Inference on the maximal rank of

time-varying covariance matrices

using high-frequency data

Abstract

We study the rank of the instantaneous or spot covariance matrix of a multidimensional continuous semi-martingale . Given high-frequency observations , , we test the null hypothesis for all against local alternatives where the average st eigenvalue is larger than some signal detection rate .

A major problem is that the inherent averaging in local covariance statistics produces a bias that distorts the rank statistics. We show that the bias depends on the regularity and a spectral gap of . We establish explicit matrix perturbation and concentration results that provide non-asymptotic uniform critical values and optimal signal detection rates . This leads to a rank estimation method via sequential testing. For a class of stochastic volatility models, we determine data-driven critical values via normed p-variations of estimated local covariance matrices. The methods are illustrated by simulations and an application to high-frequency data of U.S. government bonds.

keywords:

[class=MSC2020]keywords:

and

1 Introduction

Consider a continuous-time -valued process with instantaneous or spot covariance matrix We address the problem of testing and estimating the maximal rank of on , using discrete observations , . These high-frequency observations allow for inference without specific modeling assumptions on .

In econometrics, the maximal rank may be the number of risk factors involved in financial asset prices or the dimension of the state space of a continuous-time factor model. See Jacod & Podolskij, (2013) for a discussion of market completeness and Aït-Sahalia & Xiu, (2017) who provide a link between continuous-time factor models and principal component analysis (PCA). is well defined if is modeled by an -semi-martingale. As discussed below, the basic case is given by a Brownian martingale

| (1.1) |

with an -dimensional standard Brownian motion , and . For deterministic , we aim at inferring the rank of , , from the observed independent increments

| (1.2) |

This formulation poses a fundamental problem in nonparametric statistics, whose analysis will turn out to be non-standard.

A natural statistic for the integrated covariance on a block for some small with is the local empirical (realized) covariance matrix

| (1.3) |

The realized covariance matrix estimates the average covariance matrix

| (1.4) |

with an error of size . The average can have full rank even though holds for all . The potential inflation in the rank is a consequence of averaging spot covariance matrices with time-varying eigenspaces. We highlight the theoretical and empirical relevance of such time-varying features in deterministic and stochastic volatility models as well as financial data. This confirms Jacod et al., (2008) who state that gives no insight on the rank of . We show, however, while the st eigenvalue may be non-zero, it is still small for small block sizes when varies smoothly. Precise perturbation bounds for matrix averages indicate that the maximal size of does not only depend on the regularity of , but also significantly on the existence of a spectral gap . Small eigenvalues across blocks should favour the acceptance of the null hypothesis, while large values should lead to a rejection. This paper develops such a test with specific attention to the block size and to non-asymptotic critical values. At an abstract level a classical bias-variance dilemma seems to dictate the choice of the block size in (1.3).

By studying the null hypothesis for all versus the alternative for some , we embed our rank test into a signal detection framework. In particular, we allow for local alternatives where has average size at least where the signal strength tends to zero as . In contrast to simple consistency results under a fixed alternative, this approach not only reveals the approximate deviations from if the test accepts, but also allows to establish the minimax optimal signal detection rate in the sense of Ingster & Suslina, (2012). This rate is attained by considering the average of the empirical eigenvalues over all blocks and choosing a block size of order . The bias-variance dilemma disappears at the level of rates because of the heteroskedastic error of , which is natural for variance-type estimators, and the small size of under the null. The heteroskedasticity in combination with the bias bound also explains the surprisingly fast detection rate compared to the classical estimation rates and for the spot covariance and the integrated covariance , respectively.

For standard stochastic volatility models with regularity the rank detection rate is , opposed to the rates and for the spot covariance and integrated covariance estimation, see e.g. Fan & Wang, (2008). Compared to classical signal detection the roles of hypothesis and alternative are in a certain sense reversed. We shall understand this by an underlying concave functional instead of a convex constraint for classical regression, see e.g. Juditsky & Nemirovski, (2002) for the interplay between regularity and convexity constraints.

The critical values of our tests depend on a regularity bound for the covariance matrix function under the null hypothesis. This may be available from previous observations or other side information, but with models for at hand also data-driven critical values are feasible. We present an approach assuming a semi-martingale model for itself. The regularity in a Besov scale is , while the corresponding constant (similar to a Besov or Hölder norm) can be estimated by a -variation of norms of empirical covariance matrix increments. This setting is similar to the scalar case in Vetter, (2015), who estimates the volatility of volatility, but it involves non-differentiable matrix norms. A feasible central limit theorem permits a data-driven calibration of critical values under stochastic volatility and yields asymptotically the correct size.

On the technical side we need to control the sum of empirical eigenvalues over blocks . in (1.3) is a convex combination of independent Wishart matrices with different population covariance matrices. To obtain non-asymptotic and uniform critical values, we refine general matrix Bernstein inequalities by Tropp, (2012) and use Gaussian concentration. For the power analysis the standard lower-tail inequalities do not apply. Instead, we determine the specific eigenvalue density by establishing a stochastic domination property with respect to a fixed population covariance and use an entropy argument. Simple approaches are not feasible because the different population covariance matrices do not commute and are not sufficiently close to each other. Beyond the purposes of this paper, these results might find some independent interest.

Our method can be extended to cover idiosyncratic components, where we observe a process satisfying

| (1.5) |

with an independent -dimensional Brownian motion , and spot covariances such that . Our methods directly translate to cases where a small upper bound for is known, which gives a desirable robustness property. This provides a link to the wide class of factor models. In contrast to classical factor models for volatility (Li et al.,, 2016; Aït-Sahalia & Xiu,, 2017), we allow the eigenspaces of (factor loading spaces) to vary over time.

Estimating and testing the rank of a covariance matrix has attracted a lot of attention under different angles. The case where the covariance in (1.2) is constant (or more generally has constant null space in time) is usually trivial because the rank of the empirical covariance matrix equals the rank of as soon as . Observing , , with constant and in (1.5) leads to a spiked covariance model (Johnstone,, 2001). In this i.i.d. framework and for high dimensions Onatski et al., (2014) develop asymptotic tests on the presence of spikes and Cai et al., (2015) establish optimal rates for rank detection. In these works the spectral gap plays the role of a signal strength, while in our setting it controls the perturbations due to averaging and leads to different exponents in the detection rate. We focus on the effect of time-varying covariances and do not study additional dimension asymptotics or nuclear norm penalisations as e.g. in Christensen et al., (2021). Nevertheless, our non-asymptotic results show the dependence on the dimension and the rank explicitly. Time-varying covariances appear naturally in time series analysis. Inference on their rank, however, requires much more specific modeling assumptions on the discrete-time dynamics of . We refer to Lam & Yao, (2012) for an analysis in a stationary high-dimensional framework, to Su & Wang, (2017) for a local PCA approach to testing constant factor loadings over time and generally to the references therein for many further aspects.

