Revisiting Event Study Designs:

Robust and Efficient Estimation

Abstract

We develop a framework for difference-in-differences designs with staggered treatment adoption and heterogeneous causal effects. We show that conventional regression-based estimators fail to provide unbiased estimates of relevant estimands absent strong restrictions on treatment-effect homogeneity. We then derive the efficient estimator addressing this challenge, which takes an intuitive “imputation” form when treatment-effect heterogeneity is unrestricted. We characterize the asymptotic behavior of the estimator, propose tools for inference, and develop tests for identifying assumptions. Our method applies with time-varying controls, in triple-difference designs, and with certain non-binary treatments. We show the practical relevance of our results in a simulation study and an application. Studying the consumption response to tax rebates in the United States, we find that the notional marginal propensity to consume is between 8 and 11 percent in the first quarter — about half as large as benchmark estimates used to calibrate macroeconomic models — and predominantly occurs in the first month after the rebate.

1 Introduction

Event studies are one of the most popular tools in applied economics and policy evaluation. An event study is a difference-in-differences (DiD) design in which a set of units in the panel receive treatment at different points in time. In this paper, we investigate the robustness and efficiency of estimators of causal effects in event studies, with a focus on the role of treatment effect heterogeneity. We first develop a simple econometric framework that delineates the identification assumptions from each other and from the estimation target, defined as some average of heterogeneous causal effects. We then apply this framework in three ways. First, we analyze the conventional practice of implementing event studies via two-way fixed effect Ordinary Least Squares (TWFE OLS) regressions and show how the implicit conflation of different assumptions leads to biases. Second, leveraging event study assumptions in an explicit and principled way allows us to derive the robust and efficient estimator, along with appropriate inference methods and tests. The estimator takes an intuitive “imputation” form when treatment-effect heterogeneity is unrestricted. Finally, we illustrate the practical relevance of our approach in an application estimating the marginal propensity to spend (MPX) out of tax rebates; our MPX estimates are lower than in prior work, implying that fiscal stimulus is less powerful than commonly thought.

Event studies are frequently used to estimate treatment effects when treatment is not randomized, but the researcher has panel data allowing them to compare outcome trajectories before and after the onset of treatment, as well as across units treated at different times. By analogy to conventional DiD designs without staggered rollout, event studies are commonly implemented by two-way fixed effect regressions, such as

| (1) |

where outcome and binary treatment are measured in periods and for units , are unit fixed effects (FEs) that allow for different baseline outcomes across units, and are period fixed effects that accommodate overall trends in the outcome. Specifications like Equation 1 are meant to isolate a treatment effect from unit- and period-specific confounders. A commonly-used dynamic version of this regression includes “lags” and “leads” of the indicator for the onset of treatment, to capture treatment effects for different “horizons” since the onset of treatment and test for the parallel trajectories of the pre-treatment outcomes.

To understand the problems with conventional two-way fixed effect estimators in event-study designs and provide a principled econometric approach to overcoming these issues, in Section 2 we develop a simple framework that makes the estimation targets and underlying assumptions explicit and clearly isolated. We suppose that the researcher chooses a particular weighted average (or weighted sum) of heterogeneous treatment effects they are interested in estimating. We make (and later test) two standard DiD identification assumptions: that potential outcomes without treatment are characterized by parallel trends and that there are no anticipatory effects. We also allow for — but do not require — an auxiliary assumption that the treatment effects themselves follow some model that restricts their heterogeneity for a priori specified economic reasons. This explicit approach is in contrast to regression specifications like Equation 1, both static and dynamic, which implicitly conflate choices of estimation target and identification assumptions. Our framework covers a broad class of empirically relevant estimands beyond the standard average treatment-on-the-treated (ATT), including heterogeneous treatment effects by observed covariates and ATTs at different horizons that hold the composition of units fixed.

Through the lens of this framework, in Section 3 we uncover a set of challenges with conventional event-study estimation methods and trace them back to a mismatch between estimation target, identification assumptions, and the flexibility of the regression specification. First, we note that failing to rule out anticipation effects in “fully-dynamic” specifications (with all leads and lags of the event included) leads to an underidentification problem when there are no never-treated units, such that the dynamic path of anticipation and treatment effects over time is not point-identified. We conclude that it is important to separate out testing the assumptions about pre-trends from the estimation of dynamic treatment effects under those assumptions. Second, implicit assumptions of homogeneous treatment effects embedded in static DiD regressions like Equation 1 may lead to estimands that put negative weights on some long-run treatment effects. With staggered rollout, regression-based estimation leverages comparisons between groups that got treated over a period of time and reference groups which had been treated earlier. We label such cases “forbidden comparisons.” Indeed, these comparisons are only valid when the homogeneity assumption is true; when it is violated, they can substantially distort the weights the estimator places on treatment effects, or even make them negative. Third, in dynamic specifications, implicit assumptions about treatment effect homogeneity across groups first treated at different times lead to the spurious identification of long-run treatment effects for which no DiD comparisons valid under heterogeneous treatment effects are available. The last two challenges highlight the danger of imposing implicit treatment effect homogeneity assumptions instead of allowing for heterogeneity and explicitly specifying the target estimand. We show that these challenges are not resolved by trimming the sample to a fixed window around the event date.

From the above discussion, the reader should not conclude that event study designs are plagued by fundamental problems. On the contrary, these challenges only arise due to a mismatch between treatment effect heterogeneity and specifications which restrict it. We therefore use our framework to circumvent these issues and derive robust and efficient estimators.

In Section 4, we first establish a simple characterization for the most efficient linear unbiased estimator of any pre-specified weighted sum of treatment effects, in the baseline case of spherical errors, i.e. homoskedasticity with no serial correlation. This estimator explicitly incorporates the researcher’s estimation goal and assumptions about parallel trends, anticipation effects, and restrictions on treatment effect heterogeneity. It is constructed by estimating a flexible high-dimensional regression that differs from conventional event study specifications, and aggregating its coefficients appropriately. While spherical errors are a natural starting point, the principled construction of this estimator more generally ensures unbiasedness and yields attractive efficiency properties, as we later confirm in simulations.

In our leading case where the heterogeneity of treatment effects is not restricted, the efficient robust estimator can be implemented using a transparent “imputation” procedure. First, the unit and period fixed effects and are fitted by regressions using untreated observations only. Second, these fixed effects are used to impute the untreated potential outcomes and therefore obtain an estimated treatment effect for each treated observation. Finally, a weighted sum of these treatment effect estimates is taken, with weights corresponding to the estimation target.

To relate our efficient imputation estimator to other unbiased estimators that have been proposed in the literature, we derive two additional results showing the generality of the imputation structure. First, any other linear estimator that is unbiased in our framework with unrestricted causal effects can be represented as an imputation estimator, albeit with an inefficient way of imputing untreated potential outcomes. Second, even when assumptions that restrict treatment effect heterogeneity are imposed, any unbiased estimator can still be understood as an imputation estimator for an adjusted estimand. Together, these two results allow us to characterize estimators of treatment effects in event studies as a combination of how they impute unobserved potential outcomes and which weights they put on treatment effects.

For the efficient estimator in our framework, we provide tools for valid inference. Specifically, we derive conditions under which the estimator is consistent and asymptotically normal and propose standard error estimates. Inference is challenging under arbitrary treatment effect heterogeneity, because causal effects cannot be separated from the error terms. We instead show how asymptotically conservative standard errors can be derived, by attributing some variation in estimated treatment effects to the error terms.111While the generality of our setting only allows for conservative inference (on any robust estimator, including ours), we obtain asymptotically exact standard errors in the special case that received the most attention in the literature: when units are randomly sampled from a population and the estimand consists of average treatment effects by period–cohort pairs. Our inference results apply under mild conditions in short panels. Advancing the existing literature on DiD estimation with staggered adoption, we also provide conditions for consistency and inference that extend to panels where the number of time periods grows, as long as growth is not too fast. We also propose a leave-one-out modification to our conservative variance estimates with improved finite-sample performance.

Another important practical advantage of our approach is that it provides a principled way of testing the identifying assumptions of parallel trends and no anticipation effects, based on OLS regressions with untreated observations only. Compared to conventional specifications with leads and lags of treatment that implicitly restrict treatment effects, this approach avoids the contamination of the tests by treatment effect heterogeneity shown by [60]. Moreover, our strategy circumvents the inference problems after pre-testing that were pointed out by [37], under spherical errors. These attractive properties result from the clear separation of estimation and testing.

It is also useful to point out two limitations of our analysis. First, all event study designs assume a restrictive parametric model for untreated outcomes. We do not evaluate when these assumptions may be applicable, and therefore when the event study design are ex ante appropriate, as [39] do. We similarly do not consider estimation that is robust to violations of parallel-trend type assumptions, as [36] propose, although our framework allows relaxing those assumptions by including unit-specific trends and time-varying covariates. We instead take the standard assumptions of event study designs as given and derive optimal estimators, valid inference, and practical tests to assess whether parallel-trend assumptions hold. Second, we also do not consider event studies as understood in the finance literature, based on high-frequency panel data, which typically do not use period fixed effects [32].

