1 \sameaddress1\secondaddressWolfgang Pauli Institut, c/o Fakultät für Mathematik, Universität Wien, 1090 Vienna, Austria

Non-asymptotic analysis of stochastic approximation algorithms for streaming data

Abstract.

We introduce a streaming framework for analyzing stochastic approximation/optimization problems. This streaming framework is analogous to solving optimization problems using time-varying mini-batches that arrive sequentially. We provide non-asymptotic convergence rates of various gradient-based algorithms; this includes the famous Stochastic Gradient (SG) descent (a.k.a. Robbins-Monro algorithm), mini-batch SG and time-varying mini-batch SG algorithms, as well as their iterated averages (a.k.a. Polyak-Ruppert averaging). We show i) how to accelerate convergence by choosing the learning rate according to the time-varying mini-batches, ii) that Polyak-Ruppert averaging achieves optimal convergence in terms of attaining the Cramer-Rao lower bound, and iii) how time-varying mini-batches together with Polyak-Ruppert averaging can provide variance reduction and accelerate convergence simultaneously, which is advantageous for many learning problems, such as online, sequential, and large-scale learning. We further demonstrate these favorable effects for various time-varying mini-batches.

Key words and phrases:

stochastic algorithms, stochastic optimization, machine learning, online learning, mini-batch, streaming1991 Mathematics Subject Classification:

62L12, 62L20, 68W27, 90C251. Introduction

Machine learning-based intelligent systems are becoming more and more widespread in modern society [24, 18]. A crucial component of machine learning is optimization, which, in this context, involves estimating parameters for the intelligent systems to make decisions about future data. A growing challenge is that these future data will arrive in an endless stream, for example through sensors from real-time measurement of weather, traffic and e-commerce, to name a few; we call these streaming data. Such streaming data arrives sequentially in time-varying mini-batches. This places wide demands on computational efficiency and the robustness of the underlying optimization algorithms, which must be updated sequentially as more data becomes available.

Stochastic approximation/optimization algorithms have proven effective in handling large amounts of data and perform well across many fields ranging from smooth and strongly convex problems to complex non-convex ones; Bottou et al. [4] reviews such algorithms for large-scale problems in machine learning. Among these, the most well-known is probably the Stochastic Gradient (SG) descent introduced in Robbins and Monro [33], which forms the basis of many optimization algorithms used in machine learning [23, 36, 22, 30]. In a nutshell, these SG-based algorithms minimize the objective (a.k.a. loss or risk) of a model by iteratively updating the model parameters using stochastic approximations of its gradient. Traditionally, these gradients are processed individually or in (fixed) mini-batches taken from a (fixed) dataset. However, in our streaming framework, these gradients must be computed as a sequential stream of time-varying mini-batches.

Contributions. The objective of this paper is to solve stochastic approximation/optimization problems in a streaming framework. Our main theoretical contribution is the non-asymptotic analysis of SG-based algorithms in this streaming framework, extending the work of Bach and Moulines [1]. This means that we investigate everything from the classical SG descent to time-varying mini-batch SG-based algorithms, as well as their Polyak-Ruppert extensions. Our results show how to accelerate convergence by choosing the learning rate according to the time-varying mini-batches. In addition, we show that Polyak-Ruppert averaging [32, 34] achieves optimal convergence in terms of achieving the Cramer-Rao lower bound in this streaming framework. In particular, we show how time-varying mini-batches together with Polyak-Ruppert averaging can provide variance reduction and accelerate convergence simultaneously, without jeopardizing the computational complexity. These theoretical findings are demonstrated for various streaming settings of time-varying mini-batches.

Organization. Section 2 presents the streaming framework, in which we will analyze the stochastic algorithms. In section 3, we introduce our stochastic streaming-gradient algorithms, their projected versions and Polyak-Ruppert extensions. The main results, namely the non-asymptotic convergence analysis, are presented in section 4. These results are illustrated in section 5 for various time-varying mini-batches. In section 6, we provide some concluding remarks with related future perspectives.

2. Problem formulation

Our objective is to solve stochastic approximation/optimization problems in a streaming framework, where data arrives sequentially in time-varying mini-batches; we consider problems on the form

| (1) |

We will refer to as the objective function, but in the literature, is also known as the expected loss (and risk); See for instance Bottou et al. [4]. Let denote the global minimum of , and assume that , where is a closed convex set in . Typical convergence results measure how quickly some estimate approaches (or the function value approaches ). In this paper we are interested in bounding the quantity . As in [1, 16], we make the analysis more convenient through convexity and smoothness assumptions on in 1.111Milder degrees of convexity have been investigated; Godichon-Baggioni [13] studied SG algorithms under local strongly convexity, Karimi et al. [19] studied SG algorithms under the Polyak-Łojasiewicz condition [31, 25], and Gadat and Panloup [10] studied the Ruppert-Polyak averaging estimate under some Kurdyka-Łojasiewicz-type condition [21, 25]. The following assumptions are frequently referenced.

Assumption 1 (-quasi-strong convex [19, 28]).

The objective function is differentiable with and there exists a constant such that ,

| (2) |

Assumption 2 (-Lipschitz smoothness).

The function is -Lipschitz continuous around , i.e., there exists such that ,

| (3) |

Streaming framework and notation. Let each constitute a sequence of independent differentiable random functions (possibly non-convex) and let their gradients be unbiased estimates of , see e.g. Nesterov et al. [30] for definitions and properties of such functions. The shorthand notation of

We say that each consist of data points, which we denote by the set . For example, for a class of models parameterized by , a loss function , and a regularizer , then can be seen as the composition:

| (4) |

where is a time-varying mini-batch of i.i.d. input-output data points with generic element . The associated objective function from 1 thus corresponds to having with .

Our streaming framework includes many machine learning problems, from classification, and regression to ranking; this includes stochastic approximation (Robbins-Monro setting [33]), learning from i.i.d. data with linear, logistic, softmax, quantile and general ridge regression, and -means and geometric median under regularity conditions [18, 38, 37, 7, 30, 23]. More specifically, 4 could be the -regularized least squares regression model, with and , or the -regularized logistic regression for binary classification, with and ; here, we used .

3. Stochastic streaming gradient algorithms

SG-based algorithms, which dates back to the seminal work of Robbins and Monro [33], have become the predominant optimization algorithm for solving these stochastic approximation/optimization problems. To solve problem 1 in our streaming framework, we introduce the Stochastic Streaming Gradient (SSG) algorithm, defined as the recursion

| (SSG) | (5) |

where is the learning rate satisfying and for . This SSG algorithm sequentially processes the time-varying mini-batches. Note that if for all , , then the SSG algorithm is an online version of the well-known SG descent.