The setting in our paper is close to that of Jacod & Podolskij, (2013), who consider rank estimation and testing problems in a joint semi-martingale setup for and . They establish stable central limit theorems with convergence rate for statistics that involve an additional randomisation step. Since the integer-valued rank is their target, there is no clear concept of convergence rates or local alternatives as in our signal detection framework. While they treat general joint semi-martingale models, we focus on the pathwise properties of in terms of regularity and spectral gap. Aït-Sahalia & Xiu, (2017) detect the rank of the integrated covariance matrix in a sparse high-dimensional setting and apply this to determine the number of factors given constant factor loading spaces. More recently, Aït-Sahalia & Xiu, (2019) argue that the rank of the spot covariance matrix is often much more informative and provide empirical evidence based on the S&P 100 index. They develop an asymptotic theory for the so-called realised eigenvalues and more general spectral functions, but they focus on the case of covariance matrices with full rank. An inspiring characterisation of the realised eigenvalue is given by Jacod et al., (2008) as a natural distance to all semi-martingales with spot covariance matrix of rank at most .

In Section 2 we introduce the test statistics and discuss in theory and examples the impact of averaging on the eigenvalue perturbation. Our data example refers to U.S. government bonds and the term structure of interest rates. The main results are presented in Section 3. This includes the analysis of the tests under null hypothesis and local alternatives, the derivation of the optimal signal detection rate as well as properties of a corresponding rank estimation method. Section 4 studies the specific case of stochastic volatility models and provides data-driven critical values based on a matrix norm -variation. These techniques are applied to inference on the rank in the bond data. Mathematical tools and more technical proofs are delegated to the appendix. Some of the matrix deviation and concentration results there are stated in wider generality because they might prove useful in other circumstances as well.

2 Setting, examples and first results

Let us first fix some notation. We write or if for some constant and all . By we mean and . With and we denote random variables (also matrix-valued) such that remain bounded in probability and tend to zero in probability, respectively. Similarly, stands for random variables with . For two random variables with the same law we write .

The canonical basis in is denoted by , is an elementary matrix and denotes the identity matrix in . We introduce the sets of matrices

For the partial order says that . For we consider the ordered eigenvalues (according to their multiplicities). For matrices the Hilbert-Schmidt (or Frobenius) scalar product is and the spectral norm is given by .

We split the interval into blocks for some block length with and . On each block we consider the empirical or realised covariance from (1.3) and its mean in (1.4). Assuming model (1.1) for with deterministic or independent , we obtain from (1.2) (conditionally on )

| (2.1) |

where we follow Magnus & Neudecker, (1979) and vectorize matrices by , employ the Kronecker product for matrices and use the matrix for . If the process in (1.5) is observed, the corresponding covariance matrices in terms of are denoted by and . In this section we focus on .

We aim at a level- test for the null hypothesis of the form

| (2.2) |

Observe that the number of observations on each block should be at least because otherwise holds. The choice of the block size and of the critical value requires a deeper understanding of eigenvalue deviations under averaging and stochastic errors.

The following is an easy consequence of the variational characterisation of eigenvalues, see e.g. Tao, (2012, Proposition 1.3.4).

2.1 Lemma.

The remaining partial trace map is concave for and . In particular, the remaining partial trace of an average is larger than the average over the remaining partial trace:

| (2.3) |

Consequently, holds.

While Lemma 2.1 shows that averaging can only increase the rank, we want to understand how large can become if holds for all . Three examples are discussed before we state a precise perturbation bound. The first bivariate example shows the eigenvalue perturbation by rotating eigenvectors under Hölder regularity. For we use the matrix-valued -Hölder ball of radius

The impact of a spectral gap is clearly exposed.

2.2 Example.

Let , , and consider

Then and hold for all . We have for (use ). The average , however, has rank 2 with

Note by the assumption on . For the spectral gap has order and we obtain , which seems a natural deviation from for -Hölder continuous . Yet, a spectral gap of order , i.e. , yields a much smaller quadratic deviation from zero.

In the extreme case , PCA on the integrated covariance matrix for would result in explained (population) variance by the second component although the spot covariances are all of rank one.

The size of the eigenvalue perturbation in Example 2.2 is also attained in typical stochastic volatility models, which shows that this is not only a worst case scenario.

2.3 Example.

Stochastic volatility models are often based on -dimensional Wishart processes (Bru,, 1991), compare the matrix square Ornstein-Uhlenbeck and affine processes. The Wishart process of dimension and index is given by , with an -dimensional Brownian matrix (i.e., the entries form independent Brownian motions). For general deterministic initial value , is the initial state of . The Wishart process forms a matrix-valued Itô semi-martingale, satisfying the stochastic differential equation

with a -Brownian matrix , . A matrix square Ornstein-Uhlenbeck process, for example, satisfies the same equation, but with a more general drift term for some back-driving parameter . On short time intervals, the drift term will become negligible so that the Wishart process serves as a fundamental example.

For and an initialisation with the Wishart process has by definition rank at most . Yet, the average has almost surely full rank with an st eigenvalue of size for small .

It is straight-forward to derive these properties in the case , , , with a planar Brownian motion starting in the origin. Then

holds, implying . By Brownian scaling we see the equality in law

and that the second eigenvalue is of size . The spectral gap in is and the Hölder regularity is almost , in line with the order from Example 2.2.

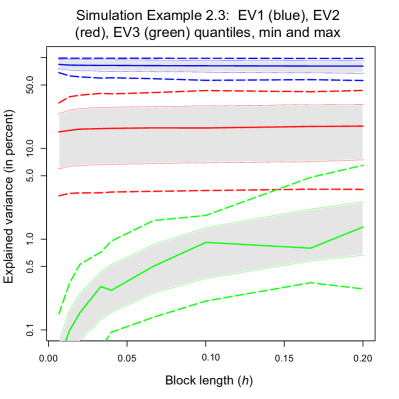

For , , and varying Figure 1(left) shows statistics of the relative explained variance of component

| (2.4) |

on a logarithmic scale in 1000 Monte-Carlo simulations. Starting values of the two non-zero eigenvalues are 1 and 0.5. The range between the 10% and 90% quantiles for each is indicated by the gray-shaded areas. The simulation round that provides the median, min and max percentage for are given by the central solid and the two dashed lines. In relative terms the third eigenvalue (green) increases up to a maximal value of 5% and a median of around 1% if covariance matrices are estimated over blocks of length , even though the third spot eigenvalues are all zero, which is attained in the limit .

