Time-inconsistent view on a dividend problem with penalty

April)

Abstract

We consider the dividend maximization problem including a ruin penalty in a diffusion environment. The additional penalty term is motivated by a constraint on dividend strategies. Intentionally, we use different discount rates for the dividends and the penalty, which causes time-inconsistency. This allows to study different types of constraints. For the diffusion approximation of the classical surplus process we derive an explicit equilibrium dividend strategy and the associated value function.

Inspired by duality arguments, we can identify a particular equilibrium strategy such that for a given initial surplus the imposed constraint is fulfilled. Furthermore, we illustrate our findings with a numerical example.

Keywords: Ruin theory; dividends; time-inconsistent stochastic control; extended Hamilton-Jacobi-Bellman equation

1 Introduction

The dividend maximization problem and many extensions of it are widely investigated in actuarial science and in particular in its risk theoretic branch. Under suitable conditions one can detect the optimal control in prespecified models.

For example, in classical diffusion settings optimal dividend strategies are of constant barrier type, cf. [Shreve et al., 1984] or [Asmussen and Taksar, 1997]. If using such a reflecting barrier strategy, this has the consequence of almost sure ruin.

On the other hand, one way to totally avoid ruin is the usage of capital injections, cf. [Kulenko and Schmidli, 2008], one of the most renowned recent extensions of the problem. While these results are theoretically remarkable, they seem not to be satisfying if one aims at a balanced situation between risk and profit.

So there exist two extremal cases: on the one hand maximizing the output regardless of consequences - always having in mind that this will cause negative social impacts on the insured, employees, the public reputation of the insurance company and its management. On the other hand, keeping a business uncompromisingly alive using capital injections, may be in conflict with owner interest.

For this reason, we want to identify a dividend strategy which suffices a particular tradeoff between ruin and profit.

Naturally, one way of tackling this problem is to consider the dividend problem under a ruin constraint. That is maximizing expected discounted dividends over a set of strategies for which the ruin probability for fixed initial surplus stays below a given level. This approach goes back to [Hipp, 2003]. Recent results in this direction are presented in [Hipp, 2018b, Hipp, 2018a, Hipp, 2020] and mentioned in a talk by Brandon Israel García Flores111Genetic Algorithms in Risk Theory: Optimizing Dividend Strategies at IME conference 2021. On a finite time horizon such a constrained dividend maximization problem is analyzed in [Grandits, 2015].

For dealing with the ruin probability constraint in the first place and for achieving a better understanding of the evolution of such constraints in the second place, we present a time-inconsistent variation or extension of [Hernández and Junca, 2015] in the following.

There are different origins of time-inconsistency in the dividend maximization problem. For example, [Zhao et al., 2014] deal with the problem using non-exponential discounting, whereas [Christensen and Lindensjö, 2019] arrive at time(space)-inconsistency when adding a moment constraint on the number of expected dividend payments.

1.1 Specification of the model

In the following we will consider the surplus process with the dynamics

| (1) |

where and are deterministic functions such that (1) is well-posed and is a standard Brownian motion on a probability space . The flow of information is given by the -completed Brownian history, denoted by . Exemplary conditions which ensure that (1) admits a strong solution are the classical linear growth and Lipschitz conditions for and , see [Karatzas and Shreve, 1991, p. 289, Theorem 2.9]. Or, the more general requirements from [Zvonkin, 1974, p. 142, Theorem 4], which are:

-

•

is bounded and measurable,

-

•

is bounded from above and away from zero, is continuous in and is Hölder continuous with parameter larger or equal than with respect to for every .

We subsequently refer to these latter conditions as conditions .

The task in the classical problem, cf. [Shreve et al., 1984], is to choose the dividend process in an optimal way, such that the discounted expected future dividends are maximized. The resulting value function is

| (2) |

where the supremum is taken over all processes which are non-decreasing, adapted, càglàd with and . The controlled surplus is

| (3) |

For assumptions on and such that (2) is well-posed, we refer to [Shreve et al., 1984].

In order to penalize early ruin [Thonhauser and Albrecher, 2007] added the term to the reward function. Based on their work, [Hernández and Junca, 2015] linked the penalty term to a constraint on in order to solve the associated constrained problem for a given initial surplus. Motivated by these previous results and by a comment in the recent contribution [Junca et al., 2019, p. 636, Remark 2.1] on an extension with different discount rates, we want to analyze the following reward function for a

This integrates the constraint

| (4) |

Here and are positive, not necessarily equal constants, and , for a process starting in at time .

We consider the following variant of this problem. We assume that and we define the set of admissible controls to be the measurable controls of feedback type . The bound is a prespecified constant.

The main purpose of considering controls of feedback type is due to the fact that we are facing a time-inconsistent stochastic control problem in the framework of [Björk et al., 2017, p. 334] and [Christensen and Lindensjö, 2019].

Note that as in the classical time-consistent case, one could try to approach the singular control problem, where the dividend rate is unbounded enabling lump sum payments, by considering the limit of to infinity in the problem with restricted dividend payments, see [Schmidli, 2008, p. 102]. But in the present case the underlying situation is different and the concept of equilibrium controls probably has to be adapted for the singular case. In order to keep our discussion as condensed as possible, we leave this task for future research.

