Post-selection inference for linear mixed model parameters using the conditional Akaike information criterion

Abstract

We investigate the issue of post-selection inference for a fixed and a mixed parameter in a linear mixed model using a conditional Akaike information criterion as a model selection procedure. Within the framework of linear mixed models we develop complete theory to construct confidence intervals for regression and mixed parameters under three frameworks: nested and general model sets as well as misspecified models. Our theoretical analysis is accompanied by a simulation experiment and a post-selection examination on mean income across Galicia’s counties. Our numerical studies confirm a good performance of our new procedure. Moreover, they reveal a startling robustness to the model misspecification of a naive method to construct the confidence intervals for a mixed parameter which is in contrast to our findings for the fixed parameters.

keywords:

conditional Akaike information criterion, fixed parameter, mixed parameter, post-selection inference, small area estimation1 Introduction

Model or variable selection appears to be a routine practice in a great majority of statistical and machine learning data analyses. Despite the additional randomness coming from data-driven model selection procedures, both specialists and practitioners tend to disregard it in the subsequent steps of statistical inference. Instead, they often use classical theory to construct confidence intervals and testing procedure even though such theory might be invalid in their context. Many authors have stressed the need to account for selection uncertainty in the context of a classical regression (e.g., Hjort and Claeskens, 2003; Leeb and Pötscher, 2003, and in a more recent surge of articles Berk et al., 2013; Ferrari and Yang, 2015; Charkhi and Claeskens, 2018; Bachoc et al., 2019). Moreover, the topic has been thoroughly discussed by, among others, Belloni et al. (2015); Lee et al. (2016); Tibshirani et al. (2016) in the field of selective inference in which both the choice of the model and the target parameter are data-driven.

Despite the interest in the post-selection inference in many statistical domains, it remains a largely neglected problem in the field of linear mixed models (LMMs). The latter have been thoroughly studied, and are broadly applied for modelling clustered or longitudinal data (Verbeke and Molenberghs, 2000; Jiang, 2007) in, among others, ecology (Bolker et al., 2009), small area estimation (Rao and Molina, 2015; Morales et al., 2021) or medicine (Francq et al., 2019). Recently Sugasawa et al. (2019) developed the first contribution towards the post-selection inference under LMM, and investigated a procedure based on a prediction error criterion for the area-level model of Fay and Herriot (1979). Their proposal involves a simultaneous estimation and a model selection of a mixed parameter, consisting of both fixed and random effects, and it is tailored to minimize the estimated mean squared error. For comparison with our method, we implement the observed best selective predictor (OBSP) of Sugasawa et al. (2019) and study its performance in simulations in Section 6. The issue of accounting for the model selection in the context of LMM has been also mentioned by Cunen et al. (2020), but the authors did not approach it in their article.

Our goal is thus to investigate post-selection inference under a classical, low-dimensional framework for fixed (regression) parameters and their linear combinations as well as a general mixed parameter. A precise estimation of the former is indispensable in any statistical analysis whereas the latter is essential in, among others, small area estimation (SAE). In particular, we address the construction of valid post-selection confidence intervals. Due to its practical relevance, we concentrate on the inference after the selection of covariates for fixed effects when random effects are present and the variance structure is not subject to the selection process. The selection of random effects involves a different strand of literature and methods. Charkhi and Claeskens (2018) studied the asymptotic distribution of estimators after model selection using Akaike’s information criterion (AIC), proposed by Akaike (1973), and applied this distribution to construct adjusted confidence intervals for fixed effects and linear combinations of them. Even though their general approach is suitable for any likelihood-based model, Charkhi and Claeskens (2018) did not consider random effects. Within the mixed model setting, we can differentiate population and cluster foci, a distinction made already by Harville (1977). In LMMs, a classical AIC has a population focus and is obtained by integrating out random effects and using a marginal log-likelihood. Hence, it is often referred to as a marginal AIC (mAIC). Due to its main target, mAIC is not appropriate for the prediction of cluster-level parameters or mixed effects. We therefore use a criterion which selects covariates in terms of minimising the prediction errors with the focus on specific random effects. Considering this aspect, Vaida and Blanchard (2005) proposed a conditional AIC under the assumption of known variance parameters. Since covariance matrices are usually unknown and need to be estimated, the assumption of Vaida and Blanchard (2005) and later of Liang et al. (2008) seems to be too stringent for a practical use. Therefore, in what follows we use a conditional AIC (cAIC) of Kubokawa (2011) who extended the proposal of Vaida and Blanchard (2005) and accounted for the estimation of the variability parameters. Our examination on the inference after cAIC-selection (henceforth we refer to it as post-cAIC inference) can thus be treated as a twofold extension of the theory of Charkhi and Claeskens (2018). First, we consider a different model selector; second, and more importantly, we focus not only on fixed effects, but also on mixed parameters consisting of both fixed and random effects.

After the proposal of Vaida and Blanchard (2005), scholars have developed several extensions to the initial information criterion with a cluster focus (see Müller et al., 2013, for an extensive review of model selection techniques under LMM). Apart from cAIC of Kubokawa (2011), Srivastava and Kubokawa (2010) defined an alternative conditional Akaike information and investigated its unbiased estimator, which resulted in a modified cAIC. Furthermore, Kawakubo and Kubokawa (2014) introduced a criterion which is appropriate to cover underspecified cases, that is, when the list of models does not include the true one (in Section 5 we adopt the terminology of Charkhi and Claeskens, 2018, and call it a misspecified setting). Another modification is to use information criteria with generalised degrees of freedom (GDF) combined with a marginal or a conditional likelihood as in Greven and Kneib (2010) and You et al. (2016). On the other hand, Lombardía et al. (2017) employed GDF with the quasi-log-likelihood which focuses on random effects and the total variability, combining a conditional and a marginal log-likelihood. Hereinafter we consider only post-cAIC inference; the comparative study of the post-selection inference using different methods with a cluster focus might be a subject of possible future research.

For the sake of comparison, we use the framework and a similar notation of Charkhi and Claeskens (2018) unless it is in conflict with ours. In Section 2 we present key concepts of LMM inference. Then we investigate three settings to construct post selection confidence intervals. We initialise with the set of nested models in Section 3 and then move towards any set of models in Section 4. In Section 5 we consider a post-selection inference for a set of misspecified models. In Section 6, we outline the outcomes of the numerical study, whereas in Section 7 we apply post-cAIC inference in a study on mean income in the counties of Galicia. We conclude with a discussion in Section 8 while deferring certain technical details to Section 9 and the supplementary material (SM) in Section 10.

2 Inference in linear mixed models

We examine the inference under individual cluster LMM, i.e., each observation belongs to one cluster, and clusters are independent. To facilitate the exposition, we provide the definition for a full model with all possible fixed parameters included, that is

| (1) |

where is a vector of target variables, and are matrices of covariates, is a vector of fixed effects, is a vector of random effects and , whereas is a vector of stochastic errors. Splitting the dimension of the covariates to the sum of is convenient for presenting our post-selection analysis, and is clarified in Section 3. We assume that , where is an h-dimensional vector of variance parameters. Furthermore, we suppose that and are positive definite matrices known up to the vector . We denote the total number of clusters by and the total number of units by . Expression (1) can be rewritten in a succinct form

| (2) |

where is an matrix of rank , is an matrix of rank , , and is block-diagonal with blocks on the diagonal. The marginal and conditional distributions of are and , respectively, where . Twice negative marginal log-likelihood and extended log-likelihood functions for modelled by equation (2) are:

Numerous methods have been established to estimate , and . By far the most popular are two-stage techniques such as the best linear unbiased estimator and the best linear unbiased predictor (BLUP), mixed-model equations of Henderson (1950), the Bayes estimation or the likelihood based inference (see, for example, Verbeke and Molenberghs, 2000; Jiang, 2007, for all essential procedures). In what follows we concentrate on the former. Regarding , we estimate it iteratively by maximizing (2) or by using the restricted log-likelihood version. Both of them were discussed by Laird and Ware (1982). In addition, one can take a derivative of (2) with respect to to obtain . Once is estimated, we plug it into to obtain . An alternative analysis is required if we tend to focus on the inferences with respect to random effects . Henderson (1950) used the extended likelihood in (2) to obtain the estimates of and predictions of :

| (5) |

which results in the same expression for as by using the marginal likelihood in (2). The mixed-model equations in (5) can be used to obtain a pseudo hat-matrix

| (6) |

where . We call the effective degrees of freedom (Hodges and Sargent, 2001). They are used as the main part of the penalty term in cAIC. It follows that (Vaida and Blanchard, 2005) and we have .

We focus on post-cAIC inference for (i) a fixed parameter in (1), (ii) a linear combination , and (iii) a general mixed parameter

| (7) |

where , and is the EBLUP of . The variability of regression parameters can be derived directly from the marginal log-likelihood in (2). Regarding the mixed effect, Henderson (1975) employed (5) to obtain a formula for the variance of in (7). Due to the presence of a random effect, this variance is often referred to as mean squared error (MSE). We thus have , where and are spelled out in the SM. Replacing in with results in an estimator

| (8) |

which is called the first-order correct MSE estimator in the SAE literature. On the contrary, an analytical second-order correct estimator is given by

| (9) |

The exact expressions for , and can be found in, for example, Rao and Molina (2015) and our SM. We use in (9) to construct naive confidence intervals which do not account for the selection uncertainty. Finally, the cAIC of Kubokawa (2011)

| (10) |

is an asymptotically unbiased estimator of the conditional Akaike information (cAI) , where is a future variable distributed according the same normal distribution as , is an estimated version of the effective degrees of freedom in (6), is the additional penalty accounting for the estimation of variance parameter . Since the exact form of cAIC for a general LMM is complex, we defer it to our SM (cf. Kubokawa, 2011, for the derivation).

