Contributions to Large Scale Bayesian Inference and Adversarial Machine Learning

(Contribuciones a la Inferencia Bayesiana a Gran Escala y al

Aprendizaje Automático Adversario)

L1.4 \DeclareBibliographyCategorymypapers

Programa de Doctorado en Ingeniería Matemática,

Estadística e Investigación Operativa por la

Universidad Complutense de Madrid y la

Universidad Politécnica de Madrid

Contributions to Large Scale Bayesian Inference and Adversarial Machine Learning

(Contribuciones a la Inferencia Bayesiana a Gran Escala y al

Aprendizaje Automático Adversario)

A thesis submitted in partial fulfillment for the

degree of Doctor of Philosophy

By

Víctor Gallego Alcalá

under the direction of

David Ríos Insua and David Gómez-Ullate Oteiza

Madrid, 2021

- Department:

-

Estadística e Investigación Operativa

Facultad de Ciencias Matemáticas

Universidad Complutense de Madrid (UCM)

Spain - Title:

-

Contributions to Large Scale Bayesian Inference and Adversarial Machine Learning

- Author:

-

Víctor Gallego Alcalá

- Advisors:

-

David Ríos Insua and David Gómez-Ullate Oteiza

- Date:

-

June 2021

Abstract

The field of machine learning (ML) has experienced a major boom in the past years, both in theoretical developments and application areas. However, the rampant adoption of ML methodologies has revealed that models are usually adopted to make decisions without taking into account the uncertainties in their predictions. More critically, they can be vulnerable to adversarial examples, strategic manipulations of the data with the goal of fooling those systems. For instance, in retailing, a model may predict very high expected sales for the next week, given a certain advertisement budget. However, the predicted variance may also be quite big, thus making the prediction almost useless depending on the risk tolerance of the company. Similarly, in the case of spam detection, an attacker may insert additional words in a given spam email to evade being classified as spam by making it to appear more legit. Thus, we believe that developing ML systems that take into account predictive uncertainties and are robust against adversarial examples is a must for critical, real-world tasks. This thesis is a step towards achieving this goal.

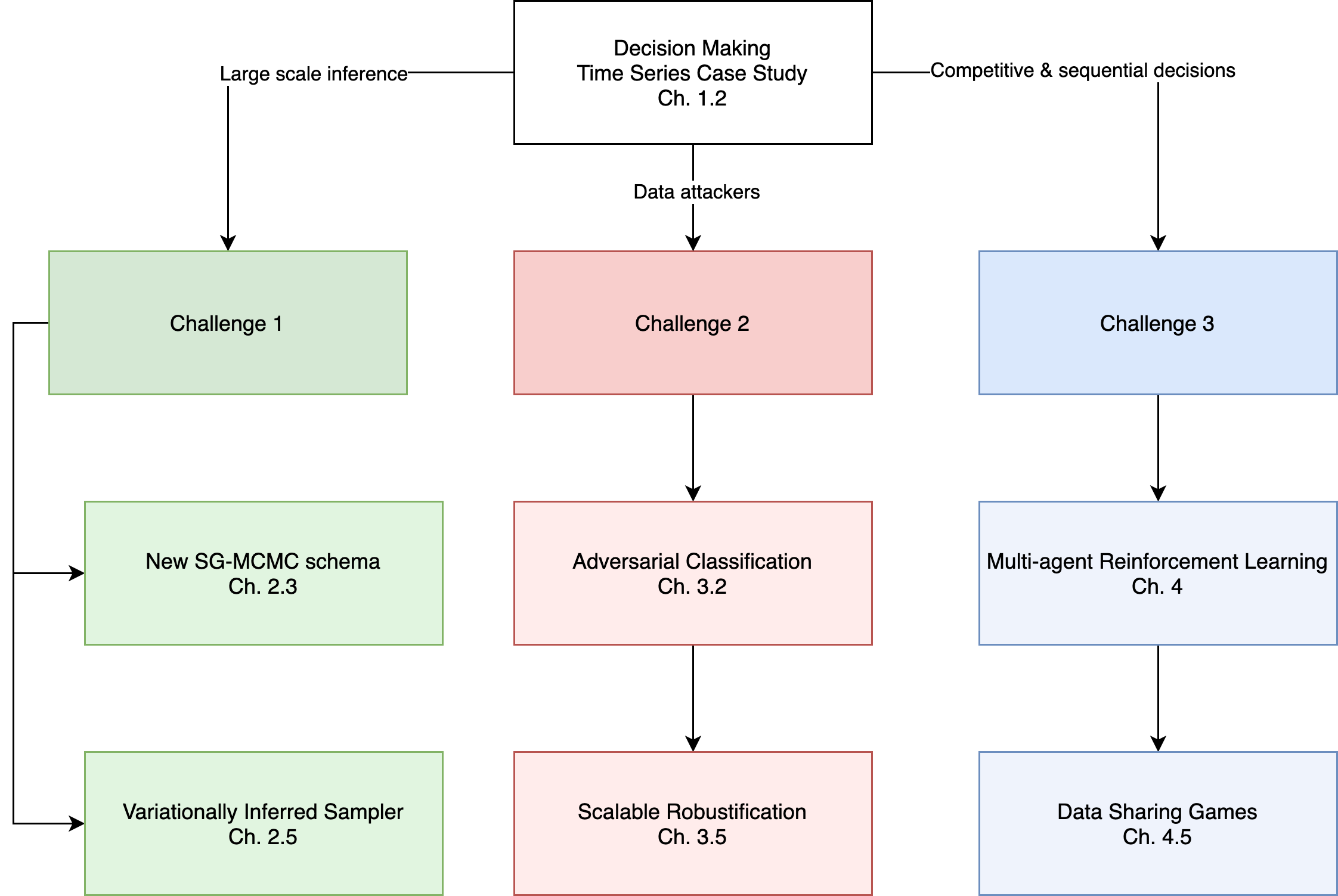

In Chapter 1, we start with a case study in retailing. We propose a robust implementation of the Nerlove–Arrow model using a Bayesian structural time series model to explain the relationship between advertising expenditures of a country-wide fast-food franchise network with its weekly sales. Its Bayesian nature facilitates incorporating prior information reflecting the manager’s views, which can be updated with relevant data. However, this case study adopted classical Bayesian techniques, such as the Gibbs sampler. Nowadays, the ML landscape is pervaded with complex models, huge in the number of parameters. This is the realm of neural networks and this chapter also surveys current developments in this sub-field. In doing this, three challenges that constitute the core of this thesis are identified.

Chapter 2 is devoted to the first challenge. In it, we tackle the problem of scaling Bayesian inference to complex models and large data regimes. In the first part, we propose a unifying view of two different Bayesian inference algorithms, Stochastic Gradient Markov Chain Monte Carlo (SG-MCMC) and Stein Variational Gradient Descent (SVGD), leading to improved and efficient novel sampling schemes. In the second part, we develop a framework to boost the efficiency of Bayesian inference in probabilistic models by embedding a Markov chain sampler within a variational posterior approximation. We call this framework “variationally inferred sampling”. This framework has several benefits, such as its ease of implementation and the automatic tuning of sampler parameters, leading to a faster mixing time through automatic differentiation. Experiments show the superior performance of both developments compared to baselines. In addition, both could be combined to further improve the results.

In Chapter 3, we address the challenge of protecting ML classifiers from adversarial examples. So far, most approaches to adversarial classification have followed a classical game-theoretic framework. This requires unrealistic common knowledge conditions untenable in the security settings typical of the adversarial ML realm. After reviewing such approaches, we present an alternative perspective on AC based on adversarial risk analysis, and leveraging the scalable Bayesian approaches from chapter 2.

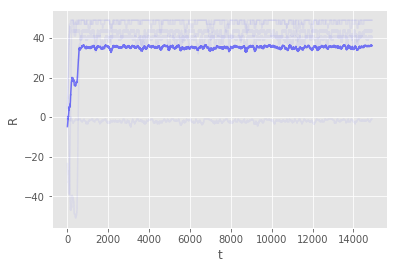

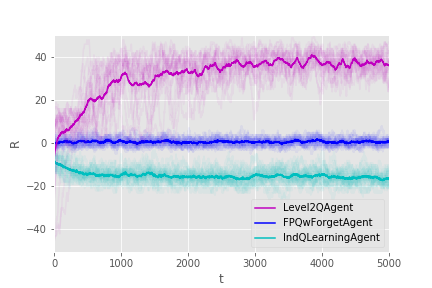

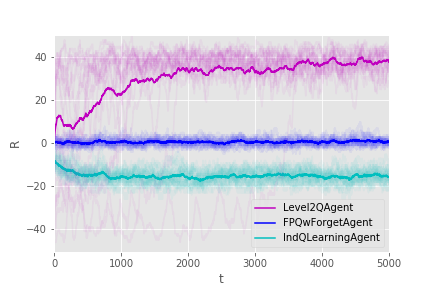

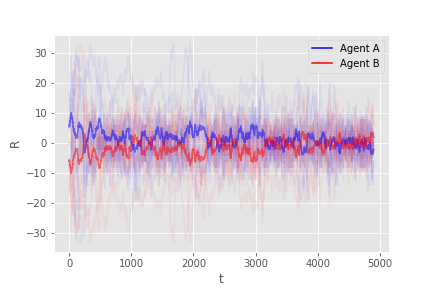

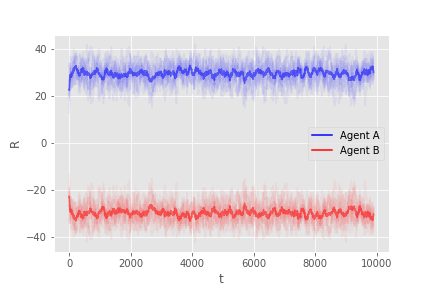

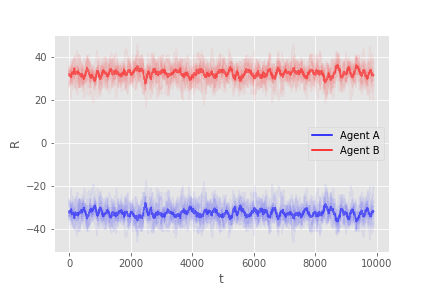

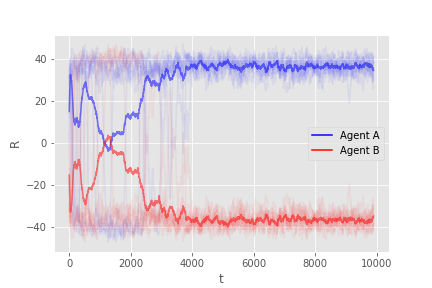

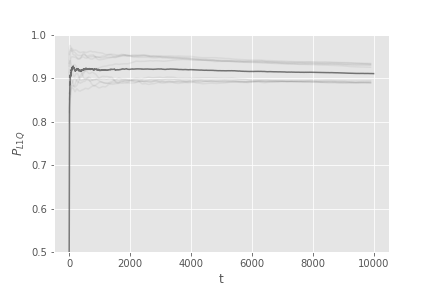

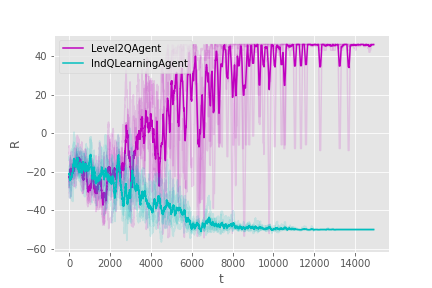

In Chapter 4, we turn our attention form supervised learning to reinforcement learning (RL), addressing the challenge of supporting an agent in a sequential decision making setting where there can be adversaries, specifically modelled as other players. We introduce Threatened Markov Decision Processes (TMDPs) as an extension of the classical Markov Decision Process framework for RL. We also propose a level- thinking scheme resulting in a novel learning approach to deal with TMDPs. After introducing our framework and deriving theoretical results, relevant empirical evidence is given via extensive experiments, showing the benefits of accounting for adversaries in RL while the agent learns.

Finally, Chapter 5 sums up with several conclusions and avenues for further work.

The following papers derived from this thesis have been published or already accepted:

- •

- •

- •

- •

- •

The following papers derived from this thesis are under submission:

- •

- •

- •

- •

- •

Resumen

El campo del aprendizaje automático (AA) ha experimentado un auge espectacular en los últimos años, tanto en desarrollos teóricos como en áreas de aplicación. Sin embargo, la rápida adopción de las metodologías del AA ha mostrado que los modelos que habitualmente se emplean para toma de decisiones no tienen en cuenta la incertidumbre en sus predicciones o, más crucialmente, pueden ser vulnerables a ejemplos adversarios, datos manipulados estratégicamente con el objetivo de engañar estos sistemas de AA. Por ejemplo, en el sector de la hostelería, un modelo puede predecir unas ventas esperadas muy altas para la semana que viene, fijado cierto plan de inversión en publicidad. Sin embargo, la varianza predictiva también puede ser muy grande, haciendo la predicción escasamente útil según el nivel de riesgo que el negocio pueda tolerar. O, en el caso de la detección de spam, un atacante puede introducir palabras adicionales en un correo de spam para evadir el ser clasificado como tal y aparecer legítimo. Por tanto, creemos que desarrollar sistemas de AA que puedan tener en cuenta también las incertidumbres en las predicciones y ser más robustos frente a ejemplos adversarios es una necesidad para tareas críticas en el mundo real. Esta tesis es un paso hasta alcanzar este objetivo.

En el capítulo 1, empezamos con un caso de estudio en el sector de la hostelería. Proponemos una implementación robusta del modelo de Nerlove-Arrow usando un modelo estructural bayesiano de series temporales para explicar la relación entre las inversiones en publicidad con las ventas semanales de una cadena nacional de restaurantes de comida rápida. Su naturaleza bayesiana facilita incorporar conocimiento a priori que refleje las creencias del gestor, y pueden actualizarse con datos observados. Sin embargo, este caso de estudio emplea técnicas bayesianas ya clásicas, como el muestreador de Gibbs. Hoy en día, el panorama del AA está repleto de modelos complejos, enormes en cuanto a número de parámetros. Este es caso de las redes neuronales, así que en este capítulo también resumimos los avances recientes en este subcampo. Tres desafíos constituyen el cuerpo de esta tesis.

