Feel-Good Thompson Sampling for Contextual Bandits and Reinforcement Learning

Abstract

Thompson Sampling has been widely used for contextual bandit problems due to the flexibility of its modeling power. However, a general theory for this class of methods in the frequentist setting is still lacking. In this paper, we present a theoretical analysis of Thompson Sampling, with a focus on frequentist regret bounds. In this setting, we show that the standard Thompson Sampling is not aggressive enough in exploring new actions, leading to suboptimality in some pessimistic situations. A simple modification called Feel-Good Thompson Sampling, which favors high reward models more aggressively than the standard Thompson Sampling, is proposed to remedy this problem. We show that the theoretical framework can be used to derive Bayesian regret bounds for standard Thompson Sampling, and frequentist regret bounds for Feel-Good Thompson Sampling. It is shown that in both cases, we can reduce the bandit regret problem to online least squares regression estimation. For the frequentist analysis, the online least squares regression bound can be directly obtained using online aggregation techniques which have been well studied. The resulting bandit regret bound matches the minimax lower bound in the finite action case. Moreover, the analysis can be generalized to handle a class of linearly embeddable contextual bandit problems (which generalizes the popular linear contextual bandit model). The obtained result again matches the minimax lower bound. Finally we illustrate that the analysis can be extended to handle some MDP problems.

1 Introduction

This paper considers the contextual bandit problem [23] as well as its generalization to contextual reinforcement learning [20]. The contextual bandit problem can be regarded as a repeated game between a player (bandit algorithm) and an adversary as follows: at time

-

•

The player observes a context from the adversary;

-

•

The player picks an action ;

-

•

The player observes a reward .

We assume that is the set of allowable actions for context . We also assume that the reward is stochastic which depends only on , and

| (1) |

where is an unknown action value function. However, we allow an adversarial opponent who may pick based on the game history

at any time . Our goal is to maximize the expected reward

where the expectation is with respect to the internal randomization of the algorithm and the randomness in observations. The maximum expected reward at is

The quality of a bandit algorithm is measured by its (frequentist) regret

In the theoretical analysis of contextual bandits, the goal is to obtain regret bounds.

A particularly important class of algorithms for contextual bandits is Thompson Sampling [34], which has been widely used in practice with good empirical performance. However, there is a lack of general frequentist regret analysis for this class of algorithms. In the analysis of Thompson Sampling, one often considers another type of regret bound called Bayesian regret. If we assume that for some that is drawn from a prior distribution , the Bayesian regret is the averaged frequentist regret over the prior:

In this paper we develop a theoretical framework to analyze Thompson Sampling for contextual bandits. The framework introduces a decoupling coefficient technique to the reduce regret analysis for Thompson Sampling into an online least squares estimation problem, which is in a style similar to [16]. We show this conversion can be done both for Bayesian regret analysis and for frequentist regret analysis. For frequentist regret, we further show that an additional exploration term called Feel-Good is needed, which favors models that are optimistic historically. With this added exploration term, we can employ standard online aggregation techniques to obtain bounds for the least squares estimation problem. Moreover, it is shown that the analysis can be extended to some settings in reinforcement learning. Our theoretical framework provides a simple mathematical framework to analyze Thompson Sampling.

2 Related Work

The contextual bandit problem can be regarded as a generalization of multi-armed bandit with side information [23]. It has many practical applications such as online advertising, recommendation systems and mobile health [26, 4, 33]. Due to its wide range of applications, there is significant effort in developing algorithms and theoretical analysis for contextual bandit problems.

In general, contextual bandit algorithms can be characterized into policy based and value based methods. Policy based methods include EXP4 [11], and empirical classification minimization based methods such as epoch greedy [23], and [15]. However, they are computationally inefficient for large problems because solving classification problems can be computationally costly. Moreover, it is often difficult to generalize such policy algorithms to handle infinite number of actions.

Related to policy based algorithms are value based methods such as various methods for linear bandits [13, 26, 1], which depend on the concept of upper confidence bound (UCB) [10]. This class of methods involve the solution of linear regression, and can handle infinitely many actions. More recently, it was observed that least squares regression oracles (rather than classification oracles) can be used to derive bandit algorithms for finite actions [16, 32], and the resulting bounds match the optimal minimax bounds in [5] for finite function family. While certain infinite action spaces can also be handled [17], either the resulting algorithm requires complex optimization for each test data, or the required structure is more restrictive than the linear bandit model of [13]. The proof technique is different from UCB, and employs a policy randomization trick of [2] for the derived policy, together with smart variance controls that depend on the regression oracles. Unfortunately, as noted by the authors of [16], their analysis based on policy randomization is difficult to extend to the reinforcement learning setting.