3 Selection properties of the cAIC in nested models

We investigate the nested sequence of likelihood models which depend on the parameter vector . More specifically, model contains covariates, in model we employ covariates, etc. The largest model contains a full vector . The parameter that is common to all models and thus not subject to the selection procedure is denoted by . Without loss of generality, we assume that adds one covariate to . Furthermore, there exists a single minimal true model in the set of general models , that is, is the smallest model order for which all non-zero components of the true vector are included. Models with are underparametrised and with overparametrised. In addition, denotes a subvector of which corresponds to model . Furthermore, in model we define , its counterparts and estimated using maximum marginal and conditional log-likelihoods as defined in equations (2) and (2) respectively. In addition, let and . Last but not least, we can distinguish , which is the true value with for , whereas is composed of non-zero elements of . If no confusion is possible, we omit the dependence on in .

The conditional Akaike information criterion for model in the set of models is formally given as , where is the conditional likelihood defined in equation (2), is a vector of estimated covariates using the marginal likelihood, and are estimated penalty terms. The index of the selected model is . To continue with the post-selection inference we need to rewrite the cAIC-based selection procedure using a set of inequalities which impose geometrical restrictions on the support of the normally distributed random variables. First, we redefine , with

where can be treated as an effective difference between the degrees of freedom imposed on the true model and on the selected model. The probability of underselection using cAIC is asymptotically zero (see Lemma 1 in Section 4 and its proof in our SM), which implies that . A similar result was demonstrated for AIC by Woodroofe (1982) and generalised by Charkhi and Claeskens (2018). If we condition on , for and for . For a full model , denote by the Fisher information matrix in a marginal setting with all parameters, and by the negative Hessian calculated from the conditional likelihood (their precise definitions are given in Section 9.1). Unless the model is correctly specified, we have . Furthermore, we define . Consequently, a submatrix of which corresponds to model is denoted by and refers only to the covariates from the considered model . Let the diagonal and the off-diagonal elements of be and , . Furthermore, let and be submatrices of and , respectively, corresponding to the model . In addition, we denote by an indicator function. Let and and and their empirical versions. Consider the sequence of nested models . It follows that the selection region for a fixed parameter is defined as follows:

for we have

| (11) |

for we have where

| (12) |

In other words, describes constraints on the domain of multidimensional normal random variables. The specific form of is defined by the set of inequalities coming from the asymptotic analysis of . Since the random effects are not subject to the selection procedure, the selection region for a mixed parameter has almost the same form for and . In fact, one would need to only replace with in (11) and (12).

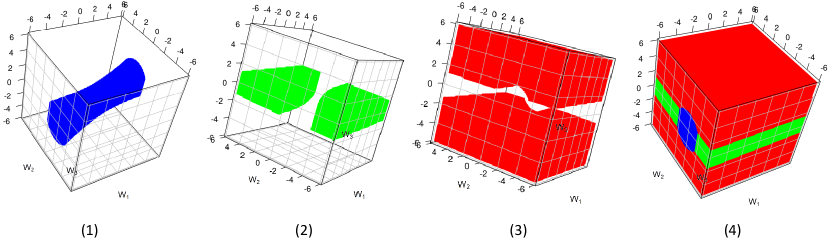

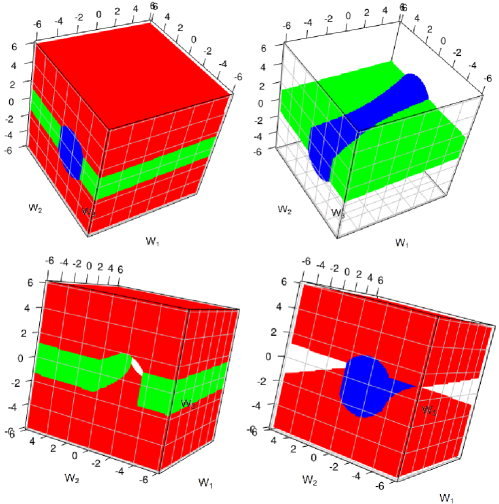

We illustrate the allowable domains for normal random variables , and using the restrictions imposed by the cAIC selection. The domains of the random effects are not affected by the geometrical restrictions. Consider , , , and suppose that is a true model containing only , that is, . Moreover, whereas . To be able to plot the domains, we need to fix or estimate the values of , and , . We thus constructed a simulated dataset using a simplified setting from Section 6, the details can be found in our SM.

Figure 1 depicts geometrical regions which restrict the domains of , and . The regions are defined by the appropriate equations in (11) and (12). Once , we have and use (1) to derive

which corresponds to the left panel of Figure 1. One obtains similar sets of equations if or (exact calculations are worked out in the SM). We conclude that a data-driven model selection heavily influences the domain of asymptotic distributions of the parameters that are subject to the selection process. The last panel of Figure 1 shows the partition of the space composed of , and . The following proposition describes the asymptotic distribution of a fixed and mixed effect after cAIC selection.

Proposition 1

Suppose that Assumptions from Section 9.1 are satisfied. Conditionally on the limiting distribution for a post-cAIC fixed parameter is

where , , is a submatrix whereas and are subvectors corresponding to a selected model . In addition, conditionally on , the limiting distribution for a post-cAIC mixed parameter is

where , and are subvectors and a submatrix corresponding to a selected model .

Proposition 1 leads to the following corollary on the asymptotic post-selection density of fixed effects. In the SM we illustrate the effect of the selection on the densities.

Corollary 1

Under the assumptions of Proposition 1, the post-cAIC density of with from is When cAIC selects the true model, , then .

Proposition 1 can be used to construct a post-cAIC confidence interval (CI) for a mixed parameter or components of a fixed effect. Using the same ideas as Charkhi and Claeskens (2018), we first focus on the latter. In fact, under the assumptions of Proposition 1, the asymptotic quantiles of the marginal distributions of , satisfy , where . Regarding a mixed effect, let and , where we keep the dependence on to stress that is calculated after cAIC selection of covariates. Post-cAIC CI for , , and , , are regions defined as

| (13) |

To retrieve critical values, we need to approximate the distribution of and using selection regions and . A detailed computational procedure involving Monte Carlo sampling is described in Section 6. We can use classical results to construct -CI which do not account for the selection uncertainty

| (14) |

, , where is a normal cumulative distribution function. We refer to intervals in (14) as naive CI. A high quantile from the normal distribution is sometimes replaced in (14) by a bootstrap based or analytically derived quantity which results in the second order correct CI (see, for example, a monograph of Rao and Molina, 2015, for a detailed discussion of the second-order correctness for a mixed parameter).

4 Selection properties of cAIC in general models

The set of candidate models substantially influences asymptotic post-selection inference (see Figures 1, 2 as well as the discussion accompanying them). Suppose that is a set composed of all possible submodels of a largest model. Second, let be the set of overparametrised models including the true model. It immediately follows that the models in are overlapping, according to the definition in Vuong (1989). Lemma 1 is an equivalent of Lemma 1 in Charkhi and Claeskens (2018) for cAIC. As one would expect, cAIC also exhibits an overselection property.

Lemma 1

Consider a set of models that contains at least one overparametrised candidate model and as a model selection criterion. Under assumptions in Section 9.1, an underparametrised model is selected with a probability converging to zero asymptotically.

The proof is deferred to our SM. Under this generalised modelling framework, the estimator of in model is denoted by . Furthermore, let and for model . In addition, , , denote a subvector and submatrices of and , respectively, corresponding to model . If the orthogonality assumption (e) in Section 9.1 holds, we obtain a simplified set of constraints given in (15). Otherwise, we follow the approach of Charkhi and Claeskens (2018) for overlapping models. Define matrix composed of two blocks. The first, , is a block diagonal matrix with on a th block. The second, , is the unitary matrix . The former corresponds to the covariates selected by cAIC. We define an extended selection matrix which indicates the diagonal and off-diagonal elements of . This matrix is necessary to construct a region similar to in (11) and (12). Let be a projection matrix that selects the elements of which belong to model , , the number of covariates in model . The extended selection matrix of dimension is a matrix composed of such that , where is the number of considered models and the projection matrices.

If assumption (e) from Section 9.1 holds, the selection region for a fixed parameter under model is

| (15) |

where , , , , , . Similarly as in Section 3, one needs to replace by to obtain the region for a mixed parameter. If the orthogonality condition (e) from Section 9.1 does not hold, define . Consider and as defined in (25) and (26). Let and . The selection regions are

| (16) | |||

| (17) |

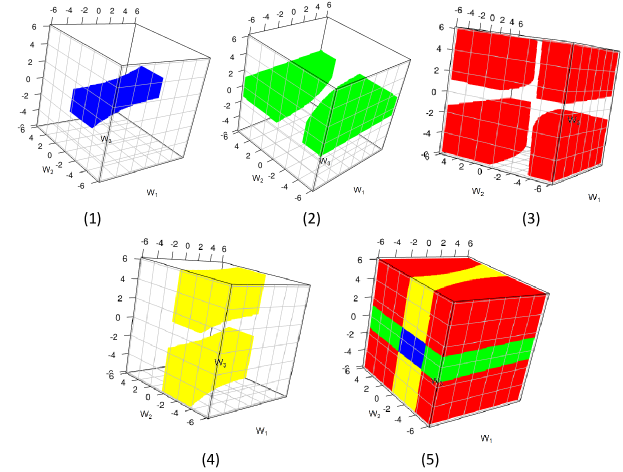

We follow up with the example from Section 3. Nevertheless, hereinafter we consider with , , as in the framework of the nested models and . Assuming , our restrictions are defined by 4 inequalities – in contrast to 3 inequalities for – which naturally affect the domain for random variables. Once , we have

which is illustrated in panel (1) of Figure 2. Similar equations can be derived for in panel (2), in panel (3) and in panel (4) (see our SM for exact expressions).

