Capital Demand Driven Business Cycles: Mechanism and Effects

Abstract

We develop a tractable macroeconomic model that captures dynamic behaviors across multiple timescales, including business cycles. The model is anchored in a dynamic capital demand framework reflecting an interactions-based process whereby firms determine capital needs and make investment decisions on a micro level. We derive equations for aggregate demand from this micro setting and embed them in the Solow growth economy. As a result, we obtain a closed-form dynamical system with which we study economic fluctuations and their impact on long-term growth. For realistic parameters, the model has two attracting equilibria: one at which the economy contracts and one at which it expands. This bi-stable configuration gives rise to quasiperiodic fluctuations, characterized by the economy’s prolonged entrapment in either a contraction or expansion mode punctuated by rapid alternations between them. We identify the underlying endogenous mechanism as a coherence resonance phenomenon. In addition, the model admits a stochastic limit cycle likewise capable of generating quasiperiodic fluctuations; however, we show that these fluctuations cannot be realized as they induce unrealistic growth dynamics. We further find that while the fluctuations powered by coherence resonance can cause substantial excursions from the equilibrium growth path, such deviations vanish in the long run as supply and demand converge.

keywords:

Business Cycles , Economic Growth , Interactions-Based Models , Dynamical Systems , Limit Cycle , Coherence Resonance1 Introduction

My view was, and still is, that the most urgent current analytical need was for a way of fitting together short-run macroeconomics, when the main action consists of variations in aggregate demand, with the long run factors represented by the neoclassical growth model, when the main action is on the supply side. Another way of saying this is that short-run and long-run models of macroeconomic behavior need a way to merge in a practical macroeconomics of the medium run (Solow, 2005).

The field of economics has long been aware of a conceptual dichotomy between studies of short-term dynamics and models of long-term growth. An early distinction was made between the Hicks IS-LM model (1937) and the Solow growth model (1956). The developments in both approaches have captured important dynamics at their respective timescales, such as short-term demand effects and endogenous drivers of long-term growth (e.g. Aghion and Howitt, 1992). Yet it is not well understood how the dynamics at different timescales are interlinked and how medium-term disequilibrium dynamics impact the long-term growth trend of the economy.

Since the World War II, the United States of America alone has faced twelve recessions. While the severe short-term consequences of these crises are appreciated, understanding of the long-lasting impact on growth remains underdeveloped. The pervasive recurrence of booms and busts has thus sparked research into the linkages between economic volatility and growth (Cooley and Prescott, 1995; Aghion and Howitt, 2006; Priesmeier and Stähler, 2011; Bakas et al., 2019). Theoretical as well as empirical investigations have turned out to be inconclusive, as authors disagree on both the sign and magnitude of the ultimate effect of volatility on growth.111 We suggest Bakas et al. (2019) for a comprehensive review of this literature. Theoretical literature is divided into two dominant strands that stem from either Schumpeterian notions, in which volatility is good for growth (based on Schumpeter, 1939, 1942), or the learning-by-doing concept (based on Arrow, 1962), where volatility is detrimental to growth. The conflicting theoretical frameworks and ambiguous empirical findings indicate that new, alternative approaches may be needed to decipher the genuine nature of the relationship between volatility and growth. Current literature does not generally consider the impact of the interactions among economic agents and their collective dynamics on long-term growth. It is this impact and its underlying mechanisms that we seek to capture and explain.

We are motivated by the micro-to-macro approach of agent-based modeling (LeBaron and Tesfatsion, 2008; Dawid and Delli Gatti, 2018; Hommes and LeBaron, 2018) and, especially, the Keynes-meets-Schumpeter class of models (Dosi et al., 2010, 2015) that study the linkages between endogenous growth and demand policy. While agent-based models successfully capture many complex phenomena, they are generally analytically intractable, making the analysis of the precise mechanics linking volatility and growth difficult. Our approach remains distinct as we aim to derive a tractable system of equations for the aggregate dynamics from micro-level interactions.

This paper’s objective is to develop a model of capital demand driven economic fluctuations, in which interactions among agents to coordinate on economic outcomes lead to periods of booms and busts, and apply it to examine how fluctuations affect the economy across different timescales and possibly shape its long-term growth. Inspired by Keynes (1936), our focus on capital demand is motivated by the observation that firms’ investment is both pro-cyclical and volatile (Stock and Watson, 1999), suggesting investment decisions play a key role in business cycles. We treat investment decision-making as an interactions-based process whereby firm managers exchange views and affect each other’s opinions. In other words, we emphasize strategic complementarity and peer influence that cause managers to coalign their individual expectations at the micro level. We use the framework developed in Gusev et al. (2015) and Kroujiline et al. (2016) to describe this interaction process mathematically and derive the macroscopic equations governing the dynamics of aggregate capital demand. To close the economy while highlighting the demand-driven effects, we attach these equations to a simple supply side component represented by the Solow growth model (1956).

As a result, we obtain a closed-form dynamical system, hereafter the Dynamic Solow model, which enables us to study a broad range of economic behaviors. The model’s primary contribution is the identification of a new mechanism of business cycles that captures their quasiperiodic nature characterized by one or several peaks in a wide distribution of cycle lengths.

We show that, for economically realistic parameters, the Dynamic Solow model admits two attracting equilibria that entrap the economy in either a contraction or expansion.222The 2008 crisis gave new impetus to revisiting the single equilibrium framework; e.g. Vines and Wills (2020) recently made the case for moving towards a multi-equilibrium paradigm. The equilibria are indeterminate (Benhabib and Farmer, 1999) as both the path to and the choice of equilibrium depend on the beliefs of the agents themselves. The entrapment is asymmetric because technological progress, introduced externally, causes the economy to stay on average longer in expansion than contraction, contributing to long-term growth. The flow of exogenous news continually perturbs the economy stochastically and prevents it from settling at either equilibrium. Over time, the economy tends to drift slowly towards the boundary between the contraction and expansion regions, making it easier for a news shock to instigate a regime transition in line with the “small shock, large business cycle” effect (Bernanke et al., 1996). This endogenous mechanism generates quasiperiodic fluctuations as it involves both deterministic dynamics and stochastic forcing.

Such a mechanism, whereby noise applied to a dynamical system leads to a quasiperiodic response, is known as coherence resonance (Pikovsky and Kurths, 1997). It occurs in situations where the system has long unclosed trajectories such that even small amounts of noise can effectively reconnect them and thus create a quasiperiodic limit cycle. Coherence resonance emerges naturally in bi-stable systems333In dynamical systems, bistability means the system has two stable equilibrium states., including our model.

The coherence resonance mechanism differentiates the Dynamic Solow model from preceding research that has often considered limit cycles as the endogenous source of economic fluctuations.444 The early literature comprises Hicks (1937), Kaldor (1940) and Goodwin (1951). Later reviews include Boldrin and Woodford (1990), Scheinkman (1990), Lorenz (1993) and Gandolfo (2009). We also note Beaudry et al. (2020) as an influential recent investigation. In particular, Beaudry et al. (2020) propose an extended Dynamic Stochastic General Equilibrium model, in which the quasiperiodic character of fluctuations comes from noise acting directly on a periodic limit cycle. We argue, however, that coherence resonance may be the preferred route to generating business cycles as it requires noise only as a catalyst, thus relying much less on random shocks to reproduce regime variability. Furthermore, we show that the fluctuations produced by a noise-perturbed limit cycle, which is as well recovered in a certain parameter range in our model, dampen long-term growth and unrealistically cause capital demand to diverge from supply in the long run.

We note that the Dynamic Solow model nests two limiting cases that match those of previous literature. In the case where capital demand is persistently higher than supply, the model recovers the exponential equilibrium growth of the classic Solow model. In the opposite case, where capital demand is persistently lower than supply, the model exhibits quasiperiodic fluctuations driven by a coherence resonance mechanism similar to that in Kroujiline et al. (2019).

We explore the Dynamic Solow model numerically across multiple timescales, from months to centuries, and identify business cycles as quasiperiodic fluctuations that most frequently last 40-70 years. These fluctuations may be associated with Kondratieff cycles if interpreted as investment driven.555Kondratieff himself attributed these cycles to capital investment dynamics. This interpretation was further advanced by a number of papers in the 1980s. Kondratieff cycles are, however, more commonly linked to technological innovation. There have also been attempts to combine investment and innovation explanations. For a review see Korotayev and Tsirel (2010). Korotayev and Tsirel (2010) employ spectral analysis to suggest the existence of long-term business cycles. However, the academic community remains divided on this issue and the research has been focused primarily on the fluctuations in the 8-12 year range. These shorter-term cycles cannot emerge in our model because it does not include accelerators such as the financial sector or household debt.

Currently, many macroeconomic models describe an economy in or near equilibrium. Most prominent is the Dynamic Stochastic General Equilibrium class of models (see Christiano et al., 2018; Kaplan and Violante, 2018, for recent reviews). While behavioral limitations and various frictions have been considered, these models operate in an adiabatic regime where equilibrium is reached more quickly than the environment changes. In other words, there is some form of perfect coordination (e.g. market clearing where supply and demand equate) among all agents at each point in time. Over long timescales this treatment may be justified, but in the near term coordination failures are inevitable, leading to pronounced fluctuations and persistent spells of disequilibrium.

The Dynamic Solow model enables us to study both the disequilibrium fluctuations and the equilibrium growth. We examine the impact of fluctuations on growth and show that fluctuations can affect economic expansion over extended time intervals. However, the deviations from the balanced growth path disappear with time as demand and supply converge asymptotically in the long run.

