Standard and fractional reflected Ornstein-Uhlenbeck processes as the limits of square roots of Cox-Ingersoll-Ross processes

Abstract

In this paper, we establish a new connection between Cox-Ingersoll-Ross (CIR) and reflected Ornstein-Uhlenbeck (ROU) models driven by either a standard Wiener process or a fractional Brownian motion with . We prove that, with probability 1, the square root of the CIR process converges uniformly on compacts to the ROU process as the mean reversion parameter tends to either (in the standard case) or to (in the fractional case). This also allows to obtain a new representation of the reflection function of the ROU as the limit of integral functionals of the CIR processes. The results of the paper are illustrated by simulations.

keywords:

Cox-Ingersoll-Ross process, reflected Ornstein-Uhlenbeck process, fractional Brownian motion.MSC 2020: 60H10; 60G22; 91G30

1 Introduction

Both the reflected Ornstein-Uhlenbeck (ROU) and the Cox-Ingersoll-Ross (CIR) processes are extremely popular models in a variety of fields. Without attempting to give a complete overview of possible applications due to the large amount of literature on the topic, we only mention that the ROU process is widely used in queueing theory [10, 30, 31, 32], in population dynamics modeling [1, 25], in economics and finance for modeling regulated markets [17, 33, 3, 4], interest rates [11] and stochastic volatility [27] (see also [9, 20] and references therein for a more details on applications of the ROU in various fields) while the most notable usages of the CIR process are related to representing the dynamics of interest rates [5, 6, 7] and stochastic volatility in the Heston model [12].

It is well-known [21, 28] that the CIR process has strong links with the standard OU dynamics; in particular, if is a -dimensional Brownian motion and is a standard -dimensional OU process given by

then it is easy to see via Itô’s formula that the process , , is the CIR process of the form

| (1) |

with and (which is a standard Brownian motion by Levy’s characterization). The value is sometimes referred to as a dimension or a number of degrees of freedom of the CIR process (see e.g. [21] and references therein) and thus, in this terminology, a square of a standard one-dimensional OU process turns out to be a CIR process with one degree of freedom w.r.t. another Brownian motion.

In this paper, we investigate a connection between the CIR and the ROU processes that is in some sense related to the one described above. Namely, in the first part we prove that the ROU process

| (2) |

where is a standard Brownian motion and is a continuous non-decreasing process that can have points of growth only at zeros of , coincides with the square root of the CIR process of the type (1) with (i.e. with one degree of freedom) driven by the same Brownian motion . Moreover, if is a sequence of positive numbers such that as , then, with probability 1, for all

| (3) |

where is the CIR process of the form

The second part of the paper discusses the connection between fractional counterparts of equations (1) and (2) driven by fractional Brownian motion with Hurst index . Namely, we consider a fractional Cox-Ingersoll-Ross process

where the integral is understood as the pathwise limit of Riemann-Stieltjes integral sums (see [23] or [8, Subsection 4.1]) and prove that with probability 1 the paths of a.s. converge to the reflected fractional Ornstein-Uhlenbeck (RFOU) process uniformly on each compact as . Moreover, an analogue of the representation (3) also takes place: if is a reflection function of the RFOU process, then, with probability 1, for each

2 Classical reflected Ornstein-Uhlenbeck and Cox-Ingersoll-Ross processes

The main goal of this section is to establish connection between Cox-Ingersoll-Ross (CIR) and reflected Ornstein-Uhlenbeck (ROU) processes in the standard Brownian setting. We shall start from the definition of a reflection function following the one given in the classical work [29].

Definition 2.1.

Let be some stochastic process. The process is called a reflection function for , if is, with probability 1, a continuous non-decreasing process such that and the points of growth of can occur only at zeros of .

Definition 2.2.

Stochastic process is called a reflected Ornshein-Uhlenbeck (ROU) process if it satisfies a stochastic differential equation of the form

| (4) |

where , and are positive constants, is a standard Brownian motion, is a reflection function for and a.s.

Remark 1.

The ROU process is well-known and studied in the literature, see e.g. [31] and references therein. Note also that, despite (4) has two unknown functions and , the solution is still unique. Indeed, let and be two stochastic processes satisfying

and

where and are the corresponding reflection functions. Assume that on some such that both and are continuous

| (5) |

and consider . Then for all ; moreover, for , therefore is non-increasing on . It means that the difference is also non-increasing on since

and the right-hand side is non-increasing w.r.t. . Whence, taking into account that due to the definition of and continuity of both and , the difference cannot be positive for any which contradicts (5). Interchanging the roles of and , one can easily verify that cannot be negative either and whence , .