In many machine learning models, there may be restrictions on the parameter space of . We embrace this by defining a projected version of SSG, given as

| (PSSG) | (6) |

where denotes the Euclidean projection onto the closed convex set in , i.e., . It is worth noting that SG-based algorithms are not gradient descent in the sense that the objective function values often increase, but only decrease on average; examples of this are illustrated in section 5. Therefore, it makes intuitive sense to use sets of stochastic gradient in each iteration, as it naturally reduces the variance and makes it easier to adjust the learning rate , which (on average) improves the convergence.

Next, let’s consider a streaming variant of the celebrated Polyak-Ruppert averaging procedure [32, 34]:

| (ASSG)/(APSSG) | (7) |

where denotes the accumulated number of data points processed at each . This averaging procedure sequentially aggregates the estimates of 5 and 6, which stabilizes and accelerates convergence [32, 29]. In particular, this average allows us to obtain the optimal Cramer-Rao lower bound. Note that 7 does not actually change the estimates produced by the SSG or PSSG algorithms, but instead simply keeps track of a running average over the estimates. Practically, as we handle data sequentially, we will make use of the recursive formula, . A detailed overview of our stochastic streaming gradient algorithms (defined in 5, 6, and 7) is presented in Algorithm 1.

4. Non-asymptotic convergence analysis

Throughout this paper, we consider learning rates of the form

with , , and chosen according to the time-varying mini-batches . This learning rate allows us to add more weight to larger mini-batches through the parameter. Note that Bach and Moulines [1] considered learning rates of the same form, but with (and ). For simplicity, we let the time-varying mini-batches be given as

with and such that for all . This setting includes classical (online) SG descent algorithms (i.e., ) and (online) mini-batch procedures of both constant and time-varying size (i.e. and ), as well as the Polyak-Ruppert average of (online) time-varying mini-batches. We will refer to as the mini-batch size and as the mini-batch rate.

Our goal is to non-asymptotic bound the quantities and , such that they solely depend on the parameters of the problem. To our knowledge, this is the first work that studies the non-asymptotic convergence behavior of SG-based algorithms and their Polyak-Ruppert averaging in a streaming framework. To do this, we assume for each the following about the (stochastic) gradients of .

Assumption 3 (unbiased gradients).

For each , the random variable is square-integrable and , .

Assumption 4-p (-expected smoothness).

For a positive integer , there exists such that , .

Assumption 5-p (-gradient noise).

For a positive integer , there exists such that .

Discussion of Assumptions 3, 4-p, and 5-p. These assumptions are standard for analyzing stochastic approximation/optimization problems with SG algorithms, e.g., see Benveniste et al. [3], Kushner and Yin [22]. Assumption 3 concerns the access to unbiased stochastic approximations of the gradient , which are common when SG algorithms are used to solve problem 1.222The principles for biased gradients are rather different, e.g., see [9, 35]. Another common assumption for SG algorithms is that they are uniformly bounded. But such an assumption is often too restrictive, as it can only hold for some loss functions [4, 14]. Instead, we make the weaker expected smoothness assumption of the gradients of in Assumption 4-p [16, 1]. The last key assumption concerns the finiteness of the gradient noise at (Assumption 5-p). It is worth noting that Assumptions 4-p and 5-p can be verified explicitly, e.g., see Gower et al. [16]. For SSG and PSSG, Assumptions 4-p and 5-p only needs to hold for , where for ASSG and APSSG, we need to bound the fourth order moment.

4.1. Stochastic streaming gradients

In this section, we analysis the SSG and PSSG algorithms from 5 and 6. To do this, we first derive an explicit upper bound on the -th estimate of 5 and 6 for any learning rate and time-varying mini-batch using classical techniques from stochastic approximations [3, 22].

Theorem 1 (SSG/PSSG).

Sketch of proof. Under Assumptions 1, 2, 3, 4-p, and 5-p with , we show that (derived using 5) satisfies the recursive relation

| (9) |

for any and fulfilling the conditions imposed on the learning rate [33]. This recursive relation is then explicitly upper bounded in a non-asymptotic manner using Proposition 5 in appendix B. Bounding the projected estimate in 6 follows directly from the fact that , [40]. Alternatively, the projected estimate can also be shown without Assumptions 4-p and 5-p, but instead with a bounded gradient assumption, e.g., see Bach and Moulines [1].

Related work. When in 8, we obtain (an online version of) the usual SG descent studied in Bach and Moulines [1]. As mentioned in Bach and Moulines [1], Theorem 1 forms an upper bound on the function values, ; this follows from the Cauchy-Schwarz inequality and Assumption 4-p.

Decay of the initial conditions. The learning rate should satisfy the conditions and as of Robbins and Monro [33]. These conditions directly imply that . Thus, our attention is on reducing the noise term without damaging the natural decay of the sub-exponential term . In particular, the non-asymptotic bound in 8 holds for any learning rate fulfilling these conditions. In addition, the scaling of in the noise term shows an obvious possibility of variance reduction.

Before considering time-varying mini-batches, we consider the constant case where follows the constant , i.e., an online (projected) mini-batch SG variant.

Corollary 1 (SSG/PSSG with constant mini-batches).

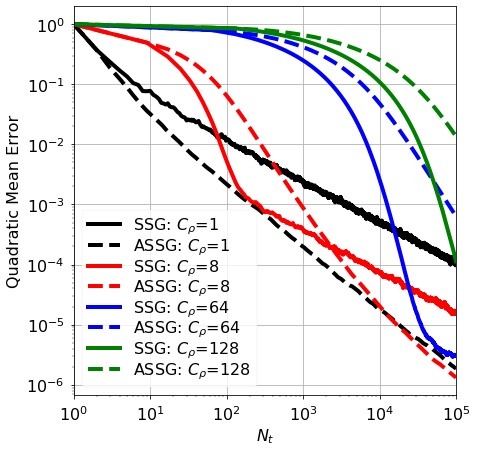

Decay of the initial conditions. The bound in Corollary 1 depends on the initial condition and the variance in the noise term. The initial condition vanish sub-exponentially fast for ; the condition of having is a natural restriction from Robbins and Monro [33]. Thus, the asymptotic term is , i.e., . Moreover, the bound in 10 is optimal (up to some constants) for quadratic functions , since the deterministic recursion in 9 would be with equality. It is worth noting that if or is chosen too large, they may produce a large constant. In addition, is positively affected by when . Obviously, the hyper-parameter only comes into play if the mini-batch size is larger than one, i.e., . Nonetheless, the effect of will decrease exponentially fast due to the sub-exponentially decaying factor in front.

