Multivariate, Heteroscedastic Empirical Bayes

via Nonparametric Maximum Likelihood

Abstract

Multivariate, heteroscedastic errors complicate statistical inference in many large-scale denoising problems. Empirical Bayes is attractive in such settings, but standard parametric approaches rest on assumptions about the form of the prior distribution which can be hard to justify and which introduce unnecessary tuning parameters. We extend the nonparametric maximum likelihood estimator (NPMLE) for Gaussian location mixture densities to allow for multivariate, heteroscedastic errors. NPMLEs estimate an arbitrary prior by solving an infinite-dimensional, convex optimization problem; we show that this convex optimization problem can be tractably approximated by a finite-dimensional version.

The empirical Bayes posterior means based on an NPMLE have low regret, meaning they closely target the oracle posterior means one would compute with the true prior in hand. We prove an oracle inequality implying that the empirical Bayes estimator performs at nearly the optimal level (up to logarithmic factors) for denoising without prior knowledge. We provide finite-sample bounds on the average Hellinger accuracy of an NPMLE for estimating the marginal densities of the observations. We also demonstrate the adaptive and nearly-optimal properties of NPMLEs for deconvolution. We apply our method to two denoising problems in astronomy, constructing a fully data-driven color-magnitude diagram of 1.4 million stars in the Milky Way and investigating the distribution of 19 chemical abundance ratios for 27 thousand stars in the red clump. We also apply our method to hierarchical linear models, illustrating the advantages of nonparametric shrinkage of regression coefficients on an education data set and on a microarray data set.

MSC 2010 subject classifications: 62C12, 62G05, 62P35.

Key words: Adaptive estimation, empirical Bayes, Gaussian mixture model, -modeling, heteroscedasticity, Kiefer-Wolfowitz estimator.

1 Introduction

Consider a -dimensional (), heteroscedastic normal observation model

| (1) |

where is a known sequence of positive-definite covariance matrices, and the underlying mean vectors are additionally assumed to be drawn from a common prior , where belongs to the collection of all probability measures on . In settings where is known, model (1) fully specifies a Bayesian model; this paper studies the common empirical Bayes setting where must be estimated. The main goal of the paper is to nonparametrically estimate and the sequence from the observed data .

By allowing for arbitrary prior distributions , model (1) captures a range of important structural assumptions on the underlying sequence . For instance, the clustering problem—where the terms of take on at most distinct values—corresponds to discrete ; sparse modeling—where most of the are zero—corresponds to . The model also accommodates more complex manifold-like structures (see e.g. Figure 1) as well as substantially more heterogeneous sequences (e.g. heavy tailed ). Rather than assume a particular form for the latent structure represented by , we apply the nonparametric maximum likelihood estimator (NPMLE), which searches over all possible forms of latent structure that a set of precise measurements could have, identifying the underlying structure that best explains the real, noisy observations. Through detailed theoretical analysis, simulations and real data analyses, we demonstrate that the NPMLE exhibits a remarkable ability to adapt to latent structure where it is present and back away when no structure is available.

Empirical Bayes methods for the normal sequence model (1) have been studied extensively in the univariate, homoscedastic setting where and (see, e.g., James and Stein, (1960); Efron and Morris, 1972a ; Efron and Morris, 1972b ; Efron and Morris, 1973a ; Efron and Morris, 1973b ; Morris, (1983); Jiang and Zhang, (2009); Efron, (2012, 2014) as well as Johnstone, (2019) for a manuscript on estimation in Gaussian sequence models). Numerous methods extend empirical Bayes to the univariate, heteroscedastic case (see Jiang et al.,, 2011; Xie et al.,, 2012; Tan,, 2016; Weinstein et al.,, 2018; Jiang,, 2020; Banerjee et al.,, 2023; Chen,, 2023; Ignatiadis and Sen,, 2023, and references therein). Relatively little attention has been given to the general case of the present paper.

1.1 Applications to denoising problems

In the multivariate, heteroscedastic setting, model (1) naturally arises in the analysis of astronomy data, where often a calibrated measurement error distribution comes attached to each observation, and typically these errors are heteroscedastic (Kelly,, 2012); also see e.g. Akritas and Bershady, (1996), Hogg et al., (2010), Anderson et al., (2018). The first part of model (1) indicates that the target sequence has, due to measurement error, been corrupted by additive, zero-mean Gaussian noise, i.e.

Interestingly, the ’s above, which typically differ across , are known in many applications where the measurement process is well-characterized. In many situations it is assumed that is itself random and independent of for all . Although each observation has a different error distribution, the observations are tied together by the assumption that the ’s are i.i.d. from some distribution , yielding model (1).

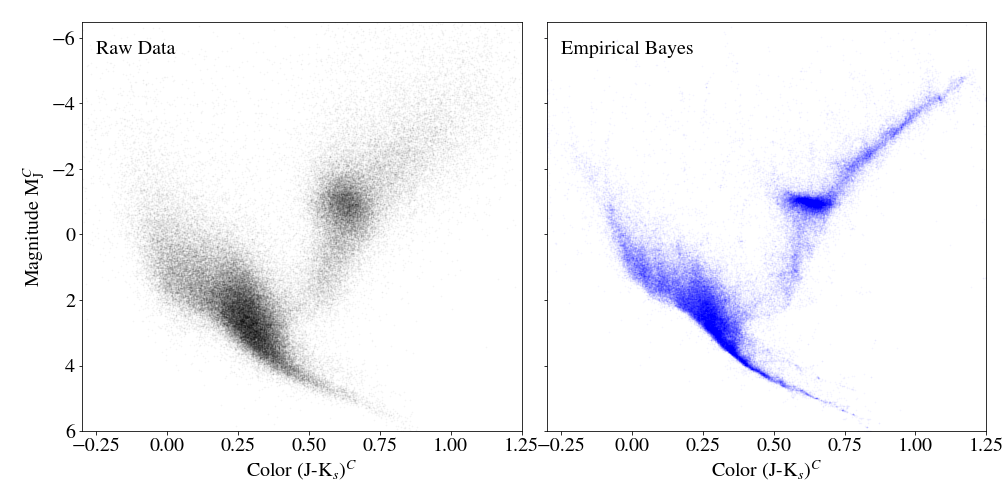

Our motivating example for model (1) involves the construction of a precise stellar color-magnitude diagram. A color-magnitude diagram (CMD) is a scatter plot of stars, displaying their absolute magnitude (a proxy for luminosity) versus color (a proxy for surface temperature) to provide a cross-sectional view of stellar evolution. The continued expansion of available stellar measurements has made purely statistical models such as model (1) increasingly attractive for denoising. One approach to estimating —which is known as Extreme Deconvolution (XD) (Bovy et al.,, 2011) and is especially popular in astronomy applications—assumes

| (2) |

and estimates the parameters via the Expectation-Maximization (EM) algorithm with split-and-merge operations designed to avoid local optima. For instance, Anderson et al., (2018) applied XD to build a low-noise CMD with million de-reddened stars from the Gaia TGAS catalogue. The XD assumption (2) that the prior is itself a mixture of -Gaussians has a number of drawbacks. Although the class of Gaussian location-scale mixtures is flexible for large , the choice of requires tuning; violations of assumption (2) for fixed induce bias in the estimation. To our knowledge, no theoretical results for the statistical properties of XD are available, making it difficult to quantify the misspecification error. Moreover, the class of all probability distributions of the form (2) is non-convex for finite , so even split-and-merge techniques employed within EM do not guarantee convergence to the global maximizer of the likelihood.

To avoid these difficulties, we extend the Kiefer and Wolfowitz, (1956) nonparametric maximum likelihood estimator (NPMLE) to incorporate multivariate and heteroscedastic errors. An NPMLE is any which maximizes the marginal likelihood of the observations . Marginally, the observations are independent, and the observation is distributed according to a Gaussian location mixture with density

| (3) |

where denotes the density of . Hence an NPMLE is any maximizer

| (4) |

In contrast to the parametric model used in XD, the nonparametric domain is convex, so solves a convex optimization problem, and tools from convex optimization may be leveraged to find principled approximations to (Koenker and Mizera,, 2014; Kim et al.,, 2020).

Given an estimate of the prior , empirical Bayes imitates the optimal Bayes analysis, known as the oracle (Efron,, 2019). If were known, optimal denoising of would be achieved through the posterior distribution . It is well known, for instance, that the oracle posterior mean

| (5) |

minimizes the squared error Bayes risk over all measurable . The NPMLE (4) yields a fully data-driven, empirical Bayes estimate of the oracle posterior mean via

| (6) |

Figure 1 shows the dimensional data set of Anderson et al., (2018), where each observation has a known error distribution and may be modeled as multivariate normal after a suitable transformation. The noise in the raw CMD of Figure 1 obscures many known features of stellar evolution, rendering the raw CMD unreliable for downstream parallax inference. The right panel of Figure 1 displays the empirical Bayes posterior means based on the NPMLE. The substantial shrinkage of our method reveals many recognizable features of the CMD, such as the red clump and a narrow red giant branch in the upper-right region of the plot, as well as the binary sequence tail distinct from the main sequence tail in the bottom-center region. The NPMLE and corresponding posterior means thus offer a powerful approach to shrinkage estimation under minimal assumptions. In Section 5.1, we continue our analysis of the Gaia TGAS data, and in Section 5.2, we present another astronomy application for denoising chemical abundance ratios of stars.

1.2 Applications to hierarchical linear modeling

Another common setting where the heteroscedastic covariances are known or can be accurately estimated is in hierarchical linear modeling. In this setting, we observe nested data with different groups, where the group contains units, and each unit has covariates and a scalar response . Consider the model

Writing and , we can write the model more compactly as

for . If for all , we can summarize each individual regression problem with the ordinary least squares (OLS) solution , which satisfies

where . Thus, the data follow the multivariate, heteroscedastic model (1), where the corresponding covariance matrices are typically known up to the scalar . If is not known, we can estimate it very accurately with

When is large, this will be a reliable estimate of the variance even if each is relatively close to . From here, we proceed as in Section 1.1, computing the NPMLE and performing shrinkage on the regression coefficients via the posterior mean

treating our estimate as the prior. A common assumption, for instance in meta-analysis (DerSimonian and Laird,, 1986), is that is itself a Gaussian , in which case the posterior mean shrinks all towards the prior mean . Our model of course allows for this possibility, but it also allows for much more complex structures , which perform nonlinear shrinkage and need not shrink all observations towards a single point. We apply the NPMLE to hierarchical linear models in two settings, an education data set (Section 5.3) and a microarray data set (Section 5.4).

