Estimating a Causal Exposure Response Function with a Continuous Error-Prone Exposure: A Study of Fine Particulate Matter and All-Cause Mortality

Abstract

Numerous studies have examined the associations between long-term exposure to fine particulate matter (PM2.5) and adverse health outcomes. Recently, many of these studies have begun to employ high-resolution predicted PM2.5 concentrations, which are subject to measurement error. Previous approaches for exposure measurement error correction have either been applied in non-causal settings or have only considered a categorical exposure. Moreover, most procedures have failed to account for uncertainty induced by error correction when fitting an exposure-response function (ERF). To remedy these deficiencies, we develop a multiple imputation framework that combines regression calibration and Bayesian techniques to estimate a causal ERF. We demonstrate how the output of the measurement error correction steps can be seamlessly integrated into a Bayesian additive regression trees (BART) estimator of the causal ERF. We also demonstrate how locally-weighted smoothing of the posterior samples from BART can be used to create a more accurate ERF estimate. Our proposed approach also properly propagates the exposure measurement error uncertainty to yield accurate standard error estimates. We assess the robustness of our proposed approach in an extensive simulation study. We then apply our methodology to estimate the effects of PM2.5 on all-cause mortality among Medicare enrollees in New England from 2000-2012.

1 Introduction

Methods for conducting causal inference with continuous exposures have gained significant traction in recent years. The goal of these methods is to estimate a causal exposure response function (ERF) that is free of confounding bias (Kennedy et al.,, 2017; Wu et al.,, 2018). Estimators of an ERF typically rely on estimates of either the generalized propensity score (GPS), a marginalized model of the outcome process, or some combination of the two to adjust for confounding. However, most of these methods make the implicit assumption that the exposure is measured without error, which is implausible in many observational study settings. For example, in modern environmental health research, air pollution exposure measurements are often derived from model-based predictions of pollutant concentrations rather than the exact pollutant concentrations experienced by an individual. Moreover, because many studies record only areal measures of residential locations such as ZIP-codes, cities, or counties, exposure measures often represent aggregated predictions across these areas. Using aggregated exposures assumes that concentrations are homogeneous within areas and experienced by all individuals residing in the area. As such, exposure measurement error is prevalent in many air pollution epidemiological studies (Kioumourtzoglou et al.,, 2014). Using an error-prone exposure (EPE) in place of the true exposure violates standard causal inference assumptions and may result in biased ERF estimates. Due to the policy-relevance of air pollution ERFs, and particularly those produced using causal inference techniques, invalid inferences caused by EPEs could have severe consequences.

While measurement error has been studied extensively outside of causal inference settings (Carroll et al.,, 2006; Cole et al.,, 2006), accounting for EPEs in causal inference is a relatively new endeavor and is mainly confined to scenarios with binary and categorical exposures (Lewbel,, 2007; Braun et al.,, 2017; Wu et al.,, 2019), or cases of measurement error in a confounder instead of the exposure (Lenis et al.,, 2017; Webb-Vargas et al.,, 2017). Beyond the issues encountered when using an EPE in a typical generalized linear model setting, accommodating an EPE in a causal model presents additional challenges in conjunction with resolving confounding bias (Braun et al.,, 2017), many of which remain unaddressed. Moreover, propagating measurement error-related uncertainty into ERF estimates is paramount for proper inference in not just causal settings, but more broadly for many environmental epidemiological studies.

We develop a multiple imputation framework for estimating causal ERFs which incorporates corrections for various types of exposure measurement error commonplace in environmental epidemiology. This approach jointly samples from three sub-models: 1) a model of the EPE, which imputes the true exposures using information from covariates and validation data when available, 2) a GPS model, which improves the accuracy of the imputations, and 3) an outcome model, which estimates the ERF using the imputed exposures while adjusting for confounders. Markov Chain Monte Carlo (MCMC) methods are used to sample from the posterior distributions of the unobserved true exposures and the expected outcome conditioned on the exposures and confounders. A Bayesian additive regression trees (BART) model is specified for the outcome sub-model to capture complex, non-linear relationships between the exposure, the covariates, and the outcome. We also show that implementing a further smoothing step on the BART-estimated ERF using local regression techniques provides accurate estimates of the ERF with fewer posterior samples than a classic Bayesian approach, all while adequately propagating the measurement error uncertainty. The latter smoothing step transitions our approach from a Bayesian estimator into one better characterized as a multiple imputation estimator, while at the same time producing smoother estimates of the ERF than the notoriously noisy BART output (Nethery et al.,, 2021).

The remainder of this article is structured as follows. We describe the motivating data example in Section 1.1. In Section 2 we introduce notation, define the measurement error sources, and identify the causal ERF model. Section 3 outlines the procedure for correcting the attenuation bias created by measurement error using multiple imputation methods, and we discuss several important caveats and limitations to our proposed methodology. Section 4 contains a simulation study. Section 5 applies the proposed method to create a measurement error-corrected causal ERF for long-term fine particulate matter (PM2.5) exposure and all-cause mortality in the Medicare population in New England, using the data described in Section 1.1. We conclude with a discussion in Section 6.

1.1 Motivating Example

PM2.5 is a well-studied air pollutant known to adversely impact numerous health outcomes (Hajat et al.,, 2002; Dominici et al.,, 2006; Brook et al.,, 2010; Zhu et al.,, 2017), including all-cause mortality (Anderson,, 2009; Di et al.,, 2017; Wu et al.,, 2020), cardiovascular disease (Dominici et al.,, 2006; Zanobetti et al.,, 2009; Pope III et al.,, 2015; Yazdi et al.,, 2019; Danesh Yazdi et al.,, 2021), and pulmonary/respiratory diseases (Dominici et al.,, 2006; Zanobetti et al.,, 2009; Rhee et al.,, 2019). In one of these studies, using a cohort of Medicare enrollees 2000-2012, Wu et al., (2019) implemented various causal inference techniques to assess whether long-term PM2.5 exposure increases the risk of all-cause mortality among older Americans ( years of age). While Wu et al., (2019) employed a regression calibration approach to resolve parts of the exposure measurement error present in this application, there were other error components that were left uncorrected. Moreover, a simple regression calibration approach may fail to adequately propagate measurement error-related uncertainty into the causal effect estimates. Additionally, Wu et al., (2019) considered exposure categories instead of examining the ERF across a continuum of exposures. Categorization of exposures implicitly assumes that participants in the same category are exposed to the same exposure level, which may induce yet another source of measurement error. We seek to investigate the same scientific question as Wu et al., (2019) using the same data but employing a novel analytic approach that: 1) corrects for additional sources of measurement error in the PM2.5 exposures and 2) models the continuous ERF as opposed to categorizing the exposure.

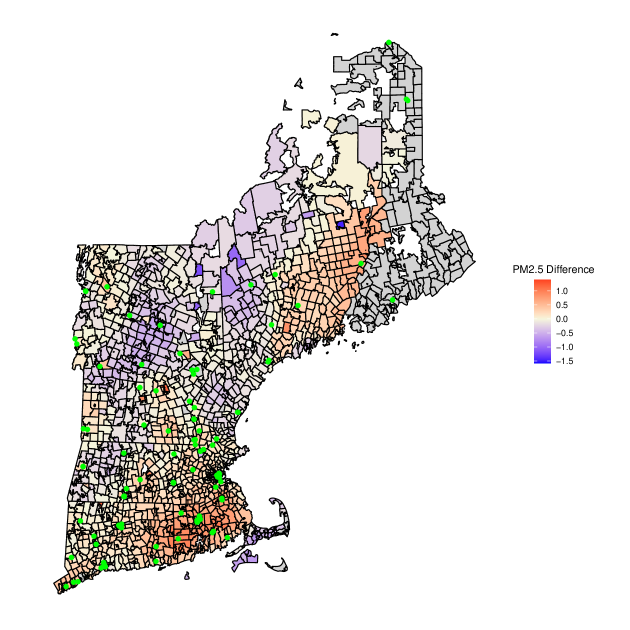

We utilize annual average PM2.5 predictions for 1km1km grid-years across the US from Di et al., (2016), which were generated via a neural network that combines information from satellite, ground monitor, and land use data. These exposure predictions have been widely used in epidemiological studies (Di et al.,, 2017; Rhee et al.,, 2019; Wu et al.,, 2019; Yazdi et al.,, 2019; Wu et al.,, 2020; Danesh Yazdi et al.,, 2021). Model assessments indicate that the accuracy of the predictions vary across regions (Di et al.,, 2016). Because these exposure predictions are error-prone, any inference drawn from them without correction may be biased. To control for this source of measurement error, we use the same ground-monitor PM2.5 data that were used to generate the grid-predicted PM2.5 measurements in the first place. We treat the measurements from these monitors as the gold standard measurements of PM2.5 exposure (i.e. error-free measurements). Our model uses the monitored data as a validation set to re-calibrate the error-prone PM2.5 measurements. PM2.5 ground monitor locations in New England are overlaid on a ZIP-code map in Figure 1.

Another limitation of the data is that the residential locations of the Medicare enrollees can only be mapped to ZIP-codes (Wu et al.,, 2020). Thus, following common practice in this setting, we use ZIP-code-years as our units of analysis and all-cause mortality rates within ZIP-code years as our outcome. This creates a misalignment between the PM2.5 exposure predictions, which occur on 1km grids, and the ZIP-codes to which we wish to assign PM2.5 exposures.

