Asynchronous and Distributed Data Augmentation for Massive Data Settings

Abstract

Data augmentation (DA) algorithms are widely used for Bayesian inference due to their simplicity. In massive data settings, however, DA algorithms are prohibitively slow because they pass through the full data in any iteration, imposing serious restrictions on their usage despite the advantages. Addressing this problem, we develop a framework for extending any DA that exploits asynchronous and distributed computing. The extended DA algorithm is indexed by a parameter and is called Asynchronous and Distributed (AD) DA with the original DA as its parent. Any ADDA starts by dividing the full data into smaller disjoint subsets and storing them on processes, which could be machines or processors. Every iteration of ADDA augments only an -fraction of the data subsets with some positive probability and leaves the remaining -fraction of the augmented data unchanged. The parameter draws are obtained using the -fraction of new and -fraction of old augmented data. For many choices of and , the fractional updates of ADDA lead to a significant speed-up over the parent DA in massive data settings, and it reduces to the distributed version of its parent DA when . We show that the ADDA Markov chain is Harris ergodic with the desired stationary distribution under mild conditions on the parent DA algorithm. We demonstrate the numerical advantages of the ADDA in three representative examples corresponding to different kinds of massive data settings encountered in applications. In all these examples, our DA generalization is significantly faster than its parent DA algorithm for all the choices of and . We also establish geometric ergodicity of the ADDA Markov chain for all three examples, which in turn yields asymptotically valid standard errors for estimates of desired posterior quantities.

1 Introduction

DA algorithms are a popular choice for Bayesian inference using Markov chain Monte Carlo. A variety of DA algorithms have been developed over the years for sampling-based posterior inference in a large class of hierarchical Bayesian models. The development of DA algorithms still remains popular because they are simple, easily implemented, and numerically stable; however, DA algorithms are very slow in massive data applications because they pass through the full data in every iteration. Taking advantage of asynchronous and distributed computations, we propose the ADDA as a scalable generalization of any DA-type algorithm. ADDA is useful for fitting flexible Bayesian models to arbitrarily large data sets, retains the convergence properties of its parent DA, and reduces to the parent DA under certain assumptions.

Consider the setup of DA algorithms. In a typical DA application, we augment “missing data” to the observed data and obtain the “augmented data” model, where the term missing data is interpreted broadly to include any additional parameters or latent variables. Under the augmented data model, the imputation (I) step draws the missing data from their conditional distribution given the observed data and the current parameter value. The I step is followed by the prediction (P) step that draws the “original” parameter from its conditional distribution given the augmented data. This completes one cycle of a DA algorithm. Starting from some initial value of the parameter, the I and P steps are repeated sequentially to obtain a Markov chain for the missing data and parameter. The marginal parameter samples from the DA algorithm form a Markov chain with the posterior distribution of parameters given the observed data as its stationary distribution [16, 42].

The convergence of the DA Markov chain to its stationary distribution can be extremely slow. This problem has been addressed by developing generalizations of many DA algorithms based on missing data models indexed by a “working parameter” that is identified under the augmented data model but not under the observed data model. Parameter expanded DA chooses any working parameter, conditional DA chooses the working parameter that leads to maximum acceleration in the convergence to the stationary distribution, and marginal DA averages over values of the working parameter drawn from its prior distribution [51, 17]. All these generalizations accelerate convergence to the stationary distribution by relaxing many restrictions in the observed data model. Modern massive data settings, however, pose severe computational challenges for DA and its parameter expanded versions in that the size of the augmented missing data can be really large, resulting in a prohibitively slow I step in every iteration of the DA or its extension.

The inefficiency of DA-type algorithms in massive data settings has received significant attention. Expectation-Maximization (EM) algorithm is the deterministic version of DA and its inefficiency is due to the slow E step [14]. Cappé and Moulines [10] have addressed this issue by developing the family of online EMs that modify the E step using stochastic approximation. They compute the conditional expectation of complete data log likelihood obtained using a small fraction of the full data and the online E step increases in accuracy as greater fraction of the full data are processed. The stochastic counterparts of online EMs are the suite of Monte Carlo algorithms based on subsampling [23, 6, 12, 13, 62, 39] and stochastic gradient descent [57, 3, 8, 15, 7, 37]; see Nemeth and Fearnhead [30] for a recent overview. All these algorithms are extremely scalable, have convergence guarantees, and are broadly applicable; however, the performance of these algorithms is sensitive to the specification of tuning parameters in hierarchical Bayesian models, including subsample size, gradient step-size, and the learning rate. Their optimal performance requires proposal tuning, which is a major limitation in their use as off-the-shelf algorithms for Bayesian inference.

Distributed Bayesian inference approaches based on the divide-and-conquer technique also rely on DA and exploit its ease of implementation. A typical application involves dividing the full data into smaller subsets, obtaining parameter draws in parallel on all the subsets using a DA-type algorithm, and combining parameter draws from all the subsets. The combined parameter draws are used as a computationally efficient alternative to the draws from the true posterior distribution. A variety of algorithms have been developed over the years at an increasing level of generality and applicability [46, 27, 29, 48, 61, 60, 21, 59, 54, 33]. There are two major limitations in all these methods. First, the combined parameter draws do not provide a Markov chain with the target posterior based on the entire data as the stationary distribution, which implies that quantification of the Monte Carlo error is challenging. Second, the theoretical guarantees of these methods are based on a normal approximation of the posterior distribution as the subset sample size and the number of subsets tend to infinity. No guarantees are available about the distance between the distribution of the combined parameter draws and the target posterior distribution.

Addressing both these problems, the proposed ADDA offers an simple approach for bypassing problems due to the slow I step using asynchronous and distributed computations, but at the same time producing a single Markov chain with the target posterior as a marginal of its stationary distribution. The key observation which enables such a construction is that for many DA settings, the missing data can be partitioned into several sub-blocks such that two conditions are satisfied. First, all these sub-blocks are mutually independent given the original parameter and the observed data. Second, the conditional posterior distribution (given the original parameter) of each sub-block depends only on an exclusive subset of the observed data; see the representative examples in Sections 3.1-3.3 for greater details.

An ADDA algorithm starts by reserving computing units called processes, where , and are the number of workers and managers, respectively. The processes could be cores in a CPU, threads in a GPU, or machines in a cluster. Every implementation of ADDA divides the full data into smaller disjoint subsets, stores them on the workers, and performs the I step in parallel on the workers. The workers communicate the results of their I steps to the manager processes that are responsible for performing the P step. The managers also track progress of the algorithm by maintaining the latest copies of I step results for every worker. Let an and an be given. Then, the managers wait for all workers to return their results with probability . With the probability , the managers wait to receive the I step results from an -fraction of the workers and perform the P step using an augmented data model that depends on the -fraction of new I step results and the ()-fraction of old I step results. This sequence of I and P steps is repeated until convergence, which generalizes the classical DA-type algorithms by using as an additional working parameter. If , then we recover a distributed generalization of the parent DA algorithm.

The parameter is introduced as a theoretical device for ensuring that any ADDA algorithm produces a Markov chain. Any positive ensures that the missing data sub-block corresponding to each worker has a positive probability to be updated at every iteration. This is crucial for establishing theoretical results about the ADDA chain, including Harris ergodicity and geometric ergodicity. In practice, can be set to be a small number for faster computations.

It is important to compare and contrast the proposed ADDA algorithm with Asynchronous Gibbs sampling algorithms that have been developed in machine learning motivated by topic models. Newman et al. [31] developed the first such algorithm, which has been extended by exploiting various synchronization schemes and computer architecture [2, 25]. The only similarity between this class of algorithms and ADDA is that the data are partitioned and stored on the workers, which run the sampling algorithm locally. The manager process is absent in asynchronous Gibbs sampling because every worker draws its local set of parameters and latent variables from the local full conditional without waiting for the full Gibbs cycle to finish. This also implies that the parameter and latent variable updates do not form a Markov chain. In simple Gaussian models, this strategy produces draws from a distribution that fails to converge to the target [18].

Terenin et al. [50] fix this issue by introducing a correction step that allows a worker to accept or reject a draw with a probability based on the corresponding acceptance ratio. This additional Metropolis step increases the computational burden and the amount of information that needs to be communicated among the workers, but the authors are able to establish convergence to the desired stationary distribution under additional regularity conditions. The sequence of iterates generated by this exact algorithm still do not form a Markov chain in general, and hence one does not have access to the standard Markov chain central limit theorem (CLT) based approaches to quantify the MCMC standard error (see the discussion below). More recently, these ideas have been extended to Bayesian variable selection using Gaussian spike-and-slab priors [4]. Developing a general theoretical understanding of these asynchronous Gibbs algorithms is still an active area of research.