1.3 Computational and statistical properties

The idea of using the NPMLE to estimate a prior distribution, due to Robbins, (1950), has seen a resurgence in recent years (Jiang and Zhang,, 2009, 2010; Koenker and Mizera,, 2014; Dicker and Zhao,, 2016; Gu and Koenker,, 2016; Koenker and Gu,, 2017; Feng and Dicker,, 2018; Kim et al.,, 2020; Efron,, 2019; Saha and Guntuboyina,, 2020; Jiang,, 2020; Polyanskiy and Wu,, 2020; Deb et al.,, 2022). These advancements, taken together, have begun to establish the NPMLE as a formidable approach to shrinkage estimation both in theory and in practice. All this prior work has focused on either the univariate setting or the homoscedastic setting , however. Our work extends the NPMLE to the practically important and more general setting of multivariate and heteroscedastic errors, uncovering a number of important differences.

Basic properties of the NPMLE that are well-understood in the univariate, homoscedastic setting (Lindsay,, 1995) have not received careful attention in more complex settings. We verify in Lemma 1 that a solution exists for every instance of the optimization problem (4), and we record the first-order optimality conditions characterizing the solution set. Similar to the univariate, homoscedastic setting, there exists a solution which is discrete with at most atoms, and the sequence of fitted values is unique, i.e. every solution has the same sequence of fitted likelihood values .

An important contribution of Lemma 1 is our reinterpretation of the characterizing system of inequalities in terms of a natural ‘dual’ mixture density . Specifically, is a heteroscedastic, -component mixture density—a convex combination of Gaussian bumps centered at the data points with weights inversely proportional to for —such that the support of every NPMLE is contained in the set of the global maximizers of . This observation has a number of important consequences that we explore in detail in Section 2; in particular, tools from algebraic statistics for studying the modes of Gaussian mixtures (Ray and Lindsay,, 2005; Améndola et al.,, 2020) translate directly into results on the support set. We leverage this connection to establish that is not necessarily unique when , even in the homoscedastic case. This finding is distinctive from the univariate, homoscedastic case where it is known that (4) has a unique solution for every problem instance (Lindsay and Roeder,, 1993). Our counterexample in Lemma 2 appears to be new and seems to invalidate prior claims of strict concavity of the log-likelihood (Marriott,, 2002; Koenker and Gu,, 2017). Whereas the fitted values are always unique, our counterexample also demonstrates that the empirical Bayes posterior means are not necessarily unique.

The problem of computing a solution is complicated by the presence of multivariate, heteroscedastic errors. The main difficulty in general is that the NPMLE solves an infinite-dimensional optimization problem. Since may be taken to be discrete with at most atoms, a solution can in principle be found with a finite mixture model. In particular, defining the set of discrete distributions with at most atoms,

maximum likelihood solutions over are also NPMLEs. Hence, the EM algorithm can be applied to optimize , as first observed by Laird, (1978), though EM over discrete distributions is prohibitively slow for moderately large and suffers from the same non-convexity issue as XD. Many algorithms (Böhning,, 1985; Lesperance and Kalbfleisch,, 1992; Wang,, 2007; Liu and Zhu,, 2007) have been proposed for finding approximate solutions to the optimization problem (4); Koenker and Mizera, (2014) identified a convex, finite-dimensional, highly scalable approximation. Instead of maximizing the log-likelihood of the data over all probability measures , the idea is to maximize the log-likelihood over , the collection of all probability measures supported on a finite set . If has elements, then is isometric to the dimensional simplex , and maximizing the likelihood corresponds to optimizing over the mixing proportions , which is a convex optimization problem. When , it is straightforward to see that is supported on the range of the data , so Koenker and Mizera, (2014) proposed taking to discretize this range. Jiang and Zhang, (2009, Proposition 5) bounded the discretization error in dimension, establishing that optimizing the weights via EM can lead to a good approximation once . Dicker and Zhao, (2016) further justified the discretization scheme in dimension by showing the discretized NPMLE is statistically indistinguishable from once the analyst uses at least atoms.

The discretization approach naturally extends to multivariate, heteroscedastic settings, but to our knowledge, no principled recommendations are available for choosing in general. Feng and Dicker, (2018) recommended taking to be a grid over a compact region containing the data. We address the key questions of how to choose this compact region and how the discretization error depends on the fineness of the grid. For choosing a compact region to discretize, a natural desideratum is that the region should contain the support of . To this end, in Proposition 4 we present compact support bounds on the NPMLE in terms of the data . When our support bounds reduce to the range of the data, reaffirming the original suggestion of Koenker and Mizera, (2014), and when but the errors are homoscedastic, it suffices to discretize the convex hull of . Interestingly, with multivariate and heteroscedastic errors, the support of the NPMLE can lie outside the convex hull of , so a different region known as the ridgeline manifold of is needed. Fortunately, this region is compact, and the NPMLE over agrees with the NPMLE over . This justifies the choice of as a cover of , and in Proposition 6, we verify that as , the log-likelihood of the discretized NPMLE approaches that of the NPMLE. We prove a quantitative bound on the gap for fixed , providing some guidance on how the discretization error depends on the fineness of the grid. In Section 4.1.1, we connect these computational guarantees to our statistical guarantees, showing that it suffices to discretize at a resolution in order to find an approximate solution that satisfies all of our statistical guarantees.

The standard gridding approach clearly suffers from the curse of dimensionality: if is a -cover of the ridgeline manifold , the number of points in typically scales like , so it is often difficult to compute the NPMLE over a fine grid even when . An alternative—the exemplar method proposed by Lashkari and Golland, (2008) (see also Böhning, (1999))—is to take the finite set to be all of the observations . In Section 3.2, we show some toy examples illustrating that the exemplar method can produce grossly suboptimal solutions, since the set is not a very fine cover of the ridgeline manifold . We propose an extension, called the exemplar+ method, to systematically sample additional points from the ridgeline manifold . We show through toy examples and simulation experiments that our proposal consistently produces approximate NPMLEs satisfying the assumptions of our theoretical guarantees, even in dimensions.