A very popular class of algorithms for contextual bandits is Thompson Sampling [34], which has been observed to perform well empirically [12, 28]. This class of algorithms can be regarded as value based, but it employs a different mechanism than UCB to perform exploration. Thompson Sampling often performs better than UCB empirically and there are many existing posterior approximation techniques developed by the Bayesian community that can be used to sample from the posterior. However, its theoretical analysis is rather limited. Although near optimal results are known for non-contextual multi-armed bandits [7], it is unclear how well the method works for the general case. In fact, even for linear bandits, the results are not optimal [8]. It is also not known whether Thompson Sampling can achieve the optimal worst case frequentist regret bound for the general contextual bandit problem considered in [16], although some related results are known for Bayesian regret which averages over a known prior distribution [30].

This paper tries to resolve this open problem. We derive a decoupling technique which allows us to turn the regret analysis of Thompson Sampling into online least squares regression bound analysis, in a style motivated by [16]. It is shown that it is possible to establish a unified analysis of both Bayesian regret and frequentist regret for Thompson Sampling. For Bayesian regret bounds, the standard Thompson Sampling algorithm is sufficient. However, for frequentist regret bounds, we show that the standard Thompson Sampling leads to a suboptimal worst case regret bound. To remedy this problem, we introduce an additional term called Feel-Good exploration that encourages optimistic exploration in Thompson Sampling. We show that with this modification, a frequentist regret bound comparable to that of [16] can be obtained for the case of finite function classes with finite action space. The analysis using the Feel-Good exploration term leads to an exploration mechanism that is different both from UCB and from the policy randomization trick considered by [16]. We note that Thompson Sampling randomizes over value functions (with deterministic greedy policy) instead of over policies as in [16] and EXP4. This allows us to generalize the analysis easily to deal with infinite action spaces and reinforcement learning.

For the case of infinite action space, we introduce a new contextual bandit model called linearly embeddable bandits, which directly generalizes linear bandits. The model allows a context dependent non-linear embedding of the linear weights, and we show that regret bounds can be obtained for general nonlinear parametric families of embeddings, which match the regret bounds of [13] for linear bandits. This improves some earlier frequentist regret bounds for Thompson Sampling, which had a suboptimal dependency on the dimensionality [8, 3], to the optimal dependency , matching those of linear UCB style methods [13, 1]. Note that Bayesian regret bounds with dependency can be obtained for linear bandits [30, 31].

It is also possible to apply the idea of Feel-Good term and its proof technique to the contextual reinforcement learning problem, which is a model studied in [20, 14]. The regret bound we obtain is similar to that of [21] for linear Markov Decision Process (MDP). For simplicity, in this work, we only consider the case that MDP transitions are deterministic, which were investigated by some earlier work [14], and leave the more general case to future work. We note that related regret bounds have been derived for Thompson Sampling for the tabular MDP case [9], and for the related method of randomized least squares value iteration [29, 38, 6]. However, our results are are different, and allows contextually dependent nonlinear embeddings of linear MDPs in an adversarial setting.

It is also worth pointing out the general analysis presented in this paper has its limitations, especially when it is applied to bandit problems with special structures. For example, even for the simple case of multi-armed structured bandit problem [25], regret bounds from this paper may be suboptimal. The same suboptimality is also present for analysis such as [16], which focused on the general nonlinear contextual bandits, but failed to obtain bound of the form for dimensional linear bandits with arms. That is, the special structure of linear bandits are not fully utilized in the nonlinear analysis of [16] and the analysis of the current paper. Similarly, results obtained in this paper do not yield optimal bounds for some other structured bandit problems such as latent bandits [27, 19].

3 Thompson Sampling

In Thompson Sampling, we consider a parameter space , a prior and a reward likelihood with negative log-likelihood

Each is associated with a function , which is an approximation of the true value function . Note that in the Bayesian regret analysis, we assume that the prior and likelihood are both correct, and for some drawn from the prior . In the frequentist regret analysis, we do not assume that either prior or the likelihood is correct.

We also define the induced action , and the value function at according to as follows:

| (2) |

In the Bayesian formulation, and assume that the prior is correctly specified, we can regard the posterior as

| (3) |

The Thompson Sampling algorithm does the following at each time step

-

•

draw ;

-

•

take action .

The resulting algorithm is presented in Algorithm 1.

The distribution of can be obtained by integrating out as:

| (4) |

where is the indicator function. Therefore Thompson Sampling is equivalent to sampling according to (4).

3.1 Suboptimality of Frequentist Regret for Thompson Sampling

In standard Thompson Sampling, a natural choice is to pick the likelihood as

| (5) |

for some appropriate . In the Bayesian setting, this corresponds to a stochastic Gaussian likelihood reward model with variance . Theoretically, the benefit of using a Gaussian model is that its concentration and anti-concentration properties are well understood, which are useful for regret analysis. However, in the frequentist setting, this likelihood model can also be used for non-Gaussian reward problems because we do not assume that the Bayesian model is correct.