El capítulo 2 va dedicado al primer desafío. En él, atacamos el problema de escalar la inferencia Bayesiana a modelos complejos o regímenes de grandes datos. En la primera parte, proponemos una visión unificadora de dos algoritmos de inferencia Bayesiana, Monte Carlo mediante cadenas de Markov con Gradientes Estocásticos y Descenso por el Gradiente Variacional Stein, llegando a esquemas mejorados y eficientes de inferencio. En la segunda parte, desarrollamos una metodología para mejorar la eficiencia de la inferencia bayesiana mediante el anidamiento de un muestreador basado en cadenas de Markov dentro de una aproximación variacional. A esta metodología la llamamos "aproximación variacional refinada". La metodología conlleva varios beneficios, como su facilidad de implementación y el ajuste automático de los hiperparámetros del muestreador, logrando tiempos de convergencia más rápidos gracias a la diferenciación automática. Los experimentos muestran el rendimiento superior de ambos desarollos comparado con algunas alternativas.

En el capítulo 3, nos centramos en el desafío de proteger clasificadores de AA de los ejemplos adversarios. Hasta ahora, la mayoría de enfoques en clasificación adversaria han seguido el paradigma clásico de teoría de juegos. Esto requiere condiciones poco realistas de conocimiento común, que no son admisibles en entornos típicos en seguridad del aprendizaje automático adversario. Tras revisar estos enfoques, presentamos una perspectiva alternativa basada en análisis de riesgos adversarios y aprovechamos las técnicas bayesianas escalables del capítulo 3.

En el capítulo 4, pasamos nuestra atención del aprendizaje supervisado al aprendizaje por refuerzo (AR), incidiendo en el desafío de apoyar un agente en un escenario de toma de decisiones secuenciales en el que puede haber adversarios, modelizados como otros jugadores. Introducimos los Procesos de Decisión de Markov Amenazados como una extensión del paradigma clásico de los procesos de decisión Markovianos. También proponemos un esquema basado en pensamiento de nivel- resultando en un nuevo algoritmo de aprendizaje. Tras introducir la metodología y derivar algunos resultados teóricos, damos evidencia empírica relevante mediante experimentos extensos, mostrando los beneficios de modelizar oponentes en AR mientras el agente aprende.

Finalmente, en el capítulo 5 terminamos con varias conclusiones y posibles extensiones para trabajo futuro.

Los siguientes artículos derivados de esta tesis ya han sido publicados o están aceptados:

- •

- •

- •

- •

- •

Los siguientes artículos derivados de esta tesis se encuentran bajo revisión:

- •

- •

- •

- •

- •

Agradecimientos

Estos cuatro años de tesis se han pasado volando. Aunque se hayan materializado en parte en este documento, no puedo olvidarme de todas las personas que, de un modo u otro, han contribuido a este trabajo.

En primer lugar, debo agradecer enormemente la labor y apoyo de mis directores durante este período. A David Ríos, especialmente por su incansable atención y paciencia, sobre todo al leer mis textos y dudas; y a David Gómez-Ullate, por darme la oportunidad de empezar en este mundo de los datos hace ya cinco años. Gracias a los dos por todas las oportunidades. Les considero verdaderos mentores de los que he podido aprender muchísimo en estos años, no solo acerca de los temas de esta tesis, así que espero seguir manteniendo nuestra relación en el futuro.

Asimismo, debo agradecer la labor del Prof. David Banks, quien me dio la oportunidad de hacer una estancia de investigación en Duke y SAMSI, resultando en una experiencia muy enriquecedora académica y vitalmente. También agradezco al Ministerio por la beca FPU16-05034, la cátedra AXA-ICMAT, el programa “Severo Ochoa”

para Centros de Excelencia en I+D, y la Fundación BBVA, entre otros.

También quería mencionar a los compañeros y amigos hechos en el grupo formado en el Datalab del ICMAT y el vecino IFT (y algunos por extensión ya, en Komorebi). Roi, David, Alberto R., Alberto T., Simón, Jorge, Bruno, April, Aitor, Alex, Nadir, Christian…

Lamento que por la pandemia apenas nos veamos ya por el campus, pero siempre me acordaré de tantos buenos momentos. También quiero mostrar mi agradecimiento a los investigadores Pablo Angulo y Pablo Suárez, por haber tenido el placer de trabajar con ellos al principio de mi carrera. Y a Marta Sanz, por estar siempre dispuesta a resolver cualquier trámite.

Por último, mención especial merecen mis padres, Sotero y María, siempre dándome su apoyo y cuidado incondicional a pesar de todo. E Irene, por acompañarme siempre ahí y quien me hizo ver que todo es posible, con toda su ilusión, ingenio y magia. Gracias, os quiero.

Chapter 1 Introduction

1.1 A motivation for Bayesian methods

Statistical decision theory [89] is a fundamental block of modern machine learning and statistics research and practice, providing fundamental tools for analyzing the vast amount of data that have become available in science, government, industry, and everyday life. Over the last century, many problems have been solved (at least partially) with probabilistic models [28], such as classifying email as spam, identifying patterns in genetic sequences, recommending similar movies or performing automatic translation between two languages. For each of these applications, a statistical model was fitted to the data, typically solving the task at hand. Since the previous applications were incredibly diverse, models came from different research communities. But there was a common theme shared amongst them: the need to support a decision using the model. Thus, statistical decision theory emerged as a powerful framework to reason between different scientific areas.

We believe that building and using probabilistic models is not a single-step task, but rather an iterative process, closely resembling the scientific method [63]. First, propose a simple model based on the latent structure that your prior knowledge make you believe exists in the data. Then, given a data set, use an inference method to approximate the posterior distribution of the parameters given the data. Lastly, use that posterior to test the model against new, test data. If not satisfied, we criticise and revise it, and we modify the model, iterating all over again. This is called the Box’s loop [34, 33]. It focuses on the scientific method, producing new knowledge through iterative experimental design, data collection, model formulation, and model criticism. Amongst all the different paradigms in statistics, the one that is closest to the previous approach to knowledge discovery is Bayesian analysis [103, 136], and this will be the one adopted in this thesis.

In the past years, we have witnessed the success of neural networks and deep learning, achieving state of the art results in many different tasks [163]. A brief introduction to deep learning will appear in Section 1.3, but let us advance a few things here. Bayesian analysis is specially compelling for this kind of models, mostly because the object of interest is now the predictive distribution,

with being a sample to be classified or regressed, the predicted target, the training dataset, and the parameters of a neural network. The previous marginalization equation expresses epistemic uncertainty, that is, uncertainty over which configuration of parameters (hypothesis) is correct, given limited data. If the posterior is sharply peaked, it makes no difference using a Bayesian approach versus the standard maximum likelihood or maximum a posteriori estimations, since just a single point mass may be a reasonable approximation to the posterior. However, neural networks are typically very underspecified by the training data available (a state of the art NN might have millions of parameters for just thousands of data points), and will thus have diffuse likelihood distributions , leading to flatter posteriors which are also multi-modal.

Indeed, there are large valleys in the loss landscape of neural networks [101], over which parameters incur very little loss, but give rise to different high performing functions which make meaningfully different predictions on the test dataset. The work of [302] also demonstrates the variety of well-performing solutions that can be expressed by a neural network posterior, as it is highly flexible. In these cases, we desire to perform Bayesian model averaging, since it leads to an ensemble of diverse yet good models, achieving better generalization and performance stability capabilities than classical training.

In this thesis, we provide several contributions to large scale Bayesian machine learning, motivated by the following case study. On the one hand, it serves us to introduce notation and key concepts, and, on the other hand, the case will motivate our three main problems of interest.

1.2 A case study in retailing

1.2.1 Context

It is widely acknowledged that a firm’s expenditure on advertising has a positive effect on sales [9, 273, 189, 289]. However, the exact relationship between them remains a moot point, see [272] for a broad survey. Since [74] seminal work several models have been proposed to pinpoint this relationship, although consensus on the best approach has not been reached yet. Two diverging model-building schools seem to dominate the marketing literature [177]: a priori models rely heavily on intuition and are derived from general principles, although usually with a practical implementation on mind ([212], or [280] and [176], inter alia); and statistical or econometric models, which usually start from a specific dataset to be modelled, e.g. [9]). Here we will mostly rely on the first type of models, viz. that of [212], which extends [74] to a dynamic setting [14] and adapts seamlessly to the state-space or structural time series approach.

Bayesian structural time series models [254], in turn, have positioned themselves in the past few years as very effective tools not only for analysing marketing time-series, but also to throw light into more uncertain terrains like causal impacts, incorporating a priori information into the model, accommodating multiple sources of variations or supporting variable selection. Although the origins of this formalism can be traced back to the 1950’s in the engineering problems of filtering, smoothing and forecasting, first with [288] and specially with [139], these problems can also be understood from the perspective of estimation in which a vector valued time series that we wish to estimate (the latent or hidden states) is observed through a series of noisy measurements . This means that, in the Bayesian sense, we want to compute the joint posterior distribution of all states given all the measurements [251]. The ever-growing computing power and release of several programming libraries in the last few years like [221, 253] have in part alleviated the difficulties in the implementation that this formalism suffers, making these methods broadly known and used. This family of models have been used successfully to, e.g., model financial time series data [45], infer causal impact of marketing campaigns [37], select variables and nowcast consumer sentiment [255], or for predicting other economic time series models like unemployment [254].

We use the formalism of Bayesian structural time-series models to formulate a robust model that links advertising expenditures with weekly sales. Due to the flexibility and modularity of the model, it will be well suited to generalization to various markets and scenarios. Its Bayesian nature also adapts smoothly to the issue of introducing prior information. The formulation of the model allows for non-gaussian innovations of the process, which will take care of the heavy-tailedness of the distribution of sales increases. We also discuss how the forecasts produced by this model can help the manager in allocating the advertising budget. The decision space is reduced to a one dimensional curve of Pareto optimal strategies for two moments of the forecast distribution (expected return and variance).

1.2.2 Theoretical background and model definition

The Nerlove-Arrow model.

Numerous formulations of aggregate advertising response models exist in the literature, e.g. [177]. The model of [212] extends the Dorfman-Steiner model to cover the situation in which current advertising expenditures affect future product demand; it is parsimonious and is considered a standard in the quantitative marketing community. We use it as our starting point.

In this model, advertising expenditures are considered similar in many ways to investments in durable plant and equipment, in the sense that they affect the present and future character of output and, hence, the present and future net revenue of the investing firm. The idea is to define an “advertising stock” called goodwill which seemingly summarizes the effects of current and past advertising expenditures over demand. Then, the following dynamics is defined for the goodwill

| (1.1) |

where is the advertising spending rate (e.g., euros or gross rating points per week), is a parameter that reflects the advertising quality (an effectiveness coefficient) and is a decay or forgetting rate. Goodwill then increases linearly with advertisement expenditure but decreases also linearly due to forgetting.

Several extensions and modifications have been proposed to this simple model: it can include a limit for potential costumers [280], a non-linear response function to advertise expenditures [176], wear-in and wear-out effects of advertising [207], interactions between different advertising channels [21], among others. Still, for most tasks, the Nerlove-Arrow model remains as a simple and solid starting point.

Bayesian structural time series models.

Structural time series models or state-space models provide a general formulation that allows a unified treatment of virtually any linear time series model through the Kalman filter and the associated smoother. Several handbooks [76, 222, 251, 287] discuss this topic in depth. We will present a few salient features that concern our modelling problem. For further details, the reader may check the aforementioned handbooks.

The state-space formulation of a time series consists of two different equations: the state or evolution equation which determines the dynamics of the state of the system as a first-order Markov process — usually parametrized through state variables — and an observation or measurement equation which links the latent state with the observed state. Both equations are also affected by noise.

| (1.2) |

The states () are not generally observable, but are linked to the observation variables through the observation equation:

| (1.3) |

We shall point out that the noise terms and are uncorrelated. We denote by the state vector describing the inner state of the system, by the matrix that generates the dynamics, and by a vector of serially uncorrelated disturbances with mean zero and covariance matrix . is the matrix that links the inner state to the observable, and is the variance of , the random disturbances of the observations.

The specification of the state-space system is completed by assuming that the initial state vector has mean and a covariance matrix and it is uncorrelated with the noise. The problem then consists of estimating the sequence of states for a given series of observations and whichever other structural parameters of the transition and observation matrices. State estimation is readily performed via the Kalman filter; different alternatives however arise when structural parameters are unknown. In the classical setting, these are estimated using maximum likelihood. In the Bayesian approach, the probability distribution about the unknown parameters is updated via Bayes Theorem. If exact computation through conjugate priors is not possible, the probability distributions before each measurement are updated by approximate procedures such as Markov chain Monte Carlo (MCMC) [254].

The Bayesian approach offers several advantages compared to classical methods. For instance, it is natural to incorporate external information through the prior distributions. In particular, this will be materialized in Section 1.2.2 where expert information is incorporated through the spike and slab prior. Another useful advantage is that, due to the Bayesian nature of the model, it is straightforward to obtain predictive intervals through the predictive distribution (see Section 1.2.2).

Model specification.

The continuous-time Nerlove-Arrow model must be first cast in discrete time so as to formulate our model in state-space. From equation (1.1), we get

where is the goodwill stock, is the advertising spending rate, is the effectiveness coefficient, the random disturbance captures the net effects of the variables that affect the goodwill but cannot be modelled explicitly, and with . This discrete counterpart of Nerlove-Arrow is a distributed-lag structure with geometrically declining weights, i.e., a Koyck model [60, 153]. Since in our setting the model includes the effect of different channels in the goodwill, we modify the previous equations to:

Now, following (1.2) and (1.3), the discrete-time Nerlove-Arrow model in state-space form will read:

- Evolution equation:

-

(1.4) where

Note that the are constant over time and that the matrix depends on the known inversion levels at time and on an unknown parameter () to be estimated from the data.

