Eliciting Truthful Reports with Partial Signals in Repeated Games

We consider a repeated game where a player self-reports her usage of a service and is charged a payment accordingly by a center. The center observes a partial signal, representing part of the player’s true consumption, which is generated from a publicly known distribution. The player can report any value that does not contradict the signal and the center issues a payment based on the reported information. Such problems find application in net metering billing in the electricity market, where a customer’s actual consumption of the electricity network is masked and complete verification is impractical. When the underlying true value is relatively constant, we propose a penalty mechanism that elicits truthful self-reports. Namely, besides charging the player the reported value, the mechanism charges a penalty proportional to her inconsistent reports. We show how fear of the uncertainty in the future incentivizes the player to be truthful today. For Bernoulli distributions, we give the complete analysis and optimal strategies given any penalty. Since complete truthfulness is not possible for continuous distributions, we give approximate truthful results by a reduction from Bernoulli distributions. We also extend our mechanism to a multi-player cost sharing setting and give equilibrium results.

1 Introduction

Consider the following repeated game where a center owns resources and one or more strategic players pay the center to consume the resources. In every round, a player self-reports their usage, which will then be used to determine their payment to the center. However, it is not always possible for the center to verify the submitted information from the players. Instead, only part of the actual consumption is revealed to the center based on some publicly known distribution. A player can report any value that is at least the revealed amount. Without any external interference, a player will naturally report exactly the revealed amount (potentially lower than the true consumption) to minimize their payment. The center then needs to determine a payment mechanism such that each player is incentivized to report their true value.

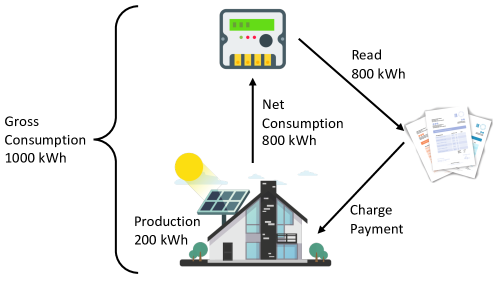

The electricity market is facing precisely the described problem. As the number of electricity prosumers increases each year, new rate structures are designed to properly calculate the electricity bill for this special type of consumers while ensuring that every customer is still paying their fair share of the network costs. Prosumers are those who not only consume energy but also produce electricity via distributed energy resources such as rooftop solar panels. Among different rate structures, net metering is a popular billing mechanism that is currently adopted in more than 40 states in the US [Nat17]. Net metering charges prosumers a payment proportional to their net consumption, i.e., gross consumption minus the production [Sol17], demonstrated in Fig. 1.1. The payment includes the electricity usage as well as grid costs that are incurred by using the electricity network.

The controversy in net metering lies in that prosumers fail to pay their share of the grid costs when they do not have local storage equipment [GJP18]. In the United States, only 4% of the solar panel owners also own the battery to store the produced solar energy [Lea21]. For those who do not own battery storage, the generated power has to be transmitted back to the grid. Accordingly, the daily consumption of power by these prosumers also needs to come from the grid instead of directly from the solar panels. In this way, most prosumers have under-paid their share of the network costs and become “free-riders” of the electricity grid. The grid is often subject to costly line upgrades and net metering unevenly shifts such costs to traditional consumers, who usually come from lower-income households [HP19]. Indeed, previous research works have suggested that prosumers should pay a part of the grid costs proportionally to their gross consumption, not net consumption [GJP18, KHNP19]. However, the gross consumption is hidden from the utility companies since only net consumption can be observed from the meter. Meanwhile, there is no incentive for prosumers to voluntarily report their true consumption as it will only increase their electricity bills.

Fortunately, the production from solar panels usually follows some pattern while the gross consumption of electricity for a typical household stays relatively constant, which is especially true for industrial sites – the major consumers for utilities [NY14, U.S20]. Thus, the observed consumption can be assumed to follow some natural distribution and the center is able to detect dishonesty when a player’s report differs from their reporting history. With this idea, we propose a simple penalty mechanism, the flux mechanism, that elicits truthful reports from players in a repeated game setting when only partial verification is possible. Particularly, a player is charged their reported value as well as a penalty due to inconsistency in consecutive reports in each round. The main goal is to ensure that every player reports their true values and no penalty payment is collected. We show that the combining effect of (i) the penalty rate and (ii) the length of the game is sufficient for inducing truthful behavior from the player for the entire game. As the horizon of the game increases, the minimum penalty rate for truth-telling as an optimal strategy decreases. In other words, it is the fear of the uncertainty in the future that incentivizes the player to be truthful today.

1.1 Our Contribution

We address the problem of eliciting truthful reports when the center sees part of the player’s private value based on some publicly known distribution. The strategic player reports some value that is at least the publicly revealed value and is charged a payment accordingly. We propose a truth-eliciting mechanism, flux mechanism, that utilizes the player’s fear of uncertainties to achieve truthfulness. In the first round, the player is charged a “regular payment” proportional to the consumption they report. Starting from the second round, besides the regular payment, the player is charged a “penalty payment”, which is times the (absolute) difference between the reports in the current and the previous rounds, where the penalty rate is set by the center before the game starts.

Intuitively, a player can save their regular payment by under-reporting their consumption, but they will then face the uncertainty of paying penalties in the future rounds due to inconsistent reports. Under most settings, if is set to be infinitely high, the players will be completely truthful to avoid any penalty payment. However, a severe punishment rule is undesirable and discourages players from participating. Therefore, we want to understand the following question.

What is the minimum penalty rate such that the player is willing to report their true value?

We observe that no finite penalty can achieve complete truthfulness for arbitrary distributions as a player’s true consumption may never be revealed exactly. We can, however, obtain approximate truthfulness for a general distribution from analyzing complete truthfulness for a corresponding Bernoulli distribution. For , the partial signal equals to the true consumption with probability and 0 with probability for . We give results for Bernoulli distributions in Main Results 1 and 2. For arbitrary distributions, we redefine as the probability for having a partial signal that is at least times the true consumption, for , to obtain -truthfulness (Main Result 3).

