Multiple Change Point Detection in Reduced Rank High Dimensional Vector Autoregressive Models

Abstract

We study the problem of detecting and locating change points in high-dimensional Vector Autoregressive (VAR) models, whose transition matrices exhibit low rank plus sparse structure. We first address the problem of detecting a single change point using an exhaustive search algorithm and establish a finite sample error bound for its accuracy. Next, we extend the results to the case of multiple change points that can grow as a function of the sample size. Their detection is based on a two-step algorithm, wherein the first step, an exhaustive search for a candidate change point is employed for overlapping windows, and subsequently a backwards elimination procedure is used to screen out redundant candidates. The two-step strategy yields consistent estimates of the number and the locations of the change points. To reduce computation cost, we also investigate conditions under which a surrogate VAR model with a weakly sparse transition matrix can accurately estimate the change points and their locations for data generated by the original model. This work also addresses and resolves a number of novel technical challenges posed by the nature of the VAR models under consideration. The effectiveness of the proposed algorithms and methodology is illustrated on both synthetic and two real data sets.

Keywords: Algorithms; Consistency; Time Series Data and their Applications.

1 Introduction

High dimensional time series analysis and their applications have become increasingly important in diverse domains, including macroeconomics (Kilian & Lütkepohl (2017), Stock & Watson (2016)), financial economics (Billio et al. (2012), Lin & Michailidis (2017)), molecular biology (Michailidis & d’Alché Buc (2013)) and neuroscience (Friston et al. (2014), Schröder & Ombao (2019)). Such data are usually both cross-correlated and auto-correlated. There are two broad modeling paradigms for capturing these features in the data: (i) dynamic factor and latent models (Bai & Ng (2008), Stock & Watson (2002, 2016), Lam et al. (2011), Li et al. (2014)), and (ii) vector autoregressive (VAR) models (Lütkepohl (2013), Kilian & Lütkepohl (2017)). The basic premise of models in (i) is that the common dynamics of a large number of time series are driven by a relatively small number of latent factors, the latter evolving over time. VAR models aim to capture the self and cross auto-correlation structure in the time series, but the number of parameters to be estimated grows quadratically in the number of time series under consideration. Various structural assumptions have been proposed in the literature to accommodate a large number of time series in the model, with that of sparsity (Basu & Michailidis (2015)) being a very popular one. However, in many applications the autoregressive dynamics of the time series exhibit also low dimensional structure, which gave rise to the introduction of reduced rank auto-regressive models (Box & Tiao (1977), Velu et al. (1986), Ahn & Reinsel (1988), Wang & Bessler (2004)). For example, brain activity data (see Example 1 in Section 6) exhibit low dimensional structure (Schröder & Ombao (2019)) and so do macroeconomic data (Stock & Watson (2016), Example 2 in Section 6). Reduced rank auto-regressive models for stationary high-dimensional data were studied in Basu et al. (2019). The key idea of such reduced rank models is that the lead-lagged relationships between the time series can not simply be described by a few sparse components, as is the case for sparse VAR models. Instead, all the time series influence these relationships and some of them are particularly pronounced (those in the sparse component). Applications in economics/finance, neuroimaging, and environmental science are important candidates for these models.

In many application areas including those mentioned above, nonstationary time series data are commonly observed. The simplest, but realistic departure from stationarity, that also leads to interpretable models for the underlying time series, is piecewise-stationarity. Under this assumption, the time series data are modeled as approximately stationary between neighbouring change-points, whereas their distribution changes at these change points. The literature on change point analysis for the two classes of modeling paradigms previously mentioned is rather sparse. Bardsley et al. (2017) developed tests for the presence of change points in functional factor models motivated by modeling the yield curve of interest rates, while Barigozzi et al. (2018) employed the binary segmentation procedure for detecting and identifying the locations of multiple change points in factor models. Change point detection for sparse VAR models has been investigated in Wang et al. (2019), Safikhani & Shojaie (2020), and Bai et al. (2020).

The objective of this study is to investigate the problem of change point detection in a reduced rank VAR model, whose transition matrices exhibit low-rank and sparse structure. The problem poses a number of technical challenges that we address in the sequel.

Formally, a piece-wise stationary VAR model of lag-1 (for introducing the basic issues related to it) for a -dimensional time series with change points is given by:

where is a coefficient matrix for the -th segment, , presents the indicator function of the -th interval, and s are independent zero mean Gaussian noise processes. It is assumed that that the coefficient matrix can be decomposed into a low-rank component plus a sparse component: namely, , where is a low-rank matrix with rank (), and is a sparse matrix with () non-zero entries.

The modeling framework differs vis-a-vis the one considered in Bai et al. (2020), since in the current work, both the low rank and the sparse components of the transition matrices are allowed to exhibit changes at break points. This flexibility rules out the use of a fused lasso based detection algorithm that is suitable for the case wherein only the sparse component is allowed to exhibit changes, which was the setting in Bai et al. (2020). As a result, a novel rolling window detection algorithm is introduced and its theoretical properties studied in the current work.

Next, we outline novel technical challenges, not present in change point analysis of sparse VAR (Safikhani & Shojaie (2020), Wang et al. (2019)) and other sparse high dimensional models (Roy et al. (2017)):

(i) The change in the transition matrix may be due to a change in the low-rank component, in the sparse component or in both. To that end, we introduce a novel sufficient identifiability condition for both detecting a single change point and decomposing the transition matrix into its low rank plus sparse components (Assumptions H1 and H2 in the sequel); then, it is extended to the case of multiple change points (Assumptions H1’ and H2’).

(ii) For the case of multiple change points, commonly used procedures, such as binary segmentation (Cho & Fryzlewicz (2015)) or fused type penalties (Safikhani & Shojaie (2020)) are not directly applicable due to the presence of the low rank component. Specifically, the former method would lead to effectively performing singular value decompositions on misspecified models involving mixtures of piece-wise low-rank and sparse models, which may lead to the imposition of very stringent conditions for ensuring detectability of the change points (see discussion on related issues in Bhattacharjee et al. (2020)). Further, it is unclear how to design fused penalties that accommodate low-rank matrices. On the other hand, dynamic programming based algorithms are applicable. However, their time complexity is , where indicates the computational cost of estimating the model parameters over the entire observation sequence. This is significantly higher complexity than the previously mentioned methods (which is , see numerical comparisons and discussion in Remark 6 and Appendix F.7).

To overcome these challenges, we develop a novel procedure based on rolling windows, wherein a single candidate change point is identified in each window and then only those exhibiting screened based on certain properties (see Section 3) are retained. This allows to leverage the theoretical results developed for the single change point. The proposed procedure based on rolling windows is naturally parallelizable, thus speeding up computations.

Note that the developed rolling window strategy is applicable to any complex statistical model exhibiting multiple change points. One needs to establish consistency properties for a single change point in a time interval and then appropriately select the length of the rolling window, to ensure that at most a single change point falls within. Hence, this development is of general interest for change point analysis.

(iii) Note that the procedure of estimating change points in low-rank plus sparse VAR models is computationally expensive, even in the presence of a single change point, since it requires performing numerous singular value decompositions. We consider a surrogate model that comes with significant computational savings and under certain regularity conditions exhibits similar accuracy to the posited model. Specifically, we posit a lag-1 VAR model, wherein the transition matrices are assumed to be weakly sparse (see, e.g., Negahban et al. (2012)), as an alternative modeling framework. The main reason is that the presence of low rank structure renders the auto-regressive parameters in the original model dense. The weak sparse assumption adequately accommodates dense structures under certain conditions and hence can prove useful in certain settings (carefully discussed in the sequel) for change point detection problems. Further, the theoretical properties of exhaustive-search based anomaly detection for weakly sparse VAR models have not been investigated in the literature, and hence this development is of independent interest.

(iv) To establish non-asymptotic error bounds on the model parameters of stationary sparse models, one needs to verify that the commonly imposed (see, e.g. Loh & Wainwright (2012)) restricted strong convexity and deviation bound conditions hold (see Propositions 4.2 and 4.3 in Basu & Michailidis (2015)).

Verifying these assumptions in the presence of change points in the posited reduced rank VAR model -which technically is equivalent to working with a misspecified model (see also discussion in Roy et al. (2017))- represents a non-trivial challenge. This issue is rigorously and successfully addressed in the sequel, together with the introduction of a new version of the deviation bound condition that allows working with misspecified models (technical details presented in Appendix A).

(v) Finally, obtaining consistent model parameters for each segment identified after detecting the change points requires some care, given the non-stationary nature of the posited model above. This is successfully addressed for the case of a single and multiple change points in Sections 2 and 3, respectively, and for the surrogate model in Section 4.

