Actuarial-consistency and two-step actuarial valuations: a new paradigm to insurance valuation

Abstract

This paper introduces new valuation schemes called actuarial-consistent valuations for insurance liabilities which depend on both financial and actuarial risks, which imposes that all actuarial risks are priced via standard actuarial principles. We propose to extend standard actuarial principles by a new actuarial-consistent procedure, which we call “two-step actuarial valuations”. In the case valuations are coherent, we show that actuarial-consistent valuations are equivalent to two-step actuarial valuations. We also discuss the connection with “two-step market-consistent valuations” from Pelsser and Stadje (2014). In particular, we discuss how the dependence structure between actuarial and financial risks impacts both actuarial-consistent and market-consistent valuations.

Keywords: Fair valuation, two-step valuation, actuarial consistent, market consistent, Solvency II, incomplete market.

1 Introduction

Insurance liabilities, such as variable annuities, are complex combinations of different types of risks. Motivated by solvency regulations, the recent focus has been towards financial risks and the so-called market-consistent valuations. In this situation, the financial market is the main driver and actuarial risks only appear as the “second step”. This paper goes against the tide and introduces the concept of actuarial-consistent valuations where actuarial risks are at the core of the valuation. We propose a two-step actuarial valuation that is first driven by actuarial information and is actuarial-consistent. Moreover, we show that actuarial-consistent valuations can always be expressed as the price of an appropriate hedging strategy.

Fundamental to insurance, an actuarial premium principle (called actuarial valuation in this paper) is typically based on a diversification argument which justifies applying the law of large numbers (LLN) among independent policyholders who face identical risks (see Denuit et al., 2006). Consistent with insurance regulation, the actuarial valuation of a claim is represented as the expectation under the real-world probability measure plus an additional risk margin to cover any undiversified and systematic risk, that is

| (1.1) |

Financial valuation, on the other hand, is based on the no-arbitrage principal. Given the prices of the available traded assets, the value of a financial claim should be determined such that the market remains free of arbitrage if the claim is traded. Therefore, financial pricing is based on the idea of hedging and replication. It was shown in Delbaen and Schachermayer (2006) that no-arbitrage pricing implies that the prices of contingent claims can be expressed as expectations under a so-called risk-neutral measure , that is

| (1.2) |

This approach dates back to the seminal paper of Black and Scholes (1973).

Insurance claims are nowadays non-trivial combinations of diversifiable and undiversifiable insurance risk, and traded financial risks. It is therefore primordial to build a valuation framework which combines traditional actuarial and financial valuation. Over the last two decades, several researchers have worked on the interplay between financial and actuarial valuation. Embrechts (2000) offers a detailed comparison of insurance and finance pricing mechanisms. Møller (2002) addresses the aspects of the interplay between finance and insurance by combining traditional actuarial and financial pricing principles. A simplifying approach in the actuarial literature is to assume independence between actuarial and financial risks444This assumption is either made under the real-world measure or the risk-neutral measure . We note that the independence under does not necessarily imply the independence under ; see Dhaene et al. (2013). We also discuss this point in Lemma 3.3. such that the valuation can be split into a product of actuarial and financial valuations (see Fung et al., 2014; Da Fonseca and Ziveyi, 2017; Ignatieva et al., 2016; Wüthrich, 2016 among others). However, the emergence of longevity-linked financial products and the pandemic situation showed us that future mortality cannot be assumed independent from evolution of the financial market (Sharif et al., 2020, Harjoto et al., 2021). For this reason, different authors proposed general valuation approaches allowing for dependencies between actuarial and financial risks. For instance, valuation under dependent mortality and interest risks was investigated in Liu et al. (2014), Deelstra et al. (2016), Zhao and Mamon (2018). Moreover, Pelsser and Stadje (2014) proposed a ‘two-step market-consistent valuation’ which extends standard actuarial principles by conditioning on the financial information. Dhaene et al. (2017) proposed a new framework for the fair valuation of insurance liabilities in a one-period setting; see also Dhaene (2020). The authors introduced the notion of a ‘fair valuation’, which they defined as a valuation which is both market-consistent (mark-to-market for any hedgeable part of a claim) and actuarial (mark-to-model for any claim that is independent of financial market evolution). This work was further extended in a multi-period discrete setting in Barigou and Dhaene (2019) and in continuous time in Delong et al. (2019). A 3-step valuation was introduced in Deelstra et al. (2020) for the valuation of claims which consists of traded, financial but also systematic risks. This approach was further generalized in Linders (2021).

Market-consistent valuation and its shortfalls

The above-mentioned papers propose different valuation principles which have in common that they are all market-consistent valuations. The Solvency II insurance regulation directive introduced a prospective and risk-based supervisory approach on January 1, 2016. Pillar 1 of this directive requires a market-consistent valuation of the insurance liabilities; see e.g. Möhr (2011). A market-consistent valuation assumes an investment in an appropriate replicating portfolio to offset the hedgeable part of the liability. The remaining part of the claim is managed by diversification and an appropriate capital buffer. However, concerns about the appropriateness of the market-consistent valuation for long-term insurance business were raised:

-

•

Le Courtois et al. (2021) pointed out market-consistency can lead to a substantial misvaluation of the effective wealth of an insurance company that deals with long-term commitments. This approach also induces high instability and excess volatility in the balance sheet indicators of an insurance company (Vedani et al., 2017, Rae et al., 2018).

-

•

Plantin et al. (2008) found that the damage done by marking-to-market (that is market-consistency) is greatest when claims are illiquid and long term, which is precisely the case of balance sheet of insurance companies.

-

•

Market-consistency tends to be pro-cyclical and the use of a 1-year Value-at-Risk increases the risk of herd behaviour, hence reducing financial stability. Market-consistent valuation tends to minimise the value of liabilities when markets are bullish and over-estimate them in times of crisis (Rae et al., 2018).

Alternative valuations to market-consistency

The second pillar of the Solvency II directive allows the insurer to proceed to an alternative assessment of the company’s overall solvency needs using different recognition and valuation bases.

In this purpose, Le Courtois et al. (2021) replaced the market-consistent framework by a utility-consistent framework that accounts for the risk aversion of the market and the long-term nature of liabilities. The framework is not anymore market-consistent but market-implied and utility-consistent. The authors found that this alternative valuation provides less volatility than the traditional market-consistent approach. Muermann (2003) investigates the valuation of catastrophe derivatives and proposes an actuarial-consistent valuation approach that is consistent with existing insurance premiums to exclude arbitrage opportunities.

Why actuarial-consistency is an important alternative ?

In the spirit of Le Courtois et al. (2021), Muermann (2003), we introduce the class of actuarial-consistent valuations for hybrid claims as an alternative for the market-consistent valuations. This new valuation framework is motivated by the requirement that any actuarial claim (such as a pure endowment) should be priced via an actuarial valuation and should not be managed using a risky investment. We will label this property of the valuation “actuarial-consistency”. Such property plays an important role in life insurance where the development of the longevity market and the longevity-linked securities is growing in the recent years (Blake and Cairns, 2020). Indeed, in several countries, the valuation of the longevity risk is often required to follow regulatory life tables that impose minimum loadings for actuarial claims. Under a market-consistent setting, the presence of undervalued longevity-linked securities might create a potential undervaluation of life insurance business. Therefore, we believe it is relevant, for certain insurance claims, to investigate valuation mechanisms that are not market-consistent and would encourage risk-free investments rather than longevity transfers to the capital market.555As pointed out in Blake and Cairns (2020), the Prudential Regulatory Authority (regulatory authority for insurance companies in the UK) expressed concerns that too much longevity risk is transferred offshore so that if the offshore reinsurance firm failed, UK pensioners might not get their pensions.