To understand the behavior of Thompson Sampling, we are particularly interested in the case considered in [16], which showed the following. Assume that the function class contains members, and . Moreover, assume that the action space is finite with , then there exists a contextual bandit algorithm which achieves a frequentist regret bound of

after steps. This matches the lower bound in [5]. It is natural to ask whether similar bounds can be obtained for Thompson Sampling in the frequentist setting.

In the following, we show that the standard implementation of Thompson Sampling in (5) leads to suboptimal regret in the worst case, which motivates the Feel-Good Thompson Sampling method introduced in this paper.

We consider two actions , and a function class with members . Moreover, we assume that is the correct reward model:

Assume further that for all :

Let be the uniform distribution on , so that each has a probability of at the beginning.

Proposition 1.

Given any , we have the following lower bound on regret for standard Thompson Sampling of (5)

Proof.

At the first step , without any information, we pick with with probability . This means that we will choose the greedy policy in Thompson sampling associated with when . Since for all , we have no information to differentiate any , and thus the posterior remains uniform over . This can only change when we choose at some time . It follows that the probability of sampling with for all is . Each takes the suboptimal action , and suffers a regret of . We thus obtain the desired bound. ∎

The result implies that at time , we have a frequentist regret bound of , which is linear in . It follows that the frequentist regret of standard Thompson Sampling is suboptimal, compared to the regret bound of achieved in [16].

3.2 Feel-Good Thompson Sampling

To overcome the difficulty of the standard Thompson Sampling, we propose the addition of an exploration term by favoring with larger . Specifically, we take

| (6) |

for some constant in the Thompson Sampling algorithm, where is a tuning parameter. The Standard Thompson Sampling in (5) is equivalent to the case of .

The additional exploration term encourages the method to choose a model with a large maximum reward on historic observations. Such a choice favors a model with a large historic maximum reward, which are model parameters that feel good based on the history. This term can be regarded as a data dependent exploration term, which we call Feel-Good exploration, and the resulting Thompson Sampling algorithm is referred to as Feel-Good Thompson Sampling.

In the example we presented, where the standard Thompson Sampling method is suboptimal, we note that the Feel-Good sampling formulation will favor the choice of . This is because is a larger reward than alternatives by a constant margin. A simple calculation suggests that with , we will choose the optimal after time steps. This leads to a regret of . The example also suggests that it is better to choose large in the beginning, and let it decay to . This can lead to regret for this example. However, for simplicity, we do not consider the method of time-varying in the theoretical analysis of this paper.

This observation implies that the standard Thompson sampling method is not aggressive enough in selecting optimistic models, and the additional Feel-Good prior remedies the problem. The resulting Feel-Good Thompson Sampling method may be regarded as an implementation of the general optimism in the face of uncertainty principle, and the Feel-Good prior can be regarded as an analogy of upper confidence bound (UCB) for posterior sampling methods. As we will show, this optimism will lead to a provably good regret bound for the general situation which matches (and generalizes) the result of [16]. Similarly a direct application of linear bandit bounds in [13, 1] to multi-armed bandits also leads to suboptimal regret, because it does not consider the special structure. It is worth pointing out that for the general contextual bandit problem consider here, the randomized least squares approach considered in [29] does not lead to sufficient exploration either. This because a perturbation of historic data does not remedy the flat posterior problem in the example of Section 3.1.

Computationally, with the addition of the Feel-Good exploration term, one has to reply on approximate MCMC inference methods to sample from the posterior distribution. While Section 6 shows that this can be done in practice, we note that for some simple problems, the standard Thompson Sampling may take advantage of distribution conjugacy, with closed form posterior distribution that is easier to sample. For complex problems where approximate MCMC inference methods are needed, the difference may not be significant.

4 Theoretical Analysis

This section derives a general regret bound for the Feel-Good Thompson Sampling method. For simplicity, we make the following boundedness assumption on the reward.

Assumption 1.

The reward is sub-Gaussian:

Moreover, we assume that for all and : .

Note that if we assume that the observed reward , then Assumption 1 holds. This is the situation we are mostly interested in. The sub-Gaussian assumption also holds with Gaussian noise of variance no more than , which is needed to analyze Bayesian regret with Gaussian likelihood.

