Clockwork Finance: Automated Analysis of Economic Security in Smart Contracts

)

Abstract

We introduce the Clockwork Finance Framework (CFF), a general purpose, formal verification framework for mechanized reasoning about the economic security properties of composed decentralized-finance (DeFi) smart contracts.

CFF features three key properties. It is contract complete, meaning that it can model any smart contract platform and all its contracts—Turing complete or otherwise. It does so with asymptotically constant model overhead. It is also attack-exhaustive by construction, meaning that it can automatically and mechanically extract all possible economic attacks on users’ cryptocurrency across modeled contracts.

Thanks to these properties, CFF can support multiple goals: economic security analysis of contracts by developers, analysis of DeFi trading risks by users, fees UX, and optimization of arbitrage opportunities by bots or miners. Because CFF offers composability, it can support these goals with reasoning over any desired set of potentially interacting smart contract models.

We instantiate CFF as an executable model for Ethereum contracts that incorporates a state-of-the-art deductive verifier. Building on previous work, we introduce extractable value (EV), a new formal notion of economic security in composed DeFi contracts that is both a basis for CFF and of general interest.

We construct modular, human-readable, composable CFF models of four popular, deployed DeFi protocols in Ethereum: Uniswap, Uniswap V2, Sushiswap, and MakerDAO, representing a combined 24 billion USD in value as of March 2022. We use these models along with some other common models such as flash loans, airdrops and voting to show experimentally that CFF is practical and can drive useful, data-based EV-based insights from real world transaction activity. Without any explicitly programmed attack strategies, CFF uncovers on average an expected $56 million of EV per month in the recent past.

1 Introduction

The innovation of smart contracts has resulted in an explosion of decentralized applications on blockchains. Abstractly, smart contracts are pieces of code that run on blockchain platforms, such as Ethereum. They support rich (even Turing-complete) semantics, can trade in the underlying cryptocurrency, and can directly manipulate blockchain state. While early blockchains were built primarily to support currency transfer, newer ones with smart contracts have enabled a wide range of sophisticated and novel decentralized applications.

One particularly exciting area where smart contracts have been influential is decentralized finance (or DeFi), a general term for financial instruments built on top of public decentralized blockchains. DeFi contracts have realized a number of financial mechanisms and instruments (e.g., automated market makers [14], atomic swaps [34], and flash loans [41]) that cannot be replicated with fiat or real world assets, and have no analog in traditional financial systems. These innovations usually take advantage of two distinctive properties of smart contracts. These are atomicity, which means (potential) execution of multi-step transactions in an all-or-nothing manner, and determinism, meaning execution of state transitions without randomness and thus a unique transaction outcome for a given blockchain state. Smart contracts can also intercommunicate on-chain, which has led to DeFi instruments that can interoperate and compose to achieve functionality that transcends their independent functionalities.

Recent years, however, have seen a plethora of high-profile attacks on DeFi contracts (see, e.g., [16] for a recent survey), with attackers stealing billions in the aggregate. These attacks are primarily financial in nature and not pure software exploits; they leverage complex financial interactions among multiple DeFi contracts whose composition is poorly understood. Existing notions of software security and traditional bug-finding tools are insufficient to reason about or discover such attacks.

A range of literature [22, 23], has attempted to apply formal verification techniques to the study of DeFi security. These works, though, have typically been used to check for attack heuristics [50] that represent conventional software bugs in smart contracts or to validate formal security properties [37, 28] akin to those in standard software verification tools. More recently, some work [51] has applied formal verification tools to the economic security of DeFi contracts, quantifying such security by identifying optimum arbitrage strategies. While an important initial step, this work has focused on predetermined, known attack strategies, and lacks the generality to discover new economic attacks, rule out classes of attacks, or provide upper bounds on the exploitable value of DeFi contracts.

Clockwork Finance.

Motivated by the limited formal exploration of the question of DeFi contracts’ economic security, in this paper we present Clockwork Finance111Our name comes from the Enlightenment notion of the cosmos as a clock, i.e., a fully deterministic and predictable machine, like the smart contract systems we consider. The Wikipedia definition of clockwork universe [1] notes: “In the history of science, the clockwork universe compares the universe to a mechanical clock … making every aspect of the machine predictable.” (CF), an approach to understanding the economic security properties of DeFi smart contracts and their composition. CF addresses the inherently economic nature of DeFi security properties by codifying the use of formal verification techniques to reason about the profit extractable from the system by a participant, rather than in terms of more traditional descriptions of software bugs as error states. CF relies on, and we introduce in this paper, the first formal definition for the economic security of composed smart contracts, which we call extractable value (EV). EV generalizes miner-extractable value (MEV)—a metric defined in [19] to study DeFi protocol impact on consensus security.222CF can be extended to other metrics of economic security, e.g., arbitrageurs’ profits, profits of permissioned actors, etc., but we leave extensions to future work.

Clockwork Finance Framework (CFF).

We realize CF in the form of a powerful mechanized tool that we call the Clockwork Finance Framework (CFF). To use CFF, a user wishing to analyze the economic security of a contract creates or reuses an existing formal model of the contract, as well as models for potentially composed contracts. CFF, together with the models we provide, offers three key functional properties:

-

•

Contract completeness: CFF is contract complete in the sense that it can model DeFi (and other) contracts, such as those in Ethereum, with equivalent execution complexity to the native platform. That is, for all possible transactions (inputs), executing the formal CFF model of a contract requires time overhead over EVM/native execution time. CFF introduces no execution blow-up or time penalty for the execution of any transaction sequence, even for complex compositions of contracts. CFF also has equal expressive power as the contract platform to which it’s applied—again, such as Ethereum.

-

•

Constant model overhead: The models we provide feature at most a (small) constant-size increase in the size (number of distinct semantic paths) of the model compared to the target contract. Oftentimes, with path pruning, our specialized models are even substantially smaller than the smart contract code being modeled. We provide a general approach for achieving this property for new CFF models. We discuss this approach and property in detail in Section 5.3.

-

•

Attack-exhaustive by construction: CFF can mechanically reason about the full space of possible state transitions for the given set of transactions and models. CFF can in principle—given sufficient computation—identify any attack expressible in our definitions as a condition of mempool transaction activity and target contract models. We ensure this by making sure our provided models are over-approximations of the studied contracts, yielding false positives in the attack search as a trade-off for efficiency, but not false negatives. We then prune these false positives through concrete validation. We discuss this property in detail along with sources of unsoundness in Section 5.2.

CFF also offers two important usability features:

-

•

Modularity: CFF models are modular, meaning that once a model is realized for a particular contract, it can be used for any CFF execution involving that contract. Modularity also means that models are arbitrarily composable in CFF: any and all models in a library can be invoked for a CFF analysis without customization.

-

•

Human-readability: Although we do not show this experimentally, we show by example that CFF models are typically easier for human users to read, understand, and reason about than contract source code.

Taken together, these properties and features make CFF highly versatile and able to support a range of different uses. Designers of DeFi contracts can use CFF to reason about the economic security of their contracts and do so, critically, while reasoning about interactions with other contracts. Arbitrage bots and miners can use the same contract models to find profitable strategies in real-time. Users can use CFF to reason about guarantees provided by the transactions they execute in the network, including the value at risk of exploits by miners, bots, and other network participants—which today is considerable in practice [19, 50]. With the rise of frontrunning-as-a-service [8], users can also use CFF to set the right fees for their transactions, which taken together with the value extractable from their transactions determines inclusion in the block. We explore these various use cases in the paper.

CFF achieves more than mere measurement of economic security: It can prove bounds on the economic security of contracts, i.e., the maximum amount adversaries can extract from them. Furthermore, it can do so using only the formally specified models of interacting contracts. CFF does not require manual coding of adversarial strategies.