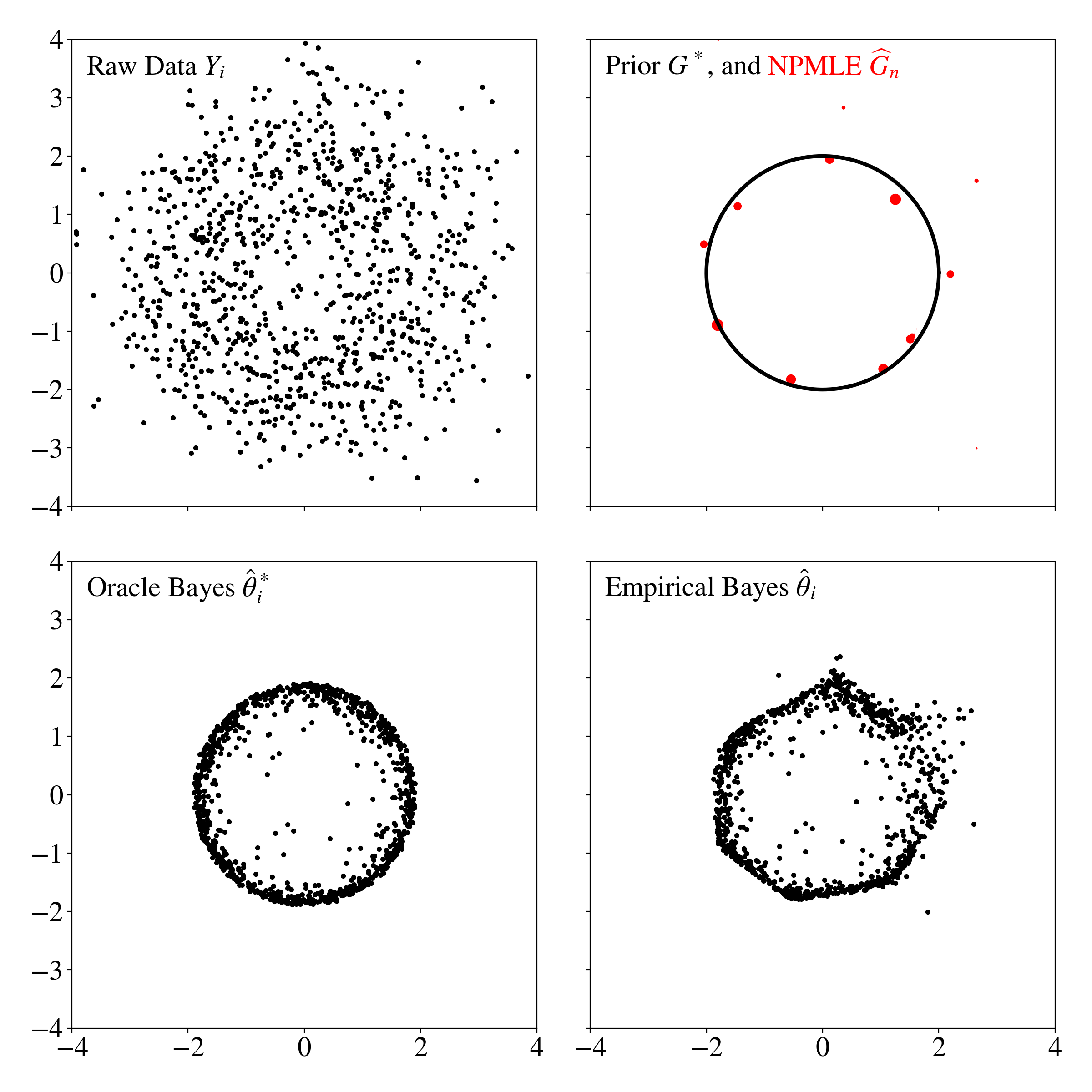

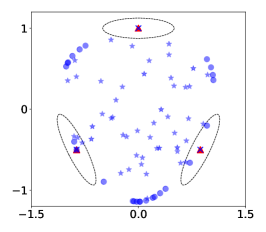

Our principled and efficient methods of computation facilitate simulation studies assessing the performance of the empirical Bayes estimate in a setting where we can actually compare to the oracle Bayes estimate . Figure 2 illustrates the method on simulated data. The means were drawn i.i.d. from a circle of radius two, and the data were drawn according to (1) using a variety of diagonal covariance matrices , taking each . Visually, it is clear that the empirical Bayes estimates improve upon the observations by shrinking towards the underlying circle; the corresponding mean squared errors were and , respectively. The oracle, which minimizes the mean squared error in expectation, attained an error of . While the oracle cannot be computed in practice because is unknown, this value sets a benchmark in simulations to which we may compare the performance of bona fide estimators. The empirical Bayes estimates not only track well with this benchmark; the individual estimates also track remarkably well with the oracle. In our simulation, the regret—defined as the mean squared error between the estimator and the oracle —was . Whereas is a function of the observed data, the oracle makes optimal use of the unknown prior , making the similarity between the two especially striking.

This striking similarity between and affirms the empirical Bayes adage that “large data sets of parallel situations carry within them their own Bayesian information” (Efron and Hastie,, 2016). However, the setting of Figure 2 is complicated by the fact the situations are not directly parallel, in that each observation has a distinct error distribution. Even in heteroscedastic settings, the extent to which we glean prior information for the purpose of denoising is captured by the empirical Bayes regret . Theorem 9 develops a detailed profile of the finite-sample regret properties of the NPMLE for denoising. We show that under certain tail conditions on the regret is bounded by a rate that is nearly parametric in , i.e. up to logarithmic multiplicative factors. The regret still converges at a slower, nonparametric rate under less structured conditions, where may have heavy tails. Furthermore, when possesses finer structure, such as the clustering problem where is a discrete measure with atoms, we prove that the regret is bounded from above by up to logarithmic multiplicative factors in . The clustering case is particularly remarkable, as the NPMLE is completely tuning-free, with no knowledge of , yet performs essentially as well as any estimator which knows the number of clusters . Thus, Theorem 9 demonstrates that the NPMLE effectively discovers structure when available and also effectively learns when structure is unavailable. Theorem 9 generalizes the regret bounds of Saha and Guntuboyina, (2020) and Jiang, (2020) who analyzed the homoscedastic setting and the univariate setting, respectively. These papers in turn built upon Jiang and Zhang, (2009) who studied the univariate, homoscedastic setting.

A key ingredient in the analysis of the regret is a more explicit representation of the estimator and oracle . The oracle posterior mean (5) has the following alternative expression, known as Tweedie’s formula (Dyson,, 1926; Robbins,, 1956; Efron,, 2011; Banerjee et al.,, 2023):

| (7) |

Similarly, our plug-in estimate can be written as

| (8) |

Tweedie’s formula clarifies that under model (1) the posterior means only depend on the prior via the marginal likelihood and its gradient. Jiang and Zhang, (2009) first leveraged this observation to relate the empirical Bayes regret to the problem of estimating the marginal density. In heteroscedastic problems, there are different marginal densities, , to estimate, and corresponding estimators . We show in Theorem 7 and Corollary 8 that the NPMLE achieves similar adaptive rates in the density estimation problem under an appropriate average Hellinger distance across all estimands .

Whereas most recent work has focused on properties of for density estimation and denoising, the NPMLE is potentially much more generally applicable as a plug-in estimate of the prior. To expand our understanding of its applicability, we present the first analysis of the deconvolution error for the NPMLE. Whereas density estimation captures the problem of describing the observations , deconvolution is the equally natural problem of interpreting the infinite-dimensional parameter . We study the accuracy of the NPMLE under a Wasserstein distance . The Wasserstein distance is particularly useful for this problem since and are typically mutually singular; in particular, may be absolutely continuous whereas is always discrete. The Wasserstein distance will be discussed in detail in Section 4. We show in Theorem 11 that attains the minimax rate of deconvolution, which happens to be a very slow, logarithmic rate . Inspired by the richness of the density estimation and denoising results, we hint at some of the adaptation properties of the NPMLE under the Wasserstein loss; Theorem 13 shows that when is a point mass distribution, the Wasserstein rate improves dramatically to up to logarithmic factors.

The rest of the paper is organized as follows: Section 2 systematically addresses basic properties of the NPMLE, including existence and non-uniqueness. Section 3 gives a full account of the approximate computation of NPMLEs. Section 4 establishes finite-sample risk bounds on the accuracy of as an estimator of for the purposes of density estimation, denoising and deconvolution. In Section 5, we apply the method to astronomy data to construct a fully data driven color-magnitude diagram of million stars and compare our method to extreme deconvolution where it has previously been applied (Anderson et al.,, 2018). We also apply the method to chemical abundance data for a smaller subset of stars that has previously been analyzed by Ratcliffe et al., (2020). We then present two applications using the hierarchical linear model, one on education data and the other on microarray data of leukemia patients. Section 6 concludes with some discussion of future work. The proofs and some simulation experiments are in the Supplementary Material. All figures and analyses in this manuscript can be reproduced using code at the following repository: https://github.com/jake-soloff/Multivariate-Heteroscedastic-NPMLE. An open source software package for computing approximate NPMLEs and empirical Bayes estimates in Python is available at: https://github.com/jake-soloff/npeb.

2 Structural properties

In this section, we establish some basic properties of solutions to the nonparametric maximum likelihood problem (4), including existence, non-uniqueness, invariance under certain transformations, and bounds on the support. These results provide a foundation both for computing (Section 3) and for understanding its statistical properties (Section 4). Our first result extends the well-known characterization of for univariate, homoscedastic errors (Lindsay,, 1995, Theorems 18-21) to our more general setting.

Lemma 1.

Problem (4) attains its maximum: there exists a discrete solution with at most atoms, and the vector of fitted likelihood values is unique. Moreover, solves (4) if and only if

The support of any is contained in the zero set ; the zero set is equal to the set of global maximizers of the -component, heteroscedastic dual mixture density

We prove Lemma 1, along with all results in this section, in Section B of the Supplementary Material. The first statement of the lemma guarantees the existence of a discrete solution, which we typically write as (here , and ), with providing an upper bound on the complexity of at least one solution. This implies that may be taken to be the maximum likelihood solution to a -component, heteroscedastic Gaussian mixture model where is selected in a data dependent manner. Since finite mixture models are nested by the number of components and , we may also say in general that is the maximum likelihood solution to an -component, heteroscedastic Gaussian mixture model.

The bound is tight: for each , there are sequences of observations and covariances such that the smallest number of components of any solution to (4) is precisely (see, e.g., Lindsay,, 1995, p. 116). However, in practice, the number of components is typically much smaller than . For instance, in the univariate, homoscedastic case, Polyanskiy and Wu, (2020) established a much stronger bound of under certain conditions on the prior distribution .

The last part of Lemma 1 states that the atoms of occur at the global maximizers of the -component Gaussian mixture , which has component distributions of the form for with weights inversely proportional to fitted likelihoods . Results on the modes of Gaussian mixtures (e.g. Ray and Lindsay,, 2005; Dytso et al.,, 2020; Améndola et al.,, 2020) thus provide information about the support of the NPMLE; in particular, our next two results exploit this connection to yield novel results on the NPMLE.

In the univariate and homoscedastic setting , it is additionally known that (4) has a unique solution for all observations (Lindsay and Roeder,, 1993). This means that, for every data set and every variance level , there is a unique probability measure such that for all , where is the unique vector of optimal likelihoods from Lemma 1. We observe, however, that uniqueness of the solution may not hold when , even with isotropic covariances .

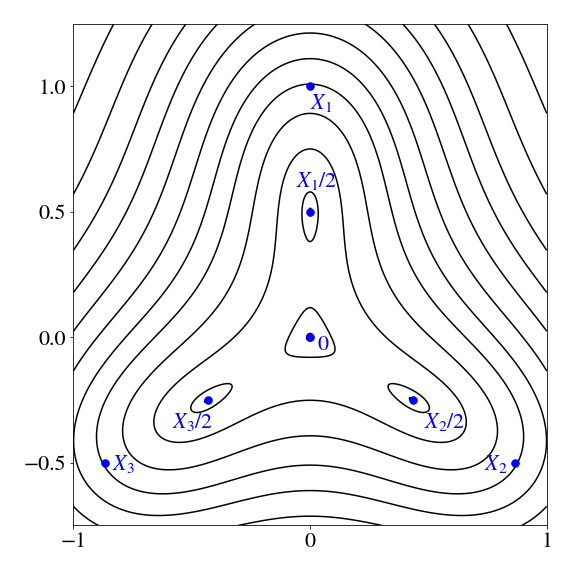

Lemma 2.

Let , and , , . Then (4) with data , covariances and has infinitely many solutions of the form

where .

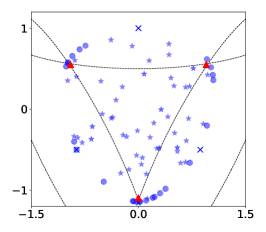

Figure 3 illustrates the counterexample given in Lemma 2. A key observation in the proof of Lemma 2 is that the dual mixture can be written explicitly as a homoscedastic mixture with uniform mixing distribution over the observations . This set-up closely follows a construction, due to Duistermaat (see Améndola et al.,, 2020), exhibiting an isotropic, homoscedastic Gaussian mixture with more modes than components. Duistermaat used the same component locations but took to obtain an example of a three-component mixture of isotropic, homoscedastic Gaussians such that the mixture has four modes. By specifically choosing , the height of the mixture is equal at all four modes, i.e. all four modes are global maximizers, and the modes are located at . By Lemma 1 any NPMLE must be supported on these modes. Representing the fitted values by a probability measure supported on the global modes is equivalent to finding a set of weights such that and solves the under-determined linear system , where is a matrix given by

Finally, we also note that although the fitted likelihoods are unique, the posterior means in this example differ for the solutions given in Lemma 2.