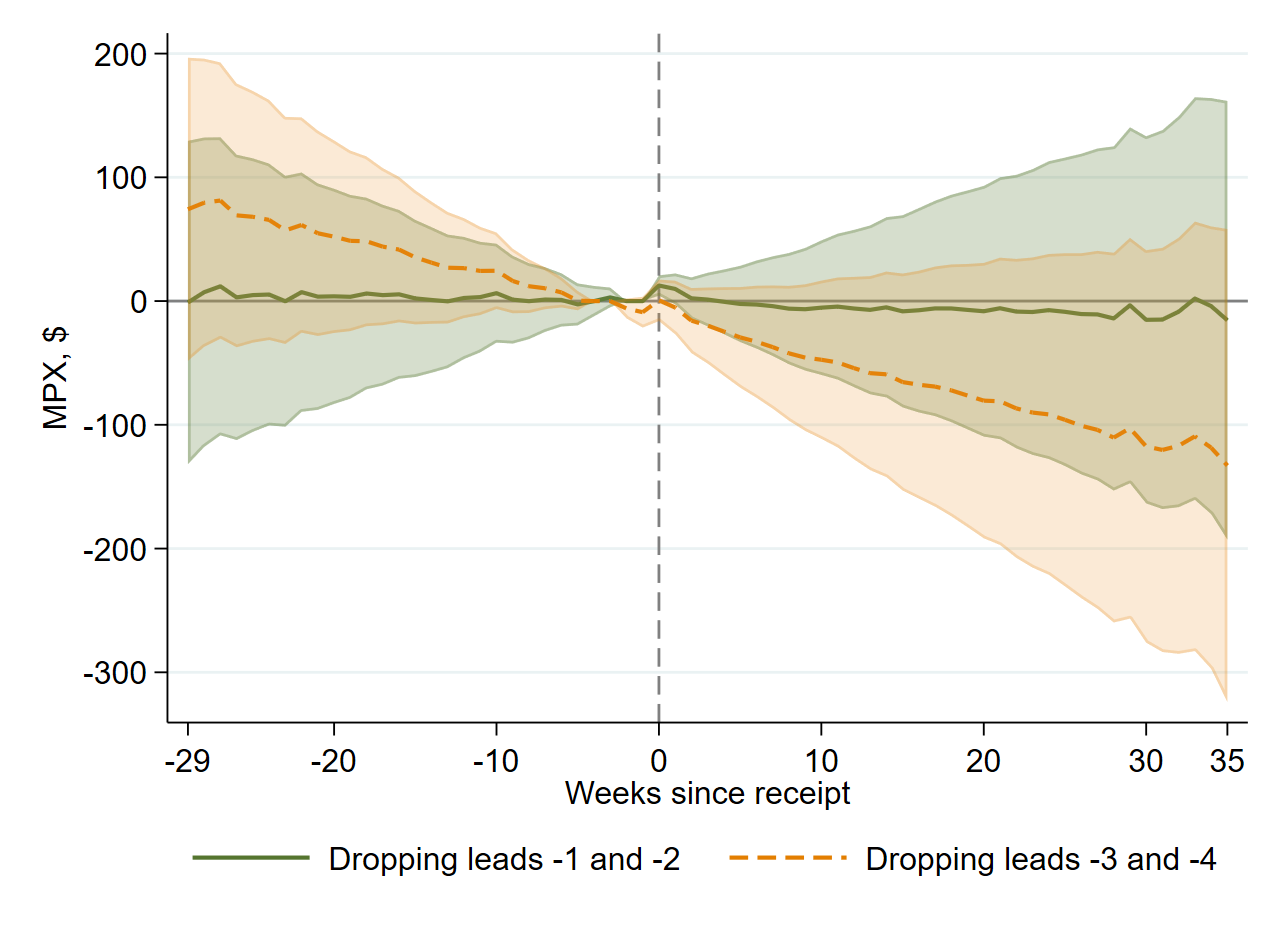

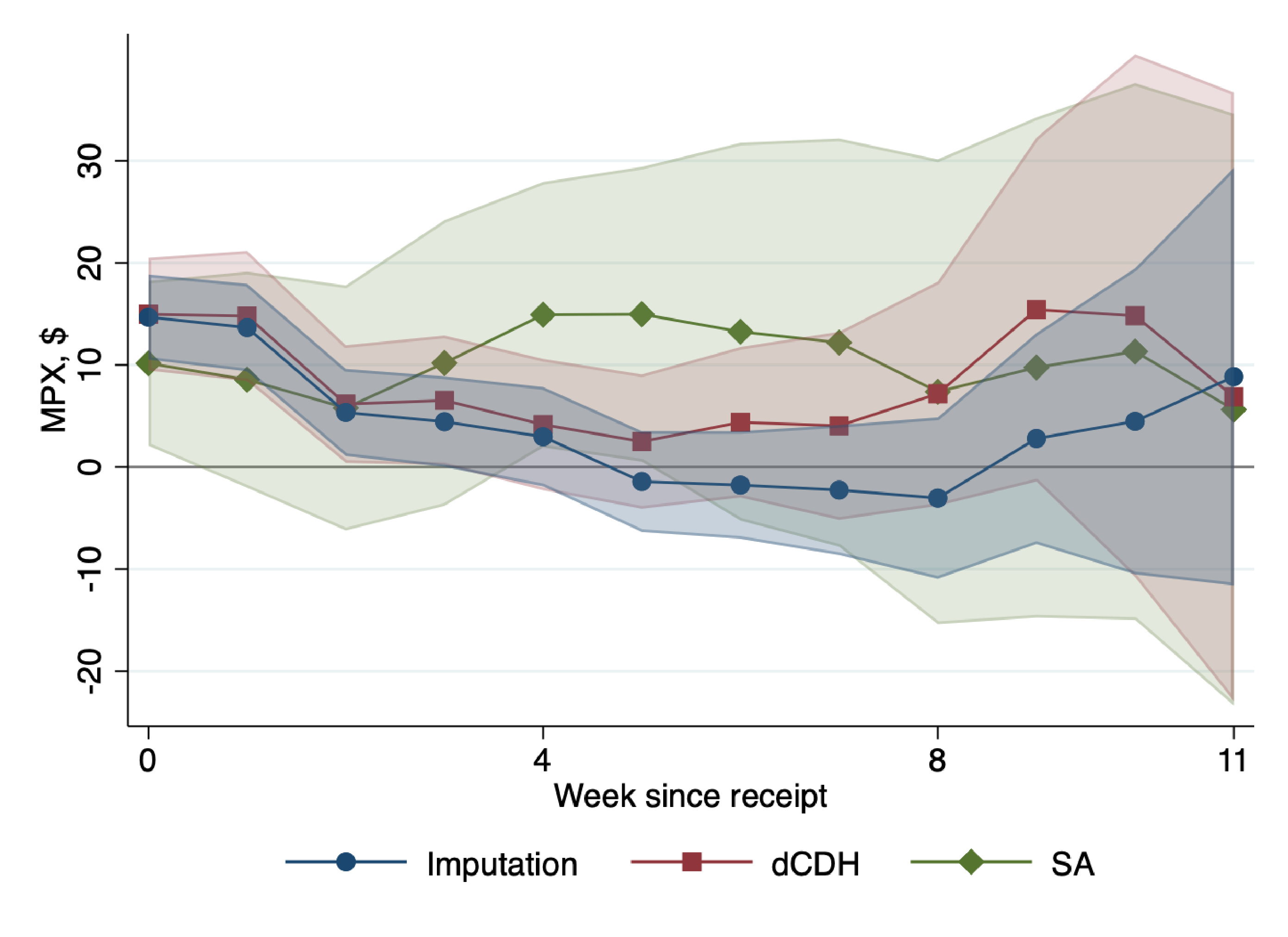

In Section 5, we illustrate the practical relevance of our theoretical insights by revisiting the estimation of the marginal propensity to spend out of tax rebates in the event study of [7]. First, we show that the choice of a binned specification used by [7] leads to a substantial upward bias in estimated MPXs. Indeed, we find that the binned specification puts a large weight on the effects happening in the first week after the rebate receipt, and negative weights on some longer-run effects, biasing the estimate upwards because the spending response quickly decays over time. Second, we highlight that, due to the implicit extrapolation of treatment effects in specifications restricting treatment effect heterogeneity, some dynamic specifications could be mistakenly interpreted as evidence for a large and persistent increase in spending. Our imputation estimator eliminates unstable patterns found across such specifications. Finally, we illustrate the underidentification problem with the fully-dynamic specification: the dynamic path of estimates is very sensitive to the choice of leads to drop.

Our findings deliver several insights for the macroeconomics literature. While commonly used estimates of the quarterly MPX covering all expenditures range from 50-90% and estimates of the quarterly MPX for nondurable expenditure range from 15-25%,222[7], [35] and [25] estimate different versions of the MPX out of tax rebates. [29], [27] and [15] provide recent reviews of the literature on the estimation of the marginal propensity to spend and consume. our estimates, when appropriately rescaled, are about half as large, at 25–37% for the MPX one quarter after tax rebate receipt for all expenditures and 8–11% for nondurables. Using the scaling methodology of [29], we estimate that the model-consistent, or “notional,” MPC in the quarter following the tax rebate ranges between 7.8% and 11.4%, compared with 15.9% to 23.4% in the original estimation of [7]. Furthermore, our preferred estimates are much more short-lived than benchmark estimates, falling to a statistical zero beyond the first month after receiving the tax rebate. Thus, our new estimates imply that fiscal stimulus may be less potent than predicted by leading macroeconomic models targeting benchmark estimates.333[34] apply our imputation estimator to the [35] quarterly data, covering the full consumption basket, and also obtain estimates around half as large as in the original study. Our analysis complements their results since, thanks to the high-frequency data, it allows us to investigate the dynamics of the effect and explain the source of the bias of conventional approaches. See also [5] for evidence that using robust event study estimation methods matters in other empirical contexts.

For convenient application of our results, we supply a Stata command, did_imputation, which implements the imputation estimator and inference for it in a computationally efficient way. Our command handles a variety of practicalities which are also covered by our theoretical results, such as time-varying covariates, triple-difference designs, and repeated cross-sections. We also provide a second command, event_plot, for producing “event study plots” that visualize the estimates with both our estimator and the alternative ones.

Our paper contributes to a growing methodological literature on event studies. To the best of our knowledge, our paper is the first and only one to characterize the underidentification and spurious identification of long-run treatment effects that arise in conventional implementations of event study designs. The negative weighting problem has received more attention. It was first shown by [12, Supplement 1]. The earlier manuscript of our paper [6] independently pointed it out and additionally explained how it arises because of forbidden comparisons and why it affects long-run effects in particular, which we now discuss in Section 3.3 below. The issue has since been further investigated by [19], [43], and [51], while [60] have shown similar problems with dynamic specifications. [60] and [37] have further uncovered problems with conventional pre-trend tests, and [41] have characterized the problems which arise from binning multiple lags and leads in dynamic specifications. Besides being the first to point out some of these issues, our paper provides a unifying econometric framework which explicitly relates these issues to the conflation of the target estimand and the underlying identification assumptions.