We also leverage data on demographic and socioeconomic status (SES) factors, as well as land-use variables which are used to aid in measurement error correction. The following potential confounder variables are collected from the US Census Bureau at the ZIP-code-year level: population density, median household income, percent population and households below poverty level, racial/ethnic composition, and distribution of educational attainment (college, some college, high school, not completed high school). Additionally, individual level information about the Medicare enrollees, including their sex, age, race, and Medicaid eligibility status (a proxy for low-income) are obtained from the Medicare record and summarized at the ZIP-code-year level. The land-use variables, collected at the grid-year level, are: surface temperature, accumulated precipitation, radiation flux, accumulated total evaporation, heat flux, precipitation rate, humidity, snow cover, cloud cover, and wind speed.

2 Preliminaries

2.1 Notation and Measurement Error

Our data involve measurements at two different spatial scales: ZIP-code-years (outcome, covariates) and 1km1km grid-years (exposure, land-use variables). In general, we refer to grid-years as cells, and cells are assumed to be nested within ZIP-code-years, which we refer to as clusters. Let be a vector of covariates for cluster () and denote the outcome variable in that cluster. While the methodology we present easily generalizes to other outcome distributions, in our applied example the are counts (e.g. number of deaths in ZIP-code-year ) with representing an offset (e.g. number of at-risk person-years in ZIP-code-year ). The combination of these two measures allows us to define the rate . We denote the cumulative density functions for the with with the associated empirical density function denoted by .

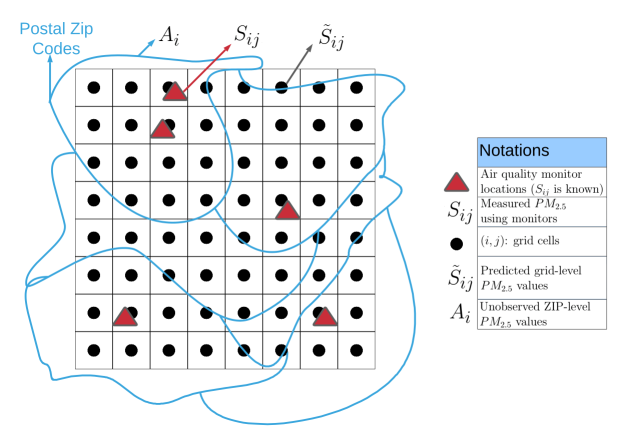

We assume there is a true exposure both on the cluster level and on the cell level. To enable alignment with the outcome data at the cluster level, the true cluster level exposure, denoted , is the latent variable we are most concerned with accurately predicting. We assume that the are continuous but unobserved for all clusters. The true cell level exposures within cluster are indexed by and are denoted as . The total number of cells is written as . We assume, as in our example, that the will only be observed for a subset of cells – the grids containing monitors – which are indexed by . We also have for every cluster and cell an observed model-predicted value of , denoted as . These predictions are the error-prone exposures. The aggregate value of these EPEs to the cluster level will be denoted with . Figure 2 illustrates the relationship between , , and in the context of our motivating application. We also allow for the existence of a set of cell level features, denoted by the vector , that might inform us about the relationship between and . In our applied example, the are land-use variables measured at the grid-year level. may contain aggregated and/or transformed values of the variables contained in .

Finally, the conditional expected value of any given variable is denoted by . The conditional probability density function of is denoted with . The generalized propensity score (GPS) is the following particular conditional probability density function: .

2.2 Measurement Error Model

We formulate the measurement error in this context as a special case of nondifferential classical error. As we noted in Section 2.1, we must contend with the problem that is rarely observed, and in most areas only the EPE measurements, , are available. Moreover, conducting a cluster level analysis relating to requires measurements of , not . Therefore, we must consider approaches for summarizing while accounting for the possible confounding influence of and the varying sizes of , and ensuring the uncertainty from this process is propagated into the final estimator.

Throughout this paper, we will assume that , which can be framed as treating the true cell level exposures as replicate measures of the corresponding cluster level exposure , each measured with some amount of error. This ‘replicate measures’ conceptualization is commonly used in the presentation of classical measurement error methods. An additional dimension of complexity is added by the need to rely on cell level exposure predictions, . This leads us to formulate the measurement error structure as a variant of the typical nondifferential classical measurement error, which can be decomposed into two components as follows:

| (1) |

Following conventions in the classical measurement error literature, we make the assumption that the measurement error is homoscedastic and conditionally independent such that:

Assumption 1 (Conditionally Independent Measurement Error).

We assume for two cells in a given cluster ;

Assumption 2 (Homoscedastic Measurement Error).

For all contained within every , we assume the measurement error conditional on has constant variance; .

The prediction error component in (1) can be characterized as a Berkson error term (Haber et al.,, 2020). The aggregation error, on the other hand, is a type of classical measurement error, implying the composite measurement error term is also a type of classical error. To help cement this understanding, ignore for a moment the prediction error term in . The goal of regression calibration is to replace classical measurement error with Berkson error. It has been noted in the regression calibration literature that Berkson error resulting from regression calibration often yields less bias than its classical error counterpart (Carroll et al.,, 2006). Our method, presented in the following sections, is developed in the same spirit, replacing with a Berkson error term via multiple imputation. Our method also allows the user to replace the prediction error component of , if desired, but doing so essentially substitutes the original Berkson prediction error with another Berkson error term. That said, re-calibrating the predictions can still be useful if we suspect . In this latter case, if we assume for all , then we can use validation data to find an unbiased predictor for , denoted by , which implies .

As we will show in Section 3, corrections for both the classical measurement error between and and any potential bias found in the predictions can be accommodated under the proposed multiple imputation framework. The imputations of the true exposures are drawn from an MCMC sampler using the full conditional likelihood in (2).

2.3 Assumptions and Identification

The methods we employ operate within the Neyman-Rubin causal model modified for continuous exposures Rubin, (1974). Let be the outcome that would occur in cluster if, possibly contrary to what is observed, it had received exposure level . We refer to the for any as the potential outcomes. For some exposure level the objective analysis is to estimate the marginal ERF, . Unlike in the binary or categorical exposure setting, where there is only a finite number of unrealized potential outcomes, with a continuous exposure there is an infinite number of unrealized potential outcomes for every unit in the study. Despite this perceived challenge, it is relatively straightforward to translate the assumptions intended for a categorical exposure under the Neyman-Rubin causal model to a continuous exposure setting necessary to identify and estimate .

To start, we invoke the stable unit treatment value assumption which consists of two conditions: 1) consistency and 2) no interference. Consistency refers to the notion that , i.e. each unit’s observed outcome is equal to its potential outcome evaluated at the true exposure experienced. We are careful to define this assumption in the setup to our problem; recognizing that is unobserved. While unobserved, the true exposure still exists, so consistency should hold. On the other hand, if we naïvely substitute for , then consistency is likely violated with respect to the EPE unless implying for all . As this assumption is unlikely to hold, it is safe to assume consistency is violated if measurement error-agnostic approaches are taken. No interference refers to the assumption that the exposure of one unit does not affect the potential outcomes of another unit. This condition is difficult to uphold in many environmental epidemiology studies, including our own applied example. Major air pollution emissions sources can affect broad areas (e.g., many ZIP-codes), which may lead to instances where the exposure assignment of one ZIP-code affects the outcome of another (Papadogeorgou et al.,, 2019). We acknowledge this limitation, yet addressing it is outside the scope of this work.

The fundamental problem in causal inference with any type of exposure is that is not intrinsically estimable since is not observed for every . However, can still be estimated under the strongly ignorable exposure assumption. With the Neyman-Rubin causal model, this requires the following two assumptions (Kennedy et al.,, 2017):

Assumption 3 (Overlap/positivity).

.

Assumption 4 (Weak unconfoundedness).

for all .

The overlap assumption requires the exposure assignment mechanism to be non-deterministic when conditioned on the covariates. In other words, the probability that a unit is exposed to any level of the exposure along the support is always greater than zero (or ). Weak unconfoundedness states that the potential outcome evaluated at does not depend on the true exposure when adjusted by the set of observed confounding variables. This implies there can be no unmeasured confounding. If all confounders for the relationship between and are measured, the latter assumption should hold even when exists but is not observed. When these assumptions hold, it is valid to draw causal conclusions either with experimental or observational data and a continuous exposure (Gill and Robins,, 2001), and assuming is known, the true causal ERF can be identified as

3 A Multiple Imputation Approach

3.1 Sampling the Exposure and Nuisance Parameters

We introduce our method by first specifying the joint likelihood function for , , and , which incorporates the components needed to address the measurement error described by (1). Supposing that every piece of data were observed, we have:

| (2) |

From a modelling perspective, we assume that the latent exposure variables are conditionally independent and approximately Normal in distribution with and , in accordance with Assumptions 1 and 2. A random effect is included in the model for to control for spatial autocorrelation between the cluster level exposures (Lee,, 2013). We assume where is a precision matrix controlling the auto-correlation structure as proposed by Leroux et al., (2000) given a binary adjacency matrix and a hyperparameter controlling the correlation between adjacent clusters. If we assume the are independent, then we can set and for all . Because is missing, we can substitute for if we suppose . However, when given a set of validation data (i.e. a subset where is observed), a more conservative approach is to instead assume and draw a sequence of posterior predictions for for all and . To do this, we can append the model to (2) and, supposing that , sample values of . Note that this addition overspecifies the full-conditional likelihood in (2), so doing so is only possible when validation data are available.

