Multiple-prior valuation of cash flows subject to capital requirements

Abstract

We study market-consistent valuation of liability cash flows motivated by current regulatory frameworks for the insurance industry. Building on the theory on multiple-prior optimal stopping we propose a valuation functional with sound economic properties that applies to any liability cash flow. Whereas a replicable cash flow is assigned the market value of the replicating portfolio, a cash flow that is not fully replicable is assigned a value which is the sum of the market value of a replicating portfolio and a positive margin. The margin is a direct consequence of considering a hypothetical transfer of the liability cash flow from an insurance company to an empty corporate entity set up with the sole purpose to manage the liability run-off, subject to repeated capital requirements, and considering the valuation of this entity from the owner’s perspective taking model uncertainty into account. Aiming for applicability, we consider a detailed insurance application and explain how the optimisation problems over sets of probability measures can be cast as simpler optimisation problems over parameter sets corresponding to parameterised density processes appearing in applications.

1 Introduction

We consider the valuation of an aggregate insurance liability cash flow in run-off. The valuation approach is a direct consequence of considering a hypothetical transfer of the liability cash flow from an insurance company to an empty corporate entity set up with the sole purpose to manage the liability run-off. The owner of this entity needs to make sure at any time, in order to continue ownership of the entity, to pay claims and also to provide buffer capital according to the externally imposed solvency capital requirement (e.g. by a regulatory framework such as Solvency II). The owner accepts ownership given a suitable initial compensation from the original insurance company wanting to transfer its liabilities. This compensation determine the value of the liability cash flow. However, the owner has the right to, at any time, any surplus exceeding what is required to manage the liability run-off and meet solvency capital requirements. Therefore, the amount of compensation that the owner finds acceptable depends of the owner’s view of such surplus.

The setting and the valuation approach we consider are similar to those considered in Engsner et al. [13]. An essential difference here is that we acknowledge that an agent who assigns a value to possible future dividends and capital injections from managing a run-off of a liability may consider a valuation functional depending on a set of pricing measures, in the incomplete market setting, rather than a single one. The agent is uncertain about which pricing measure to use and may change view depending on new information. Although this appears to be a modest difference it on the one hand lead to significant mathematical challenges and on the other hand it means that the conservative valuation functional, corresponding to expected discounted values according to the worst pricing measure, can be applied to a wide range of liability cash flows rather than having to be chosen in order to match a specific type of liability cash flow. In order to make this statement clear we may think of cash flows from life insurance. If the agent benefits from survival of policyholders, then a conservative valuation from the agents perspective corresponds to choosing a pricing measure that assigns higher probability to the occurrences of deaths compared to . However, if the agent instead benefits from deaths of policyholders, then such a no longer corresponds to conservative valuation.

Insurance liability cash flows may be partly defined in terms of financial asset prices, specific interest rates or inflations indices. For liability cash flows where this is not the case, the cash flows may show significant correlation with market prices. Therefore, any insurance liability valuation methodology must be such not to introduce arbitrage opportunities and must consider replicating portfolios that hedge the financial component of a liability cash flow, whenever that is relevant. Consequently, there is a significant literature on market-consistent insurance valuation covering single-period, multiple-period and continuous-time valuation problems with varying assumptions on the financial market forming the basis for designing replicating portfolios of varying degrees of sophistication. We refer (in chronological order) to Grosen and Jørgensen [16], Malamud et al. [19], Wüthrich et al. [27], Möhr [20], Tsanakas et al. [26], Wüthrich and Merz [28], Pelsser and Stadje [21], Engsner et al. [14], Delong et al. [9], Barigou and Dhaene [3], Engsner et al. [13], and references therein.

A common theme in the literature on market-consistent insurance valuation is that the value assigned to a liability cash flow can be expressed as the sum of a market price of a replicating portfolio and a value assigned to the replication error (notice that a substantial replication error is a common feature of insurance liabilities). The liability values in this paper are also of this kind. Rebalancing times of a dynamic replicating portfolio means that the replication error has to be reassessed over time and taking this into consideration leads to the notion of time-consistent valuation. Similarly, repeated capital requirements lead to capital costs that are not known at the initial valuation time and taking such costs into account appropriately also require time-consistent valuation. Time consistency is a key concept in the literature on dynamic risk measurement. We refer (in chronological order) to Riedel [22], Detlefsen and Scandolo [11], Rosazza Gianin [25], Cheridito et al. [5], Artzner et al. [1], Bion-Nadal [4], Cheridito and Kupper [6], Cheridito and Kupper [7], and references therein.