Remark 1.

Notice that our approach is also able to cover the situation with a constraint on the ruin probability. For this reason, we consider for the above expectation (4) the limit . We have that and

Remark 2.

If we set and send to zero in (4), we are able to identify the minimal argument for which a ruin probability constraint can be fulfilled for an and constant and . This minimal appears, since the control process can only reduce the current reserve. Hence, if the constraint cannot be reached from the level without dividends, it is not possible to satisfy (4) with a control action. In order to determine this minimal level, we consider (3) with , where is a positive constant. Consequently, we consider the hitting time of zero of a Brownian motion with drift . The corresponding probability of ruin for this process is then given by

| (5) |

see [Schmidli, 2017, p. 109, Lemma 5.21]. Certainly, if the drift is negative, we cannot fulfil the constraint (4). In the extremal case , we can satisfy (4) only if

1.2 Reformulation of the reward

Optimization problems with constraints can usually be handled using the Lagrange multiplier approach. For we define the reward function to be:

| (6a) | |||

| and for | |||

| (6b) | |||

subject to

| (7) |

Moreover, let and be such that a solution to (7) exists. In our case we assume that and that and fulfil the previously stated conditions . Further, we obtain that the solution to (7) is a strong Markov process with infinitesimal generator

for a suitable function and , see [Karatzas and Shreve, 1991, p. 322].

Remark 3.

According to [Hernández and Junca, 2015, p. 137, eq. (3)] and

[Hernández et al., 2018] we set in the function (6a), such that, if the constraint is fulfilled, the term on the right hand side is positive and corresponds to a penalization. We restrict ourselves to a fixed value . As proposed in [Øksendal, 2000, p. 259-260], we can first solve the problem for every fixed , and then choose such that the constraint (4) is fulfilled. This is treated in detail in Section 5. Nevertheless, the duality approach, especially as used in [Hernández and Junca, 2015, p. 139, Th. 4.2], is not completely applicable in our setting. This is because the game-theoretic approach, which we are going to use, is different to a classical maximization of a reward function.

Since , the objective (6a) (or (6b)) is time-inconsistent and the dynamic programming principle is not valid anymore. Therefore, we make use of the theory of time-inconsistent stochastic optimal control, see [Ekeland and Pirvu, 2008], [Ekeland et al., 2012] and [Björk et al., 2017]. For this purpose, we modify the reward function from (6a) and introduce a new variable , some artificial reference point in time. For , we define the function , to be

such that we arrive at a representation only using a running reward and a constant term. We denote this auxiliary reward function by:

| (8a) | ||||

| For we have: | ||||

| (8b) | ||||

For we obtain that the auxiliary reward function coincides with the original reward function and , respectively.

Remark 4.

Note that we have the following integrability property of the reward. For all fixed and for all and each admissible control , it holds that

| (9) |

Using the special form of and the fact that controls are bounded by , we obtain that the auxiliary reward function and the original reward function are both bounded in and . Namely, it holds that

Moreover, in the special case we obtain that

2 Equilibrium control and associated equilibrium value function

The time-inconsistencies in (8a) and (8b) prevent us from using the dynamic programming approach for deriving a maximizing dividend strategy. Instead we rely on the methodology introduced by [Björk et al., 2017]. More precisely, we are guided by [Björk et al., 2017, p. 345], [Yong, 2012, p. 23] and [Zhao et al., 2014, p. 3]. Analogously, as discussed in [Björk et al., 2017] the subsequent definition is motivated by an intrapersonal game of the management in force with its future composition. In our problem the executive management has to choose the dividend strategy, but their associated reward function is of the form (8a) or (8b), so their preferences are time-inconsistent and hence vary over time. The management of the company is naturally not appointed for life, hence it will happen that single executives or even the whole leadership changes over time. Of course, they should always act in favour of the shareholders of the company. Aiming at a time-consistent management decision results in various economic benefits. Such a line of action will improve both the stability inside the company, regarding affiliates and employees, and the general external assessment, affecting future investors and clients. In the light of these economic considerations, the present constraint (4), discussed in Section 5, also can be viewed as a comprehensive alternative to classical one-year risk considerations, e.g. conditions on the value at risk.

Definition 1 ([Björk et al., 2017, Def. 3.4, p. 336]).

Consider an admissible control and choose an other arbitrary admissible control , a fixed value and an arbitrary but fixed initial point . Consider the control defined by

| (10) |

Now, if for all

is called equilibrium control and the associated (equilibrium) value function is defined via

| (11) |

Definition 2.

The extended Hamilton-Jacobi-Bellman system of equations for a function and the given objective (6a) (and for (6b)) reads as follows for all

| (12a) | |||

| (12b) | |||

and for all

| (13a) | |||

| (13b) | |||

| (14a) | |||

| (14b) | |||

Moreover, denotes the control for which the supremum is attained. Where (12a), (13a) and (14a) correspond to the case and (12b), (13b) and (14b) belong to the case .

Remark 5.