Although the NPMLE searches over all probability measures supported on , it is useful algorithmically to reduce the search space to probability measures supported on a compact subset of . By Lemma 1, to restrict the support of the NPMLE it suffices to bound the maximizers of the -component Gaussian mixture . Ray and Lindsay, (2005, Theorem 1) showed that all critical points of a Gaussian mixture can be constrained to a compact set known as the ridgeline manifold. We record this in the following lemma.

Lemma 3.

The support of every solution to (4) is contained in the ridgeline manifold , a compact subset of defined as

| (9) | ||||

For any there is an with at most nonzeros such that .

The ridgeline manifold constrains the support of the NPMLE to a compact subset. This set is much larger than the set of critical points in Lemma 1, but crucially its definition does not depend on the weights in the dual mixture . In the univariate case , the rigdeline manifold is simply the range of the data, so the univariate NPMLE is constrained to be supported on this range. In the multivariate setting, we may further simplify depending on certain shape restrictions on the covariance matrices.

Proposition 4.

Depending on the values of we further bound the support of as follows:

-

1.

(Homoscedastic) If for all , or if are proportional up to a sequence of positive scalars, the ridgeline manifold is the convex hull of the data .

-

2.

(Diagonal Covariances) If is a diagonal matrix for every , the ridgeline manifold is contained in the axis-aligned minimum bounding box of the data

where for all .

-

3.

(General Covariances) Let be chosen such that for all , where means is a symmetric positive semidefinite matrix. Choose and such that for all . Then the ridgeline manifold is contained in the ball

where .

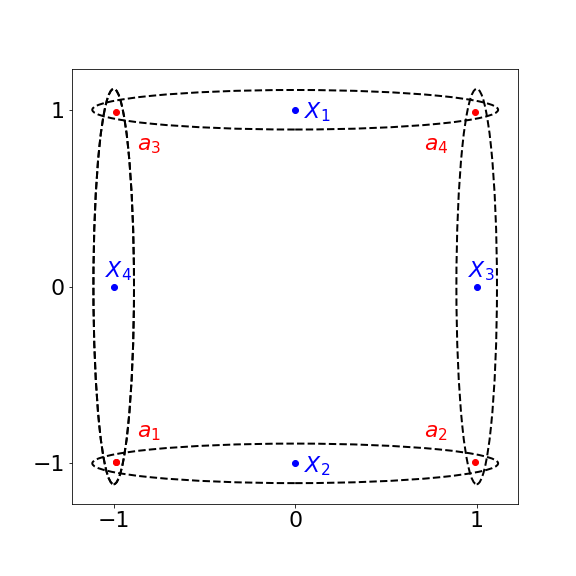

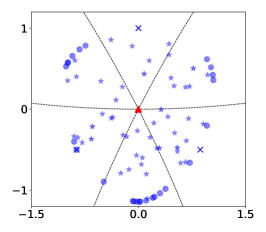

The first part of Proposition 4 in general gives the smallest possible convex body over which the support of can be constrained independently of . To see that the first part is tight, consider a fixed set of observations and isotropic covariance matrices ; as is made arbitrarily small, the support of approaches the set of observations (Lindsay,, 1995). Therefore, in general the convex hull is the smallest convex body containing the support in the homoscedastic setting and more generally the setting of proportional covariance matrices. By contrast, the convex hull of the data is in general too small to capture the support of in the heteroscedastic setting. Figure 4 presents one example with diagonal covariances where the support of is pushed towards the corners of the minimum axis-aligned bounding box of the data. Thus, the above discussion and Figure 4 indicate that both parts and of Proposition 4 give the tightest possible convex support bounds in their respective special cases.

We close this section with a brief discussion on how the NPMLE behaves under certain simple transformations of the data . Given a map , let denote the pushforward of given by , for any Borel set . In other words, if , then is the distribution of .

Lemma 5.

Fix a data set , a point and a orthogonal matrix . Consider the transformed data set where and for , with . Then

for all and all .

Lemma 5 is a straightforward consequence of the change of variables formula, but it has a number of useful corollaries. In particular, if is an NPMLE for the data set , then is an NPMLE for the modified data set , and the fitted likelihood values are the same, i.e.

for all . Thus, an NPMLE is equivariant under translations : if every observation is shifted by some fixed , then the modified NPMLE simply shifts every atom by . Similarly, the NPMLE is equivariant under orthogonal transformations, which explains why the fitted likelihood values are all equal in the rotationally symmetric toy data sets presented in Figure 3 and Figure 4.

3 Computation

The NPMLE solves a convex optimization problem (4) that is infinite-dimensional in the sense that the decision variable ranges over all probability measures on . Many numerical methods for approximately computing the NPMLE have been considered—including EM (Laird,, 1978), vertex direction and exchange methods (Böhning,, 1985), semi-infinite methods (Lesperance and Kalbfleisch,, 1992), constrained-Newton methods (Wang,, 2007), and hybrid methods (Liu and Zhu,, 2007; Böhning,, 2003)—typically described for the special case of univariate and homoscedastic errors. In this section, we discuss our strategy for computing the NPMLE as well as the challenges of scaling the computation to large data sets. To make our implementation accessible to the research community, we have developed a Python package npeb with code to fit NPMLEs in a variety of empirical Bayes problems.

We follow the approach of Koenker and Mizera, (2014), who approximated the infinite-dimensional problem by constraining the support of to a large finite set. For a non-empty, closed set , define a support-constrained NPMLE as any solution

| (10) |

where denotes the set of probability measures supported on a subset of . In particular, by definition, and by Proposition 4 we may write for a compact subset defined explicitly in terms of the data.

3.1 Computational guarantees for discretization

We now describe one strategy for choosing the discretization set . Fix . Let denote a covering of by closed hypercubes of width , i.e.

for some set of points such that . To construct the covering , we may take to be a grid of points spaced apart along each coordinate. Now define the discretized support to be the set of corners of hypercubes in ; specifically, for each hypercube in , the point for every . Because is compact, is a finite set which we denote by . Constraining the NPMLE to this finite set of atoms yields a finite-dimensional convex optimization problem over the mixing proportions. That is, the solution to (10) can be written as , where

| (11) |

and encodes an kernel matrix. The EM algorithm (Dempster et al.,, 1977) can be used to optimize directly over the mixing proportions . While this approach was advocated by Lashkari and Golland, (2008) and Jiang and Zhang, (2009), EM can be prohibitively slow (Redner and Walker,, 1984; Koenker and Mizera,, 2014). A crucial observation made by Koenker and Mizera, (2014) is that (11) is a (finite-dimensional) convex optimization problem, enabling the use of a wide array of tools from modern convex optimization; they proposed solving the dual to (11) using an interior point solver, and Gu and Koenker, (2017) provided an R implementation to solve univariate problems. Kim et al., (2020) proposed sequential quadratic programming to solve a variant of the primal problem directly, demonstrating superior scalability with the sample size .

To justify the grid approximation, some consideration of the discretization error is warranted. Our next result shows that as , the log-likelihood of the discretized NPMLE approaches that of the unconstrained, exact NPMLE; moreover, the bound on the gap depends on known quantities, so it can be used to guide a suitable choice of .

Proposition 6.

Let denote any compact set such that every solution (4) is supported on . Suppose the diameter of the set is at most , the minimum eigenvalue of each is at least , and fix . Let denote a cover of by closed hypercubes of width , and let denote the set of corners of hypercubes in . Every approximate NPMLE satisfies

| (12) |

We prove Proposition 6 in Section B of the Supplementary Material. Proposition 6 shows that we can tractably approximate the NPMLE via a finite-dimensional, convex optimization problem. As we show in Section 4, our theoretical results on the statistical properties of the NPMLE hold for any approximate solution which places nearly as high likelihood on the observations as the true prior . Proposition 6 can be used to guarantee this, since (12) yields a bound on without needing to know . Hence for sufficiently small we can guarantee that the discretization error is negligible.

Dicker and Zhao, (2016) showed in the univariate, homoscedastic case that a finely discretized NPMLE is statistically indistinguishable from the NPMLE for the purpose of density estimation. However, their analysis of the discretization error makes use of the modeling assumptions (1) and is statistical in nature, so their theoretical results provide little guidance on how much error is incurred due to discretization for a fixed data set. Our result aligns more closely with and in fact essentially generalizes Jiang and Zhang, (2009, Proposition 5), which bounded the optimality gap for a particular algorithm, discretization scheme and fixed data set. The main difference between our result and Jiang and Zhang, (2009, Proposition 5) is that the latter analyzed the EM algorithm for the mixing proportions (11), whereas by using a black-box, second-order optimization method to solve for the mixing proportions , we can solve for the discretized NPMLE much more accurately.

3.2 Exemplar+ method for moderate dimensions

The gridding discretization method does not scale well to moderate dimensions. In the approximation guarantee in Proposition 6, the number of hypercubes of width typically scales like . An alternative—known as the exemplar NPMLE—is to select the data points as the atoms (Böhning,, 1999; Lashkari and Golland,, 2008). The exemplar NPMLE is the support constrained NPMLE using the data as the atoms.

One issue with the exemplar approach is that, in general, the observations need not be close to the atoms of the NPMLE. For example, consider the heteroscedastic problem shown in Figure 4. Since all of the covariance matrices are diagonal, we know from Proposition 4 that the support of the NPMLE is contained in the axis-aligned minimum bounding box of the data. In this case, the atoms of the NPMLE are near the corners of the box, far from the observations. More generally, it is helpful to view the exemplar NPMLE of Lashkari and Golland, (2008) as selecting atoms in the ridgeline manifold with a special structure. Specifically, the exemplar method selects , , where is a standard basis vector.

