Comparing Sequential Forecasters††footnotetext: This manuscript is published in Operations Research; see https://doi.org/10.1287/opre.2021.0792.

Abstract

Consider two forecasters, each making a single prediction for a sequence of events over time. We ask a relatively basic question: how might we compare these forecasters, either online or post-hoc, while avoiding unverifiable assumptions on how the forecasts and outcomes were generated? In this paper, we present a rigorous answer to this question by designing novel sequential inference procedures for estimating the time-varying difference in forecast scores. To do this, we employ confidence sequences (CS), which are sequences of confidence intervals that can be continuously monitored and are valid at arbitrary data-dependent stopping times (“anytime-valid”). The widths of our CSs are adaptive to the underlying variance of the score differences. Underlying their construction is a game-theoretic statistical framework, in which we further identify e-processes and p-processes for sequentially testing a weak null hypothesis — whether one forecaster outperforms another on average (rather than always). Our methods do not make distributional assumptions on the forecasts or outcomes; our main theorems apply to any bounded scores, and we later provide alternative methods for unbounded scores. We empirically validate our approaches by comparing real-world baseball and weather forecasters.

1 Introduction

| Forecasters | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| FiveThirtyEight111Source: https://projects.fivethirtyeight.com/2019-mlb-predictions/games/. | 37.9% | 41.0% | 52.7% | 58.7% | 37.3% | 40.5% | 48.5% |

| Vegas-Odds.com222Source: https://sports-statistics.com/sports-data/mlb-historical-odds-scores-datasets/. | 34.9% | 37.7% | 41.0% | 50.7% | 33.7% | 37.4% | 43.1% |

| Adjusted Win Percentage | 47.1% | 47.4% | 47.6% | 47.4% | 47.2% | 47.0% | 47.2% |

| K29 Defensive Forecast | 50.0% | 50.0% | 50.9% | 51.6% | 50.7% | 49.9% | 49.1% |

| Constant Baseline | 50.0% | 50.0% | 50.0% | 50.0% | 50.0% | 50.0% | 50.0% |

| Average Joe | 40.0% | 50.0% | 60.0% | 50.0% | 30.0% | 40.0% | 50.0% |

| Nationals Fan | 70.0% | 70.0% | 80.0% | 70.0% | 60.0% | 60.0% | 70.0% |

| Did the Nationals Win? | Yes | Yes | No | No | No | Yes | Yes |

Forecasts of future outcomes are widely used across domains, including meteorology, economics, epidemiology, elections, and sports. Often, we encounter multiple forecasters making probability forecasts on a regularly occurring event, such as whether it will rain the next day and whether a sports team will win its next game. Yet, despite the ubiquity of forecasts, it is not obvious how we can formally compare different forecasters on their predictive ability, particularly in a sequential setting where they each make a prediction on a sequence of outcomes (once for each outcome).

As an illustrative example, consider the probability forecasts made on each game of the 2019 World Series by real-world (and fictitious) forecasters in Table 1. It is not clear how we can effectively model the sequence of baseball game outcomes over time, and we also do not have full information on how each forecaster comes up with their predictions. As we observe these forecasts and outcomes game-by-game, we may see one forecaster appearing to be better than the other, according to some scoring rule. But how much of that difference can be attributed to chance or luck? How much evidence do we have that one forecaster has been “genuinely” better than another, even after accounting for chance, and can we quantify this evidence without having to make assumptions about reality or how the forecasts are made?

In this work, we derive statistically rigorous procedures for sequentially comparing forecasters via the powerful tool of confidence sequences (CS) (Darling and Robbins,, 1967; Lai, 1976b, ; Howard et al.,, 2021). CSs are sequences of confidence intervals (CIs) that provide time-uniform coverage guarantees, which allow valid sequential inference under continuous monitoring and at data-dependent stopping times. The parameter of interest in this paper is the time-varying mean difference in forecast scores up to time . Most CSs we develop in our paper are also nonasymptotically valid, meaning that their coverage guarantee holds at every time point .

In addition, we derive e-processes and p-processes (Ramdas et al.,, 2022) for testing whether one forecaster outperforms the other on average, which is a composite null that we formally define in Section 4.4. An e-process is a nonnegative process such that under the null, its expectation at any stopping time is at most one. It quantifies the amount of accumulated evidence against the null up to time : a larger is more evidence against the null. Further, is a p-process — its realization at any stopping time is a valid p-value, a property referred to as anytime-valid or always-valid (Johari et al.,, 2022; Howard et al.,, 2021). These are also formally defined in Section 4.4. Throughout the paper, we define safe, anytime-valid inference (SAVI) methods as ones that satisfy either the time-uniform coverage guarantee (CS) or the anytime-valid guarantee (e- or p-processes).

The setup in which we develop our methods is game-theoretic (Shafer and Vovk,, 2019): we posit that two players participate in a forecasting game on a sequence of outcomes with an unknown distribution. This setup naturally leads to “distribution-free” inference procedures — other than requiring bounded scoring rules, we make no assumptions on the time-varying dynamics of the outcomes and forecasts, such as stationarity. We further discuss how to relax even the assumption of bounded scores using asymptotic CSs (Section C) and normalized scores (Section D).

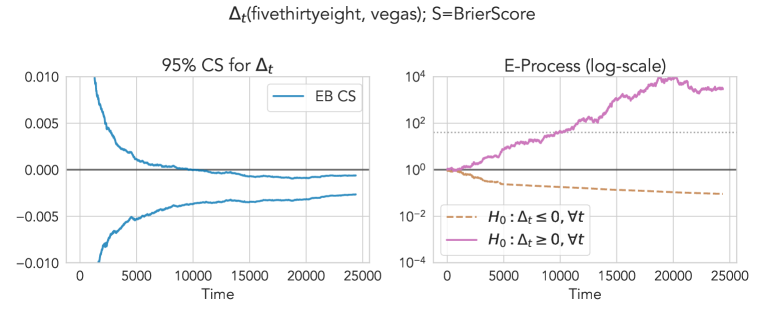

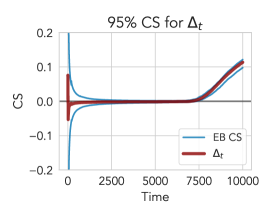

In Figure 1, we show an example of a CS and its corresponding e-processes applied to a forecasting game between two real-world forecasters, FiveThirtyEight and Vegas, on the outcomes of Major League Baseball (MLB) games. The CS in the left plot continuously tracks the expected average score differential over time and effectively visualizes the time-varying trend along with the uncertainty on its estimation. The two e-processes in the right plot each measure the accumulated evidence favoring each forecaster over time. In this example, both the CS and the e-processes show that Vegas has outperformed FiveThirtyEight on average. We return to this example in Section 5.2.

The rest of the paper is organized as follows. After discussing related work (Section 2) and preliminaries (Section 3), we derive CSs for the time-varying average forecast score differentials between two probabilistic forecasters in Sections 4.1-4.3, with the case of binary outcomes as a working example. In Section 4.4, we also derive e-processes and p-processes as duals to our CSs, providing alternative sequential inference procedures for forecast comparison. In Section 5.1, we empirically validate our CSs and compare them against fixed-time and asymptotic confidence intervals (CIs) on simulated data; in Sections 5.2 and 5.3, we apply our methods to real-world forecast comparison tasks, namely comparing game-by-game predictions in Major League Baseball (MLB) and comparing statistical postprocessing methods of ensemble weather forecasts. In addition, Section A contains omitted proofs; Section B contains technical details about the time-uniform boundary choices; Section C contains an alternative forecast comparison approach using an asymptotic CS; Sections D-F contain extensions to normalized scores (Winkler,, 1994), lag- forecasts, and predictable conditions/bounds, respectively; Section G contains extensions from binary outcomes to categorical and continuous outcomes; Section H contains detailed comparisons with the methods of Henzi and Ziegel, (2022); Diebold and Mariano, (1995); Giacomini and White, (2006); and Section I contains additional details about our simulated, MLB, and weather experiments as well as details about experimentally fine-tuning the CS width.

2 Related Work

Evaluation and Comparison of Forecasts.

Forecast evaluation is a well-studied subject in the literature of statistics, economics, finance, and climatology, dating back to the works of Brier, (1950); Good, (1952); DeGroot and Fienberg, (1983); Dawid, (1984); Schervish, (1989). The primary tool for evaluating forecasts is proper scoring rules, of which the literature is extensive. Many characterization theorems for proper scoring rules exist across different forecasting scenarios, notably including the case of probability forecasts for binary and categorical outcomes, point forecasts (e.g., mean, quantiles, and prediction intervals) for continuous outcomes, and fully probabilistic forecasts (e.g., densities and CDFs) for continuous outcomes. See, e.g., McCarthy, (1956); Savage, (1971); Schervish, (1989); Winkler et al., (1996); Grünwald and Dawid, (2004); Gneiting and Raftery, (2007); Gneiting, (2011); Abernethy and Frongillo, (2012); Dawid and Musio, (2014); Ehm et al., (2016); Ovcharov, (2018); Frongillo and Kash, (2021); Waggoner, (2021), for both classical and recent developments.