We use the above likelihood throughout this manuscript to describe how to sample posterior draws of contemporaneously with posterior predictions for . We will show in the next section how these posterior samples can be smoothed to create an estimate of the ERF. Relative to the standard regression calibration approach where only a single imputation of is used in fitting the outcome model, using a set of posterior samples (i.e. multiple imputations) of the error-corrected exposures should better propagate uncertainty attributable to the exposure measurement error into the outcome model.

We use a fully Bayesian joint modeling approach for the measurement error, GPS, and outcome models. Parameter values are sampled from the posterior distribution either by Gibbs or Metropolis-Hastings sampling steps, with an added intermediate step to generate posterior predictive samples of the latent variables and, if necessary, . We refer to this intermediate step as the imputation stage, whereas the steps involving sampling the parameters are referred to as the analysis stage. See the full details of the sampling algorithm in Supplemental Section S1.

We must carefully consider the form of and to properly address bias in the EPE model while also accounting for confounding. In our simulation study and data analysis in Sections 4 and 5, we assume linear forms for and . To better capture nonlinear associations and better avoid issues with model misspecification, splines or Gaussian processes could alternatively be specified (Antonelli et al.,, 2020; Ren et al.,, 2021).

If we assume that is a linear function of and , then the parameters determining can be drawn using a Gibbs sampling step, assuming the are fixed and known. However, we prefer to use a data-driven model for and therefore , because this model is perhaps the most essential component in (2) for finding accurate estimates of . To this end, we employ an iteratively updated BART model (Chipman et al.,, 2010). Letting index the trees for a given iteration of the MCMC, the BART model assumes

| (3) |

Here, is a function that bins observations into groups with binary trees formed by the rules contained in , and node means characterized by the set . A BART model differs from other regression tree ensembling methods because of the priors placed on and , which are used to sample values from the approximate posterior distribution of . Posterior samples are denoted by superscript , , e.g., . In each iteration of our MCMC sampler, the posterior samples of the BART parameters are drawn conditional on the current posterior sample of the exposures . The error term is assigned the distribution .

For model-fitting, we assign conjugate inverse-gamma prior distributions to the variance parameters, , and set . The regression coefficients for , , are each assigned independent Gaussian priors with default values where is a vector with every entry equal to zero and is an identity matrix (with appropriate dimensions). Additional sampling details are provided in Supplemental Section S1. For an example of how to implement a generalized linear model for instead of the BART implementation in (3), please refer to the simulation experiment in Supplemental Section S4.

3.2 Smoothing BART Output

While predictions from the BART model (e.g., means of posterior predictive samples) could be used directly to form an estimate of the ERF, these samples do not typically form a smooth function of over . Smooth ERFs are believed to be most biologically plausible relationship in many epidemiological and biomedical applications, including the effect of PM2.5 on all-cause mortality, and are more desirable for identifying causal relationships (Kim et al.,, 2018). To resolve this problem, we will project a multiply-imputed pseudo-outcome derived from the BART output onto the support of with local regression techniques. We only need a small number of imputations, i.e., a small, thinned subset of the BART posterior samples (indexed by , ), to get smooth, reliable estimates of the ERF. First, we create multiple imputations of the pseudo-outcome as

| (4) |

There are two components in this pseudo-outcome. The integral on the right hand side of the addition symbol is the marginal estimate of the ERF at . Under the more typical Bayesian framework, we could find for each . This would be equivalent to a Bayesian version of a G-computation estimator for the ERF (Keil et al.,, 2018). However, this process can be time consuming when iterating for all posterior samples instead of the imputations, in addition to yielding a non-smooth ERF. The term on the left-hand side of the addition symbol in (4) is the residual error conditioned on and . Since multiple imputation couples Bayesian methodology with regression techniques, it is necessary for each imputation that we approximate the variance for estimates of at each point which is facilitated by the addition of this residual error term. Without the residual error component, the variance estimates within each imputation would be incorrect (Antonelli et al.,, 2020).

Local regression methods offer perhaps the most flexible means of projecting the pseudo-outcomes in (4) onto the support . Given a bandwidth , the ERF estimates we obtain for each imputation are denoted by . A pointwise estimate of the ERF is summarized by . Because we regress each of the imputed pseudo-outcomes onto the support of the exposure, , the values do not form a proper posterior of . This result was noted also by Antonelli et al., (2020) who found that the posterior distribution of a regression based estimator like alone did not adequately characterize the uncertainty. To correct for this, our approach to estimation combines a kernel-weighted least-squares regression estimator similar to Kennedy et al., (2017) with the Bayesian approach of Antonelli et al., (2020). Instead of using a bootstrap estimator to find the empirical MCMC standard error used by Antonelli et al., (2020), we use an asymptotic standard error estimator derived by Kennedy et al., (2017). Details for estimating and the accompanying standard errors for using multiple imputation combining rules (Rubin,, 2004) are provided in Supplemental Section S2 along with the details on how to smooth the BART ERF estimates using kernel-weighted least-squares regression.

A simple regression calibration variation to the above approach would be to find a single imputation (i.e. ) of , let’s say , then construct an estimator of the outcome mean and substitute that estimator into (4) replacing . In this single imputation case, the ERF estimator would equal . We will see in the simulation that for a single imputation, the choice of is not so straightforward in the presence of measurement error, nor does such an approach adequately propagate the uncertainty created by measurement error without further correction. For more details on the local regression methods we apply, see Supplemental Section S2.

3.3 Issues Stemming from Congeniality

Our model contains two components, an imputation stage and an analysis stage. The imputation stage generates imputations of the latent exposures, and , while the analysis stage draws samples from the posterior distributions of the model parameters. Following the multiple imputation literature, the imputation component of our model must condition on the outcome to satisfy assumptions associated with congeniality, explained below. Congeniality states that the imputation and analysis stage models need to utilize the same data (Meng,, 1994), and violations of congeniality can bias parameter estimates. From a Bayesian perspective, non-congeniality can arise due to cutting feedback or modularizing (Zigler et al.,, 2013) the components of a joint model. The limiting distribution from an MCMC of , and by extension the limiting distribution of the exposure effect, is ill-defined when cutting feedback between the outcome and exposure model in a Bayesian setting (Plummer,, 2015). Since we are necessarily using the imputations of to fit the analysis model and construct an estimate of the ERF, then to satisfy congeniality and avoid biasing the ERF estimate, the imputation models must be conditional on the outcome. This is accomplished in our method by using a fully Bayesian joint model-fitting scheme for the EPE, GPS, and outcome models.

However, sampling the latent exposures conditioned on the outcome creates bi-directional feedback between the traditional “design stage” (GPS modeling) and analysis stage that are kept separate in most causal analyses. This seemingly defies research that emphasizes cutting feedback between the GPS and outcome model in a Bayesian causal analysis (Zigler et al.,, 2013). Notice that we include a model for the GPS in (2) that we fit in Section 3.1, yet we do not utilize the GPS in our outcome model nor our estimator of the ERF in Section S2. While the outcome data does not appear in the full conditionals for the GPS model parameters, it is used to generate new predictions of which may indirectly create feedback affecting the GPS model estimates. To counteract the feedback problems created by congeniality, we removed the GPS adjustments from the doubly-robust pseudo-outcome supposed by Kennedy et al., (2017) (which appears in the Supplemental Section S4). These GPS adjustments appear to provide no utility in our context as demonstrated by a small simulation study contained within Supplemental Section S4. In this simulation, we draw particular attention to cases where the outcome model is misspecified but the GPS is correctly specified. In this scenario, there is almost no difference between using the GPS adjusted pseudo-outcome supported by Kennedy et al., (2017), and the pseudo-outcome we suppose in (4). We contend that this null result is attributable to the feedback created by the need to use congenial models for the imputation and analysis stages of the MCMC sampler.

4 Numerical Example

4.1 Simulation Design

In this simulation study, we examine the performance of the method described in Section 3 in the presence and absence of exposure measurement error. In addition, we will evaluate the effects of model misspecification across the three components of the likelihood in (2), all while examining whether uncertainty is properly propagated into the final ERF estimate.

We test four different methods for measurement error correction. The first method naïvely ignores any measurement error and assumes is the true cluster level exposure. The second method examines an extension to the regression calibration approach proposed by Wu et al., (2019), which we adapted to consider a continuous exposure, that corrects for prediction error but disregards the remaining classical error in (1) created by the remaining aggregation error. After finding predictions for using least-squares regression conditioned on and , a single imputation of is produced by computing . We will refer to these two implementations that use either or as the “single imputation” approaches. The third and fourth methods that we examine are two “multiple imputation” approaches that follow the proposal in Section 3, with different outcome model specifications. In one of the multiple imputation variants, we let be a BART model. In another, we let be a correctly-specified log-linear Poisson model, assuming unknown coefficient values (see Supplemental Sections S3 and S4 for details). To highlight the impacts of correcting measurement error and propagating uncertainty, we utilize estimation approaches that are as similar as possible across the four competing methods aside from how they correct for measurement error. For the single imputation approaches, we construct the pseudo-outcome in (4) in the exact same manner as in the multiple imputation cases, but for a single iteration, i.e. setting . For the single imputation methods, this means using the or in place of and either or in place of , respectively. We also assume that for all (i.e. is independent), both in the data generation procedure and in the models we fit.