Main Result 1 (Theorem 3.1) For a -round game with Bernoulli distribution , the player is completely truthful if and only if the penalty rate is at least

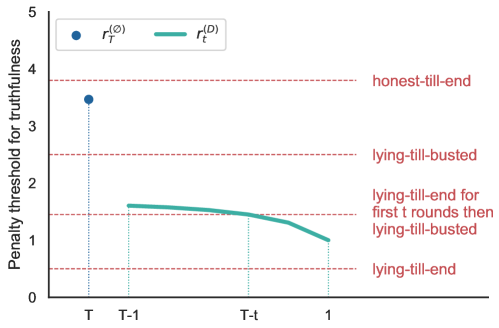

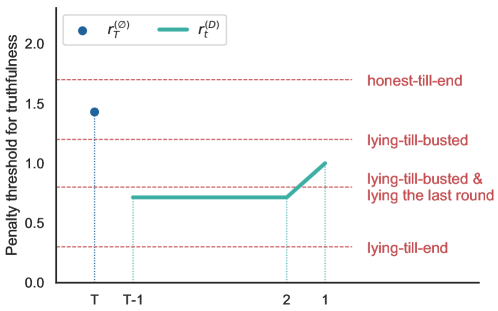

Main Result 1 gives the minimum penalty rate that guarantees complete truthfulness for distributions. We also want to understand how players would behave if the penalty rate is not as high, which describes the situation when the center is willing to sacrifice some degree of truthfulness by lowering the penalty rate. Given any penalty rate, we show that a player’s optimal strategies can be described as one or a combination of three basic strategies, lying-till-end, lying-till-busted and honest-till-end. Specifically, with a low penalty rate, the player is always untruthful to save regular payment, i.e., lying-till-end is optimal. As the penalty rate increases, the player’s optimal strategy gradually moves to lying-till-busted, which is to be untruthful until the partial signal is revealed as the true consumption for the first time and then stays truthful for the rest of the game. When the penalty rate is sufficiently high, the player would avoid lying completely and reports the truth, i.e., she is honest-till-end.

| Bernoulli Prob. | Penalty Rate | Optimal Strategy |

|---|---|---|

| lying-till-end | ||

| lying-till-busted | ||

| + lying last round | ||

| lying-till-busted | ||

| honest-till-end | ||

| lying-till-end | ||

| lying-till-end first rounds | ||

| + lying-till-busted for rest | ||

| lying-till-busted | ||

| honest-till-end |

Main Result 2 (Theorems 3.1 and 3.2) For a -round game with Bernoulli distribution , given any penalty rate , the player’s optimal strategy is summarized in Table 1, where

For arbitrary distributions, including uniform distributions, it is impossible to obtain complete truthfulness without setting penalty to infinity. Main Result 3 gives a reduction from Bernoulli distributions to general distributions for approximate truthfulness.

Main Result 3 (Theorem 4.1) Given and an arbitrary distribution with CDF , if a penalty rate achieves complete truthfulness for where and is the player’s true gross consumption, then the same achieves -approximate truthfulness for distribution .

Finally, we extend our results to multiple players. We note that if the players are charged independently, applying the flux mechanism to each individual elicits truthful reports. A more complicated but realistic setting, especially in net metering, is the cost sharing problem where the players split an overhead cost based on their submitted reports. We propose the multi-player flux mechanism where the penalty payment is the same as before but the regular payment is now a share of some overhead cost. Again, if the penalty rate is sufficiently high, the players stay truthful, regardless of others’ behavior, to avoid any penalty payment, i.e., the truthful report profile forms a dominant strategy equilibrium. As the penalty rate decreases, the truthfulness of a player may depend on other players’ actions. That is, with a lower penalty rate, a truthful report profile forms a Nash equilibrium. For both equilibrium definitions, we are interested in the following question.

What is the minimum penalty rate for the truthful report profile to form a dominant strategy or Nash equilibrium?

We give exact penalty thresholds for both truthful equilibria under Bernoulli distributions and use a reduction to obtain approximate results under arbitrary distributions in Main Result 4.

Main Result 4 (Theorems 5.1, 5.2, 5.3 and 5.4) For any -round game with distribution , truthful strategy profile is a dominant strategy equilibrium if and only if

and a Nash equilibrium if and only if

Given and any distribution with cumulative distribution function , let , where is the true gross consumption. Then -approximate truthful profile is a Nash equilibrium if

and the -approximate truthful profile is a dominant strategy equilibrium if

1.2 Related Works

Unfairness in net metering is a reflection of the famous free-rider problem, where an individual consumes a good but fails to pay or under-pays their share [Mus59]. Possible solution schemes for overcoming the free-rider problems include government taxation [GL77, PJ81], appealing to altruism [HP02, LT08], and privatization [MR04, Vol10]. Researchers in the past have analyzed free-rider problems under the context of blood donation [AT14], healthcare reforms [Cut95], climate change [Ost09], etc. A few papers, particularly, have identified the free-rider problem in net metering for electricity prosumers [HP19, KHNP19, KCE+17, NK15]. Our work follows [KHNP19], where a primitive version of the penalty mechanism is proposed for promoting a fairer electricity rate structure. We formally define the mechanism and provide the corresponding theoretical analysis.

Our setup is also similar to the public goods game, where each player is to make a contribution to a public “pool” that will then be re-distributed. Without external measures, contributing zero to the pool is a Nash equilibrium [AS11]. An application of the public goods game is the famous “tragedy of the commons” [Har68]. Reward or punishment schemes are introduced to incentivize the players to contribute the full amount [BHS03, DZT16, NPK21]. It is suggested that truthful players are willing to punish free-riders in a public goods game [FG00]. Another solution to the public goods game is to track the reputation of each player [MSK02].

Another related line of works is information elicitation with limited verification ability. [CESY12] and [BK19] worked on probabilistic verification where a lying player may be caught by a probability based on her type. Strategic classification considers the problem where individuals manipulate their input to obtain a better classification outcome [HMPW16]. For strategic classification, a number of mechanisms are proposed to inventivize truthful behavior or maximize social welfare [HILW20, LM20, ZC21].

2 Problem Statement

In this section, we formally define our problem under the single player setting and defer the extension to multiple players to Section 5. The player has a gross consumption , which is her private information. The game has rounds where as otherwise the flux mechanism becomes invalid. In each round , the center observes a partial signal, , which is randomly and independently drawn from a distribution supported on . We use to denote the penalty rate. In a flux mechanism, a player cares more about the number of rounds left in the future rather than the number of rounds has passed. Thus we use to denote the current round, where means there are rounds left, including the current round. For example, the first round is round , the last round is round , and the previous round of round is round . For round , the flux mechanism runs as follows.

