Sparse PCA: A New Scalable Estimator Based On Integer Programming

Abstract

We consider the Sparse Principal Component Analysis (SPCA) problem under the well-known spiked covariance model. Recent work has shown that the SPCA problem can be reformulated as a Mixed Integer Program (MIP) and can be solved to global optimality, leading to estimators that are known to enjoy optimal statistical properties. However, current MIP algorithms for SPCA are unable to scale beyond instances with a thousand features or so. In this paper, we propose a new estimator for SPCA which can be formulated as a MIP. Different from earlier work, we make use of the underlying spiked covariance model and properties of the multivariate Gaussian distribution to arrive at our estimator. We establish statistical guarantees for our proposed estimator in terms of estimation error and support recovery. We propose a custom algorithm to solve the MIP which is significantly more scalable than off-the-shelf solvers; and demonstrate that our approach can be much more computationally attractive compared to earlier exact MIP-based approaches for the SPCA problem. Our numerical experiments on synthetic and real datasets show that our algorithms can address problems with up to features in minutes; and generally result in favorable statistical properties compared to existing popular approaches for SPCA.

1 Introduction

Principal Component Analysis (PCA) (Hotelling, 1933) is a well-known dimensionality reduction method where one seeks to find a direction, a Principal Component (PC), that describes the variance of a collection of data points as well as possible. In this paper, we consider the spiked covariance model (Johnstone, 2001). Suppose we are given samples for , drawn independently from a multivariate normal distribution (where is the covariance matrix). We let denote the data matrix with -th row . In the spiked covariance model, we assume

| (1) |

where has unit -norm and is the identity matrix of size . We let be the Signal to Noise Ratio (SNR) of the model (1). Informally speaking, all other factors remaining same, a higher value of the SNR makes the task of estimating relatively easier. Following Bresler et al. (2018), here we consider the setting where . Given , we seek to estimate the vector (up to a sign flip) which corresponds to the true PC. If denotes an estimator of , then we can measure the quality of this estimator via the sine of the angle between and (a smaller number denoting higher accuracy). Mathematically, for such that , we define:

| (2) |

In the high dimensional regime when the number of features () is much larger than the number of samples i.e., , Johnstone and Lu (2009); Paul (2007) show that the simple PCA estimator may be inconsistent for unless one imposes additional assumptions on . A popular choice is to assume that is sparse with nonzeros—in this case, we find a PC with nonzeros (for example)—this is commonly known as the sparse PCA problem or SPCA for short (Jolliffe et al., 2003; Hastie et al., 2019). Johnstone and Lu (2009) propose the diagonal thresholding algorithm for SPCA that results in consistent estimation of the support of if (Amini and Wainwright, 2009)111The notations are used to show an inequality holds up to an universal constant that does not depend upon problem data., a notable improvement over vanilla PCA that requires to be larger than . In this paper, we study the SPCA problem under the spiked covariance model where is -sparse. We also study a generalization where the vector is approximately sparse.

In the remainder of this section, we first present an overview of current algorithms for SPCA and then summarize our key contributions in this paper.

1.1 Background and Literature Review

A well-known procedure to estimate is to consider the following optimization problem:

| (3) |

which finds a direction with at most nonzero entries that maximizes the variance of the data along that direction. Amini and Wainwright (2009) have shown that the optimal solution to this problem attains the minimax optimal rate in terms of variable selection. In fact, Amini and Wainwright (2009) show that no algorithm can recover the PC consistently unless (information theory lower bound). Problem (3) involves the maximization of a convex quadratic over a nonconvex set, and poses computational challenges. Several algorithms (Hastie et al., 2019, see for example) have been proposed to obtain good solutions to (3)—this includes both exact and approximate methods. In what follows, we review some existing algorithms and divide them into three broad categories.

Polynomial-time Algorithms: A well-known procedure to obtain convex relaxations for Problem (3) is based on Semidefinite Programming (SDP) (d’Aspremont et al., 2005, 2008). SDP-based relaxations of SPCA can recover the support of PC if the SDP returns a rank one solution and when (Amini and Wainwright, 2009). However, Krauthgamer et al. (2015) show that if , the SDP formulation may not result in a rank one solution.

In an interesting line of work, Berthet and Rigollet (2013); Wang et al. (2016) provide theoretical evidence that under the planted clique hypothesis, it may not be possible to have a polynomial-time algorithm for SPCA if . Deshpande and Montanari (2016) show that a polynomial-time method called covariance thresholding can estimate if . Moreover, when for some constant , Deshpande and Montanari (2016) show samples suffice. The recent work of Bresler et al. (2018) shows that SPCA solutions can be obtained by solving a sequence of sparse linear regression problems. One of their approaches requires solving separate Lasso-regression problems, leading to a polynomial-time algorithm.

A key difference between the SDP-relaxation approach and the covariance thresholding method lies in their computational efficiencies: the covariance thresholding method can be scaled to instances with or so, and is computationally (much more) attractive compared to SDPs which are mostly limited to instances with in the hundreds (using off-the-shelf convex optimization solvers).

Exact and MIP-based Algorithms: In another line of work, exact approaches i.e., methods that lead to a globally optimal solution to (3) have been proposed. For example, authors in Moghaddam et al. (2006) present a tailored branch-and-bound method to solve SPCA when . Fairly recently, starting with the work of Bertsimas et al. (2016) in sparse regression, there has been significant interest in exploring Mixed Integer Programming (MIP) approaches in solving sparse learning problems that admit a combinatorial description. In particular, MIP-based approaches have been proposed to address Problem (3) for moderate/small-scale instances, as we discuss below. MIP-based approaches seek to obtain the global optimum of Problem (3)—they deliver a good feasible solution and corresponding upper bounds (aka dual bounds)—taken together they certify the quality of the solution. Berk and Bertsimas (2019) present a tailored branch-and-bound method that can obtain near-optimal solutions for Problem (3) for . In a different line of work, Dey et al. (2018) present MIP-formulations and algorithms for (3) and a relaxation that replaces the -constraint on , by an -constraint resulting in a non-convex optimization problem. This approach delivers upper bounds i.e., dual bounds to (3) for up to . Other recent MIP-based approaches include Bertsimas et al. (2020) who consider mixed integer semidefinite programming (MISDP) approaches and associated relaxations of computationally expensive semidefinite constraints. In another line of work, Li and Xie (2020) discuss MISDP formulations and approximate mixed integer linear programming approaches for SPCA. Some of the approaches presented in Li and Xie (2020); Bertsimas et al. (2020) succeed in obtaining dual solutions to SPCA for or so.

In this paper, we also pursue a MIP-based approach for the SPCA problem. However, instead of Problem (3) which (in our experience) is challenging to scale to large instances, we consider a different criterion that arises from the statistical model (1). Our estimator is given by a structured sparse least squares problem—our custom MIP-based approach can solve this problem to optimality for instances up to , which is 10X larger than earlier MIP approaches (Dey et al., 2018; Li and Xie, 2020).

Heuristics: Several appealing heuristic algorithms have been proposed to obtain good feasible solutions for Problem (3) and close variants (e.g., involving an -sparsity constraint instead of the -constraint)—see for example, Zou et al. (2006); Richtárik et al. (2020); Luss and Teboulle (2013); Witten et al. (2009). A popular approach is the Truncated Power Method (Yuan and Zhang, 2013), which enjoys good statistical guarantees and numerical performance if a good initialization is available. However, in the absence of a good initialization, this method can converge to a suboptimal local solution which may be even orthogonal to the underlying PC—this is illustrated by our experiments in Section 5 and also discussed in Gataric et al. (2020). Unlike MIP-based approaches discussed above, heuristic methods do not deliver dual bounds—it may not be possible to certify the quality of the solution. In practice, some of these heuristic algorithms can lead to good feasible solutions for (3) for or so.

1.2 Outline of Approach and Contributions

The different algorithms discussed above have their respective strengths and limitations. While there is an impressive body of work on heuristics and polynomial-time algorithms for the SPCA problem, there has been limited investigation on MIP-based approaches, despite promising recent results. In this paper, our focus is to consider a MIP-based approach for the SPCA problem. However, in departure from current approaches based on MIP, which focus on (3), we consider a different estimation criterion. We make use of the spiked covariance model (1) and properties of a multivariate Gaussian distribution to arrive at a mixed integer second order cone program (MISOCP) that can be interpreted as a least squares problem with structured sparsity constraints, where the constraints arise from the spiked covariance model structure. To our knowledge, the estimator we propose and study herein has not been considered earlier in the context of the SPCA problem; and we study both statistical and algorithmic aspects of the proposed estimator.