The remainder of the paper is organized as follows. In Section 2, we formulate the model with a single change point, provide a detection procedure based on exhaustive search, and establish theoretical properties for the change point and model parameter estimates. Section 3 discusses the case of multiple change points. It introduces a two-step detection algorithm and establishes consistency of the obtained estimates for the change points and model parameters, leveraging results from Section 2. To reduce computations for detecting the change point(s) in the reduced rank VAR model, we introduce a weakly sparse surrogate model in Section 4 and establish that under certain regularity conditions on the structure of the transitions matrices of the reduced rank model, the estimated change points from the surrogate model are consistent ones for data generated by the former. Section 5 presents a number of numerical experiments to illustrate and assess the performance of the estimates obtained from the single and multiple change points detection procedures. Two real data sets (one on EEG and the other on macroeconomics data) are analyzed using the proposed detection procedures in Section 6. Some concluding remarks are drawn in Section 7. Additional technical conditions, proofs of the main results and additional numerical work are available in the Supplement.

Notation: Throughout this paper, we denote with a superscript “” the true value of the model parameters. For any matrix, we use , , and to represent the spectral, Frobenius, and nuclear norm, respectively. For any matrix , denotes its transpose, and denotes the conjugate transpose of , while the , , and norms of the vectorized form of are denoted by: , , and , respectively. We use and to represent the maximum and minimum eigenvalue of the realization matrix .

2 Single Change Point Model Formulation and Detection Procedure

We start by introducing a piece-wise stationary structured VAR(1) model that has a single change point. Suppose there is a -dimensional time series observed at points: . Further, there exists a change point, , so that the available time series can be modeled according to the following two models in the time intervals and , respectively:

| (1) | ||||

where is a vector of observed time series at time , and and are the transition matrices for the corresponding models in the two time intervals, and the dimensional error processes and are independent and identically drawn from Gaussian distributions with mean zero and covariance matrix for some fixed . It is further assumed that the transition matrices comprise of two time-varying components, a low-rank and a sparse one:

| (2) |

The rank of the low-rank components and the density (number of non-zero elements) of the sparse components are denoted by , , and , respectively, and satisfy , .

2.1 Detection Procedure

Let be a sequence of observations generated from the VAR model posited in (1) with the structure of the transition matrices given by (2). Then, for any time point the corresponding objective functions for estimating the model parameters in the intervals and are given by:

where denotes the data from time points to , and the non-negative tuning parameters , , , and control the regularization of the sparse and the low-rank components in the corresponding transition matrices.

Next, we introduce the objective function with respect to the change point: for any time point ,

| (3) |

The estimator of the change point is given by:

| (4) |

for the search domain , where, for each , the estimators , , , are derived from the optimization program (4) with tuning parameters , , , and , respectively. Algorithm 1 in Appendix B describes in detail the key steps in estimating the change point together with the model parameters.

2.2 Theoretical Properties

Next, we address the issue of identifiability of model parameters due to the posited decomposition of the transition matrices into low rank and sparse components. The key idea is to restrict the “spikiness” of the low rank component, so that it can be distinguished from the sparse component. Agarwal et al. (2012) introduced the space defined as

wherein the universal parameter defines the radius of nonidentifiability that controls the degree of separating the sparse component from the low-rank one. Note that a larger allows the low-rank component to absorb most of the signal, thus making it harder to identify the sparse component, and vice versa.

Thus, the estimators of the decomposition of the transition matrices are defined as follows, for any fixed time point :

| (5) |

Next, we introduce an important quantity for future developments, the information ratio that measures the relative strength of the maximum signal in the transition matrix generated by the low-rank component vis-a-vis its sparse counterpart, defined as:

Remark 1.

Based on the definition of the information ratio, some algebra provides guidance on the identifiability conditions that need to be imposed on the transition matrices and their constituent parts. Specifically, for the low rank component we obtain:

Analogous derivations for the sparse component yield: , where , are norm differences for the low-rank and the sparse components, respectively.

Based on Remark 1, it can be seen that: (1) when or , we have that (since in a high dimensional setting). The latter fact implies that in order for changes in the transition matrices to be identifiable -and consequently - the difference in the norm of the low-rank components must significantly exceed that of the sparse components; (2) when both and , then the quantity is strictly decreasing with respect to and . Note that in case and , . Combining these two cases leads to the conclusion that when and , the difference in the norm between the low-rank components must be larger than , the norm difference between the sparse components to guarantee that the change between the transition matrices is detectable.

The following remark discusses an extreme case, wherein the signal in the low-rank components is dominant, but their norm difference is negligible.

Remark 2.

Suppose the low-rank components are dominant (i.e. ), but their norm difference change is small; i.e. , with being a small enough constant). Then, we have:

Note that since the low rank components are constrained to be in the space -- it implies that the transition matrices are identifiable, only if and . The roles of and can be swapped to obtain that only if and , is the change in the full transition matrices identifiable, which is intuitive.

The derivations in the two Remarks provide insights into the necessary assumptions needed to establish the theoretical results, presented next.

-

(H1)

There exists a positive constant such that

where is the spacing between the change point and the boundary, and , are the jump sizes, defined as

Further, at least one of is strictly positive.

-

(H2)

(Identifiability conditions) Consider low rank matrices , , and their corresponding Singular Value Decompositions: , where , for and are orthonormal. Then,

-

(1)

there exists a universal positive constant , such that for the sparse matrices , we have: , ;

-

(2)

there exists a large enough constant , such that the diagonal matrices satisfy: ; further the orthonormal matrices and satisfy: , where . In addition, we assume that .

-

(3)

the maximal sparsity level satisfies: for a large enough positive constant .

-

(1)

-

(H3)

(Restrictions on the search domain ) The change point belongs to the search domain by and denote the search domain . Assume that, and denote as the length of the search domain, then:

where is an arbitrarily small positive constant, , and .

Remark 3.

Assumption H1 specifies the relationship between the minimum spacing between the change point and the boundaries of the observation time period and the jump sizes for the low rank and sparse components, analogously to the signal-to-noise assumption in Wang et al. (2019). Assumptions H2-(1) and H2-(2) define the restricted space for the low rank components : ; see analogous definitions and discussion in Agarwal et al. (2012), Basu et al. (2019), Bai et al. (2020) for identifying low rank and sparse matrices. Assumptions H2-(1-3) are sufficient for satisfying the identifiability condition in Hsu et al. (2011), the latter implying that the decomposition is unique. This condition is motivated by the so-called “rank-sparsity” incoherence concept (Chandrasekaran et al. 2011), with further refinements along the lines of results in Hsu et al. (2011). This assumption ensures identifiability of model parameters by putting certain conditions on the singular values, and left/right orthonormal singular vectors of the low rank component. Specifically, the new assumption controls the maximum number of non-zeros in any row or column of the sparse component, while ensuring that the low rank part has singular vectors far from the coordinate bases. Note that the new conditions do not put any additional constrains on the dimensionality and further ensure the uniqueness of the low rank plus sparse decomposition of the segment specific transition matrices.

Note that Agarwal et al. (2012) allow to be any constant, whereas we require to be vanishing to obtain consistent estimates, due to the presence of misspecification, since the location of the change points is unknown. Assumption H3 reflects the restrictions on the boundary of the search domain and connects the estimation rate to the length of the search domain (see analogous condition in Roy et al. (2017)).

For any fixed time point in the search domain , let be the tuning parameters on , and the tuning parameters on , respectively. Then, the tuning parameters of the regularization terms are selected as follows:

| (6) | ||||

for constants .

Theorem 1.

Suppose Assumptions H1-H3 hold, and select the tuning parameters according to (6). Then, as , there exists a large enough constant such that

The proof of Theorem 1 is provided in Appendix E. Note that the Theorem provides an upper bound for the change point estimation error based on the total sparsity level and the total rank of the model.

Next, we establish estimation consistency for the model parameters. First, given the estimated change point , we remove it together with its -radius neighborhoods , to ensure that the remaining time points form two stationary segments. According to Theorem 1, the radius can be of the order .

Let be the length of the -th segments after removing the -radius neighborhoods; then, we select another pair of tuning parameters:

| (7) |

for constants , that can selected using cross-validation. The procedure for selecting them, as well as in (6), is provided in Section 5.

Note that the tuning parameters provided in (7) are different from the tuning parameters in (6); the terms are eliminated, since on the selected stationary segments the optimal tuning parameters are always feasible. Based on analogous results in Agarwal et al. (2012) and Basu et al. (2019) for models whose parameters admit a low rank and sparse decomposition, the optimal tuning parameters in (7) lead to the optimal estimation rate given in the next Theorem.

Theorem 2.

The proof of Theorem 2 is provided in Appendix E.

Remark 4.

Notice that Theorem 2 provides the joint estimation rate for the low-rank and the sparse component. It comprises of two terms, wherein the first one involves the dimensions of the model parameters and converges to zero as the sample size increases, whereas the second term represents the error due to possible unidentifiability of the model parameters. However, in conjunction with Assumption H2 that restricts the space for the low rank component, the second term also converges to zero as the sample size (and hence the dimensionality of the model) increases.

3 The Case of Multiple Change Points

Section 2.2 introduced the technical framework and established the consistency rate for detecting a single change point. Next, these technical developments are leveraged to address the more relevant in practice problem of detecting multiple change points consistently.