2.4 Example.

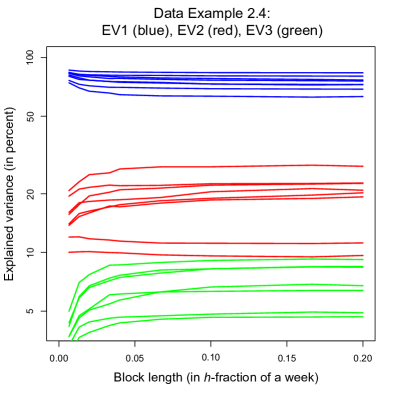

The popular Nelson & Siegel, (1987) model of the term structure of interest rates assumes a rank 2 covariance matrix across bonds of different maturities. The related two components are commonly known as level and slope factors and play an important role in asset pricing, risk management and macro-finance applications. Often larger models are proposed like the extension to three factors in Diebold & Li, (2006). We analyse U.S. government bond Exchange Traded Funds (ETFs): the iShares treasury of 3-7 years (IEI), 7-10 years (IEF) and 10-20 years (TLH). The data is obtained from the Nasdaq through the data provider LOBSTER and includes one-minute data (6.5 trading hours per day) for the first 27 weeks in 2020. Using jump-truncated one-minute log returns over one week intervals (), Figure 1(right) shows for seven selected weeks how the averaging of covariance matrices affects the explained variances (2.4) of the components. The third eigenvalue (, green) that explains usually much less than 5% of the total variance on blocks with 13 minutes length () becomes seemingly more important for larger blocks. Compared with daily data analysis (390 minutes, ), the magnitude roughly doubles. We come back to the bond example in Section 4, where Figure 3 illustrates the significant dynamics of the empirical eigenvectors.

As a first step towards deriving the critical values in (2.2), we provide a general bound for eigenvalues of averages over low-rank matrices. The proof in Appendix A.1 is inspired by the techniques in Reiß & Wahl, (2020).

2.5 Proposition.

Let be an interval of length . Consider with and for . Then

holds with the -variations of on

2.6 Remark.

As the proof reveals, asymptotically for and fixed , the quadratic bound becomes since . This provides smaller asymptotic critical values.

Notice that the bound of Proposition 2.5 is quadratic in case of a positive spectral gap , which will later allow the detection of weaker signals (smaller eigenvalues). For -Hölder-continuous , we have and we obtain the order in Example 2.2:

The bound in terms of an integrated variation criterion allows to weaken the Hölder regularity to an -Besov regularity. This is important to cover stochastic volatility models as in Example 2.3 or in Section 4 below.

3 General results

3.1 Behaviour under the null hypothesis

Let us recall the definitions of Besov spaces , see Cohen, (2003) for a nice survey. For let

with the usual modification for , denote its -modulus of continuity. Then

denotes the -seminorm of and the space consists of all functions with . For Hölder-continuous , we have for any and . By the results for Brownian motion (Ciesielski et al.,, 1993) and bounded variation functions (Cohen,, 2003), any (even discontinuous) Itô semi-martingale with bounded characteristics is almost surely an element of for any (but not for !).

3.1 Definition.

Throughout, we consider the null hypothesis that the spot covariance has at most rank . Moreover, we assume a -regularity condition for , , a level of idiosyncratic covariance and potentially a spectral gap . We set

The role of the parameters is evident and can be seen by the inclusion for , , and . Sometimes we write for to denote the law of model (1.5) with from the null hypothesis.

3.2 Corollary.

For with maximal rank on we have

For the population version of the test statistics in (2.2) this gives

Proof.

Apply Proposition 2.5 with , to bound . Without assuming a spectral gap deduce

for . The spectral gap case follows by the same arguments in terms of . ∎

We are now prepared to derive critical values for the test under the null hypotheses without and with a spectral gap. We use the more general setting of observing the process and trace back the result for directly by setting .

3.3 Theorem.

Proof.

This follows from Proposition A.11 below with . Just note and collect terms. ∎

The critical values provide uniform and non-asymptotic test levels. They clearly lead to conservative tests because the numerical values are derived from less precise upper bounds. Still, the main structure is clearly discernible: the factors or result from the population version in Corollary 3.2, adapted to , while a term of order is added to bound the expected values . The random fluctuations depend on the total sample size and give rise to the factor . Under a Hölder instead of Besov condition in , we can use in Proposition A.11. In this case, the factor in the term involving can be replaced by and the factor in the term involving can be replaced by .

We shall see below that the power of the tests is the larger the smaller the critical values are. This relation holds almost independently of the block size . In view of we can thus distinguish two main cases of idiosyncratic noise. For ( in the spectral gap case), we can choose and is asymptotically of order (, respectively). Whereas otherwise we can select a larger so that the term of order becomes negligible and holds.

The choice of the critical value is based on prior knowledge of the regularity of and the size of . Moreover, the limiting law of the test statistics is in general degenerate (deterministic) under . For specific models like the stochastic volatility model in Section 4, data-driven critical values can be established involving quantiles from additional estimation errors.

3.2 Power and optimal detection rate

The power analysis shows that the test for any choice of critical values is uniformly consistent as over local alternatives whose st eigenvalues are larger than these critical values. In other words, the st eigenvalues of may tend to zero and the tests will still detect them (with asymptotic power one), provided they remain larger than the critical values. This way we establish what is known as a separation rate between null and alternative in nonparametrics or as a detection rate in signal processing and learning. Moreover, we establish optimality in the sense that no test can distinguish null hypothesis and local alternatives with st eigenvalues converging faster to zero.

To define the alternatives formally, we would ideally like to consider covariances with for some detection rate . Due to the Riemann-type sum in the tests , however, we have to use a slightly weaker metric to measure the deviation from zero of the st eigenvalue. We ask that a box with area can be placed between the graph of and the -axis, which excludes wild spiky deviations from zero. This may be interpreted as a weak -norm over intervals.

3.4 Definition.

For , , consider the set of alternatives

The supremum is taken over all intervals of length at least .

Remark that the alternative neither involves a -smoothness constraint nor a spectral gap condition.

3.5 Theorem.

Consider for sample size the tests from (2.2) in terms of with block sizes and some critical values . Assume as and that the number of observations per block satisfies with the constant from Corollary A.9 below. Then is asymptotically consistent over the local alternatives provided and the rate is larger than a constant multiple of :

3.6 Remark.

The idiosyncratic process may be zero or non-zero under the alternative because of . In case , the consistency result can be shown to hold already for . In case it suffices to require only. The imposed lower bound on the number of observations per block is finite, but quite pessimistic (it grows exponentially in ). We were not able to establish the result under the minimal possible bound . Simulation results indicate in any case that a choice with of the order 10 produces stable results, see also Example 3.10 below.

Proof.