By extending recent work on specialized algorithms for sparse regression-type problems (Hazimeh and Mazumder, 2020; Hazimeh et al., 2020; Bertsimas and Van Parys, 2020), we propose a custom algorithm that can solve our proposed SPCA MIP formulation for instances with (and ) in minutes—the corresponding estimation accuracy of these solutions appear to be numerically better than several polynomial-time and heuristic algorithms that we compare with.

In terms of statistical properties, we establish an estimation error bound as where is the estimated PC by our method, when is -sparse. Importantly, we also establish a novel oracle-type inequality where the underlying need not be -sparse. This shows that exact sparsity on is not needed to achieve the rate as long as the PC is close enough to a vector with nonzeros (this is made precise later). Our analysis is different from the work of Johnstone and Lu (2009) who assume a certain decay for the coordinates of . In terms of variable selection, under certain regularity conditions, our method recovers the support of correctly with high probability if . We also derive error bounds for an approximate solution available from our framework222Our MIP-based algorithms deliver optimality certificates (available from dual bounds) along the course of the algorithm. These optimality certificates appear in the statistical error bounds of approximate solutions available from our optimization criterion. which can be useful in practice, especially if a practitioner decides to use an approximate solution returned by our method.

To our knowledge, this is a first work that makes use of statistical modeling assumptions to obtain a MIP-based optimization formulation for the SPCA problem, which is computationally more attractive compared to the original formulation (3). Our proposed estimator is not equivalent to (3), we establish that the statistical properties of our estimator are similar to that of an optimal solution to (3) when is small. Our contributions are summarized below:

-

1.

We provide a novel MISOCP formulation for the SPCA problem under the assumption of the spiked covariance model (1). To the best of our knowledge, our work is the first to reformulate SPCA into a computation-friendly MIP via statistical modeling reductions.

-

2.

We show that our proposed estimator has an estimation error rate of —this rate is achievable under certain conditions even if is not -sparse. We also show that if , our method recovers the support of correctly.

-

3.

We propose a custom cutting plane algorithm to solve the MISOCP describing our SPCA estimator—our approach can address instances of the SPCA problem with , and leads to significant computational improvements compared to off-the-shelf MIP solvers for the same problem.

-

4.

We demonstrate empirically that our framework can lead to SPCA estimators with superior statistical properties compared to several popular SPCA algorithms.

Notation. For a vector , let denote the -th coordinate of . For a positive integer , we let . For a matrix , let , and denote the -th coordinate, the -th row and -th column of , respectively. For a matrix and sets , we let denote the sub-matrix of with rows in and columns in . In particular, if , we let be the vector . For the data matrix and a set , we let denote . If and , we let be a sub-vector of with coordinates in . For a vector , we let denote its support, We let denote the unit Euclidean unit ball in i.e., For a vector , we let be the -pseudonorm of , denoting the number of nonzero coordinates of . We denote the smallest and largest eigenvalues of a positive semidefinite matrix , by , respectively. Similarly, , denote the smallest and largest singular values of matrix , respectively. For a convex function , denotes the set of subgradients of at . The notations denote that inequality holds up to an universal constant (i.e., one with no dependence on problem data). Throughout the paper, we use the convention . The proofs of main results can be found in the appendix.

2 Proposed Estimator

Here we present our proposed estimator for the SPCA problem. We first recall a well-known result pertaining to multivariate Gaussian distributions.

Lemma 1.

Let be a random vector from where is a positive definite matrix. For any , the conditional distribution of , given is given by

| (4) |

where, and .

The following lemma writes in terms of the parameters of the spiked covariance model (1).

Lemma 2.

For notational convenience, we let the diagonal entries of the matrix to be zero, that is, for . Lemma 2 shows that the sparsity pattern of the off-diagonal entries of is the same as that of the off-diagonal entries of . In particular, can be nonzero only if both the -th and -th coordinates of are nonzero i.e., . As we assume has nonzeros, at most values of can be nonzero. By Lemma 1, for every , we have

For a fixed , we can consider estimating the parameters by minimizing a least-squares objective under suitable (sparsity) constraints on imposed by the sparsity structure on . As runs from , we have -many least squares problems subject to (structured) sparsity constraints on . This motivates us to consider the following optimization problem which minimizes the sum of square of the residual errors, across all regression problems:

| (7a) | ||||

| s.t. | (7b) | |||

| (7c) | ||||

| (7d) | ||||

where above, the decision variables are . The binary variable controls the sparsity pattern of . The complementarity constraint (7c) states that only if ; and otherwise. The constraint (7d) ensures that has at most -many nonzeros (under the assumption that has at most nonzeros). Problem (7) is a mixed integer quadratic optimization problem with complementary constraints. We present different integer programming formulations for (7) in Section 4.

Remark 1.

It follows from (6) that the off-diagonal entries of are the entries of an asymmetric matrix with rank one. Due to computational reasons, we drop the rank constraint from Problem (7). Hence formulation (7) can be interpreted as a relaxation of formulation (3) under the covariance model (1). As we will see in our statistical error bounds, estimator (7) leads a sub-optimal error bound compared to estimator (3). However, Problem (7) is friendlier from a computational viewpoint, and via our tailored algorithms, we are able to compute optimal solutions to (7) for instances with . Recall, that in contrast, current MIP-based approaches for SPCA can deliver dual bounds for (3) for .

Our estimator (7), can be interpreted as estimating the inverse of the covariance matrix under a structured sparsity pattern (imposed by ) as determined by the the spiked covariance model (1) (see Lemma 2). To our knowledge, estimator (7) with the structured sparsity constraint has not been studied earlier in the context of the SPCA problem. A common procedure to estimate a sparse precision matrix is the nodewise sparse regression framework of Meinshausen and Bühlmann (2006), where the regression problems are solved independently across the nodes under a plain sparsity assumption on the entries of the precision matrix. (Note that we consider a structured sparsity pattern that is shared across the matrix, which may not be generally achievable via a nodewise regression approach). The framework in Bresler et al. (2018) for the SPCA problem is similar to Meinshausen and Bühlmann (2006) in that they also compute different regression problems independently of one another. Compared to Bresler et al. (2018), our joint estimation framework generally leads to improved statistical error bounds (for estimating )—see Section 3, and also better numerical performance (see Section 5).

3 Statistical Properties

In this section we explore statistical properties of our estimator. We assume throughout that data is generated as per the spiked covariance model (1) with .

Our first result shows that a solution of Problem (7) is close to the corresponding population coefficients in the squared norm. Our result allows for model misspecification—we do not assume that has exactly -many nonzero entries, and the approximation error appears in the error bound. Before stating our result, we introduce some notation. Let denote the indices of the largest coordinates of in absolute value. Given (which may have more than nonzeros), we define to be a vector that contains the largest (in absolute value) coordinates in with the other coordinates set to zero. That is, for each , we define where, is the indicator function. Correspondingly, we define as follows:

| (8) |

In other words, is a sparsification of restricted to the nonzero entries of . Therefore, the term indicates the error in approximating by —an error that stems from approximating by a -sparse vector , when may not be -sparse. In particular, if , then . Theorem 1 presents an error bound of the estimator arising from Problem (7).

Theorem 1.

In the special case when , the second term in the rhs of (9) is zero, and Theorem 1 shows that Problem (7) delivers an estimate of with an error bound of . In what follows, we show how to estimate i.e., the PC of interest, from the estimated regression coefficients .

Let us define a matrix such that

for all . From Lemma 2, it can be seen that

| (10) |

where is a diagonal matrix such that its -th diagonal entry is given by

Observe that is a rank one matrix with nonzero singular value and left singular vector . Since

the nonzero singular value of is

| (11) |

To estimate , we first obtain an estimate of and consider its leading left singular vector. We show below that if we obtain a good estimate of , then its left singular vector will be close to . Let be our estimate of . A solution obtained from Problem (7) can be used to estimate the off-diagonal coordinates of , that is, for . To estimate the diagonal entries of , since , we need an estimate of for each —let us denote this estimate by for all . Note that from the spiked covariance model assumption (see Lemma 2), when — therefore, we use as an estimate for the indices , where . For the other coordinates, we compute based on the residual variance of the -th regression problem:

| (12) |

To summarize, our estimator is given by:

| (13) |

Theorem 2 presents an error bound in estimating by .