Notably, this means that CFF can illuminate potential adversarial strategies even when they were not previously exploited in the wild. This stands in contrast to existing work, where the focus has often been on specific predefined strategies encoded manually [50], or which has required error-prone effort to define an action-space manually beyond the mere contract code executing on the system [51]. We believe that use of CFF would be a helpful part of the standard security assessment process for smart contracts, alongside bug finding, auditing, and conventional formal verification.

Contributions.

We summarize three concrete contributions and insights from our paper below:

-

•

Security Definitions (Sections 3 and 4). We provide the first formal definitions for the economic security of smart contracts and their composition and thus the first principled basis for DeFi contract designers to reason about the economic security of their protocols. Our definitions are general enough to model different types of players with different capabilities (e.g., transaction reordering, censorship, inserting malicious transactions) for influencing the system state.

-

•

Clockwork Finance Framework (CFF) and Concrete Models (Sections 3 and 5). We instantiate our definitions in our CFF tool in order to find arbitrage strategies and prove bounds on the economic security of smart contracts. We model within CFF and analyze four popular real-world contracts: Uniswap V1, Uniswap V2, SushiSwap, and MakerDAO. We compare our results again direct on-chain Ethereum Virtual Machine execution, showing that CFF execution of our models yields high-fidelity results.

-

•

Practical Attacks and Formal Proofs (Section 6). Our CFF tool automatically discovers the main attack patterns seen in practice, uncovering highly profitable attacks in an automated way for the four contracts we model. These attacks exploit the price slippage or the lack of secure financial composition of DeFi contracts, and can be used by malicious miners (or others) to profit at the expense of ordinary users. Our tool also yields formal mathematical proofs for the upper bound on the value extractable from these attacks. By our conservative estimate, the potential impact of these attacks frequently exceeds the Ethereum block reward by two orders of magnitude (i.e., 10,000%). We also validate our attacks by simulating them on an archive node and have contributed the implementation of our simulation method into the latest public release of the Erigon client software.

CFF is the first smart-contract analytics tool to achieve contract completeness, constant model overhead, and attack-exhaustiveness by construction, enabling it to bring new capabilities to ecosystem participants. Complete CFF code is available at https://github.com/defi-formal/cff/.

2 Background and Related Work

Our work intersects with several well-studied areas which we briefly introduce here as background.

2.1 Blockchain and Smart Contracts

Smart contracts are executed in transactions, which, like ACID-style database transactions [46], modify the state of a cryptocurrency system atomically (that is, either the entire transaction executes or no component of the transaction executes). A transaction’s output and validity depends on both the system’s state and the code being executed, which can read and respond to this state. The state may also include user balances of tokens representing assets or of cryptocurrencies in the underlying system. In the smart contract setting, the primary purpose of the underlying blockchain is to order transactions. The execution of a transaction sequence is then deterministic, and can be computed by all parties. The sequencing of transactions is done by actors known as miners (or validators or sequencers, terms we use interchangeably).

A unique attribute of smart contract transactions that proves critical to decentralized finance is their ability to throw an unrecoverable error, reverting any side-effects of a transaction until that point and converting the transaction into a no-op. This allows actors to execute transactions in smart contracts that are reverted if some operation fails to complete as expected or yield desired profit.

2.2 Decentralized Finance

Decentralized Finance, or DeFi, is a general term for the ecosystem of financial products and protocols defined by smart contracts running on a blockchain. As of August 2021, the Ethereum DeFi space contains roughly 80bn USD of locked capital in smart contracts [2]. DeFi protocols or instruments have already been deployed for a wide range of use cases, and allow users to borrow, lend, exchange, or trade assets on a blockchain. Abstractly, a key goal of DeFi is to create composable and modular financial instruments that do not rely on a centralized issuing party. DeFi instruments can thus interoperate programatically without human intervention or complex cooperation among issuing entities. We provide a brief background on the two specific classes of DeFi instruments featured in this work.

Lending contracts.

Some DeFi contracts lend a certain cryptocurrency (such as DAI in the Maker protocol [32]) to a user, with another user-supplied cryptocurrency (such as ETH) held by the contract as collateral. If the value of the collateral falls below a system-defined threshold, the financial instrument can automatically foreclose on the collateral to repay the loan without the cooperation of the borrower. This automated loan guarantee mitigates risk in a way attractive to lenders. Lending contracts can also underlie “stablecoin” protocols, which support tokens pegged to real-world currencies such as the U.S. dollar (e.g., as in the Maker protocol).

Decentralized exchanges.

Another example of a DeFi instrument is a decentralized exchange (“DEX”). In a DEX, users can trade between different assets that have a digital representation (e.g., on a blockchain). A DEX facilitates the exchange of assets without the risk that one party in the exchange defaults or fails to execute their end of the asset swap. This guarantee protects users from counterparty risk present in traditional exchanges, especially cryptocurrency exchanges, which have often violated users’ trust assumptions by absconding with funds [33, 35] or incorrectly executing user orders through technical errors and even fraud [45]. A special class of DEX called Automated Market Maker (“AMM”) eliminates the need for a counterparty to execute a swap. An AMM (like Uniswap or Sushiswap) maintains reserves of liquidity providers’ assets and allows swaps with a user’s assets at programatically self adjusting prices.

Miner extractable value.

A notion called MEV, or miner-extractable value, introduced in [19], measures the extent to which miners can capture value from users through strategic placement and/or ordering of transactions. Miners have the power to dictate the inclusion and ordering of mempool transaction in blocks. (Thus MEV is a superset of the front-running/arbitrage profits capturable by ordinary users or bots, because miners have strictly more power.) Previous studies of MEV have performed transaction-level measurements of the outcome of specific strategies (e.g., sandwiching attacks in [50] and pure revenue trade composition in [19]). Other work has abstracted away transaction-level dynamics, analyzing DeFi protocols such as AMMs using statistical modeling and economic agent-based simulation [7].

2.3 Formal Verification Tools

Formal verification is the study of computer programs through mathematical models in well-defined logics. It supports the proof of mathematical claims over the execution of programs, traditionally to reason about program safety and correctness. Formal verification has been applied to traditional financial systems in the past (like [38]) but as noted in Section 1, DeFi systems have novel properties not present in these older systems. Most formal verification works for smart contracts (such as [6, 23, 50, 37, 9]) do not reason about economic security and hence cannot characterize financial exploits in DeFi (i.e., they are not attack-exhaustive by construction). Recent work [51] has attempted to apply formal verification to find profitable arbitrage strategies but does not provide formal proofs of economic security. Moreover, the tool covers only certain types of manually encoded smart contract actions, so that the tool lacks contract completeness and optimal model sizes.

Our work aims to establish a clear translation interface between existing program verification tools and the unique security requirements of DeFi. We develop our models in the K Framework [43], which provides a formal semantics engine for analyzing and proving properties of programs. K allows developers to define models that are mathematically formal, machine-executable, and human-readable.

By mathematically formal, we mean that K uses an underlying theory called “matching logic” that allows claims expressed about programs in programming languages defined by K to be proven formally. Such proofs have been used in industry to verify the practical security properties of smart contracts that hold billions of dollars [25].

