.tocmtchapter \etocsettagdepthmtchaptersubsubsection \etocsettagdepthmtappendixnone

On Tilted Losses in Machine Learning:

Theory and Applications

Abstract

Exponential tilting is a technique commonly used in fields such as statistics, probability, information theory, and optimization to create parametric distribution shifts. Despite its prevalence in related fields, tilting has not seen widespread use in machine learning. In this work, we aim to bridge this gap by exploring the use of tilting in risk minimization. We study a simple extension to ERM—tilted empirical risk minimization (TERM)—which uses exponential tilting to flexibly tune the impact of individual losses. The resulting framework has several useful properties: We show that TERM can increase or decrease the influence of outliers, respectively, to enable fairness or robustness; has variance-reduction properties that can benefit generalization; and can be viewed as a smooth approximation to the tail probability of losses. Our work makes connections between TERM and related objectives, such as Value-at-Risk, Conditional Value-at-Risk, and distributionally robust optimization (DRO). We develop batch and stochastic first-order optimization methods for solving TERM, provide convergence guarantees for the solvers, and show that the framework can be efficiently solved relative to common alternatives. Finally, we demonstrate that TERM can be used for a multitude of applications in machine learning, such as enforcing fairness between subgroups, mitigating the effect of outliers, and handling class imbalance. Despite the straightforward modification TERM makes to traditional ERM objectives, we find that the framework can consistently outperform ERM and deliver competitive performance with state-of-the-art, problem-specific approaches.

Keywords: Exponential tilting, empirical risk minimization, Value-at-Risk, superquantile optimization, fairness, robustness.

1 Introduction

Many statistical estimation procedures rely on the concept of empirical risk minimization (ERM), in which the parameter of interest, , is estimated by minimizing an average loss over the data :

| (1) |

Although ERM is widely used in machine learning, it is known to perform poorly in situations where average performance is not an appropriate surrogate for the problem of interest. Significant research has thus been devoted to developing alternatives to traditional ERM for diverse applications, such as learning in the presence of noisy/corrupted data (Khetan et al., 2018; Jiang et al., 2018), performing classification with imbalanced data (Lin et al., 2017; Malisiewicz et al., 2011), ensuring that subgroups within a population are treated fairly (Hashimoto et al., 2018; Samadi et al., 2018), or developing solutions with favorable out-of-sample performance (Duchi and Namkoong, 2019).

In this paper, we suggest that deficiencies in ERM can be flexibly addressed via a unified framework, tilted empirical risk minimization (TERM). TERM encompasses a family of objectives, parameterized by a real-valued hyperparameter, . For the -tilted loss (TERM objective) is given by:

| (2) |

TERM generalizes ERM as the -tilted loss recovers the average loss, i.e., .111 is defined in (20) via the continuous extension of . It also recovers other popular alternatives such as the max-loss () and min-loss () (Lemma ‣ 2.2). As we discuss below, although tilted risk minimization is not widely used in machine learning, variants of tilting have been extensively studied in related fields including statistics, applied probability, optimization, and information theory.

1.1 Perspectives on Exponential Tilting

We begin by defining exponential tilting and discussing uses of tilting in various fields. Let be a set of parametric distributions. For any , we let be the information of under , which is defined as (Cover and Thomas, 1991):

| (3) |

Further assume that is a random variable drawn from distribution which is not necessarily matched to , i.e., the model family may be misspecified. The cumulant generating function of the information random variable, can be stated as (Dembo and Zeitouni, 2009, Section 2.2):

| (4) |

where in this paper denotes expectation with respect to the true distribution unless otherwise stated. This expectation is commonly referred to as an exponential tilt of the information density, and can induce parametric distribution shifts that have varied applications in probability, statistics, and information theory. In particular, it is noteworthy that if is an exponential family of distributions parameterized by then the tilted distribution (when normalized by ) also belongs to the same exponential family. Further, given samples the empirical cumulant generating function is defined as:

| (5) |

It is thus evident that TERM (2) can be viewed as an appropriately scaled variant of the empirical cumulant generating function in (5). Although tilting of this form has been used in a number of related disciplines, uses of exponential tilting in machine learning are relatively unexplored. We provide several perspectives on exponential tilting from other fields below.

Statistics.

Exponential tilting is well-known as a distribution shifting technique in statistics, where the main idea is to draw samples from an exponentially tilted version of the original distribution to improve the convergence properties of statistical estimation, especially when the distribution of interest belongs to an exponential family, such as Gaussian or multinomial. Common use cases include rejection sampling, rare-event simulation, saddle-point approximation (Butler, 2007, p. 156), and importance sampling (Siegmund, 1976).

Applied probability.

In large deviations theory, exponential tilting lies at the heart of deriving concentration bounds. For example, Chernoff bounds apply Markov’s inequality to which results in a parametric set of bounds by using exponential tilts of various orders. The bound may then be further optimized on the real tilt value to derive the tightest possible bound (Dembo and Zeitouni, 2009).

Information theory.

While source coding limits and channel capacity are characterized by Shannon entropy and Shannon mutual information (which are simple averages over the information (3)) (Cover and Thomas, 1991), there are other elements of information theory that are not characterized by the average, such as error exponents in channel decoding (Gallager, 1968), probability of error in list decoding (Merhav, 2014), and computational cost in sequential decoding (Massey, 1994; Arıkan, 1996). These fundamental elements of information theory are asymptotically determined by a non-zero tilted cumulant generating function of the information random variable (3) (see (Beirami et al., 2018) for further discussion).

Optimization.

Exponential tilting has also appeared as a minimax smoothing approach in optimization (Kort and Bertsekas, 1972; Pee and Royset, 2011; Liu and Theodorou, 2019). Such smooth approximations to the max often appear through LogSumExp functions, with applications in geometric programming (Calafiore and El Ghaoui, 2014, Sec. 9.7), and boosting (Mason et al., 1999; Shen and Li, 2010). We discuss min-max objectives and the connections with TERM in several subsequent sections of the paper.

Machine learning.

Despite the rich history of tilted objectives in related fields, they have not seen widespread use in ML beyond limited applications such as robust regression (Wang et al., 2013) and sequential decision making (Howard and Matheson, 1972; Borkar, 2002). In this work, we argue that tilting is a critical yet undervalued tool in machine learning. We demonstrate the effectiveness of tilting by (i) rigorously studying properties of the TERM objective, and (ii) exploring its utility for a wide range of ML applications. Surprisingly, we find that this simple extension to ERM can match or exceed state-of-the-art performance from highly tuned, bespoke solutions to common ML problems, from learning with noisy data to ensuring fair performance between subgroups. We highlight several motivating applications of TERM below and provide an outline of the remainder of the paper in Section 1.3.

1.2 Motivating Examples

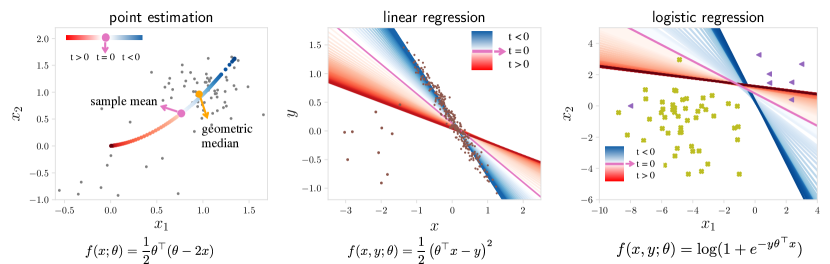

To motivate how the TERM objective (2) may be used in machine learning, we provide several running examples below, which are illustrated in Figure 1.

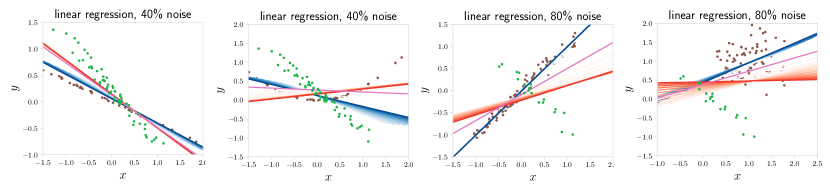

(a) Point estimation: As a first example, consider determining a point estimate from a set of samples that contain some outliers. We plot an example 2D dataset in Figure 1a, with data centered at (1,1). Using traditional ERM (i.e., TERM with ) recovers the sample mean, which can be biased towards outlier data. By setting , TERM can suppress outliers by reducing the relative impact of the largest losses (i.e., points that are far from the estimate) in (2). A specific value of can in fact approximately recover the geometric median, as the objective in (2) can be viewed as approximately optimizing specific loss quantiles (a connection which we make explicit in Section 2). In contrast, if these ‘outlier’ points are important to estimate, setting will push the solution towards a point that aims to minimize variance, as we prove in Section 2, Theorem 33.

(b) Linear regression: A similar interpretation holds for the case of linear regression (Figure 2b). As TERM finds a line of best while ignoring outliers. However, this solution may not be preferred if we have reason to believe that these ‘outliers’ should not be ignored. As TERM recovers the min-max solution, which aims to minimize the worst loss, thus ensuring the model is a reasonable fit for all samples (at the expense of possibly being a worse fit for many). Similar criteria have been used, e.g., in defining notions of fairness (Hashimoto et al., 2018; Samadi et al., 2018). We explore several use-cases involving robust regression and fairness in more detail in Section 7.