-

•

The center observes the player’ net consumption .

-

•

The player submits their reported gross consumption which is at least the net consumption, . The player may not be truthful, i.e., may not equal to .

-

•

When , the player’s payment consists of regular payment and penalty payment . When , the player only pays the regular payment.

For , we call the history of round .111The history usually refers to the record from the beginning of the game till the current round. In our mechanism, the history before yesterday does not affect the player’s action for today. Therefore, the history in round only needs to be the report for the previous day. In each round , the player wants to pay the lowest expected total payment by reporting without knowing the partial signals for future rounds. We call a mechanism truthful if the player reports for all rounds. When two reports bring the same expected payment, we break tie in favor of truthfulness. We adopt the assumption from Khodabakhsh et al. [KHNP19] that does not vary with . We explain in Appendix A an easy extension where is drawn from a known range .

3 Bernoulli Distributions

We start with the analysis of Bernoulli distribution as we show later a reduction from an arbitrary distribution to a Bernoulli distribution. We prove it is only optimal for a player to report zero or their true consumption in each round. The optimal strategies can then be characterized by three basic strategies (Definition 3.1). The penalty thresholds are computed by comparing the different combinations of the basic strategies. Due to space limit, we defer most proofs to Appendix B and focus on explaining the intuition in this section.

3.1 Basic Strategies

In a Bernoulli distribution setting, in each round , the partial signal is with probability and with probability . When the partial signal equals to the private value, i.e., , we say that the player is “busted” in round . We first define three basic strategies.

Definition 3.1 (Basic Strategies)

For Bernoulli distributed net consumption , we define the following as the three basic strategies:

-

•

lying-till-end: Report when and otherwise;

-

•

lying-till-busted: Report until for the first time, then report for all future rounds;

-

•

honest-till-end: Report for all rounds.

We note that a player’s optimal strategy for a given penalty rate can be solved by backward induction. Let denote the optimal expected cost for a player starting in round with penalty rate and report for the previous round. Then

where is the expected cost for the player starting in round and reporting (if she is allowed to), with penalty rate and history , i.e.,

The first term on the right-side of the equation above refers to the cost when the partial signal is revealed as and the player has to report . The second term refers to the cost when the partial signal is 0 and the player chooses to report . Let for all . When , i.e., the first round, there is no history . Therefore, the player simply wants to minimize the following total cost,

Solving the recursion will give the characterization of optimal strategies in Table 1, as we demonstrate in Appendix D. In what follows, we discuss a surprisingly simpler and more constructive proof by exploiting the properties of the flux mechanism, which may be of independent interest.

3.2 Main Theorems

We observe that there are two key elements that influence the decision making of the player.

-

(1)

The player’s history, for . The value of directly affects the penalty payment in round . Intuitively, a player is more reluctant to lie if is high and better off lying if is small.

-

(2)

The number of rounds left to play, i.e., . The value of indirectly influences the probability and the number of times a player will be busted in remaining rounds.

Via Lemmas 3.1-3.4, we show these are the only two elements that determine a rational player’s action. The following lemma shows that it is not optimal for a player to report a value strictly between 0 and . Moreover, if a player is untruthful in the previous round, it is better off to remain untruthful. With this lemma, we largely reduce the strategy space we need to consider.

Lemma 3.1

For any round , given , the optimal report in round is . Moreover, if and , then the optimal report is .

Next, we prove that in each round, the optimal strategy is determined by a penalty threshold such that a player will be truthful if and only if the penalty rate is above the threshold. We call them critical thresholds.

Lemma 3.2 (Critical Thresholds)

For , there is a threshold penalty rate such that reporting is optimal if and only if the penalty rate is at least ; For , there is a threshold penalty rate such that reporting is optimal for a player in round with history if and only if the penalty rate is at least .

Lemmas 3.1 and 3.2 together imply that the optimal strategy can only be one or a combination of the basic strategies. In particular, by Lemma 3.1, for any . Moreover, since can only be or , by Lemma 3.2, we only need to determine the values of and for to complete the picture of optimal strategies. In the following two lemmas, we give some properties of these thresholds.

Lemma 3.3

for .

Given the same rounds left, Lemma 3.3 says a player is more inclined to lie without a history than with a truthful history. This is straightforward as lying with a truthful history results in an additional penalty payment.

Lemma 3.4

Given , decreases as increases.

Lemmas 3.3 and 3.4 together tell us the player is least incentivized to be truthful on the first round and is the penalty threshold that ensures truthfulness for the game. We give this important threshold in Theorem 3.1.

Theorem 3.1

The minimum penalty for truthful reporting in a game of rounds with distribution is

| (3.1) |

Proof.

By the definitions of the thresholds, if the penalty and for any , then the player will be truthful. By Lemma 3.3 and 3.4, , for any . Therefore, it is only necessary to compute . By Lemma 3.1 and 3.3, it is sufficient to compare lying-till-busted and honest-till-end in the first segment:

The optimal threshold can be obtained via setting these two expected costs equal,

∎

We see as and decreases as increases. This implies the increasing length of the game incentivizes the player to speak the truth today, even when they do not have to. To understand Theorem 3.1, we observe that it is sufficient to compare lying-till-busted and honest-till-end since ensures the player to stay truthful after being busted. Before the player is busted for the first time, it is not optimal to oscillate between lying and truth-telling, as it is strictly dominated by lying completely. Therefore, the only viable strategies are lying-till-busted and honest-till-end, and the desired threshold sets the expected cost of these two strategies equal.

With a more involved argument, we get the exact values for the truthful threshold given a truthful history, i.e, the ’s. The values of and characterize the optimal strategies for a player and are an alternative representation of Table 1.

Theorem 3.2

For , . For , for and for .

Proof.