The remainder of this paper is structured as follows. In Section 2 we introduce and explain the mechanics of dynamic capital demand and the Solow growth framework within which it rests. Section 3 considers two limiting cases: first, we obtain the equilibrium growth path when capital demand exceeds supply; and second, we investigate the demand dynamics and highlight the mechanism underlying fluctuations when capital supply exceeds demand. Section 4 formulates and studies the general case of the Dynamic Solow model, focusing on the analysis of mid-term fluctuations and long-term growth. Finally, Section 5 concludes by reflecting on the work done and suggests further avenues of research.

2 The Dynamic Solow Model

This section develops the Dynamic Solow model.666M. Gusev and D. Kroujiline formulated and presented the basic ideas behind the model at the Macroeconomic Instability seminars of the ”Rebuilding Macroeconomics” project (www.rebuildingmacroeconomics.ac.uk) run by the National Institute of Economic and Social Research in London (Gusev and Kroujiline, 2020). The modeling framework is set out in Section 2.1 and the equations of the model components are derived in Sections 2.2-2.5.777The code for this model is written in Python and is available at github.com/KarlNaumann/DynamicSolowModel.

2.1 Model Structure

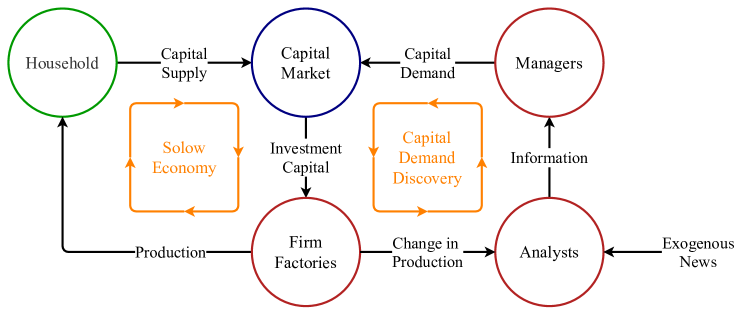

The Dynamic Solow model is illustrated in Figure 1. It consists of a dynamic demand framework that we propose to describe how firms determine capital needs and make investment decisions (right loop), to which we attach the familiar circular income flow of the Solow growth economy (left loop).888 We choose this supply-side framework for the following reasons: (i) the capital supply dynamics are less important on the timescales where we expect to find fluctuations and thus can be modeled approximately; (ii) the assumption that households save a constant fraction of income is an appropriate leading-order approximation since it is the first term in the Taylor series expansion of savings as a general function of income; and (iii) the Solow model is a parsimonious representation of economic growth, sharing the basics with many macroeconomic models, which may be helpful to extending our approach to more sophisticated settings.

In the Solow economy, households supply capital through savings and firms convert capital into output for household consumption. Both households and firms are static decision-makers. Households save a fixed share of income and firms convert all supplied capital into production. In contrast, we aim to describe how firms develop a strategic business outlook based on their reading of the current economic situation and accordingly determine their capital needs so as to adjust production capacity. Firms thus become active decision-makers, which results in a dynamically evolving capital demand.

Organizational decision-making is a complex process with competing goals and targets, often based on industry-standard business planning and operating procedures (Cyert and March, 1992; Miller and Cardinal, 1994). Without needing to make firm goals explicit, we posit that corporate decision-making can be viewed as a composite of two distinct processes occurring on different timescales. First, there is information gathering and analysis, characterized by the frequency with which exogenous information such as ad-hoc company news, monthly statistics releases or quarterly earnings reports becomes available. Second, there is the formation of firms’ expectations about the future based on the analysis of collected information, which is then translated into investment decisions. Note that the strategic aspect of investment decision-making implies longer timescales than those of information gathering and analysis.

We model this two-tier decision-making on the microscale by introducing two classes of agents: analysts who collect and analyze relevant information and managers who use this analysis to develop a business outlook and make investment decisions. There are industries where these two classes of agents actually exist (e.g. analysts and investors in finance), whereas in other situations this division serves as a metaphor for the different actions completed by an individual participant. Our objective is to derive the macro-level equations for aggregate demand from this micro setting.

External information enters the decision-making process at the analyst level. Initially, we may neglect the cost side and focus solely on revenue generation, elevating in relevance the expectation of future consumption. Motivated by recent work on extrapolative beliefs in finance (Greenwood and Shleifer, 2014; Kuchler and Zafar, 2019; Da et al., 2021), we assume that analysts base their expectations primarily on the current state of the economy by extrapolating the consumption growth into the future. As such, we wish to carve out consumption growth as the most relevant information stream and model all other news as exogenous noise (treating news shocks similarly to Angeletos and La’O, 2013; Angeletos et al., 2020; Beaudry and Portier, 2014). We can further simplify by replacing consumption with production since consumption is approximated as a constant fraction of production in the model. The resulting system acquires a feedback mechanism as higher output growth leads to increasing expectations that cause greater investment, inducing further increases in output growth and starting the process anew.

On the manager level, we emphasize the impact of the opinions and actions of competitors on decision-making, following the growing body of research on peer influence in business (Griskevicius et al., 2008) and strategic complementarity (Cooper and John, 1988; Beaudry et al., 2020). More specifically, we assume that managers exchange views within their peer network with the purpose of coaligning their expectations about the economy.

The Dynamic Solow model employs, as discussed, two different processes for capital demand and supply: firms determine capital needs dynamically via individual interactions and economic feedback while households supply capital in proportion to income. Thus, demand and supply do not necessarily match at each point in time, which brings us to the discussion of capital market clearing on different timescales. The dynamic demand discovery process occurs on timescales much shorter than the timescale of technological growth. At these short and intermediate timescales – relevant to information gathering, investment decision-making and production adjustment – prices are rigid and we expect demand and supply to behave inelastically. However, over long time horizons in which the economy is advancing along the equilibrium growth path, prices become flexible and the capital market clears via price adjustment. Therefore, we expect that demand and supply converge in the long run.

As such, the conceptual framework behind the model is now complete. The remainder of Section 2 is as follows. Section 2.2 extends the usual equation for aggregate economic production to include the (shorter) timescales at which production capacity adjusts. Section 2.3 briefly introduces a representative household and the capital motion equation. Section 2.4 derives the equations for aggregate capital demand from the micro-level agent-based formulation outlined above. Finally, Section 2.5 sets out conditions for capital market clearing.

2.2 Production

We represent aggregate output by a Cobb-Douglas production function that takes invested capital as an input,999 For simplicity, we normalize the initial technology level to unity and do not consider labor, which is equivalent to normalizing the labor component to unity or taking the variables in per capita terms. generically written as

| (1) |

with output , invested capital , capital share in production and technology growth rate . Equation (1) implies that output adjusts immediately to any change in capital. In other words, it is only valid on timescales longer than the time it takes to adjust the production capacity (e.g. the construction of a new factory or installation of new machinery). Since we are also concerned with decision-making processes that occur at much shorter timescales than production adjustment, we introduce a dynamic form of production

| (2) |

where the dot denotes the derivative with respect to time and is the characteristic timescale of production capacity adjustment.101010 In reality, the adjustment periods are asymmetric because it is easier to reduce capacity than to increase it. For simplicity, we treat capacity increases and decreases as if they were symmetric. In the short run, this equation describes the dynamic adjustment of output to new capital levels. In the long run, we recover the Cobb-Douglas production form (1) as becomes negligibly small for .

Finally, we rewrite equation (2) with log variables and as

| (3) |

2.3 Households and Capital Supply

We consider a single representative household that is the owner of the firm and thus receives as income. A fixed proportion of income, expressed as , is saved and the remainder is consumed. This is a convenient simplification that allows us to focus on the effects of dynamic capital demand. A constant savings rate can also be viewed as a leading-order Taylor expansion of household savings as a general function of income, making it a sensible first approximation.

The total savings are available to firms to invest. We denote them as capital supply . The working capital used in production, , suffers depreciation at a rate . As households are the owners of the capital, the loss is attributed to the capital supply. Consequently, the supply dynamics take the form

| (4) |

Setting , we reformulate equation (4) using log variables as

| (5) |

2.4 Dynamic Capital Demand

In this section, we derive the equations for aggregate capital demand. As set out in Section 2.1, this derivation is based on a micro-level framework that divides the firms’ investment planning into two processes occurring at different speeds: fast-paced information gathering and analysis; and slow-paced decision-making. We model these processes with two classes of interacting agents: analysts who collect and analyze relevant information; and managers who use this analysis to develop their strategic business outlook and make investment decisions.111111This modeling approach adapts the investor-analyst interaction framework, developed for the stock market in Gusev et al. (2015) and Kroujiline et al. (2016), to the macroeconomic context.

In mathematical terms, we consider two large groups of agents: analysts and managers , where and . Each analyst and manager has a positive or negative expectation about the future path of production, respectively and . The agents interact by exchanging opinions. As a result, the agents influence each other’s expectations and tend to coalign them. To stay general, we assume analysts and managers interact among themselves and with each other. These individual interactions drive the evolution of the macroscopic variables: average analyst expectation (information) and average manager expectation (sentiment).

At each moment of time , sentiment is given by

| (6) |

where and , with and representing the respective number of optimists and pessimists (). By construction, varies between and . At the leading order, we treat interaction as though each is affected by the collective opinions and (similarly constructed), each forcing in their respective directions.121212 This treatment, known as the mean-field approach, is the leading-order approximation for a general interaction topology. As a result of this simplification, we can introduce the total force of peer influence acting on each manager as

| (7) |

where and are the sensitivities and denotes general exogenous influences (to be specified later). Equation (7) implies that as the collective expectations of managers and analysts grow more optimistic, the stronger the force exerted on a pessimistic manager to reverse her views (and vice versa).