The problem of comparing forecasts while accounting for sampling uncertainty was first popularized in the case of probability forecasts by Diebold and Mariano, (1995) (DM), who proposed tests of equal (historical) forecast accuracy using the differences in forecast errors. The DM test is based on the asymptotic normality of the average forecast score differentials, and it makes stationarity assumptions about the outcomes. Giacomini and White, (2006) (GW) developed tests of conditional predictive accuracy given past information, allowing for the comparison of “which forecaster is more accurate given the information available at the time of forecasting.” The GW test thus allows for nonstationarity, although it restricts the forecasters to a fixed window size and its validity depends on mixing assumptions. Lai et al., (2011) presented a comprehensive overview of the aforementioned methods of forecast comparison and developed a martingale-based theory of scoring rules whose differentials are linear in the outcome, such as proper scoring rules. They proved the asymptotic normality of both forecast scores and score differentials, leading to an asymptotic and fixed-time CI that we use as a point of comparison in our work. More recent work by Ehm and Krüger, (2018); Ziegel et al., (2020); Yen and Yen, (2021) derive fixed-time tests of forecast dominance under all consistent scoring functions (Gneiting,, 2011). In comparison with all of these previous methods that presuppose a fixed sample size, the key difference in our work is that we develop inference methods that are valid at arbitrary data-dependent stopping times, while making virtually no assumption on the time-varying dynamics of the data generating process. The resulting graphical representations of CSs and e-processes also convey information about the entire time-varying trend of score differences, as in Figure 1, unlike classical tests and CIs that concern a single comparison at a fixed time point.

Recently, Henzi and Ziegel, (2022) constructed sequential tests of conditional forecast dominance based on e-processes (Howard et al.,, 2020; Grünwald et al.,, 2023; Shafer,, 2021; Ramdas et al.,, 2022; Vovk and Wang,, 2021). These methods are also anytime-valid and nonasymptotic; yet, they test a “strong333This distinction of strong and weak nulls come from the discussion of randomized experiments in causal inference; see, e.g., Lehmann, (1975); Rosenbaum, (1995). Within the context of forecast comparison, Ehm and Krüger, (2018) distinguish between tests of average and step-by-step conditional predictive ability, which mirrors that of weak and strong nulls. null,” which states that one forecaster is better than the other at every point in time, something we rarely believe a priori. Thus, rejecting the strong null only suggests that there exists some time point where the latter forecaster is better than the former, which may not come as much of a surprise. (One case where the strong null is appropriate is if we test two sets of forecasts produced by the same data scientist, with one forecaster using more features or more sophisticated models; but for two unrelated forecasters, we rarely expect the strong null to be true.) In contrast, our e-processes test whether one forecaster dominates the other on average over time (thus requiring consistent outperformance), and the CSs can even test such averaged nulls in a two-sided fashion (equivalently, it tests both one-sided nulls). We examine this distinction further in Sections 4.4 and 5.3; other methodological differences are summarized in Section H.1.

| Method & Key Result | Null Hypothesis | Weak | CI | SAVI | NA | DF |

| Diebold and Mariano, (1995) | ✗ | ✓ | ✗ | ✗ | ✗ | |

| Giacomini and White, (2006) | ✗ | ✗ | ✗ | ✗ | ✗ | |

| (: max. forecasting window) | ||||||

| Lai et al., (2011) | ✓ | ✓ | ✗ | ✓ | ✗ | |

| , | ||||||

| Henzi and Ziegel, (2022) | ✗ | ✗ | ✓ | ✓ | ✓ | |

| is an e-process, | ||||||

| Ours | ✓ | ✓ | ✓ | ✓ | ✓ | |

| is sub-exponential, | ||||||

| which yields a CS & an e-process | ||||||

Time-Uniform Confidence Sequences.

Confidence sequences were developed by Robbins and coauthors (Darling and Robbins,, 1967; Robbins,, 1970; Robbins and Siegmund,, 1970; Lai, 1976a, ). Recent renewed interests on CSs are partly due to best-arm identification in multi-armed bandits (Jamieson et al.,, 2014; Jamieson and Jain,, 2018), where CSs are sometimes referred to as always-valid or anytime confidence intervals. CSs are also duals to sequential hypothesis tests, analogously to CIs being dual to fixed-time hypothesis tests, and one can further derive a sequence of e-processes and p-processes given the CSs (more precisely, its underlying exponential process) (Ramdas et al.,, 2022). In Section 4.4, we make this connection explicit and discuss how our approach also leads to p-processes, or anytime-valid p-values (Johari et al.,, 2022), for weak nulls.

The recent work by Howard et al., (2021) is of particular importance in our paper, as it develops tight CSs that are uniformly valid over time under nonparametric assumptions and has widths that shrink to zero. This work and its underlying technique of developing exponential test (super)martingales (Howard et al.,, 2020; Darling and Robbins,, 1967; Ville,, 1939) have led to several interesting results, including state-of-the-art concentration inequalities for IID mean estimation (Waudby-Smith and Ramdas,, 2023) and sequential quantile estimation (Howard and Ramdas,, 2022). Our work makes the connection between the empirical Bernstein (EB) CSs derived in Howard et al., (2021) and the martingale property of forecast score differentials (Lai et al.,, 2011), leading to a novel sequential inference procedure for forecaster comparison.

3 Preliminaries

3.1 Test Supermartingales, Ville’s Inequality, and Confidence Sequences

The theory of martingales and their interpretation as a gambler’s wealth in a betting game are instrumental in deriving SAVI methods. See Ramdas et al., (2023) for a comprehensive introduction. Let be a measurable space equipped with a filtration , where each represents the accumulated information up to time . Given any probability distribution on , a sequence of random variables is called a process if it is adapted to , meaning that is -measurable for all . A process is also predictable w.r.t. if is -measurable for all . A stopping time w.r.t. is a nonnegative integer random variable that satisfies for all .

Let denote the conditional expectation w.r.t. under . A process is a supermartingale if and for each , and a martingale if “” is replaced with “”. A nonnegative supermartingale that starts at one () is called a test supermartingale (for ) (Shafer et al.,, 2011). If is a test supermartingale for , then Ville’s inequality (Ville,, 1939) states that, for any ,

| (1) |

Ville’s inequality is the primary tool for constructing confidence sequences, as illustrated in, e.g., Howard et al., (2021); in fact, it is the only admissible way to construct them (Ramdas et al.,, 2020). Given , a -confidence sequence (CS) for a time-varying sequence of target parameters is a sequence of confidence intervals (CIs) such that

| (2) |

In particular, the guarantee remains valid at arbitrary stopping times and without a prespecified sample size, so that collecting additional data over time does not invalidate it (Howard et al.,, 2021, Lemma 3):

| (3) |

This coverage guarantee at stopping times is sometimes referred to as being anytime-valid. This crucially differentiates a CS from a fixed-time CI, , which only has the following weaker guarantee:

| (4) |

In short, CSs, as opposed to CIs, are the appropriate tools for sequential inference.

3.2 Forecast Evaluation via Scoring Rules

Let be the space of all possible outcomes equipped with a -field . Let be the set of all probability distributions on and . To facilitate our discussion, the primary working example in this paper will be the space of binary outcomes and probability forecasts parametrized by their means in . But our setup can be generalized to any finite sample space with -dimensional probability forecasts , for , and -dimensional sample space , for , with point (e.g., mean and quantile) or probabilistic (e.g., CDF) forecasts. (We defer our discussion of these general cases to Section G.)

A scoring rule is any extended real-valued function444More formally, the scoring rule is required to be -quasi-integrable in its second argument, meaning that for every , is measurable and, for all , the integral exists as a possibly infinite but not indeterminate value (Bauer,, 2001; Abernethy and Frongillo,, 2012). and can be used to evaluate the performance of a (probabilistic) forecast given an observation . Following Gneiting and Raftery, (2007), we take scoring rules to be positively oriented, meaning that higher scores reflect better forecasts. A prominent example is the Brier score (Brier,, 1950), which in the binary case can be expressed as for and .

Given a forecast and a probability distribution , we can naturally extend the definition of a scoring rule to its expected score w.r.t. (conditional on ):

| (5) |

Here, we make the distinction between the scoring rule on and its expected score defined on by the notations and , respectively. We can recover the scoring rule from the expected score definition via , where is a point measure on .

A scoring rule is proper if any probability maximizes the expected score :

| (6) |

is strictly proper if the in (6) is unique. Intuitively, a proper scoring rule encourages forecasters to be honest, because if a forecaster believes that the outcome follows the distribution , then they are incentivized to honestly forecast , instead of any other distribution , as maximizes the expected score (uniquely, if is strictly proper) according to their belief. Proper scoring rules are often considered as the primary means of evaluating probabilistic forecasts, as they assess both calibration and sharpness (Winkler et al.,, 1996; Gneiting et al.,, 2007).

Classical examples of proper scoring rules for probability forecasts on binary outcomes include the following:

The Brier, spherical, and logarithmic scores are examples of strictly proper scoring rules, while the zero-one score is an example of a proper but not strictly proper scoring rule. An example of an improper scoring rule for probability forecasts is the absolute score, . Also note that all of the examples except the logarithmic score are bounded for and .

4 Anytime-Valid Inference for Average Forecast Score Differentials

In this section, we derive CSs and e-processes, as well as their corresponding sequential tests and p-processes, for the time-varying average difference in the quality of forecasts, as measured by a scoring rule. Our intuition comes from the extensive literature on evaluating and comparing probability forecasts via scoring rules (Winkler et al.,, 1996; Gneiting and Raftery,, 2007; DeGroot and Fienberg,, 1983; Schervish,, 1989; Gneiting,, 2011; Lai et al.,, 2011), combined with the powerful tool of time-uniform CSs (Darling and Robbins,, 1967; Howard et al.,, 2021). For now, our working example in this section will be the case of comparing probability forecasts on binary outcomes; we further discuss extensions to categorical and certain continuous outcomes in Section G.

4.1 A Game-Theoretic Formulation

The intuition behind our SAVI methods for forecast score differentials comes from the game-theoretic statistical framework (Shafer,, 2021; Ramdas et al.,, 2023). Consider a forecasting game where two players make probabilistic forecasts on an event that happens over time (e.g., whether it will rain on each day, whether a sports team will win its game each week, and more) and an unknown player named reality chooses a sequence of distributions that generates the outcomes that the forecasters are trying to predict. Let denote each round of the game. Though not required, we can also optionally allow having any historical data for some . The forecasting game can be formulated in general as follows — the case of probability forecasts on binary outcomes is obtained by setting ( would refer to ).

