Adversarial Regression

with Doubly Non-negative Weighting Matrices

Abstract

Many machine learning tasks that involve predicting an output response can be solved by training a weighted regression model. Unfortunately, the predictive power of this type of models may severely deteriorate under low sample sizes or under covariate perturbations. Reweighting the training samples has aroused as an effective mitigation strategy to these problems. In this paper, we propose a novel and coherent scheme for kernel-reweighted regression by reparametrizing the sample weights using a doubly non-negative matrix. When the weighting matrix is confined in an uncertainty set using either the log-determinant divergence or the Bures-Wasserstein distance, we show that the adversarially reweighted estimate can be solved efficiently using first-order methods. Numerical experiments show that our reweighting strategy delivers promising results on numerous datasets.

1 Introduction

We are interested in learning a parameter that has a competitive predictive performance on a response variable . Given training samples in which are the contexts that possess explanatory power on , learning the parameter can be posed as a weighted regression problem of the form

| (1) |

In problem (1), is a weighting function that indicates the contribution of the sample-specific loss to the objective. By aligning the covariate appropriately to the weighting term and the loss term , the generic formulation of problem (1) can be adapted to many popular learning and estimation tasks in machine learning. For example, problem (1) encapsulates the family of kernel smoothers, including the Nadaraya-Watson estimator [18, 24, 42].

Example 1.1 (Nadaraya-Watson (NW) estimator for conditional expectation).

Given the samples , we are interested in estimating the conditional expectation of given for some covariate . The NW estimator is the optimizer of problem (1) with and the weighting function is given through a kernel via . The NW estimate of admits a closed form expression

The NW estimator utilizes a locally constant function to estimate the conditional expectation . Locally linear regression [3, 34] extends the NW estimator to reduce the noise produced by the linear component of a target function [29, §3.2].

Example 1.2 (Locally linear regression (LLR)).

For univariate output and , the LLR minimizes the kernel-weighted loss with . The LLR estimate of admits a closed form expression

with , and

Intuitively, the NW and LLR estimators are special instances of the larger family of local polynomial estimators with order zero and one, respectively. Problem (1) is also the building block for local learning algorithms [8], density ratio estimation [5, pp.152], risk minimization with covariate shift [19, §4], domain adaptation [39], geographically weighted regression [9], local interpretable explanations [33], to name a few.

In all of the aforementioned applications, a prevailing trait is that the weight is given through a kernel. To avoid any confusion in the terminologies, it is instructive to revisit and distinguish the relevant definitions of kernels. The first family is the non-negative kernels, which are popularly employed in nonparametric statistics [40].

Definition 1.3 (Non-negative kernel).

A function is non-negative if for any .

In addition, there also exists a family of positive definite kernels, which forms the backbone of kernel machine learning [4, 35].

Definition 1.4 (Positive definite kernel).

A symmetric function is positive definite if for any and any choices of and , we have

| (2) |

Moreover, is strictly positive definite if we have in addition that for mutually distinct , the equality in (2) implies .

Positive definite kernels are a powerful tool to model geographical interactions [9], to characterize the covariance structure in Gaussian processes [31, §4], and to construct non-linear kernel methods [35]. Interestingly, the two above-mentioned families of kernels have a significant overlap. Examples of kernels that are both non-negative and strictly positive definite include the Gaussian kernel with bandwidth defined for any , as

the Laplacian kernel, the Cauchy kernel, the Matérn kernel, the rational quadratic kernel, etc.

It is well-known that the non-parametric statistical estimator obtained by solving (1) is sensitive to the corruptions of the training data [11, 23, 30]. Similar phenomenon is also observed in machine learning where the solution of the risk minimization problem (1) is not guaranteed to be robust or generalizable [1, 2, 14, 16, 21, 25, 44, 45, 46]. The quality of the solution to (1) also deteriorates if the training sample size is small. Reweighting, obtained by modifying , is arising as an attractive resolution to improve robustness and enhance the out-of-sample performance in the test data [32, 36, 43]. At the same time, reweighting schemes have shown to produce many favorable effects: reweighting can increase fairness [17, 22, 41], and can also effectively handle covariate shift [12, 19, 47].

While reweighting has been successfully applied to the empirical risk minimization regime in which the weights are uniformly , reweighting the samples when the weighting function is tied to a kernel is not a trivial task. In fact, the kernel captures inherently the relative positions of the relevant covariates , and any reweighting scheme should also reflect these relationship in a global viewpoint. Another difficulty also arises due to the lack of convexity or concavity, which prohibits the modifications of the kernel parameters. For example, the mapping for the Gaussian kernel is neither convex nor concave if . Thus, it is highly challenging to optimize over in the bandwidth parameter space. Alternatively, modifying the covariates will also result in reweighting effects. Nevertheless, optimizing over the covariates is intractable for sophisticated kernels such as the Matérn kernel.

Contributions. This paper relies fundamentally on an observation that the Gram matrix of a non-negative, (strictly) positive definite kernel is a non-negative, positive (semi)definite (also known as doubly non-negative) matrix. It is thus natural to modify the weights by modifying the corresponding matrix parametrization in an appropriate manner. Our contributions in this paper are two-fold:

-

•

We propose a novel scheme for reweighting using a reparametrization of the sample weights as a doubly non-negative matrix. The estimate is characterized as the solution to a min-max optimization problem, in which the admissible values of the weights are obtained through a projection of an uncertainty set from the matrix space.

-

•

We report in-depth analysis on two reweighting approaches based on the construction of the matrix uncertainty set with the log-determinant divergence and the Bures-Wasserstein distance. Exploiting strong duality, we show that the worst-case loss function and its gradient can be efficiently evaluated by solving the univariate dual problems. Consequently, the adversarially reweighted estimate can be found efficiently using first-order methods.

Organization of the paper. Section 2 introduces our generic framework of reweighting using doubly non-negative matrices. Sections 3 and 4 study two distinctive ways to customize our reweighting framework using the log-determinant divergence and the Bures-Wasserstein distance. Section 5 empirically illustrates that our reweighting strategy delivers promising results in the conditional expectation task based on numerous real life datasets.

Notations. The identity matrix is denoted by . For any , denotes the trace of , means that all entries of are nonnegative. Let denote the vector space of -by- real and symmetric matrices. The set of positive (semi-)definite matrices is denoted by (respectively, ). For any , we use to denote the Frobenius inner product between and , and to denote the Euclidean norm of .

2 A Reweighting Framework with Doubly Non-negative Matrices

We delineate in this section our reweighting framework using doubly non-negative matrices. This framework relies on the following observation: we can reparametrize the weights in (1) into a matrix and the loss terms in (1) into a matrix , and the solution to the estimation problem (1) can be equivalently characterized as the minimizer of the problem

| (3) |

Notice that there may exist multiple equivalent reparametrizations of the form (3). However, in this paper, we focus on one specific parametrization where is the nominal matrix of weights

with the elements being given by the weighting function as for , and the matrix-valued mapping satisfies

A simple calculation reveals that the objective function of (3) is equivalent to that of (1) up to a positive constant factor of 2. As a consequence, their solutions coincide.

Problem (3) is an overparametrized reformulation of the weighted risk minimization problem (1). Indeed, the objective function of problem (3) involves an inner product of two symmetric matrices, while problem (1) can be potentially reformulated using an inner product of two vectors. While lifting the problem to the matrix space is not necessarily the most efficient approach, it endows us with more flexibility to perturb the weights in a coherent manner. This flexibility comes from the following two observations: (i) there may exist multiple matrices that can be used as the nominal matrix , and one can potentially choose to improve the quality of the estimator, (ii) the geometry of the space of positive (semi)definite matrices is richer than the space of vectors.

To proceed, we need to make the following assumption.

Assumption 2.1 (Regularity conditions).

The following assumptions hold throughout the paper.

-

(i)

The function is nonnegative, and is convex, continuously differentiable for any .

-

(ii)

The nominal weighting matrix is symmetric positive definite and nonnegative.

In this paper, we propose to find an estimate that solves the following adversarially reweighted estimation problem

| (4) |

for some set of feasible weighting matrices. The estimate thus minimizes the worst-case loss uniformly over all possible perturbations of the weight . In particular, we explore the construction of the uncertainty set that is motivated by the Gram matrix obtained via some non-negative and positive definite kernels. In this way, the weighting matrix can capture more information on the pair-wise relation among training data. Hence, it is reasonable to consider the set of the form

| (5) |

By definition, any is a symmetric, positive semidefinite matrix and all elements of are nonnegative. A matrix with these properties is called doubly nonnegative. From a high level perspective, the set is defined as a ball of radius centered at the nominal matrix and this ball is prescribed by a pre-determined measure of dissimilarity . Throughout this paper, we prescribe the uncertainty set using some divergence on the space of symmetric, positive semidefinite matrices .

Definition 2.2 (Divergence).

For any , is a divergence on the symmetric positive semidefinite matrix space if it is: (i) non-negative: for all , and (ii) indiscernable: if then .