In Supplemental Section S3 we describe the various data generating mechanisms used to construct the simulation scenarios. For each scenario, we ran iterations, in each one applying each of the four methods described above. In each iteration, we obtain pointwise estimates of at equally spaced exposure values across the range . We report the relative bias, the residual mean square error, and coverage probabilities averaged across all the iterations and all the pointwise ERF estimates. We also report these same measurements for predictions at a single exposure level, , averaged across the iterations. Briefly, we vary , , , and . Note that when the prediction error is absent, whereas when the remaining classical error is absent and is limited to the prediction error. We also vary the degree of misspecification in the component models contained in (2) (Kang and Schafer,, 2007).

4.2 Simulation Results

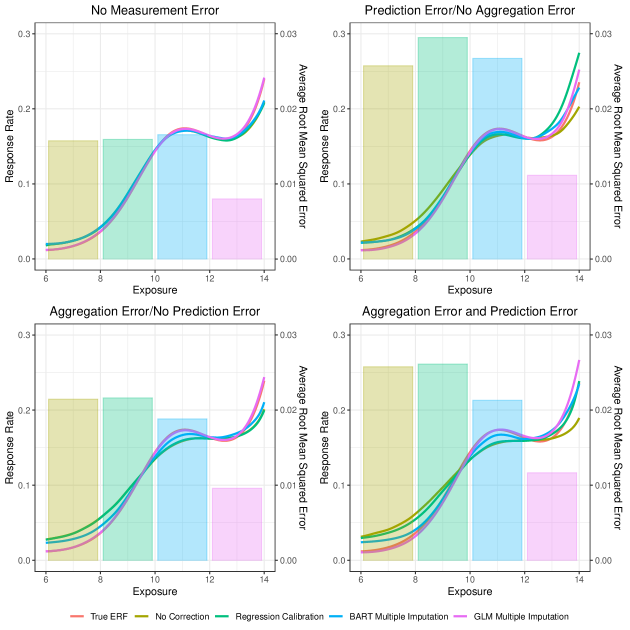

The main results of this simulation illustrate how adding measurement error can influence estimates of the ERF. Figure 3 shows the average ERF estimated with each of the four methods in Section 4.1 (relative to the true ERF) under simulation scenarios with no measurement error, prediction error only, classical error only, and both sources of error present. These results demonstrate that generating unbiased imputations of the exposure of interest is critical, whether using a single or multiple imputations. Note that from the description of the scenarios, we have when the EPE model is correctly specified. Therefore the naïve approach and the regression calibration approach, which corrects for prediction error, produce similar results as shown by the root mean squared errors displayed in Figure 3. This is because the prediction error is Berkson, so using regression calibration has a negligible effect. Also, note that the regression calibration and multiple imputation approaches perform similarly in scenarios without classical error (Figure 3, top row), but the performance of regression calibration deteriorates when we simulate measurement error with aggregation error present. Meanwhile, the multiple imputation approaches retain accuracy (Figure 3, bottom row). Some bias still lingers in each method, particularly at the extremes of the exposure support (i.e. and ). This is typical of local regression methods where there is an implicit bias-variance tradeoff through the choice of (which is set to when and when ) (Hastie et al.,, 2001). Unsurprisingly, the accuracy of the different methods we test improves as both and increase (Table 1).

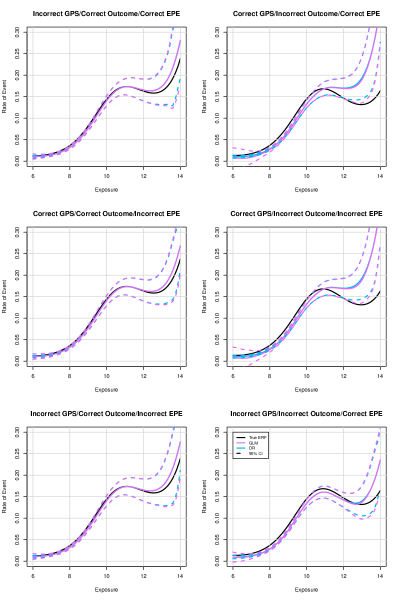

We can also see in Table 1 that the coverage probabilities from the 95% confidence interval estimates among the multiple imputation approaches offer a marked improvement over the alternatives. When using a correctly specified log-linear outcome model within a multiple imputation setting, we achieve coverage probabilities that match the nominal 95% confidence level. However, the coverage probabilities are imperfect when using a BART outcome model. BARTs’ tendency to under-report the dispersion of point estimates is well-documented (Wendling et al.,, 2018; Hahn et al.,, 2020; Nethery et al.,, 2021). The BART output also seems to produce biased estimates at several points along the curve, contributing to the low coverage probabilities. Despite this limitation, BART remains the preferred outcome model due to its strong predictive abilities even when the correct model specification is unknown (see the following paragraph). Since we average pointwise evaluations over the support , we can also see how the coverage probabilities are affected by using local regression techniques. This can be seen by examining the single pointwise evaluations at , which are closer to the nominal 95% confidence level than the average coverage probability over the pointwise evaluations.

In the second part to our simulation study, where we induce model misspecification, we observe in Table 1 that the ERF estimates are largely unaffected by outcome model misspecification alone with a BART model – remaining relatively unbiased as long as the GPS is still correctly specified. The same result is obviously not true for a parametric log-linear outcome model. Even though BART is supplied the untransformed covariates when model misspecification is present, it is quite adept at identifying complex nonlinear and interacting effects, making outcome model misspecification a moot consideration, so long as Assumptions 3 and 4 hold. That said, the coverage probability decreases considerably in scenarios with a misspecified outcome model relative to the results of the scenario where all models are correctly specified.

When the GPS model is misspecified, the level of bias increases substantially in each of the ERF estimates, both from the single imputation and multiple imputation models. A perplexing exception to this result is when both the GPS and the outcome model are misspecified, in which case the bias returns to the nominal levels observed in cases when the GPS is correctly specified and a BART outcome model is used. Given these results, and the results of the simulation in Supplemental Section S4, it is evident that finding an approximately correct GPS model may be even more important than finding a correct outcome model as we originally suggested. Doing so might decrease the precision of the imputations for . Finally, when the EPE model is “misspecified”, meaning implying , then we see the most severe levels of bias using the naïve (no correction) approach. Since the multiple imputation and regression calibration approaches correctly model and , respectively, such that and , the prediction bias does not affect the estimates of the exposure response curves using these two approaches.

5 Applied Example

Recall the example described in Section 1.1. Wu et al., (2019) used regression calibration methods on the same data to correct for measurement error for the grid-year PM2.5 predictions. Subsequently, they aggregated the corrected grid-year predictions to the ZIP-code-year level, categorized the imputed exposures based on standard EPA cutoffs, and examined a variety of GPS-based implementations including matching, sub-classification, and weighting to estimate the effect of PM2.5 on mortality. Their results suggest that increasing PM2.5 exposure led to excess mortality events.

In this analysis we re-examine the same data as Wu et al., (2019), applying the proposed multiple imputation approach to estimate the ERF relating PM2.5 with all-cause mortality. For ZIP-code-year , the exposure is the annual average PM2.5 concentration (in g/m3), the outcome is the number of deaths observed, and is the person-years at risk. We have exposure data on ZIP-code-years in New England covered by 1km1km grid-years, each with error-prone PM2.5 exposure predictions . A subset of grids within ZIP-codes have error-free PM2.5 measurements from monitoring stations in years 2000-2012 (Figure 1). While it is plausible that the and within ZIP-code-years are correlated, the majority of this correlation can be accounted for simply by conditioning on , thus enabling Assumptions 1 and 2.

For the multiple imputation approach, we assume the outcome model in (3). As in the simulation study, we implement two different single imputation approaches. In the first approach, we ignore prediction error altogether and suppose is the true exposure (we call this the “no correction” approach). In the second approach, we use least squares regression on the validation data to get the regression calibrated . We then use these single imputations of the exposure in a BART model to construct an estimate of the mean function; either or . For both the single () and multiple imputation approaches (), local regression was applied according to Section S2. We collected MCMC samples, thinned by every iterations, after a burn-in of another iterations. Diffuse priors specified in Section 3.1 were used for the GPS model parameters, the EPE model parameters, as well as for the BART model. As opposed to the simulation study, we account for spatial correlation between the ZIP-code exposures by sampling in (2). In this example, the matrix is a binary adjacency matrix with each row and column representing a different ZIP-code-year.

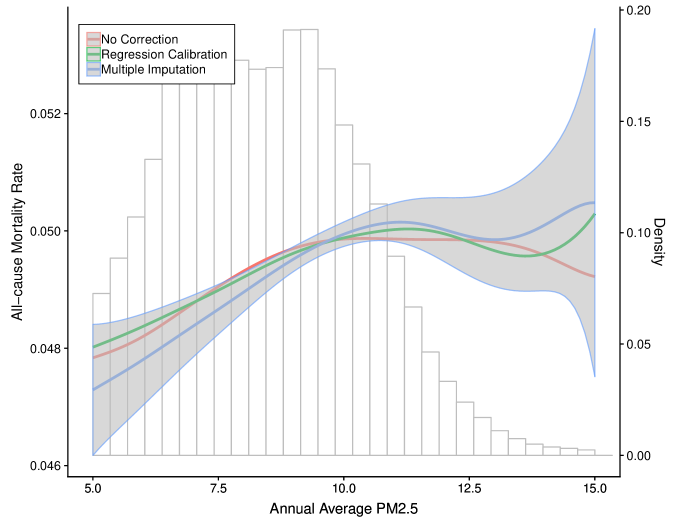

Figure 1 provides a heat-map displaying the difference between the naïve exposure imputations of and the posterior means for each ZIP-code in 2010. Here we can see substantial differences in the imputed exposure values in some areas of New England. Figure 4 shows the ERF estimates from each of the three methods we examined. In the curve estimated with multiple imputation, we can see a modest increase in the rate of all-cause mortality from when annual average PM2.5 is at g/m3 to when annual average PM2.5 is at g/m3. Relative to the uncorrected and regression calibration curves, the curve estimated with multiple imputation has a steeper gradient at lower levels of PM2.5. The steepest increase in mortality occurs when PM2.5 changes from about g/m3to g/m3, which is policy-relevant given the World Health Organization’s recent decision to lower the recommended limit of annual average PM2.5 to g/m3 (World Health Organization,, 2021).

