Bayesian Estimation of the Degrees of Freedom Parameter of the Student- Distribution—A Beneficial Re-parameterization

Abstract

In this paper, conditional data augmentation (DA) is investigated for the degrees of freedom parameter of a Student- distribution. Based on a restricted version of the expected augmented Fisher information, it is conjectured that the ancillarity DA is progressively more efficient for MCMC estimation than the sufficiency DA as increases; with the break even point lying at as low as . The claim is examined further and generalized through a large simulation study and a application to U.S. macroeconomic time series. Finally, the ancillarity-sufficiency interweaving strategy is empirically shown to combine the benefits of both DAs. The proposed algorithm may set a new standard for estimating as part of any model.

1 Introduction

The Student- distribution is a standard item in the statistician’s toolbox. Utilized as the regression error distribution, it robustifies parameter estimation against extreme observations in the data set [9]. Furthermore, the properties of Student- are classical building blocks of hierarchical models for financial \parencitesBollerslev1987,Harvey1994 and polychotomous data [1], among others.

Maximum likelihood (ML) estimation of the degrees of freedom () parameter can be cumbersome due to the complexity of the likelihood function; [23] give an overview and develop a quasi-Newton, an expectation-maximization (EM), and a score function-based approach to ML. \textcitesLiu1997 reviews extensions to the EM algorithm for the multivariate Student- distribution. In the non-asymptotic branch of frequentist literature, [8] discusses structural inference for the parameters, and \textcitesSutradhar1986,Singh1988 provide method of moments estimators for .

Bayesian treatments of robust regression date back to [7], who explores scale-mixtures of normal distributions as a tool for handling outliers and presents the Cauchy distribution as an example, which corresponds to . Still with a fixed , [44] discusses posterior inference for the parameters of a multivariate linear Student- regression using conjugate prior distributions. \textcitesRamsay1980,West1984 further extend de Finetti’s framework and provide more examples including the Student- distribution. \textcitesChib1991 demonstrate conditions, when this type of robust regression can not work due to a non-informative likelihood for .

In terms of Bayesian inference for using Markov chain Monte Carlo methods [[, MCMC;]]Tierney1994, the Gibbs sampler [12] by [15] has been established as the standard method and it comprises the main focus in this paper. The Gibbs sampler relies on the scale-mixture representation of the Student- distribution to draw a posterior sample using a model with data augmentation [[, DA;]]VanDyk2001. There exist many options for DA; however, to our knowledge, only the one outlined by [15], termed sufficient augmentation (SA), has been in use for Student-.

Multiple examples demonstrate that SA may not work well for sampling ; see, for instance, [14, efficiency values in Appendix C], or [26], who blame the hierarchical structure and the lack of marginalization for the low sampling efficiency. However, inspired by the general framework of [30], an alternative way to higher efficiency is found. They demonstrate through multiple example models that the transformation of SA to the ancillary augmentation (AA) often boosts the efficiency already quite drastically; unfortunately, whether AA or SA is superior depends on the data set. [29] propose as the way out of this data-dependence a hybrid Gibbs-sampler, which randomly picks AA or SA in every pass; they conclude that a combination of sufficiency and ancillarity may be desirable in any setting. Finally, [43] introduce the ancillarity-sufficiency interweaving strategy (ASIS), which exploits the complementary roles of AA and SA in any hierarchical model and integrates them into one generally effective recipe. The applicability and utility of ASIS is documented in the literature [[, see, e.g.,]]Kastner2014,Bitto2019,Monterrubio-Gomez2020.

The contribution of this paper is two-fold: the ancillary parameterization for the Student- distribution is introduced, and it is shown through simulations that the AA sampler explores the posterior space more efficiently than the usual SA sampler for a large set of data generating processes; furthermore, an implementation of ASIS is proposed that can be applied as a plug-and-play substitute in any MCMC procedure for models that include the Student- distribution with unknown degrees of freedom.

The remaining part of the paper is structured as follows: Section 2 introduces the model and the notation. Section 3 provides details on measurement of efficiency, the Gibbs sampling algorithm, and the corresponding conditional distributions. Section 4 showcases the efficiency of the introduced method on a large grid of simulated data sets, and Section 5 is an application inspired by [16]. Section 6 concludes.

2 Simple Student--Model

The simplest setup with Student- errors is investigated;

| (1) |

where denotes the Student- distribution with degrees of freedom, location , and variance ; the kernel of its density function is . Taking this simple model enables a pure analysis of sampling , decoupled from other effects present in larger models; furthermore, Equation (1) is an ingredient of all models employing the Student- distribution. At the same time, the simplicity of Equation (1) is not restrictive either due to the modular nature of Gibbs-sampling: in case an econometric model is extended by Student- errors, its corresponding MCMC procedure shall merely include the additional steps for drawing . This modularity is demonstrated in Section 5 through a more complex model.

As [44] points out, the density function of the Student- distribution can be formulated as a scale mixture of normal distributions, which inspires the introduction of missing data and the data augmented representation

| (2) |

where denotes the univariate normal distribution with mean and variance , and is the gamma distribution with shape and rate . [30] call Equation (2) the centered parameterization, while, following [43], we prefer the term sufficient parameterization. This terminology derives from the fact that is a sufficient statistic for .

Based on Equation (2), it is possible to derive other data augmentation schemes, where the auxiliary variable and are a priori independent; these are called ancillary parameterization. As [30] point out, one such option is to replace by , where is the cumulative distribution function (CDF) for the prior distribution of . Note that follows a standard uniform distribution a priori; therefore, the ancillary data augmentation for Equation (1) is

| (3) |

where is the inverse CDF for the prior distribution of .

