appReferences \newdatedraftdate15082022 \usdate

Costly Multidimensional Screening††thanks: I thank Mohammad Akbarpour, Gabriel Carroll, Daniel Chen, Piotr Dworczak, Mira Frick, Nima Haghpanah, Jason Hartline, Andreas Haupt, Ravi Jagadeesan, Zi Yang Kang, Yingkai Li, Paul Milgrom, Mike Ostrovsky, Anne-Katrin Roesler, Ilya Segal, Andy Skrzypacz, Takuo Sugaya, Bob Wilson, Ali Yurukoglu, and Weijie Zhong; conference and seminar participants at Stanford, NSF/NBER/CEME Decentralization Conference, Canadian Economic Theory Conference, Midwest Economic Theory Conference, ACM EC’22, Stony Brook Game Theory Conference, and SAET Conference for helpful comments and suggestions.

Abstract

A screening instrument is costly if it is socially wasteful and productive otherwise. A principal screens an agent with multidimensional private information and quasilinear preferences that are additively separable across two components: a one-dimensional productive component and a multidimensional costly component. Can the principal improve upon simple one-dimensional mechanisms by also using the costly instruments? We show that if the agent has preferences between the two components that are positively correlated in a suitably defined sense, then simply screening the productive component is optimal. The result holds for general type and allocation spaces, and allows for nonlinear and interdependent valuations. We discuss applications to multiproduct pricing (including bundling, quality discrimination, and upgrade pricing), intertemporal price discrimination, and labor market screening.

Keywords: Multidimensional screening, costly instruments, mechanism design, selection markets, price discrimination, bundling.

1 Introduction

Actions convey information. The effort to obtain credentials conveys information about the ability of a job applicant. The time spent waiting in line conveys information about the willingness to pay of a customer. The endurance of physical activity conveys information about the health status of an individual.111The New York Times reports, “The [Wal-Mart’s] memo suggests that the company could require all jobs to include some component of physical activity, like making cashiers gather shopping carts.” Wal-Mart’s health care struggle is corporate America’s, too, The New York Times, October 29, 2005. See also Zeckhauser (2021) who argues that socially wasteful ordeals play a prominent role in health care. These actions are often costly in that they are socially wasteful. However, because the preferences over these actions are correlated in some way with the private information that affects the allocation of productive assets, the informational content from these costly actions could be useful for screening. As Spence (1973b) writes, “Nonprice signaling and screening in economic and social contexts deserve more attention, in spite of the fact that they are frequently inefficient.”222Stiglitz (2002) also writes, “There is a much richer set of actions which convey information beyond those on which traditional adverse selection models have focused.”

The addition of a nonprice screening instrument significantly complicates the screening problem, by making the allocation space multidimensional. Multidimensional mechanisms are often far more powerful than one-dimensional mechanisms because they can intricately link the incentive constraints (Rochet and Stole 2003). For example, consider the following parable of Stiglitz (2002): An insurance company “might realize that by locating itself on the fifth floor of a walk-up building, only those with a strong heart would apply. […] More subtly, it might recognize that how far up it needs to locate itself depends on other elements of the strategy such as premium charged.”

In this paper, we study the effectiveness of costly nonprice screening. Under what conditions should we expect these costly instruments to be used in the design of optimal contracts? Does assuming away such nonprice screening always lead to a suboptimal mechanism in this richer space of mechanisms? To address these questions, we put forward a new multidimensional screening model. The model consists of two components: (i) a productive component which the principal intrinsically cares about (such as insurance coverage), and (ii) a costly component which the principal may utilize to help screening but destroys social surplus (such as walking up stairs).

In the model, the principal designs a mechanism to assign the productive allocations in a one-dimensional space and the costly actions in an arbitrary space . Monetary transfers are allowed. Both the principal and the agent have quasilinear preferences that are additively separable across the two components and .

Our main result states that if the agent has preferences between the two components that are positively correlated in a suitably defined sense, then simply screening the one-dimensional productive component is optimal (and essentially uniquely optimal). We also provide a partial converse showing that for a given negative correlation structure, there exist utility functions such that the optimal contract must involve costly screening.

We say that the agent’s preferences are positively correlated between the two components if the type who has higher utility for the productive allocations tends to also have lower disutility for the costly actions in the stochastic dominance sense. We allow the agent to have multidimensional private information; however, our result is new even when the agent has one-dimensional types because of the multidimensionality of the screening instruments (i.e. price and nonprice).

A basic intuition behind our result can be understood as follows. Consider the parable of Stiglitz (2002) with two types: a high-risk type and a low-risk type. Suppose the insurance company can make the contract contingent on a physical activity such as climbing the stairs. If the high-risk type is less fit, then the company could increase the coverage targeted at the low-risk type. To purchase the contract, the individual has to climb the stairs. Since the high-risk type finds it harder to climb the stairs than the low-risk type does, such a contract can be incentive compatible and increase the profit. On the other hand, suppose the task was to wait in line in order to be eligible for the contract. If the high-risk type is more likely to be unemployed and hence finds waiting less costly, then the company would not benefit from this instrument, since it makes it easier for the high-risk type to mimic the low-risk type.

However, this intuition is incomplete because it assumes monotonicity of the allocation rule which is with loss of generality in multidimensional settings.333Implementability in multidimensional environments is characterized by cyclic monotonicity (see Rochet 1987) which allows a much richer set of allocation rules. In particular, in the above example, the firm can be better off by not insuring the high-risk type. In the standard setting, this is impossible since this allocation is not monotone in the type. But suppose the firm decreases the coverage targeted at the high-risk type and its associated price but requires a long waiting time. Because the low-risk type finds it more costly to wait, such a non-monotone contract involving a nonprice instrument can be incentive compatible and even optimal (see Example 2 in Section 4.1). The main difficulty of our problem is the multidimensionality of the screening instruments — the addition of one more screening instrument significantly expands the space of implementable outcomes beyond the standard family of monotone allocation functions. This expansion applies even when the agent has one-dimensional types.

Despite this fundamental difficulty, our result shows that quite generally the simple intuition turns out to lead to the right prediction. The proof deals with the richer space of multidimensional mechanisms. It relies on two key ingredients. First, we show that if the agent has positively correlated preferences between the two components, then costly instruments can only help with upward incentive constraints. Second, we show that only downward incentive constraints are needed in any one-dimensional screening model satisfying a condition on the surplus function. This second ingredient, which we call the downward sufficiency theorem (Theorem 2), uncovers a novel property of one-dimensional screening models (see Section 4.1).

In the insurance example, our result implies that costly instruments can be useful if the higher-risk type has higher costs (e.g. climbing the floors) and cannot be useful if the higher-risk type has lower costs (e.g. waiting in line). The same result also applies to the classic setting of labor market screening. Positive correlation of preferences arises there because a higher ability applicant often tends to find both accomplishing the work easier and education less costly. Our result implies that a monopsonistic firm should not make its offers contingent on the costly signals from an applicant, despite the fact that the firm prefers a higher ability applicant (see Section 6.3). Thus, in light of Spence (1973a) who focuses on competitive markets, our result shows that whether costly instruments appear in a market depends on the distribution of market power. The reason is that when there are no outside options generated through competition, the incentive constraints bind in the opposite direction (see Section B.2).