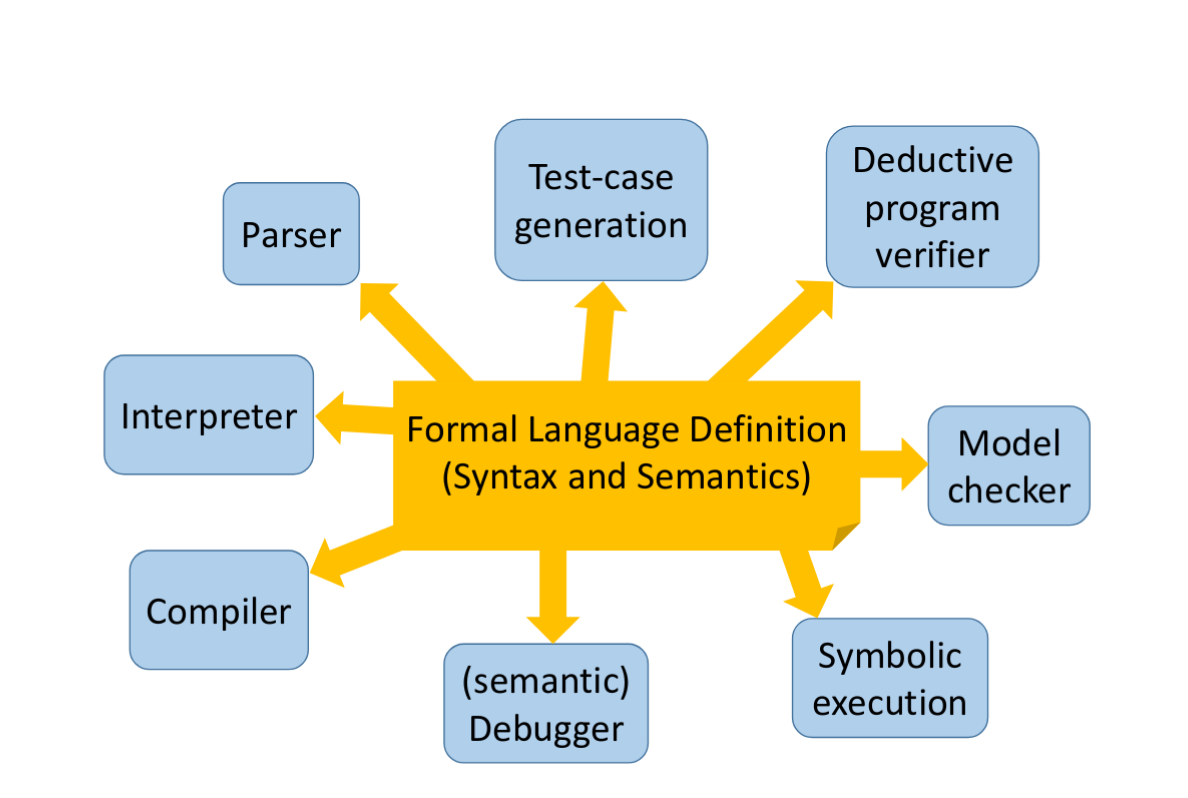

By executable, we mean that K provides concurrent and non-deterministic rewrite semantics [18] that allow for efficient execution of large programs in the developer-specified programming language model. Figure 1 shows the high-level goals of the K Framework, which include deriving an interpreter and compiler for a specified language semantics, as well as model-checking tools.

By human-readable, we mean that K provides output in a form that can serve as a reference for other mathematical models, as it uses only abstract and human-readable mathematical operations. Examples of human-readable K semantics include the Jello Paper for the Ethereum VM.333The “Jello Paper” (https://jellopaper.org/), based on [22], reimplements the original Ethereum yellow paper [47] in a machine executable, mathematically formal manner and can generate an Ethereum interpreter and contract proofs. Because DeFi contracts today lack standardized abstract models, we believe K’s abstract models are especially suitable to DeFi and hope they can ease security analysis and specification.

K is one of a number of formal verification tools; other common tools include Coq, Isabelle, etc. Indeed, several have been applied to model Ethereum-based systems in the past [6, 23, 9]. We refer the reader to [43, 17, 18] for details on the mathematical and formal foundations of K. We emphasize that our MEV-based secure composability definitions and general results are not specific to K.

3 Clockwork Finance Formalism

We introduce our formalism for Clockwork Finance in this section. It underpins the definition of extractable value (EV) we introduce in this paper. Our contract composability definitions in Section 4 are based in turn on that of EV. We let throughout denote the system security parameter.

Accounts and balances.

We use to denote the space of all possible accounts. For example, in Ethereum, accounts represent public key identifiers and are 160-bit strings (in other words, ). We define two functions, : and : (where is ), that map an account to its current balance (for a given token ) and its associated data (e.g., storage trie in Ethereum) respectively. For , as shorthand, we let denote the balance of all tokens held in and denote the account balance of token . We use denote the balance of the primary token (e.g., ETH in Ethereum444We note that our usage of token to denote ETH is non-standard. While the ETH balance is stored differently than the balance of other tokens in Ethereum, we choose to model them using the same function for a cleaner (although equivalent) formalism.).

We define the current system state mapping (or simply state) as a combination of the account balance and data; that is, for an account , . We use to denote the space of all state mappings.

Smart contracts.

As smart contracts in the system are globally accessible, we model them within the global state through the special account. We let denote the set of contracts in state of the system, which may change as new contracts are added. We use and to denote the balance of tokens and the data (e.g., contract state and code) associated with a contract in state respectively.

Transactions.

Transactions are polynomial-sized (in the security parameter) strings constructed by some player that are executed by the system and can change the system state. Abstractly, a transaction can be represented by its action: a function from to transforms the current state mapping into a new state mapping. We denote this action function by . We say that a transaction is valid in state if and use to denote the set of all valid transactions for state . Our formalism is general enough to also allow transactions that add smart contracts to the system or interact with existing ones.

Blocks.

We define a block to be an ordered list of transactions. We disregard block contents regarding consensus mechanics, e.g., nonce, blockhash, Merkle root which are not relevant for our framework. Of the block metadata, we only model the block number, denoted by . The action of a block can now be defined as the result of the action of the sequence of transactions it contains. We use to denote the state resulting from the action of on starting state . That is, where and . A block is said to be valid if all of its transactions are valid w.r.t. their input state (i.e., the state resulting from executing prior transactions sequentially).

We can analogously define the action of any sequence of transactions (even spanning multiple blocks)—a concept useful for analyzing reordering across blocks.

Network actors and mempools.

Let denote the (unbounded) set of players in our system, and denote a specific player. We use to denote the global set of all valid transactions for state , but note that not all transactions can be validly generated by all players. For a player , we define a set as the transactions that can be validly created by when the system is in state . Transactions created by players are included in a mempool for the current state. A player working as a miner to create a block may include any transactions currently in the mempool (i.e., transactions generated by other players) as well as any transactions in that generates itself. Note however, that the miner cannot change the contents of other players’ transactions, as they are digitally signed. Abstractly, a “valid block” for a miner is any sequence of transactions that the miner has the ability to include. We use to denote the set of all valid blocks that can be created by player in state if it could work as a miner. We use to denote the set of valid length block sequences such that and the other where and .

Extractable value.

Equipped with our basic formalism, we now define extractable value (EV), which intuitively represents the maximum value, expressed in terms of the primary token, that can be extracted by a given player from a valid sequence of blocks that extends the current chain. Formally, for a state , and a set of valid block sequences of length , the EV for a player with a set of accounts is given by:

where , , and .

We also define miner-extractable value, which computes the maximum value that a miner can extract in a state . Consider a player working as a miner. The of in state can now be defined as:

Note that the parameter is the length by which the chain at state is extended (including through a chain-reorg) by . The most common scenario will be extension by a single block for which we use will simply use MEV as shorthand henceforth. does not account for how difficult it is for to mine the consecutive blocks, but it is sufficient for our purpose to understand the value that can be extracted if a single miner could append multiple consecutive blocks. In Appendix B, we define a weighted notion of miner-extractable-value that takes the probability of appending multiple blocks into account. We call this “weighted MEV” or WMEV.

Remark 1 (Local vs global maximization).

The astute reader may notice that our definitions (along with our concrete CFF instantiation in Section 5) only considers the maximum value extractable in some given state . This can be considered analogous to finding a “local maximum” in the search space, leaving open the possibility that a non-optimal EV computation in the current state may lead to a higher combined EV when future states are also considered.

As a simple example, consider a transaction that gives a specific miner a profit of if it is mined when a contract has state and when the contract has state . Assume that the state change from to can only be caused (irreversibly) by a different player . Now, if mines a block when has state , local MEV maximization would say that it should include within its block. But if later causes the state change to in a new transaction, then would have made more if it waited to include .