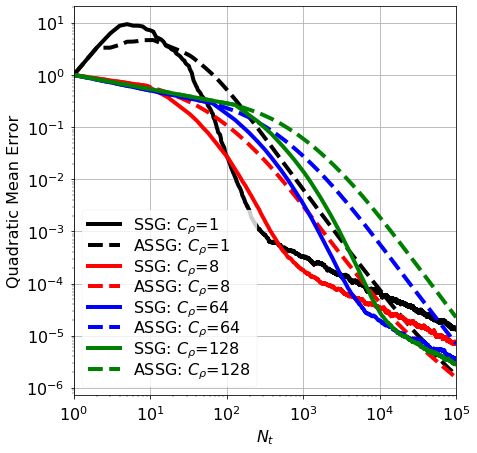

Variance reduction from larger mini-batches. Not surprisingly, larger mini-batches cause a variance reducing effect, e.g., see the illustrations in section 5. Nevertheless, 10 explicitly shows the variance reducing effect in each term, which can help us better understand how to optimally tune the learning rate. In particular, the asymptotic term is divided by , implying we should take when is large. However, this must be done with moderation as larger mini-batches simultaneously damage the sub-exponential term. Another important point from this is that mini-batches do not provide a better convergence rate, but simply scale, i.e., the slope of the rate of convergence is unchanged, but the intercept is lowered (e.g., see figure 1(a)).

Having fixed size mini-batches is not the most realistic streaming framework, these mini-batches are much more likely to vary in size over time. For the convenience of notation, let .

Corollary 2 (SSG/PSSG with time-varying mini-batches).

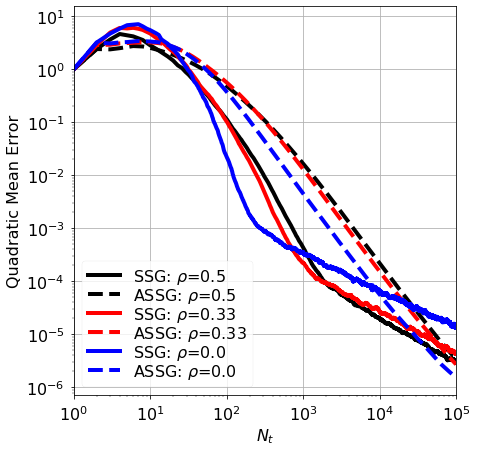

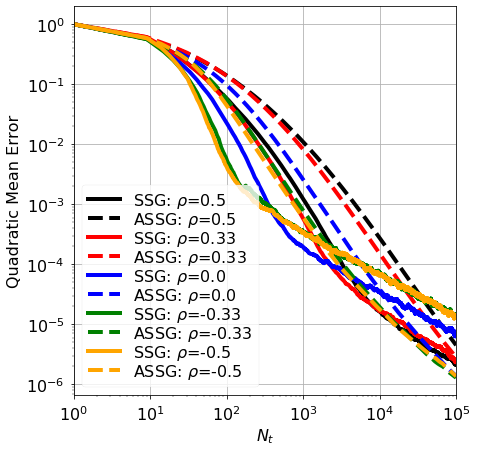

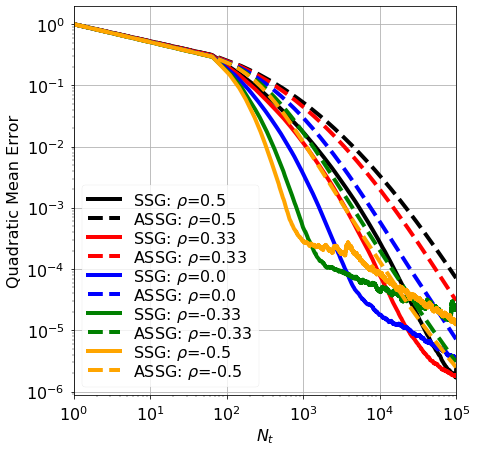

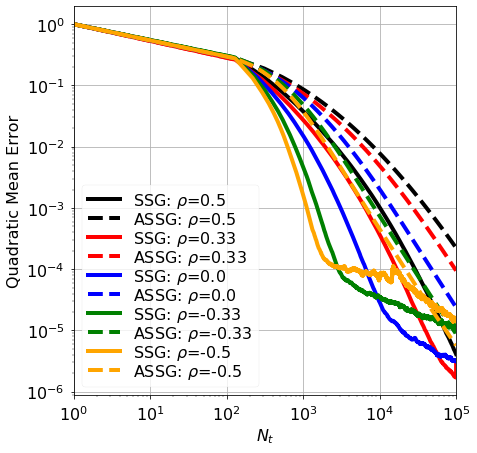

Accelerated decay with increasing mini-batches. As mentioned for Corollary 1, is a natural condition from Robbins and Monro [33]; this relaxes the condition of having for . In particular, this shows that we can accelerate convergence by taking increasing mini-batches, e.g., taking and yields when . Conversely, when , we obtain the same decay as in Corollary 1, namely, . These effects are illustrated in figures 1(b), 1(c), 1(d), and 1(e) for .

Variance reduction from larger mini-batches. Similarly to Corollary 1, the sub-exponential and asymptotic term is scaled by for , implying we should take to obtain variance reduction. However, as discussed above, this variance reduction is only beneficial in the beginning and does not contribute to a better convergence rate (relative to the slope). Thus, large mini-batch sizes and negative mini-batch rates will give (an initial) variance reduction but the same convergence rate as in Corollary 1.

4.2. Polyak-Ruppert averaging

In what follows, we consider the Polyak-Ruppert averaging estimate given in 7, where follows the recursion in 5 or 6. Besides having Assumptions 4-p and 5-p to hold for , additional assumptions are needed for bounding the Polyak-Ruppert averaging estimate. First, we make an additional smoothness assumption on the objective function .

Assumption 6 (-Lipschitz continuous Hessian operator).

The function is twice differentiable with -Lipschitz continuous Hessian operator , meaning, there exists such that ,

| (12) |

Next, in continuation of Assumption 5-p, we make the following assumption about covariance of , which we interpret as the sequence of score vectors with respect to the parameter vector .