See Appendix B.5. ∎

The optimal strategy is visualized in Figs. 3.1 and 3.2 for and , respectively. The -axis is the number of rounds left (), and the -axis is the penalty thresholds for truthfulness. We give examples of penalties via the red dashed lines. For the first round, the player refers to the blue dot representing and is truthful if and only if the penalty is above the blue dot. Afterwards, given rounds left and history , the player looks at the green curve representing and is only truthful if the penalty is above the curve. If the history is , she remains untruthful and reports . Figs. 3.1 and 3.2 visualize the optimal strategies given in Table 1. Both green curves are closely related to . An intuition is that in any round , a player pays if she is truthful and roughly if she lies, where the penalty payment comes from the previous and the next round, each with probability . The penalty that sets these two costs equal is . The actual thresholds vary upon values of and .

4 A Reduction for Arbitrary Distributions

As discussed in the introduction, only the infinite penalty rate will guarantee complete truthfulness under arbitrary distributions, yet there is still hope to obtain approximate results. The trick is to redefine being busted as having a partial signal that is less than times the true consumption, for . Then any arbitrary distribution is reduced to where is the probability that the partial signal is at least .

For approximate truthfulness, we define being -truthful as reporting at least . We reuse the arguments of comparing basic strategies from Section 3 to determine an upper bound for the penalty rate that guarantees -truthfulness. We introduce the notion of approximate truthfulness in Definition 4.1 and give the reduction in Theorem 4.1. We demonstrate the reduction with uniform distributions in Example 4.1.

Definition 4.1 (-truthfulness)

A reporting is -truthful when for all .

Theorem 4.1

Given and an arbitrary distribution with CDF , if a penalty rate achieves complete truthfulness for where , then the same achieves -approximate truthfulness for distribution .222The reduction depends on the players’ gross consumption, which is private information. In reality, if the mechanism has some information on upper bounds of , we are still able to set a penalty rate (which may not be minimum) to obtain truthfulness.

Proof.

Recall that being “busted” means the player has a realization. For general distributions, given , we redefine being busted as having a realization at least . Then the probability of being busted is . The proof is essentially the same as that of Theorem 3.1 for . We analyze the segment between the first day and the day when the player is busted. Assume the minimum report from the player during the segment is , . We compare the savings the player gets from using this strategy versus reporting and the corresponding additional penalty that she needs to pay.

The player will report every round in the segment when expected penalty exceeds expected savings. The term is canceled and the rest calculation is the same as the case where . ∎

Example 4.1

Assume partial signals follow a uniform distribution . Let be the truthful threshold of where , i.e. . Then using ensures -truthfulness for by Theorem 4.1. For uniform distributions, it is impossible to obtain complete truthfulness unless , which can be verified by setting .

5 Extension: A Cost Sharing Model

We extend the problem to the multi-player setting and focus on the cost sharing among homogeneous players. Let be the set of players with . Each player has a private value , and we assume all players are symmetric, i.e., for all (see Appendix A for a relaxation). All players in split an overhead cost , which is at least the total gross consumption, i.e., . The game has rounds in total. Given penalty rate , we analyze the following multi-player flux mechanism.

-

•

The center observes a partial signal representing player ’s net consumption for each player ;

-

•

Each player submits their reported gross consumption that is at least their net consumption, ;

-

•

If , player ’s pays regular payment and penalty payment . If , the players only pay regular payments.

We call the history for player in round and the group history. If everyone lies in a round, the overhead cost is split evenly among all players. A mechanism is truthful if every player reports for every round. We are interested in computing the minimum penalty rates such that truthful reports form a Nash equilibrium (NE) or a dominant strategy equilibrium (DSE). Informally, a strategy profile is a NE if no player wants to unilaterally deviate, and it is a DSE if no player wants to deviate no matter what the other players do. We show that approximate results for any arbitrary distribution can be deducted from an exact analysis for a Bernoulli distribution. Due to space limit, we defer all proofs to Appendix C.

Fix an arbitrary player and the other players’ strategy . Let denote the reported gross consumption by players with group history and realizations in round . A strategy is called ’s best response if it is the solution of the following recursion.

where the expected cost can be expanded as

For the first round when , the player would like to minimize the total expected cost, i.e.,

Given a strategy profile , if is a best response to for every player , then is called a Nash equilibrium. If is a best response to any (not necessarily ) for any player , is then called a dominant strategy equilibrium.

Similar to the single player setting, we avoid solving the recursion by exploiting the properties of the mechanism. Again, we start our analysis with being a Bernoulli distribution and provide a reduction for approximate truthfulness when is an arbitrary distribution. In the single player model with Bernoulli-distributed , we have shown that it is only optimal for a player to report or her actual consumption . We claim it is the same case for multiple players. Moreover, if a player lied yesterday and also has an observed consumption of 0 today, they will report 0 regardless of other player’s actions.

Lemma 5.1

For Bernoulli-distributed , reporting anything strictly between 0 and D is sub-optimal in a multi-player flux mechanism. Moreover, if , it is optimal to report .

Starting from this point, we assume that every player reports either or . When , we show that the multi-player model reduces to the single player model with a multiplicative factor of . The reason of the reduction is that the savings of switching to lying from being truthful for a player is always , regardless of what the other player does.

Lemma 5.2

When , the multi-player model reduces to single player model. The truthful penalty threshold is times (3.1).

For general , we show it is sufficient to analyze the maximum difference between lying and truth-telling for player in round given group history . In a DSE, a player achieves the biggest gain from lying if all players were lying in the previous round. We then use to compare lying and truth-telling for a player.

Theorem 5.1

For the distribution, truthful strategy profile forms a dominant strategy equilibrium if and only if

| (5.1) |

If we slowly lower the penalty from (5.1), we will hit a threshold such that truth-telling is an NE. The difference between the truthful NE and the DSE is that now we can assume that every player is truthful in the first round and show that player would not deviate unilaterally. However, we shall not assume that player remains truthful for the rest of the game. This is because if player lies in the first round, player can observe the report of in the second round and deviate from truthful behavior. We first show that if , players with truthful history stay truthful. Then we can safely assume player remains truthful throughout the game. In this way, truthful NE is reduced to the case where there is one strategic player and truthful players. It is not hard to see the threshold is precisely .