On the other hand, any ADDA algorithm inherits several attractive properties of its parent DA. First, being a generalization of the parent DA for a valid choice of , any ADDA is easy to implement and numerically stable. Second, ADDA is the stochastic counterpart of the distributed EM, is independent of the computer architecture, and has broad applicability [47]. Finally, while the marginal sequence of original parameter values generated by the ADDA algorithm is not a Markov chain (unlike the DA algorithm), the joint sequence of original and augmented parameter values is a Markov chain whose stationary distribution has the targeted posterior as a marginal. This facilitates a simpler theoretical analysis of the Monte Carlo error based on the familiar tools for analyzing Markov chains in sampling-based posterior inference; see Sections 3.1-3.3 below.

We now describe the structure and key contributions of this paper. The general framework for the ADDA algorithm is developed in Section 2.1, and Harris ergodicity of the resulting Markov chain is established in Theorem 2.1. We then develop ADDA extensions of three representative DA algorithms in Sections 3.1-3.3. There are two kinds of massive data settings that are encountered in modern applications. The first is the “massive setting”, where the number of observations or samples is extremely large, typically in the order of millions or larger. For this setting, we consider two illustrative examples: the Polya-Gamma DA algorithm [38] for Bayesian logistic regression and the marginal DA algorithm [51] for linear mixed-effects modeling. For both algorithms, the number of augmented parameters is equal to the number of observations, which makes the I step computationally very expensive, and provides motivation for applying the ADDA methodology. The corresponding ADDA extensions are specified in Algorithms 1 and 3. The second big data setting is the “massive setting”, where the number of variables in the dataset is extremely large. For this setting, we consider the Bayesian lasso DA algorithm [40] for high-dimensional regression, where the number of augmented parameters equals the (large) number of regression parameters . This provides another motivation for applying the ADDA methodology and the corresponding ADDA for the Bayesian lasso is presented in Algorithm 2.

We then undertake extensive simulation studies for each of the three representative examples to understand and evaluate the performance of the respective ADDA extensions depending on the number of workers and the update fraction . The two hallmarks of ADDA are distributed and asynchronous processing. Parallel processing by distributing the independent draws of the appropriate sub-blocks of the missing data to the workers obviously leads to faster computations with no adverse impact on mixing of the Markov chain [58]. The asynchronous updates, however, come with a tradeoff. Smaller values of the fraction lead to faster computations per iteration, but also slow down the mixing of the Markov chain; therefore, compared to the DA algorithm, the same number of iterations of the ADDA algorithm take much less time but provide less accurate estimates of desired posterior quantities. The idea, as demonstrated by our extensive simulations in Section 4, is that typically the computational gain is quite significant with a comparatively small loss of accuracy. For example, MovieLens ratings data analysis in Section 4.3 using logistic regression and linear mixed-effects models shows that the ADDA algorithm is anywhere between three to five times faster and only around less accurate than its parent after iterations; see Figures 9–12.

As mentioned above, the iterates generated by the ADDA algorithm form a Markov chain whose stationary distribution has the target posterior as a marginal. This potentially allows us to directly leverage standard MCMC approaches to quantify the Monte Carlo standard error of the resulting estimators of posterior quantities. All asymptotically consistent estimators of the MCMC standard error, however, rely on the existence of a Markov chain CLT. A standard method for establishing the existence of such a CLT is to show geometric ergodicity; that is, the distribution of the Markov chain converges geometrically fast to the stationary distribution as the number of iterations increase. It is well-known that establishing geometric ergodicity of statistical continuous state space Markov chains is in general very challenging [20]. The drift and minorization analysis typically needed for this purpose can be quite involved and “a matter of art”, requiring the analysis to be heavily adapted to the structure of individual Markov chains.

While geometric ergodicity has been established for the Markov chains corresponding to all the three DA algorithms considered in the paper, adapting these analyses to establish a similar result for the ADDA extensions is not feasible given the complications introduced by the asynchronous updates. The main reason is that the subset of missing data that is updated in any given iteration depends on the current parameter value, which implies that the marginal parameter process of the ADDA chain is not Markov in general. Also, establishing minorization conditions, which are integral parts of the original DA proofs, becomes very challenging. Through a fresh analysis which only uses appropriate drift conditions that are unbounded off compact sets, we establish geometric ergodicity for all the three ADDA extensions in Theorems 3.1, 3.2, 3.3. These results not only provide asymptotically valid standard errors but also assure the user that the ADDA Markov chain converges geometrically fast to its stationary distribution despite the asynchronous updates. Based on our analysis for the three representative examples, we believe that similar results should be true for other ADDA-based generalizations of geometrically ergodic DA algorithms, but such a general treatment is restricted by the aforementioned challenges in theoretical techniques for establishing geometric ergodicity. The proofs of the geometric ergodicity results are provided in a Supplementary Document. We conclude the paper with a discussion in Section 5.

2 Asynchronous and Distributed Data Augmentation (ADDA)

2.1 The General Framework

Consider the setup of a general ADDA algorithm. Assume that we have chosen an and reserved worker and manager processes. Let be the model parameter, and be the observed and missing data, be the augmented data. Let and denote the missing data and the parameter spaces, respectively. We assume that both sets are equipped with countably generated -algebras, and respective -finite measures and . Let denote the joint posterior density (with respect to ) of and , and and denote the conditional posterior densities of the missing data given the parameter, and the parameter given the augmented data, respectively. Let denote the missing data subset distributed to worker so that . We assume that are conditionally independent given so that . If the parameter can also be divided into conditionally independent blocks, one could introduce more than one manager process, but for ease of exposition we restrict ourselves to a setting with one manager process.

For an and an , a general implementation of an ADDA-type algorithm is described as follows:

-

(1)

The manager starts with some initial values (, ) at and sends to the workers. For , the manager

-

(M-a)

waits to receive only an -fraction of updated s (see below) from the workers with probability , and with probability , waits to receive all the updated s from the workers;

-

(M-b)

creates by replacing the relevant s with the newly received ;

-

(M-c)

draws from ; and

-

(M-d)

sends to all the worker processes and resets .

-

(M-a)

-

(2)

For , the worker ()

-

(W-a)

waits to receive from the manager process;

-

(W-b)

draws from ; and

-

(W-c)

sends to the manager process, resets , and goes to (W-a) if is not received from the manager before the draw is complete; otherwise, it truncates the sampling process, resets , and goes to (W-b).

-

(W-a)

The general steps for an ADDA algorithm are easily summarized into Asynchronous and Distributed (AD) I and P steps. The ADDA algorithm initializes (, ) at (, ) and the AD-I and AD-P steps in the th iteration for are as follows:

- AD-I step:

-

Each worker draws from for in parallel and sends to the manager (if the draw is finished before receiving ).

- AD-P step:

-

As soon as the manager receives the required fraction ( with probability and with probability ) of updated values from the workers, is drawn from , and sent to the workers.

Note that if the -fraction update regime is chosen, then the manager sets for the remaining -fraction. As soon as the workers receive , they stop any ongoing activity and proceed with the AD-I step for the th iteration.

One cycle of ADDA consists of AD-I step followed by AD-P step, and they are repeated sequentially to obtain the chain for the missing data and parameter. We emphasize again that at the end of iteration , with probability , only an -fraction of are replaced by the manager with new draws received from the workers, whereas the remaining ()-fraction of them haven’t changed. The AD-I and AD-P in ADDA are distributed generalizations of the I and P steps in its parent DA. If , then AD-I and AD-P steps reduce to the I and P steps of their parent DA.

ADDA inherits the simplicity and stability of its parent DA. Its implementation requires communication between the manager and worker processes that is easily implemented using software packages such as the parallel package in R. The most important advantage of ADDA is that its cycle is faster than the parent DA cycle by a factor of for every . The main reason is that the workers perform the AD-I steps in parallel on an -fraction of the full data, resulting in a -fold speed-up over the I step of parent DA. The P steps of ADDA and its parent DA are identical given the missing data, so their timings are also similar. If is sufficiently small, then ADDA offers a simple and general strategy for scaling any existing DA-type algorithm to massive data settings by choosing a sufficiently large . The next section carefully investigates crucial theoretical properties of the ADDA algorithm which guarantee that draws from the ADDA algorithm can be used to effectively approximate relevant posterior quantities.

2.2 Markov Property and Harris Ergodicity

The classical (parent) DA algorithm (that is, the ADDA with ) corresponds to a systematic scan two-block Gibbs sampler from the joint density . Furthermore, in the classical DA setting, solely depends on given and depends solely on given . This implies that solely depends on given so that the marginal process is Markov. This fact is often useful when establishing theoretical properties such as geometric ergodicity of the DA Markov chain (see below).