In addition, managers may be affected by a multitude of idiosyncratic factors causing them to occasionally change opinions irrespective of other participants. We treat them as random disturbances and, accordingly, introduce the transition rates as the probability per unit time for a manager to switch from a negative to positive opinion and as the probability per unit time of the opposite change. We can express the changes in and over a time interval as

| (8) | |||||

| (9) |

Noting that and , we subtract (9) from (8) to obtain in the limit

| (10) |

To complete the derivation, we must find out how the transition rates depend on peer influence: and . It follows from (8) that in the state of equilibrium, when , the condition holds. Thus can be interpreted as the ratio of optimists to pessimists. We can assume this ratio changes proportionally to a change in , that is where is a positive constant. This interpretation allows us to write , which leads to

| (11) |

Condition (11) implies correctly that for , for and for . To obtain the final condition required to determine and uniquely, we introduce the characteristic time over which individual expectations change due to random disturbances. Since and are per unit time, represents the characteristic time over which the total probability for a manager to reverse her expectation is unity:131313 Consider the impact of a random disturbance. At its end, the agent’s state will remain or change to its opposite. Introduce and as the probabilities for the agent, in state , to end up in state or , respectively, and and for the agent, in state , to end up in state or , respectively. Thus, and . Assuming that the ending state does not depend on the initial state, i.e. and , we obtain . If the disturbances are frequent on the timescale of interest, we can transform the discrete probabilities into continuous transition rates via and to recover equation (12).

| (12) |

Together conditions (11) and (12) imply the transition rates:

| (13) |

Equations (13) allow us to rewrite (10) as

| (14) |

where is absorbed into and without loss of generality. Note that acquires a dual meaning: at the micro level, is akin to the manager’s average memory timespan; at the macro level, is the characteristic time of variation in the aggregate expectation of managers.

Applying this approach to model the dynamics of analyst expectations yields the same form of the evolution equation for information :

| (15) |

where represents the analyst’s average memory timespan on the micro level and the characteristic time of the variation in the aggregate expectation of analysts on the macro level. Similarly, is the peer influence acting on the analysts’ expectations, which is linear in and with sensitivities and , and denotes general exogenous influences.

Equations (14) and (15) describe a generalized interactions-based process of decision-making. We now make several assumptions to adapt it to the capital demand discovery mechanism of the Dynamic Solow model (Figure 1).

First, we assume managers receive information only via analysts and accordingly set . Second, we assume analysts are affected, first and foremost, by the news about economic development and only thereafter by all other news. More specifically, we assume the average analyst projects the output trend forward in time (extrapolative beliefs) and we treat all other relevant news as exogenous noise. Thus we set

| (16) |

with sensitivity and news noise acting on the timescale . The latter implies that changes to expectations are impacted by short-term shocks with no relation to economic fundamentals (as suggested, for example, by Angeletos et al. (2020)).

Third, we establish separate timescales for information processing and expectation formation. That is, we assume information is received and processed much faster than it takes managers to adapt their long-term outlook and form investment decisions. Therefore: . Fourth, as is much shorter than , we assume direct interactions are less important for analysts than for managers and we take for simplicity.

The final step is to model the link between sentiment and capital demand. Consider a firm whose managers have just decided on capital allocation in line with their collective sentiment. The following day, all else being equal, the managers will not revisit this decision unless their sentiment changes. Therefore, in the short run where (that is, over time horizons where the memory of past sentiment persists), capital demand must be driven by change in sentiment. Conversely, over longer horizons where , the connection between previous decisions and sentiment becomes weaker and, therefore, investment decisions must be based on the level of sentiment itself in the long run. For lack of simpler alternatives, we superpose these two asymptotic regimes, for and for , and, as a result, arrive at a complete system of equations for capital demand:

| (17) | |||||

| (18) | |||||

| (19) |

where and represent the capital demand sensitivity to a change in sentiment and the level of sentiment , respectively; and represents the sensitivity of information to the state of the economy or, in other words, the strength of economic feedback.141414Gusev et al. (2015) derived equations (18) and (19) in the context of their generalized Ising model. The derivation presented here provides a more intuitive, albeit less rigorous, treatment. Equation (18), with as an exogenous variable, was originally obtained by Suzuki and Kubo (1968) for the classic Ising (1925) model in statistical mechanics. Following Haag and Weidlich (1983), equation (18) (often in its stationary form) has frequently appeared in the socioeconomic context. For reviews of the interactions-based approaches reliant on the statistical mechanics methods and, particularly, the applications of the Ising model and its variants to the opinion dynamics problems in economics and finance, we recommend Brock and Durlauf (2001), Bouchaud (2013) and Slanina (2013). We also note that, unlike equations (18) and (19) that are derived from the micro level, equation (17) is obtained as a phenomenological relation between business sentiment and capital demand. Equation (17) was initially suggested as a link between investor sentiment and stock market returns in Gusev et al. (2015).

2.5 Capital Market Clearing

At the relatively short time horizons relevant to information gathering, investment decision-making and production adjustment, prices are not flexible enough to efficiently match capital demand and supply , which are determined independently from each other. Accordingly, we introduce an inelastic market clearing condition for log invested capital as

| (20) |

to be satisfied at each moment in time. In contrast to the classic framework, in which all household savings are used in production, this condition implies that only a portion of savings will be invested should demand fall short of supply (with the remainder retained in household savings accounts).

Equation (20) is a local clearing condition that reflects the short-term price rigidity. Therefore, as was discussed in Section 2.1, this equation cannot remain valid over long-term horizons during which prices become sufficiently flexible to match demand and supply. As such, we supplement (20) with an asymptotic clearing condition that holds in the timescale of long-term economic growth:151515The asymptotic relation (21) means that the relative error between and goes to zero as goes to infinity.

| (21) |

Together, equations (20) and (21) interlink the supply and demand components and close the Dynamic Solow model.

At this point, it may be useful to discuss the characteristic timescales in the model. The timescales we have encountered are differentiated in length such that . Economically, information gathering occurs on a relatively short timescale, (with the publication of, for example, monthly and quarterly corporate reports and industry data releases); investment decisions require more time, (as processed through, for example, annual board meetings); and the implementation of changes to production levels takes much longer, (the time needed for material adjustments such as infrastructure development). We set , and in units of business days (250 business days = 1 year). We further assume the timespan of exogenous news events to be on average one week and set as the news noise decorrelation timescale (see C). Finally, we take technology growth rate , which implies the timescale of 160 years.161616 In equation (1), the term , commonly referred to as total factor productivity, yields a growth rate of about 0.6% p.a. for , which is not far from the estimates based on the 2005-2016 period using Fernald (2016).

3 Two Limiting Cases

In this section, we inspect two cases that follow from the market clearing condition (20): first, the supply-driven case, such that , which recovers a Solow-type growth economy; and, second, the demand-driven case, such that , in which the economic fluctuations emerge.

3.1 Supply-Driven Case

In the supply-driven case, the market clearing condition yields (firms use all available capital for production)171717It is convenient to use the non-logarithmic variables for this analysis.. Consequently, the Dynamic Solow model is reduced to equations (2) and (4) which can be expressed as a single second-order differential equation:

| (22) |

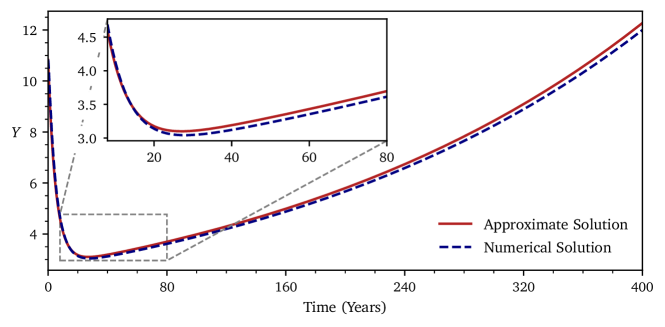

For and longer time intervals, the derivative terms in equation (22) become negligibly small and we recover the equilibrium growth path. On shorter timescales, , equation (22) describes adjustment towards the equilibrium growth path. These two effects can be observed simultaneously by deriving an approximate solution to equation (22) for (see B). The resulting production path is given by

| (23) |

where is the constant of integration.181818 This derivation is valid for the parameter values provided in A, subject to the simplifying assumption which allows us to obtain the solution in a compact form. Equation (23) explains the output dynamics between intermediate and long-term timescales, capturing both the long-term growth of the classic Solow model (given by the second exponent) and the intermediate relaxation towards the same (given by the first exponent). The approximate analytic solution (23) and the exact numerical solution to equation (22) are compared in Figure 2.

3.2 Demand-Driven Case

In the demand-driven case, the market clearing condition yields . The Dynamic Solow model is specified at this limit by equations (3) and (17)-(19) (in this case, equation 5 decouples and no longer affects production). To facilitate our analysis, we introduce the variable , which makes the model solutions bounded in the -space (see D). Economically, represents the direction and strength of economic growth. This follows from rewriting equation (3) as , noting that for production expands, for it contracts and is a production fixed point. Using , we re-express the model as a three-dimensional dynamical system that is bounded and autonomous in the absence of exogenous noise :

| (24a) | ||||

| (24b) | ||||

| (24c) | ||||

where, for convenience, .

