Precise option pricing by the COS method–How to choose the truncation range

Abstract

The Fourier cosine expansion (COS) method is used for pricing European options numerically very fast. To apply the COS method, a truncation range for the density of the log-returns need to be provided. Using Markov’s inequality, we derive a new formula to obtain the truncation range and prove that the range is large enough to ensure convergence of the COS method within a predefined error tolerance. We also show by several examples that the classical approach to determine the truncation range by cumulants may lead to serious mispricing. Usually, the computational time of the COS method is of similar magnitude in both cases.

Keywords: COS method, cosine expansion, option pricing, truncation range, Markov’s inequality

MSC 2010 Classification: 65T40, 42A10, 60E10, 91G20

1 Introduction

In mathematical finance the logarithmic price of a stock is usually modeled by a random variable . In many financial models the probability density function of exists but its precise structure is unknown. On the other hand the characteristic function of (that is, the Fourier transform of ) is often given explicitly, e.g. see models discussed in [8]. In this setting, it is necessary to compute integrals of the form

| (1) |

numerically as fast as possible, where is a function describing an insurance contract on a stock, like a call or put option, which for example protects the holder against a fall in the price of the stock. The integral is interpreted as the price of such an insurance contract. How can we compute the integral without knowing ? A straightforward, efficient and robust method to retrieve the density of a random variable from its characteristic function and to compute prices of call or put options is the COS method proposed by Fang and Oosterlee in their seminal work [8].

It is of utmost importance to price call and put options very fast because stock price models are typically calibrated to given prices of liquid call and put options by minimizing the mean-square-error between model prices and given market prices. During the optimization routine, model prices of call and put options need to be evaluated very often for different model parameters.

Under suitable assumptions, the COS method exhibits exponential convergence and compares favorably to other Fourier-based pricing techniques, see [8]. The COS method is widely applied in mathematical finance, see for instance [2, 9, 10, 12, 13, 26, 28], see [16, 17, 18] for an application of the COS method in a data-driven approach.

The main idea of the COS method is to approximate the density with infinite support on a finite range . The truncated density is then approximated by a (finite) cosine expansion. The integral (1) can then be approximated highly efficiently if describes the payoff of a put or call option and the characteristic function of is given in closed-form.

However, it is an open question how to choose the range in practice. In this article, we aim to give an answer. More precisely, given some tolerance , we derive the minimal length of the range such that the absolute difference of the approximation by the COS method and the integral in (1) is less than the tolerance.

Fang and Oosterlee [8] in Eq. (49), see also Eq. (6.44) in [22], proposed some rule of thumb based on cumulants to get an idea how to choose . In particular, they suggested

| (2) |

where , , , are the first, second, forth and sixth cumulants of . The parameter may be chosen by the user. If not stated otherwise, we use . In Section 4.3, we provide several examples where the COS method leads to serious mispricing if the truncation range is based on Equation (2). Note that there are also Fourier pricing techniques based on wavelets, see [23, 24], which do not relay on an a-priori truncation range.

This article is structured as follows: after reviewing the COS method in Section 2, we provide a new proof of convergence of the COS method using elementary tools of Fourier analysis in Section 3. Using Markov’s inequality, the proof allows us to derive a minimal length for the range given a pre-defined error tolerance. Numerical experiments and applications to model calibration can be found in Section 4. Section 5 concludes.

2 Review of the COS method.

Let be a probability density. The characteristic function of is defined by

| (3) |

Throughout the article, we assume to be centered around zero, that is , and we make no additional hypothesis on the support of . This assumption is mainly made to keep the notation simple. We summarize the approximation by the COS method proposed by [8], see also [22] for detailed explanations. For let . We define the following basis functions

and the classical cosine-coefficients of

Let . The density is approximated in three steps:

| (4) |

where indicates that the first summand (with ) is weighted by one-half, and we approximate the classical cosine-coefficients by an integral over the whole real line

The coefficients can be computed directly if the characteristic function of is given in closed-form.