Consider with for and . For choose with for and . Then by and Lemma 2.1 there are at least blocks where

holds for all . Using this bound in Corollary A.9 below, we obtain with (by assumption) for any

We take and insert to arrive at

Because of the number of blocks tends to infinity and hence

follows for any . This is the assertion when setting , . ∎

The smaller , the smaller the order of the critical values in Theorem 3.3. The bound under the alternative merely requires for some sufficiently large constant . In conclusion we can choose minimal without losing asymptotic power. Remark in this case that even for constant the test statistic does not estimate , but rather the expected st eigenvalue of the corresponding Wishart distribution. This expected value grows in and thus suffices for inference. Combining Theorems 3.3 and 3.5, the tests with thus establish the following signal detection rate.

3.7 Corollary.

Given observations, there are tests of or , respectively, versus that have uniform level and are uniformly consistent over the alternatives for if and for some suitably large constant

The parameters and may vary arbitrarily with .

3.8 Remark.

If the pure Brownian martingale model (1.1) is generalised to the semi-martingale model

including a bounded adapted drift , then the increments of involve an additional term of order such that and the corresponding test statistics in (2.2) are perturbed by a bias term of order . In this case we should employ critical values larger than , that is choose appropriately, to remain robust against these perturbations or alternatively use a mean-corrected version of the blockwise covariance estimator .

In case is stochastic and dependent on the driving Brownian motion in an adapted way, a standard procedure would be to approximate by on and to work conditionally on the underlying filtration , where the covariance can then be treated as deterministic and constant. At a population level we would work with instead of . We expect that pursuing this idea we can at best achieve similar results to those without a spectral gap. A direct analysis of might yield better results, but would certainly require to develop different techniques.

That the above rates cannot be improved follows basically from Example 2.2. In Appendix A.4 the following non-asymptotic lower bound or rather non-identifiability result is established for the case .

3.9 Proposition.

Consider the model of observing in (1.1) at times , , and arbitrary parameters , , , as well as . Then there is no non-trivial test between and :

whenever .

We conclude that the optimal detection rate is indeed

whenever is smaller than . It is quite remarkable that this rate is so much faster than the estimation rate for the spot covariance matrix . A fundamental reason is, of course, the heteroskedasticity in the estimation error which becomes small in directions where is small. Compared to the -estimation rate for positive realised integrated eigenvalues, this provides a quantitative version of the super-efficiency around zero eigenvalues (Aït-Sahalia & Xiu,, 2019, Remark 3). It should be remarked that the case has been excluded because it leads to the completely degenerate model and thus under , which can be tested perfectly.

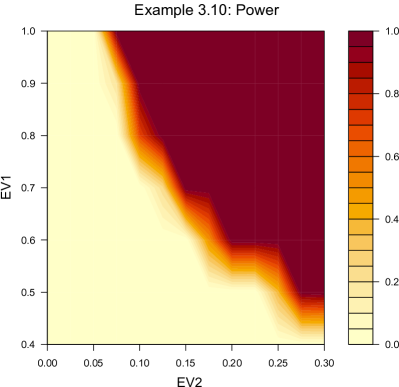

3.10 Example.

We generalise Example 2.2 with to illustrate the impact of the spectral gap and the magnitude of the second eigenvalue of the spot covariance matrix on the power and on the detection rate of the test. With and , we set . By orthogonality, and are both eigenvectors of with eigenvalues and for . By varying , we generate spot covariances under the alternative with different signal strengths .

The contour plot in Figure 2(left) displays the power, that is the probability that with from (2.2) rejects. We use the minimum of the critical values from Theorem 3.3, depending on the spectral gap . Warmer colours indicate a higher power, which is shown as a function of the average second eigenvalue (signal strength) on the -axis and the spectral gap on the -axis. We use observations in Monte Carlo iterations with . The power increases with the signal (average second eigenvalue) and with the spectral gap. The phase transition from almost zero to perfect power is very fast, especially for larger spectral gaps, in line with the mathematical analysis.

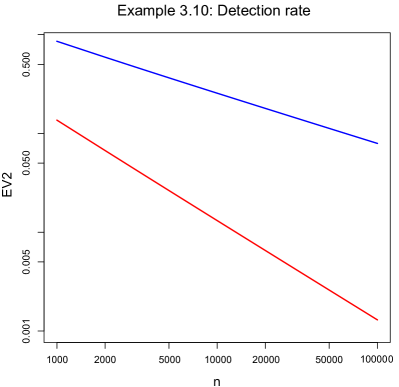

Figure 2(right) shows for the same example a log-log-plot of two signal detection rates as a function of the sample size . For the case of a spectral gap (, red) and without a spectral gap (blue) the value EV2 indicates the average second eigenvalue at which the test accepts and rejects with equal probability . This corresponds to the standard classification boundary in learning. Given the sharp phase transitions, compare Figure 2(left), the values of EV2 are almost perfectly given by the respective critical values in Theorem 3.3. Consequently, the power laws in the detection rate meet well the finite sample classification boundaries. We have chosen observations per block for each and calculated the power in Monte Carlo simulations for each case.

3.11 Remark.

Eigenvalue detection is intrinsically different from standard signal detection problems. When testing whether the regression function in nonparametric regression is zero versus local alternatives with , a smoothness or sparsity condition needs to be imposed in the alternative (Ingster & Suslina,, 2012). In our case, the smoothness condition appears under the null hypothesis , but not under the alternative. Moreover, we face a one-sided testing problem because always which is basically trivial in nonparametric regression. A major difference is, of course, that our null hypothesis is composite, allowing for a submanifold of covariance matrix functions .

There seems to be, however, also a deeper reason for the inversion of roles of and , which is the concavity of the -functional when expressing as and as (in a weak -norm over ). The concavity is inherent in the explanations for the examples in Section 2 as well as in several proofs. This should be compared with the convexity of the -norms and standard shape constraints in regression problems, compare the discussion in Juditsky & Nemirovski, (2002). From a scientific inference perspective the null hypothesis should always consider the simpler and less complex setting (Occam’s razor principle), which clearly justifies our approach even though the information geometry may favour the opposite.

3.3 A rank estimator

The rank test translates to an estimator of the rank . We denote by and the level- test for from (2.2) with critical value . A natural rank estimator uses the minimal rank bound that is accepted by sequential testing:

| (3.1) |

with suitable levels . Setting , this estimator can be rewritten in form of the optimisation problem

provided the critical values are non-decreasing in . Indeed, since subtracting the trace does not change the minimiser, we have

| (3.2) |

The summand on the right is almost surely strictly increasing in and must thus be negative for and be positive for . Hence,

follows.

Let us specify this for the tests from Theorem 3.3 without a spectral gap assumption. We fix a level and set

Then holds for all , but the difference is only in the second order term via the remaining dimension . This leads to the choice

| (3.3) |

3.12 Proposition.

Proof.