Theorem 2.

Let be as defined in Theorem 1 and be defined in (10). Suppose the assumptions of Theorem 1 hold true. Moreover, assume:

-

(A1)

For , there is a numerical constant such that . We denote this lower bound by that is, .

-

(A2)

The error in approximating by is bounded above as:

(14) and the true variances (see Lemma 2) satisfy

(15) where, recall is the support of .

-

(A3)

We have .

Let be as defined in Theorem 1 and as defined in (13). Then with high probability444See (73) for the exact probability expression. we have (i) The supports of and are the same, that is ; and (ii)

In light of Theorem 2, is close to . Furthermore, as is the leading left singular vector of , the leading singular vector of should be close to (assuming of course, a separation between the first and second leading singular values of )—see for example, Stewart and Sun (1990, Chapter V) and Wedin (1972) for basic results on the perturbation theory of eigenvectors. This leads to the following result.

Corollary 1.

3.1 Support recovery in the well-specified case

In this section, we show that (under some assumptions) Problem (7) recovers the support of correctly when . In other words, the nonzero coordinates of and are the same, where is an optimal solution to Problem (7).

Theorem 3.

A complete proof of Theorem 3 can be found in the appendix. We present an outline of our key proof strategy. For and , let us define:

With this definition in place, Problem (7) can be equivalently written as

| (18) |

To analyze Problem (18), for every , we compare the value of for a feasible to an oracle candidate where has the same support as . Then, we show that

unless , which completes the proof.

Remark 2.

In the context of support recovery in SPCA, a standard assumption appearing in the literature is: for every nonzero coordinate , we assume a lower bound (see for example, (Bresler et al., 2018)). In light of identity (6), for , this lower bound condition leads to:

which implies, Therefore, for condition (17) in Theorem 3 to hold true, it suffices to take and .

3.2 Discussion of related prior work

Following our earlier discussion, the covariance thresholding algorithm of Deshpande and Montanari (2016) leads to an estimate of with a bound on the error scaling as , which is the same as our proposal (up to logarithmic factors). Our approach is different from the covariance thresholding algorithm. We operate on the precision matrix by jointly optimizing over -many node-wise linear regression problems under a structrured sparsity assumption, while covariance thresholding operates directly on the covariance matrix. In particular, our algorithm leads to an estimate with nonzero entries appearing in a sub-matrix, which may not be available via the covariance thresholding estimator. Moreover, as a by-product of our estimation procedure criterion (7), we are able to recover (with high probability) the correct support of the PC i.e., —the covariance thresholding algorithm on the other hand, needs a data-splitting method to recover the support of . In our numerical experiments, our method appears to have a notable advantage over the covariance thresholding algorithm in terms of estimation and support recovery performance.

Our approach is related to the proposal of Bresler et al. (2018) who use connections between sparse linear regression and SPCA to propose a polynomial time algorithm for SPCA. Their algorithm requires solving separate sparse linear regression problems, each problem performs a sparse regression with the -th column of as response and the remaining columns as predictors. Each sparse regression problem has an estimation error of resulting in an overall error rate of . Based on these separate regression problems, Bresler et al. propose testing methods to identify the support of with error scaling as . The procedure of Bresler et al. (2018) requires choosing tuning parameters for each Lasso problem, which can be challenging in practice. Our approach differs in that we consider these -different regression problems jointly under a structured sparsity assumption and we require knowing the support size . We are able to estimate the matrix of regression coefficients with an estimation error scaling as (see Theorem 1), which is an improvement over Bresler et al. (2018) by a factor of . Another point of difference is that the approach of Bresler et al. (2018) requires solving separate sparse linear regression problems which can be computationally expensive when is large, while our approach requires solving one problem which we are able to scale to quite large instances by exploiting problem-structure. Our numerical experiments show that our estimator leads to superior statistical performance compared to Bresler et al. (2018).

Gataric et al. (2020) present an interesting polynomial-time algorithm for SPCA based on random projections. They show that their algorithm can achieve the minimax optimal rate in terms of estimation of the PC under certain incoherence assumptions when is sufficiently large. Their algorithm may require random projections.

To our knowledge, the oracle bounds presented under sparsity misspecification (see Theorems 1 and 2) are new. On a related note, Johnstone and Lu (2009); Cai and Zhou (2012) consider the SPCA problem when belongs to a weak ball. In another line of work, authors in Lei and Vu (2015) consider a misspecified model for SPCA where the covariance matrix might not necessarily follow a spiked model—their results are true under the so-called limited correlation condition, which differs from what we consider here.

3.3 Statistical properties of approximate solutions

As discussed earlier, an appealing aspect of a MIP-based global optimization framework, is its ability to deliver both upper and lower bounds (or dual bounds) as the algorithm progresses. These upper and dual bounds, taken together, provide a certificate of how close the current objective value is to the optimal solution, and can be useful when one wishes to terminate the algorithm early due to computational budget constraints. Below we show that the estimation error of an approximate solution is comparable to an optimal solution to (7) as long as the objective value is sufficiently close to the optimal objective. For the following result, for simplicity, we consider the well-specified case where has -nonzeros.

Proposition 1.

Suppose . Moreover, assume . If is the matrix of true regression coefficients as in Lemma 2 and is a feasible (though not necessarily an optimal) solution to Problem (7) such that

| (19) |

holds true for some . Then, if , we have

| (20) |

with high probability666An explicit expression for the probability can be found int (100).

4 Optimization Algorithms

Problem (7) is a mixed integer optimization problem with binary variables and continuous variables. When is large (e.g., of the order of a few hundred), this poses challenges for commercial solvers such as Gurobi and Mosek. Here, we propose a specialized algorithm for (7) that can scale to much larger instances compared to off-the-shelf commercial solvers. The key idea of our approach is to reformulate (7) into minimizing a convex function involving binary variables with additional cardinality constraints:

| (21) |

where, as we show subsequently, is convex. Note that Problem (21) is an optimization problem with binary variables, unlike (7) involving continuous and binary variables. To optimize (21), we employ an outer approximation algorithm (Duran and Grossmann, 1986) as we discuss below. The following section shows how to reformulate Problem (7) into form (21).

4.1 Reformulations of Problem (7)

Here we discuss different reformulations of Problem (7)—we will make use of the underlying statistical model, that will subsequently lead to important computational savings compared to approaches that do not make use of it.

Valid inequalities under model (1): In this section, we discuss some implied (aka valid) inequalities that originate from the spiked covariance model in (1)—these inequalities are constraints that are implied by the model (1) and when added to formulation (7), the resulting solution will have the same statistical properties as that of an estimator from (7). These implied inequalities (aka constraints) will allow us to obtain a structured reformulation of Problem (7) which leads to better computational properties.

Note that the complementarity constraint (7c) in formulation (7), can be linearized by using BigM constraints

| (22) |

where above, is a BigM parameter that controls the magnitude of , an optimal solution to (7) i.e., we need to be sufficiently large such that . A large (conservative) choice of the BigM parameter , would not affect the logical constraint (7c), but will affect the runtime of our mixed integer optimization algorithm (Bertsimas et al., 2016). In other words, a tight estimate of is desirable from an algorithmic standpoint. While there are several ways to obtain a good estimate of , here we make use of the statistical model (1) to obtain an estimate of . In particular, we show that it suffices to consider . To this end, note that (6) implies

| (23) |

so the absolute value of is less than . As a result, a choice of in (22) implies that is feasible for Problem (7) where, constraint (7c) is replaced by (22).

Additionally, we show that under model (1), the squared -norm of every column of can be bounded from above. From (6), for every column , we have:

| (24) |

where has the same support as . Therefore, the inequality constraint for some sufficiently large is a valid inequality for Problem (7) under model (1)—i.e., adding this inequality does not change the statistical properties of an optimal solution to the problem. In particular, owing to the sparsity structure in , this implies that . Based on these two observations, we reformulate Problem (7) as

| (25) | ||||

| s.t. |

where is a regularization parameter which controls the norm of the off-diaogonal entries of . The additional penalty in Problem (25) can be interpreted as adding ridge regularization to our original formulation in (7)—a nonzero value of in (25) leads to computational benefits, as we discuss below. Note that by setting we recover the original Problem (7).