Let be a (at least locally integrable) function. For denote

| (5) |

Then [8] observed that for large enough and replacing by its approximation (4) it holds

and called the approximation of the integral COS method.

Thus the density is approximated by a sum of cosine functions making use of the characteristic function to evaluate the cosine coefficients analytically. Working with logarithmic prices, call and put options can be described by truncated exponential functions and the cosine coefficients of call and put options can be obtained in explicit form as well. Therefore, option prices can be computed numerically highly efficiently.

3 A new framework for the COS method.

In this section, we revisit the convergence of the COS method. The proof allows us to derive a minimal length for the finite range , given some error tolerance between the integral and its approximation by the COS method.

Let and denote the sets of integrable and square integrable real-valued functions on , and by and we denote the scalar product and the norm on . We denote by the maximum value of two real numbers , .

Definition 1.

A function is called COS-admissible, if

Proposition 2.

Assume that with

then

and is COS-admissible.

Proof.

We have with

and it is sufficient to show . We will prove it for only, the proof for being almost identical.

Let . Using the classical cosine expansion of on the interval and Parseval’s identity we obtain

| (6) | ||||

Further, using the Cauchy-Schwarz inequality, we estimate

then

For one has , hence,

Hence, the assumption (2) implies . ∎

Corollary 3.

Let the density be bounded, with finite first and second moments, then is COS-admissible.

Corollary 3 already shows that the class of COS-admissible densities is very large. Next, we provide further sufficient conditions for COS-admissibility. In particular, we show that the densities of the stable distributions for stability parameter , including the Normal and the Cauchy distributions, and the density of the Pareto distribution are COS-admissible.

Corollary 4.

Let such that its characteristic function defined in (3) has a weak derivative satisfying . Then is COS-admissible.

Proof.

Example 5.

The densities of the stable distributions whose characteristic functions are of the form

for parameters , , and are COS-admissible by Corollary 4. Recall that this class includes the Normal and the Cauchy distributions.

Example 6.

The density of the Pareto distribution with scale and shape can be described by , for , and is COS-admissible. To see this, let as in Definition 1. It holds by integration by parts and using and , , that

Now we discuss the use of COS-admissible functions for the approximation of some integrals arising in mathematical finance. The next theorem shows that in particular a density with infinite support can be approximated by a cosine expansion.

Theorem 7.

Assume to be COS-admissible, then

Proof.

Let , , , , as in Section 2. Let . Recall that and for . Consider the cosine coefficients of the tails of , defined by

Then it holds , and it follows

Due to it holds . For each fixed one has as is square integrable on each . Further,

and as is COS-admissible.

Take any and choose such that and for all , then for all and all . For any , choose sufficiently large to have for all , then

which finishes the proof.∎

The next corollary shows that the integral (1) can be computed very efficiently if the characteristic function of and the classical cosine coefficients of are available in analytical form: this justifies the use of the COS method under some mild technical assumptions on the density and the function . The most important example in the applications for is the call option and the put option for some . The coefficients (5) can be obtained analytically for call and put options.

Corollary 8.

Let be COS-admissible and be locally in , that is,

| for any . |

Assume that , then the integral of the product of and can be approximated by a finite sum as follows.

Let and let and be such that

| (7) |

Let such that

| (8) |

and

| (9) |

Choose large enough so that

Then it holds for all

| (10) |

In the next corollary, we apply Corollary 8 to bounded functions and, given some , obtain explicit formulae for and such that the Inequalities (7), (8) and (9) hold. For example, put options are bounded. To find a lower bound for , we need to estimate the tail sum of . We apply Markov’s inequality to estimate the tail sum using the moment of .

If has semi-heavy tails, i.e. the tails of decay exponentially, all moments of exist and can be obtained by differentiating the characteristic function times. In a financial context, log-returns are often modeled by semi-heavy tails or lighter distributions: for instance the distribution of log-returns in the Heston model is between the exponential and the Gaussian distribution, see [7]. See [27] for an overview of Lévy models with semi-heavy tails. In particular, the Lévy process CGMY or the generalized hyperbolic processes, see [1], have semi-heavy tails.

