On Characterizing the Trade-off in

Invariant Representation Learning

Abstract

Many applications of representation learning, such as privacy preservation, algorithmic fairness, and domain adaptation, desire explicit control over semantic information being discarded. This goal is formulated as satisfying two objectives: maximizing utility for predicting a target attribute while simultaneously being invariant (independent) to a known semantic attribute. Solutions to invariant representation learning (IRepL) problems lead to a trade-off between utility and invariance when they are competing. While existing works study bounds on this trade-off, two questions remain outstanding: 1) What is the exact trade-off between utility and invariance? and 2) What are the encoders (mapping the data to a representation) that achieve the trade-off, and how can we estimate it from training data? This paper addresses these questions for IRepLs in reproducing kernel Hilbert spaces (RKHS)s. Under the assumption that the distribution of a low-dimensional projection of high-dimensional data is approximately normal, we derive a closed-form solution for the global optima of the underlying optimization problem for encoders in RKHSs. This yields closed formulae for a near-optimal trade-off, corresponding optimal representation dimensionality, and the corresponding encoder(s). We also numerically quantify the trade-off on representative problems and compare them to those achieved by baseline IRepL algorithms. Code is available at https://github.com/human-analysis/tradeoff-invariant-representation-learning.

1 Introduction

Real-world applications of representation learning often have to contend with objectives beyond predictive performance. These include cost functions corresponding to invariance (e.g., to photometric or geometric variations), semantic independence (e.g., to age or race for face recognition systems), privacy (e.g., mitigating leakage of sensitive information (Roy & Boddeti, 2019)), algorithmic fairness (e.g., demographic parity (Madras et al., 2018)), and generalization across multiple domains (Ganin et al., 2016), to name a few.

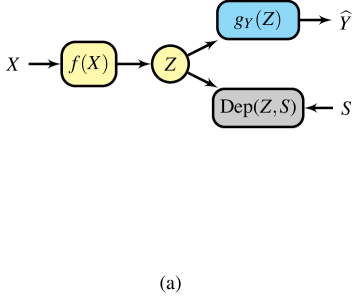

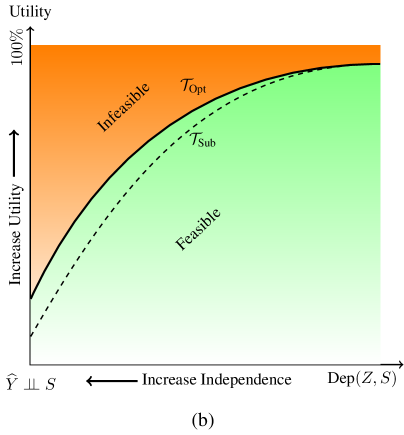

At its core, the goal of the aforementioned formulations of representation learning is to satisfy two competing objectives: Extracting as much information necessary to predict a target label (e.g., face identity) while intentionally and permanently suppressing information about a given semantic attribute (e.g., age or gender). See Figure 1 (a) for illustration. Let be the encoding of the input data from which the target attribute can be predicted. When the statistical dependency between and is not negligible, learning a representation that is invariant to the semantic attribute (i.e., ) will necessarily degrade the performance of the target prediction, i.e., there exists a trade-off between utility and invariance.

The existence of a trade-off has been well established, both theoretically and empirically, under various contexts of representation learning such as fairness (Menon & Williamson, 2018; Zhao & Gordon, 2019; Gouic et al., 2020; Zhao, 2021), invariance (Zhao et al., 2020), and domain adaptation (Zhao et al., 2019b). However, much of this body of work only establishes bounds on the trade-off rather than a precise characterization. As such, two aspects of the trade-off in invariant representation learning (IRepL) are unknown, including i) exact characterization of the trade-off inherent to IRepL and ii) a learning algorithm that achieves the trade-off. Under the assumption that the distribution of a low-dimensional projection of high-dimensional data is approximately normal, this paper studies and establishes the aforementioned properties by constraining function classes to reproducing kernel Hilbert spaces (RKHS)s.

Ideally, the utility-invariance trade-off is defined as a bi-objective optimization problem:

| (1) |

where is the encoder that extracts the representation from , predicts from the representation , and are the corresponding hypothesis classes, and is the loss function for predicting the target attribute . The function is a parametric or non-parametric measure of statistical dependence, i.e., implies and are independent, and implies and are dependent with larger values indicating greater degrees of dependence. The scalar is a user-defined parameter that controls the trade-off between the two objectives, with being the standard scenario that has no invariance constraints with respect to (w.r.t.) . In contrast, enforces (i.e., total invariance). Involving all Borel functions in and ensures that the best possible trade-off is included within the feasible solution space. For example, when and is MSE loss, the optimal Bayes estimator, is attainable.

In this paper, we consider the linear combination of utility and invariance in (1) and define the optimal utility-invariance trade-off (denoted by ) as a single objective optimization problem:

Definition 1.

| (2) |

where controls the trade-off between utility and invariance. For example, corresponds to ignoring the invariance and only optimizing the utility, while corresponds to .

The motivations behind considering this single-objective IRepL are (i) any solution to this simplified problem is a solution to the bi-objective problem in (1), (ii) even (2) is challenging to solve, and (iii) existing works have not thoroughly investigated (2). An illustration of the utility-invariance trade-off is illustrated in Figure 1 (b). In this paper, we restrict to be some RKHSs and to be a simplified version of the Hilbert-Schmidt Independence Criterion (HSIC) (Gretton et al., 2005a). Further, we replace the target loss function in (2) by as presented and justified in Sections 3.2 and 5.2.

Summary of Contributions: i) We design a dependence measure that accounts for all modes of dependence between and 111By “all modes of dependence” we mean all types of linear and non-linear relations, in contrast to only linear or monotonic relations. (under a mild assumption) while allowing for analytical tractability. ii) We employ functions in RKHSs and obtain closed-form solutions for the IRepL optimization problem. Consequently, we precisely characterize a near-optimal approximation of via encoders restricted to RKHSs. iii) We obtain a closed-form estimator for the encoder that achieves a near-optimal trade-off and establish its numerical convergence. iv) Using random Fourier features (RFF) (Rahimi et al., 2007), we provide a scalable version (in terms of both memory and computation) of our IRepL algorithm. v) We numerically quantify our (denoted by K-) on an illustrative problem as well as large-scale real-world datasets, Folktables (Ding et al., 2021) and CelebA (Liu et al., 2015), where we compare K- to those obtained by existing works.

2 Related Work

2.1 Invariant Representation Learning

The basic idea of representation learning that discards unwanted semantic information has been explored under many contexts like invariant, fair, or privacy-preserving learning. In domain adaptation (Ganin & Lempitsky, 2015; Tzeng et al., 2017; Zhao et al., 2018), the goal is to learn features that are independent of the data domain. In fair learning (Dwork et al., 2012; Ruggieri, 2014; Feldman et al., 2015; Calmon et al., 2017; Zemel et al., 2013; Edwards & Storkey, 2015; Beutel et al., 2017; Xie et al., 2017; Zhang et al., 2018; Song et al., 2019; Madras et al., 2018; Bertran et al., 2019; Creager et al., 2019; Locatello et al., 2019; Mary et al., 2019; Martinez et al., 2020; Sadeghi et al., 2019), the goal is to discard the demographic information that leads to unfair outcomes. Similarly, there is growing interest in mitigating unintended leakage of private information from representations (Hamm, 2017; Coavoux et al., 2018; Roy & Boddeti, 2019; Xiao et al., 2020; Dusmanu et al., 2021).

