Treatment Effects in Market Equilibrium†† We thank Isaiah Andrews, Joshua Angrist, Dmitry Arkhangelsky, Susan Athey, Lanier Benkard, Han Hong, Guido Imbens, Michael Kosorok, Whitney Newey, Fredrik Sävje, Paulo Somaini, Ali Yurukoglu, and seminar participants at Columbia, Harvard, Michigan State University, Princeton, Stanford, UT Austin, University of Chicago, University of Montreal, CODE, ICSDS, JSM, and the Online Causal Inference Seminar for helpful comments and discussions. This research is partially supported by a gift from Facebook. Code for the simulations in this paper is available at https://github.com/evanmunro/market-interference.

Stanford Graduate School of Business)

Abstract

When randomized trials are run in a marketplace equilibriated by prices, interference arises. To analyze this, we build a stochastic model of treatment effects in equilibrium. We characterize the average direct (ADE) and indirect treatment effect (AIE) asymptotically. A standard RCT can consistently estimate the ADE, but confidence intervals and AIE estimation require price elasticity estimates, which we provide using a novel experimental design. We define heterogeneous treatment effects and derive an optimal targeting rule that meets an equilibrium stability condition. We illustrate our results using a freelance labor market simulation and data from a cash transfer experiment.

Keywords: Equilibrium Effects, Experimental Design, Interference

1 Introduction

Modern computational infrastructure has enabled an enormous growth of randomized trials on websites and mobile applications (Kohavi et al. 2020). On many online platforms, interactions between individuals occur as they buy and sell items at the prevailing market prices. The goal of running a standard randomized control trial (RCT), where treatment is assigned with constant probability to all individuals, is often to evaluate the impact of a new policy on some outcome of interest. The standard analysis of treatment effects in a randomized trial relies on an assumption that the treatment status of one individual does not affect the outcomes of other individuals (Fisher 1935, Banerjee & Duflo 2011, Imbens & Rubin 2015), also known as the Stable Unit Treatment Value Assumption (SUTVA). When a randomized trial affects supply or demand, and market prices affect the outcome of interest, then general equilibrium effects lead to a violation of SUTVA, and measurements of the Average Treatment Effect (ATE) do not correspond to a meaningful measure of policy impact (Heckman et al. 1998).

A primary goal of this paper is to provide a framework for the analysis of randomized trials in an equilibrium setting without relying on strong parametric, distributional, or homogeneity assumptions. We integrate a price equilibrium into a stochastic model of treatment effects under interference. We use it to provide asymptotic results for various definitions of policy-relevant average and conditional average treatment effects, and to design new forms of randomized trials and targeting rules. In the process, we overcome a variety of challenges unaddressed by the existing literature on treatment effects under dense patterns of interference, including providing asymptotically exact confidence intervals for the indirect effect, and proposing general definitions of conditional estimands that can be used to construct targeting rules.

There is existing work that addresses interference by clustering units at a higher level at which SUTVA holds (Baird et al. 2018, Hudgens & Halloran 2008). In the market context, this involves finding clusters of buyers and sellers who trade only within the cluster and not across clusters. However, if a marketplace is very connected, finding a good clustering may not be feasible. Furthermore, clustering can be costly, both because it reduces power (Abadie et al. 2017) and because cluster-level designs require modifying the equilibrium in different clusters. In this paper, we focus on settings where clustering is not desirable, so that the solution must rely on unit-level randomized experimentation only. This approach results in increased power, but comes at a cost of making assumptions based on ex-ante knowledge about the structure of the market equilibrium.

Structural modeling is used in a variety of fields to analyze the effects of policies when individuals interact with one another in economic environments (Heckman et al. 1998, Duflo 2004, Abbring & Heckman 2007). Some structural models are population-level and are designed for theoretical analysis, as in Johnson (1980). Others are designed for estimating demand systems from observational data by imposing exclusion restrictions or parametric assumptions; see Ackerberg et al. (2007), Matzkin (2015), Berry et al. (1995), Berry & Haile (2021). Compared to observational data that is often at an aggregate level, experiments can be used to collect individual-level data that are much richer. As suggested in Manski (1993), collecting richer data is helpful for analyzing endogenous social effects without imposing strict assumptions on the data generating process. We build a non-parametric structural model that is designed for treatment effect inference using individual-level data from randomized experiments. Our model builds connections between the non-parametric program evaluation literature and the modeling-based approaches that have traditionally been used to analyze equilibrium effects of policies. When marketplace effects are removed, it reduces to a standard Neyman-Rubin potential outcomes model (Imbens & Rubin 2015). We are able to derive estimators, standard errors and targeted policies in equilibrium that are robust to a variety of modeling choices and can be compared directly to related results in the causal inference literature.

The starting point for our model is the potential outcomes framework that allows for cross-unit interference (Hudgens & Halloran 2008, Manski 2013, Aronow & Samii 2017). We assume that each individual’s production and consumption choices are determined by latent supply and demand curves (Angrist et al. 2000, Heckman & Vytlacil 2005). Units interact via a marketplace modeled as a classical multiple goods economy in general equilibrium, where individuals make choices on production and consumption based on their own private information as well as their expectations of what the market price equilibrium will be (Walras 1900, Mas-Colell et al. 1995). Our two main non-parametric structural assumptions are that prices equalize latent supply and demand, and the potential outcomes for each individual depend only on their own treatment and market prices. Under this structure, we show that interference is restricted in that it operates only through the -dimensional equilibrium price. That is, equilibrium prices induce an exposure mapping in the sense of Manski (2013) and Aronow & Samii (2017). When individual supply, demand and outcomes are stochastic, we show that the random equilibrium price that arises in finite samples converges to a fixed and unique price in the limit as the number of suppliers and consumers grows. We use this mean-field limit to characterize the asymptotic behavior of treatment effects.

Under interference, a meaningful policy-relevant counterfactual is the Global Treatment Effect (GTE), which is the average effect of treating all individuals in the sample compared to treating no individuals in the sample. Hu et al. (2022) show that under any pattern of interference, the sum of the average direct and indirect effects of a binary treatment is a first-order approximation to the GTE. Thus, we start by analyzing the average direct and indirect effects of a binary treatment in equilibrium (Halloran & Struchiner 1995, Hu et al. 2022, Sävje et al. 2021). We show that the direct and indirect effects of a binary treatment converge to simple and interpretable mean-field limits in large samples. The direct effect converges to the difference in expected outcomes for treated and control individuals, holding market prices fixed. The indirect effect converges to the product of the effect of the treatment on excess demand, the derivative of expected outcomes with respect to prices, and the inverse of the sensitivity of excess demand with respect to prices.

The direct effect of the treatment can be consistently estimated using a Horvitz-Thompson estimator and data from a traditional RCT, as shown in Sävje et al. (2021). We also provide a Central Limit Theorem for the Horvitz-Thompson estimator and characterize the asymptotic variance explicitly. Confidence intervals built for the direct effect using a standard RCT approach that ignores equilibrium effects are not exact. In order to perform asymptotically exact inference for the direct effect and to consistently estimate the indirect effect, which is the missing component of the policy counterfactual, estimates of price elasticities are required.

We propose an augmented unit-level randomized experiment that adds small price perturbations to a traditional Bernoulli randomized experiment. This is feasible, for example, in online marketplaces, where there are often fees for buyers and sellers that can be perturbed randomly. We show that adding small price perturbations does not affect the limiting equilibrium of the system. In previous work that characterizes the indirect effect under dense patterns of interference, estimators for the variance of the indirect effect were not available (Li & Wager 2022, Sävje et al. 2021). Under this augmented randomized experiment, we provide a central limit theorem and characterize the asymptotic variance for the indirect effect, and show that consistent estimators for the direct and indirect effect and their asymptotic variances are available.