Now, consider a standard CIR process defined as a continuous modification of the unique solution to the equation

| (6) |

where and is a classical Wiener process. It is well-known (see e.g. [15, Example 8.2]) that for the solution is non-negative a.s. for any ; moreover, the solution is strictly positive a.s. provided that , see e.g. [16, Chapter 5]. Therefore, if , the square-root process is well-defined.

For an arbitrary , consider a the stochastic process . By Itô’s formula, for any

| (7) | ||||

and, since the left-hand side of (7) converges to a.s. as , moving in the right-hand side would give us the dynamics of .

First, it is clear that for any

| (8) |

and

| (9) |

as . Further, by the monotone convergence,

| (10) |

as . Finally, by Burkholder-Davis-Gundy inequality and dominated convergence theorem, for any

where we used continuity of the distribution of for each to state that (see e.g. [21] and references therein). This implies that

| (11) |

By (11), it is evident that there exists a sequence which depends on such that

| (12) |

and along this sequence

| (13) |

a.s. because all other limits in (7) as are finite a.s. However, the integral which arises in (10) may be infinite and thus the explicit form of the limit above for now remains obscure. This issue as well as the connection of to the ROU process is addressed in the next theorem.

Theorem 2.3.

Let be the square root process, where is the CIR process defined by (6). Denote

-

(a)

If , then for any

Moreover, the square root process a.s. satisfies the SDE of the form

(14) , and the solution to this equation is unique among non-negative stochastic processes.

-

(b)

If , then

while

for any . Moreover, the square root process satisfies the SDE of the form

(15) where the process from (15) is a continuous nondecreasing process the points of growth of which can occur only at zeros of , i.e. is a reflected Ornstein-Uhlenbeck process.

Proof.

Case (a): . Denote . Our goal is to prove that the integral

is finite a.s. Define and assume that for some : . Fix , the corresponding sequence such that convergence (12) holds and an arbitrary , where , , is the set where (12) takes place (in what follows, in brackets will be omitted). Then

Obviously, for all

so, for

whence, taking into account (7)–(9), we obtain that

which is impossible a.s. We get a contradiction, whence for all and a.s. By going to the limit in (7), we immediately get (14).

Concerning the uniqueness of solution to (14), let be any of its non-negative solutions. Then, by Itô’s formula,

so satisfies equation and thus coincides with . Therefore

Case (b): . Fix and take the corresponding sequence such that (12) holds. By (7), for any

and (13) implies that there exists , , such that for all the limit

is well-defined and finite for all . It is evident that a.s. due to continuity of and the fact that . Moreover, since a.s.

is continuous in . Furthermore,

for all , and whence is non-decreasing in a.s. Finally, if , there exists an interval containing such that for all and thus

i.e. can increase only at points of zero hitting of that coincide with the ones of . Taking into the account all of the above as well as an arbitrary choice of , is the reflection function for and the latter is indeed a ROU process.

Now, let us prove that a.s. Consider a standard Ornstein-Uhlenbeck process of the form

| (16) |

with being the same Brownian motion that drives . It is evident that coincides with until a.s. and thus it is sufficient to prove that a.s. For any consider

where denotes the local time of , and observe that

Computations similar to the ones in [26, Section IV.44] indicate that the local time of is Hölder continuous in up to order over bounded time intervals and thus a.s.

Finally, assume that for some ,

with positive probability. On where this property holds, we have that

Therefore, for such , satisfies the equation of the form

on the interval , i.e. such paths of coincide with the corresponding paths of the Ornstein-Uhlenbeck process defined by (16) up until . This implies that and is nonnegative on the interval for such , which is impossible due to the non-tangent property of Gaussian processes stated by [34], see also [24]. ∎

Remark 2.

As a corollary of Theorem 2.3, we have a representation of the reflection function of the ROU process as the limit of integral functionals of the CIR processes. It is interesting that the reflection function is singular w.r.t. the Lebesgue measure (see Remark 3) while the processes that converge to it are absolutely continuous a.s.

Theorem 2.4.