It is crucial to emphasise that even though we select the same model, the initial set, in our case or , influences allowable domains. This phenomenon is clearly visible if we compare Figures 1 and 2. Consider for example . The allowable domains assuming and are shown in panel (3) of Figures 1 and 2, respectively. We immediately conclude that the domains differ significantly. The choice of is of paramount importance – it affects the distribution of all parameters, even those which are common to all models. Similarly to Figure 1, panel (5) of Figure 2 presents the partition of the 3-dimensional space.

The following proposition describes the asymptotic distribution of a regression parameter and a mixed parameter after cAIC selection from a general set of models.

Proposition 2

(I) Suppose that Assumptions from Section 9.1 are satisfied. A limiting distribution for the post-cAIC fixed parameter is

where , , defined in (15), is a submatrix and , subvectors corresponding to a selected model . In addition, the limiting distribution for a post-cAIC mixed parameter is

where , and are subvectors, whereas is a submatrix corresponding to model .

Similarly as in Section 3, Proposition 1 leads to a corollary on the asymptotic post-selection density of fixed effects.

Corollary 2

Under the assumptions of Proposition 1, the limiting post-cAIC density of with from is , where , are -vectors of non-zero values.

One employs the density in Corollary 2 to construct confidence intervals for post-cAIC elements of . The asymptotic quantile satisfies , where imposes the restrictions on the j components. The form of the confidence intervals is almost identical as in (13) – we only need to replace with . The same applies to the CI for a fixed parameter. Proposition 2 leads us to the result on a linear combination . We have

5 Selection properties of cAIC in misspecified models

In this section we provide some uniformly valid results which do not require the assumption of the existence of the true model. To do so, we need to extend the misspecification framework of Charkhi and Claeskens (2018) to account for clustered data and cAIC model selection. In a series of papers Leeb and Pötscher (2003, 2006, 2008) proved that uniform results for post-selection estimators are not available for the traditional quantities , which we considered in Sections 3 and 4. These results are general and apply to various selection procedures such as LASSO or AIC (see Tibshirani et al., 2018; Charkhi and Claeskens, 2018). Nevertheless, under a misspecified setting (Charkhi and Claeskens, 2018), considering nonstandard targets (Berk et al., 2013) or modified pivots (Tibshirani et al., 2018), uniform results are attainable.

In our misspecified setting, the true parameter vector does not exist, because all models are misspecified or the true density is not a member of a parametric family. To be able to prove the uniform convergence, we use a framework with asymptotics based on a pseudo triangular array adapted for dependent data. In practice we collect one data sample. Thus our construction serves only to demonstrate the theoretical results. If we had a possibility to collect different samples, we assume that the observed vectors might be represented in an extended, vector based triangular array , that is, we suppose that and were independent for and for different samples. Let and as well as and be the true joint marginal and joint extended density and distribution of . In what follows, all probabilities are computed with respect to the true distributions and . Within this framework, the estimation of and often requires the same conditions imposed on marginal and extended loglikelihoods. If no confusion is possible, we state them using which stands for or . Since the likelihood might be misspecified, we use White’s (1994) quasi-likelihood framework for modelling. Models can be thus represented as

with the number of parameters in , and a compact set. The collection of all models is denoted by . Following Definition 2.2 in White (1994), the true class of distribution is defined by for each . When no confusion is possible, we skip the subscript . Furthermore, for each and each , and are measurable for all , . We suppose that is almost surely continuous and continuously differentiable on . The existence of the marginal and extended likelihood estimators follows from the extension of Lemma 2.1 in Gallant and White (1988), that is we adapt their results to account for modelling independent vectors, rather than independent scalars. The ideas of the proof are general enough to be applied in this setting. We therefore assume that there exist estimators , maximising and over . Furthermore, we call the pseudo-true values and the maximisers of

if such exists. These maximisers depend on the sample size , the true joint density and the model densities. Denote with . For the marginal likelihood we have , , that is, vectors of length . On the other hand, for the extended parameters the vectors , are of length .

Lemma 2 refers only to the extended vector of parameters due to our mixed parameter focus. An equivalent statement is valid for fixed parameters estimated using the marginal loglikelihood. In addition, recall that the estimating equations for the fixed parameters using marginal and extended loglikelihood result in the same expression (see Section 2 and references therein for more details). Even though the extended likelihood is not a proper likelihood as it includes non-observable random effects, the general results of Lemma 2.1 in Gallant and White (1988) are applicable in this setting. Therefore,

Lemma 2

Define where is a block matrix with th block equal to . We thus have

| (18) |

where and as defined in Section 9.1.

We assume that there exists an estimator of such that , where is the Euclidean matrix norm operator and we suppose that (for a discussion about the existence of such estimators see White, 1994, §8.3). The uniform convergence result (18) is also valid for a pivotal statistic:

5.1 Post-selection inference for misspecified models

As we do above, we define a selection region using pairwise comparisons between misspecified models from a set . Define . Model is selected if , for each . As it was stated in Section 3, this is equivalent with , where in this section

and is defined in an analogous way with replaced by . As we showed in Sections 3 and 4, when both models are correctly specified, the difference of the conditional log-likelihoods can be described using scaled chi-squared random variables. Vuong (1989) investigated the conditions under which the difference of marginal likelihoods converges assuming model misspecification. A full characterization of the asymptotic distribution is possible only in case of the similarity of likelihoods. Since in our selection procedure we only consider fixed effects, similar arguments, that is, Taylor expansions of the conditional likelihoods around the true value can be used to prove divergence in our setting. We thus focus on the misspecified setting in the case of the similarity of the conditional likelihoods, that is for . Following Charkhi and Claeskens (2018), we consider a general set of models and suppose that it includes the smallest model nested in all other models. Our strategy is to compare all models with the smallest one and then determine the final regions using, as before, pairwise comparisons. For each , we have

where and as defined in Section 9.1, the third line is a direct result of . The expansion for follows along the same lines, we just need to replace with . Once we compare them we obtain

In addition, is a diagonal matrix with blocks and corresponding to models and . Following the same reasoning as in the proof of Proposition 2 in Section 4, we obtain the asymptotic selection event for model .

Proposition 3

The selection region for mixed parameter assuming a set of misspecified models is

Suppose that the assumptions from Lemma 2 hold. Then we have

| (19) |

6 Simulation study

We carried out an empirical simulation study to assess the performance of post-cAIC CI for a regression parameter, a linear combination of its components and a mixed parameter. In our analysis, we compare post-cAIC CI in (13) with naive intervals in (14). In case of the mixed parameter, we construct them using the first- and second-order correct MSE estimators in (8) and (9), respectively. It is well known that mixed-parameters are quite robust to misspecification of the shape of random effects (McCulloch and Neuhaus, 2011). We investigate the performance of our new method as well as the robustness of naive CI to model misspecification for fixed and mixed effects. The literature offers us a benchmark when it comes to the post-selection inference for mixed parameters under LMM. More specifically,, we compare our post-cAIC intervals with post-OBSP intervals constructed using OBSP for area-level parameters and post-selected MSE developed by Sugasawa et al. (2019). Since the authors focused on the area-level model only and did not consider the construction of the intervals, we somewhat extend their work regarding these two aspects.

The data generation process was inspired by Charkhi and Claeskens’s (2018) procedure. Namely, we assume a nested error regression model (NERM) with a true vector of fixed parameters , and , , . We consider two settings for and ; under setting 1 (S1) whereas under setting 2 (S2) . We wish to mimic two types of asymptotic regimes. In the first case, we assume that with fixed such that . Then, in the second case we suppose that is fixed and such that . The former scenario is popular in SAE (Rao and Molina, 2015) and longitudinal studies (Verbeke and Molenberghs, 2000), whereas the latter in repeated cross-sectional studies. Further, and , where is a positive definite matrix with 1 on the diagonal and 0.25 elsewhere. In case of post-cAIC inference for a linear combination of fixed effects , we computed linear combinations in each simulation, and set , that is, vectors were means of cluster covariates. Under NERM, the computation of the second term of the penalty in cAIC defined in (10) is simplified (a spelled out formula can be found in Kubokawa, 2011, Section 4.3). We consider three different model sets. Denote by the extended selection matrix when the first parameters are present in all models. In our empirical study we examine which is a matrix (5 covariates and 10 covariance terms), (a matrix) and (a matrix). Since all model sets led to the same conclusions, the results under and are deferred to the SM. We run our simulations until model with parameters had been selected times. In each simulation run, we estimate the matrix defined in Section 3 for a full model. Its submatrix corresponds to the model selected in a particular simulation. We apply a result derived from Proposition 2 (I) to calculate the confidence intervals. Observe that one should employ (II) if the orthogonality condition from Section 9.1 does not hold. Nevertheless, following the practice of Charkhi and Claeskens (2018), we use (I) which leads to good numerical outcomes. In the SM, we describe a procedure to obtain post-cAIC CI as a practical algorithm. Furthermore, we provide some practical guidance on sampling from a multivariate truncated normal.