We can find a suitable value of with the help of the bound for in Proposition 2. For some Lévy models, the density is given in closed-form, see [27], and can be estimated directly. In the next corollary, we propose to approximate the tails of by a density , which is given in closed-form. We suggest to use the Laplace density, which decays exponentially just like a density with semi-heavy tails. The (central) Laplace density has only one free parameter describing the variance. One can use a moment-matching method to calibrate the Laplace density , setting the variances corresponding to and equal.

The Laplace density with mean zero and variance () is given by

| (11) |

Corollary 9 (COS method, Markov range).

Let both the density and the function be bounded, with for all and some . For some even natural number assume the moment of exists and denote it by , i.e.

| (12) |

Let and

| (13) |

Assume there is some such that

| (14) |

Set

| (15) |

Choose large enough. Then it holds for all , that

| (16) |

Proof.

It holds by Markov’s inequality and the definition of

Hence Equation (7) is satisfied. Next we show Inequality (8) holds. Let as in Corollary 8. As is bounded by it holds . Using the upper bound (14) and the expressions (11) it follows

The second last inequality follows by the definition of and the last inequality holds as . Hence Inequality (8) is satisfied. To show that also Inequality (9) is respected, we use Proposition 2. It holds

Remark 10.

The original proof of the convergence of the COS method given in [8] is somewhat more restrictive compared to the results stated in Corollary 8 because it is assumed that the sum over the cosine coefficients of the payoff function is finite, i.e.,

| (17) |

see Lemma 4.1 in [8]. In particular, the cosine coefficients of a put option decay as , see Appendix A, and do not satisfy Equation (17). On the other hand, according to Corollary 9, put options can be priced very well by the COS method.

Remark 11.

Remark 12.

The smoother , the smaller may be chosen to obtain a good approximation, see [8] and references therein.

Remark 13.

The COS method has also been applied to price exotic options like Bermudan, American or discretely monitored barrier and Asian options, see [9, 10, 28]. One of the central idea when pricing these exotic options is the approximation of the density of the log returns by a cosine expansion as in Theorem 7. But some care is necessary when applying Corollary 8 to obtain a truncation range, because the truncation range also depends on the payoff function itself.

The COS method has been extended to the multidimensional case, see [26], using a heuristic truncation range similar to Equation (2). In a future research, we would like to generalize our results, in particular generalize Definition 1, Theorem 7 and Corollary 9, and derive a truncation range in a multidimensional setting.

4 Applications

In this section, we apply Corollary 9 to some stock price models. We use the following setting: let be a probability space. is a risk-neutral measure. Let be a positive random variable describing the price of the stock at time . The price of the stock today is denoted by . We assume there is a bank account paying continuous compounded interest . Let

| (18) |

be the centralized log-returns. is the expectation of the log-returns under the risk-neutral measure and can be obtained from the characteristic function of . Because the density of is centered around zero, it is justified to approximate the density of by a symmetric interval . In [8] a slightly different centralization of the log-returns has been considered. The characteristic function of is denoted by and the density of is denoted by . In this setting, the price of a put option is given by

| (19) |

where

| (20) |

We approximate the integral at the right-hand-side of Equation (19) by the COS method. The cosine coefficients of can be obtained in explicit form, see Appendix A or [8]. The price of a call option is given by the put-call parity.

There are two formulae to choose the truncation range for the COS method: the cumulants range, based on Equation (2) and the Markov range, based on Corollary 9. To obtain the former, one needs to compute the first, second and forth cumulants. Regarding the second, one need to compute the moment. We will see that , or represent a reasonable choice. The moment and the cumulant are similar concepts and can be obtained from the derivative of the characteristic function. In Sections 4.1 till 4.4 we compare both formulae under the following aspects:

-

•

How does the choice of the truncation range affect the number of terms ? Certainly the larger the range, the larger we have to set to obtain a certain precision.