We suspect that the minor differences between the three curves are primarily attributable to the small variation of the classical measurement error, , which we found to be equal to about 0.0187 ( CI: 0.0183-0.0189). The posterior mean for the conditional prediction error variance, , on the other hand was 1.340 ( CI: 1.212, 1.446). However, as we demonstrated in the simulation study, correcting for the prediction error is secondary to correcting for the classical measurement error including the aggregation error, except when . This reasoning is further cemented in this illustrative example – we can see that , and so the difference between the curves with no measurement error correction and regression calibration is relatively small.

6 Discussion

We developed a multiple imputation framework that addresses exposure measurement error when estimating a causal ERF. We adapted a Bayesian approach for correcting measurement error to generate imputations of the true exposures assuming non-differential classical measurement error. We then constructed a flexible representation of the ERF using kernel smoothed output from a Bayesian additive regression tree. These two steps interface with one another over several iterations. Since the final estimator isn’t formally Bayesian due to post-processing the BART adjusted pseudo-outcome with kernel weighted least squares regression, we regard it as a multiple imputation-based estimator. We then described some issues that we encountered with this approach regarding the seeming conflict that exists between cutting feedback and appeasing rules about congeniality. We provided several simulated numerical examples that showcase why correcting for exposure measurement error within a causal-analysis is important to obtain unbiased estimates and valid inferences.

In the real data example, we estimated the exposure response function associating all-cause mortality with annual average PM2.5 exposures. At first glance, the three curves we estimate with varying degrees of measurement error correction all seem fairly similar for this particular analysis. These results seem to indicate that there is little benefit to correcting for measurement error while estimating ERFs, though the attenuation at lower PM2.5 levels is meaningful. However, the reason for the similarities are mainly due to the low levels of measurement error. As measurement error increases, so does the attenuation bias. Indeed, our attempts to correct for measurement error in our applied example does not seem to have a large impact on the results associating PM2.5 with mortality. Therefore, this analysis helps validate other analyses that used similar data but did not correct for measurement error.

While Medicare data limitations necessitate use of ZIP-code aggregate exposures in our analysis, there are various simplifications to Sections 2 and 3 that can be made to accommodate scenarios where certain measurement error sources are absent. If we were provided individual level outcomes and error-prone exposure data, then the measurement error would be closer to a Berkson-type rather than classical (Bateson and Wright,, 2010). Accounting for measurement error in this problem would require a different EPE model than the one proposed, however, adapting our framework should be straightforward given the adaptability of the Bayesian framework that we outlined (Carroll et al.,, 2006). Lastly, our approach assumes non-differential measurement error, which in our context means that is unaffected by given . More work is required to generalize this methodology to be useful in cases where the measurement error is differential.

Another line of future work involves relaxing the independence and homoscedastic assumptions surrounding the measurement error (Assumptions 1 and 2). Since these models are deployed within an MCMC framework, more sophisticated spatiotemporal modelling techniques might be employed to better understand the measurement error residing in the data. Second, alternatives to the parametric GPS and EPE models were not implemented in this work. However, more flexible nonparametric methods may help reduce model-dependency of the ERF. We relaxed some of this model-dependency by using a BART outcome model. However, the BART implementation we employed assumes the outcome is approximately Gaussian. There is an option for fitting log-linear BART models (Murray,, 2021) which might ameliorate some of the problems we encountered with BART, like the poor coverage probabilities observed in the simulation study (Hahn et al.,, 2020). However, at the time of writing, code to fit this alternative BART model could not be obtained. This problem may also be addressed by choosing a different outcome model as demonstrated in the simulations.

Acknowledgements

Funding was provided by the National Institute of Health (NIH) grants (T32 ES007142, R01 ES030616, R01 ES028033, R01 ES026217, K01 ES032458-01) and HEI grant 4953-RFA14-3/16-4. The contents are solely the responsibility of the grantee and do not necessarily represent the official views of the funding agencies. Further, the funding agencies do not endorse the purchase of any commercial products or services related to this publication.

Reproducible R Code

References

- Anderson, (2009) Anderson, H. R. (2009). Air pollution and mortality: A history. Atmospheric Environment, 43(1):142–152.

- Antonelli et al., (2020) Antonelli, J., Papadogeorgou, G., and Dominici, F. (In Press 2020). Causal inference in high dimensions: A marriage between bayesian modeling and good frequentist properties. Biometrics.

- Bateson and Wright, (2010) Bateson, T. F. and Wright, J. M. (2010). Regression calibration for classical exposure measurement error in environmental epidemiology studies using multiple local surrogate exposures. American journal of epidemiology, 172(3):344–352.

- Braun et al., (2017) Braun, D., Gorfine, M., Parmigiani, G., Arvold, N. D., Dominici, F., and Zigler, C. (2017). Propensity scores with misclassified treatment assignment: A likelihood-based adjustment. Biostatistics, 18(4):695–710.

- Brook et al., (2010) Brook, R. D., Rajagopalan, S., Pope III, C. A., Brook, J. R., Bhatnagar, A., Diez-Roux, A. V., Holguin, F., Hong, Y., Luepker, R. V., Mittleman, M. A., et al. (2010). Particulate matter air pollution and cardiovascular disease: an update to the scientific statement from the american heart association. Circulation, 121(21):2331–2378.

- Carroll et al., (2006) Carroll, R. J., Ruppert, D., Stefanski, L. A., and Crainiceanu, C. M. (2006). Measurement error in nonlinear models: a modern perspective. Chapman and Hall/CRC, Boca Raton, FL, USA.

- Chipman et al., (1998) Chipman, H. A., George, E. I., and McCulloch, R. E. (1998). Bayesian cart model search. Journal of the American Statistical Association, 93(443):935–948.

- Chipman et al., (2010) Chipman, H. A., George, E. I., and McCulloch, R. E. (2010). Bart: Bayesian additive regression trees. The Annals of Applied Statistics, 4(1):266–298.

- Cole et al., (2006) Cole, S. R., Chu, H., and Greenland, S. (2006). Multiple-imputation for measurement-error correction. International journal of epidemiology, 35(4):1074–1081.

- Danesh Yazdi et al., (2021) Danesh Yazdi, M., Wang, Y., Di, Q., Wei, Y., Requia, W. J., Shi, L., Sabath, M. B., Dominici, F., Coull, B. A., Evans, J. S., et al. (2021). Long-term association of air pollution and hospital admissions among medicare participants using a doubly robust additive model. Circulation, 143(16):1584–1596.

- Di et al., (2016) Di, Q., Koutrakis, P., and Schwartz, J. (2016). A hybrid prediction model for pm2. 5 mass and components using a chemical transport model and land use regression. Atmospheric environment, 131:390–399.

- Di et al., (2017) Di, Q., Wang, Y., Zanobetti, A., Wang, Y., Koutrakis, P., Choirat, C., Dominici, F., and Schwartz, J. D. (2017). Air pollution and mortality in the medicare population. New England Journal of Medicine, 376(26):2513–2522.

- Dominici et al., (2006) Dominici, F., Peng, R. D., Bell, M. L., Pham, L., McDermott, A., Zeger, S. L., and Samet, J. M. (2006). Fine particulate air pollution and hospital admission for cardiovascular and respiratory diseases. Jama, 295(10):1127–1134.

- Gill and Robins, (2001) Gill, R. D. and Robins, J. M. (2001). Causal inference for complex longitudinal data: the continuous case. Annals of Statistics, pages 1785–1811.

- Haber et al., (2020) Haber, G., Sampson, J., and Graubard, B. (2020). Bias due to berkson error: issues when using predicted values in place of observed covariates. Biostatistics, 22(4):858–872.

- Hahn et al., (2020) Hahn, P. R., Murray, J. S., and Carvalho, C. M. (2020). Bayesian regression tree models for causal inference: Regularization, confounding, and heterogeneous effects (with discussion). Bayesian Analysis, 15(3):965–1056.

- Hajat et al., (2002) Hajat, S., Anderson, H., Atkinson, R., and Haines, A. (2002). Effects of air pollution on general practitioner consultations for upper respiratory diseases in london. Occupational and environmental medicine, 59(5):294–299.

- Hastie et al., (2001) Hastie, T., Tibshirani, R., and Friedman, J. (2001). The Elements of Statistical Learning. Springer Series in Statistics. Springer New York Inc., New York, NY, USA.

- Kang and Schafer, (2007) Kang, J. D. Y. and Schafer, J. L. (2007). Demystifying Double Robustness: A Comparison of Alternative Strategies for Estimating a Population Mean from Incomplete Data. Statistical Science, 22(4):523 – 539.