If we denote the adversarially reweighted loss function associated with by

then can be equivalently rewritten as

| (6) |

A direct consequence is that the function is convex in as long as the loss function satisfies the convex property of Assumption 2.1(i). Hence, the estimate can be found efficiently using convex optimization provided that the function and its gradient can be efficiently evaluated. Moreover, because is a divergence, . Hence by setting , we will recover the nominal estimate that solves (1). In Section 3 and 4, we will subsequently specify two possible choices of that lead to the desired efficiency in computing as well as its gradient. Further discussion on Assumption 2.1 is relegated to the appendix. We close this section by discussing the robustness effects of our weighting scheme (4) on the conditional expectation estimation problem.

Remark 2.3 (Connection to distributionally robust optimization).

Consider the conditional expectation estimation setting, in which is the solution of the minimum mean square error estimation problem

In this setting, our reweighting scheme (4) coincides with the following distributionally robust optimization problem

with the nominal conditional distribution defined as . The ambiguity set is a set of conditional probability measures of constructed specifically as

Remark 2.3 reveals that our reweighting scheme recovers a specific robustification with distributional ambiguity. This robustification relies on using a kernel density estimate to construct the nominal conditional distribution, and the weights of the samples are induced by . Hence, our scheme is applicable for the emerging stream of robustifying conditional decisions, see [13, 20, 27, 28].

Remark 2.4 (Choice of the nominal matrix).

The performance of the estimate may depend on the specific choice of the nominal matrix . However, in this paper, we do not study this dependence in details. When the weights are given by a kernel, it is advised to choose as the Gram matrix.

3 Adversarial Reweighting Scheme using the Log-Determinant Divergence

We here study the adversarially reweighting scheme when the is the log-determinant divergence.

Definition 3.1 (Log-determinant divergence).

For any positive integer , the log-determinant divergence from to amounts to

The divergence is the special instance of the log-determinant -divergence with [10]. Being a divergence, is non-negative and it vanishes to zero if and only if . It is important to notice that the divergence is only well-defined when both and are positive definite. Moreover, is non-symmetric and in general. The divergence is also tightly connected to the Kullback-Leibler divergence between two Gaussian distributions, and that , where is a normal distribution with mean 0 and covariance matrix .

Suppose that is invertible. Define the uncertainty set

For any positive definite matrix , the function is convex, thus the set is also convex. For this section, we examine the following optimal value function

| (7) |

which corresponds to the worst-case reweighted loss using the divergence . The maximization problem (7) constitutes a nonlinear, convex semidefinite program. Leveraging a strong duality argument, the next theorem asserts that the complexity of evaluating is equivalent to the complexity of solving a univariate convex optimization problem.

Theorem 3.2 (Primal representation).

For any and , the function is convex. Moreover, for any such that , let be the unique solution of the convex univariate optimization problem

| (8) |

then , where . Moreover, the symmetric matrix is unique and doubly nonnegative.

Notice that the condition is not restrictive: if , then Assumption 2.1(i) implies that the incumbent solution incurs zero loss with for all . In this case, is optimal and reweighting will produce no effect whatsoever. Intuitively, the infimum problem (8) is the dual counterpart of the supremum problem (7). The objective function of (8) is convex in the dual variable , and thus problem (8) can be efficiently solved using a gradient descent algorithm.

The gradient of is also easy to compute, as asserted in the following lemma.

Lemma 3.3 (Gradient of ).

The function is continuously differentiable at with

where is defined as in Theorem 3.2 using the parametrization

| (9) |

The proof of Lemma 3.3 exploits Danskin’s theorem and the fact that is unique in Theorem 3.2. Minimizing is now achievable by applying state-of-the-art first-order methods.

Sketch of Proof of Theorem 3.2. The difficulty in deriving the dual formulation (8) lies in the non-negativity constraint . In fact, this constraint imposes individual component-wise constraints, and as such, simply dualizing problem (7) using a Lagrangian multiplier will entail a large number of auxiliary variables. To overcome this difficulty, we consider the relaxed set . By definition, we have , and omits the nonnegativity requirement . The set is also more amenable to optimization thanks to the following proposition.

Proposition 3.4 (Properties of ).

For any and , the set is convex and compact. Moreover, the support function of satisfies

for any symmetric matrix .

Moreover, we need the following lemma which asserts some useful properties of the matrix .

Lemma 3.5 (Properties of ).

For any , the matrix is symmetric, nonnegative, and it has only two non-zero eigenvalues of value .

The proof of Theorem 3.2 proceeds by first constructing a tight upper bound for as

| (10) |

where the inequality in (10) follows from the fact that , and the equality follows from Proposition 3.4. Notice that has one nonnegative eigenvalue by virtue of Lemma 3.5 and thus the constraint already implies the condition . Next, we argue that the optimizer of problem (10) can be constructed from the optimizer of the infimum problem via

The last step involves proving that is a nonnegative matrix, and hence . As a consequence, the inequality (10) holds as an equality, which leads to the postulated result. The proof is relegated to the Appendix.

4 Adversarial Reweighting Scheme using the Bures-Wasserstein Type Divergence

In this section, we explore the construction of the set of possible weighting matrices using the Bures-Wasserstein distance on the space of positive semidefinite matrices.

Definition 4.1 (Bures-Wasserstein divergence).

For any positive integer , the Bures-Wasserstein divergence between and amounts to

For any positive semidefinite matrices and , the value is equal to the square of the type-2 Wasserstein distance between two Gaussian distributions and [15]. As a consequence, is a divergence: it is non-negative and indiscernable. However, is not a proper distance because it may violate the triangle inequality. Compared to the divergence studied in Section 3, the divergence has several advantages as it is symmetric and is well-defined for all positive semidefinite matrices. This divergence has also been of interest in quantum information, statistics, and the theory of optimal transport.

Given the nominal weighting matrix , we define the set of possible weighting matrices using the Bures-Wasserstein divergence as

Correspondingly, the worst-case loss function is

| (11) |

Theorem 4.2 (Primal representation).

For any and , the function is convex. Moreover, for any such that , let be the unique solution of the convex univariate optimization problem

| (12) |

then , where . Moreover, the symmetric matrix is unique and doubly nonnegative.

Thanks to the uniqueness of and Danskin’s theorem, the gradient of is now a by-product of Theorem 4.2.

Lemma 4.3 (Gradient of ).

A first-order minimization algorithm can be used to find the robust estimate with respect to the loss function . Notice that problem (12) is one-dimensional, and either a bisection search or a gradient descent subroutine can be employed to solve (12) efficiently.

Sketch of Proof of Theorem 4.2. The proof of Theorem 4.2 follows a similar line of argument as the proof of Theorem 3.2. Consider the relaxed set . By definition, omits the nonnegativity requirement and thus . The advantage of considering arises from the fact that the support function of the set admits a simple form [26, Proposition A.4].

Proposition 4.4 (Properties of ).

For any and , the set is convex and compact. Moreover, the support function of satisfies

The upper bound for can be constructed as

| (13) |

where the inequality in (13) follows from the fact that , and the equality follows from Proposition 4.4. In the second step, we argue that the optimizer of problem (13) can be constructed from the optimizer of the infimum problem via

The last step involves proving that is a nonnegative matrix by exploiting Lemma 3.5, and hence . Thus, inequality (13) is tight, leading to the desired result.

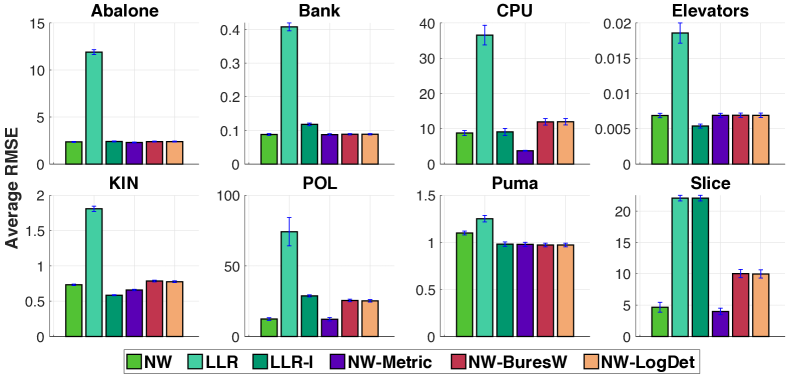

5 Numerical Experiments on Real Data

We evaluate our adversarial reweighting schemes on the conditional expectation estimation task. To this end, we use the proposed reweighted scheme on the NW estimator of Example 1.1. The robustification using the log-determinant divergence and the Bures-Wasserstein divergence are denoted by NW-LogDet and NW-BuresW, respectively. We compare our NW robust estimates against four popular baselines for estimating the conditional expectation: (i) the standard NW estimate in Example 1.1 with Gaussian kernel, (ii) the LLR estimate in Example 1.2 with Gaussian kernel, (iii) the intercepted of LLR estimate (i.e., only the first dimension of ), denoted as LLR-I, and (iv) the NW-Metric [29] which utilizes the Mahalanobis distance in the Gaussian kernel.

Datasets. We use 8 real-world datasets: (i) abalone (Abalone), (ii) bank-32fh (Bank), (iii) cpu (CPU), (iv) kin40k (KIN), (v) elevators (Elevators), (vi) pol (POL), (vii) pumadyn32nm (PUMA), and (viii) slice (Slice) from the Delve datasets, the UCI datasets, the KEEL datasets and datasets in Noh et al. [29]. Due to space limitation, we report results on the first 4 datasets and relegate the remaining results to the Appendix. Datasets characteristics can also be found in the supplementary material.