-

•

Are there (important) examples where the COS method fails using the Markov or the cumulants truncation range?

-

•

How can we avoid to evaluate the derivative of the characteristic function to compute the moment or cumulant of the log-returns, each time we apply the COS method, for performance optimization?

In addition, we provide insights which moment to use for the Markov range and we will apply the Markov range to all models discussed in [8]. All numerical experiments are carried out on a modern laptop (Intel i7-10750H) using the software R and vectorized code without parallelization.

4.1 Black-Scholes and Laplace model

In the Black-Scholes model, see [3], is normally distributed. In the Laplace model, see [20], is Laplace distributed, see Equation (11) for the density of the Laplace distribution. Both distributions are simple enough such that the quantile functions are given explicitly. There are also closed-form solutions for the prices of call and put options under both models.

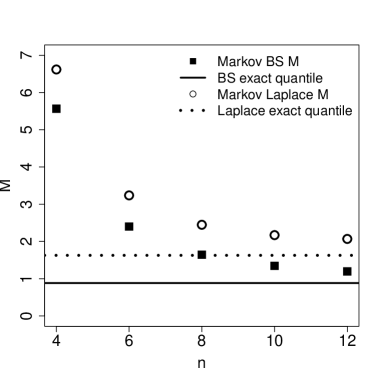

Figure 1 compares , defined by the moment of , see Equation (13), to the quantiles of . The higher , the sharper Markov’s inequality. At least for the Normal and Laplace distributions, good values for are obtained for . Using higher than the moment only marginally improves . If not stated otherwise, we will therefore use the moment to obtain the Markov truncation range for the COS method.

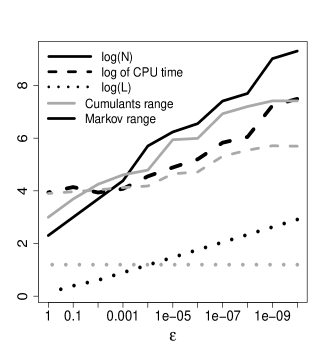

Consider an at-the-money call option on a stock with price today and with one year left to maturity. Assume the interest rates are zero. The left panel of Figure 2 displays over the error tolerance for the Markov and the cumulants range. The figure also shows the minimal value for such that the absolute difference of the true price of the option and the approximation of the price using the COS method is below the error tolerance . The the computational time to compute the option price by the COS method using steps is also indicated.

For a reasonable error tolerance, e.g. , the minimal value of to ensure the COS method is close enough to its reference price is at most twice as large using the Markov range instead of the cumulants range.

So using the Markov range based on the moment instead of the well-established cumulants range, at most doubles the computational time of the COS method for the same level of accuracy. We see a similar pattern for advanced stock price models, see Table 1.

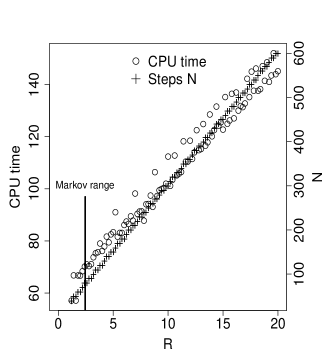

The right panel of Figure 2 shows the effect of size of the truncation range, which is between one and a hundred times the volatility , on the computational time of the COS method. Setting , we see a linear relationship between the size of the truncation range and the minimal value for to ensure convergence of the COS method for the Laplace model. The computational time is directly related to . Setting the truncation range too large, increases the computational time unnecessarily. Thus Corollary 9 may help to save computational time as well. For example, using the Markov range instead of , where is the volatility of the log-returns, reduces the computational time by more than a factor two.

|

|

| Panel A | Panel B |

4.2 Advanced models

Fang and Oosterlee, see [8], applied the COS method with the cumulants range to three advanced stock price models with different parameters, namely the Heston model, see [11], the Variance Gamma model (VG), see [19], and the CGMY model, see [5]. We repeat the empirical study using the Markov range instead.