- Keil et al., (2018) Keil, A. P., Daza, E. J., Engel, S. M., Buckley, J. P., and Edwards, J. K. (2018). A bayesian approach to the g-formula. Statistical methods in medical research, 27(10):3183–3204.

- Kennedy et al., (2017) Kennedy, E. H., Ma, Z., McHugh, M. D., and Small, D. S. (2017). Nonparametric methods for doubly robust estimation of continuous treatment effects. Journal of the Royal Statistical Society. Series B, Statistical Methodology, 79(4):1229.

- Kim et al., (2018) Kim, W., Kwon, K., Kwon, S., and Lee, S. (2018). The identification power of smoothness assumptions in models with counterfactual outcomes. Quantitative Economics, 9(2):617–642.

- Kioumourtzoglou et al., (2014) Kioumourtzoglou, M.-A., Spiegelman, D., Szpiro, A. A., Sheppard, L., Kaufman, J. D., Yanosky, J. D., Williams, R., Laden, F., Hong, B., and Suh, H. (2014). Exposure measurement error in pm 2.5 health effects studies: a pooled analysis of eight personal exposure validation studies. Environmental Health, 13(1):1–11.

- Lee, (2013) Lee, D. (2013). Carbayes: An r package for bayesian spatial modeling with conditional autoregressive priors. Journal of Statistical Software, 55(13):1–24.

- Lenis et al., (2017) Lenis, D., Ebnesajjad, C. F., and Stuart, E. A. (2017). A doubly robust estimator for the average treatment effect in the context of a mean-reverting measurement error. Biostatistics, 18(2):325–337.

- Leroux et al., (2000) Leroux, B. G., Lei, X., and Breslow, N. (2000). Estimation of disease rates in small areas: a new mixed model for spatial dependence. In Statistical models in epidemiology, the environment, and clinical trials, pages 179–191. Springer.

- Lewbel, (2007) Lewbel, A. (2007). Estimation of average treatment effects with misclassification. Econometrica, 75(2):537–551.

- Meng, (1994) Meng, X.-L. (1994). Multiple-Imputation Inferences with Uncongenial Sources of Input. Statistical Science, 9(4):538 – 558.

- Murray, (2021) Murray, J. S. (2021). Log-linear bayesian additive regression trees for multinomial logistic and count regression models. Journal of the American Statistical Association, 116(534):756–769.

- Nethery et al., (2021) Nethery, R. C., Mealli, F., Sacks, J. D., and Dominici, F. (2021). Evaluation of the health impacts of the 1990 clean air act amendments using causal inference and machine learning. Journal of the American Statistical Association, 116(535):1128–1139.

- Papadogeorgou et al., (2019) Papadogeorgou, G., Mealli, F., and Zigler, C. M. (2019). Causal inference with interfering units for cluster and population level treatment allocation programs. Biometrics, 75(3):778–787.

- Plummer, (2015) Plummer, M. (2015). Cuts in bayesian graphical models. Statistics and Computing, 25(1):37–43.

- Pope III et al., (2015) Pope III, C. A., Turner, M. C., Burnett, R. T., Jerrett, M., Gapstur, S. M., Diver, W. R., Krewski, D., and Brook, R. D. (2015). Relationships between fine particulate air pollution, cardiometabolic disorders, and cardiovascular mortality. Circulation research, 116(1):108–115.

- Ren et al., (2021) Ren, B., Wu, X., Braun, D., Pillai, N., and Dominici, F. (2021). Bayesian modeling for exposure response curve via gaussian processes: Causal effects of exposure to air pollution on health outcomes. arXiv preprint arXiv:2105.03454.

- Rhee et al., (2019) Rhee, J., Dominici, F., Zanobetti, A., Schwartz, J., Wang, Y., Di, Q., Balmes, J., and Christiani, D. C. (2019). Impact of long-term exposures to ambient pm2. 5 and ozone on ards risk for older adults in the united states. Chest, 156(1):71–79.

- Rubin, (1974) Rubin, D. B. (1974). Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of educational Psychology, 66(5):688.

- Rubin, (2004) Rubin, D. B. (2004). Multiple imputation for nonresponse in surveys. John Wiley & Sons, New York, NY, USA.

- Webb-Vargas et al., (2017) Webb-Vargas, Y., Rudolph, K. E., Lenis, D., Murakami, P., and Stuart, E. A. (2017). An imputation-based solution to using mismeasured covariates in propensity score analysis. Statistical methods in medical research, 26(4):1824–1837.

- Wendling et al., (2018) Wendling, T., Jung, K., Callahan, A., Schuler, A., Shah, N., and Gallego, B. (2018). Comparing methods for estimation of heterogeneous treatment effects using observational data from health care databases. Statistics in medicine, 37(23):3309–3324.

- World Health Organization, (2021) World Health Organization (2021). New who global air quality guidelines aim to save millions of lives from air pollution. https://www.who.int/.

- Wu et al., (2019) Wu, X., Braun, D., Kioumourtzoglou, M.-A., Choirat, C., Di, Q., and Dominici, F. (2019). Causal inference in the context of an error prone exposure: air pollution and mortality. The Annals of Applied Statistics, 13(1):520.

- Wu et al., (2020) Wu, X., Braun, D., Schwartz, J., Kioumourtzoglou, M., and Dominici, F. (2020). Evaluating the impact of long-term exposure to fine particulate matter on mortality among the elderly. Science advances, 6(29):eaba5692.

- Wu et al., (2018) Wu, X., Mealli, F., Kioumourtzoglou, M.-A., Dominici, F., and Braun, D. (2018). Matching on generalized propensity scores with continuous exposures. arXiv:1812.06575.

- Yazdi et al., (2019) Yazdi, M. D., Wang, Y., Di, Q., Zanobetti, A., and Schwartz, J. (2019). Long-term exposure to pm2. 5 and ozone and hospital admissions of medicare participants in the southeast usa. Environment international, 130:104879.

- Zanobetti et al., (2009) Zanobetti, A., Franklin, M., Koutrakis, P., and Schwartz, J. (2009). Fine particulate air pollution and its components in association with cause-specific emergency admissions. Environmental Health, 8(1):1–12.

- Zhu et al., (2017) Zhu, L., Ge, X., Chen, Y., Zeng, X., Pan, W., Zhang, X., Ben, S., Yuan, Q., Xin, J., Shao, W., et al. (2017). Short-term effects of ambient air pollution and childhood lower respiratory diseases. Scientific reports, 7(1):1–7.

- Zigler et al., (2013) Zigler, C. M., Watts, K., Yeh, R. W., Wang, Y., Coull, B. A., and Dominici, F. (2013). Model feedback in bayesian propensity score estimation. Biometrics, 69(1):263–273.

Tables and Figures

| GPS | Outcome | EPE | Relative Bias | 95% Coverage Probability | |||||||||||||||||

| No Correction |

|

|

|

No Correction |

|

|

|

||||||||||||||

| 400 | 2,000 | 1 | 1 | 0.35 (-0.09) | 0.28 (-0.09) | 0.21 (-0.06) | -0.03 (-0.02) | 0.44 (0.52) | 0.53 (0.54) | 0.75 (0.78) | 0.83 (0.90) | ||||||||||

| 400 | 2,000 | 1 | 2 | 0.42 (-0.11) | 0.30 (-0.09) | 0.28 (-0.06) | -0.05 (-0.02) | 0.39 (0.40) | 0.52 (0.46) | 0.74 (0.73) | 0.70 (0.91) | ||||||||||

| 400 | 2,000 | 2 | 1 | 0.38 (-0.12) | 0.32 (-0.11) | 0.22 (-0.08) | -0.03 (-0.02) | 0.39 (0.45) | 0.45 (0.48) | 0.71 (0.70) | 0.85 (0.90) | ||||||||||

| 400 | 2,000 | 2 | 2 | 0.42 (-0.14) | 0.29 (-0.13) | 0.21 (-0.08) | -0.05 (-0.02) | 0.36 (0.35) | 0.45 (0.44) | 0.71 (0.62) | 0.75 (0.92) | ||||||||||

| 400 | 4,000 | 1 | 1 | 0.30 (-0.06) | 0.21 (-0.06) | 0.20 (-0.04) | -0.03 (-0.02) | 0.53 (0.66) | 0.63 (0.69) | 0.78 (0.78) | 0.80 (0.91) | ||||||||||

| 400 | 4,000 | 1 | 2 | 0.31 (-0.08) | 0.18 (-0.07) | 0.21 (-0.05) | -0.06 (-0.02) | 0.47 (0.58) | 0.63 (0.65) | 0.78 (0.76) | 0.64 (0.92) | ||||||||||

| 400 | 4,000 | 2 | 1 | 0.29 (-0.09) | 0.23 (-0.08) | 0.19 (-0.06) | -0.02 (-0.02) | 0.47 (0.58) | 0.55 (0.64) | 0.74 (0.72) | 0.86 (0.92) | ||||||||||

| 400 | 4,000 | 2 | 2 | 0.30 (-0.11) | 0.19 (-0.10) | 0.15 (-0.07) | -0.04 (-0.02) | 0.42 (0.48) | 0.58 (0.52) | 0.76 (0.71) | 0.69 (0.93) | ||||||||||

| 800 | 4,000 | 1 | 1 | 0.29 (-0.08) | 0.21 (-0.07) | 0.12 (-0.03) | -0.04 (0.00) | 0.42 (0.45) | 0.53 (0.52) | 0.76 (0.75) | 0.77 (0.96) | ||||||||||