Game 1 (Comparing Sequential Forecasters).

For rounds :

-

1.

Forecasters 1 and 2 make their forecasts, , respectively. The order in which the forecasters make their forecasts is not specified.

-

2.

Reality chooses . is not revealed to the forecasters.

-

3.

is sampled and revealed to the forecasters.

We now elaborate on the role of each player in Game 1.

Forecasters 1 & 2.

At each round , the two forecasters can make their forecasts using any information available to them. This includes historical and previous outcomes , any of the previous forecasts made, , , as well as any other side information available to either forecaster. They cannot, however, make their predictions using any of ’s (or information from the future). For example, when predicting the outcome of the next baseball game, the forecasters’ filtration may include not only all of previous games’ results but also any side information that either forecaster may have, such as which players are starting the game and whether there are injuries. The setup also allows for the case where two forecasters have different side information, as our results are completely agnostic to such details.

This game-theoretic framework for forecast comparison is prequential (Dawid,, 1984), in the sense that we put no restrictions on how these forecasts are generated, and we only evaluate forecasters based on the forecasts they did make and the outcomes that did occur, as opposed to forecasts they would have made had the outcomes been different.

Reality.

In our game, Reality is the player that determines the unknown distribution of the eventual outcome conditioned on its past, which notably includes the forecasters’ choices and . In the binary case, for example, Reality chooses the conditional mean sequence of the outcomes given everything it has seen. Reality can essentially choose “however they want,” and they can even choose after seeing or . Put differently, the framework is agnostic to what information Reality sees: Reality may only see its past choices and (optionally) the past outcomes , or it may act adversarially after seeing and . In particular, could also be a point distribution at .

We note that the distribution-free property of our methods corresponds to the fact that the game places no distributional assumptions on the time-varying dynamics of , such as stationarity, Markovian or other conditional independence assumptions.

The Statistician.

The statistician, who stands outside of the game, has the goal of comparing the predictive performance of the two forecasters according to a chosen scoring rule and based only on the observed data , without making any assumptions about the behavior of any player involved.555Specifically, we do not explicitly consider strategic issues arising from (say) the choice of the scoring rule or the method of comparison. In other words, we consider the comparison problem separately from the elicitation problem (how to elicit honest forecasts). A separate line of work considers these important, but orthogonal, issues. The statistician may choose to update their inferential conclusions as the game progresses. How the statistician achieves such a goal will be the focus of the subsequent sections.

4.2 The Measure-Theoretic Setup

We now formalize Game 1 in the context of comparing the two probabilistic forecasters over time. Let and be two sequences of forecasts in , for a sequence of outcomes in . In the binary case, the forecasts will take values in and the outcomes in . We can define Game 1 in a measure-theoretic sense by specifying the associated filtrations, i.e., a sequence of “information sets” with which we perform inference. Our formulation is closely related to the setup of Lai et al., (2011), although we make the game-theoretic intuitions explicit.

The “Observable” Forecaster Filtration .

We first define the filtration with which the two forecasters generate their forecasts, denoted as . For each , let represent any information available to the forecasters before making their predictions at time , as described in the previous subsection. Mathematically, this means that , , and are adapted w.r.t. . Note that also includes the information available to the statistician, making this the “observable” filtration that contrasts with the “oracle” filtration (defined below).

The “Oracle” Game Filtration .

The game filtration, denoted as , represents all sets of information associated with Game 1. The parameter of interest (unknown to the statistician) is defined w.r.t. this “oracle” filtration. More precisely, for each , includes not only everything in but also any information available to Reality before the outcome is realized, including Reality’s choice . Mathematically, this implies that , , and are predictable w.r.t. , while is adapted w.r.t. . The setup allows for the flexible choices of Reality described in the previous subsection, as it does not preclude Reality’s actions in any way.

In the remainder of the paper, we use the notation to denote the conditional expectation with respect to the game filtration for each . In the case of binary (and categorical) outcomes, because the outcome distribution is completely specified by their mean, we simply let denote the (unknown) conditional mean of the outcome given for each , with a slight abuse of notation. In such cases, we have that

| (7) |

where refers to the conditional expectation over .

Comparing Sequential Forecasters via Average Forecast Score Differentials.

With the aforementioned setup, we can now use scoring rules to assess and compare the quality of the two forecasters over time. We define the average (forecast) score differential between the sequences of forecasts and , up to time , as the average difference in expected scores:

| (8) |

where denotes the expectation over conditioned on the game filtration , which includes both forecasts and as well as . The time-varying parameter provides an intuitive way of quantifying the difference in the quality of forecasts made up to time . We highlight that helps us infer whether one forecaster is better than the other on average (over time), as opposed to one strictly dominating the other (Giacomini and White,, 2006; Henzi and Ziegel,, 2022). This estimand is also used in Lai et al., (2011)’s asymptotic CI.

The parameter is not observable to the statistician or the forecasters, because reality’s moves are unknown and never observed. We thus define the empirical average (forecast) score differential as the unbiased estimate of each summand in (8), also averaged over time:

| (9) |

is completely observable to the statistician after time .

The statistician’s goal then becomes quantifying how far is from , while accounting for the uncertainty associated with sampling at each time . To this end, we define the pointwise (forecast) score differential and its empirical counterpart . Then, it is immediate that the cumulative sums of deviations, defined by and

| (10) |

forms a martingale, i.e., . Previous work including Seillier-Moiseiwitsch and Dawid, (1993); Lai et al., (2011) use this property to derive the asymptotic normality of empirical average score differentials. In the following sections, we illustrate how can further be uniformly and non-asymptotically bounded by constructing exponential test supermartingales. As a result, we will be able to estimate and cover using CSs and also test its sign using e-processes.

4.3 Time-Uniform Confidence Sequences for Average Score Differentials

4.3.1 Time-Uniform Boundaries and Exponential Test Supermartingales

We now show that we can uniformly bound the difference between and over time using uniform boundaries and test supermartingales. To do this, we start with a cumulative sum process as well as its intrinsic time , which is the variance process for (to be defined later). Our goal is then to uniformly bound the sum over the intrinsic time , which corresponds to bounding the difference between and over time due to (10).

Following Howard et al., (2020), for any sum process and its intrinsic times , we define a (one-sided) uniform boundary with crossing probability as any function of the intrinsic time that gives a time-uniform bound on the sums:

| (11) |

that is, with probability at least , the sums are upper-bounded by at all times . By similarly computing a uniform boundary to , we can also obtain a time-uniform lower bound on . (Alternatively, we can directly define a two-sided sub- uniform boundary, which satisfies . An example is Robbins, (1970)’s two-sided normal mixture that we describe in Section 4.3.4.) The upper and lower bounds then jointly form a time-uniform CS on by rearranging the terms.

How do we show that there exists such a uniform boundary for our definitions of ? Howard et al., (2020, 2021) show that there exists such a uniform boundary if, for each , the exponential process defined by and

| (12) |

is a test supermartingale w.r.t. . Here, is a “CGF-like” function (Howard et al.,, 2020), with a scale parameter , that controls how fast can grow relative to the intrinsic time . It is called a “CGF-like” function because it closely resembles (or equals) a cumulant generating function (CGF) of a mean-zero random variable. In this paper, we use two functions:

-

•

, which is the CGF of a centered Gaussian with variance ;

-

•

, which is a rescaled CGF of a centered Exponential with scale .

If is a test supermartingale for each for some , then we say that is sub- with variance process . In particular, we say that is sub-Gaussian or sub-exponential, with variance process and scale , if it is sub- or sub- respectively; these generalize the definitions of sub-Gaussian and sub-exponential random variables to cumulative sums w.r.t. intrinsic time. The uniform boundary defined using is then called a sub- uniform boundary.

Our goal is now to identify the conditions with which is indeed a test supermartingale and use different functions to obtain different uniform boundaries and hence CSs.

4.3.2 Warmup: Hoeffding-Style Confidence Sequences

We first derive an illustrative example of a CS for solely based on the sub-Gaussianity of the empirical pointwise score differentials . While the resulting CS is not the tightest one in our case, its derivation is simple enough to showcase the general pipeline for deriving CSs.

Recall the problem setup in Section 4.2, and for each , consider two probability forecasts on a binary outcome with unknown mean . Since , , and are all bounded, we know that the pointwise score differentials for are also bounded for many of the scoring rules we’ve discussed (e.g., for the Brier, spherical, and zero-one scores). If for some , we know that is -sub-Gaussian (Hoeffding,, 1963) conditioned on the game filtration , meaning that for all .

Now, for each , define the cumulative sum and the intrinsic time . It then follows that, for each , the exponential process given by is a test supermartingale:

| (13) |

Hence, there exists a sub-Gaussian uniform boundary for such that the time-uniform guarantee in (11) holds. By rearranging terms and also using the analogous argument for , we arrive at our first CS. Hereafter, the notation denotes the interval .

Theorem 1 (Hoeffding-style confidence sequences for ).

Suppose that is -sub-Gaussian conditioned on for , for some . Then, for any ,

| (14) |

where is any (one-sided) sub-Gaussian uniform boundary with crossing probability and scale (or alternatively, a two-sided version with crossing probability and scale ).