Several papers have proposed ways to address these problems, introducing estimators that remain valid when treatment effects can vary arbitrarily [52, 60, 50, 58, 10]. An important limitation of these robust estimators is that their efficiency properties are not known.444There are three notable exceptions. [58] consider a two-stage generalized method of moments (GMM) estimator and establish its semiparametric efficiency under heteroskedasticity in a large-sample framework with a fixed number of periods. However, they find this estimator to be impractical, as it involves many moments, e.g. almost as many as the number of observations in the application they consider. Second, [38] characterize the efficient DiD estimator which leverages random timing of the treatment, rather than a more conventional parallel trends assumption, as we do. Finally, [55] builds on our framework to characterize the efficiency properties of difference-in-differences estimators when error terms follow a random walk — the opposite case from our benchmark analysis of efficiency which imposes no serial correlation of errors. In Section A.5, we generalize our results to intermediate cases, allowing for models of heteroskedasticity and serial correlation. A key contribution of our paper is to derive a practical, robust, and finite-sample efficient estimator from first principles. We show that this estimator takes a particularly transparent form under unrestricted treatment effect heterogeneity, while our construction also yields efficiency when some restrictions on treatment effects are imposed. By clearly separating the testing of underlying assumptions from the estimation step imposing these assumptions, we simultaneously increase estimation efficiency and avoid problems with inference after pre-testing under spherical errors. Our estimator uses all pre-treatment periods for imputation, as appropriate under the standard DiD assumptions, while alternative estimators use more limited information.555This efficiency gain relative to [52] and [60] is obtained without stronger assumptions. The [50] assumptions are also equivalent to ours when there is only one period before any unit is treated and there are no covariates (see [58]).