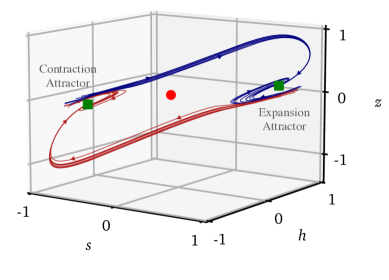

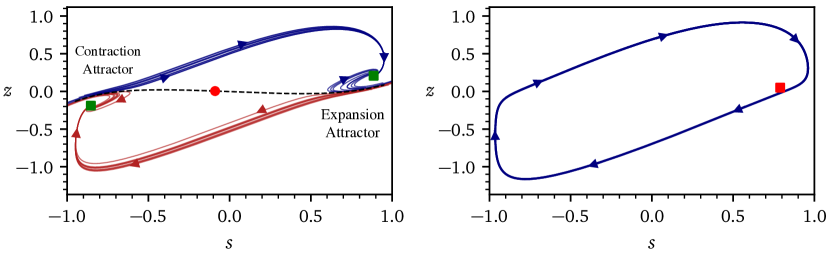

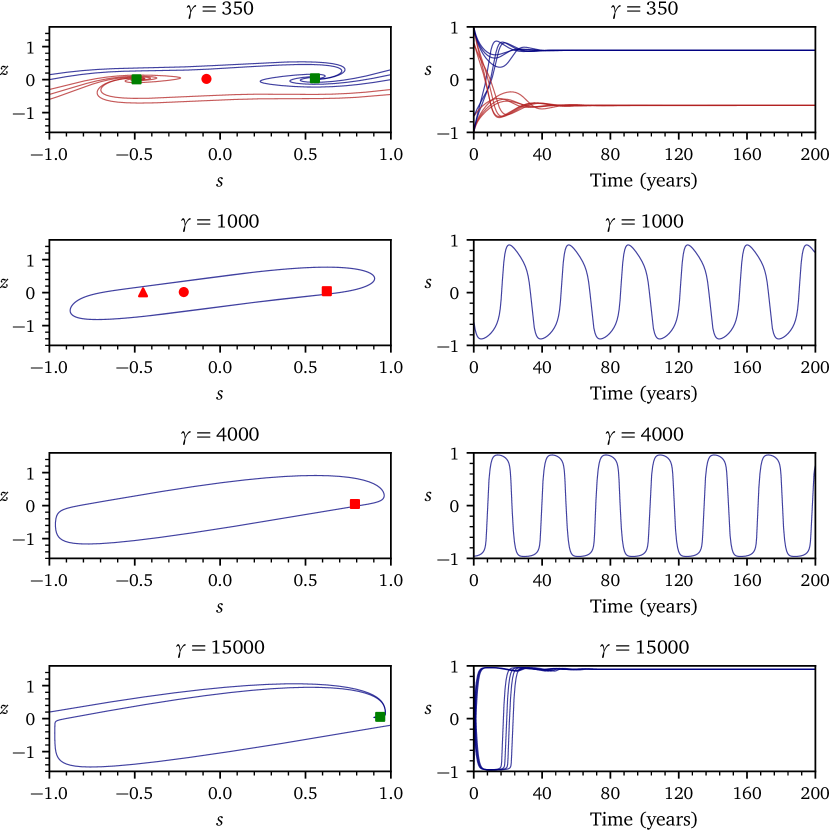

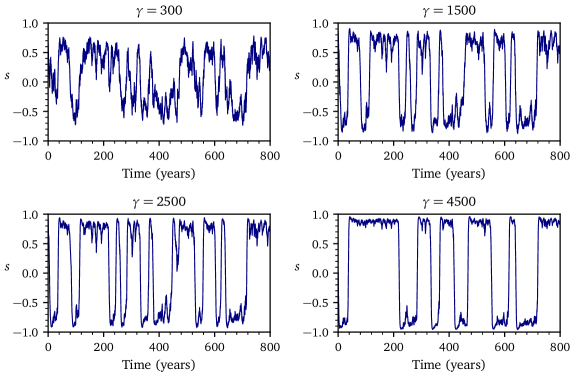

This dynamical system is parametrized and examined in detail in C. For the relevant range of parameters it has three equilibria: a stable focus where sentiment is positive () and the economy is expanding (), a stable focus where sentiment is negative () and the economy is contracting () and an unstable saddle point in between.191919For convenience, we classify 3D equilibrium points using more familiar 2D terminology. As such: (i) the stable (unstable) node has three negative (positive) real eigenvalues; (ii) the focus has one real and two complex eigenvalues and is stable if the real eigenvalue and the real parts of complex eigenvalues are all negative and unstable otherwise; and (iii) the saddle is always unstable as it has three real eigenvalues that do not all have the same sign. In the figures, the stable points are green and unstable points are red, while the nodes are marked by triangles, foci by squares and saddles by circles. The location, basin of attraction and stability of the equilibria are primarily affected by the parameters (sensitivity to sentiment levels) and (sensitivity to economic feedback). In particular, an increasing strengthens convergence towards the equilibria, so the system acquires greater stability.

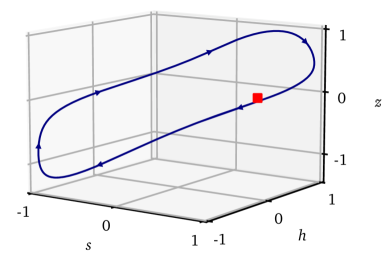

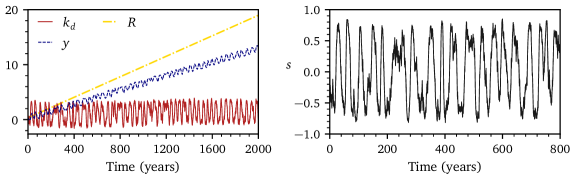

If is below a certain critical value, equations (24) generate a periodic limit cycle. The idea that limit cycles provide a mechanism of economic fluctuations dates back to Kalecki (1937), Kaldor (1940), Hicks (1950) and Goodwin (1951). The empirical irrelevance of periodic limit cycles led to a diminished interest in this research direction202020 Nevertheless, a similar line of research has been pursued in overlapping generations models and innovation cycles. See Hommes (2013) and Beaudry et al. (2020) for references. ; however, Beaudry et al. (2020) have reinitiated the discussion by proposing that cyclicality can arise from stochastic limit cycles “wherein the system is buffeted by exogenous shocks, but where the deterministic part of the system admits a limit cycle”. In our system, exogenous news noise similarly detunes limit cycle periodicity. This mechanism, however, cannot explain the “small shock, large crisis” effect or reproduce the general variability present in the real-world economy. At the other extreme, our system generates noise-prevailing behaviors with weak cyclicality. Neither extreme accurately reflects empirical observations and thus we seek a sensible balance between these features in a parameter regime that produces significant dynamic effects but precedes the limit cycle formation (C).

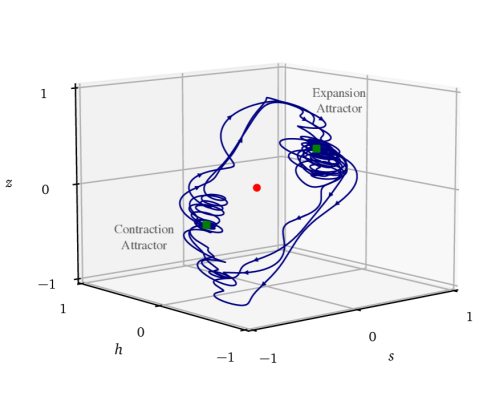

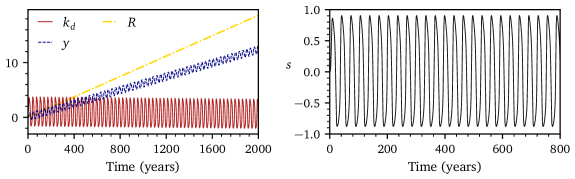

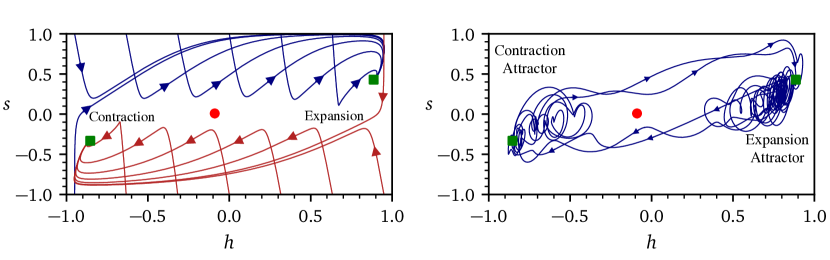

To this end, we consider a subcritical regime with above but close to its critical value at which the limit cycle emerges. In this situation, henceforth referred to as the coherence resonance regime, the foci are always stable, thus acting as attractors entrapping the economy. In Figures 3 and 4, we compare the phase portraits (i.e. the system trajectories for ) of the coherence resonance and limit cycle regimes. In the coherence resonance case, we take note of the unclosed largescale trajectories that pass near one attractor and converge to the other. These trajectories, which can be viewed as segments of a limit cycle, are the pathways along which the economy moves between contraction and expansion.

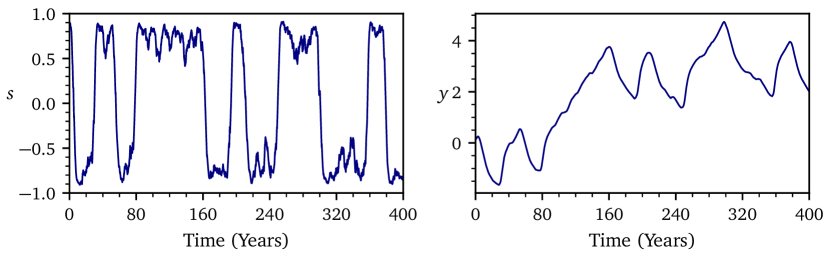

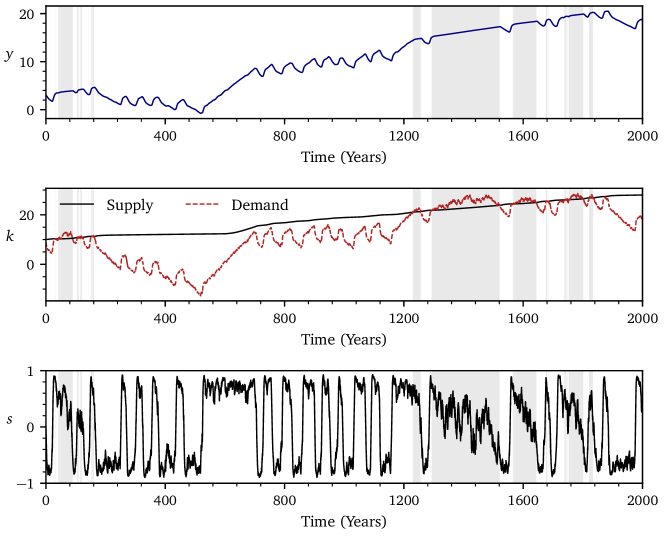

The dynamics of business cycles for nonzero are visualized in Figure 5. The economy’s trajectory displays distinctly bi-stable behavior as it spends most of its time near each focus and transits swiftly between them. When captive to an attractor, the trajectory follows an orbit around the corresponding focus, buffeted by exogenous noise , preventing it from settling. Simultaneously, the economy drifts slowly towards the boundary between attracting regions (Figure 4(left)), making it easier for a random news shock to thrust it across the boundary to be caught by the other attractor. The news shocks thus fulfill a dual purpose: they perturb the economy from equilibrium and provide a trigger that alternates the economic regime between expansions and recessions.