Theorem 5.2

For the distribution, truthful strategy profile forms a Nash equilibrium if and only if

| (5.2) |

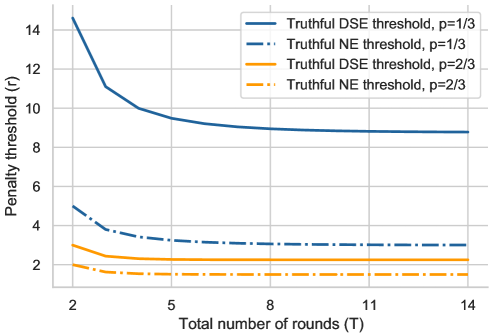

We visualize penalty thresholds in Fig. 5.1 for different ’s and ’s. The -axis is the total number of rounds for a game and the -axis is the penalty rate that guarantees the specified equilibrium. The blue and orange lines are penalty thresholds for and , respectively. The solid and dashed lines are thresholds for truthful DSE and NE, respectively. All four thresholds in Fig. 5.1 decrease as increases, suggesting that the increasing length of the game promotes truthful equilibria. From expressions (5.1) and (5.2), we see that the DSE and NE thresholds tend to be the same as approaches 1.

Similar to the single-player model, we extend the results for Bernoulli distributions to approximate results for general distributions. Given , we redefine being busted as having an observed consumption at least . For the dominant strategy equilibrium, we find the threshold such that being -truthful is a dominant strategy. For Nash equilibrium, we first define the approximate truthful NE, which is a natural extension of the complete truthful NE.

Theorem 5.3

Given and some general distribution , let . The -truthful strategy profile forms a dominant strategy equilibrium if

| (5.3) |

Definition 5.1 (-truthful Nash equilibrium)

Given , a reporting profile is an -truthful Nash equilibrium if for all and no player wants to deviate from being -truthful in any round.

Theorem 5.4

Given and some general distribution , let . The -truthful strategy profile forms a Nash equilibrium if

| (5.4) |

We see that both the penalty thresholds, (5.3) and (5.4) are close to times their Bernoulli thresholds, (5.1) and (5.2), for . Recall that in the single-player model, -truthfulness can be obtained by directly using the Bernoulli threshold with . In the multi-player model, however, we have to multiply the Bernoulli threshold with a factor of , which suggests it is more difficult to get every player to speak the truth under the cost sharing setting. We note that both penalty rates (5.3) and (5.4) are upper bounds for the actual thresholds. This is because we treat any report greater than as . We conjecture that the exact thresholds are not far from thresholds (5.3) and (5.4).

6 Conclusion and Open Problems

We propose a penalty mechanism for eliciting truthful self-reports when only partial signals are revealed in a repeated game. A player faces trade-off between under-reporting today and paying a penalty in the future due to the uncertainty of partial signals. We find that the length of the game naturally reduces the minimum penalty rate that incentivizes truth-telling. Given any penalty rate, we give a characterization of the optimal strategies under both single- and multiple-player settings for any distribution. We identify a penalty rate that achieves complete truthfulness for Bernoulli distributions, which can be used in a reduction to obtain approximate truthfulness for arbitrary distributions.

A possible future direction is to extend our results to asymmetric multi-player settings where players do not have the same gross consumption or the same distribution for partial signals. For heterogeneous players, we may then consider, in addition to truthfulness, the fairness of the mechanism. It would be interesting to develop a definition of fairness for the cost sharing model and compute the fairness ratios accordingly. It is also worthwhile to derive other truthful and fair mechanisms that do not involve penalty.

References

- [AS11] Marco Archetti and István Scheuring. Coexistence of cooperation and defection in public goods games. Evolution: International Journal of Organic Evolution, 65(4):1140–1148, 2011.

- [AT14] Ignacio Abásolo and Aki Tsuchiya. Blood donation as a public good: an empirical investigation of the free rider problem. The European Journal of Health Economics, 15(3):313–321, 2014.

- [BHS03] Hannelore Brandt, Christoph Hauert, and Karl Sigmund. Punishment and reputation in spatial public goods games. Proceedings of the royal society of London. Series B: biological sciences, 270(1519):1099–1104, 2003.

- [BK19] Ian Ball and Deniz Kattwinkel. Probabilistic verification in mechanism design. In Proceedings of the 2019 ACM Conference on Economics and Computation, pages 389–390, 2019.

- [CESY12] Ioannis Caragiannis, Edith Elkind, Mario Szegedy, and Lan Yu. Mechanism design: from partial to probabilistic verification. In Proceedings of the 13th acm conference on electronic commerce, pages 266–283, 2012.

- [Cut95] David M Cutler. The cost and financing of health care. The American Economic Review, 85(2):32–37, 1995.

- [DZT16] Yali Dong, Boyu Zhang, and Yi Tao. The dynamics of human behavior in the public goods game with institutional incentives. Scientific reports, 6(1):1–7, 2016.

- [FG00] Ernst Fehr and Simon Gächter. Cooperation and punishment in public goods experiments. American Economic Review, 90(4):980–994, 2000.

- [GJP18] Axel Gautier, Julien Jacqmin, and Jean-Christophe Poudou. The prosumers and the grid. Journal of Regulatory Economics, 53(1):100–126, 2018.

- [GL77] Theodore Groves and John Ledyard. Optimal allocation of public goods: A solution to the” free rider” problem. Econometrica: Journal of the Econometric Society, pages 783–809, 1977.

- [Har68] Garrett Hardin. The tragedy of the commons: the population problem has no technical solution; it requires a fundamental extension in morality. science, 162(3859):1243–1248, 1968.

- [HILW20] Nika Haghtalab, Nicole Immorlica, Brendan Lucier, and Jack Z Wang. Maximizing welfare with incentive-aware evaluation mechanisms. arXiv preprint arXiv:2011.01956, 2020.

- [HMPW16] Moritz Hardt, Nimrod Megiddo, Christos Papadimitriou, and Mary Wootters. Strategic classification. In Proceedings of the 2016 ACM conference on innovations in theoretical computer science, pages 111–122, 2016.

- [HP02] Jean Hindriks and Romans Pancs. Free riding on altruism and group size. Journal of Public Economic Theory, 4(3):335–346, 2002.

- [HP19] Quentin Hoarau and Yannick Perez. Network tariff design with prosumers and electromobility: Who wins, who loses? Energy Economics, 83:26–39, 2019.

- [KCE+17] Ioannis Koumparou, Georgios C Christoforidis, Venizelos Efthymiou, Grigoris K Papagiannis, and George E Georghiou. Configuring residential pv net-metering policies–a focus on the mediterranean region. Renewable Energy, 113:795–812, 2017.