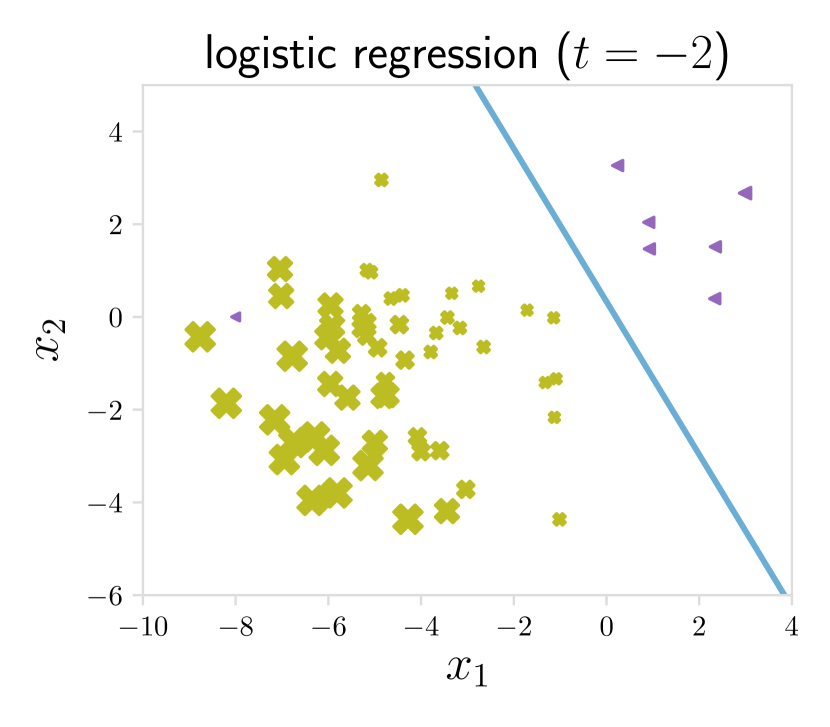

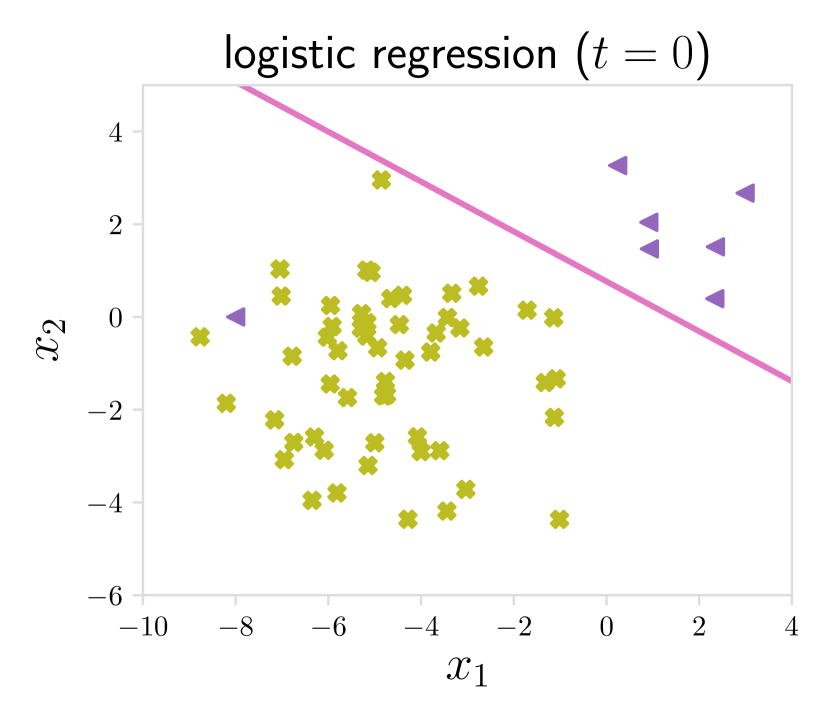

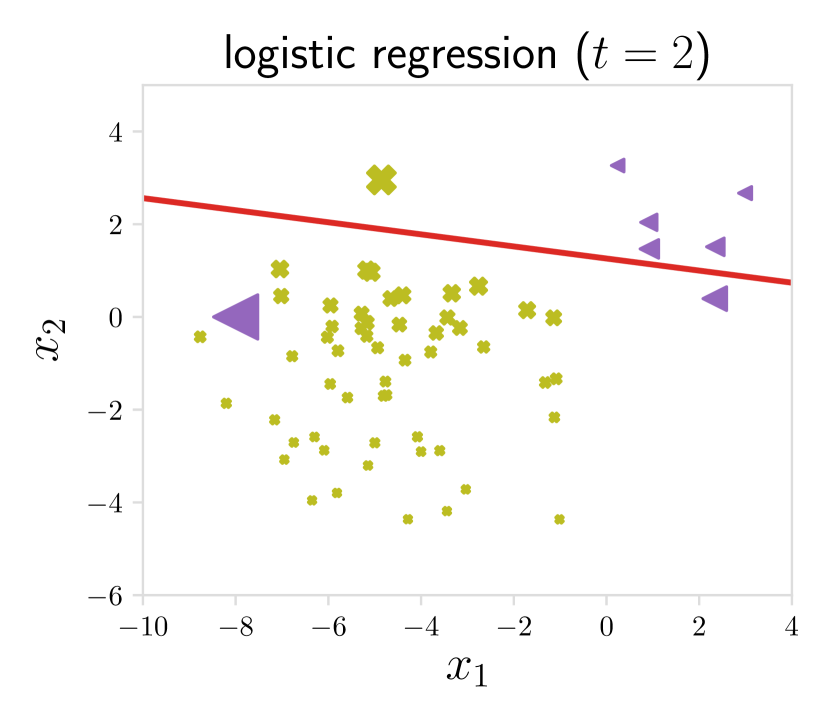

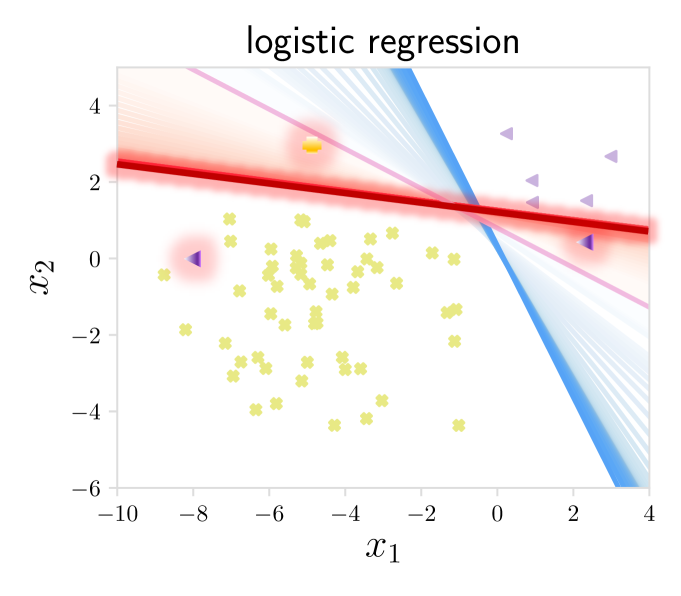

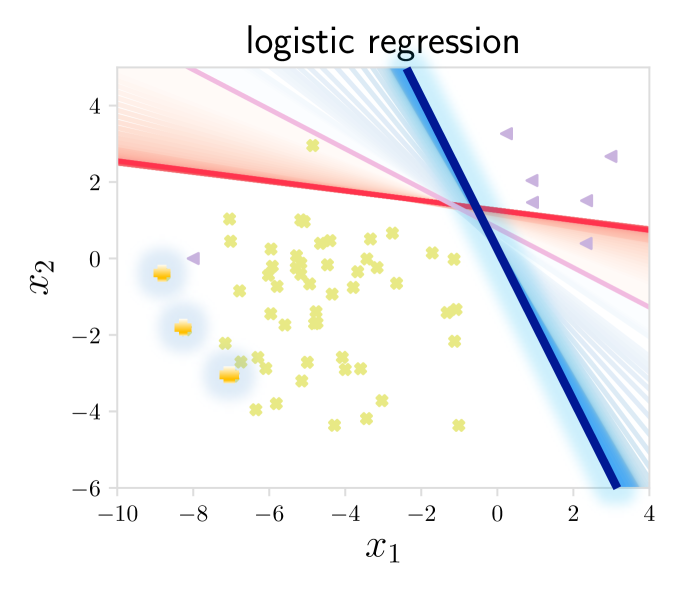

(c) Logistic regression: Finally, we consider a binary classification problem using logistic regression (Figure 2c). For , the TERM solution varies from the nearest cluster center (), to the logistic regression classifier (), towards a classifier that magnifies the misclassified data (). We note that it is common to modify logistic regression classifiers by adjusting the decision threshold from , which is equivalent to moving the intercept of the decision boundary. This is fundamentally different than what is offered by TERM (where the slope is changing). As we show in Section 7, this added flexibility affords TERM with competitive performance on a number of classification problems, such as those involving noisy data, class imbalance, or a combination of the two.

1.3 Contributions

In this work, we explore the use of tilting in machine learning through TERM, a simple, unified framework that can flexibly address various challenges with empirical risk minimization. We first analyze the objective and its solutions, showcasing the behavior of TERM with varying tilt parameters (Section 2). We also establish connections between TERM and related approaches such as distributionally robust optimization in Section 3.

We rigorously analyze the relations between TERM and other risks (e.g, Value-at-Risk (VaR), Conditional Value-at-Risk (CVaR), and Entropic Value-at-Risk (EVaR)) in Section 4. In particular, we introduce a new risk measure based on TERM, called Tilted Value-at-Risk (TiVaR), to approximate VaR. We show that TiVaR can provide a better approximation of VaR than CVaR in certain regimes, and improves upon EVaR in all regimes.

We develop efficient first-order batch and stochastic methods for solving TERM, both for hierarchical and non-hierarchical cases (Section 5 and 6). We provide convergence rates scaling with the hyperparameter on both convex and non-convex problems for both batch and stochastic algorithms. Our solvers run within 2–3 wall-clock time compared with that of ERM in all explored case studies.

Finally, we show via numerous case studies that TERM is competitive with existing, problem-specific state-of-the-art solutions (Section 7). We also extend TERM to handle compound issues, such as the simultaneous existence of noisy samples and imbalanced classes (Section 6). Our results demonstrate the effectiveness and versatility of tilted objectives in machine learning.

We note that the material in this paper was presented in part at ICLR 2021 (Li and Beirami et al., 2021). Compared to this earlier work, the current manuscript provides additional historical background of tilting (Section 1), establishes stronger and novel relationships between tilted losses and other risk-averse objectives in the literature (Section 3 and Section 4), provides convergence guarantees for our stochastic solver of TERM (Section 5), offers comprehensive details on applications of the framework in practice, and considers new applications of TERM to meta-learning and heteroskedastic deep learning (Section 7).

Outline.

This paper is organized as follows. We discuss general properties and interpretations of TERM in Section 2. We connect TERM with other prior risk measures in Section 3 and propose a new risk motivated by TERM in Section 4. In Section 5, we develop both batch and stochastic algorithms for optimizing TERM and provide convergence guarantees for them. We extend TERM to hierarchical multi-objective tilting in Section 6 and demonstrate the flexibility and competitive performance of the TERM framework via real-world applications in Section 7. We discuss related work in Section 8 and conclude the paper with Section 9.

2 TERM: Properties and Interpretations

To better understand the performance of the -tilted losses in (2), in this section we provide several interpretations of the TERM solutions, leaving the full proofs to the appendix. We make no distributional assumptions on the data, and study properties of TERM under the assumption that the loss function forms a generalized linear model, e.g., loss and logistic loss. However, we also obtain favorable empirical results using TERM with other objectives such as PCA and deep neural networks in Section 7, motivating the extension of this part of our theory beyond GLMs in future work.

2.1 Assumptions

We first provide notation and assumptions that are used throughout our theoretical analyses. The results in this paper are derived under one of the following three nested assumptions (the assumptions become progressively more restrictive, i.e., ):

Assumption 1 (Continuous differentiability).

For the loss function belongs to the differentiability class (i.e., continuously differentiable) with respect to

Assumption 2 (Smoothness and strong convexity condition).

Assume that Assumption 1 is satisfied. In addition, for any , belongs to differentiability class (i.e., twice differentiable with continuous Hessian) with respect to . We further assume that there exist such that for and any

| (6) |

where is the identity matrix of appropriate size (in this case ), and there does not exist any such that for all

Assumption 3 (Generalized linear model condition (Wainwright and Jordan, 2008)).

Assume that Assumption 2 is satisfied. Further, assume that the loss function is given by

| (7) |

where is a convex function such that there exists where for any

| (8) |

and

| (9) |

This set of assumptions become the most restrictive with Assumption 3, which essentially requires that the loss be the negative log-likelihood of an exponential family. While the assumption is stated using the natural parameter of an exponential family for ease of presentation, the results hold for any bijective and smooth reparameterization of the exponential family. For example, Assumption 3 is satisfied by the commonly used loss for regression and logistic loss for classification (see toy examples (b) and (c) in Figure 1). assumes a reasonable regularity on the dataset . For instance, in the case of linear regression (), it reduces to the standard regularity assumption (where ). While Assumption 3 is not satisfied when we use neural network function approximators in Section 7, we observe favorable numerical results motivating the extension of these results beyond the cases that are theoretically studied in this paper.

In the sequel, many of the results are concerned with characterizing the -tilted solutions defined as the parametric set of solutions of -tiled losses by sweeping ,

| (10) |

where is an open subset of Further, let the optimal tilted objective be defined as

| (11) |

We state a final assumption, on , below.

Assumption 4 (Strict saddle property (Definition 4 in Ge et al. (2015))).

We assume that the set is non-empty for all . Further, we assume that for all is a “strict saddle” as a function of , i.e., for all local minima, , and for all other stationary solutions, , where is the minimum eigenvalue of the matrix.

We use the strict saddle property in order to reason about the properties of the -tilted solutions. In particular, since we are solely interested in the local minima of the strict saddle property implies that for every for a sufficiently small , for all

| (12) |

where denotes a -ball of radius around We will show later in Section 2.2 that the strict saddle property is readily verified for under Assumption 2, and we need Assumption 4 to be able to reason about .

2.2 General Properties of TERM

We begin by noting several general properties of the TERM objective (2). In particular: (i) is -Lipschitz continuous in if is -Lipschitz (Lemma ‣ 2.2); (ii) If is strongly convex, the -tilted loss is strongly convex for (Lemma ‣ 2.2); and (iii) Given a smooth , the -tilted loss is smooth for all finite (Lemma ‣ 2.2). We state these properties more formally below.

Lemma 0 (Lipschitzness of ).

For any and , if for , is -Lipschitz conditnuous in , then is -Lipschitz in .

Lemma 0 (Tilted Hessian and strong convexity for ).

Under Assumption 2, for any

| (13) | ||||

| (14) |

In particular, for all and all the -tilted objective is strongly convex. That is

| (15) |

Lemma ‣ 2.2 and ‣ 2.2 are proved in Appendix A. Lemma ‣ 2.2 also implies that under Assumption 2, the strict saddle assumption (Assumption 4) is readily verified.

Lemma 0 (Smoothness of ).