This mechanism can be classified as coherence resonance, a phenomenon whereby noise applied to a dynamical system leads to a quasiperiodic response (Pikovsky and Kurths, 1997). Coherence resonance normally occurs in bi-stable systems that are stochastically forced and in which key variables evolve on different timescales. The Dynamic Solow model satisfies these requirements: (i) news shocks provide a stochastic force; (ii) two stable equilibria emerge in the relevant parameter range; and (iii) the separation of characteristic timescales follows from the dynamics of corporate decision-making processes. The three-dimensionality of equations (24) introduces an important novel feature into the classic two-dimensional case of coherence resonance: the above-mentioned slow drift of the economy’s trajectory, which gradually increases the probability of regime transition.212121 This drift imposes a slow timescale on the frequency of the economy’s fluctuations by modulating the probability of regime transition. This effect was first observed and explained for a similar dynamical system in Kroujiline et al. (2019). This novel feature nonetheless leaves the basic mechanism unchanged: exogenous noise forces the economy across the boundary separating the regions of different dynamics, effectively reconnecting the trajectories between attractors. As a result, the economy undergoes quasiperiodic fluctuations consisting of alternating periods of expansion and recession punctuated by sharp transitions (as in Figure 6).

While both coherence resonance and limit cycle occur in the economically realistic range of parameters (see C), we will show that only coherence resonance is compatible with the long-term economic growth when studying the asymptotic convergence of capital supply and demand in the presence of fluctuations driven by the coherence resonance and limit cycle mechanisms in Section 4.2.

4 Business Cycles and Long-Term Growth in the General Case

While the supply- and demand-driven cases have been instructive for highlighting the mechanisms underlying economic dynamics, their applicability as standalone models is limited as supply and demand converge in the long run (equation (21)). As such, our primary focus is on the general case in which supply and demand coevolve, potentially leading to an interplay of supply- and demand-driven dynamics. We formulate the general case in Section 4.1, study long-term growth rates in Section 4.2 and examine economic fluctuations in Section 4.3.

4.1 Formulation of the General Case

In the general case, invested capital can alternate between (demand-driven regime) and (supply-driven regime) in accordance with the market clearing condition (20). As discussed in Section 2.1, firms’ decision-making processes are influenced by feedback from the economy. However, the supply-driven regime represents a special situation in which firms’ investment decisions do not affect economic output as production is determined in this case solely by capital availability. In other words, the supply-driven regime implies a Solow-type growth economy propelled by expectations of future consumption so high as to induce firms to utilize all capital supplied by households in production. Therefore, , which is positive in this regime, holds no additional information for managers, who are already overwhelmingly bullish about the economy. The idiosyncratic news remains the only source of nontrivial information, thereby becoming the focus of managers and analysts alike. Thus, economic feedback vanishes as a decision factor in the supply-driven regime.

Following this argument, we account for regime-dependent variation in feedback strength by introducing a regime-specific factor that regulates the impact of feedback in equation (19):

| (25) |

where

| (26) |

The Dynamic Solow model is then represented in the general case by the following system of equations:

| (27) | ||||

| (28) | ||||

| (29) | ||||

| (30) | ||||

| (31) | ||||

| (32) | ||||

| (33) |

where (27) is the dynamic equation governing production; (28) describes the motion of capital supply; (29)-(31) govern the feedback-driven dynamics that link information , sentiment and capital demand ; (32) defines the locally-inelastic market clearing condition; and (33) represents long-term market clearing that takes the form of an asymptotic boundary condition at large .

4.2 Growth and Convergence in the Long Run

The Dynamic Solow model (27)-(33) covers two regimes with different dynamics: a demand-driven regime with endogenous fluctuations and a supply-driven regime without them. Both regimes are expected to participate in the model’s general case, owing to the convergence of supply and demand in the long run under equation (33).

Equation (33) is central to our present analysis. Based on the regime definitions, this equation is satisfied when supply grows faster than demand in the supply-driven regime and, conversely, when demand grows faster than supply in the demand-driven regime. Under the demand-driven regime, the two possible mechanisms of fluctuations – limit cycle and coherence resonance – may entail different growth rates, validating the mechanism if demand grows fast enough to satisfy (33) and invalidating it otherwise.

This section aims to determine (i) the impact of fluctuations on growth; (ii) the mechanism of fluctuations compatible with equation (33); and (iii) the actual growth dynamics realized in the model. We first consider separately the supply- and demand-driven regimes (Sections 4.2.1 and 4.2.2) and then tackle the general case (Section 4.2.3). D provides the derivations of the equations herein.

4.2.1 Asymptotic Growth in the Supply-Driven Case ()

We show in D that the economy’s long-term growth in the supply-driven case is given by

| (34) | ||||

| (35) |

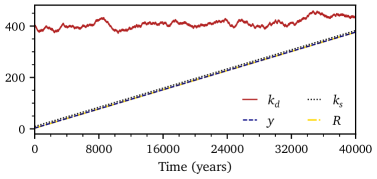

where , and represent, respectively, the log output, log supply and log demand growth rates; is the capital share in production; and denotes the classic Solow growth rate. As expected, the growth rate is not influenced by demand dynamics and matches . These estimates are verified by numerical simulations (see Figure 7). Note that supply always catches up with demand as in this case.

4.2.2 Asymptotic Growth in the Demand-Driven Case ()

We show in D that the economy’s long-term growth in the demand-driven case satisfies

| (36) |

According to this equation, output becomes dependent on demand, which itself undergoes endogenous fluctuations, and thus demand dynamics affect the long-term behavior of the economy. The magnitude of determines whether the economy expands faster or slower than the classic Solow economy: if and if (the latter condition including an important case when that yields an especially slow growth rate ). Next, we estimate numerically under the effect of limit cycle and coherence resonance.

Figure 8 depicts the growth dynamics driven by a periodic limit cycle (). We observe that stays close to zero and and match closely in accordance with (36), meaning the economy grows only through improvements in production efficiency. Figure 9 displays similar dynamics for the limit cycle perturbed by exogenous noise . It follows that limit cycles, whether periodic or stochastic, lead to a growth rate of less than .

The above result can be explained by noting that an economy on a limit cycle trajectory spends roughly an equal amount of time in expansion () as in contraction () and, consequently, exhibits on this trajectory a long-term average value of zero. In D, we find that is proportional to the long-term average of , implying tends to zero as well; therefore, demand can never catch up with supply due to the difference in their growth rates. In sum, the fluctuations generated by a limit cycle detract from long-term growth and fail to satisfy equation (33).

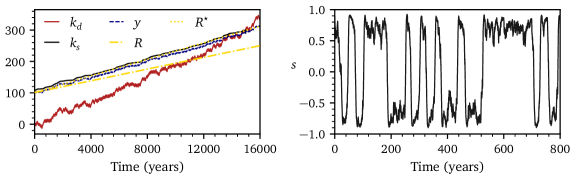

Coherence resonance induces a drastically different long-term dynamic despite the visually similar fluctuations (see Figure 10). Demand grows asymptotically at , leading to accelerated economic growth of in accordance with equation (36). This fast-paced growth, made possible by excess capital, , available for investment in the demand-driven regime, is explained by technological progress (), causing the economy to spend on average more time in expansion than contraction. We further observe that ; that is, demand grows faster than both supply and output.222222This result is consistent with equation (36), which can be rewritten as , so that since and . Therefore, demand powered by coherence resonance always catches up with supply.

4.2.3 Asymptotic Growth in the General Case

We have shown that fluctuations affect growth in the demand-driven regime of the Dynamic Solow model. In particular, limit cycles generate fluctuations that contribute negatively to growth, thus failing to satisfy the asymptotic boundary condition (33). Therefore, such fluctuations cannot be realized, which rules out limit cycles as the mechanism responsible for business cycles.

By contrast, coherence resonance produces fluctuations that contribute positively to growth, so that demand always catches up with supply. As this occurs, the system transits into the supply-driven regime in which supply grows faster than demand. Once supply has exceeded demand, the system switches back into the demand-driven dynamics. The regime cycle has thus come full circle, ensuring (33) is satisfied in the long run. As such, the economy’s path realized in the general case is forged by a regime interplay where the supply-driven equilibrium dynamics and the demand-driven fluctuations, powered by coherence resonance, continuously succeed one another.