The ADDA can be interpreted as a hybrid Gibbs sampler. The AD-P step is a systematic scan step for sampling the parameter from its conditional posterior distribution given , but the AD-I step is a “random subset scan” step which updates a random subset of the missing data . Other hybrid versions of systematic and random scan Gibbs steps have been considered in the literature. Backlund et al. [5] consider a DA setup where the parameter is partitioned into two blocks. They construct and study a hybrid sampler that performs a systematic scan step for the entire missing data at each iteration and updates exactly one of the two parameter blocks with fixed probabilities and , respectively. A general (non-DA) setting with multiple blocks is considered in [26], where a sampler updates a single coordinate in each iteration. The choice of the block to update is made randomly based on a vector of fixed probabilities which depend on the block index that was updated in the previous iteration; therefore, this strategy subsumes the traditional systematic and random scan samplers as special cases. The ADDA is significantly different from the above strategies and updates a randomly chosen subset of the conditionally independent blocks of the missing data , while performing a systematic scan update of the entire parameter . Note also that the probabilities of choosing various relevant subsets at a given iteration can in general depend on the current value of the parameter .

A simple observation shows that process in ADDA is Markov. For an ADDA algorithm with , the knowledge of makes the entire past irrelevant for generating . Specifically, is conditionally independent of given ; therefore, the process is still Markov. It is also easily seen that both the AD-P step and the AD-I step leave invariant. This is promising but to use the ADDA iterates to approximate relevant posterior expectations and quantiles, we need to establish Harris ergodicity. The following theorem shows that the ADDA Markov chain is Harris ergodic as long as is positive, the original DA chain is Harris ergodic, and its transition kernel satisfies a mild absolute continuity condition.

Theorem 2.1.

Let denote the transition kernel of the parent DA chain which is equivalent to the ADDA chain with , and denote the joint posterior distribution of and . Assume that is absolutely continuous with respect to for every . Then, if and the parent DA chain is Harris ergodic, the ADDA chain is Harris ergodic.

The proof of the theorem is given in Supplementary Section A.1. The assumption is needed because it ensures that there is a positive probability that each worker returns an updated value at each iteration. This allows us to leverage the Harris ergodicity of the parent DA chain to establish relevant properties of the ADDA chain. If , then assumptions regarding the computer architecture and the processing power of the workers will need to be made to guarantee Harris ergodicity; for example, see Terenin et al. [50]. This can get quite messy and tricky to ensure in real-life computing. Using is an elegant and clean way of side-stepping these issues. Of course, smaller values of epsilon are preferred for faster computations.

Theorem 2.1 is a fundamental step towards understanding theoretical properties of the process in ADDA but is still far from the end. An important next step is to establish a CLT for the process in order to provide asymptotically valid standard error bounds for MCMC based approximations. As discussed before, the standard method of establishing a CLT is to establish geometric ergodicity; however, proving geometric ergodicity can be quite challenging in general. The proof of geometric ergodicity for a large majority of statistical Markov chains is not available. For Markov chains where a proof is available, it is typically based on drift and minorization conditions, which are specifically tailored for the particular chain at hand.

In the next section, we illustrate the application of ADDA on logistic regression, high-dimensional variable selection, and linear mixed-effects modeling. For the three examples, the process in the parent DA is known to be geometrically ergodic. Extension of each of these proofs to ADDA is difficult for at least one of two main reasons. First, each cycle of ADDA updates (with probability) a random -fraction of the . This random subset update significantly complicates the transition density in terms of establishing a minorization condition involved in the proof of geometric ergodicity. Second, some of the parent DA geometric ergodicity proofs focus on the marginal process , which is a Markov chain in the parent DA setting, and extend the result to the full process . This strategy fails in the ADDA setting because the process is not in general Markov. We provide results establishing geometric ergodicity for the ADDA chains in the three above-mentioned models in the next section. A key idea in the three proofs is to identify and establish geometric drift conditions, where the drift functions are unbounded off compact sets. Some of these proofs are established under weaker conditions than those required for the parent DA chains.

3 Applications

3.1 ADDA for Bayesian Logistic Regression

Consider the implementation of Pólya-Gamma DA for Bayesian logistic regression [38]. Let be the sample size, be the regression coefficients, and be the response, number of trials, covariates for sample , respectively, where , , . The hierarchical model for logistic regression is

| (1) |

The DA algorithm augments the model in (1) with Pólya-Gamma random variables specific to the samples, and cycles between the I and P steps for a large number of iterations starting from a given value of :

-

PG.1

(I step) Draw given from PG(, ) for , where PG is the Pólya-Gamma distribution.

-

PG.2

(P step) Draw given and from (, ), where , , , and is the diagonal matrix of s.

The marginal Markov chain of the draws collected in step PG.2 has the posterior distribution of in (1) as its invariant distribution [11, 56, 55].

The ADDA algorithm with Pólya-Gamma DA algorithm as its parent DA modifies step PG.1. Let and . Then, following the notation of Section 2.1, the Pólya-Gamma DA has

For many datasets, the sample size can be really large. For example, the MovieLens data analyzed in Section 4.3 has 10 million samples. Instead of updating s in every iteration, ADDA updates only an fraction of them (with probability ) and reduces to its parent DA when . The ADDA algorithm runs after we randomly split the samples into disjoint subsets and store them on worker processes. Let be the number of samples assigned to worker , be the th augmented sample on worker () and . Note that s in are rearranged to match the ordering of samples in so that .

The ADDA extension of Pólya-Gamma DA for a given and initializes (, ) at (, ) and the AD-I and AD-P steps in the th iteration are as follows:

The ADDA cycles generate the Markov chain . The following Theorem establishes the geometric ergodicity of when and its proof is in Supplementary Materials Section A.3.

Theorem 3.1.

If , the Markov chain as described in Algorithm 1 is geometrically ergodic.

The convergence analysis of the parent PG DA chain has been performed in the literature. In particular, Choi and Hobert [11] show that the parent PG DA chain is uniformly ergodic (using the marginal chain) if proper priors are used. Following this work, Wang and Roy [56] show the geometric ergodicity of the PG DA chain with flat priors. The uniform ergodicity proof for the parent DA chain in Choi and Hobert [11] for the binary and proper prior setting is based on a minorization argument on the marginal chain; however, this proof strategy fails for ADDA because the process for is not Markov. As a result, we take a different approach where we establish a geometric drift condition using a function of , which is unbounded off compact sets. Wang and Roy [56] follow a similar strategy for the proving geometric ergodicity of the parent DA chain with improper priors, but they focus on the marginal chain instead of the chain. Furthermore, the previous two works consider the parent DA chain when the response is binary, whereas Theorem 3.1 deals with the ADDA chain in a more general binomial setting.

3.2 ADDA for Bayesian High Dimensional Variable Selection

Consider Bayesian high dimensional variable selection using a Bayesian lasso shrinkage prior [40]. Let be the sample size, be the regression coefficients, be the response vector, and be the design matrix. The Bayesian lasso DA algorithm augments dimension with local shrinkage parameter (), and the hierarchical model for variable selection is

| (2) |

where is an identity matrix, is the variance of idiosyncratic error term, , and are hyper-parameters. The DA algorithm for variable selection starts with some initial values of and and cycles between the I and P steps for a large number of iterations:

-

BL.1

(I step) Draw given from Inverse-Gaussian() for .

-

BL.2

(P step) Draw given and as

(3)

The Markov chain of the draws collected in step BL.2 has the posterior distribution of in (3.2) as its invariant distribution [40, Lemma 1].

This DA is different from Pólya-Gamma DA in that the I step in BL.1 draws latent variables instead of . In high-dimensional problems, and updating in every iteration is time consuming even when is small. Following Section 2.1, the Bayesian lasso DA has

Unlike Pólya-Gamma DA, the computational bottleneck in the I step happens when is large. The ADDA algorithm starts by partitioning into disjoint subsets denoted as . The elements of and are stored on worker processes. Let , be the and elements on worker , and (). The disjoint partitioning ensures that . Note that the ’s are rearranged so that

The ADDA extension of Bayesian lasso DA, at any iteration, updates (with probability ) only an fraction of , and with probability updates all of . Clearly, the ADDA extension reduces to the parent DA when . For a given and , the ADDA extension of the Bayesian Lasso DA initializes at and the AD-I and AD-P steps in the th iteration are as follows:

-

•

given from Inverse-Gamma , where , and ; and

-

•

given from N.

Similar to the Pólya-Gamma DA extension, this ADDA cycles generate the Markov chain . The following theorem establishes the geometric ergodicity of when , and the proof is given in Supplementary Materials Section A.5.

Theorem 3.2.

If and , the Markov chain described in Algorithm 2 is geometrically ergodic.

Geometric ergodicity of a three block version of the parent DA chain was established in [22], and geometric ergodicity for the parent DA chain described in BL.1 and BL.2 above was established in [41]. Both these proofs make use of drift and minorization. In particular, [41] prove results on the marginal chain, and leverage them to establish geometric ergodicity of the parent DA chain. As mentioned previously, this route is not available to us, as the marginal is not Markov, and establishing minorization with the asynchronous updates is nontrivial. As such, similar to the Polya-Gamma ADDA setting, our proof of Theorem 3.2 is based on establishing a geometric drift condition using a drift function that is unbounded off compact sets.