While it is theoretically possible to define a “global maximum” for EV, computing it requires knowing the probability distribution of future transactions, i.e., how new transactions will be created and ordered within blocks (including by other players). In other words, it requires perfect knowledge of the strategy of all other players in the system, which is unrealistic.

We therefore focus in this work only on the maximum EV for a particular state. We emphasize however, that our definition is exact w.r.t. this local value.

Remark 2 (MEV subsumes other attacks).

We highlight that our notion of MEV subsumes not only arbitrage but all attacks that can be carried out based on the current state of the system by a profit-seeking player. Notably, this includes not only common strategies such as frontrunning, backrunning, and sandwich attacks [50], but also attacks with significant complexity observed in the wild, such as [39, 12].

A common theme within these complex attacks in particular has been to use flash loans to borrow a significant amount of some token(s) and use this capital to extract profit by violating an implicit assumption in another contract (e.g., the valuation of a pool or token), before returning the loan. Such attacks can be explored from the current state without requiring additional state changes from other players, thereby allowing for our local computation of extractable value. We further note that since a miner is in a strictly more privileged position than any other permissionless player in the system, these strategies are exploitable by a miner. Moreover, in any competitive race to extract these opportunities, the miner will ultimately have the option to capture the resulting revenue. This provides intuition for why MEV is more general than arbitrage or attacks.

We include a concrete example of such a flash-loan based attack within CFF in Section 6.5.

Since we focus on economic security, we consider only profit-seeking players and our definition of MEV therefore does not capture attacks that exploit a vulnerability but do not necessarily result in financial gain. Such attacks are considered traditional exploits, not economic ones.

3.1 Decentralized Finance Instruments

DeFi instruments.

We define DeFi instruments quite broadly, as smart contracts that interact with tokens in some way other than through transaction fees. We provide three concrete examples of DeFi instruments, which we use in running examples throughout the paper and as building blocks to discuss properties at higher levels of abstraction.

In particular, we specify here: (1) A simplified Uniswap contract; (2) A simplified Maker contract; and (3) A simple betting contract. We note that while we use simplified versions of the original contracts, they are still useful as didactic tools and for analyzing the core semantic properties underlying contract composition. Note, however, that our instantiations of the contracts in the CFF (see Section 5) include the missing details, i.e., are complete and usable for real-world data.

Uniswap contract.

The Uniswap automated market maker contract [4] allows a player to execute exchanges between two tokens (usually ETH and another token), according to a market-driven exchange rate. The contract assumes the role of the counterparty for such an exchange. Uniswap uses an automated market maker formula, called the formula or the constant product formula. We discuss a simplified version here that does not deal with liquidity provisions, transaction fees, and rounding. Abstractly, for tokens and , the number of coins and for these tokens in the contract always satisfies the invariant , where is a constant. This equation can be used to determine the exchange rate between and . If coins of are sold (to the contract), coins of will be received (by the user) so as to satisfy:

Figure 2 shows the pseudocode for our simplified Uniswap contract for the tokens and . It contains a function exchange() which allows a user to sell InAmount tokens of InToken to the contract in exchange for OutToken tokens where . The number of OutToken tokens received by the user is given by the market maker formula.

Contract

function exchange(InToken, OutToken, InAmount):

if then

else Output

Maker contract.

The Maker protocol allows users to generate and redeem the collateral-backed “stablecoin” Dai through Collateralized Debt Positions (CDPs). Users can take out a loan in Dai by depositing the required amount of an approved cryptocurrency (e.g., ETH) as collateral, and can pay back the loan in Dai to free up their collateral. If a user’s collateral value relative to their debt falls below a certain threshold called the “Liquidation Ratio” (), then their collateral is auctioned off to other users in order to close the debt position. Maker uses a set of external feeds as price oracles to determine the value of the collateral. A separate governance mechanism is used to determine parameters like the Liquidation Ratio, stability fees (interest charged for the loan), etc., and also to approve external price oracle feeds and valid collateral types. We consider here a simplified version of Maker’s single-collateral CDP contract that does not model stability fees, or liquidation penalties. The contract allows users to take out (or pay back) loans denominated in token by depositing (or withdrawing) the appropriate collateral in token , and allows for liquidation as soon as the debt-to-collateral ratio drops below the Liquidation Ratio. The contract is detailed in Figure 3.

It should be noted that the amount of collateral liquidated and received by the liquidator as well as the debt (in Dai) paid off by the liquidator in exchange for the collateral depends on the outcome of a 2-phase auction. If the auction is perfectly efficient, the winning bidder pays off an equivalent amount of debt for receiving the offered collateral. On the other hand, when the auction is inefficient due to system congestion, collusion, transaction censoring, etc., the winning bidder can receive the entire collateral on offer without paying off an equivalent amount of debt. In our simplified Contract , we assume that liquidation is perfectly efficient.

Contract

if then

if and then

if and then

if then

if then

return

Betting contract.

To better understand composition failures, we introduce a simple betting contract and study its interaction with the previous contracts. Abstractly, the betting contract allows a user to place a bet against the contract on a future token exchange rate as determined by using Uniswap as a price oracle. By price oracle, we mean that the exchange rate between tokens as determined by the Uniswap contract is used to drive decisions in another contract.

In Figure 4, we specify the contract that takes bets on the relative future price of token X to ETH. Specifically, suppose that is initialized with a deposit of 100 ETH tokens. A user Alice can now call bet() and deposit 100 of her own ETH tokens to take a position against the contract. If at some point before the expiration time , the Uniswap contract contains more ETH tokens than X tokens, (i.e., the Uniswap contract values X more than ETH), Alice can call getreward() to claim 200 ETH from the contract, which includes her initial 100 ETH bet, along with her 100 ETH reward. Otherwise, Alice loses her initial bet.

For simplicity, our contract only contains a single bet, but it is straightforward to design similar contracts with more restrictions and/or functionalities (e.g., allowing another user to play the counterparty in the bet).

Contract

// Contract also initialized with 100 ETH tokens when created.

function bet():

if and then

else Output

function getreward():

if and and and (current time is at most ) then

else Output

4 DeFi Composability

Smart contracts don’t exist in isolation. A natural question, therefore, is when contracts “compose securely.” Abstractly, for a particular notion of security, does the security of a contract change when another contract is added to the system? In this paper, since our primary motivation is to analyze DeFi instruments, we focus on an economic notion of composable security. In particular, we look at how the extractable value of the system changes when new contracts are added to it. The economic composability of an existing DeFi instrument w.r.t. now pertains to the added monetary value that can be extracted if is introduced into the system. That is, is composable w.r.t. if adding to the system does not give an adversary significantly higher extraction gains. For brevity, throughout this paper, we let composability refer to this specific notion, but note that it is orthogonal to previously considered notions (in, e.g., [27, 31]).

Ideally, we want contracts to be “robust” enough to compose securely with all other contracts. Unfortunately, this may be too strong a notion in practice. We thus parameterize our definitions to allow restricted or partial composability. Definition 1 defines the simplest notion of contract composability.

Definition 1 (Defi Composability).

Consider state and player . A DeFi instrument is -composable under if

Here is the state resulting from executing a transaction that adds the contract to (no-op if already exists). Although the composability of pertains to all contracts in , when looking at the specific interaction with a , we may also write that is -composable with .

In other words, allowing a player to interact with contract in a limited capacity (using at most the tokens that the player controls in ) does not significantly increase the profit the player can extract form the system. Note that Definition 1 can easily be extended to consider several states and or players.

4.1 Characteristics of Contract Composition

We find that DeFi instruments that are secure under composition according to Definition 1 are surprisingly uncommon, especially when two instruments depend on each other (e.g., one contract using the other as a price oracle). Intuitively, manipulating one contract can change the execution path of the other contract. In this section, we analyze the composition among the contracts (, , and ) introduced in Section 3.1 to highlight interesting characteristics that can arise from smart contract composition. Note that for this simplified, didactic analysis, we do not make use of our CFF tool. We summarize our observed characteristics below.