Notice that the condition (14a) (or (14b)) is the natural one in order to obtain the representation (16a) (or (16b)). In this instance we are conscious that the representation (14b) is not exactly in line with [Björk et al., 2017], since following their representation, we would have to consider the function

with the associated equation and the corresponding boundary conditions ( at and for to infinity). But since we want to use a verification argument to confirm our solution as the value function, we prefer boundary conditions in terms of deterministic functions. Hence, we impose the following conditions which imply (14a) (or (14b)):

| (15) | ||||

in addition to the requirement that is bounded. The above requirements (15) for also yield (14b), since

3 Verification Theorem

In this section we state and prove the associated verification theorem. The required regularity of the involved function is due to the applicability of a suitable version of Itô’s formula and the properties of a constructible explicit solution.

Theorem 1 (Verification Theorem).

Given a real-valued function for a value , which is bounded for all and for all . In addition, suppose that , and are bounded for all and for all . Furthermore, let solve the extended HJB system in Definition 2, where is an admissible control for which the supremum is attained.

Then,

-

-

is an equilibrium control according to Definition 1,

-

-

is the associated value function and

-

-

has the representation, for all :

(16a) and (16b)

Proof.

At first, we are going to show that . We are certainly guided by the work of [Björk et al., 2017, p. 345], [Yong, 2012, p. 23] and [Zhao et al., 2014, p. 3].

We start with showing the stochastic representation of , for that reason we use a modified version of Itô’s formula, cf. [Leobacher et al., 2015, p. 7, Thm. 2.9], and take expectations. Let and be fixed, further we set and use the bounded derivatives of in addition to (13a) to obtain

Now the usage of boundary conditions from (14a), the boundedness as discussed in Remark 4 and the dominated convergence theorem (or even monotone convergence if because ) leads to the desired form

This gives indeed

In the second part we prove that is indeed an equilibrium control. Therefore, we consider, as proposed in Definition 1, an arbitrary admissible control , and arbitrary but fixed in order to define for and as in (10). Set , then we have

The first subsequent equality holds due to the definition of and the strong Markov property. For the second one we need that (16a) holds true for different values in the first and second argument of ,

Moreover, taking this into account and using the version of Itô’s formula from

[Leobacher et al., 2015, p. 7, Thm. 2.9], we end up with

| (17) | ||||

The expectation of the stochastic integral part of (17) is zero. This holds true since and are continuous in and and the controlled process is adapted and continuous, we get that the integrand of the stochastic integral is predictable. Furthermore, and are bounded in and and hence the stochastic integral is indeed a martingale for general admissible controls .

Further, we divide (17) by and consider the limit inferior for to zero. Using bounded convergence to interchange limit and expectation and Lebesgue’s differentiation theorem [Wheeden and Zygmund, 1977, p. 100, 108-109], we obtain the second equality in (18)

| (18) | ||||

Moreover, we use (12a) for the last inequality in (18) to finally obtain that is an equilibrium control. This gives that . ∎

Remark 6.

In the theory of stochastic optimal control, the classical solution approach suggests to prove a verification theorem and present a suitable solution satisfying the needed regularity requirements. For the sake of completeness, we want to mention the result by [Lindensjö, 2019], where it is shown that, under regularity assumptions, it is even necessary for the equilibrium to solve the extended HJB system. We adopt the notation of the following theorem and just mention that our defined extended HJB equation is a special case of the extended HJB system II in [Lindensjö, 2019]. We omit further details and refer to the original source.

Theorem 2 ( [Lindensjö, 2019, p. 431, Theorem 3.12] ).

A regular equilibrium solves the extended HJB system II.

4 Classical solution approach

In this section we are able to reveal an explicit solution to the above stated time-inconsistent problem under the assumption of constant coefficients, i.e., and .

Remark 7.

Please notice that in the subsequent analysis we can send and do not violate its general validity if . Since in this instance the function , which will be constructed subsequently, solves the associated ODE (39) also in the limiting case.

On the contrary, if this function is zero in the limiting case and cannot fulfil the condition in (39). Therefore, the present problem for reduces, as , to the unconstrained classical dividend problem with the value function shifted by the constant and optimal threshold height .

We follow the classical line of attack as in [Zhao et al., 2014]. Since we have to solve the equation (12a),

we obtain as in the classical problem for the maximizing argument

Moreover, if we assume that our function is increasing and concave in , there exists a threshold level such that for and for . Under this premise and taking account of Remark 5, fulfilling the following equation is sufficient for the solution of the extended HJB equation in Definition 2:

| (28) |

In order to take advantage of Theorem 1 we make the following well guessed ansatz:

| (29) |

where is the solution of

| (34) |

and solves

| (39) |

The above equations lead to the following solutions

where

Due to the conditions and , we obtain and . On the other hand we have for :

where

From the conditions and , we obtain and . Furthermore, we ask for the following smooth fit conditions for ,

| (40) | |||

| (41) | |||

| (42) |

Note that the condition (42) is in contrast to the smooth fit condition of the classical dividend problem. In our case, we have to make sure that .