We also introduce the two-step actuarial valuations. Instead of first considering the hedgeable part of the claim, the two-step actuarial valuation will first price the actuarial part of the claim using an actuarial valuation. We show that every two-step actuarial valuation is actuarial-consistent. Moreover, if the valuation is coherent, we show the reciprocal: any actuarial-consistent valuation has a two-step actuarial representation. The two-step valuations are general in the sense that they do not impose linearity constraints on the actuarial and financial valuations. Therefore, they allow to account for the diversification of actuarial risks and/or the incompleteness of the financial market (e.g. non-linear financial pricing with bid-ask prices).

Hedge-based valuations were first introduced in Dhaene et al. (2017) to define the market-consistent valuations. We show that actuarial-consistent valuations can always be expressed as hedge-based valuations. The hedging strategy used in an actuarial-consistent valuation will only invest in the risk-free asset when valuating an actuarial claim. This is in contrast with the market-consistent hedge-based valuations, which may use the financial market to hedge actuarial claims.

The paper also provides a detailed comparison between two-step market and two-step actuarial valuations. We discuss how the dependence structure between actuarial and financial claims impacts both actuarial and market-consistent valuations. In the context of solvency regulations, we show how the two-step actuarial valuation can be decomposed into a best estimate (expected value) plus a risk margin to cover the uncertainty in the actuarial risks. The procedure will be illustrated with a portfolio of life insurance contracts with dependent financial and actuarial risks.

The rest of the paper is structured as follows. In Section 2, we describe financial and actuarial valuations. Section 3 discusses the notion of actuarial-consistency and introduces two-step actuarial valuations. In Section 3.3, we provide a detailed comparison between actuarial-consistent valuations and market-consistent valuations. Section 4 presents a cost-of-capital valuation based on the two-step actuarial valuation and a detailed numerical application of the two-step actuarial valuation on a portfolio of equity-linked contracts. Section 5 concludes the paper.

2 Actuarial and financial valuations

All random variables introduced hereafter are defined on the probability space . Equalities and inequalities between r.v.’s have to be understood in the -almost sure sense. The space of bounded random variables is denoted by or for short. A contingent claim is a random liability of an insurance company that has to be paid at the deterministic future time . Formally, a discounted claim is modeled by the random variable . In what follows we are interested in the valuation of discounted claims.

Suppose a -algebra is the information available to the agent. We define a -conditional valuation as follows.

Definition 2.1 (-conditional valuation)

A -conditional valuation is a mapping satisfying the following properties:

-

•

Normalization: .

-

•

Translation-invariance: For any and , we have

-

•

Convexity: For any and with , we have

-

•

Positive homogeneity: For any and any positive , we have

Note that if is chosen to be the trivial -algebra, then is a real number and we simply write the valuation without conditioning on .

Apart from the properties in Definition 2.1, other properties that a valuation may have are

-

•

Monotonicity: for any , if .

-

•

Fatou property: for , , and , then

Coherent valuations (also known as coherent risk measures) can be understood as a worst-case expectation with respect to some class of probability measures. This can be motivated by the desire for robustness: the valuator does not only want to rely on a single measure for the occurrence of future events but prefers to test a set of plausible measures and value with the worst-case scenario. A few dual representations of coherent valuations are available in the literature. Here we present the most popular version, which is defined for bounded random variables on a general space; see e.g. Delbaen and Biagini (2000).

Definition 2.2 (Coherent valuation)

A coherent valuation with Fatou property has the following representation for any

where is a collection of probability measures absolutely continuous w.r.t. .

In general, one can show that the set of coherent valuations is positive homogeneous, translation-invariant, subadditive and monotone, see e.g. Artzner et al. (1999).

Coherent valuations are linear valuations in the following sense.

Definition 2.3 (Linear valuation)

A valuation is linear, if there exists a finitely additive measure absolutely continuous w.r.t. , , such that for any

In this paper, we assume risks can be divided in two groups: financial and actuarial risks. Then a hybrid discounted claim is a combination of both the actuarial as well as the financial risks. The financial risks are traded on a public exchange and market participants can buy and sell these financial risks at any quantity. The non-traded risks are referred to as actuarial risks. We note that a similar split was considered in Wüthrich (2016) between financial events (stocks, asset portfolio, inflation-protected bonds, etc) and insurance technical events (death, car accident, medical expenses, etc). Moreover, we remark that the issue of insurance-linked securities (e.g. longevity bonds) implies that a non-traded actuarial risk may become a traded financial risk.

2.1 Financial Valuation

We assume there is a financial market with traded assets and denote by the price process of assets, where is the risk-free asset assumed to be constant and equal to . We also refer to the traded assets as financial risks. The -algebra generated by the financial risks is denoted by .

A financial claim is an -measurable random variable defined on the financial probability space. Otherwise stated, a financial claim only depends on the financial risks and its realization is completely known given the realization of the financial risks . The set of all discounted financial claims is denoted by . We can always express a discounted financial claim as a function of the financial risks. We have:

| (2.1) |

for some function 666We assume that all functions we encounter are Borel measurable..

The financial risks are traded on the financial market and all market participants can observe the prices at which each asset can be bought and sold. Note, however, that we do not assume that the price at which one can buy and sell at time is equal. We assume that a financial valuation principle is available to determine the price at which one can buy the traded payoffs:

The choice of the financial valuation principle depends on the additional assumptions we impose on the financial market. Traditional financial pricing assumes that the market is complete and arbitrage-free such that the pricing rule is linear and unique (Black and Scholes, 1973). However, the existence of transaction costs and non-hedgeable payoffs lead to non-linear and non-unique valuations. In such situations, the market will decide which valuation principle is used and one has to use calibration to back out the valuation principle from the available traded assets. Below, we consider different possible choices for the financial valuation for different market situations.

-

1.

The law of one price. Assume the market is arbitrage-free, frictionless and that all financial assets are discretely traded in the market and can be bought and sold at a unique price. One can prove that in this market setting, the no-arbitrage condition is equivalent with the existence of an equivalent martingale measure (EMM) (Dalang et al., 1990). In this financial market where one can buy and sell any asset at a unique price, the financial valuation principle can be determined as follows:

The financial valuation is in this situation a linear valuation principle.

-

2.

Imperfect market and bid-ask prices. In classical finance, markets are usually modelled as a counterparty for market participants. It is assumed that markets can accept any amount and direction of the trade (buy or sell) at the going market price. However, due to market imperfection, there is in practice a difference between the price the market is willing to buy (bid price) and the price the market is willing to sell (ask price). This difference, called the bid-ask spread, creates a two-price economy. In particular, the value which corresponds with the price required by the market to take over the financial claim will typically be higher than the risk-neutral price. Indeed, the asymmetry in the market allows that market to take a more prudent approach when determining the price . Instead of using a single risk-neutral probability measure, a set of ”stress-test measures” is selected from the set of martingale measures and the price is determined as the supremum of the expectations w.r.t. the stress-test measures:

where is a convex set of probability measures absolutely continuous with respect to the original probability. For more details on conic finance, we refer to Madan and Cherny (2010) and Madan and Schoutens (2016).

In the remainder of the paper, we consider coherent financial valuations to account for bid-ask spread and market imperfections.