Let be a continuous modification of a standard Brownian motion, , , be given constants and be an arbitrary sequence such that , . For any from this sequence, consider the CIR process given by

and denote its square root by . Then, with probability 1,

-

1)

the limit is well-defined, finite and non-negative for any ;

-

2)

the limit process is a ROU process satisfying the equation of the form

with and being the reflection function for ;

-

3)

for any

(17) and

(18)

Proof.

Denote the CIR process of the form

By Theorem 2.3, there exists , , such that for all and each , , are continuous and the latter satisfy equations of the form

with the integral . Furthermore, since each is a CIR process that satisfies conditions of the comparison theorem from [14], this can be chosen such that for all

| (19) |

Fix (in what follows, we will omit in brackets for notational simplicity). Since the sequence is non-increasing for each , there exists a pointwise limit . Moreover, it is evident that and since

the limit is well-defined, nonnegatove and finite.

In order to obtain the claim of the theorem, it is sufficient to check that the function defined above is indeed a reflection function for , i.e. is continuous and nondecreasing process that starts at zero and the points of growth of which occur only at zeros of . Note that continuity of would also imply the uniform convergences (17) and (18) on each compact . Indeed, since for all , and continuity of would imply continuity of , Dini’s theorem guarantees (17). The same argument applies to (18): the right-hand side of

is non-increasing w.r.t. , therefore for each and

and Dini’s theorem implies (18) as well.

By (19), continuity of and the fact that , there exists an interval such that for all and . Thus for any

i.e. for all .

For reader’s convenience, we will split the further proof into four steps.

Step 1: in non-decreasing. Monotonicity of is obvious since for any fixed and

Step 2: right-continuity. Let us show that is continuous from the right. For any fixed , denote (the right limit exists since is non-decreasing) and assume that . Due to the monotonicity of , this implies that for all

| (20) |

Now, take such that for all

and such that

As it was noted previously, for each the values of are non-increasing when . Thus for any

i.e.

which contradicts (20). Therefore, , i.e. is right-continuous.

Step 3: left-continuity. Now, let us show that is continuous from the left. Assume that it is not true and there exists such that (note that is well-defined due to the monotonicity of ). Since may have only positive jumps, so does and, moreover, the points of jumps of and coincide. This implies that and we now consider two cases.

Case 1: . Then (note that is right-continuous by Step 2) and there exists an interval such that for all . This implies that

i.e. cannot have a jump at . This means that cannot have a jump at point either and we obtain a contradiction.

Case 2: and . Fix , and let be a random variable such that for all

Take and such that and note that there exists such that . Since as , there exists such that . Moreover, thus one can define

Observe that and for all , whence

which contradicts the assumption that . This contradiction together with all of the above implies that (and thus ) is continuous at each point .

Step 4: points of growth. Now, let us prove that the points of growth of may occur only at zeros of . Indeed, let be such that . Since is continuous, there exists such that for any

This, in turn, implies that for all and

and thus for any

Therefore and does not grow in some neighbourhood of . ∎

Remark 3.

It is well-known (see e.g. [2, Appendix A] or [37, Subsection 3.3.1]) that the absolute value of OU and ROU processes with non-zero mean reversion levels do not coincide. In turn, in the “symmetric” case with zero mean reversion parameter, absolute value of the OU process and ROU process have the same distribution but do not coincide pathwisely. Theorem 2.3 allows to clarify this subtle difference in the following manner.

Let be some standard Brownian motion and

be a standard Ornstein-Uhlenbeck process with non-random positive initial value . By Itô’s formula,

where is a standard Brownian motion (which can be easily verified by Levy’s characterization). Thus, the process , , is a CIR process w.r.t. . By Theorem 2.3, the square root process , , is a reflected Ornstein-Uhlenbeck process with respect to satisfying the SDE of the form

| (21) |

with being the reflection function for . Since , by Tanaka’s formula

| (22) | ||||

with being the local time of at zero. Comparing (21) and (22), we obtain that , i.e. the reflection function of the ROU process coincides with local time at zero of the OU process .

3 Fractional Cox-Ingersoll-Ross and fractional reflected Ornstein-Uhlenbeck processes

Let now be a continuous modification of a fractional Brownian motion with Hurst index . Consider a stochastic differential equation of the form

| (23) |

where is a given constant, , , . According to [23] (see also [8]), SDE (23) a.s. has a unique pathwise solution such that for all , and the subset of where this solution exists does not depend on , , or (in fact, the solution exists for all such that is locally Hölder continuous in ). Moreover, it can be shown (see [23, Theorem 1] or [8, Subsection 4.1]) that the process , , satisfies the SDE of the form

| (24) |

where and the integral with respect to the fractional Brownian motion exists as the pathwise limit of the corresponding Riemann-Stieltjes integral sums. Taking into account the form of (24), the process can be interpreted as a natural fractional generalisation of the Cox-Ingersoll-Ross process with being its square root.