- Observation equation:

-

(1.5) where are the observed sales at time and .

Modularity and additional structure.

The above model is very flexible in the sense that it can be defined modularly, in as much as different hidden states evolve independently of the others (i.e. the evolution matrix can be cast in block-diagonal form). This greatly simplifies their implementation and allows for simple building-blocks with characteristic behavior. Typical blocks specify trend and seasonal components — which can be helpful to discover additional patterns in the time series— or explanatory variables that can be added to further reduce uncertainty in the model and bridge the gap between time series and regression models. Via the superposition principle [222, Chapter 3] we could include additional blocks in our model

Regression components. Spike and slab variable selection.

To take into account the effects of external explanatory variables such as the weather or sport events, a regression component can be easily incorporated into the model through

where the state is constant over time to favor parsimony.

A spike and slab prior [201] is used for the regression component, since it can incorporate prior information and also facilitate variable selection. This is specially useful for models with a large number of regressors, a typical setting in business scenarios. Let denote a binary vector that indicates whether the regressors are included in the regression. Specifically, if and only if . The subset of for which will be denoted . Let be the residual variance from the regression part. The spike and slab prior [104] can be expressed as

A usual choice for the prior is a product of Bernoulli distributions:

The manager of the firm may elicit these in various ways. A reasonable choice when detailed prior information is unavailable is to set all . Then, we may specify an expected number of non-zero coefficients by setting , where is the total number of regressors. Another possibility is to set if the manager believes that the th regressor is crucial for the model.

Model estimation and forecasting

Model parameters can be estimated using Markov Chain Monte Carlo simulation, as described in Chapter 4 of [222] or [254]. We follow the same scheme.

Let be the set of model parameters other than and . The posterior distribution can be simulated with the following Gibbs sampler

-

1.

Simulate .

-

2.

Simulate .

-

3.

Simulate .

Defining and repeatedly iterating the above steps gives a sequence of draws . In our experiments, we set and discard the first 2000 draws to avoid burn-in issues.

In order to sample from the predictive distribution, we follow the usual Bayesian approach summarized by the following predictive equation, in which denotes the sequence of observed values, and denotes the set of values to the forecast

assuming conditional independence of and given . Thus, it is sufficient to sample from , which can be achieved by iterating through equations (1.3) and (1.2). With these predictive samples we can compute statistics of interest regarding the predictive distribution such as the mean or variance (MC estimates of and , respectively) or quantiles of interest.

Robustness.

We can replace the assumption of Gaussian errors with student- errors in the observation equation, thus leading to the model

Typically, in these settings we set to impose a finite variance, and this variance parameter can be estimated from data using empirical Bayes methods, for instance. In this manner, we allow the model to predict occasional larger deviations, which is reasonable in the context of forecasting sales. For instance, a special event not taken into account through the predictor variables may lead to an increase in the sales for that week.

1.2.3 Case Study. Data and parameter estimation

Data analysis.

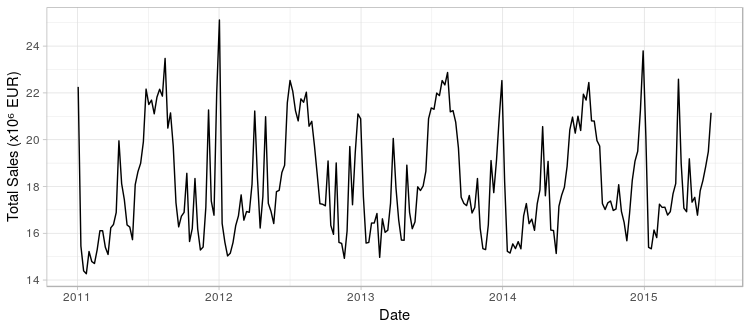

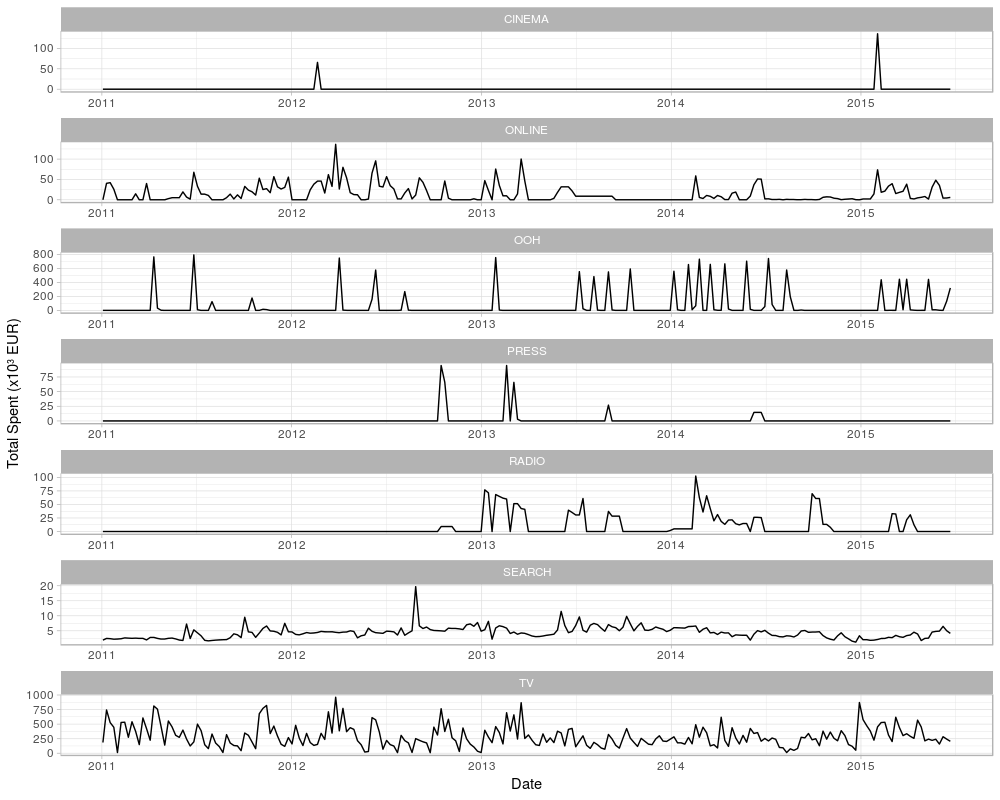

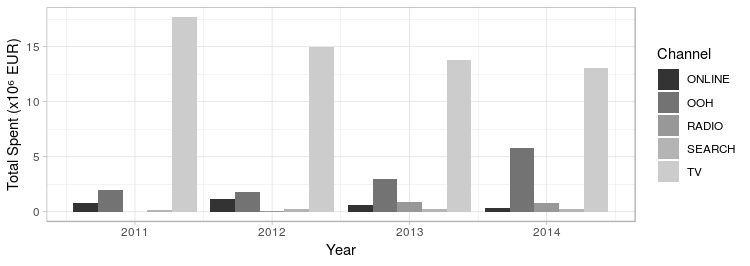

The time series analyzed in this case study contains the total weekly sales of a country-wide franchise of fast food restaurants, Figure 1.1, covering the period January 2011 - June 2015, thus comprising 234 observations. The total weekly sales is in fact the aggregated sum from the individual sales of the whole country network of 426 franchises. Along with the sales figures, the series includes the investment levels in advertising during this period for seven different channels viz. OOH (Out-of-home, i.e. billboards), Radio, TV, Online, Search, Press and Cinema, Figure 1.2, .

Note different scales on y-axis.

From such graphs we observe that:

-

•

In Figure 1.1, the series has a characteristic seasonal pattern that shows peaks in sales coinciding with Christmas, Easter and summer vacations.

-

•

In Figure 1.2 we observe that the investment levels at each channel vary largely in scale, with investments in TV, and OOH dominating the other channels.

-

•

The investment strategies adopted by the firm at each channel are also qualitatively different. Some of them show spikes while others depict a relatively even spread investment across time.

A handful of other predictors which are also known to affect sales will be used in the model, all of them weekly sampled

-

•

Global economic indicators: unemployment rate (Unemp_IX), price index (Price_IX) and consumer confidence index (CC_IX).

-

•

Climate data: average weekly temperature (AVG_Temp) and weekly rainfall (AVG_Rain) along the country.

-

•

Special events: holidays (Hols) and important sporting events (Sport_EV).

Experimental setup.

Following the notation in Section 1.2.2, we consider three model variants for the particular dataset in increasing order of complexity

-

•

Baseline model, which makes use of no external variables

-

•

Auto-regression: this model (we will refer to it as RA) incorporates the external ambient and investment variables, so the equation of the model becomes

(1.6) We select an expected model size111Defined as the average number of selected regression features. of 5 in the spike and slab prior, letting all variables to be treated equally.

-

•

Regression (forcing): the model has same equation as Eq. (1.6) (we will refer to it as RF). However, in the prior we force investment variables to be used by setting their corresponding , and imposing an expected model size of 5 for the rest of the variables.

In all cases, only the five main advertising channels (TV, OOH, ONLINE, SEARCH and RADIO) will be used; the remaining two (CINEMA and PRESS) are sensibly lower both in magnitude and frequency than the others so we can safely disregard them in a first approximation.

As customary in a supervised learning setting with time series data, we perform the following split of our dataset: since it comprises four years of sales, we take the first two years of observations as training set, and the rest as holdout, in which we assess several predictive performance criteria. Before fitting the data, we scale the series to have zero mean and unit variance as this increases MCMC stability. Reported sales forecasts are transformed back to the original scale for easy interpretation. The models were implemented in R using the bsts package [253].

1.2.4 Discussion of results

It is customary to aim at models achieving good predictive performance. For this reason, we test our three models using two metrics

-

•

Mean Absolute Percentage Error

where denotes the actual value; , the mean one-step-ahead prediction; and, is the length of the hold-out period.

-

•

Cumulative Predicted Sales over a year

where denotes the set of time-steps contained in year .

These scores are reported in Table 1.1 with sales in million EUR. Note that the models which include external information (RA and RF) achieve better accuracy than the baseline. In addition, predictions are unbiased, since cumulative predictions are extremely close to their observed counterparts. Overall, we found the predictive performance of our models to be successful for a business scenario, as we achieve under 5% relative absolute error using the variants augmented with external information. This is clearly useful for a decision maker who wants to forecast their weekly sales one week ahead to within a 5% error in the estimation.

| Model | MAPE | ||

|---|---|---|---|

| B | 5.85% | 9660 | 9627 |

| RA | 4.62% | 9680 | 9613 |

| RF | 4.59% | 9665 | 9582 |

| Cumulative True Sales: | 9666 | 9610 | |

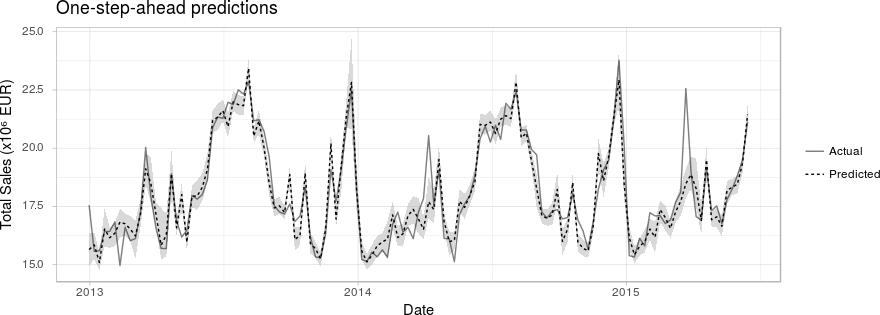

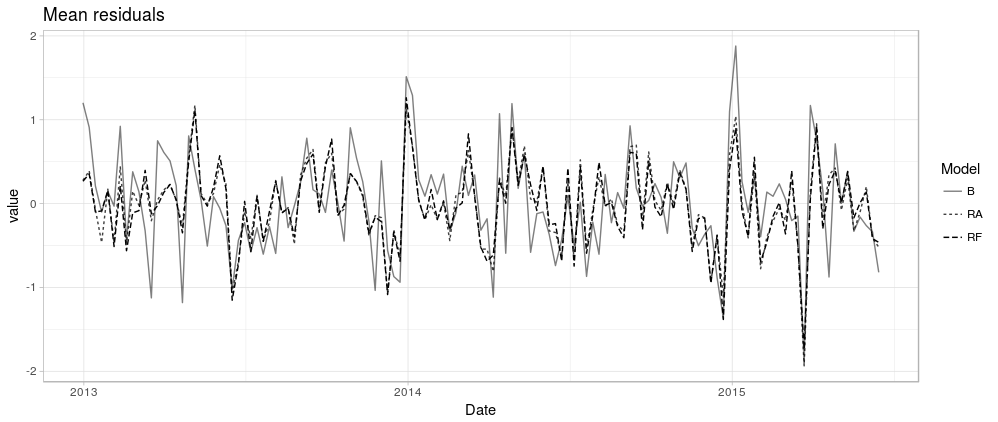

Figure 1.3 displays the predictive ability of model RF over the hold-out period. The model seems sufficiently flexible to adapt to fluctuations such as Christmas peaks. Predictive intervals also adjust their width with respect to the time to reflect varying uncertainty, yet in the worst cases they are sufficiently narrow. Further information can be tracked in Figure 1.4, where mean standardized residuals are plotted for each model variant. Notice that the residuals for models RA and RF are roughly comparable, being both sensibly smaller than those of the baseline. This means that the simpler Nerlove-Arrow model benefits from the addition of the ambient variables , as suggested in Table 1.1.