Setup. For each dataset, we randomly split samples for training, samples for validation to choose the bandwith of the Gaussian kernel, and samples for test. More specially, we choose the squared bandwidth for the Gaussian kernel from a predefined set . For a tractable estimation, we follow the approach in Brundsdon et al. [9] and Silverman [37] to restrict the relevant samples to nearest neighbors of each test sample with . The range of the radius has 4 different values . Finally, the prediction error is measured by the root mean square error (RMSE), i.e., where is the test sample size (i.e., ) and is the conditional expectation estimate at the test sample . We repeat the above procedure times to obtain the average RMSE. All our experiments are run on commodity hardware.

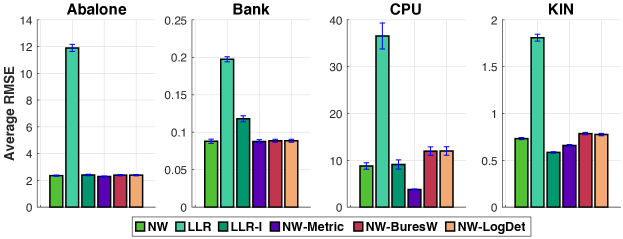

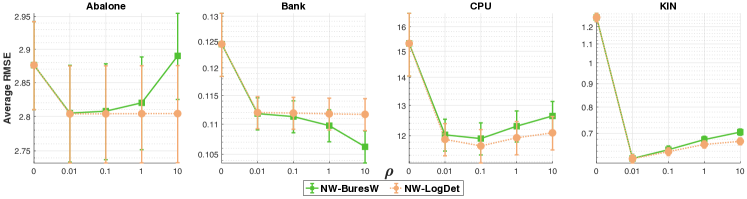

Ideal case: no sample perturbation. We first study how different estimators perform when there is no perturbation in the training data. In this experiment, we set the nearest neighbor size to , and our reweighted estimators are obtained with the uncertainty size of .

Figure 1 shows the average RMSE across the datasets. The NW-Metric estimator outperforms the standard NW, which agrees with the empirical observation in Noh et al. [29]. More importantly, we observe that our adversarial reweighting schemes perform competitively against the baselines on several datasets.

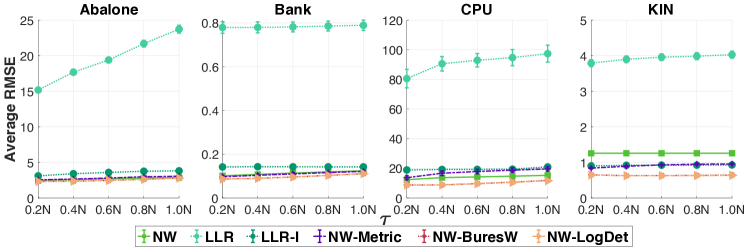

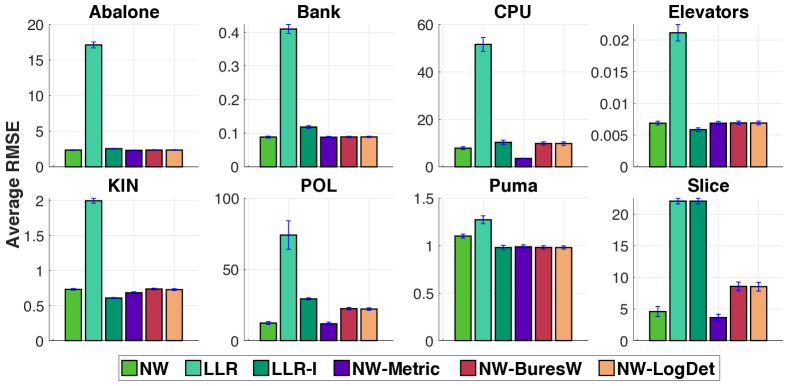

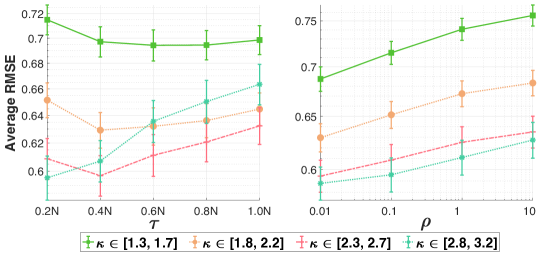

When training samples are perturbed. We next evaluate the estimation performances when nearest samples from the training neighbors of each test sample are perturbed. We specifically generate perturbations only in the response dimension by shifting , where is sampled uniformly from . We set and as the experiment for the ideal case (no sample perturbation).

Figure 2 shows the average RMSE for with varying perturbation level . The performance of the NW, LLR, LLR-I, and NW-Metric baselines severely deteriorate, while both NW-LogDet and NW-BuresW can alleviate the effect of data perturbation. Our adversarial reweighting schemes consistently outperform all baselines in all datasets for the perturbed training data, across all 5 perturbations .