Remark 4.

It is evident that the solution to (24) is unique in the class of non-negative stochastic processes with paths that are Hölder-continuous up to the order . Indeed, by the fractional pathwise counterpart of the Itô’s formula (see e.g. [35, Theorem 4.3.1]) the square root of the solution must satisfy the equation (23) until the first moment of zero hitting. However, as it was noted above, the solution to (23) is unique and strictly positive a.s., i.e. never hits zero.

Now, let us recall the definition of the reflected fractional Ornstein-Uhlenbeck (RFOU) process.

Definition 3.1.

Stochastic process is called a fractional reflected Ornshein-Uhlenbeck (RFOU) process if it satisfies a stochastic differential equation of the form

| (25) |

where , and are positive constants, is a fractional Brownian motion, is a reflection function for in the sense of Definition 2.1 and a.s.

Remark 5.

When it comes to the connection between FCIR and RFOU processes, there is a notable difference from the standard Brownian case discussed in section 2: in the standard case the ROU process turned out to coincide with the square root of the CIR process with which is not true for the fractional case. More precisely, if , is strictly positive a.s. and thus cannot coincide with the RFOU process. Furthermore, for [22, Theorem 6] claims existence and uniqueness of solution to (24) when , and this solution turns out to stay in zero after hitting it, i.e. its square root is also different from the RFOU process. However, it is still possible to establish a clear connection between FCIR and RFOU processes highlighted in the next theorem.

Theorem 3.2.

Let be a continuous modification of a fractional Brownian motion with Hurst index , , , be given constants. For any , consider a square root process given by

Then, with probability 1,

-

1)

the limit is well-defined, finite and non-negative for any ;

-

2)

the limit process is a RFOU process satisfying the equation of the form

(26) -

3)

for any

and

Proof.

Let such that is locally Hölder continuous in be fixed (for notational simplicity, we will omit it in brackets). As it was noted above, for such all are well-defined and strictly positive. Moreover, by the comparison theorem (see e.g. [23, Lemma 1] or [8, Lemma A.1]), for all and

This implies that for any fixed the limits and are well-defined, non-negative and finite. Furthermore, by comparison theorem, each exceeds the fractional Ornstein-Uhlenbeck of the form

and hence there exists an interval such that for all and . Thus for any

i.e. for all .