The statement (14) is equivalent to saying that, with probability at least , is contained in for all time , or that . This CS is called a Hoeffding-style CS, as it extends Hoeffding, (1963)’s inequality for the sums of independent sub-Gaussian random variables to the sequential case. In the sub-Gaussian case, it is also possible to construct a two-sided boundary without separately constructing a one-sided boundary. This is due to a classical result by Robbins, (1970) that we restate later in (17), so the upper and lower confidence bounds need not be constructed separately; in practice, the one-sided and two-sided variants are nearly identical (Howard et al.,, 2021). We further discuss the possible choices of the uniform boundary in Section 4.3.4.

The condition for Theorem 1 (and for Theorem 2 that will follow shortly) is satisfied by many scoring rules for probability forecasts on binary or categorical outcomes, including the Brier, spherical, and zero-one scores. For the unbounded logarithmic score, one can use its truncated variant for some small ; although the score is no longer proper, our methods remain valid. The condition is also satisfied for scoring rules on bounded continuous outcomes, such as Brier and quantile scores on -valued outcomes (See Section G).

4.3.3 Main Result: Empirical Bernstein Confidence Sequences

Now we are ready to present our main result, which is the derivation of a tight CS for . The key difference from the Hoeffding-style CS is that we now use an empirical estimate of the variance process for the cumulative sums, leading to a variance-adaptive CS that is often much tighter in practice.666The improvement from a Hoeffding-style CS to an empirical Bernstein CS mirrors the improvement from Hoeffding’s inequality to empirical Bernstein’s inequality for bounded random variables in the fixed-sample case. Recall the problem setup in Section 4.2 once again.

Theorem 2 (Empirical Bernstein confidence sequences for ).

Suppose that for each , for some . Also, let , where is any -valued predictable sequence w.r.t. . Then, for any ,

| (15) |

where is any sub-exponential uniform boundary with crossing probability and scale .

As before, the statement (15) is equivalent to saying that, with probability at least , is contained in for all time , or that . The proof is provided in Section A.2. Theorem 2 (and its proof) can be viewed as an extension of Theorem 4 in Howard et al., (2021) to our setup of sequential forecast comparison.

Like the Hoeffding-style CS in Theorem 1, the EB CS estimates the conditional predictive ability in an anytime-valid and distribution-free manner. The EB CS is further variance-adaptive because its width is a function of the empirical variance process , and we illustrate this empirically in Section 5. As before, we can use any bounded scoring rules, which in the binary and categorical cases include the Brier, spherical, and zero-one scores (proper), as well as the truncated logarithmic score (improper); scoring rules for bounded continuous outcomes can similarly be used. In addition, for unbounded proper scores for binary forecasts, such as the logarithmic score, we show in Section D that a normalized version of the average score differential, due to Winkler, (1994), can be used.

The choice of the uniform boundary is discussed in the following subsection. A reasonable choice for the predictable sequence is the average of previous score differentials, i.e., , although a smarter choice may lead to tighter CS. For the rest of this paper, our default choice of CS for will be that of Theorem 2, using , unless specified otherwise.

4.3.4 Choosing the Uniform Boundary via the Method of Mixtures

The specific choice of the uniform boundary controls the tightness of the CS across time, and an extensive list of choices for is covered in detail in Howard et al., (2021). While the simplest uniform boundaries are given as linear functions of the intrinsic time (Howard et al.,, 2020), curved uniform boundaries can produce CSs that are tighter across time. Here, we focus on a type of curved boundaries called the conjugate-mixture boundary; another option, called the polynomial stitching boundary, is also discussed in Section B.2. Either boundary type is applicable to both Theorems 1 and 2.

The conjugate-mixture (CM) boundary (Howard et al.,, 2021), denoted as , represents a class of uniform boundaries arising from the method of mixtures, the first instance of which was derived by Darling and Robbins, (1967). The key idea is summarized as follows. Since is a test supermartingale for every , it follows that for any distribution on , the mixture is also a test supermartingale. Choosing to be conjugate (in the Bayesian sense) to then gives a closed-form expression for . For example, if is sub-Gaussian with (Theorem 1), then choosing to be a Gaussian results in the normal mixture boundary (Robbins,, 1970); if is sub-exponential with (Theorem 2), then choosing as a Gamma results in a gamma-exponential mixture boundary.

To elaborate, by Lemma 2 of Howard et al., (2021), if is a test supermartingale for each and is any probability distribution on , then the following function is a sub- uniform boundary with crossing probability :

| (16) |

where . Because is a test supermartingale, Ville’s inequality says that , which in turn implies that . Similarly, if is also sub-, then the above procedure also gives the lower bound on .

Importantly, the uniform boundary (16) can be used for both Theorems 1 and 2, with the choice of differing in each case. For the Hoeffding-style CS in Theorem 1, a two-sided normal mixture boundary can be computed directly in closed-form by choosing to be (Robbins,, 1970):

| (17) |

where is a free parameter. In practice, can be chosen to optimize the width of the resulting CS at a pre-specified intrinsic time. A one-sided normal mixture boundary can also be derived in closed-form (Howard et al.,, 2021).

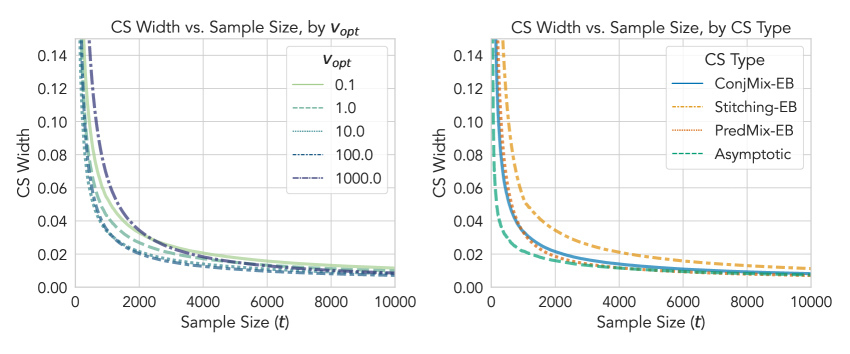

For the EB CS in Theorem 2, a one-sided gamma-exponential mixture boundary , with as a Gamma, can be computed efficiently using a numerical root finder ( has a closed form, and the boundary is obtained numerically; see Section B.1 for details). The one-sided boundary can be used for computing both the upper and lower confidence bounds of the EB CS. If a closed-form boundary is needed, then the polynomial stitching boundary (Section B.2) can be used. Also, while the CM boundary has an asymptotic rate of as illustrated in (17), it is usually tighter than the polynomial stitched boundary in practice. In fact, the CM boundary is unimprovable in the case of sub-Gaussian random variables without additional assumptions (Howard et al.,, 2021, Proposition 4).

| Type | CS | Intrinsic Time | Uniform Boundary |

| Hoeffding-Style | Normal Mixture | ||

| (Theorem 1) | Polynomial Stitching | ||

| Emp. Bernstein | , | Gamma-Exponential Mixture | |

| (Theorem 2) | predictable | Polynomial Stitching | |

Table 3 summarizes the choice of uniform boundaries and the CSs we derived for estimating . In our experiments, we use the conjugate-mixture uniform boundary by default, although we also perform an empirical comparison between the different choices as well as their hyperparameters in Section I.4. We use the publicly available implementation of the polynomial stitching and CM uniform boundaries by Howard et al., (2021).777https://github.com/gostevehoward/confseq

4.4 Sequential Tests, e-Processes and p-Processes

While our derivation so far has focused on CSs, we can also derive e-processes and p-processes (Shafer and Vovk,, 2019; Vovk and Wang,, 2021; Grünwald et al.,, 2023; Ramdas et al.,, 2020). In particular, an e-process can be derived as a lower bound on the exponential test supermartingale (12) that we used to construct the CS in the previous section. This correspondence is general to any exponential process upper-bounded by a test supermartingale, as noted in, e.g., Ramdas et al., (2020); Howard et al., (2021); our work utilizes this fact to introduce alternative sequential inference procedures with the same anytime-valid and distribution-free guarantees.

Weak and Strong Null Hypotheses.

Before deriving e- and p-processes, we first make clear the null hypotheses that correspond to the CS derived in Theorem 2. We define the weak one-sided null as

| (18) |

implies that, across all times , the first forecaster () is no better than the second forecaster () on average. Note that is a composite null, in the sense that it consists of all joint distributions on such that for all under . is analogously defined as .

We now illustrate how the CSs derived in Theorem 1 and Theorem 2 would correspond to sequential tests of the weak one-sided nulls and , drawing from the duality between CSs and sequential tests (Johari et al.,, 2022; Howard et al.,, 2021; Ramdas et al.,, 2020). Specifically, because the upper and lower confidence bounds are often constructed separately, the -level CS for denoted as satisfies with probability at least and that with probability at least . Thus, if for any time we find that or , then we can reject either or with high probability. More generally, the CSs readily provide a valid stopping rule for rejecting , a fact that we summarize in the following corollary. Below, we follow Robbins’ power-one testing framework which uses one-sided stopping rules that only stop on rejecting the null (and do not stop otherwise).

Corollary 1 (A sequential test for using a CS).

The stopping rule (19) is equivalent to deciding that has been better (worse) than if is entirely above (below) zero. The anytime-validity of this rule implies that the statistician can, e.g., periodically perform the test as increases and update their decision accordingly. On one extreme, the statistician can choose to perform the test after every round , or on the other extreme, they can test just once at a designated time (while leaving open the possibility of revisiting the experiment some time later). Compared to a standard hypothesis test for a stationary mean, the underlying can change its course over time, so in general it may not be sufficient to test once at in order to have power against the weak null. See Section 5 for an illustration and Section 6 for a further discussion.

We note that separately testing for both and is not equivalent to simply testing for , which is equivalent to . Rather, the sequential test (19) is the combination of two separate sequential tests in (19) for and , each at the significance level . The interpretation of the CS as two simultaneous sequential tests allows the user to continuously monitor the score differential on both sides via the CS-based stopping rule (19).