S Meth. CP (L) CP (L) CP (L) CP (L) CP (L) CP (L) S1 p.-cAIC 93.2 (1.144) 94.4 (0.818) 95.9 (0.582) 96.2 (0.467) 95.9 (0.831) 94.1 (0.768) 94.8 (0.806) 96.2 (0.531) 95.8 (0.379) 96.5 (0.320) 96.8 (0.363) 96.0 (0.251) N 92.9 (1.099) 93.8 (0.796) 95.0 (0.560) 95.8 (0.456) 93.9 (0.748) 93.0 (0.727) 66.8 (0.569) 72.3 (0.377) 69.6 (0.267) 70.4 (0.218) 69.2 (0.256) 66.9 (0.175) S2 p.-cAIC 92.4 (0.849) 93.6 (0.622) 95.0 (0.439) 97.1 (0.355) 94.3 (0.589) 94.3 (0.540) 93.1 (0.807) 93.1 (0.521) 95.7 (0.378) 96.7 (0.323) 97.2 (0.371) 96.4 (0.254) N 92.3 (0.837) 93.5 (0.618) 94.9 (0.435) 97.1 (0.353) 93.1 (0.558) 93.7 (0.527) 64.5 (0.562) 68.3 (0.373) 70.8 (0.264) 67.2 (0.216) 68.1 (0.255) 66.7 (0.175)

Table 1 presents coverage probabilities (CP) and lengths (L) for post-cAIC (p.-cAIC) and naive (N) CI for the components of fixed parameters . CP and L were calculated as an average over simulation runs. The superiority of post-cAIC is unquestionable as its coverage always oscillates around the nominal level. In contrast, the naive CI for never surpasses , which is a consequence of treating a chosen model as given. Our results are in alignment with those in Charkhi and Claeskens (2018), in which post-AIC CI are studied for fixed parameters in a modelling setting without random effects. Let us investigate the effect of including covariates to our parameter of interest. Table 2 displays coverage probabilities and average lengths for linear combinations of the components of fixed parameters. We present two randomly selected linear combinations and which stands for the average over parameters. While we can observe an improvement of the performance of the naive CI in comparison with Table 1, the undercoverage still persist. In contrast, post-cAIC CI perform better overall with a coverage close to the nominal level.

S Meth. Par. CP (L) CP (L) CP (L) CP (L) CP (L) CP (L) S1 p.-cAIC 95.4 (1.411) 97.7 (0.990) 94.7 (0.711) 98.6 (0.577) 96.6 (0.891) 93.9 (0.751) 96.6 (1.631) 94.5 (0.923) 96.3 (0.669) 98.0 (0.575) 96.2 (0.870) 94.5 (0.793) 95.3 (1.374) 95.8 (0.998) 96.7 (0.711) 97.1 (0.572) 96.5 (0.891) 94.5 (0.786) N 89.6 (1.155) 94.2 (0.820) 91.0 (0.608) 95.5 (0.467) 92.9 (0.765) 93.6 (0.731) 88.9 (1.186) 91.9 (0.837) 94.1 (0.596) 94.2 (0.480) 93.3 (0.752) 93.3 (0.728) 92.0 (1.159) 92.3 (0.844) 93.4 (0.594) 94.1 (0.487) 93.5 (0.758) 93.3 (0.731) S2 p.-cAIC 94.1 (1.155) 97.3 (0.864) 94.1 (0.534) 97.0 (0.451) 96.8 (0.672) 94.2 (0.568) 95.0 (0.997) 96.6 (1.053) 96.7 (0.538) 97.8 (0.625) 96.0 (0.665) 94.5 (0.548) 95.2 (1.117) 97.0 (0.844) 97.0 (0.597) 97.6 (0.485) 96.0 (0.661) 94.5 (0.560) N 87.4 (0.910) 94.0 (0.697) 91.7 (0.460) 95.1 (0.406) 91.5 (0.571) 93.3 (0.537) 92.3 (0.841) 86.9 (0.769) 94.7 (0.479) 87.2 (0.437) 93.1 (0.580) 93.9 (0.530) 91.0 (0.912) 92.3 (0.677) 92.9 (0.477) 93.9 (0.390) 93.1 (0.571) 93.5 (0.532)

S Meth. CP (L) CP (L) CP (L) CP (L) CP (L) CP (L) S1 p.-cAIC 94.9 (1.646) 95.5 (1.660) 95.4 (1.645) 95.5 (1.641) 95.3 (1.213) 95.1 (0.871) N1 93.6 (1.564) 94.8 (1.607) 95.1 (1.615) 95.2 (1.619) 94.9 (1.192) 94.9 (0.864) N2 95.1 (1.648) 95.2 (1.636) 95.3 (1.629) 95.3 (1.629) 95.1 (1.202) 95.0 (0.868) p.-OBSP 94.8 (1.628) 95.2 (1.632) 95.2 (1.626) 95.3 (1.627) 95.1 (1.200) 94.3 (0.867) S2 p.-cAIC 93.4 (1.518) 94.9 (1.550) 95.5 (1.539) 95.5 (1.529) 95.2 (1.161) 95.0 (0.849) N1 91.7 (1.422) 93.7 (1.481) 94.9 (1.502) 95.1 (1.503) 94.7 (1.140) 94.9 (0.843) N2 96.4 (1.669) 95.5 (1.567) 95.5 (1.537) 95.5 (1.526) 95.3 (1.165) 95.1 (0.851) p.-OBSP 93.5 (1.516) 94.5 (1.524) 95.3 (1.523) 95.3 (1.516) 95.1 (1.154) 94.3 (0.848)

Finally, we study the performance of CI for mixed effects which are linear combinations of fixed and random effects; the latter are partly intended to smooth model misspecifications. Table 3 shows coverage probabilities and lengths for post-cAIC (p.-cAIC), post-OBSP (p.-OBSP) and naive confidence intervals constructed using the first-(N1) and the second-(N2) order correct MSE estimators under selection matrix . CP and L were calculated as an average over the simulation runs and mixed parameters. Regarding post-cAIC confidence intervals, they attain a nominal coverage or suffer from a minor undercoverage when a sample size is small. The performance of post-OBSP intervals is similar. In addition, in both cases the intervals are very often narrower than in the case of a naive method N2. Yet, the most striking feature is a surprisingly good performance of the second-order naive intervals. They almost always reach the nominal level and they are only slightly wider than the post-selection intervals. Although the naive CI are not theoretically valid, because they ignore the selection step in their asymptotic distributions, it seems that the are extremely robust to this misspecification.

7 Post-cAIC inference of income data in Galicia

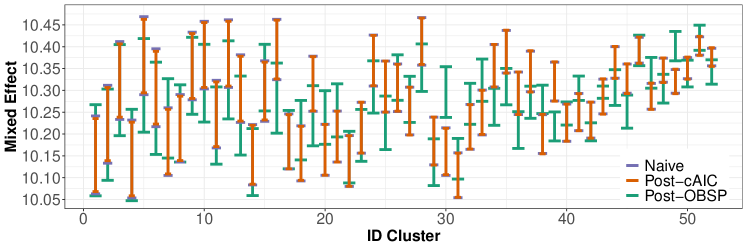

We illustrate our post-cAIC procedure by constructing confidence intervals for the average of rescaled household incomes in 52 counties of Galicia in north-western Spain. We make use of the 2015 Structural Survey of Homes in Galicia (SSHG) with 9203 households, yet with certain areas where the number of units is small with , see Reluga et al. (2021) for a detailed study about household income on the original scale using the same data set. Galicia is subdivided into 53 counties (comarcas), but the data were not collected in county Quiroga. The SSHG contains covariates on different sources of income, personal characteristics (for example, age, education level) as well as information on the household status (such as number of household members, mortgage situation, etc.). The originally observed is the yearly family household income per capita. It is well known that income data are right skewed, and our dependent variable exhibits this feature too. As our theory relies on normality, we follow a standard practice in the SAE literature and transform it by , where constant minimises the Fisher skewness of the model residuals with as a response. Constant is selected from a grid within the range of household incomes (the same approach was used, among others, by Marhuenda et al., 2017). We analyse two estimators for the cluster-level means of the household income which are popular in SAE: EBLUP of a mixed parameter and a linear combination of the estimated regression parameters in (7). The latter is called the regression-synthetic estimator in the survey statistic and SAE literature (Rao and Molina, 2015). More specifically, we consider and , where is the official estimate of covariate means which we calculate from the SSHG (the details of the calculations are deferred to the SM). As was illustrated in Sections 3 and 4, the initial set of models is crucial in the post-cAIC inference. We therefore did not use all possible covariates in the SSHG. In contrast, we selected eight covariates which are the most correlated to the outcome variable. We then constructed 16 models, and each of them contained an intercept and a subset of four covariates with the highest correlation (correlation coefficients, the inclusion of covariates in considered models and the results of the selection criteria can be found in our SM). cAIC selected Model 1 with an intercept and four covariates whereas OBSP of Sugasawa et al. (2019) Model 12 with an intercept and seven covariates.

Figure 3 presents naive confidence intervals constructed using the second-order correct MSE, post-cAIC and post-OBSP confidence intervals for the mixed parameter. We did not plot naive CI with first-order correct MSE because they were indistinguishable from the second-order intervals. First, some of the post-OBSP confidence intervals do not overlap with naive or post-cAIC intervals, because distinct models were selected by cAIC and OBSP. In the majority of counties, the post-cAIC CI are narrower than their naive and post-OBSP counterparts. This conclusion is confirmed by the descriptive statistics shown in our SM and in accordance with our simulation findings. Different widths of naive and post-cAIC intervals are related to the sample size of each county.

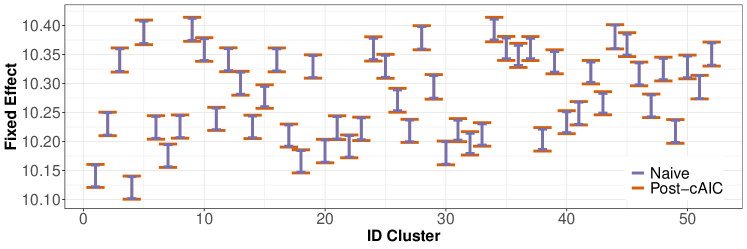

Figure 4 shows naive and post-cAIC confidence intervals for the synthetic-regression estimates. In contrast to Figure 3, post-cAIC CI are wider than naive CI. Even though the difference between post-cAIC and naive intervals in this study is minor, the latter have a tendency to undercover because they do not account for the model selection, cf. Table 2.