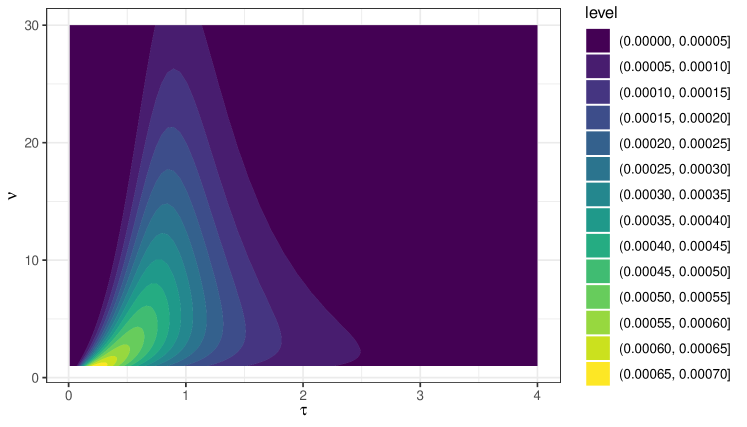

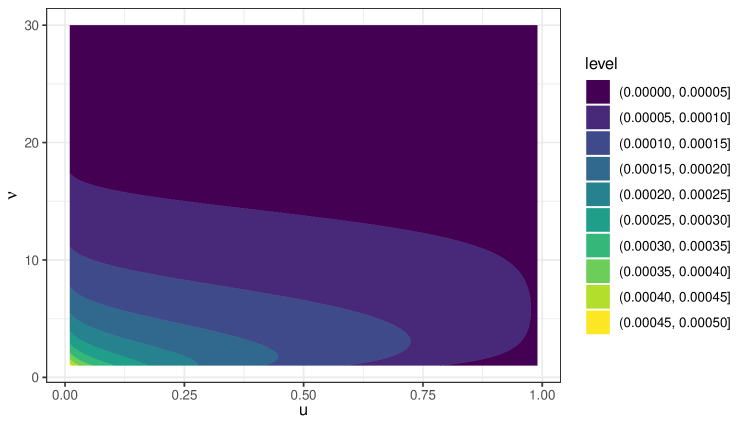

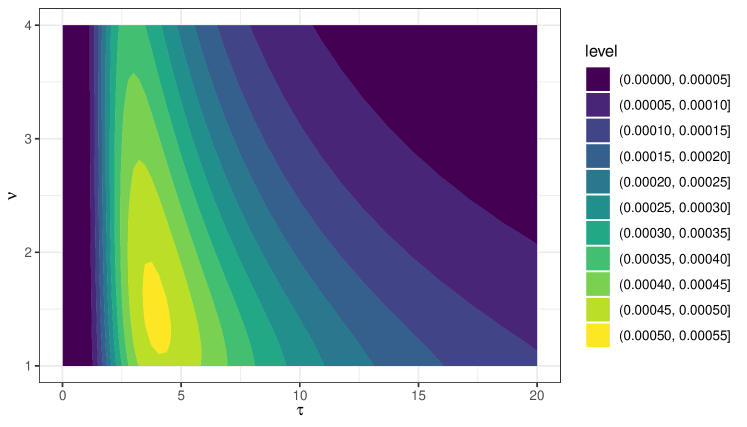

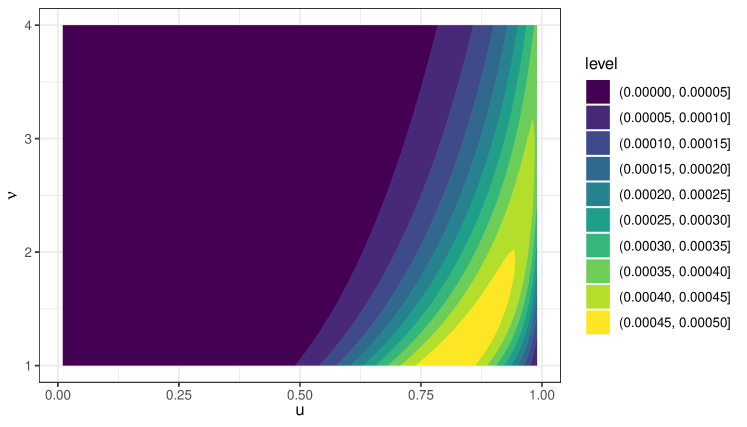

As demonstrated by [43], for improved sampling efficiency, it is beneficial to consider both a sufficient and an ancillary data augmentation scheme in the design of an MCMC sampling algorithm. The added value in using both stems in the differences between the joint distributions and ; two slices for each distribution are depicted in Figures 1 and 2, respectively. The figures show contour plots of unnormalized111There is no closed form for these distributions, and normalization is done over the shown window, which contains most of the probability mass. posterior densities and for small () and large () observation error. The top panel of Figure 1 depicts rotating shapes, which signals that the dependence between and is different at different parts of the space. In comparison, this rotation is non-visible in the bottom panel, and, thus, dependence between and seems less complex; moreover, for the shown range, the shapes of isolines resemble concentric standard ellipses, which is a sign for approximate posterior independence between and ; a Gibbs-sampler can explore such a space very efficiently. Figure 2 shows an example, where a suspect outlier is modeled using Student- errors and a small value for is expected; here, the dependence between and varies less in space than the dependence between and . In conclusion, SA seems beneficial for fat tailed observations; on the other hand, AA may excel for lighter tailed observations.

The Bayesian description of the model is completed by the prior distribution . Following [15], an exponential distribution is assumed;

| (4) |

where denotes the rate parameter. This choice is motivated by the availability of a suitable sampling procedure for SA using this prior [14]. It is to be noted, that the adaptation of the proposed methods to alternative priors, such as the uniform distribution over an interval [5] or a gamma distribution [27], is uncomplicated. This is discussed in Section 3.2.