Table 1 shows the minimal value of to ensure the approximation of the price of an option by the COS method is close enough to its reference price, which is taken from [8], for both truncation ranges. For those models, we conclude that using the Markov range based on the moment and an error tolerance of instead of the cumulants range, increases by about the factor and by about the factor . (Using the moment for the Markov range and an error tolerance of increases and by about the factor four). The terms directly determine the computational time of the COS method.

| Model |

Para-

meters |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Heston | 4 | 8 | 3.4 | 9.4 | 220 | 580 | 216 | 387 | ||

| Heston | 4 | 4 | 3.4 | 12 | 120 | 420 | 171 | 318 | ||

| Heston | 4 | 8 | 11.1 | 28 | 130 | 280 | 187 | 319 | ||

| Heston | 4 | 4 | 11.1 | 39.6 | 80 | 260 | 154 | 269 | ||

| VG | 4 | 8 | 0.8 | 2.3 | 630 | 950 | 242 | 326 | ||

| VG | 4 | 4 | 0.8 | 2.9 | 80 | 360 | 89 | 167 | ||

| VG | 4 | 8 | 1.9 | 4.3 | 100 | 190 | 80 | 103 | ||

| VG | 4 | 4 | 1.9 | 6.9 | 40 | 150 | 68 | 88 | ||

| CMGY | 4 | 8 | 5.6 | 12.5 | 110 | 230 | 113 | 153 | ||

| CMGY | 4 | 4 | 5.6 | 21.1 | 60 | 220 | 87 | 136 | ||

| CGMY | 4 | 8 | 13.4 | 32.9 | 40 | 100 | 89 | 100 | ||

| CGMY | 4 | 4 | 13.4 | 62.4 | 30 | 130 | 75 | 108 | ||

| CGMY | 4 | 8 | 98 | 254.6 | 40 | 100 | 81 | 102 | ||

| CGMY | 4 | 4 | 98 | 484.3 | 30 | 140 | 71 | 108 | ||

| MJD | M1 | 4 | 8 | 0.9 | 4 | 390 | 164 | |||

| MJD | M1 | 6 | 8 | 2.8 | 4 | 270 | 390 | 128 | 164 | |

| MJD | M2 | 6 | 8 | 5.8 | 18.2 | 5750 | 1444 | |||

| CGMY | M3 | 4 | 8 | 1.5 | 9 | 1990 | 658 | |||

| Heston | M4 | 2 | 8 | 1.3 | 3.7 | 190 | 211 |

4.3 Examples where COS method diverges

In the Merton jump diffusion model (MJD), see [21], which is a generalization of the Black-Scholes model, the stock price is modeled by a jump-diffusion process: the number of jumps are modeled by a Poisson process with intensity , i.e. the expected number of jumps in the time interval is . The instantaneous variance of the returns, conditional on no arrivals of jumps, is given by . The jumps are log-normal distributed. The expected percentage jump-size is described by . The variance of the logarithm of the jumps is described by .

For model M1 we choose

and for model M2, we set

For both models we set and and analyze a call option with strike .

Under the Merton jump diffusion model the characteristic function and the density of the log-returns and pricing formulae for put and call option are given in closed-form in terms of an infinite series. We use the first one hundred terms of that series to obtain reference prices for model M1 and M2 and we also apply the Carr-Madan formula, see [6], to confirm the reference prices.