For the first two conditions (40) and (41) immediately yield

Since , and , we get that and . Analogously, (40) and (41) give for that

Because and , we obtain , and . The last condition (42) reveals the exact candidate equilibrium threshold level . Indeed, we are looking for a value such that

Therefore, we analyze the following function

| (43) |

We have to find a such that . If this root exists, we denote it by .

Remark 8.

Concerning the dependence of the equilibrium threshold level on we obtain that: if tends to zero, then , , and if , we obtain and .

If we obtain and . Which means that the function reduces to

| (46) |

Therefore, the threshold level tends to the solution of the equation , as tends to zero. Moreover, if , we arrive at the optimal threshold of the classical problem

| (47) |

since ruin is for sure. This corresponds to the same control strategy as if equals zero. Furthermore, the statement of Lemma 1 also holds true for the special case , which just means that is replaced by .

Lemma 1.

If

then G(b)=0 admits a unique positive solution denoted by .

Proof.

Analogously as in [Zhao et al., 2014, p. 6, Lemma 4.1], we know that by assumption and is strictly monotonically decreasing since for all . This can be seen using . Finally, we have that

since

The last inequality is true because the first factor is positive and , see also [Asmussen and Taksar, 1997, p. 4, Lemma 2.1]. Altogether, we obtain the desired result. ∎

Finally, we get the following candidate solution:

| (53) |

with on the whole domain since the coefficients are chosen such that (40) and (41) are fulfilled.

Theorem 3.

For the time-inconsistent stochastic optimal control problem with objective (6a) and state process (7) the function defined in (53) solves the equilibrium HJB equation in Definition 2 in case that

| (54) |

Furthermore, the function is an equilibrium value function where is the unique positive solution of the equation and

| (57) |

is the equilibrium control according to Definition 1.

Proof.

We have to make sure that in (53) and in (57) satisfy the assumptions for the usage of Theorem 1. Using the explicit representation (57) we immediately observe that . Hence, we start with showing that in (53) together with (40), (41) and (42) solves the extended HJB equation. For that reason it is straightforward to insert into the equation (28) and observe that it is a solution (using (40) and (41)).

Further, using the assumption (54), Lemma 1 yields that there exists a unique positve such that (42) is fulfilled. Moreover, this gives that .

Using (28) at and yields that and . Together with (42), we obtain that is twice continuously differentiable. Summing up, we have that in addition to the fact that is twice continuously differentiable in .

Furthermore, we show that is concave for , i.e. .

First of all, we immediately observe that for , since and .

On the other hand, we have that

and since for , we obtain that for . This, together with , yields that for . This in turn implies for that . Since is twice continuously differentiable in we obtain . Finally, this yields that is concave.

We already know that for . Combining this with concavity, we obtain that for and for . On top of that, the function is strictly monotonically increasing since . For the case this holds because the first derivative is even larger than one. For we have the desired monotonicity from .

Altogether, the behaviour of the first and second derivatives of yields that, if this function fulfils the equation (28), it solves equations (12a) and (13a). On top of that is bounded in and , hence we have that (15) implies (14a) as mentioned in Remark 5. Since

for every fixed we have:

The last step, for verifying that and fulfil the requirements of the verification theorem, is to show that and its relevant derivatives are bounded. Since,

and is a constant, we obtain that the first derivative in is bounded. Furthermore, we observe, using and , that is bounded, and by building the respective derivatives that also and are bounded.

Altogether, we can apply Theorem 1 and obtain that is the equilibrium value function and is the associated equilibrium control.

∎

Analogous to Theorem 3 we can deal with the remaining parameter constellation.

Proposition 1.

Proof.

We proceed exactly in the same way as in the proof for Theorem 3. It can be verified that solves the equation (28) with . Furthermore, since and for all in addition to for all we obtain that

for all and . Hence, and fulfil (12a) and (13a). Moreover, is bounded and satisfies the correct boundary condition, which yields that it fulfils (14a). Finally, and it satisfies the extended HJB equation. Since , , and are all bounded in and , the requirements of Theorem 1 are fulfilled. Consequently, is the equilibrium value function and the associated equilibrium control. ∎

4.1 Parameter areas

The arising inequality in Theorem 3 splits the parameter space into different areas, such that this classification gives rise to an interpretation. First of all, we know that the classical dividend threshold is positive if which is equivalent to

| (58) |

see Schmidli (2008). Otherwise, if (58) is not fulfilled, we have that . Furthermore, note that by the properties of in (43) we obtain that the equilibrium dividend threshold fulfills . As a matter of fact, we obtain the following cases, which are also illustrated in Table 1.

-

1.

If (58) is fulfilled and , then we obtain also that . The condition (58) can be viewed as an advantageous parameter configuration which motivates the controller to take less risk and to payout dividends only at a surplus level larger than zero in order to prevent ruin for a longer time. The prospect is advantageous since the maximal reachable value of dividends (the right-hand side of (58)) is relatively large compared to the variance of the uncontrolled surplus divided by its mean (the left-hand side of (58)). Note that and . Moreover, we observe that if decreases, then the threshold level increases since one wants to prevent ruin and the associated larger penalty even more.

-

2.