3 Bayesian Estimation

Two Gibbs-samplers are implemented that correspond to AA and SA, respectively; both of them consist of sequentially drawing random values from two conditional posterior distributions. Above all, primary interest lies in how quickly the two resulting Markov chains mix, given different sets of observations; i.e., how close the posterior sample for is to a set of independent draws. In particular, fast mixing is a desirable requirement for any MCMC procedure. [40] discuss several measures for mixing and propose to minimize the expected augmented Fisher information matrix

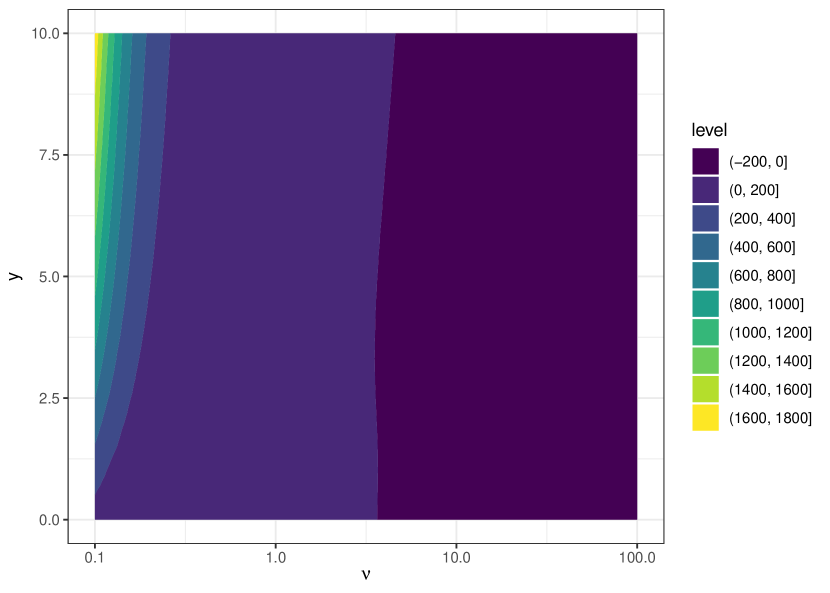

for choosing between DAs, where for SA and for AA. Although a simple derivation gives , where denotes the number of observations and is the digamma function, we have been unsuccessful at computing analytically. Fortunately, Monte Carlo (MC) estimation is possible. Figure 3 exemplifies the difference between the estimated and for data sets of size 1. The break even point (BEP) between AA and SA is at almost independently from ; that is where AA overtakes SA at this benchmark as increases.222For the evaluation of , a MC sample of length was simulated from using the algorithm in Section 3.2; next, is evaluated at points ; finally, the average of the values is taken to be the estimator for . The numerical second derivative of is approximated using Richardson’s extrapolation with 6 steps, which is implemented in the hessian function from the software package numDeriv [18].

The comparison of and through MC quickly becomes impractical for larger data sets. Therefore, an extensive computer simulation is conducted and empirical measurement of mixing is computed. Ideally, the latter is based on exact sampling from the four conditional posterior distributions.

3.1 Conditional Posterior Distributions

Given data points , the specification for is conditionally conjugate [15], and, therefore, sampling from is straightforward. Next, as [30] mention, sampling from can be reduced to sampling .

The rejection sampling (RS) method by [15] is employed for : denote by the unique solution to

where is a sufficient statistic. By finding , the normalizing constant in is estimated indirectly, which is necessary for RS. Then, a proposal is drawn from an exponential distribution with rate , and it is retained with probability

Last, we are unaware of exact sampling procedures for . A modern and easy-to-implement substitute is to employ adaptive Metropolis [[, AM;]]Haario2001 within Gibbs, which can be used to sample from any unnormalized density that can be evaluated. However, contrary to RS, AM produces an auto-correlated Markov chain, and therefore it is inferior to RS in our setup. As a simple improvement, independent sampling is approximated by repeating AM in one step of the Gibbs-sampler. Our implementation of AM proposes for the logarithm of through a Gaussian random walk with variance . Next, is accepted or rejected according to the Metropolis ratio . The proposal distribution is tuned to achieve the famous [11, 10, 34] by increasing or decreasing after batches of several hundred draws; this is similar to the examples by [35].

3.2 MCMC Algorithm

Following [15], Equation (2) naturally translates into the following MCMC scheme, henceforth termed algorithm SA, which simulates from the posterior distribution :

-

1.

Initialize ;

-

2.

Draw independently for each ;

-

3.

Draw , where using RS;

-

4.

Repeat Steps 2 and 3.

For alternative prior distributions, Step 3 can be replaced by AM as long as it is possible to evaluate the prior density function . This change may affect the mixing speed for two reasons: autocorrelation is introduced into the Markov chain, and might be altered.

Next, the two novel algorithms are introduced. Corresponding to Equation (3), algorithm AA samples from the posterior distribution ;

-

1.

Initialize ;

-

2.

Draw independently for each by first drawing and then computing [[, inspired by]]Papaspiliopoulos2007;

-

3.

Draw , where using AM; this step includes the evaluation of ; repeat this step times;

-

4.

Repeat Steps 2 and 3.

This is algorithm is trivially modified for other prior distributions: the Metropolis ratio needs to be adapted to the new prior density.

Finally, algorithm ASIS combines SA and AA:

-

1.

Initialize ;

-

2.

Do Steps 2 and 3 of SA;

-

3.

Compute for ;

-

4.

Do Step 3 of AA;

-

5.

Repeat Steps 2 through 4.

Notice that ASIS is not a sequence of SA and AA; is not sampled separately. Rather, focus lies on the differences between and , which are exploited in a minimal setup.

Correctness of the implementations for AA, SA, and ASIS is confirmed using a variant on Geweke’s test [17]. Specifically, if a new vector of observations is simulated at the end of every round of the particular algorithm, then the sampling distribution of is equivalent to its prior; and this is verified visually with the help of quantile-quantile-plots.

4 Simulation Study

In order to make a general comparison between the mixing of AA, SA, and ASIS, an extensive simulation study is conducted. To this end, the algorithms in Section 3.2 are implemented in the R language [32, version 4.1.0]. Then, multiple independent posterior Markov chains are generated for data simulated from Equation (1); for AA, is set. Next, convergence of the Markov chains is automatically validated by ensuring that their value [41] is smaller than the recommended ; this is done using the rhat function of the R package posterior \parencitesrposterior. Finally, relative numerical efficiencies [[, RNE;]]Geweke1989 of the chains are reported. RNE is defined for an identically distributed but serially correlated Monte Carlo sample and a function of interest as , where is a consistent estimator for the variance of the distribution and is a consistent estimator for the spectral density of , .333RNE is the reciprocal of the inefficiency factor reported in other works \parencitesNakajima2009a. This computation is implemented in function effectiveSize from the coda package [31].