We introduce a new strategy for selecting atoms , called the exemplar+ NPMLE, which aims to get a more representative sampling of points in the ridgeline manifold . By Proposition 4, all possible atoms for can be generated by vectors of the form where is a probability vector that is -sparse. The original exemplar method considers only that are -sparse. We propose to randomly sample, for each , weight vectors that are -sparse. See Algorithm 1 for a precise description of our proposal.

Algorithm 1 is motivated by the observation that different sparsity levels for will give better approximations to the support of the NPMLE depending on the scale of the covariance matrices . Figure 5 illustrates this point. When the covariances are sufficiently small (relative to the distance between observations), the support of the NPMLE will be nearly the observations: this is where the original exemplar method will be most accurate. However, as the scales of the covariance matrices grow, the atoms of the NPMLE occur at where .

The toy examples in Figure 5 suggest that we should not set any of the ’s equal to . We propose to set the counts equal to and . This ensures both that the exemplar+ always produces a higher likelihood than the original exemplar method, and that the computational cost is not much higher since we only require twice the number of atoms, regardless of the dimension .

As we shall see in Section 4, for our statistical guarantees, the main condition on an approximate NPMLE is that its likelihood is larger than the likelihood of the true prior. In Appendix A of the Supplementary Material, we show in simulations that exemplar+ consistently satisfies this requirement across a variety of choices of . In fact, the gap between the two likelihoods grows considerably in moderate dimensions (in our experiment we tested up to ). This suggests that the exemplar+ method is especially well-suited for applications in moderate to high dimensions.

4 Statistical properties

The NPMLE applies as a plug-in estimator of the prior distribution for many purposes. The traditional statistical setting is density estimation, where working in a Gaussian mixture model greatly simplifies the problem of estimating the marginal density of each observation . In particular, is a natural, tuning-free estimate of the true marginal density . Another problem setting—at the heart of empirical Bayes methodology—is to imitate the Bayesian inference we would conduct if we knew . Denoising, using as plug-in estimators of the true posterior means , represents the most basic instantiation. Finally, often we wish to compare to the prior directly. Since we are estimating the prior given observations from a convolution model , deconvolution refers to the problem of estimating .

In this section, we establish that the NPMLE is well-suited for all three disparate targets of estimation: the marginal densities , the oracle posterior means and the prior . We allow for the possibility that is any approximate NPMLE, with the exact conditions being given in each theorem; hence, potential non-uniqueness (established in Lemma 2) is not an issue in practice. Throughout this section, we use the standard notation to mean for some positive constant depending only on problem parameters .

4.1 Density estimation: average Hellinger accuracy

As the distribution of varies with , we consider the density estimation quality of the NPMLE (4) in terms of the average squared Hellinger distance, i.e. for ,

where denotes the usual squared Hellinger distance between a pair of densities . In the homoscedastic case where , our proposed loss function agrees with the usual squared Hellinger distance. Our first result bounds the average squared Hellinger accuracy of the NPMLE. In order to accommodate general heteroscedastic , we state our results in terms of uniform upper and lower bounds on the spectra of all of the matrices, i.e. for all . To state the result, some additional notation is needed. We fix a positive scalar and a non-empty compact set . Define the rate function controlling the squared Hellinger distance

| (13) |

where denotes the -moment of under , and denotes the -enlargement of the set . Note that we have suppressed the dependence of on the upper bound .

The following result states that bounds the rate in average Hellinger accuracy both with high probability and in expectation. The scalar and compact set are free parameters. Note that the first term on the right-hand side of (13) is increasing in and , whereas the second is decreasing in each. In principle, then, we may tune the values of and to optimize the rate function . Later in this section, we discuss a number of special cases where a more explicit rate can be obtained.

Theorem 7.

Suppose where for all . Any (approximate) solution of (4) such that

| (14) |

satisfies

| (15) |

for all , provided . Moreover,

| (16) |

We prove Theorem 7 in Section C of the Supplementary Material. Our proof extends Theorem 2.1 of Saha and Guntuboyina, (2020) on the multivariate, homoscedastic case and Theorem 4 of Jiang, (2020) on the univariate, heteroscedastic case , which in turn build upon Theorem 1 of Zhang, (2009) on the univariate, homoscedastic case. The general theory on rates of convergence for maximum likelihood estimators (Wong and Shen,, 1995; van de Geer,, 2000) can in principle be used to bound . Our proof technique deviates from the general theory by directly bounding the likelihood for outside some pre-specified domain (controlled by the choice of set ), and then covering the set of densities within the domain in the metric.

Theorem 7 provides a sharp bound in many special cases of . For a given we need to optimize over the choices of and the nonempty compact set to obtain the smallest value of the rate function . Our next result performs this calculation for various assumptions on the prior .

Corollary 8.

Suppose where for all . Suppose is any approximate NPMLE such that

| (17) |

Let denote the -dimensional closed ball of radius centered at .

-

1.

(Discrete support) If , then

-

2.

(Compact support) If has compact support , then

-

3.

(Simultaneous moment control) Suppose that there is a compact and , such that for all (recall as above). Then

-

4.

(Finite moment) Suppose that there is a compact and such that . Then

Given the general result in Theorem 7, Corollary 8 follows directly from the calculations of Saha and Guntuboyina, (2020) in Corollary 2.2 and Theorem 2.3. Corollary 8 captures an important adaptation property of the NPMLE. The cases described in the result are nested in the sense that implies , implies , and implies ; consequently the rates get progressively worse as our assumptions weaken. This means that the NPMLE, despite searching over all probability measures , obtains better rates when structure is present in the prior .

Most strikingly, when has discrete support with support points, the rate in is up to logarithmic factors without assuming any knowledge of . This rate matches the minimax rate over all discrete distributions with at most support points (Saha and Guntuboyina,, 2020), meaning we could not expect to do much better even if were known. In the extreme case where , the observations actually come from a simple Gaussian, i.e. with common mean , so our result says we don’t lose much in the rate when we model the density with a mixture even when it turns out to be a simple Gaussian. Similarly, in , the rate adapts to the size of the support without prior knowledge of this support or even a bound on its size. Up through simultaneous moment control , the dimension only affects the rate as a function of through the logarithmic factor. Hence, the NPMLE avoids the usual curse of dimensionality to some extent, while still achieving consistency in the heavier tailed setting . The logarithmic factors in our bounds might be reduced slightly but cannot be eliminated as they are present in the minimax lower bounds (Kim and Guntuboyina,, 2022).

4.1.1 Implications for the Discretization Rate

Theorem 7 establishes that up to a multiplicative constant (depending only on the dimension and bounds on the eigenvalues of the covariance matrices) the quantity controls the average Hellinger accuracy of the NPMLE. This also holds for approximate solutions to the optimization problem (4) that, in accordance with (14), place nearly as much likelihood on the data as does the true prior . It is natural to compare the requirement (14) with our computational guarantee on the discretization error (12) from Proposition 6. The free parameter which controls the discretization error is the resolution , which represents the width of the hypercubes we use to cover the ridgeline manifold or any of its outer-approximations from Proposition 4. Thus, in order to satisfy the main requirement of Theorem 7, we need to take such that

Observe from the definition of that for all and all compact . Absorbing additional terms depending on ,, and and assuming for simplicity that , choosing such that

| (18) |

suffices for the discretized NPMLE to be statistically indistinguishable from a global maximizer.

The inequality (18) gives a preliminary bound on the rate at which the discretization level should decrease with . Still, recall from Proposition 6 that denotes the diameter of the ridgeline manifold , so does depend on . To sketch the dependence, let us consider a representative example where has sub-Gaussian tails and all of the ’s are diagonal. In this case, by Proposition 4 part , the ridgeline manifold is contained in the axis-aligned minimum bounding box of the data

Due to the tail condition, the length of each side of this hyper-rectangle grows like with high probability up to multiplicative factors depending on : hence, the diameter also scales like with high probability up to multiplicative factors depending on and . We have thus shown that it suffices to discretize at a resolution of . The number of points in our covering is of order . In the univariate case , this slightly improves the finding of Theorem 2 of Dicker and Zhao, (2016), who showed that an -discretization of the range of the data suffices for the same rate in Hellinger distance. Their bound on the large-deviation probability is also logarithmic, i.e. whereas our equation (15) is polynomial in . Our analysis also clarifies that the sense in which we need approximate NPMLE (14) is through the likelihood of the observations, relative to the true prior , which could be useful for comparing alternative approaches to approximating the NPMLE using simulations where we know .

4.2 Denoising: an oracle inequality

In this section we turn to the problem of estimating the oracle posterior means ; see (5). We evaluate the performance of (see (6)) as an estimator for using the mean squared error risk measure:

Since is the optimal estimator of given model (1), the above mean squared error quantifies the price of misspecifying with the data-driven estimator . Hence, this loss is also known as the per-instance empirical Bayes regret.

Our next result states that the rate function governing the Hellinger accuracy (see (13)) also upper bounds the regret, up to additional logarithmic factors. We provide the same special cases of the rate as those stated in Corollary 8.

Theorem 9.

Suppose where for all . Let denote any approximate NPMLE satisfying (17) and

| (19) |

Fix some and a nonempty, compact set . Define as in (13). For all ,

| (20) |

In particular, consider the following special cases for :

-

1.

(Discrete support) If , then

-

2.

(Compact support) If has compact support , then

-

3.

(Simultaneous moment control) Suppose that there is a compact and , such that for all . Then

-

4.

(Finite moment) Suppose that there exists a compact and such that . Then

Theorem 9 shows that the denoising problem shares the adaptation features as the density estimation problem. Since we have assumed for all , the same set of results also hold for the scaled regret

Compared with the Hellinger accuracy results in the previous section, the denoising guarantees in Theorem 9 have an additional condition (19) that the approximate NPMLE places higher likelihood on the data than the slightly perturbed priors . This condition is used to ensure that the likelihood of each individual observation is not too small. This condition can be directly verified for any approximate NPMLE, and in particular it necessarily holds for any discretized NPMLE such that the observations are a subset of the atoms , as is the case with the exemplar+ method (as long as ) in Section 3.2.