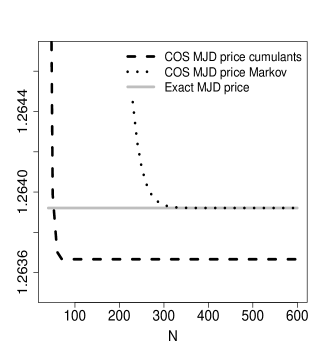

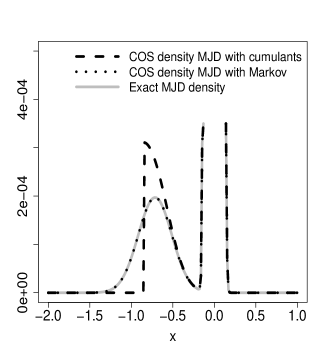

The left panel of Figure 3 shows the reference price of a call option under model M1 and the prices using the COS method with the truncation range based on cumulants ( using four cumulants) and Markov’s inequality ( using the moment). An application of Corollary 9 provides a satisfactory result. However, we clearly see the approximation of the price by the COS method does not converge properly using the cumulants range. The relative error is about two basis points (BPS), a significant difference, independent how large we choose . The cumulants range is too short and does not fully capture the second mode (the jump) of the MJD density, as shown by the right panel of Figure 3.

Next we test the cumulants range with six cumulants for the MJD model. The truncation range using six cumulants for model M1 is large enough to ensure the convergence of the COS model, see Table 1. But the cumulants range with six cumulants applied to model M2 is and is not large enough to ensure convergence within the required precision (). Why? If a jump occurs, the expected jump size of the log-returns is equal to

which is not inside the interval . Hence, again, the second mode of the density, i.e. the jump, is not fully captured by the truncation interval based on six cumulants. We report the prices for model M2 using different numeric approximations

The price is obtained by the closed-form solution of the call price in terms of an infinite series using the first one hundred terms. is obtained by the Carr-Madan formula where the damping-factor is set to , we use points and the truncated Fourier domain is set to . is obtained by the COS method with terms and using the moment and to obtain the truncation range. is obtained by the COS method also with terms and using six cumulants to obtain the truncation range.

Model M3 is a CGMY model with parameters and . Consider an at-the-money call option on a stock with price today and with years left to maturity. Assume the interest rates are zero. Using the cumulative range with four cumulants, the relative error of the approximation by the COS method and the reference price is about one basis point, a significant difference, see Table 2, and does not improve when increasing .

Model M4 is the Heston model with the following parameters: speed of mean-reversion , level of mean-reversion , vol of vol , initial vol and correlation . Consider an at-the-money call option on a stock with price today and with years left to maturity. Assume the interest rates are zero. Set .

Using the cumulative range based only on the second cumulant, the truncation range is and the price of the option by the COS method is .

On the other hand, is the price of the option based on the Markov range, which is . We used . Using a larger does not change the first three digits of the prices anymore. We also applied the Carr-Madan formula to confirm the price .

|

|

| Panel A | Panel B |

| Terms N | Markov abs. error | Cumul. abs. error | Markov rel. error in BPS | Cumul. rel. error in BPS |

|---|---|---|---|---|

4.4 Application to model calibration

Usually, one proceeds as follows to calibrate a stock price model, like the Heston model, to real market data: given a set of market prices of put and call options, minimize the mean square error between market prices of the options and the corresponding prices predicted by the model. During the optimization phase, model prices need to be computed very often, e.g. by the COS method.

We assume the model is described by parameters. Let be the smallest and largest maturity of the put and call options, respectively let be the space of feasible parameters of the model.

Let be the centralized log returns for the parameter and maturity . To compute the price of a put or call option with strike by the COS method via Corollary 9, we need to estimate the moment

to obtain an estimate for the truncation range of the density of . The moment could directly be determined by differentiating the characteristic function exactly times using a computer-algebra-system.

In general, evaluating the derivative of a characteristic function each time the COS method is called, might slow down the total calibration time significantly because the derivative of the characteristic function of some models can be very involved. For fixed , we therefore let

In the case of the Heston model, the function is continuous, see Lemma 1 in [25]. We propose to identify a function as an approximation of upfront before the calibration procedure. The evaluation of is expected to be fast. One might for example obtain for a (large) sample in and defined by a non-linear regression.

Training to the sample takes some time but need to be done only once. The idea is to use as an approximation of to obtain the truncation range via Corollary 9. Even if is only a rough estimate of the moment, we expect this approach to work well because Markov’s inequality usually overestimates the tail sum, which provides us with a certain “safety margin”.