Given that the model we’ve been using so far allows for unrestricted heterogeneity across agents, it is also interesting to see whether we can estimate how treatment effects vary with pre-treatment characteristics—and exploit this heterogeneity to learn improved policies. In Section 4, we analyze heterogeneous effects and optimal treatment rules under equilibrium interference. In settings where SUTVA holds, there is a large literature on characterizing heterogeneity in treatment effects and treatment targeting (Manski 2004, Athey & Imbens 2016, Wager & Athey 2018, Van der Weele et al. 2019). Optimal policy in this setting depends on the sign and magnitude of the conditional average treatment effect (CATE) (Manski 2004). However, in the presence of interference, the CATE alone does not explain who should be treated to optimize outcomes; and in fact the standard definition of the CATE is ill-specified (since it relies on SUTVA). Given this background, our first contribution is to define conditional estimands under general patterns of interference that connect to a meaningful policy counterfactual and are useful in defining optimal targeting rules. We propose the conditional average direct effect (CADE), which is the expected effect of changing the treatment of an individual with covariate on their own outcomes, and the conditional average indirect effect (CAIE), which is the expected effect of changing the treatment of an individual with covariate on everyone else’s outcomes. We show that the sum of the CADE and the CAIE, scaled appropriately, is equal to the expected increase in average outcomes for a marginal increase in the treatment probability of an individual with covariate . Just as the ADE is equal to the ATE when interference is removed, the CADE is equal to the CATE when interference is removed. Under the model of Section 2, the CADE and the CAIE converge to mean-field limits, that depend on a combination of average price elasticities and conditional average direct effects of the treatment on outcomes and excess demand.

The sum of the CADE and the CAIE can be used to estimate the optimal unconstrained treatment rule using the experiment of Section 3, which includes price perturbations. The structure of the conditional estimands under equilibrium interference, however, is such that it is possible to use data from a standard RCT, without price elasticity estimates, to estimate the optimal targeting rule when it is constrained to have the same equilibrium effect as the RCT. The optimal treatment rule takes the form of a hyperplane in the space of the conditional average direct effects of the treatment on both outcomes and excess demand. The gain of this targeting rule over a uniform rule is estimable using a data splitting approach. This provides a metric of heterogeneity under equilibrium interference that is estimable using data from a standard RCT and readily available software for CATE estimation.

Finally, in Section 5, we demonstrate the consistency and coverage properties of our treatment effect and variance estimators using simulations of a marketplace with a supply-side nudge intervention that affect individuals directly and indirectly through market prices. We also include an empirical illustration of the equilibrium-stable targeting rule using data from a large cash transfer experiment in Mexico published by Gertler et al. (2012). The targeting rule results in significantly higher estimated average agricultural income for households in the data sample, when average land usage under the targeting policy is constrained to be equal to that of the uniform policy from the original RCT.

1.1 Related Work

As discussed in the introduction, most existing work on treatment effect estimation under equilibrium effects (or other types of interference) adopts a standard randomization-based framework, where SUTVA holds for higher-level clusters of units (Baird et al. 2018, Basse et al. 2019, Hudgens & Halloran 2008, Karrer et al. 2021, Liu & Hudgens 2014, Tchetgen & VanderWeele 2012). Another related approach is the network interference model, which posits that interference operates along a network and the connections between units are sparse (Athey et al. 2018, Leung 2020, Sävje et al. 2021). The sparsity of connections then enables randomization-based methods for studying cluster-randomized experiments to be extended to this setting. In our setting, however, the interference pattern produced by marketplace price effects is dense and simultaneously affects all units, so cluster- or sparsity-based methods are not applicable.

There is very little available work on targeting treatments under interference. One notable exception is Viviano (2019), who estimates treatment allocation rules in a network interference model. However, his results rely on sparsity of the network structure and so they are not directly comparable to ours. Furthermore, Viviano (2019) proceeds via direct empirical welfare maximization over a restricted policy class as in, e.g., Kitagawa & Tetenov (2018) and Athey & Wager (2021), and so he doesn’t define CATE-like quantities in his model. We also note recent work by Sahoo & Wager (2022) on policy learning in a model where agents can strategically modify covariates used for treatment assignment and the policymaker has a budget constraint. They show that this setting results in a type of interference, and consider methods that account for this. Again, however, their approach relies on a form of direct welfare maximization and they do not consider CATE-like quantities.

We use total differentiation of the mean-field equilibrium condition to characterize the sensitivity of the mean-field equilibrium price with respect to the treatment in terms of estimable elasticities and treatment effects. In a theoretical analysis, Johnson (1980) uses a low-skilled labor market-clearing condition to characterize the effects of immigration on domestic employment. Similar techniques are used to express policy effects in terms of estimable elasticities in a variety of non-equilibrium settings; see Chetty (2009). In this paper, we start with a non-parametric stochastic model of a finite-sample marketplace, which has an equilibrium condition that is not differentiable or amenable to traditional techniques. We show that average effects in this stochastic model have limits which correspond to population quantities that are amenable to “sufficient statistics”-type analysis. This leads to valid inference strategies and an analysis of heterogeneity that are not available when working with a population model directly.

In empirical work with observational data, instrumental variables approaches have been used in both parametric and non-parametric settings to estimate price elasticities or a weighted average of elasticities (Angrist et al. 1996, Berry & Haile 2021). Angrist & Krueger (2001) reviews IV approaches and their relation to causal inference for observational data. There is a variety of more recent work on using IV approaches to identify causal effects in a variety of settings beyond a price equilibrium, an incomplete list includes Heckman & Pinto (2018), Chesher & Rosen (2017), and Vazquez-Bare (2022). In our paper, we require an estimate of price elasticities to perform inference on average treatment effects. The price elasticities required are an average over all individuals in the market, rather than a weighted average as in the Local Average Treatment Effect literature. Our introduction of price perturbations can be interpreted as creating an ideal instrumental variable for the market price, where by construction everyone in the market is a complier so that the required price elasticities are estimated exactly. In settings where it is not possible to randomize individual-level fees, then with additional assumptions, a more structured IV-based approach could be used instead for estimating elasticities. Given there is already a large existing literature on price elasticity estimation in settings where there is more limited variation available in the data, we do not explore this direction further in this paper.

In development economics, there is concern that interventions can have general equilibrium effects that have a meaningful welfare impact but are not captured by standard randomized control trials. Banerjee et al. (2021) uses a cluster-randomized experiment to show that, in certain remote villages, in-kind food subsidies can have an impact of market prices. Other recent work on general equilibrium effects in development settings includes the structural approach of Duflo (2004) and the cluster-based approach of Muralidharan et al. (2017) and Egger et al. (2022). Our results suggest that it is possible for researchers to evaluate general equilibrium effects without running a cluster-randomized experiment, if the market of interest has a large number of buyers and sellers and convincing estimates of relevant price elasticities are available.

Reducing policy effects to estimable parameters without fully specifying a model has a long history in economics, see Marschak (1953) and Heckman (2008). Wolf (2019) uses a semi-structural approach to decompose the effect of macroeconomic shocks into partial equilibrium effects and general equilibrium effects (e.g., price effects), but uses time series methods to estimate the price effects, in contrast to the unit-level approach presented in this paper. Heckman et al. (1998) uses a calibrated overlapping generations model to estimate equilibrium treatment effects in a model of school choice in a labor market equilibrium. Neilson et al. (2019) uses a randomized control trial to estimate the direct effect of information provision on school choice but simulates a fully parametric structural model to evaluate equilibrium effects of the treatment. Compared to this existing work, our approach is unique in that it takes a fully non-parametric approach to analyzing general equilibrium effects based on unit-level experiments that reduces to the standard Neyman-Rubin potential outcomes framework when equilibrium effects are removed.

Our use of latent choice models—specifically latent supply and demand curves—to construct potential outcomes builds on a long tradition in econometrics going back to the work of Roy (1951) and Heckman (1979) on endogenous selection models. Heckman & Vytlacil (2005) offer a more recent synthesis line of work, and use it to derive instrumental variable estimators for a number of policy-relevant variables. The specific latent choice model used here is most closely related to that used in Angrist et al. (2000), who used it to characterize the behavior of two-stage least squares estimators when used to estimate supply and demand elasticities.

Our approach relies on positing a stochastic model where the types of individuals are generated by an underlying probability distribution, and analyzing effects in the limit as the number of individuals in the model grows large. This approach is inspired by mean-field modeling. There is a large literature that uses the mean-field limit to study large-scale stochastic systems in operations research, engineering and physics (Mézard et al. 1987, Tsitsiklis & Xu 2013, Vvedenskaya et al. 1996). Also related are economic models where players respond to the average behavior in the system (Weintraub et al. 2008, Hopenhayn 1992, Krusell & Smith 1998).