Assumption 7 (Covariance of the scores).

There exists a non-negative self-adjoint operator such that .

Note that the operator always exists when is finite for order in Assumption 5-p.

4.2.1. Polyak-Ruppert averaging of stochastic streaming gradients (ASSG)

As in section 4.1, we conduct a general study for any learning rate and time-varying mini-batch when applying the Polyak-Ruppert averaging estimate from 7, where follows the recursion in 5, i.e., the ASSG.

Theorem 2 (ASSG).

As noticed in Polyak and Juditsky [32], the leading term achieves the Cramer-Rao lower bound [27, 10]. Note that the leading term is invariant of the learning rate and the time-varying mini-batches . Moreover, the bound is without inverting the Hessian. Next, the processes and can be bounded by the recursive relations in 8 and 23. There are no sub-exponential decaying terms for the initial conditions in Theorem 2, which is a common problem for averaging. However, as mentioned previously, we are more interested in advancing the decay of the asymptotic terms. To ease notation, we make use of the functions , given as

with , such that for any . Note that if , if , and if . Hence, for any , , where the notation hides logarithmic factors.

Corollary 3 (ASSG with constant mini-batches).

Accelerated decay the initial conditions. By averaging, we have increased the rate of convergence from to the optimal rate (when we compare to SSG with constant mini-batches in Corollary 1). The two subsequent terms are the main remaining terms decaying at the rate and , which suggest taking . The remaining terms are negligible. Next, it is worth noting that having in Corollary 3, we would give no impact in the main remaining terms from the mini-batch size . At last, as we do not rely on sub-exponentially decaying terms, we need to be more careful when picking our hyper-parameters, e.g., taking too large may cause to be significant. Nevertheless, the term consisting of decay at a rate of at least .

Corollary 4 (ASSG with time-varying mini-batches).

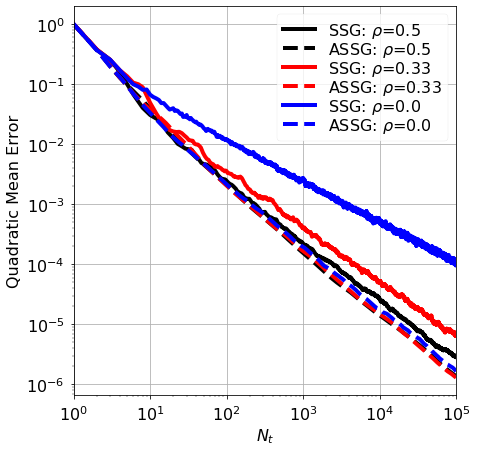

Robustness towards mini-batch rate : Following the arguments above, the two main remainder terms suggest that , e.g., by setting , we should pick . Likewise, if , we yield the same conclusion as in Corollary 3, namely . However, these hyper-parameter choices are not resilient against any time-varying streaming rate . Nonetheless, we can robustly achieve for any by setting and . In other words, we can achieve the same convergence for any time-varying mini-batch rate by having and ; this is illustrated in figures 1(f) and 2(f).

4.2.2. Polyak-Ruppert averaging of projected stochastic streaming gradients (APSSG)

In this section, we analyze the projected Polyak-Ruppert averaging estimate (a.k.a. APSSG), where follows the recursion in 6. To avoid calculating the six-order moment, we make the unnecessary assumption that is uniformly bounded on ; the derivation of the six-order moment can be found in Godichon-Baggioni [12].

Assumption 8 (-bounded stochastic gradients).

Let with denoting the frontier of . Assume there exists such that , a.s., with .

Corollary 5 (APSSG with constant mini-batches).

Corollary 6 (APSSG with time-varying mini-batches).

5. Experiments

In this section, we demonstrate the theoretical results presented in section 4 for various time-varying mini-batches. The performance is measured over one-hundred replications of the quadratic mean error, i.e., and . Note that averaging over several replications gives a reduction in variability, which mainly benefits the SSG and PSSG. All metrics are shown in log-scale and normalized such that the first iteration is one, namely, .

5.1. Linear regression

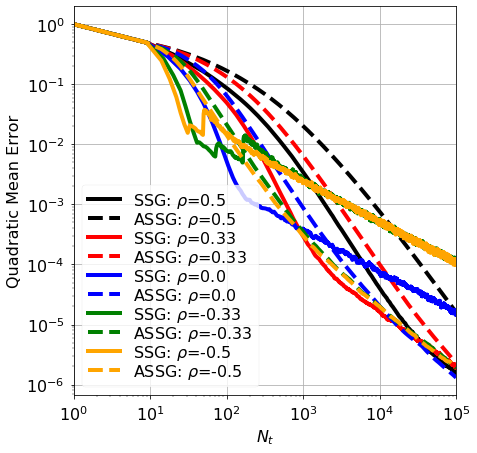

We continue the generic notation from section 2, where the linear regression is defined by , where is the measure, is a random feature vector, is the parameters vector, and is a random variable with zero mean, and and are independent and identically distributed. Thus, is the minimizer of . In this example, we fix , set , and let and be standard Gaussian. It is well-known that can substantially impact convergence; when is too large, instability can occur, leading to an explosion during the first iterations. If is too small, the convergence can become very slow and destroy the desired learning rate. To focus on the various time-varying mini-batches, we set and .