Beyond such direct implications, our result also delivers new insights into multidimensional mechanism design problems that may at first glance appear to be unrelated. First, consider a multiple-good monopolist selling different qualities of bundles. A common selling strategy in streaming services is to offer the bundle of all content at various qualities (e.g. with or without advertising). When is such a strategy optimal? Our key insight is that selling the bundle of all goods can be viewed as the productive component, and selling smaller bundles instead of the grand bundle can be viewed as the costly instruments for screening values of the grand bundle. As an application, in Section 5.2, we generalize a recent result of Haghpanah and Hartline (2021), who derive sufficient conditions for the optimality of pure bundling, to a multiple-good monopoly setting that allows for both probabilistic bundling and quality discrimination. The optimal mechanism in our setting generally involves price discrimination but does so only along the vertical (quality) dimension.

Second, using this perspective on bundling, as another application, we derive conditions on the optimality of selling a menu of nested bundles for a multiproduct monopolist (see Section 6.1). This application allows the buyer to have non-additive values, complementing a recent paper of Bergemann et al. (2021) who study the additive case.

Third, using the perspective that delay is costly, we also derive implications on intertemporal price discrimination. Stokey (1979) shows that if consumers only differ in their values for a good but not in their patience, then the optimal dynamic selling mechanism is static and does not involve intertemporal price discrimination. What happens if consumers differ in both their values and patience? As an application, we show that intertemporal price discrimination can be profitable when consumers’ values and patience are negatively correlated, but it is always unprofitable when consumers’ values and patience are positively correlated (see Section 6.2).

The main contributions of this paper are thus three-fold. First, we provide a unified framework for studying mechanism design with both price and nonprice screening instruments. Such a framework necessarily involves multidimensional allocations and hence requires analysis significantly different from the standard one-dimensional case. Our result provides a parsimonious benchmark to systematically understand how costly instruments should be optimally used in mechanism design.

Second, we offer a new perspective on multidimensional screening. Our framework identifies conditions under which optimal multidimensional mechanism design can be reduced to the one-dimensional case. There are very few general results in the multidimensional screening literature despite much research in the past decades (Rochet and Stole 2003; Carroll 2017). Our framework provides one, through the simple economics of costly screening. Our result holds for general type spaces, general allocation spaces, general utility functions. Motivated by applications — including insurance markets, labor markets, and monopoly regulation — our model allows for interdependent preferences.

Third, these methods can be used to analyze other mechanism design problems. Our applications demonstrate how different mechanism design problems can be formulated in a way that fits our framework by viewing a certain set of allocations as “damages.” In contrast to the results from the damaged good literature, our multidimensional framework distinguishes between different kinds of damage (e.g. reducing quality vs. requiring waiting) and characterizes when to use which kind of damage.

On the technical side, the contribution is a novel nonlocal approach to mechanism design. The standard approach to mechanism design uses the envelope theorem to characterize the transfers associated with each implementable allocation rule, and then optimizes over the set of implementable allocation rules. This is possible in one-dimensional settings because the set of implementable allocation rules is characterized by a simple monotonicity condition. In multidimensional environments, the set of implementable allocations is much richer. On the other hand, ignoring the implementablity constraints and optimizing only with the local IC constraints generally leads to non-implementable outcomes.

Instead, our proof method works as follows. First, for a given incentive compatible multidimensional mechanism, we reconstruct an alternative one-dimensional mechanism that improves upon the original one but only satisfies a particular class of IC constraints, the set of downward incentive constraints. Next, our key technical result, the downward sufficiency theorem, shows quite broadly that upward incentive constraints can be ignored in one-dimensional models. This result is proved by a novel variational argument. These steps together provide an alternative to the current approach to multidimensional mechanism design that relies heavily on linear programming duality and requires problem-specific techniques (e.g. Haghpanah and Hartline 2021, Bergemann et al. 2021). We postpone the detailed discussion of previous literature to Section 7, after presenting our results.

The remainder of the paper proceeds as follows. Section 2 presents our model. Section 3 presents the main result and a partial converse. Section 4 presents the proof of the main result. Section 5 presents a stronger result in a special case of the model and its application to multiple-good monopoly pricing. Section 6 discusses additional applications. Section 7 discusses related literature. Section 8 concludes.

2 Model

A principal wants to screen an agent. The agent has private information summarized by a multidimensional type , where and for a finite ; for convenience, sometimes we also refer to as and as . We use the superscripts , to indicate the productive and costly components, respectively.

Both and are assumed to be compact. Let denote the type space; let denote the space of Borel probability measures on , equipped with the weak-∗ topology. The agent’s type is drawn from a commonly known distribution .

The space of productive allocations is a compact subset of ; the space of costly instruments is an arbitrary measurable space.

Both the principal and the agent have quasilinear preferences that are additively separable across the two components: The principal’s (ex post) payoff is given by

and the agent’s payoff is given by

where stands for transfers. The utility functions for the productive component , are assumed to be continuous on ; those for the costly component , are allowed to be any bounded measurable functions on . The principal has interdependent preferences if or depends on the agent’s type.

The (ex post) surplus functions for the two components are denoted by

The defining feature of the costly component is that any allocation is socially wasteful under complete information: for all and all ,

There is an element (with measurable) representing no costly screening:

We say the instruments are strictly costly if (2) holds strictly for all and all .

A mechanism is a measurable map

satisfying the usual incentive compatibility (IC) and individual rationality (IR) constraints:

Let denote the space of mechanisms. The principal wants to solve

A mechanism involves no costly screening if for all and does not depend on , in which case the mechanism screens only the productive component.

We make the following assumptions on the productive component.

Assumption A1 (Productive Component).

-

(1.1)

is nondecreasing in .

-

(1.2)

has strict increasing differences: for any , ,

-

(1.3)

has weak single-crossing differences: for any , ,

To state our notion of positive correlation of preferences between the two components, we introduce some notation. Let denote the usual stochastic order for -valued random variables, i.e. if for all bounded nondecreasing (measurable) functions . Let denote the regular conditional distribution of given .444See e.g. Klenke (2013, pp. 180-185).

Assumption A2 (Positive Correlation of Preferences).

-

(2.1)

is nondecreasing in .

-

(2.2)

for all in the support.

2.1 Discussion of Assumptions

Mechanism Space.

As formally defined, our model restricts attention to deterministic mechanisms. However, when there are finitely many pure allocations, we may be able to redefine the allocation spaces to be the probabilities. We take this approach in Section 5.2 where we show how probabilistic bundling by a multiple-good monopolist is nested in this framework.

In the model, there is no feasibility constraint across the allocation spaces and . However, for any subset , we may constrain the feasible allocations by requiring . Provided that , our main result is unaffected by such constraints (since the optimum in the original problem would still be feasible).

Additive Separability.

At this level of generality, additive separability is imposed to distinguish between the productive and the costly component. In applications, even when this assumption may at first glance appear to be violated, a suitable transformation of the problem may yield an additively separable structure. For example, our applications on bundling with non-additive values (Section 5.2, Section 6.1) and intertemporal price discrimination (Section 6.2) can be formulated in a way that fits this framework.

Monetary Transfers.

In the model, money is perfectly transferable. However, by rescaling, our model accommodates some environments in which monetary transfers can be imperfect. Suppose for any mechanism the principal’s payoff is given by

where is any positive constant (that may represent, for example, adjustment for tax). We can factor out and see that the principal’s problem is equivalent to that with the scaled objective . If satisfies the weak increasing differences condition555That is, for all , . and , then this problem automatically fits our model.

Productive Component.

Assumptions (1.1) and (1.2) are the classic assumptions of one-dimensional screening problems. For future reference, we say a one-dimensional screening problem is standard if it satisfies Assumptions (1.1) and (1.2).666A no-trade outcome , in the sense that , is allowed but not required in the model. In particular, if is the no-trade outcome, then Assumption (1.1) is not needed because it would be implied by Assumption (1.2).