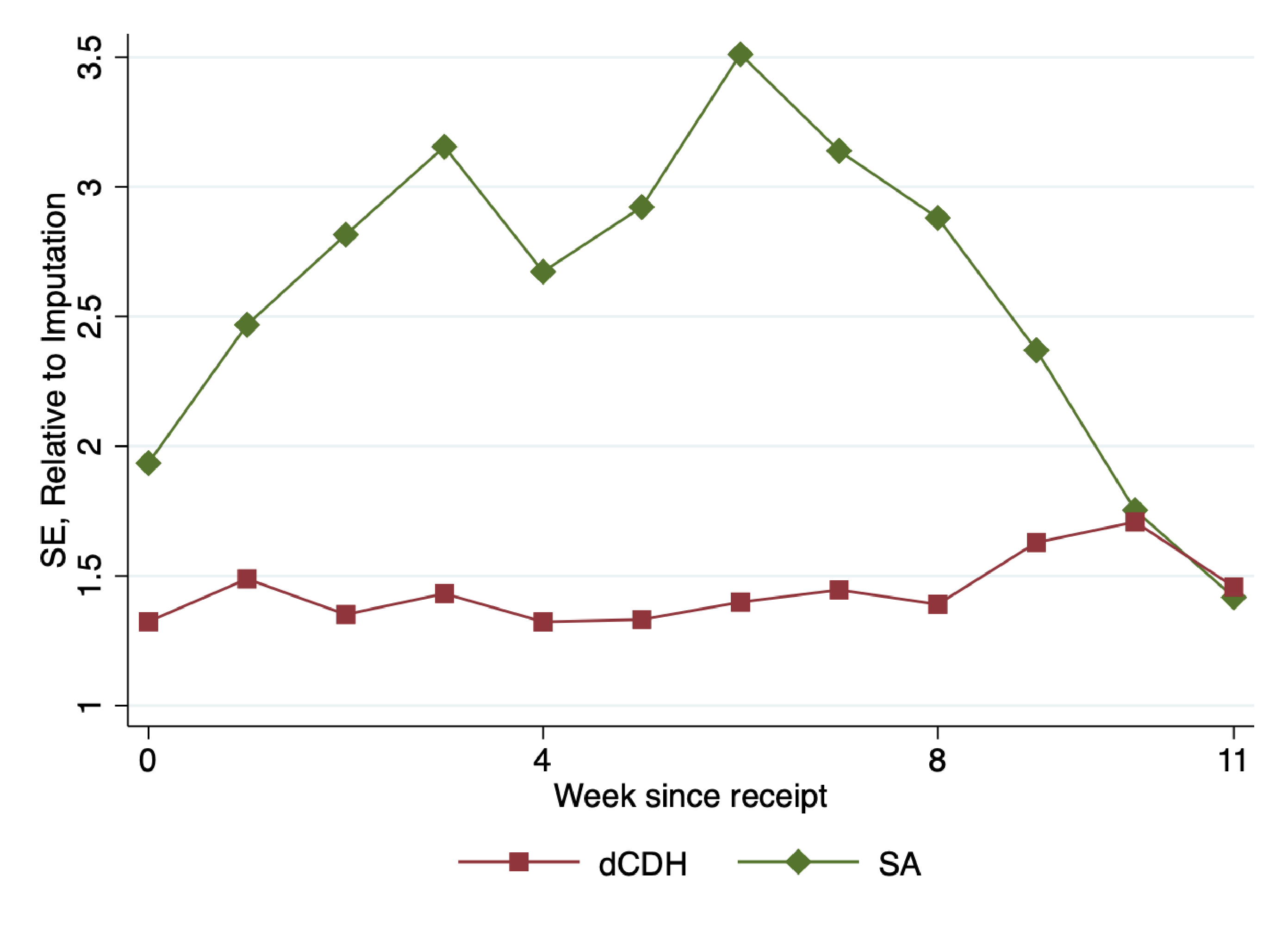

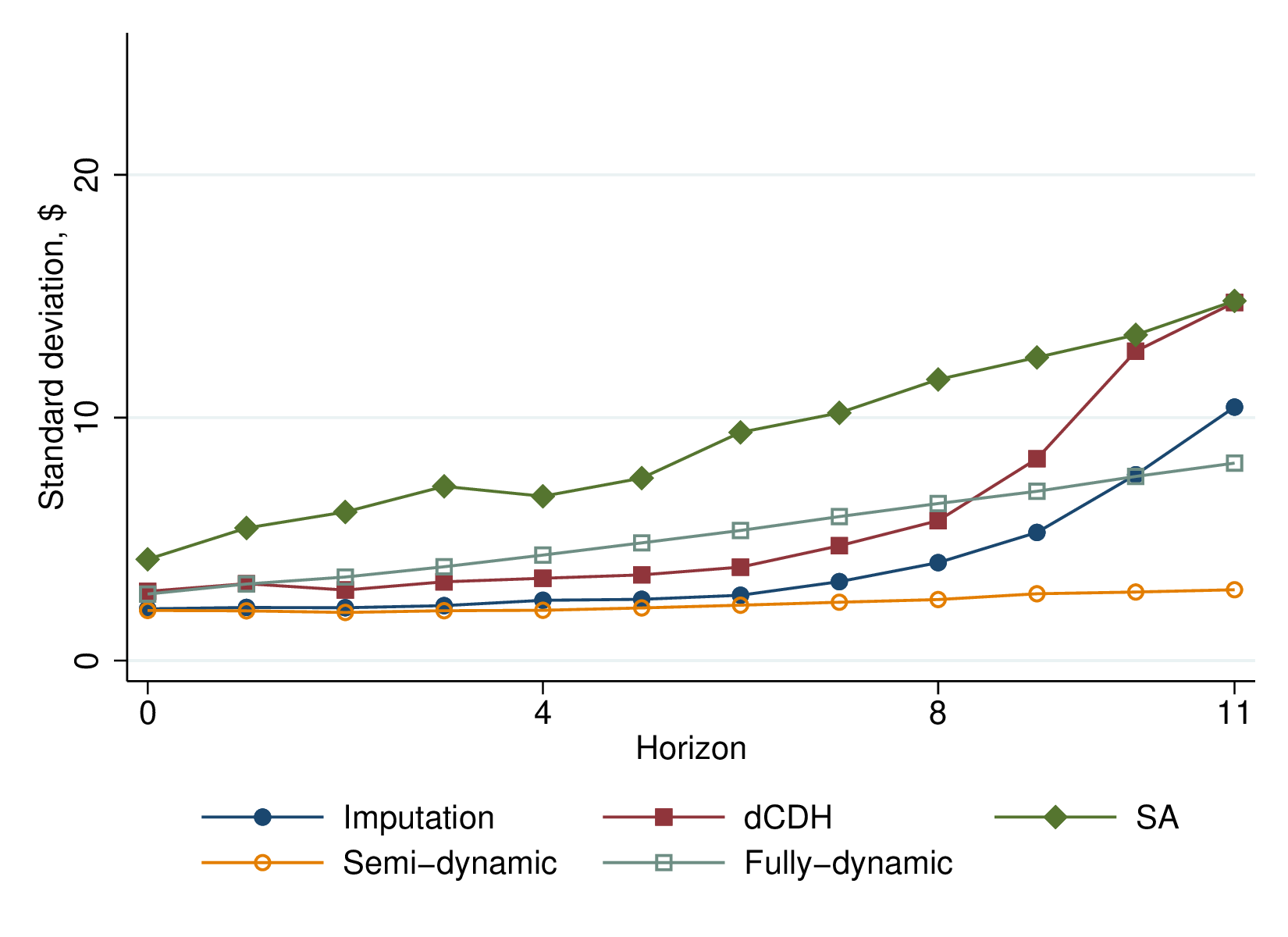

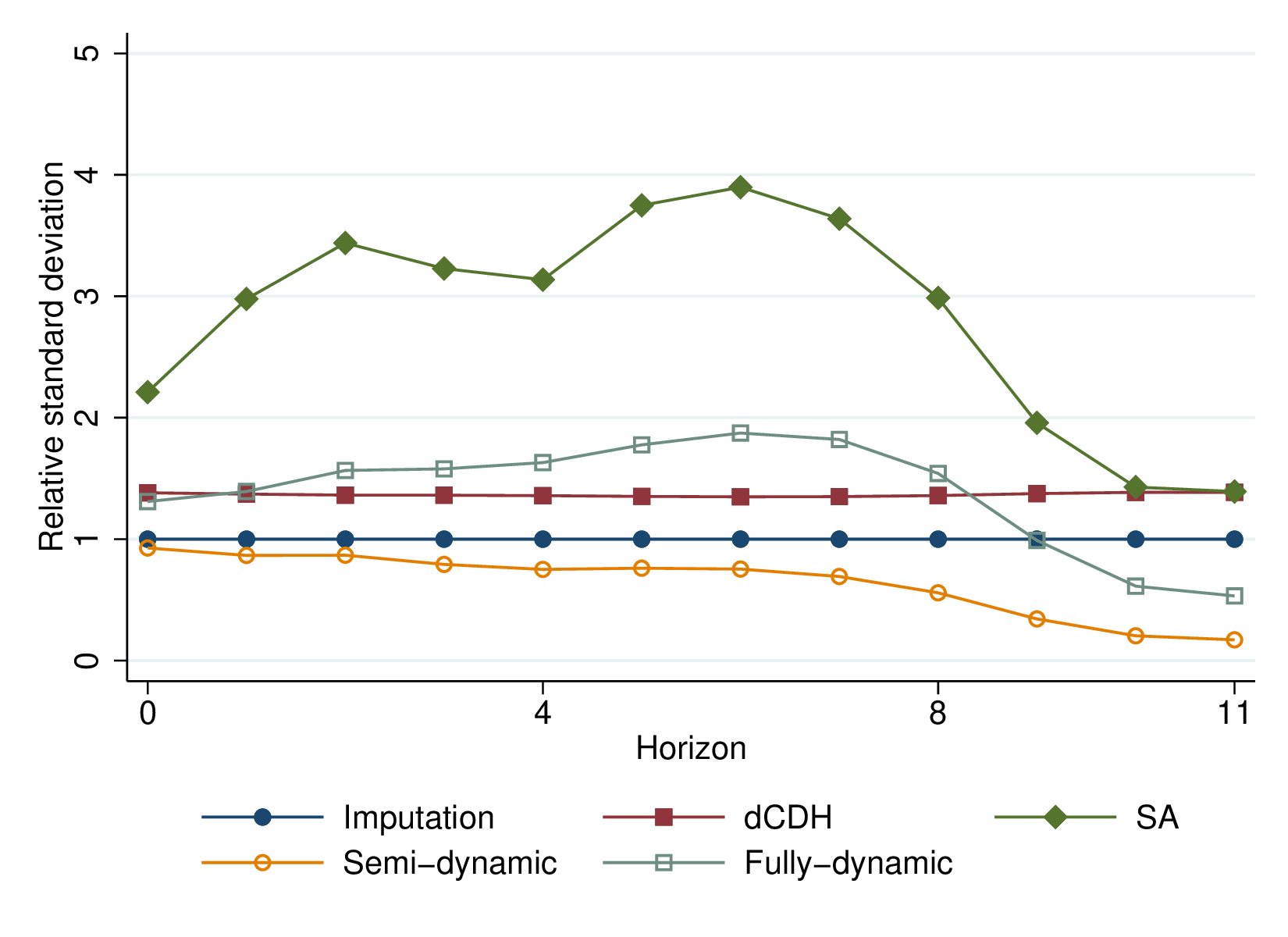

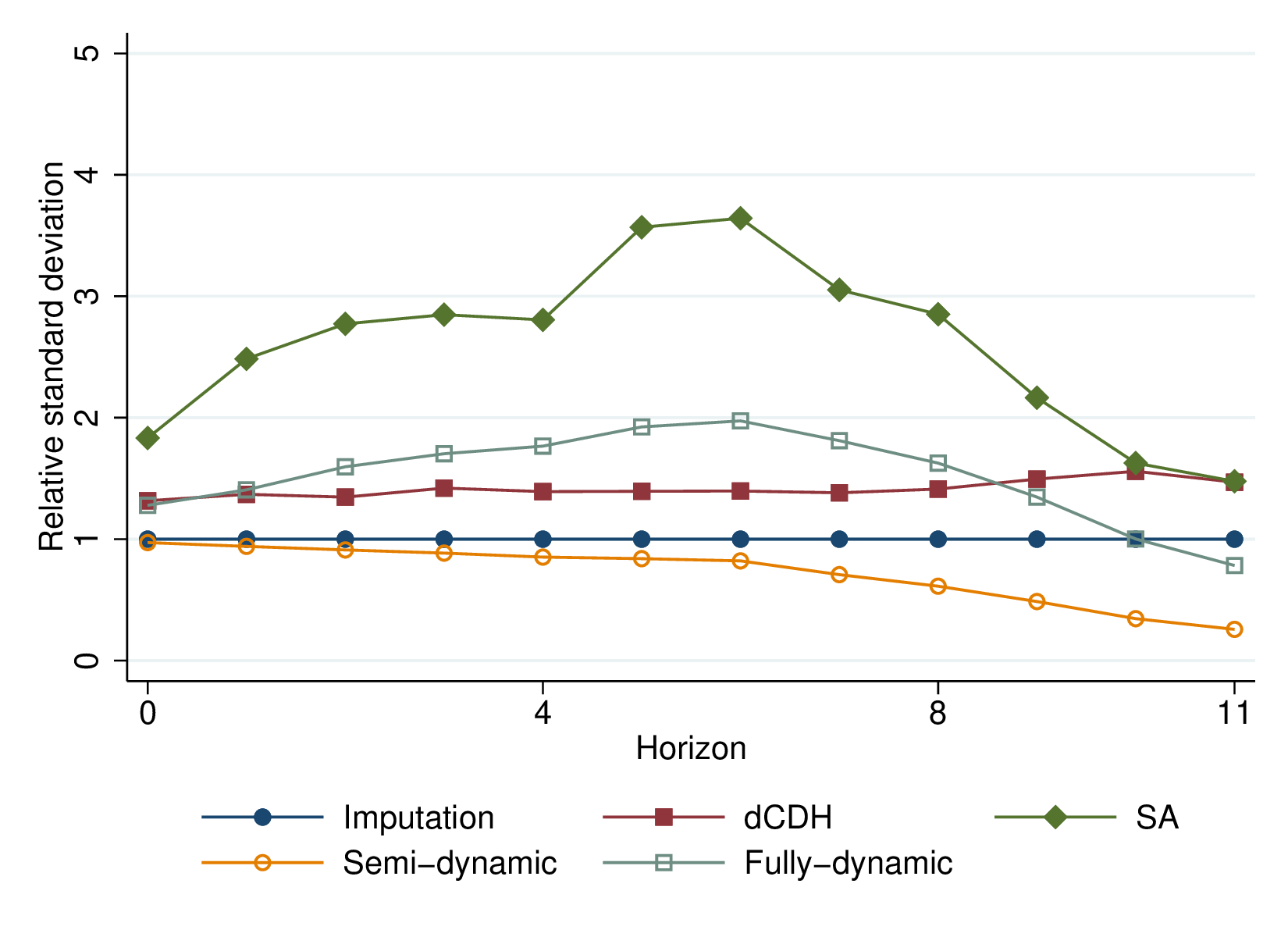

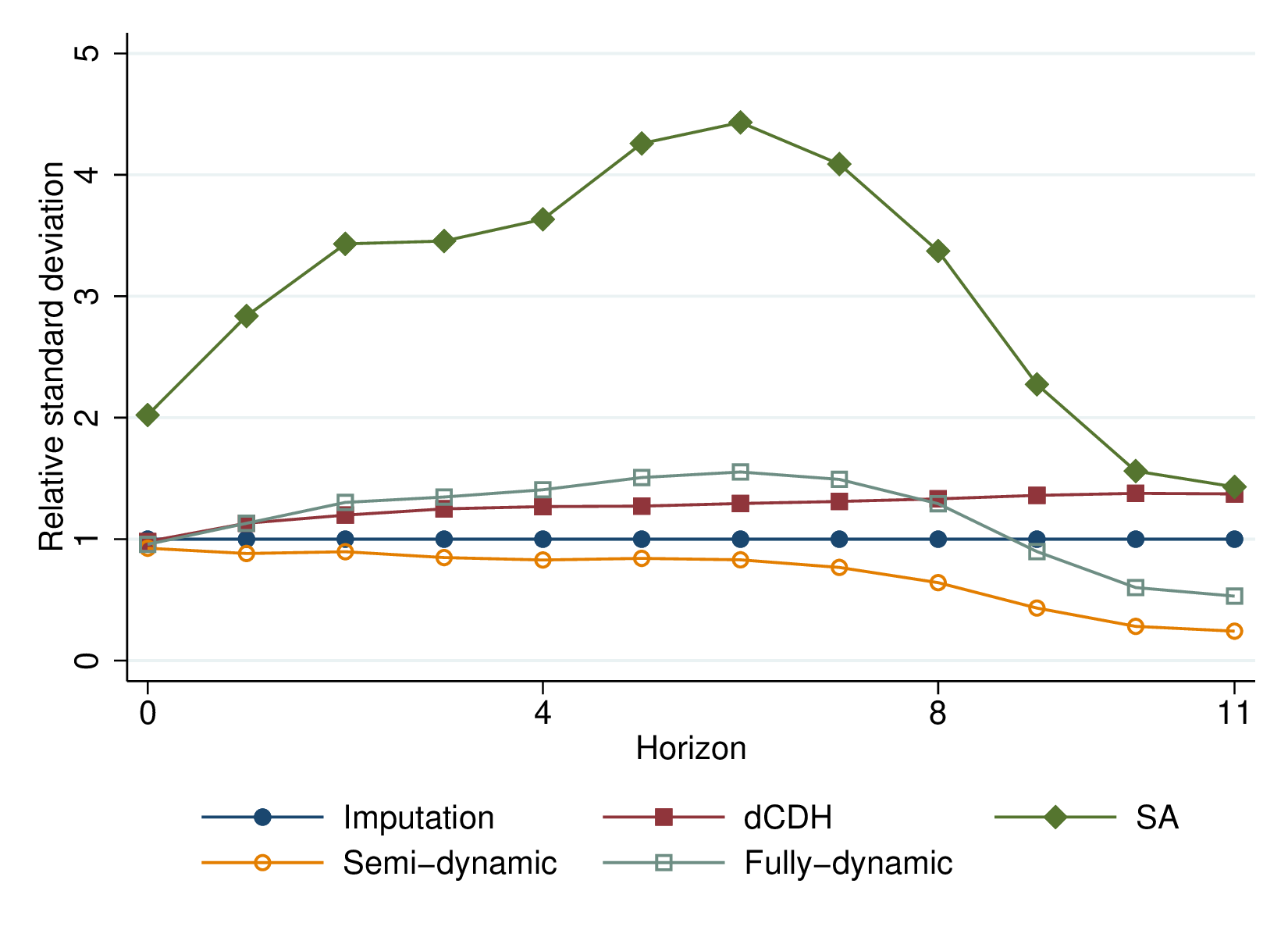

In the MPX application, we find large gains of our imputation estimator: the confidence interval is about 50% longer for each week relative to the rebate for [52], and 2–3.5 times longer for [60] (which without extra controls are equivalent to the two versions of the [50] estimator). We confirm these gains in a simulation study, finding that the standard deviations of alternative robust estimators are 1.3–3.6 times higher with spherical errors, and that these gains are generally preserved under heteroskedasticity and serial correlation of errors.

Finally, our paper is related to a nascent literature that develops robust estimators similar to the imputation estimator. To the best of our knowledge, this idea has been first proposed for factor models [18, 48]. [4] consider a general class of “matrix-completion” estimators for panel data that first impute untreated potential outcomes by regularized factor- and fixed-effects models and then average over the implied treatment-effect estimates. The imputation idea has been explicitly applied to fixed-effect estimators in event studies by [31], [16], [45], and [17]. Specifically, the counterfactual estimator of [31], the two-stage estimator of [16], [45], and [17], and a version of the matrix-completion estimator from [4] without factors or regularization coincide with the imputation estimator in our model for the specific class of estimands their papers consider. Relative to these papers, we make four contributions: we derive a general imputation estimator from first principles, show its efficiency, provide tools for valid asymptotic inference when unit fixed effects are included, and show its robustness to pre-testing. Subsequently to our work, [62] derives a two-way Mundlak estimator, which is also equivalent to the imputation estimator for a restricted class of estimands in complete panels with controls that are not allowed to change over time (but that may have time-varying effects). The robustness and efficiency properties of our estimator are not limited to those situations.

2 Setting

We consider estimation of causal effects of a binary treatment on an outcome in a panel of units and periods . We focus on “staggered rollout” designs in which being treated is an absorbing state. For each unit there is an event date when switches from 0 to 1 forever: , where is the number of periods since the event date (“horizon”). Some units may never be treated, denoted by . Units with the same event date are referred to as a cohort.

We do not make any random sampling assumptions and work with a set of observations of total size , which may or may not form a complete panel. We similarly view the event date for each unit, and therefore all treatment indicators, as fixed. We define the set of treated observations by of size and the set of untreated (i.e., never-treated and not-yet-treated) observations by of size .666Viewing the set of observations and event times as non-stochastic is not essential. In Section A.1, we show how this framework can be derived from one in which both are stochastic, by appropriate conditioning. Our conditional framework avoids random sampling assumptions made in other work on DiD designs (e.g. [51], [60], and [50]).

We denote by the period- stochastic potential outcome of unit if it is never treated. Causal effects on the treated observations are denoted . We suppose a researcher is interested in a statistic which sums or averages treatment effects over the set of treated observations with pre-specified non-stochastic weights that can depend on treatment assignment and timing, but not on realized outcomes:

Estimation Target.

.

For notation brevity, we consider scalar estimands.

Different weights are appropriate for different research questions. The researcher may be interested in the overall ATT, formalized by for all . In event study analyses a common estimand is the average effect periods since treatment for a given horizon : for . Our approach also allows researchers to specify target estimands that place unequal weights on units within the same cohort-by-horizon cell. For example, one may be interested in weighting units by their size, or in estimating a “balanced” version of horizon-average effects: the ATT at horizon computed only for the subset of units also observed at horizon , such that the gap between two or more estimates is not confounded by compositional differences. Finally, we do not require the to add up to one; for example, a researcher may be interested in the difference between average treatment effects at different horizons or across some groups of units (e.g. women and men), corresponding to .777More broadly, the choice of weights allows for estimation of treatment effect heterogeneity by observed characteristics . Indeed, the slope of the linear projection of on some observable (which may or may not be time-varying) is a weighted sum of treatment effects, for and . The same logic generalizes when is a vector, via the Frisch–Waugh–Lowell theorem. This approach also allows for tests of restrictions on treatment effect heterogeneity, e.g. to assess whether ATTs vary across time horizons.

To identify , we consider three assumptions. We start with the parallel-trends assumption, which imposes a two-way fixed effect (TWFE) model on the untreated potential outcomes.

Assumption 1 (Parallel trends).