Whereas if (58) is not fulfilled and hence , the future prospect is such that the controller in the classical problem () would pay out dividends at any surplus level. Especially if is negative, this strategy can be interpreted as the ruin strategy since ruin is certain in this case. But given that a penalty exists (), in case of ruin, we can distinguish the following two cases:

-

i)

If for

the impact of the penalty is too severe and we obtain that . This yields that dividends are paid out only for positive surplus levels as in the first case. We observe that the penalty in case of ruin has a stronger deterrent effect and therefore one wants to prevent ruin.

-

ii)

On the other hand, if meaning that the weight on the penalty is moderate, we obtain that also . In this case the penalty is not severe enough and the equilibrium strategy suggests to pay out dividends at any surplus level even if it is more likely that ruin occurs compared to the use of a positive threshold level.

-

i)

| if | ||

| if |

5 Meeting the constraint

In the following we discuss the motivating problem, i.e. dividend maximization including the constraint (4). We try to find a solution which fulfils the constraint for fixed , this means in a precommitment sense. Up to now we have found for every fixed an equilibrium threshold strategy and an associated value function. If

| (59) |

there exists a unique equilibrium threshold level for the associated time-inconsistent problem. If the equilibrium threshold is . Concerning (59) note that .

In the case , we observe from equation (43), , that if , tends to .

The factor next to is negative and consequently monotonically increasing in , so this term vanishes for .

The same holds true if and .

On the other hand, if and , equation (46), now , yields that , where is the classical threshold level.

Hence, we consider in the following . The case and can be analogously treated.

But, for and , we have for all that . Therefore, the ruin probability is one in this case.

This yields that the constraint cannot be fulfilled and the equilibrium threshold level coincides with the classical threshold level.

Focusing on the constraint (4), we can rewrite , which is constructed to solve (39),

| (60) |

For an arbitrary threshold level we define:

| (61) |

Here and is the process (7) with . A solution to equation (39), incorporating (40) and (41), for has the form . Hence, we have,

This can be seen using a Feynman-Kac type argument. According to (40) and (41), is continuously differentiable in . For the equilibrium threshold with , we have . On top of this, if , we obtain

from (5).

5.1 Determining the matching for

In the following, we can present two propositions which are based on Proposition 3.2 and Proposition 4.1 from [Hernández and Junca, 2015]. Certainly, our approach also covers the particular situation of . Therefore, we obtain similar results as in [Hernández and Junca, 2015], but for the diffusion model with bounded dividend rate.

Proposition 2.

Proof.

Since the relation between and the equilibrium threshold results from equation (43), we define for a given the corresponding value of to be

Where we have that

and

For these two functions we have that , , and .

Moreover, if , then , which in turn gives that .

Finally, this yields that and we obtain the first statement, since and for .

For the second statement let , we obtain that and since is monotonically decreasing, we get that for all . This along the lines of the classical dividend problem.

As before, we see that for all . This, in combination with and for , proves the second assertion.

∎

Remark 9.

For fulfilling the required constraint, we have to choose the pair dependent on the current state (setting ). This means that we have a solution of the constrained problem in a precommitment sense. This notion is well explained in [Delong, 2018]. Since we cannot fulfil the constraint for a finite if , we only consider the case . In the special case we are only able to meet the constraint if we never pay out dividends, which corresponds to a threshold at infinity.

Proposition 3.

For every given and every there exists a pair with and , such that is the equilibrium threshold level for (57) with parameter and further for this triple it holds that

| (62) |

and

| (63) |

Proof.

In the following we consider the different cases:

1.) with 1a) and 1b) ; on the other hand 2.) with 2a) and 2b) . Moreover, note that since we always have that .

Firstly, let and , then we can take the equilibrium threshold to be since the constraint is already fulfilled. Moreover, has to be zero, such that the second part of the objective function vanishes.

Since , all choices of yield an equilibrium threshold at level zero. Hence, we can take .

If , and consequently

we have that there exists a unique such that (remember ). Using Proposition 2, there exists a unique such that is an equilibrium threshold.

Secondly, if and , we have to take such that we can meet the constraint.

As before we can set since is the equilibrium threshold level for . On the other hand, if and hence

then there exists a unique such that . Due to Proposition 2, there exists a unique , such that is an associated equilibrium threshold. ∎

Since we have revealed an equilibrium control strategy and the associated equilibrium value function for the objective (6a), we cannot use the properties of a maximal reward function as in (2). Hence, standard duality statements do not apply.

We summarize our achievements as follows. For a given ruin constraint level we can identify the correct threshold level , such that the constraint (4) is fulfilled for a given initial state . Subsequently, we can specify a value , such that is the threshold level of an equilibrium control strategy (57) for the equilibrium value function as in (53).

Notice that the equilibrium threshold level and the associated is depending on the current state , in such a way that (62) and (63) for this is only fulfilled at .

In contrast to [Hernández and Junca, 2015], we only obtain one part of the analogous duality statements. Let be the equilibrium control for a problem with general parameter , and the corresponding equilibrium control such that the constraint for is fulfilled in

The last equality holds true, because the penalty term vanishes in for as in (63).

Remark 10.