8 Discussion

We developed the asymptotic theory for post-cAIC inference. We employed our theoretical derivation to construct post-cAIC confidence intervals for mixed and fixed parameters under LMM. To the best of our knowledge, this is the first contribution which addresses post-selection inference under a general LMM framework. We tested finite sample properties of our proposal in simulations and a data example. In simulation scenarios, our post-cAIC CI performed well in terms of the coverage probability and average length. In contrast, the naive intervals performed very poorly in the numerical analysis of fixed parameters. Surprisingly, though, naive intervals for mixed parameters yielded satisfactory results. This demonstrates their robustness to possible model misspecifications and may justify their usage among practitioners. Nevertheless, we believe that theoretically valid methods, which are generally applicable, should always be preferred if they perform equally good as naive methods and they are not too intricate to implement. In follow-up studies, more extensive simulations will be needed to thoroughly examine the startling feature of naive intervals.

Finally, we developed post-cAIC after model selection with cluster focus, using the cAIC of Kubokawa (2011). The post-cAIC methodological advancements might be put forward in a similar way for other conditional Akaike information criteria, because the majority of them is composed of twice the conditional log-likelihood and a penalty function. Consider, for example, the cAIC of Srivastava and Kubokawa (2010), that is . To derive the selection region and hence post- CI, we could follow analogous steps as those for the cAIC of Vaida and Blanchard (2005) and modify the penalty function. A comprehensive account of the conditional Akaike criteria for which post-selection analysis is similar to ours is included in the review paper of Müller et al. (2013).

9 Technical details

9.1 Assumptions

We denote by an -dimensional sphere centred at with radius , and by its complement. In addition, stands for or which refer to a conditional or a marginal framework.

-

1.

For each , as , in probability.

-

2.

There exists such that is twice continuously differentiable in for all large . We define the score vector and the negative Hessian matrix .

-

3.

For some , as , there exist nonrandom positive-definite continuous matrices such that for in in probability.

-

4.

in distribution once .

-

5.

Orthogonality of the models under : for , , we have that , where the expectation is taken with respect to the true model.

The derivation of the cAIC of Kubokawa (2011), and first- and second-order correct MSE estimators require additional regularity conditions. Since we do not use them explicitly in the following derivations, they are deferred to the SM together with algebraic derivations, the proof of Lemma 1, and details on the structure of matrices and .

9.2 Asymptotic post-selection derivations

9.2.1 Statement and proof of Lemma 3

We need to guarantee a joint convergence of estimators which is obtained in Lemma 3.

Lemma 3

Suppose that Assumptions in Section 9.1 are valid. For any fixed ordering of , we denote by the size of . It follows that in distribution, where is partitioned such that is the th block.

The proof follows from the Taylor expansion applied to as in Charkhi and Claeskens (2018), that is , . The asymptotic distribution of the estimators is immediate using the multivariate central limit theorem .

9.2.2 Proof of Proposition 1

By Lemma 3, there is a joint convergence of estimators from different models. Geometrical regions can be defined by pairwise comparisons of the values. Therefore, for we write

We focus on the second term on the right-hand side in the first line of (9.2.2). Considering the model with a full set of parameters and by condition from Section 9.1, we have . We thus obtain and with replaced with . On the other hand, it follows that

| (21) |

| (22) |

Since we used maximum likelihood to estimate , the first term on the right-hand side of (22) is . Similarly the second term is also 0 which is a consequence of algebraic derivations in the SM. Moreover, does not include the random effect. Since , the convergence in probability of , to , follows from the continuous mapping theorem, and the rate was proven in Theorem 2.3 of Kubokawa (2011). Combining results of (9.2.2), (21) and (22), it follows that

| (23) |

where , as defined in Section 3. Furthermore, observe that is equivalent to . On the other hand, applying Lemma 3 and the reasoning above we have a joint convergence of to , that is, converges to a scaled, chi-square distribution, where is distributed according to a multivariate normal distribution, and stands for . As a result, the difference between two conditional likelihoods corresponds to the difference between these two chi-square random variables, and can be written using a summation sign. We use these sums to define the selection region , and by continuous mapping theorem we have .

We concentrate now on the post-cAIC CI for a mixed parameter . Since is not subject to the selection process, no geometrical restrictions are imposed on the support of the asymptotic normal distribution of random effects. Hence, to construct we need to enlarge the dimensionality of to account for random effects, that is . We have and the first term on the right hand side converges to a normally distributed random variable. Denote and consider the selection of model :

| (24) | |||

where the second line is a consequence of .

9.2.3 Proof of Proposition 2

Similarly as for , we calculate the set with constraints by pairwise comparisons of the values. Therefore we slightly rewrite the expression in (23). Consider , . It follows that which implies . The region in Proposition 2 (I) is defined using the extended selection matrix and an analogous analysis as in (24). Regarding Proposition 2 (II), observe that

| (25) |

where is a diagonal matrix with blocks and corresponding to models and . is a diagonal matrix with the same structure as with blocks , . Using Lemma 3 and a continuous mapping theorem, equation (25) equals asymptotically .

To obtain a selection region for a mixed parameter, denote by a diagonal matrix with two blocks, that is

| (26) |

Finally, we need to account for the lack of orthogonality multiplying by which leads to .

9.2.4 Proof of Lemma 2

The result follows from a uniform version of the Lindeberg-Feller central limit theorem and the continuous mapping theorem demonstrated by Kasy (2018) for a general vector and applied by Charkhi and Claeskens (2018) to a likelihood based model. The same arguments outlined in the latter are valid within our settings with misspecified models.

9.2.5 Proof of Proposition 3

The proof of Proposition 3 proceeds along identical steps as the proof of Proposition 4 in Charkhi and Claeskens (2018) changing the types of likelihoods and parameters of interest. Consider and ,where as defined in Proposition 2. It follows that

| (27) |

If we combine equation (24) and Lemma 2, it follows that the difference between the expression in equation (27) and

converges to 0, as stated in equation (19).

10 Supplementary material

This section contains additional theoretical derivations and numerical results. Specifically, in Section 10.1 and Section 10.2 we present spelled-out formulas of the mean squared error and the cAIC of Kubokawa (2011). The selection properties of cAIC are presented in Section 10.3. Afterwards, we present more numerical results of the simulations in Section 10.4 and additional details on the data example in Section 10.5. Finally in Section 10.6 we provide an extended list of assumptions and further technical proofs. To facilitate the readability of additional results, all tables are included at the end of this document.

10.1 MSE of mixed parameter

In this section we present explicitly the constituents of matrices and . The former follows immediately if we rewrite the mixed model equations in (5) using the strategy of Gilmour et al. (1995).

Regarding , we have:

where . The direct calculation under linear mixed models (LMM) can be found in Gumedze and Dunne (2011).

On the other hand, the first order MSE estimator for a mixed parameter is given by

where

with . In the small area estimation (SAE) literature, this estimator is called first-order correct, because . In addition, accounts for the variability of once is known, and for the variability arising from the estimation of . An analytical second-order correct estimator is given by

| (28) |

where with denoting the asymptotic covariance matrix, and .

10.2 cAIC of Kubokawa (2011)

Before spelling out the exact form of cAIC, we define the derivatives with respect to and differential operators with respect to

| (29) |

where may denote a scalar, a vector or a matrix. In addition, the th element of and th of are and . cAIC of Kubokawa (2011) defined in (10) includes a correction term . We have

| (30) |

where , are defined in Section 9.1 and .

10.3 Selection properties of cAIC

10.3.1 Nested models

In Figure 1 we presented the allowable domains for random variables , and using the restrictions imposed by the cAIC selection. These figures were plotted based on our simulated dataset with , , , , and . Under this model, the expression to estimate in equation (30) is substantially simplified and spelled out in Kubokawa (2011). We estimated using empirical versions of and defined in Section 2, and we obtained (the numbers are rounded to 3 digits)

This exemplary setting was chosen in a subjective way, and other choices are possible too. Table 4 displays estimated values of , and cAIC for the models from sets defined above and defined in Section 4. Figure 1 depicts geometrical regions which restrict the domains of , and . The regions are defined by the appropriate equations from Section 3 applied to the selection between models , and defined therein. Once , the exact sets of inequalities was derived in Section 3. In addition, it was depicted in panel (1) of Figure 1. If , we have

which is presented in panel (2) of Figure 1. Finally, for , we have

which is illustrated in panel (3) of Figure 1.

Figure 5 shows the partition of 3-dimensional space composed of , and . In the remaining three panels, we provide the partition of the space made by two of selected models. The purpose of Figure 5 is to show that the restrictions partition the 3-dimensional space and that there is no overlap. Of course, in practice we select only one model which would correspond to only one of these regions.

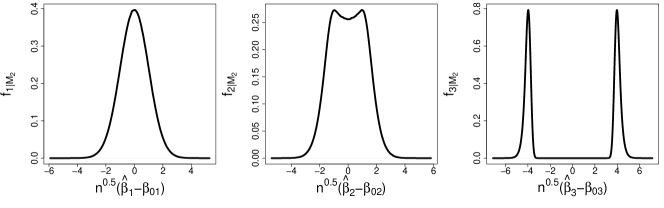

Finally, we illustrate the effect of the selection on the limiting densities. Figure 6 depicts post-selection densities of , and assuming that we select model with , whereas the true model is with (see Figure 3 in Charkhi and Claeskens, 2018, which depicts AIC post-selection densities). We can immediately notice several features. First of all, the asymptotic density of does not seem to be affected, which is plausible since the true model includes . Furthermore, seems to be affected only slightly in the centre of its density. In contrast, the post-selection density of is heavily influenced by the cAIC selection procedure – the density is bimodal with much larger high quantiles than in case of the normal distribution presented in the left panel of Figure 6. This clearly shows that the application of standard quantiles might lead to wrong conclusions, for example while constructing confidence intervals or carrying out tests.