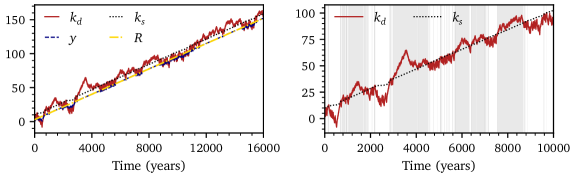

Our simulations show the economy grows asymptotically at the Solow rate . This result is not entirely unexpected. As capital supply and demand converge over the long run, capital invested into production during the supply- and demand-driven regime segments of the economy’s trajectory must also match asymptotically, as follows from (32). Consequently, the economy’s average growth rate across supply-driven segments is equal to the average growth rate across demand-driven segments. As the economy expands at in the supply-driven regime, the same growth rate is achieved, on average, across the demand-driven segments,232323The demand-driven economy cannot reach the asymptotic growth rate as a result of the segments’ finite duration and an adverse growth bias due to the typical alignment of demand-driven segments with recessionary periods. meaning is also the overall rate of expansion. Figure 11 displays a simulation capturing the realized asymptotic growth path in the general case and highlights the interplay of the supply- and demand-driven dynamics.

To sum up, the asymptotic growth rates in the demand-driven regime depend on the mechanism underlying economic fluctuations. Fluctuations driven by a limit cycle cannot be realized since they do not satisfy the convergence between supply and demand in the long run. The economy’s trajectory realized in the general case of the Dynamic Solow model consists of a chain of supply-driven regimes in which the economy experiences the equilibrium growth and demand-driven regimes in which fluctuations emerge via coherence resonance. Overall, the economy grows asymptotically at the classic Solow rate . Although fluctuations can cause large excursions from this equilibrium growth path, the deviations disappear on the large timescales relevant for the convergence of supply and demand.

4.3 Business Cycle Dynamics

Our analysis of asymptotic growth in the preceding section has led us to conclude that coherence resonance is the relevant endogenous mechanism underlying economic dynamics as it enables the convergence of capital demand and supply over the long run. In this section, we focus on the intermediate timescale to examine endogenous fluctuations produced by the Dynamic Solow model (27)-(33) in the coherence resonance regime.

.

Figure 12 depicts a typical realization of the economy’s trajectory over the medium term. The economy undergoes a sequence of supply- and demand-driven dynamic behaviors, as indicated, respectively, by shaded and unshaded segments. In the demand-driven case, in which demand is below supply, sentiment (lower panel) exhibits distinctively bi-stable behavior, staying for long periods near the positive (expansion) and negative (contraction) equilibria and traversing quickly the distance between them during economic regime transitions. This sentiment behavior leads to fluctuations in demand (middle panel) that, in turn, induce business cycles around the long-term growth trend (upper panel). Conversely, during periods when supply is the limiting factor, sentiment follows a random walk due to the absence of economic feedback and the supply-driven economy exhibits the equilibrium growth dynamics.

The long-term simulations demonstrate that demand stays below supply on average of the time. This can be interpreted as the firms’ decision to hold excess capital (as, for example, noted in Fair, 2020) as the entire capital supply is made available to firms, implying a capital utilization rate below 100% over extended periods.242424The utilization rate measures current production as a proportion of potential production. In our context, the analogous measure is the ratio of capital in production in the demand-driven regime to capital available . For empirical evidence of firms holding excess capital, see the FRED series “Capacity Utilization: Total Index” (CAPUTLB50001SQ) or the Census Bureau’s National Emergency Utilization Rate. See also Murphy (2017) for a study of the persistence of excess capital.

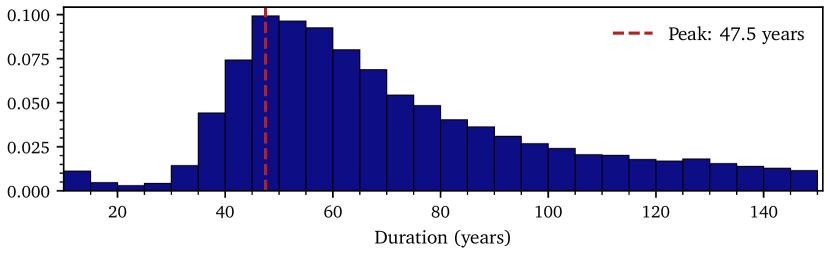

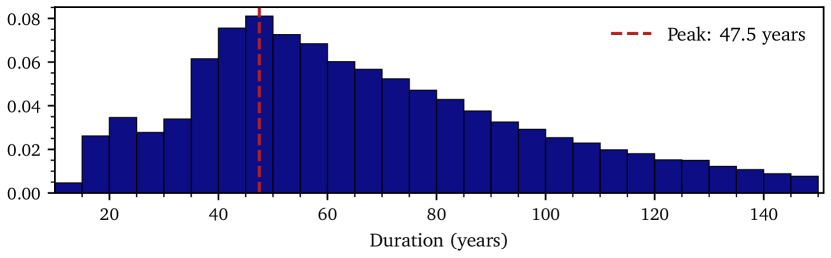

Figure 13 is a histogram of business cycle periods simulated by the model. It displays a wide distribution with a peak in the 40-70 year interval (with over 50% of the periods falling into this range), indicating the presence of quasiperiodic fluctuations. To confirm the source of these fluctuations, we inspect the distribution of the lengths of sentiment cycles, defined as the roundtrip of sentiment between the positive and negative equilibria (such as those depicted in the lower panel in Figure 12). This distribution, shown in Figure 14, also peaks at 40-70 years. It follows that business cycles are, as expected, linked to sentiment transitions from one equilibrium to the other driven by coherence resonance. Therefore, we affirm coherence resonance is the relevant mechanism forming the quasiperiodic fluctuations in output captured in Figure 13.

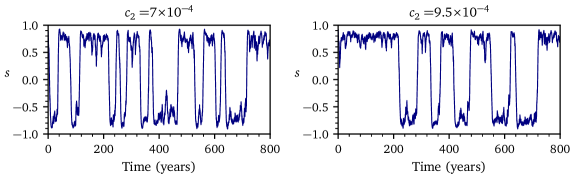

In C, we show that parameter , which defines the sensitivity of capital demand to sentiment, is key to the business cycle duration: the lower , the shorter the average duration of business cycles. We also show there that the model admits coherence resonance only if is above a certain critical value and tune the model to be in a regime with close to this value. It follows that coherence resonance – as a mechanism of business cycles driven by firms’ investment – imposes a natural minimum duration threshold, ruling out fluctuations with a characteristic timespan shorter than the Kondratieff-like 40-70 years.

In current literature, business cycles are typically estimated to last 8-12 years. However, a direct comparison of the duration would be misleading as our model, centered on capital demand dynamics, does not include links to the faster-paced processes, such as credit or equity market dynamics, that can accelerate business cycles through further interactions with the real economy. In other words, our model captures capital demand driven cycles, which are arguably just one of a number of fluctuation modes that reinforce or otherwise affect each other to produce the business cycles observed in the real world.

On that point, we take note of Kroujiline et al. (2019) that studies combined effects in a coupled macroeconomic system, attaching the interactions-based stock market model of Gusev et al. (2015) (capable of producing relatively short-term endogenous cycles) to the simple phenomenological model of the economy of Blanchard (1981) (within which output follows slow relaxation dynamics) to obtain quasiperiodic fluctuations with the same frequency as observed business cycles. A natural next step would be to investigate whether a more advanced coupled system, where both the financial sector and the real economy experience nonlinear endogenous dynamics at different frequencies can replicate and explain observed macroeconomic behaviors in greater detail.252525Such as the stock market model of Gusev et al. (2015) and the present Dynamic Solow model of the economy, which share a similar framework for micro-level interactions.

5 Conclusion

In this paper we have developed the Dynamic Solow model, a tractable macroeconomic model that captures dynamic behaviors across multiple timescales, and applied it to study economic fluctuations and their impact on long-term growth.

Our model consists of a dynamic capital demand component, representing an interactions-based process whereby firms determine capital needs and make investment decisions, and a simple capital supply component in the form of a Solow growth economy. These components are interlinked via a capital market, which comprises a local inelastic market clearing condition reflecting short-term price rigidity and an asymptotic market clearing condition valid for timescales in which prices are sufficiently flexible to match supply and demand. Starting from the micro-level interactions among firms, we derived the macroscopic equations for capital demand that constitute the dynamic core of the model and attached them to a capital motion equation for a static representative household (providing a dynamic version of the Cobb-Douglas production equation to capture short-term processes) and the aforementioned market clearing conditions. As a result, we have obtained a closed-form nonlinear dynamical system that allows for the examination of a broad range of economic behaviors.

The Dynamic Solow model admits two characteristic regimes, depending on whether capital demand exceeds supply or not. When demand exceeds supply, supply drives output and the dynamic demand component decouples from the rest of the economy, placing the economy on the familiar equilibrium growth path. Otherwise, demand drives output and the model is shown, for economically realistic parameters, to possess two attracting equilibria, one where the economy contracts and the other where it expands. This bi-stable geometry gives rise to business cycles manifested as endogenous fluctuations, wherein the economy’s long entrapment in recessions and expansions is punctuated by rapid alternations between them. We show that, in our model, the economy’s realized trajectory is forged by an interplay of these regimes such that the supply-driven equilibrium dynamics and demand-driven fluctuations continuously succeed one another. We further show that the economy spends around 70% of its time in the demand-driven regime, indicating fluctuations represent a prevalent economic behavior.

We identify a coherence resonance phenomenon, whereby noise applied to a dynamical system leads to a quasiperiodic response, to be the mechanism behind demand-driven fluctuations. In our model, exogenous noise (representing news received by analysts) instigates the economy’s transition from one equilibrium to the other, resulting in recurrent booms and busts. As such, news shocks act as a catalyst, which is compatible with the “small shocks, large cycle” effect observed in the real-world economy. In addition, under a different range of parameter values, we obtain a stochastic limit cycle (i.e. a limit cycle perturbed by exogenous noise) likewise capable of generating endogenous fluctuations. We show, however, that this type of fluctuations cannot be realized as the growth dynamics induced by it do not allow supply and demand to converge in the long run. While both limit cycle and coherence resonance mechanisms are hardwired in our model, in the sense that the parameter ranges must be appropriately selected, we conjecture that in reality the economy self-regulates towards the coherence resonance parameter ranges via long-term price adjustment responsible for the convergence of supply and demand in the long run.