For any , let be the smoothness parameter of twice differentiable :

| (16) |

where is the Hessian of at and denotes the largest eigenvalue. Under Assumption 2, for any is a -smooth function of . Further, for 222 denotes the set of non-positive real numbers.

| (17) |

where is defined in Assumption 2. For

| (18) |

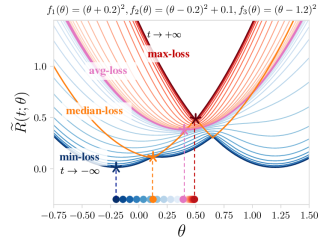

Lemma ‣ 2.2 (proved in Appendix A.1) indicates that -tilted losses are -smooth for all . is bounded for all negative and moderately positive , whereas it scales linearly with as , which has been previously studied in the context of exponential smoothing of the max (Kort and Bertsekas, 1972; Pee and Royset, 2011). This can also be observed visually via the toy example in Figure 2.

As discussed in Section 1, TERM can recover traditional ERM (), the max-loss (), and the min-loss (). We formally state this in Lemma ‣ 2.2 below.

Lemma 0.

Under Assumption 1,

| (19) | ||||

| (20) | ||||

| (21) |

where is the max-loss and is the min-loss333When the argument of the max-loss or the min-loss is not unique, for the purpose of differentiating the loss function, we define as the average of the individual losses that achieve the maximum, and as the average of the individual losses that achieve the minimum.:

| (22) |

Note that Lemma ‣ 2.2 has been studied or observed before in the entropic risk literature (e.g., Ahmadi-Javid, 2012), as well as other contexts (Cohen and Shashua, 2014). This lemma also implies that is the ERM solution, is the min-max solution, and is the min-min solution. In other words, a benefit of TERM is that it offers a continuum of solutions between the min and max losses.

Providing a smooth trade-off between these specific losses can be beneficial for a number of practical use-cases—both in terms of the resulting solution and the difficulty of solving the problem itself. We empirically demonstrate the benefits of such a trade-off in Section 7. We also visualize the solutions to TERM for a toy problem in Figure 2, which allows us to illustrate several special cases of the general framework. Interestingly, we additionally show that the TERM solution can be viewed as a smooth approximation to the tail probability of losses, which effectively minimizes quantiles of losses such as the median loss (Section 4). In Figure 2, it is clear to see why this may be beneficial, as the median loss (orange) can be highly non-smooth in practice. In Theorem ‣ 2.2 and ‣ 2.2 below, we formally characterize how tilted objectives change as a function of values (proofs provided in Appendix A).

Theorem 0 (Tilted objective is increasing with ).

Under Assumption 3, for all and all

| (23) |

Theorem 0 (Optimal tilted objective is increasing with ).

Under Assumption 3, for all and all

| (24) |

Recall that TERM as and corresponds to min-loss and max-loss, respectively. We discuss in Section 4.2 that solving TERM with any can indeed be viewed as approximately minimizing the -th smallest loss () among all individual losses. As we increase from to the corresponding value of sweeps in . Theorem ‣ 2.2 hence roughly states that the optimal -th smallest loss is non-decreasing with , which is intuitively expected.

We next provide two interesting interpretations of the TERM framework to further understand its behavior.

2.3 Interpretation 1: Re-Weighting Samples to Magnify/Suppress Outliers

As discussed via the toy examples in Section 1, TERM can be tuned (using ) to magnify or suppress the influence of outliers. We make this notion rigorous by exploring the gradient of the -tilted loss in order to reason about the solutions to the objective defined in (2).

Lemma 0 (Tilted gradient).

For a smooth loss function ,

| (25) |

where tilted weights are given by

| (26) |

Proof.

Lemma ‣ 2.3 provides the gradient of the tilted objective, which has been studied previously in the context of exponential smoothing (see Pee and Royset (2011, Proposition 2.1)). From this, we can observe that the tilted gradient is a weighted average of the gradients of the original individual losses, where each data point is weighted exponentially proportional to the value of its loss. Note that recovers the uniform weighting associated with ERM, i.e., . For positive this has the effect of magnifying the outliers—samples with large losses—by assigning more weight to them, and for negative it suppresses the outliers by assigning less weight to them (Figure 3).

Generalizing the notion of tilted gradients (weighted average of individual gradients), we define tilted empirical mean over any -vector below, which will be used throughout the paper.

Definition 0 (Tilted empirical mean and variance).

For , let weighted empirical mean with weights (where stands for dimensional simplex) be defined as

| (28) |

Tilted empirical mean is weighted empirical mean with tilted weights, i.e.,

| (29) | ||||

| (30) |

where is defined in Eq. (26), and is defined in Eq. (10). We also refer to as the “-tilted empirical mean”. Similarly, tilted empirical variance is defined as

| (31) | ||||

| (32) |

and we refer to as the “-tilted empirical variance”.

As discussed before, the full gradient of TERM is tilted empirical mean of individual gradients with weights proportional to . In the next section as well as Appendix A.3, we will prove other properties of TERM using tilted empirical mean and variance defined here.

2.4 Interpretation 2: Empirical Bias/Variance Trade-off

Another key property of the TERM solutions is that for any , -tilted empirical variance of the losses across all samples will decrease if we increase by a small amount of value. We formally stated this in Theorem 33.

Note that is -tilted empirical variance defined in Eq. (32). Hence, for any , the -tilted empirical variance among losses will decrease if we increase by a small value. When , reduces to standard empirical variance. In particular, Theorem 33 states that the empirical variance of the loss vector decreases if is chosen to be a small positive value. Therefore, it is possible to trade off between optimizing the average loss vs. reducing variance, allowing the solutions to potentially achieve a better bias-variance trade-off for generalization (Maurer and Pontil, 2009; Bennett, 1962; Hoeffding, 1994). At a high level, this property is consistent with and extends the approximation of TERM mentioned by Liu and Theodorou (2019, Section V.A), which approximates TERM as the empirical risk regularized with variance of the loss at . We rely on this property to achieve better generalization in classification in Section 7.

In addition to empirical variance across all losses, there are other related distribution uniformity measures. In Theorem ‣ 2.4 below, we also prove that entropy of the weight distribution at solution tilted by close to is increasing with , which indicates that larger ’s encourages more uniform solutions measured via entropy.

Theorem 0 (Gradient weights become more uniform by increasing ).

Full proofs of the theorems presented in this section can be found in Appendix A.3. In the next section, we connect TERM to other objectives. Note that the results in all subsequent sections do not require the GLMs assumption, unless stated otherwise.

3 Connections to Other Risk Measures

In this section (and subsequently in Section 4) we explore TERM by comparing, contrasting, and drawing connections between TERM and other common risk measures. To do so, we first introduce a distributional version of TERM, which is closely related to entropic risk (measure) in previous literature (Ahmadi-Javid, 2012; Föllmer and Schied, 2004). Entropic risk, denoted as , can be viewed as the scaled cumulant generating function of , i.e.,

| (36) |

We note that entropic risk is usually defined over in the literature (Föllmer and Schied, 2004). In Eq. (36) above, we naturally extend its definition to support . The TERM objective is the empirical version of entropic risk (). One of the contributions of this work can be viewed as providing an operational meaning to the value of the (empirical) entropic risk and rigorously investigating its properties for . In the next sections (Section 3.1–Section 3.3), we characterize various relations between tilted risks (TERM or entropic risk) and other common risk measures, both in terms of the empirical variants (involving TERM) and distributional forms (involving entropic risk).

3.1 TERM and Rényi Cross Entropy

We begin by demonstrating that TERM can be viewed as form of Rényi cross entropy minimization, which helps to explain the uniformity properties of TERM discussed in Section 2.4. Consider the cross entropy between and defined by

| (37) |

Hence, minimizing is equivalent to minimizing the cross entropy between the true distribution and the postulated distribution. The empirical variant of (37) would be empirical risk minimization (1).

For let Rényi cross entropy of order between and be defined as:444 is defined via continuous extension.

| (38) |

Rényi cross entropy can be viewed as a natural extension of cross entropy, and in fact it recovers cross entropy for i.e., Rényi cross-entropy can also be viewed as a natural extension of Rényi entropy, which it recovers when i.e., where Rényi entropy of order is defined as

| (39) |

It is straightforward to see that the entropic risk can be expressed in terms of Rényi cross entropy:

| (40) |

Equivalently, in the empirical world, TERM can be expressed as:

| (41) |

where denotes the uniform -vector and with defined in Eq. (26), and for any two -vectors and

| (42) |

In other words, if we treat the loss as log-likelihood of the sample under this implies that TERM is the Rényi entropy of order between the uniform vector and the normalized likelihood vector of all samples, . Hence, minimizing over is encouraging the uniformity of in the sense of the Rényi cross entropy with the uniform vector.

3.2 TERM as a Regularizer to Empirical Risk

TERM can also be interpreted as a form of regularization in traditional ERM. We first note that by Taylor series expansion at , TERM can be approximately decomposed into empirical risk regularized by times the empirical variance of the loss, for small (Liu and Theodorou, 2019, Section V.A). Here, we provide an exact interpretation of TERM as regularized ERM for all . We first look at the distributional case, i.e., relating to cross entropy as follows.

Lemma 0.

The entropic risk of order can be stated as:

| (43) |

where denotes KL divergence between two distributions and is a mismatched tilted distribution defined as (Salamatian et al., 2019, Definition 1)

| (44) |

Proof.

Consider the following equation:

| (45) |

which directly implies the desired identity. ∎

In other words, entropic risk of order is equivalent to the cross entropy risk regularized via a tilted mismatched distribution. Let denote the tilted weight vector of the samples. Our next result is an empirical variant of Lemma ‣ 3.2.

Lemma 0.

TERM objective can be restated as follows:

| (46) |

where is the empirical risk (1), denotes the uniform -vector, i.e., and where for -vectors and

| (47) |

Proof.

The proof is a consequence of the following identity:

| (48) |

∎

Hence, TERM aims to minimize an average loss regularized by the KL divergence between the weight vector (which exponentially tilts the individual losses) and the uniform vector.

3.3 TERM and Distributionally Robust Risks

Finally, we note that TERM is closely related to distributionally robust optimization (DRO) objectives (e.g., Namkoong and Duchi, 2017; Duchi and Namkoong, 2019; Chen and Paschalidis, 2020; Gürbüzbalaban et al., 2022; Duchi and Namkoong, 2018). In particular, TERM with is equivalent to a form of DRO with a max-entropy regularizer, i.e., the constraint set is determined by a KL ball around uniform distribution (Föllmer and Knispel, 2011; Qi et al., 2020b; Shapiro et al., 2014):

| (49) |

and the corresponding relations in the distributional form is

| (50) |

This relation is also a special case of Donsker-Varadhan Variational Formula (Dupuis and Ellis, 1997). We note that similar connections between DRO and TERM have also been explored in concurrent works by Qi et al. (2020a, b) specifically in the limited context of stochastic optimization methods for solving class imbalance with .

In the next section, we propose a new risk motivated by TERM, which may be of independent interest.