A vast majority of this body of work is empirical. They implicitly look for single or multiple points on the trade-off between utility and semantic information and do not explicitly seek to characterize the whole trade-off front. Overall, these approaches are not concerned with or aware of the inherent utility-invariance trade-off. In contrast, with the cost of restricting encoders to lie in some RKHSs, we precisely characterize the trade-off and propose a practical learning algorithm that achieves this trade-off.

2.2 Adversarial Representation Learning

Most practical approaches for learning fair, invariant, domain adaptive, or privacy-preserving representations discussed above are based on adversarial representation learning (ARL). ARL is typically formulated as

| (3) |

where is the loss function of a hypothetical adversary , who intends to extract the semantic attribute through the best estimator within the hypothesis class , and is the utility-invariance trade-off parameter. ARL is a special case of (2) where the negative loss of the adversary, plays the role of . However, this form of adversarial learning suffers from a critical drawback. The induced independence measure is not guaranteed to account for all modes of non-linear dependence between and if the adversary loss function is not bounded like MSE or cross-entropy (Adeli et al., 2021; Grari et al., 2020). In the case of MSE loss, even if the loss is maximized at a bounded value, where the corresponding representation is also bounded, it still does not guarantee that is attainable (see Appendix H for more details). This implies that designing the adversary loss in ARL to account for all types of dependence is challenging and can be infeasible for some loss functions.

2.3 Trade-Offs in Invariant Representation Learning:

Prior work has established the existence of trade-offs in IRepL, both empirically and theoretically. In the following, we categorize them based on properties of interest.

Restricted Class of Attributes: A majority of existing work considers IRepL trade-offs under restricted settings, e.g., binary and/or categorical attributes and . For instance, Zhao et al. (2019a) uses information-theoretic tools and characterizes the utility-fairness trade-off in terms of lower bounds when both and are binary labels. Later McNamara et al. (2019) provided both upper and lower bounds for binary labels. By leveraging Chernoff bound, Dutta et al. (2020) proposed a construction method to generate an ideal representation beyond the input data to achieve perfect fairness while maintaining the best performance on the target task. In the case of categorical features, a lower bound on utility-fairness trade-off has been provided by Zhao & Gordon (2019) for the total invariance scenario (i.e., ). In contrast to this body of work, our trade-off analysis applies to multi-dimensional continuous/discrete attributes. To our knowledge, the only prior results under a general setting are Sadeghi et al. (2019) and Zhao et al. (2020). However, in Zhao et al. (2020), both and are restricted to be continuous/discrete or binary simultaneously (e.g., it is not possible to have binary while is continuous).

Characterizing Exact versus Bounds on Trade-Off: To the best of our knowledge, all existing approaches except Sadeghi et al. (2019), which obtains the trade-off for the linear dependence only, characterize the trade-off in terms of upper and/or lower bounds. In contrast, we precisely characterize a near-optimal trade-off with closed-form expressions for encoders belonging to some RKHSs.

Optimal Encoder and Representation: Another property of practical interest is the optimal encoder that achieves the desired point on the utility-invariance trade-off and the corresponding representation(s). Existing works which only study bounds on the trade-off do not obtain the encoder that achieves those bounds. For example, Sadeghi et al. (2019) develop a learning algorithm that obtains a globally optimal encoder, but only under a linear dependence measure between and . HSIC, a universal measure of dependence, has been adopted by prior work (e.g., Quadrianto et al. (2019)) to quantify all types of dependencies between and . However, these methods adopt stochastic gradient descent for optimizing the underlying non-convex optimization problem. As such, they fail to provide guarantees that the representation learning problem converges to a global optimum. In contrast, we obtain a closed-form solution for the globally optimal encoder and its corresponding representation while detecting all modes of dependence between and .

2.4 Kernel Method

The technical machinery of our kernel method for representation learning is closely related to kernelized component analysis (Schölkopf et al., 1998). Kernel methods have been previously used for fair representation learning by Pérez-Suay et al. (2017) where the Rayleigh quotient is employed to only search for a single point in the utility-invariance trade-off. To find the entire trade-off, Sadeghi et al. (2019) used kernelized ARL with a linear adversary and target estimator. Kernel methods also have been used to measure all modes of dependence between two RVs, pioneered by Bach & Jordan (2002) in kernel canonical correlation (KCC). Building upon KCC, later, Gretton et al. (2005a; b; 2006) have introduced HSIC, constrained covariance (COCO), and maximum mean discrepancy (MMD), to name a few. Inspired by these works, a variation of HSIC is adopted as a measure of dependence in this paper.

3 Problem Setting

3.1 Notation

Scalars are denoted by regular lowercase letters, e.g., , . Deterministic vectors are denoted by boldface lowercase letters, e.g., , . We denote both scalar-valued and multidimensional random variables (RV)s by regular upper case letters, e.g., , . Deterministic matrices are denoted by boldface upper case letters, e.g., , . The entry at -th row, -th column of a matrix is denoted by or . or simply denotes an identity matrix; and denote -tuple vectors of ones and zeros, respectively. We denote the trace of a square matrix by . The pseudo-inverse of a matrix is denoted by . We denote finite or infinite sets by calligraphy letters, e.g., , .

3.2 Problem Setup

Consider the probability space , where is the sample space, is a algebra on , and is a probability measure on . We assume that the joint RV, containing the input data , the target label , and the semantic attribute , is a RV on with joint distribution . Furthermore, and can also belong to any finite set, such as a categorical set. This setting enables us to work with both classification and multidimensional regression tasks, where the semantic attribute can be either categorical or multidimensional continuous/discrete RV.

Assumption 1.

We assume that the encoder consists of functions from to in a universal RKHS (e.g., RBF Gaussian kernel), where universality ensures that can approximate any Borel function with arbitrary precision (Sriperumbudur et al., 2011).

Hence, the representation RV can be expressed as

| (4) |

where is the dimensionality of the representation. As we will discuss in Corollary 4.1, unlike common practice where is chosen on an ad-hoc basis, it is an object of interest for optimization. We consider a general scenario where both and can be continuous/discrete or categorical, or one of or is continuous/discrete while the other is categorical. To accomplish this, we replace the target loss, in (2) by the negative of a non-parametric measure of dependence, i.e., . The main reason for this replacement is that maximizing statistical dependency between the representation and the target attribute can flexibly learn a representation applicable to different downstream target tasks, including regression, classification, clustering, etc (Barshan et al., 2011). Particularly, Theorem 6 in Section 5.2 indicates that with an appropriate choice of involved RKHS for , we can learn a representation that lends itself to an estimator that performs as optimally as a Bayes estimator i.e., . Furthermore, in an unsupervised setting, where there is no target attribute , the target loss can be replaced by , which implicitly forces the representation to be as dependent on the input data . This scenario is of practical interest when a data producer aims to provide an invariant representation for an unknown downstream target task.

4 Choice of Dependence Measure

We only discuss since we adopt the same dependence measure for . Accounting for all possible non-linear relations between RVs is a key desideratum of dependence measures. A well-known example of such measures is mutual information (MI) (e.g., MINE (Belghazi et al., 2018)). However, calculating MI for continuous multidimensional representations is analytically challenging and computationally intractable. Kernel-based measures are an alternative solution with the attractive properties of being computationally feasible/efficient and analytically tractable (Gretton et al., 2005b).

Definition 2.