There exist non-stochastic and such that for all .888In estimation, we will set the fixed effect of either one unit or one period to zero, such as . This is without loss of generality, since the TWFE model is otherwise over-parameterized.

An equivalent formulation requires to be the same across units for all periods and (whenever and are observed).

Parallel trend assumptions are standard in DiD designs, but their details may vary. First, we impose the TWFE model on the entire sample. Although weaker assumptions can be sufficient for identification of [[, e.g.,]]Callaway2021, those alternative restrictions depend on the realized treatment timing. Since parallel trends is an assumption on potential outcomes, we prefer its stronger version which can be made a priori.999Specifically, Assumption 4 in [50] requires that the TWFE model only holds for all treated observations (), observations directly preceding the treatment onset (), and in all periods for never-treated units. Similarly, [19] proposes to impose parallel trends on a “variance-weighted” average of units, as the weakest assumption under which static specifications we discuss in Section 3 identify some average of causal effects. While technically weaker, this assumption may be hard to justify ex ante without imposing parallel trends on all units as it is unlikely that non-parallel trends will cancel out by averaging. Moreover, Assumption 1 can be tested by using pre-treatment data, while minimal assumptions cannot. Second, we impose Assumption 1 at the unit level, while sometimes it is imposed on cohort-level averages. Our approach is in line with the practice of including unit, rather than cohort, FEs in DiD analyses and allows us to avoid biases in incomplete panels where the composition of units changes over time. Moreover, we show in Section A.2 that, under random sampling and without compositional changes, assumptions on cohort-level averages imply Assumption 1.

Our framework extends immediately to richer models of :

Assumption 1′ (General model of ).

For all , , where is a vector of unit-specific nuisance parameters, is a vector of nuisance parameters associated with common covariates, and and are known non-stochastic vectors.

The first term in this model of nests unit FEs, but also allows to interact them with some observed covariates unaffected by the treatment status, e.g. to include unit-specific trends. This term looks similar to a factor model, but differs in that regressors are observed. The second term nests period FEs but additionally allows any time-varying covariates, i.e. . In Section A.1 we clarify that have to be unaffected by treatment and strictly exogenous to be included in the specification.

We next rule out anticipation effects, i.e. the causal effects of being treated in the future on current outcomes (e.g. [1]):

Assumption 2 (No anticipation effects).

for all .

Assumptions 1 and 2 together imply that the observed outcomes for untreated observations follow the TWFE model. It is straightforward to weaken this assumption, e.g. by allowing anticipation for some periods before treatment: this simply requires redefining event dates to earlier ones. However, some form of this assumption is necessary for DiD identification, as there would be no reference periods for treated units otherwise.

Finally, researchers sometimes impose restrictions on causal effects, explicitly or implicitly. For instance, may be assumed to be homogeneous for all units and periods, or only depend on the number of periods since treatment (but be otherwise homogeneous across units and calendar periods). We will consider such restrictions as a possible auxiliary assumption:

Assumption 3 (Restricted causal effects).

for a known matrix of full row rank.

It will be more convenient for us to work with an equivalent formulation of Assumption 3, based on free parameters driving treatment effects rather than restrictions on them:

Assumption 3′ (Model of causal effects).

, where is a vector of unknown parameters and is a known matrix of full column rank.

Assumption 3′ imposes a parametric model of treatment effects. For example, the assumption that treatment effects all be the same, , corresponds to and . Conversely, a “null model” that imposes no restrictions is captured by and .

If restrictions on the treatment effects are implied by economic theory, imposing them will increase estimation power. Often, however, such restrictions are implicitly imposed without an ex ante justification, but just because they yield a simple model for the outcome. We will show in Section 3 how estimators that rely on this assumption can fail to estimate reasonable averages of treatment effects, let alone the specific estimand , when the assumption is violated.101010We view the null Assumption 3 as a conservative default. We note, however, that this makes the assumptions inherently asymmetric in that they impose restrictive models on potential control outcomes (Assumption 1), but not on treatment effects . This asymmetry reflects the standard practice in staggered rollout DiD designs and is natural when the structure of treatment effects is ex ante unknown, while our framework also accommodates the case where the researcher is willing to impose structure. Restrictions on treatment effects, when appropriate, are also useful for external validity: unless some structure is imposed on treatment effects, one cannot use estimates from past data to inform future policy, for instance extending a given treatment to currently untreated units. However, one can use our framework without restrictions to learn about the structure of treatment effects, e.g. whether they vary across cohorts for each horizon.