4.1 Setup of Data Generating Process

A grid of true values and data set lengths is considered for the comparison. This covers “realistic” values [[, ;]]Gelman2013a and both problematic regions of low and high degrees of freedom. Moreover, dependence on the size of the data set can be evaluated. Then, for each of the 99 setups, five data sets are simulated from Equation (1). Furthermore, to examine prior sensitivity, values are considered, which correspond to prior expectations of through for . In addition, following the recommendations for the computation of , four independent Markov chains are simulated with initial values (these receive the same during post-processing), for each of the three algorithms and each setup. Overall, samples of length are drawn after a burn-in phase of length , and samples with are removed.

4.2 Posterior Estimates

A sample of interval estimators for is presented in Table 1 for and . With the exception of two cells, the estimates by AA, SA, and ASIS are similar for all values of . The twin of these exceptions is an example of a general caveat about AA: for a long vector of heavy-tailed observations, the numerical evaluation of may fail within AA; especially for values at the outskirts of the posterior distribution. The issue materializes as a constant estimator in Table 1.444 Our implementation for is based on the built-in R function qgamma. Typically, the Markov chain is constant in these settings because the MH step always rejects; in all other settings, AA is reliable. Consequently, by choosing (our implementation of) AA, one assumes a complex restriction on the prior distribution . Moreover, the three rows for provide two further insights. First, obviously, even at sample size , most of the posterior mass is closer to the prior expectation of than to 100; indeed, the prior choice is quite influential compared to the flat likelihood for light-tailed data. Second, the variation in the estimates from SA is the largest in this row both in relative and in absolute terms; the quantile ranges between and . This sheds light on the outstandingly deteriorating effectiveness of SA as increases; this is discussed in Section 4.3. As a result, its finite sample properties make SA less reliable for estimating a large . Importantly, ASIS does not suffer from any of the aforementioned issues; indeed, it combines the best of both worlds.

| Initial | 2 | 10 | 100 | ||

|---|---|---|---|---|---|

| AA | |||||

| SA | |||||

| 1 | ASIS | ||||

| AA | |||||

| SA | |||||

| 2 | ASIS | ||||

| AA | |||||

| SA | |||||

| 5 | ASIS | ||||

| AA | |||||

| SA | |||||

| 20 | ASIS | ||||

| AA | |||||

| SA | |||||

| 100 | ASIS |

4.3 Sampling Efficiency

Detailed results are presented in Table 2. In most cases of practical interest, i.e., where the observations have finite variance by assumption, the RNE of AA is at least comparable to that of the classical SA; and, for lighter-tailed inputs, AA is incomparably more efficient. Nevertheless, as discussed in Section 4.2, AA may fail; these cases are marked as missing values in Table 2. In particular, AA breaks down for the combination of a data set of length simulated with , and a chain with initialization ; however, apparent from the results, lighter-tailed data sets may be increasingly affected as their size grows. On the other hand, AA is reliable in all other settings. Luckily, ASIS proves to be a solution in this regard, as SA does not suffer from the issue; therefore, the chain can move out of this initial bad region. Moreover, ASIS outperforms both AA and SA in all setups. Even an RNE of 100% is reached for the small , which is measurably on par with an i.i.d. sample.

| 1.5 | 2 | 2.5 | 3 | 4 | 5 | 10 | 20 | 50 | 100 | |||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 23.2 | 39.6 | 53.1 | 63.9 | 70.2 | 77.6 | 81.7 | 87.7 | 90.1 | 90.9 | 91.1 | ||

| 100 | 4.3 | 15.4 | 22.0 | 30.5 | 38.2 | 45.5 | 51.6 | 60.4 | 68.0 | 70.9 | 71.3 | |

| 1000 | - | - | 23.3 | 29.9 | 36.3 | 43.7 | 48.1 | 45.1 | 39.3 | 44.4 | 46.6 | |

| AA | 10000 | - | - | - | - | 37.3 | 43.2 | 48.9 | 45.3 | 28.4 | 21.8 | 24.5 |

| 10 | 45.5 | 31.8 | 25.7 | 22.5 | 21.2 | 19.8 | 19.5 | 19.2 | 19.7 | 19.8 | 19.8 | |

| 100 | 45.4 | 32.7 | 24.7 | 19.2 | 15.4 | 10.0 | 7.2 | 4.4 | 4.0 | 3.9 | 3.9 | |

| 1000 | 44.4 | 31.3 | 23.2 | 17.8 | 14.2 | 9.5 | 6.8 | 2.2 | 1.0 | 0.9 | 0.9 | |

| SA | 10000 | 44.6 | 31.5 | 23.5 | 18.2 | 14.5 | 9.9 | 7.1 | 2.3 | 0.7 | 0.3 | 0.2 |

| 10 | 76.7 | 80.8 | 86.0 | 90.4 | 93.1 | 95.3 | 96.8 | 99.4 | 99.8 | 100.6 | 100.6 | |

| 100 | 63.1 | 59.5 | 58.9 | 60.4 | 62.1 | 65.5 | 65.4 | 68.3 | 73.5 | 74.3 | 76.1 | |

| 1000 | 63.0 | 60.3 | 60.6 | 61.6 | 63.1 | 64.1 | 64.1 | 49.6 | 40.9 | 45.3 | 48.0 | |