Remark 10.

(On the proof of Theorem 9 in Section D of the Supplementary Material) Our proof extends Theorem 3.1 of Saha and Guntuboyina, (2020) on the multivariate, homoscedastic case and Theorem 1 of Jiang, (2020) on the univariate, heteroscedastic case , which in turn build upon Theorem 5 of Jiang and Zhang, (2009) on the univariate, homoscedastic case. Jiang and Zhang, (2009) and Jiang, (2020) used a related notion of regret

Tweedie’s formula relates the oracle (7) and empirical Bayes (8) posterior means to the corresponding marginal likelihoods, so the density estimation results of the previous section turn out to be useful for proving Theorem 9 as well. In particular, we consider Bayes rules for priors in a covering of the Hellinger ball

which, by Theorem 7, contains with high probability. For a fixed prior , the denominator in the correction factor of Tweedie’s formula

namely , can be small. To avoid dividing by near-zero quantities, we regularize the above Bayes rule by replacing the denominator with for a small positive . To handle heteroscedastic errors, we show that Tweedie’s formula, even its regularized form, is equivariant under scale transformations.

4.3 Deconvolution: estimating the prior

We turn to the fundamental question of how well estimates . This is known as the deconvolution problem and has received much attention in the statistical literature (Meister,, 2009; Fan,, 1991; Zhang,, 1990; Carroll and Hall,, 1988). Indeed, the original consistency results (Kiefer and Wolfowitz,, 1956; Pfanzagl,, 1988) for the NPMLE focused on weak convergence of to as . While most prior work on deconvolution has focused on deconvolution with homoscedastic error distributions, Delaigle and Meister, (2008) (also see Staudenmayer et al.,, 2008) allowed for heteroscedastic errors but relied on kernel estimators which contain additional smoothing parameters. By contrast, the NPMLE provides a tuning-free estimate of the mixing distribution , yet to our knowledge, non-asymptotic bounds on the rate of convergence for in the deconvolution problem are not known.

In practice, the true prior may not be discrete even though always has a discrete solution, and even if both distributions are discrete, their supports will typically differ. Our loss function must allow for comparisons of probability measures with potentially disjoint supports. Nguyen, (2013) established that a natural loss for this problem is the Wasserstein distance from the theory of optimal transport

where are two probability measures and denotes the set of couplings of and , i.e. joint distributions over such that and . Indeed, even the likelihood criterion is intimately related to the Wasserstein distance: in the homoscedastic case , it is known that the NPMLE (4) equivalently solves an entropic-regularized optimal transport problem (Rigollet and Weed,, 2018).

Nguyen, (2013) connected the deconvolution error to the density estimation error between the mixtures, i.e. in a homoscedastic Gaussian deconvolution setting. By leveraging similar techniques as well as the support bounds of Proposition 4, we arrive at the following upper bound on the deconvolution error.

Theorem 11.

Suppose where and is a diagonal matrix for each . Suppose further that for some . Let denote any approximate NPMLE supported on the minimum axis-aligned bounding box of the data satisfying (17). Then there is a function such that, for all sample sizes with ,

with probability at least .

Theorem 11 (proved in Section E of the Supplementary Material) upper bounds the rate of convergence under the Wasserstein distance by the extremely slow logarithmic rate . It is well known that the smoothness of the Gaussian errors makes the deconvolution more difficult; in fact, the logarithmic rate is minimax optimal (Dedecker and Michel,, 2013).

Remark 12.

(On Theorem 11) To our knowledge, Theorem 11 is novel, and the rate of convergence for the NPMLE under a Wasserstein distance has not been studied previously. The structure of the proof follows the proof of Theorem 2 of Nguyen, (2013). To deal with the fact that and are typically singular, we convolve each with a distribution with full support but low variance. Compared to our results on the density estimation and denoising problems, Theorem 11 makes additional assumptions on the problem structure, specifically that the covariance matrices are diagonal and that is compactly supported. Many practical applications satisfy the diagonal covariances restriction, including both of our applications in Section 5.

A common feature to our results on density estimation and denoising have been that the NPMLE adapts to the complexity of . It is reasonable to conjecture, then, that in the deconvolution problem, will also enjoy some adaptation properties under the Wasserstein distance. We close this section with a sharper result on the Wasserstein rate in the special case where the observations are drawn from Gaussian distributions with common mean .

Theorem 13.

Suppose , i.e. where and for all . Let denote any approximate NPMLE satisfying (17) and supported on where , , and . Then

with probability at least for all .

If the approximate NPMLE of Theorem 13 is selected according to the strategy described in Section 3, then by Proposition 4 part its support will be contained within the ball . This additional assumption on the support of the approximate NPMLE is needed to have some control over the moments of .

Up to logarithmic factors, the -rate in Theorem 13 agrees with Corollary 4.1 of Ho and Nguyen, (2016) for the MLE of an overfitted mixture. Specifically, their result compared the MLE of -component finite Gaussian mixture to a true mixing distribution with components. Wu and Yang, (2020) and Doss et al., (2020) also derived the -rate for a different estimator under a different Wasserstein metric. All of these previous results were restricted to the homoscedastic setting. In our setting, and is the data-dependent order of the NPMLE. The best known bound on is logarithmic in (Polyanskiy and Wu,, 2020), whereas Ho and Nguyen, (2016) required to be fixed as . When is known, a faster -rate is possible (Heinrich and Kahn,, 2018) and is achieved by the MLE in a well-specified finite mixture model, i.e. setting (Ho and Nguyen,, 2016).

While the slower -rate appears to be the price of flexibility of the NPMLE, Theorem 13 establishes that the NPMLE indeed adapts to structure in . Our analysis is greatly simplified by the assumption , since there is only one coupling between and . We leave for future work the important question of the extent to which adapts to more general distributions .

5 Applications

In this section, we first expand upon our discussion of denoising the color-magnitude diagram (CMD) from Section 1, and then present three additional applications. The second application illustrates the performance of our method on an astronomy problem with dimensions; the remaining two applications use hierarchical linear regression on education and biomedical data.

5.1 Color-magnitude diagram

Our modeling strategy is closely related to the work of Anderson et al., (2018). To compare our method to extreme deconvolution (Bovy et al.,, 2011), we use the same stellar sample, relaxing only their assumption that the prior is a mixture of Gaussians; by contrast, we allow to be an arbitrary probability measure. Specifically, we assume that after a suitable transformation of the color and magnitude measurements, the pair, denoted , come from a two-dimensional Gaussian mixture with known covariance .

Figure 1 in Section 1 shows the plot of the observed data (left) and estimated posterior means (right), the latter constituting the denoised CMD. Contrasting our CMD with theirs (Anderson et al.,, 2018, Figure 7), which we do not depict here, it appears that ours performs more shrinkage overall. Our CMD has rather sharp tails in the bottom of the plot (i.e. the main sequence) and the top right (i.e. the tip of the red-giant branch) as well as a definitive cluster in the center-right (i.e. the red clump).

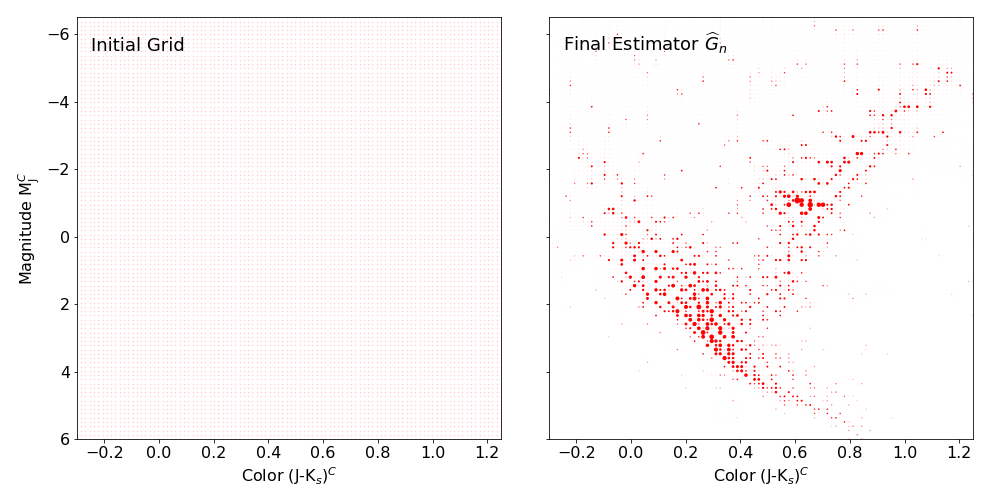

There are also important differences between the NPMLE and extreme deconvolution in the estimated prior . Figure 6 shows the initial and final iterates in the computation of the NPMLE. We are ultimately using a discrete distribution to model the prior, and since all of the covariance matrices are diagonal, by Proposition 4 we have restricted the support points to lie in the minimum axis-aligned bounding box of the data. By contrast, extreme deconvolution models the prior as itself a Gaussian mixture, so the estimated prior (Anderson et al.,, 2018, Figure 4) actually is supported on all of .

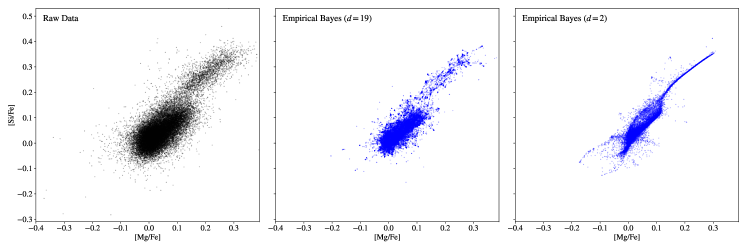

5.2 Chemical abundance ratios

Our second data set is taken from the Apache Point Observatory Galactic Evolution Experiment survey (APOGEE); see Majewski et al., (2017), Abolfathi et al., (2018). We examine chemical abundance ratios for the red clump (RC) stars given in the DR14 APOGEE red clump catalog; see Ratcliffe et al., (2020) where this data set has been studied. Following the pre-processing in Ratcliffe et al., (2020) to remove the outliers with anomalous abundance measurements, the data set contains observations of relative chemical abundances.