Assumption (1.3) is a new condition that is imposed on the surplus function. For future reference, we refer to Assumption (1.3) as the surplus condition. It is satisfied in common one-dimensional screening problems. For example, this condition automatically holds when the principal’s preferences are not interdependent, given Assumption (1.2). In general, however, this condition differs from Assumption (1.2). Sufficient conditions for this surplus condition include, for example, (i) is strictly increasing in , or (ii) the cross partial derivative . This assumption ensures that there is a monotone efficient allocation rule. It is not satisfied when the principal’s preference to trade with low types is so strong that any socially efficient allocation rule is not monotone. This is an important assumption that is used in our key technical result, the downward sufficiency theorem (Theorem 2). In Section 4.1, we further explain this condition and provide a counterexample when this condition fails.

Positive Correlation.

Assumption (2.1) says that encodes the strength of the agent’s preferences on the costly component such that higher represents higher willingness to pay for any . Assumption (2.2) then defines the positive correlation structure between the agent’s preferences for the two components. The condition is known as stochastic monotonicity (Müller and Stoyan 2002). We say is stochastically nondecreasing in whenever Assumption (2.2) holds. This is an asymmetric condition. It says that observing a high conveys good news about in the sense of stochastic dominance. A sufficient condition for Assumption (2.2) is that are affiliated in the sense of Milgrom and Weber (1982) (see Lemma 9 in Section B.3). Assumption (2.2) is weaker than affiliation. For example, when , may be negatively correlated with each other, while is positively correlated with according to this notion.

3 Main Result

Our main result says that if the agent has positively correlated preferences between the productive and costly components, then simply screening the one-dimensional productive component is optimal and essentially uniquely optimal:

Theorem 1.

In the case of negatively correlated preferences, we show a partial converse. We say the utility functions , , , are admissible if they satisfy all the assumptions in Section 2 including the strict version of (2). For a real-valued continuous random variable , let denote the “binarization” of .

Proposition 1.

Suppose is absolutely continuous; , ; and there exists some such that is stochastically nonincreasing in and , are not independent. Then, there exist admissible utility functions such that any mechanism screening only the productive component is strictly dominated by a mechanism involving costly screening.

We postpone the explanation and proof of Theorem 1 to Section 4. 1 can be shown by a simple construction that sets . The intuition is as follows. The principal can always create a menu of two nontrivial options for the agent: (i) getting the favorite allocation in at a high price, and (ii) getting the same allocation at a low price but with some costly activity. The proof shows that if is negatively correlated with as defined in the statement, then there exist some admissible utility functions for the agent such that this way of price discrimination is always more profitable for the principal than selling the elements in alone. The appendix provides details.

4 Proof of the Main Result

In this section, we provide the proof of Theorem 1 under the additional assumption that . In addition, we also assume that so that the agent has only one-dimensional types. The main difficulty of the proof already appears in this simplest case. The appendix provides the proof of the general case.

4.1 Examples and the Approach

Before presenting the proof, to illustrate the basic intuition outlined in the introduction and why it is incomplete, we begin with a sequence of examples.

Consider a health insurance setting with two types: is the low-risk type and is the high-risk type (with equal probabilities). The low-risk type has value for the insurance, whereas the high-risk type has value . It costs the insurance firm to serve the low-risk type, and to serve the high-risk type. Equivalently,

Because the utilities are linear in the allocation , the optimal one-dimensional mechanism has three possibilities: (i) trade with both types with full insurance (i.e. ), (ii) trade with only the high type with full insurance, or (iii) trade with neither of the types. Option (i) yields profit , option (ii) yields profit , and option (iii) yields profit . Thus, without any costly instrument, the principal gets profit .

Example 1.

Suppose we add a costly instrument such as a physical activity for which the low-risk type has cost and the high-risk type has cost :

The agent has negatively correlated preferences here because the high-risk type has a higher utility for the insurance but also higher disutility for the costly action. The principal can mitigate the adverse selection problem by offering , which can be interpreted as requiring the physical activity in order to purchase the insurance plan (e.g. locating the office on a walk-up building). The high-risk type, finding the physical activity too costly, does not purchase this plan. Then, the principal gets profit . ∎

Example 2.

Suppose, instead, we add a costly instrument such as waiting in line for which the low-risk type has cost and the high-risk type has cost :

The agent has perfectly correlated preferences here because the high-risk type has a higher utility for the insurance but also lower disutility for the costly action. Perhaps surprisingly, the costly instrument can still be useful. In particular, consider a menu of two options , which can be interpreted as a full insurance plan with a price , and a low-coverage plan that has a price but requires some amount of waiting. The low-risk type, finding waiting too costly, purchases the full insurance plan. The high-risk type, finding the low-coverage plan cheap, purchases the low-coverage plan. With this menu, the principal gets profit . ∎

Note that in both Example 1 and Example 2, the insurance allocation is not monotone: the high-risk type gets lower coverage than the low-risk type does. This cannot arise under any one-dimensional mechanism. The possibility of using an additional instrument significantly expands the space of implementable allocations, which is the main difficulty in proving our result.

A key observation is that the costly instrument in Example 2 is used in a different way from that in Example 1. The costly action in Example 2 is required for the eligibility to purchase the low-coverage option targeted at the high-risk type, whereas the costly action in Example 1 is required for the eligibility to purchase the full-coverage option targeted at the low-risk type. That is, the costly instrument is used to deter the upward deviation under positive correlation of preferences, whereas it is used to deter the downward deviation under negative correlation of preferences.

If we can rule out upward deviations to begin with, we can then show that the costly instruments is ineffective under positive correlation of preferences. This is precisely the route our proof takes. But it turns out that ruling out upward deviations is involved.

Suppose, in Example 2, we ignore the upward deviation. Then, the principal optimally sets a price of for the full insurance plan targeted at the low-risk type, and pays the high-risk type to stay out of the market. This yields a profit . But, of course, this is not incentive compatible: the low-risk type wants to take the payment as well. Thus, the downward incentive constraint is not sufficient.

Example 3.

Suppose, as in Example 2, the costly instrument is waiting in line, but it costs instead of to serve the high-risk type, i.e. . Note that the set of incentive compatible mechanisms is the same as in Example 2. In particular, the menu induces the same self-selection as before, and hence gives the principal profit

But this menu is now strictly dominated by simply selling to both types without any costly screening, because that gives the principal profit

| ∎ |

Example 3 differs from Example 2 in that the cost of serving the high-risk type is now lower than the value of the high-risk type (i.e. ). More generally, let be the cost of serving the high type. Note that the surplus function for the productive component satisfies the surplus condition, Assumption (1.3), if and only if . Note also that by the same calculation as in Example 3, the menu is no more profitable than simply selling the full insurance plan to both types if and only if . Even though the costly instrument expands the space of implementable outcomes just as before, it turns out that the surplus condition, equivalent to here, guarantees that the optimum does not make use of the much richer set of mechanisms.777Note that this is not the case under Example 1 where the agent has negatively correlated preferences: even if instead of , the optimum still uses the costly instrument because that gives profit .

The reason, as alluded to earlier, is intimately linked to whether we can ignore upward incentive constraints. Our key technical result, the downward sufficiency theorem, asserts that as long as the surplus condition holds, only downward incentive constraints are needed in one-dimensional screening models. By a reconstruction argument, we also show that if the agent has positively correlated preferences between the two components, then costly instruments can only help with upward incentive constraints. Our main result follows by combining these two ingredients.