| ASIS | 10000 | 62.5 | 59.7 | 60.5 | 62.0 | 63.3 | 65.3 | 64.4 | 50.0 | 29.3 | 21.9 | 25.1 |

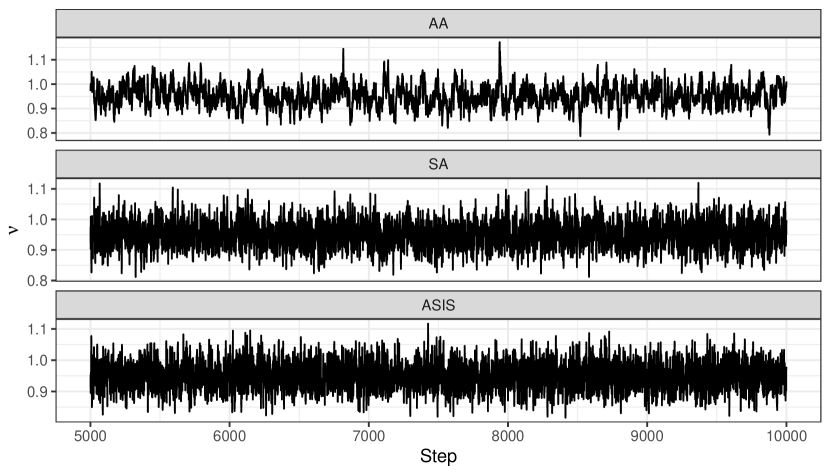

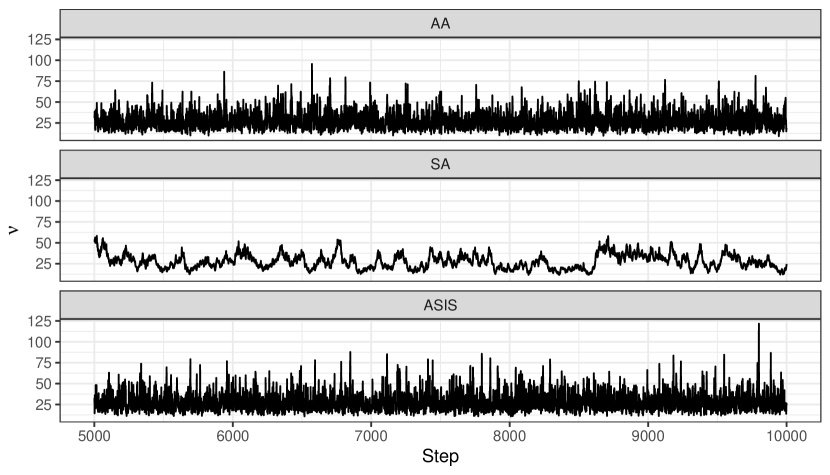

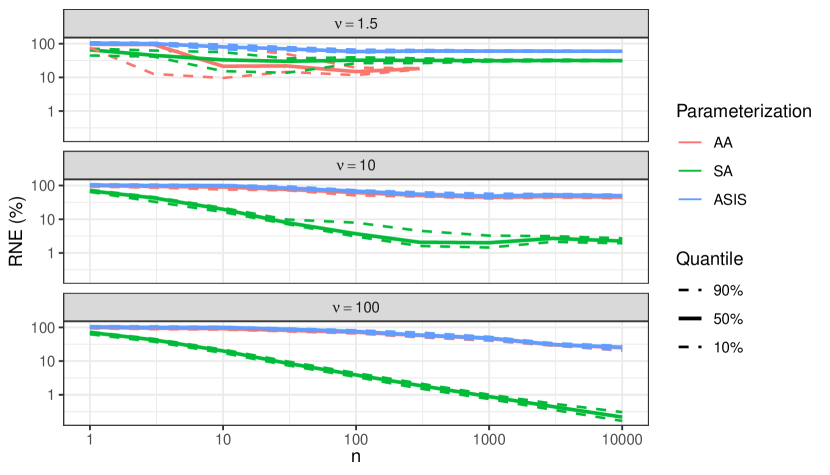

Some further results are highlighted using visualizations. First, Figure 4 is a demonstration of the differences between AA, SA, and ASIS using trace plots: these are shown for hand-picked but representative examples. The top three panels correspond to very heavy-tailed input data () and a good initialization for AA; SA and ASIS mix quickly, but AA seems to slightly lag behind. In contrast, the bottom three panels represent the case of a light-tailed input vector (); now, AA and ASIS show good performance, but SA is highly ineffective.

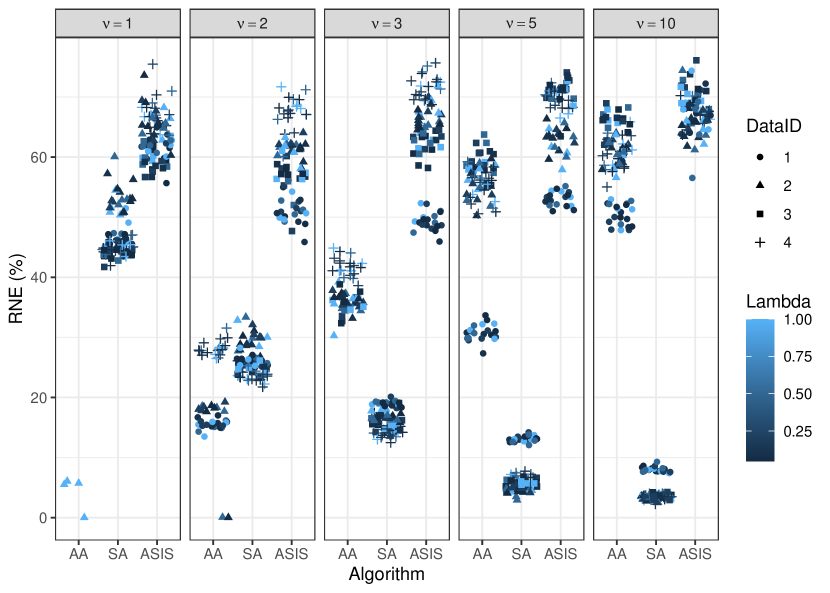

Next, Figure 5 depicts a sample of RNE values conditional on the algorithm, , , and the simulated data set; for improved readability, the plot is restricted to , , and four out of five data sets. Clearly, the sampling efficiency strongly depends on the exact properties of the observations. For instance, the data set with is an outlier in the panel for ; and the reason for the comparably poor performance of AA is the extreme outlier contained in the data. Similar behavior can be observed in the rightmost panel for , which is due to the same random seed being used for generating data sets with the same . Further, at this sample size, does not affect RNE. Indeed, there is no clustering of colors in any of the 15 columns. Since cancels out in the Fisher information, this speaks for the similarity between RNE and or . In summary, part of the conclusion of Figure 5 is consistent with that of Figure 3: SA outperforms AA only for particularly heavy-tailed input data. However, the data do affect the BEP, which, in addition, comes at a lower than the aforementioned value 4: between 2 and 3. Finally and most importantly, ASIS is immune to both the numerical issues of AA and the quickly deteriorating efficiency of SA.