Characteristic 1.

Composability is state dependent—contracts may be -composable in state but not in another state .

Characteristic 2.

Composability depends on the actions allowed for a player. For instance, contracts may be composable if only transaction reordering is allowed but not if the creation of new transactions is allowed as well.

Characteristic 3.

A contract may not be composable with another instance of itself.

Characteristic 4.

It is often possible to introduce adversarial contracts that break composability with minimal resources. Thus it is important to consider composability not just of existing contracts, but also over such adversarial contracts.

To provide intuition for these properties, we will analyze the following contract compositions. Section 4.2 considers the use of as a price oracle for either or . Section 4.3 analyzes the composition between multiple independent instances of . Section 4.4introduces a new bribery contract that can be used to inject non-composability into the system.

4.2 Uniswap as a Price Oracle

Example 1 ( as a price oracle for ).

Consider a simplified Uniswap contract () that exchanges the tokens BBT and ETH, and a betting contract () that uses it as a price oracle.

In particular, consider a system state such that (or alternatively contains other contracts that do not affect the composability). Suppose that in state , contains BBT tokens and ETH tokens such that . To denote the Uniswap transactions contained in the mempool in state :

-

•

Let be the set of transactions that sell BBT tokens to the contract in exchange for ETH tokens. Suppose the total number of BBT tokens transacted is .

-

•

Let be the set of transactions that sell ETH to the contract in exchange for BBT tokens. Suppose that the total number of ETH transacted is .

For a player , let and be the number of ETH and BBT tokens held by in the state that are not within pending transactions in the mempool. Note that can use transactions from other accounts within the mempool as well as any transactions it can create with its own capital to create a block. Note that even if does not have the hash power to mine blocks, it can pay some other miner to order transactions according to its preference. Let be the state resulting from adding to state .

Composability is state dependent.

It is easy to see that contracts that are independent of each other and provide orthogonal functionalities should compose securely in all states. In most real-world cases, however, we want to analyze the composability of contracts that are not independent and may in fact depend on each other’s state. In such situations, whether two contracts compose securely will almost always depend on the characteristics of the current system state.

We use Example 1 to provide intuition to this observation. Specifically, we show that and are composable in states with a small number of available tokens, while in other states, an adversary can extract more MEV from the composition. Suppose that we define the number of liquid tokens in the Uniswap contract as follows: For player and state , we say that there are liquid BBT tokens and liquid ETH tokens. We will now show how composability can be affected by the number of liquid tokens in the current state.

-

a)

Composability in states with a small number of liquid tokens. When , i.e., the number of liquid tokens is sufficiently small, and do in fact compose securely. This is because regardless of what transactions creates or how it orders existing transactions in the transaction pool, at no point in the execution of a created block can the number of ETH tokens in exceed the number of BBT tokens in it. In other words, cannot maliciously create a short term fluctuation in the exchange rate in order to claim a reward from . Note that while can still cause the exchange rate to be manipulated even if it cannot cause the number of ETH tokens to exceed the number of BBT tokens, since we are focusing only on composability with here specifically, will not be able to claim the reward from .

Consequently, any value that can extract in state (obtained by adding to state ) can also be extracted in state . Equivalently, . We conclude that is -composable under .

-

b)

Non-composability in other states. Suppose now that our low liquidity assumption was no longer valid. In particular, we will consider states such that , and . At least 100 ETH is necessary in our example to actually take a bet against the betting contract. To extract more value in state , a malicious miner can proceed as follows:

-

1)

Insert a transaction that takes a bet against the contract by depositing 100 ETH.

-

2)

Order all transactions in the set . This raises the amount of ETH in temporarily.

-

3)

Insert a transaction (a call to getreward()) to claim the reward of 100 ETH (in addition to its original bet) from due to the short term price fluctuation in .

-

4)

Order the transactions in to buy ETH from .

Abstractly, by ordering all transactions that sell ETH to first, can create a short-term volatility in the exchange rate between ETH and BBT, allowing to claim the reward from . When the block created by executes, since all transactions that add ETH to are ordered first, there will be more ETH tokens than BBT tokens by the time the ’s transaction to claim the reward from executes. This sudden change in the amount of ETH is only temporary as the remaining transactions in the block will reduce the number of ETH tokens. Note that this reordering attack is still possible in the case that and the natural or “fair” transaction order would not cause such a large change in the exchange rate during normal execution. Yet, the malicious miner was able to profit simply by reordering user transactions.

-

1)

Composability depends on the allowed actions.

In the context of Example 1, if cannot insert its own transactions for , then composability holds even if and , since cannot create a large enough price fluctuation simply from the transactions in the mempool. However, if has the ability to insert its own transactions, it can use the previously mentioned procedure to extract the reward from . can also insert its transactions before and after user transactions to take advantage of the short term slippage in the Uniswap price. This strategy resembles the sandwiching attack described in [50], which combines frontrunning and backrunning. It also allows to capitalize on the price differential between limit orders and market orders.

Uniswap as a price oracle for Maker.

Similar problems would arise if Uniswap is used as a price oracle in the Maker contract. By reordering Uniswap transactions, and thereby manipulating the exchange rate, a miner can cause the value of a user’s collateral to fall below the acceptable threshold, and trigger a liquidation event. Furthermore, the miner can buy the user’s collateral tokens in the liquidation event, and later sell them for a profit when the exchange price returns to normal.

4.3 Composition of multiple AMMs

Perhaps surprisingly, we find that even multiple contracts deployed with the same code need not be composable with each other. An interesting example of this non-composability is seen when two automated market makers (AMM) contracts co-exist in a system. Example 2 highlights this observation.

Example 2.

Consider state containing two instances, and , of the Uniswap contract that exchange between the same two tokens (BBT and ETH). Let be the number of BBT and ETH tokens respectively in , and let be the number of BBT and ETH tokens respectively in .

Lemma 2.

If , then there exists a such that for any , a miner with at least ETH (equiv. BBT) tokens can achieve an end balance of more than ETH (equiv. BBT) tokens by only interacting with and .

Proof.

We prove for ETH tokens but note that the proof is exactly the same for BBT tokens. Let . Consider the following sequence of transactions: (1) Deposit ETH in contract to retrieve tokens of BBT; (2) Deposit the BBT tokens in to get tokens of ETH. We will show that when , there exists a such that depositing () tokens in step (1) results in more than tokens in step (2).

First, suppose that ETH tokens are deposited in in the first step. This results in BBT tokens, which when deposited in gives back ETH tokens. Similarly, if ETH tokens were first deposited in , then the user would end up with ETH tokens. Now, we consider the following cases:

Case (1) . Let . Therefore, which gives . In other words, depositing first in and then in yields more ETH tokens than the initial deposit.

Case (2) . This is analogous to the first case. Let . Therefore, which gives . In other words, depositing first in and then in yields more ETH than the initial deposit. ∎

4.4 MEV Bribery Contracts

New contracts can be introduced into the system specifically with the goal of breaking composability. One such example is that of bribery contracts. The existence of MEV in a system can give rise to new bribery-based incentives for miners to choose the final transaction ordering. For instance, a user could bribe a miner to give her transactions preferential treatment (e.g., a better exchange rate for Uniswap transactions). Such bribes can be carried out securely through bribery contracts. Consider the following simple example.

Example 3.

A user and a miner enter into a bribery smart contract with a payout as follows: submits two valid transaction orderings, and , such that is preferred by ; if is the finalized order, receives a payout proportional to the difference to the user in value of and .

Intuitively, is “bribing” the miner to provide with a more profitable transaction ordering. To maximize its profit, a miner may potentially enter into multiple such bribery contracts with other users, and pick the best one to complete. Bribery contracts could also pose a threat to the long term stability of the system; given enough incentive, it could be worthwhile to mine a consensus block on a stale chain, thereby attempting to rewrite blockchain history. This is similar to time-bandit attacks, which as observed in [19] can be highly detrimental for current blockchain consensus protocols.