Remark 3.

Perspective Formulation: Formulation (25) involves bounded continuous variables and binary variables—the binary variables activate the sparsity pattern of the continuous variables. In MIP problems with a similar structure (i.e., where bounded continuous variables are set to zero by binary variables), the perspective reformulation is often used to obtain stronger MIP formulations (Frangioni and Gentile, 2006; Aktürk et al., 2009; Günlük and Linderoth, 2010). In other words, these MIP formulations lead to tight continuous relaxations, which in turn can lead to improved runtimes in the overall branch-and-bound method. Here we apply a perspective relaxation on the squared -term , appearing in the objective in (25). This leads to the following MIP formulation:

| (26) | ||||

| s.t. | ||||

where above we have introduced auxiliary nonnegative continuous variables and added rotated second order cone constraints for all . When then ; when then, at an optimal solution, . Note that (26) is an equivalent reformulation777That is, the optimal objectives of both these problems are the same, and an optimal solution to (26) leads to an optimal solution to (25) and vice-versa. of Problem (25). However, when , the interval relaxation of formulation (26) (obtained by relaxing all binary variables to the unit interval), results in a tighter relaxation compared to the interval relaxation of (25) (Hazimeh et al., 2020). Our proposed custom algorithm solves Problem (26) to optimality, and can handle both cases and .

A convex integer programming formulation for (26): When , Problem (26) is a MISOCP888In the special case of , this can be expressed as a mixed integer quadratic program. Commercial solvers like Gurobi, Mosek can reliably solve MISOCPs for small-moderate scale problems. However, formulation (26) involves -many continuous variables and -many binary variables — posing computational challenges for modern MIP solvers. Therefore, we propose a tailored algorithm to solve Problem (26). To this end, we first reformulate Problem (26) into a convex integer program i.e., in the form (21). To lighten notation, let be the matrix with the column replaced with zero. For , let us define the following function:

| (27) | ||||

| s.t. | ||||

obtained by minimizing (26) partially wrt all continuous variables, with a fixed . In light of formulation (27), we see that Problem (26) is equivalent to (21) where is replaced with .

Proposition 2 shows that is convex and characterizes its subgradient. Before presenting the proposition, we introduce some notation. For , define

| (28) |

when ; and when . Let be a matrix, with its -th column given by:

| (29) |

Define matrices as follows

| (30) | ||||

Proposition 2.

Note that in (27) is implicitly defined via the solution of a quadratic program (QP). For a vector which is dense, calculating in (27) requires solving -many QPs each with variables. However, for a feasible which is -sparse, calculating requires solving -many QPs each with variables, which is substantially faster—furthermore, these QPs are independent of each other and can hence be solved in parallel. Similar to the case of evaluating the objective , we do not have a closed form expression for a subgradient of (cf Proposition 2), but this can be computed for as a by-product of solving the QP in (27).

4.2 Outer Approximation Algorithm

We present an outer approximation (or cutting plane) algorithm (Duran and Grossmann, 1986) to solve Problem (21). Our algorithm requires access to an oracle that can compute the tuple where, is a subgradient of at an integral . We refer the reader to Proposition 2 for computation of when . As is convex, we have for all . Therefore, if are feasible for (21), we have:

| (31) | ||||

where, is a lower bound to the map on . At iteration , the outer approximation algorithm finds , a minimizer of under the constraints of Problem (21). This is equivalent to the mixed integer linear program:

| (32) | ||||

| s.t. | ||||

As the feasible set of Problem (21) contains finitely many elements, an optimal solution is found after finitely many iterations999This is true as the lower bound obtained by the outer approximation in each iteration removes the current solution form the feasible set, unless it is optimal—see Duran and Grossmann (1986) for details., say, . In addition, is a lower bound of the optimal objective value in (21); and leads to an upper bound for Problem (21). Consequently, the optimality gap of the outer approximation algorithm can be calculated as where LB is the current (and the best) lower bound achieved by the piecewise approximation in (32), and UB is the best upper bound thus far. The procedure is summarized in Algorithm 1.

Remark 4.

Outer approximation based methods are commonly used to solve nonlinear integer programs, and have been used recently in the context of -sparse regression problems (Bertsimas and Van Parys, 2020; Behdin and Mazumder, 2021). Our approach differs in that we consider structured sparsity, and use a perspective formulation which is motivated by the underlying spiked covariance model resulting in a MISOCP (26). In particular, Bertsimas and Van Parys (2020) consider an outer approximation method for a ridge regularized sparse regression problem where the tuple can be computed in closed form, which is in contrast to our setting where is available implicitly (cf Proposition 2). Bertsimas et al. (2020) consider an outer approximation approach for sparse PCA, but they consider a mixed integer semidefinite optimization problem, which is computationally more demanding than what we propose here.

4.2.1 Initializing Algorithm 1

While Algorithm 1 leads to an optimal solution to (21) (irrespective of the initialization used), we have empirically observed that a good initial solution can decrease the number of the iterations and the overall runtime of the algorithm. We describe an initialization scheme that we found to be useful in our work. We first obtain a screened set , with size a constant multiple of , with the hope that this contains many of the true nonzero coefficients. In our experiments, we use the diagonal thresholding algorithm (Johnstone and Lu, 2009) with a larger number of nonzeros to obtain the candidate set with . We then consider a restricted version of Problem (25) with for all to obtain an estimate for . This reduced problem contains -binary variables, which is considerably easier to solve compared to the original formulation with -binary variables. In our experiments, this usually leads to a good initialization for Problem (21).

5 Numerical Experiments

We demonstrate the performance of our approach via numerical experiments on synthetic and real datasets and present comparisons with several state-of-the-art SPCA algorithms. We have implemented all algorithms in Julia and use Gurobi v9.1.1 to solve the mixed integer linear sub-problems. We refer to our framework as SPCA-SLS (where SLS stands for Structured Least Squares). An implementation of our framework SPCA-SLS in Julia is available at:

5.1 Synthetic Data

In this section, we use synthetic data and consider different scenarios and values for parameters in the model. In all experiments, we set the SNR value to which is a lower SNR level compared to experiments in Deshpande and Montanari (2016); Bresler et al. (2018)—this makes the problems statistically harder.

Experimental Setup. For a fixed set of values of , each coordinate of the PC, , is drawn independently from . Next, randomly chosen coordinates of are set to zero and is normalized as to have unit -norm. We draw samples from the multivariate normal distribution with mean zero and covariance .

Competing Methods. We present comparisons with the following algorithms for SPCA, as discussed in Section 1.1:

-

•

The Truncated Power Method (shown as TrunPow)(Yuan and Zhang, 2013)—this is a heuristic method

-

•

The Covariance Thresholding (shown as CovThresh)(Deshpande and Montanari, 2016)—this is a polynomial-time method with good theoretical guarantees

-

•

The method by Bresler et al. (2018) (shown as SPCAvSLR)—we use a Lasso for every node, leading to a polynomial-time algorithm.

All the above methods can handle problems with . We do not consider other MIP-based methods and the SDP-based relaxations (See Section 1.1) in our experiments, as they are unable to handle the problem sizes we consider here.

Parameter Selection. For our proposed algorithm (i.e., SPCA-SLS, which considers (26)), and the truncated power method, we assume that the sparsity level is known. The parameter in (26) is set to zero unless stated otherwise. Following the discussion of Yuan and Zhang (2013) on initialization, we initialize TrunPow by with randomly chosen in where is the vector with all coordinates equal to zero except coordinate equal to one. For CovThresh, we choose the threshold level based on the theoretical results of Deshpande and Montanari (2016) as for some101010In our experiments, we choose a value of that leads to the best estimation performance. . For SPCAvSLR, we use Lasso for each nodewise regression problem and use a tuning parameter as per the recommendation of Bresler et al. (2018).