2.2 Actuarial valuation

Suppose there are non-traded risks (also called actuarial risks) which we denote by the price process of the actuarial risks. The -algebra generated by is denoted by .

An actuarial claim is a -measurable random variable defined on the actuarial probability space. Equivalently stated, an actuarial claim only depends on and its realization is completely known given the realization of the actuarial risks . If we denote the set of discounted actuarial claims by , we can write any discounted claim as a function of the actuarial risks:

for some function .

We assume that a valuation principle is chosen to price actuarial claims. The actuarial valuation principle is based on the idea of pooling and diversification. A completely diversifiable portfolio can be valued with its expectation under the physical measure . However, there is always an amount of residual actuarial risk present because one cannot aggregate an infinite amount of policies. Moreover, there are also systematic actuarial risks (e.g. longevity risk) which cannot be diversified away. Indeed, aggregating a large number of systematic risks will not result in the desired risk reduction. For this reason, actuarial valuations include a risk margin to cover any non-diversifiable risk. Below, we briefly discuss the most important actuarial valuation principles (also called actuarial premium principles).

-

1.

Linear valuation:

The risk margin is modelled by an appropriate change of measure from to . In terms of life tables, the change of measure can be interpreted as a switch from the second order life table (best-estimate survival or death probabilities) to a first order life table (survival or death probabilities that are chosen with a safety margin). For more details, see for instance Wüthrich (2016) and Norberg (2014).

-

2.

Standard deviation principle:

(2.2) with .

In this case, the loading equals times the standard deviation. It is well-known that is required in order to avoid getting ruin with probability 1 (see e.g. Kaas et al. (2008)). We note that the standard deviation principle is neither linear nor coherent. -

3.

Coherent valuation:

where is a coherent valuation. We recall that the coherent valuation can also be represented as a supremum of a set of measures (see Definition 2.2). Therefore, model risk can be taken into account by considering a family of different distributions and the actuarial claim is valuated with the most conservative one.

2.3 Hybrid claims

Recall that a claim is defined on the probability space , which is a combination of the financial and the actuarial probability space. The -algebra contains and . That is .

Assume the valuation is used to valuate discounted claims in . A general claim in can contain both financial and actuarial risks and therefore the valuation of claims in cannot be solely based on the financial or the actuarial valuation principles. Moreover, the financial and actuarial risks are dependent. Therefore, observing the values of financial (resp. actuarial) claims can provide information about the valuation of actuarial (resp. financial) claims.

Define by the set of financial claims which are independent of the actuarial risks and by the actuarial claims which are independent of the financial information:

We say that is a pure financial claim, whereas is called a pure actuarial claim. A pure financial claim does not contain any information about the actuarial risks and therefore the actuarial valuation should not be used to valuate a pure financial claim. Hence, the valuation of a pure financial claim should only involve the financial valuation . Similarly, the valuation of a pure actuarial claim should only be based on the actuarial valuation . We require that the valuation principle is consistent with the financial valuation and the actuarial principle in that should correspond with financial valuation for pure financial claims and with the actuarial valuation when considering pure actuarial claims.

Definition 2.4 (Orthogonal-consistency)

A valuation is said to be orthogonal consistent with the financial valuation and the actuarial valuation if we have that for ,

| (2.3) |

We will show later that the two-step actuarial valuation introduced in this paper is orthogonal consistent with the financial and actuarial valuations.

Similar to Dhaene et al. (2017), a hybrid claim is a claim which depends on both the actuarial as well as the financial information, i.e. a hybrid claim can be expressed as follows:

Different valuation frameworks can be considered depending on how financial and actuarial valuations are merged together. In Section 3, we propose a two-step valuation which applies a financial valuation after conditioning on actuarial information. For this reason, we briefly introduce the concept of conditional valuations hereafter.

3 Actuarial-consistent valuations

Given a financial valuation principle and an actuarial valuation principle , we search for general valuations that are consistent with both the financial valuation and the actuarial valuation , and study their properties.

This section starts with introducing the concept of actuarial-consistency. Condition (2.3) for a valuation states that actuarial claims which are independent of the financial information, should be valued using the actuarial valuation principle . A valuation is actuarial-consistent if all actuarial claims are priced with an actuarial valuation, even the ones that may be dependent to financial information.

Definition 3.1 (Actuarial-consistency)

A valuation is called actuarial consistent (ACV) with an actuarial valuation if for any actuarial claim the following holds:

| (3.1) |

Actuarial consistency postulates that an actuarial valuation is applied for all actuarial claims. Note that actuarial consistency is stronger than condition (2.3), which only states that independent actuarial claims are priced using the actuarial valuation. In Dhaene et al. (2017), the authors define a similar notion of actuarial consistency, but the condition only holds for the claims which are independent of the financial filtration .

In this section we define two new classes of actuarial-consistent valuations. The first class are the actuarial hedge-based valuations and the second class are the two-step actuarial valuations.

3.1 Actuarial hedge-based valuations

In this section we consider a one-period setting, where we value a claim at time and determine a corresponding risk management strategy.

We start with introducing the class of actuarial-consistent hedgers. In Dhaene et al. (2017), the authors showed that any market-consistent valuation can be represented as the time-0 value of a market-consistent hedger in a one-period setting. This result was further generalized in Barigou and Dhaene (2019), Chen et al. (2021). Similarly, in this section, we establish the relationship between actuarial-consistent valuations and their corresponding hedgers.

A trading strategy is a real-valued vector where the component denotes the number of units invested in asset at time until maturity with the asset 0 is the risk-free asset with constant interest rate . We denote the set of all these static trading strategies by .

Definition 3.2

A hedger is a function which maps a claim into a trading strategy and satisfies the following conditions

-

1.

is normalized: .

-

2.

is translation invariant: , for any and

The trading strategy is called the hedge for the claim . Now, we define the class of actuarial-consistent hedgers.

Definition 3.3

A hedger is said to be an actuarial-consistent hedger if there exists a valuation such that

An actuarial-consistent hedger will only allow investments in the risk-free bank account for actuarial claims. The higher potential returns in risky assets can be used to protect against the future losses from a claim. However, when an investment in risky assets is used for managing an actuarial claim, the insurer will be exposed to movements on the financial market. By considering actuarial-consistent hedgers, the insurer only adds risky investments to the portfolio if the claim he is trying to hedge contains financial risks.

Example 1 (Actuarial-consistent hedgers)

Hereafter, we consider two examples of actuarial-consistent hedgers.

-

1.

Consider the hedger such that

where is the financial risks defined in subsection 2.1 and is the set of all hedging strategies, that is the set of all - dimensional real-valued vectors. Such hedger invests risk-free for actuarial claims and invests following quadratic hedging for all remaining claims. By construction, such hedger is actuarial consistent. For details on risk-minimizing strategies for insurance processes, we refer to (Møller, 2001, Delong et al., 2019).

-

2.

Assume that an insurer considers the two-step actuarial valuation for any claim :

where is an -conditional valuation and is an actuarial valuation.

If the insurer invests the whole value in risk-free asset, the following hedger is used:

(3.2) Such hedger is naturally an actuarial-consistent hedger.

In the following lemma, we show how one can decompose a hybrid claim into an actuarial and financial part and define an actuarial-consistent hedger.

Lemma 3.1

Consider a hybrid claim and a hedger . We decompose the claim into two parts as follows:

Note that . Define the hedger as follows:

Then, is an actuarial hedger.

Proof. Consider an actuarial claim . Then is measurable and therefore and . Since a hedger is translation invariant, we then find:

which shows we have an actuarial-consistent hedger.