We also note a handful of recent papers that leverage stochastic modeling and mean-field type results in a causal inference setting. Johari et al. (2020) use a mean-field model to examine the benefits of a two-sided randomization design in two-sided market platforms and quantify the bias due to interference between market participants. Li & Wager (2022) study large sample results for treatment effect estimation under network interference, where units are placed at vertices of an “exposure graph” and a unit’s potential outcome may depend on another unit’s treatment if and only if they are connected by an edge in the graph; they further posit that the exposure graph is randomly generated from a graphon model. Finally, Wager & Xu (2021) consider a model of a marketplace that matches exogenous demand to endogenous supply, with interference via supply cannibalization. They propose using zero-mean perturbations to estimate a revenue gradient and optimize a continuous decision variable dynamically. Our work also uses zero-mean perturbations as part of a unit-level experiment, but is otherwise distinct, given our focus is on treatment effects of a binary intervention in a general price equilibrium.

2 Treatment Effects under Market Interference

2.1 Treatment Effects Under Interference

We first review a definition of treatment effects in the potential outcomes framework when individuals are sampled from a population, which will allow us to model general interference patterns between units. Consider a system comprised of individuals who are sampled independently from a population, where individual has features . We will work in a setting where there is a binary treatment assigned to each individual with Bernoulli probability . The treatment allocation function is . In this paper, we will study both a “standard” RCT where the treatment probability is constant for every individual, and more general settings where the treatment probability can vary with pre-treatment covariates. We assume that overlap holds.

Assumption 1.

Treatments are sampled from a Bernoulli distribution, . For every , .

The vector of treatments for a sample of individuals is . The effect of treatment vector on an individual’s outcome, conditional on all other randomness in the system, is captured by the notion of potential outcomes. We will define the potential outcomes for the sample as the family of mappings , such that is the outcome associated with individual under the treatment assignment . Under interference, potential outcomes for a vector of treatments are only well-defined conditional on the realization of the sample of individuals, which is indicated by the subscript . Since both the sample and the treatment vector are drawn randomly, is a random variable that depends on both the treatment and the characteristics of other individuals with in the sample. Note that this formulation is in contrast to the setting under SUTVA where an individual’s potential outcome depends only on their own treatment , and does not depend on the treatments or characteristics of other individuals in the sample (Hudgens & Halloran 2008, Manski 2013, Aronow & Samii 2017).

Let be the expectation of over the random treatment vector , conditional on all other sources of randomness in the variable . We can define the average direct effect of a binary treatment as the average marginal effect on an individual’s outcome by changing their own treatment:

Here, the notation represents the random vector we obtain by first sampling , and then setting its -th coordinate to a fixed value . Next, we define the average indirect effect of a binary treatment to be the average marginal effect on everyone else’s outcomes by changing an individual’s treatment:

Note also that and depend on potential outcomes , which are stochastic, and therefore are random variables themselves. Furthermore, they depend on the treatment allocation rule , so the ADE for one treatment rule may differ from the ADE under a treatment distribution induced by a different allocation rule. The direct effect defined above is a standard quantity in the causal inference literature (e.g., Halloran & Struchiner 1995, Sävje et al. 2021). The indirect effect is an analogue to the designed to capture the marginal effect of treating -th unit on other units. Hu et al. (2022) discuss both estimands at length, and in particular show that in a number of parametric models for interference, and capture natural parametric notions of interference. Furthermore, the sum of the two effects corresponds to a meaningful policy counterfactual for any treatment rule . This is the effect of a marginal increase in the treatment probability for each individual on average outcomes:

This is a first order approximation to the Global Total Effect (GTE), which is the average effect of treating everyone compared to treating nobody on outcomes:

is the relevant effect for a policymaker making the decision of whether or not to rollout a treatment to a slightly larger fraction of the population. is the relevant effect for making the decision to rollout treatment to everybody. Without interference, and is estimable using data from an RCT where treatment is assigned with constant probability.

Without further restrictions, the ADE and AIE can be difficult to analyze or estimate in a general causal inference model. The goal of this work is to show that we can both characterize and estimate , and by leveraging the fact that interference is mediated via equilibrium prices.

2.2 Potential Outcomes in a Stochastic General Equilibrium Model

In this section, we provide a stochastic model of potential outcomes in a market economy. The market contains a total of types of goods that individuals may buy or sell (an example of our setting is a two-sided market, where some individuals only sell goods and others only buy). The supply and demand of various goods are coordinated via a price equilibrium that approximately clears the market.

We first describe how we can add some structure to the potential outcomes model introduced earlier to capture individuals’ interactions in a market equilibrium. The assumption that we make is that all dependence among individuals’ outcomes is captured by an equilibrium price. In the language of the literature on treatment effects under interference, this means that a market equilibrium statistic along with an individual’s treatment defines an exposure for each individual (Manski 2013, Aronow & Samii 2017).

Assumption 2.

Interference Operates Through Market-Clearing Prices. Let two independent samples from the population be identified by subscripts and . If and , then .

In other words, individual influences outcomes of individual only through their effect on the equilibrium that the market reaches, and not directly through peer effects or some other network interference mechanism. This assumption captures market models where individuals interact through a Nash equilibrium, and choices depend on an individual’s (correct) expectation of market prices, rather than the specific strategies of other individuals in the game.

Assumption 2 implies that potential outcomes in our model can be expressed as , where the function does not depend on the realized sample. It captures the -th unit’s response to its own treatment and to market prices. We are now ready to describe the mechanism that generates the equilibrium price, . In addition to a outcome function , we assume that each individual has a -dimensional excess demand function , which also depends on an individual’s treatment and market prices. is a demand function and is a supply function. For each individual, their outcome, excess demand functions, and characteristics are sampled i.i.d. from some distribution . is the -dimensional price that ensures supply and demand are approximately matched in the resulting stochastic and non-parametric general equilibrium model.

| (1) |

For any vector of treatment assignments , this defines a potential market price conditional on the realization of the excess demand functions for each individual in the sample. The observed market clearing-price is a random variable that depends on the set of realized excess demand functions and the treatment vector . Realized outcomes and excess demand are

Up until this point, the model corresponds to a stochastic Walrasian general equilibrium model (Mas-Colell et al. 1995) with heterogeneous agents and very few assumptions on agent behavior. In our equilibrium model, we can now write and as

| (2) |

In the next section, we will use this stochastic model to examine the behavior of the equilibrium as the market size grows large, which is a key step towards characterizing treatment effects.

2.3 Mean-Field Prices

In this section, we introduce an important concept in our analysis, the mean-field equilibrium price, and demonstrate that the finite sample market-clearing price converges to it at an appropriate rate as the market size grows. To do so, we first set out several regularity assumptions that will ensure that the mean-field equilibrium price is unique, differentiable, and that the convergence to the mean-field price occurs. This requires some additional notation. In the previous section, we described our sampling model, which is that are drawn i.i.d. from a distribution . These functions are in a class, which we define as and . An equivalent representation for the random functions is and for random .

Assumption 3.

Regularity at a Sample Level.

-

1.

is such that the equilibrium price is always an element of some compact set .

-

2.

and are uniformly bounded.

-

3.

and are each a universal Donsker class of functions.

-

4.

For all , and are continuous in with probability 1.

-

5.

In expectation, the equilibrium price sets aggregate excess demand close to zero. For each , where .

The first regularity assumption indicates that we can restrict attention to a compact set in when looking for an equilibrium price. A sufficient condition for this to hold is that for all vectors of prices larger than some upper bound, then all excess demand functions in are weakly negative, and for all prices smaller than some lower bound, then all excess demand functions in are weakly positive. The second assumption rules out infinite potential outcomes, supply or demand. The third assumption says that for any probability distribution governing the random treatments and the random functions, then the function classes indexed by the price are -Donsker. This is a weak assumption that does not rule out typical choices of outcome or excess demand function. Sufficiently smooth functions, such as Lipschitz functions in 1 dimension, are a Donsker class, as are functions with some discontinuities, including step functions and monotonic functions. More generally, Benkeser & Van Der Laan (2016) indicates the class of all cadlag multivariate functions of bounded variation are Donsker classes; see van der Vaart & Wellner (1997) and van der Vaart (1998) for a variety of other examples. Continuity almost everywhere requires that for any given market price, the set of outcome or excess demand functions that are discontinuous there must have 0 probability. If demand functions are step functions, for example, then the location of the step must have a continuous distribution. We don’t require that the finite sample price exactly sets excess demand equal to zero; the final assumption is a restriction on the approximation error of the finite sample price. This assumption implies both that and that .