The downward sufficiency theorem is proved by a variational argument. For an arbitrary mechanism that satisfies all downward incentive constraints but violates some upward incentive constraints, we show that it can be improved by a carefully chosen sequence of modifications. This theorem is distinct from the classic results on the local incentive constraints. It is well known that the local downward incentive constraints are always binding for any one-dimensional screening model. However, as Example 2 shows, this does not imply that we can ignore the upward incentive constraints. With more than two types, it is also well known that the local downward incentive constraints are generally not sufficient — various procedures of ironing are needed (Myerson 1981, Mussa and Rosen 1978). There is no known tractable method of ironing in multidimensional environments since the space of implementable outcomes is much richer (Rochet and Stole 2003).888For example, there is no tractable ironing method using cyclic monotonicity which characterizes implementability in multidimensional environments. Our approach makes essential use of the global downward incentive constraints.

The rest of this section presents the proof, organized as follows. Section 4.2 shows how the reconstruction works. Section 4.3 proves the downward sufficiency theorem. Section 4.4 briefly discusses how the imperfect correlation case can be reduced to the perfection correlation case.

4.2 Reconstruction

Suppose we are given a mechanism . Consider the following reconstruction:

The reconstruction maintains the same allocations for the productive component, involves no costly screening, and uses transfers to keep all types at their previous utility levels, assuming they report truthfully.

Assuming truthful reporting, this increases the total surplus while giving the same surplus to the agent, and therefore increases the principal’s payoff. Indeed, the change in principal’s payoff is

The last inequality is strict if and the instruments are strictly costly.

Because the reconstruction maintains the utility for each type under truthful reporting, satisfies all IR constraints. However, this mechanism is not necessarily IC. Indeed, suppose for illustration that is strictly increasing, and for some , binds under . Consider the same deviation under :

| (2) |

where the first and the last line follow by construction, the second line uses the binding IC constraint, and the third line uses that is strictly increasing. Therefore, is not satisfied under .

This demonstrates that the reconstruction does not work directly. However, the same reasoning also shows that all downward IC constraints are still satisfied after this reconstruction. Indeed, consider a downward deviation for any :

| (3) |

where the first and the last line follow by construction, the second line follows from being IC, and the third line follows from that is nondecreasing. Therefore, satisfies all downward IC constraints.

Let denote the space of measurable maps that are (i) IR, (ii) involve no costly screening, and (iii) satisfy all downward IC constraints.

The reconstruction argument gives the following lemma:

Lemma 1.

Consider any . There exists some such that

If the instruments are strictly costly and , then the above inequality is strict.

By Lemma 1, it is, therefore, always an upper bound for the principal to optimize over . Because , the principal then solves the following:

| (4) | |||||

This problem is a one-dimensional screening problem except that all upward IC constraints are ignored. For future references, we use to denote the version of problem (4) with both the downward and upward IC constraints.

4.3 Downward Sufficiency Theorem

Theorem 2 (Downward sufficiency).

Consider any standard one-dimensional screening problem. Suppose the surplus function satisfies the weak single-crossing differences condition. Then, there exists an optimal solution to (4) that also satisfies all upward IC constraints.

Even with a continuous type space, this theorem cannot be proved by using a local approach because, as discussed in Section 4.1, the infinitesimal downward IC constraints are not sufficient. One approach to prove this theorem is to construct a double continuum of Lagrange multipliers that place weights only on the downward constraints (under additional convexity assumptions). But doing so requires a new construction for each instance of and . It is also unclear what the dual variables should be.

Our approach is variational. We first prove Theorem 2 for the case of finite and then for the general case using approximation. Let us suppose and order types by . Let denote the distribution of . We assume that has full support. Without loss of generality, suppose and . A mechanism is then specified by and . The principal’s problem is given by

| (5) | |||||

We replace to as the existence of the solution is easy to see by compactness arguments. In this finite-type case, we prove a stronger claim than Theorem 2 by showing that every optimal downward IC mechanism must satisfy all upward incentive constraints. For any feasible solution to (5) that fails some upward incentive constraints, we will perturb it to obtain a new feasible solution that strictly improves the objective.

We start with some carefully chosen definitions. Fix any allocation rule . Let

be the running maximum index set of (including the last index).

A -shaped region is a set of indices of the form

such that (i) and are two consecutive elements of , and (ii) . By definition, there is a finite sequence of -shaped regions. Let be the number of -shaped regions. We write and as the starting and end index of the -th -shaped region .

An optimal downward transfer operator (or simply transfer operator) is a map

such that for any , is an optimal solution to the following problem:

| (6) |

subject to the same downward IC and IR constraints as in (5). That is, maps an allocation rule to the optimal transfer rule that implements in a downward IC fashion. At this stage, it is unclear whether such an operator is defined for all .

Step 1:

Our first step is to show that such an operator exists and is unique. In fact, we explicitly characterize , which will be used repeatedly in the perturbation argument in Step 2. For notational convenience, we write (or simply ) and as a shorthand for and , respectively.

Claim 1.

There exists a unique transfer operator . For any , is the solution to the system of equations defined by the following constraints with equality: , and

for all . In particular, for all ,

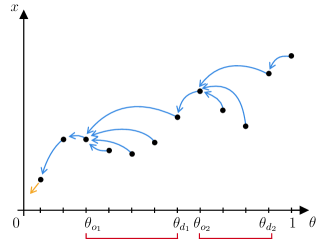

In words, for an arbitrary , there exists a unique optimal subject to that is IR and downward IC. Moreover, for a given , the binding IC constraints for go from every index to the largest element in that is strictly less than . Figure 1 illustrates how the -shaped regions and the binding constraints in Claim 1 are identified.

As the figure shows, equivalently, the local IC constraints bind until one travels into a -shaped region (beginning with say index ) where the binding constraints then point toward . This provides some further intuition about (1), as (1) can then be written as

where is the region where is monotone in an appropriate sense.999Formally, . The first sum arises from the binding local downward IC constraints, and the second sum arises from the binding nonlocal downward IC constraints. If is monotone, then (4.3) will reduce to the standard transfer formula in one-dimensional screening models, in which only the local downward IC constraints matter (for transfers). However, importantly, we cannot rule out any by implementability here since we do not have upward incentive constraints. The transfer rule depends on the shape of the allocation rule .

Proof of Claim 1.

Relax all the constraints in (6) except the ones indicated in Claim 1. We will show the following: First, these constraints must bind in the relaxed problem. Second, these constraints binding imply all downward IC constraints and all IR constraints. Third, there is a unique solution to the system of equations defined by these binding constraints. Claim 1 then follows.

Note that for every , there is precisely one corresponding constraint for some . If this constraint does not bind at some mechanism , then simply set for some small enough so that still holds. This clearly increases the objective. It also does not distort other IC constraints. Indeed, the only other IC constraints this change affects are of the form for some , but

Therefore, all the IC constraints identified in Claim 1 must bind. Similarly, binds.

Given that these constraints bind, we now show that they imply all the downward IC constraints in (6). We first collect two lemmas:

Lemma 2 (Local to global).

Let . If , hold and , then .

Lemma 3 (Global to local).

Let . If , bind and , then .

Lemma 2 is standard; it follows from a revealed-preference argument using the single-crossing property of (we include a proof in the appendix for completeness). Lemma 3 appears to be new; it requires two binding IC constraints and follows from a revealed-preference argument that subtracts the two constraints. The appendix provides details.

We show all downward IC constraints are satisfied by induction on the number of -shaped regions . When , all downward IC constraints hold by successively applying Lemma 2 and building up from the adjacent local downward constraints. Suppose the claim holds for . Let us denote the last region as with starting index and end index . By the inductive hypothesis, all downward IC constraints are satisfied if . We divide the remaining pairs with into two cases:

-

Case (2): . Note that for all . Then, follows by from Case (1), from the inductive hypothesis, , and Lemma 2.