The remaining part of the proof is identical to the one of Theorem 2.4. ∎

4 Simulations

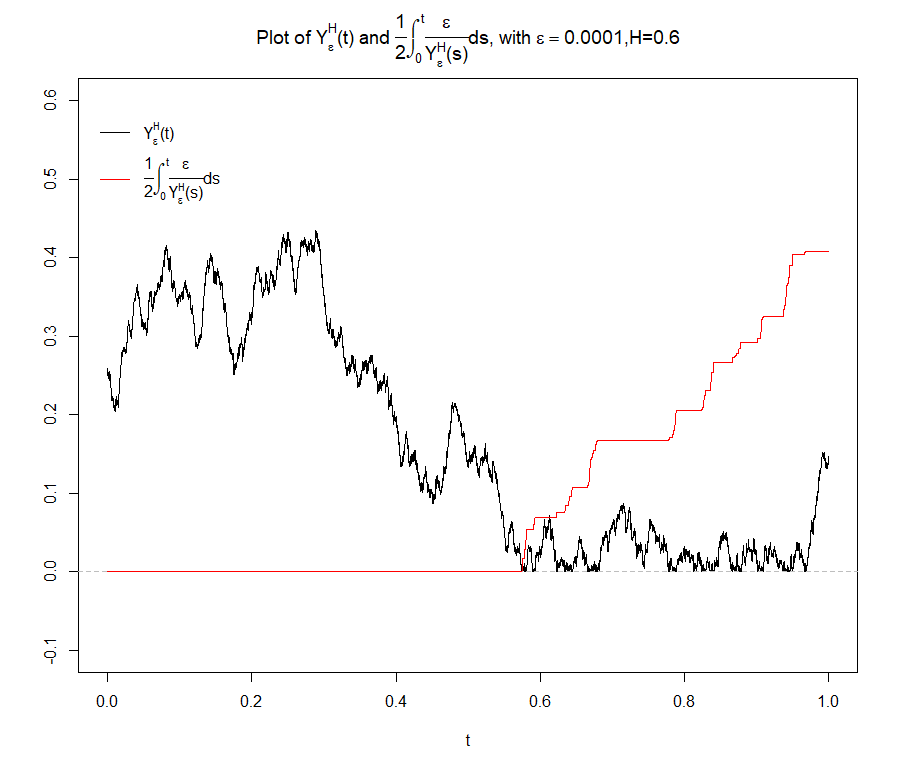

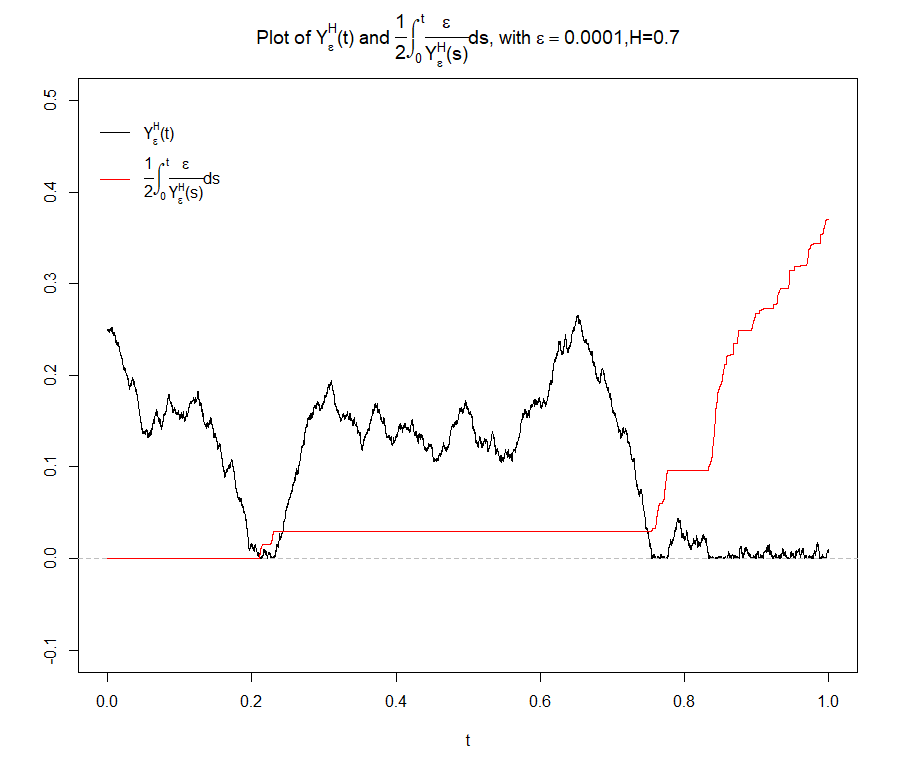

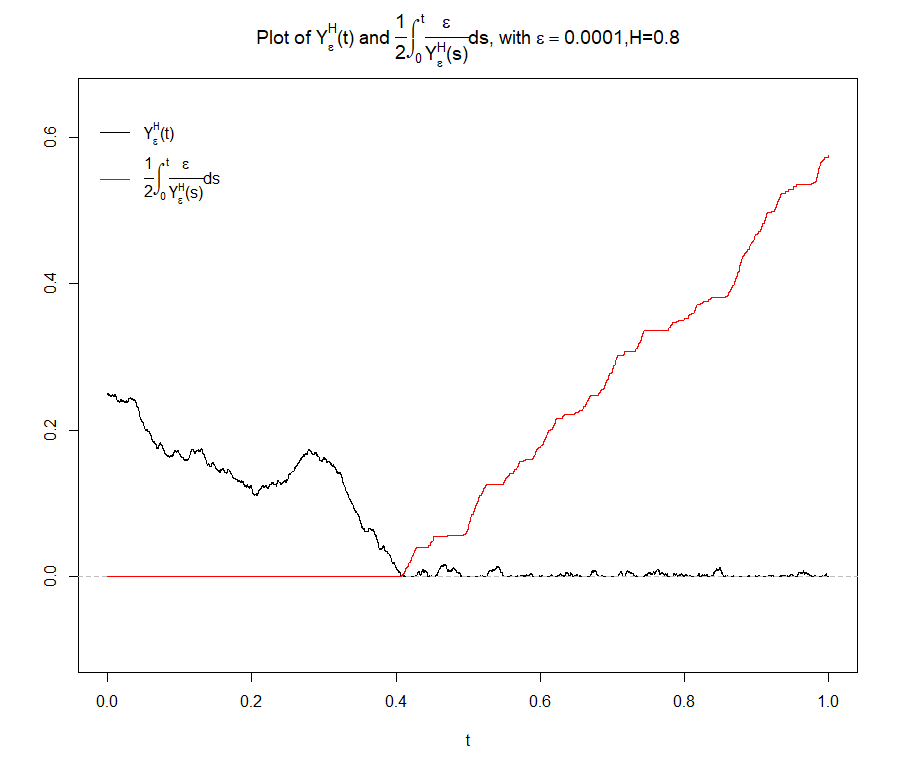

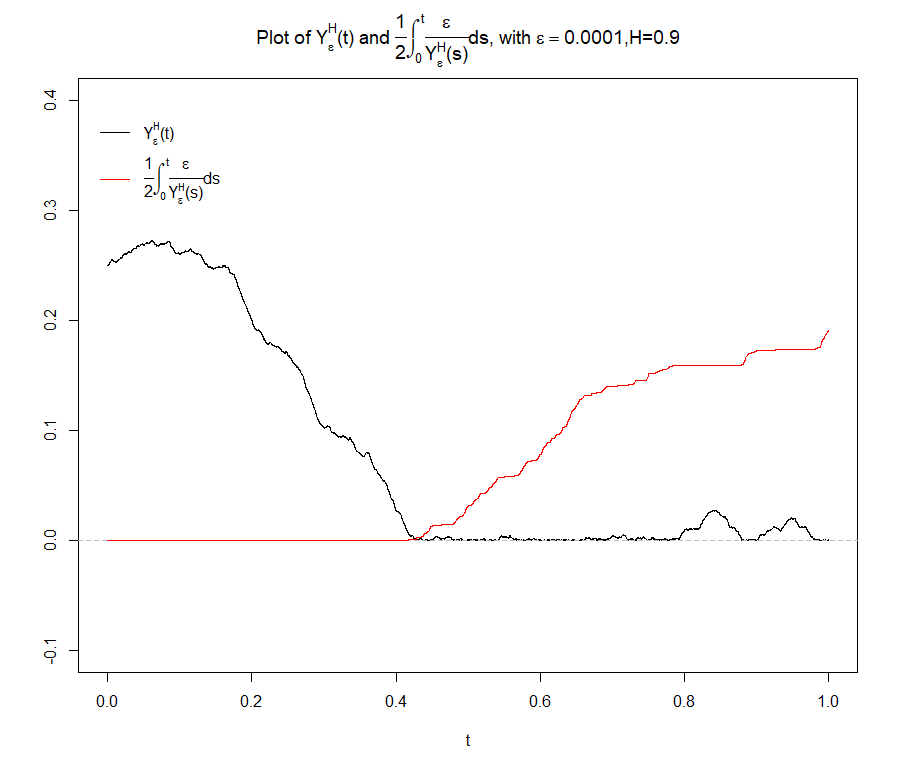

Let us illustrate the results with simulations. On Fig. 1, the black paths depict simulated trajectories of the square root of the FCIR process given by an equation of the form

with , , , and different Hurst indices ; the red lines are the corresponding integrals . In order to simulate , the backward Euler approximation technique from [18] was used, see also [13, 36].

(a)

(b)

(c)

(d)

Theorem 3.2 states that the red line approximates the reflection function of the RFOU process and it can be clearly seen that the plot is well agreed with the theory: the integral shows notable growth only when the corresponding path of is very close to zero.