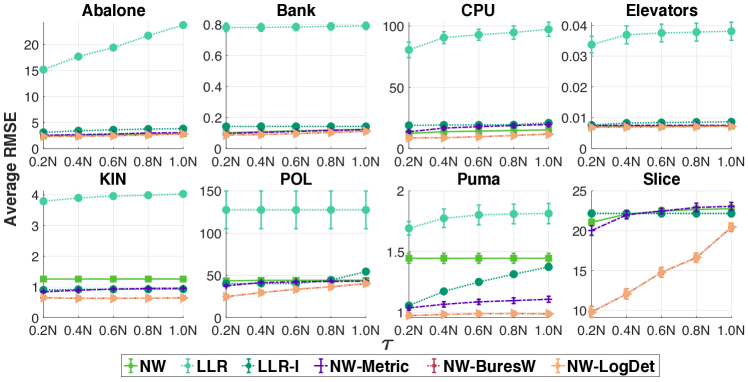

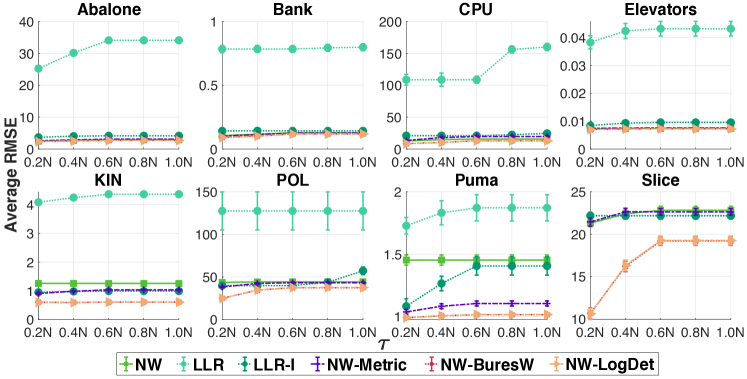

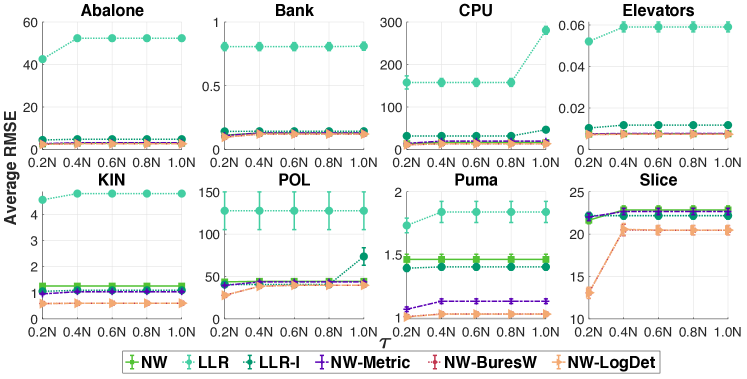

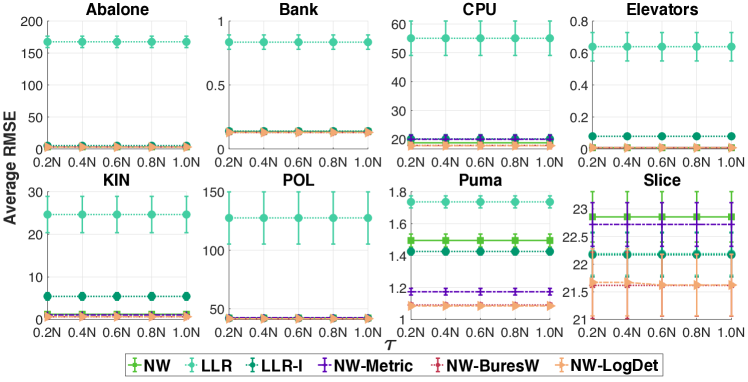

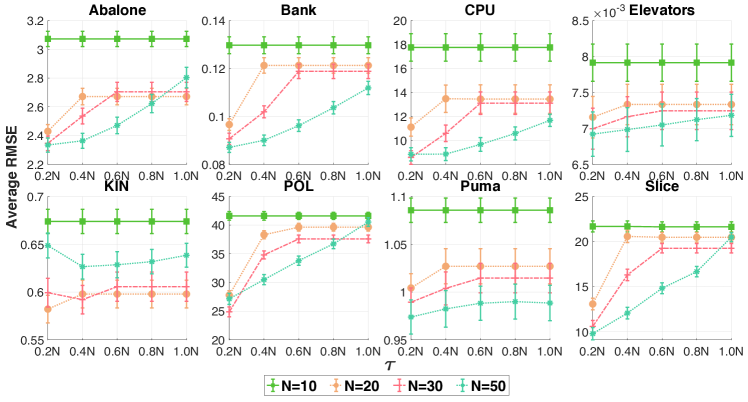

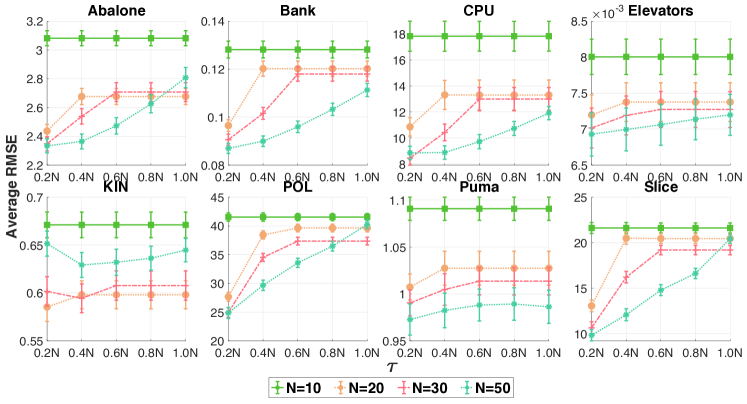

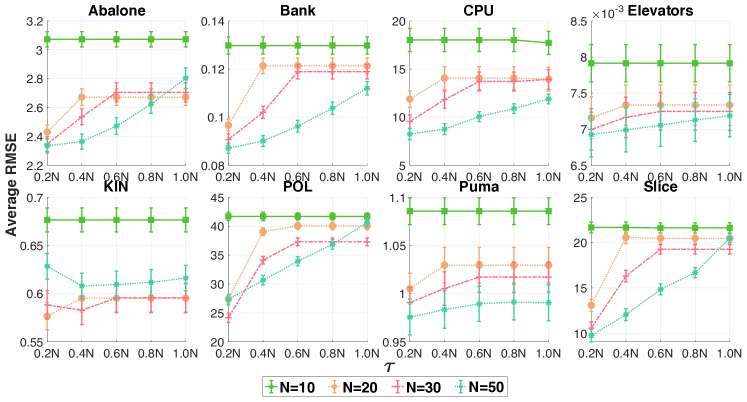

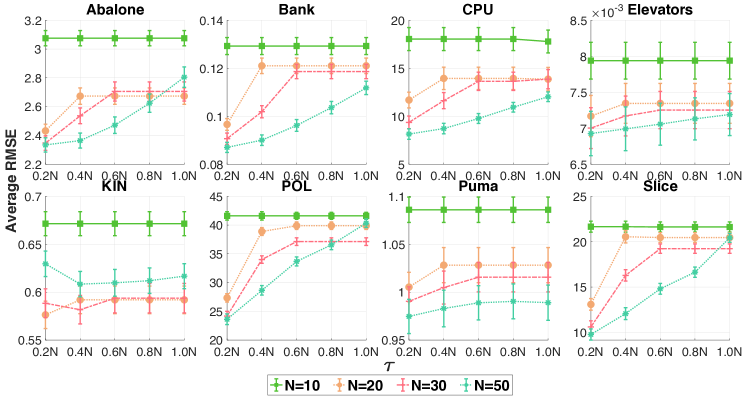

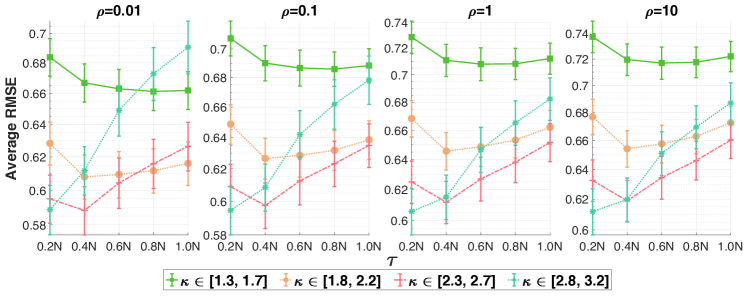

We then evaluate the effects of the uncertainty size and the nearest neighbor size on NW-LogDet and NW-BuresW.