We start by formulating the piece-wise VAR model with multiple change points. Consider the -dimensional VAR(1) process with change points ; then, the model under consideration is written as:

| (8) |

where and represent the decomposition of the -th transition matrix into its low-rank and sparse components, and denotes the indicator function for the -th stationary segment. Analogously to the single change point case, we define the sparsity level and rank for the components in each segment, wherein and , (i.e., and ). Finally, ’s are independent and independently distributed zero mean Gaussian noise processes with covariance matrices , .

For detecting the change points and estimating the model parameters consistently, the following minor modifications to Assumptions H1-H3 are required:

-

(H1’)

There exists a positive constant such that

where is the minimum spacing defined as , and the minimum norm differences (jump sizes) between two consecutive segments are defined as: , and .

-

(H2’)

Consider low rank matrices , and their corresponding Singular Value Decompositions: , where , for . Then,

-

(1)

there exists a universal positive constant , such that for the sparse matrices , we have: , ;

-

(2)

there exists a large enough constant , such that the diagonal matrices satisfy: , and the orthonormal matrices and such that: , where . In addition, we assume that .

-

(3)

the maximal sparsity level satisfies: for a large enough positive constant .

-

(1)

-

(H3’)

There exists a vanishing positive sequence such that, as ,

for a positive constant .

Assumptions H1’ and H2’ are direct extensions of Assumptions H1 and H2 to the multiple change points setting. Assumption H3’ provides a minimum distance requirement on the consecutive change points and connects the estimation rate and the minimum spacing between change points.

Our detection algorithm will leverage results from the single change point case, and thus, we introduce additional assumptions next. As mentioned in the introduction, the use of fused type penalties is not applicable to the low-rank component and hence an entire different detection procedure is required.

3.1 A Two-step Algorithm for Detecting Multiple Change Points and its Asymptotic Properties

-

•

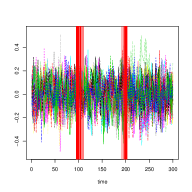

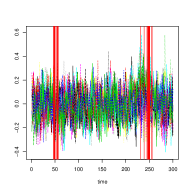

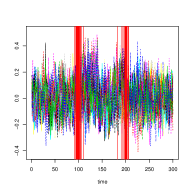

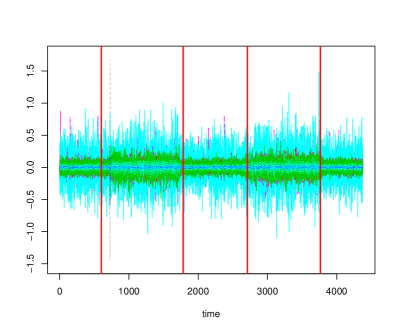

Step 1: It is based on Algorithm 1 provided in Appendix B that detects a single change point, additionally equipped with a rolling window mechanism to select candidate change points. We start by selecting an interval , of length and employ on it the exhaustive search Algorithm 1 to obtain a candidate change point . Next, we shift the interval to the right by time points and obtain a new interval , wherein and . The application of Algorithm 1 to yields another candidate change point . This procedure continues until the last interval that can be formed, namely , where and denotes the number of windows of size that can be formed. The following Figure 1 depicts this rolling-window mechanism. The blue lines represent the boundaries of each window, awhile the green dashed lines represent the candidate change point in each window. Note that the basic assumption for Algorithm 1 is that there exists a single change point in the given time series. However, it can easily be seen in Figure 1 that not every window includes a single change point.

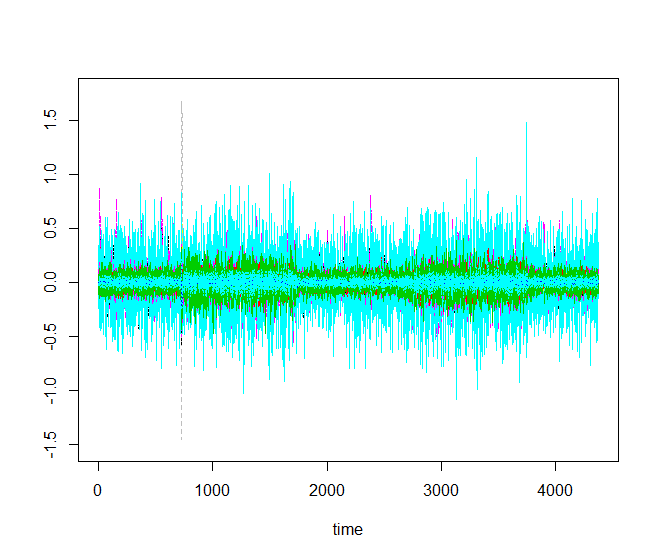

Figure 1: Depiction of the rolling windows strategy. There are three true change points: , , and (red dots); the boundaries of the rolling-window are represented in blue lines; the estimated change points in each window are plotted in green dashed lines, where the subscript indicates the index of the window used to obtain it. To showcase the last point, we compare the behavior of Algorithm 1 on an interval with and without a change point based on data generated from a low-rank plus sparse VAR process with . We select two windows of length , one containing a change point at and another not containing a change point. Plots of the objective function (3) used in Algorithm 1 for these two windows are depicted in the left and right panels of Figure 2, respectively.

Figure 2: Plots of the objective functions obtained by an application of Algorithm 1, in the presence (left panel) and absence (right panel) of a true change point. It can be seen that in the presence of a change point, a clearly identified minimum close to the true change point exists. Contrary, in the absence of a change point, the objective function is mostly flat without a clearly identified minimum. Next, we introduce an assumption on the size of the window used in the detection procedure:

-

(H4)

Let denote the length of the window in the rolling window algorithm. Further, the minimum spacing and the vanishing sequence are defined as in Assumption H3’, and let denote the length by which the window is shifted to the right; it is assumed that:

Assumption H4 restricts , so that asymptotically can not include more than a single true change point and also is not too small, so that the deviation bound and restricted eigenvalue conditions used for establishing theoretical properties of the estimates of the model parameters hold for each time segment (see Appendix A). Further, this assumption places an upper bound on the shift , to ensure that no true break point close to the boundary of windows would be missed by the proposed algorithm. The shift size can vary in ; a small helps reduce the finite sample estimation error for locating the break points, while a large speeds up the detection procedure, by considering fewer rolling windows.

Next, we establish theoretical guarantees for Step 1 of the proposed detection procedure. Denote by the set of candidate change points and by the set of true change points. Specifically, is defined as:

where is the -th rolling-window. Following Chan et al. (2014), we define the Hausdorff distance between two countable sets on the real line as:

Next, we extend Theorem 1 to the multiple change points scenario:

Proposition 1.

Suppose Assumptions H1’-H3’ and H4 hold, and select the tuning parameters for each rolling window according to (6). Then, as , there exists a large enough constant such that

Proposition 1 shows that the number of candidate change points identified in Step 1 of the algorithm is an overestimate of the true number of change points. Hence, a second screening step is required to remove the redundant ones.

-

(H4)

-

•

Step 2: Let the candidate change points from Step 1 be denoted by , . Then, model (8) can be rewritten in the following form:

where and denote for the low-rank and sparse components of the transition matrix in the interval . We define and for ease of presentation use and instead of and for . We also define matrices and . Estimates for and are obtained as the solution to the following regularized regression problem:

with tuning parameters . Next, we define the objective function with respect to :

(9) Then, for a suitably selected penalty sequence , specified in the upcoming Assumption H5, we consider the following information criterion defined as:

(10) The second step selects a subset of initial change points from the first step by solving:

Algorithm 2 in Appendix B describes in detail the key steps for screening the candidate change points by minimizing the information criterion.

The following two additional assumptions on the minimum spacing and the selection of tuning parameters are required to establish the main theoretical results.

-

(H5)

Assume that and as .

-

(H6)

Suppose are a set of change points obtained from the Step 1, we consider the following scenarios: (a) if , select and , for ; (b) if there exist two true change points and such that and , select and ; (c) otherwise, select and , for some large constant .

Assumption H5 connects the screening penalty term , defined with the information criterion (10), and the minimum spacing allowed between the change points. Assumption H6 provides the specific rate of the tuning parameters used in the regularized optimization problem formulated in (9). Note that Assumption H6 is required even in standard lasso regression problems for independent and identically distributed data and in the absence of change points (Zhang & Huang 2008). In the literature on change points analysis with misspecified models, a more complex selection of the tuning parameters is needed (Chan et al. 2014, Roy et al. 2017). Then, the following Theorem establishes the main result of estimating consistently the number of change points and their locations.

Theorem 3.

Suppose Assumptions H1’–H3’, and H4–H6 hold. As , the minimizer of (10) satisfies: . Further, there exists a large enough positive constant so that

Remark 5.

For a finite number of change points , the sequence can be selected as for some small . Assuming that the maximum rank among all the low-rank components and the maximum sparsity level among all the sparse components satisfy , then the order of detecting the relative location -- becomes in Theorem 3. Finally, one can choose the penalty tuning parameter to be of order in this setting, and the minimum spacing to be at least of order in accordance to Assumption H3’. Comparing the consistency rates provided in Theorem 3 with those in Safikhani & Shojaie (2020), the additional term reflects the complexity of estimating the low-rank components in the model.