4 Tilted Value-at-Risk and Value-at-Risk

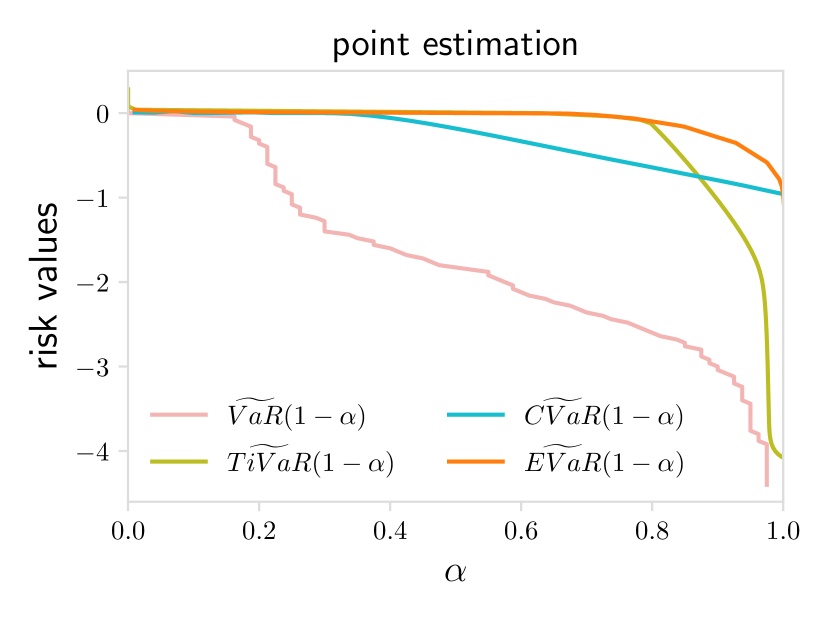

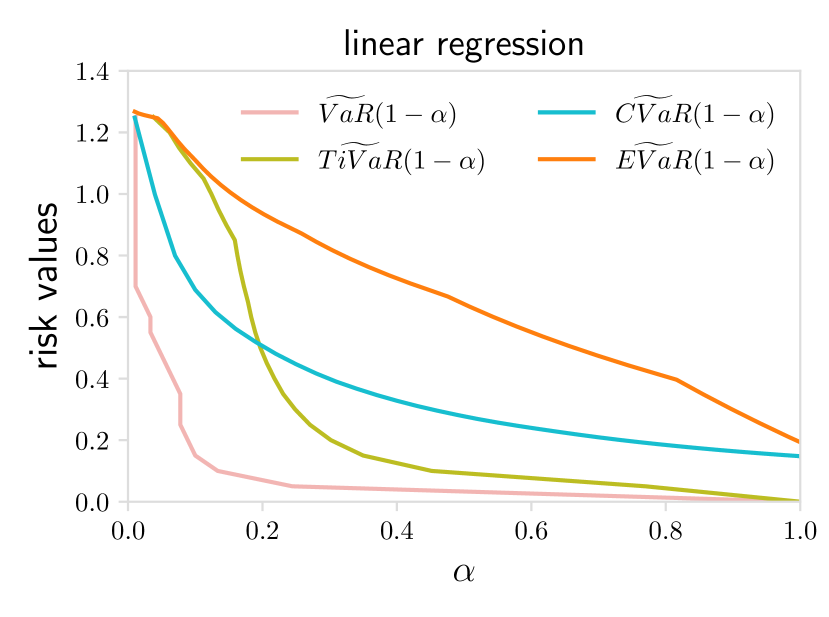

In this section we provide connections between TERM and risk measures such as Value-at-Risk (VAR) that specifically target loss quantiles. In particular, based on TERM, we propose a new risk—Tilted Value-at-Risk (TiVaR) and discuss its relations with existing risks (Section 4.2). We find that TiVaR is a computationally efficient alternative to VaR that provides tighter approximations to VaR than prior risks, which again helps to motivate the use of TERM.

4.1 Tail Probabilities of Losses and Value-at-Risk (VaR)

The tail probabilities of losses focus on quantiles of losses that exceed a certain threshold, as formally defined below.

Definition 0 (Tail probability of losses).

For all let denote the probability of the losses no smaller than , i.e.,

| (51) |

Equivalently, define the empirical variant over samples for :

| (52) |

where is the indicator function.

Notice that quantifies the fraction of the data for which loss is at least . For example, optimizing for 90% of the individual losses (ignoring the worst-performing 10%) could be a more reasonable practical objective than the pessimistic min-max objective. Another common application of this is to use the median in contrast to the mean in the presence of noisy outliers.

Using tail distribution of losses, Value-at-Risk (VaR) (Jorion, 1996) with confidence () is defined as

| (53) |

and the empirical variant for is

| (54) |

Notice that when we view the loss as log-likelihood of a parametric probability distribution function, (Definition ‣ 4.1) can be viewed as the complementary cumulative distribution function (CDF) of the information random variable . Given the definition of VaR, can also be viewed as ‘inverted’ VaR, as we formalize and prove in Lemma ‣ 4.1 and ‣ 4.1 below. Let

| (55) | ||||

| (56) |

where and is defined in Definition ‣ 4.1. Optimizing is equivalent to optimizing VaR. Formally, we have the following lemmas.

Lemma 0.

Assume is strictly decreasing with . We note

| (57) |

Note that is non-increasing as increases by definition. The additional strict monotonic assumption on can be easily satisfied if is a continuous random variable and is in the range of . Lemma ‣ 4.1 is proved as follows.

Proof.

First, we note for any and such that , we have . Otherwise, there exist and which in turn implies that

| (58) |

contradicting . The proof completes combining with the fact that the function value of can achieve at any . ∎

Lemma ‣ 4.1 below describes the empirical variant, which does not require the strict monotonic assumption.

Lemma 0.

For any where is defined as the optimal tilted objective as in Eq. (11), let . Then

| (59) |

Both tail distribution of losses and VaR are usually non-smooth and non-convex, and solving them to global optimality is very challenging. In the next section, we show that TiVaR (an objective based on TERM) provides a good upper bound on VaR, and is computationally more efficient, as VaR is not even continuous. In parallel, in Appendix B, we prove that TERM also provides a reasonable approximate solution to the minimizer of tail probability of losses (i.e., inverted VaR).

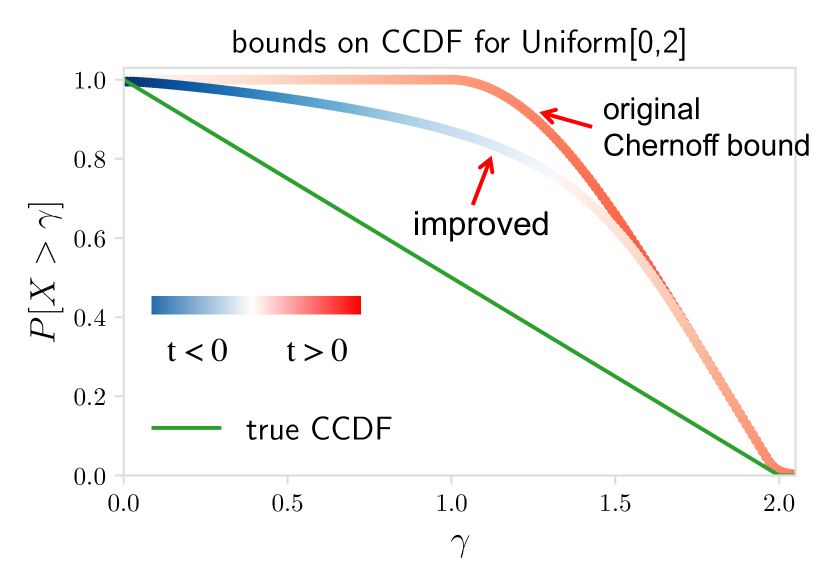

The proof of one of the main theorems of this section (Theorem 187) relies on a new variant of Chernoff bound for non-negative random variables, which may be of independent interest.

Theorem 0 (Chernoff bound for non-negative random variables).

Let be a non-negative random variable. Further assume that for all . Then for ,

| (60) |

where the latter term is the generic Chernoff bound with .

Proof.

The theorem holds by applying Markov’s inequality twice on and , and noting that

| (61) |

∎

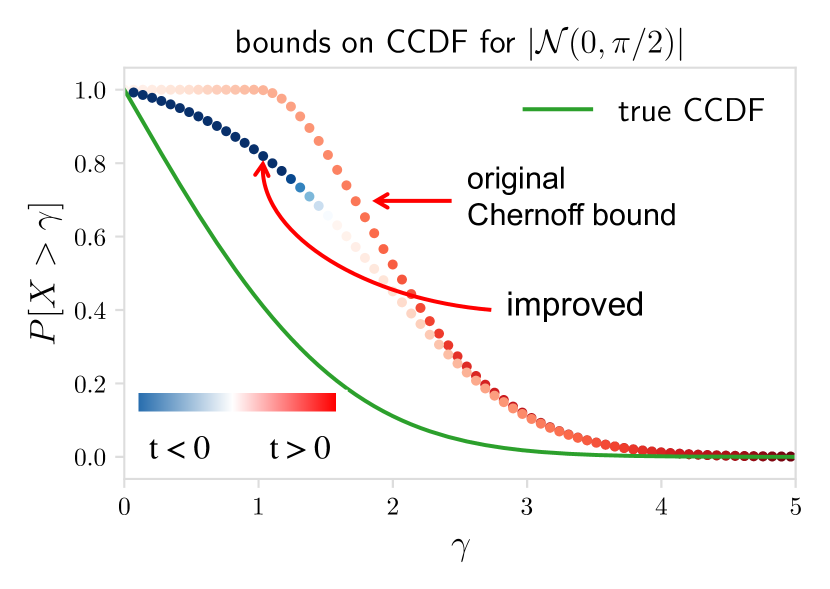

Theorem ‣ 4.1 presents a tighter Chernoff bound for non-negative random variables. To the best of our knowledge, despite the fact that this bound is a simple extension of the generic Chernoff bound, and the existing variants of Chernoff bounds in prior works (Boucheron et al., 2013; Yang and Rosenthal, 2017), we have not seen the result we have here appear elsewhere in this form. In particular, notice that the search for an optimal value of has been extended from non-negative values to all real numbers. This can result in significantly tighter bounds, especially in small deviations regime, as visualized empirically on two simple distributions in Figure 15, Appendix B. We will see how this leads to significantly better bounds in robustness applications.

4.2 TiVaR: Tilted Value-at-Risk

In this section, we introduce a new risk measure, called Tilted Value-at-Risk (TiVaR). To put TiVaR in perspective, we briefly state other existing risks first. Conditional Value-at-Risk (CVaR) minimizes the average risk of tail events where the risk is above some threshold (Rockafellar et al., 2000; Rockafellar and Uryasev, 2002). One form of CVaR is

| (62) |

It is worth noting that CVaR is a dual formulation of DRO with an uncertainty set that perturbs arbitrary parts of the data by an amount up to (Rockafellar et al., 2000; Curi et al., 2020). Formally, the dual of DRO is . Some previous works implicitly minimize CVaR by only training on samples with top- losses (e.g., Fan et al., 2017). Entropic Value-at-Risk (EVaR) is proposed as an upper bound of CVaR and VaR that could be more computationally efficient (Ahmadi-Javid, 2012). EVaR with a confidence level is defined as:

| (63) |

Similarly, for , the empirical variants of CVaR and EVaR are

Notice that TERM objective appears as part of the objective in , and particularly optimizing with respect to would be equivalent to solving TERM for some value of implicitly defined through (see Lemma ‣ B and Lemma ‣ B in the appendix).

It is known that (Ahmadi-Javid, 2012) which directly yields . Meanwhile, to the best of our knowledge, it is not clear from existing works how entropic risk (or TERM) is related to VaR or EVaR. Next, based on TERM, we propose a new risk-averse objective Tilted Value-at-Risk, showing that it upper bounds VaR and lower bounds EVaR.

Definition 0 (Tilted Value-at-Risk (TiVaR)).

Let TiVaR for be defined as

| (64) |

Similarly, empirical TiVaR is defined for ,

| (65) |

We note that TiVaR is not a coherent risk measure (see the work of Artzner (1997); Artzner et al. (1999) for definition of coherent risks), despite that it can be tighter than CVaR in some cases, as discussed in detail later. We next present our main result on relations between TiVaR, VaR, and EVaR.

Theorem 0.

For and any ,

| (66) |

Similarly, for and any ,

| (67) |

We defer the proof to Appendix B, where the main steps include applying the new Chernoff bound variant (Theorem ‣ 4.1). Theorem ‣ 4.2 indicates that is a tighter approximation to than .

Comparing TiVaR and CVaR.