The distribution of the business cycle periods simulated by our model displays a peak in the Kondratieff range of 40-70 years, demonstrating the quasiperiodic character of demand-driven fluctuations. We further find coherence resonance imposes a minimum duration threshold that rules out fluctuations peaking at shorter lengths. This result seems sensible because our model, centered on capital demand dynamics, has no links to faster-paced processes (such as credit or equity market dynamics) that can accelerate fluctuations to be in line with the observed business cycles. A natural extension would be to develop a coupled system, within which both the financial sector representing such faster-paced processes and the real economy experience nonlinear endogenous dynamics at different characteristic frequencies.

Our simulations show that although demand-driven fluctuations occasionally cause large excursions from the equilibrium growth path, the deviations vanish in the long run as supply and demand converge. In our model, the equilibrium growth path is defined by the Solow growth rate in which technology growth appears, simplistically, as a fixed exogenous parameter. From this perspective, endogenizing technological progress in the model may help better understand the long-term impact of fluctuations on growth, presenting an intriguing topic for future research.

6 Acknowledgments

We deeply thank J.-P. Bouchaud who contributed to the early stages of this work and Dmitry Ushanov for contributing ideas on the numerical analysis of the model. We also thank Mikhail Romanov for helpful comments and suggestions. This research was conducted within LGT Capital Partners and the Econophysics & Complex Systems Research Chair, the latter under the aegis of the Fondation du Risque, the Fondation de l’Ecole polytechnique, the Ecole polytechnique and Capital Fund Management. Maxim Gusev and Dimitri Kroujiline are grateful to LGT Capital Partners for financial support. Karl Naumann-Woleske also acknowledges the support from the New Approaches to Economic Challenges Unit at the Organization for Economic Cooperation and Development (OECD).

References

- Aghion and Howitt (1992) Aghion, P., Howitt, P., 1992. A Model of Growth Through Creative Destruction. Econometrica 60, 323–351. doi:10.2307/2951599.

- Aghion and Howitt (2006) Aghion, P., Howitt, P., 2006. Joseph Schumpeter Lecture Appropriate Growth Policy: A Unifying Framework. Journal of the European Economic Association 4, 269–314. doi:10.1162/jeea.2006.4.2-3.269.

- Angeletos et al. (2020) Angeletos, G.M., Collard, F., Dellas, H., 2020. Business-Cycle Anatomy. American Economic Review 110, 3030–3070. doi:10.1257/aer.20181174.

- Angeletos and La’O (2013) Angeletos, G.M., La’O, J., 2013. Sentiments. Econometrica 81, 739–779. doi:10.3982/ECTA10008.

- Arrow (1962) Arrow, K.J., 1962. The Economic Implications of Learning by Doing. The Review of Economic Studies 29, 155–173. doi:10.2307/2295952.

- Bakas et al. (2019) Bakas, D., Chortareas, G., Magkonis, G., 2019. Volatility and growth: A not so straightforward relationship. Oxford Economic Papers 71, 874–907. doi:10.1093/oep/gpy065.

- Beaudry et al. (2020) Beaudry, P., Galizia, D., Portier, F., 2020. Putting the Cycle Back into Business Cycle Analysis. American Economic Review 110, 1–47. doi:10.1257/aer.20190789.

- Beaudry and Portier (2014) Beaudry, P., Portier, F., 2014. News-Driven Business Cycles: Insights and Challenges. Journal of Economic Literature 52, 993–1074.

- Benhabib and Farmer (1999) Benhabib, J., Farmer, R.E.A., 1999. Chapter 6 Indeterminacy and sunspots in macroeconomics, in: Handbook of Macroeconomics. Elsevier. volume 1, pp. 387–448. doi:10.1016/S1574-0048(99)01009-5.

- Bernanke et al. (1996) Bernanke, B., Gertler, M., Gilchrist, S., 1996. The Financial Accelerator and the Flight to Quality. The Review of Economics and Statistics 78, 1–15.

- Blanchard (1981) Blanchard, O.J., 1981. Output, the stock market, and interest rates. The American Economic Review 71, 132–143.

- Boldrin and Woodford (1990) Boldrin, M., Woodford, M., 1990. Equilibrium models displaying endogenous fluctuations and chaos: A survey. Journal of Monetary Economics 25, 189–222. doi:10.1016/0304-3932(90)90013-T.

- Bouchaud (2013) Bouchaud, J.P., 2013. Crises and Collective Socio-Economic Phenomena: Simple Models and Challenges. Journal of Statistical Physics 151, 567–606.

- Brock and Durlauf (2001) Brock, W., Durlauf, S., 2001. Interactions-based models, in: Handbook of Econometrics. Elsevier, pp. 3297–3380.

- Christiano et al. (2018) Christiano, L.J., Eichenbaum, M.S., Trabandt, M., 2018. On DSGE Models. Journal of Economic Perspectives 32, 113–140. doi:10.1257/jep.32.3.113.

- Cooley and Prescott (1995) Cooley, T., Prescott, E., 1995. Economic growth and business cycle, in: Frontiers of Business Cycle Research. Princeton University Press, Princeton, N.J.

- Cooper and John (1988) Cooper, R., John, A., 1988. Coordinating Coordination Failures in Keynesian Models. The Quarterly Journal of Economics 103, 441–463. doi:10.2307/1885539.

- Cyert and March (1992) Cyert, R.M., March, J.G., 1992. Behavioral Theory of the Firm. 2nd edition ed., Wiley-Blackwell, Cambridge, Mass., USA.

- Da et al. (2021) Da, Z., Huang, X., Jin, L.J., 2021. Extrapolative beliefs in the cross-section: What can we learn from the crowds? Journal of Financial Economics 140, 175–196. doi:10.1016/j.jfineco.2020.10.003.

- Dawid and Delli Gatti (2018) Dawid, H., Delli Gatti, D., 2018. Agent-Based Macroeconomics, in: Handbook of Computational Economics. Elsevier. volume 4, pp. 63–156. doi:10.1016/bs.hescom.2018.02.003.

- Dosi et al. (2015) Dosi, G., Fagiolo, G., Napoletano, M., Roventini, A., Treibich, T., 2015. Fiscal and monetary policies in complex evolving economies. Journal of Economic Dynamics and Control 52, 166–189. doi:10.1016/j.jedc.2014.11.014.

- Dosi et al. (2010) Dosi, G., Fagiolo, G., Roventini, A., 2010. Schumpeter meeting Keynes: A policy-friendly model of endogenous growth and business cycles. Journal of Economic Dynamics and Control 34, 1748–1767. doi:10.1016/j.jedc.2010.06.018.

- Fair (2020) Fair, R.C., 2020. Some important macro points. Oxford Review of Economic Policy 36, 556–578. doi:10.1093/oxrep/graa011.

- Fernald (2016) Fernald, J.G., 2016. Reassessing Longer-Run U.S. Growth: How Low? Federal Reserve Bank of San Francisco, Working Paper Series , 01–25doi:10.24148/wp2016-18.

- Gandolfo (2009) Gandolfo, G., 2009. Economic Dynamics. Fourth ed., Springer-Verlag, Berlin Heidelberg.

- Goodwin (1951) Goodwin, R., 1951. The Nonlinear Accelerator and the Persistence of Business Cycles. Econometrica 19, 1–17. doi:10.2307/1907905.

- Greenwood and Shleifer (2014) Greenwood, R., Shleifer, A., 2014. Expectations of Returns and Expected Returns. The Review of Financial Studies 27, 714–746. doi:10.1093/rfs/hht082.

- Griskevicius et al. (2008) Griskevicius, V., Cialdini, R., Goldstein, N., 2008. Applying (and Resisiting) Peer Influence. MIT Sloan Management Review 49.

- Gusev and Kroujiline (2020) Gusev, M., Kroujiline, D., 2020. A Simple Economic Model with Interactions. SSRN Scholarly Paper ID 3552539. Social Science Research Network. Rochester, NY. doi:10.2139/ssrn.3552539.

- Gusev et al. (2015) Gusev, M., Kroujiline, D., Govorkov, B., Sharov, S.V., Ushanov, D., Zhilyaev, M., 2015. Predictable markets? A news-driven model of the stock market. Algorithmic Finance 4, 5–51. doi:10.3233/AF-150042.

- Haag and Weidlich (1983) Haag, G., Weidlich, W., 1983. Concepts and Models of a Quantitative Sociology: The Dynamics of Interacting Populations. First ed., Springer.

- Hicks (1937) Hicks, J.R., 1937. Mr. Keynes and the "Classics"; A Suggested Interpretation. Econometrica 5, 147–159. doi:10.2307/1907242.

- Hicks (1950) Hicks, J.R., 1950. A Contribution to the Theory of the Trade Cycle. Oxford University Press, Oxford.

- Hommes (2013) Hommes, C., 2013. Behavioral Rationality and Heterogeneous Expectations in Complex Economic Systems. Cambridge University Press, Cambridge. doi:10.1017/CBO9781139094276.

- Hommes and LeBaron (2018) Hommes, C.H., LeBaron, B.D., 2018. Handbook of Computational Economics. Volume 4, Heterogeneous Agent Modeling. volume 4 of Handbook of Computational Economics. North Holland, Amsterdam.

- Ising (1925) Ising, E., 1925. Beitrag zur Theorie des Ferromagnetismus. Zeitschrift für Physik 31, 253–258. doi:10.1007/BF02980577.

- Kaldor (1940) Kaldor, N., 1940. A Model of the Trade Cycle. The Economic Journal 50, 78–92. doi:10.2307/2225740.

- Kalecki (1937) Kalecki, M., 1937. A Theory of the Business Cycle. The Review of Economic Studies 4, 77–97. doi:10.2307/2967606.