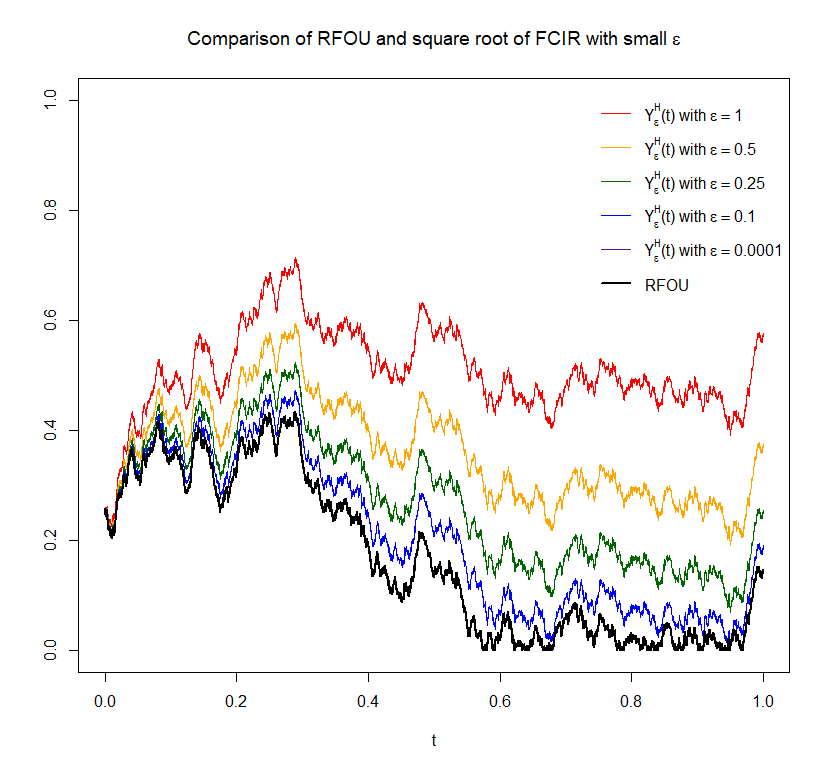

Fig. 2 illustrates the uniform convergence of paths of to the path of RFOU process as . On the picture, , , , and the path of the FROU process was simulated using the Euler-type method:

When , the path of (purple) is so close to the corresponding path of the ROU process (bold black) that they are not distinguishable on the plot.

Acknowledgements

The present research is carried out within the frame and support of the ToppForsk project nr. 274410 of the Research Council of Norway with title STORM: Stochastics for Time-Space Risk Models. The first author is supported by the National Research Fund of Ukraine under grant 2020.02/0026.

References

- [1] O.O. Aalen and H.K. Gjessing, Survival models based on the Ornstein-Uhlenbeck process, Lifetime data analysis 10 (2004), p. 407–423.

- [2] C.A. Ball and A. Roma, Stochastic volatility option pricing, Journal of financial and quantitative analysis 29 (1994), pp. 589–607.

- [3] L. Bo, D. Tang, Y. Wang, and X. Yang, On the conditional default probability in a regulated market: a structural approach, Quantitative finance 11 (2011), p. 1695–1702.

- [4] L. Bo, Y. Wang, and X. Yang, Some integral functionals of reflected SDEs and their applications in finance, Quantitative finance 11 (2011), p. 343–348.

- [5] J.C. Cox, J.E. Ingersoll, and S.A. Ross, A re-examination of traditional hypotheses about the term structure of interest rates, The journal of finance 36 (1981), p. 769–799.

- [6] J.C. Cox, J.E. Ingersoll, and S.A. Ross, An intertemporal general equilibrium model of asset prices, Econometrica: journal of the Econometric Society 53 (1985), p. 363.

- [7] J.C. Cox, J.E. Ingersoll, and S.A. Ross, A theory of the term structure of interest rates, Econometrica: journal of the Econometric Society 53 (1985), p. 385.

- [8] G. Di Nunno, Y. Mishura, and A. Yurchenko-Tytarenko, Sandwiched SDEs with unbounded drift driven by Holder noises, ArXiv 2012.11465 (2020).

- [9] V. Giorno, A.G. Nobile, and R. di Cesare, On the reflected Ornstein–Uhlenbeck process with catastrophes, Applied mathematics and computation 218 (2012), p. 11570–11582.

- [10] V. Giorno, A.G. Nobile, and L.M. Ricciardi, On some diffusion approximations to queueing systems, Advances in applied probability 18 (1986), p. 991–1014.

- [11] R.S. Goldstein and W.P. Keirstead, On the term structure of interest rates in the presence of reflecting and absorbing boundaries, SSRN Electronic Journal (1997).

- [12] S.L. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Review of Financial Studies 6 (1993), pp. 327–43.

- [13] J. Hong, C. Huang, M. Kamrani, and X. Wang, Optimal strong convergence rate of a backward Euler type scheme for the Cox–Ingersoll–Ross model driven by fractional Brownian motion, Stochastic processes and their applications 130 (2020), p. 2675–2692.