Lemma 3.1 illustrates how one can derive an actuarial-consistent hedger using a general hedger. The claim can be interpreted as the actuarial part of the claim .

Assume that we have a claim and a hedger . If we want to invest in the hedge , we have to pay its time- value which is given by . In the next lemma, we show that the resulting financial value is actuarial consistent if the hedger is actuarial consistent.

Lemma 3.2

The following two statements are equivalent.

-

1.

The valuation can be expressed as follows

(3.3) where is an actuarial-consistent hedger.

-

2.

is actuarial consistent.

Proof. Assume is an actuarial-consistent hedger and the valuation is given by (3.3). Then for any actuarial claim , we have that . Taking into account , we find that is actuarial consistent. Assume now that is an actuarial-consistent valuation. Defining as in (3.2) shows that where is an actuarial-consistent hedger.

In order to determine a hedge-based value of one first splits this claim into a hedgeable claim, which (partially) replicates , and a remaining claim. The value of the claim is then defined as the sum of the financial value of the hedgeable claim and the actuarial value of the remaining claim, determined according to a pre-specified actuarial valuation.

Definition 3.4

A valuation is called an actuarial hedge-based valuation with financial valuation and actuarial-consistent valuation if it can be expressed as follows:

where is an actuarial-consistent hedger.

In the following theorem, we prove that the class of actuarial-consistent valuations is equal to the class of actuarial hedge-based valuations.

Theorem 3.1

A valuation is an actuarial-consistent valuation if, and only if, it is an actuarial hedge-based valuation.

Proof. Assume is an actuarial hedge-based valuation, i.e. we have that

where is an actuarial hedger. Consider an actuarial claim . Then

for some actuarial valuation . Then it is straightforward to verify that

which shows that an actuarial hedge-based valuation is a actuarial-consistent valuation.

Assume now that is an actuarial-consistent valuation. Then it follows from Lemma 3.2 that

where . Define the valuation as follows:

Then is an actuarial hedge-based valuation. Moreover, since , we also find that , which ends the proof.

We remark that all the results in this subsection are satisfied for general valuations that are only normalized and translation-invariant. Positive homogeneity and convexity properties, which are assumed for a valuation in Definition 2.1, are not necessary for the equivalence result of Theorem (3.1) to hold.

3.2 Two-step actuarial valuations

Hereafter, we introduce a class of actuarial-consistent valuations which we call two-step actuarial valuations. More specifically, in a first step we compute the financial value of conditional on actuarial scenarios (the values of the actuarial assets ), i.e. . Since this conditional payoff depends only on actuarial scenarios and is then -measurable, in the second step the quantity should be valuated via a standard actuarial valuation . We remark that the two-step actuarial valuation is the reversed version of the two-step market valuation of Pelsser and Stadje (2014), where financial and actuarial valuations are applied in different orders. We will show in Lemma 3.3 that under strong assumptions, both valuations lead to the same result.

Definition 3.5 (Two-step actuarial valuation)

The valuation is called a two-step actuarial valuation if there exists an -conditional valuation such that

| (3.4) |

where is an actuarial valuation.

Hence, the two-step actuarial valuation consists of applying the market-adjusted valuation to the residual risk which remains after having conditioned on the future development of the actuarial risks, i.e. . It is straightforward to verify that the two-step actuarial valuation is orthogonal consistent.

Example 2

As an example of a two-step actuarial valuation, we note that Møller (2002) proposed a modified version of the standard deviation principle:

| (3.5) |

which corresponds to applying the traditional standard deviation principle to the no-arbitrage price of conditional on the actuarial filtration (see Equation (5.5) in Møller (2002)).

In the following theorem, we show that any two-step actuarial valuation is actuarial-consistent. Moreover, if the valuation is coherent, we provide a characterization of the two-step actuarial valuation.

Theorem 3.2 (Characterization of actuarial consistency)

The following properties hold:

-

1.

Any two-step actuarial valuation is actuarial-consistent.

-

2.

If is a coherent and actuarial-consistent valuation with a linear actuarial valuation , then there exists an -conditional coherent valuation such that for any ,

where

with .

Proof. (1) To prove that is actuarial consistent, it is sufficient to notice that for any ,

where we have used that is -measurable.

(2) Because is coherent, we have that

Since is linear, there exists such that

By the same arguments in the proof of Proposition 3.3 of Pelsser and Stadje (2014), we can decompose as with . Thus

Now we define . It is straightforward to verify that is a -conditional valuation. All we are left to show is

This can be proved using the same arguments in the proof of Theorem 3.10 of Pelsser and Stadje (2014).

Corollary 3.1

The following holds:

-

1.

Any two-step actuarial and any actuarial hedge-based valuation is actuarial-consistent.

-

2.

Any actuarial-consistent valuation is an actuarial hedge-based valuation.

3.3 Comparisons of two-step actuarial valuation and two-step financial valuation

Motivated by solvency regulations, the recent actuarial literature focused on market-consistent valuations which essentially require that financial risks are priced with a risk-neutral valuation. In this section, we provide a detailed comparison between actuarial-consistent and market-consistent valuations.

Definition 3.6 (Strong market-consistency)

A valuation is called strong market-consistent (strong MCV) if for any financial claim the following holds:

| (3.6) |

In the literature, market-consistency is usually defined via a condition identical or similar to the condition (3.6) (see e.g. Pelsser and Stadje (2014), Dhaene et al. (2017) and Barigou et al. (2019)). When the financial valuation is linear, Proposition 3.3 of Pelsser and Stadje (2014) shows that the strong market-consistency is equivalent to the following weak market-consistency.

Definition 3.7 (Weak market-consistency)

A valuation is called weak market-consistent (weak MCV) if for any financial claim the following holds:

| (3.7) |

We remark that Assa and Gospodinov (2018) also investigated these two types of market-consistency, that they called market-consistency of type I and type II.

Following the definition of the two-step market valuation in Pelsser and Stadje (2014), we define the class of two-step financial valuations.

Definition 3.8 (Two-step financial valuation)

The valuation is called a two-step financial valuation if there exists an -conditional valuation such that

where is a financial valuation.

After having defined two broad classes of two-step valuations: market-consistent and actuarial-consistent valuations, a natural question arises: Could we always define a fair valuation that is market-consistent and actuarial-consistent?

Definition 3.9 (Fair valuation)

A two-step valuation is fair if it is weak market consistent and actuarial consistent.

In general, it will not always be possible to define a fair valuation. Indeed, in a general probability space in which financial and actuarial risks are dependent, there is ambiguity on the valuation to be used: a market-consistent valuation calibrated to market prices or an actuarial-consistent valuation calibrated to historical actuarial data.

In the following lemma, we show that when financial risks and actuarial risks are independent, then the two-step financial valuation and the two-step actuarial valuation coincide.

Lemma 3.3

Assume that and are independent and for any it can be expressed as with and . If a two-step valuation with a linear second step valuation is a fair valuation, then

where and .

Proof. Since is actuarial consistent with a linear second step actuarial valuation, there exists a -conditional valuation such that

where in the second step we used the positive homogeneity of and the last step is due to the independence of and . Because is also weak market consistent, we have

Then the desired result follows.

With the emergence of the market for longevity derivatives, a valuator needs to make a choice between market-consistency and actuarial-consistency. For instance, consider a market with some traded longevity bonds and there is an issue of a new longevity product. One needs to decide to use either a market-consistent approach based on the traded longevity bonds in the market or an actuarial-consistent approach based on longevity trend assumptions.