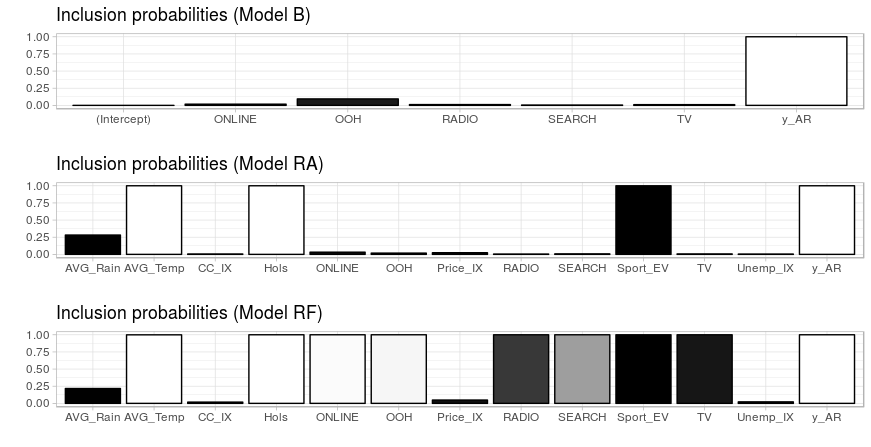

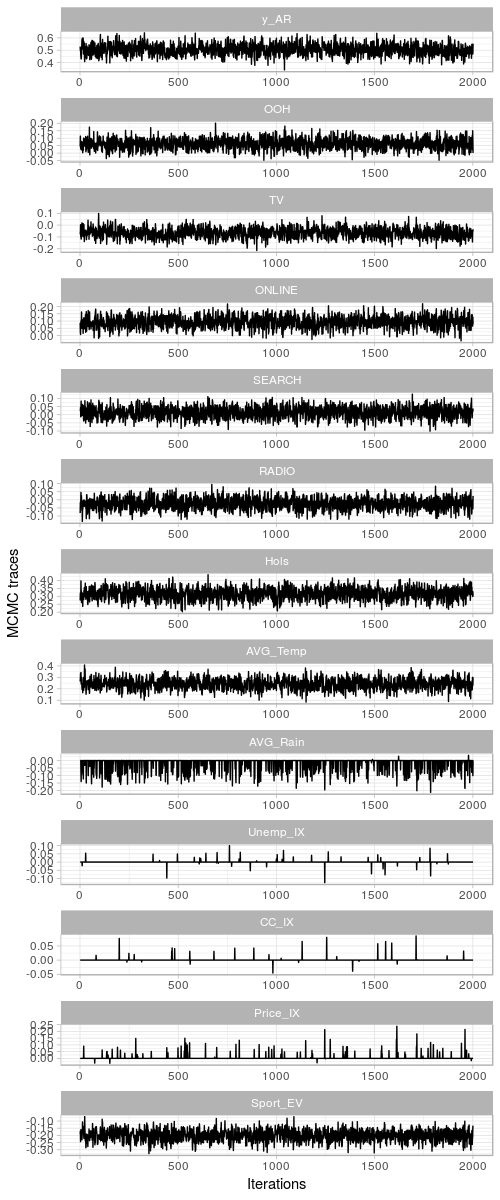

Having built good predictive models, we inspect them more closely with the aim of performing valuable inferences in our business setting. The average estimated parameter and expected standard deviations of the coefficients for the different advertising channels are displayed in Table 1.2. We also show the weights of the ambient variables for the augmented models RA and RF in Table 1.3, as well as the probability of a variable being selected in the MCMC simulation for a given model in Figure 1.5. Convergence diagnostics of the MCMC scheme are reported in Appendix 1.A.

| Model B | Model RA | Model RF | ||||

| Channel | mean | sd | mean | sd | mean | sd |

| y_AR | 8.00e-01 | 5.10e-02 | 5.17e-01 | 4.50e-02 | 5.07e-01 | 4.55e-02 |

| OOH | 9.30e-03 | 3.11e-02 | 1.15e-03 | 9.54e-03 | 6.10e-02 | 3.54e-02 |

| ONLINE | 1.10e-03 | 9.25e-03 | 1.95e-03 | 1.23e-02 | 9.04e-02 | 4.01e-02 |

| RADIO | -5.34e-04 | 6.80e-03 | -2.61e-05 | 2.30e-03 | -2.57e-02 | 3.42e-02 |

| TV | -2.85e-04 | 5.12e-03 | -5.53e-05 | 3.71e-03 | -6.14e-02 | 4.21e-02 |

| SEARCH | 1.51e-05 | 2.74e-03 | 8.58e-05 | 2.49e-03 | 1.38e-02 | 3.50e-02 |

| Model RA | Model RF | |||

|---|---|---|---|---|

| Channel | mean | sd | mean | sd |

| Sport_EV | -2.06e-01 | 3.80e-02 | -2.00e-01 | 3.71e-02 |

| AVG_Temp | 2.57e-01 | 4.43e-02 | 2.43e-01 | 4.65e-02 |

| Hols | 3.10e-01 | 3.70e-02 | 3.15e-01 | 3.72e-02 |

| AVG_Rain | -2.86e-02 | 5.01e-02 | -1.96e-02 | 4.14e-02 |

| Price_IX | 1.38e-03 | 1.15e-02 | 3.60e-03 | 1.92e-02 |

| Unemp_IX | 6.34e-05 | 3.32e-03 | 2.36e-04 | 7.79e-03 |

| CC_IX | 6.27e-07 | 2.94e-03 | 2.85e-04 | 5.50e-03 |

Looking at the ambient variables, the following comments seem in order:

-

•

From Table 1.3 we see that the socio-economic indicators (unemployment rate, inflation and consumer confidence) do not seem statistically relevant for this problem.

-

•

Looking at the sign of the coefficients of the most significant regressors (Hols, Sport_EV, AVG_Temp and AVG_Rain) we see that they are as we would naturally expect. Moreover, their absolute value is well above the error in both models RA and RF, a strong indicator of their influence in the expected weekly sales (cf. Table 1.3, Figure 1.5).

-

•

We see, for instance, that sporting events are negatively correlated with sales. This can be interpreted as follows: major sporting events in the country where the data have been recorded receive a large media coverage and are followed by a significant fraction of the population. The chain in this study has no TVs broadcasting in their restaurants, so customers probably choose alternative places to spend their time on a day when Sport_EV = 1.

-

•

The sign of Hols and AVG_Temp is positive, showing strong evidence for the fact that sales increase in periods of the year where potential customers have more leisure time, like national holidays or summer vacation.

-

•

One would expect AVG_Rain to be negatively correlated with restaurant sales, but in our study (despite having negative sign) it is not statistically significant. A possible explanation is that AVG_Rain records average rainfall over a large country.

Next, we turn our attention to the investment variables across different advertising channels.

-

•

The advertising channels are almost never selected in model RA, and their coefficients are not significantly higher than their errors to be considered influential in the model. In model RF, however, there is strong evidence that their effect is more than a random fluctuation (cf. Table 1.2, Figure 1.5).

-

•

The negative sign in both RADIO and TV in all three models suggests that (at least locally) part of the expenditures in these two channels should be diverted towards other channels with positive sign on their coefficients, specially to the channel with the strongest positive coefficient (ONLINE and OOH).

-

•

It is interesting that the trend that shows the year-to-year advertising budget of this firm (cf. figure 1.6) has a significant reduction in TV expenditures and a big increase in OOH. RADIO however is not reduced accordingly but increased, and ONLINE — which our model considers the best local inversion alternative — follows the inverse path222It has to be noted, however, that ONLINE expenditures are typically correlated with discounts, coupons and offers, and this information was not available to us..

-

•

The autoregressive term is close to , which means that the immediate effect of advertising is roughly half to the long run accumulated effects.

Budget allocation. Model-based solutions.

Based on the above, we propose a model which can be used as a decision support system by the manager, helping her in adopting the advertising investment strategy. The company is interested in maximizing the expected sales for the next period, subject to a budget constraint for the advertising channels and also a risk constraint, i.e., the variance of the predicted sales must be under a certain threshold. This optimization problem based on one-step-ahead forecasts can be formulated as a non linear, but convex, problem that depends on parameter :

| subject to | |||||

where is the total advertising budget for week and is a parameter that controls the risk of the sales. We have made explicit the dependence on the regressor variables and advertisement investments in the mean and variance expressions. Solving for different values of , we obtain a continuum of Pareto optimal investment strategies that we can present to the manager, each one representing a different trade-off between risk and expected sales that we can plot in a risk-return diagram. This approach greatly reduces the decision space for the manager.

A possible alternative would be to rewrite the objective function as

which may be regarded as a lower quantile if the predictive samples are normally distributed. As in the previous approach, different values of represent different risk-return trade-offs.

If the errors in the observation equation (1.3) are normal, the computations for expected predicted sales and the above variance can be done exactly, and quickly, using conjugacy as in [283, 3.7.1]. Otherwise, the desired quantities must be computed through Monte Carlo simulation, as in Section 1.2.2.

Note that due to the nature of the state-space model, it is straightforward to extend the previous optimization problem over timesteps, for . The two objectives would be the expected total sales and the total risk over the period . For normally distributed errors, the predicted sales on the period also follow a Normal distribution, which makes computations specially simple.

The above optimization problem may not need to be solved by exhaustively searching over the space of possible channel investments. In a typical business setting, the manager would consider a discrete set of investment strategies that are easy to interpret, so she may perform simulations of the predictive distribution and use the above strategy to discard the Pareto suboptimal strategies.

1.2.5 Discussion

We have developed a data-driven approach for the management of advertising investments of a firm. First, using the firm’s investment levels in advertising, we propose a formulation of the Nerlove-Arrow model via a Bayesian structural time series to predict an economic variable (global sales) which also incorporates information from the external environment (climate, economical situation and special events). The model thus defined offers low predictive errors while maintaining interpretability and can be built in a modular fashion, which offers great flexibility to adapt it to other business scenarios. The model performs variable selection and allows to incorporate prior information via the spike-and-slab prior. It can handle non-gaussian deviations and also provides hints to which of the advertising channels are having positive effects upon sales. The model can be used as a basis for a decision support system by the manager of the firm, helping with the task of allocating ad investments.

This model could be expanded in several ways. For instance, in regimes where the data is of high frequency or there are large amounts of it, the Gibbs sampler from Section 1.2.2 could be replaced with a more scalable sampler, such as the ones developed in Chapter 2 of this thesis. We could also take into account the presence of competing retailing firms, which could impact the expected sales of the supported franchise. The next two chapters are devoted to taking the account the presence of adversaries in ML models, both in classification (Chapter 3) and reinforcement learning settings (Chapter 4). For this we require first briefly reviewing some earlier work.

1.3 State of the art models and big data

1.3.1 Introduction

The history of neural network (NN) models have gone through several waves of popularity. The first one starts with the introduction of the perceptron by [246] and its training algorithm for classification in linearly separable problems. Limitations brought up by [200] somehow reduced the enthusiasm about these models by the early 70’s. The next period of success coincides with the emergence of results presenting NNs as universal approximators, e.g. [66]. Yet technical issues and the emergence of other paradigms like support vector machines led, essentially, to a new stalmate by the early 2000’s. Finally, several of the technical issues were solved, coinciding with the availability of faster computational tools, improved algorithms and the emergence of large annotated datasets. These produced outstanding applied developments leading, over the last decade, to the current boom surrounding deep NNs [110].

This section overviews recent advances in NNs. There are numerous reviews with various emphasis including physical [47], computational [57], mathematical [279] and pedagogical [13] pùrposes, notwithstanding those concerning different application areas, from autonomous driving systems (ADS) [116] to drug design [121], to name but a few. Our emphasis is on statistical aspects and, more specifically, on Bayesian approaches to NN models for reasons that will become apparent during this thesis but include mainly: the provision of improved uncertainty estimates, which is of special relevance in decision support under uncertainty; their increased generalization capabilities; their enhanced robustness against adversarial attacks; their improved capabilities for model calibration; and the possibility of using sparsity-inducing priors to promote simpler NN architectures.

1.3.2 Shallow neural networks

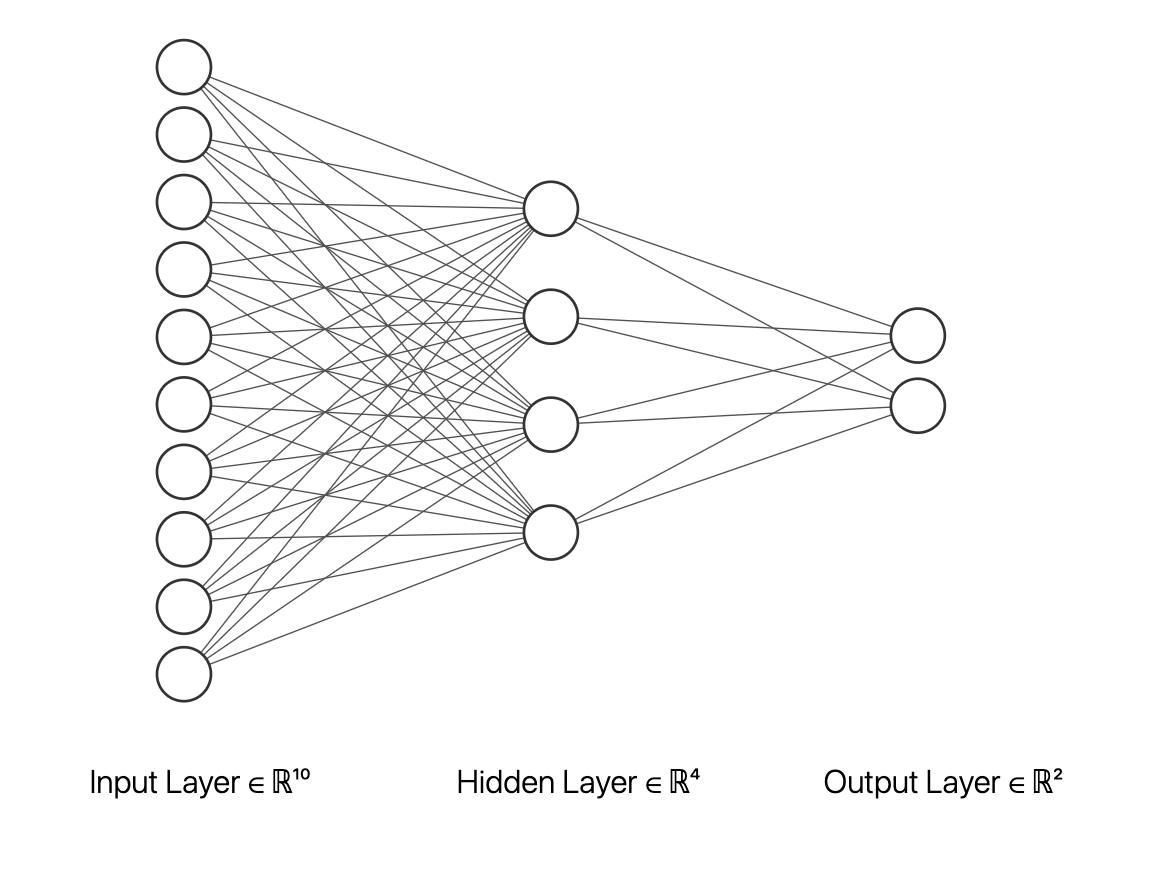

This section briefly introduces key concepts about shallow networks to support later discussions on current approaches. Our focus will be mainly on nonlinear regression problems. Specifically, we aim at approximating an -variate response (output) with respect to explanatory (input) variables through the model

| (1.7) | |||||

This defines a neural network with one hidden layer with hidden neurons and logistic activation functions. Figure 1.7 sketches a graphical model of a shallow NN with 10 inputs, 4 hidden nodes and 2 outputs.