We next define expected outcome and excess demand functions for individuals in treatment and control. For ,

The mean-field market price is defined as the price that sets the expected excess demand to zero when the treatment is allocating according to : We next impose some additional assumptions on the population outcome and excess demand functions.

Assumption 4.

Regularity at a Population Level.

-

1.

, , and are twice continuously differentiable in for all and with bounded derivatives, where is a column vector stacking and .

-

2.

For all , .

-

3.

The Jacobian is full rank.

-

4.

The matrix is full rank.

While we allow for some non-differentiability at the individual level, the first assumption indicates that we require more smoothness in the moments of the outcomes and excess demand functions. Next, in order for our policy effects to be well defined, we require the mean-field price to be unique and to exactly clear the market. In a single good market, this would only require continuity and strict monotonicity of in . However, in a market with multiple goods, uniqueness and existence of the equilibrium price can be shown by ensuring the mean-field excess demand function is a contraction. Contraction mapping approaches are commonly used to prove equilibrium existence and uniqueness in models of strategic behavior; see for example Cornes et al. (1999) and Van Long & Soubeyran (2000). Other approaches that rely on more primitive assumptions are also possible; under a zero-degree homogeneity assumption in excess demand then a gross-substitutes condition ensures uniqueness (Arrow & Hahn 1971). The last two parts of Assumption 4 ensure that the asymptotic distribution of the finite sample equilibrium price is well defined. The proof of Proposition 1, given in Appendix A.2, is an application of the Banach fixed point theorem.

Proposition 1.

Assumption 4 implies the existence and uniqueness of .

We can now show that as the number of participants in the market grows large, the sample equilibrium price converges to the unique mean-field price; furthermore, this convergence occurs at a rate. The proofs of Theorem 2, given in Appendix A.3, rely on general results for -estimators discussed in, e.g., van der Vaart (1998). Agarwal & Somaini (2018) use a similar technique to characterize the asymptotic distributions of equilibrium cutoffs in school choice mechanisms.

2.4 Mean-Field Treatment Effects

In this section, we show that the random variables and , defined in (2), converge to meaningful mean-field quantities. These mean-field quantities are useful for two reasons. First, they are interpretable, and provide some insight on how interference occurs in a market, and in what settings the indirect effect will be stronger or weaker. Second, they will provide the foundation for our estimation strategy in Section 3. The following theorem is one of our main results and is proved in Appendix A.5.

Theorem 3.

For the result, a key component of the proof is to leverage the convergence of the finite sample equilibrium price to the mean-field price (Theorem 2). We use it to show that the agents’ outcomes become asymptotically independent as grows, which subsequently allows us to evoke the law of large numbers. Showing convergence for is more challenging; the proof relies on an asymptotically linear representation of and concentration results for Donsker classes of functions.

By imposing some non-parametric and stochastic assumptions on the structure of interference, we have shown that the complex expression for the indirect effect in (2) converges to a simple mean-field expression. Our first observation is that the direct effect converges to the difference in the mean-field outcome function evaluated at and . In the next section, we show that this can be estimated with a differences in means estimate. This finding is in line with Sävje et al. (2021), who show that estimators that target the average treatment effect under no-interference settings generally recover the average direct effect under interference. However, our results will go beyond those of Sävje et al. (2021), since we provide a central limit theorem and asymptotically exact confidence intervals for the direct effect.

The indirect effect, which is a key component of the policy counterfactual , is not estimable using variation in treatment only. The mean-field indirect effect is the product of the gradient of the expected outcome function with respect to prices, and the treatment effect on excess demand scaled by the gradient of excess demand with respect to prices. By the implicit function theorem, this is equivalent to the product of the gradient of the outcome function with respect to prices and the sensitivity of market prices to raising everyone’s treatment assignment probability. In settings where the treatment impacts market prices through excess demand, and outcomes are sensitive to market prices, then interference effects and the indirect effect are stronger. In the next section, we will show how each component of and can be estimated using unit-level experiments.

3 Estimation and Inference

In this section we analyze various estimators of treatment effects that use data from unit-level randomized experiments. We first derive the the limiting distribution of a Horvitz-Thompson estimator when data is generated from a standard RCT where for all . This estimator is consistent for the Average Direct Effect, but its asymptotic variance depends on price-elasticity terms that cannot be estimated using data from an RCT that randomizes treatment only. We show that if confidence intervals are constructed using a variance estimator based on the asymptotic variance without price interference, then coverage will not be asymptotically exact.

In order to perform inference for the direct effect and to perform estimation and inference for the indirect effect, we introduce an augmented randomized trial, with Bernoulli randomization for the treatment and local perturbation of market prices to estimate price elasticities. The estimator for the ADE remains unchanged from the standard RCT. Algorithmically, the estimator for the AIE looks like a combination of a Horvitz-Thompson estimator and a weak instrumental variables estimator. Under the augmented randomized experiment, we show how to construct asymptotically valid confidence intervals for both effects.

3.1 Estimation for the Direct Effect in a Standard RCT

In this section, we derive and analyze the asymptotic distribution of differences-in-means types estimators that use data from a standard RCT, described below.

Design 1.

Standard RCT. . is the treatment probability, which is constant.

We use the notation to represent the mean-field equilibrium price when treatment is assigned according to Definition 1. Following a number of recent papers, including Sävje et al. (2021) and Li & Wager (2022), we consider estimating the direct effect using a Horvitz-Thompson Estimator:

| (4) |

Theorem 4.

Our first result, proven in Appendix A.7, is that—even under interference that occurs through market prices—the Horvitz-Thompson estimator converges to the mean-field direct effect at a rate and is asymptotically normal. In other words, mirroring the finding of Sävje et al. (2021), we see that an analyst who ignored marketplace effects and used a Horvitz-Thompson estimator designed for RCT with SUTVA would still consistently target a well defined estimand, namely the ADE. However, unlike in an RCT with SUTVA, this estimand no longer captures the total effect of the intervention.

Furthermore, the asymptotic variance of the Horvitz-Thompson estimator in our model has an additional term due to interference effects. Specifically, this additional term is due to stochastic fluctuations in , and depends on price elasticities. The asymptotic variance of the Horvitz-Thompson estimator in the no-interference case is . A consistent estimator for this is , where is the empirical variance for -length vector and is the empirical mean. If we use the no-interference variance estimator in settings with marketplace interference to construct confidence intervals, then the confidence intervals are not asymptotically exact unless the treatment does not impact the derivative of expected outcomes with respect to prices. Whether they under or overcover depends on the sign of the covariance between and . In order to construct confidence intervals that are always asymptotically exact, we require estimates of price sensitivity of outcomes and excess demand. In the next section, we develop an augmented randomized experiment that allows us to estimate these price sensitivities and to estimate , which is not estimable with treatment randomization only.

3.2 Augmented Randomized Experiment

In order to estimate the AIE or the build confidence intervals for the ADE, we need to get a handle on price elasticities. Here, we do so by considering an augmented experiment that introduces small, unit level price perturbation into our randomization design. The excess demand and outcome processes remain the same as in the previous section, but prices are shifted at an individual level by for individual . This affects the equilibrium in finite samples. The equilibrium price now depends on the realized sample of individuals, the vector of treatments , and a vector of price perturbations :

Under the perturbed equilibrium price, the realized outcomes and excess demand are and

In order to estimate price elasticities, we restrict ourselves to price experiments that meet Definition 1 below. These are price experiments which are unobtrusive in the sense that they don’t disturb the price equilibrium in the limit. Although we allow some experimentation with price, we cannot simply randomize prices globally and estimate the entire excess demand function, for example. There are two reasons for this. First, while it may be possible to make very small changes to individual-level fees on a platform in order to estimate price elasticities, it would be too costly in terms of customer experience to run global price experiments where prices fluctuated more widely. Second, from a technical perspective, extending our results on estimation for the direct effect to the setting with price experimentation requires that we measure outcomes close to the mean-field equilibrium where there is no price experimentation present.