In the following example, we illustrate this point and compare a market-consistent and an actuarial-consistent valuation in the presence of a longevity bond. In particular, we compare the following two valuations: for any , we define

| (3.8) | ||||

| (3.9) |

Here for simplicity, we abuse the notation a little. In (3.8), the conditional valuation is in fact for some . That is in (3.8) is an absolutely continuous probability measure with respect to conditional on . In (3.9), is an absolutely continuous probability measure with respect to in the usual sense; that is for some . in (3.8) is the usual actuarial valuation defined on while in (3.9) is a conditional valuation defined on sharing similar structure with . For example, if , then .

Example 3 (Comparison between MCV and ACV)

(a) Consider a portfolio of pure endowments for Belgian insureds of age at time . The pure endowment guarantees a sum of 1 if the policyholder is still alive at maturity. The aggregate payoff can be written as

with the number of policyholders who survive up to the maturity time . Moreover, we assume that the financial market is composed of two assets: a risk-free asset and a longevity bond for which the payoff at maturity is , the equivalent of but for the Dutch population. First, we determine the value by the two-step actuarial valuation:

The actuarial-consistent valuation would suggest a full investment in the risk-free asset. Secondly, assuming that the Belgian population live slightly shorter than the Dutch population777For the reader interested in Dutch and Belgian mortality projections, we refer to Antonio et al. (2017): with , we determine the value according to the two-step financial valuation:

where is the current price of the longevity bond. The market-consistent valuation would then suggest a full investment in the Dutch longevity bond.

(b) In order to better grasp the difference between the actuarial-consistent and market-consistent valuations, we introduce the following modelling assumptions.

Assume that the interest rate , and the bivariate Belgian-Dutch population follows the distribution: with

Hence, both Belgian and Dutch populations are normal distributed with correlation . Hereafter, we compare the two-step actuarial and financial valuations given by

| (3.10) | ||||

| (3.11) |

where is the standard deviation principle (2.2) and is the conditional standard deviation principle:

The two-step actuarial valuation of is given by

| (3.12) |

To determine the two-step financial valuation, we first notice that by standard results of normal distributions, we have

Let us further assume that the distribution of under is

where is the market price of risk for the longevity bond. Therefore, we find that

| (3.13) |

We can compare the two-step actuarial valuation (3.12) with the two-step financial valuation (3.13). Intuitively, the difference should reflect two aspects:

-

1.

The dependence between Belgian and Dutch populations.

-

2.

The risk premium on the Dutch longevity bond.

The results confirm the intuition: the difference is given by

| (3.14) |

We observe that the higher the correlation , the higher the difference (this reflects the point 1.). Moreover, the absolute difference is an increasing function of the market price of risk (this reflects the point 2.).

If the valuator can choose between the risk-free investment or the Dutch longevity bond, he will go for the longevity bond if the benefits are higher than the costs, i.e. if the risk reduction of investing in the longevity bond is higher than the extra price he has to pay (given by Equation (3.14)). The prices at time of both approaches and the residual losses at maturity are given in the table below:

From the table, we observe that the investment in the longevity bond leads to a decrease in the volatility of the residual loss but an increase in the expected loss. Notice that in case of comonotonic or countermonotonic risks (i.e. ), the claim can be completely hedged with the longevity bond and the residual loss equals 0. The valuator will typically go for the longevity bond if the risk reduction (computed in terms of Value-at-Risk for simplicity) is higher than the extra price to pay:

On the other hand, if the longevity bond price is too high in comparison with the risk reduction, an actuarial-consistent valuation is then preferable.

Remark 3.3

In this paper, we do not argue that one method is better than another; each one has pros and cons. While the second method allows to transfer the risk to the financial market, it comes also with a price: the liabilities become totally dependent on the longevity bond. In particular, an adverse shock on the Dutch population or a counter-party’s default will have a direct effect on the assets backing the liabilities.

More generally, as pointed out by Vedani et al. (2017), market-consistent valuations are directly subject to market movements, and can lead to excess volatility, depending on the calibration sets chosen by the actuary. We also refer to Rae et al. (2018) for different concerns around the appropriateness of market-consistency to the insurance business.

In the next example, we consider the valuation of a hybrid claim via a two-step financial and actuarial valuation, and investigate the difference between the two-step operators.

Example 4 (Two-step valuations for hybrid claims)

Consider an equity-linked contract for a life , which pays the call option in case the policyholder is alive at time and 0 otherwise. We recall that the stock can go up to 200 or down to 50, the strike and the policyholder survival is modelled by the indicator . Therefore, the payoff of this contract is given by

| (3.15) |

Similar to Example 3, we consider the two-step financial and actuarial valuations given by Equations (3.10) and (3.11) for the hybrid payoff (3.15):

-

1.

Two-step financial valuation: The value of is given by

If we note that

then we find that the two-step financial value of is

(3.16) where is the -probability that goes up: and is the -probability that the policyholder is alive given that the stock goes up: .

-

2.

Two-step actuarial valuation: The value of is given by

Noting that

then we find that the two-step actuarial value of is

(3.17) where is the -probability that the policyholder is alive: and is the -probability that the stock goes up given that the policyholder is alive: .

If we compare the two-step financial and actuarial values (3.16) and (3.17), the structure is similar but the dependence between financial and actuarial risks is taken into account differently. In the first case, it is via the -probability of actuarial risks given financial scenarios, i.e. while in the second case, it is via the -probability of financial risks given actuarial scenarios, i.e. . In case of independence under and , both valuations are equal. In case of dependence, both valuations (3.16) and (3.17) will in general be different as we illustrate below:

Let us further assume that the difference between and is given by a constant market price of risk :

Therefore, by Bayes’ Theorem, we find that

After simplifications, we find that

Similar to Example 3, we observe that the difference between the two-step valuations relies mainly on

-

•

The risk premium which reflects the difference between the real-world measure and the risk-neutral measure .

-

•

The dependence between actuarial and financial risks (expressed as the difference between and as well as the difference between and ).

We remark that in the literature, it is common to assume that financial and actuarial claims are independent (either under or 888Note that independence under does not necessarily imply independence under , see Dhaene et al. (2013).). In that case, one can define a valuation that is MCV and ACV since the valuation is decoupled into two independent valuations, one for financial claims and one for actuarial claims. Even though extracting the -dependence might be more complicated, different papers investigated the valuation under dependent financial and actuarial risks (see e.g. Liu et al., 2014, Deelstra et al., 2016, Zhao and Mamon, 2018).

Example 4 (continued)

If we assume independence under in the two-step financial valuation or independence under in the two-step actuarial valuation, both valuations lead to a fair valuation. This is in line with Lemma 3.3.

4 Cost-of-capital valuation based on the two-step actuarial approach

Based on the two-step actuarial valuation introduced in Section 3, we show how we can define a cost-of-capital valuation as a sum of a best estimate and a risk margin, different but in the same spirit as solvency regulations. Moreover, we illustrate such valuation on a portfolio of equity-linked life insurance contracts with dependent financial and actuarial risks in Section 4.2.

4.1 Best estimate, risk margin and cost-of-capital valuation

4.1.1 Best estimate

In Article 77 of the DIRECTIVE 2009/138/EC (European Commission (2009)), the best estimate is defined as the “the probability-weighted average of future cash-flows taking account of the time value of money” (expected present value of future cash-flows). Hence, the best estimate of an insurance liability can be interpreted as an appropriate estimation of the expected present value based on actual available information.