Let us designate with and the network parameters. will be considered a hyperparameter. Clearly, the model is linear in but non-linear in . Interest in this type of models stems from results such as those of [66] who presents them as universal approximators: any continuous function in the -dimensional unit cube may be approximated by models of type when the functions are sigmoidal (as with the logistic) and . Our discussion focuses on .

Classical approaches.

Given observations , maximum likelihood estimation (MLE) computes the log-likelihood and maximises it leading to the classical non-linear least squares problem

| (1.8) |

Quite early, researchers paid attention to the introduction of regularisers, such as weight decay penalization [156], so as to improve model generalization, leading to the modified optimisation problem

| (1.9) |

where represents the regularisation term. For example, in the above mentioned case, the additional term is .

Typically problems (1.8) and (1.9) are solved via steepest gradient descent [199] through iterations of the type

where is frequently chosen as a fixed small learning rate parameter and is the gradient of function , with respect to . Very importantly, the structure of the network and the chain rule of calculus facilitates efficient estimation of the gradients via backpropagation, e.g. [249].

A problem entailed by NN model estimation is the highly multimodal nature of the log-likelihood for three reasons: invariance with respect to arbitrary relabeling of parameters (these may be handled by means of order constraints among the parameters); inherent non-linearity; and, finally, node duplicity (which may be dealt with a model reflecting uncertainty about the number of nodes, as explained below). A way to mitigate multimodality is to use a global optimization method, like multistart, but this is very demanding computationally in this domain.

Finally, note that the same kind of NN models may be used for nonlinear auto-regressions in time series analysis [197] and non-parametric regression [237]. Moreover, similar models may be used for classification purposes, although this requires modifying the likelihood [28] to e.g.

| (1.10) |

that is, a draw from a multinomial distribution with classes. Class probabilities can be computed using the softmax function,

Bayesian approaches.

We discuss now Bayesian approaches to shallow NNs. assuming standard priors in Bayesian hierarchical modeling, see e.g. [160]: and , completed with priors over the hyperparameters , , , and . In this model, an informative prior probability model is meaningful as parameters are interpretable. For example, the ’s would reflect the order of magnitude of the data ; typically positive and negative values for would be equally likely, calling for a symmetric prior around 0 with a standard deviation reflecting the range of plausible values for . Similarly, a range of reasonable values for the logistic coefficients will be determined mainly to address smoothness issues.

Initial attempts to perform Bayesian analysis of NNs, adopted arguments based on the asymptotic normality of the posterior, as in [195] and [41]. However these methods fail if they are dominated by less important modes. [41] mitigate this by finding several modes and basing inference on weighted mixtures of the corresponding normal approximations, but we return to the same issue as some important local modes might have been left out. An alternative view was argued by [195]: inference from such schemes is considered as approximate posterior inference in a submodel defined by constraining the parameters to a neighborhood of the particular local mode. Depending on the emphasis of the analysis, this might be reasonable, especially if in a final implementation our aim is to set the parameters at specific values, the usual scenario in deep learning. We prefer though to propagate the uncertainty in parameters, since this allows better predictions, e.g. [234].

For this, an efficient Markov chain Monte Carlo (MCMC) scheme may be used [205]. It samples from the posterior conditionals when available (steps 3, 9), and use Metropolis steps (4-8), otherwise. To fight potential inefficiencies due to multimodality, two features are built in for fast and effective mixing over local posterior modes: whenever possible, the weights are partially marginalized; second, these weights are resampled jointly. The key observation is that, given , we actually have a standard hierarchical normal linear model [89]. This facilitates sampling from the posterior marginals of the weights (step 3) and hyperparameters (step 9) and allows marginalizing the model with respect to the ’s to obtain the marginal likelihood (step 3), where designates the hyperparameters. The procedure runs like the described in Algorithm 1.1.

For proposal generation distributions , normal multivariate distributions are adopted. Appropriate values for can be found by trying a few alternative choices until acceptance rates around 0.25 are achieved [100].

Combined with model augmentation to a variable architecture, this leads to a useful scheme for complete shallow NN analyses as it allows for the identification of architectures supported by data, by contemplating as an additional parameter. A random with a prior favoring smaller values reduces posterior multimodality. Moreover, as marginalization over requires inversion of matrices of dimension related to , avoiding unnecessarily large hidden layers is critical to mitigating computational effort. Thus, we assume a maximum size for the network and introduce indicators suggesting whether node is included () or not (). We also include a linear regression term to favor parsimony. On the whole, the model becomes

Learning is done through a reversible jump sampler [115] embedding our first algorithm. As a consequence, we perform inference about the architecture based on the distribution of .

[210] proposed using an algorithm merging conventional Metropolis-Hastings chains with sampling techniques based on dynamic simulation, the currently popular Hamiltonian Monte Carlo (HMC) approaches. Let us designate by the NN weights, , and denote the potential energy function as

where are hyperparameters controlling regularization, similarly to (1.9). Let us also introduce the Hamiltonian

with momentum variables of the same dimension as ; such variables serve to accelerate the walk towards posterior modes. Then, the HMC scheme would be as described in Algorithm 1.2.

1.3.3 Deep neural networks

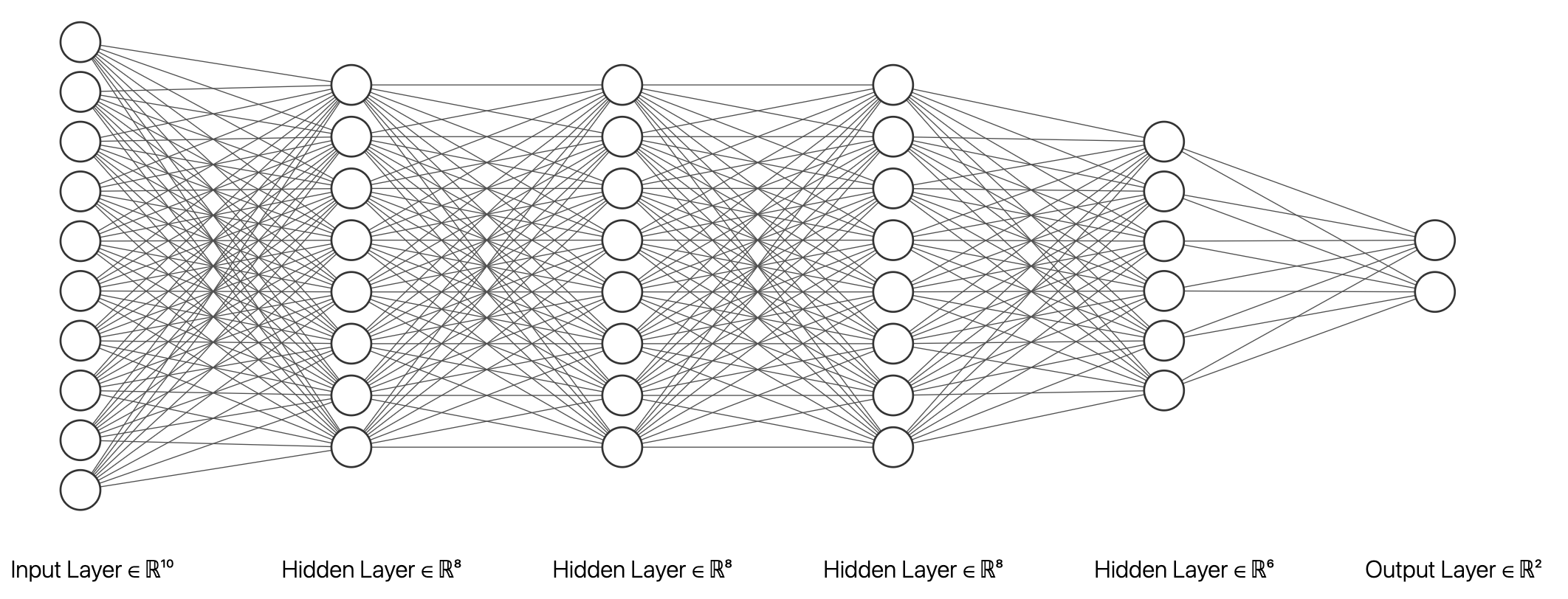

Training by backpropagation has been in use for many years by now. The decade of the 2010’s witnessed major developments leading to the boom around deep learning [110] or inference and prediction with deep NNs. Such advances include: the availability of fast GPU kernels and routines facilitating much faster training; the access to massive amounts of data (e.g. Imagenet), which prevented overfitting to smaller datasets; the creation of new architectures, which prevented convergence issues, such as the vanishing gradient problem; and, finally, the provision of automatic differentiation libraries such as Tensorflow, Caffe or Theano. Figure 1.8 displays an example of what are now designated deep NNs, that is NNs with more than one hidden layer, four in the portrayed case.

A deep NN may be defined through a sequence of functions , each parametrized by some weights of dimension (the corresponding number of hidden nodes) with the output of each layer being the input of the following one, as in

Lastly, we compute a prediction from the hidden activations of the last layer, as in Eq. (1.7)

Modern architectures do not longer require the functions to be sigmoidal (like the logistic functions in (1.7)) and include the rectified linear unit (ReLU), the leaky ReLU or the exponential LU. In particular, these functions mitigate the vanishing gradient problem [151] that plagued earlier attempts with deep architectures using sigmoidal activation functions. Besides, such activation functions have other benefits likes being faster to compute both the activation and its derivative.

Beyond the above generic deep architectures a few important specialised models have emerged which are relevant in specific application domains, as we describe now.

Convolutional neural networks

CNNs are typically used in computer vision tasks and related signal processing applications. Stemming from the work by Le Cun and coauthors [161, 164] and their original LeNet5 design, they achieved major successes in competitions [155] leading to architectures like AlexNet [155], VGGNet [261] or GoogleNet [269], reaching superhuman performance in image recognition tasks.

In CNNs, the layer transformation is taken to be a convolution with some 2D or 3D kernel; this makes the network able to recognise patterns independently of their location or scale in the input, a desirable property in computer vision tasks known as spatial equivariance. In addition, by replacing a fully-connected layer with a small kernel (typically, in the 2D case these are of shapes or ), there is weight sharing amongst the unit from the previous layer and this allows reducing the number of parameters and prevents overfitting. Thus, the typical convolutional network layer is composed of several sub-layers:

-

•

A convolution operation, as before, serving as an affine transformation of the representation from the previous layer. A layer can apply several convolutions in parallel to produce a set of linear activations.

-

•

A non-linear layer, such as the rectifier (based on the ReLU function), converting the previous activations to nonlinear ones.

-

•

An optional pooling layer, which replaces the output of the net at a certain position with a summary statistic of the nearby outputs (typically the mean or the maximum).

Recurrent neural networks

RNNs are typically used for sequence processing, as in natural language processing (NLP), e.g. [123] and [58]. They have feedback connections which make the network aware of temporal dependencies in the input. Let denote the -th token (usually a word, but could even be a smaller part) in the input sequence. A simple recurrent layer can be described as

with the output at that time-step given by

where is a non-linear activation function, such as the logistic or the hyperbolic tangent functions. This is the Elman network [65]. Note that weights are shared between different time-steps. For training purposes, all of the previous loops must be unrolled back in time, and then perform the usual gradient descent routine. This is called backpropagation through time [286]. Backpropagating through long sequences may lead to problems of either vanishing or exploding gradients. Thus, simple architectures like Elman’s cannot be applied to long inputs, as those arising in NLP. As a consequence, gating architectures which improve the stability have been proposed, and successfully applied in real-life tasks, such as long short-term memory (LSTM) [123] and gated recurrent unit (GRU) networks [56].

Transformers

These architectures substitute the sequential processing from RNNs by a more efficient, parallel approach inspired by attention mechanisms [278, 15]. Their basic building components are scaled dot-product attention layers: let be the embedding333An embedding layer is a linear layer that projects a one-hot representation of words into a lower-dimensional space. of the -th token in an input sequence; this is multiplied by three weight matrices to obtain: 1) a query vector, ; 2), a key vector ; and, 3) a value vector, . The output of the attention layer is computed, parallelizing along the input position , through

a weighted average of the components of the value vector, where the average is computed as a normalized dot product between the key and query vectors. Thus, the attention layer produces activations for every token that contains information not only about the token itself, but also a combination of other relevant tokens weighted by the attention weights.