| 800 | 4,000 | 1 | 2 | 0.35 (-0.11) | 0.22 (-0.09) | 0.12 (-0.04) | -0.07 (0.00) | 0.37 (0.38) | 0.50 (0.44) | 0.72 (0.74) | 0.62 (0.96) | ||||||||||

| 800 | 4,000 | 2 | 1 | 0.36 (-0.10) | 0.29 (-0.09) | 0.15 (-0.04) | -0.04 (0.00) | 0.37 (0.38) | 0.41 (0.39) | 0.73 (0.71) | 0.82 (0.96) | ||||||||||

| 800 | 4,000 | 2 | 2 | 0.43 (-0.12) | 0.31 (-0.10) | 0.13 (-0.04) | -0.06 (0.00) | 0.35 (0.30) | 0.43 (0.38) | 0.72 (0.72) | 0.65 (0.94) | ||||||||||

| 800 | 8,000 | 1 | 1 | 0.20 (-0.06) | 0.15 (-0.05) | 0.10 (-0.03) | -0.04 (-0.01) | 0.50 (0.67) | 0.65 (0.69) | 0.78 (0.83) | 0.74 (0.94) | ||||||||||

| 800 | 8,000 | 1 | 2 | 0.26 (-0.06) | 0.16 (-0.05) | 0.10 (-0.03) | -0.07 (0.00) | 0.44 (0.56) | 0.59 (0.60) | 0.72 (0.76) | 0.59 (0.94) | ||||||||||

| 800 | 8,000 | 2 | 1 | 0.22 (-0.08) | 0.17 (-0.07) | 0.10 (-0.03) | -0.04 (-0.01) | 0.45 (0.52) | 0.55 (0.58) | 0.78 (0.78) | 0.78 (0.94) | ||||||||||

| 800 | 8,000 | 2 | 2 | 0.28 (-0.08) | 0.19 (-0.07) | 0.11 (-0.03) | -0.07 (-0.01) | 0.42 (0.45) | 0.56 (0.53) | 0.73 (0.74) | 0.62 (0.94) | ||||||||||

| 800 | 4,000 | 2 | 1 | ✓ | 0.91 (-0.09) | 0.30 (-0.09) | 0.15 (-0.04) | -0.03 (0.00) | 0.30 (0.47) | 0.42 (0.40) | 0.71 (0.73) | 0.76 (0.93) | |||||||||

| 800 | 4,000 | 2 | 1 | ✓ | 0.18 (-0.20) | 0.11 (-0.20) | -0.01 (-0.14) | 0.04 (0.00) | 0.25 (0.02) | 0.32 (0.03) | 0.55 (0.14) | 0.32 (0.96) | |||||||||

| 800 | 4,000 | 2 | 1 | ✓ | ✓ | 0.60 (-0.22) | 0.11 (-0.20) | -0.01 (-0.14) | 0.05 (0.00) | 0.19 (0.02) | 0.30 (0.02) | 0.55 (0.15) | 0.32 (0.97) | ||||||||

| 800 | 4,000 | 2 | 1 | ✓ | 0.52 (-0.06) | 0.46 (-0.05) | 0.29 (-0.01) | -0.03 (0.00) | 0.45 (0.54) | 0.49 (0.58) | 0.75 (0.82) | 0.75 (0.93) | |||||||||

| 800 | 4,000 | 2 | 1 | ✓ | ✓ | 1.28 (0.02) | 0.59 (-0.02) | 0.40 (0.02) | -0.03 (0.00) | 0.34 (0.66) | 0.49 (0.61) | 0.74 (0.82) | 0.74 (0.93) | ||||||||

| 800 | 4,000 | 2 | 1 | ✓ | ✓ | 0.15 (-0.21) | 0.08 (-0.20) | -0.05 (-0.15) | -0.09 (-0.05) | 0.18 (0.01) | 0.28 (0.01) | 0.44 (0.08) | 0.37 (0.77) | ||||||||

| 800 | 4,000 | 2 | 1 | ✓ | ✓ | ✓ | 0.52 (-0.25) | 0.02 (-0.23) | -0.09 (-0.16) | -0.09 (-0.05) | 0.15 (0.00) | 0.25 (0.00) | 0.41 (0.04) | 0.38 (0.72) | |||||||

Supplement to “Estimating a Causal Exposure Response Function with a Continuous Error-Prone Exposure: A Study of Fine Particulate Matter and All-Cause Mortality”

S1 MCMC Sampling Algorithm

In this supplement, we describe the MCMC sampling steps and provide additional details about the multiple imputation measurement error correction method that we present in Section 3. We will assume a BART model for the outcome, and Gaussian linear models for the GPS and EPE with and . Much of this methodology reflects the demonstrations provided in Chapter 9 of Carroll et al., (2006), if more information is desired.

Later on in the analysis stage we will require prior distributions for the parameter values in the likelihood model of (2). We suppose that exposure variance components follow conjugate inverse-gamma distributions, i.e. , , and . Each of the mean parameters for the GPS and EPE models contained in the vectors and are assigned a Gaussian prior with mean zero and variance or , respectively.

Before we proceed, there is some additional notation that we will need to define. Let denote a diagonal matrix with dimensions matching either the length of or , whichever is appropriate in the context that it appears. Finally, define the vectors , , , and the matrix .

To begin, initialize , , and for all and . We must also initialize the parameter values , , , , , , , , , and . For do:

-

•

Imputation Stage

-

1.

Sample where

Replace known quantities of when ;

-

2.

To sample , we will need to consider the full conditional likelihood:

For all , sample and for some pre-specified value that will achieve a sufficiently high acceptance probability. Set

where

-

1.

-

•

Analysis Stage

-

3.

Using the subset of individuals from , sample the prediction error mean parameters

and set ;

-

4.

Sample the GPS mean parameters

where is the th row and th column of , and

Then set ;

-

5.

Sample the prediction error variance

-

6.

Sample the GPS variance

-

7.

Sample the classical error variance

- 8.

- 9.

-

10.

Sample using a conjugate inverse-gamma prior distribution according to Chipman et al., (2010), supposing as the weights.

-

3.

With the posterior samples of the outcome model, , and the exposure imputations , we can proceed to fit the ERF using the local regression method described in Section S2.

S2 Kernel Weighted Least Squares Regression Details

In this supplement, we provide the details of the smoothing step outlined in Section 3.2. Given a bandwidth , the pseudo-outcomes in (4) are regressed onto fixed points by solving for where

| (5) |

and

For a given bandwidth representing the standard deviation of a Gaussian probability density function centered around , the kernel weights are equivalent to

As we mentioned already in the manuscript, the values do not form a proper posterior of . Instead, think of the as one of imputations for the ERF evaluated at , meaning we must use combining rules intended for multiple imputation to estimate the variance of . For each , we require the pointwise variance estimates for each . For this we can use a subtle modification to the locally-weighted least-squares variance estimator following the form

where and

| (6) |

Like the distribution for , the cumulative and empirical density functions for are written as and , respectively. At this point we can obtain a variance estimate using the combining rules of Rubin, (2004) with

where is the (1,1) element of . This approach is ideologically similar to Antonelli et al., (2020) who also use combining rules after regressing posterior samples onto the exposure to estimate the ERF.

The bandwidth can be chosen by cross-validation. This is accomplished by partitioning , , into one of several folds to find that minimizes the cross-validated mean squared error via grid search.

S3 Simulation Details

Sections S3.1 and S3.2 contains a complete description of the data generating mechanisms for the simulation study design in Section 4.1. We also provide the additional simulation results when at least one of the measurement error sources is set to , , , or both in Section S3.1. Contained within this table are results that partially align with the subfigures in Figure 3 (top-row and bottom-left subfigures when and ).

S3.1 Correct Specification

For cluster , let , , which we use to generate

with . For , we sample with . The associated predictions for are subsequently generated with the distribution where . The outcome counts are generated from a Poisson distribution with

In addition, we vary the total number of cells, when and when . The number of measurements in each of the clusters is distributed uniformly across when and or and . When and or and , then the number of measurements is uniformly distributed across . The offsets are generated from the uniform distribution . We fix the proportion of exposures that are within the validation set (i.e. when is “observed”) to .

S3.2 Incorrect Specification

We would also like to examine the potential sources of bias and error that might occur when we misspecify each of the three models in (2) - the outcome model, the generalized propensity score (GPS), and the error prone exposure model (EPE). Under correct specification, the data are generated using the the models described above in Section S3.1. Using the same definitions for as above, define , , , and (Kang and Schafer,, 2007). The transformations are subsequently scaled and centered to have a mean of zero and a marginal variance of one. Under a misspecified GPS scenario we generate

yet the GPS models are fit using the original covariates . Likewise, scenarios where the outcome model is misspecified means we generate with

However, we continue to fit the outcome models with the original (i.e. untransformed) covariates similar to the scenarios where the GPS is misspecified. Finally, when the EPE model is misspecified, then we introduce prediction bias, generating where and . In this scenario, the naïve approach will produce biased results since there is no adjustment for the added prediction bias. In the regression calibration and multiple imputation approaches, however, this bias is corrected for when addressing the prediction error, and therefore the downstream estimates of the ERF should be unbiased when the other models are well approximated. For these misspecification scenarios, we fix , , , , and .