The significance of ASIS becomes even more apparent through Figure 6. A summary of RNE is displayed for AA, SA, and ASIS, as it decreases with increasing and . Above all, the larger is, the greater the difference between the slopes for SA and ASIS. Based on the bottom panel, one may hypothesize that the RNE of SA is linearly proportional to for light-tailed input; this should be connected to the multiplicative term in . Finally, for the last time, the dominance of ASIS is conspicuous.

5 Application

The efficiency of ASIS is evaluated on an extension of the 14 U.S. macroeconomic time series by [28] as part of the model specified by \textcitesGeweke1992,Geweke1993,Geweke1994a; these three closely connected publications are followed in this section. The data set can be downloaded with the R package tseries \parencitesrlang2021,tseries2020.555The data set was formerly stored in the data archive of the Journal of Business and Economic Statistics, currently at http://korora.econ.yale.edu/phillips/data/np&enp.dat. The observation series are annual, they start between 1860 and 1909, and all end in 1988.

5.1 Model Specification

The model is a re-parameterized auto-regressive linear model of lag five with a time trend and Student- increments, and, as highlighted by [15], it is an alternative to the specifications employed by [28] and others. To underline the time-series nature of the data set, index is used in this section instead of . Formally, observations for are assumed to be explained through

| (5) |

where is the lag operator, is the intercept, is the slope of the main time trend, and the series stands for the cyclic deviations from the trend. The cycle is assumed to vary according to the fifth degree polynomial specification for with parameters and .

Following [15], the following prior distributions are assumed;

| (6) |

where is the first observation and it is not included in (5), and is the indicator function that takes for and otherwise. These prior distributions are in line with the hypotheses in the original work, where the model is employed with Gaussian increments () to show that business cycles deviate from a linear time trend in a non-stationary manner. Finally, Equation (4) is adopted for with .

A variant on the algorithm by [15] is implemented;

-

1.

Initialize as the ordinary least squares (OLS) estimate (enforcing the bounds for if needed), as the sample variance given the OLS estimates, , and ;

-

2.

Draw given all other variables from a bivariate normal distribution;

-

3.

Draw given all other variables from a multivariate normal distribution;

-

4.

Draw given all other variables from a non-standard distribution using rejection sampling;

-

5.

Draw and (for SA), (for AA), or both (for ASIS) given all other variables as in Section 3.2; note that is a sufficient statistic;

-

6.

Draw given all other variables from a scaled inverse-chi-square distribution with degrees of freedom.

Our modification only affects Step 5, where the method described in Section 3 is applied. The exact distributions and methods of the remaining steps can be found in \textcitesGeweke1993 and in the software code as part of the Supplementary Material.

Similarly to Section 3.2, correctness of our implementations for Steps 1-5 is ensured through Geweke’s test [17]; the prior distributions are recovered by simulating data from Equation (5) at the end of each pass. This does not work for Step 6 due to being improper. There, the empirical quantile function of the conditional posterior distribution is compared to the theoretical quantile function.

5.2 Posterior Estimates

For all 14 variables, a posterior sample of size is drawn after a burnin of passes using AA, SA, and ASIS, resulting in 42 Markov chains; after the verification of convergence through trace plots, these numbers are considered to be adequate. There were no numerical issues with the computation of as part of AA.

Estimated posterior distributions are summarized in Table 3. The three algorithms largely agree on the results, and there do not seem to be systematic biases present. The figures suggest highly heavy-tailed posterior distributions for in all cases, given the prior information. Median values range between approximately and , and, therefore, they fall on both sides of the previously measured BEP’s.

| Median | 80% Credible Interval | |||||

|---|---|---|---|---|---|---|

| AA | SA | ASIS | AA | SA | ASIS | |

| CPI | ||||||

| Employment | ||||||

| GNP Deflator | ||||||

| Industrial Production | ||||||

| Interest Rate | ||||||

| Money Stock | ||||||

| Nominal GNP | ||||||

| Real GNP | ||||||

| Real per Capita GNP | ||||||

| Real Wages | ||||||

| Stock Prices | ||||||

| Unemployment Rate | ||||||

| Velocity | ||||||

| Wages | ||||||

5.3 Sampling Efficiency

RNE of all chains is reported in Table 4. Parallels can be found to Table 2: AA is most efficient compared to SA for large posterior medians. Although other parts of the Gibbs sampler also affect the figures, the median seems to be a strong factor in the ratio between the RNE’s of AA and SA. In both columns, the lowest value belongs to Interest Rate, and one of the largest to Stock Prices, respectively. Moreover, the two columns predominantly stay close in magnitude.

| RNE (%) | |||||

|---|---|---|---|---|---|

| AA | SA | ASIS | AA / SA | Median | |

| CPI | 11.1 | 4.7 | 13.2 | 2.4 | |

| Employment | 10.6 | 2.8 | 10.3 | 3.7 | |

| GNP Deflator | 14.6 | 8.0 | 19.9 | 1.8 | |

| Industrial Production | 12.7 | 3.2 | 12.6 | 3.9 | |

| Interest Rate | 7.7 | 6.6 | 7.9 | 1.2 | |

| Money Stock | 20.3 | 4.4 | 23.9 | 4.6 | |

| Nominal GNP | 13.8 | 7.3 | 18.0 | 1.9 | |

| Real GNP | 13.8 | 4.3 | 13.1 | 3.2 | |

| Real per Capita GNP | 10.7 | 4.0 | 11.6 | 2.7 | |

| Real Wages | 27.6 | 4.5 | 31.5 | 6.1 | |

| Stock Prices | 35.4 | 5.8 | 40.4 | 6.1 | |

| Unemployment Rate | 14.7 | 4.2 | 14.0 | 3.5 | |

| Velocity | 14.9 | 3.0 | 14.4 | 5.0 | |

| Wages | 9.3 | 4.6 | 11.9 | 2.0 | |

6 Discussion

In this paper, efficient Bayesian estimation of the degrees of freedom parameter for the Student- distribution is investigated. Specifically, the mixing speed of AA and SA is compared through various methods: an estimate for the expected augmented Fisher information, an extensive simulation study, and a suitable application. AA is found to be beneficial both for real-world data and in most synthetic setups. However, for extreme starting values, AA is found to be completely unreliable.