Remark 6.

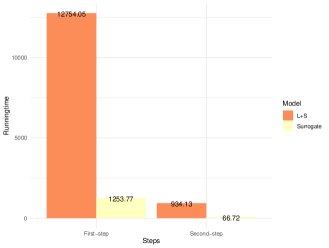

Computational cost of the rolling windows strategy. For the proposed -dimensional VAR model with observations and window size , where , the computational complexity of the first step is of order , and the second screening step is of order , where is the computational cost for model parameters estimation for every search. Hence, the overall complexity is .

The following corollary provides the error bound for consistent estimation of the low-rank and the sparse components, which is directly extended from Theorem 2 to the multiple change points scenario. To obtain the stationary time series for each segments, we employ the exact same technique of removing -radius neighborhoods for every estimated change point. In accordance to Theorem 3, the radius should be at least of order for some large constant . Denote the length of the -th stationary segment by , after removing the -radius neighborhoods for each estimated change point.

Corollary 1.

Given the estimated change points: , let Assumptions H1’-H3’ and H4 hold and remove the -radius neighborhoods for each for . Further, by using the following tuning parameters: , where are positive constants. For , there exist universal positive constants such that for each selected segment, the estimated low-rank and the sparse components satisfy

-

•

Step 3 (Optional): After the second Step, the results in Theorem 3 and Corollary 1 ensure accurate estimation of the number of change points and their locations, as well as of the underlying model parameters across the stationary segments. However, a further refinement and hence a tighter bound on the result provided in Theorem 3 can be obtained through the following re-estimation procedure (see also discussion on this point in Wang et al. (2019)). Specifically, the conclusions in Theorem 3 ensure that almost surely and also provide good estimates of the boundaries of the stationary segments. Then, for an estimated change point , consider a “refined” interval for , where . Then, we define the objective function:

and a “refined” change point together with the refitted model parameters corresponds to:

(11)

According to the proposed refinement, we derive the following corollary:

Corollary 2.

Suppose Assumptions H1’–H3’, and H4–H6 hold. As , the minimizer of (11) satisfies:

Remark 7.

Note that in the bound of Corollary 2, the maximum density across all sparse components appears as a linear term, instead of a quadratic one in Theorem 3. This refinement is primarily of theoretical interest, since as the numerical work in Section 5.2 indicates the detection procedure based on Steps 1 and 2 achieves very accurate estimates of the change points and the model parameters.

Remark 8.

Corollary 2 indicates that the high probability finite sample bound on the estimation error depends on the maximum sparsity level among the sparse components, the maximum rank among the low rank components, the dimension , and the signal strength , of the sparse and low rank components. Note that the issue of obtaining asymptotic distributions for the estimated change points is a rather complicated task and has not been addressed in the literature even for much simpler models, including sparse mean shift models.

4 A Fast Procedure Based on a Surrogate Model

Remark 6 shows that identifying multiple change points in a low-rank and sparse VAR model is computationally expensive, due to the presence of the nuclear norm and the need for selecting the tuning parameters through a 2-dimensional grid search.

The question addressed next is whether there are settings wherein the nature of the signal in the norm difference is such that it can be adequately captured by a less computationally demanding surrogate model. For example, if the norm difference is primarily due to a large enough change in the sparse component, it is reasonable to expect that a surrogate VAR model with a sparse transition matrix may prove adequate under certain regularity conditions. However, if the norm difference is due to a change in the low-rank component, which by construction is dense, a pure sparse VAR model will not be adequate; however, a weakly sparse model may be sufficient. Indeed, some numerical evidence suggests that this is the case. Figure 3 presents plots of the objective functions of the original and the surrogate weakly sparse model under the same experimental setting for a low-rank plus sparse VAR process with , , and a single change point at with changes in both the low-rank and sparse components.

As can be seen, the plot for the surrogate weakly sparse model shares a similar pattern to that of the true model. However, in practice, we can not a priori guarantee a change both in the low-rank and the sparse component, simultaneously. Therefore, an extra assumption is required to ensure the detectability of the change points. Before we state it, we first introduce formally the surrogate piece-wise weakly sparse VAR model.

4.1 Formulation of the Surrogate Weakly Sparse VAR Model

A real matrix is weakly sparse, if it satisfies

| (12) |

for some ; namely, its entries are restricted in an ball of radius (Negahban et al. 2012). Note that when , this set converges to an exact sparse model, that is, , if and only if has at most nonzero elements. When , the set enforces a certain rate of decay on the ordered absolute values of .

We focus the discussion on detecting a single change point and establish under what conditions the change point can be estimated consistently based on the weakly sparse surrogate model. Subsequently, we extend the result to the case of multiple change points using the proposed rolling window strategy.

Since the focus is on the weakly sparse VAR model, the detection procedure provided in Section 2 requires some modification, whose details are given in Appendix C.

We assume that , for some and . We also introduce a modification on the Assumptions made in Sections 2 and 2.2. Based on Remark 1 and using the same notation as in the results in Sections 2.2 and 3, the counterpart of Assumption H1 becomes:

-

(W1)

The weakly sparse assumption on the ’s singles out spiky entries. Hence, one of the following needs to hold:

-

(1)

If , then we require the minimum spacing and the jump size satisfy:

-

(2)

Otherwise, the change point is identifiable as long as:

-

(1)

Remark 9.

Assumption W1 is based on Remark 1. Note that if the low-rank components dominate the signal, then an adequate change in them is required to identify the change point; otherwise, we need different information ratios together with distinct spiky entries in the sparse components. The latter sufficient condition indicates that the changes in the spiky entries play an important role in identifying the change points. For the second case, if the low-rank components are not dominant in both segments, then an adequately large change in the sparse components is sufficient to determine the change point.

4.2 Theoretical Properties

The following proposition provides a lower bound for the radius , so that the true transition matrices that admit a low-rank plus sparse decomposition do belong to the above defined ball. We only discuss the case . Analogous results for the other cases can be derived in a similar manner.

Proposition 2.

Let be fixed and be the radius of defined in (12). Further, the transition matrices for the data generating model satisfy the following decomposition: and , where , , , and are the corresponding low-rank and sparse components. Then, belong to if satisfies:

where and .

Before we extend Theorem 1 to the surrogate weakly sparse model, a modification to the selection of tuning parameters is required. Recall that (6) identifies the tuning parameters for the low-rank plus sparse model, while for the surrogate weakly sparse model, the only parameter is the transition matrix for . Along with the notation defined in (6), the tuning parameters are given by:

| (13) |

where are some positive constants selected by the similar method as and in (6), the selection procedure is provided in the next section. Since we employ the same exhaustive search algorithm in Algorithm 1, a similar assumption as H3 on the search domain is required.

-

(W2)

Using similar definitions to Assumption H3, denote the search domain by , and let to be the length of . Then, we assume that,

We are now in a position to extend the result in Theorem 1 in the following proposition, whose proof is provided in Appendix E.

Proposition 3.

Suppose Assumptions W1 and W2 hold and the transition matrices and in (1) belong to the set for some fixed constant and radius , such that for some constant . Then, by employing Algorithm 1 and using the tuning parameters as in (13), there exists a large enough constant such that, with respect to the jump size , as

The following Proposition extends the above result to the case of multiple change points based on the rolling window strategy previously described. The window size can be selected by substituting the vanishing sequence in Assumption H4 by the vanishing sequence defined in Assumption W3 below, for the weakly sparse model.

Proposition 4.

Suppose Assumptions W1 and W2 hold and the transition matrices , belong to the set for some fixed constant and the -ball radius satisfies that . Then, by employing the rolling window strategy, we obtain the candidate change points set . Then, as , there exists a large enough constant such that,

where .

Recall that the rolling-window mechanism will result in a number of redundant candidate change points. By using the surrogate weakly sparse model, we obtain a few redundant candidate change points as well. Therefore, we need to remove those redundant change points by using a similar screening step as introduced in the two-step algorithm in Section 3.1. Similarly, we also extend Assumptions H3’, H5 and H6 to the weakly sparse scenario -Assumptions W3 and W4 given in Appendix C- in order to formally introduce the theoretical results for the surrogate model. Employing the selected tuning parameters as detailed in Assumptions W3 and W4, we can establish consistent estimation of the change points.

Proposition 5.

Suppose Assumptions W1–W4 hold and denote the minimizer of (7) in Appendix C by . Then, as , there exists a large enough positive constant such that

Remark 10.

Proposition 5 provides the consistency rate of the final estimated change points obtained by the surrogate weakly sparse model. In the case of being finite, we select the vanishing sequence to be of order for some arbitrarily small constant . Therefore, the consistency rate in Proposition 5 becomes . According to Assumption W3, the penalty term can be selected to be of the order and the minimum spacing in the weakly sparse model must be at least .

5 Performance Evaluation

We start by investigating the performance of the exhaustive search algorithm for a single change point detection for the low-rank plus sparse VAR model and its surrogate counterpart and the two-step algorithm for detecting multiple change points for these models.