Since transformer-based models are more amenable to parallelization, they have been trained over massive datasets in the NLP domain, leading to architectures such as Bidirectional Encoder Representations for Transformers (BERT) [71] or the series of Generative pre-trained Transformer (GPT) models [231, 232, 40].

Generative models

The models from the previous paragraph belong to the discriminative family of models. Discriminative models directly learn the conditional distribution from the data. Generative models, as opposed to discriminative ones, take a training set, consisting of samples from a distribution , and learn to represent an estimation of that distribution, resulting in another probability distribution, . Then, one could fit a distribution to the data by performing MLE,

or MAP estimation if a prior over the parameters is also placed. Fully visible belief networks [90] are a class of models that can be optimized this way. They are computationally tractable since they decompose the probability of any given dimensional input as . Current architectures that fall into this category include WaveNet [215] and pixel recurrent neural networks [214].

Generative adversarial networks

GANS perform density estimation in high-dimensional spaces formulating a game between two players, a generator and a discriminator [111]. They belong to the family of generative models; however, GANs do not explicitly model a distribution , i.e., they cannot evaluate it, only generate samples from it. GANs define a probabilistic graphical model containing observed variables (the input data, like an image or text) and latent variables . Then, both players can be represented as two parameterized functions via NNs. Thus, the generator will be of the form , i.e., a NN that takes as input a latent vector and is parameterized through weights . Note that the last layer will depend on the shape and range of the data . Likewise, the discriminator will be a function receiving a (fake or real) sample and outputting a probability for each of these two classes. Therefore, the final activation function will be the sigmoid function. Each network has its own objective function and, consequently, both networks would play a minimax game. Now, both players update their weights sequentially, typically using SGD or any of its variants.

Classical approaches.

In principle, we could think of using with deep NNs the approach in Section 1.3.2. However, large scale problems bring in two major computational issues: first, the evaluation of the gradient of the loss wrt the parameters requires going through all observations becoming too expensive when is large; second, estimation of the gradient component for each point requires a much longer backpropagation recursion through the various levels of the deep network, entailing again a very high computational expense.

Fortunately, these computational demands are mitigated through the use of classical stochastic gradient descent (SGD) methods [244] to perform the estimation [31]. SGD is the current workhorse of large-scale optimization and allows training deep NNs over large datasets by mini-batching: rather than going through the whole batch at each stage, just pick a small sample (mini batch) of observations and do the corresponding gradient estimation by backpropagation. This is reflected in the Algorithm 1.3, which departs from an initial .

The standard Robbins-Monro conditions require that and for convergence to the optimum.

Recent work has explored ways to speed up convergence towards the local optimum, leading to several SGD variants, including the addition of a momentum, as in AdaGrad, Adadelta or Adam [146, 75, 297]. The essence of these methods is to take into account not only a moving average of the gradients, but also an estimate of its variance, so as to dynamically adapt the learning rate. Let us finally mention several techniques to improve generalization and convergence of neural networks, such as dropout [265], batch normalization [137] or weight initialization [105].

1.3.4 Examples

We illustrate learning with deep NNs with two examples portraying different architectures and application domains. Code for the experiments was done using the pytorch library [219] and is released at https://github.com/vicgalle/nn-review.

CNNs for image recognition.

We describe an image classification task with a standard CNN, VGG-19, showcasing the superior performance when compared to non-convolutional and non-deep approaches in this application domain. As benchmark, we use the CIFAR-10 dataset [154], which consists of 60000 32x32 colour images in 10 classes. As baselines, we use a linear multinomial regression model, and a three hidden layer NN (MLP) with 200 units each with ReLU activations. As Bayesian features for this experiment, note the use of Gaussian prior over parameters, which benefits performance compared to the vanilla MLE. Notice also that, in CNNs, we are also imposing an implicit prior, which consists in restricting the set of linear layers to be convolutions, a particular case of linear operator.

All models are trained for 200 epochs444An epoch is defined as a pass over the full training dataset. and minibatches of 128 samples, using SGD with learning rate of 0.1 and momentum of 0.9. The learning rate is adapted with the cosine annealing scheme in [185]. We place independent Gaussian priors over all parameters (thus equivalent to regularization) and use SWA on top of the SGD optimizer, to make predictions using an ensemble of 100 posterior samples, in a Bayesian way.

Figure 1.9 presents five random images from the test set and Table 1.4 displays results. Notice how the linear model performs poorly with just a test accuracy of 38%, whereas increasing the flexibility of the models critically improves accuracy. Indeed, the MLP performs slightly better. However, by imposing strong priors about the dataset, such as translation equivariance thanks to the convolutional layers and pooling, state-of-the-art results are achieved with VGG-19.

| Model | Test acc. |

|---|---|

| Linear | |

| MLP | |

| VGG-19 |

Transformer and recurrent models for sentiment analysis.

This is an example with text to undertake sentiment analysis, classifying movie reviews with architectures tailored to NLP tasks. As benchmark, we use the IMBD movie review dataset from [191], in which a review in raw text must be classified into one of two classes: positive or negative sentiment.

The recurrent model consists of a LSTM network with two layers, each with hidden dimension of 256 plus a dropout of 0.5 serving as a regularizer. We also consider a simple Transformer-based model, with two encoder layers, of hidden dimension 10 plus similar dropout. For both models, the input sequence is represented as a list of one-hot encoded vectors, representing the presence of a word from a vocabulary of the 5000 most common tokens. This representation is embedded into a space of 100 dimensions (16 in the Transformer case) by means of an affine transformation, before applying architecture-specific layers. Both models are trained using the Adam optimizer with a constant learning rate of 0.001. We also consider a bigger, transformer-based model consisting of the recent RoBERTa architecture [184], initially pretrained on a big corpus of unsupervised raw English text, and then fine tuned for two epochs on the IMDB training set.

Table 1.5 shows two random examples from the IMDB dataset. Results over the full test set are displayed in Table 1.6. Notice how the Transformer-based models are superior to the recurrent baseline, and the extra benefits thanks to the usage of transfer learning.

| Text input | Prediction | True label |

|---|---|---|

| HOW MANY MOVIES ARE THERE GOING TO BE IN WHICH AGAINST ALL ODDS, A RAGTAG TEAM BEATS THE BIG GUYS WITH ALL THE MONEY?!!!!!!!! There’s nothing new in "The Big Green". If anything, you want them to lose. Steve Guttenberg used to have such a good resume ("The Boys from Brazil", "Police Academy", "Cocoon"). Why, OH WHY, did he have to do these sorts of movies during the 1990s and beyond?! So, just avoid this movie. There are plenty of good movies out there, so there’s no reason to waste your time and money on this junk. Obviously, the "green" on their minds was money, because there’s no creativity here. At least in recent years, Disney has produced some clever movies with Pixar. | Negative | Negative |

| When I first heard that the subject matter for Checking Out was a self orchestrated suicide party, my first thought was how morbid, tasteless and then a comedy on top of that. I was skeptical. But I was dead wrong. I totally loved it. The cast, the funny one liners and especially the surprise ending. Suicide is a delicate issue, but it was handled very well. Comical yes, but tender where it needed to be. Checking Out also deals with other common issues that I believe a lot of families can relate with and it does with tact and humor. I highly recommend Checking Out. A MUST SEE. I look forward to its release to the public. | Positive | Positive |

| Model | Test acc. |

|---|---|

| LSTM | |

| Simple Transformer | |

| RoBERTa |

1.4 Challenges

The reflections motivated by the case study in Section 1.2, using classical Bayesian approaches, and the review in Section 1.3, have led us to enumerate the following three major challenges, object of study in this thesis.

1.4.1 Challenge 1. Large scale Bayesian inference

MCMC algorithms such as the ones presented in Section 1.2.2 or 1.3.2 have become standard in Bayesian inference [89]. However, they entail a significant computational burden in large datasets. Indeed, computing the corresponding acceptance probabilities requires iterating over the whole dataset, which often does not even fit into memory. Thus, they do not scale well in big data settings. As a consequence, several approximations have been proposed.

Stochastic Gradient Markov chain Monte Carlo.

SG-MCMC methods are based on the discretization of stochastic differential equations that have the desired target distribution as its limit. [190] provide a complete framework that encompass many earlier proposals and facilitate such discretization, as well as a practical tool for devising new samplers and testing the correctness of proposed samplers. We aim at drawing samples from the posterior , with potential function . Define also auxiliary variables , with , and sample from , with hamiltonian , such that . Marginalizing the auxiliary variables gives us the desired distribution on .

In general, all continuous Markov processes that one might consider for sampling can be written as a stochastic differential equation (SDE) of the form:

| (1.12) |

where denotes the deterministic drift, frequently related to , is a -dimensional Wiener process, and is a positive semidefinite diffusion matrix. Note, though, that some care must be taken to choosing and to yield the desired stationary distribution. [190] propose a recipe for constructing SDEs with the correct stationary distribution through , and where is a skew-symmetric curl matrix (representing the deterministic traversing effects seen in HMC procedures) and the diffusion matrix determines the strength of the Wiener process-driven diffusion. When is positive semidefinite and is skew-symmetric, the convergence of the above dynamics to the desired distribution follows; moreover both matrices can be adjusted to attain faster convergence to the posterior distribution. [190] show that by properly choosing the matrices one can recover numerous samplers such as SGLD [284] or a corrected SG-HMC [55].

In practice, simulation actually relies on a discretization of the SDE, leading to a (full-data) update rule

| (1.13) |

Calculating entails evaluating the gradient of which, with deep NN models, becomes very intensive computationally as it relies on a sum over all data points. Instead, we use a sampled data subset , with the corresponding potential for these data being , leading to the approximation

| (1.14) |

where is an estimate of the variance of the error. This provides the stochastic gradient—or minibatch— variant of the sampler. Note also that all of these approaches could be combined with recent heuristics to improve the convergence of SG-MCMC methods, such as the adoption of cyclical step sizes to explore more efficiently the posterior [264].

Variational Bayes.

Variational inference (VI) [29] tackles the approximation of with a tractable parameterized distribution . The goal is to find parameters so that the distribution (referred to as variational guide or variational approximation) is as close as possible to the actual posterior, with closeness typically measured through the Kullback-Leibler divergence , reformulated into the ELBO

| (1.15) |

the objective to be optimized, usually through SGD techniques.

A standard choice for is a factorized Gaussian distribution , with mean and covariance matrix defined through a deep NN conditioned on the observed data . Note though that other distributions can be adopted as long as they are easily sampled and their log-density and entropy evaluated. A problem is that these approximations often underestimate the uncertainty. Some developments partly mitigate this issue by enriching the variational family include normalizing flows [236] or the use of implicit distributions [132].