4.5 Remarks on Composability

We end with some remarks on our composition examples.

Takeaways for smart contract developers.

Unfortunately, as our composition examples show, the security of a DeFi smart contract may not always depend solely on the contract’s code; design flaws in other contracts—even those deployed much later—may cause composability failures. This is problematic for contract developers since it implies that security of their contracts may in fact be out of their hands.

Remark on capital requirements.

Several of our DeFi composability attacks in this section require the miner to possess some initial capital to carry out malicious transaction reorderings and extract MEV. Despite this, we note that in the real world, capital requirements will rarely be barriers to exploiting the system, even for smaller players, particularly due to the availability of flash loans.Flash loans are essentially risk-free loans that can be offered any time arbitrage or other profitable system behavior can be executed atomically, which is often the case. Flash loans also do not compose with contracts that were designed without flash loans; the attacks in [41] are an example of this. Consequently, adding flash loans to any of our non-composability examples will only exacerbate the impact of malicious transaction reordering.

5 Clockwork Exploration in K

Equipped with our formalism for reasoning about the security of DeFi instruments, we now discuss how best to apply it to real-world contracts. To establish a formal methodology for DeFi security, we instantiate our Clockwork Finance Framework (CFF) in the K framework for mechanized proofs. Appendix C.1 elaborates on why we chose K.

We first describe challenges with formal verification and how we overcome them for CFF (Section 5.1). We describe the design and implementation of CFF, with an emphasis on the soundness and completeness properties in Section 5.2. We then discuss how our CFF executable models are obtained and their properties in Section 5.3. Finally, we use the Uniswap contract (Figure 2) as an example to describe our CFF executable models (Section 5.4).

5.1 Scaling Formal Verification for CFF

Unfortunately, simply applying formal verification tools out-of-the-box to our models turns out to be impractical. To understand why, we need to step back and consider the number of paths from the start of model execution to termination of execution that must be explored by any formal verification tool, in an attempt to exhaustively prove a specific property holds in all possible executions. While general sound formal verification techniques are known to be undecidable, in practice they usually suffice for typical programs, where execution semantics are primarily linear. Branching conditions (e.g., control-flow branches) generally cause an increase in the number of paths to explore. Here, the number of paths that must be explored could be exponential in the number of branches in the program.

However, in our setting, miners can choose any ordering of transactions (others’ transactions plus their inserted transactions) when creating a block. This means that the number of unique paths needed to fully explore the search space is where is the number of transactions to which we apply our CFF. This is asymptotically and concretely more expensive than usual program verification proofs, and consequently impractical for even a modest number of transactions. One existing parallel in the literature is to semantics of concurrency (see e.g., [24]), in which many possible interleavings must be reasoned about. Nonetheless, most such tools either work with a small concurrency parameter, or do not attempt to exhaustively analyze the full state space of interleavings. They attempt only to find plausible bugs based on observed behavior.

Search-space reduction.

To make formal verification practical, we must first reduce the search space to a tractable set of paths. We found that reasoning about all possible transaction orders in the formal model directly results in a large amount of repeated computation as equivalent states are explored (e.g., by re-ordering non-dependent transactions).

Therefore, we apply the following optimizations (both general and DeFi instrument specific) to our analysis to reduce the number of paths by excluding semantically equivalent orderings. First, transactions carry a per user serialization number (“nonce”) such that transactions that are mined out of order are considered invalid. Thus, we consider orderings equivalent if for each non-miner player, the longest consecutive (by nonce) subsequence of transactions is the same (since transactions not belonging to these subsequences are invalid). Second, transactions that interact with different contracts (such as swaps on different Uniswap pairs) are independent of each other. They produce equivalent orderings if reordered relative to one another. Third, we allow for models to incorporate application-specific optimizations. We do so, for example, for our AMM models. The constant-product AMM function is provably path independent [14]. For example, if the miner makes multiple sequential trades selling an asset, exploring their reorderings will have no effect. This optimization cuts the work required by our tool by orders of magnitude, and allows CFF to explore problem instances with larger number of transactions. Note that the above optimizations555We encode our optimizations in the run_uniswapv2_experiments & the run_mcd_experiments files provided in our Github repository. are all sound. While we would ideally like to avoid application-specific optimizations even if sound, and our tool does support this, we found that they substantially improved performance. Similar optimizations will likely be helpful for any MEV analysis.

5.2 Design and Implementation

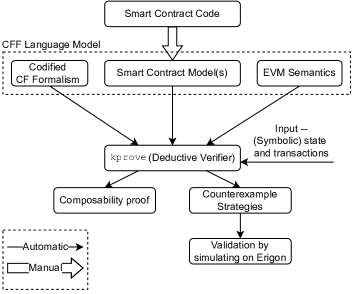

Figure 5 shows the CFF architecture. The core of CFF is the language model whose syntax and semantics are fed to the K framework to automatically generate the deductive verifier kprove along with other tools for parsing, compiling, and symbolic execution of transactions. Note that because of gas limits on the size of a block and computation done in a transaction, the semantics of our language model are decidable. Due to [44], this implies that the deductive verifier we obtain is sound and complete for any reachability property of our language model. Since we model the problem of economic security as a reachability problem (of a state with certain MEV), CFF is attack exhaustive for the transactions and contracts it is given. Any sources of unsoudness in our verification come from our language model, which we now describe.

The first component of our language model defines the specific parameters for the MEV computation as per in the CF model (Section 3). It starts with defining a transaction type, block type, and player types. A player of type “miner” can produce a block by deciding the order of the mempool transactions and any inserted new transactions. Note that the miner cannot manipulate others’ transaction contents, as transactions are digitally signed by their creators. While our formalism from Section 3 allows for arbitrary transaction insertions (including inserting transactions that create new contracts!), our implementation, for tractability, only handles user-specified templates of inserted transactions. These are template transactions because their calldata is allowed to have symbolic parameters rather than concrete values. The lack of arbitrary transaction insertions in our implementation is one source of unsoundness when CFF proves upper bounds on MEV as a measure of economic security. Fortunately, this is not a theoretical limitation since limits on block sizes in Ethereum and other blockchains also constrain the number and type of permissible insertions. (e.g., a transaction cannot exceed the block size). Moreover, arbitrary transaction insertions are observed only rarely in the wild, and incur high gas fees. Barring transaction insertions that create a contract, given enough computing resources, CFF can be extended to reason about all types of insertions by enumerating all possible interactions with the given contracts.

The second component of our language model defines the semantics of the smart contract code and specific smart contract models. The K Framework has built-in semantics of basic arithmatic and logical operations. We enrich it with definitions of currency transfers and smart contract storage. These limited semantics are sufficient to express our smart contract models, and make the verification much faster than incorporating full EVM semantics. We then manually translate the smart contract code into CFF models written in K; we give details in Section 5.3. This needs to be done only once for each contract. Note that our limited semantics of EVM and the way we obtain our CFF models mean that any successful trace obtained in the actual smart contract can be obtained in our CFF models (but not vice-versa). We elaborate on this in Section 5.3. As a result, the proofs of economic security found by CFF on the smart contract models for the given transactions also hold for the actual smart contracts (i.e., there are no false positives introduced here). However, this over-approximation introduces false negatives, i.e., the counterexample strategies (sequence of transaction) found by kprove may not all be valid on the actual smart contracts. To validate potential counterexample strategies, CFF simulates the sequence of transactions in these strategies on an archive node at the appropriate block height. This validation step is fully automatic and takes on average 39 milliseconds per counterexample with a standard deviation of 22 milliseconds.

We have contributed our implementation for simulating transactions at a given block height into the latest public release of the Erigon (popular Ethereum client) software and is now accessible via the eth_callBundle JSON-RPC API.