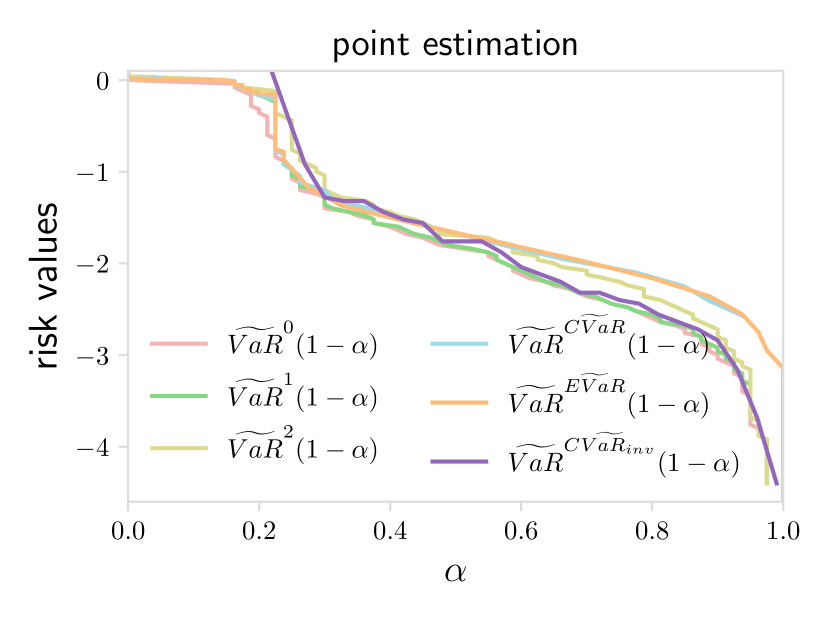

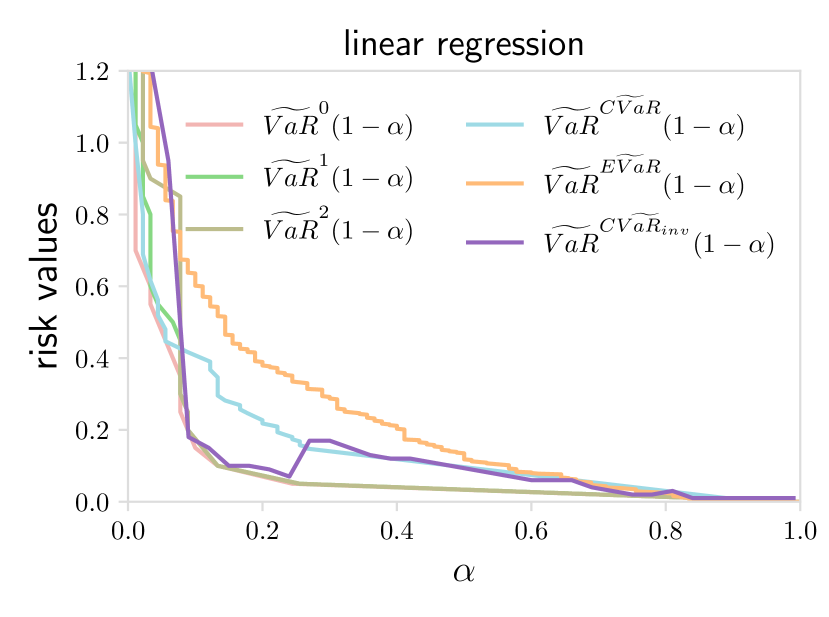

In general, TiVaR and CVaR are not directly comparable, as both of them can be viewed as approximations to VaR and neither dominates the other, i.e., one risk can be tighter than the other depending on the quantile value, 1-. In the regimes where is a large value between some intermediate constant and 1, TiVaR provides a tighter approximation to VaR than CVaR. For instance, in the extreme case when , will be close to the min-loss (), while the value of is the mean of the losses (). reduces to the min-loss in this case. In other words, both and sweep the values between the min-loss and max-loss; whereas sweeps the values between the avg-loss and max-loss. We compare TiVaR with CVaR and other risks in Figure 4 on mean estimation and linear regression problems, and demonstrate that TiVaR is tighter than CVaR especially when is close 1 (corresponding to robustness applications).555While CVaR focuses on upper quantiles, one may explore ‘inverse’ CVaR to better approximate the lower quantiles. However, inverse CVaR, ranging from avg-loss to min-loss, is not a valid upper bound of VaR. Despite this, we empirically explore this approximation to solving VaR, among others, in Appendix B.

We also note that there exist other risk-averse or risk-seeking formulations that focus on the upper or lower tail of losses, such as the mean-semideviation framework (Kalogerias and Powell, 2018). Mean-semideviation recovers a set of risk measures including mean-upper-semideviations and entropic mean-semideviation. Nevertheless, these risks usually cannot handle both fairness and robustness in a single formulation, and can incur more per-iteration gradient evaluations or worse convergence rates compared to vanilla ERM (Kalogerias and Powell, 2018; Gürbüzbalaban et al., 2022; Zhu et al., 2023).

Finally, we draw connections between the above results and the -loss, defined as the -th smallest loss of (i.e., -loss is the min-loss, -loss is the max-loss, -loss is the median-loss). Formally, let be the -th order statistic of the loss vector. Hence, is the -th smallest loss, and particularly

| (68) |

Thus, for any we define

| (69) |

Note that

| (70) |

While minimizing the -loss is more desirable than ERM in many applications, the -loss is non-smooth (and generally non-convex), and is challenging to solve for large-scale problems (Jin et al., 2020; Nouiehed et al., 2019). TERM offers a good approximation to -loss as well. Note that if we fix , minimizing -loss is equivalent to minimizing where . Based on the bound of , we obtain a bound on -loss:

Corollary 0

For all and all

| (71) |

Proof.

Corollary ‣ 4.2 optimizes over all over the upper bound of , which can be relaxed to searching over positive ’s, as stated in Corollary ‣ 4.2 below.

Corollary 0

For all and all

| (73) |

5 Solving TERM

In this section, we develop first-order batch (Section 5.1) and stochastic (Section 5.2) optimization methods for solving TERM, and rigorously analyze the effects that has on the convergence of these methods.

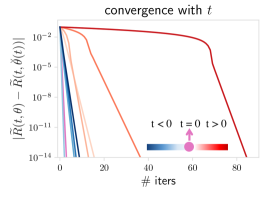

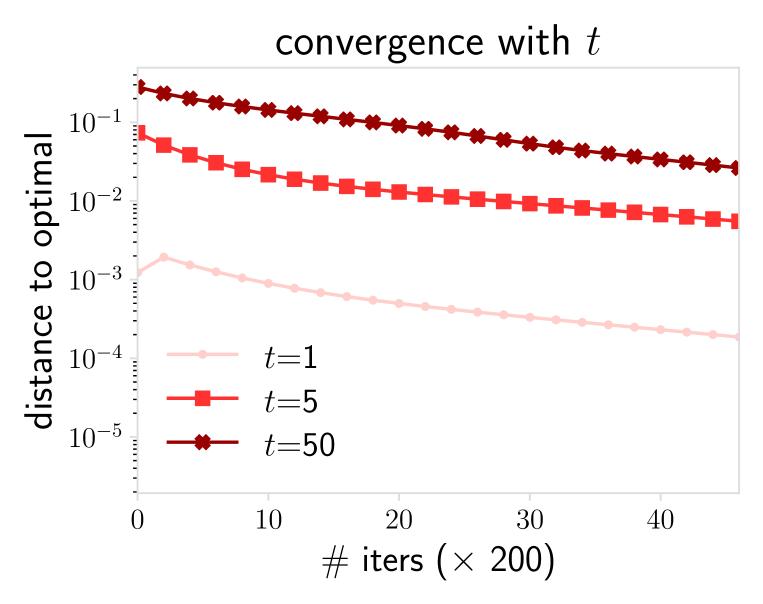

Recall that in Section 2.2, we discuss the Lipschitzness, convexity, and smoothness properties of TERM. -tilted loss remains strongly convex for so long as the original loss function is strongly convex. On the other hand, for sufficiently large negative , the -tilted loss becomes non-convex. Hence, while the -tilted solutions for positive are unique, the objective may have multiple (spurious) local minima for negative even if the original loss function is strongly convex. For negative , we seek the solution for which the parametric set of -tilted solutions obtained by sweeping (i.e., defined in Eq. (10)) remains continuous (as in Figure 1a-c and Figure 2). To this end, for negative , we solve TERM by smoothly decreasing from observing that the solutions form a continuum in empirically. Despite the non-convexity of TERM with , we find that this approach produces effective solutions to multiple real-world problems in Section 7. Additionally, as the objective remains smooth, it is still relatively efficient to solve. On the toy problem studied in Figure 2, we plot the convergence with in Figure 5 below.

5.1 First-Order Batch Methods

TERM solver in the batch setting is summarized in Algorithm 1. The main steps include running gradient descent on , which involve computing the tilted gradients (i.e., a weighted aggregation of individual gradients (Lemma ‣ 2.3)) of the objective. We also provide convergence results in Theorem ‣ 5.1– ‣ 5.1 below for Algorithm 1.

Theorem 0 (Convergence of Algorithm 1 for strongly-convex problems).

Under Assumption 2, there exist and that do not depend on such that for any setting the step size after iterations:

| (74) |

Proof.

Note that under additional assumptions on -Lipschitzness of we can plug in the explicit smoothness constants established by Lowy and Razaviyayn (2021, Lemma 5.3) to obtain explicit constants in the convergence rate, i.e., and . Theorem ‣ 5.1 indicates that solving TERM to a local optimum using gradient-based methods tends to be as efficient as traditional ERM for small-to-moderate values of (Jin et al., 2017), which we corroborate via experiments on multiple real-world datasets in Section 7. This is in contrast to solving for the min-max solution, which would be similar to solving TERM as (Kort and Bertsekas, 1972; Pee and Royset, 2011; Ostrovskii et al., 2020).

Theorem 0 (Convergence of Algorithm 1 for smooth problems satisfying PL conditions).

Assume is -smooth and (possibly) non-convex. Further assume is -PL for any where . There exist and that do not depend on such that for any setting the step size after iterations:

| (75) |

Proof.

Theorem ‣ 5.1 applies to both convex and non-convex smooth functions satisfying PL conditions. Again, here we can plug in explicit smoothness parameter (Lowy and Razaviyayn, 2021, Lemma 5.3) if is Lipschitz. We next state results without the PL condition assumption for completeness.

Theorem 0 (Convergence of Algorithm 1 for non-convex smooth problems).

Assume is -smooth and (possibly) non-convex. Setting the step size after iterations, we have:

| (76) |

where for , where are independent of and , and for , .

Theorem ‣ 5.1 also covers the case of convex with . We note that for non-convex problems, when , the convergence rate is independent of under our assumptions. We also observe this on a toy problem in Figure 5. In all applications we studied in Section 7 with negative ’s, TERM runs the same number iterations as those of ERM.

5.2 First-Order Stochastic Methods

To obtain unbiased stochastic gradients, we need to have access to the normalization weights for each sample (i.e., ), which is often intractable to compute for large-scale problems. Hence, we use , a term that incorporates stochastic dynamics, to estimate the tilted objective , which is used for normalizing the weights as in (25). In particular, we do not use a trivial linear averaging of the current estimate and the history to update . Instead, we use a tilted averaging to ensure an unbiased estimator (if is not being updated).

On the other hand, the TERM objective can be viewed as a composition of functions and , and could be optimized based on previous stochastic compositional optimization techniques (e.g., Wang et al., 2017; Qi et al., 2020b, a; Wang et al., 2016a; Ghadimi et al., 2020). Similar to Wang et al. (2017), we maintain two sequences (in our context, the model and the objective estimate ) throughout the optimization process. This (non-hierarchical) stochastic algorithm is summarized in Algorithm 2 below.

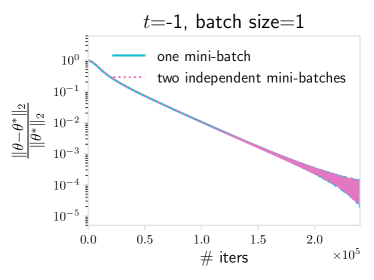

For the purpose of analysis, we sample two independent mini-batches to obtain the gradient of the original loss functions and update , respectively (described in Algorithm 5 for completeness). As we will see in Theorem ‣ 5.2, the additional randomness allows us to achieve better convergence rates compared with the algorithm proposed in Wang et al. (2017) instantiated to our objective. Our rate of this simple algorithm matches the rate of more complicated ones (Qi et al., 2020a), and developing optimal optimization procedures is out of the scope of this work. Empirically, we observe that sampling two mini-batches yield similar performance as using the same mini-batch to query the individual losses and the weights (Figure 17 in Appendix C.2). Therefore, we employ the cheaper variant of just involving one mini-batch (Algorithm 2) in the corresponding experiments.

The stochastic algorithm developed here requires roughly the same time/space complexity as mini-batch SGD, and thus scales similarly for large-scale problems. It can also help mitigate the potential numerical issues in implementation caused by the exponential tilting operator. We find that these methods perform well empirically on a variety of tasks (Section 7).

Theorem 0 (Convergence of Algorithm 5 for strongly-convex problems).