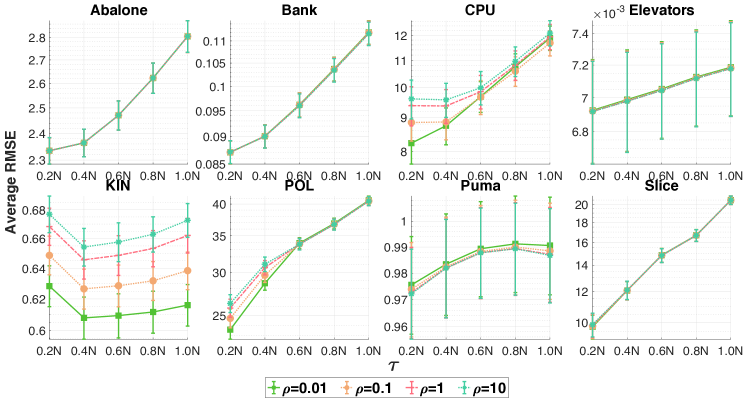

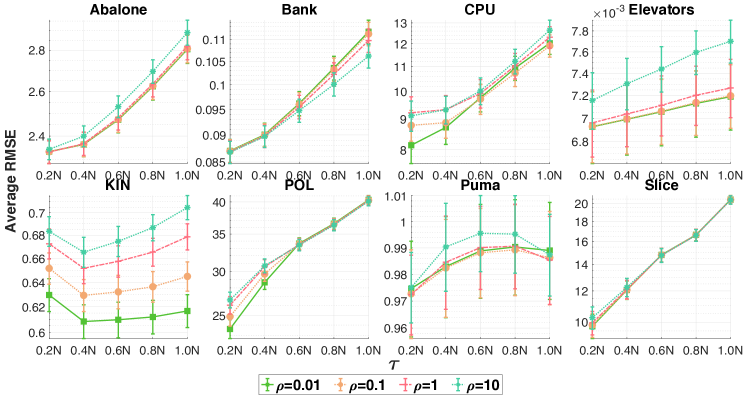

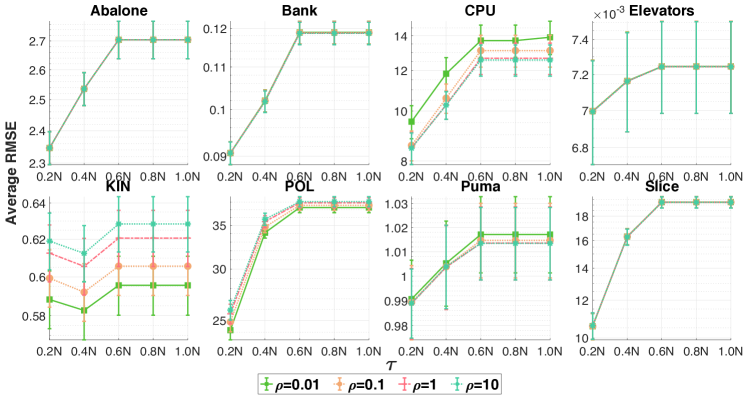

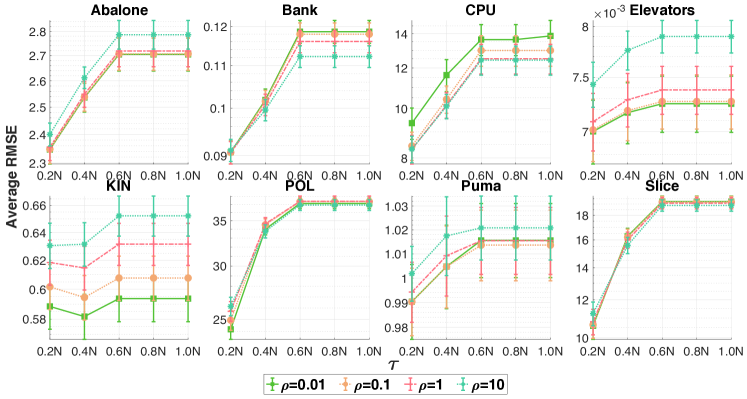

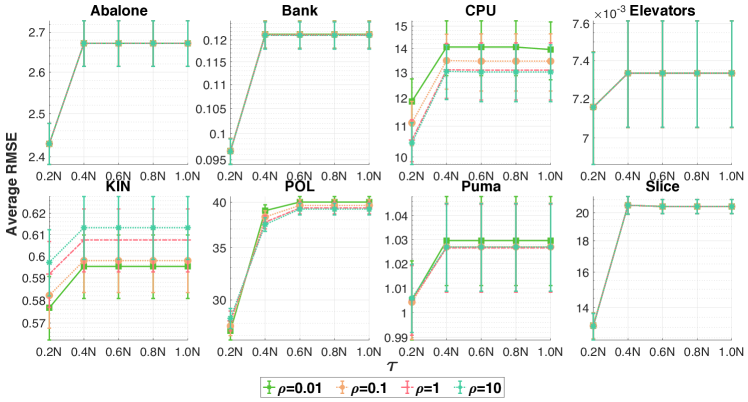

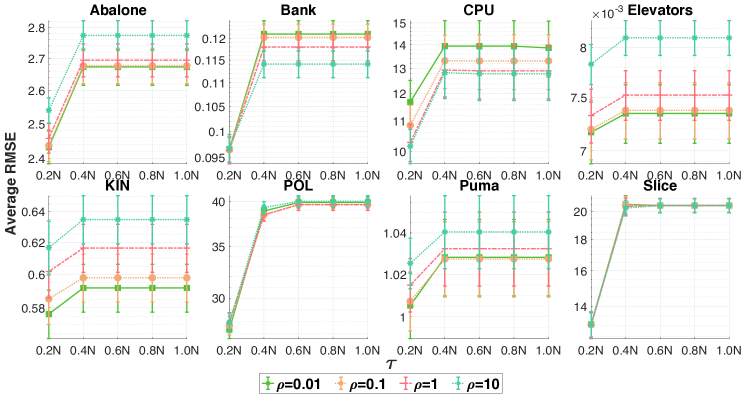

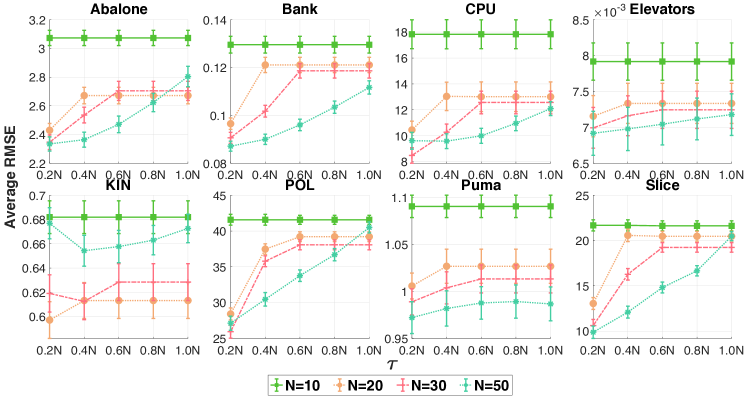

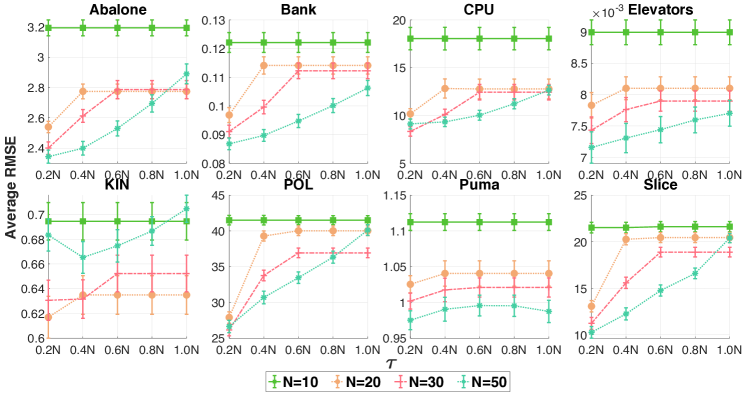

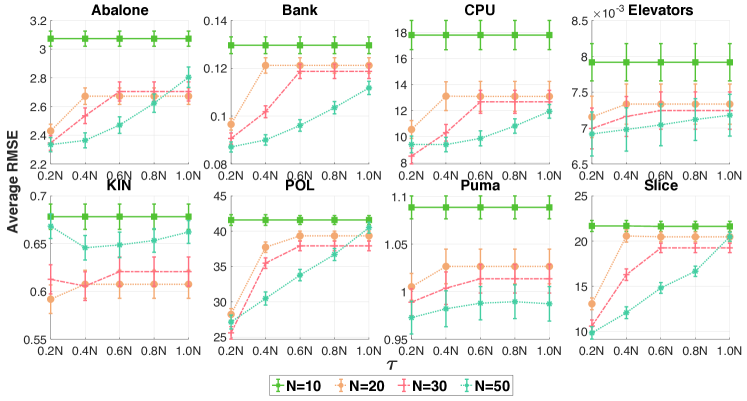

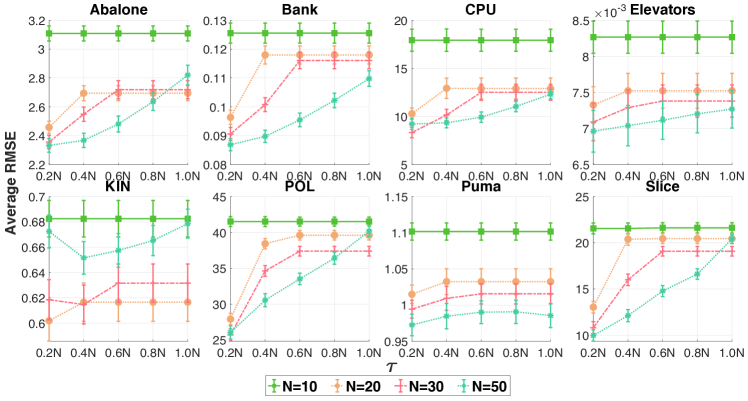

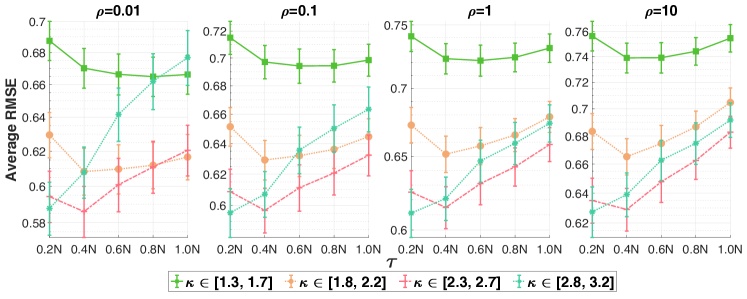

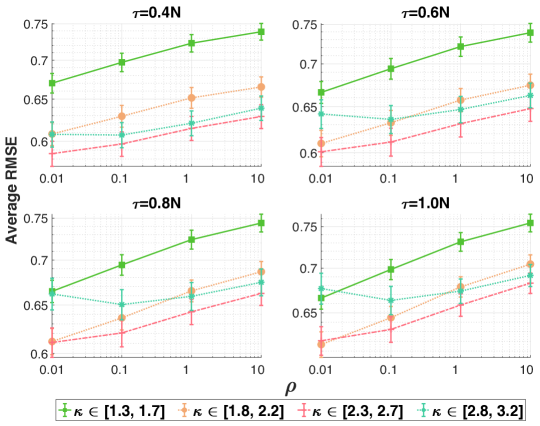

Effects of the uncertainty size . In this experiment, we set the nearest neighbor size to , the perturbation . Figure 3 illustrates the effects of the uncertainty size for the adversarial reweighting schemes. Errors at indicate the performance of the vanilla NW estimator. We observe that the adversarial reweighting schemes perform well at some certain and when that is increased more, the performances decrease. The uncertainty size plays an important role for the adversarial reweighting schemes in applications. Tuning may consequently improve the performances of the adversarial reweighting schemes.

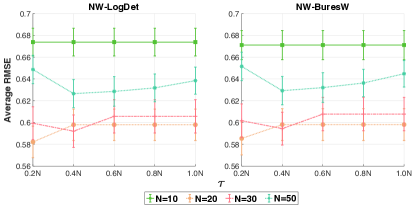

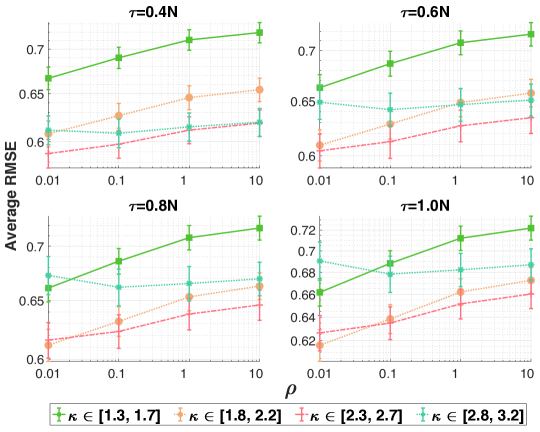

Effects of the nearest neighbor size . In this experiment, we set the uncertainty size to .