Based on our two-step actuarial valuation, we can define a broad notion of best estimate for a general claim . Indeed, one can then generate stochastic actuarial scenarios, determine the financial price in each scenario and then average over the different scenarios. This leads to the following definition.

Definition 4.1 (Best estimate)

For any claim , the best estimate is given by

| (4.1) |

where is an absolutely continuous probability measure with respect to conditional on .

It turns out that the best estimate appears as a two-step actuarial valuation for which there is no distortion of the different measures, i.e. and . In general, the expression (4.1) could be hardly tractable since we can possibly have an infinite number of actuarial scenarios. For practical purposes, we will often consider the approximated best estimate defined by

| (4.2) |

for a finite number of actuarial scenarios: .

The best estimate in Equation (4.1) appears as an average of risk-neutral valuations which are applied to the risk which remains after having conditioned on the actuarial filtration. Hereafter, we consider some special cases:

-

•

For any actuarial risk , we find that

-

•

For any product claim with independent actuarial and financial risks (under ), we find that

(4.3) Hence, the actuarial risk is priced via real-world expectation and the financial risk via risk-neutral expectation. In fact, for the Equation (4.3) to hold, it is sufficient that the financial claim is independent from the actuarial filtration .

4.1.2 Risk margin

In order to motivate the risk margin, we recall that the best estimate is centered around the risk

This risk represents the risk-neutral financial price of conditional on the actuarial information. Looking at the tail of this (actuarial) risk will provide information on the actuarial scenarios which yield the worst financial price. Hence, applying an actuarial valuation on this conditional financial price allows to measure the impact of the actuarial uncertainty on the risk-neutral price. This motivates the following definition.

Definition 4.2 (SCR for actuarial risk)

For any claim and any actuarial valuation , the SCR for actuarial risk is given by

| (4.4) |

It turns out that the SCR appears as a two-step actuarial valuation for which we deducted the best estimate. If the valuation is coherent, thanks to the representation theorem (see Theorem 2.2), the SCR for actuarial risk can be represented as

where the supremum is taken over a set of probability measures absolutely continuous to . Hence, the SCR for actuarial risk can be interpreted as a worst case scenario: we can consider a family of stressed actuarial models (e.g. different mortality dynamics) and define the SCR as the value under the worst-case model.

4.1.3 Cost-of-capital valuation of insurance liabilities

In Solvency II, the fair value of insurance liabilities is defined as the sum of the best estimate and the risk margin in which the latter is defined as the cost of capital needed to cover the unhedgeable risks.

In the spirit of regulatory directives, we define a cost-of-capital valuation (CoC valuation) based on our two-step actuarial valuation. This CoC valuation is defined as the sum of the best estimate (expected present value) plus the risk margin (cost to cover unhedgeable risks) where the latter represents the cost of providing the SCR for actuarial risk. For a general overview of the cost-of-capital approach, we refer to Wüthrich and Merz (2013) and Möhr (2011).

Definition 4.3 (Cost-of-capital valuation)

For any claim and any actuarial valuation , the cost-of-capital value of is defined by

| (4.5) |

with

where is the cost-of-capital rate and stands for the SCR for actuarial risk.

4.2 Numerical application: Portfolio of GMMB contracts

In this subsection, we show how to determine the cost-of-capital value (4.5) for a portfolio of guaranteed minimum maturity benefit (GMMB) contracts underwritten at time on persons of age . In particular, we detail the numerical procedure for the best estimate and the SCR for actuarial risk. Moreover, we compare the fair valuation with the setting of Brennan and Schwartz (1976) in which complete diversification of mortality is assumed.

The GMMB contract offers at maturity the greater of a minimum guarantee and a stock value if the policyholder is still alive at that time. Let be the remaining lifetime of insured at contract initiation. The payoff per policy can be written as

| (4.6) |

with

Here, is the number of policyholders who survived up to time and is the value of the stock at time .

We consider a continuous time setting for the stock and the force of mortality dynamics. Let us assume that the dynamics of the stock process and the population force of mortality are given by

| (4.7) | ||||

| (4.8) |

with and are positive constants, and . Here, and are independent standard Brownian motions. The specification of a non-mean reverting Ornstein-Uhlenbeck (OU) process (4.8) for the mortality model allows negative mortality rates. However, Luciano and Vigna (2008) and Luciano et al. (2017) showed that the probability of negative mortality rates is negligible with calibrated parameters. The benefit of such specification is to allow tractability of mortality rates. Indeed, under Equation (4.8), is a Gaussian process and is normal distributed.

4.2.1 Best-estimate computation

Since we want to determine the best estimate mortality, we assume that there is no risk premium in the actuarial market or, equivalently, that Equation (4.8) holds under and . Therefore, the calibration of the mortality intensity is performed by estimating its dynamic under the real-world measure, and then using it under the risk-neutral measure.999A similar approach is considered in Luciano et al. (2017) For the stock process, we define

where represents the market price of equity risk. We can then write the dynamics under as follows

| (4.9) | ||||

| (4.10) |

The best estimate for the aggregate payoff (4.6) is given by

Under the independence assumption between the force of mortality and the stock dynamics, one can easily show that the best estimate simplifies into

| (4.11) | ||||

| (4.12) | ||||

| (4.13) |

with

We remark that the survival probability can be obtained in closed-form (for details, see for instance Mamon (2004)):

with

| (4.14) |

Under the dependence assumption, we provide in the next proposition the approximated best estimate for the portfolio of GMMB contracts.

Proposition 1

If we denote by the survival rates for each actuarial scenario101010We assume that the actuarial scenarios are generated by a Monte-Carlo sample of i.i.d. observations, the approximated best estimate for the aggregate payoff of GMMB contracts:

is given by

| (4.15) |

with

Proof. The proof based on classical arguments of stochastic calculus can be found in Appendix A.

The approximated best estimate (4.15) appears as an average of Black-Scholes call option prices which are adjusted for the dependence between the population force of mortality and the stock price processes. In each call option, there is an adjustement of the current stock price to , taking into account the realized survival rate in each actuarial scenario. It is also worth noticing that in case of independence (), the approximated best estimate (4.15) converges to the best estimate (4.13).

To determine the best estimate (4.15), we only need to generate survival rates () and plug them into the Black-Scholes option pricing formulas. Since the force of mortality dynamics is given by

one can prove (for details, see Appendix A) that

We generate mortality paths. The benchmark parameters for the stock and the force of mortality are given in Table 1. The mortality parameters follow from Luciano et al. (2017) while the financial parameters are based on Bernard and Kwak (2016). The mortality parameters correspond to UK male individuals who are aged at time

| Parameter set for numerical analysis |

|---|

| Force of mortality model: |

| Financial model: |

| Best estimate | Best estimate | ||

|---|---|---|---|

| -1.0 | 1.01132 | 0 | 1.00667 |

| -0.9 | 1.01086 | 0.1 | 1.00618 |

| -0.8 | 1.01041 | 0.2 | 1.00568 |

| -0.7 | 1.00995 | 0.3 | 1.00517 |

| -0.6 | 1.00950 | 0.4 | 1.00466 |

| -0.5 | 1.00904 | 0.5 | 1.00414 |

| -0.4 | 1.00858 | 0.6 | 1.00360 |

| -0.3 | 1.00811 | 0.7 | 1.00307 |

| -0.2 | 1.00764 | 0.8 | 1.00252 |

| -0.1 | 1.00716 | 0.9 | 1.00196 |

| 1.0 | 1.00141 |

Table 2 displays the best estimate per policy obtained using Equation (4.15) for a range of correlation coefficients: . We observe that the best estimate slightly decreases with the increase of the correlation parameter. This can be justified by a compensation effect between the mortality and the stock dynamics:

-

•

In case of positive dependence, high mortality scenarios (respectively low mortality scenarios) are linked with high stock values (respectively low stock values). In consequence, the expected value of the claim

will be reduced since high values of survivals will be associated with low financial guarantees, , and vice-versa.