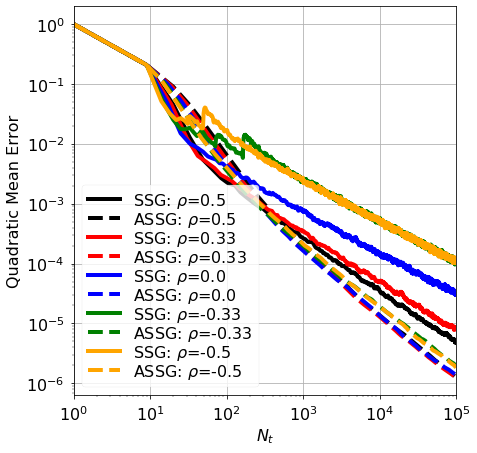

Discussion. In figure 1(a), we consider constant mini-batches to illustrate the results in Corollaries 1 and 3. This figure show a solid decay rate proportional to for any mini-batch size with , as shown in Corollary 1. In particular, the mini-batches does not provide better convergence rates, but simply scales the error, i.e. the slope of the rate of convergence is unchanged, but the intercept is lowered. As explained after Corollary 3, we see an acceleration in decay by averaging. Both algorithms show a noticeable reduction in variance when increases which are particularly beneficial in the beginning. Next, in figures 1(b), 1(c), 1(d), and 1(e), we vary the mini-batch rate for (fixed) mini-batch sizes , , , and , respectively, with . These figures shows an increase in decay of the SSG when the mini-batch rate increase. Despite this, we still achieve better convergence for the ASSG algorithm, which seems more immune to the different choices of mini-batch rate , e.g., see the discussion after Corollary 4. We know this from Corollary 2, as for . In addition, we see that has a positive effect on the noise (i.e., variance reduction), but if becomes too large, it may slow down convergence (as seen in figure 1(e)). Alternatively, we could think around the problem in another way: how can we choose and such that we have obtain decay of for any . In other words, for any arrival schedule that may occur, how should we choose our hyper-parameters such that we achieve decay of . As discussed after Corollary 4, one example of this could be achieved by setting and such that for any . Figure 1(f) shows an example of this where we (indeed) achieve the same decay rate for any mini-batch rate .

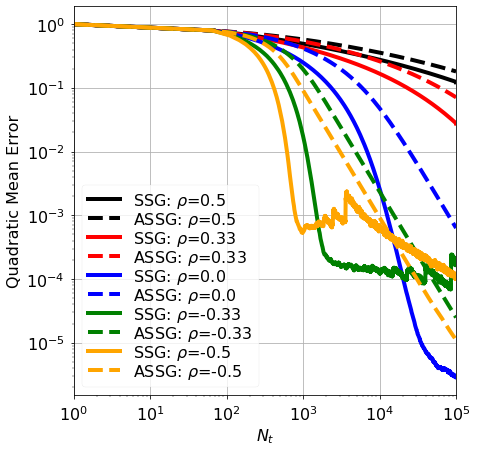

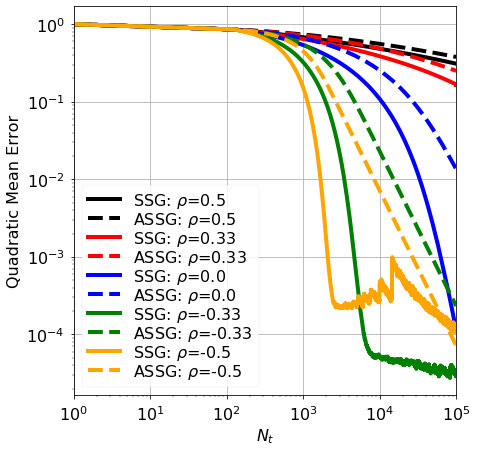

5.2. Geometric median

Robust estimators such as the geometric median may be preferred over the mean when the data is noisy; the geometric median is a generalization of the real median introduced by Haldane [17]. In addition, SG-based algorithms are preferred in our streaming framework, as they can process large samples of high-dimensional data efficiently [7, 12, 8]. The geometric median of is found by minimizing the objective using gradients of the form . Properties of this geometric median, such as existence, uniqueness and robustness, can be found in, e.g., Kemperman [20], Gervini [11]. Note that this objective function only possesses locally strong convexity properties [7]. But by projecting the gradients, one could adapt the proof of Gadat and Panloup [10] to a streaming setting. Otherwise, if is bounded, one can adapt Cardot et al. [6] to the streaming setting showing that the estimates are bounded, and there is no use to project it in this case. Similarly to section 5.1, we fix and let be standard Gaussian centered at . Moreover, following the reasoning of Cardot et al. [7], we set , and let .

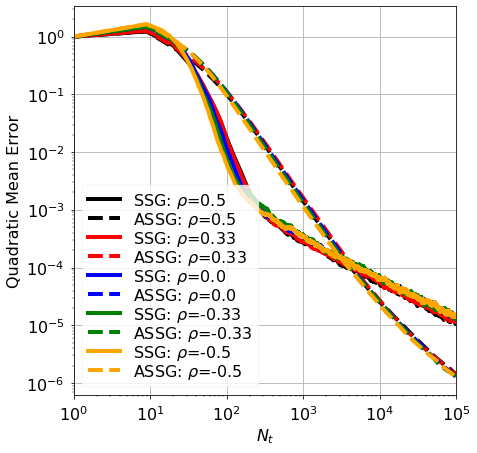

Discussion. Figure 2(a) shows the variance reduction effect for different constant mini-batches with . However, the robustness of the geometric median leaves only a small positive impact for further variance reduction. Thus, too large (constant) mini-batch sizes hinders the convergence as we make too few iterations. These findings can be extended to figures 2(b), 2(c), 2(d), and 2(e), where we vary the mini-batch rate for mini-batch sizes , , , and , respectively, with . The lack of convergence improvements comes from , which means we do not exploit the potential of using more observations to accelerate convergence. As shown in figure 2(f), we can achieve this acceleration by simply taking . In addition, provides improved convergence robust to any mini-batch rate . Choosing a proper is particularly important when is large, as robustness is an integral part of the geometric median.

6. Conclusions

We introduced a streaming framework for analyzing stochastic approximation/optimization problems. This streaming framework was analogous to solving optimization problems using time-varying mini-batches that arrive sequentially. We provided non-asymptotic convergence rates for different gradient-based algorithms; this included the famous Stochastic Gradient (SG) descent (a.k.a. Robbins-Monro algorithm), mini-batch SG, and time-varying mini-batch SG algorithms, as well as their iterated averages (a.k.a. Polyak-Ruppert averaging). We showed how time-varying mini-batches together with Polyak-Ruppert averaging can provide variance reduction and accelerate convergence simultaneously. We further demonstrated the beneficial effect of adapting learning to the time-varying mini-batches under different streaming settings.

