∎

Shangchun Road 995, Pudong, Shanghai 201209, China

22email: iambabyface@hotmail.com

Three fundamental problems in risk modelling on big data: an information theory view

Abstract

Since Claude Shannon founded Information Theory, information theory has widely fostered other scientific fields, such as statistics, artificial intelligence, biology, behavioural science, neuroscience, economics, and finance. Unfortunately, actuarial science has hardly benefited from information theory. So far, only one actuarial paper on information theory can be searched by academic search engines. Undoubtedly, information and risk, both as Uncertainty, are constrained by entropy’s law. Today’s insurance big data era means more data and more information. It is unacceptable for risk management and actuarial science to ignore information theory. Therefore, this paper aims to exploit information theory to discover performance limits of insurance big data systems and seek guidance for risk modelling and the development of actuarial pricing systems.

Keywords:

risk information theory information entropy big data actuarial science1 Introduction

Since Claude Shannon published his most important paper “A mathematical theory of communication” in 1948, Information Theory has been established and widely fostered many scientific fields, such as statistics, artificial intelligence, biology, behavioral science, neuroscience, economics, and finance. Even in finance, which is most similar to actuarial science, for example, there is a lot of studies applying information theory, such as the financial value of information barron1988a , portfolio theory ambachtsheer2005beyond , credit ratings bariviera2015efficiency , and the impact of social media on financial markets zheludev2015when . In contrast, there is only one paper on information theory in actuarial science so far. Reference sachlas2014residual discussed the residual entropy and past entropy in actuarial science and survival models for the deductible and limit of insurance claims. Unfortunately, from the search results of academic search engines, it can be said that actuarial science has hardly benefited from information theory.

First of all, theoretical research of risk theory and actuarial science requires information theory. By definition, both risk (in risk theory) and information (in information theory) are uncertainties theoretically. In the universe, everything is energy, and information is also energy. All spontaneous energy evolution processes, including risk processes, obey the second law of thermodynamics, also known as the Principle of Entropy Increase. Undoubtedly, information and risk, both as uncertainties, are constrained by information entropy’s law. Obviously, information theory also applies to risk theory and actuarial science.

Secondly, the practical application of risk management in the insurance industry (such as self-driving car insurance, cyber insurance etc.) also requires information theory. Today’s insurance industry has entered an era of insurance big data. This means that more huge amounts of data (i.e. information) can be used for actuarial modeling and risk management. Faced with massive information of big data, it is unacceptable for risk management and actuarial science to continue to ignore information theory.

Therefore, in order to meet the above theoretical and practical requirements, this paper aims to exploit information theory to discover the performance limits of insurance big data systems, and seek guidance for risk modeling and the development of actuarial pricing systems.

The rest of this paper is organized as follows. Setion 2 presents a novel communication system framework of risk model, which promotes the actuarial model to achieve both more risk classification and less pricing error. Section 3 ascribes risk classifications to a refinement problem of risk decoding, which can be solved by refinement of risk output event. Section 4 shows that the mutual information between risk input and output determines the performance of the actuarial model, and deterministic or causal model is the optimal actuarial model. Section 5 proposes that risk big data might cause risk information distortion, and lossless data collection design can significantly improve the performance of the actuarial model. Conclusions section summarizes main conclusions of this research and discusses future research outlook.

2 Communication system framework of risk model

2.1 Traditional risk model

The traditional actuarial risk model is the currently popular experience rating model, which predicts future losses (net risk premium) based on the historical loss (claim) experience of the insured subject. The experience rating model can be abstracted into the schematic diagram as below.

Where, is the real world risk level(unknown hidden variable) and is the posterior estimated risk; and are the underwriting risk variables (rate factors) and risk event (e.g. accident loss record) of the insured subject. The core mathematical problem is to solve the conditional probability distribution of the risk level under the observed conditions of and :

The experience rating risk model implies a time-invariant assumption, that is, the future and historical remain unchanged. This obviously contradicts to our common sense, for instance, the risk of traffic accidents during rush hours is much higher than slack hours. It can be seen that traditional risk models cannot meet the requirements of precise pricing of big data.