In the asymptotic setting, we have because of , . Hence, the definition of and Theorem 3.5 gives for some sufficiently large constant that

tends to zero. ∎

Our rank estimator strictly controls the probability of selecting a too large rank. If we assume , then the probability of choosing a too small rank for any fixed model tends to zero asymptotically because any continuous with lies in some for sufficiently small . The uniform control of Proposition 3.12 is much stronger than standard pointwise consistency results in the literature. For with sufficiently small we conjecture that even the joint error probability decays as fast as . Similar results can be obtained in the spectral gap case with the asymptotics .

Compared to the Bai & Ng, (2002) and Aït-Sahalia & Xiu, (2017) estimators, designed in a slightly different setting, we observe that an exact form of the penalty is provided by bounding the error of overestimating the rank by non-asymptotically. We believe that the approach (3.1) of determining by sequential testing is both, from a conceptual and a practical point of view, very attractive, while the optimisation formulation (3.3) allows a better comparison with other existing rank detection methods.

4 Stochastic volatility models

For certain stochastic volatility models we can access the bias bounds and for our test statistics by an estimation procedure. Assume that the covariance can be modeled by a continuous semi-martingale

| (4.1) |

satisfying the following assumptions, where denotes all linear maps between vector spaces and .

4.1 Assumption.

Fix . is a -dimensional Brownian motion, is an -bounded, adapted covariance drift and is an -bounded, adapted covariance diffusivity. To avoid clumsy vectorisations, we interpret as a matrix-valued integrator with linear combinations of the coordinates in each entry.

The regularity conditions , hold for all and some constants , , . All processes , and as well as the -measurable initial condition in are defined on the same filtered probability space as and . Moreover, and are independent. Model (4.1) enforces the symmetric matrix to be positive semidefinite for all .

In this section we consider only the case where we observe directly, i.e. and . In the case the subsequent approach will generally overestimate the -variations and lead to more conservative tests.

The first limit result shows that the bias bound from Corollary 3.2 can be expressed asymptotically by the normed p-variation

and the expectation is taken with respect to an independent random vector (in general, is thus random via ).

Proof.

Bounding the drift and using the regularity of we derive

Hence, taking conditional expectation and arguing for via Cauchy-Schwarz inequality with , we find

because the mapping is Lipschitz continuous so that with a uniform bound on we deduce . Moreover, we directly get uniformly in

We conclude by profiting from the martingale difference structure

Because of the total -approximation error is of order . ∎

We shall estimate on a coarser grid with block length . For scalar models it is known that estimators for the volatility of volatility have at best rate (Hoffmann,, 2002). If no subtle bias corrections are employed, the standard rate is (almost) , see Vetter, (2015) and the discussion therein. Since we cannot ensure differentiability of the matrix norm without further assumptions, we are content with a consistent estimator achieving at best the rate . To render the influence of the finite variation part in (4.1) sufficiently small, we use second differences. Techniques from discretisation of processes give the following central limit theorem, proved in Appendix A.5.

4.3 Theorem.

To obtain a feasible central limit theorem we need to estimate the variance term consistently. This can be accomplished using the -powers of norms as well as the product of -powers on adjacent blocks.

4.4 Proposition.

The last two results allow to replace the term , , in the critical values of Theorem 3.3 by plus a Gaussian quantile depending on the estimated variance of . For the lower order terms in the critical values of Theorem 3.3 become negligible and we obtain level- tests with quite simple data-driven critical values.

4.5 Corollary.

Proof.

By Proposition A.11 below (set , , with ), we have on the event

where we use and almost surely. Therefore Proposition 4.2 and yield on

By the Central Limit Theorem 4.3, the consistency results of Proposition 4.4 and Slutsky’s lemma we conclude

Another application of Slutsky’s lemma implies that

is at least . This gives the result for the test . ∎

In Fan & Wang, (2008, Theorem 2) it is shown that a standard kernel estimator of the spot covariance is consistent uniformly over . Moreover, the convergence rate up to log factors is derived together with a limiting distribution. Since the eigenvalue map is Lipschitz continuous (with respect to the spectral norm), the same uniform rate of convergence holds for such that

| (4.3) |

These properties can also be derived for our blockwise realised covariance matrix as an estimator of for when . This enables completely data-driven critical values also in the spectral gap case. The next result is proved in Appendix A.5.

4.6 Corollary.

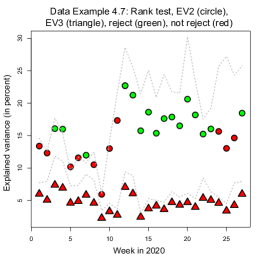

4.7 Example.

We apply the test with estimated critical values to the bond data already studied in Example 2.4 above. Choose the block length (26 minutes), that is 15 blocks per day and blocks per week. On those 75 blocks we calculate the test statistic (2.2) for and . Critical values are taken from Corollary 4.6 with estimators and taken on blocks of size (65 minutes). We use and choose .

Figure 3(left) displays the test results along with the explained variance for each of the first 27 weeks in 2020. Circles and triangles show the explained variances (2.4) for the second and third eigenvalues, respectively. The colours indicate whether the test accepts (red) or rejects (green) the hypothesis of rank 1 (circles) or rank 2 (triangles). We see that in some weeks rank 1 is accepted, while always a maximal rank 2 is accepted versus rank 3 alternatives. The dashed lines visualise the corresponding explained variances (2.4) when weekly integrated covariance matrices () are used. Notice that the time period includes the Corona pandemic and major disruptions of financial markets from March (week 10) onwards.

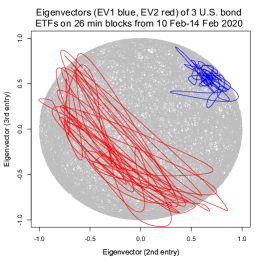

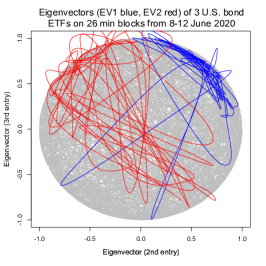

We highlight two specific weeks. We find that the test rejects rank 1 in week 7 (Feb. 10-14) but fails to reject in week 24 (June 8-12). Both weeks seem to exhibit with about 12% and 15% similarly large explained variance of a second principal component. Figure 3(center and right) reveal the source of the different test decisions by plotting the normalized (length one, first entry positive) first (blue) and second (red) eigenvectors of on the upper hemisphere of the unit ball. The movement of eigenvectors is much stronger in week 24 than in week 7. The larger the movements the larger are the calibrated critical value. In other words, faster dynamics may lead to a larger test statistics under the null, which is why rank 1 is not rejected in week 24. The example shows how periods of high (co)volatility coincide with periods of large movements in eigenvectors and how this can affect the inference on the rank.