While we formulated our setting for staggered-adoption DiD designs with binary treatments in panel data, our framework applies without change in many related research designs. In repeated cross-sections, a different random sample of units (e.g., individuals) from the same groups (e.g., regions) is observed in each period. Unit FEs are not possible to include but can be replaced with group FEs in Assumption 1′: . In triple-differences designs, the data have two dimensions in addition to periods, e.g. corresponds to a pair of region and demographic group . Assumption 1′ can be specified as .111111Another variation is when the outcome is measured in a single period but across two cross-sectional dimensions, such as regions and birth cohorts , with the treatment implemented in a set of regions for the cohorts born after some cutoff period (e.g., [22]). Then one may write . With non-binary treatment intensity, our setting applies if each unit is observed untreated before and treated with heterogenous intensity (that may or may not vary over time) from period . Assumptions 1 and 2 can apply, and the researcher can consider estimands such as the “ATT per unit of intensity”, , by setting proportionally to . The challenges we describe in Section 3 for standard staggered DiDs and the solutions of Section 4 directly apply in all of these cases.121212This is also the case of non-staggered DiD designs, in which units receive treatment in a single period or never. Our insights in Section 3 and Section 4 are still relevant if continuous covariates or unit-specific trends are included (see [40] and [46] for related ideas).

3 Challenges Pertaining to Conventional Practice

In this section, we first introduce the common two-way fixed effects regressions with restricted treatment effect heterogeneity that have traditionally been used in DiD designs. We then discuss several estimation challenges that pertain to these specifications, including underidentification in certain dynamic specifications, negative weighting, and spurious identification of long-run causal effects. We conclude the section by discussing how our framework also relates to other problems that have been pointed out by [37] and [60].

3.1 Conventional Restrictive Specifications in Staggered Adoption DiD

Causal effects in staggered adoption DiD designs have traditionally been estimated via OLS regressions with two-way fixed effects, using specifications that implicitly restrict treatment effect heterogeneity across units. While details may vary, the following specification covers many studies:

| (2) |

Here and are the unit and period (“two-way”) fixed effects, and are the numbers of included “leads” and “lags” of the event indicator, respectively, and is the error term. The first lead, , is often excluded as a normalization, while the coefficients on the other leads (if present) are interpreted as measures of “pre-trends,” and the hypothesis that is tested visually or statistically. Conditionally on this test passing, the coefficients on the lags are interpreted as a dynamic path of causal effects: at periods after treatment and, in the case of , at longer horizons binned together. We will refer to this specification as “dynamic” (as long as ) and, more specifically, “fully-dynamic” if it includes all available leads and lags except , or “semi-dynamic” if it includes all lags but no leads.

Viewed through the lens of the Section 2 framework, these specifications make implicit assumptions on untreated potential outcomes, anticipation and treatment effects, and the estimand of interest. First, they make Assumption 1 but, for , do not fully impose Assumption 2, allowing for anticipation effects for periods before treatment.131313One can alternatively view this specification as imposing Assumption 2 but making a weaker Assumption 1 which includes some pre-trends into . This difference in interpretation is immaterial for our results. Typically this is done as a means to test Assumption 2 rather than to relax it, but the resulting specification is the same. Second, equation Equation 2 imposes strong restrictions on causal effect heterogeneity (Assumption 3), with treatment (and anticipation) effects assumed to only vary by horizon and not across units and periods otherwise. Most often, this is done without an a priori justification. If the lags are binned into the term with , the effects are further assumed to be time-invariant once periods have elapsed since the event. Finally, dynamic specifications do not explicitly define the estimands as particular averages of heterogeneous causal effects, even though researchers often consider that effects may vary across observations, as evidenced by a literature on the interpretation of OLS estimands going back to at least [2] and [23].

Besides dynamic specifications, equation Equation 2 also nests a very common specification used when a researcher is interested in a single parameter summarizing all causal effects. With , we have the “static” specification in which a single treatment indicator is included:

| (3) |

In line with our Section 2 setting, the static equation imposes the parallel trends and no anticipation Assumptions 1 and 2. However, it also makes a particularly strong version of Assumption 3 — that all treatment effects are the same. Moreover, the target estimand is again not written out as an explicit average of potentially heterogeneous causal effects.

In the rest of this section we turn to the challenges associated with OLS estimation of equations Equation 2 and Equation 3. We explain how these issues result from the conflation of the target estimand, Assumption 2 and Assumption 3, providing a new and unified perspective on the problems of static and dynamic specifications with restricted treatment effect heterogeneity.

3.2 Under-Identification of the Fully-Dynamic Specification

The first problem pertains to fully-dynamic specifications and arises because a strong enough Assumption 2 is not imposed. We show that those specifications are under-identified if there is no never-treated group:

Proposition 1.

If there are no never-treated units, the path of coefficients is not point-identified in the fully-dynamic specification. In particular, for any , the path fits the data equally well, with the fixed effect coefficients appropriately modified.

Proof.

All proofs are given in Appendix B. ∎

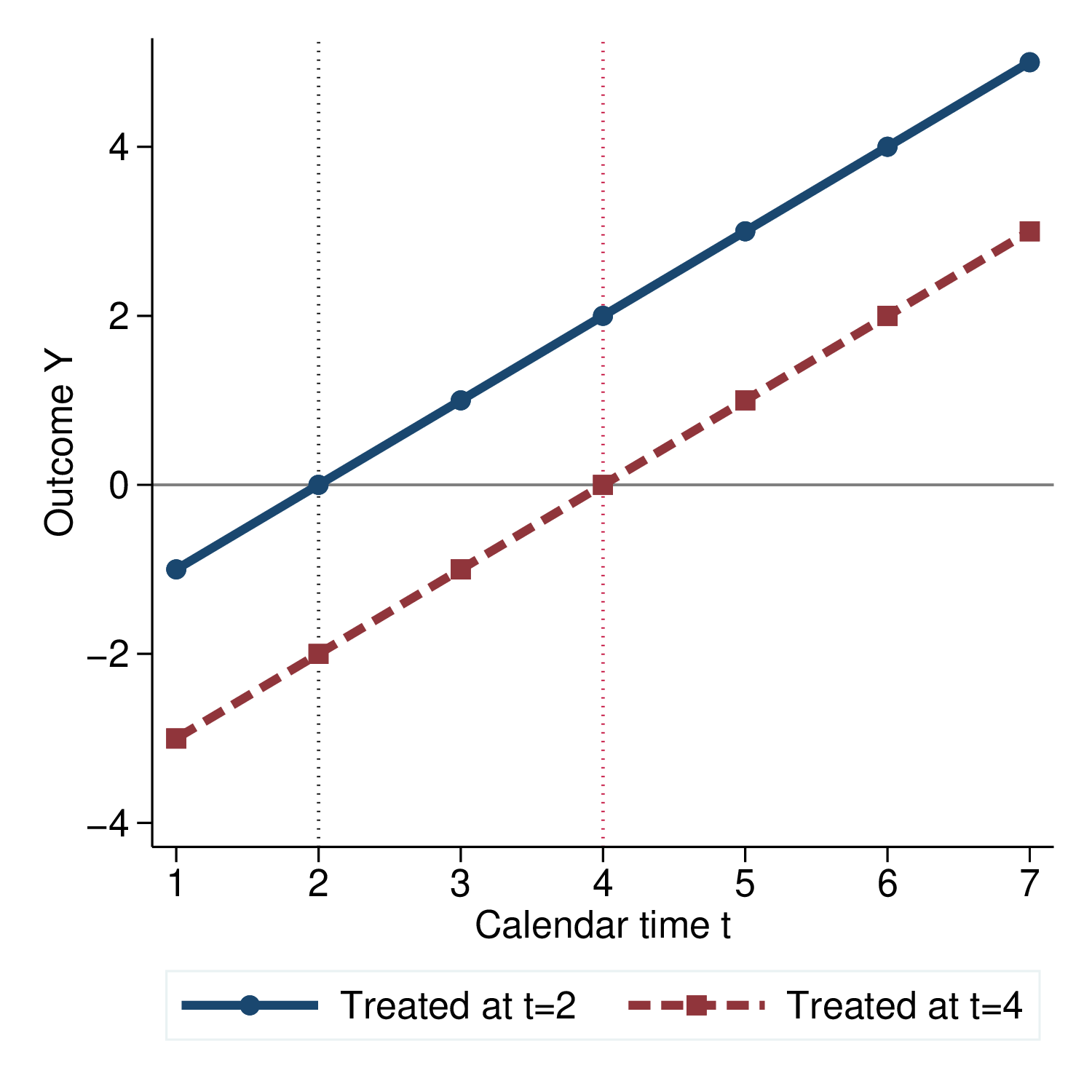

To illustrate this result with a simple example, Figure 1 plots the outcomes for a simulated dataset with two units (or equal-sized cohorts), one treated at and the other at . Both units exhibit linear growth in the outcome, starting from different levels. There are two interpretations of these dynamics. First, treatment could have no impact on the outcome, in which case the level difference corresponds to the unit FEs, while trends are just a common feature of the environment, through period FEs. Alternatively, note that the outcome equals the number of periods since the event for both groups and all time periods: it is zero at the moment of treatment, negative before, and positive after. A possible interpretation is that the outcome is entirely driven by causal effects and anticipation of treatment. Thus, one cannot hope to distinguish between unrestricted dynamic causal effects and a combination of unit effects and time trends.141414Formally, the problem arises because a linear time trend and a linear term in the cohort (subsumed by the unit FEs) can perfectly reproduce a linear term in horizon . Therefore, a complete set of treatment leads and lags, which is equivalent to the horizon FEs, is collinear with the unit and period FEs.

Notes: This figure shows the evolution of outcomes over seven periods for two units (or cohorts), for the illustrative example of Section 3.2. Vertical lines mark the periods in which the two units are first treated.

The problem may be important in practice, as statistical packages may resolve this collinearity by dropping an arbitrary unit or period indicator. Some estimates of would then be produced, but because of an arbitrary trend in the coefficients they may suggest a violation of parallel trends even when the specification is in fact correct, i.e. Assumptions 1 and 2 hold and there is no heterogeneity of treatment effects for each horizon (Assumption 3).

To break the collinearity problem, stronger restrictions on anticipation effects, and thus on for untreated observations, have to be introduced. One could consider imposing minimal restrictions on the specification that would make it identified. In typical cases, only a linear trend in is not identified in the fully dynamic specification, while nonlinear paths cannot be reproduced with unit and period fixed effects. Therefore, just one additional normalization, e.g. in addition to , breaks multicollinearity.151515Additional collinearity arises, e.g., when treatment is staggered but happens at periodic intervals.