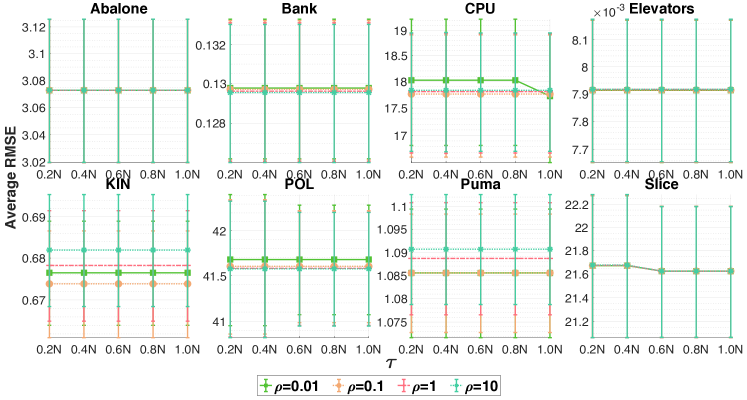

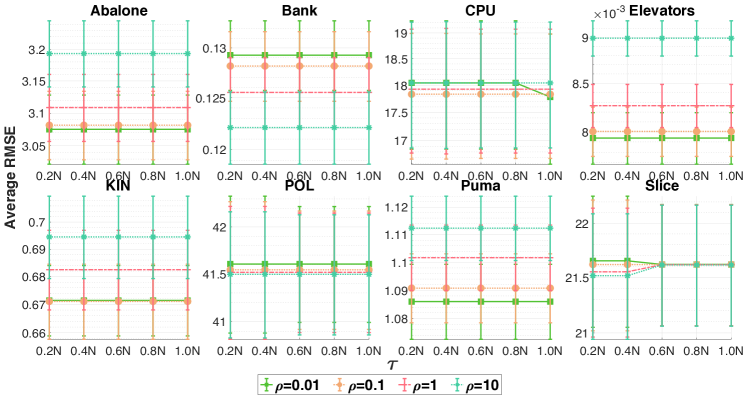

Figure 4 shows the effects of the nearest neighbor size for the adversarial reweighting schemes under varying perturbation in the KIN dataset. We observe that the performances of the adversarial reweighting schemes with perform better than those with . Note that when is increased, the computational cost is also increased (see Equation (1) and Figure 6). Similar to the cases of the uncertainty size , tuning may also help to improve performances of the adversarial reweighting schemes.

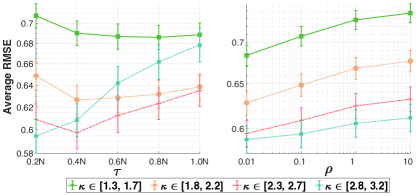

Under varying shifting w.r.t. . In this experiment, we set the nearest neighbor size to . Figure 5 illustrates the performances of NW-LogDet under varying shifting w.r.t. in the KIN dataset. For the left plots of the Figures 5, we set the uncertainty size to when varying the perturbation . We observe that the adversarial reweighting schemes provide different degrees of mitigation for the perturbation under varying shifting w.r.t. . For the right plots of the Figures 5, we set the perturbation to when varying the uncertainty size . We observe that the reweighting schemes under varying shifting w.r.t. have the same behaviors as in Figure 3 when we consider the effects of the uncertainty size (i.e., when ). Similar results for NW-BuresW are reported in the supplementary material.

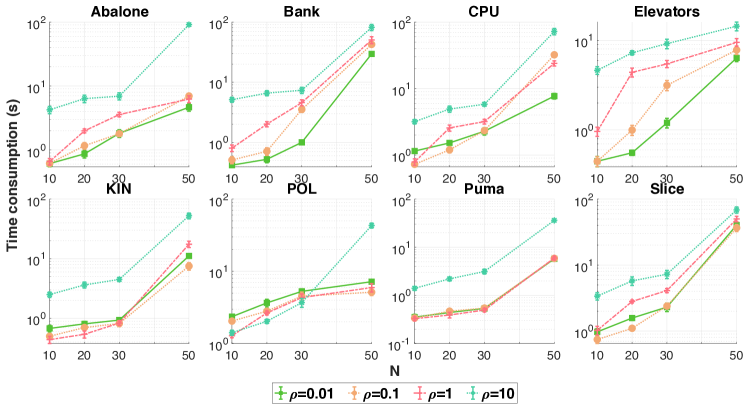

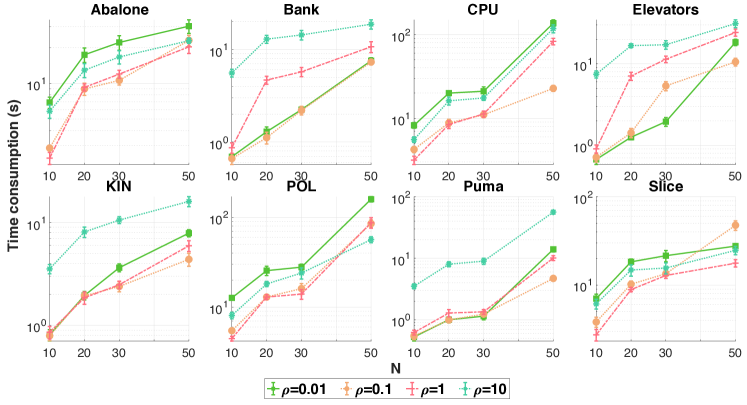

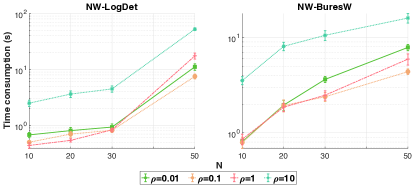

Time consumption. In Figure 6, we illustrate the time consumption for the adversarial reweighting schemes under varying neighbor size and uncertainty size in the KIN dataset. The adversarial reweighting schemes averagely take about seconds for their estimation. When and/or increases, the computation of the adversarial reweighting schemes take longer. This is intuitive because the dimension of the weight matrix scales quadratically in the neighbor size . Bigger uncertainty size implies a larger feasible set , which leads to longer computing time to evaluate and its gradient.

Concluding Remarks. We introduce two novel schemes for sample reweighting using matrix reparametrization. These two invariants are particularly attractive when the original weights are given through kernel functions. Note that the adversarial reweighting with Bures-Wasserstein distance can be generalized to cases where the nominal weighting matrix is singular, unlike the reweighting with the log-determinant divergence .

Remark 5.1 (Invariant under permutation).

Our results hold under any simultaneous row and column permutation of the nominal weighting matrix and the mapping . To see this, let be any -dimensional permutation matrix, and let and . Then

where is calculated as in Theorem 3.2 for , and as in Theorem 4.2 for . The proof relies on the fact that , that both and are permutation invariant (in the sense that ), and that the inner product is also permutation invariant. Similar results hold for the gradient information, and hence the optimal solution of is preserved under row and column permutations of and .

Acknowledgements. Material in this paper is based upon work supported by the Air Force Office of Scientific Research under award number FA9550-20-1-0397. Support is gratefully acknowledged from NSF grants 1915967, 1820942, 1838676, Simons Foundation grant (), JSPS KAKENHI grant 20K19873, and MEXT KAKENHI grants 20H04243, 21H04874. We thank the anonymous referees for their constructive feedbacks that helped improve and clarify this paper.

References

- [1] David Alvarez-Melis and Tommi S Jaakkola. On the robustness of interpretability methods. arXiv preprint arXiv:1806.08049, 2018.

- [2] Dario Amodei, Sundaram Ananthanarayanan, Rishita Anubhai, Jingliang Bai, Eric Battenberg, Carl Case, Jared Casper, Bryan Catanzaro, Qiang Cheng, and Guoliang Chen. Deep speech 2 : End-to-end speech recognition in English and Mandarin. In Proceedings of The 33rd International Conference on Machine Learning, volume 48, pages 173–182, 2016.

- [3] Christopher G Atkeson, Andrew W Moore, and Stefan Schaal. Locally weighted learning. Lazy Learning, pages 11–73, 1997.

- [4] Christian Berg, Jens Peter Reus Christensen, and Paul Ressel. Harmonic Analysis on Semigroups: Theory of Positive Definite and Related Functions. Springer, 1984.

- [5] Alain Berlinet and Christine Thomas-Agnan. Reproducing Kernel Hilbert Space in Probability and Statistics. Kluwer Academic Publishers, 2004.

- [6] Dimitri Bertsekas. Convex Optimization Theory. Athena Scientific, 2009.

- [7] Dimitri P. Bertsekas. Control of Uncertain Systems with a Set-Membership Description of Uncertainty. PhD thesis, Massachusetts Institute of Technology, 1971.

- [8] Léon Bottou and Vladimir Vapnik. Local learning algorithms. Neural Computation, 4(6):888–900, 11 1992.

- [9] Chris Brunsdon, Stewart Fotheringham, and Martin Charlton. Geographically weighted regression. Journal of the Royal Statistical Society: Series D (The Statistician), 47(3):431–443, 1998.

- [10] Zeineb Chebbi and Maher Moakher. Means of Hermitian positive-definite matrices based on the log-determinant -divergence function. Linear Algebra and its Applications, 436(7):1872 – 1889, 2012.

- [11] Simon Du, Yining Wang, Sivaraman Balakrishnan, Pradeep Ravikumar, and Aarti Singh. Robust nonparametric regression under Huber’s -contamination model. arXiv preprint arXiv:1805.10406, 2018.

- [12] John C Duchi, Tatsunori Hashimoto, and Hongseok Namkoong. Distributionally robust losses against mixture covariate shifts. Under review, 2019.

- [13] Adrián Esteban-Pérez and Juan M Morales. Distributionally robust stochastic programs with side information based on trimmings. arXiv preprint arXiv:2009.10592, 2020.

- [14] Amirata Ghorbani, Abubakar Abid, and James Zou. Interpretation of neural networks is fragile. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 3681–3688, Jul. 2019.