10.3.2 General models

The choice of is of paramount importance – it affects the distribution of all parameters, even those which are common to all models. We follow up with the example in Section 10.3.2. In particular, we consider with , , as in the framework of the nested models, and (see Table 4 for specific values of estimated , and cAIC). We derive a set of inequalities which impose the restrictions on the domain of random variables once , or (the inequalities under were given in Section 10.3.2). If , the allowable domain is presented in panel (2) of Figure 2 which was constructed using the following set of equations

For , we have

presented in panel (3) of Figure 2. Finally, if our selection process chooses , it follows that

which is presented in panel (4) of Figure 2.

10.4 Additional results of our simulation study

In this section we provide the simulation results obtained for two extended selection matrices and , i.e. when the first three (respectively four) covariates are included in all models. The simulation setting is the same as described in Section 6. We consider three model sets. Selection matrix correspond to a model set in which some models exclude truly nonzero covariates. In contrast, describes a model set in which all models are forced to include truly nonzero covariates, whereas corresponds to a set in which we force all models to include truly nonzero parameters, but also an irrelevant covariate . Before presenting additional simulations, we describe a practical procedure to obtain post-selected confidence intervals in a form of an algorithm:

-

1.

In a numerical study, generate a suitable dataset to fit NERM.

-

2.

Define the initial set of candidate models .

-

3.

Fit the model to the data and obtain consistent estimators , and using maximum likelihood (or restricted maximum likelihood for and ).

-

4.

Estimate cAIC for all models in and select model with the smallest value of the information criterion.

-

5.

Calculate matrices , and which are the empirical counterparts of the matrices , and in the model with all parameters.

-

6.

Retrieve matrices and , which are submatrices of and , respectively, corresponding to model .

-

7.

Calculate quadratic constrains that define selection regions for the set of general models in Section 4.

-

8.

Using for instance an R package tmg, select Monte Carlo samples from a truncated, multivariate normal distribution such that and , .

-

9.

Retrieve high quantiles and from the empirical post-cAIC distributions of and , that is

-

10.

Construct post-cAIC confidence intervals for and , .

It might be quite difficult to find starting values to sample from -dimensional truncated multivariate distribution which is necessary to construct post-cAIC intervals for mixed parameters. We suggest thus selecting them randomly. In addition, since the constraints are imposed only on the asymptotic distribution of the fixed effects, it seems to be more efficient to first sample from -dimensional truncated distribution and afterwards from -dimensional multivariate normal to mimic the asymptotic distribution of the random effects. The former serves in the construction of the post-cAIC intervals for fixed effects. These are not subject to restrictions because they are not involved in the selection procedure. Then we merge them into a matrix with the first columns from the truncated normal distribution and the next columns from the multivariate normal distribution. The aforementioned procedure is valid for all contexts we considered in Sections 3, 4 and 5, that is, when assuming nested models, a general set of models and for misspecified models.

We turn to the additional simulation results. Tables 5, 6 and 7 present coverage probabilities (CP) and lengths (L) for post-cAIC (p.-cAIC) and naive (N) confidence intervals for the components of fixed parameters within three different model sets which correspond to selection matrices , , and . Table 5 completes the results in Table Table 1 under . The results for and resemble those we found for and respectively. In this case, covariate is relevant, i.e. truly nonzero, but not included in all models. Regarding Table 6 it is remarkable that although all truly nonzero covariates are included in each model, the naive CI fails to provide a good coverage not only for and , but also for . In contrast, when the irrelevant covariate is always included, Table 7 shows that the naive CI fails mainly for which is truly zero. In sum, while the post-cAIC intervals lead to a close to nominal coverage under all settings, the undercoverage of the naive method is the most striking feature in the tables. Tables 8, 9 and 10 present coverage probabilities and lengths of CI for linear combinations of the components of fixed parameters under the same three selection matrices , , and . The performance of post-cAIC intervals is better overall than the one of the naive intervals except for the small sample sizes. Tables 11 and 12 show coverage probabilities and lengths for post-cAIC (p.-cAIC), post-OBSP (p.-OBSP) and naive intervals constructed using the first-order (N1) and the second-order (N2) correct MSE estimators for a mixed parameter under two different selection matrices and . We can draw the same conclusions as in case of Table 3.

10.5 Post-cAIC inference with income data from Galicia

In this section, we provide additional details about the post-cAIC inference applied to study the average household income in counties of Galicia. First, we focus on the estimation of the parameters of interest. Second, we complete the model selection analysis.

In Section 7, we calculate the EBLUP using the survey estimates of covariate means and the means of transformed household income. The SSHG does include the official estimates of total and mean at the county level, but we retrieved them using the standard formulas:

| (31) |

where refers to the estimated county size , to the sample in county and to the sample weight.

In Section 7 we admitted not to having used all covariates available form the SSHG. On the basis of the previous, related studies (Boubeta et al., 2016; Reluga et al., 2021), we selected a set of 16 covariates which included those describing characteristics of the household and a member of this household who was considered as a main person. We analysed five binary variables describing the type of the household: household with 1 person (Typ1), household with more than one person (Typ2), household with a couple with children (Typ3), household with a couple without children (Typ4) and household with a single parent (Typ5). Furthermore we considered variables regarding the status of the property: without mortgage (Ten1) and with mortgage (Ten2), and the difficulties of the household at the end of the month: some difficulties (Dif2) and a lot of difficulties (Dif3). When it comes to the covariates describing the main person, we analysed a variable indicating the place of birth: Galicia (Birth1) and Spain except for Galicia (Birth2), and the eduction: primary (Edu1) and secondary (Edu2). We have also analysed a covariate indicating if the size of the municipality was smaller than ten thousands inhabitants (Size), a biological gender (Sex) as well as age: less than forty four years old (Age1) and between forty five and sixty four years old (Age2).

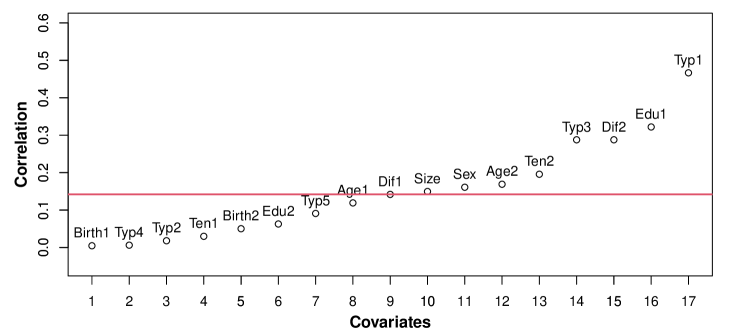

Figure 7 shows the Spearman’s correlation coefficients between transformed income and covariates. We can see that the correlation between the transformed income and variables Typ1, Edu1, Dif2 and Typ3 is the strongest. We thus included them into each model. After that we inserted to the final set of models only those covariates with the correlation coefficients higher than the median value. We ended up with the set of eight variables and models. Table 13 presents the inclusion of covariates into different models, whereas the selection criteria are outlined in Table 14. In the left part of Table 15 we can see the descriptive statistics of the lengths of the post-cAIC, post-OBSP and naive intervals for a mixed parameter in the left. The descriptive statistics for the regression-synthetic estimates are presented in the right part of Table 15.

10.6 Additional assumptions

The derivation of the extended cAIC of Kubokawa (2011) as well as the first- and second-order correct MSE estimators requires some additional regularity conditions. Let be the eigenvalues of , and , , the eigenvalues of , and defined in (29), , ordered such that , , . Moreover we assume

-

R.1

Rate of convergence: , , , i.e., and are of the same asymptotic order.

-

R.2

, , and , contain only finite values.

-

R.3

Covariance matrices and have a linear structure with respect to .

-

R.4

with for .

-

R.5

for and .

-

R.6

satisfies: , and for any .

-

R.7

can be expanded as , where , and .

-

R.8

and satisfy that , and , where , .

10.7 Additional derivations and proofs

First, we provide a proof of Lemma 1. Second, we present two algebraic properties.

10.7.1 Proof of Lemma 1

To prove the stated overselection property of cAIC, we proceed along similar steps as in the proof of Lemma 1 in Charkhi and Claeskens (2018). Let be the smallest true model. For all it holds

where the last line follows from

as well as and .

10.7.2 Algebraic derivations

The purpose of this section is to show the equivalence between the marginal and the conditional fixed parameters, that is . Recall that is the estimated EBLUE defined as a solution of minimisation of equation 2, whereas is an empirical counterpart of derived from the equation for below equation (9.2.2). In addition, we have , and define , , , , . Recall that is EBLUP, which might be estimated using a two-stage procedure or the extended likelihood. We make use of Properties 1 and 2 to obtain the equivalence between and .

Property 1

For matrices , and for non-singular matrices , , Rao (1973) showed that

| (32) |

Property 2

Property 2 is left without proof, because it only consists of simple but tedious algebraic transformations. In what follows, we show the equivalence between and . We have

where we used Property 2 in the first equation and Property 1 in the last equation. On the other hand

The desired result follows applying the third line of Property 2 and replacing , and with , and .

References

- Akaike (1973) Akaike, H. (1973) Information theory and an extension of the maximum likelihood principle. In Proc. 2nd Int. Symp. Info. Theory, Tsahkadsor, Armenia, USSR, Septemebr 2-8, 1971, 267–281. B.Petrov & F.Cski, eds. Budapest: Akadémiai Kiadó.