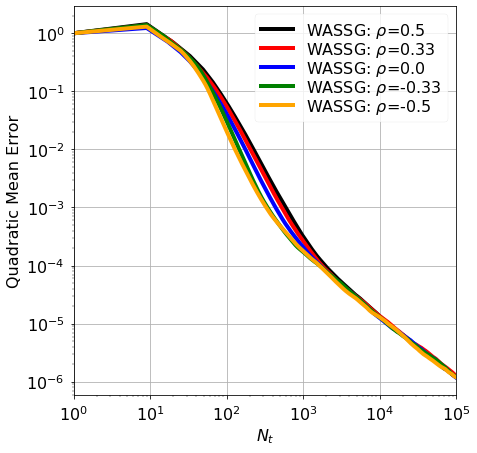

Future perspectives. There are several ways to expand our work: first, we can extend our analysis to include time-varying mini-batches of any size. Second, many machine learning problems encounter correlated variables and high-dimensional data, thus an extension to non-strongly convex objectives would be advantageous [2], e.g., in Werge and Wintenberger [39], they use SG-based algorithms to make adaptive volatility predictions through optimization of the GARCH model. Third, Assumption 3 requires unbiased (and independent) gradient estimates, thus, an obvious extension could incorporate a more realistic dependency assumption, thereby increasing the applicability. Moreover, studying dependence may give insight into how to process dependent information optimally. Next, a natural extension would be to modify our Polyak-Ruppert averaging estimate from 7 to a weighted averaged version [26, 5]:

| (WASSG) | (14) |

for with following 5 or 6. One can limit the effect of bad initializations by placing more weight on the newest estimates. Following the demonstrations in section 5, an example of this WASSG estimate can be found in figure 3(b) with use of . Here we see that although the WASSG estimate in 14 may not achieve a better final error (compared to the ASSG and APSSG estimates in figures 1(f) and 2(f)), it still achieves a better decay along the way, often referred to as parameter tracking.

The authors thank the anonymous reviewer for the valuable and helpful comments.

References

- Bach and Moulines [2011] F. Bach and E. Moulines. Non-asymptotic analysis of stochastic approximation algorithms for machine learning. Advances in neural information processing systems, 24, 2011.

- Bach and Moulines [2013] F. Bach and E. Moulines. Non-strongly-convex smooth stochastic approximation with convergence rate o (1/n). Advances in neural information processing systems, 26, 2013.

- Benveniste et al. [2012] A. Benveniste, M. Métivier, and P. Priouret. Adaptive algorithms and stochastic approximations, volume 22. Springer Science & Business Media, 2012.

- Bottou et al. [2018] L. Bottou, F. E. Curtis, and J. Nocedal. Optimization methods for large-scale machine learning. Siam Review, 60(2):223–311, 2018.

- Boyer and Godichon-Baggioni [2022] C. Boyer and A. Godichon-Baggioni. On the asymptotic rate of convergence of stochastic newton algorithms and their weighted averaged versions. Computational Optimization and Applications, pages 1–52, 2022.

- Cardot et al. [2012] H. Cardot, P. Cénac, and J.-M. Monnez. A fast and recursive algorithm for clustering large datasets with k-medians. Computational Statistics & Data Analysis, 56(6):1434–1449, 2012.

- Cardot et al. [2013] H. Cardot, P. Cénac, and P.-A. Zitt. Efficient and fast estimation of the geometric median in hilbert spaces with an averaged stochastic gradient algorithm. Bernoulli, 19(1):18–43, 2013.

- Cardot et al. [2017] H. Cardot, P. Cénac, and A. Godichon-Baggioni. Online estimation of the geometric median in hilbert spaces: Nonasymptotic confidence balls. The Annals of Statistics, pages 591–614, 2017.

- d’Aspremont [2008] A. d’Aspremont. Smooth optimization with approximate gradient. SIAM Journal on Optimization, 19(3):1171–1183, 2008.

- Gadat and Panloup [2023] S. Gadat and F. Panloup. Optimal non-asymptotic analysis of the ruppert–polyak averaging stochastic algorithm. Stochastic Processes and their Applications, 156:312–348, 2023.

- Gervini [2008] D. Gervini. Robust functional estimation using the median and spherical principal components. Biometrika, 95(3):587–600, 2008.

- Godichon-Baggioni [2016] A. Godichon-Baggioni. Estimating the geometric median in hilbert spaces with stochastic gradient algorithms: Lp and almost sure rates of convergence. Journal of Multivariate Analysis, 146:209–222, 2016.

- Godichon-Baggioni [2019] A. Godichon-Baggioni. Lp and almost sure rates of convergence of averaged stochastic gradient algorithms: locally strongly convex objective. ESAIM: Probability and Statistics, 23:841–873, 2019.

- Godichon-Baggioni [2021] A. Godichon-Baggioni. Convergence in quadratic mean of averaged stochastic gradient algorithms without strong convexity nor bounded gradient. arXiv preprint arXiv:2107.12058, 2021.

- Godichon-Baggioni and Portier [2017] A. Godichon-Baggioni and B. Portier. An averaged projected robbins-monro algorithm for estimating the parameters of a truncated spherical distribution. Electronic Journal of Statistics, 11(1):1890–1927, 2017.

- Gower et al. [2019] R. M. Gower, N. Loizou, X. Qian, A. Sailanbayev, E. Shulgin, and P. Richtárik. Sgd: General analysis and improved rates. In International conference on machine learning, pages 5200–5209. PMLR, 2019.

- Haldane [1948] J. Haldane. Note on the median of a multivariate distribution. Biometrika, 35(3-4):414–417, 1948.

- Hastie et al. [2009] T. Hastie, R. Tibshirani, J. H. Friedman, and J. H. Friedman. The elements of statistical learning: data mining, inference, and prediction, volume 2. Springer, 2009.

- Karimi et al. [2016] H. Karimi, J. Nutini, and M. Schmidt. Linear convergence of gradient and proximal-gradient methods under the polyak-łojasiewicz condition. In Joint European conference on machine learning and knowledge discovery in databases, pages 795–811. Springer, 2016.

- Kemperman [1987] J. Kemperman. The median of a finite measure on a banach space. Statistical data analysis based on the L1-norm and related methods (Neuchâtel, 1987), pages 217–230, 1987.

- Kurdyka [1998] K. Kurdyka. On gradients of functions definable in o-minimal structures. In Annales de l’institut Fourier, volume 48, pages 769–783, 1998.

- Kushner and Yin [2003] H. Kushner and G. G. Yin. Stochastic approximation and recursive algorithms and applications, volume 35. Springer Science & Business Media, 2003.

- Lan [2020] G. Lan. First-order and stochastic optimization methods for machine learning. Springer, 2020.

- LeCun et al. [2015] Y. LeCun, Y. Bengio, and G. Hinton. Deep learning. nature, 521(7553):436–444, 2015.

- Lojasiewicz [1963] S. Lojasiewicz. A topological property of real analytic subsets. Coll. du CNRS, Les équations aux dérivées partielles, 117(87-89):2, 1963.

- Mokkadem and Pelletier [2011] A. Mokkadem and M. Pelletier. A generalization of the averaging procedure: The use of two-time-scale algorithms. SIAM Journal on Control and Optimization, 49(4):1523–1543, 2011.