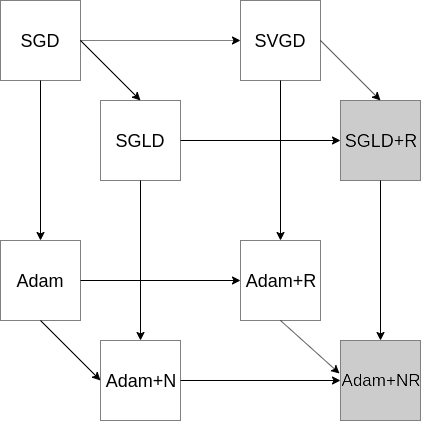

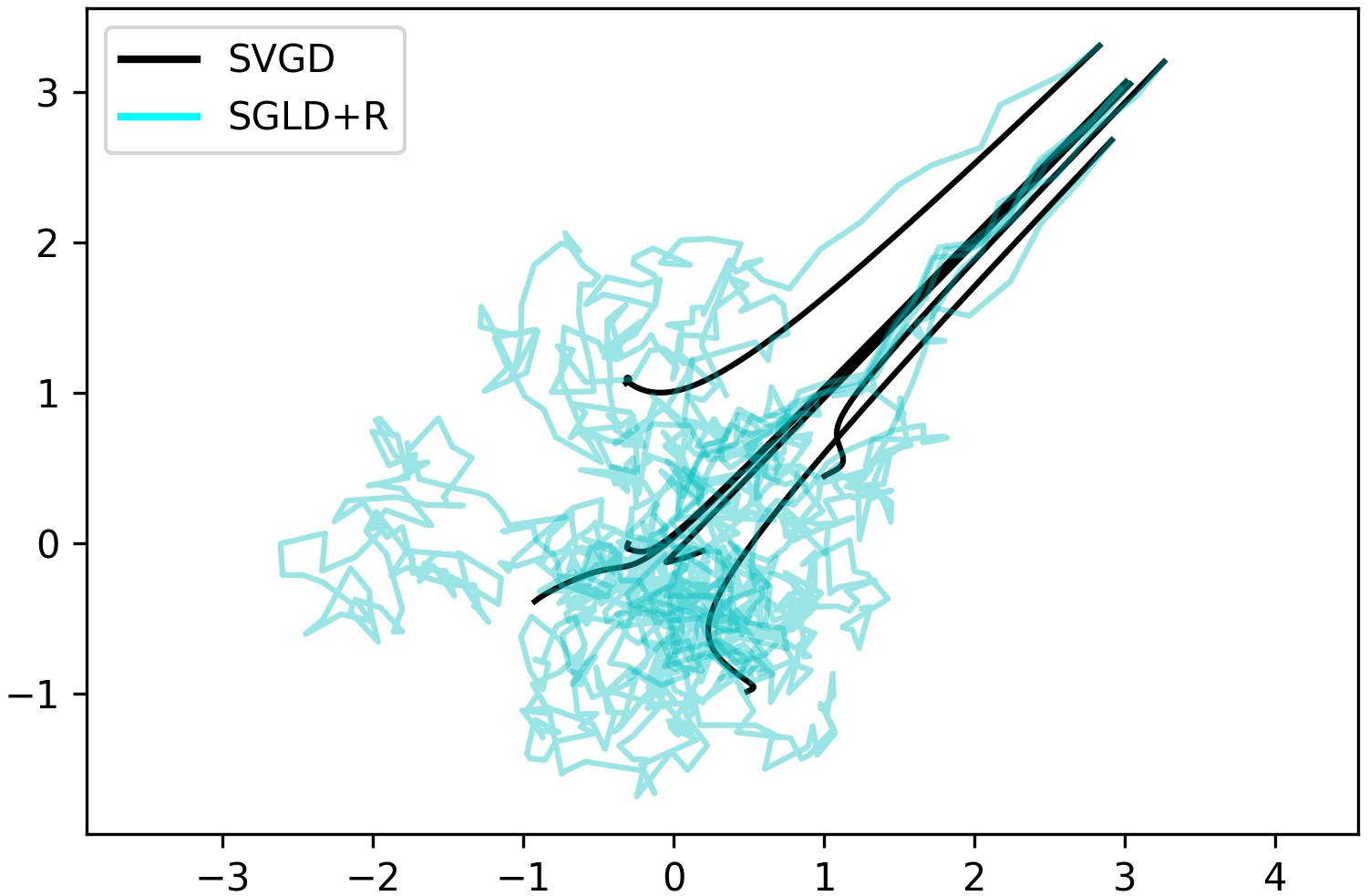

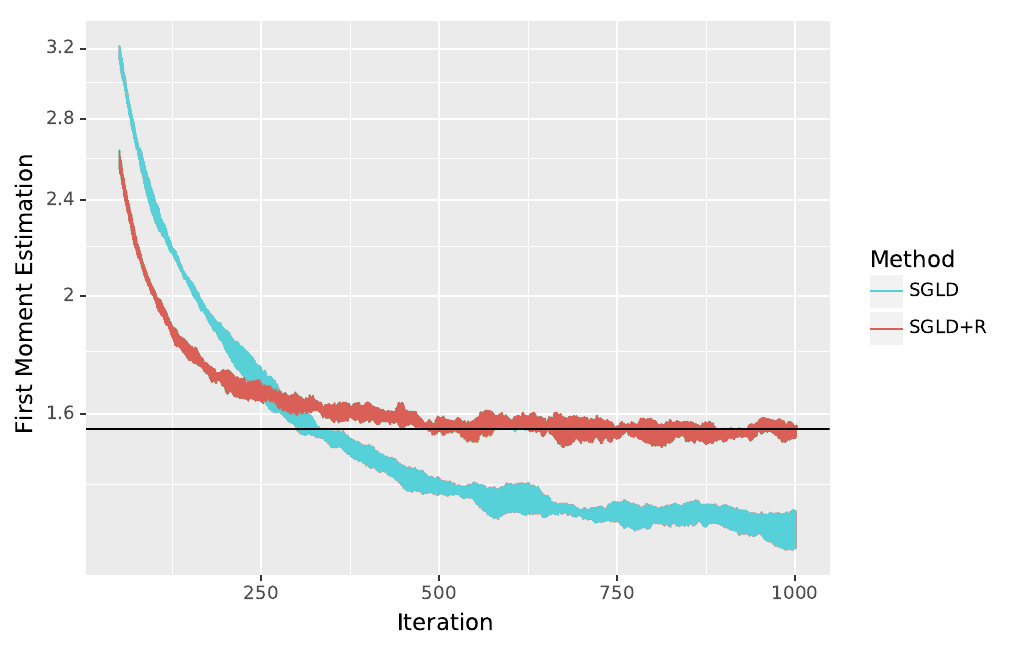

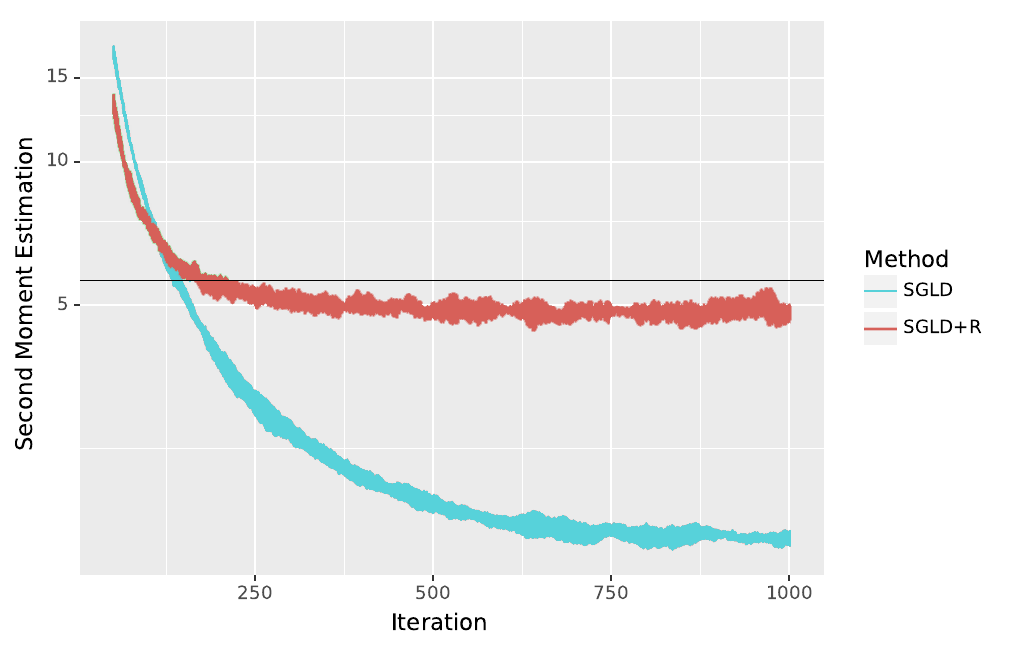

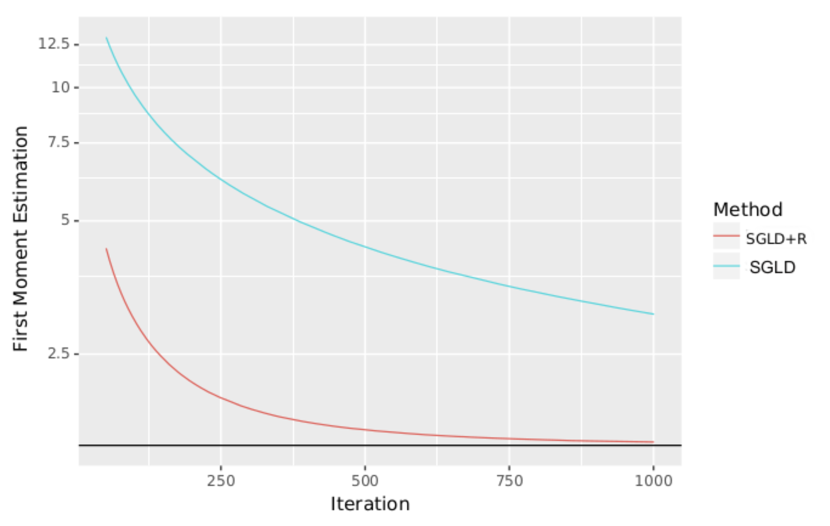

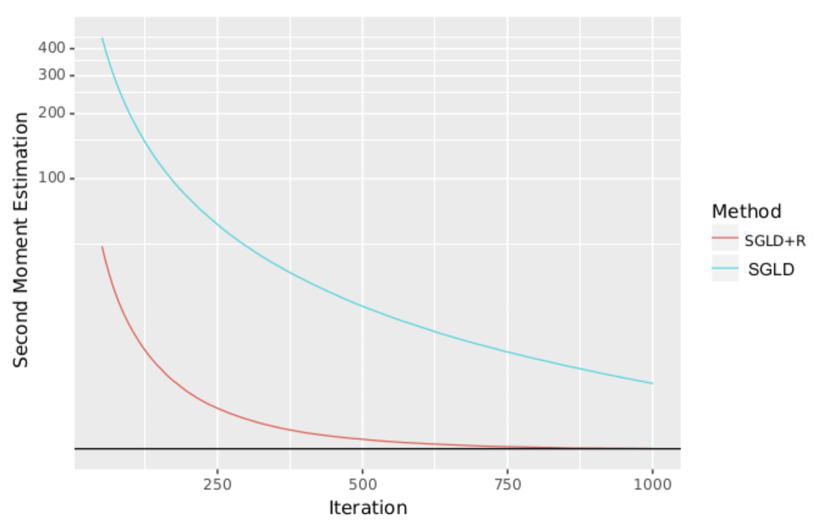

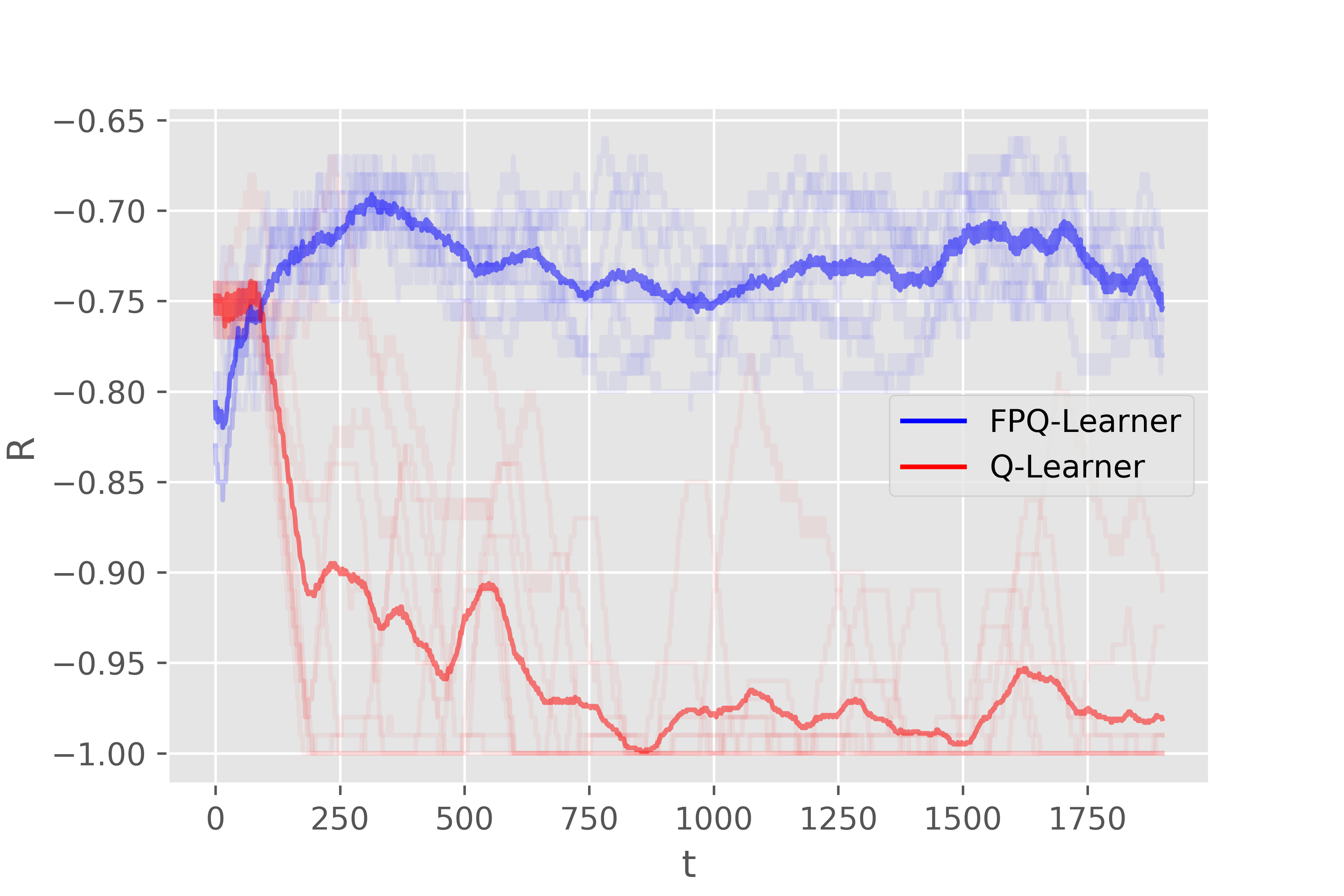

In Chapter 2 we will further review these approaches and propose two frameworks to further scale up Bayesian inference in challenging settings. The first is based on augmenting an SG-MCMC sampler with multiple, parallel chains, incorporating interactions between particles so they can explore the posterior more efficiently. The second is a novel variational approximation that serves to automatically adapt the hyperparameters of any SG-MCMC sampler.