- [15] C.R. Givens and R.M. Shortt. A class of Wasserstein metrics for probability distributions. The Michigan Mathematical Journal, 31(2):231–240, 1984.

- [16] Moritz Hardt, Eric Price, Eric Price, and Nati Srebro. Equality of opportunity in supervised learning. In Advances in Neural Information Processing Systems, volume 29, pages 3315–3323, 2016.

- [17] Tatsunori Hashimoto, Megha Srivastava, Hongseok Namkoong, and Percy Liang. Fairness without demographics in repeated loss minimization. In International Conference on Machine Learning, pages 1929–1938, 2018.

- [18] Trevor Hastie, Robert Tibshirani, and Jerome Friedman. The Elements of Statistical Learning. Springer, 2009.

- [19] Weihua Hu, Gang Niu, Issei Sato, and Masashi Sugiyama. Does distributionally robust supervised learning give robust classifiers? In Proceedings of the 35th International Conference on Machine Learning, 2018.

- [20] Rohit Kannan, Güzin Bayraksan, and James R Luedtke. Residuals-based distributionally robust optimization with covariate information. arXiv preprint arXiv:2012.01088, 2020.

- [21] JooSeuk Kim and Clayton D. Scott. Robust kernel density estimation. The Journal of Machine Learning Research, 13:2529–2565, 2012.

- [22] Preethi Lahoti, Alex Beutel, Jilin Chen, Flavien Prost Kang Lee, Nithum Thain, Xuezhi Wang, and Ed Chi. Fairness without demographics through adversarially reweighted learning. In Advances in Neural Information Processing Systems, 2020.

- [23] Haoyang Liu and Chao Gao. Density estimation with contaminated data: Minimax rates and theory of adaptation. arXiv preprint arXiv:1712.07801v3, 2017.

- [24] Elizbar A Nadaraya. On estimating regression. Theory of Probability & Its Applications, 9(1):141–142, 1964.

- [25] Hongseok Namkoong and John C Duchi. Variance-based regularization with convex objectives. In Advances in Neural Information Processing Systems 30, pages 2971–2980, 2017.

- [26] Viet Anh Nguyen, S. Shafieezadeh-Abadeh, D. Kuhn, and P. Mohajerin Esfahani. Bridging Bayesian and minimax mean square error estimation via Wasserstein distributionally robust optimization. arXiv preprint arxiv:1910.10583, 2019.

- [27] Viet Anh Nguyen, Fan Zhang, Jose Blanchet, Erick Delage, and Yinyu Ye. Distributionally robust local non-parametric conditional estimation. In Advances in Neural Information Processing Systems 33, 2020.

- [28] Viet Anh Nguyen, Fan Zhang, Jose Blanchet, Erick Delage, and Yinyu Ye. Robustifying conditional portfolio decisions via optimal transport. arXiv preprint arXiv:2103.16451, 2021.

- [29] Yung-Kyun Noh, Masashi Sugiyama, Kee-Eung Kim, Frank Park, and Daniel D Lee. Generative local metric learning for kernel regression. In Advances in Neural Information Processing Systems, pages 2452–2462, 2017.

- [30] Pranav Rajpurkar, Robin Jia, and Percy Liang. Know what you don’t know: Unanswerable questions for squad. In Proceedings of the 56th Annual Meeting of the Association for Computational Linguistics, pages 784–789, 2018.

- [31] Carl Edward Rasmussen and Christopher K. I. Williams. Gaussian Processes for Machine Learning (Adaptive Computation and Machine Learning). The MIT Press, 2005.

- [32] Mengye Ren, Wenyuan Zeng, Bin Yang, and Raquel Urtasun. Learning to reweight examples for robust deep learning. In International Conference on Machine Learning, pages 4334–4343. PMLR, 2018.

- [33] Marco Tulio Ribeiro, Sameer Singh, and Carlos Guestrin. “Why should I trust you?" Explaining the predictions of any classifier. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1135–1144, 2016.

- [34] David Ruppert and Matthew P Wand. Multivariate locally weighted least squares regression. The Annals of Statistics, pages 1346–1370, 1994.

- [35] Bernhard Scholkopf and Alexander J Smola. Learning with kernels: support vector machines, regularization, optimization, and beyond. Adaptive Computation and Machine Learning series, 2018.

- [36] Jun Shu, Qi Xie, Lixuan Yi, Qian Zhao, Sanping Zhou, Zongben Xu, and Deyu Meng. Meta-weight-net: Learning an explicit mapping for sample weighting. In Advances in Neural Information Processing Systems, volume 32, pages 1917–1928, 2019.

- [37] Bernard W Silverman. Density Estimation for Statistics and Data Analysis. CRC Press, 1986.

- [38] Bharath K Sriperumbudur, Kenji Fukumizu, and Gert RG Lanckriet. Universality, characteristic kernels and RKHS embedding of measures. Journal of Machine Learning Research, 12(7), 2011.

- [39] Masashi Sugiyama, Shinichi Nakajima, Hisashi Kashima, Paul Von Buenau, and Motoaki Kawanabe. Direct importance estimation with model selection and its application to covariate shift adaptation. In Advances in Neural Information Processing Systems, volume 7, pages 1433–1440, 2007.

- [40] Alexandre B Tsybakov. Introduction to Nonparametric Estimation. Springer, 2008.

- [41] Serena Wang, Wenshuo Guo, Harikrishna Narasimhan, Andrew Cotter, Maya Gupta, and Michael I Jordan. Robust optimization for fairness with noisy protected groups. In Advances in Neural Information Processing Systems, 2020.

- [42] Geoffrey S Watson. Smooth regression analysis. Sankhyā: The Indian Journal of Statistics, Series A, pages 359–372, 1964.

- [43] Yifan Wu, Tianshu Ren, and Lidan Mu. Importance reweighting using adversarial-collaborative training. In NIPS 2016 Workshop, 2016.

- [44] Muhammad Bilal Zafar, Isabel Valera, Manuel Rodriguez, Krishna Gummadi, and Adrian Weller. From parity to preference-based notions of fairness in classification. In Advances in Neural Information Processing Systems, volume 30, pages 229–239, 2017.

- [45] Rich Zemel, Yu Wu, Kevin Swersky, Toni Pitassi, and Cynthia Dwork. Learning fair representations. In Proceedings of the 30th International Conference on Machine Learning, volume 28, pages 325–333, 2013.

- [46] Chongjie Zhang and Julie A Shah. Fairness in multi-agent sequential decision-making. In Advances in Neural Information Processing Systems, volume 27, pages 2636–2644, 2014.

- [47] Jingzhao Zhang, Aditya Menon, Andreas Veit, Srinadh Bhojanapalli, Sanjiv Kumar, and Suvrit Sra. Coping with label shift via distributionally robust optimisation. arXiv preprint arXiv:2010.12230, 2020.

Appendix A Proofs and Additional Discussions

A.1 Proofs of Section 3

In the following, the symbol will be used to represent both Frobenius norm of matrices and standard Euclidean norm of vectors. Also for a matrix , we let to denote its Frobenius norm and let to represent its maximum eigenvalue. In order to prove Proposition 3.4, we begin by computing the support function of the convex cone of symmetric positive definite (SPD) matrices.

Lemma A.1 (Support function of SPD matrices).

For any matrices and , we have , and if in addition and . Also for each ,

Proof of Lemma A.1.

Since is symmetric, we can decompose it as with being a diagonal matrix formed by eigenvalues of and being an orthogonal matrix whose columns are normalized eigenvectors of . Then and hence

where we have used the fact to obtain the inequality. In case and , then as all diagonal elements of are nonpositive with at least one negative element we have . These give the first part of the lemma.

For the second part, let be an eigenvector of corresponding to eigenvalue . In case , by taking with and letting we see that tends to . This implies that . For the case , we instead take with and let to conclude that . On the other hand, due to the first part of the lemma we always have . Therefore, the desired result follows. ∎

For Proposition 3.4

Proof of Proposition 3.4.

The set is bounded. Indeed, if then which is trivially bounded. If , then any satisfies . Since is similar to the matrix , we can rewrite this as

| (14) |

We claim that this implies that is bounded in the sense that there exist numbers depending only on and such that . To see this, let () be the eigenvalues of . Then (14) gives

Because the function is non-negative for every , we then find that is bounded. Therefore, must be bounded between two positive constants depending only on and . Now let be an eigenvalue of and let be its associated eigenvector. Then , and so

where and respectively denote the smallest and largest eigenvalues of . It follows that . Thus all eigenvalues of are bounded between two positive constants, and the claim is proved.

One now can rewrite as

The function is convex and continuous on the set , thus the set is convex and compact.

We now proceed to provide the support function of . One can verify that is the Slater point of the convex set . Assume momentarily that , using a duality argument, we find

| (15) |

where the last equality follows from strong duality [6, Proposition 5.3.1], and . Note that is not an optimal solution to the minimization problem (15). Indeed, if the maximum eigenvalue of is strictly positive, then the objective value of problem (15) evaluated at is by Lemma A.1. However, because is compact and bounded, we have . In case the maximum eigenvalue of is nonpositive, then from Lemma A.1 we see that the objective value of problem (15) evaluated at is , while . Thus, the infimum in problem (15) can be restricted to .