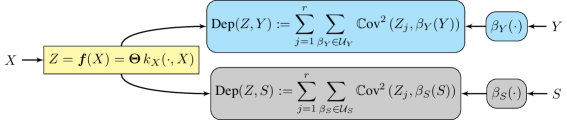

Let be the training data, containing i.i.d. samples from the joint distribution . Invoking the representer theorem (Shawe-Taylor & Cristianini, 2004), it follows that for each () we have where s are the learnable linear weights. Consequently, it follows that

| (5) |

where and .

Principally, if and only if (iff) for all Borel functions and belonging to the universal RKHSs and , respectively. Alternatively, iff HSIC where HSIC (Gretton et al., 2005a) is defined as

| (6) |

where and are countable orthonormal basis sets for the separable universal RKHSs and , respectively. However, since where is defined in (4), calculating necessitates the application of a cascade of kernels, which limits the analytical tractability of our solution. Therefore, we adopt a simplified version of HSIC that considers transformation on only but affords analytical tractability for solving the IRepL optimization problem. We define this measure as

| (7) |

where for s defined in (4). We note that Dep, unlike HSIC and other kernelization-based dependence measures, is not symmetric. However, symmetry is not necessary for measuring statistical dependence. To guarantee the boundedness of Dep and , we make the following assumption in the remainder of this paper.

Assumption 2.

We assume that and are separable222A Hilbert space is separable iff it has a countable orthonormal basis set. and the kernel functions are bounded:

| (8) |

The measure in (7) captures all modes of non-linear dependence under the assumption that the distribution of a low-dimensional projection of high-dimensional data is approximately normal (Diaconis & Freedman, 1984), (Hall & Li, 1993). To see why this reasoning is relevant, we note from (5) that can be expressed as , where and . This indicates that for large and small (which is the case for most real-world datasets), is indeed a low-dimensional projection of high-dimensional data. In other words, is approximately a jointly Gaussian RV. In our numerical experiments in Section 6, we empirically observe that enjoys an almost monotonic relation with the underlying invariance measure and captures all modes of dependency in practice, especially as . Nevertheless, if the normality assumption on the distribution of fails, Dep reduces to measuring the linear dependency between and for all Borel functions . This corresponds to measuring the mean independency of from , i.e., how much information a predictor (linear and non-linear) can infer (in the sense of MSE) about from . See Appendix H for more technical details on mean independency.

Lemma 1.

Let be the Gram matrices corresponding to and , respectively, i.e., and , where covariance is empirically estimated as

It follows that, the corresponding empirical estimator for is

| (9) |

where is the centering matrix, is a full column-rank matrix in which (Cholesky factorization), and is the Gram matrix corresponding to . Furthermore, the empirical estimator in (9) has a bias of and a convergence rate of .

Proof.

Finally, we note that the dependence measure between and can be defined similarly.

5 Exact Kernelized Trade-Off

Consider the optimization problem corresponding to in (2). Recall that is an -dimensional RV, where the embedding dimensionality is also a variable to be optimized. A common desideratum of learned representations is that of compactness (Bengio et al., 2013) to avoid learning representations with redundant information where different dimensions are highly correlated to each other. Therefore, going beyond the assumption that each component of (i.e., s) belongs to the universal RKHS , we impose additional constraints on the representation. Specifically, we constrain the search space of the encoder to learn a disentangled representation (Bengio et al., 2013) as follows

| (10) |

In the above set, the part enforces the covariance matrix of to be an identity matrix. Such disentanglement is also used in principal component analysis (PCA). It encourages the variance of each entry of to be one and different entries of to be uncorrelated with each other. The regularization part, encourages the encoder components to be as orthogonal as possible to each other and to be of unit norm, which aids with numerical stability during empirical estimation (Fukumizu et al., 2007). As the following theorem states formally, such disentanglement is an invertible transformation; therefore, it does not nullify any information.

Theorem 2.

Let be an arbitrary representation of the input data, where . Then, there exists an invertible Borel function , such that belongs to .

Proof.

The main idea is to search for an explicit expression for in terms of the invertible operator , where is induced by the bi-linear functional , and is the identity operator from to itself. See Appendix C for complete proof. ∎

This Theorem implies that the disentanglement preserves the performance of the downstream task since any target network can revert the disentanglement and access the original representation . In addition, any deterministic measurable transformation of will not add any information about that does not already exist in .

We define our K as

| (11) |

where is the utility-invariance trade-off parameter. Fortunately, the above optimization problem lends itself to a closed-form solution.

Theorem 3.

Consider the operator to be induced by the bi-linear functional and define and , similarly. Then, a global optimizer for the optimization problem in (11) is the eigenfunctions corresponding to the largest eigenvalues of the following generalized eigenvalue problem

| (12) |

where is the disentanglement regularization parameter defined in (10), and is the adjoint of .

Proof.

Remark 1.

If the trade-off parameter (i.e., no semantic independence constraint is imposed) and , the solution in Theorem 3 is equivalent to a supervised kernel-PCA. On the other hand, if (i.e., utility is ignored and only semantic independence is considered), the solution in Theorem 3 is the eigenfunctions corresponding to the smallest eigenvalues of , which are the directions that are the least explanatory of the semantic attribute .

Now, consider the empirical counterpart of the optimization problem (11),

| (13) |

where is given in (9) and is defined similarly.

Theorem 4.

Let the Cholesky factorization of be , where () is a full column-rank matrix. Let , then a solution to (13) is

where and the columns of are eigenvectors corresponding to the largest eigenvalues of the following generalized eigenvalue problem.

| (14) |

Further, the objective value of (13) is equal to , where are the largest eigenvalues of (14).

Proof.

Corollary 4.1.

Embedding Dimensionality: A useful corollary of Theorem 4 is characterizing optimal embedding dimensionality as a function of the trade-off parameter, :

To examine these results, consider two extreme cases: i) If there is no semantic independence constraint (i.e., ), all eigenvalues of (14) are non-negative since is a non-negative definite matrix and is a positive definite matrix. This indicates that is equal to the maximum possible value (that is equal to ), and therefore it is not required for to nullify any information in . ii) If we are only concerned about semantic independence and want to ignore the target task utility (i.e., ), all eigenvalues of (14) are non-positive and therefore would be the number of zero eigenvalues of (14). This indicates that in (9) is equal to zero, since is zero for zero eigenvalues of (14) when . In this case, adding more dimension to will necessarily increase .

The following Theorem characterizes the convergence behavior of empirical K to its population counterpart.

Theorem 5.

Assume that and are bounded by one and for any and for which . Then, for any and , with probability at least , we have

Proof.

Note that, for any in the training set, can be calculated as . We can assume that is bounded. For example, in RBF Gaussian and Laplacian RKHSs, both of which are universal, . This implies that , where is -th row of in equation (5). One always can normalize by dividing it by the maximum of over s, or by dividing by the maximum of over s and s. Notice that this normalization is only a scalar multiplication and has no effect on the invariance of to and the utility of any downstream target task predictor .

5.1 Numerical Complexity

Computational Complexity: If in (14) is provided in the training dataset, then the computational complexity of obtaining the optimal encoder is , where is the numerical rank of the Gram matrix . However, the dominating part of the computational complexity is due to the Cholesky factorization, , which is . Using random Fourier features (RFF) (Rahimi et al., 2007), can be approximated by , where . In this situation, the Cholesky factorization can be directly calculated as

| (15) |

As a result, the computational complexity of obtaining the optimal encoder becomes , where the RFF dimension, , can be significantly less than the sample size with negligible error on the approximation .

Memory Complexity: The memory complexity of (14), if calculated naively, is since and are by matrices. However, using RFF together with Cholesky factorization , , the left-hand side of (14) can be re-arranged as

| (16) |

where and therefore, the required memory complexity is . Note that and can be calculated similarly.