Our analysis follows the basic technique of online aggregation methods, such as [35, 22, 18]. This technique was used in the analysis of Bayesian model averaging [37], which is closely related to Thompson Sampling (with the only difference of averaging over instead of sampling from the posterior distribution). It was also employed in the analysis of EXP4 bandit algorithm [11], which can be regarded as the partial information counterpart of its full information analog Hedge in [18]. Note that both Hedge and EXP4 sample from the posterior, and thus their theoretical analysis is related to ours. However, unlike Thompson Sampling considered in this paper, both Hedge and EXP4 employed exponents that are not continuous. Therefore they are difficult to implement efficiently. In comparison, MCMC methods such as SGLD [36] can be employed for Feel-Good Thompson Sampling, as demonstrated in Section 6.

In order to analyze Thompson Sampling, we have to introduce new ideas in addition to online aggregation. Define for , the truncated function value

Observe that . The starting point of our analysis is the following decomposition of the regret at time as

| (7) |

On the right hand side, the first term is often referred to as the Bellman error in the reinforcement learning literature, which needs to be controlled. The second term is the Feel-Good exploration term.

The key technique to control the term is based on the decoupling of the Thompson sampling action choice from . We introduce the following definition, which can be used to control the first term, and can be used to quantify the complexity of exploration in Thompson Sampling. The key motivation of this definition is to convert the Bellman error with respect to the action taken by the current policy (no exploration) to least squares error with independently sampled actions (in such case the exploration is automatically achieved by independent sampling). It plays the same role as what UCB does in the traditional bandit analysis. Conceptually the definition is also related to the idea of information ratio studied by [30, 24], which may be regarded as another way to handle exploration.

Definition 1 (Decoupling Coefficient).

Let be a contextual bandit with value function . Given any , , and , we define as the smallest quantity so that for all probability distributions on , and the induced random policy on , the following inequality holds

In this paper, we only consider decoupling coefficient that is independent of . More generally, we may also allow to depend on . Using (4), we obtain the following inequality for all :

| (8) | ||||

| where |

Note that on the left hand side, the action depends on , but on the right hand side, and are drawn independently from their respective posterior distributions. Armed with (8), we can bound the regret for Thompson Sampling by least squares loss as follows.

| (9) |

The term can be bounded using the standard techniques in the analysis of online aggregation algorithms. The following lemma shows that is upper bounded by the number of actions, which corresponds to the situation considered in [16].

Lemma 1.

Assume that for some . Then for any , .

Proof.

Consider any , , and . For any , let . We have

where follows from the algebraic inequality , and follows from the definition of . By summing over , we obtain

This leads to the desired inequality in Definition 1. ∎

We can now obtain the following general Bayesian regret bound for the standard Thompson Sampling as follows.

Proposition 2.

Proof.

We note that in the Bayesian setting, all are realizable. This implies that , and . Moreover, the marginal of , averaged over , is . Therefore in (9),

Since the model is correct, we know that with for all , , and . We thus have

By summing over to , and then optimizing over on the right hand side, we obtain the desired bound. ∎

The result implies that we can essentially obtain a Bayesian regret bound for Thompson Sampling from Bayesian online least squares regression bound, and such a result is analogous to [16]. For frequentist regret, both and can be further bounded using online aggregation techniques. This leads to the following result, which is a special case of Theorem 2.

Theorem 1.

In Theorem 1, the least squares regression loss is further bounded by the log partition function. As we will show in Section 5, the latter can be easily estimated for various problems. While it is possible to establish a similar bound for the cumulative least square regret loss in Proposition 2 in various cases, the proof technique will be more involved. This is because in the frequentist setting, we are allowed to use a small , and apply techniques from online aggregation, while in the Bayesian setting, we have to set , where is the variance of the reward. This learning rate is not sufficiently small to use online aggregation techniques. Therefore more specialized analysis is needed. Since this paper focuses on the simpler online aggregation technique for bounding the least squares loss, we will not derive bounds for Bayesian least squares regression. Nevertheless, the analogy of Proposition 2 and Theorem 1 demonstrates the fact that the Feel-Good exploration is not needed in the Bayesian regret analysis, although it is crucial in the frequentist regret analysis.

We can further extend the analysis to handle certain infinite action spaces with the following linearly embeddable contextual bandit model

| (10) |

where and are known functions. This model is a generalization of contextual bandits with finite actions, and contextual bandits with linear payoff functions. The key of this model is the separation of parameter and action , so that possibly infinite number of actions can all be embedded into a -dimensional linear space. The definition also resembles the definition of Bellman factorization and Bellman rank in [20] for contextual MDPs. However, the definition of Bellman rank in [20], when applied to contextual bandits, leads to an embedding dimension of , and it does not handle infinite actions directly. In comparison, the modified factorization in (10) may be regarded as a context and action dependent version of the Bellman factorization, and hence we may refer to its embedding dimension as the context-action dependent Bellman rank for contextual bandits.

The following result generalizes Lemma 1 for linearly embeddable contextual bandits. The proof can be found in Appendix B.

Lemma 2.