We illustrate this idea for the Heston model. First, we define for the Heston model, which has five parameters: the speed of mean reversion , the mean level of variance , the volatility of volatility , the initial volatility and the correlation . We assume

We randomly choose values in and compute for each of those values by a Monte Carlo simulation. (The derivative of the characteristic function of the Heston model is extremely involved).

Then we train a small random forest, see [4], consisting of decisions trees. We choose a random forest for interpolation because the calibration is straightforward. We are confident that other interpolation methods, e.g. based on neural networks, produce similar results.

Next, we define a test set and choose values in randomly. [15] calibrated the Heston model to a time series of time points in Summer 2017 of real market data of put and call options, including calm and more volatile trading days. We add those parameters to our test set with a maturity of half a year.

For each parameter set, we compute a reference price333We computed the reference price by the COS method using an approximating range two times larger than the Markov range and terms. We verified the reference price by the Carr-Madan formula, where the damping-factor is set to , we use points and the truncated Fourier domain is set to . of three call options with strikes . We choose , and .

We obtain very satisfactory results approximating prices of call options by the COS method if the truncation range is obtained via Corollary 9, where the moment is estimated by the random forest . The maximal absolute error for the market data test set over all options is less than for . The maximal absolute error for the random test set is less than for .

Last we comment on the CPU time: computing one option price by the COS method for takes about microseconds using the software R and vectorized code without parallelization. To evaluate on parameter sets using R’s package randomForest, also without parallelization, takes on average microseconds per set.

5 Conclusions

The COS method is used to compute certain integrals appearing in mathematical finance by efficiently retrieving the probability density function of a random variable describing some log-returns from its characteristic function. The main idea is to approximate a density with infinite support on a finite range by a cosine series.

We provided a new framework to prove the convergence of the COS method, which enables us to obtain an explicit formula for the minimal length of the truncation range, given some maximal error tolerance between the integral and its approximation by the COS method.

The formula for the truncation range is based on Markov’s inequality and it is assumed that the density of the log-returns has semi-heavy tails. To obtain the truncation range, we need the moment of the (centralized) log-returns. The larger , the sharper Markov’s inequality. From numerical experiments, we concluded that , or even is a reasonable choice.

The moment could directly be determined from the derivative of the characteristic function. In the case of the Heston model, the characteristic function is too involved and instead we successfully employed a machine learning approach to estimate the moment.

Acknowledgments

We thank two anonymous referees for many valuable comments and suggestions enabling us to improve the quality of the paper.

Appendix A Cosine-coefficients for a put option

Define as in Equation (18) to compute the price of a put option with strike by the COS method using Markov’s inequality for the truncation range. The characteristic function of is given by

where the expectation can be computed from the characteristic function of by

Compute moment of with tricks from Section 4.4 or by

Choose and set and as in Equations (13) and (15). Let

If , compute the cosine-coefficients of , defined in Equation (20), by

and can be computed easily:

and

Choose large enough and set

Then it holds for the price of a European put option

where indicates that the first term in the summation is weighted by one-half. The price of a call option can be computed using the put-call parity.

References

- [1] J. Albin and M. Sundén, On the asymptotic behaviour of Lévy processes, Part I: Subexponential and exponential processes. Stoch Process Their Appl 119(1) (2009) 281–304.

- [2] C. Bardgett, E. Gourier, M. Leippold, Inferring volatility dynamics and risk premia from the S&P 500 and VIX markets. J. Finance Econ. 131 (2019) 593–618.

- [3] F. Black, M. Scholes, The pricing of options and corporate liabilities. J. Polit. Econ. 81(3) (1973) 637–654.

- [4] L. Breiman, Random forests. Mach. Learn. 45(1) (2001) 5–32.

- [5] P. P. Carr, H. Geman, D. B. Madan, M. Yor, The fine structure of asset returns: An empirical investigation. J. Bus. 75(2) (2002) 305–332.