- [KHNP19] Ali Khodabakhsh, Jimmy Horn, Evdokia Nikolova, and Emmanouil Pountourakis. Prosumer pricing, incentives and fairness. In Proceedings of the Tenth ACM International Conference on Future Energy Systems, pages 116–120, 2019.

- [Lea21] Laura Leavitt. Solar batteries: How renewable battery backups work. https://www.cnet.com/home/energy-and-utilities/solar-batteries-how-renewable-battery-backups-work/, 2021. Accessed: 2022-08-13.

- [LM20] Annie Liang and Erik Madsen. Data and incentives. In Proceedings of the 21st ACM Conference on Economics and Computation, pages 41–42, 2020.

- [LT08] Susan K Laury and Laura O Taylor. Altruism spillovers: Are behaviors in context-free experiments predictive of altruism toward a naturally occurring public good? Journal of Economic Behavior & Organization, 65(1):9–29, 2008.

- [MR04] Keith E Maskus and Jerome H Reichman. The globalization of private knowledge goods and the privatization of global public goods. Journal of International Economic Law, 7(2):279–320, 2004.

- [MSK02] Manfred Milinski, Dirk Semmann, and Hans-Jürgen Krambeck. Reputation helps solve the ‘tragedy of the commons’. Nature, 415(6870):424–426, 2002.

- [Mus59] Richard A Musgrave. The theory of public finance; a study in public economy. Kogakusha Co., 1959.

- [Nat17] National Conference of State Legislators. State net metering policies. https://www.ncsl.org/research/energy/net-metering-policy-overview-and-state-legislative-updates.aspx, 2017. Accessed: 2022-08-13.

- [NK15] Ahlmahz I Negash and Daniel S Kirschen. Combined optimal retail rate restructuring and value of solar tariff. In 2015 IEEE Power & Energy Society General Meeting, pages 1–5. IEEE, 2015.

- [NPK21] Laila Nockur, Stefan Pfattheicher, and Johannes Keller. Different punishment systems in a public goods game with asymmetric endowments. Journal of Experimental Social Psychology, 93:104096, 2021.

- [NY14] Steven Nadel and Rachel Young. Why is electricity use no longer growing? In American Council for an Energy-Efficient Economy Washington, 2014.

- [Ost09] Elinor Ostrom. A polycentric approach for coping with climate change. Available at SSRN 1934353, 2009.

- [PJ81] Ernest C Pasour Jr. The free rider as a basis for government intervention. The Journal of Libertarian Studies, 5(4):453–464, 1981.

- [Sol17] Solar Energy Industry Associations. Net metering. https://www.seia.org/initiatives/net-metering, 2017. Accessed: 2021-09-01.

- [U.S20] U.S. Energy Information Administration. Hourly electricity consumption varies throughout the day and across seasons. https://www.eia.gov/todayinenergy/detail.php?id=42915, 2020. Accessed: 2021-11-03.

- [Vol10] Alexander Volokh. Privatization, free riding, and industry-expanding lobbying. International Review of Law and Economics, 30(1):62–70, 2010.

- [ZC21] Hanrui Zhang and Vincent Conitzer. Incentive-aware pac learning. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 35, pages 5797–5804, 2021.

Appendix: Missing Materials

Appendix A Justifying the Assumption that Gross Consumption is Constant

In the prosumer pricing problem, we adopt the assumption from Khodabakhsh et al. [KHNP19] that , the gross electricity usage, remains constant throughout the time horizon. According to U.S. Energy Information Administration, the electricity usage typically follows a daily pattern, which means within some period (e.g., day, month or season), the electricity consumption does not vary much [U.S20]. This is especially true for industrial sites, which are the major consumers for utilities [NY14]. Therefore, we can always discretize the time horizon into sub-intervals such that the electricity consumption within each interval is relatively constant.

To relax this assumption, let the gross consumption for each round come from a known range, i.e., . The center knows the and but does not necessarily know for any . We show that our results extend straightforwardly. Recall that in the analysis of Bernoulli distributions, we compare the basic two strategies and find the penalty rate that sets the two expected costs equal. We can find an upper bound for the truthful threshold by bounding the expected cost of lying-till-busted and honest-till-end from below and above, respectively. Then the resulting penalty rate is simply the original threshold (3.1) times the ratio . For the reduction from Bernoulli distributions to any arbitrary distribution with cdf , given , we now define and use the same argument to obtain an upper bound of penalty rate that achieves -truthfulness. For the multi-player model, we add the multiplicative ratio in every expression for an upper bound of the desired penalty rate. This relaxation will also help add heterogeneity to the multi-player model.

Appendix B Missing Proofs in Sections 3

B.1 Proof for Lemma 3.1

Proof.

To see the first sentence, we can observe that the cost function is a linear function of today’s report and thus either or achieves the optimality. To see the second sentence, we consider the last round in the optimal strategy such that when but . It is obvious if is the last round, and thus we assume . By reporting in round , the expected total cost afterward is

where the inequality is because for any and ,

The last term is exactly the expected total cost by reporting 0 in round but adopting the same strategy with the optimal one afterward, which is contradiction with being optimal. Thus we complete the proof of the lemma. ∎

B.2 Proof for Lemma 3.2

Proof.

Note that by Lemma 3.1, can only be or . Moreover, for any . Therefore, we only need to show the existence of and for . It suffices to show the following claim: For any round with , if the optimal strategy is given penalty rate , then is also optimal for any ; if the optimal strategy is given penalty rate , then is also optimal for any .

To prove the claim, we use induction on . When , it is easy to see that exists and is equal to 1. Consider rounds left and the optimal strategy is to report given penalty and (or no history if ). If we increase penalty to , by induction, the optimal strategy for future rounds either remains the same or switch to from . Given history and report , the payment for thin round is independent from penalty rate . Therefore, reporting is still optimal. A similar argument can be made for reporting . ∎

B.3 Proof for Lemma 3.3

Proof.

Given the same rounds left, it is straightforward to see that players with a truthful history is more incentivized to lie compared to when she has no history. This is because she needs to pay an additional payment of whenever she has a truthful history. Mathematically, let . Then we have

The above inequalities show that when , the player prefers truth-telling over lying when she has a truthful history, which implies . ∎

B.4 Proof for Lemma 3.4

Proof.