Definition 1.

Unobtrusive Experiment. The distribution of is such that and

| (5) |

A price experiment that follows Definition 1 generates a finite sample market price with the same asymptotic distribution as . Without any further assumptions on outcomes or excess demand, this condition limits our experimentation to mean-zero perturbations, whose size decreases with sample size.

Design 2.

Augmented Randomized Experiment

-

1.

For , is drawn i.i.d. from with .

-

2.

For , , is drawn i.i.d. and uniformly at random from .

-

3.

The perturbation size decreases as the sample size increases. with .

The following Proposition shows that Theorem 2 and Theorem 4 still hold in the perturbed system, which implies that the augmented price experiment introduced meets Definition 1.

Proposition 5.

The mean-field equilibrium under Design 2 has price , which is unchanged from the equilibrium under Design 1. We now develop a point estimator for the indirect effect. Our proposal consists of a combination of Horvitz-Thompson estimators and estimators of price elasticities. The strategy is plug-in estimation based on the functional form for derived in Theorem 3. The estimator is

Let be the -length vector of outcomes, is the matrix of price perturbations, and is the matrix of excess demand observations. Then, is a vector that estimates . The direct effects of the treatment on excess demand are estimated via a Horvitz-Thompson estimator,

| (6) |

Our next result, proved in Appendix A.7, provides a central limit theorem for our indirect effect estimator. This estimator converges at a rate that depends on the magnitude of the price perturbations , and is always slower than the -rate obtained for the direct effect. In deriving this result, it is helpful to note that algorithmically is the product of a weak instrumental variables estimator and a differences in mean estimator. We can then use standard results on the asymptotic variance of IV estimators to guide our analysis.

Theorem 6.

Under general patterns of interference, inference on the indirect effect is challenging (Sävje et al. 2021, Li & Wager 2022). Under dense patterns of interference, there are not consistent estimators for the variance of the indirect effect available in previous work. There are two reasons why our paper overcomes this difficulty. Although our interference pattern is dense, it is structured in that all interference happens through the market price, and the market price forms by satisfying a score condition. This structure leads to an analytical functional form for the variance of the indirect effect, provided in Theorem 6. Second, with data from a richer randomized experiment that includes small price perturbations, we are able to estimate each component of this variance, and the variance for the indirect effect. , where

and and are vectors estimated from regressions of treated and control outcomes on price perturbations. is a matrix which is computed via regressions of each component of excess demand on price perturbations. Meanwhile, for the variance of the indirect effect, we consider where . The asymptotic normal approximation can be used to build confidence intervals for the direct and indirect estimates. For example, for a confidence level of 95%, the confidence intervals are constructed as

The proofs of the following results are given in Appendix A.8.

Remark.

To derive the asymptotic variance of the indirect effect, we can use the delta method to decompose it into one term that depends on and the asymptotic variance of , and one term that depends on and the asymptotic variance of , see Appendix A.7 for details. The second term is asymptotically negligible, since converges at a slower rate than the differences in means estimator. However, we found in simulations that including a second order correction that retains the asymptotically negligible second term leads to better coverage under a wider variety of choices for the perturbation size when the sample size is smaller. is a plug-in estimator for the first term depending only on the asymptotic variance of and . adds a plug-in estimator for the second term, including an estimator for the variance of : where and .

4 Heterogeneous Treatment Effects

So far, we defined a potential outcomes model that captured equilibrium interference but reduced to the Neyman-Rubin model without interference. We then used this model to define average direct and indirect treatment effects under general treatment allocation rules. In the previous section, we proposed estimators for these effects that relied on data generated from randomized trials where the treatment was assigned with constant probability. In this section, we return to general treatment rules and discuss heterogeneous effects and optimal targeting when there is interference through an equilibrium statistic.

The planner controls the treatment allocation function where . The conditional expectation functions are defined as and . We are interested both in quantifying how relevant treatment effects vary with , and how this information can be used to guide choices of that achieve better outcomes.

4.1 Definitions of Conditional Treatment Effects Under Interference

Under SUTVA, the CATE is defined as (Imbens 2004). Without interference, the optimal unconstrained targeting rule allocates treatments only to those with a positive CATE (Manski 2004). In budget-constrained settings, treatments are allocated to those with the largest CATEs above a threshold (Bhattacharya & Dupas 2012). When an individual’s outcome depends on the entire vector of treatments, then the CATE is not well-defined, so it is not possible to immediately extend the existing optimal policy results. There is a much broader space of possible conditional estimands under interference than with SUTVA. Should the estimand be defined under changes to a single individual’s treatment or multiple? Should the estimand be conditional on the treated individual’s covariate, or the covariate of individuals whose treatment response is measured? We begin this section by proposing two definitions of conditional estimands that play a similar role to the ADE and the AIE, but for targeted treatments. Their sum corresponds to a global policy counterfactual that is useful for optimizing covariate-dependent treatment assignment.

Definition 2 proposes the Conditional Average Direct Effect (CADE) and the Conditional Average Indirect Effect (CAIE) under interference. The CADE is the expected effect of treating an individual with covariate value on their own outcomes in a sample of individuals. The CAIE is is the expected effect of treating an individual with covariate value on everyone else’s outcomes in a sample of individuals. When interference is removed, the CADE is equal to the CATE, and the CAIE is zero.

Definition 2.

The Conditional Average Direct Effect is defined as

The Conditional Average Indirect Effect is defined, where , as

The CATE, defined under SUTVA, is a population-level quantity that does not depend on the sample size. Both the CADE and the CAIE are non-random quantities defined in terms of expectations over random outcome functions and treatments. However, unlike the CATE, the conditional average treatment effects defined under interference do depend on the sample size .

We next connect these definitions of heterogeneous effects to a counterfactual of average outcomes with respect to the policy . This result is valid under general patterns of interference. In Section 2, we reported the results of Hu et al. (2022), showing the sum of and is equal to the effect on average outcomes of an infinitesimal increase in each individual’s treatment probability. This is a local approximation to , which is relevant for making a decision on whether or not to treat everyone. For heterogenous effects, comparable results are not currently available in the literature. In Proposition 8, we show that the expected derivative of average outcomes with respect to the treatment probability of an individual who has covariate is the sum of and .

Proposition 8.

Under the assumptions of Theorem 3,

A policymaker may be interested in taking advantage of heterogeneous responses to treatment in the population by implementing a targeting rule, rather than a treatment rule with uniform probability. Proposition 8 shows that the sum of the CADE and the CAIE is relevant for making the decision on which group’s treatment probability to increase, and which to decrease, when covariates are discrete, and the objective is maximizing expected outcomes.

The next step, in Theorem 9, is to derive limits of the heterogeneous effects in our stochastic equilibrium model. This allows us to interpret what influences the CADE and CAIE in settings with interference through market prices.

Theorem 9.

Under the Assumptions of Theorem 3, the limit of the conditional average direct effect is:

The limit of the conditional average indirect effect is:

These limits are interpretable and suggest estimation strategies for and . The limit of the CADE is the direct treatment effect on outcomes conditional on , holding the equilibrium price fixed. The limit of the CAIE is the direct treatment effect on excess demand conditional on , multiplied by an elasticity correction that does not depend on . The augmented randomized experiment from Design 2 can be used to estimate the elasticity corrections and the conditional average treatment effects required to estimate and .

For the elasticity corrections, the market price is an aggregate statistic, so individuals with different covariates all respond to the same market prices. A change in excess demand of a given size always has the same impact on the market price. As a result, although individuals responses to the treatment through outcomes or excess demand are heterogeneous, the elasticity correction that transforms the to is unconditional. This implies that a group of individuals’ effect on the system depends on their covariates only through conditional direct effects. Estimators for and from the previous section of the paper apply directly.