- Bachoc et al. (2019) Bachoc, F., Leeb, H. and Pötscher, B. M. (2019) Valid confidence intervals for post-model-selection predictors. Ann. Statist., 47, 1475–1504.

- Belloni et al. (2015) Belloni, A., Chernozhukov, V. and Kato, K. (2015) Uniform post-selection inference for least absolute deviation regression and other z-estimation problems. Biometrika, 102, 77–94.

- Berk et al. (2013) Berk, R., Brown, L., Buja, A., Zhang, K. and Zhao, L. (2013) Valid post-selection inference. Ann. Statist., 41, 802–837.

- Bolker et al. (2009) Bolker, B. M., Brooks, M. E., Clark, C. J., Geange, S. W., Poulsen, J. R., Stevens, M. H. H. and White, J.-S. S. (2009) Generalized linear mixed models: a practical guide for ecology and evolution. Trends Ecol. Evol., 24, 127–135.

- Boubeta et al. (2016) Boubeta, M., Lombardía, M. J. and Morales, D. (2016) Empirical best prediction under area-level poisson mixed models. Test, 25, 548–569.

- Charkhi and Claeskens (2018) Charkhi, A. and Claeskens, G. (2018) Asymptotic post-selection inference for the Akaike information criterion. Biometrika, 105, 645–664.

- Cunen et al. (2020) Cunen, C., Walløe, L. and Hjort, N. L. (2020) Focused model selection for linear mixed models with an application to whale ecology. Ann. Appl. Stat., 14, 872–904.

- Fay and Herriot (1979) Fay, R. E. and Herriot, R. A. (1979) Estimates of income for small places: An application of James-Stein procedures to census data. J. Am. Statist. Assoc., 74, 269–277.

- Ferrari and Yang (2015) Ferrari, D. and Yang, Y. (2015) Confidence sets for model selection by F-testing. Stat. Sin., 25, 1637–1658.

- Francq et al. (2019) Francq, B. G., Lin, D. and Hoyer, W. (2019) Confidence, prediction, and tolerance in linear mixed models. Stat. Med., 38, 5603–5622.

- Gallant and White (1988) Gallant, A. and White, H. (1988) A Unified Theory of Estimation and Inference for Nonlinear Dynamic Models. Wiley–Blackwell, New Jersey.

- Gilmour et al. (1995) Gilmour, A. R., Thompson, R. and Cullis, B. R. (1995) Average information REML: an efficient algorithm for variance parameter estimation in linear mixed models. Biometrics, 51, 1440–1450.

- Greven and Kneib (2010) Greven, S. and Kneib, T. (2010) On the behaviour of marginal and conditional AIC in linear mixed models. Biometrika, 97, 773–789.

- Gumedze and Dunne (2011) Gumedze, F. and Dunne, T. (2011) Parameter estimation and inference in the linear mixed model. Linear Algebra Appl., 435, 1920–1944.

- Harville (1977) Harville, D. A. (1977) Maximum likelihood approaches to variance component estimation and to related problems. J. Am. Statist. Assoc., 72, 320–338.

- Henderson (1950) Henderson, C. R. (1950) Estimation of genetic parameters. Ann. Math. Statist., 21, 226–252.

- Henderson (1975) — (1975) Best linear unbiased estimation and prediction under a selection model. Biometrics, 31, 423–447.

- Hjort and Claeskens (2003) Hjort, N. L. and Claeskens, G. (2003) Frequentist model average estimators. J. Am. Statist. Assoc., 98, 879–899.

- Hodges and Sargent (2001) Hodges, J. S. and Sargent, D. J. (2001) Counting degrees of freedom in hierarchical and other richly-parameterised models. Biometrika, 88, 367–379.

- Jiang (2007) Jiang, J. (2007) Linear and generalized linear mixed models and their applications. Springer, New York.

- Kasy (2018) Kasy, M. (2018) Uniformity and the delta method. J. Econom. Methods, 8, 1–19.

- Kawakubo and Kubokawa (2014) Kawakubo, Y. and Kubokawa, T. (2014) Modified conditional AIC in linear mixed models. J. Multiv. Anal., 129, 44–56.

- Kubokawa (2011) Kubokawa, T. (2011) Conditional and unconditional methods for selecting variables in linear mixed models. J. Multiv. Anal., 102, 641–660.

- Laird and Ware (1982) Laird, N. M. and Ware, J. H. (1982) Random-effects models for longitudinal data. Biometrics, 38, 963–974.

- Lee et al. (2016) Lee, J. D., Sun, D. L., Sun, Y. and Taylor, J. E. (2016) Exact post-selection inference, with application to the lasso. Ann. Statist., 44, 907–927.

- Leeb and Pötscher (2003) Leeb, H. and Pötscher, B. M. (2003) The finite-sample distribution of post-model-selection estimators and uniform versus nonuniform approximations. Econ. Theory, 19, 100–142.

- Leeb and Pötscher (2006) — (2006) Can one estimate the conditional distribution of post-model-selection estimators? Ann. Statist., 34, 2554–2591.

- Leeb and Pötscher (2008) — (2008) Can one estimate the unconditional distribution of post-model-selection estimators? Econ. Theory, 24, 338–376.

- Liang et al. (2008) Liang, H., Wu, H. and Zou, G. (2008) A note on conditional AIC for linear mixed-effects models. Biometrika, 95, 773–778.

- Lombardía et al. (2017) Lombardía, M. J., López-Vizcaíno, E. and Rueda, C. (2017) Mixed generalized Akaike information criterion for small area models. J. R. Statist. Soc. A, 180, 1229–1252.

- Marhuenda et al. (2017) Marhuenda, Y., Molina, I., Morales, D. and Rao, J. (2017) Poverty mapping in small areas under a twofold nested error regression model. J. R. Statist. Soc. A, 180, 1111–1136.

- McCulloch and Neuhaus (2011) McCulloch, C. E. and Neuhaus, J. M. (2011) Misspecifying the shape of a random effects distribution: why getting it wrong may not matter. Stat. Sci, 26, 388–402.

- Morales et al. (2021) Morales, D., Esteban Lefler, M., Perez, A. and Hobza, T. (2021) A Course on Small Area Estimation and Mixed Models: Methods, Theory and Applications in R. Springer.

- Müller et al. (2013) Müller, S., Scealy, J. L. and Welsh, A. H. (2013) Model selection in linear mixed models. Stat. Sci., 28, 135–167.

- Rao (1973) Rao, C. R. (1973) Linear statistical inference and its applications. Wiley New York.

- Rao and Molina (2015) Rao, J. N. K. and Molina, I. (2015) Small area estimation. John Wiley & Sons.

- Reluga et al. (2021) Reluga, K., Lombardía, M. J. and Sperlich, S. A. (2021) Simultaneous inference for linear mixed model parameters with an application to small area estimation. arXiv:1903.02774.

- Srivastava and Kubokawa (2010) Srivastava, M. S. and Kubokawa, T. (2010) Conditional information criteria for selecting variables in linear mixed models. J. Multiv. Anal., 101, 1970–1980.

- Sugasawa et al. (2019) Sugasawa, S., Kawakubo, Y. and Datta, G. S. (2019) Observed best selective prediction in small area estimation. J. Multiv. Anal., 173, 383–392.

- Tibshirani et al. (2018) Tibshirani, R. J., Rinaldo, A., Tibshirani, R. and Wasserman, L. (2018) Uniform asymptotic inference and the bootstrap after model selection. Ann. Statist., 46, 1255–1287.

- Tibshirani et al. (2016) Tibshirani, R. J., Taylor, J., Lockhart, R. and Tibshirani, R. (2016) Exact post-selection inference for sequential regression procedures. J. Am. Statist. Assoc., 111, 600–620.

- Vaida and Blanchard (2005) Vaida, F. and Blanchard, S. (2005) Conditional Akaike information for mixed-effects models. Biometrika, 92, 351–370.

- Verbeke and Molenberghs (2000) Verbeke, G. and Molenberghs, G. (2000) Linear Mixed Models for Longitudinal Data. Springer.

- Vuong (1989) Vuong, Q. H. (1989) Likelihood ratio tests for model selection and non-nested hypotheses. Econometrica, 57, 307–333.

- White (1994) White, H. (1994) Estimation, Inference and Specification Analysis. Econometric Society Monographs. Cambridge University Press.

- Woodroofe (1982) Woodroofe, M. (1982) On model selection and the arc sine laws. Ann. Statist., 10, 1182–1194.

- You et al. (2016) You, C., Müller, S. and Ormerod, J. T. (2016) On generalized degrees of freedom with application in linear mixed models selection. Stat. Comput., 26, 199–210.