5.2 Target Task Performance in K

Assume that the desired target loss function is MSE. Then, in the following Theorem, we show that maximizing over can learn a representation that is informative enough for a target predictor on to achieve the most optimal estimation, i.e., the Bayes estimator ().

Theorem 6.

Let be the optimal encoder by maximizing Dep, where and is a linear RKHS. Then, there exist and such that is the Bayes estimator, i.e.,

Proof.

This Theorem implies that not only can preserve all the necessary information in to predict optimally, the learned representation is simple enough for a linear regressor to achieve optimal performance.

6 Experiments

In this section, we numerically quantify our K through the closed-form solution for the encoder obtained in Section 5 on an illustrative toy example and two real-world datasets, Folktables and CelebA.

6.1 Baselines

We consider two types of baselines: (1) ARL (the main framework for IRepL) with MSE or Cross-Entropy as the adversarial loss. Such methods are expected to fail to learn a fully invariant representation (Adeli et al., 2021; Grari et al., 2020). These include (Xie et al., 2017; Zhang et al., 2018; Madras et al., 2018), and SARL (Sadeghi et al., 2019). Among these baselines, except for SARL, all baselines are optimized via iterative minimax optimization, which is often unstable and not guaranteed to converge. On the other hand, SARL obtains a closed-form solution for the global optima of the minimax optimization under a linear dependence measure between and , which may fail to capture all modes of dependence between and . (2) HSIC-based adversarial loss that accounts for all modes of dependence, and as such, is theoretically expected to learn a fully invariant representation (Quadrianto et al., 2019). However, since stochastic gradient descent is used for learning, it lacks convergence guarantees to the global optima.

6.2 Datasets

Gaussian Toy Example: We design an illustrative toy example where and are mean independent in some dimensions but not fully independent in those dimensions. Specifically, and are -dimensional continuous RVs and generated as follows,

| (17) |

where and are applied point-wise. To generate the target attribute, we define four binary RVs as follows.

where is the indicator function, and we set , so it holds that for . Finally, we define as a -class categorical RV concatenated by s. Since is dependent on through all the dimensions of , a wholly invariant (i.e., ) should not contain any information about . However, since is only mean independent of (i.e., ), ARL baselines with MSE as the adversary loss, i.e., Xie et al. (2017); Zhang et al. (2018); Madras et al. (2018) and SARL cannot capture the dependency of to and result in a representation that is always dependent on (see Section H for theoretical details). We sample instances from independently and split these samples equally into training, validation, and testing partitions.

Folktables: We consider a fair representation learning task on Folktables (Ding et al., 2021) dataset (a derivation of the US census data). Specifically, we consider 2018-WA (Washington) and 2018-NY (New York) census data where the target attribute is the employment status (binary for WA and categories for NY and the semantic attribute is age (discrete value between and years). We seek to learn a representation that predicts employment status while being fair in demographic parity (DP) w.r.t. age. DP requires that the prediction be independent of , which can be achieved by enforcing . The WA and NY datasets contain and samples, each constructed from different features. We randomly split the data into training (), validation (), and testing () partitions. Further, we adopt embeddings for categorical features (learned in a supervised fashion to predict ) and normalization for continuous/discrete features (dividing by the maximum value).

CelebA: CelebA dataset (Liu et al., 2015) contains face images of different celebrities with standard training, validation, and testing splits. Each image is annotated with different attributes. We choose the target attribute as the high cheekbone attribute (binary) and the semantic attribute as the concatenation of gender and age (a -class categorical RV). The objective of this experiment is similar to that of Folktables. Since raw image data is not appropriate for kernel methods, we pre-train a ResNet-18 (He et al., 2016) (supervised to predict ) on CelebA images and extract features of dimension . These features are used as the input data for all methods.

6.3 Evaluation Metrics

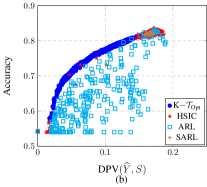

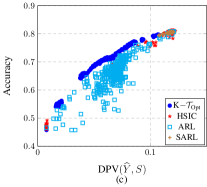

We use the accuracy of the classification tasks (-class classification for Gaussian toy example, employment prediction for Folktables, and high cheekbone prediction for CelebA) as the utility metric. For Folktables and CelebA datasets, we define DP violation as

| (18) |

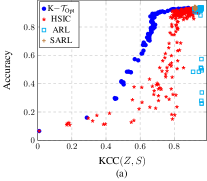

and use it as a metric to measure the variance (unfairness) of the prediction w.r.t. the semantic attribute . For the Gaussian toy example, the above metric is not suitable since is a continuous RV. To circumvent this difficulty, we employ KCC (Bach & Jordan, 2002)

| (19) |

as a measure of invariance of to , where and are RBF-Gaussian RKHS. The reason for using KCC instead of HSIC is that, unlike HSIC, KCC is normalized. Therefore it is a more readily interpretable measure for comparing the invariance of representations between different methods.

6.4 Choice of Pair

The existence of a utility-invariance trade-off ultimately depends on the statistical dependency between target and semantic attributes. If Dep is negligible, a trade-off does not exist. Keeping this in mind, we first chose the semantic attribute to be a sensitive attribute for Folktables (i.e., age) and CelebA (i.e., concatenation of age and gender) datasets. Then, we calculated the data imbalance (i.e., ) and KCC for all possible s. Finally, we chose with a small data imbalance and a moderate KCC. For Folktables dataset, and KCC. For CelebA dataset, and KCC.

6.5 Implementation Details

For all methods, we pick different values of (s for the Gaussian toy example and s for Folktables and CelebA datasets) between zero and one for obtaining the utility-invariance trade-off. We train the baselines that use a neural network for encoder five times with different random seeds. We let the random seed also change the training-validation-testing split for the Folktables dataset (CelebA and Gaussian datasets have fixed splits).

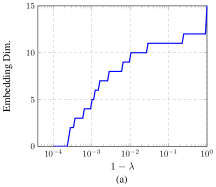

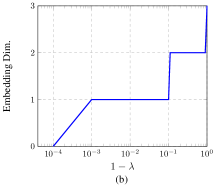

Embedding Dimensionality: None of the baseline methods have any strategy to find the optimum embedding dimensionality (), and they all set to a constant w.r.t. . Therefore, for baseline methods, we set (i.e., the minimum dimensionality required to classify different categories linearly) for the Gaussian toy example and (i.e., the minimum dimensionality required to classify different categories linearly) for Folktables-NY dataset, that is also equal to when . For K-, we use in Corollary 4.1. See Figure 3 for the plot of versus for the toy Gaussian and Folktables-NY datasets. For Folktables-WA and CelebA datasets, is equal to one, and therefore we let for all methods and all .

K (Ours): We let , , and be RBF Gaussian RKHS, where we compute the corresponding band-widths (i.e., s) using the median strategy introduced by Gretton et al. (2007). We optimize the regularization parameter in the disentanglement set (10) by minimizing the corresponding target losses over s in on validation sets. RFF (as discussed in Section 5.1) is adopted for all datasets. For RFF dimensionality, we started with a small value. Then, we gradually increased it until we reached the maximum possible performance for (i.e., the standard unconstrained representation learning) on the corresponding validation sets. Through this process, the final RFF dimensionality is for the Gaussian dataset, for the Folktables dataset, and for the CelebA dataset.

SARL (Sadeghi et al., 2019): SARL method is similar to our K except that and are linear RKHSs, and therefore we set and similar to that of K.