In Artzner et al. [2] and Deelstra et al. [8] it is argued that diversifiable insurance risk should only be assigned a value corresponding to the -expectation of such risk since the law of large numbers applies if the insurance company may form arbitrarily large portfolios. In our setting this argument is not valid since the corporate entity to which the insurance company’s aggregate liability is transferred is a separate entity (referred to as reference undertaking in Solvency II) that may not be merged with other corporate entities. In that sense the entity to which the liabilities are transferred may be seen as a special purpose vehicle. Although this entity benefits from diversification when capital requirements are computed, it can not diversify the liability further.

Optimal stopping with multiple priors for agents assessing risk in terms of dynamic convex risk measures is analyzed in Cheridito et al. [5]. Similar problems are analyzed in Engelage [12], where the framework of optimal stopping with multiple priors in [23] is extended to so-called dynamic variational preferences. From an applied perspective: whereas all priors/probability measures in a given set of priors are treated as equally likely in the framework in Riedel [23], introducing (dynamic) penalty terms as in Cheridito et al. [5] and Engelage [12] means that the optimizing agent may assign different (dynamic) weights to the priors in the optimization problem. Optimal stopping is a key element in our approach to valuation since the owner of the entity managing the run-off of the liability, just as shareholders in general, has limited liability. At any time, taking the value of assets and future liability cash flows into account, if a capital injection is needed to meet capital requirements, the owner may choose between making a capital injection of not. Without such a capital injection, ownership is terminated and the the remaining assets are transferred to policyholders. Therefore, the rational owner determines optimal stopping times.

Although we assume that the replicating portfolio is chosen to ensure that the valuation of the liability cash flow is market consistent, we do not discuss market consistency in detail since this was treated in detail in Engsner et al. [13] and the material on market consistency in Engsner et al. [13] applies without any modification also in the present paper. However, we emphasise that we advocate choosing a replicating portfolio in agreement with what recommended by EIOPA in [10, Article 38] in Article 38(h) on the Reference Undertaking: ”the assets are selected in such a way that they minimise the Solvency Capital Requirement for market risk that the reference undertaking is exposed to”. The reference undertaking in Solvency II is similar in spirit to the corporate entity managing the run-off of the liability in the present paper.

The paper is organised as follows. Section 2 presents the valuation framework. Basic assumptions, notation and terminology are introduced in Subsection 2.1. Subsection 2.2 introduces the agents involved and explains how capital requirements and limited liability are key ingredients in the valuation philosophy that originates from the idea of a hypothetical transfer of an insurance company’s liabilities to an empty corporate entity. Definitions and results are presented in Subsection 2.2 for very general capital requirements. Subsection 2.3 then specialises by considering capital requirements given in terms of conditional monetary risk measures, in line with current regulatory frameworks. Section 3 presents a general construction of a parametric set of priors that cover natural choices for applications and shows that the set of priors satisfies the properties making it suitable for optimal stopping with multiple priors. Section 4 considers a specific insurance application that illustrates the use of the valuation framework and the results presented.

2 The valuation framework

2.1 Preliminaries

We consider time periods , corresponding time points , and a filtered probability space , where with , and denotes the real-world measure. For , we write for the normed linear space of -measurable random variables with norm . We write for the normed linear space of -measurable essentially bounded random variables. Equalities and inequalities between random variables should be interpreted in the -almost sure sense. A stopping time is a function such that for .

For two probability measures equivalent to and a stopping time , the probability measure , , is called the pasting of and in . It is often convenient to express the pasting of in in terms of the density processes with respect to ,

The density process given by

corresponds to the pasting of in . Equivalently, we can write

A set of probability measures equivalent to is called stable under pasting if for any and any stopping time , the pasting of in is an element in . We call such a set stable under pasting. Such sets are also referred to as m-stable, time consistent or rectangular in the related literature.

We assume the existence of a financial market containing assets for which -adapted price processes and , , are available. is the price process of a (predictable) locally riskless bond. The price processes correspond to traded assets for which reliable price quotes are available. We take the price process of the locally riskless bond as numéraire process and in what follows all financial values are discounted by this numéraire. This saves us from having to explicitly take interest rates processes into account and makes the mathematical expressions less involved. We will also allow for -adapted cash flows that depend on insurance events independent of the filtration generated by the traded assets. In particular, we consider an incomplete market setting. We assume that the set of equivalent martingale measures (for each , is equivalent to and the -discounted price processes are -martingales) is non-empty. By Proposition 6.43 in Föllmer and Schied [15] the set is stable under pasting. We will consider a non-empty subset . We refer to as a market risk neutral probability measure. We use the conventions and for sums over an empty index set and the infimum of an empty set. We use the notation .