2.2 Communication system framework of risk model

2.2.1 Time-varying risk assumption

In the real world, risk changes over time generally. Assuming that the risk in Fig. 1 is time variant, the risk model becomes as follows

Where, the original in Fig. 1 is replaced to , which represents the time-varying risk level, and is the corresponding estimated risk level. Mathematically, can be regarded as a function of time , or even a stochastic process .

2.2.2 Risk informationization

According to the Merriam-Webster Dictionary, risk is possibility of loss or injury. Following the definition of information measurement in Shannon Information Theory moser2012a , the information measurement of risk is the information (or uncertainty) measurement of loss or injury. Consequently, the actuarial problem in Fig. 2 becomes the information problem of the communication system in Fig. 3 as below.

Paragraph headings

Use paragraph headings as needed.

As illustrated in Fig. 3, the original actuarial estimation process(from to ) in Fig. 2 is transformed into the risk information transmission process(from to ) in Fig. 3. Where, originates from real-world risk source; With the risk encoder, the unknown risk is collected as the risk input by big data acquisition; generates risk event through the risk mapper; Relying on the risk decoder, the event can be decoded into risk estimate finally. Further, this risk system is decomposed into three simple input-output subsystems, namely risk encoder, risk mapper, and risk decoder.

2.3 Equivalence of actuarial problems: information problems

In the context of insurance big data, the actuarial model adds two new requirements. One is more risk classification, the other is higher pricing accuracy. If the set of various risk levels is represented as set , the first requirement of risk classification can be described as the following mathematical problem

Where, is the number of risk levels in the risk classification set . Element represents a certain risk level in set . The probability of pricing errors with risk level , can be defined as follows

| (1) |

Where, and are the real and estimated risk of respectively. Similarly, the second requirement for precise pricing can be described as the following mathematical problem

However, it seems that two mathematical problems and are paradoxical: In case of more risk classification, it means contains more uncertainty; In case of more risk classification precise pricing, it implies has less uncertainty. This paradox is consistent with the aggregation operation in experience rating: aggregation can reduce pricing errors but decay risk classification meanwhile.

Once the actuarial risk model is modeled as a risk communication system, the traditional actuarial problem can be transformed into one problem of information transmission from real-world risk to estimated risk . Thus, according to the mutual information theorem of information theory cover2006elements , the optimal risk modeling criterion is directly inferred to maximize the mutual information between real and estimated risk. According to the idea of information theory, the above two mathematical problems can be transformed into the following information expressions

Where, is the information entropy of , and is the mutual information between and . is equivalent to (more uncertainty means greater entropy information entropy), and is equivalent to (less uncertainty means greater mutual information). Thus, information theory eliminates the paradox caused by the two requirements and creates the achievability of the optimal actuarial model.

Further, according to Fig. 3, the whole risk information transmission system is composed of risk encoder, risk mapper, and risk decoder three subsystems. Consequently, the information problems of the whole risk communication system can be decomposed into the information problems of three subsystems. The following sections will discuss these information issues in detail.

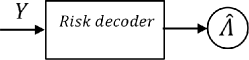

3 Refinement problem of risk decoding

3.1 Information entropy of risk decoding process

Next, focus on the risk decoder in Fig. 3, an input and output systems shown as below.

According to the lemma of mutual information transmission (i.e. Data processing inequality) moser2012a , the following inequality is obtained

| (2) |

Mathematically, inequality (2) reveals that, maximization of depends on the maximization of , which prerequisite is to maximize (i.e. the information entropy of risk event ). Therefore, increasing the information entropy of risk event is a necessary condition for achieving more risk classification.

3.2 Solution: refinement of risk event

Let be the set of risk event , and divide into mutually disjoint sets, , satisfying

| (3) |

Then is called a -refinement of risk event set . Apparently, it holds

| (4) |

Equation (4) shows that, it is mathematically feasible to refine risk event for more risk classifications.