Assume is -Lipschitz in , i.e., ,666For notation consistency between the max-loss and min-loss for any sample and any iteration, we use to denote the lower bound of . We note that defined in Definition 11. and for and . Assume has compact domain . Assume is -strongly convex (Assumption 2) with uniformly bounded stochastic gradient, i.e., for and . Denote . Assume the batch size is 1. For ,

| (77) |

where

| (78) |

and

| (79) |

Our assumptions are standard compared with those in related literature (Wang et al., 2017; Qi et al., 2020b). The uniformly bounded stochastic gradient of assumption can be satisfied by the bounded gradient of , which can be a limiting condition but has appeared in previous works on stochastic compositional optimization (Qi et al., 2020b; Wang et al., 2016a). If the objectives are coercive, which typically holds in practice (Bertsekas, 1997), Algorithm 2 will have bounded iterates and thus the compact domain assumption would hold. We defer full proofs to Appendix C.2. The main steps involve bounding the expected estimation error conditioning on the previous iterates .

Discussions.

The theorem indicates that Algorithm 2 starts to make progress after iterations, with convergence rate . Both and could scale exponentially with in the worst-case analysis, but it does not completely reflect the dependence of Algorithm 2 on for modest values of . Empirically, we observe that the stochastic TERM solver with moderate values of can converge faster compared with stochastic min-max solvers, which has a rate of for strongly convex problems (Levy et al., 2020). This leaves open for future work understanding the exact scaling of the convergence rate of stochastic TERM as

Next, we present convergence results on non-convex smooth problems, without and with the assumptions of PL-conditions. We defer all proofs to Appendix C.2.

Theorem 0 (Convergence of Algorithm 5 for non-convex smooth problems).

Assume is -Lipschitz in , i.e., , and for and . Assume is -smooth with uniformly bounded stochastic gradient, i.e., for and . Assume the batch size is 1. Denote , then for ,

| (80) |

6 TERM Extended: Hierarchical Multi-Objective Tilting

We consider an extension of TERM that can be used to address practical applications requiring multiple objectives, e.g., simultaneously achieving robustness to noisy data and ensuring fair performance across subgroups. Existing approaches typically aim to address such problems in isolation. To handle multiple objectives with TERM, let each sample be associated with a group i.e., These groups could be related to the labels (e.g., classes in a classification task), or may depend only on features. For any we define multi-objective TERM as:

| (83) |

and is the size of group . We evaluate the gradient of the hierarchical multi-objective tilt objective in Lemma ‣ 6 below.

Lemma 0 (Hierarchical multi-objective tilted gradient).

Similar to the tilted gradient (25), Lemma ‣ 6 indicates that the multi-objective tilted gradient is a weighted sum of the gradients, making TERM similarly efficient to solve. Multi-objective TERM recovers sample-level TERM as a special case for (Lemma ‣ 6), and reduces to group-level TERM with .

Lemma 0 (Sample-level TERM is a special case of hierarchical multi-objective TERM).

Under Assumption 1, hierarchical multi-objective TERM recovers TERM as a special case for . That is

| (86) |

Proof.

The proof is completed by noticing that setting in (85) recovers the original sample-level tilted gradient. ∎

Note that all properties discussed in Section 2 carry over to group-level TERM. We validate the effectiveness of hierarchical tilting empirically in Section 7.3, where we show that TERM can significantly outperform baselines to handle class imbalance and noisy outliers simultaneously, while underperforming a much more complicated method in their setup. Note that hierarchical tilting could be extended to hierarchies of greater depths (than two) to simultaneously handle more than two objectives at the cost of one extra tilting hyperparameter per each additional optimization objective. For instance, we state the multi-objective tilting for a hierarchy of depth three in Appendix C.1.

6.1 Solving Hierarchical TERM

To solve hierarchical TERM in the batch setting, we can directly use gradient-based methods with tilted gradients defined for the hierarchical objective in Lemma ‣ 6. Note that Batch hierarchical TERM with reduces to solving the sample-level tilted objective (2). We summarize this method in Algorithm 3.

We next discuss stochastic solvers for hierarchical multi-objective tilting. We extend Algorithm 2 to the multi-objective setting, presented in Algorithm 4. At a high level, at each iteration, group-level tilting is addressed by choosing a group based on the tilted weight vector. Sample-level tilting is then incorporated by re-weighting the samples in a uniformly drawn mini-batch. Similarly, we estimate the tilted objective for each group via a tilted average of the current estimate and the history. While we sample the group from which we draw the minibatch, for small number of groups, one might want to draw one minibatch per each group and weight the resulting gradients accordingly.

7 TERM in Practice: Use Cases

We now showcase the flexibility, wide applicability, and competitive performance of the TERM framework through empirical results on a variety of real-world problems such as handling outliers (Section 7.1), ensuring fairness and improving generalization (Section 7.2), and addressing compound issues (Section 7.3). Despite the relatively straightforward modification TERM makes to traditional ERM, we show that -tilted losses not only outperform ERM, but either outperform or are competitive with state-of-the-art, problem-specific tailored baselines on a wide range of applications. We provide implementation details in Appendix D.2. All code, datasets, and experiments are publicly available at github.com/litian96/TERM. The applications explored are summarized in Table 1 below.

| Applications | Sections | |

|---|---|---|

| Mitigating noisy outliers () | Robust regression | Sec. 7.1.1 |

| Robust classification | Sec. 7.1.2 | |

| Low-quality annotators | Sec. 7.1.3 | |

| Fairness and generalization () | Fair PCA | Sec. 7.2.1 |

| Fair federated learning | Sec. 7.2.2 | |

| Fair meta-learning | Sec. 7.2.3 | |

| Handling class imbalance | Sec. 7.2.4 | |

| Improving generalization via variance reduction | Sec. 7.2.5 | |

| Hierarchical multi-objective tilting | Class imbalance and random noise | Sec. 7.3.1 |

| Class imbalance and adversarial noise | Sec. 7.3.2 | |

Choosing .

In applications when we consider tradeoffs between different objectives (e.g., fair meta-learning and federated learning), we perform a grid search over from {0.1, 1, 2, 5, 10, 50, 100, 200} on the validation set and pick the one with the best fairness performance while not degrading mean performance. When there is not a single t dominating other values (e.g., fair PCA), we report results under different values of . In our initial robust regression experiments, we find that the performance is robust to various ’s, and we thus use a fixed for all experiments involving negative (Section 7.1 and Section 7.3). For all values of tested, the number of iterations required to solve TERM is within 2 that of standard ERM, with the same per-iteration complexity.

7.1 Mitigating Noisy Outliers ()

We begin by investigating TERM’s ability to find robust solutions that reduce the effect of noisy outliers. We note that we specifically focus on the setting of ‘robustness’ involving random additive noise; the applicability of TERM to more adversarial forms of robustness would be an interesting direction of future work. We do not compare with approaches that require additional clean validation data (e.g., Roh et al., 2020; Veit et al., 2017; Hendrycks et al., 2018; Ren et al., 2018), as such data can be costly to obtain in practice.

7.1.1 Robust Regression

Label noise.

We first consider a regression task with noise corrupted targets, where we aim to minimize the root mean square error (RMSE) on samples from the Drug Discovery dataset (Olier et al., 2018; Diakonikolas et al., 2019). The task is to predict the bioactivities given a set of chemical compounds. We compare against linear regression with an loss, which we view as the ‘standard’ ERM solution for regression, as well as with losses commonly used to mitigate outliers—the loss and Huber loss (Huber, 1964). We also compare with consistent robust regression (CRR) (Bhatia et al., 2017) and STIR (Mukhoty et al., 2019), recent state-of-the-art methods specifically designed for label noise in robust regression. In this particular problem, TERM is equivalent to exponential squared loss, studied in (Wang et al., 2013). We apply TERM at the sample level with an loss, and generate noisy outliers by assigning random targets drawn from on a fraction of the samples.

In Table 2, we report RMSE on clean test data for each objective and under different noise levels. We also present the performance of an oracle method (Genie ERM) which has access to all of the clean data samples with the noisy samples removed. Note that Genie ERM is not a practical algorithm and is solely presented to set the expected performance limit in the noisy setting. The results indicate that TERM is competitive with baselines on the 20% noise level, and achieves better robustness with moderate-to-extreme noise. We observe similar trends in scenarios involving both noisy features and targets (Appendix D.1). CRR tends to run slowly as it scales cubicly with the number of dimensions (Bhatia et al., 2017), while solving TERM is roughly as efficient as ERM.

| objectives | test RMSE (Drug Discovery) | ||

|---|---|---|---|

| 20% noise | 40% noise | 80% noise | |

| ERM | 1.87 (.05) | 2.83 (.06) | 4.74 (.06) |

| 1.15 (.07) | 1.70 (.12) | 4.78 (.08) | |

| Huber (Huber, 1964) | 1.16 (.07) | 1.78 (.11) | 4.74 (.07) |

| STIR (Mukhoty et al., 2019) | 1.16 (.07) | 1.75 (.12) | 4.74 (.06) |

| CRR (Bhatia et al., 2017) | 1.10 (.07) | 1.51 (.08) | 4.07 (.06) |

| TERM | 1.08 (.05) | 1.10 (.04) | 1.68 (.03) |

| Genie ERM | 1.02 (.04) | 1.07 (.04) | 1.04 (.03) |

Label and feature noise.

Here, we present results involving both feature noise and target noise. We investigate the performance of TERM on two datasets (cal-housing (Pace and Barry, 1997) and abalone (Dua and Graff, 2019)) used in Yu et al. (2012). Both datasets have features with 8 dimensions. We generate noisy samples following the setup in Yu et al. (2012)—sampling 100 training samples, and randomly corrupting 5% of them by multiplying their features by 100 and multiply their targets by 10,000. From Table 3 below, we see that TERM significantly outperforms the baseline objectives in the noisy regime on both datasets.

| objectives | test RMSE (cal-housing) | test RMSE (abalone) | ||

|---|---|---|---|---|

| clean | noisy | clean | noisy | |

| ERM | 0.766 (0.023) | 239 (9) | 2.444 (0.105) | 1013 (72) |

| 0.759 (0.019) | 139 (11) | 2.435 (0.021) | 1008 (117) | |

| Huber (Huber, 1964) | 0.762 (0.009) | 163 (7) | 2.449 (0.018) | 922 (45) |

| CRR (Bhatia et al., 2017) | 0.766 (0.024) | 245 (8) | 2.444 (0.021) | 986 (146) |

| TERM | 0.745 (0.007) | 0.753 (0.016) | 2.477 (0.041) | 2.449 (0.028) |

| Genie ERM | 0.766 (0.023) | 0.766 (0.028) | 2.444 (0.105) | 2.450 (0.109) |

Unstructured random v.s. adversarial noise.

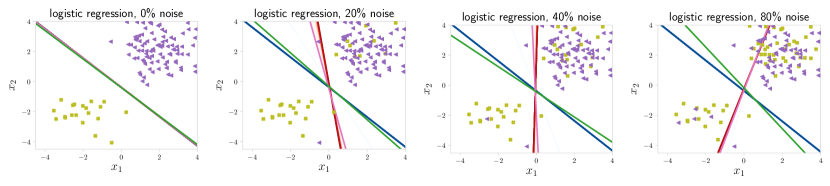

As a word of caution, we note that the experiments thus far have focused on random noise. This makes it possible for the methods to find the underlying structure of clean data even if the majority of the samples are noisy outliers. To gain more intuition on these cases, we generate synthetic two-dimensional data points and test the performance of TERM under 0%, 20%, 40%, and 80% noise for linear regression. TERM with performs well in all noise levels (Figure 6 and 7). However, as one might expect, TERM with negative ’s could potentially overfit to outliers if they are constructed in an adversarial way. In the examples shown in Figure 8, under 40% noise and 80% noise, TERM has a high error measured on the clean data (green dots).