Results. We consider different scenarios for our numerical experiments. First, we compare our newly proposed custom algorithm to a commercial solver in Section 5.1.1. Next, we fix and and investigate the effect of changing on the statistical and computational performance of different methods in Section 5.1.2. Then, we fix and vary in Section 5.1.3. Finally, we run our algorithm on a large dataset with in Section 5.1.4. To compare the quality of estimation for each algorithm, we report in our figures, where is the recovered PC and is the true PC. To compare the quality of the support recovery, we report false positives and false negatives as where is the correct support and is the estimated support. We perform the experiments on 10 replications, and summarize the results.

5.1.1 Optimization performance: Comparison with MIP solvers

Before investigating the statistical performance of our proposed approach, we show how our proposed algorithm can solve large-scale instances of Problem (26).

We use our custom algorithm to solve Problem (26) with — we call this SPCA-SLS. We also consider (26) with a small value of , taken to be where is the initial solution—we call this SPCA-SLSR. We compare our approaches with Gurobi’s MIP solver which is set to solve (26) with . We run experiments for different values of . In Table 1, we report the average optimality gap achieved after at most 5 minutes, for SPCA-SLS, SPCA-SLSR and Gurobi’s MIP-solver. We observe that Gurobi quickly struggles to solve (26) when — our custom approach on the other hand, can obtain near-optimal solutions to (26) for up to . For reference, recall that problem (26) involves -many continuous variables — therefore, our approaches SPCA-SLS, SPCA-SLSR are solving quite large MIP problems to near-optimality within a modest computation time limit of minutes. We also see that SPCA-SLSR provides better optimality gaps—we believe this due to the use of the perspective formulation, which leads to tighter relaxations.

| SPCA-SLS | SPCA-SLSR | Gurobi | SPCA-SLS | SPCA-SLSR | Gurobi | |

|---|---|---|---|---|---|---|

| - | - | |||||

| - | - | |||||

| - | - | |||||

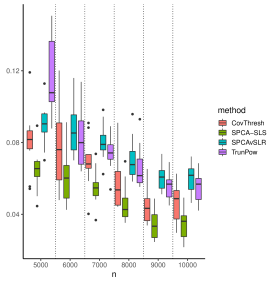

5.1.2 Estimation with varying sample sizes ()

In this scenario, we fix and let and . We compare our algorithm with the competing methods outlined above. Our experiments in this scenario are done on a machine equipped with two Intel Xeon Gold 5120 CPU 2.20GHz, running CentOS version 7 and using 20GB of RAM. The runtime of our method is limited to 2 minutes111111For the examples in Figure 1, our custom algorithm provides optimality gaps less than and for and , respectively (after 2 minutes). As a point of comparison, off-the-shelf MIP-solvers are unable to solve these problem instances (cf Table 1)..

The results for these examples are shown in Figure 1: we compare the estimation (top panels) and support recovery (bottom panels) performance of different algorithms. In terms of estimation, increasing results in a lower estimation error as anticipated by our theoretical analysis in Section 3. In addition, our method SPCA-SLS appears to work better than competing algorithms and leads to lower estimation error. SPCA-SLS also appears to provide the best support recovery performance in these cases. The method CovThresh does not lead to a sparse solution and therefore has a high false positive rate, but may still lead to good estimation performance. On the other hand, SPCAvSLR has a higher false negative rate compared to CovThresh which leads to worse estimation performance.

|

|

|

|

|---|---|---|

|

|

|

|

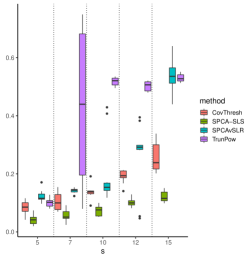

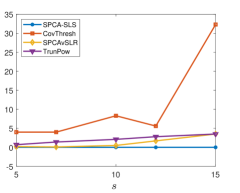

5.1.3 Estimation with varying sparsity levels ()

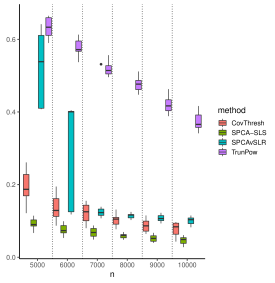

In this scenario, we fix and and consider different sparsity levels . We compare our SPCA-SLS algorithm with competing methods outlined above. We use the same computational setup as in Section 5.1.2.

The results for this scenario (estimation and support recovery properties) are shown in Figure 2. As it can be seen, increasing results in worse statistical performance. However, our proposed approach continues to work better than other estimators in terms of estimation and support recovery121212In all these cases, our algorithm delivers a near-optimal solution. The MIP-optimality gaps are and for values of , respectively. The runtime of our method is limited to 2 minutes..

| Estimation Error, | Support Recovery, | ||

|---|---|---|---|

|

|

|

|

|

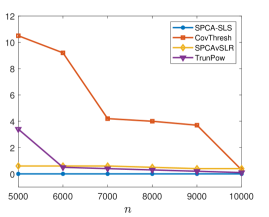

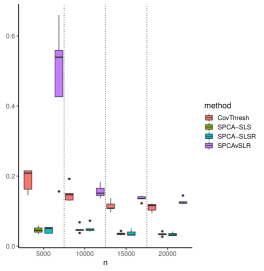

5.1.4 A large-scale example with

To show the scalability of our algorithm, we consider instances with . We perform a set of experiments on a personal computer. We use a machine equipped with AMD Ryzen 9 5900X CPU 3.70GHz, using 32GB of RAM. However, in our experiments, Julia did not use more than 12GB of RAM. We set and . The runtime of our methods is limited to 5 minutes.

In this case, we explore Algorithm 1 applied to two cases of Problem (26): (a) we consider the unregularized case denoted by SPCA-SLS and (b) chosen as in Section 5.1.1, denoted by SPCA-SLSR. We use (b) to demonstrate the effect of the perspective regularization in (26). The results for this case are shown in Figure 3, which compares the estimation performance of different algorithms. As it can be seen, our method leads to better estimation performance compared to other SPCA methods. Moreover, having (in case of SPCA-SLSR) does not negatively affect the estimation performance of our method, while it helps to achieve stronger optimality certificates131313For , SPCA-SLS and SPCA-SLSR provide optimality gaps under and , respectively. For , SPCA-SLS and SPCA-SLSR provide optimality gaps under and , respectively..

|

|

|

|

|---|

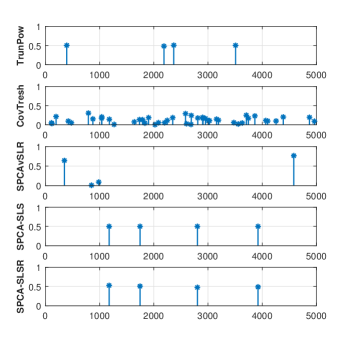

5.2 Real dataset example

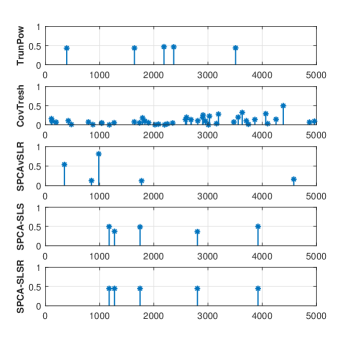

To show the scalability of our algorithm and to compare them with other well-known algorithms, we do further numerical experiments on the Gisette dataset (Guyon et al., 2005). This dataset is a handwritten digit recognition dataset with samples and features. We run SPCA-SLS, SPCA-SLSR (with chosen as in Section 5.1.1), TrunPow, SPCAvSLR and CovTresh for this data matrix and two values of . Parameter selection is done similar to the synthetic data experiments in Section 5.1. We use the same personal computer from Section 5.1.4 with Julia process limited to 6GB of RAM usage. To compare the results of different methods, we plot the absolute values of estimated PCs and examine the sparsity pattern of the associated eigenvector. Figure 4 shows the results for two values of — interestingly, we observe that the sparsity patterns available from different algorithms are different, with CovTresh leading to a denser support.

|

|

6 Conclusion

In this paper, we consider a discrete optimization-based approach for the SPCA problem under the spiked covariance model. We present a novel estimator given by the solution to a mixed integer second order conic optimization formulation. Different from prior work on MIP-based approaches for the SPCA problem, our formulation is based on the properties of the statistical model, which leads to notable improvements in computational performance. We analyze the statistical properties of our estimator: both estimation and variable selection properties. We present custom cutting plane algorithms for our optimization formulation that can obtain (near) optimal solutions for large problem instances with features. Our custom algorithms offer significant improvements in terms of runtime, scalability over off-the-shelf commercial MIP-solvers, and recently proposed MIP-based approaches for the SPCA problem. In addition, our numerical experiments appear to suggest that our method outperforms some well-known polynomial-time and heuristic algorithms for SPCA in terms of estimation error and support recovery.