The functions and defined in (60) and (61) characterize the evolution of the constraint, or more precisely, of the level . Suppose that the level , the initial surplus and the corresponding equilibrium strategy with threshold height are initially fixed. Then, at some point in time with , the constraint level

is reached for and original admissible strategy . From the Markov property we get that is an -martingale. Consequently, the strategy is the particular equilibrium control for which the constraint level is sharp if the process is restarted at . This means that the quality of the strategy is preserved if the constraint is adapted. The martingale property of shows that these adaptions are consistent over time.

5.2 Quality of the solution

As mentioned above we do not obtain classical duality results, nevertheless using our explicit form we are able to optimize within the class of threshold strategies. Namely, we can rewrite the constrained optimization problem

| (64) |

Using that is the maximizing argument of the classical problem, together with for all , we obtain for an arbitrary but fixed that (64) simplifies to

Whereas is defined as follows

| (65) |

Finally, the optimal threshold of the constrained problem will be this . Since and for all . Note, that the optimal threshold depends on the initial value . If the constraint cannot be fulfilled.

Recalling the proof of Proposition 3, we observe that our chosen equilibrium threshold of the penalized problem coincides with the optimal threshold . This just means that if , then we can take which is the optimal threshold of the constrained problem and . This yields .

If , then we take , which is again the optimal threshold in the constrained problem. In this case, we have to take for the penalized reward function such that corresponds to an equilibrium control, but for the initially fixed . Again we obtain by Proposition 3.

Note, that the constraint is only fulfilled for this initial and the penalized function will change for a different since is not zero and depends on . In the end, from (64) is optimal in the family of threshold strategies, but our analysis shows that for a certain it is also an equilibrium control from the general class of strategies for the time-inconsistent penalized problem.

On top of this, we have computed the optimal threshold for the penalized problem with fixed

| (66) |

The optimal threshold will depend on the initial and the solution is therefore in a precommitment sense.

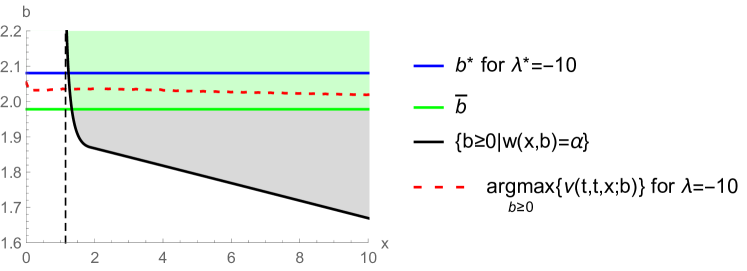

Altogether, we illustrate these findings in Figure 1, where the dashed red line corresponds to the -dependent optimal threshold of (66) for . Furthermore, in Figure 1 the green area is limited by the green line and by the black line which corresponds to those such that . Consequently, this boundary of the green area exactly equals our optimal threshold level as in (65) for different . We can observe that if is close to we cannot use anymore. Hence, we have to take a threshold which corresponds to the equilibrium threshold for a value . This is for example illustrated by the blue line for the value .

5.3 Concerning the ruin probability

As mentioned in Remark 8, if we send to zero, there are some differences depending on the relation between and .

The above procedure can be repeated, if we look at the limit to zero for .

But, if , the equation , see (46), does not depend on anymore. The second term in vanishes if tends to zero. This yields that for any , we obtain the same equilibrium threshold level, namely, the classical threshold . This is because for any finite threshold strategy, the ruin probability is one. Therefore, and .

Moreover, the classical threshold is the only reasonable solution, since the reward function differs only by a constant from the classical reward function in the time-consistent situation.

We are aware of the fact that the reward function could be increased by using a precommitment solution which takes account of the potentially high penalty and has therefore a ruin probability smaller than one. The drawback of such solutions is that one has to restrict (or even specify) the strategies in order to verify the desired optimality in that class of controls.

6 Graphical illustrations

In this short section we present a numerical example, which displays the dependence of the equilibrium threshold on the differing discount rate and the parameter . In the corresponding plots one nicely observes that the proposed type of duality considerations are highly legitimate.

6.1 The case

In the following, we consider the exemplary parameters displayed in Table 2.

| 2 | 1 | 0.1 | 1.9 | 0.5 |

|---|

If we do not vary and , we set and .