- Kaplan and Violante (2018) Kaplan, G., Violante, G.L., 2018. Microeconomic Heterogeneity and Macroeconomic Shocks. Journal of Economic Perspectives 32, 167–194. doi:10.1257/jep.32.3.167.

- Keynes (1936) Keynes, J.M., 1936. The General Theory of Employment, Interest, and Money. Macmillan, London.

- Korotayev and Tsirel (2010) Korotayev, A.V., Tsirel, S.V., 2010. A Spectral Analysis of World GDP Dynamics: Kondratieff Waves, Kuznets Swings, Juglar and Kitchin Cycles in Global Economic Development, and the 2008–2009 Economic Crisis. Structure and Dynamics 4.

- Kroujiline et al. (2016) Kroujiline, D., Gusev, M., Ushanov, D., Sharov, S.V., Govorkov, B., 2016. Forecasting stock market returns over multiple time horizons. Quantitative Finance 16, 1695–1712. doi:10.1080/14697688.2016.1176241.

- Kroujiline et al. (2019) Kroujiline, D., Gusev, M., Ushanov, D., Sharov, S.V., Govorkov, B., 2019. An endogenous mechanism of business cycles. Algorithmic Finance , 1–22doi:10.3233/AF-190292.

- Kuchler and Zafar (2019) Kuchler, T., Zafar, B., 2019. Personal Experiences and Expectations about Aggregate Outcomes. The Journal of Finance 74, 2491–2542. doi:10.1111/jofi.12819.

- LeBaron and Tesfatsion (2008) LeBaron, B., Tesfatsion, L., 2008. Modeling Macroeconomies as Open-Ended Dynamic Systems of Interacting Agents. American Economic Review 98, 246–250. doi:10.1257/aer.98.2.246.

- Lorenz (1993) Lorenz, H.W., 1993. Nonlinear Dynamical Economics and Chaotic Motion. Second ed., Springer-Verlag, Berlin Heidelberg. doi:10.1007/978-3-642-78324-1.

- Miller and Cardinal (1994) Miller, C.C., Cardinal, L.B., 1994. Strategic Planning and Firm Performance: A Synthesis of More than Two Decades of Research. The Academy of Management Journal 37, 1649–1665. doi:10.2307/256804.

- Murphy (2017) Murphy, D., 2017. Excess capacity in a fixed-cost economy. European Economic Review 91, 245–260. doi:10.1016/j.euroecorev.2016.11.002.

- Pikovsky and Kurths (1997) Pikovsky, A., Kurths, J., 1997. Coherence resonance in a noise-driven excitable system. Physical Review Letters 78, 775–778.

- Priesmeier and Stähler (2011) Priesmeier, C., Stähler, N., 2011. Long dark shadows or innovative spirits? the effects of (smoothing) business cycles on economic growth: A survey of the literature. Journal of Economic Surveys 25, 898–912. doi:10.1111/j.1467-6419.2011.00694.x.

- Scheinkman (1990) Scheinkman, J.A., 1990. Nonlinearities in Economic Dynamics. The Economic Journal 100, 33–48. doi:10.2307/2234182.

- Schumpeter (1939) Schumpeter, J.A., 1939. Business Cycles: A Theoretical, Historical, and Statistical Analysis of the Capitalist Process. McGraw Hill, New York.

- Schumpeter (1942) Schumpeter, J.A., 1942. Capitalism, Socialism, and Democracy. Harper and Brothers, New York.

- Slanina (2013) Slanina, F., 2013. Essentials of Econophysics Modelling. Oxford University Press, Oxford. doi:10.1093/acprof:oso/9780199299683.001.0001.

- Solow (1956) Solow, R.M., 1956. A Contribution to the Theory of Economic Growth. The Quarterly Journal of Economics 70, 65. doi:10.2307/1884513.

- Solow (2005) Solow, R.M., 2005. Reflections on Growth Theory, in: Handbook of Economic Growth. Elsevier. volume 1, Part A, pp. 3–10.

- Stock and Watson (1999) Stock, J.H., Watson, M.W., 1999. Business Cycle Fluctuations in U.S. Macroeconomic Time Series, in: Taylor, J.B., Woodford, M. (Eds.), Handbook of Macroeconomics. Elsevier, New York. volume 1A, pp. 3–64. doi:10.3386/w6528.

- Suzuki and Kubo (1968) Suzuki, M., Kubo, R., 1968. Dynamics of the Ising Model near the Critical Point. I. Journal of the Physical Society of Japan 24, 51–60. doi:10.1143/JPSJ.24.51.

- Vines and Wills (2020) Vines, D., Wills, S., 2020. The rebuilding macroeconomic theory project part II: Multiple equilibria, toy models, and policy models in a new macroeconomic paradigm. Oxford Review of Economic Policy 36, 427–497. doi:10.1093/oxrep/graa066.

Appendix A Model Variables and Parameters

| Definition | Type | Base Case Value | |

| Production (Section 2.2) | |||

| Production | Variable | - | |

| Capital in production | Variable | - | |

| Log production | Variable | - | |

| Log capital in production | Variable | - | |

| Production characteristic timescale (business days) | Constant | ||

| Initial technology level | Constant | 1 | |

| Daily technology growth rate | Constant | ||

| Capital share in production | Constant | ||

| Capital Supply (Section 2.3) | |||

| Capital supply | Variable | - | |

| Log capital supply | Variable | - | |

| Proportion of income saved | Constant | ||

| Daily depreciation rate | Constant | ||

| Capital Demand (Section 2.4) | |||

| Capital demand | Variable | - | |

| Log capital demand | Variable | - | |

| Sentiment level | Variable | - | |

| Information level | Variable | - | |

| Capital demand sensitivity to | Constant | ||

| Capital demand sensitivity to | Constant | ||

| Sentiment herding factor | Constant | ||

| Sentiment sensitivity to | Constant | ||

| Feedback strength factor | Constant | ||

| News shocks | Exogenous noise | - | |

| Sentiment characteristic timescale (business days) | Constant | ||

| Information characteristic timescale (business days) | Constant | ||

| News shocks characteristic timescale (business days) | Constant | ||

| Limiting Cases (Section 3) | |||

| Production growth indicator | Variable | - | |

| Constant | 0.001 | ||

| General Case (Section 4) | |||

| Asymptotic growth rates of log variables | Variable | - | |

| Classic Solow growth rate (daily) | Constant | ||

| Technology growth timescale (business days) | Constant | ||

Appendix B Approximate Solution in the Supply-Driven Regime

In this appendix, we solve equation (22) approximately through use of the boundary layer technique and obtain the economy’s path in analytic form in the intermediate and long run under the supply-driven regime ().

The starting point of our derivation is equation (22), for convenience repeated here:

| (37) |

Recall that , where is the timescale in which output adjusts to changes in the level of capital and is the timescale of output growth in the long run. We aim to capture the dynamics on these two timescales by solving equation (37) on the interval . For simplicity, we assume that , which implies that is much larger than and on the interval , allowing us to derive a more compact solution.

First, we consider equation (37) for . In this outer region, and we can approximate the solution to (37) by the solution to equation:

| (38) |

which is given by

| (39) |

Next, we consider equation (37) on the interval , where and is not necessarily substantively smaller than . In this inner region, we can approximate the solution to (37) by the solution to

| (40) |

This is the Bernoulli equation and its solution is given by

| (41) |

where is the constant of integration.

Solutions and must match in the overlapping interval . This is satisfied for any value of since and , as follows from (39) and (41). Thus, we approximate the solution to equation (37) in this region by

| (42) |

The approximate solution to equation (37) that is uniformly valid for all is given by

| (43) |

where has been rescaled for convenience.

As a final step, we obtain the solution for output by inverting the equation of capital motion (4):

| (44) |

Note that on the interval due to the simplifying assumption . Therefore, the corresponding uniform approximation for output , valid for all , is given by

| (45) |

Appendix C Model Parameterization

In this appendix, we examine the model’s parameters and discuss how they affect the behavior of the dynamical system (24) in the phase space.

We begin with equation (24b) that describes sentiment dynamics. Parameter defines the relative importance of the herding and random behaviors of firms. In an unforced situation (), the number of stable equilibrium points, to which the firms’ sentiment converges, doubles at from one to two. For , random behavior prevails since there is a single equilibrium at , meaning firms fail to reach a consensus opinion. Conversely, for , herding behavior rules as equation (24b) generates a polarized, bi-stable environment with one pessimistic () and one optimistic () equilibrium states. It is sensible to assume , otherwise firms would unrealistically behave either randomly or in perfect synchronicity. We set , implying a slight prevalence of herding over randomness. In addition, we set to ensure that analysts’ influence on firms’ managers likewise appears in the leading order.

We now consider the information dynamics in (24c). The terms under the hyperbolic tangent describe the impacts of economic growth and exogenous news on the collective opinion of analysts . We assume these two sources of information are of equal importance. Thus, we expect that in the feedback term and we model as an Ornstein-Uhlenbeck process with an standard deviation and short decorrelation timescale . Note that and accordingly .

Finally, we inspect the economic dynamics in (24a). In this equation, different terms determine leading behaviors on separate timescales. We show in D that the last three terms (with technology growth rate estimated on the basis of observed total factor productivity) are in balance in the long run. However, if we consider short timescales, the change in sentiment becomes dominant. Thus, equation (24a) can be approximated in the short run as and we set . We also note that by construction to ensure that the term does not contribute to capital demand dynamics on short timescales. Hence we expect .

As highlighted in Section 2, there is a segregation of characteristic timescales that emerges naturally from the types of decisions faced by the different agents in the model: . This segregation facilitates the transfer of the impact of instantaneous news shocks across multiple timescales. The estimates for the timescales are discussed in Section 2.5.