We restrict our attention to two abundances among the dimensions, namely, [Si/Fe]-[Mg/Fe]. To explore the dependence of our estimator on the dimensionality of the data, we consider two distinct empirical Bayes analyses. The first fits the NPMLE on all dimensions, estimating the posterior mean and then plotting only the components of our estimates corresponding to the two abundances of interest [Si/Fe]-[Mg/Fe]. The second analysis discards the other coordinates and then computes the -dimensional NPMLE on those same abundances.

In Figure 7 we plot the observed data (left) and estimated posterior means using Gaussian denoising under the estimated prior . The estimates based on the full dimensional data set are in the center panel, and the estimates based on only the dimensions are on the right. In two dimensions, the denoised data reveals a very interesting structure — it shows that the variables [Si/Fe] and [Mg/Fe] are strongly correlated. The observations for the upper right cluster of stars could be lying on one dimensional manifold; something that is not at all visible when plotting the original data. On the other hand, the NPMLE based on the full dimensional data set performs much less aggressive shrinkage. We believe that the dimension-dependent logarithmic factor in the Definition (13) of plays a nontrivial role in this relatively small data set. For example, setting and , the log factor is approximately , i.e., much smaller than ; on the other hand, changing to in the same formula gives a logarithmic factor of over billion. The dimension-dependent logarithmic factor is not simply an artifact of our analysis: Kim and Guntuboyina, (2022) prove a minimax lower bound for Hellinger accuracy which contains a similar, dimension dependent logarithmic factor.

5.3 Math scores in U.S. public schools

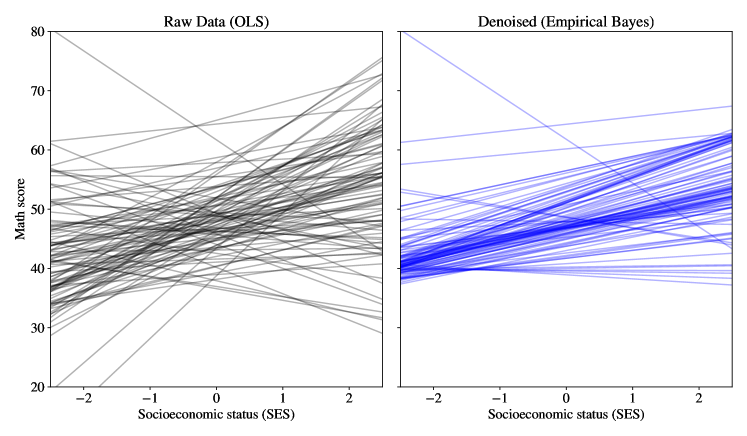

Our third data set comes from the Education Longitudinal Study of 2002, collected by the National Center for Education Statistics of the U.S. Department of Education. We apply our approach to hierarchical linear models described in Section 1.2 and compare to a Bayesian analysis of Hoff, (2009). Specifically, we look at a survey including math test scores and normalized socioeconomic status (SES) of 10th grade students. The survey has information across different large public high schools on a total of children. We consider a dimensional hierarchical regression setting where the response represents the math score of student in school , and contains the corresponding SES score and an intercept term. The number of students surveyed in each school varies significantly, ranging from to with a median of students. The goal is to estimate separate regression coefficients for each school , but if we simply compute OLS separately for each school, then the estimates for schools with small will be especially poor.

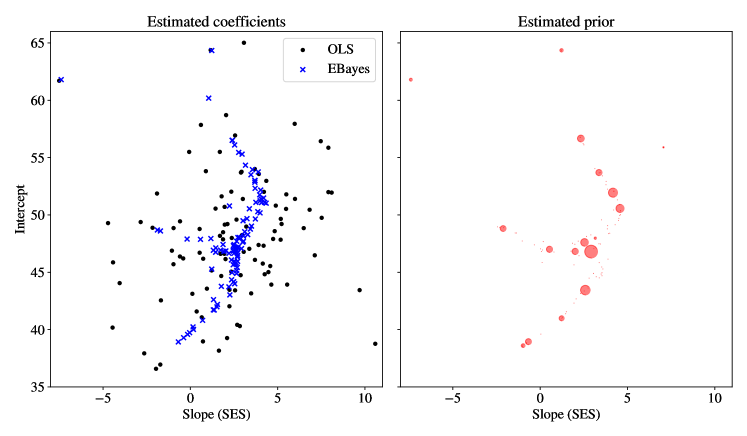

In Figure 8, we compare the empirical Bayes regression lines to the OLS estimates. We see that the empirical Bayes method shrinks the bulk of slopes quite aggressively, but they are not shrunk towards a single point. The standard fully Bayesian analysis (which can be seen in Figure 11.3 of Hoff,, 2009) models the prior as a normal distribution, placing further priors on its parameters. An important difference is that all of the regression coefficients are shrunk towards a single point under a normal prior. By contrast, for our method, the multiple locations to shrink towards and their relative weights are determined by the NPMLE , as depicted in the bottom right panel of Figure 8.

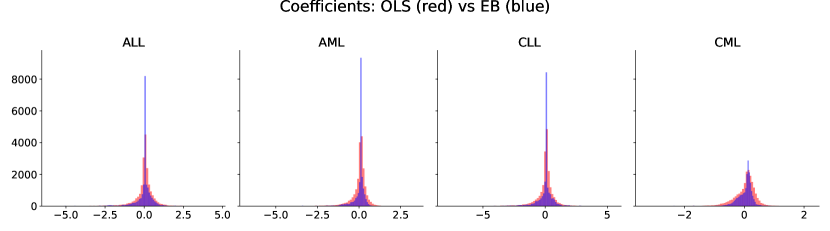

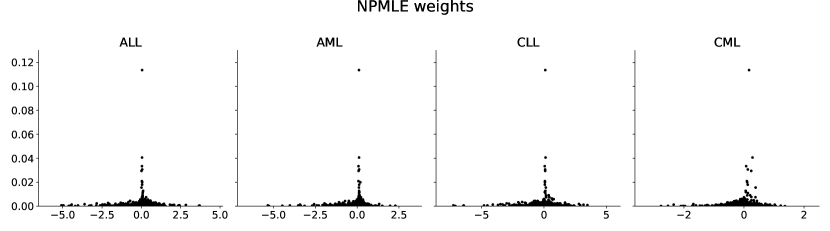

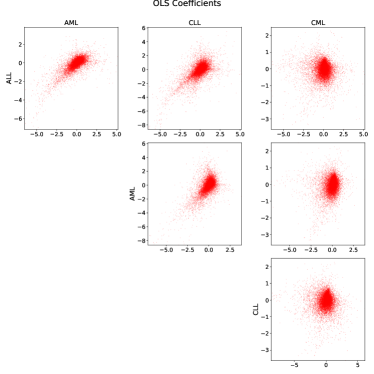

Below: The left panel contains the same information as above, but directly plotting the values of and rather than the regression lines. The right panel contains the discrete NPMLE , where the area of each dot is proportional to the corresponding weight.

(a) Histogram of coefficients estimated with OLS (red) and empirical Bayes (blue).

(b) The NPMLE weights.

(c) Pairwise scatterplots of coefficient estimates for OLS (red) and empirical Bayes (blue).

5.4 Microarray data

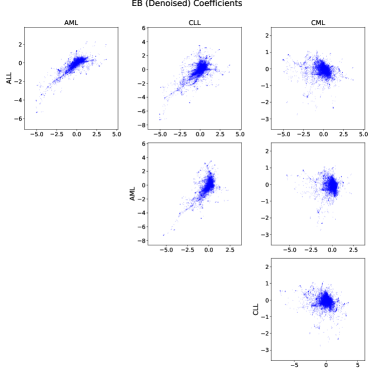

Our fourth data set (Aibar et al.,, 2023) is a subset of the Microarray Innovations in Leukemia (MILE) study (Kohlmann et al.,, 2008; Haferlach et al.,, 2010). The data contains bone marrow samples of patients with one of four types of leukemia (abbreviated ALL, AML, CLL, CML) as well as non-leukemia patients. We are interested in estimating the contrast of the difference in expression levels for each leukemia type compared to the non-leukemia baseline. We observe genes and samples per gene. We use a one-hot encoding for each type as well as an intercept term, so : specifically, for each patient and each leukemia type , set if patient has that cancer type, and otherwise. We model the expression of gene in patient as

where . For each cancer TYPE, represents the effect of that cancer type on the expression level of gene , relative to the non-leukemia baseline. In the hierarchical linear model, we treat the -dimensional vectors of regression coefficients as i.i.d. from some prior . As in Section 1.2, we first compute the OLS estimates separately for each gene . Next, we compute the pooled estimate of the observation variance . Finally, we compute the exemplar+ NPMLE and the estimated posterior means .

In Figure 9, we compare the empirical Bayes estimates to the OLS estimates. From both the marginal histograms in 9(a) and the plots of the weights in 9(b), it is clear that the NPMLE promotes sparsity by shrinking coefficients towards the spikes near zero. Three of the four types have a spike very close to zero, whereas the fourth type (CML) places its spike on small but positive effects. In genomics applications where we are interested in multiple effects, we can consider multiple kinds of sparsity. The first kind is a strong form of sparsity, where for most . For the second, for most and most types, but for any given gene , need not imply for some other type . The NPMLE permits both forms of sparsity, so we do not need to know a priori which form is more appropriate.