For the sake of comparison, we also define the strong one-sided null as

| (21) |

is defined analogously as . The recent work by Henzi and Ziegel, (2022) develops e-processes (defined in the next paragraph) and sequential tests for this null. In contrast to , corresponds to saying that the first forecaster () is no better than the second forecaster () at every time step . Thus, the strong null implies the weak null , but not vice versa. The critical distinction here is that rejecting only tells us that outperformed at some time step , but it does not tell us if either was better on average over time. To give a concrete example, fix (say, indicating Sundays), and define

| (22) |

In other words, is generally worse than but marginally better than every th time step (e.g., every Sunday). Because the strong null is false, any (powerful) sequential test for the strong null will reject it, and yet this may be a confusing conclusion as is generally a better forecaster.

Sub-exponential E-processes for the Weak Null.

We now show that the exponential test supermartingale underlying the CS in Theorem 2 can also be transformed to directly measure evidence against the weak one-sided null (rather than make a decision at a level ). Formally, an e-process (Ramdas et al.,, 2022) for a (possibly composite) null hypothesis is defined as a nonnegative process , starting at one (), such that:

| (23) |

where we define . The larger the value of , the more the evidence against the null. In particular, if the null is true, then it is unlikely to observe large values of the process at any stopping times (by Markov’s inequality, ). An e-process is anytime-valid by definition (23) (validity at arbitrary stopping times), analogous to the anytime-validity of a CS in Equation 3, and the term ‘process’ is also used to emphasize this property. An e-process can also be interpreted in a fully game-theoretic statistical sense: an e-process for a composite null measures the minimum wealth among bets against each member of the null (Ramdas et al.,, 2022), such that it only grows large when there is evidence against all members. At a fixed , is also called an e-variable, and its realization is called an e-value (Vovk and Wang,, 2021; Grünwald et al.,, 2023).

We can now define and show an e-process that corresponds to Theorem 2. (We can also define an analogous e-process corresponding to Theorem 1, but this is omitted due to space constraints.) The following e-process is for the weak one-sided null and is related to the lower confidence bound of the CS from Theorem 2; the e-process for is analogous and related to the upper confidence bound of the CS. Recall once again the problem setup in Section 4.2.

Theorem 3 (Sub-exponential E-processes for ).

Assume the same conditions as Theorem 2. Then, for each ,

| (24) |

Furthermore, given a probability distribution on , the mixture process is an e-process for .

The proof, provided in Section A.3, shows that under each , is upper-bounded by a exponential test supermartingale for , namely in (12). Because a process is upper-bounded by a test supermartingale for if and only if it is an e-process for (Ramdas et al.,, 2020), this establishes that is an e-process in the sense of (23). It then follows that , so is also an e-process.

The e-process of Theorem 3 is an anytime-valid inference procedure that provides a measure of accumulated evidence against the weak one-sided null at any stopping time. By definition, it is expected to be small under the weak null, and we only expect to see it grow large when the weak null does not hold. In comparison with Henzi and Ziegel, (2022)’s e-process for the strong null, we see that our e-process provides a more useful notion of evidence for saying that one forecaster outperforms another. In the example of (22), an e-process for the strong null can grow large, even though is generally a better forecaster; in contrast, our e-process (24) for the weak null is expected to remain small. In Section 5.3, we provide an empirical comparison of the two e-processes.

Choosing (or ) for E-processes.

Theorem 3 tells us that the expected value of and are bounded by 1 at all stopping times under the null, for any choice of or any mixture distribution . In practice, we default to using a mixture e-process with the conjugate distribution , as in Section 4.3.4. For the sub-exponential e-process, the gamma-exponential mixture as before provides a closed form for the function in (16), so that can be computed efficiently. The expression for is included in Section B.1.

P-processes.

Finally, we remark that any e-process for can also be converted into an p-process for , i.e., the sequence that satisfies: for any ,

| (25) |

A p-process evaluated at any stopping time , i.e. , is a p-value, but unlike a classical p-value, a p-process is valid at arbitrary stopping times.

Any e-process can be converted into a p-process via

| (26) |

following derivations from, e.g., Ramdas et al., (2020, 2022). We also remark that can alternatively be defined from a CS as the smallest for which the -level CS does not include zero (Howard et al.,, 2021), so all three notions (CS, e-process, and p-process) are closely related.

5 Experiments

In this section, we run both simulated and real-data experiments for sequential forecast comparison using our CSs as well as e-processes. All code and data sources for the experiments are made publicly available online at https://github.com/yjchoe/ComparingForecasters.

5.1 Numerical Simulations

As our first experiment, we compare our Hoeffding-style and EB CSs (Theorems 1 and 2, respectively) on simulated data with the asymptotic fixed-time CIs due to Theorem 2 of Lai et al., (2011). The main goal is to confirm that the CSs cover time-varying average score differentials uniformly, unlike the fixed-time CI, and are also nearly as tight as the CI.

In our simulated experiments, we also include an asymptotic CS for time-varying means, recently developed by Waudby-Smith et al., (2021), as an additional tool for anytime-valid inference. Asymptotic CSs can be viewed as alternatives to their non-asymptotic counterparts, including the ones we introduced in Section 4, and they trade off non-asymptotic validity to achieve versatility and also comparatively smaller widths at smaller sample sizes. A formal review of asymptotic CSs in the context of sequential forecast comparison is included in Section C.

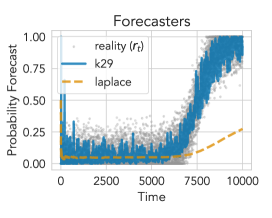

As for our simulated data, we generate a sequence of non-IID binary outcomes and compare different forecasters using our CSs. The overall simulation pipeline closely follows Game 1, with , , and . At each round , each forecaster makes a probability forecast , then reality chooses , and finally is sampled. The forecasts and are made only using the previous outcomes, i.e., . The Reality’s choices is specifically chosen to be non-IID and contain sharp changepoints, as shown in Figure 2. This serves as a challenging test case for the EB CS, as the sharp changepoints make it difficult to quickly adapt to the underlying variance. See Section I.1.1 for further details.

At the end of each round , we compute the 95% Hoeffding-style and EB CS for , using Theorems 1 and 2 respectively. We use the Brier score as our default scoring rule, but we also explore other scoring rules later in the section. As for the hyperparameter choices for sub- uniform boundaries, we are guided by preliminary experiments in Section I.4.

We consider several forecasters, which are drawn with lines in Figure 2. These include the constant baseline, i.e., (constant_0.5), as well as the Laplace forecasting algorithm (laplace) , where . We further add predictions using the K29 defensive forecasting algorithm (k29) (Vovk et al.,, 2005), which is a game-theoretic forecasting method that yields calibrated forecasts. The method depends on the choice of a kernel function, and here we use the Gaussian RBF with bandwidth . The mix_01_noiseless forecaster is defined as for and for ; the mix_01 forecaster is a noisy version that adds an independent noise to by (clipped at 0 and 1), where is drawn IID from Student’s -distribution with 1 degree of freedom. The mix_10_noiseless forecaster is defined as and the mix_10 forecaster is analogously defined.

The choices of forecasters and Reality are made in such a way that the unknown parameter , for , can not only change its sign but also have different variances over time. For example, the mix_10 forecaster outperforms () the mix_01 forecaster on average during , while the sign then reverses () for . Among the algorithmic forecasters, the K29 variants consistently perform better than the Laplace algorithm, especially when using sharper kernels, because they are better at modeling the sharp changepoints over time.

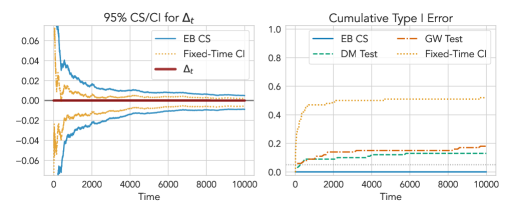

In Figure 3, we plot the 95% Hoeffding-style CS (Theorem 1), EB CS (Theorem 2), and a fixed-time CI for (top left), as well as their widths (top right), the corresponding e-process (bottom left), and the cumulative miscoverage rates (bottom right). First, both CSs successfully cover at any given time point, and their widths decrease as more outcomes are observed. As expected, the width of the EB CS decays more quickly than the width of the Hoeffding CS due to its use of the empirical variance term () but more slowly than the fixed-time CI, matching the patterns observed in Howard et al., (2021); Waudby-Smith et al., (2021). As noted before, the fixed-time CI is only valid at a fixed time and not uniformly over time, despite its tighter width, and this is illustrated by its large cumulative miscoverage rate, i.e., (estimated over the repeated sampling of under ). In contrast, the EB CS888The EB CS is computed with the polynomial stitching bound for computational efficiency. keeps its cumulative miscoverage rate well below (it is in fact zero, as it is constructed using supermartingales and not martingales). In Section H.2, we also include an analogous plot comparing our methods with other classical tests (Diebold and Mariano,, 1995; Giacomini and White,, 2006).

The sub-exponential e-processes for (solid green) and (dotted purple) show how they accurately track the accumulated evidence for/against each forecaster over time. For example, the e-process for stays below 1 during , when neither forecaster outperforms the other, and grows large during when data shows more evidence against the null hypothesis that because the true in fact becomes positive. It then decreases back to values below 1 during , when the true becomes negative. We note that the gray dotted line indicates the value ; testing whether an e-process exceeds corresponds to a level- sequential test equivalent to the one stated in Corollary 1. In fact, the plots show that the points at which the -level EB CS excludes zero (on either side) are precisely when either e-process exceeds , illustrating the duality between the CS and the e-process.