For the conditional average treatment effects on and on , then estimators for the CATE under SUTVA are consistent for the CADE under market interference. In the unconditional setting, we showed in Section 3 that the Horvitz-Thompson estimator, an estimator for the ATE when SUTVA holds, is consistent for the ADE even with equilibrium interference, and Sävje et al. (2021) shows that this holds for any pattern of interference. The argument in Theorem 4 extends to the conditional setting. There are a variety of consistent estimators for the CATE that take as input from an experiment that randomizes . See, for example, Athey et al. (2019) for a random-forest based estimator that we use to estimate the CADE on and on in Section 5.

The results in Proposition 8 link the sum of the CADE and the CAIE to the expected change in average outcomes from increasing the treatment probability of individuals with covariate . This result implies that estimators for the CADE and the CAIE can be used to optimize expected outcomes without constraints by (repeatedly) adjusting in the direction of the estimated derivative of expected outcomes with respect to .

4.2 Equilibrium-Stable Targeting

In the previous section, we briefly discussed how estimates of and could be used to (locally) optimize an unconstrained targeting policy. There are a variety of constrained targeting rules that may be of interest. Here, we focus on one specific question of this type, namely what is the optimal treatment assignment policy that does not move equilibrium prices relative to those seen in the experiment? There are two reasons to consider this class of targeting rules. First, a conservative policymaker may be reluctant to significantly modify the equilibrium—even if it is beneficial on average to individuals—and so they may want to know how much they can improve outcomes without changing the equilibrium. Second, from a practical point of view, we find that the answer to this question admits a simple econometric strategy, and can be answered without needing to estimate price elasticities and without recourse to an augmented experimental design. Instead, the optimal equilibrium-stable targeting rule (and its performance) can be estimated using data from a baseline RCT following Design 1, as long as the RCT collects outcome and relevant supply and demand data at an individual level.

The optimization problem for the equilibrium-stable policy is to maximize expected outcomes while ensuring the mean-field equilibrium price under the policy , which is , is unchanged from one where individuals are treated with uniform probability for all :

| (7) |

In Proposition 10, we show that when the targeting policy is restricted to have the same equilibrium effect as a baseline policy, then solving for that optimal policy takes the form of a tractable linear optimization problem.

Proposition 10.

In contrast to the previous sections of the paper, we do not require estimates of price elasticities to estimate this rule. We can estimate a solution to this using a dataset from a standard RCT by solving a linear program, where for each unit we plug in an estimate of and .

Furthermore, the optimal rule has an intuitive structure. Proposition 11 describes how the optimal treatment rule takes the form of a separating hyerplane, where individuals are treated if their CADE on Y lies above a line defined in - space. The absolute value of each element of the coefficient can be interpreted as a shadow price. It is the incremental value of an incremental relaxation of the constraint that the equilibrium price under the targeted policy is equal to the equilibrium price under the uniform policy. Its sign indicates in which direction the constraint that is relaxed in order to increase the objective.

Proposition 11.

Assume that is discrete. A rule is a solution to Proposition 10 if and only if it has the following form,

| (8) |

for some and , and satisfies the equilibrium-stability constraint .

This rule can be interpreted as follows. Ignoring the equilibrium effect, the optimal targeting rule allocates any individual with to treatment. Let’s assume that in a setting with this results in a larger treatment effect on excess demand than the uniform RCT. In order to respect the equilibrium-stability constraint, this rule is adjusted, so that those with negative and small but negative and large are treated, and those with positive and small but positive and large are controlled. The amount of this adjustment depends on the magnitude of .

Compared to the rule that allocates treatment to those with a positive CADE on Y and ignores equilibrium effects, the optimal equilibrium-stable rule will always have lower expected outcomes, but will also have a different equilibrium effect. Our preferred benchmark is the uniform rule that assigns treatment with probability and has the same equilibrium effect in expectation as the targeting rule. We can evaluate the gain of the heterogeneous treatment rule over the uniform rule using data from an RCT and a data-splitting procedure.

We use the following procedure, which operates on a dataset with a vector of outcomes , a vector of randomly assigned treatments , a matrix of covariates and a vector of excess demand . When , finding is straightforward. The estimated score condition is monotonic in a single , so we can start at and adjust it either up or down until the score condition is equal to zero. When , extending this procedure requires solving a plug-in version of the linear program to estimate .

-

1.

On a training dataset of size , estimate and using a consistent estimator for conditional average treatment effects, such as the causal forest of Athey et al. (2019).

-

2.

Let . Choose such that

-

3.

On a test dataset of size , evaluate and and compute for each .

-

4.

The gain in the targeting rule compared to the uniform rule is computed as

-

5.

The equilibrium stability of the targeting rule on the test set is computed as

This metric is zero when the targeting rule is equilibrium-stable for the test set.

In the next section, we will use this procedure illustrate the gain of an equilibrium-stable targeting rule over a uniform rule that targets using data from a cash transfer experiment.

5 Simulation and Application

In the first part of this section, we highlight the results from Sections 2 and 3 using a simulation of a “nudge” intervention in a two-sided market for freelance labor. We illustrate how looking at only the direct effect of the intervention (via a difference in means estimator) from an RCT results in a substantial over-estimate of the global treatment effect. We confirm numerically that, when treatments affect market prices, the indirect effect can have a substantial magnitude—but is estimable in finite samples via our proposed unit level augmented experiment. We also find that in finite samples our asymptotic approximations for the distributions of the direct and indirect effect are accurate enough to yield confidence intervals with good coverage properties. In the second part of this section, we estimate the equilibrium-stable targeting rule of Section 4 using data from a cash transfer experiment.

5.1 Simulation of Market for Freelance Labor

We simulate a two-sided market where, depending on the market price and their own preferences, suppliers with heterogeneous costs choose whether to complete 0, 1 or 2 jobs on the platform. On the other side of the market, consumers will book a job if the market price is less than their heterogeneous value for the job. The market price is set to clear the market for freelance labor. In the absence of an intervention, suppliers who have cost less than the market price will always complete one job, but will complete two jobs only 30% of the time (even though it is profitable for them). The treatment is an intervention, such as a reminder, that encourages active suppliers to complete a second job on the platform. We simulate the effect of an intervention that is highly effective; a supplier that receives the message will complete two jobs 70% of the time, as long as it is profitable for them to do so. The platform operator is interested in estimating the effect on average supplier revenue of rolling out this intervention, which is the Global Treatment Effect.

Formally, the demand and supply functions are

if an individual is a supplier on the platform. follows a standard uniform distribution, and we have that both and are sampled from a distribution. Half of a sample of individuals are suppliers and the other half are consumers. Supplier revenue is . The market price for contract work sets the average excess demand to zero.