However, minimal identified models rely on ad hoc identification assumptions which are a priori unattractive. For instance, just imposing means that anticipation effects are assumed away and periods before treatment, but not in other pre-periods. This assumption therefore depends on the realized event times. Instead, a systematic approach is to impose the assumptions — some forms of no anticipation effects and parallel trends — that the researcher has an a priori argument for and which motivated the use of DiD. Such assumptions also give much stronger identification power.161616Our suggestion to impose identification assumptions at the estimation stage does not mean that those assumptions should not also be tested; we discuss testing in detail in Section 4.4.

3.3 Negative Weighting in the Static Regression

We now show how, by imposing Assumption 3 instead of specifying the estimation target, the static TWFE specification does not identify a reasonably-weighted average of heterogeneous treatment effects: the underlying weights may be negative, particularly for the long-run causal effects. The issues we discuss here also arise in dynamic specifications that bin multiple lags together.

First, we note that, if the parallel-trends and no-anticipation assumptions hold, the static specification identifies some weighted average of treatment effects:171717This result was previously stated in Theorem 1 of [51] for general designs, and later in Appendix C of [6] for staggered adoption designs.

Proposition 2.

If Assumptions 1 and 2 hold, then the estimand of the static specification in Equation 3 satisfies for some weights that do not depend on the outcome realizations and add up to one, .

The underlying weights can be computed from the data using the Frisch–Waugh–Lovell theorem (see equation Equation 17 in the proof of Proposition 2) and only depend on the timing of treatment for each unit and the set of observed units and periods. The static specification’s estimand, however, cannot be interpreted as a proper weighted average, as some weights can be negative, which we illustrate with a simple example:

Proposition 3.

Suppose Assumptions 1 and 2 hold and the data consist of two units (or equal-sized cohorts), and , treated in periods 2 and 3, respectively, both observed in periods (as shown in Table 1). Then the estimand of the static specification Equation 3 can be expressed as .

| Event date |

|---|

Notes: This table shows the evolution of expected outcomes over three periods for two units (or cohorts), for the illustrative example of Proposition 3. Without loss of generality, we normalize .

This example illustrates the severe short-run bias of the static specification: the long-run causal effect, corresponding to the early-treated unit and the late period 3, enters with a negative weight (). Thus, larger long-run effects make the coefficient smaller.

This problem results from what we call “forbidden comparisons” performed by the static specification. Recall that the original idea of DiD estimation is to compare the evolution of outcomes over some time interval for the units which got treated during that interval relative to a reference group of units which didn’t, identifying the period FEs. In the Proposition 3 example, such an “admissible” comparison is between units and in periods 2 and 1, . However, panels with staggered treatment timing also lend themselves to a second type of comparisons — which we label “forbidden” — in which the reference group has been treated throughout the relevant period. For units in this group, the treatment indicator does not change over the relevant period, and so the restrictive specification uses them to identify period FEs, too. The comparison between units and in periods 3 and 2, , in Proposition 3 is a case in point. While a comparison like this is appropriate and increases efficiency when treatment effects are homogeneous (which the static specification was designed for), forbidden comparisons are problematic under treatment effect heterogeneity. For instance, subtracting not only removes the gap in period FEs, , but also deducts the evolution of treatment effects , placing a negative weight on . The restrictive specification leverages comparisons of both types and estimates the treatment effect by .181818The proof of Proposition 2 shows why long-run effects in particular are subject to the negative weights problem. In general, negative weights arise for the treated observations, for which the residual from an auxiliary regression of on the two-way FEs is negative. [51] show that, in complete panels, the unit FEs are higher for early-treated units (which are observed treated for a larger shares of periods) and period FEs are higher for later periods (in which a larger shares of units are treated). The early-treated units observed in later periods correspond to the long-run effects.

Fundamentally, this problem arises because the specification imposes very strong restrictions on treatment effect homogeneity, i.e. Assumption 3, instead of acknowledging the heterogeneity and specifying a particular target estimand (or perhaps a class of estimands that the researcher is indifferent between).

With a large number of never-treated units or a large number of periods before any unit is treated (relative to other units and periods), our setting becomes closer to a classical non-staggered DiD design, and therefore negative weights disappear, as our next result illustrates:

Proposition 4.

Suppose all units are observed for all periods and the earliest treatment happens at . Let be the number of observations for never-treated units before period and be the number of untreated observations for ever-treated units since . Then there is no negative weighting, i.e. , if and only if .191919 and respectively correspond to the numbers of admissible and forbidden 2x2 DiD comparisons available for the earliest-treated units in the latest period . The gap between them drives negative weights with complete panels, as in [43, Proposition 1].

Even when weights are non-negative, they may remain highly unequal and diverge from the estimands that the researcher is interested in. Our preferred strategy is therefore to commit to the estimation target and explicitly allow for treatment effect heterogeneity, except when some form of Assumption 3 is ex ante appropriate.

3.4 Spurious Identification of Long-Run Effects in Dynamic Specifications

Another consequence of inappropriately imposing Assumption 3 concerns estimation of long-run causal effects. Conventional dynamic specifications (except those subject to the underidentification problem) yield some estimates for all coefficients. Yet, for large enough , no averages of treatment effects are identified under Assumptions 1 and 2 with unrestricted treatment effect heterogeneity. Therefore, estimates from restrictive specifications are fully driven by unwarranted extrapolation of treatment effects across observations and may not be reliable, unless strong ex ante reasons for Assumption 3 exist.

This issue is well illustrated in the example of Proposition 3. To identify the long-run effect under Assumptions 1 and 2, one needs to form an admissible DiD comparison, of the outcome growth over some period between unit and another unit not yet treated in period 3. However, by period 3 both units have been treated. Mechanically, this problem arises because the period fixed effect is not identified separately from the treatment effects and in this example, absent restrictions on treatment effects. Yet, the semi-dynamic specification

will produce an estimate via extrapolation. Specifically, two different parameters, and , are identified by comparing the two units in periods 2 or 3, respectively, with period 1. Therefore, when imposing homogeneity of short-run effects across units, , we estimate the long-run effect as the sum of and :

However, when , this estimator is biased.

In general, the gap between the earliest and the latest event times observed in the data provides an upper bound on the number of dynamic coefficients that can be identified without extrapolation of treatment effects. This result, which follows by the same logic of non-identification of the later period effects, is formalized by our next proposition:

Proposition 5.

Suppose there are no never-treated units and let Then, for any non-negative weights defined over the set of observations with (that are not identically zero), the weighted sum of causal effects is not identified by Assumptions 1 and 2.202020The requirement that the weights are non-negative rules out some estimands on the gaps between treatment effects for which are in fact identified. For instance, adding period to the Table 1 example, the difference would be identified (by ), even though neither nor is identified.

Robust estimators, including the one we characterize in Section 4, can only be computed for identified estimands, never resulting in spurious estimates.

We finally note that the challenges described in Section 3 apply even if the sample is “trimmed” to a fixed window around the event time; see Section A.3.

4 Imputation-Based Estimation and Testing

To overcome the challenges affecting conventional practice, we now derive the robust and efficient estimator and show that it takes a particularly transparent “imputation” form when no restrictions on treatment-effect heterogeneity are imposed. We then perform asymptotic analysis, establishing the conditions for the estimator to be consistent and asymptotically normal, derive conservative standard error estimates for it, and discuss appropriate pre-trend tests.

Throughout, we continue to suppose that the researcher chose the estimation target and assumed a model of (Assumption 1′) and no anticipation. Some model of treatment effects (Assumption 3) may also be assumed, although our main focus is on the null model, under which treatment effect heterogeneity is unrestricted. Letting for , we thus have under Assumptions 1′, 2 and 3′:

| (4) |

We assume throughout that is identified. Proposition A1 provides conditions for identification. First, we provide a general rank condition on the matrices of unit-specific and other covariates that requires that the covariate space of treated observations is spanned by that of the untreated ones. This assumption allows us to estimate from the untreated observations those nuisance parameters that are necessary to impute control outcomes of the treated observations, thus providing identification. Second, we derive specific conditions for the case where the parameter represents time fixed effects and may vary over time but not across units (as with unit FEs and unit-specific linear trends). In this case, we show that there is identification if (i) the are not collinear for any relevant unit and (ii) there is at least one untreated unit at the end of the time period of interest.

4.1 Efficient Estimation

For our efficiency result, we impose an additional assumption on the error variances:

Assumption 4 (Spherical errors).

Error terms are spherical, i.e. homoskedastic and mutually uncorrelated across all : .

While this assumption is strong, our efficiency results also apply without change under dependence that is due to unit random effects, i.e. if for that satisfy Assumption 4 and for some . Moreover, these results are straightforward to relax to any known form of heteroskedasticity or mutual dependence.212121For instance, if error terms are uncorrelated and have known variances (up to a scaling factor), efficiency requires the estimation step (Step 1) of Theorems 1 and 2 to be performed with weights proportional to . One example for this is when the data are aggregated from individuals randomly drawn from group in period and spherical individual-level errors, in which case efficiency is obtained with weights proportional to . Under Assumption 4 and allowing for restrictions on causal effects, we have:

Theorem 1 (Efficient estimator).

Suppose Assumptions 1′, 2, 3′ and 4 hold. Then among the linear unbiased estimators of , the (unique) efficient estimator can be obtained with the following steps:

-

1.

Estimate by the OLS solution from the regression Equation 4 (where we assume that is identified);

-

2.

Estimate the vector of treatment effects by ;

-

3.

Estimate the target by .

Moreover, this estimator is unbiased for under Assumptions 1′, 2 and 3′ alone, even when error terms are not spherical.