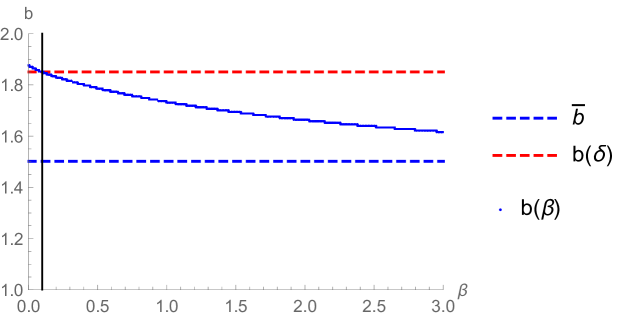

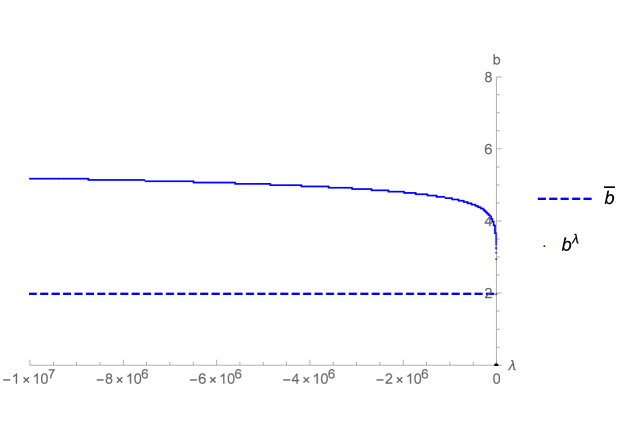

The change of the threshold, if we alter the underlying discount rate , is illustrated in Figure 2. We can observe that if we send to infinity the equilibrium threshold tends to the classical optimal threshold level .

Furthermore, we are able to reproduce the results from [Thonhauser and Albrecher, 2007], namely, in our setting we have to take besides , where denotes the constant in the penalty term of [Thonhauser and Albrecher, 2007]. The corresponding optimal control threshold is denoted by .

On the other hand, the dependence on for a fixed value of is depicted in Figure 3.

The behaviour of the equilibrium threshold for different values of is similar for positive and for the limit to zero.

Clearly, this is due to the fact that the equation still depends on if , as already mentioned in Remark 8.

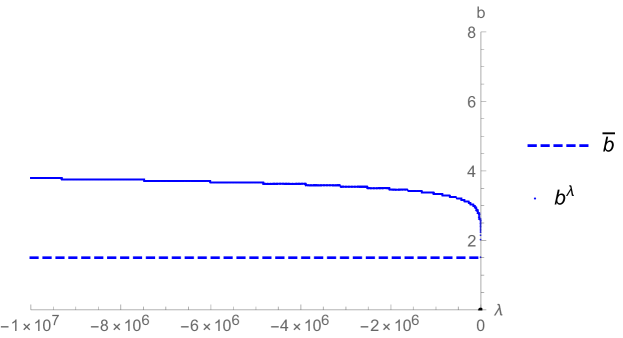

6.2 The case

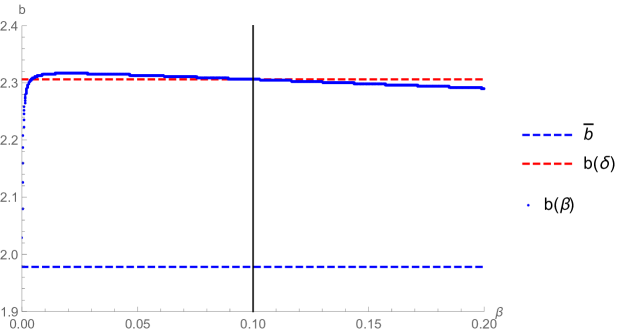

We consider again the parameters from Table 2 with the exception of . If we send to zero, we obtain that since the equation is independent of as can be seen in Figure 4. Moreover, this yields that the solution equals the classical threshold for all . As in the above case, the equilibrium threshold tends to the classical optimal threshold level for to infinity. Varying the value of and keeping constant, we obtain a similar behaviour as in the previous case, which can be observed in Figure 5. Furthermore, in Figure 5 (as in Figure 3 above) we notice that the equilibrium threshold increases very slowly if we decrease . In fact, the equilibrium threshold remains close to the classical threshold even for very small values of , in comparison to the other parameters. This indicates that, even for relatively small , the penalty in case of ruin is not deterrent enough to cause a high threshold level.

7 Conclusion

In this contribution we solve a time-inconsistent variation of the dividend maximization problem for a diffusion surplus process. This problem arises from imposing a constraint on the Laplace transform of the ruin time in the classical dividend problem. In order to include even a constraint on the ruin probability, we consider different discount rates in the dividend and the penalty term, which in fact leads to the time-inconsistency of the problem.

The presented verification theorem, which links an extended system of HJB-equations to an equilibrium dividend strategy and its value function, is applicable for state dependent diffusion coefficients. In the particular case of constant coefficients - the classical diffusion approximation - we are able to construct an explicit solution. This allows us to link the proposed reward function to the constrained dividend problem. In fact, we are able to fulfil the original constraint in a precommitment sense, i.e. for a given initial surplus level. Moreover, the reward function of the problem including a penalty coincides with the reward function of the classical dividend problem at this given initial surplus, since the penalty term vanishes.

Finally, the obtained equilibrium strategy is of threshold type, which is based on the restriction to Markovian controls and partly by the focus on an infinite time horizon.

This has the consequence that a constraint on the ruin probability itself can only be feasible if the drift term of the surplus process is larger than the maximal payout rate. Otherwise, the equilibrium is achieved by ignoring the constraint. In conclusion, the time-inconsistent approach allows us to assess the performance of a strategy in terms of an equilibrium over time.

8 Funding Information

This research was funded in whole, or in part, by the Austrian Science Fund (FWF) P 33317. For the purpose of open access, the author has applied a CC BY public copyright licence to any Author Accepted Manuscript version arising from this submission.