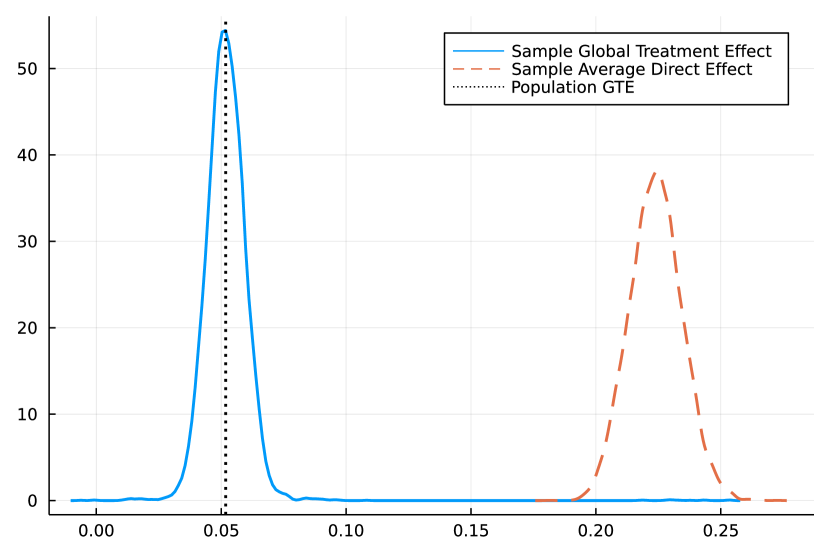

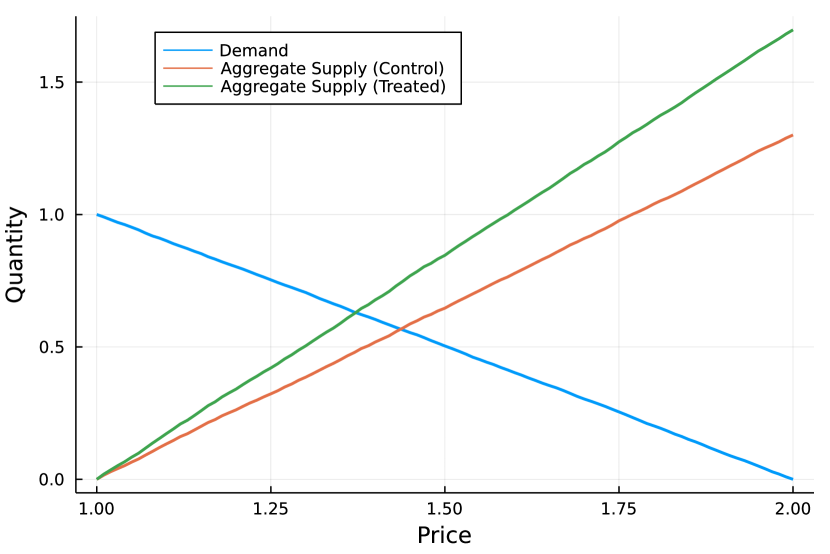

In Figure 1(a), we plot the smoothed distribution of the average direct effect and the global treatment effect, computed over 10,000 samples of a marketplace, where each sample is of 2,000 individuals. An RCT estimates the ADE, which is more than triple the Global Treatment Effect. Figure 1(b) explains why the ADE and GTE are so different in this setting. The figure shows the effect of the treatment on aggregate supply for a sample of 10,000 individuals. Aggregate demand is unchanged from the treatment. The treatment makes it more likely that already profitable suppliers complete a second job, which shifts the slope of the supply curve. This impacts the market-clearing price for the control market compared to the treated market. Holding market prices fixed, the effect of the treatment is a large positive increase in revenue. However, when the effect on market prices is taken into account, which is represented by a large negative indirect effect, then the global treatment effect is much lower.

In Table 1, we report the results of a Monte Carlo simulation with 10,000 repetitions and a sample size of to evaluate the bias, variance, and coverage properties of the estimators and confidence intervals for and . The ground truth and are calculated numerically. The table illustrates that the bias of the average direct effect and indirect effect estimator based on the augmented randomize experiment are low in finite samples. Furthermore, the coverage when and are used to construct confidence intervals in finite samples is very close to the asymptotic confidence level of 95%. If only data from an RCT was available, then an estimate for the AIE is not available, while the estimator for the ADE remains a Horvitz-Thompson estimator. The naive confidence interval that assumes no-interference for the direct effect can be computed using data from an RCT. In this simulation, the naive approach gives asymptotically conservative confidence intervals, so has slightly wider confidence intervals, and over-covers compared to the asymptotically exact approach.

| Estimate | Bias | S.D. | Coverage | |

|---|---|---|---|---|

| 0.227 | 0.004 | 0.06 | 0.957 | |

| -0.173 | -0.003 | 0.05 | 0.954 |

5.2 Targeting Cash Transfers

There is a large literature in development economics that randomly allocates cash transfers to households and evaluates the short and long-term impacts on a variety of outcomes, including consumption, savings and investment (Haushofer & Shapiro 2016), health (Haushofer et al. 2020), and criminal behavior (Hidrobo et al. 2016, Blattman et al. 2017).111See the research paper explorer at https://www.givedirectly.org/cash-evidence-explorer/ for a more comprehensive review of cash transfer RCTs.

Depending on the characteristics of the local economies where cash transfers are allocated and the type of outcome evaluated, there may be equilibrium interference that impacts the evaluation of the transfer program. Cunha et al. (2019), for example, find meaningful price impacts for in-kind transfers in an evaluation in Mexico, while Egger et al. (2022) find minimal price impacts for a large scale cash transfer in Kenya. The results in Section 3 indicate that estimating the Global Total Effect of an intervention using data from an RCT requires estimating of elasticities of outcomes, supply, and demand with respect to prices. However, our results in Section 4 indicate that even without price elasticities, we can use data from an RCT to analyze the gain from exploiting heterogeneity in the data when we constrain equilibrium effects under a targeted policy to be equal to that under the RCT.

We examine the publicly available data from the replication package of Gertler et al. (2012), which examined the long-term impacts of PROGRESA, a conditional cash transfer program in Mexico which was rolled out randomly at a community-level, beginning in 1998. The community-level assignment was due to logistical and operational constraints, rather than an attempt to control spillovers, so we expect that given the proximity of treatment and control households, they would have interacted with one another in many markets.

The program included a monthly stipend of 50 pesos per month, and an additional educational stipend, depending on the number of the children in the household, with the total capped at 550 pesos per month. There are 320 treatment communities, which were immediately enrolled in the program, and 186 control communities, which were phased into treatment over time. The data from Gertler et al. (2012) contains a variety of baseline covariates from the 1997 ENCASEH census for households originally classified as poor and eligible for the intervention, as well as measurements from evaluation surveys that were given to all households in treatment and control communities every 6 months, starting in 1998. The evaluation surveys collected a variety of data on household education, consumption, investments, savings, and agricultural income. We follow the original paper in pooling data from October 1998 to November 1999, which was the purely experimental period, before control households began to be enrolled in the program. We are interested in using a subset of the data to answer a specific question, which is how a policymaker could target a PROGRESA-like subsidy to households to maximize agricultural income, when land usage under the targeted policy is constrained to be equal to that of the RCT. We compute the structure of the targeting rule, and estimate how much the optimal targeted policy raises outcomes compared to the uniform policy.

Before describing our results, we first explain a few caveats that should be kept in mind. First, depending on how quickly prices adjust and the geographic proximity of treated and control households, the community-level assignment could result in different equilibrium conditions for treated and control households. For the purposes of illustrating our method, we assume that treated and control individuals are responding to similar market prices in the experimental period, so that the conditional direct effects we measure do not include an equilibrium effect. Second, a general cash subsidy likely results in equilibrium effects of varying strength that occur through an enormous variety of channels, including the labor market, commodities markets, and even financial markets. For this exercise, we assume that the farm subsidy has an equilibrium effect on outcomes through a single good only, which is the usage of land. Last, it is possible that the usage of land is very slack, so that if the treatment increases usage of land, there is no effect on the actual market demand for land. We assume that the net usage of land does proxy for the net market demand for land in our sample, so that our constraint on land usage corresponds to an equilibrium stability condition.

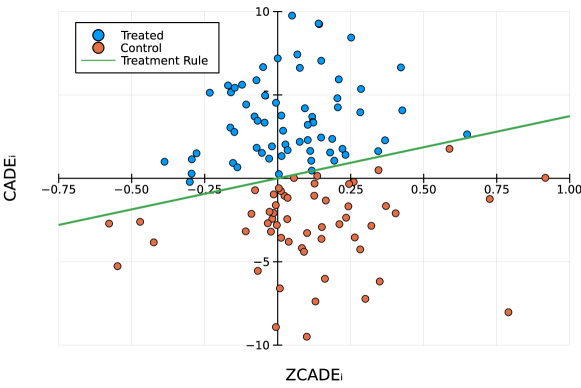

In Figure 2, we illustrate the optimal rule estimated using a sample of households from Waves 2-4 of the survey. There are 20 covariates in , which are all pre-treatment household demographic characteristics from 1997, such as age and gender of the head of household, the existing landholdings and animal ownership of the household, and whether or not the house had electricity. The outcome is agricultural income per individual in the household, including crop sales, sales from animal products, and home consumption. Ignoring equilibrium effects, a good targeting rule allocates treatment to those individuals who are estimated to have a positive CADE. This rule, however, results in a larger impact on demand for land compared to the RCT, since on average, those who increase their agricultural income using the subsidy also increase their usage of land. However, there is some heterogeneity in the usage of land. The optimal rule that respects the equilibrium constraint allocates treatment to those with . We can see that for the most part, it is those with a positive CADE that are treated. However, those with a large have their treatment status flipped from the naive rule that ignores the equilibrium constraints. Those, for example, who use a lot of additional land but have a small impact on agricultural income, are dropped from the equilibrium-stable targeting rule.

| Gain | Equilibrium-Stability | ||

|---|---|---|---|

| Estimate | 2.27 | -0.006 | 0.92 |

| Standard Error | (0.44) | (0.021) | (1.12) |

We then evaluate the gain in the targeted rule compared to the uniform rule using the data-splitting approach described at the end of Section 4.2. The results are reported in Table 2. We find that the lift is 2.27 and significantly different from zero at a 5% level. In this example, there is modest heterogeneity in outcomes and demand for land. When this is exploited via the optimal equilibrium-stable targeting rule, the point estimate for the gain over the uniform rule is positive and large. The equilibrium stability metric is -0.006 with a standard error of 0.44, so on average the treatment rule estimated on the training set is disturbing the equilibrium on the test set by a very small amount, compared to the uniform rule.