-

•

On the other hand, in case of negative dependence, high survival rates will be linked with high financial guarantees, which implies a higher uncertainty and an increase of the best estimate.

4.2.2 Cost-of-capital value computation

The cost-of-capital value of the insurance liability is then determined by

where the cost-of-capital rate is fixed at and the SCR for actuarial risk is given by

for some coherent actuarial valuation . For this numerical illustration, we consider the TVaR measure with a confidence level .

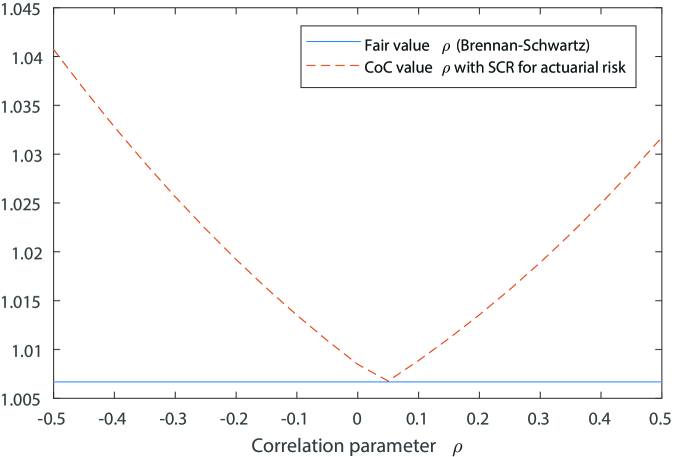

Figure 1 represents the CoC value of for a range of correlation coefficients: . Overall, we observe an increase of the CoC value of the GMMB contract under dependent mortality and equity risks. However, this effect is less pronounced for positive dependence. By comparison, the fair value of under the assumption that mortality can be completely diversified (denoted by for Brennan and Schwartz (1976)), is given by Equation (4.13):

| (4.16) | ||||

| (4.17) | ||||

From Figure 1, we clearly observe that this assumption underestimates the fair value of the contract since it does not take into account the actuarial uncertainty and the possible dependence with the financial market.

5 Concluding remarks

In this paper, we have proposed a general actuarial-consistent valuation for insurance liabilities based on a two-step actuarial valuation. Actuarial-consistency requires that traditional actuarial valuation based on diversification applies to all actuarial risks. We have shown that every two-step actuarial valuation is actuarial-consistent and in the coherent setting, any actuarial-consistent valuation has a two-step actuarial valuation representation. We also studied under which conditions it is feasible to define a valuation that is actuarial-consistent and market-consistent. In general, it is not possible and the valuator should decide whether the valuation is driven by current market prices or historical actuarial information.

Based on our two-step actuarial valuation, we have defined a cost-of-capital valuation in which the valuation is defined as the sum of a best estimate (expected value) and a risk margin (cost of providing the SCR for actuarial risks). The detailed numerical illustration has shown the important impact on risk management when relaxing the independence assumption between actuarial and financial risks. In an extended B-S financial market, we determined the cost-of-capital value of a GMMB contract under dependent financial and actuarial risks. It turns out that the dependence structure has an important impact on the fair valuation and the related SCR.

As pointed out by Liu et al. (2014), Solvency II Directive strongly recommends the testing of capital adequacy requirements on the assumption of mutual dependence between financial markets and life insurance markets. In that respect, we believe that our two-step framework provides a plausible setting for the valuation of insurance liabilities with dependent financial and actuarial risks.

Acknowledgements

Karim Barigou acknowledges the financial support of the Research Foundation - Flanders (FWO) (PhD funding) and the Joint Research Initiative on “Mortality Modeling and Surveillance” funded by AXA Research Fund (postdoc funding). The authors would also like to thank Jan Dhaene from KU Leuven for useful discussions and helpful comments on this manuscript. Finally, we sincerely thank the editor and anonymous referees for their pertinent remarks that significantly improved the quality of the manuscript.

References

- (1)

- Antonio et al. (2017) Antonio, K., Devriendt, S., de Boer, W., de Vries, R., De Waegenaere, A., Kan, H.-K., Kromme, E., Ouburg, W., Schulteis, T., Slagter, E. et al. (2017), ‘Producing the dutch and belgian mortality projections: a stochastic multi-population standard’, European Actuarial Journal 7(2), 297–336.

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D. (1999), ‘Coherent measures of risk’, Mathematical finance 9(3), 203–228.

- Assa and Gospodinov (2018) Assa, H. and Gospodinov, N. (2018), ‘Market consistent valuations with financial imperfection’, Decisions in Economics and Finance 41(1), 65–90.

- Barigou et al. (2019) Barigou, K., Chen, Z. and Dhaene, J. (2019), ‘Fair dynamic valuation of insurance liabilities: Merging actuarial judgement with market-and time-consistency’, Insurance: Mathematics and Economics 88, 19–29.

- Barigou and Dhaene (2019) Barigou, K. and Dhaene, J. (2019), ‘Fair valuation of insurance liabilities via mean-variance hedging in a multi-period setting’, Scandinavian Actuarial Journal 2019(2), 163–187.

- Bernard and Kwak (2016) Bernard, C. and Kwak, M. (2016), ‘Semi-static hedging of variable annuities’, Insurance: Mathematics and Economics 67, 173–186.

- Black and Scholes (1973) Black, F. and Scholes, M. (1973), ‘The pricing of options and corporate liabilities’, Journal of political economy 81(3), 637–654.

- Blake and Cairns (2020) Blake, D. and Cairns, A. J. (2020), ‘Longevity risk and capital markets: the 2018–19 update’, Annals of Actuarial Science 14(2), 219–261.

- Brennan and Schwartz (1976) Brennan, M. J. and Schwartz, E. S. (1976), ‘The pricing of equity-linked life insurance policies with an asset value guarantee’, Journal of Financial Economics 3(3), 195–213.

- Chen et al. (2021) Chen, Z., Chen, B., Dhaene, J. and Yang, T. (2021), ‘Fair dynamic valuation of insurance liabilities via convex hedging’, Insurance: Mathematics and Economics 98, 1–13.

- Da Fonseca and Ziveyi (2017) Da Fonseca, J. and Ziveyi, J. (2017), ‘Valuing variable annuity guarantees on multiple assets’, Scandinavian Actuarial Journal 2017(3), 209–230.

- Dalang et al. (1990) Dalang, R. C., Morton, A. and Willinger, W. (1990), ‘Equivalent martingale measures and no-arbitrage in stochastic securities market models’, Stochastics: An International Journal of Probability and Stochastic Processes 29(2), 185–201.

- Deelstra et al. (2020) Deelstra, G., Devolder, P., Gnameho, K. and Hieber, P. (2020), ‘Valuation of hybrid financial and actuarial products in life insurance by a novel three-step method’, ASTIN Bulletin 50(3), 709–742.

- Deelstra et al. (2016) Deelstra, G., Grasselli, M. and Van Weverberg, C. (2016), ‘The role of the dependence between mortality and interest rates when pricing guaranteed annuity options’, Insurance: Mathematics and Economics 71, 205–219.