7.1.2 Robust Classification

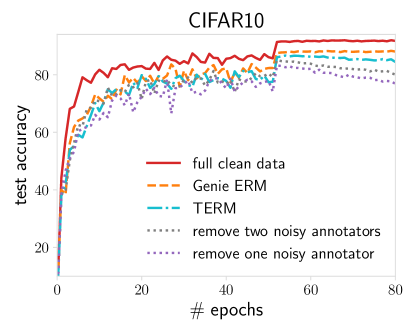

Deep neural networks can easily overfit to corrupted labels (e.g., Zhang et al., 2017). While the theoretical properties we study for TERM (Section 2) do not directly cover objectives with neural network function approximations, we show that TERM can be applied empirically to DNNs to achieve robustness to noisy training labels. MentorNet (Jiang et al., 2018) is a popular method in this setting, which learns to assign weights to samples based on feedback from a student net. Following the setup in Jiang et al. (2018), we explore classification on CIFAR10 (Krizhevsky et al., 2009) when a fraction of the training labels are corrupted with uniform noise—comparing TERM with ERM and several state-of-the-art approaches (Kumar et al., 2010; Ren et al., 2018; Zhang and Sabuncu, 2018; Krizhevsky et al., 2009). As shown in Table 4, TERM performs competitively with 20% noise, and outperforms all baselines in the high noise regimes. We use MentorNet-PD as a baseline since it does not require clean validation data. In Appendix D.1, we show that TERM also matches the performance of MentorNet-DD, which requires clean validation data. To help reason about the performance of TERM, we also explore a simpler, two-dimensional logistic regression problem in Figure 19, Appendix D.1, finding that TERM with = is similarly robust across the considered noise regimes.

| objectives | test accuracy (CIFAR10, Inception) | ||

|---|---|---|---|

| 20% noise | 40% noise | 80% noise | |

| ERM | 0.775 (.004) | 0.719 (.004) | 0.284 (.004) |

| RandomRect (Ren et al., 2018) | 0.744 (.004) | 0.699 (.005) | 0.384 (.005) |

| SelfPaced (Kumar et al., 2010) | 0.784 (.004) | 0.733 (.004) | 0.272 (.004) |

| MentorNet-PD (Jiang et al., 2018) | 0.798 (.004) | 0.731 (.004) | 0.312 (.005) |

| GCE (Zhang and Sabuncu, 2018) | 0.805 (.004) | 0.750 (.004) | 0.433 (.005) |

| TERM | 0.795 (.004) | 0.768 (.004) | 0.455 (.005) |

| Genie ERM | 0.828 (.004) | 0.820 (.004) | 0.792 (.004) |

7.1.3 Low-Quality Annotators

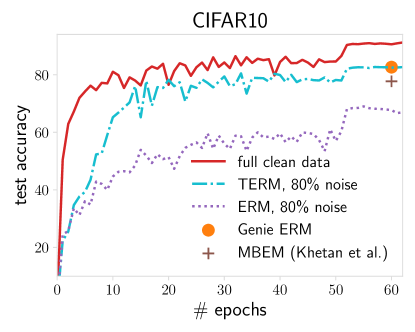

It is not uncommon for practitioners to obtain human-labeled data for their learning tasks from crowd-sourcing platforms. However, these labels are usually noisy in part due to the varying quality of the human annotators. Given a collection of labeled samples from crowd-workers, we aim to learn statistical models that are robust to the potentially low-quality annotators. As a case study, following the setup of (Khetan et al., 2018), we take the CIFAR-10 dataset and simulate 100 annotators where 20 of them are hammers (i.e., always correct) and 80 of them are spammers (i.e., assigning labels uniformly at random). We apply TERM at the annotator group level in (83), which is equivalent to assigning annotator-level weights based on the aggregate value of their loss. As shown in Figure 9, TERM is able to achieve the test accuracy limit set by Genie ERM, i.e., the ideal performance obtained by completely removing the known outliers. We note in particular that the accuracy reported by (Khetan et al., 2018) (0.777) is lower than TERM (0.825) in the same setup, even though their approach is a two-pass algorithm requiring at least to double the training time. We provide full empirical details and investigate additional noisy annotator scenarios in Appendix D.1.

7.2 Fairness and Generalization ()

In this section, we show that positive values of in TERM can help promote fairness via learning fair representations and enforcing fairness during optimization, and offer variance reduction for better generalization.

7.2.1 Fair Principal Component Analysis (PCA)

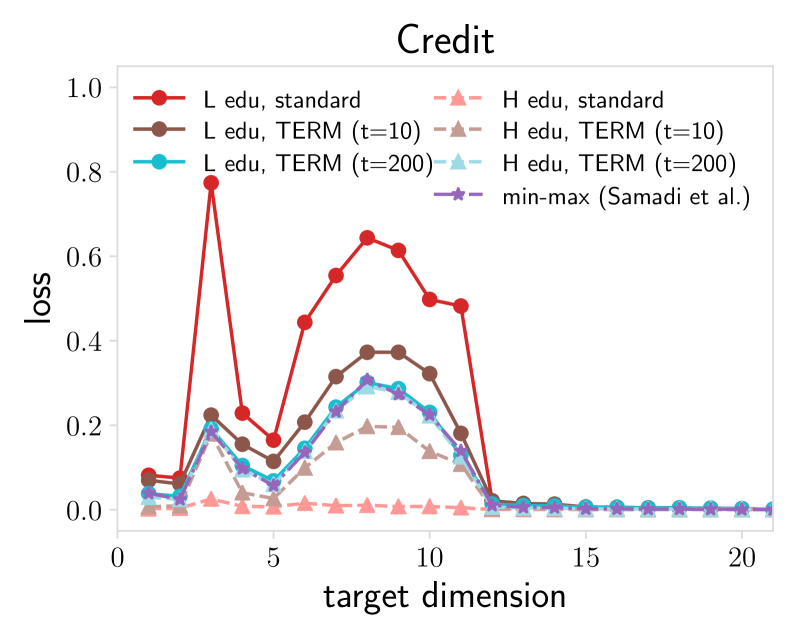

We explore the flexibility of TERM in learning fair representations using PCA. In fair PCA, the goal is to learn low-dimensional representations which are fair to all considered subgroups (e.g., yielding similar reconstruction errors) (Samadi et al., 2018; Tantipongpipat et al., 2019; Kamani et al., 2019). Despite the non-convexity of the fair PCA problem, we apply TERM to this task, referring to the resulting objective as TERM-PCA. We tilt the same loss function as in Samadi et al. (2018): where is a subset (group) of data, is the current projection, and is the optimal rank- approximation of . Instead of solving a more complex min-max problem using semi-definite programming as in Samadi et al. (2018), which scales poorly with problem dimension, we apply gradient-based methods, re-weighting the gradients at each iteration based on the loss on each group. In Figure 10, we plot the aggregate loss for two groups (high vs. low education) in the Default Credit dataset (Yeh and Lien, 2009) for different target dimensions . By varying , we achieve varying degrees of performance improvement on different groups—TERM () recovers the min-max results of (Samadi et al., 2018) by forcing the losses on both groups to be (almost) identical, while TERM () offers the flexibility of reducing the performance gap less aggressively. We also provide convergence plots for different values of in this application (Figure 11), and observe slower convergence for larger values of , which is consistent with our analyses in Section 2 and 5. However, we do not observe exponential dependence on from the convergence curves, which suggest that the theoretical dependence on in convergence proofs for the solvers may be an artifact of our proof techniques, and might possibly be further improved by other analysis techniques for typical practical use cases.

7.2.2 Fair Federated Learning

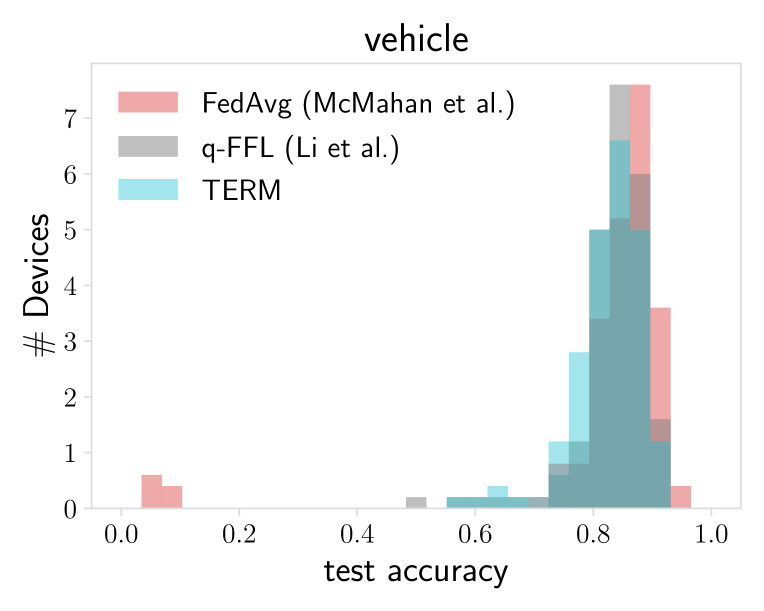

Federated learning involves learning statistical models across massively distributed networks of remote devices or isolated organizations (McMahan et al., 2017; Li et al., 2020a). Ensuring fair (i.e., uniform) performance distribution across the devices is a major concern in federated settings (Mohri et al., 2019; Li et al., 2020b), as using current approaches for federated learning (FedAvg (McMahan et al., 2017)) may result in highly variable performance across the network. Li et al. (2020b) consider solving an alternate objective for federated learning, called -FFL, to dynamically emphasize the worst-performing devices, which is conceptually similar to the goal of TERM, though it is applied specifically to the problem of federated learning and limited to the case of positive . Here, we compare TERM with -FFL in their setup on the vehicle dataset (Duarte and Hu, 2004) consisting of data collected from 23 distributed sensors (hence 23 devices). We tilt the regularized linear SVM objective at the device level. At each communication round, we re-weight the accumulated local model updates from each selected device based on the weights estimated via Algorithm 4. From Figure 12, we see that similar to -FFL, TERM () can also significantly promote the accuracy on the worst device while maintaining the overall performance. The statistics of the accuracy distribution are reported in Table 7.2.2 below.

| objectives | test accuracy | ||

|---|---|---|---|

| average | worst 10% | stdev | |

| FedAvg | 0.853 (.078) | 0.421 (.007) | 0.173 (.001) |

| -FFL () | 0.862 (.029) | 0.704 (.033) | 0.064 (.005) |

| TERM () | 0.853 (.027) | 0.707 (.009) | 0.061 (.003) |

7.2.3 Fair Meta-Learning

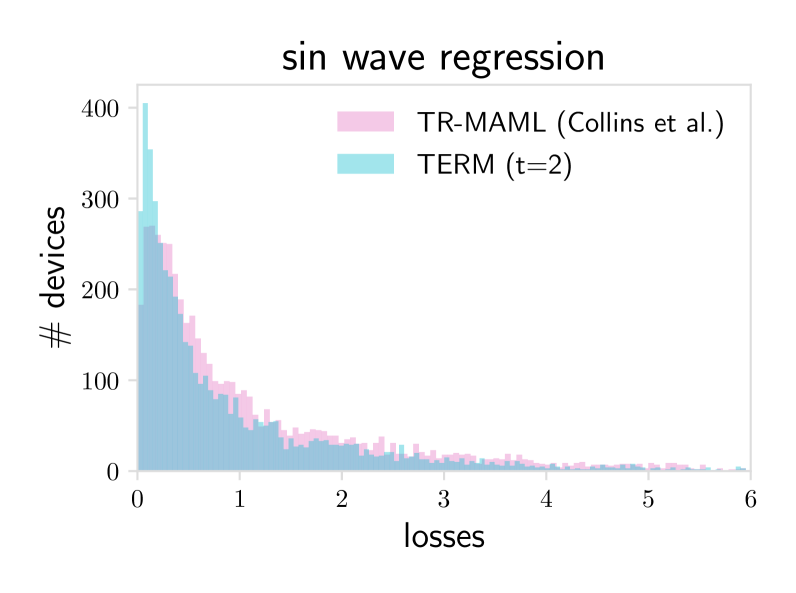

Meta-learning aims to learn a shared initialization across all tasks such that the initialization can quickly adapt to unseen tasks (i.e., meta-testing tasks) using a few samples. In practice, the resulting performance across meta-testing tasks can vary due to different data distributions associated with these tasks. One of the popular meta-learning methods is MAML (Finn et al., 2017), whose objective is to minimize the sum of empirical losses across tasks generated from after one step of adaptation, i.e., . Previous works have proposed a min-max variant of MAML to encourage a more fair (uniform) performance distribution by optimizing the worst meta-training task called TR-MAML (Collins et al., 2020). We apply TERM to MAML by replacing the ERM formulation with tilted losses. Following the setup in Collins et al. (2020), we evaluate TERM on the popular sin wave regression problem. For a fair comparison, we perform task-level tilting for TERM, and operates on task-level reweighting for TR-MAML. From Table 7.2.3, we see that TERM with not only decreases the standard deviation of test errors, but also achieves lower mean errors than MAML. As the number of tasks is large (5,000), solving the min-max variant (TR-MAML) is challenging, and results in slightly worse performance than TERM.

| methods | mean | std | max | worst 10% |

|---|---|---|---|---|

| MAML | 1.23 | 1.63 | 19.1 | 5.16 |

| TR-MAML | 1.25 | 1.51 | 14.31 | 4.85 |

| TERM () | 1.14 | 1.33 | 13.59 | 4.29 |

7.2.4 Handling Class Imbalance

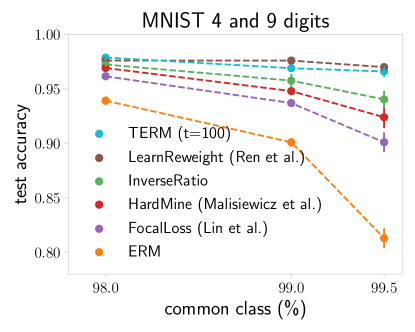

Next, we show that TERM can reduce the performance variance across classes with extremely imbalanced data when training deep neural networks. We compare TERM with several baselines which re-weight samples during training, including assigning weights inversely proportional to the class size (InverseRatio), focal loss (Lin et al., 2017), HardMine (Malisiewicz et al., 2011), and LearnReweight (Ren et al., 2018). Following the setting of Ren et al. (2018), the datasets are composed of imbalanced and digits from MNIST (LeCun et al., 1998). In Figure 14, we see that TERM obtains similar (or higher) final accuracy on the clean test data as the state-of-the-art methods. We note that compared with LearnReweight, which optimizes the model over an additional balanced validation set and requires three gradient calculations for each update, TERM neither requires such balanced validation data nor does it increase the per-iteration complexity.