If then the inner supremum problem admits the unique optimal solution

| (16) |

which is obtained by solving the first-order optimality condition. By placing this optimal solution into the objective function and arranging terms together with using the definition of , we have

| (17) |

To complete the proof, we show that the reformulation (17) holds even for or . Notice that if or , then the left-hand side of (17) evaluates to 0. If , the infimum problem on the right-hand side of (17) also attains the optimal value of 0 asymptotically as decreases to 0. If and , then the infimum problem on the right-hand side of (17) also attains the optimal value of 0 asymptotically as increases to by the l’Hopital rule

This observation completes the proof. ∎

For an real matrix , its spectral radius is defined as the largest absolute value of its eigenvalues. The following elementary fact is well known.

Lemma A.2 (Nonnegativity of inverse).

Let be an real matrix such that and all its entries are nonnegative. Then the matrix is invertible and all entries of are nonnegative.

Proof of Lemma A.2.

For completeness, we include a proof here. By Gelfand’s formula, we have

Thus there exist constants and such that for every . Therefore, the Neumann series

converges. This together with the assumption about the nonnegativity of implies that all entries of are nonnegative. ∎

For Theorem 3.2

Proof of Theorem 3.2.

We find

| (18a) | ||||

| (18b) | ||||

| (18c) | ||||

where equality (18a) is the definition of as in (7), inequality (18b) follows from the fact that , and equality (18c) follows from Proposition 3.4. Notice that has one nonnegative eigenvalue by virtue of Lemma 3.5 and thus the constraint implies the condition .

The strictly positive radius condition implies the existence of a Slater point of the set . By [6, Proposition 5.5.4], the existence of a solution that minimizes the dual problem (18c) is guaranteed. Moreover, the objective function of problem (18c) is strictly convex, and thus the solution is unique. By inspecting (16), the solution

Assumption 2.1 implies that both and are nonnegative matrices. Also the spectral radius of is smaller than by the feasibility of in problem (18c). Hence the matrix is nonnegative by Lemma A.2.

As , we conclude that is a matrix with nonnegative entries. Moreover, is also positive semidefinite. Thus is doubly nonnegative. This observation completes the proof. ∎

For Lemma 3.3

For Lemma 3.5

Proof of Lemma 3.5.

The symmetry of follows from definition. The nonnegativity of follows from Assumption 2.1. Let be an eigenvalue of , then solves the characteristic equation . By exploiting the form of and by the determinant formula for the arrowhead matrix, the eigenvalue then solves the algebraic equation . This completes the proof. ∎

A.2 Proofs of Section 4

For Theorem 4.2

Proof of Theorem 4.2.

The statement regarding and the expression of and follows from [26, Proposition A.4]. It remains to show that is nonnegative. Indeed, the constraint implies that the spectral radius of is smaller than . Therefore, the inverse matrix is nonnegative according to Lemma A.2. The matrix is thus the product of three nonnegative matrices and thus it is also nonnegative. ∎

For Lemma 4.3

A.3 Discussions on Assumption 2.1

Assumption 2.1(i) is standard in the machine learning literature and it holds naturally in many classification and regression tasks. Regarding Assumption 2.1(ii), the non-negativity of follows directly if the weighting function is also non-negative. As shown below, positive definiteness holds under mild conditions of the training data and the weighting kernel.

Lemma A.3 (Positive definite nominal weighting matrix).

Suppose that the weighting function can be represented by a strictly positive definite kernel in the sense that for and for some distinct covariates . Then

is positive definite with for .

The proof of Lemma A.3 follows by noticing that is the Gram matrix of a kernel , and hence is a positive definite matrix [38, pp. 2392].

The next result shows that given any weight , there exists a matrix satisfying Assumption 2.1(ii). Notice that it is always possible to choose the numbers satisfying the specified conditions below.

Lemma A.4 (Existence of ).

Given any nonnegative weights for , let be a symmetric matrix with all entries zero except for those on the first row and first column, and on the diagonal as follows

Then is positive definite and nonnegative if are chosen such that , , and for , where denotes the th leading principal minor of the matrix which is independent of .

Proof of Lemma A.4.

It is clear that is symmetric and nonnegative. The conditions on also ensures that for every . Thus is positive definite as well. ∎

For the given non-negative weights , Lemma A.4 shows that there are infinitely many doubly non-negative matrices that satisfy the condition for .

In practice, the choice of can impact the performance of our robust estimate, and fine-tuning the elements of may improve the predictive power. For the scope of this paper, we aim to improve the robustness of NW and LLR estimators and therefore will mainly focus on the scenario described in Lemma A.3 where is given by a strictly positive definite kernel.

Appendix B Implementation Details

B.1 Gradient Information

We provide here the gradient information for the convex problems (8) and (12). This information can be exploited to derive fast numerical routines to find the optimal dual solution .

Denote by the objective function of problem (8). The gradient of is

Let be the objective function of problem (12). The gradient of is

B.2 Implementation

Following Lemma 3.5, for a fixed value of , we can rewrite the low-rank matrix using the eigenvalue decomposition , where is a diagonal matrix and is an orthonormal matrix. Therefore, we can leverage the Woodbury matrix identity to implement the inverse in gradient computation (e.g., and ) efficiently. For examples, (i)

where we have exploited the fact that with being the identity matrix; and (ii)

Therefore, the inverse in gradient (e.g., and ) is computed on matrices.

Appendix C Additional Empirical Results

Details of datasets.

Table 1 lists the detailed statistical characteristics of the datasets used in our experiments.

| Abalone | Bank | CPU | Elevators | KIN | POL | Puma | Slice | |

|---|---|---|---|---|---|---|---|---|

| #samples | 4177 | 8192 | 8192 | 16599 | 40000 | 15000 | 8192 | 53500 |

| #features | 7 | 32 | 21 | 17 | 8 | 26 | 32 | 384 |

Further results for the ideal case: no sample perturbation.

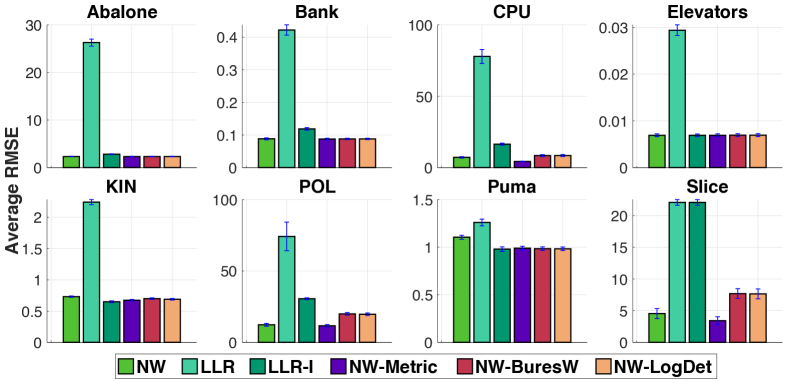

We illustrate further empirical results for all datasets and with different nearest neighbor size (e.g., similar to Figure 1 with the nearest neighbor size ).

Further results for the cases when training samples are perturbed.

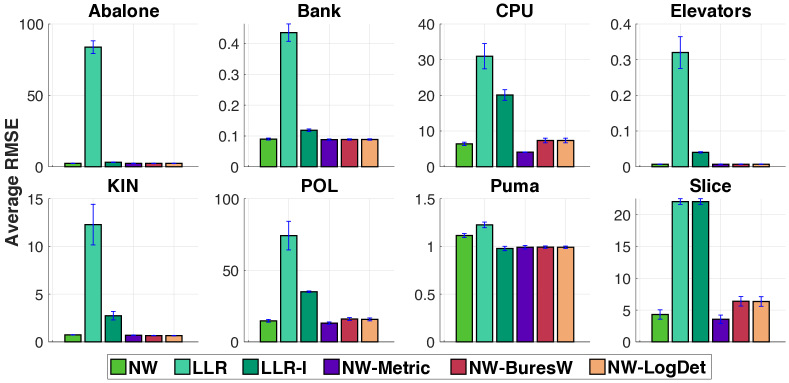

We illustrate further empirical results for all datasets with different nearest neighbor size (e.g., similar to Figure 2 where the nearest neighborr size ).

Further results for the effects of the uncertainty size .

We illustrate further empirical results for different nearest neighbor size in all 8 datasets (e.g., similar to Figure 3 where the nearest neighbor size and the perturbation ). Note that when , the reweighting schemes are equivalent to the vanilla NW estimator.

- •

- •

- •

- •

Further results for the effects of the nearest neighbor size .

We illustrate further empirical results for different uncertainty size in all 8 datasets (e.g., similar to Figure 4 where in the KIN dataset).

- •

- •

- •

- •

Further results for varying shifting w.r.t. .

We first illustrate corresponding results for NW-BuresW in Figure 31, similar as results in Figure 5 for NW-LogDet.

We next illustrate further empirical results for different uncertainty size and different perturbation in the KIN dataset (e.g., similar to Figure 5 and Figure 31 where for the left plots and for the right plots).

- •

- •

Further results for effects of on computational time.

We illustrate further effects of on computational time in all 8 datasets (e.g., similar to Figure 6 for the KIN dataset).