- Murata and Amari [1999] N. Murata and S.-i. Amari. Statistical analysis of learning dynamics. Signal Processing, 74(1):3–28, 1999.

- Necoara et al. [2019] I. Necoara, Y. Nesterov, and F. Glineur. Linear convergence of first order methods for non-strongly convex optimization. Mathematical Programming, 175(1):69–107, 2019.

- Nemirovski et al. [2009] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization, 19(4):1574–1609, 2009.

- Nesterov et al. [2018] Y. Nesterov et al. Lectures on convex optimization, volume 137. Springer, 2018.

- Polyak [1963] B. T. Polyak. Gradient methods for minimizing functionals. Zhurnal Vychislitel’noi Matematiki i Matematicheskoi Fiziki, 3(4):643–653, 1963.

- Polyak and Juditsky [1992] B. T. Polyak and A. B. Juditsky. Acceleration of stochastic approximation by averaging. SIAM journal on control and optimization, 30(4):838–855, 1992.

- Robbins and Monro [1951] H. Robbins and S. Monro. A stochastic approximation method. The annals of mathematical statistics, pages 400–407, 1951.

- Ruppert [1988] D. Ruppert. Efficient estimations from a slowly convergent robbins-monro process. Technical report, Cornell University Operations Research and Industrial Engineering, 1988.

- Schmidt et al. [2011] M. Schmidt, N. Roux, and F. Bach. Convergence rates of inexact proximal-gradient methods for convex optimization. Advances in Neural Information Processing Systems, 24:1458–1466, 2011.

- Shalev-Shwartz et al. [2012] S. Shalev-Shwartz et al. Online learning and online convex optimization. Foundations and Trends® in Machine Learning, 4(2):107–194, 2012.

- Steinwart and Christmann [2011] I. Steinwart and A. Christmann. Estimating conditional quantiles with the help of the pinball loss. Bernoulli, 17(1):211–225, 2011.

- Teo et al. [2007] C. H. Teo, A. Smola, S. Vishwanathan, and Q. V. Le. A scalable modular convex solver for regularized risk minimization. In Proceedings of the 13th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 727–736, 2007.

- Werge and Wintenberger [2022] N. Werge and O. Wintenberger. Adavol: An adaptive recursive volatility prediction method. Econometrics and Statistics, 23:19–35, 2022.

- Zinkevich [2003] M. Zinkevich. Online convex programming and generalized infinitesimal gradient ascent. In Proceedings of the 20th international conference on machine learning (icml-03), pages 928–936, 2003.

Appendix A Proofs

In this appendix, we provide detailed proofs of the results. Purely technical results used in the proofs can be found in appendix B. Let be an increasing family of -fields, namely with . Furthermore, we expand the notation with such that . Meaning, , we have . Thus, by the independence of the differentiable random functions , Assumption 3 yields that , with .

A.1. Proofs for section 4

The section is structured such that we start by analyzing the recursive relations and bounding them for every choice of learning rate and time-varying mini-batch . Next, we look at specific choices of and .

Proof of Theorem 1.

Taking the quadratic norm on both sides of 5, expanding it, and take the conditional expectation, yields

| (15) |

To bound the second term (on the right-hand side) of 15, we first expand it as follows,

| (16) |

For first term of 16, we utilize the Lipschitz continuity of , together with Assumptions 3, 4-p, and 5-p, to obtain

| (17) |

using . Next, for the second term in 16: as for all , we have

since and are -measurable for all , and similarly, as is -measurable and -measurable for all , we also have

where as is -Lipschitz continuous and . Thus, we obtained a bound for the second term (on the right-hand side) of 15 using the bounds of the two terms in 16:

| (18) |

For the third term (on the right-hand side) of 15 we use that is -quasi-strong convex and is -measurable,

| (19) |

by Assumption 3. Combining the inequalities from 19 and 18 into 15 and taking the expectation on both sides of the inequality, yields the recursive relation (9):

with with some . At last, by Proposition 5, we obtain the desired inequality in 8, namely

using that , , and that . ∎

Proof of Corollary 1.

By Theorem 1, we have the upper bound giving as

| (20) |

as , with . The sum term in can be bounded with the help of integral tests for convergence, , as . Likewise, plugging into the first term of 20, gives

using the integral test for convergence. Next, as is decreasing, then . Combining all these findings into 20, gives us

| (21) |

with . At last, converting 21 into terms of using , yields the desired. ∎

Proof of Corollary 2.

For convenience, we divided the proof into two cases to comprehend that for all . First, we bound each term of 8 (from Theorem 1) after inserting and into the inequality. Here, we use if , if , and for . Thus, for , the first term of 8 can be bounded, as follows:

using that and the integral test for convergence. In a same way, for , one has

Likewise, with the help of integral tests for convergence, we have for , that , as and . For , one has since . Next, as for , then we can bound the last term of 8 by

using . Likewise, if , we have

since and . Combining all these findings gives

| (22) |

where with and . To write this in terms of , we use the bounds following bounds: for , we have that

thus, . Similarly, for , we have that , i.e, . ∎

A.2. Proofs for section 4.2

Lemma 1 (ASSG/APSSG).

Proof of Lemma 1.

We will now derive the recursive step sequence for the fourth-order moment using the same arguments as in proof for Theorem 1. Thus, one can show that

using is measurable. Note, by Assumption 3, we have

as is -quasi-strong convex. Combining this with Cauchy-Schwarz inequality (i.e., ), we obtain the simplified expression:

Next, recall Young’s inequality for products, i.e., for any , we have ,

giving us

| (24) |

To bound the second and fourth-order terms in 24, we would need to study the recursive sequences: firstly, utilizing the Lipschitz continuity of , together with Assumptions 4-p and 5-p, and that is -measurable (Assumption 3), we obtain

| (25) |

for any using the bound . Thus, we can bound the second-order term in 24 by

| (26) |

following the same steps in the proof of Theorem 1, but with use of 25. Bounding the fourth-order term is a bit heavier computationally, but let us recall that . Then, we have that

| (27) |

as . For the first term of 27, we have

using the bound from 25, , and that for all . To bound the second term of 27, we ease notation by denoting by , giving us

By Cauchy-Schwarz inequality, we can bound the first term , by

using that for all . Next, since implies , we have

using Cauchy-Schwarz inequality and the bound in 25. In the same way, as includes , we can rewrite as

where . Finally, we can rewrite as

where , and

Thus, the fourth-order term of 24, is bounded by

| (28) |

Combining the bound from 26 and 28 into 24, we can bound the fourth-order moment by the recursive relation:

By Young’s inequality for products, one have

which yields the bound on ,

| (29) |

Taking, the expectation on both sides of the inequality in 29 yields the recursive relation for the fourth-order moment:

| (30) |

with for some . By Proposition 5, we achieve the (upper) bound of in 30, given as

where is given by

| (31) |

with use of

At last, bounding the projected estimate 6 follows from that , . ∎

A.2.1. Proofs for section 4.2.1

Proof of Theorem 2.