2.2 Valuation with general capital requirements

We consider an insurance company with an aggregate insurance liability corresponding to a liability cash flow given by the -adapted stochastic process . Regulation forces the insurance company to comply with externally imposed capital requirements. The requirements put restrictions on the asset portfolio of the insurance company. A subset of the assets forms a replicating portfolio with -adapted cash flow intended to, to some extent, offset the liability cash flow. Depending on the degree of replicability of the liability cash flow, the replicating portfolio could be anything from simply a position in the numéraire asset to a portfolio that is rebalanced dynamically according to some strategy. is the residual liability cash flow. We will, in accordance with current solvency regulation (Möhr [20] and prescribed by EIOPA, see [10, Article 38]) define the value of the liability cash flow by considering a hypothetical transfer of the liability and the replicating portfolio to a separate entity referred to as a reference undertaking. The reference undertaking has initially neither assets nor liabilities and its sole purpose is to manage the run-off of the liability. The benefit of ownership is the right to receive certain dividends/surplus, defined below, until either the run-off of the liability cash flow is complete or until letting the reference undertaking default on its obligations to the policyholders. The term default means termination of ownership of the reference undertaking. The precise details are as follows,

-

•

At time : The liabilities corresponding to the cash flow , the replicating portfolio corresponding to the cash flow and an amount in the numéraire are supposed to be transferred from the insurance company to the reference undertaking, where is the amount making the reference undertaking precisely meet the externally imposed capital requirement. In return, an agent aspiring ownership of the reference undertaking must first pay the original insurance company an amount corresponding to the value of receiving future dividends resulting from managing the run-off of the liability. In case there are several agents aspiring ownership, the one offering the highest amount wins the ownership.

In summary: the new owner of the reference undertaking receives compensation from the original insurance company as compensation for accepting to receive the liabilities and replicating portfolio and agreeing to manage the liability run-off.

-

•

At time : By paying the amount to the original insurance company, the owner receives full ownership of the reference undertaking. However, the cash-flow of the replicating portfolio (possibly defined in terms of a dynamic strategy) cannot be modified by the owner, for instance in order to boost dividend payments in a way that may not be in the interest of policyholders.

-

•

At time : The owner has the option to either default on its obligations to the policyholders or not to default.

The decision to default means to give up ownership and transfer and the replicating portfolio to the policyholders. The owner neither receives any dividend payment nor incurs any loss upon a decision to default.

If and given the decision not to default, a new amount in the numéraire asset is needed to make the reference undertaking precisely meet the externally imposed capital requirement. If , then the positive surplus is paid to the owner and , which the policyholders are entitled to, is paid to the policyholders. If , then the owner faces a deficit that must be offset by injecting . Also in this case is paid to the policyholders.

If , then the above description of cash flows to policyholders and owner applies upon setting .

-

•

At time : If the owner has not defaulted on its obligations, then the situation is completely analogous to that at time described above.

From the above follows that the owner of the reference undertaking has to decide on a decision rule defining under which circumstances default occurs. The default time is a stopping time , where denotes the set of stopping times taking values in . The event is to be interpreted as a complete liability run-off without default at any time. Formally, .

The cumulative cash flow to the owner can be written as

| (1) |

For ease of notation, define the payoff process by

| (2) |

Note that this payoff process is predictable. The conservative value of the cash flow (1) is

| (3) |

We assume that the owner of the reference undertaking chooses a default time maximizing the value (3). Consequently, the value at time of the reference undertaking is

| (4) |

For , the value of the reference undertaking at time , given no default at times , is given by the completely analogous expression upon replacing and in (4) by the essential supremum and essential infimum (see Appendix A.5 in Föllmer and Schied [15] for details) and conditioning on rather than . Notice that since no cash flows occur at times , the value of the reference undertaking is zero at time . The value of the reference undertaking can thus be identified as the value of an American type derivative. Details on arbitrage-free pricing of American derivatives can be found in Section 6.3 in [15].

Since we are considering sets of probability measures we need the cash flows to be suitably integrable with respect to all . The following notion of uniform integrability, from Riedel [23], will be used. The process in (2) is bounded by a -uniformly integrable random variable in the sense that there exists such that

| (5) |

We now define the value of the reference undertaking, corresponding to what an external party would pay to become owner of the entity managing the run-off of the liability, and also the value of the residual liability. The sum of the latter and the market price of the replicating portfolio is the value of the original liability to policyholders and therefore is a theoretical aggregate premium.

Definition 1.

Let be a set of market risk neutral probability measures. Consider sequences and with for for every , and for for every . Define and, for ,

| (6) |

is the value of the reference undertaking at time given no default at times . is the value of the residual liability at time given no default at times .