3.3 ADDA for Linear Mixed-Effects Modeling

Consider the setup for linear mixed-effects models [51]. Let be the number of observations, be the number of subjects, be the response, fixed effects covariates, and random effects covariates, respectively, for subject , and be the number of fixed and random effects, be the fixed effect, and be a positive definite covariance matrix. Then, the linear mixed-effects model assumes that

| (4) |

where and are the random effect and idiosyncratic error for subject , and are mutually independent, is the covariance matrix of random effects, is the error variance, is an identity matrix, , , and the dimensions of , , , are chosen appropriately. The s are unobserved and the interest lies in inference on .

The DA algorithm for posterior inference on is based on modified random effects. Let be a non-singular matrix, stacks the columns of into a -dimensional vector, , , , , and be the matrix with as its th row block, where for . The prior distributions on and are assigned as

| (5) |

where , denotes a symmetric positive definite matrix, and IW stands for inverse Wishart distribution. Then, the DA algorithm for posterior inference in linear mixed-effects modeling starts with some given value of and repeats the following I and P steps for a large number of iterations:

-

LM.1

(I step) Draw given and from Normal for , where

(6) -

LM.2

(P step) Draw and given in a sequence of three steps:

(7) where , , , and .

This DA is different from the previous two DA algorithms in Sections 3.1 and 3.2 due to the presence of random effects. Following Section 2.1, we have

The main computational bottleneck here is the repeated sampling of in the I step LM.1 when is large. For example, the MovieLens data analyzed in Section 4.3 has . The ADDA-based extension of this algorithm starts by partitioning into disjoint subsets denoted as . Let , be the augmented sample on worker , and (). Note that due to the the disjoint partitioning. Define the statistics for worker as

| (8) |

Then, the augmented data sufficient statistics for worker play an important role in both the DA and ADDA algorithms. In particular, and in P step of the parent DA in (7) become

| (9) |

where

| (10) |

Here, is the scale parameter of the Wishart density in (7). Note that is obtained by arranging () in the order of samples in and binding them along the rows.

The ADDA extension of the linear mixed effects DA, at any iteration, updates (with probability ) only an fraction of , and with probability updates all of . Clearly, the ADDA extension reduces to the parent DA in steps LM.1–LM.2 when . For a given and , the ADDA extension of the marginal DA initializes at and the AD-I and AD-P steps in the th iteration are as follows:

Denote the Markov chain obtained from this ADDA algorithm as .

The convergence analysis of the linear mixed-effect model parent DA chain is extremely challenging. In fact, the literature on geometric ergodicity of the parent DA chain described in LM.1 and LM.2, to the best of our knowledge, focuses only on the special case when the is diagonal and is fixed to be the identity matrix; for example, see [45] and [1]. Following [45, 1], we assume that for the convergence analysis; however, unlike these analyses of the parent DA chain, we do not restrict to be a diagonal matrix. Algorithm 3, without the updates (i.e., is fixed at ), provides a Markov chain . In this setting, from the priors used in (5), only the prior for given is modified to the prior for given as for some . We need the following assumptions for our geometric ergodicity result.

Assumption 3.1.

-

(a)

() and , where .

-

(b)

The prior shape parameter for satisfies .

-

(c)

The matrix from the prior distribution on , and the degrees of freedom from the prior distribution on satisfy , where and denotes that .

Assumption (a) is quite reasonable, especially since the ADDA algorithm is geared towards applications with large and typically small values of and (such as the MovieLens data analyzed in Section 4.3.3). Assumptions (b) and (c) on the prior hyper-parameters might seem restrictive, but it is important to keep in mind that we are in a challenging setting with a general non-diagonal for which convergence results are unavailable even in the parent DA setting. As discussed previously, the asynchronous updates in the ADDA setting present additional challenges in the analysis; however, we are still able to establish geometric ergodicity in this more general ADDA setting, as described in the result below.

Theorem 3.3.

4 Experiments

4.1 Setup

We evaluate the numerical accuracy and computational efficiency of ADDA algorithms using their parent DA algorithms as the benchmarks. In all our simulated and real data analyses, and , , , , where the first two and last two values of represent small and large choices of , respectively. Every experiment with a given choice of is replicated ten times. Before running an ADDA algorithm, the full data are split (based on the samples or parameter dimensions) into disjoint subsets that are stored on worker machines. The parent DA algorithm uses the full data. We use the choice in our simulations and in the real data analyses. The choice is best for fast computations that are required for multiple simulation replications; however, it is not clear if the ADDA chain is Harris ergodic with this choice because Theorem 2.1 requires that . In our simulations with 20,000 iterations for ADDA algorithms with , we have rarely encountered a situation where a worker never sends its I step results to the manager. Our observations from the real data analyses suggests that one could set to be or to maintain theoretical convergence guarantees while compromising very little on the computational gains.

The (empirical) accuracy of an ADDA algorithm relative to its parent DA algorithm is defined using the total variation distance. Let be a function of the underlying parameter with components that is of interest to the practitioner. Denote the posterior density estimates of using iterations of the ADDA algorithm and its parent DA as and , respectively. Then, the accuracy metric based on for the ADDA algorithm at the end of iterations is defined as

| (12) |

where and are given, is the total variation distance between and , and because for every . We estimate using kernel density estimation in two steps. First, we select the first draws of from the ADDA algorithm and its parent DA, respectively, to estimate and using the bkde function in the KernSmooth R package. Second, these estimates are used to numerically approximate the integral in (12) and obtain the () estimates. The overall accuracy metric estimate based on for the ADDA algorithm is computed by averaging the estimates of as

| (13) |

The larger the estimate, the better an ADDA algorithm is at approximating its parent DA algorithm.

The Monte Carlo standard errors in an application of ADDA algorithm and its parent DA algorithm are computed using the overlapping batch means method. This method is implemented in the mcse function of mcmcse R package [19, 53]. Following the notation from the previous paragraph, let and respectively be outputs of the mcse function using the first draws of from the ADDA algorithm for a given and its parent DA algorithm (). Then, a metric for comparing their overall Monte Carlo standard errors is

| (14) |

The smaller the value of , better is the agreement between Monte Carlo standard errors of the ADDA algorithm and its parent DA.

We now undertake an extensive experimental evaluation of the proposed ADDA framework using both simulated datasets (Section 4.2) and the MovieLens data (Section 4.3). The simulation study focuses on using the metrics in (13) and (14) to evaluate the accuracy of the ADDA algorithm in approximating its parent DA algorithm. Due to the relatively small sample/missing data size to facilitate multiple replications for various choices, a runtime comparison is not undertaken in Section 4.2. For the MovieLens data in Section 4.3 however (with up to samples), we present both an accuracy and runtime comparison for both the logistic regression and the linear mixed model settings. All ADDA algorithms are implemented in R using the parallel package. The ease of implementation and reproducibility drive this choice. For this data, our ADDA implementations using the parallel package show three to five times gains in run-times for all the choices of (see Figure 12). We expect the run-time gains to be even better if the asynchronous updates for the ADDA algorithms are implemented carefully using MPI [32]. However, this requires significant additional programming efforts and will be addressed in future research.

4.2 Simulated Data Analyses

This section focuses on two broad classes of applications. The first class consists of logistic regression and linear mixed-effects models, where the computational bottlenecks arise due to massive sample size; see Sections 4.2.1 and 4.2.3. In these models, the samples are partitioned into subsets and stored on the worker machines. Section 4.2.2 focuses on high-dimensional variable selection using the Bayesian lasso, where the parent DA is inefficient due to the augmentation of local shrinkage parameters specific to the regression coefficients. Unlike the former two models, here we partition the augmented parameters into subsets and store them on worker machines.

4.2.1 Logistic Regression

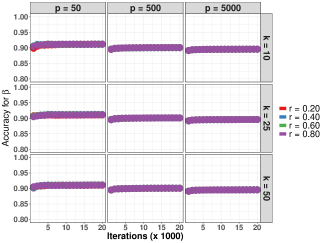

We evaluate the empirical performance of the ADDA Algorithm 1 for logistic regression in (1) with , and for every . The entries of are set to and alternatively starting from and the entries of are independent standard normal random variables. We use them to simulate using the hierarchical model in (1). The rows of and are randomly split into subsets that are stored on the worker machines. The ADDA and its parent run for 20000 iterations and draws are collected at the end of every iteration.

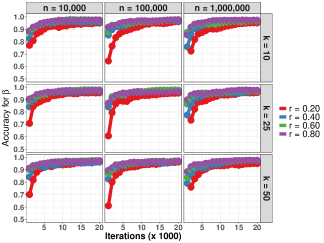

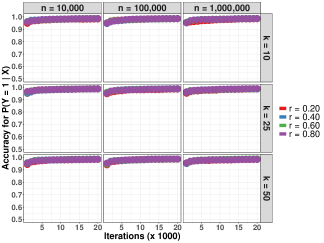

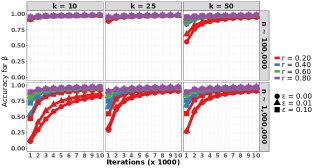

The metric is evaluated for and , respectively (Figure 1). The values for depend on values but are fairly insensitive to the choice of . For every , the values for are (initially) the largest when and decrease with . However, The differences between values for different choices of are negligible after for . On the other hand, values for are comparatively insensitive to the choice of , and after the differences for different choices of are negligible after .