- Delbaen and Biagini (2000) Delbaen, F. and Biagini, S. (2000), Coherent risk measures, Springer.

- Delbaen and Schachermayer (2006) Delbaen, F. and Schachermayer, W. (2006), The mathematics of arbitrage, Springer Science & Business Media.

- Delong et al. (2019) Delong, Ł., Dhaene, J. and Barigou, K. (2019), ‘Fair valuation of insurance liability cash-flow streams in continuous time: Theory’, Insurance: Mathematics and Economics 88, 196–208.

- Denuit et al. (2006) Denuit, M., Dhaene, J., Goovaerts, M. and Kaas, R. (2006), Actuarial theory for dependent risks: measures, orders and models, John Wiley & Sons.

-

Dhaene (2020)

Dhaene, J. (2020), Actuarial and financial

valuation principles.

Lecture notes.

http://www.jandhaene.org/presentations - Dhaene et al. (2013) Dhaene, J., Kukush, A., Luciano, E., Schoutens, W. and Stassen, B. (2013), ‘On the (in-) dependence between financial and actuarial risks’, Insurance: Mathematics and Economics 52(3), 522–531.

- Dhaene et al. (2017) Dhaene, J., Stassen, B., Barigou, K., Linders, D. and Chen, Z. (2017), ‘Fair valuation of insurance liabilities: Merging actuarial judgement and market-consistency’, Insurance: Mathematics and Economics 76, 14–27.

- Embrechts (2000) Embrechts, P. (2000), ‘Actuarial versus financial pricing of insurance’, The Journal of Risk Finance 1, 17–26.

- European Commission (2009) European Commission (2009), ‘Directive 2009/138/ec of the european parliament and of the council of 25 november 2009 on the taking-up and pursuit of the business of insurance and reinsurance (solvency ii)’.

- Fung et al. (2014) Fung, M. C., Ignatieva, K. and Sherris, M. (2014), ‘Systematic mortality risk: An analysis of guaranteed lifetime withdrawal benefits in variable annuities’, Insurance: Mathematics and Economics 58, 103–115.

- Harjoto et al. (2021) Harjoto, M. A., Rossi, F., Lee, R. and Sergi, B. S. (2021), ‘How do equity markets react to covid-19? evidence from emerging and developed countries’, Journal of Economics and Business 115, 105966.

- Ignatieva et al. (2016) Ignatieva, K., Song, A. and Ziveyi, J. (2016), ‘Pricing and hedging of guaranteed minimum benefits under regime-switching and stochastic mortality’, Insurance: Mathematics and Economics 70, 286–300.

- Kaas et al. (2008) Kaas, R., Goovaerts, M., Dhaene, J. and Denuit, M. (2008), Modern actuarial risk theory: using R, Vol. 128, Springer Science & Business Media.

- Le Courtois et al. (2021) Le Courtois, O., Majri, M. and Shen, L. (2021), ‘Utility-consistent valuation schemes for the own risk and solvency assessment of life insurance companies’, Asia-Pacific Journal of Risk and Insurance 15(1), 47–79.

-

Linders (2021)

Linders, D. (2021), 3-step hedge-based

valuation: fair valuation in the presence of systematic risks.

Working paper.

http://www.daniellinders.com - Liu et al. (2014) Liu, X., Mamon, R. and Gao, H. (2014), ‘A generalized pricing framework addressing correlated mortality and interest risks: a change of probability measure approach’, Stochastics An International Journal of Probability and Stochastic Processes 86(4), 594–608.

- Luciano et al. (2017) Luciano, E., Regis, L. and Vigna, E. (2017), ‘Single- and cross-generation natural hedging of longevity and financial risk’, Journal of Risk and Insurance 84(3), 961–986.

- Luciano and Vigna (2008) Luciano, E. and Vigna, E. (2008), ‘Mortality risk via affine stochastic intensities: calibration and empirical relevance’, Belgian Actuarial Bulletin 8, 5–16.

- Madan and Cherny (2010) Madan, D. B. and Cherny, A. (2010), ‘Markets as a counterparty: an introduction to conic finance’, International Journal of Theoretical and Applied Finance 13(08), 1149–1177.

- Madan and Schoutens (2016) Madan, D. and Schoutens, W. (2016), Applied Conic Finance, Cambridge University Press.

- Mamon (2004) Mamon, R. S. (2004), ‘Three ways to solve for bond prices in the vasicek model’, Advances in Decision Sciences 8(1), 1–14.

- Möhr (2011) Möhr, C. (2011), ‘Market-consistent valuation of insurance liabilities by cost of capital’, ASTIN Bulletin 41(2), 315–341.

- Møller (2001) Møller, T. (2001), ‘Risk-minimizing hedging strategies for insurance payment processes’, Finance and Stochastics 5(4), 419–446.

- Møller (2002) Møller, T. (2002), ‘On valuation and risk management at the interface of insurance and finance’, British Actuarial Journal 8(4), 787–827.

- Muermann (2003) Muermann, A. (2003), ‘Actuarially consistent valuation of catastrophe derivatives’, The Wharton Financial Institution Center Working Paper Series pp. 03–18.

- Norberg (2014) Norberg, R. (2014), ‘Life insurance mathematics’, Wiley StatsRef: Statistics Reference Online .

- Pelsser and Stadje (2014) Pelsser, A. and Stadje, M. (2014), ‘Time-consistent and market-consistent evaluations’, Mathematical Finance 24(1), 25–65.

- Plantin et al. (2008) Plantin, G., Sapra, H. and Shin, H. S. (2008), ‘Marking-to-market: panacea or pandora’s box?’, Journal of accounting research 46(2), 435–460.

- Rae et al. (2018) Rae, R., Barrett, A., Brooks, D., Chotai, M., Pelkiewicz, A. and Wang, C. (2018), ‘A review of solvency ii: has it met its objectives?’, British Actuarial Journal 23.

- Sharif et al. (2020) Sharif, A., Aloui, C. and Yarovaya, L. (2020), ‘Covid-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the us economy: Fresh evidence from the wavelet-based approach’, International Review of Financial Analysis 70, 101496.

- Vedani et al. (2017) Vedani, J., El Karoui, N., Loisel, S. and Prigent, J.-L. (2017), ‘Market inconsistencies of market-consistent european life insurance economic valuations: pitfalls and practical solutions’, European Actuarial Journal 7(1), 1–28.

- Wüthrich (2016) Wüthrich, M. V. (2016), Market-Consistent Actuarial Valuation, EEA Series, Springer.

- Wüthrich and Merz (2013) Wüthrich, M. V. and Merz, M. (2013), Financial modeling, actuarial valuation and solvency in insurance, Springer.

- Zhao and Mamon (2018) Zhao, Y. and Mamon, R. (2018), ‘An efficient algorithm for the valuation of a guaranteed annuity option with correlated financial and mortality risks’, Insurance: Mathematics and Economics 78, 1–12.

Appendix A Appendix: Proof of Proposition 1

Proof. We recall that the dynamics of the stock process and the population force of mortality under are given by

| (A.1) | ||||

| (A.2) |

with and are positive constants, and . Here, and are independent standard Brownian motions under . From (A.2), we note that

Hence, the force of mortality is a Gaussian process:

Moreover, we find that

with

We can also remark that

which leads to

We can then assume that

where is a standard normal r.v. independent of .

From

we find that

The stock price at time can be written as

with

Finally, we find that

which ends the proof.