The gap between our smart contract models and the actual corresponding smart contracts can be closed by substituting the second component of our language model with KEVM [22]. There is a tradeoff, however: the performance of CFF would degrade with use of KEVM. We leave exploration of KEVM integration to future work. We also believe there is room for a wide range of hybrid approaches, including randomized testing / fuzzing, symbolic execution, concolic testing [48], and machine learning, to attempt to learn and optimize for this state transition model.

5.3 Equivalence and Over-Approximation in CFF models

We now discuss a general approach we used for creating our models. This is not the only way to create CFF models, but is the most formal possible approach, allowing for a clear equivalence between the EVM executing on-chain and the CFF model. The approach proceeds in three steps:

-

1.

Path decomposition/verification (before CFF): Perform a path decomposition of the target smart contract, a standard technique required for formal verification of smart contracts in KEVM [22] (outside of CFF). For the highest possible assurance, developing a fully validated model requires some developer effort beyond developing the EVM code, but minimal effort beyond developing a formal proof. Developing unvalidated models is possible, but in our development of CFF we have instead started with a formal proof about the target EVM code (see [49]) and built a CFF model from there.

-

2.

Pruning/selection and refinement: Select all relevant paths in (1), prune reverting or non-MEV-relevant paths (e.g., utility functions), and import these remaining paths into a CFF model. This process can mainly be automated from (1), but some minimal developer judgment on which paths to include can improve analysis speed.

-

3.

Argument of equivalence: If any changes to the obtained path formulas are desired, e.g., variable renaming for readability, argue equivalence of the CFF model in (2) to the path decomposition/formal EVM proof in (1) (see our example code for Uniswap equivalence).

We expand on each on these three steps below.

(1) Path decomposition.

The first step is simply performing a standard complete symbolic exploration of the EVM bytecode of the smart contract. This is a general pattern of smart contract development that is not specific to our work. To prove a contract correct in the K framework, K executes the EVM code against the KEVM semantics [22] on fully symbolic input and EVM state, and decomposes all possible return values of the contract into a mathematical formula over all possible inputs. This involves many possible paths, which represent symbolic branches through the EVM contract code. A contract is said to be verified in K if desired security properties hold as invariants on every such path. A formal specification of a contract’s behavior in K is equivalent to a specification of its behavior on each possible path.

This path decomposition step is not mandatory (one can simply directly give a mathematical specification as on the bottom of Figure 6 without decomposing EVM code), but it leads to high assurance models by construction, and requires little developer effort beyond a formal proof (which has independent value), so it is the technique we choose to describe.

This approach is standard for verifying high-assurance smart contracts. An ideal case study is provided specifically for Uniswap in a report commissioned by Uniswap to demonstrate the security of their contracts, described in [49]. We directly use the results published for the Uniswap EVM contract by Runtime Verification Inc. of the process above to generate our CFF model of Uniswap. We execute their proofs of correctness for Uniswap to extract all paths in the EVM code. One such example path is shown in the upper box of Figure 6, for the tokenToEthInput function, which swaps a token for ETH.

This generated path states that, if the listed path condition (Line 3) is met across input and world state (where the variable names have been manually labeled in some cases by the author of the formal proof, in this case Runtime Verification, Inc.), the return value of the EVM call (Line 2) will be successful and will output the formula listed. This formula contains variables that can be sourced from the input or world state.

The box just above the horizontal line in Figure 6 is another path in which EVM execution reverts when the input and world state meet different conditions.

(2) Pruning/selection and refinement.

In our CFF model, we include a simplified variant of the top path, shown below the line in Figure 6. We do not include the reverting bottom path, and can simplify the resulting path conditions (our model has no concept of e.g. deadlines).

By choosing to omit all reverting paths, we are able to study the properties of interactions between the compositions of non-reverting paths without reasoning about the complex branching and path conditions that may lead to these reverts, simplifying our underlying queries to K (the size of the Z3 [36] formula kprove queries on the backend is proportional to the complexity of the models [44]).

Omitting reverts will never reduce the amount of MEV found by our search. The only consequence will be that some attack we explore would revert in an actual execution, but will not in our analysis. This can only add, not remove, MEV to each execution. We allow for initial discovery of such executions through our automated tool, and filter them out through our automated validation described in 5.2.

(3) Argument of equivalence.

The final step is to argue that each path in our CFF model is equivalent to a successful path generated by contract verification. There are two possibilities. One can manually algebraically inspect the formulas, reasoning about equivalence on-paper. There is a very direct argument in this case that the formulas are structurally the same by inspection, modulo variable renaming.

For automatic equivalence, one can turn to unification, a standard technique for creating a map of variable renamings in syntactically equivalent formulas, to create a substitution of variable names. This can be automated to verify a large number of paths against automatically performed path decomposition. We provide an example argument using unification [3] in the cff_model_equivalence directory. This example shows that our Uniswap CFF model is equivalent to the deconstructed paths from the Uniswap EVM code listed above it (arguing that the bottom and top of Figure 6 are equivalent).

Using the above three-step approach, as we have demonstrated for Uniswap, yields several convenient properties of the resulting CFF models, which hold for all models we provide:

Over-approximation.

Following this technique for model construction, any resulting model is an over-approximation of the EVM bytecode: it models exactly all non-reverting paths on which the underlying contract successfully executes a transaction, and avoids modeling code paths in the contract bytecode or EVM-related semantic rules/details that do not affect relevant state or balances.

Such a model will over-approximate attacks, yielding some attacks that do not actually work on-chain because they may trigger an unmodeled reverting path (which we call false positives). Because weeding out false positives is cheap and easily parallelizable, while reasoning about attacks is expensive and scales with underlying code complexity, the less literal approach of simplifying our model and filtering out reverting paths as needed allows us to explore a wider space of attacks than use of an exact but more complex model.

Our techniques do not generate false negatives, or non-reverting paths that could have occurred in practice but are not explorable by our search. This is because we maintain all non-reverting paths in our models, and strictly relax the relevant path conditions, as we show by example for Uniswap.

We say that under this relaxation—which allows for false positives but not false negatives—our models are over-approximations of the underlying contracts.

Development overhead.

Note that constructing the models according to the three-step strategy we’ve described requires virtually no developer effort/overhead for a developer who has already created a formal proof of contract correctness. Because formal verification is a popular technique for high-assurance contracts, in many cases, robust CFF models can be extracted from existing formal models with minimal additional developer effort. If developers do not want to formally verify their contracts, their CFF models must be coded manually and may prove less secure, as they will need to manually reason about or concretely validate the models’ correctness against an EVM deployment (Section 6.1). Note that this practice is still supported by our framework: we allow for reasoning about models that are not created using our three-step approach, or may be different than the EVM code they represent, as this may be useful for creating new contracts, perhaps before EVM code is even developed. Our intent is here instead to showcase the possibility and process for developing high-assurance, useful models such as our Uniswap model.

Constant model overhead.

If models are developed using the above technique of symbolic path decomposition, we argue that our model size has a constant overhead compared to the corresponding smart contracts. In our work, the model used for verification is only the set of paths we deem relevant. Because we strictly remove paths and conditions from the verified EVM to create an over-approximation, our models are by definition smaller in both number and complexity of semantic rules than a complete contract model (the two relevant scaling metrics for formal language models). While the exact number of paths removed depends on the target contract, this puts our approach in contrast to approaches such as [51], which require, e.g., a path definition for each token pair, and thus scales poorly in size compared to the EVM contract itself.

5.4 CFF Uniswap Model

6 Experimental Evaluation

Using our full CFF models (not the simplified ones from above), we ran several experiments on data from Uniswap V1, Uniswap V2, SushiSwap, and MakerDAO, which we detail here. We aim to experimentally address several key questions:

-

1.

Are our CFF models accurate in reproducing the on-chain behavior of corresponding contracts? How efficient is this execution?

-

2.