Acknowledgments

This research was partially supported by grants from the Office of Naval Research (ONR-N000141812298) and the National Science Foundation (NSF-IIS-1718258).

Proofs and Technical Details

Appendix A Proofs of Main Results

Before proceeding with the proof of main results, we present an extended version of Lemma 1 that we use throughout the proofs.

Lemma 3.

Let be such that for ,

Then, and are independent for every . Moreover, for every ,

A.1 Proof of Theorem 1

To prove this theorem, we first mention a few basic results that we use throughout the proof.

Lemma 4 (Theorem 1.19, Rigollet and Hütter (2015)).

Let be a random vector with , then

| (33) |

where denotes the unit Euclidean ball of dimension .

Lemma 5.

Suppose (with ) be a data matrix with independent rows, with the -th row distributed as (with positive definite ) where . The following holds:

with probability at least for some universal constants .

Proof.

Let be the eigendecomposition of with diagonal containing the eigenvalues of . Let . For any such that , we have:

showing that . Therefore, by Theorem 4.6.1 of Vershynin (2018), the following holds

| (34) |

with probability at least for some universal constants . Moreover,

Combining the above with (34), we arrive at the first inequality in this lemma. The proof for the third inequality follows by an argument similar to the above, but for . ∎

Lemma 6.

Suppose the rows of the matrix are iid draws from a multivariate Gaussian distribution . Moreover, suppose for any such that ,

Then, if , with probability at least , we have:

(We recall that is a sub-matrix of restricted to the columns indexed by ).

Proof.

Suppose is fixed. Take for some constant . By Lemma 5, with probability greater than

We consider a union bound over all possible sets (of size at most ):

where is due to the inequality .

Therefore, with probability greater than , we have

Finally, the result follows by choosing large enough to have and such that

∎

Lemma 7.

For fixed , and , we have

| (35) |

for some universal constants (We recall that is the spiked covariance matrix from (1)).

Proof.

The proof of Theorem 1 is based on the following technical lemma.

Lemma 8.

Proof.

Let be the true regression coefficients.

By taking to represent the support of and noting that for , we can see that the matrix is feasible for Problem (7).

Using the optimality of and feasibility of for Problem (7), we have:

| (37) |

where we used the representation by Lemma 3. By the inequality ,

| (40) |

For convenience, let us introduce the following notation:

| (41) | ||||

| (42) |

Note that . In the rest of the proof, denotes the probability w.r.t. the data matrix (which includes ). Note that can be nonzero only if (as can be nonzero for and , respectively) so for . As a result, one has

| (43) |

where the inequality (43) takes into account the definition of in (41) and the observation that

Let be the matrix with column removed. Let be an orthonormal basis for the linear space spanned by , for . For a fixed set and , and ,

| (44) |

where is due to the independence of and from Lemma 3, is due to the fact that is in the column span of , is due to Lemma 4 and the conditional distribution , and is due to and . Therefore, by taking

with in (44), we get

| (45) |

where in the second inequality in (45) we used the assumption . Therefore, by taking and

| (46) |

we have

| (47) |

where is due to (43), are true because of union bound, follows by noting that: for , if

then

Inequality above, is due to (45) and the fact that , is due to the inequality and is true as . By (40) and (47), and substituting from (46),

with the probability greater than . ∎

Proof of Theorem 1.

Let be the matrix with column removed. Let us define the following events:

| (48) | ||||

for some constant . From (35) for fixed , with probability at least , we have:

| (49) |

Let and . Noting that for all , and by a union bound over all , the following holds true

| (50) |

Note that for any , with ,

Hence, by Lemma 6, as ,

For the rest of the proof, we assume (for all ) and the event of Lemma 8 hold true. Note that the intersection of these events holds true with probability at least

| (51) |

by union bound.

Let . Recall that for all . We have the following:

| (52) |

Next, note that

| (53) |

for some sufficiently large constant (that we discuss later), where is due to the inequality , is due to event defined in (48) and is true as we assumed . As a result, from (52) and (53),

| (54) |

On event for ,

| (55) |

where in the first inequality, we used the convention . As a result, for

| (56) |

where is due to (54), is due to (55) and (50), is by taking , is true because and is true as for . Therefore,

| (57) |

where is true as for and is true because of (56). In addition,

| (58) |

where above, we used event to arrive at the second inequality. Starting with (57), we arrive at the following:

where above, is due to Lemma 8, is true because of (58) and is true as by the assumption of the theorem. ∎

A.2 Proof of Theorem 2

We first present a few lemmas that are needed in the proof of Theorem 2.

Lemma 9 (Lemma 8, Raskutti et al. (2011)).

Let . Suppose , and is such that . We have

with probability greater that .

Lemma 10.

Proof.

Let us define the following events:

| (60) | ||||

where is defined in (41) for . As has iid normal coordinates with bounded variance, similar to (50), by Bernstein inequality

Moreover, based on Lemma 9, we have:

| (61) |

for all . In the rest of the proof, we assume (for all ) and the event of Theorem 1 hold true. By union bound, this happens with probability greater than

One has for a fixed ,

| (62) |

where follows as we are considering the event . Additionally, noting that for we have:

| (63) |

where is true as , is due to Lemma 8 and is true because of (58).

Lemma 11.

Proof.

Define the event

Note that and by Bernstein inequality,

| (66) |

for some numerical constant as . Note that from Lemma 10,

| (67) |

and from Theorem 1,

| (68) |

The rest of the proof is on the intersection of events for all and events in (67) and (68), with probability of at least

To lighten the notation, let . By (12), one has

| (69) |

where uses the representation and is a result of the inequality . Note that

| (70) |

where is due to Lemma 8, is due to (58) and is due to (14). Additionally,

| (71) |

by Lemma 10. Moreover, from (6), so . By substituting (70), (71) into (69), and considering that event hold true, we have

where the second inequality is by the fact and the last inequality follows by observing that as . ∎

Proof of Theorem 2.

Part i) We prove this part by contradiction. Suppose there exists such that . In this case, while for , . Therefore by assumption (A1):

| (72) |

with probability greater than

where is true because of the condition in the theorem and the fact , is true because for , and , is due to Theorem 1 and is because of (14). Note that if is chosen large enough, (72) leads to a contradiction—this shows and as , we arrive at .

A.3 Proof of Theorem 3

We first introduce some notation that we will be using in this proof.

Notation. In this proof, we use the following notation. For any , we let be the submatrix of with columns indexed by . For and , we let be the submatrix of with rows in and columns in . We define the operator and max norm of as

respectively. We denote the projection matrix onto the column span of by . Note that if has linearly independent columns, . In our case, as the data is drawn from a normal distribution with a full-rank covariance matrix, for any with , has linearly independent columns with probability one. The solution to the least squares problem with the support restricted to ,

| (74) |

for and is given by

Consequently, we denote the optimal objective in (74) by

| (75) |

We let be the sample covariance. Throughout this proof, we use the notation for and otherwise. Finally, for , positive definite and , we let

| (76) |

Note that is the Schur complement of the matrix

| (77) |

Let us define the following events for and :

| (78) | ||||

where are some given universal constants and . In the following lemmas, we prove that the above events hold true with high probability.

Lemma 12.

Proof.

Let the event be defined as (recall, ):

By Lemma 7 and union bound, as , . For the rest of the proof, we assume holds true. As a result, for any with ,

| (81) |

for some constant and . For that is sufficiently large, we have . Hence, by Weyl’s inequality,

As a result,

where is achieved by substituting in Theorem 3 and noting . This proves the inequality in display (79).

Similar to (81), for any and with ,

| (82) |

One has

where is by Corollary 2.3 of Zhang (2006) and is due to Weyl’s inequality. Finally,

This completes the proof of (80). ∎

Lemma 13.

Let us define the event

Then, .

Proof.