-

•

Data generation: (1) We generate the time series data with a single change point at from model (1). We set the true ranks , , and the information ratio for most of the cases considered, unless otherwise specified. The low-rank components and are designed by randomly generating an orthonormal matrix and singular values to obtain , and , where represents the -th column of matrix U. Then, the sparse components share the same 1-off diagonal structure with values and , respectively. The error term is normally distributed from . (2) In the multiple change points case, we create the time series data from model (8) with change points, the true ranks are randomly chosen from: unless otherwise specified, and the information ratios are fixed to . The low-rank components are designed in a similar way as the single change point case, and the -th sparse components are generated by .

-

•

Tuning parameter selection: To select the tuning parameters related to optimization problem (3), we can use the theoretical values of and provided in (6) and (7), and select the constants and by using a grid search as follows:

-

(1)

Choose an equally spaced sequence within as the range for constants and to construct the grid ;

-

(2)

Next, extract a time point every time points (we set in all numerical settings) to construct the testing set , and use the remaining time points as the training set , and denote the corresponding estimated transition matrix with respect to the tuning parameters ;

-

(3)

Select the tuning parameters satisfying:

-

(1)

-

•

Window size selection: The width of the rolling window plays an important role in the multiple change points scenario. In practice, we can manually select a suitable window-size, or we may use the following strategy. In Assumption H4, we provided conditions on the window size and rolling step size . Next, we discuss an iterative procedure for determining these two parameters in practice.

(1) Start with , and , where is selected from 1 to 0.5 (equally spaced) and is a constant; (2) For a given , apply Algorithm 2 and obtain the final set of change points ; (3) Repeat (2) until the number of the final set of change points does not change. Return the corresponding window size . -

•

Model evaluation: We evaluate the performance of our algorithm by using the mean and standard deviation of the estimated change point locations relative to the number of observations as well as the boxplots for the estimated change point for each case. We use estimated rank, sensitivity (SEN), specificity (SPC), and relative error (RE) for the whole transition matrices and the low-rank and the sparse components as additional metrics to evaluate the performance of model.

For multiple change points settings, we also measure the selection rate. Specifically, a detected change point is counted as a success for the true change point , if and only if . Then, the selection rate is defined by calculating the percentage of simulation replications with successes.

All numerical experiments are run in R 3.6.0 on the uf HiPerGator Computing platform with 4 Intel E5 2.30 GHz Cores and 16 GB memory. The code and scripts for simulation examples and applications are available at https://github.com/peiliangbai92/LSVAR_cpd.

5.1 Performance for Detecting A Single Change Point

We investigate the following factors: the dimension of the model , the sample size , the differences in the norm, and of the two low-rank and sparse components, respectively and the information ratio . The following parameters settings are considered in our investigation. A full summary is provided in the form of a Table in Appendix F.1.

-

(A)

In the first setting, we consider the case that the low-rank component exhibits a very small change while the sparse one a large change. Further, the “total signal” in the transition matrix comes mostly from the sparse component and therefore, .

-

(B)

This setting is similar in structure to A: the low-rank components exhibit very small change, while the sparse components change by a significant amount, but the “total signal” in the transition matrix comes mostly from the former; i.e., for .

-

(C)

The structure of this setting is as in B, but different values of are considered.

-

(D)

This setting is the reverse of B, wherein the low-rank components exhibit a large change, while the sparse ones a very small ones, and further .

-

(E)

This setting is similar in structure to C, but the information ratio .

-

(F)

The setting is similar to E, but an increasing is considered.

The results for these settings over 50 replications are given in Table 1. The first two columns record the mean and standard deviation of the estimated change point location, the third and fourth columns are the estimated ranks for the low-rank components, the fifth and sixth columns give the sensitivity and specificity of the estimated sparse components, and finally the last column shows the relative norm error of the estimated transition matrix to the truth , and we also provide the relative error of the estimated sparse components (low-rank components) (or ) to the truth (or ).

| mean | sd | SEN | SPC | Total RE/ Sparse RE / Low-rank RE | |||

|---|---|---|---|---|---|---|---|

| A.1 | 0.498 | 0.002 | |||||

| A.2 | 0.499 | 0.002 | |||||

| A.3 | 0.499 | 0.002 | |||||

| B.1 | 0.530 | 0.090 | |||||

| B.2 | 0.532 | 0.089 | |||||

| B.3 | 0.534 | 0.089 | |||||

| C.1 | 0.522 | 0.056 | |||||

| C.2 | 0.497 | 0.005 | |||||

| C.3 | 0.502 | 0.031 | |||||

| C.4 | 0.497 | 0.005 | |||||

| D.1 | 0.494 | 0.011 | |||||

| D.2 | 0.494 | 0.008 | |||||

| D.3 | 0.495 | 0.007 | |||||

| E.1 | 0.477 | 0.048 | |||||

| E.2 | 0.478 | 0.026 | |||||

| E.3 | 0.496 | 0.015 | |||||

| F.1 | 0.495 | 0.053 | |||||

| F.2 | 0.487 | 0.039 | |||||

| F.3 | 0.495 | 0.023 |

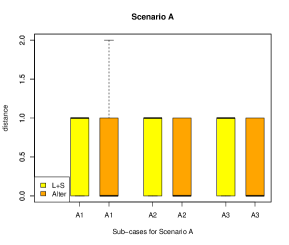

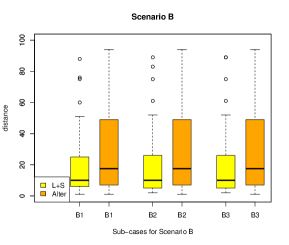

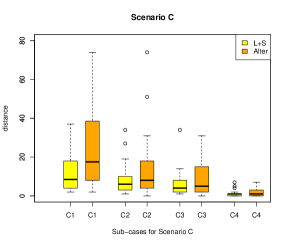

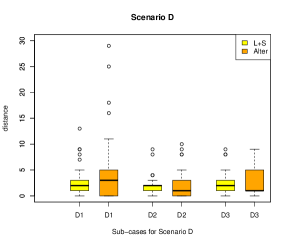

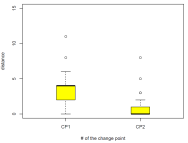

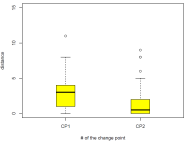

For settings A and D, where the dominant components change significantly, the algorithm identifies the change point extremely accurately, as evidenced by the mean estimate over 50 replicates and the very small standard deviation recorded. Further, the ranks of are accurately estimated under setting A, and the specificity and sensitivity of is close to 1. Under setting D, there is deterioration in the estimation of the rank of , as well as in the sensitivity of both and . In settings B and E, where there is a small change in the dominant component, the estimates of the change point deteriorate and also exhibit larger variability (especially in setting B). Under setting B, estimation of the rank of is also off, as is the sensitivity for the sparse components. Note that all estimated model parameters under setting E are very accurate, with a small deterioration in the specificity of the ’s. In settings C and F, we examine how the behavior of the information ratio influences the accuracy of the change point detection. As the difference between and increases, the estimation accuracy improves of the change point improves markedly. The same happens for the model parameters under setting F. Note that the results for settings C and F are in accordance with Remark 1 that discusses how the detectability of the full transition matrix is controlled by the information ratio. We provide the performance of single change point detection based on the surrogate model in Table 4 in Appendix F.1.

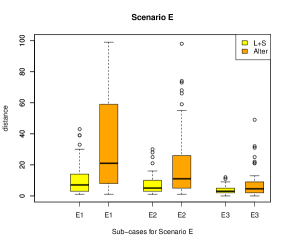

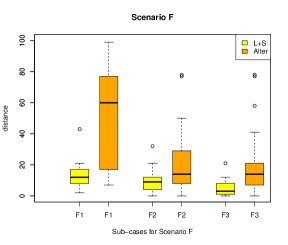

Figure 4 depicts boxplots based on 50 replicates of the distance between the location of the true change point and its estimate, i.e., . The yellow bars correspond to the full low-rank plus sparse model, while the orange ones to the surrogate model. In accordance to previous findings, under settings A and C, the results are comparable, as well as certain cases for setting E. On the other hand, under settings B, D and F, the full model clearly outperforms the surrogate one, even though in settings F2 and F3 the differences become smaller as the corresponding differences in the information ratios increase.

5.2 Performance for Detecting Multiple Change Points

We consider the same settings for each change point, as in case A in Section 5.1 with modified and , respectively. The specific scenarios under consideration are as follows:

-

(L)

In the first case, we consider settings with different number of change points. Specifically, we investigate the following three cases: (1) with , , , , and ; (2) with , , , , and ; (3) with , , , , and .

-

(M)

In the second case, we consider large enough to satisfy with two change points: and .

-

(N)

In the last scenario, the change in sparsity patterns is considered. We consider a different sparsity pattern rather than the 1-off diagonal structure in the sparse components.

The detailed model parameters are listed in the Table 5 in the Appendix F.2.