Can our models yield mechanized proofs about the extent of security of DeFi contracts and their composition while handling transaction reorderings and generic transaction insertions by miners?

-

3.

Is use of our CFF models economically sensible in uncovering DeFi exploits on-chain?

Experimental setup.

We ran most of our experiments on a mid-range server, equipped with an AMD EPYC 7401P 24-core server processor, 128GB of system memory, and a solid-state drive. For our computations, only the result is written to disk, and therefore our code is primarily CPU-intensive. We did not observe substantial memory overhead. For our parallelism experiments only, we used an AWS cluster of c5 instances with 256 vCPUs unless specified otherwise.

Dataset collection.

We used Google’s BigQuery Ethereum to download every swap and liquidity event generated (until May 16, 2021) by Uniswap V1, Uniswap V2, and SushiSwap. These are three Uniswap-like AMMs that see substantial volume and are relevant to our analyses. In total, we collected 50,038,981 swaps, 2,317,917 liquidity addition events, and 844,709 liquidity removal events traded for 39,329 token pairs. For each token pair, we created a chronological log of events.

For MakerDAO, we used BigQuery to download all the log events generated (until May 16, 2021) by its core smart contract666https://github.com/makerdao/dss/blob/master/src/vat.sol which manipulates CDPs (“vaults”) and updates stability fees and oracle prices. This data includes 322,771 CDP manipulation events (including 284 liquidations) across 18,642 CDPs and 25 collateral types. For each collateral type, we created a chronological log of all relevant events.

6.1 Execution Validation and Performance Experiments

We start with experiments to validate our CFF models with on-chain data and show the performance of our CFF tool.

CFF model validation.

We executed our CFF models on the collected data to ensure that our framework computes the correct final state, i.e., actual on-chain state. For the data from the three AMMs, we ran our executable semantics and inspected the resulting chain. We found that the resulting chain state from our CFF models matches exactly the on-chain state.

We evaluated our CFF Maker model similarly. We found that the stability fees and final debt and collateral values for each CDP before liquidation exactly match the chain state. Since we do not model the liquidation auction mechanism, we do not expect the Maker model to accurately derive the state after liquidation events. MEV reported in our experiments only depends on the state before the first liquidation. The state after liquidation does not affect our results.

We provide scripts to download, process, and validate data for each protocol in the all-data sub-folder of our repository. This validation mechanism highlights the importance of executable formal semantics: execution is a key requirement for validating abstract formal models against real-world data.

CFF performance and parallelism.

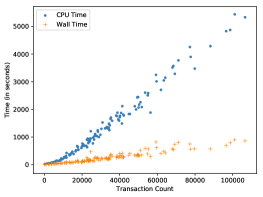

We evaluate the performance for two types of functionalities. First, for different UniswapV2 token pairs, we execute all corresponding on-chain transactions that manipulate the state in the same order as they happened. This measures the execution time of our model, or the time to derive the full on-chain state from the list of transactions. Figure 7 shows the time taken for our CFF to derive the state for different pairs as a function of the number of transactions executed for the pair. K’s internal execution engine intrinsically gives roughly a 4x parallel speedup, which can be seen in the figure as a speedup of real/wall execution time over the amount of total CPU time required to compute model state. These results, combined with our model validation, answer our first experimental question. Our modeling execution engine is sufficiently performant to ensure that our models’ output matches the full chain state on Ethereum for all relevant transactions using only commodity hardware. For instance, the most active pairs traded on any AMM contained about 100k transactions in our data, and it took under 2 hours of CPU time to parse this data and perform end-to-end model validation.

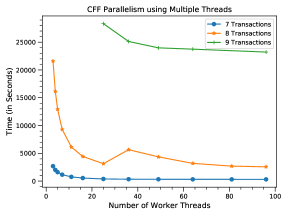

Second, we evaluate the performance for exploring all possible reorderings available to a miner as part of their extraction of MEV, and analyze how the computation of optimal miner orderings can be efficiently parallelized. This will allow us to use our models to also find transaction orderings not exploited by past miners. For these experiments, we use an AWS c5.metal instance optimized for computation. This machine features 96 3.9 GHz cores running on Intel’s Second Generation Xeon Cascade Lake processors, with 192GiB of available memory. In Figure 8, we report the average execution times for attacks with 7, 8 and 9 transactions to be reordered using different number of CPU cores. As discussed in Section 6.3, blocks with 10 or more relevant transactions (i.e., transactions interacting with our models) are rare. Transactions chosen for this particular figure are UniswapV2 transactions and MakerDAO transactions explored using a composition of our UniswapV2 and MakerDAO models, so as to be representative of our MEV extraction experiments described in Section 6.4 ; changing to a different transaction type that deals with our other models does not have any material impact on the reported numbers. Since we used a 96-core machine for our experiments, and given that K provides a 4x parallel speedup, we find that the real wall clock time converges to the fastest execution speed at around 24 worker threads before CPU limitations are reached. Given that our parallel exploration of possible state spaces has no synchronization between parallel workers, the embarrassingly parallel nature of this problem suggests future scaling across machines to be a natural direction for handling larger problem instances. Before the scale ceiling of 24 parallel workers is hit, approximately linear scaling is visible in Figure 8, with some overhead associated with scheduling threads and managing shared system resources.

6.2 Mechanized Proofs and Symbolic Invariants

We now use the deductive program verifier (kprove) from the K framework along with our refined CFF models to assess the security of the composition of Sushiswap and UniswapV2. To achieve this, we have to specify the initial state of the two contracts along with the set of transactions interacting with these particular contracts. These transactions include the user transactions as well any given symbolic transactions inserted by the miner. We also specify a reachability claim that MEV is no greater than 0. If the two contracts compose securely as per our definition in Section 3, then running kprove generates a deductive proof for the specified claim. On the other hand, when the composition under the specified initial state is insecure, kprove automatically generates a counterexample strategy (i.e. sequence of transactions) and a symbolic invariant for MEV in terms of the symbols appearing in the initial state or inserted transaction template. More precisely, the symbolic invariant is a set of (satisfiable) formulae representing the amount of MEV in terms of the variables appearing in the specified initial state and the transactions applied to it.

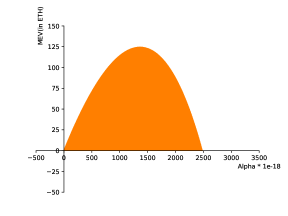

While our CFF can reason about the security of any specification of initial state and set of transactions, we describe an example detailed specification in Appendix C.4 capturing one of the biggest arbitrage opportunities7770x2c79cdd1a16767e90d55a1598c833f77c609e972ea0fa7622b70a67646a681a5 observed on-chain involving two AMMs as reported in [40]. To capture this arbitrage opportunity, we specify the AMM states at blocknumber 10854887, the user transactions interacting with the AMMs, and swap transactions inserted by miner with symbolic parameters (representing the size of miner’s trade). We plot the MEV formula output by our CFF representing the available MEV opportunity as a function of the size of the trades inserted by the miner in Appendix C.4. The arbitrageur in this arbitrage made a profit of 76 ETH, while our CFF reports a higher MEV of 123 ETH not captured by miners.

This example illustrates the power of CFF in finding opportunities left on the table by arbitrageurs currently. Note that our refined mechanized models account for fees, slippage, and integer rounding and hence, the size of the opportunity available to the miner is slightly less than the theoretical value derived in Section 4. We provide the full specification in proofs sub-folder of our repository. CFF can also mechanically reason about the security of many AMMs composed together, as well as more complex composed smart contracts, but we leave this to future work.

6.3 AMM Experiments

We ran a series of experiments on our CFF models for the three AMMs to quantify the MEV extractable from them, and prove the utility of our models further by furnishing real-world insights into available MEV. Our experiments are intended to validate the ability of our tool to uncover profit-seeking miner strategies, and can easily be used for other DeFi contracts.

Reordering to lower-bound MEV.