Our data analysis does not give empirical evidence that the U.S. term structure for maturities between 3 and 20 years exceeds rank 2 in the first six months of 2020.

Appendix A Further results and proofs

A.1 Matrix deviation results

We provide explicit deviation bounds for eigenvalues under averaging.

Proof of Proposition 2.5.

Set and denote by the ordered eigenvalues (with multiplicities) of . The standard eigenvalue-norm bound implies for any

because of . In particular, it is smaller than the mean of over and we conclude by the convexity of the norm

Since for the minimum in the asserted inequality is attained at in view of , it remains to show under the assumption .

We use the spectral decomposition with the rank-one projections onto the eigenspaces of corresponding to . We apply the resolvent identity

assuming that is not an eigenvalue of , and obtain

Taking transposes, we also have and we can further expand

| (A.1) |

Therefore by functional calculus with we have for

We know by the first part and the assumption on . Hence, we conclude and is indeed not an eigenvalue of for any . By integrating over , the linear term vanishes and

Since and , we have and we can bound

Finally, use

as well as and to obtain the assertion. ∎

A.1 Proposition.

Proof.

Write . For (a) we argue by triangle inequality and :

For (b) we proceed as for the derivation of (A.1). For consider and use with the orthogonal projection onto the orthogonal complement of the kernel of and equivalently onto the range of . Then

Because of and we can bound . We expand and arrive at

To obtain (c), we integrate the previous bounds. From (a) and Proposition 2.5 we obtain by the convexity of the norm and Hölder’s inequality

where we bounded the integral over by the integral over in the last step. Bounding yields

This gives the assertion for because the minimum in the asserted bound is then attained at the first argument. Otherwise, holds by Proposition 2.5. Then the same arguments as before, but using part (b) give

The claim therefore follows with . ∎

A.2 Upper matrix concentration bounds

Concentration results for the maximal eigenvalue of sums over independent, but non-identically distributed Wishart matrices are established. We follow the proof of the matrix Bernstein inequalities in Tropp, (2012), but argue differently from the subexponential case there because we face non-commuting matrices.

A.2 Theorem.

Let , , be independent Gaussian random vectors for some . Let and

Then we have the upper tail bound

and the expectation bound

Proof.

Let us write and note , . We start with the master tail bound from the trace exponential (Tropp,, 2012, Theorem 3.6) and obtain

The function is increasing on and holds for , which is easily checked by a power series expansion. Functional calculus and then show

We use and to arrive at

Observe that is a rank-one matrix with non-zero eigenvalue and corresponding eigenprojector . By functional calculus we thus have

Writing in the basis of eigenvectors of , the coordinates are independent Gaussian -distributed, in particular holds for . This implies

For simple -density identities yield for

Using independence of the coordinates and this result for , we find for

We derive a simpler bound, using for and :

So far, we have thus established for

Inserting and applying for symmetric matrices , the upper tail bound follows.

The expectation bound follows from integrating

over . ∎

A.3 Remark.

It is easy to check that holds as usual for matrix Bernstein inequalities. In dimension the so far best known deviation bound by Laurent & Massart, (2000) is

We observe that we merely lose by a linear dependence of the constants in the dimension for the matrix concentration bound. We could argue as Laurent & Massart, (2000) and win in the constants for the isotropic case , but in general we face the problem that and do not commute.

We combine the matrix Bernstein inequality with a Gaussian concentration argument to obtain a subexponential deviation inequality for a triangular scheme of maximal eigenvalues.

A.4 Theorem.

Let , , , be independent Gaussian random vectors for some . Let

and . Then we have with probability at least for any

Proof.

The expectation bound of Theorem A.2 together with the inequality yields

We write with independent and use the Gaussian concentration (Ledoux & Talagrand,, 1991, Equation (1.6)) to deduce for that

is at most , where is the Lipschitz constant of the functional . defines a norm on so that

Taking squares and applying the Cauchy-Schwarz inequality for the expectation as well as for , we thus find with probability at least

It remains to insert the expectation bound and to set . ∎

A.3 Lower matrix concentration bounds

Lower tail bounds for the minimal eigenvalue are required to establish the asymptotic power of the tests under the alternative and need not be precise in the constants for our needs. They must, however, be tight in the sense that they prescribe correctly the probability for minimal eigenvalues approaching zero. The standard Chernoff bounds for bounded random matrices (Tropp,, 2012) or the concentration bounds for empirical covariance matrices (Koltchinskii & Mendelson,, 2015) still produce positive tail bounds at zero, which only for increasing sample size become negligible. We also need to cope with constant sample sizes on each block while averaging over an increasing number of blocks.

The proof is surprisingly intricate because the covariance matrices need not be jointly diagonalisable. First, we establish a stochastic dominance property for sums of Wishart matrices via explicit density calculations when each population covariance matrix is larger than a fixed covariance matrix. In a second step we use the entropy of the Grassmanian manifold to exhibit such a fixed covariance matrix for a fraction of all summands. We are not aware of any more direct argument. In particular, the number of summands required is pretty large and a tighter bound would certainly be desirable. Let us start with determining explicitly the eigenvalue density for sums of different Wishart matrices.

A.5 Lemma.

Let with and consider , a centred Gaussian matrix with and an invertible covariance matrix . Then the eigenvalues of have the joint Lebesgue density

with and in terms of the zero matrix . We write when integrating with respect to the normalised Haar measure on the orthogonal matrix group .

Proof.

Extending the density result by James, (1960) to the non-i.i.d. setting, we consider the random matrix with orthogonal transformations independent of . The idea is that and share the same eigenvalues. The Lebesgue density of is given by the Gaussian mixture

We have the singular-value decomposition with some orthogonal matrices , . Then is uniquely determined by and

holds for independent orthogonal matrices , because of the group invariance of Haar measure. Consequently, by Theorem 3.2.17 and the proof of Theorem 3.2.18 in Muirhead, (2009) the eigenvalues of have density

with constant . ∎

The preceding density together with a symmetrisation argument yields a stochastic dominance property for the smallest eigenvalue and an explicit bound on its Laplace transform.

A.6 Theorem.

Let , , be independent -dimensional Gaussian random vectors. Suppose that holds for with some . Then we have the stochastic order

where i.i.d. holds under . Moreover, we can bound the Laplace transform for any and by

A.7 Remark.

It seems intuitive that becomes smaller when the are replaced by . This does not follow directly, however, by a standard coupling argument.

Proof.

Note first that the result is trivial if is not invertible, that is . For we always have and the stochastic order is immediate. Henceforth, we therefore assume and .