Assume that (10) holds. For any . If for all , , and , then .

Note that the result assumes that for all . In some cases, this condition holds. However, in the general case of potentially misspecified prior, this condition may not hold for all . Since we know the true reward , it is possible to check this condition in the Thompson Sampling algorithm, and force the posterior to be the set that satisfies the condition. In such case, we may consider the following generalized posterior:

| (11) |

where may depend on both and . In order to apply Lemma 2, we are particularly interested in the choice of

| (12) |

Note that (11) becomes (3) when . Therefore we can focus on the generalized Thompson Sampling algorithm, with of (3) replaced by (11) in the theoretical analysis. In practice, we may only need to use the standard choice of (3) instead of the more complex (11). In fact it might be possible that the condition can be relaxed with a more careful analysis (for example, this condition is not required in Lemma 1). If this is the case, then (11) is not necessary.

Theorem 2.

Theorem 2 holds for contextual bandits with linearly embeddable payoffs in (10), which allows infinitely many arms. With defined in (12), we obtain from Lemma 2

We may pick and in Theorem 2. This implies the following bound

| (13) |

Note that since is a constant (ignoring logarithmic factor) for parametric models, one can set to obtain a regret. Some detailed examples are presented below.

5 Examples

We assume that the optimal value function can be well approximated within . That is, there is so that the model is nearly correctly specified in that

| (14) |

for some small .

5.1 Finite function class

We set , , and

for some . From (14), with some algebraic manipulations, we know that

Moreover, we have for all and .

Assume we have , with prior on each function. Since , we know that

We obtain from (13) that

5.2 Parametric Function Class

We assume that (10) holds with , and assume that we have a prior on with density function . We again take and take .

Assume that both and are Lipschitz around . There exists a constant so that for a sufficiently large , if we let , then :

We obtain from (14) that for all ,

It follows that for all , , and thus .

Moreover, we have for all :

Note that the sub-Gaussian noise condition in Assumption 1 implies that , therefore

This implies that

Now by setting

for some , we obtain the following result:

Consider the Gaussian prior case with

and . We obtain a regret bound of bound of

By choosing , we obtain a bound

For linear bandits, where we have and , the bound becomes

which matches that of [13, 1], and thus is not improvable. In comparison, ignoring logarithmic terms, the previous results for standard Thompson Sampling in [8, 3] led to a frequentist regret bound of , which is inferior to what we obtain here for Feel-Good Thompson Sampling.

6 Simulation Study

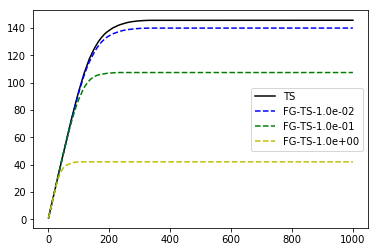

We use a numerical example to show that the algorithm considered in this paper can be implemented using standard MCMC sampling techniques. Moreover under appropriate conditions, Feel-Good Thompson Sampling can indeed lead to better regret than standard Thompson Sampling. This verifies the theoretical analysis. In this example, we consider a simple non-contextual linear bandit problem, with . Let be the optimal parameter, be the optimal arm, and with and . We consider Gaussian prior with . If we draw from this prior, , which is consistent with the fact that . For each , the observation is generated by adding a uniform random noise from to . We implemented Feel-Good Thompson Sampling algorithm with , where corresponds to the standard Thompson Sampling. We set in this example, which appears to be an appropriate choice for this problem. For simplicity, we set in (6), and run the experiments for times. We then plot the average regret versus time in Figure 1. It shows that for this example, there is a benefit of using the Feel-Good exploration.

Our implementation of the Feel-Good Thompson Sampling method employs stochastic gradient Langevin dynamics (SGLD) [36]. At each time step , we select a data point uniformly at random, and use the following stochastic gradient update rule:

with . Here we run random SGLD updates at each time , with a fixed learning rate .

7 Generalization to Reinforcement Learning

We consider a simple extension of our analysis to contextual episodic Markov decision process (MDP) with unknown but deterministic transitions, denoted by . Similar contextual MDP models were also studied recently in [20, 14]. Here and are state and action spaces. The number is the length of each episode. and are the state transition probability measures and the random rewards. In this work, we assume that the transition probability is deterministic (but unknown), and leave the general case to future work.

The player interacts with this contextual episodic MDP as follows. In each episode ,

-

•

A context is picked arbitrarily by an adversary.

-

•

At each step

-

–

The player observes the state

-

–

The player picks a valid action (we allow a subset of actions in to be valid for each state in )

-

–

The player receives a random reward

-

–

The player reaches a new state deterministically.

-

–

-

•

The episode terminates after steps.