ARL (Xie et al., 2017; Zhang et al., 2018; Madras et al., 2018): The representation is extracted via the encoder , which is an MLP ( hidden layers and , neurons for Gaussian data; hidden layers and , neurons for Folktables and CelebA datasets). The architectural choices were based on starting with a single linear layer and gradually increasing the number of layers and neurons until over-fitting was observed. This results in the number of encoder parameters for the Gaussian toy example to be , while K has . For Folktables and CelebA, number of parameters is and , respectively, for ARL and and for K. The representation is then fed to a target task predictor and a proxy adversary , both of which are MLPs with hidden layers with neurons for Gaussian data and hidden layers with neurons for Folktables and CelebA. All involved networks () are trained end-to-end. We use stochastic gradient descent-ascent (SGDA) Xie et al. (2017) with AdamW (Loshchilov & Hutter, 2017) as an optimizer to alternately train the encoder, target predictor, and proxy adversary. We use a batch size of for Gaussian data; and for Folktables and CelebA. Then, the corresponding learning rates are optimized over by minimizing the target loss on the corresponding validation sets.

6.6 Results

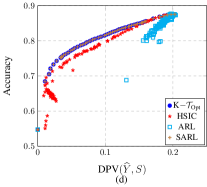

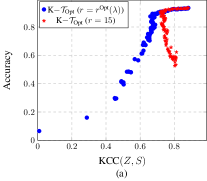

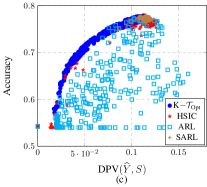

Utility-Invariance Trade-offs: Figures 4 and 5 show the utility-invariance and Dep-Dep trade-offs for the toy Gaussian, Folktables-WA, Folktables-NY, and CelebA datasets. The invariance measure for the Gaussian toy example is KCC (19), and the invariance measure for Folktables and CelebA datasets is the fairness measure, DPV (18). We make the following observations: 1) K is highly stable and almost spans the entire trade-off front for all datasets except Folktables-NY, which can be due to the inability of scalarized single-objective formulation in (2), in contrast to the constrained optimization in (1), to find all Pareto-optimal points. 2) There is almost the same trend in the trade-off between Dep and Dep (Figure 5) as the utility-invariance trade-off (Figure 4). This is a desirable observation since Dep-Dep trade-off is what we optimized in (11) as a surrogate to utility-invariance trade-off. 3) The baseline method HSIC-IRepL, despite using a universal dependence measure, leads to a sub-optimal trade-off front due to the lack of convergence guarantees to the global optima. 4) The baselines, ARL and SARL, span only a small portion of the trade-off front in the Gaussian toy example since some dimensions of the semantic attribute in (6.2) are mean independent (but not entirely independent) to some dimensions of . Therefore the adversary does not provide any information to the encoder to discard from the representation. Moreover, in this dataset, ARL and SARL baselines do not approach , i.e., KCC cannot be attained for any value of the trade-off parameter . 5) ARL shows high deviation on the Folktables dataset due to the unstable nature of the minimax optimization. 6) SARL performs as well as our K for CelebA dataset. This is because both and are categorical for the CelebA dataset, and therefore linear RKHS on one-hot encoded attribute performs just as well as universal RKHSs (Li et al., 2021).

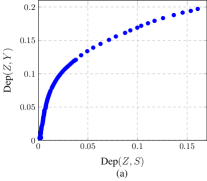

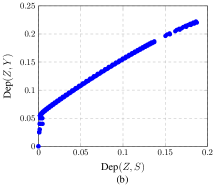

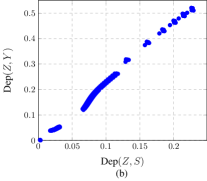

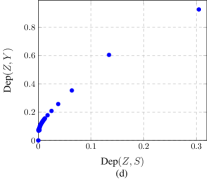

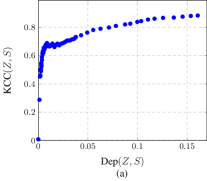

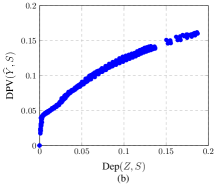

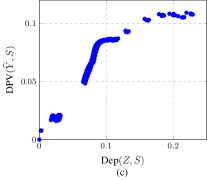

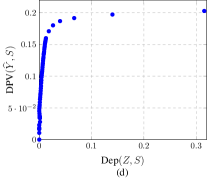

Universality of : We empirically examine the practical validity of our assumption in Section 4 and verify if our dependence measure , defined in (7), can capture all modes of dependency between and . Figure 6 (a) shows the plot of the universal dependence measure KCC versus Dep for the Gaussian dataset and Figures 6 (b, c) illustrate the relationship between DPV and Dep for Folktables and CelebA datasets, respectively. We observe a non-decreasing relation between the corresponding invariance measures and Dep. More importantly, as (or ) so does . These observations verify that accounts for all modes of dependence between and .

6.7 Ablation Study

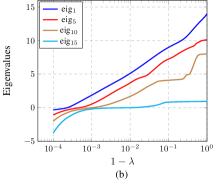

Effect of Embedding Dimensionality: In this experiment, we examine the significance of the embedding dimensionality, , discussed in Corollary 4.1. We obtain the utility-invariance trade-off when the embedding dimensionality is fixed to . A comparison between the utility-invariance trade-off induced by and the fixed is illustrated in Figure 7 (a). We observe that not only the utility-invariance trade-off for fixed is dominated by that of , but also, using fixed is unable to achieve the total invariance representation, i.e., . Further, some of the largest eigenvalues of (14) versus the invariance trade-off parameter are plotted in Figure 7 (b). We recall from Corollary 4.1 that, for any given , is the number of non-negative eigenvalues of (14).

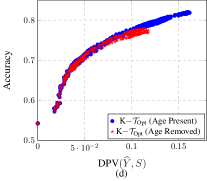

Effect of Semantic Attribute Removal: In this experiment, we examine the effect of removing (i.e., age) from the input data in the Folktables-WA dataset and examine whether this removal helps the utility-invariance trade-off. Figure 7 (c) shows the utility-invariance trade-off resulting from all methods, and Figure 7 (d) compares removing and keeping the age information from the input data for K. Observe that: 1) There is almost the same trend in both keeping and removing the age attribute from the input data for all methods. 2) Removing the age attribute from input data slightly degrades the utility-invariance trade-off due to the lower information contained in the input data.

7 Conclusion

Invariant representation learning (IRepL) often involves a trade-off between utility and invariance. While the existence of such trade-off and its bounds have been studied, its exact characterization has not been investigated. This paper took steps towards addressing this problem by i) establishing the exact kernelized trade-off (denoted by K), ii) determining the optimal dimensionality of the data representation necessary to achieve a desired optimal trade-off point, and iii) developing a scalable learning algorithm for encoders in some RKHSs to achieve K. Numerical results on an illustrative example and two real-world datasets show that commonly used adversarial representation learning-based techniques cannot attain the optimal trade-off estimated by our solution.

Our theoretical results and empirical solutions shed light on the utility-invariance trade-off for various settings, such as algorithmic fairness and privacy-preserving learning under the scalarization of the bi-objective trade-off formulation. Furthermore, the trade-off in IRepL is also a function of the involved dependence measure that quantifies the dependence of learned representations on the semantic attribute. As such, the trade-off obtained in this paper is optimal for HSIC-like dependence measures. Studying the bi-objective trade-off (rather than the scalarization) and employing other universal measures are possible directions for future work.