Notice that

The general upper bound

| (7) |

does neither depend on the filtration nor on the capital requirements, and is typically much easier to compute than . Therefore, this upper bound provides a useful conservative estimate of . This statement is illustrated in the numerical example in Section 4. Notice that in general

| (8) |

In particular, the general lower bound

| (9) |

may be attractive since it is typically easier to compute than , see Section 4 for an illustration. Computing means solving a standard optimal stopping problem for each followed by finding the maximum of the obtained values .

Notice that the value of the original liability cash flow follows directly from the procedure for transferring the liabilities and replicating portfolio to an external party (the new owner of the reference undertaking) accepting the transfer: equals the sum of the market value of the replicating portfolio and the value of the residual liability:

where is any market risk neutral probability measure making the expectation equal the market value of the replicating portfolio. For details on the market consistency of the value we refer to the material on market consistency in Engsner et al. [13].

We intend to build on the theory of multiple prior optimal stopping in Riedel [23] where four assumptions on a set of probability measures are imposed in order for key results to hold. These assumptions are -uniform integrability together with properties (i)-(iii) of the following definition.

Definition 2.

A set of probability measures is suitable for multiple prior optimal stopping if the following properties hold. (i) Each is equivalent to ; (ii) is stable under pasting; (iii) For each ,

is weakly compact in .

Remark 1.

If satisfies the properties (i)-(iii) in Definition 2, then it follows from Theorem 2 in Riedel [23] that the lower bound in (9) equals . This holds since for such the inequality in (8) is in fact a minimax identity. Notice also that for an arbitrary equivalent to , satisfies properties (i)-(iii) in Definition 2.

As a basis for applying the theory to be presented, we will later in Section 3 explicitly construct a useful set satisfying the properties in Definition 2 and present a detailed numerical example in Section 4.

We are now ready to state a key result which shows that defined in terms of a multiple prior optimal stopping problem may equivalently be defined as the solution to a backward recursion.

Theorem 1.

Let be a set of probability measures satisfying properties (i)-(iii) of Definition 2. Consider sequences , , with for for every , and for for every . Set and assume that in (2) is bounded by a -uniformly integrable random variable. Then

(i) If the sequences and are given by Definition 1, then

| (10) | ||||

| (11) |

Remark 2.

Stability under pasting of is a necessary requirement in Theorem 1. However, we show later in Theorem 6 that instead of the weak compactness property (iii) in Definition 2, which is assumed in Theorem 1, it is sufficient to verify weak relative compactness together with some natural additional properties. Notice that a bounded and uniformly integrable subset of is weakly relatively compact in (Theorem A.70 in [15]). Without weak compactness we can however not guarantee that there exists a which solves the optimization problems (10) and (11).

Proof of Theorem 1.

We will first consider the problem

| (12) |

We define the multiple prior Snell envelope of with respect to as in [23] by

| (13) |

We know from Theorem 1 in [23] that

| (14) |

and that is an optimal stopping time that solves (12). Define by

We claim that the relation holds. Indeed, from (14),

Therefore, from (13), we have the relation

Since this holds for arbitrary adapted , the claim is proved and gives

Hence, we have shown (10) from which (11) is an immediate consequence. This concludes the proof of statement (i). ∎

2.3 Valuation with capital requirements by conditional monetary risk measures

We now consider the valuation problem in the setting where the capital requirements are given in terms of conditional monetary risk measures.

Definition 3.

For and , a conditional monetary risk measure is a mapping satisfying

| (15) | |||

| (16) | |||

| (17) |

A sequence of conditional monetary risk measures is called a dynamic monetary risk measure.

The natural conditional monetary risk measures corresponding to current regulatory frameworks are defined in terms of conditional quantile functions. For integer , , and -measurable , let

and define the conditional versions of value-at-risk and average value-at-risk as

Both and are conditional monetary risk measures in the sense of Definition 3 for . Given conditional monetary risk measures we consider here

| (18) |

Notice that if is given and is given by Definition 1, then also is given and therefore is well defined by setting . Moreover, we may write

| (19) |

where

Theorem 2.

Proof of Theorem 2.

Theorem 2 has consequences that should be seen as necessary requirements of any sound valuation method. If for some constant , then the corresponding value . If we consider two residual liability cash flows and such that for every , then the corresponding values satisfy . Similarly, if the sequence of conditional monetary risk measures are replaced by a more prudent choice such that for every , then the corresponding values satisfy .

Let be given by , where ,

where is a suitable conditional monetary risk measure such as or . It is reasonable to require that is a -supermartingale which is equivalent to which implies . In particular, the -supermartingale property guarantees the existence of a nonnegative “risk margin” .

Theorem 3.

Let for . Let , for , be a conditional monetary risk measure such that

| (23) |

Then there exists a set of probability measures such that is a -supermartingale.