S4 Congeniality Simulation

In this supplement, we run a small simulation study to demonstrate how using a GPS-based estimator has almost no influence over the accuracy of the ERF estimate while adhering to rules of congeniality (Meng,, 1994). As we mentioned in Section 3.3, the requirements of congeniality seem to conflict with the principles of cutting feedback in causal models fit with Bayesian methods (Zigler et al.,, 2013). To demonstrate how the feedback created by congeniality can affect estimators that condition on the GPS, we will need to incorporate the GPS into our pseudo-outcome. This implementation was described by Kennedy et al., (2017), who specify the following pseudo-outcome which we have adapted slightly to fit into the multiple imputation framework:

| (7) |

The first part of this pseudo-outcome, on the left-hand side of the addition symbol, characterizes an estimator of residual error conditioned on the stabilized inverse probability weights constructed from the posterior samples of the GPS. If the outcome model is correctly specified, then the average of these debiased residuals will approach zero as approaches infinity. The second part of (7), on the right-hand side of the addition symbol, is the marginalized outcome model. When the outcome model is misspecified, then the estimator of the residual error will counteract the asymptotic bias generated by the marginalized outcome model, thus allowing for an alternative means to debias the estimate so long as the GPS is correctly specified. Thus, this pseudo-outcome facilitates doubly-robust estimation when used in tandem with locally-weighted regression methods, at least in cases where imputing the exposure is not necessary.

Consider the simulation scenarios in Section S3, and in particular the misspecification scenarios in Section S3.2. We will once again fit the model in (2), but substitute with . Moreover, in an effort to better examine the doubly-robust properties of the pseudo-outcome in (7), which can be masked by the flexibility of a BART model, we will fit the likelihood in (2) assuming is a Poisson model, , where

| (8) |

Note that the simulated outcome data without misspecification is generated using the same model, where – are known. Otherwise, the smoothing steps outlined in Section S2 remain unchanged other than to substitute with the form in (8). The Gaussian models that we assumed for with for all , , and in Section 4 are also implemented in the same fashion here. The algorithm described in Section S1 is used to generate posterior draws of the latent exposures and unknown parameter values.

We are most interested in the scenarios where the outcome model is misspecified and the GPS is correctly specified. For an estimator to be doubly-robust, it must produce unbiased estimates in these scenarios. There are two curves for every subfigure in Figure S1, one where we use and the other where we use . Both curves use Gaussian kernel weighted least squares regression to project the respective pseudo-outcomes onto . Examining the scenarios where the GPS is correctly specified but the outcome model is misspecified, we can see that the two curves are nearly identical despite one using a doubly-robust form. Therefore, the utility of a doubly-robust estimator in this framework yields little to no benefit. The observed bias that we detect when the outcome model is misspecified and the GPS model is correctly specified, we contend, is due to the feedback created between the GPS and the outcome model from the requirements of congeniality to support multiple imputation.

The above analysis guided the development of our framework in the main manuscript. In an effort to limit any potential deleterious impacts created by feedback that may or may not exist given our limited testing, we decided to refrain from incorporating the GPS into our estimator of the ERF, even though we lose the possibility of achieving the doubly-robust property. However, from this simulation study, we did not see any benefit to using a doubly-robust estimator since it would seem that the outcome model needs to be correctly specified anyway. To make up for this loss, we decided to incorporate BART into our estimator of the ERF. BART is a nonparametric approach that provides added flexibility in cases of outcome model misspecification. We concede that more work is required to better understand how to ameliorate the feedback issue for GPS-based estimators of the ERF with a latent exposure variable.

Tables and Figures

| Relative Bias | 95% Coverage Probability | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| No Correction |

|

|

|

No Correction |

|

|

|

||||||||||||||

| 400 | 4,000 | 0 | 0 | 0.19 (-0.03) | 0.20 (-0.03) | 0.20 (-0.03) | 0.02 (-0.02) | 0.65 (0.75) | 0.65 (0.72) | 0.75 (0.80) | 0.90 (0.87) | ||||||||||

| 400 | 4,000 | 0 | 1 | 0.31 (-0.04) | 0.23 (-0.03) | 0.25 (-0.02) | 0.00 (-0.02) | 0.56 (0.64) | 0.66 (0.67) | 0.79 (0.78) | 0.91 (0.88) | ||||||||||

| 400 | 4,000 | 0 | 2 | 0.26 (-0.07) | 0.14 (-0.07) | 0.15 (-0.05) | 0.00 (-0.02) | 0.51 (0.64) | 0.63 (0.69) | 0.80 (0.78) | 0.90 (0.88) | ||||||||||

| 400 | 4,000 | 1 | 0 | 0.20 (-0.06) | 0.21 (-0.06) | 0.18 (-0.05) | 0.03 (-0.02) | 0.57 (0.70) | 0.57 (0.70) | 0.74 (0.76) | 0.93 (0.92) | ||||||||||

| 400 | 4,000 | 2 | 0 | 0.24 (-0.07) | 0.24 (-0.08) | 0.20 (-0.06) | 0.02 (-0.02) | 0.50 (0.62) | 0.50 (0.62) | 0.69 (0.75) | 0.93 (0.90) | ||||||||||

| 400 | 2,000 | 0 | 0 | 0.34 (0.01) | 0.35 (0.01) | 0.39 (0.02) | 0.02 (-0.02) | 0.64 (0.75) | 0.64 (0.76) | 0.74 (0.78) | 0.91 (0.90) | ||||||||||

| 400 | 2,000 | 0 | 1 | 0.27 (-0.06) | 0.17 (-0.06) | 0.19 (-0.04) | 0.00 (-0.02) | 0.53 (0.66) | 0.64 (0.66) | 0.76 (0.75) | 0.88 (0.92) | ||||||||||

| 400 | 2,000 | 0 | 2 | 0.31 (-0.10) | 0.18 (-0.08) | 0.19 (-0.05) | -0.01 (-0.02) | 0.42 (0.48) | 0.59 (0.54) | 0.76 (0.71) | 0.85 (0.86) | ||||||||||

| 400 | 2,000 | 1 | 0 | 0.25 (-0.08) | 0.24 (-0.07) | 0.19 (-0.06) | 0.01 (-0.02) | 0.49 (0.58) | 0.49 (0.62) | 0.69 (0.73) | 0.93 (0.90) | ||||||||||

| 400 | 2,000 | 2 | 0 | 0.35 (-0.09) | 0.35 (-0.09) | 0.24 (-0.07) | 0.02 (-0.02) | 0.44 (0.47) | 0.45 (0.52) | 0.67 (0.72) | 0.92 (0.89) | ||||||||||

| 800 | 8,000 | 0 | 0 | 0.09 (-0.02) | 0.10 (-0.02) | 0.10 (-0.02) | 0.00 (-0.01) | 0.69 (0.81) | 0.68 (0.80) | 0.78 (0.84) | 0.93 (0.94) | ||||||||||

| 800 | 8,000 | 0 | 1 | 0.13 (-0.04) | 0.08 (-0.03) | 0.10 (-0.02) | -0.01 (-0.01) | 0.57 (0.76) | 0.68 (0.78) | 0.79 (0.81) | 0.88 (0.94) | ||||||||||

| 800 | 8,000 | 0 | 2 | 0.18 (-0.06) | 0.10 (-0.05) | 0.10 (-0.02) | -0.01 (-0.01) | 0.49 (0.62) | 0.55 (0.70) | 0.78 (0.84) | 0.87 (0.92) | ||||||||||

| 800 | 8,000 | 1 | 0 | 0.16 (-0.04) | 0.15 (-0.04) | 0.12 (-0.02) | 0.01 (-0.01) | 0.57 (0.74) | 0.56 (0.74) | 0.75 (0.84) | 0.97 (0.96) | ||||||||||

| 800 | 8,000 | 2 | 0 | 0.21 (-0.05) | 0.21 (-0.05) | 0.15 (-0.03) | 0.01 (-0.01) | 0.50 (0.62) | 0.52 (0.68) | 0.72 (0.80) | 0.97 (0.96) | ||||||||||

| 800 | 4,000 | 0 | 0 | 0.11 (-0.02) | 0.11 (-0.01) | 0.12 (-0.02) | 0.01 (0.00) | 0.69 (0.82) | 0.70 (0.84) | 0.79 (0.90) | 0.94 (0.94) | ||||||||||

| 800 | 4,000 | 0 | 1 | 0.21 (-0.05) | 0.14 (-0.04) | 0.13 (-0.03) | -0.02 (0.00) | 0.50 (0.62) | 0.65 (0.67) | 0.76 (0.76) | 0.87 (0.93) | ||||||||||

| 800 | 4,000 | 0 | 2 | 0.28 (-0.09) | 0.18 (-0.07) | 0.11 (-0.03) | -0.03 (-0.01) | 0.39 (0.42) | 0.55 (0.56) | 0.74 (0.76) | 0.76 (0.94) | ||||||||||

| 800 | 4,000 | 1 | 0 | 0.19 (-0.06) | 0.18 (-0.06) | 0.13 (-0.04) | 0.01 (-0.01) | 0.48 (0.57) | 0.48 (0.56) | 0.72 (0.76) | 0.96 (0.94) | ||||||||||

| 800 | 4,000 | 2 | 0 | 0.28 (-0.09) | 0.28 (-0.08) | 0.17 (-0.04) | 0.01 (-0.01) | 0.42 (0.45) | 0.42 (0.48) | 0.69 (0.76) | 0.96 (0.94) | ||||||||||