- [14] N. Ikeda and S. Watanabe, A comparison theorem for solutions of stochastic differential equations and its applications, Osaka Journal of Mathematics 14 (1977), pp. 619 – 633.

- [15] N. Ikeda and S. Watanabe, Stochastic Differential Equations and Diffusion Processes, Elsevier, 1981.

- [16] I. Karatzas and S.E. Shreve, Brownian Motion and Stochastic Calculus, Springer New York, 1998.

- [17] P.R. Krugman, Target zones and exchange rate dynamics, The Quarterly Journal of Economics 106 (1991), p. 669–682.

- [18] K. Kubilius, Estimation of the Hurst index of the solutions of fractional SDE with locally Lipschitz drift, Lithuanian Association of Nonlinear Analysts (LANA). Nonlinear Analysis. Modelling and Control 25 (2020), p. 1059–1078.

- [19] C. Lee and J. Song, On drift parameter estimation for reflected fractional Ornstein–Uhlenbeck processes, Stochastics. An International Journal of Probability and Stochastic Processes 88 (2016), p. 751–778.

- [20] V. Linetsky, On the transition densities for reflected diffusions, Advances in applied probability 37 (2005), p. 435–460.

- [21] Y. Maghsoodi, Solution of the extended CIR term structure and bond option valuation, Mathematical Finance. An International Journal of Mathematics, Statistcs and Financial Economics 6 (1996), p. 89–109.

- [22] A. Melnikov, Y. Mishura, and G. Shevchenko, Stochastic viability and comparison theorems for mixed stochastic differential equations, Methodology and computing in applied probability 17 (2015), p. 169–188.

- [23] Y. Mishura and A. Yurchenko-Tytarenko, Fractional Cox–Ingersoll–Ross process with non-zero “mean”, Modern Stochastics: Theory and Applications 5 (2018), pp. 99–111.

- [24] V.I. Piterbarg, Twenty Lectures About Gaussian Processes, Atlantic Financial Press, 2015.

- [25] L.M. Ricciardi, Stochastic population theory: Diffusion processes, in Mathematical Ecology, Springer Berlin Heidelberg (1986), p. 191–238.

- [26] L.C.G. Rogers and D. Williams, Diffusions, Markov Processes and Martingales, Cambridge University Press, 2000.

- [27] R. Schöbel and J. Zhu, Stochastic volatility with an Ornstein–Uhlenbeck process: An extension, Review of finance 3 (1999), p. 23–46.

- [28] T. Shiga and S. Watanabe, Bessel diffusions as a one-parameter family of diffusion processes, Zeitschrift fur Wahrscheinlichkeitstheorie und Verwandte Gebiete 27 (1973), p. 37–46.

- [29] A.V. Skorokhod, Stochastic equations for diffusion processes in a bounded region, Theory of Probability & Its Applications 6 (1961), pp. 264–274.

- [30] A.R. Ward and P.W. Glynn, A diffusion approximation for a Markovian queue with reneging, Queueing systems 43 (2003), p. 103–128.

- [31] A.R. Ward and P.W. Glynn, Properties of the reflected Ornstein–Uhlenbeck process, Queueing systems 44 (2003), p. 109–123.

- [32] A.R. Ward and P.W. Glynn, A diffusion approximation for a GI/GI/1 queue with balking or reneging, Queueing systems 50 (2005), p. 371–400.

- [33] X. Yang, X. Li, G. Ren, Y. Wang, and L. Bo, Modeling the exchange rates in a target zone by reflected Ornstein-Uhlenbeck process, SSRN Electronic Journal (2012). Available at http://dx.doi.org/10.2139/ssrn.2107686.

- [34] D. Ylvisaker, A note on the absence of tangencies in Gaussian sample paths, The Annals of Mathematical Statistics 39 (1968), pp. 261–262.

- [35] M. Zähle, Integration with respect to fractal functions and stochastic calculus. I, Probability theory and related fields 111 (1998), p. 333–374.

- [36] S.Q. Zhang and C. Yuan, Stochastic differential equations driven by fractional Brownian motion with locally Lipschitz drift and their implicit Euler approximation, Proceedings of the Royal Society of Edinburgh: Section A Mathematics (2020), p. 1–27.

- [37] J. Zhu, Applications of Fourier transform to smile modeling, Springer Berlin Heidelberg, 2010.