Together, these cover all the downward IC constraints and prove the inductive step. The IR constraints follow easily from and and that is nondecreasing.

The binding constraints define a system of equations for . With some calculations, it is not hard to see that these equations can be solved successively starting from the lowest one. In particular, by induction, the solution is uniquely defined by (1). ∎

Step 2:

Consider any feasible to (5) that does not satisfy some upward IC constraints. We are now ready to construct a perturbation that strictly improves on .

There are two cases: (i) is monotone and (ii) is not monotone. The first case is simple. As noted before, when is monotone, reduces to the standard transfer formula and hence must satisfy all incentive constraints including the upward ones. Then, cannot be identically equal to . But that implies can be strictly improved by by Claim 1.

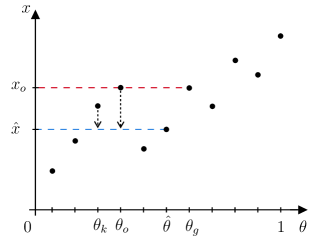

Consider the second case where is not monotone. Then, there must exist a -shaped region. Let be the first -shaped region, its starting index, and its end index.

By definition of , it suffices to construct a perturbation of such that strictly improves upon . The perturbation we construct will act on a carefully chosen set of types. In particular, let

denote the first index after with associated allocation no less than . Put if the above set is empty. Then, either or .

Let

denote the largest allocation for indices strictly between and . We have . Let be the first index achieving the above maximum and let .

Let

denote the first index whose associated allocation is strictly higher than . Since , we have . Because is the first -shaped region, we have

Claim 2.

The objective of (5) under is strictly higher than that under .

Proof of Claim 2.

The main difficulty here is that is a complicated operator because of the binding nonlocal incentive constraints. The perturbed allocation is constructed in such a way that it maintains the form of in the following sense. Define function by

for all , where is the power set operator. For any allocation rule , let be the running maximum index set as defined earlier. Then, by (1), .

Lemma 4.

Consider any two allocation rules with running maximum index sets . Suppose , and for all . Then,

The appendix provides the proof of this lemma. Note that by construction , always satisfy the conditions in Lemma 4. Applying Lemma 4 to , gives , where is the running maximum index set of . We show that the objective of (5), after plugging in , weakly increases on the parts involving (which may be an empty set) and strictly increases on the parts involving (which always exist).

Fix any . Plugging into the objective of (5) and collecting terms involving gives

Now consider the terms involving . Because , there is no IC constraint pointing toward by Claim 1. Therefore, there is only one such term:

Note that is feasible to assign to . Moreover, since , doing so maintains the form of by Lemma 4, and thus generates a payoff also according to the above formula. The fact that is optimal then implies

that is,

Because and , by the weak single-crossing differences property of ,

Moreover, because , by the strict increasing differences property of ,

Combining (4.3) and (4.3) gives

proving that the part of the objective involving increases.

Because this holds for all , to conclude our proof, it remains to show that the part of the objective involving strictly increases. Plugging into (5) and collecting terms involving gives

By the same argument as the previous case, we have

For any , by the strict increasing differences property of ,

Together they imply

where the strict inequality also uses that has full support. ∎

Step 3:

We prove Theorem 2 for general type space by approximation. We give a sketch of the argument here and leave the details to the appendix. Let denote the distribution on . Recall that denotes the version of program with all IC constraints (both downward and upward). Let denote the optimal value of given . We show that equals to the optimal value of . Suppose, for contradiction, there exists some feasible for such that

We first construct an appropriate sequence approximating .

Lemma 5.

Suppose is Lipschitz continuous on . Then, there exists a sequence with finite and full support such that

-

(i)

;

-

(ii)

.

Suppose for a moment that are continuous on and is Lipschitz continuous. Note that restricted to is a feasible solution to the finite-type version of (4) with . By Step 2, we have . Because is a bounded continuous function on , using Lemma 5 and taking limits on both sides of the above, we have

contradicting (4.3). However, the situation is more delicate in general. The proof (in the appendix) relies on the Stone–Weierstrass theorem and Lusin’s theorem.

Finally, to conclude Theorem 2, it suffices to show the existence of an optimal solution to the full IC program . Even though this is a standard one-dimensional problem, the existence result appears to be new at this level of generality.

Lemma 6.

Any standard one-dimensional screening problem has a solution.

The proof (in the appendix) proceeds by showing the space of IC and IR mechanisms is sequentially compact in the product topology. The argument uses a generalized version of Helly’s selection theorem from Fuchino and Plewik (1999).

4.4 Reduction

For the more general case of positive correlation (instead of perfect correlation), we reduce it to a set of subproblems each of which has . Suppose and is stochastically monotone in . Let be an independent uniform draw. Note that the random vector can be simulated by

where is the generalized inverse function of . Our positive correlation condition states that shifts upward in the sense of stochastic dominance as increases. This implies that is a nondecreasing function. Therefore, if we reveal the realization of to the principal and let the principal design a mechanism contingent on , the problem reduces to the case in which for some nondecreasing function . Now, simply define and . For each realization of , we can apply our result from the previous two subsections to the screening problem with utility functions and perfect correlation . Thus, for each realization of , simply screening the productive component is optimal, but that mechanism does not depend on and hence must be optimal in the original problem.

Remark 1.

In the more general case where is multidimensional, to perform the above reduction, we use an insight due to Haghpanah and Hartline (2021) who make use of a classic result of Strassen (1965) on monotone coupling. For measurability issues, we prove a measurable monotone coupling lemma (see Lemma 7 in Section B.3), building on a result by Kamae and Krengel (1978).

5 Monopoly Pricing with Costly Signals

Before discussing other applications of Theorem 1 in Section 6, we specialize the main model to a setting of monopoly pricing with costly signals. In this setting, a monopolist sells a spectrum of quality-differentiated goods and can make the menu of offers contingent on the costly actions that a buyer may take.

In Section 5.1, we show that if the buyer’s utility functions are multiplicatively separable within each component, then the positive correlation of preferences condition can be weakened to the positive correlation between the preferences for the productive component and the marginal rates of substitution between the productive and costly components.

In Section 5.2, we consider a multiple-good monopolist selling different qualities of bundles (with no costly signals). This environment generalizes the classic multiple-good monopoly problem by allowing for both probabilistic bundling and quality discrimination. We show that (a relaxation of) this problem can be mapped to a monopolist selling a spectrum of quality-differentiated goods without bundling but with costly signals as in Section 5.1. A key insight is that one can view selling the grand bundle as the productive component, and selling a smaller bundle instead of the grand bundle as a costly instrument for screening a consumer’s value for the grand bundle. Using this perspective, we generalize a result of Haghpanah and Hartline (2021). In particular, we show that under their stochastic ratio monotonicity condition, the general feature of the optimal mechanism is to post a menu of different qualities of the grand bundle — the monopolist screens only the productive component and does not use any of the “costly signals.”

Setup.

A monopolist sells a quality-differentiated spectrum of goods. A buyer of type receives utility from consuming the good of quality . The seller incurs a cost to produce the good of quality for type . Suppose is nondecreasing in and has strict increasing differences, and that the surplus function has weak single-crossing differences. (The continuity and compactness assumptions in Section 2 are also maintained.)

Besides offering a menu of products of different qualities and prices, the monopolist can make the offers contingent on various costly signals (e.g. waiting in line, collecting coupons, walking up stairs). A costly signal is represented by . To obtain a signal , a buyer of type incurs a cost that is nonincreasing in (so represents the willingness to endure various costly activities).