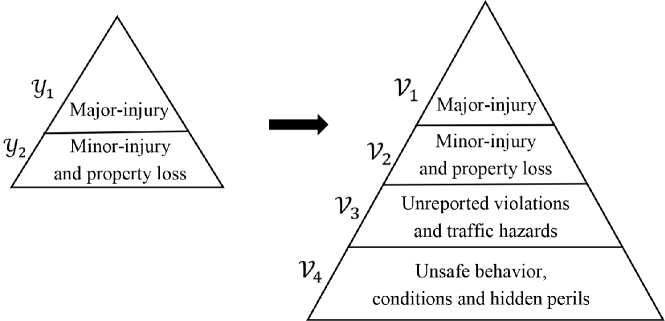

Fortunately, the Heinrich’s Safety Triangle(Heinrich’s Law) heinrich1959industrial also ensures that the refinement of risk event has strong operability. Taking car insurance as an example, autonomous driving big data can refine risk event as Fig. 5.

In Fig. 5, traditional car insurance can achieve a 2-refinement of risk event, (Major-injury) and (Minor-injury/property loss); With the aid of self-driving technology, insurance companies can achieve a 4-refinement of risk event, by appending (Unreported violations and traffic hazards) and (Unsafe behavior, conditions and hidden perils).

Significance

The essence of risk event refinement is to ensure that risk events () contain more risk information redundancy than estimated risks (), so as to improve the capacity of risk decoding.

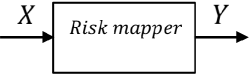

4 Capacity problem of risk mapping

4.1 Mutual information of risk mapping process

Just like inequality (2), there is also a data processing inequality as follow

| (5) |

Where, and are the risk input and output of risk mapper, and is the mutual information between and . describes the reliability (or shared information) that risk input variables () generate (mapping) risk events (). For a noisy (or erroneous) risk model, Risk Mapping Capacity is the maximum reliable mapping rate, which depends on the mutual information and information entropy (inequality (5) gives these bounds). Therefore, the design of a good risk model should relate to optimize and .

4.2 Solution: maximization of risk mapping capacity

According to Shannon’s Channel Coding Theorem cover2006elements moser2012a , the limit of the reliable risk mapping rate is the maximum mutual information (i.e. the ”common uncertainty” of and ). Thus, entropy and mutual information, can be used to determine the optimality of an actuarial system.

According to monotonicity and convexity of mutual information, is a convex function of for fixed (which means that the actuary cannot change the pricing variables except for the actuarial model ). It can be derived from its convexity as

| (6) |

Where is the supremum of . Equation (6) implies that when and are close to one-to-one mapping, mutual information tends to achieve the maximum value.

According to another property of mutual information, with equality holding iff is a function of . That is

| (7) |

Combining equation (6) and (7), it shows that deterministic risk generating model will cause

| (8) |

In causal inference theory, is called structural equation by pearl2018theoretical .

Taking rear-end collision risk as an example, according to the vehicle dynamic model in reference brill1972a , let

| (9) |

Where, and represent the initial speed and braking deceleration of the preceding vehicle 1, and are the initial speed and braking deceleration of the following vehicle 2, and and represent the time headway (gap) and reaction time of the following vehicle driver; is the risk event outcome variable. Here , , , , ,and belong to the risk input (), and belongs to the risk output ().

Under the condition that is known, whether a collision occurs can be judged directly based on the calculation result of (: no collision; : collision). Apparently the actuarial dynamics models similar to (9) can satisfy maximization of risk mapping capacity, because of their one-to-one mapping.

Significance

Maximization of actuarial model’s risk mapping capacity is to create deterministic or causal risk generating model.

5 Distortion problem of risk variables

5.1 Information entropy of big data risk variables

Finally look at the risk encoder in Fig. 3, an input and output system shown as below

As shown in Fig. 7, the role of the risk encoder is to sample real-world risks () as big data risk input variables (). Risk variables are usually continuous time variables, and are discrete time variables. According to the Nyquist-Shannon sampling theorem cover2006elements : Discrete sampling sequence may have information loss. Therefore, how to find the less-distortion and compact representation of real world risk information? This is the essential problem of risk encoder, which is directly related to the design of data collection on big data.

5.2 Constraints of risk big data design: multi-objective optimization

According to Shannon’s Source Coding Theorem cover2006elements moser2012a , insurance big data variables () should be designed with redundant information to carry the information entropy of real risk as lossless as possible. This can be expressed mathematically as

| (10) |

Where, is a strong constraint, and is a weak constraint, because is usually unknown.