6 Concluding remarks

In this paper we study the NPMLE as an estimator of a prior distribution in the presence of multivariate, heteroscedastic measurement errors. We resolve a number of basic questions on the existence, uniqueness, and support of the NPMLE, where in several cases the answers differ significantly from the traditional univariate, homoscedastic setting. Our analysis identifies a dual mixture density with Gaussian components at each observation, whose modes contain the atoms of the NPMLE. Our characterization implies that the NPMLE is supported in the ridgeline manifold , which is a compact subset of defined in terms of the observations and corresponding covariance matrices . This support reduction allows us to approximate the NPMLE by a finite-dimensional convex optimization over the mixing proportions, and we develop a novel approach to bounding the discretization error, justifying the gridding scheme proposed by Koenker and Mizera, (2014). Our real data applications show that this approach is viable for practical astronomy problems. Our theoretical results in Section 4 provide strong justification for using the NPMLE in a variety of contexts—estimating the prior, marginal densities, and oracle posterior means.

We conclude by outlining some possible future research directions. Computation remains an important barrier for large-scale applications. Specifically, for problems with a large number of samples, e.g. , some additional forms of approximation are warranted, such as stochastic optimization or binning via coresets (see also Ritchie and Murray, (2019) on approaches for scaling Extreme Deconvolution to large data sets). Another open problem is to come up with more principled approach to the exemplar+ method, specifically for choosing the counts and for sampling the weights ’s.

Next, while our framework allows the prior to be arbitrary, the underlying assumption—that the means are identically distributed—can sometimes be difficult to justify for heteroscedastic observations. The i.i.d. assumption reflects the belief that the observation covariance is uninformative for the corresponding mean . This assumption led to reasonable results in our applications but may be problematic in other settings. In the univariate, heteroscedastic case, Weinstein et al., (2018) proposed grouping observations with similar variances and applying a spherically symmetric estimator separately within each group. Their approach is capable of capturing dependence between and , at the expense of not sharing information across groups. Moving beyond binning the variances , Chen, (2023) models the conditional distribution as a flexible location-scale family. To our knowledge, these approaches have not been extended to multivariate settings. Thus, in multivariate settings there remains the important problem of how to model the relationship between and .

Finally, there remain a number of open statistical questions for future work. Our analysis of the denoising problem focuses on estimating the posterior mean based on the unknown prior , but there are numerous inferential goals one could target with an approximate prior. The analyst might summarize the empirical posteriors using a different functional, such as the posterior median or the posterior mean of some transformed parameter. This question warrants a more general analysis evaluating the quality of the empirical posterior distributions for the true, unknown posteriors.

Acknowledgements

We thank Bridget L. Ratcliffe for providing both astronomy data sets and Nikos Ignatiadis for suggesting the microarray data set. J.A.S. would like to thank Jacob Steinhardt and Serena Wang for their valuable feedback on an early draft. We are grateful to Kevin Chen for correcting a step in the proof of Theorem 9, to Yihong Wu for correcting the statement of Proposition 4.

Funding

J.A.S. was supported by NSF Grant DMS-2023505 and by the Office of Naval Research under the Vannevar Bush Fellowship program under grant number N00014-21-1-2941. A.G. was supported by NSF CAREER Grant DMS-16-54589. B.S. was supported by NSF Grant DMS-2015376.

Appendix A Additional experiments

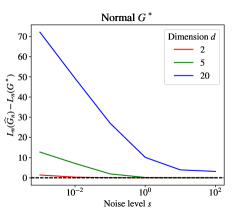

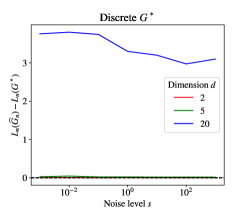

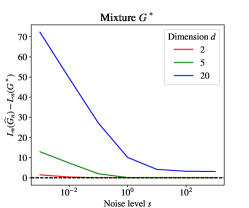

We ran a series of simulation experiments to assess the plausibility of Assumption (14) of Theorem 7, which requires the likelihood of the approximate NPMLE to be nearly as large as the likelihood . We compute the exemplar+ NPMLE for simulated homoscedastic data sets, where the covariances are for all . In Figure 10, we plot the difference as a function of the noise level , for various choices of and dimensions . The gap was positive across all experimental conditions: in fact, the gap between the two likelihoods grows considerably in high dimensions. We thus believe that the exemplar+ NPMLE is suitable for our applications.

Appendix B Proofs of Results in Sections 2 and 3

B.1 Proof of Lemma 1

The following uses similar techniques to those of Lindsay, (1995, Section 5.2), which contains a subset of our result in the homoscedastic case.

Proof of Lemma 1.

By convexity, the first-order optimality condition for is

where

When is a point mass we write instead of . It suffices to check for all because .

For the first part of the Lemma, define . Observe that

Since is continuous and , the set is closed, and by boundedness of the Gaussian likelihood, is compact. Hence is convex and compact, and is strictly concave and coordinate-wise monotone over . Thus, attains its maximum at a unique (non-zero) boundary point . Observe : by Carathéodory’s theorem, any boundary point can be written as for some .

Suppose is contained in the support of the NPMLE. Given , define a new probability measure via . Since for , the mixture

remains a valid probability measure for . Since maximizes the log-likelihood of over a range including both negative and positive values, the derivative of the log-likelihood is zero at , i.e.

so for all such that . This implies for all measurable , from which we may conclude . Finally, observe that

so is equivalent to . This proves the last statement of the Lemma, that is equal to the set of global maximizers of . ∎

B.2 Proof of Lemma 2

Proof of Lemma 2.

By Lemma 5, the fitted values are equal. By Lemma 1, the atoms of occur at the global modes of , where . Since , the fitted values are also equal to the global maximum of , i.e.

for each . Note that for all , so is an NPMLE. Now let . It suffices to check the fitted values of at the observations. For ,

Similarly, for ,

and, for ,

This verifies that is also an NPMLE, so every convex combination is an NPMLE. ∎

B.3 Proof of Lemma 3

Proof of Lemma 3.

The fact that follows Ray and Lindsay, (2005, Theorem 1). Observe that is compact as it is the continuous image of the simplex, a compact set.

For the last claim, let , and let . Note implies :

By Carathéodory’s theorem, there is some with at most nonzeros such that . Rearranging, we find that . ∎

B.4 Proof of Proposition 4

Proof of Proposition 4.

In the proportional covariances case , we have

As ranges over the simplex, so does . Thus , proving (i). If each is diagonal, letting denote the coordinate of ,

proving (ii). For (iii), using concavity of the minimum eigenvalue,

so . ∎

B.5 Proof of Lemma 5

Proof of Lemma 5.

By the change of variables formula,

completing the proof. ∎

B.6 Proof of Proposition 6

Proof of Proposition 6.

Write , and for each , let such that . Next, define a positive measure supported on the corners of such that and

| (21) |

where . Now fix and , and let and . By the moment identity (21) and by Jiang and Zhang, (2009, A.27),

Let . Summing the above inequality over ,

Since is supported on , by optimality of ,

Combining our findings,

Using the elementary inequality for , we obtain

for . ∎

Appendix C Proof of Theorem 7

The following notation will be used throughout this section:

-

1.

denotes a closed ball in .

-

2.

For a positive integer , let .

-

3.

Given a pseudo-metric space and , let denote the -covering number, i.e. the smallest positive integer such that there exist such that

Any such a set is known as an -net or -cover of under the pseudo-metric . When is a subset of Euclidean space we write instead of .

-

4.

We use the shorthand , the matrices being viewed as fixed. Let

-

5.

For and , let denote the -enlargement .

-

6.

Define the semi-norm

Similarly, define

Our proof generalizes and builds upon prior techniques for analyzing the Hellinger accuracy of the NPMLE (Zhang,, 2009; Saha and Guntuboyina,, 2020; Jiang,, 2020). The basic structure of our argument is to recognize, given the approximation (14) in the likelihood, that we may trivially rewrite the large deviation probability for the NPMLE as a joint probability

If were a fixed probability measure such that , the right-hand side of the last display similarly simplifies as

Since is not fixed, we first approximate it using a covering argument, and then bound the right-hand side of the previous display using Markov’s inequality.

Proof of Theorem 7.

Suppose for some the NPMLE satisfies

We bound the probability

for .

Take to be an -net of under . For each , let be a distribution satisfying

and . By construction of the -net, there is such that

On the event , the NPMLE acts as a witness that , so by the triangle inequality

| (22) |

This gives

Defining , we have

| (23) |

on the event . Hence

| (24) | ||||

| (25) | ||||

| (26) |

By a union bound and Markov’s inequality, the first term (25) is bounded by

| (27) |

Writing out the expectation,

Putting together the pieces, the first term (25) is bounded by

| (28) | ||||

For the second term (26), observe by Markov’s inequality

To reduce clutter write and . The above expectation is further upper bounded by

The last inequality follows from Lemma 15. Note we need

to ensure . Taking , we have , so

Noting , choose , so . We directly apply Saha and Guntuboyina, (2020, Suppl. Lemma A.7) for the integral

To bound the metric entropy, i.e. where denotes the size of our -net , we apply Lemma 18

where the scalar in the above display corresponds to used in the lemma. Assuming ,

Similarly , so

Combining our findings,

for any . Absorbing the dependence on and into constants, take such that

If we then take ,

This proves (15). To prove (16), integrate the tail from (15),

for , completing the proof. ∎

We now state and prove the lemmas needed in the proof of Theorem 7.

Lemma 15.

Let and independently, and , where . Then

for any , where is the -moment of under .

Proof.

Lemma 16.

(Moment matching, part i) Let . Suppose is such that

for some , and that

for some . Then

Proof.

For each , write

On , , so

Write the pdf as where is a polynomial of degree and the remainder satisfies

By hypothesis, , so

completing the proof. ∎

Lemma 17.

(Moment matching, part ii) For any , there is a discrete distribution supported on with at most

atoms such that

Proof.

The idea is to choose to match moments, and then apply the previous lemma. The proof is identical to Saha and Guntuboyina, (2020, Suppl. Lemma D.3), except that we take . ∎

Lemma 18.

There exists positive constants and depending on alone such that for every compact set , and we have

| (30) |

Proof.