Model 24.386 25.449 26.450 25.369 cAIC 429.245 430.323 431.334 430.236

S Meth. CP (L) CP (L) CP (L) CP (L) CP (L) CP (L) S1 p.-aAIC 94.9 (0.500) 94.1 (0.401) 94.6 (0.270) 95.2 (0.229) 93.5 (0.262) 94.1 (0.179) 98.7 (0.819) 98.9 (0.649) 99.9 (0.441) 99.6 (0.384) 99.3 (0.369) 99.6 (0.245) 87.4 (0.742) 97.1 (0.570) 94.3 (0.388) 92.2 (0.310) 92.2 (0.318) 88.3 (0.217) N 94.6 (0.487) 93.3 (0.389) 94.3 (0.265) 94.4 (0.222) 92.6 (0.258) 93.9 (0.176) 93.2 (0.517) 93.0 (0.366) 94.0 (0.252) 93.8 (0.207) 93.6 (0.244) 94.2 (0.173) 70.0 (0.577) 72.7 (0.361) 70.2 (0.264) 66.5 (0.220) 71.5 (0.249) 67.2 (0.178) S2 p.-cAIC 94.0 (0.495) 94.8 (0.399) 94.2 (0.270) 95.5 (0.228) 93.4 (0.263) 94.1 (0.179) 99.1 (0.854) 99.6 (0.691) 99.7 (0.466) 99.8 (0.402) 99.6 (0.400) 99.5 (0.245) 89.5 (0.759) 97.5 (0.616) 95.1 (0.419) 92.6 (0.321) 93.7 (0.341) 86.2 (0.214) N 93.6 (0.483) 94.2 (0.384) 93.3 (0.262) 94.1 (0.220) 92.6 (0.257) 94.0 (0.175) 93.9 (0.510) 92.5 (0.361) 94.1 (0.249) 93.1 (0.205) 93.5 (0.243) 94.1 (0.173) 70.4 (0.571) 74.3 (0.354) 72.0 (0.261) 69.5 (0.217) 69.1 (0.248) 67.4 (0.177)

S Meth. CP (L) CP (L) CP (L) CP (L) CP (L) CP (L) S1 p.-cAIC 92.9 (1.131) 94.1 (0.786) 94.3 (0.561) 94.1 (0.454) 94.7 (0.782) 94.0 (0.744) 94.2 (0.499) 93.5 (0.396) 94.8 (0.269) 95.5 (0.225) 93.3 (0.263) 94.2 (0.177) 94.3 (0.526) 93.4 (0.385) 95.2 (0.259) 95.3 (0.211) 94.4 (0.253) 93.7 (0.333) 92.2 (0.758) 94.5 (0.471) 93.4 (0.349) 92.7 (0.292) 93.7 (0.333) 93.9 (0.339) 91.3 (0.746) 93.1 (0.497) 93.6 (0.353) 92.3 (0.290) 93.9 (0.339) 95.2 (0.237) N 92.6 (1.103) 94.1 (0.779) 94.3 (0.555) 94.1 (0.453) 93.5 (0.745) 93.4 (0.727) 93.9 (0.488) 92.7 (0.388) 94.6 (0.265) 95.1 (0.222) 92.1 (0.258) 93.9 (0.176) 93.6 (0.517) 91.6 (0.365) 94.4 (0.252) 94.4 (0.207) 93.7 (0.244) 69.8 (0.249) 69.4 (0.578) 71.9 (0.360) 68.5 (0.265) 67.5 (0.220) 69.8 (0.249) 67.8 (0.256) 66.4 (0.569) 72.5 (0.377) 69.8 (0.267) 68.9 (0.218) 67.8 (0.256) 67.1 (0.175) S2 p.-cAIC 92.2 (0.844) 94.2 (0.598) 94.1 (0.425) 94.1 (0.346) 93.6 (0.562) 94.1 (0.532) 94.4 (0.493) 94.2 (0.392) 94.9 (0.267) 95.2 (0.222) 93.6 (0.263) 94.6 (0.177) 93.2 (0.519) 93.8 (0.380) 94.9 (0.256) 93.3 (0.209) 95.0 (0.252) 93.7 (0.332) 92.5 (0.751) 96.4 (0.466) 93.5 (0.345) 92.6 (0.290) 93.7 (0.332) 93.5 (0.341) 88.7 (0.739) 93.0 (0.495) 92.2 (0.352) 91.0 (0.288) 93.5 (0.341) 95.1 (0.237) N 92.2 (0.839) 94.2 (0.598) 93.9 (0.425) 94.3 (0.346) 92.9 (0.552) 94.0 (0.527) 94.0 (0.483) 94.0 (0.384) 94.5 (0.262) 95.0 (0.219) 92.7 (0.257) 94.5 (0.175) 92.8 (0.510) 91.6 (0.361) 94.2 (0.249) 92.7 (0.205) 93.8 (0.243) 68.2 (0.248) 69.9 (0.570) 74.6 (0.354) 68.5 (0.260) 67.4 (0.217) 68.2 (0.248) 66.7 (0.255) 65.5 (0.561) 72.0 (0.373) 67.8 (0.264) 66.7 (0.215) 66.7 (0.255) 66.7 (0.175)

S Meth. CP (L) CP (L) CP (L) CP (L) CP (L) CP (L) S1 p.-cAIC 92.4 (1.118) 94.5 (0.787) 93.8 (0.559) 95.3 (0.453) 94.6 (0.780) 93.1 (0.742) 94.1 (0.496) 94.8 (0.394) 94.5 (0.268) 94.3 (0.223) 94.7 (0.261) 94.0 (0.176) 94.7 (0.521) 93.4 (0.372) 95.0 (0.255) 95.5 (0.209) 95.4 (0.247) 95.0 (0.175) 94.8 (0.586) 95.1 (0.364) 94.6 (0.268) 93.2 (0.223) 95.3 (0.250) 94.7 (0.179) 91.4 (0.754) 93.2 (0.502) 93.9 (0.354) 94.3 (0.288) 94.4 (0.340) 94.5 (0.236) N 92.0 (1.106) 94.5 (0.781) 93.7 (0.554) 95.2 (0.452) 94.1 (0.746) 92.7 (0.726) 94.1 (0.491) 94.7 (0.392) 94.3 (0.266) 94.3 (0.222) 94.4 (0.259) 94.0 (0.176) 94.6 (0.520) 93.1 (0.369) 94.8 (0.254) 95.5 (0.208) 95.2 (0.245) 94.9 (0.173) 94.6 (0.581) 95.0 (0.363) 94.4 (0.266) 93.1 (0.220) 95.2 (0.249) 94.6 (0.178) 69.1 (0.573) 71.4 (0.380) 71.3 (0.268) 70.5 (0.218) 70.6 (0.257) 70.2 (0.176) S2 p.-cAIC 92.7 (0.852) 94.8 (0.597) 93.3 (0.426) 95.3 (0.346) 94.4 (0.561) 94.4 (0.561) 93.7 (0.492) 95.8 (0.388) 94.9 (0.266) 93.7 (0.221) 94.1 (0.260) 94.1 (0.260) 94.7 (0.515) 92.7 (0.367) 94.6 (0.252) 94.7 (0.207) 95.7 (0.246) 95.7 (0.246) 95.2 (0.579) 94.9 (0.356) 94.2 (0.263) 93.6 (0.220) 95.7 (0.249) 95.7 (0.249) 91.0 (0.754) 93.6 (0.499) 93.3 (0.352) 93.8 (0.286) 94.3 (0.342) 94.3 (0.342) N 92.6 (0.850) 95.0 (0.597) 93.3 (0.426) 95.3 (0.346) 94.0 (0.552) 94.0 (0.552) 93.5 (0.486) 95.8 (0.387) 94.8 (0.263) 93.7 (0.220) 94.0 (0.258) 94.0 (0.258) 94.5 (0.514) 92.4 (0.363) 94.0 (0.250) 94.4 (0.205) 96.0 (0.244) 95.6 (0.244) 95.1 (0.574) 94.9 (0.356) 93.9 (0.261) 93.4 (0.217) 95.3 (0.248) 95.3 (0.248) 69.7 (0.565) 73.5 (0.375) 71.0 (0.265) 70.7 (0.216) 70.1 (0.256) 70.2 (0.256)

S Meth. CP (L) CP (L) CP (L) CP (L) CP (L) CP (L) S1 p.-cAIC 91.5 (1.152) 94.3 (1.018) 97.7 (0.699) 97.2 (0.515) 96.6 (0.891) 93.9 (0.751) 91.4 (1.305) 97.9 (1.118) 94.0 (0.572) 96.3 (0.500) 96.2 (0.870) 94.5 (0.793) 97.8 (1.571) 96.2 (0.967) 97.0 (0.690) 95.7 (0.464) 97.1 (0.904) 96.0 (0.864) 95.3 (1.374) 95.8 (0.998) 96.7 (0.711) 97.1 (0.572) 96.5 (0.891) 94.5 (0.786) N 91.8 (1.171) 90.7 (0.886) 94.7 (0.574) 96.0 (0.469) 92.9 (0.765) 93.6 (0.731) 88.9 (1.211) 93.7 (0.868) 94.5 (0.577) 95.1 (0.470) 93.3 (0.752) 93.3 (0.728) 92.7 (1.179) 93.4 (0.835) 93.9 (0.572) 95.6 (0.459) 93.4 (0.750) 93.6 (0.737) 92.0 (1.159) 92.3 (0.844) 93.4 (0.594) 94.1 (0.487) 93.5 (0.758) 93.3 (0.731) S2 p.-cAIC 96.1 (1.071) 97.5 (0.723) 97.9 (0.584) 96.9 (0.389) 96.3 (0.721) 94.4 (0.548) 96.1 (1.329) 98.0 (0.904) 99.2 (0.568) 96.9 (0.451) 97.6 (0.728) 93.7 (0.538) 98.3 (1.334) 97.5 (0.785) 95.2 (0.618) 98.7 (0.495) 95.1 (0.625) 96.2 (0.585) 95.2 (1.117) 97.0 (0.844) 97.0 (0.597) 97.6 (0.485) 96.0 (0.661) 94.5 (0.560) N 93.6 (0.934) 94.9 (0.623) 92.4 (0.476) 95.7 (0.366) 91.8 (0.581) 93.5 (0.529) 86.4 (0.946) 89.5 (0.675) 95.7 (0.453) 94.0 (0.393) 93.4 (0.572) 93.5 (0.529) 92.4 (0.937) 94.7 (0.670) 90.1 (0.493) 96.4 (0.379) 93.3 (0.569) 94.1 (0.535) 91.0 (0.912) 92.3 (0.677) 92.9 (0.477) 93.9 (0.390) 93.1 (0.571) 93.5 (0.532)