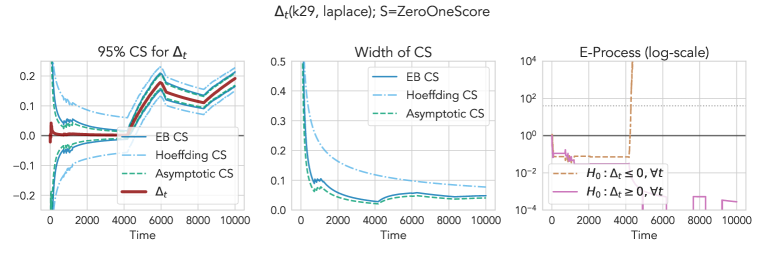

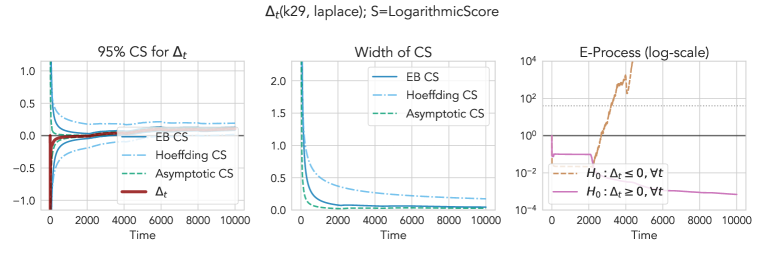

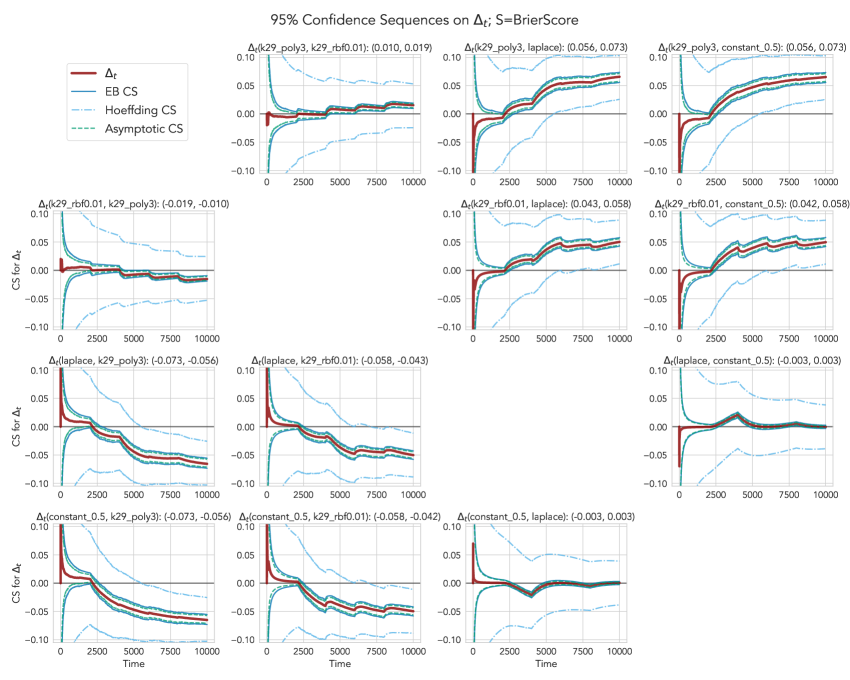

In Figure 4, we now plot the 95% CSs (left), their widths (middle), and also the corresponding e-processes (right) for comparing the k29_poly3 forecaster against the laplace baseline, using the spherical score (strictly proper), zero-one score (proper), the -truncated logarithmic score () (improper). We observe that all variants of CSs always cover the true over time, at , and its width decreases similarly to the case of Brier scores and eventually approaches that of the asymptotic CS. In terms of the width comparison between EB and Hoeffding CSs, we see that the EB CS is generally much tighter than the Hoeffding CS, and it decreases more slowly around time steps when there are sharp changepoints in . This can be explained by the variance-adaptive nature of the EB CS, which would use larger values of intrinsic time at sharp changepoints, whereas the Hoeffding CS simply uses irrespective of the variance process. The sub-exponential e-processes for and illustrate the accumulated evidence for the first forecaster in all three cases around the same time the CS moves entirely above zero, illustrating the duality between the two methods.

We include a plot of all pairwise comparisons between four of the forecasters in Section I.1.2.

5.2 Comparing Forecasters on Major League Baseball Games

As our first real-world application of the CSs, we consider the problem of predicting wins and losses for baseball games played in the Major League Baseball (MLB). Sports game prediction is particularly suitable for our setting, because there are multiple publicly available probability forecasts on the outcome of each game (e.g., FiveThirtyEight, betting odds, and pundits/experts), that are frequently updated across time. There is also no obvious assumption to be reasonably made about the outcome of the games, such as stationarity or assumptions of parametric models. Recall Table 1 for an illustration of various probability forecasts made on MLB games.

We specifically focus on predicting the outcome of MLB games over ten years (2010-2019), culminating in the 2019 World Series between the Houston Astros and the Washington Nationals. We use every regular season and postseason MLB game from 2010 to 2019 as our dataset. We convert each game as a single time point in chronological order, leading to a total of games. As for the forecasters, we consider the following:

-

•

538: Game-by-game probability forecasts by FiveThirtyEight on every MLB game since 1871, available at https://data.fivethirtyeight.com/#mlb-elo.

-

•

vegas: Pre-game closing odds made on each game by online sports bettors, converted and scaled to probabilities, as reported by https://Vegas-Odds.com.999https://sports-statistics.com/sports-data/mlb-historical-odds-scores-datasets/

-

•

constant: a constant baseline corresponding to for each .

-

•

laplace: A seasonally adjusted Laplace algorithm, representing the season win percentage for each team. The final adjust win percentage from the previous season, reverted to the mean by one-third, is used as the baseline probability for the next season. The final probability forecast for a game between two teams is rescaled to sum to 1.

-

•

k29: The K29 algorithm applied to each team, using the Gaussian kernel with , computed using data from the current season only. The final probability forecast for a game between two teams is rescaled to sum to 1.

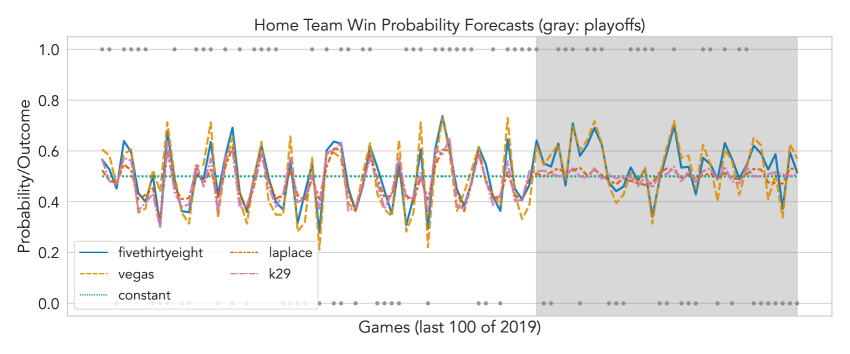

In Section I.2.1, we give further details about the five forecasters and also plot their forecasts on the last 200 games of 2019.

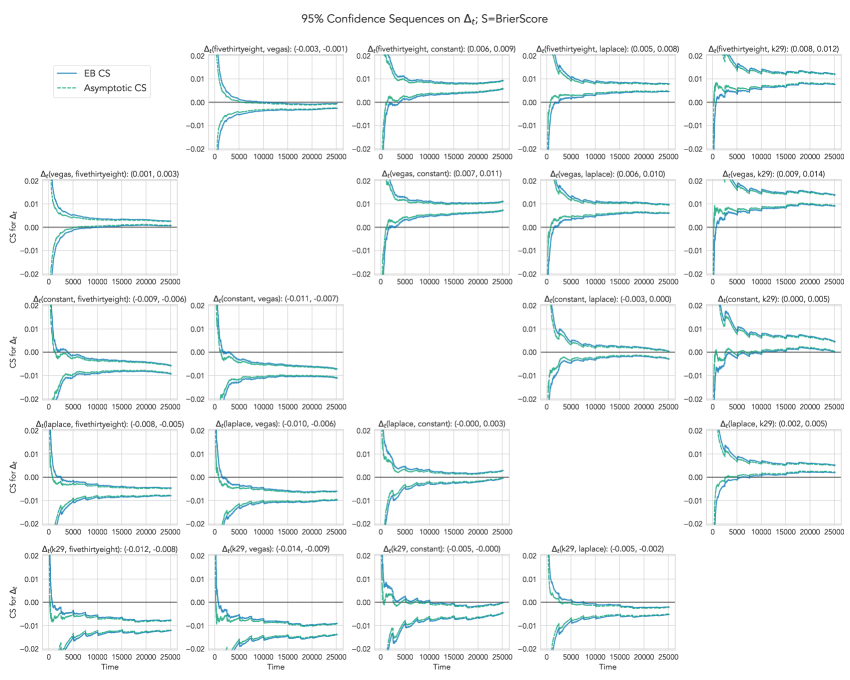

We perform all pairwise comparisons of the five aforementioned forecasters on the 10-year win/loss predictions. See Sections I.4 for details on tuning the free hyperparameter on the uniform boundary. First, as we showed in Figure 1, we compare the two publicly available forecasters in 538 () and vegas (), finding that the vegas forecaster has marginally outperformed the 538 forecaster: after games, 95% EB CS for is , and the e-value for is . The fact that the vegas forecaster (marginally) outperformed the 538 forecaster is interesting, especially given that the primary goal of sports bettors is not to maximize predictive accuracy but their overall profit.101010https://fivethirtyeight.com/features/the-imperfect-pursuit-of-a-perfect-baseball-forecast/ Yet, given the relatively small score difference and also the inherent uncertainty in sports game outcomes,111111https://projects.fivethirtyeight.com/checking-our-work/mlb-games/ more fine-grained comparisons between real-world sports forecasters (e.g., regular season vs. playoffs, team-specific comparisons, and comparisons with or without specific side information) remain interesting future work.