The goal of MDP is to optimize the expected cumulative rewards:

It is known that the optimal policy can be derived from the function of the MDP, which is denoted by at step (). It satisfies the Bellman’s equation:

where at each state with action , we observe reward and transit to state deterministically. For simplicity, we assume that . We also use the convention

The regret of an MDP algorithm at each time step is defined as:

Consider a set of function classes , and for each , . For notation simplicity, we assume that , and in order to simplify the notations, we do not introduce a parameter into the function definition. Moreover, we assume that contains the information of so that we can recover from . This can always be made possible by concatenating and regard the result as .

We can also define

and we can introduce the Bellman operator :

where is the observed reward at , and is the next state.

7.1 Thompson Sampling

Consider one episode with context , and sequence which is appropriated generated. To apply Thompson Sampling, we define for and for :

and we let

Here is the data dependent Feel-Good exploration prior term, which encourages high quality exploration for reinforcement learning. We note that we do not have to incorporate for because denotes the overall value function of the model, and thus is sufficient for our purpose.

Let the history . At episode , we define the posterior of as

| (15) |

Given drawn from the posterior, the Thompson Sampling method employs the associated greedy policy as: at step and state , we pick an action that maximizes the value according to the model

| (16) |

This policy, conditioned on the context , induces a distribution on , which we denote as

The Thompson Sampling algorithm for RL is given in Algorithm 2.

7.2 Regret Analysis

We have the following assumption.

Assumption 2 (Realizability).

Assume that .

The following assumption extends (10) for contextual bandits. It is a relatively strong assumption, but similar assumptions were also required in related works such as [20, 21].

Assumption 3.

A contextual MDP is linearly embeddable, if given any context , and , we have the following representation for :

| (17) |

where .

This decomposition can be regarded as a context and action dependent version of the Bellman factorization and Bellman rank in [20], and our definition can naturally handle infinite action spaces. The linearly embeddable condition generalizes the linear MDP model of [21], where we allow contextually dependent weights that can be a nonlinear function with unknown embedding to be learned. For simplicity, in the analysis, we will avoid dealing with range conditions for RL by imposing the following conditions directly. Alternatively, we may also employ the truncation technique used in our bandit analysis to handle out of range function values.

Assumption 4.

We assume that there exists so that for all :

Moreover, we assume that for all :

Next, we will use the following key observation, referred to as the value-function error decomposition in [20]. Given any and . Let be the trajectory of the greedy policy , we have

| (18) |

where

With the above decomposition, we may introduce the decoupling coefficient for MDP below, which generalizes Definition 1 for contextual bandits. For simplicity, we only consider the case of in Definition 1.

Definition 2 (Decoupling Coefficient).

Consider a contextual MDP . Given any on . Let

Then is the smallest quantity so that for all :

Using Definition 2, we can obtain the following regret bound from (18):

| (19) |

where

Note that (19) is an analogy of (9). The following lemma is a generalization of Lemma 2 for contextual bandits. The proof is essentially the same.

Lemma 3.

Assume that the linear embedding in Assumption 3 holds for the contextual MDP . Then .

Using the above definition, we can use the same proof technique as that of contextual bandits to obtain a regret bound for reinforcement learning. The proof is given in the appendix.

Theorem 3.

To interpret the regret bound, we note that if and we take , then the bound becomes

For dimensional parametric function class, then, similar to Section 5.2, we have

where is the true value function. By taking

we obtain

which is similar to the contextual bandit case, and similar to results of [21] for linear MDPs.

8 Conclusion

This paper presents a general analysis of Thompson Sampling. Contrary to the conventional thinking that the random sampling of Thompson Sampling leads to sufficient exploration, we showed that the standard choice of likelihood function in Thompson Sampling can be suboptimal due to the lack of aggressiveness to encourage optimistic exploration. To remedy this problem, we proposed a modification of Thompson Sampling with an additional Feel-Good exploration term. The resulting method can be viewed as an implementation of the general optimism in the face of uncertainty principle for Thompson Sampling. It was shown that this method led to minimax optimal regret bound for the general contextual bandit problem with finite actions. Moreover, we extended the analysis to handle infinite actions when the action space is linearly embeddable, with regret bound matching known lower bounds.

We also demonstrated that this new theoretical framework for Thompson Sampling can be extended to the reinforcement learning setting. Our analysis of Feel-Good exploration employs a new proof technique using decoupling coefficient to handle exploration. It reduces the online regret bound analysis into an online least squares estimation problem, which in spirit is similar to [16]. We then bound the online least squares loss using aggregation techniques. In comparison, the technique of [16] cannot be directly generalized to handle reinforcement learning, as noted by the authors there. While this paper considers the simple case of unknown deterministic transition dynamics for reinforcement learning, more general situation with random transitions can also be handled. We leave detailed studies to future work.