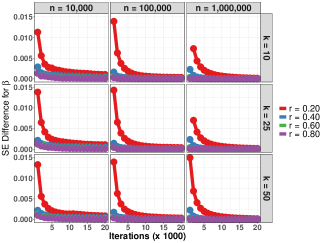

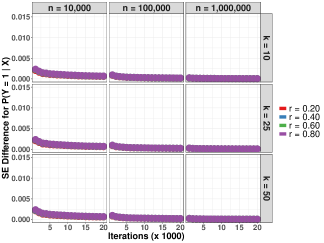

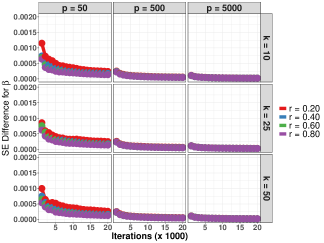

The metric for and , respectively, decays to 0 as increases (Figure 2). For every and , the values for are the largest when but quickly decay to 0 as increases. The values for quickly decay to 0 as increases and are comparatively insensitive of the choices of . This shows that values for both parameters are close to 0 for every , and if is sufficiently large and that the Monte Carlo standard errors of parameter estimates obtained using ADDA Algorithm 1 and its parent are comparable in massive data settings.

4.2.2 High Dimensional Variable Selection

We evaluate the empirical performance of the ADDA Algorithm 2 for Bayesian variable selection. We vary and such that and . The first entries of in (3.2) are set to 0 and the next entries are set to and alternatively starting from . The entries of are independent standard normal random variables. We use them to simulate using the model in (3.2) with . The columns of are randomly split into subsets that are stored on the worker machines. The ADDA algorithm and its parent DA are run for 20000 iterations and draws are collected at the end of every iteration.

For and every , the value is high and value is low (Figure 3). The values are fairly high even for small , increase slightly with , and are insensitive to the choice of and . The high-dimensionality of the variable selection problem increase with , so values decrease slightly with for a given . Agreeing with this observation, values also decay to 0 as increases and the decay is insensitive to the choices of , and . We conclude that ADDA Algorithm 2 is an accurate asynchronous and distributed generalization of the Bayesian Lasso DA algorithm.

Theorem 3.2 implies that the Bayesian Lasso ADDA chain converges to the same stationary distribution as the parent DA chain for any in the high-dimensional regime. Our empirical results support this assertion irrespective of the choice of , even when and is small.

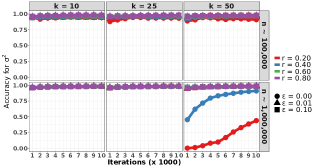

4.2.3 Linear Mixed-Effects Modeling

We evaluate the empirical performance of the ADDA Algorithm 3 for linear mixed-effects modeling with , , , and for every . Following Li et al. [27], the entries of , the entries of are set to or with equal probability satisfying Assumption 3.1, , and (), , , . We use them to simulate using the hierarchical model in (4). The rows of , and are split into disjoint subsets that are stored on the worker machines. The ADDA algorithm and its parent are run for 20000 iterations and , and draws are collected at the end of every iteration.

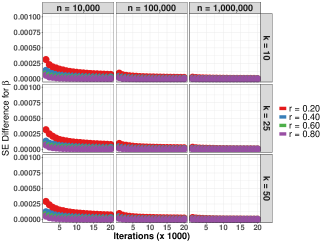

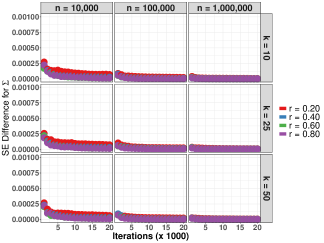

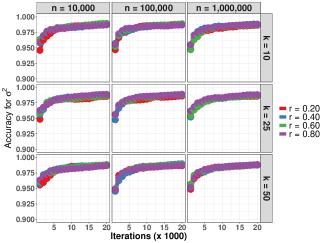

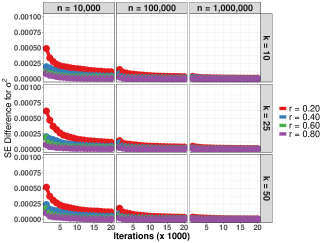

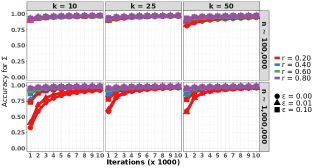

We evaluate the metric for equalling , , and , respectively (Figures 4 – 6). The values for , , and show similar patterns for every values as increases from 1 to 20000. The accuracies for all the three parameters are very high and increase with . The values are insensitive to the choices of , , and . We conclude that ADDA estimates the posterior distributions for these parameters with the same accuracy as its parent DA.

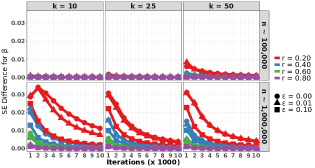

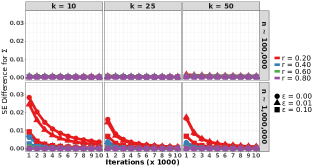

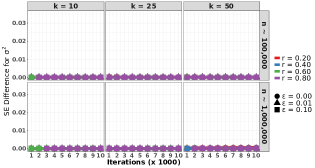

The SE metric for , , and , respectively, decays to 0 as increases (Figures 5 and 6). The decay patterns of SE values for , and are similar in that they are the highest when for every and quickly decay to 0 as increases. For all the three parameters and every , we observe that as increases, SE values decays to 0 more quickly. This shows that parameter estimates obtained using ADDA algorithm and its parent have similar standard errors in massive data settings.

4.3 Real Data Analysis

4.3.1 MovieLens Data

We use the MovieLens ratings data (http://grouplens.org) that contain more than 10 million movie ratings from about 72 thousand users, where each rating ranges from 0.5 to 5 in increments of 0.5. Starting with Perry [35], a modified form of this data has been used for illustrating scalable inference in linear mixed-effects models [48, 47, 49]. Specifically, a movie’s category is defined using its genre: action category includes action, adventure, fantasy, horror, sci-fi, or thriller genres; children category includes animation or children; drama category includes crime, documentary, drama, film-noir, musical, mystery, romance, war, or western; and comedy category includes comedy genre only.

Three predictors are defined using this data. The first predictor encodes a movie’s category using three dummy variables with action category as the baseline. If a movie belongs to categories, then its category predictor is for each of the categories. The second and third predictors capture a movie’s popularity and a user’s mood. The popularity predictor of a movie equals logit, where users rated the movie and of them gave a rating of 4 or higher. The user’s mood predictor equals 1 if the user gave the previously 30 rated movies a rating of 4 or higher and 0 otherwise. The second and third predictors are treated as numeric variables.

We model this data using logistic regression and linear mixed-effects model in Sections 4.3.2 and 4.3.3 below. Before fitting the logistic regression model, the response in MovieLens data is modified for defining the -valued response. If the user’s rating in a given sample is greater than 3, then the response is 1; otherwise, the response is 0. No modification is required for the application of linear mixed-effects model. The original PG DA and marginal DA algorithms for logistic regression and linear mixed-effects modeling, respectively, are slow if we use with the full MovieLens data; therefore, we analyze randomly selected subsets of the MovieLens data to facilitate posterior computations and estimation of Acc and SE metrics.

4.3.2 Logistic Regression

We randomly select two subsets of users in the MovieLens data such that the total number of ratings in them are about and , respectively. The MovieLens data with modified -valued responses are analyzed using logistic regression model in (1) with six predictors, including an intercept. There are three dummy variables for the movie categories and one each for a movie’s popularity and a user’s mood. The vector is -dimensional. The responses and predictors in the modified data are collected into the response vector and design matrix . We apply the ADDA Algorithm 1 used in Section 4.2.1 with two modifications: the number of iterations is 10,000 instead of 20,000 and . This setup is replicated ten times by randomly choosing the users in each replication.

Accuracy comparisons. The and metrics are evaluated for and , where is the predictor for a popular movie. When , the values for and are fairly similar and very high for every (Figures 7 and 8). If , then the setup of Theorem 3.1 is violated. In this setting we observe slower convergence of the values to 1 when and are relatively large and small, respectively (; ).

Monte Carlo standard error comparisons. Likewise, when , the values are insensitive to the choice of and decay to 0 quickly after . For the same reasons as discussed in the previous paragraph, the convergence of to 0 is much slower when , especially when and are relatively large and small, respectively.