Broader Impact

IRepL can enable many machine learning systems to generalize to the domains that have not been trained on or prevent the leakage of private (sensitive) information while being effective for the desired prediction task(s). In particular, IRepL has a direct application in fairness which is a significant societal problem. Even though this paper aims to characterize the utility-invariance trade-off as a byproduct, our paper proposes an algorithm that learns fair representations of data. More generally, these approaches can enable machine learning systems to discard specific data before making predictions. We point out that demographic parity, the fairness criterion considered in this paper, can be unsuitable as a fairness criterion in some practical scenarios (Hardt et al., 2016; Chouldechova, 2017) and other fairness criteria like equalized odds (EO) or equality of opportunity (EOO) (Hardt et al., 2016) should be considered. The method proposed in this paper can be extended to other notions of fairness, such as EO and EOO, by modifying Dep to capture the dependency between and , given . We leave this extension to future work.

Acknowledgements: This work was supported in part by financial assistance from the U.S. Department of Commerce, National Institute of Standards and Technology (award #60NANB18D210) and the National Science Foundation (award #2147116).

References

- Adeli et al. (2021) Ehsan Adeli, Qingyu Zhao, Adolf Pfefferbaum, Edith V Sullivan, Li Fei-Fei, Juan Carlos Niebles, and Kilian M Pohl. Representation learning with statistical independence to mitigate bias. IEEE/CVF Winter Conference on Applications of Computer Vision, pp. 2513–2523, 2021.

- Bach & Jordan (2002) Francis R Bach and Michael I Jordan. Kernel independent component analysis. Journal of Machine Learning Research, 3(6):1–48, 2002.

- Barshan et al. (2011) Elnaz Barshan, Ali Ghodsi, Zohreh Azimifar, and Mansoor Zolghadri Jahromi. Supervised principal component analysis: Visualization, classification and regression on subspaces and submanifolds. Pattern Recognition, 44(7):1357–1371, 2011.

- Belghazi et al. (2018) Mohamed Ishmael Belghazi, Aristide Baratin, Sai Rajeshwar, Sherjil Ozair, Yoshua Bengio, Aaron Courville, and Devon Hjelm. Mutual information neural estimation. International Conference on Machine Learning, pp. 531–540, 2018.

- Bengio et al. (2013) Yoshua Bengio, Aaron Courville, and Pascal Vincent. Representation learning: A review and new perspectives. IEEE Transactions on Pattern Analysis and Machine Intelligence, 35(8):1798–1828, 2013.

- Bertran et al. (2019) Martin Bertran, Natalia Martinez, Afroditi Papadaki, Qiang Qiu, Miguel Rodrigues, Galen Reeves, and Guillermo Sapiro. Adversarially learned representations for information obfuscation and inference. International Conference on Machine Learning, 2019.

- Beutel et al. (2017) Alex Beutel, Jilin Chen, Zhe Zhao, and Ed H Chi. Data decisions and theoretical implications when adversarially learning fair representations. arXiv preprint arXiv:1707.00075, 2017.

- Calmon et al. (2017) Flavio Calmon, Dennis Wei, Bhanukiran Vinzamuri, Karthikeyan Natesan Ramamurthy, and Kush R Varshney. Optimized pre-processing for discrimination prevention. Advances in Neural Information Processing Systems, pp. 3992–4001, 2017.

- Chouldechova (2017) Alexandra Chouldechova. Fair prediction with disparate impact: A study of bias in recidivism prediction instruments. big data 5, 2 (2017), 153–163. arXiv preprint arXiv:1610.07524, 2017.

- Coavoux et al. (2018) Maximin Coavoux, Shashi Narayan, and Shay B Cohen. Privacy-preserving neural representations of text. arXiv preprint arXiv:1808.09408, 2018.

- Creager et al. (2019) Elliot Creager, David Madras, Jörn-Henrik Jacobsen, Marissa A Weis, Kevin Swersky, Toniann Pitassi, and Richard Zemel. Flexibly fair representation learning by disentanglement. International Conference on Machine Learning, 2019.

- Diaconis & Freedman (1984) Persi Diaconis and David Freedman. Asymptotics of graphical projection pursuit. The Annals of Statistics, pp. 793–815, 1984.

- Ding et al. (2021) Frances Ding, Moritz Hardt, John Miller, and Ludwig Schmidt. Retiring adult: New datasets for fair machine learning. arXiv preprint arXiv:2108.04884, 2021.

- Dusmanu et al. (2021) Mihai Dusmanu, Johannes L Schönberger, Sudipta N Sinha, and Marc Pollefeys. Privacy-preserving visual feature descriptors through adversarial affine subspace embedding. IEEE Conference on Computer Vision and Pattern Recognition, 2021.

- Dutta et al. (2020) Sanghamitra Dutta, Dennis Wei, Hazar Yueksel, Pin-Yu Chen, Sijia Liu, and Kush Varshney. Is there a trade-off between fairness and accuracy? A perspective using mismatched hypothesis testing. International Conference on Machine Learning, pp. 2803–2813, 2020.

- Dwork et al. (2012) Cynthia Dwork, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Richard Zemel. Fairness through awareness. Innovations in Theoretical Computer Science Conference, pp. 214–226, 2012.

- Edwards & Storkey (2015) Harrison Edwards and Amos Storkey. Censoring representations with an adversary. arXiv preprint arXiv:1511.05897, 2015.

- Feldman et al. (2015) Michael Feldman, Sorelle A Friedler, John Moeller, Carlos Scheidegger, and Suresh Venkatasubramanian. Certifying and removing disparate impact. ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pp. 259–268, 2015.

- Fukumizu et al. (2007) Kenji Fukumizu, Francis R Bach, and Arthur Gretton. Statistical consistency of kernel canonical correlation analysis. Journal of Machine Learning Research, 8(2), 2007.

- Ganin & Lempitsky (2015) Yaroslav Ganin and Victor Lempitsky. Unsupervised domain adaptation by backpropagation. International Conference on Machine Learning, 2015.

- Ganin et al. (2016) Yaroslav Ganin, Evgeniya Ustinova, Hana Ajakan, Pascal Germain, Hugo Larochelle, François Laviolette, Mario Marchand, and Victor Lempitsky. Domain-adversarial training of neural networks. Journal of Machine Learning Research, 17(1):2096–2030, 2016.

- Gouic et al. (2020) Thibaut Le Gouic, Jean-Michel Loubes, and Philippe Rigollet. Projection to fairness in statistical learning. arXiv preprint arXiv:2005.11720, 2020.

- Grari et al. (2020) Vincent Grari, Oualid El Hajouji, Sylvain Lamprier, and Marcin Detyniecki. Learning unbiased representations via Rényi minimization. arXiv preprint arXiv:2009.03183, 2020.

- Gretton et al. (2005a) Arthur Gretton, Olivier Bousquet, Alex Smola, and Bernhard Schölkopf. Measuring statistical dependence with Hilbert-Schmidt norms. International Conference on Algorithmic Learning Theory, pp. 63–77, 2005a.

- Gretton et al. (2005b) Arthur Gretton, Ralf Herbrich, Alexander Smola, Olivier Bousquet, and Bernhard Schölkopf. Kernel methods for measuring independence. Journal of Machine Learning Research, 6(12):2075–2129, 2005b.

- Gretton et al. (2006) Arthur Gretton, Karsten Borgwardt, Malte Rasch, Bernhard Schölkopf, and Alexander J. Smola. A kernel method for the two-sample-problem. Advances in Neural Information Processing Systems, 19, 2006.

- Gretton et al. (2007) Arthur Gretton, Kenji Fukumizu, Choon Hui Teo, Le Song, Bernhard Schölkopf, and Alexander J. Smola. A kernel statistical test of independence. Advances in Neural Information Processing Systems, 20:585–592, 2007.