Proof of Theorem 3.

Notice that the supermartingale requirement is equivalent to

| (24) |

It is sufficient to find some such that the statement holds for . We construct this by defining a suitable -martingale corresponding to the change of measure from to .

Let , let denote the -conditional distribution function of , and let . Let , with , be a -martingale satisfying

where is independent of and uniformly distributed on and, conditional of , and are countermonotone. Let be some -measurable random variable satisfying

By construction,

Moreover, on ,

∎

Property (23) in Theorem 3 is satisfied by which is an example of so-called strictly expectation bounded risk measures, see Definition 5 and Example 3 in Rockafellar et al. [24].

The following lemma is useful for constructing a bounding -uniformly integrable random variable.

Lemma 1.

For any -uniformly integrable , is a -uniformly integrable random variable.

Proof of Lemma 1.

We need to show that

If we set , then is -uniformly integrable since it is of the form . Hence by the law of iterated expectations for -uniformly integrable random variables (Lemma 1 in [23]),

Notice that since for any ,

and, due to -uniformly integrability of , we may choose to make the second term on the right-hand side sufficiently small. Since

the events satisfy as . For any and ,

| (25) |

Consider a sequence such that and as . Applying this sequence to (25), taking the supremum over and letting proves the statement of the lemma. ∎

The following theorem says that if the conditional monetary risk measures defining in (18) satisfy natural and verifiable bounds, then statements in Theorem 1 hold also in this setting.

Theorem 4.

Let be a set of probability measures satisfying properties (i)-(iii) of Definition 2. Consider sequences , , with for for every , and for for every . Let and let be defined by (18). Assume that is -uniformly integrable. If the conditional monetary risk measures in (18) satisfy either

| (26) |

or

| (27) |

then defined in (2) satisfies that is bounded by a -uniformly integrable random variable. In particular, the statements in Theorem 1 hold.

Proof of Theorem 4.

Set

By Lemma 1 all variables are -uniformly integrable. We will show by induction that, for all , there exist constants such that

| (28) |

from which the statement of the theorem follows. Note that (28) trivially holds for . In order to show the induction step, assume that (28) holds with replaced by . If (27) holds, then

where the law of iterated expectations for -uniformly integrable random variables (Lemma 1 in [23]) was used in the last step. If (26) holds, then similarly

We also note that

which implies . We have proved that (28) holds, i.e. the induction step. By the induction principle (28) holds for all and the proof is complete. ∎

3 Construction of sets of probability measures for multiple prior optimal stopping

Our aim here is to define a useful set of parametric probability measures that enables the analysis of a wide range of models and that provide solutions to the multiple-prior optimization problem (6). In particular, the set constructed below will imply that optimization over can be reduced to optimization over the set of parameters, see Theorem 6 for the precise statement.

We will define a useful set of probability measures, satisfying all the requirements for applying key results on multiple prior optimal stopping, by defining the corresponding set of density processes of the form

where is a set of parameters and and are defined below.

On , a probability measure absolutely continuous with respect to corresponds to a Radon-Nikodym derivative and together with the filtration give rise to the density process given by . Similarly, a set of probability measures, absolutely continuous with respect to , corresponds to the set of Radon-Nikodym derivatives. Write for the closure of and let be the set of probability measures corresponding to the Radon-Nikodym derivatives . For two probability measures with Radon-Nikodym derivatives the Radon-Nikodym derivative of the pasting of in is

The following result is both of independent interest and will be relevant for constructing stable sets of probability measures, depending on a parameter, that are useful for multiple prior optimal stopping problems.

Theorem 5.

Given , let be a set of probability measures equivalent to that is convex and stable under pasting. Let be the corresponding set of Radon-Nikodym derivatives and let be the closure of . Let and . Then

-

(i)

The set corresponding to is convex and stable under pasting.

-

(ii)

For each , is convex and closed in .

-

(iii)

If is -uniformly integrable, then for each , is weakly relatively compact in and is weakly compact in .

-

(iv)

If is -uniformly integrable, then, for any -measurable -uniformly integrable random variable ,

and similarly with replaced by .

Remark 3.

Since for (and similarly for ), by Lemma 4.10 in Kallenberg [17], is uniformly integrable if

(and similarly for ).

Proof of Theorem 5.

For both statements and , it is straightforward to verify that convexity holds so we only prove the remaining claims.