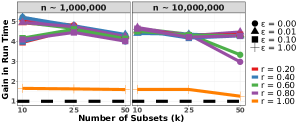

Run-time comparisons. The ADDA Algorithm 1 is three to five times faster than its parent DA (Figure 12(a)). The gain in run-times are insensitive to the choices of or . The minor variations in run-time gains are present due to the varying loads on the cluster when the computations are performed. For example, when and , the gain in run-times are close to three for and . On the other hand, the gains are close to five for the same values of but equalling or . A distributed (or parallel) implementation of the parent DA corresponds to an ADDA with (or ). For every choice of , and , the asynchronous implementations of ADDA with are two to three times faster than the distributed implementation of parent DA. An interesting observation is that the gain in runtime going from to is more significant than going from to . One possible reason is that there is a small minority of workers in each iteration who take significantly more time than others. Introducing asynchronous computation can allow us (with probability ) to bypass these workers for that particular iteration and speed up the computation. Overall, the results strongly demonstrate the utility of the proposed ADDA approach, as summarized below.

Conclusions. We conclude that for a sufficiently large and every , the and values for the ADDA chain corresponding to Algorithm 1 are close to 1 and 0, respectively, as long as is positive. The ADDA chain is also three to five times faster than its parent DA depending on . The asynchronous computations are advantageous in that ADDA with are two to three times faster than the distributed implementation of parent DA. This shows that the ADDA Algorithm 1 is a promising alternative to PG DA for accurate and efficient Bayesian inference in logistic regression models for massive data.

4.3.3 Mixed-Effects Modeling

We randomly select two subsets of users in the MovieLens data such that the total number of ratings in them are approximately and , respectively. We apply Algorithm 3 for fitting linear mixed-effects models to the two subsets. There are six fixed and random effects predictors, including an intercept, three dummy variables for the movie categories, and the remaining two for a movie’s popularity and a user’s mood. The dimensions of and are and , respectively. We fit the linear mixed effects model in (4) following the previous section, except that we run the DA algorithm for 10,000 instead of 20,000 iterations and use three choices of . This setup is replicated ten times by randomly choosing the users in each replication.

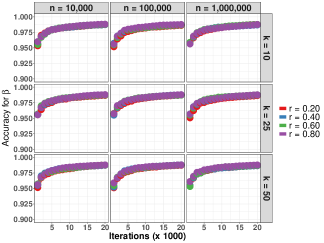

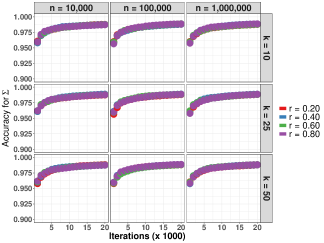

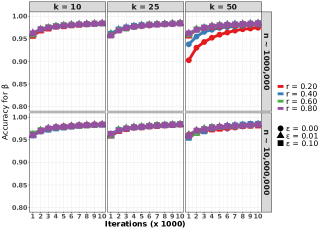

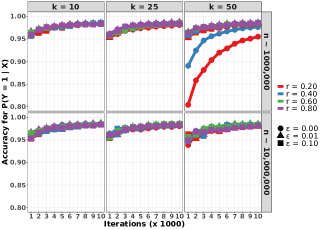

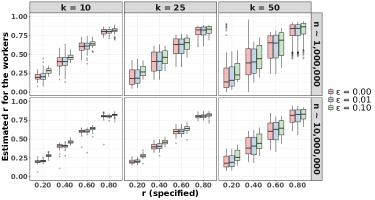

Accuracy comparisons. We evaluate and metrics for , , and , respectively. When and , the values for , , and converge to 1 quickly for every (Figures 9 and 11). For smaller values, is relatively low for and ; however, the differences between values disappear for a sufficiently large given .

On the other hand, when the convergence of to 1 is very slow compared to the previous cases. For example, values for are noticeably small when and . This is a consequence of violating the assumptions of Theorem 3.3; therefore, we recommend choosing a small but positive in practice.

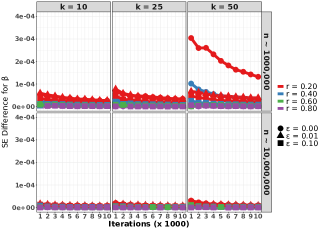

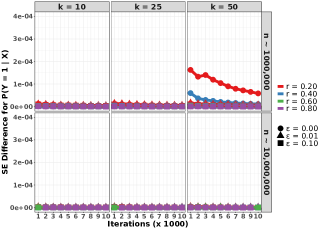

Monte Carlo standard error comparisons. Theorem 3.3 also impacts the decay of values to 0 when . Specifically, if , then values for , , and converge to 0 quickly for every (Figures 10 and 11). This pattern is maintained for even when . The values for and decay to 0 relatively slowly for every when is large, , and ; however, if is sufficiently large, then the value is small for every choice of , and .

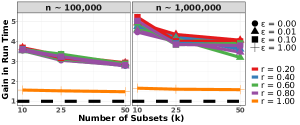

Run-time comparisons. The ADDA Algorithm 3 is three to five times faster than its parent DA for all the choices of and (Figure 12(b)). For a given , the gain in run-time increases with for every and . On the other hand, for a given , the gain in run-times decreases with increasing for every and due to the increased communication among manager and worker processes. Similar to our observations in logistic regression, a distributed (or parallel) implementation of the parent DA is two to three times slower than the asynchronous implementations of ADDA with and for every choice of , and . Unlike the case for logistic regression, varying loads on the cluster have a minimal impact on the run-times.

Conclusions. If is positive and is sufficiently large, then the and values of Algorithm 3 are close to 1 and 0, respectively, for every . The ADDA chain corresponding to Algorithm 3 is also three to five times faster than its parent DA depending on . The asynchronous computations are more efficient than parallel computations in that ADDA with is faster than the distributed implementation of parent DA. We conclude that ADDA Algorithm 3 is a promising alternative to the marginal DA for accurate and efficient Bayesian inference in linear mixed-effects models for massive data.

5 Discussion

It is interesting to explore extensions of our ADDA schemes and theoretical results. First, linear mixed-effects have been an important class of models for evaluating the performance of a new class of DA algorithms [28, 51, 52]. The excellent empirical performance of ADDA in Sections 4.2.3 and 4.3.3 suggests that it is possible to extend the ADDA scheme to other classes of hierarchical Bayesian models. For example, if the random effects in a linear mixed-effects model are assigned a multivariate distribution, then the I and P steps of the new model are similar to those in Section 3.3 [36]. This implies that the Algorithm 3 is easily extended to robust extensions of linear mixed-effects models.

Second, our real data analysis illustrates the dependence of accuracy and Monte Carlo standard errors on the choice of . Due to varying loads on worker processes in a cluster, some workers return their I step results to the manager more often than others. Our empirical results suggest this variability decreases with . For example, if we define the empirical estimate of for a worker as the fraction of the number of times the manager accepts its I step results over the total number of DA iterations, then empirical estimates of are closer to the true as increases for every and worker process; see Figure 13. Furthermore, the Bernstein-von Mises theorem implies that the posterior distribution becomes increasingly Gaussian as increases. We are exploring techniques for balancing the Monte Carlo error (depending on ) and the statistical error (depending on ) for providing some guidance on the choice of and total number of MCMC iterations so that a desired accuracy is achieved by the ADDA algorithm.

Our DA extensions based on ADDA exploit two features of the augmented data model. First, the augmented data subsets are mutually independent given the original parameter and the observed data. Second, the conditional posterior distribution of the missing data on any subset depends only on the local copy of the observed data. Both assumptions are violated in models for time series data, including hidden Markov models (HMMs) and Gaussian state-space models. DA has been widely used for posterior inference and predictions in these models, but it suffers from similar computational bottlenecks in massive data settings that have been highlighted in this paper. Recently, this problem has been addressed for HMMs using online EM [9, 24] and the divide-and-conquer technique [54]. As part of future research, we will focus on extending the original DA algorithms using ADDA for scalable posterior inference and predictions in HMMs and related state-space models.

Acknowledgements

Sanvesh Srivastava is partially supported by grants from the Office of Naval Research (ONR-BAA N000141812741) and the National Science Foundation (DMS-1854667/1854662). The code used in the experiments is available at https://github.com/blayes/ADDA.

References

- Abrahamsen and Hobert [2019] Abrahamsen, T. and J. P. Hobert (2019). Fast monte carlo markov chains for bayesian shrinkage models with random effects. Journal of Multivariate Analysis 169, 61–80.

- Ahmed et al. [2011] Ahmed, A., Y. Low, M. Aly, V. Josifovski, and A. J. Smola (2011). Scalable distributed inference of dynamic user interests for behavioral targeting. In Proceedings of the 17th ACM SIGKDD international conference on Knowledge discovery and data mining, pp. 114–122.

- Ahn et al. [2012] Ahn, S., A. Korattikara, and M. Welling (2012). Bayesian posterior sampling via stochastic gradient Fisher scoring. Proceedings of the 29th International Conference on Machine Learning.

- Atchadé and Wang [2021] Atchadé, Y. and L. Wang (2021). A fast asynchronous mcmc sampler for sparse bayesian inference. arXiv preprint arXiv:2108.06446.