7.2.5 Improving Generalization via Variance Reduction

| objectives | accuracy () | accuracy () | overall accuracy (%) | |||

|---|---|---|---|---|---|---|

| train | test | train | test | train | test | |

| ERM | 0.841 (.005) | 0.822 (.009) | 0.971 (.000) | 0.966 (.002) | 0.944 (.000) | 0.934 (.003) |

| Linear SVM | 0.873 (.003) | 0.838 (.013) | 0.965 (.000) | 0.964 (.002) | 0.951 (.001) | 0.937 (.004) |

| CVaR (Rockafellar et al., 2000) | 0.877 (.004) | 0.844 (.013) | 0.972 (.000) | 0.964 (.003) | 0.952 (.001) | 0.937 (.003) |

| LearnReweight (Ren et al., 2018) | 0.860 (.004) | 0.841 (.014) | 0.960 (.002) | 0.961 (.004) | 0.940 (.001) | 0.934 (.004) |

| FocalLoss (Lin et al., 2017) | 0.871 (.003) | 0.834 (.013) | 0.970 (.000) | 0.966 (.003) | 0.949 (.001) | 0.937 (.004) |

| HRM (Leqi et al., 2019) | 0.875 (.003) | 0.839 (.012) | 0.972 (.000) | 0.965 (.003) | 0.952 (.001) | 0.937 (.003) |

| RobustRegRisk (Duchi et al., 2019) | 0.875 (.003) | 0.844 (.010) | 0.971 (.000) | 0.966 (.003) | 0.951 (.001) | 0.939 (.004) |

| TERM () | 0.864 (.003) | 0.840 (.011) | 0.970 (.000) | 0.964 (.003) | 0.949 (.001) | 0.937 (.004) |

| ERM+ (thresh = 0.26) | 0.943 (.001) | 0.916 (.008) | 0.919 (.001) | 0.917 (.003) | 0.924 (.001) | 0.917 (.002) |

| RobustRegRisk+ (thresh=0.49) | 0.943 (.000) | 0.917 (.005) | 0.928 (.001) | 0.928 (.002) | 0.931 (.001) | 0.924 (.001) |

| TERM () | 0.942 (.001) | 0.917 (.005) | 0.926 (.001) | 0.925 (.002) | 0.929 (.001) | 0.924 (.001) |

A common alternative to ERM is to consider a distributionally robust objective, which optimizes for the worst-case training loss over a set of distributions, and has been shown to offer variance-reduction properties that benefit generalization (e.g., Duchi and Namkoong, 2019; Sinha et al., 2018; Chen and Paschalidis, 2020; Duchi and Namkoong, 2018). While not directly developed for distributional robustness, TERM also enables variance reduction for positive values of (Theorem 33), which can be used to strike a better bias-variance trade-off for generalization. We compare TERM with several baselines including robustly regularized risk (RobustRegRisk) (Duchi and Namkoong, 2019), linear SVM (Ren et al., 2018), Conditional Value-at-Risk (CVaR) (Rockafellar et al., 2000; Soma and Yoshida, 2020), LearnRewight (Ren et al., 2018), FocalLoss (Lin et al., 2017), and HRM (Leqi et al., 2019) on the HIV-1 dataset (Rögnvaldsson, 2013; Dua and Graff, 2019) originally investigated by Duchi and Namkoong (2019). We examine the accuracy on the rare class (), the common class (), and overall accuracy.

The mean and standard error of accuracies are reported in Table 7. RobustRegRisk and TERM offer similar performance improvements compared with other baselines, such as linear SVM, CVaR, LearnRewight, FocalLoss, and HRM. Note that here RobustRegRisk (Duchi and Namkoong, 2019) and CVaR (Rockafellar et al., 2000) can both be viewed as specific instances of the distributionally robust optimization framework, with different uncertainty sets. For larger , TERM achieves similar accuracy in both classes, while RobustRegRisk does not show similar trends by sweeping its hyperparameters. It is common to adjust the decision threshold to boost the accuracy on the rare class. We do this for ERM and RobustRegRisk and optimize the threshold so that ERM+ and RobustRegRisk+ result in the same validation accuracy on the rare class as TERM (). TERM achieves similar performance to RobustRegRisk without the need for an extra tuned hyperparameter.

7.3 Solving Compound Issues: Hierarchical Multi-Objective Tilting

Finally, in this section, we focus on settings where multiple issues, e.g., class imbalance and label noise, exist in the data simultaneously. We discuss two possible instances of hierarchical multi-objective TERM to tackle such problems. One can think of other variants in this hierarchical tilting space which could be useful depending on applications at hand.

7.3.1 Class Imbalance and Random Noise

We explore the HIV-1 dataset (Rögnvaldsson, 2013), as in Section 7.2. We report both overall accuracy and accuracy on the rare class in four scenarios: (a) clean and 1:4, the original dataset that is naturally slightly imbalanced with rare samples represented 1:4 with respect to the common class; (b) clean and 1:20, where we subsample to introduce a 1:20 imbalance ratio; (c) noisy and 1:4, which is the original dataset with labels associated with 30% of the samples randomly reshuffled; and (d) noisy and 1:20, where 30% of the labels of the 1:20 imbalanced dataset are reshuffled.

| objectives | test accuracy (HIV-1) | |||||||

|---|---|---|---|---|---|---|---|---|

| clean data | 30% noise | |||||||

| 1:4 | 1:20 | 1:4 | 1:20 | |||||

| overall | overall | overall | overall | |||||

| ERM | 0.822 (.009) | 0.934 (.003) | 0.503 (.013) | 0.888 (.006) | 0.656 (.014) | 0.911 (.006) | 0.240 (.018) | 0.831 (.011) |

| CVaR (Rockafellar et al., 2000) | 0.844 (.013) | 0.937 (.003) | 0.621 (.011) | 0.906 (.005) | 0.651 (.015) | 0.909 (.006) | 0.252 (.014) | 0.834 (.010) |

| GCE (Zhang and Sabuncu, 2018) | 0.822 (.009) | 0.934 (.003) | 0.503 (.013) | 0.888 (.006) | 0.732 (.021) | 0.925 (.005) | 0.324 (.017) | 0.849 (.008) |

| LearnReweight (Ren et al., 2018) | 0.841 (.014) | 0.934 (.004) | 0.800 (.022) | 0.904 (.003) | 0.721 (.034) | 0.856 (.008) | 0.532 (.054) | 0.856 (.013) |

| RobustRegRisk (Duchi et al., 2019) | 0.844 (.010) | 0.939 (.004) | 0.622 (.011) | 0.906 (.005) | 0.634 (.014) | 0.907 (.006) | 0.051 (.014) | 0.792 (.012) |

| FocalLoss (Lin et al., 2017) | 0.834 (.013) | 0.937 (.004) | 0.806 (.020) | 0.918 (.003) | 0.638 (.008) | 0.908 (.005) | 0.565 (.027) | 0.890 (.009) |

| HAR (Cao et al., 2021) | 0.842 (.011) | 0.936 (.004) | 0.817 (.013) | 0.926 (.004) | 0.870 (.010) | 0.915 (.004) | 0.800 (.016) | 0.867 (.012) |

| TERMsc | 0.840 (.010) | 0.937 (.004) | 0.836 (.018) | 0.921 (.002) | 0.852 (.010) | 0.924 (.004) | 0.778 (.008) | 0.900 (.005) |

| TERMca | 0.844 (.014) | 0.938 (.004) | 0.834 (.021) | 0.918 (.003) | 0.846 (.015) | 0.933 (.003) | 0.806 (.020) | 0.901 (.010) |

In Table 8, hierarchical TERM is applied at the sample level and class level (TERMsc), where we use the sample-level tilt of for noisy data. We use class-level tilt of for the 1:4 case and for the 1:20 case. We compare against baselines for robust classification and class imbalance (discussed previously in Sections 7.1 and 7.2), where we tune them for best performance (Appendix D.2). Similar to the experiments in Section 7.1, we avoid using baselines that require clean validation data (e.g., Roh et al., 2020). We compare TERM with an additional baseline of HAR (Cao et al., 2021), a recent work addressing the issues of noisy and rare samples simultaneously with adaptive Lipschitz regularization. While different baselines (except HAR) perform well in their respective problem settings, TERM and HAR are far superior to all baselines when considering noisy samples and class imbalance simultaneously (rightmost column in Table 8). Finally, in the last row of Table 8, we simulate the noisy annotator setting of Section 7.1.3 assuming that the data is coming from 10 annotators, i.e., in the 30% noise case we have 7 hammers and 3 spammers. In this case, we apply hierarchical TERM at both class and annotator levels (TERMca), where we perform the higher level tilt at the annotator (group) level and the lower level tilt at the class level (with no sample-level tilting). We show that this approach can benefit noisy/imbalanced data even further (far right, Table 8), while suffering only a small performance drop on the clean and noiseless data (far left, Table 8).

7.3.2 Class Imbalance and Adversarial Noise

We evaluate hierarchical tilting on a more difficult task involving more adversarial noise with deep neural network models. We take the setup studied in Cao et al. (2021). The noise is created by exchanging labels of 40% samples which come from similar classes (‘cat’ and ‘dog’, ‘vehicle’ and ‘automobile’) in the CIFAR10 dataset. To simulate class imbalance, only 10% of the training data from these four noisy classes are subsampled. For TERM, we apply group-level positive tilting by linearly scaling from 0 to 3, and perform sample-level negative tilting within each class with scaling from 0 to -2. Table 9 reports the results of hierarchical TERM (TERMsc) compared with HAR (Cao et al., 2021) and other baselines. We see that TERM underperforms HAR, and outperforms all other approaches. Note that HAR is a more complicated method which requires to perform end-to-end training for two times with higher per-iteration complexity (involving second-order information), while TERM is a simple method and enjoys the same training time as that of ERM on this problem.

| objectives | test accuracy (CIFAR10, ResNet32) | |

|---|---|---|

| noisy, rare class | clean, common class | |

| ERM | 0.529 (.012) | 0.944 (.001) |

| GCE (Zhang and Sabuncu, 2018) | 0.482 (.006) | 0.916 (.003) |

| MentorNet (Jiang et al., 2018) | 0.541 (.010) | 0.903 (.005) |

| MW-Net (Shu et al., 2019b) | 0.554 (.011) | 0.917 (.005) |

| HAR (Cao et al., 2021) | 0.635 (.008) | 0.943 (.002) |

| TERMsc | 0.585 (.014) | 0.913 (.003) |

8 Related Approaches in Machine Learning

Here we discuss related problem-specific works in machine learning addressing deficiencies of ERM. We roughly group them into alternate aggregation schemes, alternate loss functions, and sample re-weighting schemes.

Alternate aggregation schemes.