Theorem 1 then says that if is positively correlated with according to our notion, then the monopolist never makes more profits by using these costly signals. Therefore, if the monopolist in fact uses these instruments, then we should expect that the consumers with higher willingness to pay tend to incur higher costs to obtain the signals (both measured with respect to the constant marginal value for money). In fact, sometimes we can say more when the buyer’s utility functions are multiplicatively separable within each component, which we turn to next.

5.1 Marginal Rates of Substitution Between Two Components

We follow the notation in the above setup, and let be , any measurable space, any compact subset of , and any compact subset of . We say that the buyer has multiplicatively separable utilities within each additive component if for any quality , signal , and price , the buyer’s payoff can be written as

where is a continuous and strictly increasing function satisfying , and is a bounded measurable function satisfying for some .101010Note that a utility of the form provides (essentially) no additional generality.

We say that the monopolist’s cost function is not interdependent if does not depend on , in which case without loss of generality we let .

Recall the notation . Let and . Note that . We interpret as the (negative) marginal rates of substitution between the productive and costly components.111111The substitution here is between the utility from the productive component and the disutility from the costly component, and hence has negative marginal rates. In this setting, we show that our assumption of positive correlation between and can be weakened to that between and .121212This is in general not necessarily a weaker condition; it is so in this case because .

Proposition 2.

Suppose the seller’s cost function is continuous, nondecreasing in , and not interdependent; the buyer’s utilities are multiplicatively separable; and is stochastically nondecreasing in . Then, there exists an optimal mechanism that involves no costly screening.

The intuition behind this result can be understood in the same way as in the proof of the main result (Section 4). We show that when the marginal rates of substitution are increasing in the values, instead of using the costly signals, the principal can simply adjust the allocations of the productive component while maintaining the downward IC constraints. Because downward IC constraints are sufficient, the result follows. Unlike in Section 4, in this case we substitute the costly signals with a decrease in the productive allocations holding the monetary transfers fixed, which is why the marginal rates of substitution between the two components play an important role here.

Proof of 2.

By Lemma 7 in Section B.3, as in Section 4.4, it suffices to show the case where for some nondecreasing function . Thus, we may assume for all , is deterministic conditional on and nondecreasing in . Fix any that is IC and IR. We may assume , because the monopolist can simply replace all options with negative profits in the menu with and weakly increase the total profit (since the monopolist’s cost function does not depend on the buyer’s type). Now we apply a reconstruction argument as follows. Consider the modification: ,

Because is continuous and strictly increasing with , is defined on . Moreover, because is IR and , we have for all . So the modification is well-defined and pointwise. In other words, the modified mechanism decreases the productive allocation to substitute the costly screening so that all types have the same utilities as before, assuming truthful reporting.

Because is nondecreasing, this modification increases the objective, assuming truthful reporting. It is IR by construction. Moreover, it is downward IC: for any ,

The first inequality holds because is IC. The second inequality holds because and . Invoking Theorem 2 concludes the proof. ∎

5.2 Bundling and Quality Discrimination

We now show an application to a multiple-good monopoly problem allowing for both probabilistic bundling and quality discrimination.

A monopolist sells many goods to a unit mass of consumers. For each bundle , a random consumer has value for getting the highest quality version of the bundle with probability one. We assume that for all and . The monopolist can use probabilistic bundling, captured by a bundling allocation rule . In addition, the monopolist can adjust the quality of each bundle, captured by a quality allocation rule . A type- consumer’s payoff is given by

The monopolist incurs a cost to improve the quality of a bundle, with a payoff given by

where is a continuous, nondecreasing, and convex function on with . This cost structure assumes that the cost of producing a bundle of some quality does not depend on the size of the bundle, which is perhaps more suitable for digital goods.

Let be the value of a random consumer for the grand bundle and be the profile of values for each bundle relative to the grand bundle.

Proposition 3.

If is stochastically nondecreasing in , then an optimal mechanism exists and can be implemented by a menu of prices for different qualities of the grand bundle.

This result is a natural consequence of 2 once one views selling the grand bundle as the productive component, and selling a smaller bundle instead of the grand bundle as a costly instrument for screening a consumer’s value for the grand bundle.

Proof of 3.

By convexity of and Jensen’s inequality, we have

Therefore, it is an upper bound on the monopolist’s revenue to maximize the objective

For this auxiliary problem, let us also relax the constraint to . Then, because enter both the consumer’s utility and the objective in the same way, it is without loss of generality to let for all .

We now reformulate this problem as a problem of monopoly pricing with costly signals. Let be the value of the grand bundle. For any proper bundle , let

be the difference of values for bundle and the grand bundle . In words, is the negative value for getting bundle instead of . Let , and let be the profile of the differences.

We use to denote the initial allocation of the grand bundle, and to denote the allocation of the “costly signals” as follows. An assignment represents assigning bundle with probability while decreasing the probability of the grand bundle also by . The consumer’s payoff can be rewritten as

For any substochastic allocation (i.e. ), we can replicate it by setting

Therefore, the auxiliary problem (5.2) can be further relaxed to

For any , we have . Since is stochastically nondecreasing in , we have is stochastically nondecreasing in . So 2 applies to (5.2). Let be the optimal solution to (5.2) that involves no costly screening.

We construct an allocation rule in the original problem as follows:

| , for all ; , for all . |

Because probabilities and qualities enter the consumer’s utility in the same way and is IC and IR, is also IC and IR. The revenue of the monopolist under is

the optimal value of (5.2). Hence, is optimal for the monopolist in the original problem; moreover, screens using only the qualities of the grand bundle. ∎

Remark 2.

3 says that under the stochastic ratio monotonicity condition, the monopolist can restrict attention to selling only the grand bundle at various qualities. Because that is a one-dimensional problem à la Mussa and Rosen (1978), the solution can be explicitly characterized. When there is no cost for quality improvement (), the optimal mechanism is to sell the grand bundle at the highest quality with a posted price. This special case is due to Haghpanah and Hartline (2021). In general, however, the optimal mechanism involves price discrimination. But 3 shows that such price discrimination is only done by creating different qualities of the grand bundle.

6 Additional Applications

6.1 Bundling with Nested Bundles

Complementary to Section 5.2, rather than quality discrimination, companies may also offer a menu of bundles that are nested (e.g. cable TV providers offer a basic package and a premium package including sports channels). Bergemann et al. (2021) refer to such selling strategies as upgrade pricing and provide sufficient conditions under which they are optimal when consumers have additive values. We provide a different set of sufficient conditions on the optimality of upgrade pricing with non-additive values, as an application of our main result.

For this application, we restrict attention to one-dimensional types and deterministic bundling mechanisms. For example, consider two items . Let , , and be the value of item , the value of item , and the value of the bundle for type , respectively. We assume that are continuous, nondecreasing in (e.g. represents income), and that (e.g. there is free disposal).

Proposition 4.

If is strictly increasing, and is nonincreasing, then an optimal mechanism exists and can be implemented with a menu of nested bundles .

In terms of the cable TV service example, this result says that if a higher-income consumer has a higher incremental value for sports channels, and a lower incremental value for basic channels, then it suffices for the seller to consider a two-tier menu that features a basic package and a premium package including sports channels. This result holds for any distribution of . Despite its seeming simplicity, it cannot be derived with any known result in the literature (see Section B.1 for a parametric example).