Table 2 presents the mean and standard deviation of the estimated locations of the change points, relative to the sample size , together with the selection rate, as defined at the beginning of the current section. For all cases under settings L and M, the two-step algorithm obtains very accurate results, also exhibiting little variability. The complex random sparse pattern considered in setting N leads to a small deterioration in the selection rate. The locations of the estimated change points together with box plots of for scenario N over 50 replicates are depicted in the Appendix F.2.

| points | truth | mean | sd | selection rate | points | truth | mean | sd | selection rate | ||

| L.1 | 1 | 0.1667 | 0.1667 | 0.0004 | 1.00 | M.1 | 1 | 0.3333 | 0.3331 | 0.0005 | 1.00 |

| 2 | 0.3333 | 0.3333 | 0.0003 | 1.00 | 2 | 0.6667 | 0.6665 | 0.0004 | 1.00 | ||

| 3 | 0.5000 | 0.4999 | 0.0003 | 1.00 | M.2 | 1 | 0.3333 | 0.3329 | 0.0003 | 1.00 | |

| 4 | 0.6667 | 0.6665 | 0.0004 | 1.00 | 2 | 0.6667 | 0.6667 | 0.0006 | 1.00 | ||

| 5 | 0.8333 | 0.8335 | 0.0004 | 1.00 | N.1 | 1 | 0.3333 | 0.3311 | 0.0125 | 0.94 | |

| L.2 | 1 | 0.1000 | 0.0999 | 0.0002 | 1.00 | 2 | 0.6667 | 0.6656 | 0.0056 | 0.98 | |

| 2 | 0.2500 | 0.2500 | 0.0000 | 1.00 | N.2 | 1 | 0.1667 | 0.1683 | 0.0115 | 0.92 | |

| 3 | 0.4000 | 0.3999 | 0.0002 | 1.00 | 2 | 0.8333 | 0.8267 | 0.0181 | 0.94 | ||

| 4 | 0.6000 | 0.6000 | 0.0000 | 1.00 | N.3 | 1 | 0.3333 | 0.3302 | 0.0121 | 0.98 | |

| 5 | 0.8000 | 0.7999 | 0.0001 | 1.00 | 2 | 0.6667 | 0.6655 | 0.0119 | 0.98 | ||

| L.3 | 1 | 0.1000 | 0.1000 | 0.0000 | 1.00 | ||||||

| 2 | 0.3000 | 0.3000 | 0.0000 | 1.00 | |||||||

| 3 | 0.5000 | 0.5000 | 0.0000 | 1.00 | |||||||

| 4 | 0.7000 | 0.6999 | 0.0002 | 1.00 | |||||||

| 5 | 0.9000 | 0.8998 | 0.0002 | 1.00 |

5.3 A Simulation Scenario Based on a EEG Data Set

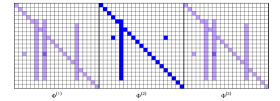

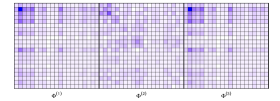

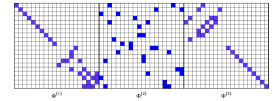

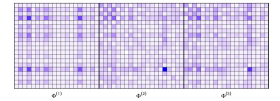

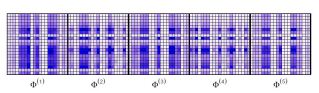

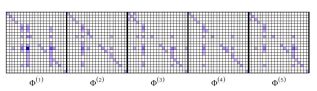

For this scenario, the sparsity structure is extracted from the EEG data set analyzed in Section 6.1. Specifically, the setting under consideration is as follows: , , with two change points located at and , respectively. The structure of the transition matrices is obtained by using the results presented in the application section (see Figure 6 in the Section G.2. in the supplement). We keep the non-zero elements (see Figure 5) and set their magnitudes at random to 0.4, -0.6, and 0.4, respectively. The low rank components are generated by using the spectral decomposition with ranks equal to 1, 3, and 1. The estimated sparse and low rank structures are illustrated in Figure 5:

The results are summarized in Table 3.

| points | truth | mean | sd | selection rate | |

|---|---|---|---|---|---|

| General sparsity pattern | 1 | 0.3333 | 0.3328 | 0.002 | 1.00 |

| 2 | 0.6667 | 0.6663 | 0.007 | 1.00 |

It can be seen that based on a low rank and sparse structure motivated by real data, the proposed algorithm exhibits a very satisfactory performance.

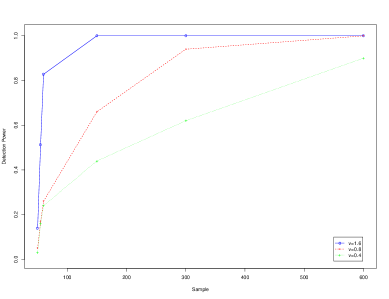

5.4 Impact of the Signal-to-noise Ratio on the Detection Rate

The signal-to-noise ratio (SNR) is defined as (see also Wang et al. (2020), Rinaldo et al. (2021)):

wherein the minimum jump size, and is the minimum spacing, i.e. . We set and with two change points located at and , respectively. Further, we set the minimum jump size to = 0.8, 1.0, and 1.6, and the resulting SNR takes the values 0.27, 0.33, and 0.53. The results are given Table 4.

| SNR | points | truth | mean | sd | selection rate |

|---|---|---|---|---|---|

| 0.27 | 1 | 0.3333 | 0.3412 | 0.017 | 0.90 |

| 2 | 0.6667 | 0.6702 | 0.012 | 0.94 | |

| 0.33 | 1 | 0.3333 | 0.3330 | 0.002 | 1.00 |

| 2 | 0.6667 | 0.6687 | 0.004 | 1.00 | |

| 0.57 | 1 | 0.3333 | 0.3332 | 0.002 | 1.00 |

| 2 | 0.6667 | 0.6665 | 0.001 | 1.00 |

As expected, for small SNR the detection accuracy deteriorates, both in terms of the selection rate of change points, as well as their locations. However, for SNR around or greater than 1, it becomes very satisfactory. Additional results are provided in Section F.3 in the Supplement.

Remark 11 (Additional numerical results and comparisons).

Additional numerical results including (i) for the surrogate model, (ii) for additional scenarios for multiple change points, (iii) for run times between the low rank plus sparse and the surrogate models, (iv) with a factor model exhibiting change points, (v) between a factor and the low rank plus sparse models under a misspecified data generating mechanism, (vi) comparison between the proposed two-step algorithm and the TSP algorithm in Bai et al. (2020), and (vi) between the two-step rolling window strategy and a dynamic programming algorithm are presented in Appendices F.1-F.7, respectively.

6 Applications

6.1 Change Point Detection in EEG Signals

There has been work in the literature on analyzing EEG data using low-rank models for task related signals, since the latter exhibit low-rank structure (Liu et al. 2018, Jao et al. 2018). Next, we employ the full low-rank plus sparse model to detect change points in data from Trujillo et al. (2017). This data set recorded 72 channels of continuous EEG signals by using active electrodes. The sampling frequency is 256Hz and the total number of time points per EEG electrode is 122880 over 480 seconds. The stimulus procedure is that after a resting state (eliminated from the data set) lasting 8 mins, the subject alternates between a 1-min period with eyes open followed by a 1-min period with eyes closed, repeated four times. Hence, we expect that the employed model captures the low-rank structure associated with the task at hand (open/closed eyes), while the sparse component can capture idiosyncratic behavior across repetitions of the task.

To illustrate the proposed methodology, two subjects are selected; differences in the EEG signals over time are visible for the first subject, but not for the second one. The data are de-trended, by calculating the moving average of each EEG signal and removing it. Specifically, the period average, which is an unbiased estimator of trend, is given by ; we select in accordance to the frequency of the data, and we obtain the de-trended time series by removing the period average. In this work, we use 21 selected EEG channels and time points in the middle of the whole time series. According to the experiments described in Trujillo et al. (2017), there are five open/closed eyes segments in the selected time period with four change points approximately at locations: , , , and . The data are plotted in Figure 2 in Appendix G.2. Selection of the tuning parameters is based on the guidelines given in Appendix G.1. Note that to separate adequately the sparse component from the low-rank one, we set based on its theoretical values provided in Assumption H2.

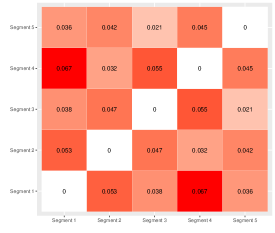

The change points estimated by the two-step algorithm are , , and . The estimated change points are close to those identified based on the designed experiment. In order to quantify the differences among the estimated components across segments, we use the Hamming distance for both sparse and low-rank ones. The results are shown in Figure 6 in the form of a heat map that confirms the high degree of similarity between all “eyes closed” segments (1, 3, 5) and all “eyes open” segments (2, 4), thus further confirming the accuracy of the methodology. We also provide the estimated low-rank and the sparse patterns for 5 segments in Figure 3, and the correlation networks for the sparse components in Figure 4 in Appendix G.2.