References

- [Asmussen and Taksar, 1997] Asmussen, S. and Taksar, M. (1997). Controlled diffusion models for optimal dividend pay-out. Insurance Math. Econom., 20(1):1–15.

- [Björk et al., 2017] Björk, T., Khapko, M., and Murgoci, A. (2017). On time-inconsistent stochastic control in continuous time. Finance Stoch., 21(2):331–360.

- [Christensen and Lindensjö, 2019] Christensen, S. and Lindensjö, K. (2019). Moment constrained optimal dividends: precommitment & consistent planning. Preprint.

- [Delong, 2018] Delong, Ł. (2018). Time-inconsistent stochastic optimal control problems in insurance and finance. Collegium of Economic Analysis Annals, (51):229–254.

- [Ekeland et al., 2012] Ekeland, I., Mbodji, O., and Pirvu, T. A. (2012). Time-consistent portfolio management. SIAM J. Financial Math., 3(1):1–32.

- [Ekeland and Pirvu, 2008] Ekeland, I. and Pirvu, T. A. (2008). Investment and consumption without commitment. Math. Financ. Econ., 2(1):57–86.

- [Grandits, 2015] Grandits, P. (2015). An optimal consumption problem in finite time with a constraint on the ruin probability. Finance Stoch., 19(4):791–847.

- [Hernández and Junca, 2015] Hernández, C. and Junca, M. (2015). Optimal dividend payments under a time of ruin constraint: exponential claims. Insurance Math. Econom., 65:136–142.

- [Hernández et al., 2018] Hernández, C., Junca, M., and Moreno-Franco, H. (2018). A time of ruin constrained optimal dividend problem for spectrally one-sided Lévy processes. Insurance Math. Econom., 79:57–68.

- [Hipp, 2003] Hipp, C. (2003). Optimal dividend payment under a ruin constraint: discrete time and state space. Blätter der DGVFM, 26(2):255–264.

- [Hipp, 2018a] Hipp, C. (2018a). Company value with ruin constraint in a discrete model. Risks, 6(1).

- [Hipp, 2018b] Hipp, C. (2018b). Company value with ruin constraint in Lundberg models. Risks, 6(3).

- [Hipp, 2020] Hipp, C. (2020). Optimal dividend payment in De Finetti models: survey and new results and strategies. Risks, 8(3).

- [Junca et al., 2019] Junca, M., Moreno-Franco, H. A., Pérez, J. L., and Yamazaki, K. (2019). Optimality of refraction strategies for a constrained dividend problem. Adv. in Appl. Probab., 51(3):633–666.

- [Karatzas and Shreve, 1991] Karatzas, I. and Shreve, S. E. (1991). Brownian Motion and Stochastic Calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition.

- [Kulenko and Schmidli, 2008] Kulenko, N. and Schmidli, H. (2008). Optimal dividend strategies in a Cramér-Lundberg model with capital injections. Insurance Math. Econom., 43(2):270–278.

- [Leobacher et al., 2015] Leobacher, G., Thonhauser, S., and Szölgyenyi, M. (2015). On the existence of solutions of a class of SDEs with discontinuous drift and singular diffusion. Electron. Commun. Probab., 20:no. 6, 14.

- [Lindensjö, 2019] Lindensjö, K. (2019). A regular equilibrium solves the extended HJB system. Oper. Res. Lett., 47(5):427–432.

- [Øksendal, 2000] Øksendal, B. (2000). Stochastic Differential Equations. Springer-Verlag Berlin Heidelberg. Fifth edition.

- [Schmidli, 2008] Schmidli, H. (2008). Stochastic Control in Insurance. Probability and its Applications (New York). Springer-Verlag London, Ltd., London.

- [Schmidli, 2017] Schmidli, H. (2017). Risk Theory. Springer Actuarial. Springer, Cham.

- [Shreve et al., 1984] Shreve, S. E., Lehoczky, J. P., and Gaver, D. P. (1984). Optimal consumption for general diffusions with absorbing and reflecting barriers. SIAM J. Control Optim., 22(1):55–75.

- [Thonhauser and Albrecher, 2007] Thonhauser, S. and Albrecher, H. (2007). Dividend maximization under consideration of the time value of ruin. Insurance Math. Econom., 41(1):163–184.

- [Wheeden and Zygmund, 1977] Wheeden, R. L. and Zygmund, A. (1977). Measure and Integral. Marcel Dekker, Inc., New York-Basel. An introduction to real analysis, Pure and Applied Mathematics, Vol. 43.

- [Yong, 2012] Yong, J. (2012). Time-inconsistent optimal control problems and the equilibrium HJB equation. Math. Control Relat. Fields, 2(3):271–329.

- [Zhao et al., 2014] Zhao, Q., Wei, J., and Wang, R. (2014). On dividend strategies with non-exponential discounting. Insurance Math. Econom., 58:1–13.

- [Zvonkin, 1974] Zvonkin, A. K. (1974). A transformation of the phase space of a diffusion process that will remove the drift. Math. USSR Sb., 22:129–149.