This result is an immediate consequence of Theorem 1 provided that one takes the same point of view as in Section 5 by considering selling item instead of the bundle as a costly instrument. It is not hard to see that any menu of nested bundles that does not include the grand bundle cannot be optimal. For any number of items and any menu of nested bundles that includes the grand bundle, in Section B.1, we provide sufficient conditions under which the menu constitutes an optimal selling mechanism.

6.2 Intertemporal Price Discrimination with Private Discounting

Let be a general discount function, where is a compact set of discount rates , and is a finite set of delivery dates including . The discount function is nonincreasing in , with . For example, under exponential discounting and under hyperbolic discounting.

The buyer privately observes his discount rate and value , with a payoff given by

where is the quality of the good and is the price at time . We assume that is continuous, strictly increasing, and satisfies .

The seller has a continuous, nondecreasing cost for producing the good of quality . She wants to design an optimal selling mechanism that specifies the quality, delivery time, and payment for each reported type. A mechanism involves no intertemporal price discrimination if for all .

The next example shows that if a buyer who has a higher value tends to be less patient, then intertemporal price discrimination can be profitable:

Example 4.

Suppose and , where and . Suppose and . The buyer has equal probabilities of having either or . If , then the buyer’s value is drawn from uniform . If , then the buyer’s value is drawn from uniform . Without intertemporal price discrimination, the seller’s optimal strategy is a posted price which yields payoff . However, consider offering for the no-delay option, and for the delayed option. Note that all types with choose the no-delay option, and all types with and choose the delayed option. This yields the seller payoff . ∎

The next result shows that if a buyer who has a higher value tends to be more patient, then intertemporal price discrimination is unprofitable:

Proposition 5.

If is stochastically nonincreasing in , then an optimal mechanism exists and involves no intertemporal price discrimination.

This result is an immediate consequence of 2. This result does not restrict the marginal distributions of and , but only requires a condition on their joint distribution. Stokey (1979)’s classic result can be seen as a special case of this result with being a constant (all types have the same patience), , , and . Our result shows that whether intertemporal price discrimination is profitable depends on the correlation of consumers’ values and patience.

6.3 Labor Market Screening

A monopsonistic firm wants to hire a worker to perform a task. The firm gets a payoff for hiring a worker of ability , where is continuous, nondecreasing in . The worker suffers a cost for performing the task, where is continuous, strictly decreasing in . Let be the probability of hiring the worker.

The firm can ask the applicant to obtain a credential. Suppose that it costs to the worker to obtain a -level credential. Both and are the worker’s private information. For a given wage level , hiring probability , and credential level , the firm’s payoff is , and the worker’s payoff is .

Proposition 6.

If is stochastically nonincreasing in , then an optimal mechanism exists and does not require any credential.

This result is an immediate consequence of Theorem 1. This result contrasts with the common perception of costly signals in competitive labor markets (Spence 1973a). To clarify, in Section B.2, we consider a competitive screening model in which multiple firms compete and are allowed to screen with both work allocations and costly instruments. We show that costly screening can appear in equilibrium. The intuition is that with outside options generated through competition, the binding incentive constraints become the upward ones, which is exactly the opposite to the monopsonistic case.

7 Related Literature

This paper proposes a unified mechanism design framework allowing for both price and nonprice screening instruments, characterizes the exact optimum in a general multidimensional screening model, and bridges costly screening and multidimensional screening to obtain new insights into applications such as bundling and price discrimination.

Costly Screening.

Several previous papers have analyzed mechanism design with a costly instrument when monetary transfers are limited or not feasible. In his pioneering study, Banerjee (1997) studies how a bureaucracy can use red tape as an effective screening device when agents are budget-constrained. A recent line of work studies the design of surplus-maximizing mechanisms when monetary transfers are not feasible and agents engage in a one-dimensional costly activity (Hartline and Roughgarden 2008, Condorelli 2012, Chakravarty and Kaplan 2013).131313See also Acemoglu and Wolitzky (2011) for related moral hazard problems; Ambrus and Egorov (2017) for related delegation problems; and Malladi (2020) for related non-Bayesian screening problems. We study a profit-maximizing mechanism design problem allowing for both flexible transfers and heterogeneous preferences over costly actions. These features together, in contrast to past work, imply that our model necessarily has multiple screening instruments and requires analysis significantly different from the single-dimensional case.

Multidimensional Screening.

The structure of multidimensional screening differs significantly from its single-dimensional counterpart and remains elusive to fully characterize despite much research over the past decades (Rochet and Stole 2003). Much of the literature focuses on the multiple-good monopoly problem. When there is a single good, the optimal mechanism is simply a posted price (Myerson 1981, Riley and Zeckhauser 1983). However, as soon as there is more than one good, seemingly simple special cases remain poorly understood. Significant progress has been made in developing duality approaches to certify optimality of candidate mechanisms (Rochet and Chone 1998, Daskalakis et al. 2017; Cai et al. 2016, Carroll 2017). In response to the analytical difficulty, several recent papers study either approximately optimal mechanisms (Babaioff et al. 2014, Cai et al. 2016, Hart and Nisan 2017), or worst-case optimal mechanisms (Carroll 2017, Che and Zhong 2021, Deb and Roesler 2021).

In contrast to past work, we consider a multidimensional screening model in which all dimensions except one are surplus destructive. The multiple-good monopoly problem can be viewed as a special case of our framework by redefining the allocation space. Using this perspective, we obtain new insights into bundling, quality discrimination, upgrade pricing, and intertemporal price discrimination.

Our proof method uses a novel nonlocal approach, different from both the Myersonian approach commonly used in the one-dimensional settings and the duality approach commonly used in the multidimensional settings. For a given multidimensional mechanism, we reconstruct an alternative, one-dimensional mechanism that satisfies all downward incentive constraints. We then show via a variational argument that the set of downward incentive constraints is sufficient for one-dimensional screening problems satisfying the surplus condition. Because of the multidimensionality of the screening instruments (i.e. price and nonprice), the main difficulty of our problem appears already when the agent has one-dimensional types. To deduce the more general case, our proof builds on the insight of Haghpanah and Hartline (2021) who make use of Strassen’s theorem to decompose a multidimensional type space. When proving their result, Haghpanah and Hartline (2021) explicitly construct a set of dual variables that only place weights on downward constraints — the existence of such dual variables can be seen as a special case of our main technical result, the downward sufficiency theorem, which states that only downward incentive constraints are needed in one-dimensional models.

Damaged Goods.

There is a line of work studying damaged goods and the profitability of price discrimination (or pure bundling) (Deneckere and McAfee 1996, Anderson and Dana Jr 2009, Haghpanah and Hartline 2021, Ghili forthcoming). A key difference between our result and the results obtained in this literature is that our framework distinguishes between different kinds of damage (e.g. reducing quality vs. requiring waiting) and characterizes when to use which kind of damage. For example, in our bundling application, quality discrimination is used but mixed bundling is not used under the optimal mechanism; in our intertemporal price discrimination application, quality discrimination is used but delay is not used under the optimal mechanism. This is also the reason why our framework allows us to characterize when it is optimal to sell a given menu of nested bundles, a selling strategy necessarily involving damages.

8 Conclusion

This paper studies the effectiveness of costly instruments in a general multidimensional screening model. The model consists of two components: a one-dimensional productive component and a multidimensional costly component. Our main result says that if the agent’s preferences are positively correlated between the two components in a suitably defined sense, then the costly instruments are ineffective — the optimal mechanism simply screens the one-dimensional productive component.