6.2 An Application to Macroeconomics Data

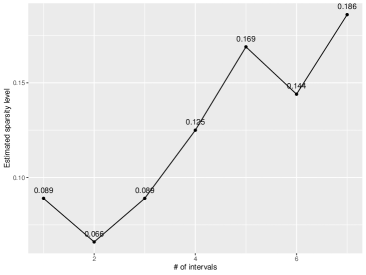

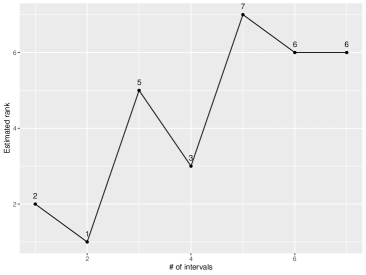

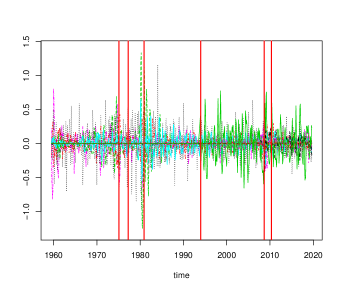

We consider the macroeconomics data obtained from the FRED database McCracken & Ng (2016). This data set comprises of 19 key macroeconomic variables, corresponding to the “Medium” model analyzed in Bańbura et al. (2010) and covering the 1959–2019 period (723 observations). The original time series data are non-stationary and we de-trend them by taking first differences.

To select the tuning parameters , we employ a 2-dimensional grid search procedure. In our analysis, we set based on its theoretical value in Assumption H2 to ensure identifiability of the sparse component from the low-rank one. The estimated change points are listed in Table 5, while the sparsity levels and ranks for each segment are plotted in Figure 7. The selected change points are presented in Figure 5 in Appendix G.3. A detailed discussion (due to space constraints) of related events is also provided in Appendix G.3.

| Date (mm/dd/yyyy) | Candidate Related Events |

|---|---|

| 02/01/1975 | Aftermath of 1973 oil crisis |

| 04/01/1977 | Rapid build-up of inflation expectations |

| 12/01/1980 | Rapid increase of interest rates by the Volcker Fed |

| 01/01/1994 | Multiple events - see Appendix G.3 |

| 09/01/2008 | Recession following collapse of Lehman Brothers |

| 05/01/2010 | Recovery from the Great Financial crisis of 2008 |

We also compare the results using the detection strategy based on the static factor model in Barigozzi et al. (2018). According to Fama & French (1996), we set the maximum number of factors to three and the estimated change points are listed in Table 6.

| Date (mm/dd/yyyy) | Candidate Related Events |

|---|---|

| 12/01/1979 | Rapid increase of interest rates by the Volcker Fed |

| 01/01/1985 | Multiple events |

| 11/01/1993 | Multiple events |

| 04/01/2008 | Prequel to the Great Financial Crisis |

The factor model misses important events, including the economic recovery following the Financial Crisis of 2008 and the recession following the first oil crisis of 1973. Further, it identifies a change point in early April of 2008, even though most of the macroeconomic (as opposed to financial market) indices started deteriorating in the summer of 2008 and tumbled in the 3rd quarter, following the collapse of Lehman Brothers in mid-September.

7 Concluding Remarks

The paper addressed the problem of multiple change point detection in reduced rank VAR models. The key innovation is the development of a two-step strategy that obtains consistent estimates of the change points and the model parameters. Other strategies for detecting multiple change points in high-dimensional models, such as fused penalties or binary segmentation type of procedures, either require very stringent conditions or are not directly applicable. Further, dynamic programming entails a quadratic computational cost in the number of time points compared to a linear cost for the proposed strategy. To enhance computational efficiency, we introduced a surrogate weakly sparse model and identified sufficient conditions under which the aforementioned 2-step strategy detects change points in low-rank and sparse VAR models as accurately as using the correctly specified model, but at significant computational gains.

In the algorithmic and technical results presented, similar to the case of a sparse VAR model with change points (Wang et al. (2019)), we assume a simple structure on the error terms, i.e., in segment , , where is a fixed constant independent of . Such a simple structure on the covariance matrices of error terms ensures the identifiability of change points, since a change in the transition matrices would imply that the second order structure (the auto-correlation function) of the stochastic process before and after the change points have changed, thus the definition of change points becomes meaningful. It is of interest to investigate in future work a general covariance matrix , or even segment specific ones , including conditions that lead to changes in the segment specific auto-correlation function of the process.

Further, the proposed strategy is directly applicable to other forms of structured sparsity in the transition matrix of the VAR model, including low-rank plus structured sparse, or structured sparse plus sparse, as discussed for stationary models in Basu et al. (2019).

Finally, the presentation focused on a VAR model with a single lag, but both the modeling framework and the developed 2-step detection strategy can be extended to processes with in a similar manner, as presented in Basu et al. (2019).

References

- (1)

- Agarwal et al. (2012) Agarwal, A., Negahban, S., Wainwright, M. J. et al. (2012), ‘Noisy matrix decomposition via convex relaxation: Optimal rates in high dimensions’, The Annals of Statistics 40(2), 1171–1197.

- Ahn & Reinsel (1988) Ahn, S. K. & Reinsel, G. C. (1988), ‘Nested reduced-rank autoregressive models for multiple time series’, Journal of the American Statistical Association 83(403), 849–856.

- Bai & Ng (2008) Bai, J. & Ng, S. (2008), ‘Large dimensional factor analysis’, Foundations and Trends® in Econometrics 3(2), 89–163.

- Bai et al. (2020) Bai, P., Safikhani, A. & Michailidis, G. (2020), ‘Multiple change points detection in low rank and sparse high dimensional vector autoregressive models’, IEEE Transactions on Signal Processing 68, 3074–3089.

- Bańbura et al. (2010) Bańbura, M., Giannone, D. & Reichlin, L. (2010), ‘Large bayesian vector auto regressions’, Journal of applied Econometrics 25(1), 71–92.

- Bardsley et al. (2017) Bardsley, P., Horváth, L., Kokoszka, P. & Young, G. (2017), ‘Change point tests in functional factor models with application to yield curves’, The Econometrics Journal 20(1), 86–117.

- Barigozzi et al. (2018) Barigozzi, M., Cho, H. & Fryzlewicz, P. (2018), ‘Simultaneous multiple change-point and factor analysis for high-dimensional time series’, Journal of Econometrics 206(1), 187–225.

- Basu et al. (2019) Basu, S., Li, X. & Michailidis, G. (2019), ‘Low rank and structured modeling of high-dimensional vector autoregressions’, IEEE Transactions on Signal Processing 67(5), 1207–1222.

- Basu & Michailidis (2015) Basu, S. & Michailidis, G. (2015), ‘Regularized estimation in sparse high-dimensional time series models’, The Annals of Statistics 43(4), 1535–1567.

- Bhattacharjee et al. (2020) Bhattacharjee, M., Banerjee, M. & Michailidis, G. (2020), ‘Change point estimation in a dynamic stochastic block model’, Journal of Machine Learning Research 21(107), 1–59.

- Billio et al. (2012) Billio, M., Getmansky, M., Lo, A. W. & Pelizzon, L. (2012), ‘Econometric measures of connectedness and systemic risk in the finance and insurance sectors’, Journal of financial economics 104(3), 535–559.

- Bordo & Eichengreen (2007) Bordo, M. D. & Eichengreen, B. (2007), A retrospective on the Bretton Woods system: lessons for international monetary reform, University of Chicago Press.

- Box & Tiao (1977) Box, G. E. & Tiao, G. C. (1977), ‘A canonical analysis of multiple time series’, Biometrika 64(2), 355–365.

- Chan et al. (2014) Chan, N. H., Yau, C. Y. & Zhang, R.-M. (2014), ‘Group lasso for structural break time series’, Journal of the American Statistical Association 109(506), 590–599.

- Chandrasekaran et al. (2011) Chandrasekaran, V., Sanghavi, S., Parrilo, P. A. & Willsky, A. S. (2011), ‘Rank-sparsity incoherence for matrix decomposition’, SIAM Journal on Optimization 21(2), 572–596.

- Cho & Fryzlewicz (2015) Cho, H. & Fryzlewicz, P. (2015), ‘Multiple-change-point detection for high dimensional time series via sparsified binary segmentation’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 77(2), 475–507.

- Csörgö & Horváth (1997) Csörgö, M. & Horváth, L. (1997), Limit theorems in change-point analysis, Vol. 18, John Wiley & Sons Inc.

- Davis et al. (2006) Davis, R. A., Lee, T. C. M. & Rodriguez-Yam, G. A. (2006), ‘Structural break estimation for nonstationary time series models’, Journal of the American Statistical Association 101(473), 223–239.

- Eichengreen (2014) Eichengreen, B. (2014), Hall of mirrors: The great depression, the great recession, and the uses-and misuses-of history, Oxford University Press.

- Fama & French (1996) Fama, E. F. & French, K. R. (1996), ‘Multifactor explanations of asset pricing anomalies’, The journal of finance 51(1), 55–84.

- Friedrich et al. (2008) Friedrich, F., Kempe, A., Liebscher, V. & Winkler, G. (2008), ‘Complexity penalized m-estimation: fast computation’, Journal of Computational and Graphical Statistics 17(1), 201–224.