- Hall & Li (1993) Peter Hall and Ker-Chau Li. On almost linearity of low dimensional projections from high dimensional data. The Annals of Statistics, pp. 867–889, 1993.

- Hamm (2017) Jihun Hamm. Minimax filter: Learning to preserve privacy from inference attacks. Journal of Machine Learning Research, 18(1):4704–4734, 2017.

- Hardt et al. (2016) Moritz Hardt, Eric Price, Nati Srebro, et al. Equality of opportunity in supervised learning. In Advances in Neural Information Processing Systems, pp. 3315–3323, 2016.

- He et al. (2016) Kaiming He, Xiangyu Zhang, Shaoqing Ren, and Jian Sun. Deep residual learning for image recognition. Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, pp. 770–778, 2016.

- Hoeffding (1994) Wassily Hoeffding. Probability inequalities for sums of bounded random variables. In The Collected Works of Wassily Hoeffding, pp. 409–426. Springer, 1994.

- Jacod & Protter (2012) Jean Jacod and Philip Protter. Probability essentials. Springer Science & Business Media, 2012.

- Kokiopoulou et al. (2011) Effrosini Kokiopoulou, Jie Chen, and Yousef Saad. Trace optimization and eigenproblems in dimension reduction methods. Numerical Linear Algebra with Applications, 18(3):565–602, 2011.

- Li et al. (2021) Yazhe Li, Roman Pogodin, Danica J Sutherland, and Arthur Gretton. Self-supervised learning with kernel dependence maximization. arXiv preprint arXiv:2106.08320, 2021.

- Liu et al. (2015) Ziwei Liu, Ping Luo, Xiaogang Wang, and Xiaoou Tang. Deep learning face attributes in the wild. IEEE International Conference on Computer Vision, 2015.

- Locatello et al. (2019) Francesco Locatello, Gabriele Abbati, Thomas Rainforth, Stefan Bauer, Bernhard Schölkopf, and Olivier Bachem. On the fairness of disentangled representations. Advances in Neural Information Processing Systems, pp. 14611–14624, 2019.

- Loshchilov & Hutter (2017) Ilya Loshchilov and Frank Hutter. Decoupled weight decay regularization. arXiv preprint arXiv:1711.05101, 2017.

- Madras et al. (2018) David Madras, Elliot Creager, Toniann Pitassi, and Richard Zemel. Learning adversarially fair and transferable representations. arXiv preprint arXiv:1802.06309, 2018.

- Martinez et al. (2020) Natalia Martinez, Martin Bertran, and Guillermo Sapiro. Minimax pareto fairness: A multi objective perspective. International Conference on Machine Learning, pp. 6755–6764, 2020.

- Mary et al. (2019) Jérémie Mary, Clément Calauzenes, and Noureddine El Karoui. Fairness-aware learning for continuous attributes and treatments. International Conference on Machine Learning, pp. 4382–4391, 2019.

- McNamara et al. (2019) Daniel McNamara, Cheng Soon Ong, and Robert C Williamson. Costs and benefits of fair representation learning. AAAI/ACM Conference on AI, Ethics, and Society, pp. 263–270, 2019.

- Menon & Williamson (2018) Aditya Krishna Menon and Robert C Williamson. The cost of fairness in binary classification. Conference on Fairness, Accountability and Transparency, pp. 107–118, 2018.

- Pérez-Suay et al. (2017) Adrián Pérez-Suay, Valero Laparra, Gonzalo Mateo-García, Jordi Muñoz-Marí, Luis Gómez-Chova, and Gustau Camps-Valls. Fair kernel learning. Joint European Conference on Machine Learning and Knowledge Discovery in Databases, pp. 339–355, 2017.

- Quadrianto et al. (2019) Novi Quadrianto, Viktoriia Sharmanska, and Oliver Thomas. Discovering fair representations in the data domain. Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition, pp. 8227–8236, 2019.

- Rahimi et al. (2007) Ali Rahimi, Benjamin Recht, et al. Random features for large-scale kernel machines. Advances in Neural Information Processing Systems, 3(4):5, 2007.

- Roy & Boddeti (2019) Proteek Roy and Vishnu Naresh Boddeti. Mitigating information leakage in image representations: A maximum entropy approach. IEEE Conference on Computer Vision and Pattern Recognition, 2019.

- Ruggieri (2014) Salvatore Ruggieri. Using t-closeness anonymity to control for non-discrimination. Transactions on Data Privacy, 7(2):99–129, 2014.

- Sadeghi et al. (2019) Bashir Sadeghi, Runyi Yu, and Vishnu Boddeti. On the global optima of kernelized adversarial representation learning. IEEE International Conference on Computer Vision, pp. 7971–7979, 2019.

- Schölkopf et al. (1998) Bernhard Schölkopf, Alexander Smola, and Klaus-Robert Müller. Nonlinear component analysis as a kernel eigenvalue problem. Neural Computation, 10(5):1299–1319, 1998.

- Shawe-Taylor & Cristianini (2004) John Shawe-Taylor and Nello Cristianini. Kernel methods for pattern analysis. Cambridge University Press, 2004.

- Song et al. (2019) Jiaming Song, Pratyusha Kalluri, Aditya Grover, Shengjia Zhao, and Stefano Ermon. Learning controllable fair representations. International Conference on Artificial Intelligence and Statistics, 2019.

- Sriperumbudur et al. (2011) Bharath K Sriperumbudur, Kenji Fukumizu, and Gert RG Lanckriet. Universality, characteristic kernels and RKHS embedding of measures. Journal of Machine Learning Research, 12(7), 2011.

- Strawderman (1999) Robert L Strawderman. The symmetric eigenvalue problem (classics in applied mathematics, number 20). Journal of the American Statistical Association, 94(446):657, 1999.

- Tzeng et al. (2017) Eric Tzeng, Judy Hoffman, Kate Saenko, and Trevor Darrell. Adversarial discriminative domain adaptation. IEEE Conference on Computer Vision and Pattern Recognition, 2017.

- Xiao et al. (2020) Taihong Xiao, Yi-Hsuan Tsai, Kihyuk Sohn, Manmohan Chandraker, and Ming-Hsuan Yang. Adversarial learning of privacy-preserving and task-oriented representations. Proceedings of the AAAI Conference on Artificial Intelligence, pp. 12434–12441, 2020.

- Xie et al. (2017) Qizhe Xie, Zihang Dai, Yulun Du, Eduard Hovy, and Graham Neubig. Controllable invariance through adversarial feature learning. Advances in Neural Information Processing Systems, pp. 585–596, 2017.

- Zemel et al. (2013) Rich Zemel, Yu Wu, Kevin Swersky, Toni Pitassi, and Cynthia Dwork. Learning fair representations. International Conference on Machine Learning, pp. 325–333, 2013.

- Zhang et al. (2018) Brian Hu Zhang, Blake Lemoine, and Margaret Mitchell. Mitigating unwanted biases with adversarial learning. AAAI/ACM Conference on AI, Ethics, and Society, 2018.

- Zhao (2021) Han Zhao. Costs and benefits of wasserstein fair regression. arXiv preprint arXiv:2106.08812, 2021.

- Zhao & Gordon (2019) Han Zhao and Geoffrey J Gordon. Inherent tradeoffs in learning fair representations. arXiv preprint arXiv:1906.08386, 2019.