As a solution, ASIS is proposed to combine the good parts of AA and SA. It is found to be as efficient as the better of AA and SA and also invulnerable compared to AA. Moreover, ASIS is easy to implement as soon as AA and SA have been derived.

Lastly, it is to be highlighted that the prime interest of the present work is the simulation-based description of the mixing speed of algorithms AA, SA, and ASIS. In particular, the results are helpful for understanding the effect of re-parameterization on sampling efficiency, which is independent from execution time. Therefore, optimization for effective sampling rate, which is a runtime-adjusted variant of RNE, and, granted, which is of most relevance to end users but is highly dependent on many factors [22], is not considered in the paper at hand. One would almost certainly turn away from rejection sampling nowadays and rather experiment with other modern methods. This remains for future research.

Acknowledgement

We would like to thank Gregor Kastner for useful suggestions and helpful comments.

References

- [1] James H. Albert and Siddhartha Chib “Bayesian Analysis of Binary and Polychotomous Response Data” In Journal of the American Statistical Association 88.422, 1993, pp. 669–679 DOI: 10.1080/01621459.1993.10476321

- [2] Angela Bitto and Sylvia Frühwirth-Schnatter “Achieving Shrinkage in a Time-Varying Parameter Model Framework” In Journal of Econometrics 210.1 Elsevier B.V., 2019, pp. 75–97 DOI: 10.1016/j.jeconom.2018.11.006

- [3] Tim Bollerslev “A Conditionally Heteroskedastic Time Series Model for Speculative Prices and Rates of Return” In The Review of Economics and Statistics 69.3, 1987, pp. 542 DOI: 10.2307/1925546

- [4] Paul-Christian Bürkner, Jonah Gabry, Matthew Kay and Aki Vehtari “posterior: Tools for Working with Posterior Distributions”, 2021 URL: https://mc-stan.org/posterior/

- [5] Siddhartha Chib, Federico Nardari and Neil Shephard “Markov Chain Monte Carlo Methods for Stochastic Volatility Models” In Journal of Econometrics 108.2, 2002, pp. 281–316 DOI: 10.1016/S0304-4076(01)00137-3

- [6] Siddhartha Chib, Jacek Osiewalski and Mark F.J. Steel “Posterior Inference on the Degrees of Freedom Parameter in Multivariate Regression Models” In Economics Letters 37.4, 1991, pp. 391–397 DOI: 10.1016/0165-1765(91)90076-W

- [7] Bruno de Finetti “The Bayesian Approach to the Rejection of Outliers” In Proceedings of the Berkeley Symposium on Mathematical Statistics and Probability 4.1, 1961, pp. 199–210

- [8] Donald A.. Fraser “Necessary Analysis and Adaptive Inference” In Journal of the American Statistical Association 71.353, 1976, pp. 99–110 DOI: 10.1080/01621459.1976.10481486

- [9] Andrew Gelman et al. “Models for Robust Inference” In Bayesian Data Analyais New York: ChapmanHall/CRC, 2013, pp. 435–447 DOI: 10.1201/b16018

- [10] Andrew Gelman, Walter R. Gilks and Gareth Owen Roberts “Weak Convergence and Optimal Scaling of Random Walk Metropolis algorithms” In The Annals of Applied Probability 7.1, 1997 DOI: 10.1214/aoap/1034625254

- [11] Andrew Gelman, Gareth Owen Roberts and Walter R. Gilks “Efficient Metropolis Jumping Rules” In Bayesian Statistics 5 – Proceedings of the Fifth Valencia International Meeting Clarendon Press, Oxford, UK, 1994, pp. 599–607

- [12] Stuart Geman and Donald Geman “Stochastic Relaxation, Gibbs Distributions, and the Bayesian Restoration of Images” In IEEE Transactions on Pattern Analysis and Machine Intelligence 6.6, 1984, pp. 721–741 DOI: 10.1109/TPAMI.1984.4767596

- [13] John F. Geweke “Bayesian Inference in Econometric Models Using Monte Carlo Integration” In Econometrica 57.6, 1989, pp. 1317 DOI: 10.2307/1913710

- [14] John F. Geweke “Priors for Macroeconomic Time Series and Their Application”, 1992, pp. 1–52

- [15] John F. Geweke “Bayesian Treatment of the Independent Student- Linear Model” In Journal of Applied Econometrics 8.S1, 1993, pp. S19–S40 DOI: 10.1002/jae.3950080504

- [16] John F. Geweke “Priors for Macroeconomic Time Series and Their Application” In Econometric Theory 10.3-4, 1994, pp. 609–632

- [17] John F. Geweke “Getting It Right: Joint Distribution Tests of Posterior Simulators” In Journal of the American Statistical Association 99.467, 2004, pp. 799–804 DOI: 10.1198/016214504000001132

- [18] Paul Gilbert and Ravi Varadhan “numDeriv: Accurate Numerical Derivatives”, 2019 URL: https://cran.r-project.org/package=numDeriv

- [19] Heikki Haario, Eero Saksman and Johanna Tamminen “An Adaptive Metropolis Algorithm” In Bernoulli 7.2, 2001, pp. 223–242 DOI: 10.2307/3318737

- [20] Andrew C. Harvey, Esther Ruiz and Neil Shephard “Multivariate Stochastic Variance Models” In The Review of Economic Studies 61.2, 1994, pp. 247–264 DOI: 10.2307/2297980