- [6] P. P. Carr, D. P. Madan, Option valuation using the fast Fourier transform. J. Comput. Financ 2(4) (1999) 61–73.

- [7] A. A. Drǎgulescu, V. M. Yakovenko, Probability distribution of returns in the Heston model with stochastic volatility. Quant Finance 2(6) (2002) 443–453.

- [8] F. Fang, C. W. Oosterlee, A novel pricing method for European options based on Fourier-cosine series expansions. SIAM J. Sci. Comp. 31 (2009) 826–848.

- [9] F. Fang, C. W. Oosterlee, Pricing early-exercise and discrete barrier options by Fourier-cosine series expansions. Num. Math. 114 (2009) 27–62.

- [10] F. Fang, C. W. Oosterlee, A Fourier-based valuation method for Bermudan and barrier options under Heston’s model. SIAM J. Fin. Math. 2 (2011) 439–463.

- [11] S. L. . Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6(2) (1993) 327–343.

- [12] L. A. Grzelak, C. W. Oosterlee, On the Heston model with stochastic interest rates. SIAM J. Fin. Math. 2 (2011) 255–286.

- [13] A. Hirsa, Computational methods in finance. CRC Press, 2012.

- [14] L. Hörmander, The analysis of linear partial differential operators I. Distribution theory and Fourier analysis. 2nd edition. Springer-Verlag, 1990.

- [15] G. Junike, W. Schoutens, H. Stier, Performance of advanced stock price models when it becomes exotic: an empirical study. Ann. Financ. (2021), https://doi.org/10.1007/s10436-021-00396-2.

- [16] Á. Leitao, C. W. Oosterlee, L. Ortiz-Gracia, S. M. Bohte, On the data-driven COS method. Appl. Math. Comput. 317 (2018) 68–84.

- [17] S. Liu, A. Borovykh, L. A. Grzelak, C. W. Oosterlee, A neural network-based framework for financial model calibration. J. Math. Ind. 9(1) (2019) 1–28.

- [18] S. Liu, C. W. Oosterlee, S. M. Bohte Pricing options and computing implied volatilities using neural networks. Risks 7(1) (2019) 1–22.

- [19] D. B. Madan, P. P. Carr, E. C. Chang, The variance gamma process and option pricing. Rev. Financ. 2(1) (1998) 79–105.

- [20] D. B. Madan, Adapted hedging. Ann. Financ. 12(3) (2016) 305–334.

- [21] R. C. Merton, Option pricing when underlying stock returns are discontinuous. J. Financ. Econ. 3(1-2) (1976) 125–144.

- [22] C. W. Oosterlee, L. A. Grzelak, Mathematical Modeling and Computation in Finance: With Exercises and Python and Matlab Computer Codes. World Scientific, 2020.

- [23] L. Ortiz-Gracia, C. W. Oosterlee, Robust pricing of European options with wavelets and the characteristic function, SIAM J. Sci. Comp. 35(5) (2013) B1055-B1084.

- [24] L. Ortiz-Gracia, C. W. Oosterlee, A highly efficient Shannon wavelet inverse Fourier technique for pricing European options, SIAM J. Sci. Comp. 38(1) (2016) B118–B143.

- [25] P. Ruckdeschel, T. Sayer, A. Szimayer, Pricing American options in the Heston model: a close look at incorporating correlation. J. Deriv. 20(3) (2013) 9–29.

- [26] M. J. Ruijter, C. W. Oosterlee, Two-dimensional Fourier cosine series expansion method for pricing financial options. SIAM J. Sci. Comp. 34 (2012) B642–B671.

- [27] W. Schoutens, Lévy processes in finance: pricing financial derivatives. Wiley, 2003.

- [28] B. Zhang, C. W. Oosterlee, Efficient pricing of European-style Asian options under exponential Lévy processes based on Fourier cosine expansions. SIAM J. Fin. Math. 4 (2013) 399–426.