- Friston et al. (2014) Friston, K. J., Bastos, A. M., Oswal, A., van Wijk, B., Richter, C. & Litvak, V. (2014), ‘Granger causality revisited’, Neuroimage 101, 796–808.

- Hartigan & Wong (1979) Hartigan, J. A. & Wong, M. A. (1979), ‘Algorithm as 136: A k-means clustering algorithm’, Journal of the Royal Statistical Society. Series C (Applied Statistics) 28(1), 100–108.

- Hsu et al. (2011) Hsu, D., Kakade, S. M. & Zhang, T. (2011), ‘Robust matrix decomposition with sparse corruptions’, IEEE Transactions on Information Theory 57(11), 7221–7234.

- Jao et al. (2018) Jao, P.-K., Chavarriaga, R. & Millán, J. d. R. (2018), Using robust principal component analysis to reduce eeg intra-trial variability, in ‘40th Annual Conference of the IEEE Engineering in Medicine and Biology Society (EMBC)’, IEEE, pp. 1956–1959.

- Kareken (1978) Kareken, J. H. (1978), ‘Inflation: an extreme view’, Quarterly Review (win).

- Kilian & Lütkepohl (2017) Kilian, L. & Lütkepohl, H. (2017), Structural vector autoregressive analysis, Cambridge University Press.

- Lam et al. (2011) Lam, C., Yao, Q. & Bathia, N. (2011), ‘Estimation of latent factors for high-dimensional time series’, Biometrika 98(4), 901–918.

- Li et al. (2014) Li, G., Qin, S. J. & Zhou, D. (2014), ‘A new method of dynamic latent-variable modeling for process monitoring’, IEEE Transactions on Industrial Electronics 61(11), 6438–6445.

- Lin & Michailidis (2017) Lin, J. & Michailidis, G. (2017), ‘Regularized estimation and testing for high-dimensional multi-block vector-autoregressive models’, The Journal of Machine Learning Research 18(1), 4188–4236.

- Liu et al. (2018) Liu, F., Wang, S., Qin, J., Lou, Y. & Rosenberger, J. (2018), Estimating latent brain sources with low-rank representation and graph regularization, in ‘International Conference on Brain Informatics’, Springer, pp. 304–316.

- Loh & Wainwright (2012) Loh, P.-L. & Wainwright, M. J. (2012), ‘High-dimensional regression with noisy and missing data: provable guarantees with nonconvexity’, The Annals of Statistics pp. 1637–1664.

- Lütkepohl (2013) Lütkepohl, H. (2013), Introduction to multiple time series analysis, Springer Science & Business Media.

-

McCracken & Ng (2016)

McCracken, M. W. & Ng, S. (2016),

‘Fred-md: A monthly database for macroeconomic research’, Journal of

Business & Economic Statistics 34(4), 574–589.

https://doi.org/10.1080/07350015.2015.1086655 - Michailidis & d’Alché Buc (2013) Michailidis, G. & d’Alché Buc, F. (2013), ‘Autoregressive models for gene regulatory network inference: Sparsity, stability and causality issues’, Mathematical biosciences 246(2), 326–334.

- Negahban et al. (2012) Negahban, S. N., Ravikumar, P., Wainwright, M. J. & Yu, B. (2012), ‘A unified framework for high-dimensional analysis of -estimators with decomposable regularizers’, Statistical Science 27(4), 538–557.

- Orphanides (2004) Orphanides, A. (2004), ‘Monetary policy rules, macroeconomic stability, and inflation: A view from the trenches’, Journal of Money, Credit and Banking pp. 151–175.

- Rinaldo et al. (2021) Rinaldo, A., Wang, D., Wen, Q., Willett, R. & Yu, Y. (2021), Localizing changes in high-dimensional regression models, in ‘International Conference on Artificial Intelligence and Statistics’, PMLR, pp. 2089–2097.

- Roy et al. (2017) Roy, S., Atchadé, Y. & Michailidis, G. (2017), ‘Change point estimation in high dimensional markov random-field models’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 79(4), 1187–1206.

- Safikhani & Shojaie (2020) Safikhani, A. & Shojaie, A. (2020), ‘Joint structural break detection and parameter estimation in high-dimensional non-stationary var models’, Journal of the American Statistical Association (Theory and Methods), to appear .

- Schröder & Ombao (2019) Schröder, A. L. & Ombao, H. (2019), ‘Fresped: Frequency-specific change-point detection in epileptic seizure multi-channel eeg data’, Journal of the American Statistical Association 114(525), 115–128.

- Stock & Watson (2002) Stock, J. H. & Watson, M. W. (2002), ‘Forecasting using principal components from a large number of predictors’, Journal of the American Statistical Association 97(460), 1167–1179.

- Stock & Watson (2016) Stock, J. H. & Watson, M. W. (2016), Dynamic factor models, factor-augmented vector autoregressions, and structural vector autoregressions in macroeconomics, in ‘Handbook of macroeconomics’, Vol. 2, Elsevier, pp. 415–525.

- Trujillo et al. (2017) Trujillo, L. T., Stanfield, C. T. & Vela, R. D. (2017), ‘The effect of electroencephalogram (eeg) reference choice on information-theoretic measures of the complexity and integration of eeg signals’, Frontiers in neuroscience 11, 425.

- Velu et al. (1986) Velu, R. P., Reinsel, G. C. & Wichern, D. W. (1986), ‘Reduced rank models for multiple time series’, Biometrika 73(1), 105–118.

- Wang et al. (2020) Wang, D., Yu, Y. & Rinaldo, A. (2020), ‘Univariate mean change point detection: Penalization, cusum and optimality’, Electronic Journal of Statistics 14(1), 1917–1961.

- Wang et al. (2019) Wang, D., Yu, Y., Rinaldo, A. & Willett, R. (2019), ‘Localizing changes in high-dimensional vector autoregressive processes’, arXiv preprint arXiv:1909.06359 .

- Wang & Bessler (2004) Wang, Z. & Bessler, D. A. (2004), ‘Forecasting performance of multivariate time series models with full and reduced rank: An empirical examination’, International Journal of Forecasting 20(4), 683–695.

- Zhang & Huang (2008) Zhang, C.-H. & Huang, J. (2008), ‘The sparsity and bias of the lasso selection in high-dimensional linear regression’, The Annals of Statistics 36(4), 1567–1594.

Supplementary Material for Multiple Change Point Detection in Reduced Rank High Dimensional Vector Autoregressive Models

In the Supplement, we first present conditions related to the underlying VAR processes in Appendix A, the detection algorithms are provided in Appendix B, a comparison of the true and the surrogate model is provided in Appendix C, then introduce auxiliary lemmas with their proofs in Appendix D, followed by the proofs of then main Theorems in Appendix E, the results for additional numerical experiments in Appendix F, and the supplementary results for real-data applications in Appendix G.

Appendix A Conditions on VAR Processes

Recall that the piece-wise stationary structured VAR(1) model is given by:

| (14) | ||||

where is a vector of observed time series at time , , are the low-rank components and , are the sparse matrices for the corresponding models in the two time intervals. The -dimensional noise process and are independent and identically distributed from Gaussian distributions; , where denotes the identity matrix and is a fixed constant. In this modeling formulation, there are two independent VAR processes over the whole time interval ; the first process is observed up to time and the second VAR process is observed afterwards. In other words, there are two stationary VAR processes concatenated together at the (unknown) time . The independence assumption on these two VAR processes makes it possible to write down the density function of the stochastic process as the product of the density functions of the two stationary processes, thus properly defining the infinite-dimensional distribution of the stochastic process .

Stability. To show consistency of both change points and model parameters, we assume that the VAR(1) model in (14) is piece-wisely stable. Formally, we assume that the characteristic polynomial with respect to the -th segment satisfies for . This is a common assumption for stationary VAR processes (Lütkepohl 2013, Basu & Michailidis 2015). This assumption also indicates that the spectral density function for the -th segment of the VAR model:

is upper bounded in the spectral norm. In addition, we also assume that

(i) the maximum eigenvalue is bounded:

(ii) the minimum eigenvalue is bounded away from zero:

As discussed in Basu & Michailidis (2015), it is known that and reflect the stability of a VAR process and they are related to and as follows:

where and , respectively. For the specific low-rank plus sparse structure for the underlying VAR process, we can verify that for each segment, an upper bound of is given by:

where is the maximum singular value of .

Next, we introduce two key assumptions, required in our theoretical proofs that are commonly made for high-dimensional regularized estimation problems.

-

•

Restricted strong convexity. We start by introducing the weighted regularizer that combines the penalties for the low-rank and the sparse components. Specifically, for any pair of positive numbers, we define the weighted regularizer with respect to the low-rank matrix and the sparse matrix as:

and the associated norm is given by:

Then, the restricted strong convexity (RSC) condition becomes:

Definition 1 (Restricted Strong Convexity (RSC)).

A generic linear operator satisfies the RSC condition with respect to the associated norm with curvature constant and tolerance constant if:

-

•