As pointed out in Section 2, bounds obtained in this paper may not be optimal for certain structured bandit problems. It will be interesting to explore whether such structures can be incorporated into our analysis to improve the resulting bounds.

Appendix A Proof of Theorem 2

.

We use the following estimate, which directly follows from the sub-Gaussian definition of noise.

Lemma 4.

Consider defined in (6). If , then

Proof.

Now using (21), we obtain:

Therefore

| (22) |

The last inequality follows from , which follows from the Hölder’s inequality.

The following lemma is standard in the analysis of online aggregation methods.

Lemma 5.

We have

Proof.

Define

then

Let . It follows from that

We have

In the above derivation, used the Jensen’s inequality and the concavity of ; used Lemma 4. This proves the lemma. ∎

Appendix B Proof of Lemma 2

First, we prove the case with . Consider any , , and . Define

Let () be an orthonormal basis of eigenvectors of . It follows that

| (24) | ||||

| (25) |

where used the fact that when , and we let

| (26) |

We have

where the last inequality used Young’s inequality for products. We can obtain the following bound by using (26) to simplify the first term, and (25) to simply the second term.

This implies the desired inequality in Definition 1 with .

For finite , we consider any , . We define

where

Let

Then , and . We have

where the first inequality is due to Lemma 2 with applied to . This proves the desired result.

Appendix C Proof of Theorem 3

Lemma 6.

If , then

Proof.

Let be the noise, and

be the Bellman residual.

Since , we obtain from Chernoff bound that

Since for : after some algebraic manipulations, we can get

we have for :

| (27) |

Since given , is a deterministic sequence of , and the only randomness is from , it follows that

where in the above derivation, we have applied (27) with in , (27) with in , and so on…

It follows that

| (28) |

where the last inequality is due to the Jensen’s inequality applied to as a convex function of .

The following lemma is similar to Lemma 5. The proof is identical.

Lemma 7.

Consider defined in (20). We have

Acknowledgment

The author would like to thank Christoph Dann for discussions about related works.

References

- [1] Yasin Abbasi-Yadkori, Dávid Pál, and Csaba Szepesvári. Improved algorithms for linear stochastic bandits. In NIPS, volume 11, pages 2312–2320, 2011.

- [2] Naoki Abe and Philip M Long. Associative reinforcement learning using linear probabilistic concepts. In ICML, pages 3–11. Citeseer, 1999.

- [3] Marc Abeille and Alessandro Lazaric. Improved regret bounds for thompson sampling in linear quadratic control problems. In International Conference on Machine Learning, pages 1–9. PMLR, 2018.

- [4] Alekh Agarwal, Sarah Bird, Markus Cozowicz, Luong Hoang, John Langford, Stephen Lee, Jiaji Li, Dan Melamed, Gal Oshri, Oswaldo Ribas, et al. Making contextual decisions with low technical debt. arXiv preprint arXiv:1606.03966, 2016.

- [5] Alekh Agarwal, Miroslav Dudík, Satyen Kale, John Langford, and Robert Schapire. Contextual bandit learning with predictable rewards. In Artificial Intelligence and Statistics, pages 19–26. PMLR, 2012.

- [6] Priyank Agrawal, Jinglin Chen, and Nan Jiang. Improved worst-case regret bounds for randomized least-squares value iteration. arXiv preprint arXiv:2010.12163, 2020.

- [7] Shipra Agrawal and Navin Goyal. Further optimal regret bounds for Thompson sampling. In Artificial intelligence and statistics, pages 99–107, 2013.

- [8] Shipra Agrawal and Navin Goyal. Thompson sampling for contextual bandits with linear payoffs. In International Conference on Machine Learning, pages 127–135, 2013.

- [9] Shipra Agrawal and Randy Jia. Optimistic posterior sampling for reinforcement learning: worst-case regret bounds. In Advances in Neural Information Processing Systems, volume 30, 2017.

- [10] Peter Auer. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research, 3(Nov):397–422, 2002.

- [11] Peter Auer, Nicolo Cesa-Bianchi, Yoav Freund, and Robert E Schapire. The nonstochastic multiarmed bandit problem. SIAM journal on computing, 32(1):48–77, 2002.

- [12] Olivier Chapelle and Lihong Li. An empirical evaluation of Thompson sampling. Advances in neural information processing systems, 24:2249–2257, 2011.

- [13] Varsha Dani, Thomas P Hayes, and Sham M Kakade. Stochastic linear optimization under bandit feedback. In COLT, 2008.

- [14] Christoph Dann, Nan Jiang, Akshay Krishnamurthy, Alekh Agarwal, John Langford, and Robert E Schapire. On oracle-efficient PAC RL with rich observations. In Advances in Neural Information Processing Systems, volume 31, 2018.