1.4.2 Challenge 2. Security of machine learning

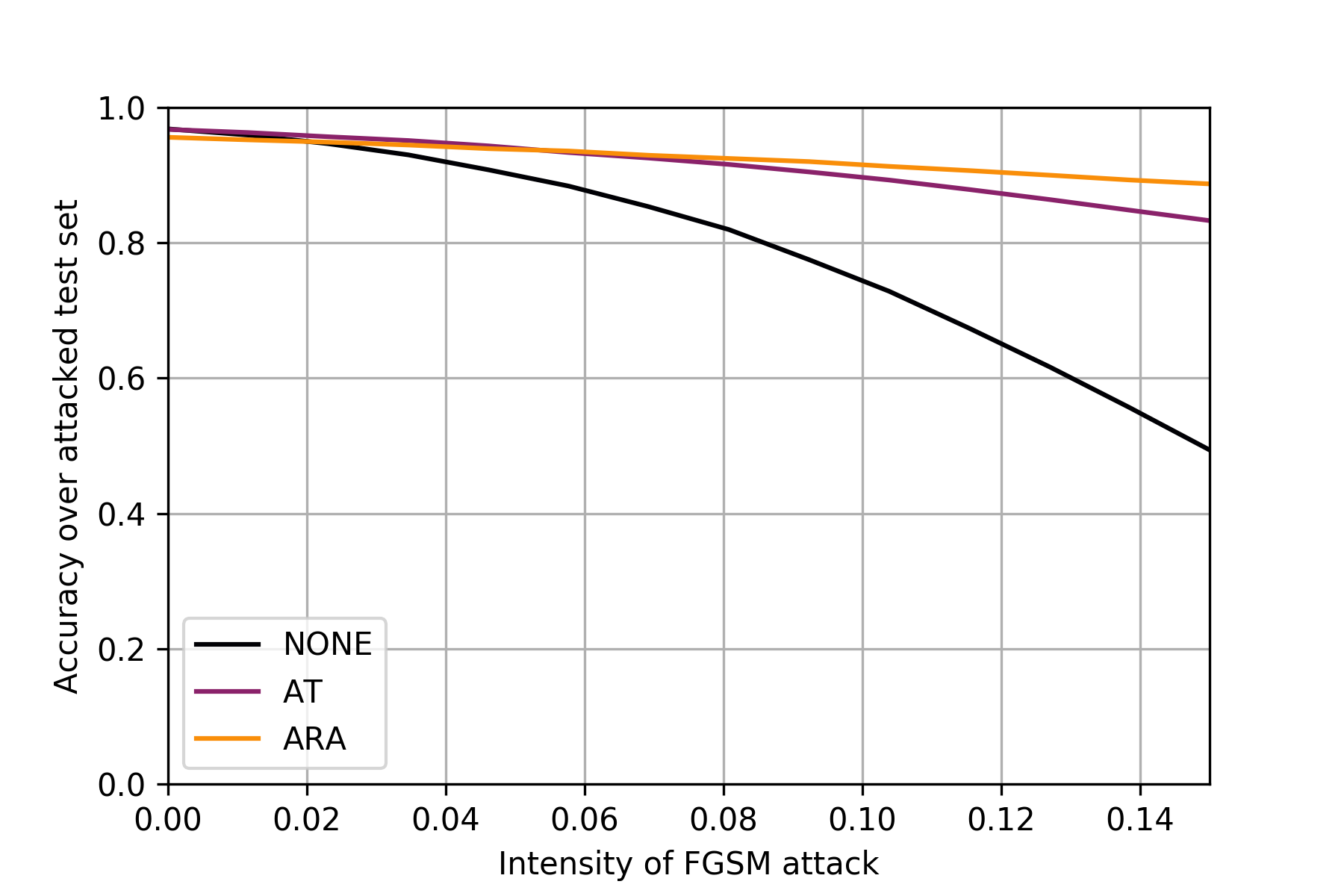

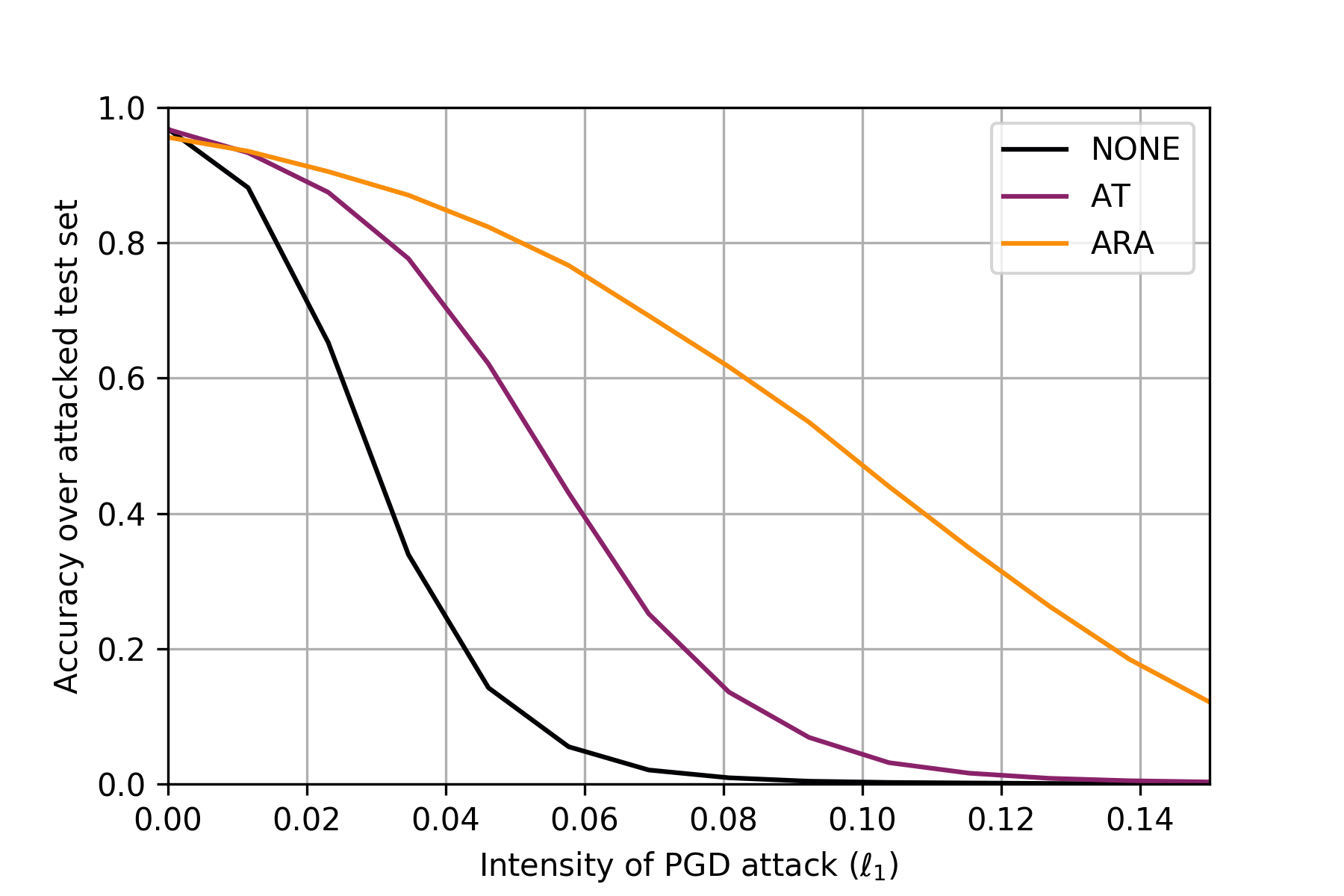

As described, over the last decade an increasing number of processes are being automated through deep NN algorithms, being essential that these are robust and reliable if we are to trust operations based on their output. State-of-the-art algorithms, as those described above, perform extraordinarily well on standard data, but have been shown to be vulnerable to adversarial examples, data instances targeted at fooling them [109]. The presence of adaptive adversaries has been pointed out in areas such as spam detection [296] and computer vision [109], among many others. In those contexts, algorithms should acknowledge the presence of possible adversaries to protect from their data manipulations. As a fundamental underlying hypothesis, NN based systems rely on using independent and identically distributed (iid) data for both training and operations. However, security aspects in deep learning, part of the emergent field of adversarial machine learning (AML), question such hypothesis, given the presence of adaptive adversaries ready to intervene in the problem to modify the data and obtain a benefit. In addition, time series models, such as the introduced in Section 1.2 can also be subject to adversarial attacks [142, 4], so it is of great interest to develop model-agnostic defences.

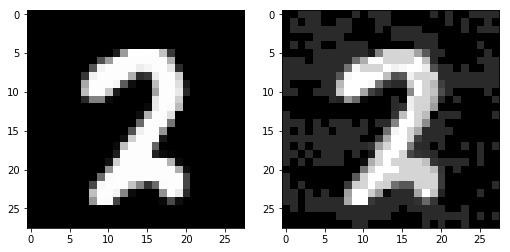

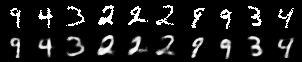

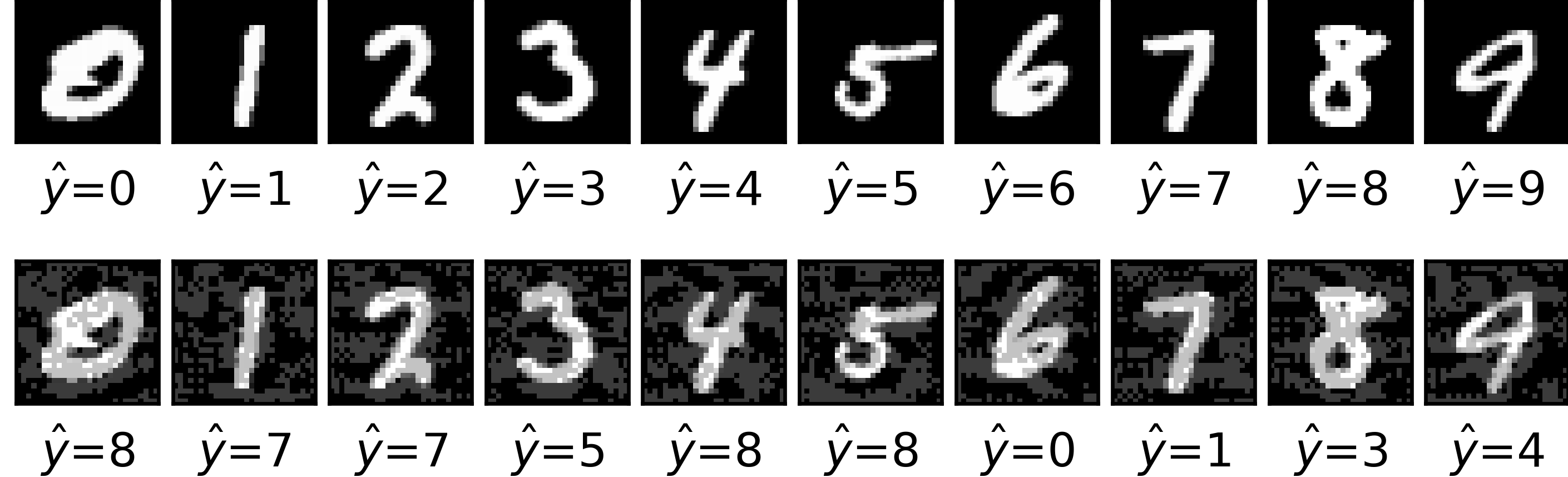

As a motivating example, vision algorithms (Section 1.3.4) are at the core of many AI applications such as autonomous driving systems (ADSs) [116]. The simplest and most notorious attack examples to such algorithms consist of modifications of images in such a way that the alteration becomes insignificant to the human eye, yet drives a model trained on millions of images to misclassify the modified ones, with potentially relevant security consequences. With a relatively simple CNN model, we are able to accurately predict 99% of the handwritten digits in the MNIST data set. However, if we attack those data with the fast gradient sign method [270], accuracy gets reduced to 62%. Fig. 1.10 provides an example of an original MNIST image and a perturbed one: to our eyes both images look like a 2, but the classifier rightly identifies a 2 in the first case, whereas it suggests a 7 after the perturbation.

Stemming from the pioneering work in adversarial classification [69], the prevailing paradigm in AML models the confrontation between learning-based systems and adversaries through game theory. This entails common knowledge assumptions [118] which are questionable in security applications as adversaries try to conceal information. As [83] points out, there is a need for a framework that guarantees robustness of ML against adversarial manipulations in a principled manner.

The usual approach for robustifying models against these examples is adversarial training (AT) [192] and its variants, based on solving a bi-level optimisation problem whose objective function is the empirical risk of a model under worst case data perturbations. However, recent pointers urge modellers to depart from using norm based approaches [48] and develop more realistic attack models.

AML is a difficult area which rapidly evolves and leads to an arms race in which the community alternates cycles of proposing attacks and of implementing defences that deal with them. However, as mentioned, it is based on game theoretic ideas and strong common knowledge conditions. The challenge is thus to develop defence mechanisms that are sufficiently scalable to the increasingly complex ML models using in real life. Chapter 3 examines these issues, providing a scalable defence procedure inspired by ARA [239, 16].

1.4.3 Challenge 3. Large scale competitive decision making

In real life scenarios, decision makers rarely have to take a single action. Instead, multiple decisions must be made, with the former actions making a causal impact on the later ones. For example, in the case study from Section 1.2, the decision maker might desire to plan ahead for a year the budget allocations of all the advertising channels. Thus, we have to delve into the realm of sequential decision making [89, 72]. There are many paradigms to tackle this problem, such as optimal control theory [149]. Since this thesis is also focused on Machine Learning, we adopt the framework of Reinforcement Learning (RL) to deal with sequential decisions while making the decision maker able to learn from her experiences [268, 138]. RL differs from supervised learning in not needing labelled input/output pairs be presented, and in not needing sub-optimal actions to be explicitly corrected. Instead the focus is on finding a balance between exploration (of uncharted experiences) and exploitation (of current knowledge). Of course, RL can also benefit from recent developments in deep, neural architectures to further enhance its efficiency in complex and highly dimensional environments [203].

However, RL typically only deals with one agent (the decision maker), taking actions against her environment, which is assumed to be stationary. Realistic settings have to take into account the presence of other rational agents. These can be potential collaborators to cooperate, but also could be adversaries. For instance, in the case study from Section 1.2 we could have modeled competitors also taking decisions that in a way, also affect the expected sales of the supported franchise. Under this dynamic, non-stationary environment, traditional RL techniques dramatically fail, and it is a necessity to develop novel frameworks that acknowledge the presence of other players. This is the field of multi-agent Reinforcement Learning (MARL), which usually takes grounding in game-theoretical approaches [42, 159].

Game Theory has also its own drawbacks, whereas Adversarial Risk Analysis (ARA) offers a more realistic view, leveraging Bayesian ideas [18]. The challenge is thus how to adapt the ARA methodology into the sequential learning nature of RL, with low computational requirements in order to allow for scalability. Chapter 4 deals with some of these issues.

1.5 Thesis structure