For our symmetrisation argument let so that is the identity and flips the sign of the last coordinate. Then by the invariance for we can introduce a random sign flip with a Rademacher random variable in the density formula for of Lemma A.5 with to obtain

where is the th column of . Treating also the matrices and as random (under ), we may introduce the joint density

In the case for all we use such that the exponent

is independent of . Denoting by the density in terms of , the likelihood ratio can be written as

with some constant . Noting

the exponent is a quadratic form in . Since is positive semi-definite by assumption, we can write with some and . This shows that

is always increasing in . Hence, the likelihood ratio is increasing in . Integrating and for out, we thus deduce that is stochastically larger under than under , which is the stochastic order result.

In view of the stochastic order yields further for the Laplace transform with i.i.d.

Using the bound for the density of in the proof of Proposition 5.1 in Edelman, (1988), we obtain for

With this gives the asserted bound. ∎

For a sufficiently large number of summands the previous bound can be generalised to the setting where each summand has a population covariance where only the size of the eigenvalue is lower bounded.

A.8 Corollary.

Let , , be independent -dimensional Gaussian random vectors with for all and some . Set with a fixed constant only depending on and and assume . Then we have the Laplace transform bound for :

Proof.

Denote by the orthogonal projection onto the -dimensional eigenspace of corresponding to . By the metric entropy result for Grassmannian manifolds (Pajor,, 1998, Proposition 6) and the relationship with internal covering numbers there is a family of -dimensional subspaces of such that with orthogonal projections onto

and has cardinality less than for some universal constant . Hence, by a counting argument there are and with for all with . For and we then obtain

We apply Theorem A.6 in dimension for the restrictions , to the subspace , for , , and with and obtain

as claimed. ∎

Given the Laplace transform result we obtain a deviation inequality for a triangular scheme over different Wishart matrices. This is exactly what we need for analysing our test statistics under the alternatives.

A.9 Corollary.

Let , , , be independent -dimensional random vectors with for all and some . Without loss of generality suppose the order . Set and assume with the constant from Corollary A.8. Then we have for all and the lower tail bound

where the constant only depends on and .

A.10 Remark.

Let us note that is the weak- norm of the vector .

Proof.

By elementary properties of binomial coefficients and Gamma functions we have . We thus infer from Corollary A.8

The classical Chernoff argument yields for and any

Choosing and applying , gives the asserted bound with . ∎

A.4 Technical results for Section 3

A.11 Proposition.

Consider the test statistics in (2.2) and assume for all . Let

denote the average -variation of over blocks and introduce the constants

Then we have with probability at least for any and :

-

(a)

without a spectral gap assumption

-

(b)

under the spectral gap assumption

A.12 Remark.

It is implicitly understood that the appearing -variations and -norms of and are all finite.

The bounds consist in each case of four different contributions. The first and asymptotically dominant term comes from the deterministic bias. The second and third capture the additional bias induced by the expected st eigenvalue of and scales in the number of observations on a block like for the subgaussian deviations and for the subexponential deviations. The dependence on comes from bounding the maximum of blockwise integrals by an -norm, similarly to Sobolev embeddings, and one might think of for a first intuition. The size of random fluctuations scales with the total number of observations so that the fourth term is of order . In the case of a spectral gap, the squared error structure induces a natural -variation bound. The proof reflects exactly this error decomposition. Concerning the dimension dependence we conjecture that the linearity up to logarithmic terms of and in the remaining dimension is also necessary.

Proof.

To establish part (a), let us consider for each block the eigenspace of eigenvectors corresponding to the smallest eigenvalues of . With the orthogonal projection onto we introduce the -lower right minors

| (A.2) |

By the Cauchy interlacing law (e.g., Johnstone, (2001) or Tao, (2012)),

Introduce . We apply the matrix deviation inequality for triangular schemes from Theorem A.4 in dimension with , . From Corollary 3.2 we obtain

in the absence of a spectral gap. Then Proposition A.1 and Hölder’s inequality yield

and by Jensen’s inequality

The quantities in Theorem A.4 are therefore bounded as

By Theorem A.4 with we thus have with probability at least for any

In the case (b) of a spectral gap we use and as before, but employ the quadratic matrix deviation bounds. Then Corollary 3.2 yields

By Proposition A.1 and Hölder’s inequality we have

as well as

The quantities in Theorem A.4 are in this case bounded as

We apply Theorem A.4 exactly as before and arrive at the result in (b). ∎

Proof of Proposition 3.9..

Let us first treat the case , , and . Consider the covariance function from Example 2.2 for , satisfying . On the other hand, the constant covariance lies in the alternative even for . Because of for all , the observations , , have the same law under and which entails for any test , as asserted. In the case observe the inclusions

Therefore, the result for , where , extends to this case. Altogether we have thus shown the assertion for , , .

We reduce the general case to this particular choice. Indeed, for general it suffices to consider covariance functions that are diagonal with a large constant (larger than ) in the coordinates and equal to zero in the coordinates , while equal to the above -covariance functions in the entries with coordinates . Then all Hölder and eigenvalue conditions are clearly fulfilled. Moreover, given that the result is proved for with the Hölder constant , then the covariance with from above is in . The eigenvalue bound scales with the factor as well. The same holds for and the general assertion follows by a simple rescaling argument. ∎

A.5 Technical results for Section 4

Throughout we work under the model (4.1) and Assumption 4.1 for and with the blockwise estimators where . We first show two approximation results before establishing the Central Limit Theorem 4.3.

A.13 Lemma.

Uniformly over

where for

Proof.

From Equation (2.1), conditioning on , we infer

using and thus . Applying this to as well, we can expand

Together with the expansion for and the regularity condition on we obtain

The regularity of yields via the Burkholder-Davis-Gundy inequality

All constants depend uniformly in on the regularity conditions in Assumption 4.1. ∎

Lemma A.13 allows to derive the asymptotics of the conditional expectations and variances of the normed second differences.

A.14 Proposition.

We have

as well as

Proof.

We inject the value into Lemma A.13 and obtain

This is immediate for and follows for by and an application of Cauchy-Schwarz inequality to the squared norm in Lemma A.13. In the proof of Proposition 4.2 was established so that a Riemann sum approximation yields

Putting the asymptotics together yields the conditional expectation result.

Arguing similarly for the conditional variances, we calculate

| (A.3) |

On the other hand, we obtain for the squared conditional expectations

The difference of the expressions gives the result for the variance. ∎

Proof of Theorem 4.3.

First observe that implies and the -terms in Proposition A.14 are asymptotically negligible.

We use the conditional expectation and variance results from Proposition 4.2 and the fact that is an even function of Brownian increments to apply a standard stable limit theorem (Theorem 4.2.1 in Jacod & Protter, (2011), compare also its application there in Theorem 5.3.5(i-)), noting that we need not require the differentiability of the functional because the linear term becomes already negligible by our choice of . ∎

Proof of Proposition 4.4.

By Lemma A.13 and , uniformly in , we find

From (A.3) we obtain

Looking at -moments, we deduce directly that

which is since . Standard martingale arguments (Jacod & Protter,, 2011, Lemma 2.2.11(a)) therefore yield

and thus the first limiting result.