First, fix and such that . Let and . Moreover, let

Note that is in the column span of and the matrix has rank at most as has columns. In addition, by Lemma 3, and are independent. By following an argument similar to (44) (considering an orthonormal basis for the column span of ), for , we have:

| (83) |

Let

for . As a result, by (83),

Next, note that by the definition of ,

where the second equality follows from the definition of and the third equality follows from the definition of . This completes the proof for a fixed . Finally, we use union bound over all possible choices of , and . As a result, is bounded from above as

∎

Lemma 14.

Let

Then,

Proof.

First, fix such that . Note that , and as is a projection matrix. In addition, and are independent by Lemma 3 as . Therefore,

| (84) |

By Hanson-Wright inequality (see Theorem 1.1 of Rudelson and Vershynin (2013) and the calculations leading to (6.7) of Fan et al. (2020)), for , the following

| (85) |

holds with probability greater than for some . Note that by (84), the event in (85) implies

Take for that is sufficiently large. As by Lemma 2, this leads to

with probability greater than , which completes the proof for a fixed . Similar to Lemma 13, we use union bound to achieve the desired result. ∎

Lemma 15.

Let

Then,

Proof.

The proof is similar to the proof of (6.7) in Fan et al. (2020). However, we recall that the work of Fan et al. (2020) considers a fixed design , while here, we deal with random design.

First, fix and such that and . Let be the column span of . Moreover, let be orthogonal complement of as subspaces of column spans of and , respectively. Let be projection matrices onto , respectively. With this notation in place, one has

Note that . In addition, by Lemma 3, and are independent. As a result,

Therefore, by Hanson-Wright inequality, for , we have:

Take for that is sufficiently large so we have

Then, similar to Lemma 13, we use union bound to complete the proof. ∎

Lemma 16.

Let us define the event

One has

| (86) |

Proof.

Proof of Theorem 3.

In this proof, we assume events given in (78) (for all , as shown in Lemmas 12–16, above) hold true. Note that by Lemmas 12, 13, 14, 15 and 16, this happens with probability greater than

| (88) |

Suppose with . Let

Recalling the definition of from (75), we have the following (see calculations in (6.1) of Fan et al. (2020)):

| (89) |

and

| (90) |

For and , let us define:

| (91) |

Note that in (91), if , then and . On the other hand, if , we have as for . With this definition in place, Problem (7) can be equivalently written as

| (92) |

To analyze Problem (92), for every , we compare the value of for a feasible to a “oracle” candidate where has the same support as . Then, we show that

unless , which completes the proof. We let and be a feasible support for Problem (92). We also recall that , and . We consider three cases.

Case 1 (): In this case, we have and . As a result, we have

| (93) |

where is true because and by (89) and is due to the event in (78).

Case 2 (): In this case, we have and . As a result, we have the following:

| (94) |

where is due to (90), is due to the inequality , is due to event ,

is because of event and is due to event .

Case 3 (): In this case, and . As a result, we have

| (95) |

where is due to (89), (90), is true because of events and , is due to event , is due to event and by taking , and is true by taking large enough so

Considering the sum of all terms appearing in (93), (94) and (95), the difference between optimal cost of is at least

| (96) |

when , because there are instances in cases 1 and 2 above. This shows cannot be optimal unless . ∎

A.4 Proof of Proposition 1

Proof.

In this proof, we use the following results. From (55),

| (97) |

with probability greater than as . From (47),

| (98) |

with probability greater than Moreover, from (66),

| (99) |

with probability greater than as . Therefore, the intersection of events appearing in (97), (98) and (99) holds true with probability at least

| (100) |

By the assumptions of the proposition,

| (101) |

where is by the representation by Lemma 3, is by the definition of in Lemma 3. Next, note that for ,

| (102) |

where the above inequality follows from the observation . As a result, from (101) and (102), we arrive at

| (103) |

From (103), (97), (98) and (99), we have:

with probability at least as large as the quantity appearing in (100). This completes the proof. ∎

A.5 Proof of Proposition 2

Proof.

Part 1) The map appearing in the cost function of (27), that is:

| (104) |

is jointly convex in . Let the (3-dimensional) rotated second order cone be denoted by

Note that is convex. Using the above notation, Problem (27) can be written as

| (105) | ||||

| s.t. | ||||

Let

Note that as is a convex set, defined above is also convex. Let denote the characteristic function of a set ,

Note that if is a convex set, is a convex function. With this notation in place, Problem (105) can be written as

| (106) |

where is defined in (104). Based on our discussion above, the function is convex. As is obtained after a marginal minimization of a jointly convex function over a convex set, the map is convex on (Boyd and Vandenberghe, 2004, Chapter 3).

Part 2) We prove this part for . The proof for is similar.

Note that as the objective function of (105) is convex [see Part 1] and its feasible set contains a strictly feasible element, strong duality holds for (105) by Slater’s condition (see Boyd and Vandenberghe (2004), Section 5.2.3). We start by obtaining the dual of (105) for a fixed . Considering Lagrange multipliers , , , and for problem constraints, the Lagrangian for this problem or (for short), can be written as

| (107) | ||||

where is a vector of all ones. By setting the gradient of the Lagrangian w.r.t. , and equal to zero, we get

| (108) | ||||

By rearranging some terms above, we get

| (109) | ||||

Additionally, note that as , we have . By substituting (109) into (107), we can obtain a dual of (105) which is given by

| (110) | ||||

| s.t. |

For the rest of proof, we assume as we focus on the subgradient for feasible binary solutions. To this end, we make use of the following result.

Claim: We claim at optimality of the primal/dual pair (105)/(110), for

| (111) | ||||

where is given by (28).

Proof of Claim: First, note that at optimality, from (109), which proves the second equation in the claim. To prove the rest of the claim, we consider the following cases:

-

1.

: In this case, from (109) we have so

-

2.

: In this case, similar to the above case (1), so

-

3.

: In this case, from complementary slackness we have and as , we have . This implies . Therefore, from (108),

This completes the proof of claim (111).

In (110), the cost function is larger if the value of is smaller. Therefore, at optimality, we have that

| (112) |

| (113) |

(which implies ). This is true as by (111), for . By this choice of , the optimal value of are given by (30). This true as for , if , the contribution of in the dual cost is . If , the contribution of this term is zero. In other cases, by taking such as in (30), the contribution of is zero which is dual optimal. For , the choice of leads to which is dual optimal. In addition, by complementary slackness, at optimality, . In (110), is written as the maximum of linear functions of , therefore, the gradient of the dual cost function w.r.t at an optimal dual solution, is a subgradient of by Danskin’s Theorem (Bertsekas, 1997). Finally, the gradient of cost in (110) w.r.t. is and the gradient w.r.t. is

by claim (111). ∎

References

- Aktürk et al. (2009) M Selim Aktürk, Alper Atamtürk, and Sinan Gürel. A strong conic quadratic reformulation for machine-job assignment with controllable processing times. Operations Research Letters, 37(3):187–191, 2009.

- Amini and Wainwright (2009) Arash A. Amini and Martin J. Wainwright. High-dimensional analysis of semidefinite relaxations for sparse principal components. Ann. Statist., 37(5B):2877–2921, 10 2009. doi: 10.1214/08-AOS664. URL https://doi.org/10.1214/08-AOS664.

- Behdin and Mazumder (2021) Kayhan Behdin and Rahul Mazumder. Archetypal analysis for sparse nonnegative matrix factorization: Robustness under misspecification. arXiv preprint arXiv:2104.03527, 2021.

- Berk and Bertsimas (2019) Lauren Berk and Dimitris Bertsimas. Certifiably optimal sparse principal component analysis. Mathematical Programming Computation, 11(3):381–420, 2019.

- Berthet and Rigollet (2013) Quentin Berthet and Philippe Rigollet. Optimal detection of sparse principal components in high dimension. Ann. Statist., 41(4):1780–1815, 08 2013. doi: 10.1214/13-AOS1127. URL https://doi.org/10.1214/13-AOS1127.

- Bertsekas (1997) Dimitri P Bertsekas. Nonlinear programming. Journal of the Operational Research Society, 48(3):334–334, 1997.

- Bertsimas and Van Parys (2020) Dimitris Bertsimas and Bart Van Parys. Sparse high-dimensional regression: Exact scalable algorithms and phase transitions. The Annals of Statistics, 48(1):300–323, 2020.

- Bertsimas et al. (2016) Dimitris Bertsimas, Angela King, and Rahul Mazumder. Best subset selection via a modern optimization lens. The annals of statistics, 44(2):813–852, 2016.