6 Discussion

Analyzing the performance of randomized control trials in settings with equilibrium effects is needed given the rapid growth of experimentation both in practice and in research studies. The Neyman-Rubin framework that relies on SUTVA rules out interaction effects that can have an important impact on decision-relevant treatment effects. A parametric structural model may capture a variety of complex equilibrium effects, but is not robust to misspecification, which can be problematic when individuals behave in complex and heterogeneous ways. A model of treatment effects under general patterns of interference is intractable without clustering or other assumptions.

This paper shows that it is fruitful to marry ex-ante knowledge about the structure of an economic environment with a non-parametric stochastic model of treatment effects under interference. This leads to a characterization of asymptotic properties of treatment effects and estimators of those treatment effects based on new and existing experimental designs that are robust to a wide range of modeling choices. Results on estimation, inference, and optimal targeting in complex environments with some economic structure imposed can then be easily contrasted with the large body of work that studies casual inference under SUTVA.

There are a variety of avenues for future work possible. One limitation of our approach is that we analyze the large sample limit of the market place where the number of suppliers and the number of buyers grow large; an analysis of experiments in settings where firms have significant market power would likely require different techniques. In general, extending our results to a broader class of equilibrium mechanisms would be of considerable interest.

References

- (1)

- Abadie et al. (2017) Abadie, A., Athey, S., Imbens, G. W. & Wooldridge, J. (2017), When should you adjust standard errors for clustering?, Technical report, National Bureau of Economic Research.

- Abbring & Heckman (2007) Abbring, J. H. & Heckman, J. J. (2007), ‘Econometric evaluation of social programs, part iii: Distributional treatment effects, dynamic treatment effects, dynamic discrete choice, and general equilibrium policy evaluation’, Handbook of econometrics 6, 5145–5303.

- Ackerberg et al. (2007) Ackerberg, D., Benkard, C. L., Berry, S. & Pakes, A. (2007), ‘Econometric tools for analyzing market outcomes’, Handbook of econometrics 6, 4171–4276.

- Agarwal & Somaini (2018) Agarwal, N. & Somaini, P. (2018), ‘Demand analysis using strategic reports: An application to a school choice mechanism’, Econometrica 86(2), 391–444.

- Angrist et al. (2000) Angrist, J. D., Graddy, K. & Imbens, G. W. (2000), ‘The interpretation of instrumental variables estimators in simultaneous equations models with an application to the demand for fish’, The Review of Economic Studies 67(3), 499–527.

- Angrist et al. (1996) Angrist, J. D., Imbens, G. W. & Rubin, D. B. (1996), ‘Identification of causal effects using instrumental variables’, Journal of the American statistical Association 91(434), 444–455.

- Angrist & Krueger (2001) Angrist, J. D. & Krueger, A. B. (2001), ‘Instrumental variables and the search for identification: From supply and demand to natural experiments’, Journal of Economic perspectives 15(4), 69–85.

- Aronow & Samii (2017) Aronow, P. M. & Samii, C. (2017), ‘Estimating average causal effects under general interference, with application to a social network experiment’, The Annals of Applied Statistics 11(4), 1912–1947.

- Arrow & Hahn (1971) Arrow, K. J. & Hahn, F. (1971), ‘General competitive analysis’.

- Athey et al. (2018) Athey, S., Eckles, D. & Imbens, G. W. (2018), ‘Exact p-values for network interference’, Journal of the American Statistical Association 113(521), 230–240.

- Athey & Imbens (2016) Athey, S. & Imbens, G. (2016), ‘Recursive partitioning for heterogeneous causal effects’, Proceedings of the National Academy of Sciences 113(27), 7353–7360.

- Athey et al. (2019) Athey, S., Tibshirani, J. & Wager, S. (2019), ‘Generalized random forests’, The Annals of Statistics 47(2), 1148–1178.

- Athey & Wager (2021) Athey, S. & Wager, S. (2021), ‘Policy learning with observational data’, Econometrica 89(1), 133–161.

- Baird et al. (2018) Baird, S., Bohren, J. A., McIntosh, C. & Özler, B. (2018), ‘Optimal design of experiments in the presence of interference’, Review of Economics and Statistics 100(5), 844–860.

- Banerjee & Duflo (2011) Banerjee, A. & Duflo, E. (2011), Poor economics: A radical rethinking of the way to fight global poverty, Public Affairs.

- Banerjee et al. (2021) Banerjee, A., Hanna, R., Olken, B. A., Satriawan, E. & Sumarto, S. (2021), Food vs. food stamps: Evidence from an at-scale experiment in indonesia, Technical report, National Bureau of Economic Research.

- Basse et al. (2019) Basse, G. W., Feller, A. & Toulis, P. (2019), ‘Randomization tests of causal effects under interference’, Biometrika 106(2), 487–494.

- Benkeser & Van Der Laan (2016) Benkeser, D. & Van Der Laan, M. (2016), The highly adaptive lasso estimator, in ‘2016 IEEE international conference on data science and advanced analytics (DSAA)’, IEEE, pp. 689–696.

- Berry et al. (1995) Berry, S., Levinsohn, J. & Pakes, A. (1995), ‘Automobile prices in market equilibrium’, Econometrica: Journal of the Econometric Society pp. 841–890.

- Berry & Haile (2021) Berry, S. T. & Haile, P. A. (2021), Foundations of demand estimation, in ‘Handbook of Industrial Organization’, Vol. 4, Elsevier, pp. 1–62.

- Bhattacharya & Dupas (2012) Bhattacharya, D. & Dupas, P. (2012), ‘Inferring welfare maximizing treatment assignment under budget constraints’, Journal of Econometrics 167(1), 168–196.

- Blattman et al. (2017) Blattman, C., Jamison, J. C. & Sheridan, M. (2017), ‘Reducing crime and violence: Experimental evidence from cognitive behavioral therapy in liberia’, American Economic Review 107(4), 1165–1206.

- Boucheron et al. (2013) Boucheron, S., Lugosi, G. & Massart, P. (2013), Concentration inequalities: A nonasymptotic theory of independence, Oxford university press.

- Chesher & Rosen (2017) Chesher, A. & Rosen, A. M. (2017), ‘Generalized instrumental variable models’, Econometrica 85(3), 959–989.

- Chetty (2009) Chetty, R. (2009), ‘Sufficient statistics for welfare analysis: A bridge between structural and reduced-form methods’, Annu. Rev. Econ. 1(1), 451–488.

- Cornes et al. (1999) Cornes, R., Hartley, R. & Sandler, T. (1999), ‘Equilibrium existence and uniqueness in public good models: An elementary proof via contraction’, Journal of Public Economic Theory 1(4), 499–509.

- Cunha et al. (2019) Cunha, J. M., De Giorgi, G. & Jayachandran, S. (2019), ‘The price effects of cash versus in-kind transfers’, The Review of Economic Studies 86(1), 240–281.

- Duflo (2004) Duflo, E. (2004), ‘The medium run effects of educational expansion: Evidence from a large school construction program in indonesia’, Journal of Development Economics 74(1), 163–197.

- Egger et al. (2022) Egger, D., Haushofer, J., Miguel, E., Niehaus, P. & Walker, M. (2022), ‘General equilibrium effects of cash transfers: experimental evidence from kenya’, Econometrica 90(6), 2603–2643.

- Fisher (1935) Fisher, R. A. (1935), The Design of Experiments, Oliver and Boyd, Edinburgh.