For the second result the same arguments give

where we only note that the error bound does not change when pulling instead of out of the second stochastic integral. We obtain for the conditional expectation by conditional independence of Brownian increments

The remaining arguments are then exactly as for the fourth moment result. ∎

Proof of Corollary 4.6..

Set . By Proposition A.11 below (inject , , , with ) we have on the event

where we use and almost surely. Therefore Proposition 4.2 and yield on

From (4.3) and we deduce that then also

holds. By the Central Limit Theorem 4.3, the consistency results of Proposition 4.4 and Slutsky’s lemma we conclude

Another application of Slutsky’s lemma thus implies

is at least . This gives the result for the test . ∎

References

- Aït-Sahalia & Xiu, (2017) Aït-Sahalia, Y. & Xiu, D. (2017). Using principal component analysis to estimate a high dimensional factor model with high-frequency data. Journal of Econometrics, 201(2), 384–399.

- Aït-Sahalia & Xiu, (2019) Aït-Sahalia, Y. & Xiu, D. (2019). Principal component analysis of high-frequency data. Journal of the American Statistical Association, 114(525), 287–303.

- Bai & Ng, (2002) Bai, J. & Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica, 70(1), 191–221.

- Bru, (1991) Bru, M.-F. (1991). Wishart processes. Journal of Theoretical Probability, 4(4), 725–751.

- Cai et al., (2015) Cai, T., Ma, Z., & Wu, Y. (2015). Optimal estimation and rank detection for sparse spiked covariance matrices. Probability theory and related fields, 161(3-4), 781–815.

- Christensen et al., (2021) Christensen, K., Nielsen, M. S., & Podolskij, M. (2021). High-dimensional estimation of quadratic variation based on penalized realized variance. arXiv 2103.03237.

- Ciesielski et al., (1993) Ciesielski, Z., Kerkyacharian, G., & Roynette, B. (1993). Quelques espaces fonctionnels associés à des processus gaussiens. Studia Mathematica, 2(107), 171–204.

- Cohen, (2003) Cohen, A. (2003). Numerical analysis of wavelet methods. Elsevier.

- Diebold & Li, (2006) Diebold, F. & Li, C. (2006). Forecasting the term structure of government bond yields. Journal of Econometrics, 130(2), 337–364.

- Edelman, (1988) Edelman, A. (1988). Eigenvalues and condition numbers of random matrices. SIAM journal on matrix analysis and applications, 9(4), 543–560.

- Fan & Wang, (2008) Fan, J. & Wang, Y. (2008). Spot volatility estimation for high-frequency data. Statistics and its Interface, 1(2), 279–288.

- Hoffmann, (2002) Hoffmann, M. (2002). Rate of convergence for parametric estimation in a stochastic volatility model. Stochastic processes and their applications, 97(1), 147–170.

- Ingster & Suslina, (2012) Ingster, Y. & Suslina, I. A. (2012). Nonparametric goodness-of-fit testing under Gaussian models, volume 169. Springer.

- Jacod et al., (2008) Jacod, J., Lejay, A., & Talay, D. (2008). Estimation of the brownian dimension of a continuous itô process. Bernoulli, 14(2), 469–498.

- Jacod & Podolskij, (2013) Jacod, J. & Podolskij, M. (2013). A test for the rank of the volatility process: the random perturbation approach. The Annals of Statistics, 41(5), 2391–2427.

- Jacod & Protter, (2011) Jacod, J. & Protter, P. (2011). Discretization of processes, volume 67. Springer.

- James, (1960) James, A. T. (1960). The distribution of the latent roots of the covariance matrix. The Annals of Mathematical Statistics, 31(1), 151–158.

- Johnstone, (2001) Johnstone, I. M. (2001). On the distribution of the largest eigenvalue in principal components analysis. Annals of Statistics, 29(2), 295–327.

- Juditsky & Nemirovski, (2002) Juditsky, A. & Nemirovski, A. (2002). On nonparametric tests of positivity/monotonicity/convexity. Ann. Statist., 30(2), 498–527.

- Koltchinskii & Mendelson, (2015) Koltchinskii, V. & Mendelson, S. (2015). Bounding the smallest singular value of a random matrix without concentration. International Mathematics Research Notices, 2015(23), 12991–13008.

- Lam & Yao, (2012) Lam, C. & Yao, Q. (2012). Factor modeling for high-dimensional time series: Inference for the number of factors. The Annals of Statistics, 40(2), 694 – 726.

- Laurent & Massart, (2000) Laurent, B. & Massart, P. (2000). Adaptive estimation of a quadratic functional by model selection. Annals of Statistics, 28(5), 302–1338.

- Ledoux & Talagrand, (1991) Ledoux, M. & Talagrand, M. (1991). Probability in Banach Spaces: Isoperimetry and Processes. Springer.

- Li et al., (2016) Li, W., Gao, J., Li, K., & Yao, Q. (2016). Modeling multivariate volatilities via latent common factors. Journal of Business & Economic Statistics, 34(4), 564–573.

- Magnus & Neudecker, (1979) Magnus, J. R. & Neudecker, H. (1979). The commutation matrix: some properties and applications. The Annals of Statistics, 7(2), 381–394.

- Muirhead, (2009) Muirhead, R. J. (2009). Aspects of multivariate statistical theory, volume 197. John Wiley & Sons.

- Nelson & Siegel, (1987) Nelson, C. & Siegel, A, F. (1987). Parsimonious modeling of yield curves. Journal of Business, 60(4), 473–489.

- Onatski et al., (2014) Onatski, A., Moreira, M. J., Hallin, M., et al. (2014). Signal detection in high dimension: The multispiked case. The Annals of Statistics, 42(1), 225–254.

- Pajor, (1998) Pajor, A. (1998). Metric entropy of the grassmann manifold. Convex Geometric Analysis, 34, 181–188.

- Reiß & Wahl, (2020) Reiß, M. & Wahl, M. (2020). Nonasymptotic upper bounds for the reconstruction error of PCA. Annals of Statistics, 48(2), 1098–1123.

- Su & Wang, (2017) Su, L. & Wang, X. (2017). On time-varying factor models: Estimation and testing. Journal of Econometrics, 198(1), 84–101.

- Tao, (2012) Tao, T. (2012). Topics in random matrix theory, volume 132. American Mathematical Soc.

- Tropp, (2012) Tropp, J. A. (2012). User-friendly tail bounds for sums of random matrices. Foundations of computational mathematics, 12(4), 389–434.

- Vetter, (2015) Vetter, M. (2015). Estimation of integrated volatility of volatility with applications to goodness-of-fit testing. Bernoulli, 21(4), 2393 – 2418.