Following Polyak and Juditsky [32], we rewrite 5 to

| (32) |

where denotes . Observe that

where is invertible with lowest eigenvalue greater than , i.e., . Thus, summing the parts and using the Minkowski’s inequality, we obtain the inequality:

As is a square-integrable martingale increment sequences on (Assumption 3), we have

| (33) |

using Assumption 7. To ease notation, we denote by . Next, note that for all , we have the relation in 32, giving us

leading to

Hence, with the notion of this expression can be simplified to

| (34) |

For the martingale term, we have

| (35) |

by Cauchy-Schwarz inequality and Assumption 4-p. For all , the rest term is directly bounded by 12:

| (36) |

with the notion . Finally, combining the terms from 33, 34, 35, and 36, gives us

| (37) |

where , which can be simplified into 13 by shifting the indices and collecting the terms. ∎

Proof of Corollary 3.

As for all , we simplify the bound for in 13 to

| (38) |

The second-order moment is bounded by Corollary 1 but with use of 21 as we work in terms of . The fourth-order moment from Lemma 1 can be simplified to:

using that is decreasing as . Regarding defined in 31, we can bound it by

using and . Note that is a finite constant, independent of . To bound the first term of 38, namely , we remark that , one has (since ),

| (39) |

For simplicity, let us denote

as . Thus, the first part of 39 is bounded as follows:

Furthermore, with the help of an integral test for convergence, one has , such that the second part of 39 can be bounded by

By combining this, we get

| (40) |

Similarly, second term of 38, can be bounded by

using as is decreasing. In a same way, one has

Bound the last term of 38, is done as follows,

Thus, by collecting the terms above, we obtain:

where . ∎

Proof of Corollary 4.

The steps of the proof follows the ones of Corollary 3 with the smart notation of and : The bound for in 13 is given by

| (41) |

where the learning rate and time-varying mini-batches are on the form and . The second-order moment is upper bounded by 22 from Corollary 2. The fourth-order moment from Lemma 1 can be simplified as follows,

as for any and , and

using that for . Next, for , we have

using that . If , one directly have

With the notion of and , we can combine the two -cases as follows:

We will in the following bound the terms for but afterwards we will translate it to terms in . If , the first relation is , e.g., see the proof of Corollary 2. Similarly, , thus, . If , one has and , i.e., .

Bounding , we first note that . Thus, by the mean value inequality, we obtain for :

| (42) |

as since . For , the mean value inequality gives us

as is a decreasing sequence and . Thus, for any , we have

By using this, we obtain a bound on given as

Next, let us denote

since . Thus,

Furthermore, with the help of an integral test for convergence, we have

Summarising, we obtain

Similarly, for , one have

For , we insert the definition of our learning functions, giving us

Bounding , follows the ideas from above, using that ; it can be upper bounded by

Likewise, for , we can bound by

where the second term can be bounded as

and the third term by

By collecting these bounds, we get

Combining our findings from above, we have

This can be simplified to the desired using given by , consisting of the finite constants , and . ∎

A.2.2. Proofs for section 4.2.2

Theorem 3 (APSSG).

Proof of Theorem 3.

Denote by with given by 7 using from 6. As in the proof Theorem 2, we follow the steps of Polyak and Juditsky [32], in which, we can rewrite 6 to

where and . Thus, summing the parts, using the Minkowski’s inequality, and bounding each term gives us the same bound as in Theorem 2, but with an additional term regarding , namely

| (43) |

using Godichon-Baggioni [12, Lemma 4.3]. Next, we note that , since

as is Lipschitz and for any . Moreover, as in Godichon-Baggioni and Portier [15, Theorem 4.2], we know that , where with denoting the frontier of . Thus, 43 can then be bounded by

using that the sequence is either constant or time-varying, meaning . ∎

Proof of Corollary 5.

The proof follows directly from Corollary 3 with use of Theorem 3. ∎

Proof of Corollary 6.

The proof follows directly from Corollary 4 with use of Theorem 3. ∎

Appendix B Technical propositions

Appendix B contains purely technical results used in the proofs presented in appendix A. In what follows, we use the convention , , and .

Proposition 1.

Let be a positive sequence. For any , and , we have

| (44) |

Proof of Proposition 1.

Proposition 2.

Let be a positive sequence. Let and such that for all , , then

| (45) |

Proof of Proposition 2.

Proposition 3.

Let and be positive sequences. For any , we can obtain the (upper) bounds:

| (46) |

with . Furthermore, suppose that for all , , then

| (47) |

Proof of Proposition 3.

We obtain the inequality in 46 directly by Proposition 1:

Similarly, for the inequality in 47, we have

by Proposition 2. ∎

Proposition 4.

Let , , , and be some positive sequences satisfying the recursive relation:

| (48) |

with and . Denote , and suppose that for all , one has . Then, for and decreasing, we have the upper bound on :

| (49) |

for all with the convention that if .

Proof of Proposition 4.

Applying the recursive relation from 48 times, we derive:

where can be seen as a transient term only depending on the initialisation , and a stationary term . The transient term can be divided into two products, before and after ,

Using that , and since for all , we have , it comes

by applying the (simple) bound for all . We derive that

| (50) |

Next, the stationary term can (similarly) be divided into two sums (after and before ):

The first stationary term (with can be bounded as follows: if , we have

by Proposition 3. Furthermore, if , we get

where as for all . Thus, for all ,

| (51) |

where if . The second stationary term can be bounded, thanks to Proposition 1, as follows:

by the definition of , thus

| (52) |

Then, using the bound for in 51 and in 52, we can bound by

| (53) |

Finally, combining the bound for in 50 and in 53, we achieve the bound for , namely the upper bound in 49. ∎

The following proposition is a more simplistic but rougher version of the bound in Proposition 4.

Proposition 5.

Let , , , and be some positive sequences satisfying the recursive relation in 48. Denote , and suppose that for all , one has . Then, for and decreasing, we have for all ,

| (54) |