- Bertsimas et al. (2020) Dimitris Bertsimas, Ryan Cory-Wright, and Jean Pauphilet. Solving large-scale sparse pca to certifiable (near) optimality. arXiv preprint arXiv:2005.05195, 2020.

- Boyd and Vandenberghe (2004) Stephen Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Bresler et al. (2018) Guy Bresler, Sung Min Park, and Madalina Persu. Sparse pca from sparse linear regression. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, NIPS’18, page 10965–10975, Red Hook, NY, USA, 2018. Curran Associates Inc.

- Cai and Zhou (2012) T. Tony Cai and Harrison H. Zhou. Optimal rates of convergence for sparse covariance matrix estimation. Ann. Statist., 40(5):2389–2420, 10 2012. doi: 10.1214/12-AOS998. URL https://doi.org/10.1214/12-AOS998.

- d’Aspremont et al. (2005) Alexandre d’Aspremont, Laurent E Ghaoui, Michael I Jordan, and Gert R Lanckriet. A direct formulation for sparse pca using semidefinite programming. In Advances in neural information processing systems, pages 41–48, 2005.

- Deshpande and Montanari (2016) Yash Deshpande and Andrea Montanari. Sparse pca via covariance thresholding. The Journal of Machine Learning Research, 17(1):4913–4953, 2016.

- Dey et al. (2018) Santanu S Dey, Rahul Mazumder, and Guanyi Wang. A convex integer programming approach for optimal sparse pca. arXiv preprint arXiv:1810.09062, 2018.

- Duran and Grossmann (1986) Marco A Duran and Ignacio E Grossmann. An outer-approximation algorithm for a class of mixed-integer nonlinear programs. Mathematical programming, 36(3):307–339, 1986.

- d’Aspremont et al. (2008) Alexandre d’Aspremont, Francis Bach, and Laurent El Ghaoui. Optimal solutions for sparse principal component analysis. Journal of Machine Learning Research, 9(Jul):1269–1294, 2008.

- Fan et al. (2020) Jianqing Fan, Yongyi Guo, and Ziwei Zhu. When is best subset selection the” best”? arXiv preprint arXiv:2007.01478, 2020.

- Frangioni and Gentile (2006) A. Frangioni and C. Gentile. Perspective cuts for a class of convex 0–1 mixed integer programs. Math. Program., 106(2):225–236, May 2006. ISSN 0025-5610.

- Gataric et al. (2020) Milana Gataric, Tengyao Wang, and Richard J Samworth. Sparse principal component analysis via axis-aligned random projections. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 82(2):329–359, 2020.

- Günlük and Linderoth (2010) Oktay Günlük and Jeff Linderoth. Perspective reformulations of mixed integer nonlinear programs with indicator variables. Mathematical programming, 124(1):183–205, 2010.

- Guyon et al. (2005) Isabelle Guyon, Steve Gunn, Asa Ben-Hur, and Gideon Dror. Result analysis of the nips 2003 feature selection challenge. In Advances in Neural Information Processing Systems, volume 17. MIT Press, 2005.

- Hastie et al. (2019) Trevor Hastie, Robert Tibshirani, and Martin Wainwright. Statistical learning with sparsity: the lasso and generalizations. Chapman and Hall/CRC, 2019.

- Hazimeh and Mazumder (2020) Hussein Hazimeh and Rahul Mazumder. Fast best subset selection: Coordinate descent and local combinatorial optimization algorithms. Operations Research, 68(5):1517–1537, 2020.

- Hazimeh et al. (2020) Hussein Hazimeh, Rahul Mazumder, and Ali Saab. Sparse regression at scale: Branch-and-bound rooted in first-order optimization. arXiv preprint arXiv:2004.06152, 2020.

- Hotelling (1933) Harold Hotelling. Analysis of a complex of statistical variables into principal components. Journal of educational psychology, 24(6):417, 1933.

- Johnstone (2001) Iain M. Johnstone. On the distribution of the largest eigenvalue in principal components analysis. Ann. Statist., 29(2):295–327, 04 2001. doi: 10.1214/aos/1009210544. URL https://doi.org/10.1214/aos/1009210544.

- Johnstone and Lu (2009) Iain M Johnstone and Arthur Yu Lu. On consistency and sparsity for principal components analysis in high dimensions. Journal of the American Statistical Association, 104(486):682–693, 2009.

- Jolliffe et al. (2003) Ian T Jolliffe, Nickolay T Trendafilov, and Mudassir Uddin. A modified principal component technique based on the lasso. Journal of computational and Graphical Statistics, 12(3):531–547, 2003.

- Krauthgamer et al. (2015) Robert Krauthgamer, Boaz Nadler, Dan Vilenchik, et al. Do semidefinite relaxations solve sparse pca up to the information limit? The Annals of Statistics, 43(3):1300–1322, 2015.

- Lei and Vu (2015) Jing Lei and Vincent Q. Vu. Sparsistency and agnostic inference in sparse PCA. The Annals of Statistics, 43(1):299 – 322, 2015.

- Li and Xie (2020) Yongchun Li and Weijun Xie. Exact and approximation algorithms for sparse pca. arXiv preprint arXiv:2008.12438, 2020.

- Luss and Teboulle (2013) Ronny Luss and Marc Teboulle. Conditional gradient algorithms for rank-one matrix approximations with a sparsity constraint. siam REVIEW, 55(1):65–98, 2013.

- Meinshausen and Bühlmann (2006) Nicolai Meinshausen and Peter Bühlmann. High-dimensional graphs and variable selection with the Lasso. The Annals of Statistics, 34(3):1436 – 1462, 2006.

- Moghaddam et al. (2006) Baback Moghaddam, Yair Weiss, and Shai Avidan. Spectral bounds for sparse pca: Exact and greedy algorithms. In Advances in neural information processing systems, pages 915–922, 2006.

- Paul (2007) Debashis Paul. Asymptotics of sample eigenstructure for a large dimensional spiked covariance model. Statistica Sinica, 17(4):1617–1642, 2007.

- Raskutti et al. (2011) G. Raskutti, M. J. Wainwright, and B. Yu. Minimax rates of estimation for high-dimensional linear regression over -balls. IEEE Transactions on Information Theory, 57(10):6976–6994, 2011.

- Richtárik et al. (2020) Peter Richtárik, Majid Jahani, Selin Damla Ahipaşaoğlu, and Martin Takáč. Alternating maximization: Unifying framework for 8 sparse pca formulations and efficient parallel codes. Optimization and Engineering, pages 1–27, 2020.

- Rigollet and Hütter (2015) Phillippe Rigollet and Jan-Christian Hütter. High dimensional statistics. Lecture notes for course 18S997, 2015.

- Rudelson and Vershynin (2013) Mark Rudelson and Roman Vershynin. Hanson-Wright inequality and sub-gaussian concentration. Electronic Communications in Probability, 18(none):1 – 9, 2013.

- Stewart and Sun (1990) G.W. Stewart and Ji-guang Sun. Matrix Perturbation Theory. Computer science and scientific computing. Academic Press, 1990.

- Vershynin (2018) Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- Wang et al. (2016) Tengyao Wang, Quentin Berthet, and Richard J. Samworth. Statistical and computational trade-offs in estimation of sparse principal components. The Annals of Statistics, 44(5):1896 – 1930, 2016.

- Wedin (1972) Per-Åke Wedin. Perturbation bounds in connection with singular value decomposition. BIT Numerical Mathematics, 12(1):99–111, 1972.

- Witten et al. (2009) Daniela M Witten, Robert Tibshirani, and Trevor Hastie. A penalized matrix decomposition, with applications to sparse principal components and canonical correlation analysis. Biostatistics, 10(3):515–534, 2009.

- Yuan and Zhang (2013) Xiao-Tong Yuan and Tong Zhang. Truncated power method for sparse eigenvalue problems. Journal of Machine Learning Research, 14(Apr):899–925, 2013.

- Zhang (2006) Fuzhen Zhang. The Schur complement and its applications, volume 4. Springer Science & Business Media, 2006.

- Zou et al. (2006) Hui Zou, Trevor Hastie, and Robert Tibshirani. Sparse principal component analysis. Journal of computational and graphical statistics, 15(2):265–286, 2006.