An equivalent statement of Lemma 3.4 is that given a penalty , if a player is truthful when there are rounds left, then she is also truthful when there are rounds left. Let us prove the alternate statement.

Assume and that the player is truthful when there are rounds left. Let denote the optimal cost for a player if she reports in the current round and there are rounds left. Since the player is truthful when there are rounds left, we have

Now assume there are rounds left and the player is free to lie in the first round. By Lemma 3.1, there are the following two cases.

-

•

player reports in the first round

If the player also reports in the second round, she pays . Otherwise she pays , which is dominated by reporting for both rounds.

-

•

player reports in the first round

Then the player’s total expected payment is

Therefore, the optimal strategy is to report in the first two rounds and the rest of the game is exactly the same as when there are rounds left. ∎

B.5 Proof for Theorem 3.2

Proof.

We first show the proof for by induction on . Let . Assume there are rounds left. Note that increases in , which means that if , then for , i.e., the player stays truthful for the rest of the rounds. Similar to the argument in Theorem 3.1, we compare the expected payments of the two strategies, namely lying-till-busted (“lying”) and being honest, within a segment. Note that the segment now starts with being busted, because the player has a truthful history.

The penalty that results in truthfulness sets these two payments equal, i.e. .

The proof for is slightly different. First note that for , it is not hard to see the threshold by comparing the cost of being honest (i.e., ) and the cost of lying (i.e., ). For rounds left, we apply the same argument above, with the consideration that the player will switch to lying in the very last round if she is allowed to. Therefore, we have

The penalty that sets the above two expected costs equal is . ∎

Appendix C Missing Proofs in Section 5

C.1 Proof for Lemma 5.1

Proof.

We can use a similar argument in the proof for Lemma 3.1 to prove that if a player lied yesterday, it is better off to lie today. We consider the last round in the optimal strategy such that when but . It is obvious if is the last round, and thus we assume . By reporting in round , the expected total cost afterward is

which is the expected total cost by reporting 0 in round but adopting the same strategy with the optimal one afterward. This contradicts that is optimal.

To see that partial reporting is optimal, rewrite the payment for the current round as

whose second derivative is negative with respect to . This means that the payment function is concave in and will take minimum at either of the endpoints and . ∎

C.2 Proof for Lemma 5.2

Proof.

In the single player model, if a player switches to lying from being honest, she saves for regular payment and then pays penalty if she has a truthful history. Now in the two player model, since players are symmetric, we fix the action of player 2 and see what happens with player 1.

| player 2 | |||

|---|---|---|---|

| Honest | Lying | ||

| player 1 | Honest | ||

| Lying | |||

No matter if player 2 is honest or lying, for player 1, switching to lying would save and may cost a penalty payment of . By applying the same argument seen in Section 3.1 with the new expected savings and penalties, we get the same penalty threshold, except with a multiplicative factor. ∎

C.3 Proofs for Theorem 5.1 and 5.2

For general strategic players, we develop an alternative way to compute the penalty thresholds for NE and DSE. Interestingly, we only need to make use of the following important definition, , to derive a universal framework for equilibrium proofs.

Definition C.1

Let denote the expected cost for player with when there are rounds left and the group history is . Define

as the difference in the expected payments by reporting versus for player , given rounds left and the reports of other players, .

To simplify the notation, we remove the superscript in the definition and write . By Lemma 5.1, is a string of size consisting of ’s and ’s. We first present a technique to obtain upper bounds of given .

Lemma C.1

Some upper bounds of :

-

(i)

-

(ii)

Proof.

We prove (i) where and the proof for (ii) is similar. Let . We prove by induction.

Base case. . With probability , having a or history pays the same regular payment and the history needs to pay penalty. With probability , only the history pays the regular payment.

Note that in the second equality represents the number of players being busted in .

Induction step. Assume Lemma C.1 is true for . Consider rounds left.

∎

An important property of is that it is monotone increasing as the number of ’s in increases. One way to understand this property is that a player with a zero history is more likely to lie in the next rounds, which in turn increases the expected regular payment if player is truthful. We prove this property mathematically in Lemma C.2.

Lemma C.2

If contains more zeros than , then

Proof.

First note that the only non-trivial case is when the penalty is just high enough such that players with truthful history stay truthful and players with 0 history lie whenever realization is 0. Since every player is symmetric, players with the same history will act the same. If the penalty is too low, does not depend on and . Same when the penalty is too high then players will be truthful regardless of history. Now we can assume players with truthful history stay truthful regardless of the realization and players with zero history lie whenever possible. We prove by induction on .

Base case. . Let contain zero’s (and ’s). Then we have

where

and

Note that and ’s depend on . On the other hand, ’s do not depend on and is an increasing sequence in . Now consider that contains zeros, and . Then we have

Induction step. Assume the lemma is true for . We prove for rounds left. Assume again contains zero’s.

where ’s are the same as earlier, and ’s are now

By induction, increases in . Thus, ’s is again an increasing sequence in . We re-use the argument in the base case and prove for with zeros. ∎

With this property, we develop a framework for the equilibrium proofs of both DSE and NE:

-

1.

Determine what look like based on the type of the equilibrium we are trying to compute;

-

2.

Upper bound with an expression using , , , and (see Lemma C.1);

-

3.

Compare player ’s expected payment on the first round when she lies or tells the truth using ;

-

4.

Find the penalty rate that sets the two expected payments equal, and that is the desired penalty threshold.

Proof for Theorem 5.1

Proof.

Fix a player . To show that being truthful is a dominant strategy for player , we want to look at the situation that maximizes the difference between truth-telling and lying for player , which is precisely when every other player is lying as much as possible, by Lemma C.2. Now we assume every other player reports whenever they can. We compare the expected cost of being truthful and lying on the very first round.

where represents the number of players in that are busted in round . We would like to find the penalty rate such that . By Lemma C.1, we have

which is negative when . Since we are analyzing the case that maximizes the differences in lying and truth-telling, we can say that truthfulness is a Nash equilibrium if and only if the penalty rate is above the given threshold. ∎

Proof for Theorem 5.2

Proof.