- [21] Gregor Kastner and Sylvia Frühwirth-Schnatter “Ancillarity-Sufficiency Interweaving Strategy (ASIS) for Boosting MCMC Estimation of Stochastic Volatility Models” In Computational Statistics and Data Analysis 76 Elsevier B.V., 2014, pp. 408–423 DOI: 10.1016/j.csda.2013.01.002

- [22] Hans-Peter Kriegel, Erich Schubert and Arthur Zimek “The (Black) Art of Runtime Evaluation: Are We Comparing Algorithms or Implementations?” In Knowledge and Information Systems 52.2, 2017, pp. 341–378 DOI: 10.1007/s10115-016-1004-2

- [23] Kenneth L. Lange, Roderick J.A. Little and Jeremy M.G. Taylor “Robust Statistical Modeling Using the Distribution” In Journal of the American Statistical Association 84.408, 1989, pp. 881–896 DOI: 10.1080/01621459.1989.10478852

- [24] Chuanhai Liu “ML Estimation of the Multivariate Distribution and the EM Algorithm” In Journal of Multivariate Analysis 63.2, 1997, pp. 296–312 DOI: 10.1006/jmva.1997.1703

- [25] Karla Monterrubio-Gómez et al. “Posterior Inference for Sparse Hierarchical Non-stationary Models” In Computational Statistics and Data Analysis 148 Elsevier B.V., 2020, pp. 106954 DOI: 10.1016/j.csda.2020.106954

- [26] Jouchi Nakajima and Yasuhiro Omori “Leverage, Heavy-Tails and Correlated Jumps in Stochastic Volatility Models” In Computational Statistics and Data Analysis 53.6 Elsevier B.V., 2009, pp. 2335–2353 DOI: 10.1016/j.csda.2008.03.015

- [27] Jouchi Nakajima and Yasuhiro Omori “Stochastic Volatility Model with Leverage and Asymmetrically Heavy-Tailed Error Using GH Skew Student’s Distribution” In Computational Statistics and Data Analysis 56.11, 2012, pp. 3690–3704 DOI: 10.1016/j.csda.2010.07.012

- [28] Charles R. Nelson and Charles I. Plosser “Trends and Random Walks in Macroeconmic Time Series” In Journal of Monetary Economics 10.2, 1982, pp. 139–162 DOI: 10.1016/0304-3932(82)90012-5

- [29] Omiros Papaspiliopoulos and Gareth Owen Roberts “Stability of the Gibbs Sampler for Bayesian Hierarchical Models” In Annals of Statistics 36.1, 2008, pp. 95–117 DOI: 10.1214/009053607000000749

- [30] Omiros Papaspiliopoulos, Gareth Owen Roberts and Martin Sköld “A General Framework for the Parametrization of Hierarchical Models” In Statistical Science, 2007 DOI: 10.1214/088342307000000014

- [31] Martyn Plummer, Nicky Best, Kate Cowles and Karen Vines “CODA: Convergence Diagnosis and Output Analysis for MCMC” In R News 6.1, 2006, pp. 7–11

- [32] R Core Team “R: A Language and Environment for Statistical Computing”, 2021 R Foundation for Statistical Computing URL: https://www.r-project.org/

- [33] James O. Ramsay and Melvin R. Novick “PLU Robust Bayesian Decision Theory: Point Estimation” In Journal of the American Statistical Association 75.372, 1980, pp. 901–907 DOI: 10.1080/01621459.1980.10477570

- [34] Gareth Owen Roberts and Jeffrey S. Rosenthal “Optimal Scaling for Various Metropolis-Hastings Algorithms” In Statistical Science 16.4, 2001 DOI: 10.1214/ss/1015346320

- [35] Gareth Owen Roberts and Jeffrey S. Rosenthal “Examples of adaptive MCMC” In Journal of Computational and Graphical Statistics 18.2, 2009, pp. 349–367 DOI: 10.1198/jcgs.2009.06134

- [36] Radhey S. Singh “Estimation of Error Variance in Linear Regression Models with Errors Having Multivariate Student- Distribution with Unknown Degrees of Freedom” In Economics Letters 27.1, 1988, pp. 47–53 DOI: 10.1016/0165-1765(88)90218-2

- [37] Brajendra C. Sutradhar and Mir M. Ali “Estimation of the Parameters of a Regression Model with a Multivariate Error Variable” In Communications in Statistics - Theory and Methods 15.2, 1986, pp. 429–450 DOI: 10.1080/03610928608829130

- [38] Luke Tierney “Markov Chains for Exploring Posterior Distributions” In The Annals of Statistics 22.4, 1994, pp. 1701–1728 DOI: 10.1214/aos/1176325750

- [39] Adrian Trapletti and Kurt Hornik “tseries: Time Series Analysis and Computational Finance”, 2020 URL: https://cran.r-project.org/package=tseries

- [40] David A van Dyk and Xiao-Li Meng “The Art of Data Augmentation” In Journal of Computational and Graphical Statistics 10.1, 2001, pp. 1–50 DOI: 10.1198/10618600152418584

- [41] Aki Vehtari et al. “Rank-Normalization, Folding, and Localization: An Improved for Assessing Convergence of MCMC” In Bayesian Analysis Advance Publication, 2021, pp. 1–38 DOI: 10.1214/20-BA1221

- [42] Mike West “Outlier Models and Prior Distributions in Bayesian Linear Regression” In Journal of the Royal Statistical Society: Series B (Methodological) 46.3, 1984, pp. 431–439 DOI: 10.1111/j.2517-6161.1984.tb01317.x

- [43] Yaming Yu and Xiao-Li Meng “To Center or Not to Center: That Is Not the Question—An Ancillarity-Sufficiency Interweaving Strategy (ASIS) for Boosting MCMC Efficiency” In Journal of Computational and Graphical Statistics 20.3, 2011, pp. 531–570 DOI: 10.1198/jcgs.2011.203main

- [44] Arnold Zellner “Bayesian and Non-Bayesian Analysis of the Regression Model with Multivariate Student- Error Terms” In Journal of the American Statistical Association 71.354, 1976, pp. 400–405 DOI: 10.1080/01621459.1976.10480357