- Backlund et al. [2018] Backlund, G., J. P. Hobert, Y. J. Jung, and K. Khare (2018). A hybrid scan gibbs sampler for bayesian models with latent variables. arXiv preprint arXiv:1808.09047.

- Bardenet et al. [2017] Bardenet, R., A. Doucet, and C. Holmes (2017). On markov chain monte carlo methods for tall data. The Journal of Machine Learning Research 18(1), 1515–1557.

- Bierkens et al. [2019] Bierkens, J., P. Fearnhead, and G. Roberts (2019). The zig-zag process and super-efficient sampling for bayesian analysis of big data. The Annals of Statistics 47(3), 1288–1320.

- Bouchard-Côté et al. [2018] Bouchard-Côté, A., S. J. Vollmer, and A. Doucet (2018). The bouncy particle sampler: A nonreversible rejection-free markov chain monte carlo method. Journal of the American Statistical Association 113(522), 855–867.

- Cappé [2011] Cappé, O. (2011). Online EM algorithm for hidden Markov models. Journal of Computational and Graphical Statistics 20(3), 728–749.

- Cappé and Moulines [2009] Cappé, O. and E. Moulines (2009). Online EM algorithm for latent data models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 71(3), 593–613.

- Choi and Hobert [2013] Choi, H. M. and J. P. Hobert (2013). The polya-gamma gibbs sampler for bayesian logistic regression is uniformly ergodic. Electronic Journal of Statistics 7, 2054–2064.

- Daskalakis et al. [2018] Daskalakis, C., N. Dikkala, and S. Jayanti (2018). Hogwild!-gibbs can be panaccurate. In Advances in Neural Information Processing Systems, pp. 32–41.

- De Sa and Chen [2018] De Sa, C. and V. Chen (2018). Minibatch gibbs sampling on large graphical models. In Proceedings of the 35th International Conference on Machine Learning.

- Dempster et al. [1977] Dempster, A. P., N. M. Laird, and D. B. Rubin (1977). Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society. Series B (Methodological) 39(1), 1–38.

- Fearnhead et al. [2018] Fearnhead, P., J. Bierkens, M. Pollock, G. O. Roberts, et al. (2018). Piecewise deterministic markov processes for continuous-time monte carlo. Statistical Science 33(3), 386–412.

- Hobert [2011] Hobert, J. P. (2011). The data augmentation algorithm: Theory and methodology. Handbook of Markov Chain Monte Carlo, 253–293.

- Hobert and Marchev [2008] Hobert, J. P. and D. Marchev (2008). A theoretical comparison of the data augmentation, marginal augmentation and px-da algorithms. Annals of Statistics 36, 532–554.

- Johnson et al. [2013] Johnson, M. J., J. Saunderson, and A. Willsky (2013). Analyzing hogwild parallel gaussian gibbs sampling. In Advances in Neural Information Processing Systems, pp. 2715–2723.

- Jones et al. [2006] Jones, G. L., M. Haran, B. S. Caffo, and R. Neath (2006). Fixed-width output analysis for markov chain monte carlo. Journal of the American Statistical Association 101(476), 1537–1547.

- Jones and Hobert [2001] Jones, G. L. and J. P. Hobert (2001). Honest exploration of intractable probability distributions via markov chain monte carlo. Statistical Science, 312–334.

- Jordan et al. [2019] Jordan, M. I., J. D. Lee, and Y. Yang (2019). Communication-efficient distributed statistical inference. Journal of the American Statistical Association 114(526), 668–681.

- Khare and Hobert [2013] Khare, K. and J. P. Hobert (2013). Geometric ergodicity of the bayesian lasso. Electronic Journal of Statistics 7, 2150–2163.

- Korattikara et al. [2014] Korattikara, A., Y. Chen, and M. Welling (2014). Austerity in MCMC land: Cutting the Metropolis-Hastings budget. In Proceedings of the 31st International Conference on Machine Learning, pp. 181–189.

- Le Corff and Fort [2013] Le Corff, S. and G. Fort (2013). Online expectation maximization based algorithms for inference in hidden markov models. Electronic Journal of Statistics 7, 763–792.

- Lee et al. [2014] Lee, S., J. K. Kim, X. Zheng, Q. Ho, G. A. Gibson, and E. P. Xing (2014). On model parallelization and scheduling strategies for distributed machine learning. In Advances in neural information processing systems, pp. 2834–2842.

- Levine et al. [2005] Levine, R. A., Z. Yu, W. G. Hanley, and J. J. Nitao (2005). Implementing random scan gibbs samplers. Computational Statistics 20(1), 177–196.

- Li et al. [2017] Li, C., S. Srivastava, and D. B. Dunson (2017). Simple, scalable and accurate posterior interval estimation. Biometrika 104, 665–680.

- Meng and Van Dyk [1999] Meng, X.-L. and D. A. Van Dyk (1999). Seeking efficient data augmentation schemes via conditional and marginal augmentation. Biometrika 86(2), 301–320.

- Minsker et al. [2017] Minsker, S., S. Srivastava, L. Lin, and D. B. Dunson ((2017)). Robust and scalable Bayes via a median of subset posterior measures. Journal of Machine Learning Research.

- Nemeth and Fearnhead [2021] Nemeth, C. and P. Fearnhead (2021). Stochastic gradient Markov chain Monte Carlo. Journal of the American Statistical Association, 1–18.

- Newman et al. [2009] Newman, D., A. Asuncion, P. Smyth, and M. Welling (2009). Distributed algorithms for topic models. Journal of Machine Learning Research 10(8).

- Nielsen [2016] Nielsen, F. (2016). Introduction to HPC with MPI for Data Science. Springer.

- Ou et al. [2021] Ou, R., D. Sen, and D. Dunson (2021). Scalable bayesian inference for time series via divide-and-conquer. arXiv preprint arXiv:2106.11043.

- Pal and Khare [2014] Pal, S. and K. Khare (2014). Geometric ergodicity for bayesian shrinkage models. Electronic Journal of Statistics 8(1), 604–645.

- Perry [2017] Perry, P. O. (2017). Fast moment-based estimation for hierarchical models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 79(1), 267–291.

- Pinheiro et al. [2001] Pinheiro, J. C., C. Liu, and Y. N. Wu (2001). Efficient algorithms for robust estimation in linear mixed-effects models using the multivariate t distribution. Journal of Computational and Graphical Statistics 10(2), 249–276.

- Plassier et al. [2021] Plassier, V., M. Vono, A. Durmus, and E. Moulines (2021). Dg-lmc: A turn-key and scalable synchronous distributed mcmc algorithm. arXiv preprint arXiv:2106.06300.

- Polson et al. [2013] Polson, N. G., J. G. Scott, and J. Windle (2013). Bayesian inference for logistic models using pólya–gamma latent variables. Journal of the American statistical Association 108(504), 1339–1349.

- Quiroz et al. [2019] Quiroz, M., R. Kohn, M. Villani, and M.-N. Tran (2019). Speeding up mcmc by efficient data subsampling. Journal of the American Statistical Association 114(526), 831–843.

- Rajaratnam et al. [2015] Rajaratnam, B., D. Sparks, K. Khare, and L. Zhang (2015). Scalable bayesian shrinkage and uncertainty quantification for high-dimensional regression. arXiv preprint arXiv:1509.03697.

- Rajaratnam et al. [2019] Rajaratnam, B., D. Sparks, K. Khare, and L. Zhang (2019). Uncertainty quantification for modern high-dimensional regression via scalable bayesian methods. Journal of Computational and Graphical Statistics 28(1), 174–184.

- Robert and Casella [2013] Robert, C. and G. Casella (2013). Monte Carlo statistical methods. Springer Science & Business Media.

- Roberts and Rosenthal [2001] Roberts, G. O. and J. S. Rosenthal (2001). Markov chains and de-initializing processes. Scandinavian Journal of Statistics 28(3), 489–504.

- Roberts and Rosenthal [2006] Roberts, G. O. and J. S. Rosenthal (2006). Harris recurrence of metropolis-within-gibbs and trans-dimensional markov chains. The Annals of Applied Probability, 2123–2139.

- Román and Hobert [2015] Román, J. C. and J. P. Hobert (2015). Geometric ergodicity of gibbs samplers for bayesian general linear mixed models with proper priors. Linear Algebra and its Applications 473, 54–77.

- Scott et al. [2016] Scott, S. L., A. W. Blocker, F. V. Bonassi, H. A. Chipman, E. I. George, and R. E. McCulloch (2016). Bayes and big data: the consensus Monte Carlo algorithm. International Journal of Management Science and Engineering Management 11(2), 78–88.

- Srivastava et al. [2019] Srivastava, S., G. DePalma, and C. Liu (2019). An asynchronous distributed expectation maximization algorithm for massive data: The dem algorithm. Journal of Computational and Graphical Statistics 28(2), 233–243.