- [15] Miroslav Dudik, Daniel Hsu, Satyen Kale, Nikos Karampatziakis, John Langford, Lev Reyzin, and Tong Zhang. Efficient optimal learning for contextual bandits. In UAI, 2011.

- [16] Dylan Foster and Alexander Rakhlin. Beyond ucb: Optimal and efficient contextual bandits with regression oracles. In International Conference on Machine Learning, pages 3199–3210. PMLR, 2020.

- [17] Dylan J Foster, Claudio Gentile, Mehryar Mohri, and Julian Zimmert. Adapting to misspecification in contextual bandits. Advances in Neural Information Processing Systems, 33, 2020.

- [18] Yoav Freund and Robert E Schapire. A decision-theoretic generalization of on-line learning and an application to boosting. Journal of computer and system sciences, 55(1):119–139, 1997.

- [19] Joey Hong, Branislav Kveton, Manzil Zaheer, Yinlam Chow, Amr Ahmed, and Craig Boutilier. Latent bandits revisited. arXiv preprint arXiv:2006.08714, 2020.

- [20] Nan Jiang, Akshay Krishnamurthy, Alekh Agarwal, John Langford, and Robert E Schapire. Contextual decision processes with low Bellman rank are PAC-learnable. In International Conference on Machine Learning, pages 1704–1713. PMLR, 2017.

- [21] Chi Jin, Zhuoran Yang, Zhaoran Wang, and Michael I Jordan. Provably efficient reinforcement learning with linear function approximation. In Conference on Learning Theory, pages 2137–2143. PMLR, 2020.

- [22] Jyrki Kivinen and Manfred K Warmuth. Averaging expert predictions. In European Conference on Computational Learning Theory, pages 153–167. Springer, 1999.

- [23] John Langford and Tong Zhang. Epoch-greedy algorithm for multi-armed bandits with side information. Advances in Neural Information Processing Systems (NIPS 2007), 20:1, 2007.

- [24] Tor Lattimore and Andras Gyorgy. Mirror descent and the information ratio. In Conference on Learning Theory, pages 2965–2992. PMLR, 2021.

- [25] Tor Lattimore and Rémi Munos. Bounded regret for finite-armed structured bandits. Advances in Neural Information Processing Systems, 27:550–558, 2014.

- [26] Lihong Li, Wei Chu, John Langford, and Robert E Schapire. A contextual-bandit approach to personalized news article recommendation. In Proceedings of the 19th international conference on World wide web, pages 661–670, 2010.

- [27] Odalric-Ambrym Maillard and Shie Mannor. Latent bandits. In International Conference on Machine Learning, pages 136–144, 2014.

- [28] Ian Osband and Benjamin Van Roy. Why is posterior sampling better than optimism for reinforcement learning? In Doina Precup and Yee Whye Teh, editors, Proceedings of the 34th International Conference on Machine Learning, volume 70, pages 2701–2710. PMLR, 2017.

- [29] Ian Osband, Benjamin Van Roy, Daniel J Russo, and Zheng Wen. Deep exploration via randomized value functions. Journal of Machine Learning Research, 20(124):1–62, 2019.

- [30] Daniel Russo and Benjamin Van Roy. Learning to optimize via posterior sampling. Mathematics of Operations Research, 39(4):1221–1243, 2014.

- [31] Daniel Russo and Benjamin Van Roy. An information-theoretic analysis of Thompson sampling. The Journal of Machine Learning Research, 17(1):2442–2471, 2016.

- [32] David Simchi-Levi and Yunzong Xu. Bypassing the monster: A faster and simpler optimal algorithm for contextual bandits under realizability. Available at SSRN, 2020.

- [33] Ambuj Tewari and Susan A Murphy. From ads to interventions: Contextual bandits in mobile health. In Mobile Health, pages 495–517. Springer, 2017.

- [34] William R Thompson. On the likelihood that one unknown probability exceeds another in view of the evidence of two samples. Biometrika, 25(3/4):285–294, 1933.

- [35] Volodya Vovk. Competitive on-line statistics. International Statistical Review, 69(2):213–248, 2001.

- [36] Max Welling and Yee W Teh. Bayesian learning via stochastic gradient Langevin dynamics. In Proceedings of the 28th international conference on machine learning (ICML-11), pages 681–688, 2011.

- [37] Yuhong Yang and Andrew Barron. Information-theoretic determination of minimax rates of convergence. Annals of Statistics, pages 1564–1599, 1999.

- [38] Andrea Zanette, David Brandfonbrener, Emma Brunskill, Matteo Pirotta, and Alessandro Lazaric. Frequentist regret bounds for randomized least-squares value iteration. In International Conference on Artificial Intelligence and Statistics, pages 1954–1964. PMLR, 2020.