In Table 4, we further compare every other forecaster against the vegas forecaster by estimating the average Brier score differential using the 95% EB CS. We also show the corresponding sub-exponential e-processes (Theorem 3) for the null of , which translates to saying that vegas is not assumed to be better under the null, evaluated at time . Furthermore, we include comparisons involving the logarithmic score, namely via the average Winkler score (Proposition 4, Section D) that quantifies the relative “skill” of forecasters (Winkler,, 1994; Lai et al.,, 2011) as measured by a scoring rule (the logarithmic score, in this case). The Winkler score approach allows us to utilize unbounded proper scoring rules, such as the logarithmic score, when dealing with binary outcomes. Because the score is normalized and thus always maximized at 1, we can construct a one-sided CS with an upper confidence bound (UCB), and also construct an e-process against the null . A negative UCB or a high value in the e-process indicates that is significantly worse than in relative skill.

Our results show that none of the other forecasters, including the 538 forecaster, have outperformed vegas, both in terms of the Brier score and the Winkler-logarithmic score.

We include a plot of all pairwise comparisons between the five forecasters in Section I.2.2.

| Forecaster | ||

| 538 | (-0.00265, -0.00061) | 2979.0 |

| laplace | (-0.00980, -0.00596) | |

| k29 | (-0.01392, -0.00905) | |

| constant | (-0.01115, -0.00713) | |

| Forecaster | ||

| 538 | ( , -0.01012) | |

| laplace | ( , -0.04723) | |

| k29 | ( , -0.14684) | |

| constant | ( , -0.05165) | |

5.3 Comparing Statistical Postprocessing Methods for Weather Forecasts

As our second real-data experiment, we compare a set of statistical postprocessing methods for weather forecasts (Vannitsem et al.,, 2021), following the recent work by Henzi and Ziegel, (2022). Statistical postprocessing here refers to the process of correcting for biases and dispersion errors in ensemble weather forecasts, which are produced by perturbing the initial conditions of numerical weather prediction (NWP) methods. As ensemble forecasts are commonly used in state-of-the-art weather forecasting systems as a means of producing probabilistic forecasts, statistical postprocessing is considered a key component of modern weather forecasting.

Given 24-hour precipitation data from 2007 to 2017 at four locations (Brussels, Frankfurt, London Heathrow, and Zurich), our goal is to compare three postprocessing methods over time: isotonic distributional regression (IDR; Henzi et al., (2021)), heteroscedastic censored logistic regression (HCLR; Messner et al., (2014)), and a variant of HCLR without its scale parameter (HCLR_). We use the Brier score throughout this section. See Section I.3 for details regarding data as well as a plot of the three forecasting methods.

Our main goal here is to sequentially compare the three statistical postprocessing methods using the EB CS and the sub-exponential e-process. As noted in Sections 2 and 4.4, the inferential conclusions drawn from the sub-exponential e-process (Theorem 3) are different from Henzi and Ziegel, (2022)’s e-process, which provides a test of conditional forecast dominance at all times (i.e., the strong null), instead of average (i.e., the weak null). Given that the weak null is larger than the strong null, we would generally expect the sub-exponential e-process for the weak null to be smaller than Henzi and Ziegel, (2022)’s e-process for the strong null. On the other hand, the two methods are similar in that they are both valid at arbitrary (data-dependent) stopping times.

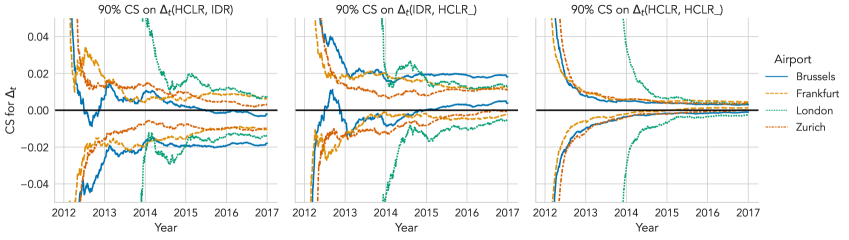

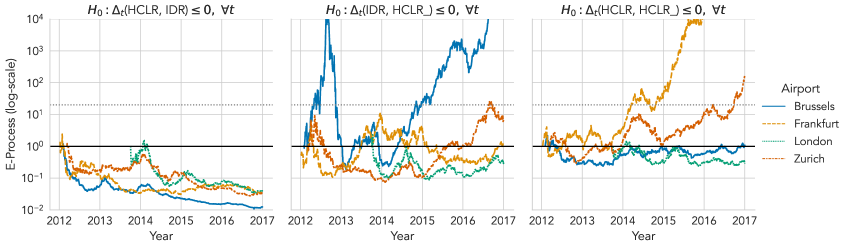

In Figure 5, we plot both the 90% EB CS on (top) as well as the sub-exponential e-processes for the weak one-sided null (bottom), between HCLR and IDR, IDR and HCLR_, and HCLR and HCLR_ on 1-day PoP forecasts at the four airport locations. Note that we compare the same three pairs as Henzi and Ziegel, (2022), who compare e-processes for the strong one-sided null . The EB CS is computed using Theorem 2 and the gamma-exponential mixture boundary (16); the analogous mixture e-processes are then computed using Theorem 3. We use the significance level of for the EB CS, corresponding the threshold of for each one-sided e-process.

We first note from Figure 5 that the lower bound of our 90% EB CS on and the e-process for share a similar trend over time, where the e-process grows large when the lower bound grows significantly larger than zero, implying that the forecaster is better than the forecaster , using the stopping rule (19). Whereas the CS provides a (two-sided) estimate of with uncertainty, the e-process explicitly gives the amount of evidence for whether one is better than the other. This illustrates how the two procedures complement each other for anytime-valid inference on . We also remark that, although we only plot the e-processes for one-sided null , we can further compute the e-processes for , and they would correspond to the upper confidence bounds of the EB CSs.

Based on these results, we find from the 90% EB CSs that IDR forecasts are found to outperform both HCLR and HCLR_ 1-day forecasts for Brussels and that HCLR forecasts outperform HCLR_ forecasts for Frankfurt and Zurich, but we do not find significant differences at other locations between other pairs. The e-processes (thresholded at 20) lead to the same conclusions, and they clearly visualize at which point in time is one forecaster first found to outperform the other and how that pattern changes. For example, when comparing IDR to HCLR_ for Brussels, IDR is found to be better as early as 2012, and it also shows the period between late 2012 and late 2015 where it is no longer found to be better, before eventually regaining evidence favoring IDR starting 2016.

When we compare the sub-exponential e-processes for the weak null with the e-processes for the strong null , which are drawn in Figure 3 of Henzi and Ziegel, (2022), we find that e-processes for the strong null are large whenever e-processes for the weak null are also large, but not vice versa. For example, the comparison of IDR against HCLR_ in Frankfurt is only found to have strong evidence against the strong null, but not the weak null. This is consistent with our previous discussion in Section 4.4 that the strong null implies the weak null and thus is easier to “reject” (or gather evidence against). For example, in Frankfurt, we can infer we only have strong evidence that IDR has outperformed HCLR_ at some point in time between 2012 and 2017, but we do not have sufficient evidence that IDR has outperformed HCLR_ on average in the same time period.

In Section E, we include e-processes for comparing lag- forecasts in the same setting.

6 Extensions and Discussion

In the following, we discuss some related points that were not highlighted in previous sections.

On the use of unbounded scoring rules.

Our main results in Theorems 2 and 3 require the use of bounded scoring rules, which may be restrictive in certain use cases. If the score differentials are unbounded, a general solution would be to use the asymptotic CS (Section C), which assumes that only moments are bounded. When it comes to unbounded proper scores for binary outcomes, such as the logarithmic score, the Winkler score (Section D), which we used in Section 5.2, offers a nonasymptotic and anytime-valid solution.

Comparing forecasts of lag .

In general forecasting scenarios, we may encounter forecasts that are made rounds ahead of when the outcome is revealed at time . In these cases, the expected score differential we seek to estimate should be conditioned on the filtration available at the time of forecasting, rather than the filtration at round . We formally derive methods for comparing lag- forecasts in Section E. These include lagged sequential e-values (Arnold et al.,, 2023), which are not e-processes themselves but can nevertheless quantify the evidence against the weak null (and a “less weak” variant), as well as p-processes and e-processes that are more conservative. The technical details follow the recent discussions by Arnold et al., (2023); Henzi and Ziegel, (2022). Constructing a more powerful e-process and also a CS for the lagged weak null remains a challenging problem.

On “looking ahead” in distribution-free sequential inference on time-varying means.

Our methods are valid without any assumptions about the time-varying dynamics of the forecast score differentials , and in particular we avoid conditions involving stationarity or mixing. A large e-value against at some stopping time tells us that has achieved a better conditional predictive performance than up to on average. The utility of comparing forecasters in such a descriptive sense is often significant in the real world: determining a winner in real-world forecasting competitions can often land significant cash prizes (e.g., financial forecasting121212https://m6competition.com) and/or media attention (e.g., election and sports forecasting).

This also means that the inferential conclusions drawn from our methods need not extrapolate to future time steps, because hypothetically the forecasters or Reality (from Game 1) can completely change their behaviors going forward. Indeed, there is a distinction between saying that one has done better than the other and that one is going to be better than the other in the future — the former is descriptive, while the latter is predictive. All our methods provide evidence and uncertainty related to the former statement. Because we do not make any assumption that says “the future will resemble the past,” no method can make conclusive statements about the latter without clairvoyance. Our setup highlights that past performance can be compared in a distribution-free manner, while predictions of future performance will require nontrivial distributional assumptions.