Based on the discussion, we first assume that every player is truthful in the first round and . We want to prove that some player does not want to deviate from being truthful in the next round. Then it follows that the threshold for truthful NE is equivalent to the case with single sophisticated player and truthful players. Since the threshold (5.2) is exact in the model with one sophisticated and truthful players, this threshold is the exact threshold for truthful Nash equilibrium.

C.4 Proof for Theorem 5.3

Proof.

Let . Assume, for contradiction, that the player adopts some strategy that has a minimum reporting of , . We compare the expected costs of this strategy and the strategy of being -truthful. We re-define as follows:

Similar to the proof in Theorem 5.1, we want to upper bound . Here we show the computation of for and using the recursion argument in the proof of Lemma C.1, we can show that

| (C.1) |

After that, we use the same argument in the proof of Theorem 5.1 to obtain the threshold for the first day and Theorem 5.3 follows. Now we prove the statement for . If the net consumption for the last day exceeds (which happens with probability ), then the difference between the penalty payments is . Otherwise the player can save some regular payment by reporting some where . Let denote the number of players being busted beside the target player. Then and . Therefore,

and

given , which is satisfied because actual threshold for in (5.3) is higher. Using the recursion argument in Lemma C.1, we can obtain the expression (C.1). ∎

C.5 Proof for Theorem 5.4

Proof.

Similar to the proof of Theorem 5.2, we only need to show that players who had a -truthful history would stay truthful. We redefine as in the proof of Theorem 5.3 and use a similar argument in Theorem 5.2 to show that for and . Then we can safely assume that players stays -truthful in the entire game. Now we compare player ’s expected savings and penalties by reporting some from being -truthful.

Expected penalties exceed expected savings when . ∎

Appendix D Recursion Approach

In Section 3.1, we briefly mentioned that we can solve for the optimal cost for the Bernoulli distribution via recursion. In the recursion proof, we compute explicitly the expression for for and for the first round. Here, we provide such expressions and optimal strategies can be easily derived from these expressions. We note that we presented the alternative proof in the main article because it showcases the essence of our proposed mechanism. Moreover, the recursion approach would be computationally heavy for continuous distributions whereas the proof in the main body can be extended to any general distributions.

The following is the complete proof via backward induction. For simplicity, we set , which does not affect the results. We break the proof into four cases and together, the four cases paint the picture of the optimal strategy under the Bernoulli distributions for the single player model.

| Case 1 | and OR and |

|---|---|

| Case 2 | and |

| Case 3 | and |

| Case 4 | and |

Case 1. and OR and

Lemma D.1

For any , when and OR when and , given yesterday’s arbitrary report ,

which is achieved by setting . If , is the unique optimal report; if , the optimal report is any value .

Proof.

We prove the lemma by induction. When ,

| (D.1) |

The coefficient for is either (if ) or (if ). Both are non-negative for . Therefore, by setting , we achieved the optimal cost:

Assume the lemma is true for round . For round and given yesterday’s report ,

The coefficient for is as follows

When , both coefficients are non-negative. Therefore, choosing is optimal and the optimal cost is

By induction, we proved the lemma. ∎

Theorem D.1

If and , or if and , the player’s optimal strategy is lying-till-end.

Proof.

Lemma D.1 showed that the theorem is true for every day except the first day. We now show that the theorem is true for the first day.

The coefficient for is non-negative in both cases. So the optimal choice for the first day is also zero. Along with the Lemma D.1, we’ve shown the optimal strategy is lying-till-end for and with optimal cost

∎

Case 2. and

Lemma D.2

For any , when and , given yesterday’s arbitrary report ,

which is achieved by setting .

Proof.

We prove the lemma by induction. When ,

Since , and . Thus is a valley function with respect to and takes minimum by setting . Therefore, can be written as

Assume up to round , the lemma holds. For round and yesterday’s report ,

where

If ,

Note that the coefficient of is times the following

where the inequality is due to .

If ,

where the coefficient of is positive. Thus the minimum of is achieved at , i.e.,

By induction, we proved the lemma. ∎

Theorem D.2

When and , the optimal strategy is lying-till-busted for the first rounds and lying in the last round.

Proof.

Let us consider the first day.

The coefficient for is positive when , thus . ∎

Case 3. and

Lemma D.3

For , , and any , given yesterday’s arbitrary report ,

which is achieved by setting .

Proof.

We prove the lemma by induction. When , the expected cost is

The coefficient for is for and is positive. The coefficient is for and is negative. This implies that is a valley function and the minimum is achieved by setting . Thus the optimal cost for is

Assume up to round , the lemma holds. For round and yesterday’s report ,

where

When , the coefficient for is as follows

which is always positive. When , the coefficient is as follows

which is negative when

| (D.2) |

Note that from Equation (D.2), we see when , the right-hand-side is smaller than . Thus given , the function is a valley function, and the minimum is achieved by setting . The optimal cost in round is then

By induction, we proved the lemma. ∎

Theorem D.3

When , if , honest-till-end is the optimal strategy; if , lying-till-busted is optimal.

Case 4. and

For any , let

and

Claim D.1

When , .

Proof.

The derivative of with respect to is strictly positive:

The edge cases can be checked manually. Thus, is increasing w.r.t. . ∎

Claim D.2

When and , if and only if and .

Proof.

We simplify the expression as follows.

Thus if and only if

∎

Next, we further distinguish the following subcases for each .

SubCase 4.1. and

We start with the last day,

Given , , achieved by setting .

Now we consider the rounds after the first rounds, i.e., the last rounds.

Lemma D.4

When and , given yesterday’s arbitrary report ,

| (D.4) |

which is achieved by setting for any and by setting for .

Proof.

For ,

Given and , is a valley function and takes minimum at . Thus,

In general, for any ,

By Claim D.2, for , since . Then is a valley function and takes minimum at . For , since . Then the coefficient for in both cases is positive and the expected cost takes minimum at . ∎

Finally, we consider the first day,

where the coefficient for is positive. Thus on the first day, the optimal . In conclusion, we have the following theorem.

Theorem D.4

When , , and , the optimal strategy is lying-till-end for the first rounds, and lying-till-busted for the rest of the game.

SubCase 4.2.

When , as we have seen in previous subcase,

where

Thus if and only if

In conclusion, we have the following theorem.

Theorem D.5

When , if , the optimal strategy is lying-till-busted; if , the optimal strategy is honest-till-end.