- Srivastava et al. [2018] Srivastava, S., C. Li, and D. B. Dunson (2018). Scalable Bayes via barycenter in Wasserstein space. Journal of Machine Learning Research 19, 312–346.

- Srivastava and Xu [2021] Srivastava, S. and Y. Xu (2021). Distributed Bayesian Inference in Linear Mixed-Effects Models. Journal of the Computational and Graphical Statistics.

- Terenin et al. [2020] Terenin, A., D. Simpson, and D. Draper (2020, 26–28 Aug). Asynchronous gibbs sampling. In S. Chiappa and R. Calandra (Eds.), Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, Volume 108 of Proceedings of Machine Learning Research, Online, pp. 144–154. PMLR.

- Van Dyk and Meng [2001] Van Dyk, D. A. and X.-L. Meng (2001). The art of data augmentation. Journal of Computational and Graphical Statistics 10(1), 1–50.

- Van Dyk and Park [2008] Van Dyk, D. A. and T. Park (2008). Partially collapsed gibbs samplers: Theory and methods. Journal of the American Statistical Association 103(482), 790–796.

- Vats et al. [2019] Vats, D., J. M. Flegal, and G. L. Jones (2019). Multivariate output analysis for markov chain monte carlo. Biometrika 106(2), 321–337.

- Wang and Srivastava [2021] Wang, C. and S. Srivastava (2021). Divide-and-conquer bayesian inference in hidden markov models. arXiv preprint arXiv:2105.14395.

- Wang and Roy [2018a] Wang, X. and V. Roy (2018a). Analysis of the pólya-gamma block gibbs sampler for bayesian logistic linear mixed models. Statistics & Probability Letters 137, 251–256.

- Wang and Roy [2018b] Wang, X. and V. Roy (2018b). Geometric ergodicity of pólya-gamma gibbs sampler for bayesian logistic regression with a flat prior. Electron. J. Statist. 12(2), 3295–3311.

- Welling and Teh [2011] Welling, M. and Y. W. Teh (2011). Bayesian learning via stochastic gradient Langevin dynamics. In Proceedings of the 28th International Conference on Machine Learning, pp. 681–688.

- Wilkinson [2018] Wilkinson, D. J. (2018). Stochastic modelling for systems biology. Chapman and Hall/CRC.

- Wu and Robert [2019] Wu, C. and C. P. Robert (2019). Parallelising mcmc via random forests. arXiv preprint arXiv:1911.09698.

- Xu et al. [2018] Xu, G., Z. Shang, and G. Cheng (2018). Optimal tuning for divide-and-conquer kernel ridge regression with massive data. In International Conference on Machine Learning, pp. 5483–5491. PMLR.

- Xue and Liang [2019] Xue, J. and F. Liang (2019). Double-parallel monte carlo for bayesian analysis of big data. Statistics and computing 29(1), 23–32.

- Zhang and De Sa [2019] Zhang, R. and C. M. De Sa (2019). Poisson-minibatching for gibbs sampling with convergence rate guarantees. In Advances in Neural Information Processing Systems, pp. 4922–4931.

A Supplemental Document for “Asychronous and Distributed Data Augmentation for Massive Data Settings”

A.1 Proof of Theorem 2.1

Since both the AD-I and AD-P step leave the joint posterior distribution invariant, it is enough to establish that the ADDA chain is irreducible, aperiodic and Harris recurrent. Note that the ADDA chain is a mixture of the parent DA chain(with prob ), and a pure asynchronous chain where only an -fraction update regime is chosen for the workers (with prob ). Since the original DA chain is irreducible and aperiodic, it follows that the ADDA chain is also irreducible and aperiodic. Lastly, let and denote the transition kernels for the ADDA chain and the purely asynchronous chain mentioned above. Then, for any with , , where the inequality follows from the assumption that is absolute continuous wrt. . Let denote a realization of the ADDA Markov chain. Then for any , we have

Here is the indicator function. By repeating the above argument, we get that

With , by letting go to infinity, it follows that . Then by Theorem 6 of [44], the ADDA chain is Harris recurrent.

A.2 The switched ADDA chain and geometric ergodicity

Let denote the transition kernel of the ADDA chain described in Section 2.1, and denote the transition kernel of the switched ADDA chain, where the AD-P step is performed before the AD-I step. Hence, the one-step dynamics of the switched ADDA chain from to is described as follows. The manager draws from and distributes it to the workers. The worker generates a draw from and sends to manager (the draw is truncated if the next value is received from the manager before the draw is finished). As soon as the manager receives the new s from the required fraction of workers ( with probability , and with probability ), it assigns for the remaining fraction, and proceeds with the next draw. For both the ADDA and the switched ADDA chain, the marginal -process is not in general Markov. However, it can be easily seen that the marginal process for both chains is Markov. This follows from the fact that for both chains, the distribution of the latest value given the entire past depends only on the immediately previous value, and the distribution of the latest value given the entire past depends only on the immediately previous and values.

Let denote a realization of the switched ADDA chain. Since

for any Borel subset of , it follows that if the switched ADDA chain is geometrically ergodic for any choice of initial distribution, then so is its marginal chain .

Now, let denote a realization of the ADDA chain. Note that can be denoted as for an appropriate function . Also

It follows that the marginal chain is homogeneously functionally de-initializing for . It follows by Corollary 2 of [43] that if is geometrically ergodic for any choice of initial distirbution, then so is . Finally, by noting that the time homogeneous Markov chains and have the same transition mechanism gives the following lemma.

Lemma A.1.

If the switched ADDA chain with transition kernel is geometrically ergodic for any choice of initial distribution, then so is the ADDA chain with transition kernel .

A.3 Proof of Theorem 3.1

We will prove geometric ergodicity of the switched ADDA chain, which will be enough to establish geometric ergodicity of the ADDA chain based on Lemma A.1.

In the following calculation of conditional expectations, if not otherwise specified, we assume conditioning on the data. Define the drift function where where is a fixed positive number that will be defined later in the proof. Notice the support for is , and for any , is compact in . Thus the function introduced is unbounded off compact sets in . It remains to show that a geometric drift condition holds, i.e. to show that there exist a and , such that

| (15) |

where the expectation is taken with respect to the transition kernel of .

Firstly notice that

| (16) |

Here

| (17) | |||||

where and .

Now consider the inner part of the double expectation in (16). In the AD-I step, there is at least a probability that worker gets to send an updated value to the manager. It follows that:

We now focus on the second term in (A.3).

| (19) | |||

| (20) |

Then to deal with , we establish the following Lemma:

Lemma 1.

For , and any integer , there exist a positive number , which is a function of and only, such that

The proof of this Lemma is given in Supplemental Section A.4. By this Lemma and setting , we have

| (21) |

Thus for the outer expectation of (16), we need to consider .

Recall that , thus where

| (22) |

and

| (23) |

Then by the moment generating function of folded normal random variable, and combining the above equations, we have

| (24) |

where , which is a function of known constants only.

A.4 Proof of Lemma 1

The density of PG is written as

| (26) |

Case 1: b = 0

| (28) | |||||

For , , thus

| (29) |

where converges. Thus by letting the proof is complete.

Case 2: b 0

When and ,

| (30) | |||||

where the first and last inequality follows from for any , and the second inequality follows from results in Case 1.

A.5 Proof of Theorem 3.2

We will prove geometric ergodicity of the switched ADDA chain, which will be enough to establish geometric ergodicity of the ADDA chain based on Lemma A.1.

Define the following drift function:

| (31) | |||||

where and are positive numbers which are to be defined later. It can be easily seend that the above drift function is unbounded off compact sets for the parameters . Thus, we can proceed to show that by choosing proper and , there exist some constants and such that

| (32) |

Here this expectation is with respect to the transition kernel of , and can be written as

| (33) |

Under the assumption , for a fixed acceptance rate , there is a probability of at least that is updated at a given iteration. Hence,

| (34) | |||||

where is an arbitrary positive number, and the last inequality holds because for any positive number and . Similarly we can establish

| (35) | |||||

where is an arbitrary positive number.

To calculate , note that , given and that the corresponding worker successfully sends update to the manager, is Generalized Inverse Gaussian(GIG) distributed with parameters . More specifically, if the corresponding worker successfully sends update to the manager, then

| (37) | |||||

By [34, eq, (3.15)], for ,

| (38) |

Here , where is an arbitrary positive number. Here where depends on and only, thus is irrelevant of the parameters .

Then we proceed to calculate expectation of (36) conditional on . Notice

Further more By Proposition A1 in [34]

| (39) |

where is the ’th entry of a matrix and is the maximum eigenvalue of . Then it follows that

| (41) |

where . Notice goes to zero when , by choosing close enough to , we can have , which leads to

| (42) | |||||

| (43) |

Then for the outer expectation of (33), we first establish the following inequalities:

| (44) |

where guarantees that the first bound is positive. It follows that

where .

Finally by setting , we can establish the drift condition as:

| (46) | |||||

Thus the proof of (32) is completed by letting , and as defined above.

A.6 Proof of Theorem 3.3