- Zhao et al. (2018) Han Zhao, Shanghang Zhang, Guanhang Wu, José MF Moura, Joao P Costeira, and Geoffrey J Gordon. Adversarial multiple source domain adaptation. Advances in Neural Information Processing Systems, 31:8559–8570, 2018.

- Zhao et al. (2019a) Han Zhao, Jianfeng Chi, Yuan Tian, and Geoffrey J Gordon. Trade-offs and guarantees of adversarial representation learning for information obfuscation. arXiv preprint arXiv:1906.07902, 2019a.

- Zhao et al. (2019b) Han Zhao, Remi Tachet Des Combes, Kun Zhang, and Geoffrey Gordon. On learning invariant representations for domain adaptation. International Conference on Machine Learning, pp. 7523–7532, 2019b.

- Zhao et al. (2020) Han Zhao, Chen Dan, Bryon Aragam, Tommi S Jaakkola, Geoffrey J Gordon, and Pradeep Ravikumar. Fundamental limits and tradeoffs in invariant representation learning. arXiv preprint arXiv:2012.10713, 2020.

Appendix A A Population Expression for Definition in (7)

A population expression for in (7) is given in the following.

where is independent of with the same distribution as .

Proof.

We first note that this population expression is inspired by that of HSIC (Gretton et al., 2005a).

Consider the operator induced by the linear functional . Then, it follows that

where (a) is due to Parseval relation for orthonormal basis and (b) is from the definition of . ∎

Appendix B Proof of Lemma 1

Lemma 1.

Let be Gram matrices corresponding to and , respectively, i.e., and , where covariance is empirically estimated as

It follows that, the corresponding empirical estimation for is

| (20) |

where is the centering matrix, and is a full column-rank matrix in which (Cholesky factorization), and is the Gram matrix corresponding to . Furthermore, the empirical estimator in (9) has a bias of and a convergence rate of .

Proof.

Firstly, let us reconstruct the orthonormal set when i.i.d. observations are given. Invoking representer theorem, for two arbitrary elements and in , we have

where is a full column-rank matrix and is the Cholesky factorization of . As a result, searching for is equivalent to searching for where is any complete orthonormal set for . Using empirical expression for covariance, we get

where and .

We now show that the bias of for estimating in (9) is . To achieve this, we split into three terms as,

| (21) | |||||

Let denote the set of all -tuples drawn without replacement from . Moreover, let and denote the element of an arbitrary matrix at -th row and -th column. Then, it follows that

(I):

where and are independently drawn from the joint distribution .

(II):

| (23) | |||||

(III):

Using above calculations together with Lemma 2 lead to

We now obtain the convergence of . Consider the decomposition in (21) together with (B), (23), and (B). Let , then it follows that

where and . For convenience, we omit the term and add it back in the last stage.

Define and consider the following U-statistics (Hoeffding, 1994)

Then, from Hoeffding’s inequality (Hoeffding, 1994) it follows that

where we assumed that is bounded by one and is bounded by for any and .

Further, if , it holds that

Consequently, we have

Therefore, with probability at least , it holds

| (25) |

∎

Appendix C Proof of Theorem 2

Theorem 2.

Let be an arbitrary representation of the input data, where . Then, there exist an invertible Borel function , such that, belongs to .

Proof.

Recall that the space of disentangled representation is

where . Let denote the identity operator from to . We claim that , where

is the desired invertible transformation. To see this, construct

The inverse of is where

∎

Appendix D Proof of Theorem 3

Theorem 3.

Consider the operator to be induced by the bi-linear functional and define and , similarly. Then, a global optimizer for the optimization problem in (11) is the eigenfunctions corresponding to the largest eigenvalues of the following generalized eigenvalue problem

| (26) |

where is the disentanglement regularization parameter defined in (10), and is the adjoint of .

Proof.

Consider in (7):

where the last step is due to Parseval’s identity for orthonormal basis set. Similarly, we have . Recall that , then it follows that

where is the adjoint operator of . Further, note that is equal to . As a result, the optimization problem in (26) can be restated as

where denotes identity operator from to . This optimization problem is known as generalized Rayleigh quotient (Strawderman, 1999) and a possible solution to it is given by the eigenfunctions corresponding to the largest eigenvalues of the following generalized problem

∎

Appendix E Proofs of Theorem 4 and Corollary 4.1

Theorem 4.

Let the Cholesky factorization of be , where () is a full column-rank matrix. Let , then a solution to (13) is

where and the columns of are eigenvectors corresponding to the largest eigenvalues of the following generalized eigenvalue problem.

| (27) |

Further, the supremum value of (13) is equal to , where are largest eigenvalues of (14).

Proof.

Consider the Cholesky factorization, where is a full column-rank matrix. Using the representer theorem, the disentanglement property in (10) can be expressed as

As a result, is equivalent to

where .

Let and consider the optimization problem in (13):

| (28) | |||||

where the second step is due to (9) and

It is shown in Kokiopoulou et al. (2011) that an333Optimal is not unique. optimizer of (28) is any matrix whose columns are eigenvectors corresponding to largest eigenvalues of generalized problem

| (29) |

and the maximum value is the summation of largest eigenvalues. Once is determined, then, any in which is optimal (denoted by ). Note that is not unique and has a general form of

However, setting to zero would lead to minimum norm for . Therefore, we opt . ∎

Corollary 4.1.

Embedding Dimensionality: A useful corollary of Theorem 4 is characterizing optimal embedding dimensionality as a function of trade-off parameter, :

Appendix F Proof of Theorem 5

Theorem 5.

Assume that and are bounded by one and for any and for which . Then, for any and , with probability at least , we have

Proof.

Recall that in the proof of Lemma 1 we have shown that with probability at least , the following inequality holds

Using the same reasoning for , with probability at least , we have

Since and , it follows that with probability at least ,

We complete the proof by noting that, the following inequality holds for any bounded and :

∎

Appendix G Optimality of Target Task Performance in K

We show that maximizing can lead to a representation that is sufficient to result in the optimal Bayes prediction of .

Theorem 6.

Let be the optimal encoder by maximizing Dep, where and is a linear RKHS. Then, there exist and such that is the Bayes estimator, i.e.,

Proof.

We only prove this theorem for the empirical version due to its convergence to the population counterpart. The optimal Bayes estimator can be the composition of the kernelized encoder and a linear regressor on top of it. More specifically, can approach to if we optimize , , and all together. This is because can approximate any Borel function (due to the universality of ) and, since , can be surjective. Let and . Further, let and be the centered (i.e., mean subtracted) version of and , respectively. We firstly optimize for any given , , and :

Then, optimizing over would lead to

where denotes the orthogonal projector onto the column space of and a possible minimizer is or equivalently . Since the MSE loss is a function of the range (column space) of , we can consider only with orthonormal columns or equivalently . In this setting, it holds . Now, consider optimizing . We have, where is the centering matrix. Let and , then it follows that

where are largest eigenvalues of the following generalized problem

and . This resembles the eigenvalue problem in Section E, equation (29) where , is a linear RKHS and . ∎

Appendix H Deficiency of Mean-Squared Error as A Measure of Dependence

Theorem.

Let contain all Borel functions, be a -dimensional RV, and be MSE loss. Then,

Proof.

Let , , and denote the -th entries of , , and , respectively. Then, it follows that

where the second step is due to the optimality of conditional mean (i.e., Bayes estimation) for MSE (Jacod & Protter, 2012) and the last step is because independence between and leads to an upper bound on MSE. Therefore, if , then . On the other hand, if , then it follows immediately that . ∎

This theorem implies that an optimal adversary does not necessarily lead to a representation that is statistically independent of , but rather leads to being mean independent of the representation .