To prove , consider any stopping time and . Take such that and in . Since and is stable under pasting, the Radon-Nikodym derivative of the pasting of in is also an element in . Therefore, statement (i) is proved if we show that there exists a subsequence such that

| (29) |

Since, for ,

we see that in . Since convergence in implies convergence in probability which in turn implies a.s. convergence along some subsequence , we have

where we used the fact that and are strictly positive a.s. Since the terms of the sequence on the left-hand side are positive and all have expected values equal to , this sequence is uniformly integrable. Therefore, by Proposition 4.12 in [17], the a.s. convergence can be replaced by convergence in , i.e. (29) holds.

We now prove . Consider an convergent sequence with limit . We will prove that . Take an arbitrary and let . Set

By construction and in . Hence, . Since and in the proof of is complete.

We now prove . From and follow that is convex and stable under pasting and, for each , is a convex and closed subset of . A convex and closed subset of is weakly closed (Theorem A.63 in [15]). A bounded and uniformly integrable subset of is weakly relatively compact (Theorem A.70 in [15]). Each is a bounded subset of :

Hence, weak relative compactness of follows if is uniformly integrable. Similarly for . Moreover, is uniformly integrable if is uniformly integrable, as the following argument shows. By Lemma 4.10 in [17], since , is -uniformly integrable if and only if . If the latter holds, then in particular which is equivalent to

Hence, is -uniformly integrable if is -uniformly integrable. By the same argument, is uniformly integrable if is uniformly integrable. However, is uniformly integrable since it is the closure of a uniformly integrable set in . Hence, is weakly compact in for every . The proof of is complete.

It remains to prove . Notice first that

Take and with in . Therefore, which implies . Moreover, since , and

and convergence in implies convergence in probability. Since is -uniformly integrable, is -uniformly integrable. Therefore, implies in . This further implies that in since

In particular,

which implies that there exists a subsequence such that

Therefore, for any ,

The same argument shows the corresponding identity for . The proof is complete. ∎

Consider a parameter set which is taken to be a subset of a complete and separable metric space. For each , let be a measurable function on such that is -measurable for each . It is assumed that the -measurable random variables satisfy

| (30) | |||

| (31) |

For each , let be an -measurable random element in the space of probability measures on equipped with the topology of weak convergence. Let be the set of all such random probability measures. For for all , let

| (32) |

Notice that, due to properties (30) and (31), is a positive -martingale with . Let

and let be the -closure of . For , let

and let and be defined analogously.

Definition 4.

Denote by the sets of probability measures corresponding to the sets of Radon-Nikodym derivatives with respect to .

Notice that corresponds to only considering measures in (32). We will show in Theorem 6 that has the properties assumed in Theorem 1. We also show that Theorem 1 holds also for .

Theorem 6.

Consider the sets and in Definition 4.

-

(i)

The sets and are convex and stable under pasting.

-

(ii)

For every , is closed in .

-

(iii)

If is -uniformly integrable, then is weakly relatively compact in and is weakly compact in for every .

-

(iv)

If is -uniformly integrable, then, for any -measurable -uniformly integrable random variable ,

and similarly with replaced by .

Proof of Theorem 6.

We first prove . We first prove convexity and stability under pasting for the set of probability measures with Radon-Nikodym derivatives with respect to . We first prove convexity. Note that for a density process with ,

Consider density processes with , let and set . Then

and the convexity property follows since

We now prove stability under pasting. Consider density processes with , and let be a stopping time. Then

and since are -measurable,

which proves stability under pasting. Theorem 5 completes the proof of .

Notice that follows immediately from together with Theorem 5. Similarly, follows immediately from together with Theorem 5.

It remains to prove . The two last identities in follow from the definition of and :

The first identity follows from Theorem 5. The proof is complete. ∎

4 Gaussian example

In this section we consider an application illustrating the general theory presented up to this point. We consider a setting where the liability cash flow is Gaussian, both under and under any . We consider two cases:

-

Case 1

In this case we assume that . Recall that is not stable under pasting: this decision maker does not consider probability measures corresponding to switching between probability measures in depending on information revealed over time.

-

Case 2

In this case we assume that . This decision maker exhibits a behaviour that is time consistent. Notice that is considerably larger than .

The liability cash flow is assumed to be fully nonhedgeable by financial assets and consequently we take which means that . In order to make the illustration clear, we choose . Let denote the exposure adjusted cumulative amount of payments to policyholders for accident year , where is a known exposure measure for accident year . The evolution of the exposure adjusted cumulative amounts is assumed to satisfy

where all are independent and with respect to . Suppose that we are uncertain about the parameter values and want to consider probability measures , , such that

where all are independent and with respect to . We choose a parameter set that describes the uncertainty about the parameter values.