Ultimately, the decision to take the inferential conclusion and extrapolate it toward the future is (and should be) left to the practitioner’s own beliefs. If a practitioner opts to make additional assumptions about Reality, then in principle, the conclusions drawn from our methods can extend to settings that the assumptions allow. If one is willing to assume, say, that the score differentials are constant, then the inferential conclusions will straightforwardly extrapolate to future time steps (in the assumed setting). Furthermore, the variance-adaptive EB CS will remain tight, because the underlying variance remains constant. It should be noted that, even under such assumptions, which are often made by classical methods like the Diebold and Mariano, (1995) test, anytime-valid approaches avoid the “p-hacking” problem that the classical methods are susceptible to.

Acknowledgements

YJC and AR thank Alexander Henzi, Johanna F. Ziegel, Rafael M. Frongillo, and the anonymous reviewers for their valuable feedback on this work. AR acknowledges funding from NSF DMS 1916320. Research reported in this paper was sponsored in part by the DEVCOM Army Research Laboratory under Cooperative Agreement W911NF-17-2-0196 (ARL IoBT CRA). The views and conclusions contained in this document are those of the authors and should not be interpreted as representing the official policies, either expressed or implied, of the Army Research Laboratory or the U.S. Government. The U.S. Government is authorized to reproduce and distribute reprints for Government purposes notwithstanding any copyright notation herein.

References

- Abernethy and Frongillo, (2012) Abernethy, J. D. and Frongillo, R. M. (2012). A characterization of scoring rules for linear properties. In Mannor, S., Srebro, N., and Williamson, R. C., editors, Proceedings of the 25th Annual Conference on Learning Theory, volume 23 of Proceedings of Machine Learning Research, pages 27.1–27.13, Edinburgh, Scotland. PMLR.

- Arnold et al., (2023) Arnold, S., Henzi, A., and Ziegel, J. F. (2023). Sequentially valid tests for forecast calibration. The Annals of Applied Statistics, 17(3):1909 – 1935.

- Bauer, (2001) Bauer, H. (2001). Measure and Integration Theory. De Gruyter, Berlin, New York.

- Brier, (1950) Brier, G. W. (1950). Verification of forecasts expressed in terms of probability. Monthly Weather Review, 78(1):1–3.

- Darling and Robbins, (1967) Darling, D. A. and Robbins, H. (1967). Confidence sequences for mean, variance, and median. Proceedings of the National Academy of Sciences, 58(1):66–68.

- Dawid, (1984) Dawid, A. P. (1984). Statistical theory: the prequential approach. Journal of the Royal Statistical Society: Series A (General), 147(2):278–290.

- Dawid and Musio, (2014) Dawid, A. P. and Musio, M. (2014). Theory and applications of proper scoring rules. Metron, 72(2):169–183.

- DeGroot and Fienberg, (1983) DeGroot, M. H. and Fienberg, S. E. (1983). The comparison and evaluation of forecasters. Journal of the Royal Statistical Society: Series D (The Statistician), 32(1-2):12–22.

- Diebold and Mariano, (1995) Diebold, F. X. and Mariano, R. S. (1995). Comparing predictive accuracy. Journal of Business & Economic Statistics, 13(3).

- Dunsmore, (1968) Dunsmore, I. (1968). A Bayesian approach to calibration. Journal of the Royal Statistical Society: Series B (Methodological), 30(2):396–405.

- Durrett, (2019) Durrett, R. (2019). Probability: Theory and examples, volume 49. Cambridge University Press.

- Ehm et al., (2016) Ehm, W., Gneiting, T., Jordan, A., and Krüger, F. (2016). Of quantiles and expectiles: consistent scoring functions, Choquet representations and forecast rankings. Journal of the Royal Statistical Society: Series B (Statistical Methodology), pages 505–562.

- Ehm and Krüger, (2018) Ehm, W. and Krüger, F. (2018). Forecast dominance testing via sign randomization. Electronic Journal of Statistics, 12(2):3758–3793.

- Fan et al., (2015) Fan, X., Grama, I., and Liu, Q. (2015). Exponential inequalities for martingales with applications. Electronic Journal of Probability, 20:1–22.

- Frongillo and Kash, (2021) Frongillo, R. M. and Kash, I. A. (2021). General truthfulness characterizations via convex analysis. Games and Economic Behavior, 130:636–662.

- Giacomini and White, (2006) Giacomini, R. and White, H. (2006). Tests of conditional predictive ability. Econometrica, 74(6):1545–1578.

- Gneiting, (2011) Gneiting, T. (2011). Making and evaluating point forecasts. Journal of the American Statistical Association, 106(494):746–762.

- Gneiting et al., (2007) Gneiting, T., Balabdaoui, F., and Raftery, A. E. (2007). Probabilistic forecasts, calibration and sharpness. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(2):243–268.

- Gneiting and Raftery, (2007) Gneiting, T. and Raftery, A. E. (2007). Strictly proper scoring rules, prediction, and estimation. Journal of the American Statistical Association, 102(477):359–378.

- Good, (1971) Good, I. (1971). Comment on “Measuring information and uncertainty” by Robert J. Buehler. Foundations of Statistical Inference, pages 337–339.

- Good, (1952) Good, I. J. (1952). Rational decisions. Journal of the Royal Statistical Society: Series B (Methodological), 14(1):107–114.

- Grünwald et al., (2023) Grünwald, P., de Heide, R., and Koolen, W. (2023). Safe testing. Journal of the Royal Statistical Society: Series B (Statistical Methodology) (to appear).

- Grünwald and Dawid, (2004) Grünwald, P. D. and Dawid, A. P. (2004). Game theory, maximum entropy, minimum discrepancy and robust Bayesian decision theory. the Annals of Statistics, 32(4):1367–1433.

- Henzi and Ziegel, (2022) Henzi, A. and Ziegel, J. F. (2022). Valid sequential inference on probability forecast performance. Biometrika, 109(3):647–663.

- Henzi et al., (2021) Henzi, A., Ziegel, J. F., and Gneiting, T. (2021). Isotonic distributional regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 83(5):963–993.

- Hoeffding, (1963) Hoeffding, W. (1963). Probability inequalities for sums of bounded random variables. Journal of the American Statistical Association, 58(301):13–30.

- Howard and Ramdas, (2022) Howard, S. R. and Ramdas, A. (2022). Sequential estimation of quantiles with applications to A/B testing and best-arm identification. Bernoulli, 28(3):1704–1728.

- Howard et al., (2020) Howard, S. R., Ramdas, A., McAuliffe, J., and Sekhon, J. (2020). Time-uniform Chernoff bounds via nonnegative supermartingales. Probability Surveys, 17:257–317.

- Howard et al., (2021) Howard, S. R., Ramdas, A., McAuliffe, J., and Sekhon, J. (2021). Time-uniform, nonparametric, nonasymptotic confidence sequences. The Annals of Statistics, 49(2):1055 – 1080.

- Jamieson and Jain, (2018) Jamieson, K. and Jain, L. (2018). A bandit approach to multiple testing with false discovery control. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, pages 3664–3674.

- Jamieson et al., (2014) Jamieson, K., Malloy, M., Nowak, R., and Bubeck, S. (2014). lil’UCB: An optimal exploration algorithm for multi-armed bandits. In Conference on Learning Theory, pages 423–439. PMLR.

- Johari et al., (2022) Johari, R., Koomen, P., Pekelis, L., and Walsh, D. (2022). Always valid inference: Continuous monitoring of A/B tests. Operations Research, 70(3):1806–1821.

- (33) Lai, T. L. (1976a). Boundary crossing probabilities for sample sums and confidence sequences. The Annals of Probability, 4(2):299–312.

- (34) Lai, T. L. (1976b). On confidence sequences. The Annals of Statistics, 4(2):265–280.

- Lai et al., (2011) Lai, T. L., Gross, S. T., and Shen, D. B. (2011). Evaluating probability forecasts. The Annals of Statistics, 39(5):2356–2382.

- Lehmann, (1975) Lehmann, E. L. (1975). Nonparametrics: Statistical methods based on ranks. Holden-Day.

- Matheson and Winkler, (1976) Matheson, J. E. and Winkler, R. L. (1976). Scoring rules for continuous probability distributions. Management Science, 22(10):1087–1096.

- McCarthy, (1956) McCarthy, J. (1956). Measures of the value of information. Proceedings of the National Academy of Sciences, 42(9):654–655.

- Messner et al., (2014) Messner, J. W., Mayr, G. J., Wilks, D. S., and Zeileis, A. (2014). Extending extended logistic regression: Extended versus separate versus ordered versus censored. Monthly Weather Review, 142(8):3003–3014.

- Molteni et al., (1996) Molteni, F., Buizza, R., Palmer, T. N., and Petroliagis, T. (1996). The ECMWF ensemble prediction system: Methodology and validation. Quarterly Journal of the Royal Meteorological Society, 122(529):73–119.

- Murphy, (1988) Murphy, A. H. (1988). Skill scores based on the mean square error and their relationships to the correlation coefficient. Monthly Weather Review, 116(12):2417–2424.

- Ovcharov, (2018) Ovcharov, E. Y. (2018). Proper scoring rules and Bregman divergence. Bernoulli, 24(1):53–79.

- Ramdas et al., (2023) Ramdas, A., Grünwald, P., Vovk, V., and Shafer, G. (2023). Game-theoretic statistics and safe anytime-valid inference. Statistical Science (to appear).