Next, we use the following packing argument: the sets are disjoint, so that if then . Therefore, by a volume comparison,

Set and , so that

The second term is non-zero if and only if ; the claimed bound follows from the inequality .

We now conclude the proof of Lemma 13. Recall, by Eq. (31), that our goal is to bound , where is bounded in Eq. (33). We treat separately small and large terms in the sum.

-

•

Small terms: -s such that . Note that there are such terms. Bound

(recall and the definition of in Eq. (27)). Assuming

(34) we have

Plugging into Eq. (33) and Lemma 14,

for some universal . Recalling again that there are such terms, and that, by definition (Eq. (26)),

(35) the total sum of the small terms is

where, for the second inequality, we used . Consequently, whenever

the sum is exponentially decaying in , and in particular . Again, recalling Eq. (35), the following condition on is sufficient to get exponential decay:

(36) -

•

Large terms: such that . Note that there are such terms (recall the definition of in Eq. (27)). Bounding , we estimate, using and assuming condition (34),

so that, using Eq. (33),

Again, since there are such terms, the total contribution is

where, for the second inequality, we again used . This is exponentially decreasing in whenever

(37)

Appendix E Proof of Lemma 7

Recall the choice of from Eq. (11). Decompose, rather arbitrarily, , so that for some . Note that if , then for some . Following Proposition 1 Eq. (7),

Clearly, , therefore,

where holds since this is the product of independent random variables. Furthermore, clearly,

Let , so that, finally,

| (38) |

We continue case-by-case, depending on the magnitude of :

-

(i)

Suppose that , where is a sufficiently small constant. Since has an exponential tail and , there is some such that

therefore

for small enough , whenever is chosen sufficiently small compared to .

-

(ii)

Note that by [Palombi et al., 2012], increases with . Consequently, for all , (i) implies that . Now, suppose that , where is such that for all ,

Note that such indeed exists, since the above ratio as . Then

so that . Consequently, for some other .

-

(iii)

. Consider the function

so that

We are done if we show that the infimum is non-zero, and it clearly suffices to show that . To do this, recall that has a density supported on . Therefore, as ,

so that indeed as .

Appendix F Proof of Theorem 1

We shall use the following eigenvalue perturbation result [Wainwright, 2019, Theorem 8.5]:

Lemma 15

Let be positive semidefinite, with a positive spectral gap: . Let be its largest eigenvector. Suppose that is positive semidefinite with . Let be its maximal eigenvector, with the sign chosen such that (part of the claim is that the largest eigenspace of is 1-dimensional). Then

where is the projection onto the orthogonal complement of .

We apply Lemma 15 with and , using the error bounds developed so far. For brevity, denote

| (39) |

Lemma 16

Assume the setup of Lemma 5, with large, , and .

Assume either of the following conditions hold:

-

•

and .

-

•

and .

Then with probability , one has

Proof. We consider two cases:

- •

- •

Proof of Theorem 1.

We apply Lemma 15. Write, as before, , so . Using the decomposition Eq. (19), and recalling the notation in Eq. (20), we conclude that under the conditions of Lemma 16, with probability ,

Note that the term does not appear, since it corresponds to a components of the difference which is parallel to . Using Lemmas 6, 11 and 12, (Lemma 7), and , we conclude that the following holds with probability :

-

•

Suppose that and . Then

Note that the requirement may effectively be omitted from the statement of the Theorem. The reason is that a bound of the form , for any , is completely vacuous (since are unit vectors). As we are not keeping track of the exact constants, it suffices to note that the first term in the upper bound becomes meaningful only when .

-

•

Suppose that and . Then

The requirement is omitted from the statement of the Theorem, for the same reason as in the previous case.

Appendix G Proof of additional lemmas

In this section, we provide several short proofs, that were omitted from the main text due to space constraints.

G.1 Proof of Lemma 2

Upper bound: ; clearly, implies , so .

Lower bound: Writing , the event implies . Thus,

where follows since these are independent events.

G.2 Proof of Lemma 3

By the Gaussian correlation inequality [Royen, 2014, Latała and Matlak, 2017], for quasiconcave777 is quasiconcave if for all . Note that: (i) A concave function is quasiconcave; (ii) The indicator function of a convex set is quasiconcave (but not concave)., and one of whom symmetric, . Consequently, for convex, . The Lemma follows by taking .

G.3 Proof of Lemma 6

Appendix H Auxiliary technical lemmas

The following are tail bounds for some norms of a Gaussian random vector:

Lemma 17

Let . Then

-

(i)

:

-

(ii)

:

Proof. (i) is the well-known inequality of Laurent and Massart [Laurent and Massart, 2000, Lemma 1]. (ii) is a special case of the Borell-TIS inequality; alternatively, it follows from the Gaussian Lipschitz concentration inequality, e.g. [Boucheron et al., 2013, Theorem 5.6], with the elementary bound .

The following is an immediate corollary:

Lemma 18 ( bound for a uniform vector in )

Suppose that . There are absolute constants such that

Next is Chernoff’s inequality for Bernoulli random variables [Vershynin, 2018, Theorem 2.3.1, Exercise 2.3.2]:

Lemma 19 (Chernoff’s inequality)

Let be independent Bernoulli random variables. Set and . Then for all ,

In particular, there are some absolute constants such that

We recall some properties of the sub-Gaussian and sub-exponential norms. The following is taken from [Vershynin, 2018, Chapter 2]:

Definition 1 (Orlicz norm)

Let be convex, strictly increasing such that

For a random variable , define its -Orlicz norm by

| (40) |

For a random vector , its -Orlicz norm is .

It is not hard to show that is indeed a norm. The choices

correspond to the sub-Gaussian and sub-exponential norms respectively. is sub-Gaussian (resp. sub-exponential) in the “usual” sense if and only if (resp. ); see [Vershynin, 2018, Chapter 2] for more background. We briefly mention some properties of these norms that are used in the paper:

Lemma 20

The following holds:

-

1.

.

-

2.

( do not need to be independent).

-

3.

Centralization lemma: for .

-

4.

For independent : , for some universal.

-

5.

Hoeffding’s lemma: for a bounded random variable, .

The following is Bernstein’s inequality for sums of independent sub-exponential random variables [Vershynin, 2018, Theorem 2.8.1]:

Lemma 21 (Bernstein’s inequality)

Let be independent and sub-exponential. Set . Then for all ,

where is an absolute constant.

Lastly, we cite a concentration inequality for sample covariance matrices with sub-Gaussian measurements [Vershynin, 2018, Theorem 4.6.1]:

Lemma 22

Let be independent, centered and sub-Gaussian. Denote .

Let be the sample covariance. There is such that with probability at least ,

(Note that in [Vershynin, 2018, Theorem 4.6.1], the result is stated for isotropic vectors, meaning . However, the proof goes through, verbatim, also without this assumption.)