Suppose that with are observed at time and that with , , are observed at times and therefore contain cash flows that are part of the outstanding liability to the policyholders. The (incremental) liability cash flow is given by

Notice that is here considered to be a known constant. Direct computations give

The filtration is given by the -algebras , and . In order to have the correct evolution with respect to of the cumulative amounts it is seen that we must require that

This corresponds to, in the setting of Section 3, choosing

| (33) | ||||

where denotes the density function of . By Remark 3, the set is -uniformly integrable if

which holds here since and both take values in bounded intervals bounded away from . The sets are of type for measurable sets such that . Therefore, it follows from Theorem 6 that the set in Definition 4 satisfies the requirements for multiple prior optimal stopping. In particular, Theorem 1 holds with .

can be chosen to reflect parameter uncertainty. To illustrate how such a choice may be implemented, consider the regression estimators from Lindholm et al.[18] based on data from accident years :

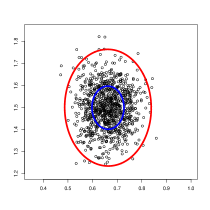

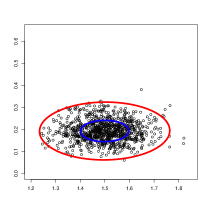

Here denotes the index of the first accident year observed. These estimators are unbiased and uncorrelated. We now proceed with a numerical illustration, with parameter values , , and for . Based on these parameter values and a large number of simulated independent standard normal , leading to iid copies of , we estimate times. Figure 1 presents scatter plots, which suggests that the iid vectors of estimators are approximately -distributed, where and are the sample mean and sample covariance matrix. We can therefore shape an approximative confidence region with confidence level of the parameter values by the squared Mahalanobis distance as

where is the (lower triangular) Cholesky decomposition of , is the distribution function of the and is the unit sphere in . For the evaluation at time 1, only needs to be considered, leading to a set satisfying that

is the orthogonal projection of onto the coordinate plane: . Explicitly,

where is the unit sphere in , is the subvector of the last two entries of and is the Cholesky decomposition of the submatrix of . Similarly, to compute the upper bound of in (34), only need to be considered, leading to a similar set .

The left plot in Figure 1 shows a scatted plot of iid estimates of together with boundaries for (blue) and for (red). The right plot in Figure 1 shows a scatted plot of iid estimates of together with boundaries for (blue) and for (red).

Let be conditional monetary risk measures defined in terms of conditional quantiles with respect to , such as, for , or . In both cases, is a constant for an -measurable and independent of with respect to . Then

4.1 Case 1: computing upper and lower bounds for

In this case does not satisfy the conditions of Theorem 1 and therefore we can not compute by backward recursion. However, upper and lower bounds for are easily computed. From (7) we have the upper bound

| (34) |

From (9) we have the lower bound

In the setting of Section 3, for each , with , we solve the backward recursion

and then compute

Notice that corresponds to the quantities in the special case . Computing is simpler than computing since the former involves just one optimisation over the parameter set rather than nested optimisations for the latter.

We now demonstrate how is computed in the current Gaussian setting. As shown above (which does not depend on ) and

where with respect to and independent of , and

Straightforward calculations show that

Consequently,

from which can be estimated with arbitrary accuracy by simulating iid copies of with respect to and computing the empirical estimate, and can be estimated similarly by simulating iid copies with respect to and approximating the expectation by the empirical mean. Finally,

Table 1 shows numerical values for lower bounds and for upper bounds . These values are based on , , with and parameters sets of varying size corresponding to with . The main message of Table 1 is that the intervals are very narrow for small and therefore the upper bound is an accurate estimate of when is small. Notice that the upper bound is both easily computed and has attractive theoretical properties.

4.2 Case 2: computing and an upper bound for

In this case and the general lower bound coincides with and therefore its computation by backward recursion is somewhat involved. However, the upper bound is still fairly straightforward to compute. Notice that the lower bound computed for Case 1 is a lower bound for in the current Case 2 since .

We begin by computing the upper bound using the law of iterated expectations, extended to the multiple prior setting, and Theorem 6:

Notice that, with ,

where and similarly for . Therefore,

is calculated explicitly as above. Computing means computing

where, with some abuse of notation, we consider to be defined for parameters rather than . In practice, this means determining a function such that for suitably many simulated iid copies of and approximating . Given the choice of , is approximated by its empirical estimate based on simulated iid copies with respect to of

Similarly, is approximated by, for each in a dense subset of , simulating iid copies with respect to of

estimating by the empirical mean, and computing the minimum of these expectations over the values. Finally, is estimated by the difference of the estimates of and .

Table 1 shows numerical values for lower bounds and for upper bounds with the same parameter values as those considered for Case 1. Similarly to Case 1, the intervals are very narrow for small and therefore the upper bound is an accurate estimate of when is small.