Our proof provides clear insights into why this result holds. First, we show that costly instruments can loosen upward but not downward IC constraints on the costly component. Next, we show that positive correlation of preferences then converts the IC constraints on the costly component to those on the productive component without changing the direction. Finally, we show that the set of downward IC constraints is sufficient for any one-dimensional screening problem satisfying the surplus condition. Therefore, costly instruments cannot help the principal when the agent’s preferences are positively correlated between the two components.

Armed with this understanding, we have also shown how additional results follow naturally. With negatively correlated preferences, we show a partial converse. With multiplicatively separable preferences within each component, we show a stronger result in terms of the marginal rates of substitution between the two components. Using the perspective of screening with costly instruments, as applications, we also provide new insights into multiproduct pricing (bundling, quality discrimination, upgrade pricing), intertemporal price discrimination, and labor market screening.

Appendix A Omitted Proofs

Proof of 1.

Without loss of generality, we may assume . Let . Because has a continuous distribution, there exists some constant such that

Similarly define for . Since is stochastically nonincreasing in , we have and are positively upper orthant dependent (Müller and Stoyan 2002, pp. 121-125), and hence

Because , are not independent, we have

and thus

Define

where will be determined shortly. Let be a continuous approximation of such that for all . It is clear that we may select to be nondecreasing. Let and . Since , . Since , there exists some . Now let

This construction gives admissible utility functions. Consider offering the following menu of three options:

Let the agent choose among these, breaking tie in favor of the principal. This yields a payoff of at least

for the principal. Screening the productive component alone yields a payoff of at most

for the principal. Note that are both continuous on , and

Thus, there exists some such that . With this choice of , the above construction then gives admissible utility functions such that the menu of three options strictly dominates any mechanism screening only the productive component. ∎

Proof of Lemma 2.

Write out and :

Adding these two yields

Hence,

Using , , and the strict increasing differences property of , we have

Thus follows. ∎

Proof of Lemma 3.

Write out the binding constraints and :

Subtracting these two yields

Hence,

Using , , and the strict increasing differences property of , we have

Thus follows. ∎

Proof of Lemma 4.

Fix any subset , any index , and any allocation rule . We claim that if , then

Let be the two consecutive indices in such that . Note that for any ,

since . For any , we can write

and . Thus for any . Also, the fact that the above holds for implies that for any .

Now, write with . By assumption, . Then, by the definition of , for all , we have

Thus, we can repeatedly apply the result from the previous paragraph and obtain

which proves the lemma. ∎

Proof of Lemma 5.

We maintain the notation of Step 3 in Section 4.3. Without loss, let and . The construction works as follows. Fix any . Partition into intervals . Let

For any , let

(The minimum is attained since is compact.) For notational convenience, we reindex so that it runs over from to . Let

We have finite and full support. Note that

We first show property in the statement. Recall that for this lemma we assume is Lipschitz continuous on . Then, there exists some constant such that for any ,

Let be any optimal solution to the full IC program with . Let be the extension of to the right:

Note that is a monotonic function on . Define in the same way. We claim , when restricted to , is a feasible solution to with . To see this, offer the menu to all types in . Type is indifferent between and . Type finds optimal. Therefore, any type between and finds optimal since has strict increasing differences. By construction,

Since is feasible to with , we have

Because are constant over each interval , by (A) and (A), we have

| (A.3) |

Then, it follows that

Taking on both sides gives property in the statement.

We now show property in the statement. It suffices to prove the weak convergence in . Let , be the CDFs of , . We have . Fix any . Note that in the stochastic dominance order, and hence

Let be such that . Note that

If , then we have

Otherwise, since , we have . Thus,

Hence, in either case, we have

Using (A), (A), and that is right-continuous, we have

Therefore, converges to pointwise, and hence . ∎

Proof of Lemma 6.

Recall is the set of IC and IR mechanisms for the one-dimensional type space . We want to show the following program has a solution:

We first show that it is without loss to restrict the range of to some interval for large enough. By the IR constraints, we have . By the IC constraints, for any , we have

Hence, for all ,

because if the above is violated at any type , the principal gets strictly less than

but that can be easily obtained by offering a single option. Thus, the claim holds for .

Then, (with the product topology); we use the notation . By the dominated convergence theorem, the objective is sequentially continuous on . It is clear that is nonempty. The existence result follows once we show is sequentially compact. Fix any sequence in . Let

be the equilibrium payoff of type . For any , by IC, we have

Therefore, is a monotone function (increase if necessary). Since has strict increasing differences, is also a monotone function. Note that are linearly ordered and sequentially compact sets. By the Helly’s selection theorem for monotone functions on linearly ordered sets (Fuchino and Plewik 1999, Theorem 7), there exists a subsequence that converges pointwise. Applying the same theorem again on , we obtain a subsubsequence that converges pointwise. Therefore,

also converges pointwise by continuity of . Thus, there exists some such that

in the product topology. Being the pointwise limit of measurable real-valued functions, is measurable; so is . Moreover, for any ,

by continuity of and that for all . Therefore, satisfies all IC constraints. Similarly, satisfies all IR constraints. So , and hence is sequentially compact. ∎

Completion of Proof of Theorem 2.

We complete the proof of Theorem 2 by filling in the details of Step 3 in Section 4.3.

Recall that we want to show the optimal value of (4) equals to . We first show it for Lipschitz continuous , and then extend it to all continuous . Without loss, we assume . Suppose for contradiction that there exist some feasible for (4) and some such that

Let . By Lusin’s theorem (see e.g. Aliprantis and Border 2006, Theorem 12.8), there exists a compact set such that are continuous on and . Since is compact, is attained. If , we augment by adding . Since is a singleton disjoint from the compact set , we have continuous on the augmented set as well. Since is IR, , and hence

where is the distribution of conditional on . We pick an approximation sequence for according to Lemma 5. By (A), for all large enough, we have

where is an optimal solution to the full IC problem with , and is the extension of to the right, as defined in the proof of Lemma 5. As in the proof of Lemma 5, satisfies all IC and IR constraints for type space . As in the proof of Lemma 6, (A) then holds for . By feasibility, (A), and (A), we have

In the last inequality, we have used that is a downward IC and IR mechanism for and that Theorem 2 holds for finite type spaces (see Step 2 in Section 4.3). Because are bounded and continuous on , and is continuous on the compact space , we have is bounded and continuous on . But, since in , taking limits on both sides of the above and using (A), we see that

which is a direct contradiction to (A).

Now we let be any continuous function on . Since is compact, as a consequence of the Stone–Weierstrass theorem (see e.g. Aliprantis and Border 2006, Theorem 9.13), the set of Lipschitz continuous real-valued functions on is dense in the space of continuous functions on (with the sup norm). Therefore, there exists a sequence of Lipschitz continuous functions converging uniformly to . Passing to a subsequence if necessary, we may assume that for all ,

Using the above and the earlier result applied to , we have for all ,

Taking then gives the desired inequality.

Completion of Proof of Theorem 1.

We first note that the argument in Section 4 holds for any compact , any measurable space , and any compact . Thus, we only need to generalize it to the case of imperfect correlation (stochastic monotonicity), where can also be potentially multidimensional.

We start by introducing the following lemma:

Lemma 7 (Measurable Monotone Coupling).

If is stochastically nondecreasing in , then there exist a measurable space ; an -valued random variable , independent of ; and a measurable function nondecreasing in the first argument such that

The proof of this lemma is in Section B.3, building on a result of Kamae and Krengel (1978).

Let be the decomposed monotonic path given a realization . For any type space , recall is the set of IC and IR mechanisms. Let . It then follows that

| (A.10) |

Because is independent of , the inner expectation integrates with respect to the same marginal distribution of regardless of the realization of .

By the proof in Section 4, we have that (i) for all realizations of ,