In practice, the cost of big data collection is unavoidable. Therefore, (10) must consider the cost constraints, namely

| (11) |

Where, is the cost function of big data collection (), and is the upper bound of cost.

In addition, it is worth emphasizing that the big data design of () will directly affect the risk mapping capacity of the actuarial model (i.e. risk mapper). According to monotonicity and convexity of mutual information, is a concave function of for fixed (which means the actuarial model unchanged). It can be derived from its concavity as

| (12) |

Equation (12) implies the fact that, not all insurance big data can be modeled as an excellent actuarial pricing model, only the big data collection design optimized by mutual information can realize the best performance of the actuarial model.

Reference shinar2019crash presents an interesting and extreme example, assuming that driving risk (safety) model does not consider human factors such as driver’s distraction, and only depends on the frequencies of wearing shoes observation variables in accident samples, it is easy to conclude: “Wearing shoes is the inevitable cause of the crash, because almost all drivers were wearing shoes when crashes occurred.” If the probability of driver wearing shoes is 99.999%, substituting the probability into (12), there is

| (13) |

According to ’s concavity, it can be directly inferred that the risk variable of wearing shoes is a very poor risk characteristic variable, so it is impossible to model it as a good actuarial model.

6 Conclusions

The traditional actuarial model is prone to cause ecological paradox and Simpson’s paradox due to their correlation statistical assumptions, which were reported in Reference davis2004possible , a research on traffic big data. In this paper, the big data risk model is tackled as a risk information input-output system. This novel modeling framework can apply well-developed information theory to simultaneously achieve more risk classifications and less pricing errors.

The most important contribution of this work is to provide a new perspective of big data actuarial modeling, which enables actuaries to use more sophisticated mathematical tools such as information theory and system dynamics for risk modeling. In particular, specific approaches for optimizing the performance of big data actuarial models are proposed, including big data collection design, risk event refinement, and even causal (deterministic) modelling.

The work in this paper could have the potential to be widely used in insurance big data risk modeling, especially self-driving car insurance, cyber insurance.

References

- (1) Keith Ambachtsheer, Beyond portfolio theory: The next frontier, Financial Analysts Journal 61 (2005), no. 1, 29–33.

- (2) Aurelio Fernandez Bariviera, Luciano Zunino, M. Belen Guercio, Lisana B. Martinez, and Osvaldo A. Rosso, Efficiency and credit ratings: a permutation-information-theory analysis, Research Papers in Economics (2015).

- (3) A.R. Barron and T.M. Cover, A bound on the financial value of information, IEEE Transactions on Information Theory 34 (1988), no. 5, 1097–1100.

- (4) Edward A. Brill, A car-following model relating reaction times and temporal headways to accident frequency, Transportation Science 6 (1972), no. 4, 343–353.

- (5) Thomas M. Cover and Joy A. Thomas, Elements of information theory (wiley series in telecommunications and signal processing), 2006.

- (6) Gary A. Davis, Possible aggregation biases in road safety research and a mechanism approach to accident modeling, Accident Analysis & Prevention 36 (2004), no. 6, 1119–1127.

- (7) H. W. Heinrich, Industrial accident prevention: a scientific approach, 1959.

- (8) Stefan M. Moser and Po-Ning Chen, A student’s guide to coding and information theory, 2012.

- (9) Judea Pearl, Theoretical impediments to machine learning with seven sparks from the causal revolution, Proceedings of the Eleventh ACM International Conference on Web Search and Data Mining, 2018, pp. 3–3.

- (10) Athanasios Sachlas and Takis Papaioannou, Residual and past entropy in actuarial science and survival models, Methodology and Computing in Applied Probability 16 (2014), no. 1, 79–99.

- (11) David Shinar, Crash causes, countermeasures, and safety policy implications, Accident Analysis & Prevention 125 (2019), 224–231.

- (12) Ilya Zheludev, Robert Smith, and Tomaso Aste, When can social media lead financial markets, Scientific Reports 4 (2015), no. 1, 4213–4213.