References

- [1] Artzner, P., Delbaen, F., Eber, J.-M., Heath, D., Ku, H.: Coherent multiperiod risk adjusted values and Bellman’s principle. Annals of Operations Research 152, 5-22, 2007

- [2] Artzner, P., Eisele, K.-T., Schmidt, T.: No arbitrage in insurance and the QP-rule. Available at SSRN: https://ssrn.com/abstract=3607708 or http://dx.doi.org/10.2139/ssrn.3607708

- [3] Barigou, K., Dhaene, J.: Fair valuation of insurance liabilities via mean variance hedging in a multi period setting. Scandinavian Actuarial Journal 2019, 163-187, 2019

- [4] Bion-Nadal, J.: Dynamic risk measures: Time consistency and risk measures from BMO martingales. Finance and Stochastics 12, 219-244, 2008

- [5] Cheridito, P., Kupper, M., Delbaen, F.: Dynamic monetary risk measures for bounded discrete-time processes. Electronic Journal of Probability 11, 57-106, 2006

- [6] Cheridito, P., Kupper, M.: Recursiveness of indifference prices and translation-invariant preferences. Mathematics and Financial Economics 2, 173-188, 2009

- [7] Cheridito, P., Kupper, M.: Composition of time-consistent dynamic monetary risk measures in discrete time. International Journal of Theoretical and Applied Finance 14, 137-162, 2011

- [8] Deelstra, G., Devloder, P., Gnameho, K., Hieber, P.: Valuation of hybrid financial and actuarial products in life insurance by a novel three-step method. ASTIN Bulletin 50, 709-742, 2020

- [9] Delong, L., Dhaene, J., Barigou, K.: Fair valuation of insurance liability cash-flow streams in continuous time: Theory. Insurance: Mathematics and Economics 88, 196-208, 2019

- [10] European Commission: Commission Delegated Regulation (EU) 2015/35 of 10 October 2014. Official Journal of the European Union, 2015

- [11] Detlefsen, K., Scandolo, G.: Conditional and dynamic convex risk measures. Finance and Stochastics 9, 539-561, 2005

- [12] Engelage, D.: Optimal stopping with dynamic variational preferences. Journal of Economic Theory 146, 2042-2074, 2011

- [13] Engsner, H., Lindensjö, K., Lindskog, F.: The value of a liability cash flow in discrete time subject to capital requirements. Finance and Stochastics 24, 125-167, 2020

- [14] Engsner, H., Lindholm, M., Lindskog, F.: Insurance valuation: A computable multi-period cost-of-capital approach. Insurance: Mathematics and Economics 72, 250-264, 2017

- [15] Föllmer, H., Schied, A.: Stochastic Finance: An Introduction in Discrete Time, 4th edn. Walter de Gruyter, 2016

- [16] Grosen, A., Jørgensen, P. L.: Life insurance liabilities at market value: an analysis of insolvency risk, bonus policy, and regulatory intervention rules in a barrier option framework. Journal of Risk and Insurance 69, 63-91, 2002

- [17] Kallenberg, O.: Foundations of Modern Probability, 2nd edn. Springer (2002)

- [18] Lindholm, M, Lindskog, F, Wahl, F: Valuation of non-life liabilities from claims triangles. Risks 5(3), 2017

- [19] Malamud, S., Trubowitz, E., Wüthrich, M. V.: Market consistent pricing of insurance products. ASTIN Bulletin 38, 483-526, 2008

- [20] Möhr, C.: Market-consistent valuation of insurance liabilities by cost of capital. ASTIN Bulletin 41, 315-341, 2011

- [21] Pelsser, A., Stadje, M.: Time-consistent and market-consistent evaluations. Mathematical Finance 24, 25-65, 2014

- [22] Riedel, F.: Dynamic coherent risk measures. Stochastic Processes and their Applications 112, 185-200, 2004

- [23] Riedel, F.: Optimal stopping with multiple priors. Econometrica 77, 857-908, 2009

- [24] Rockafellar, R. T., Uryasev, S., Zabarankin, M.: Generalized deviations in risk analysis. Finance and Stochastics 10 51-74, 2006

- [25] Rosazza Gianin, E.: Risk measures via g-expectations. Insurance: Mathematics and Economics 39, 19-34, 2006.

- [26] Tsanakas, A., Wüthrich, M. V., C̆erný, A.: Market value margin via mean-variance hedging. ASTIN Bulletin 43, 301-322, 2013

- [27] Wüthrich, M. V., Embrechts, P., Tsanakas, A.: Risk margin for a non-life insurance runoff. Statistics and Risk Modeling 28, 299-317, 2011

- [28] Wüthrich, M. V., Merz, M.: Financial Modeling, Actuarial Valuation and Solvency in Insurance. Springer, 2013