Under Assumptions 1′, 2 and 3′, regression Equation 4 is correctly specified. Thus, this estimator for is unbiased by construction, and efficiency under spherical error terms is a direct consequence of the Gauss–Markov theorem. Moreover, OLS yields the most efficient estimator for any linear combination of , including . While assuming spherical errors may be unrealistic in practice, we think of this assumption as a natural conceptual benchmark to decide between the many unbiased estimators of .222222This benchmark appears natural as it parallels the Gauss-Markov theorem which also relies on spherical errors. In Monte Carlo simulations (Section A.11), the estimator performs well even under deviations from spherical errors. In Section A.5 we generalize the results to parametric models of heteroskedasticity and serial correlation, in the spirit of generalized least squares (GLS) and relating to [62].

In the important special case of unrestricted treatment effect heterogeneity, has a useful “imputation” representation. The idea is to estimate the model of using the untreated observations and leverage it to impute for treated observations . Then, observation-specific causal effect estimates can be averaged appropriately. Perhaps surprisingly, the estimation and imputation steps are identical regardless of the target estimand. Applying any weights to the imputed causal effects yields the efficient estimator for the corresponding estimand. We have:

Theorem 2 (Imputation representation for the efficient estimator).

With a null Assumption 3′ (that is, if ), the unique efficient linear unbiased estimator of from Theorem 1 can be obtained via an imputation procedure:

-

1.

Within the untreated observations only (), estimate the and (by ) by OLS in

(5) -

2.

For each treated observation () with , set and to obtain the estimate of ;

-

3.

Estimate the target by a weighted sum .

The imputation representation offers computational and conceptual benefits. First, it is computationally efficient as it only requires estimating a simple TWFE model, for which fast algorithms are available [54, 11]. This is in contrast to the OLS estimator from Theorem 1, as equation Equation 4 has regressors in addition to the fixed effects, which are high-dimensional unless a low-dimensional model of treatment effect heterogeneity is imposed.

Second, the imputation approach is intuitive and transparently links the parallel trends and no-anticipation assumptions to the estimator. Indeed, [24] write: “At some level, all methods for causal inference can be viewed as imputation methods, although some more explicitly than others” (p. 141). We formalize this statement in the next proposition, which shows that any estimator unbiased for can be represented in the imputation way, but the way of imputing the may be less explicit and no longer efficient.

Proposition 6 (Imputation representation for all unbiased estimators).

Under Assumptions 1′ and 2, any linear estimator of that is unbiased under arbitrary treatment-effect heterogeneity (that is, a null Assumption 3) can be obtained via imputation:

-

1.

For every treated observation, estimate expected untreated potential outcomes by some unbiased linear estimator using data from the untreated observations only;

-

2.

For each treated observation, set ;

-

3.

Estimate the target by a weighted sum .

This result establishes an imputation representation when treatment effects can vary arbitrarily. Proposition A2 in the appendix establishes that the imputation structure applies even when restrictions are imposed, albeit with an additional step in which the weights defining the estimand are adjusted in a way that does not change under the imposed model.232323As a special case, we can still write the efficient estimator from Theorem 1 as an imputation estimator from Theorem 2 with alternative weights on the imputed treatment effects. Proposition A4 shows that these adjusted weights solve a quadratic variance-minimization problem with a linear constraint that preserves unbiasedness under Assumption 3. We also provide an explicit formula for the resulting weights in Proposition A3. In this sense, unbiased causal inference is equivalent to imputation in our framework.

4.2 Asymptotic Properties

Having derived the linear unbiased estimator for in Theorem 1 that is also efficient under spherical error terms, we now consider its asymptotic properties without imposing that assumption. We study convergence along a sequence of panels indexed by the sample size , where randomness stems from the error terms only, as in Section 2. Our approach applies to asymptotic sequences where both the number of units and the number of time periods may grow, but the assumptions are least restrictive when the number of time periods remains constant or grows slowly, as in short panels.

Instead of assuming that error terms are spherical, we now assume that error terms are clustered by units .

Assumption 5 (Clustered error terms).

Error terms are independent across units and have bounded variance, for uniformly.

The key role in our results is played by the weights that the Theorem 1 estimator places on each observation. Since the estimator is linear in the observed outcomes , we can write it as with non-stochastic weights , derived in Proposition A3 in the appendix.

We now formulate high-level conditions on the sequence of weight vectors that ensure consistency, asymptotic normality, and will later allow us to provide valid inference. These results apply to any unbiased linear estimator of , not just the efficient estimator from Theorem 1 – that is, if the respective conditions are fulfilled for the weights , then consistency, asymptotic normality, and valid inference follow as stated. For the specific estimator introduced above, we then provide sufficient low-level conditions for short panels.

First, we obtain consistency of under a Herfindahl condition on the weights that takes the clustering structure of error terms into account.

Assumption 6 (Herfindahl condition).

Along the asymptotic sequence, , for weights in the unbiased linear estimator .

The condition on the clustered Herfindahl index states that the sum of squared weights vanishes, where weights are aggregated by units. One can think of the inverse of the sum of squared weights, , as a measure of effective sample size, which Assumption 6 requires to grow large along the asymptotic sequence. If it is satisfied, and variances are uniformly bounded, we obtain consistency of :242424The Herfindahl condition can be restrictive since it allows for a worst-case correlation of error terms within units. When such correlations are limited, other sufficient conditions may be more appropriate instead, such as with , where . Here is a measure of the maximal joint covariation of all observations for one unit. If error terms are uncorrelated, then , since the maximal eigenvalue of corresponds to the maximal variance of an error term in this case, which is bounded by . An upper bound for is the maximal number of periods for which we observe a unit, since the maximal eigenvalue of is bounded by the sum of the variances on its diagonal.

Proposition 7 (Consistency of ).

We note that the large number of unit-specific parameters cannot generally be estimated consistently in panels with a small number of time periods, raising a potential incidental-parameters problem. However, consistency of does not rely on consistency for unit-specific parameters, since our estimator averages over many units.

We next consider the asymptotic distribution of the estimator around the estimand.

Proposition 8 (Asymptotic normality).

If the assumptions of Proposition 7 hold, there exists such that is uniformly bounded, the weights are not too concentrated in the sense that , and the variance does not vanish, for , then we have that .

This result establishes conditions under which the difference between estimator and estimand is asymptotically normal. Besides regularity, this proposition requires that the estimator variance does not decline faster than . It is violated if the clustered Herfindahl formula is too conservative: for instance, if the number of periods is growing along the asymptotic sequence while the within-unit over-time correlation of error terms remains small. Alternative sufficient conditions for asymptotic normality can be established in such cases, e.g. along the lines of Footnote 24.

So far, we have formulated high-level conditions on the weights of any linear unbiased estimator of . Section A.7 presents low-level sufficient conditions for consistency and asymptotic normality of the imputation estimator for the benchmark case of a panel with unit and period FEs, a fixed or slowly growing number of periods, and no restrictions on treatment effects. Unlike Propositions 7 and 8, these conditions are imposed directly on the weights chosen by the researcher, and not on the the implied weights , such that the researcher can assess more directly whether the asymptotic approximation is likely to be precise. In particular, the estimator achieves consistency and asymptotic normality in the common case where the number of time periods is fixed, the size of all cohorts increases, the weights on treatment effects do not vary within the same period and cohort, and the sum of (absolute) weights is bounded. In addition, the sufficient conditions are also fulfilled when the number of periods grows slowly and when weights differ across observations within the same cohort and period, but not by too much. With covariates other than unit and period FEs, e.g. with unit-specific linear trends, the general weight conditions in Assumption 6 and Proposition 8 can also be used to verify consistency and asymptotic normality. In those cases, the sufficient conditions are typically fulfilled for convex combinations of cohort-average treatment effects whenever the size of cohorts grows sufficiently fast relatively to the number of periods (see Section A.7).

4.3 Conservative Inference

We next estimate the variance of , which equals with clustered error terms (Assumption 5). We start with the case where treatment effect heterogeneity is unrestricted (i.e. ). As in [51], exact inference becomes infeasible when treatment effects are heterogeneous, but conservative inference is possible. Following Section 4.2, the inference tools we propose apply to a generic linear unbiased estimator but we use them for the efficient estimator . Our strategy is to estimate individual error terms by some and then use a plug-in estimator,

| (6) |

Estimating the error terms presents two challenges, which become apparent when we consider the benchmark choice based on the regression residuals in the regression Equation 4. The first challenge is the incidental-parameters problem in estimating . However, by using cluster-robust variance estimates, our inference does not suffer from this problem since the variance estimator does not rely on the consistent estimation of any more, similar to the insight of [42].

A second challenge arises from unrestricted treatment-effect heterogeneity. In Theorem 2, treatment effects are estimated by fitting the corresponding outcomes perfectly, with residuals for all treated observations. This issue is not specific to our estimation procedure: one generally cannot distinguish between and from observations of for treated observations, making it impossible to produce unbiased estimates of (see Lemma 1 in [56] for a similar impossibility result).

While unbiased estimation of is not possible, we show that this variance can be estimated conservatively. Our variance estimator is based on an auxiliary parsimonious model of treatment effects. We do not require this model to be correct, in the sense that inference is weakly asymptotically conservative under misspecification. However, auxiliary models which better approximate will make confidence intervals tighter and closer to asymptotically exact. In the computation of we set for the treated observations equal to the residuals of the auxiliary model. We require the model to be parsimonious, such that it does not overfit and the residuals include . When the model is incorrect, also include a component due to the misspecification of , leading to conservative inference.

We formalize the auxiliary model by considering estimators for each which satisfy two properties: (1) converges to some non-stochastic limit and (2) if the auxiliary model is correct, . The following theorem presents conditions under which our construction yields asymptotically conservative inference:

Theorem 3 (Conservative clustered standard error estimates).

Assume that the assumptions of Proposition 7 hold, that the model of treatment effects is trivial (), that the estimates converge to some non-random in the sense that , that from Theorem 1 is sufficiently close to in the sense that , and that and are uniformly bounded and the weights are not too concentrated in the sense that . Then the variance estimate

| (7) |

is asymptotically conservative: where . If for all , , meaning that the variance estimate is asymptotically exact.

The theorem shows that the proposed variance estimate addresses the two challenges laid out above. First, the estimates remain valid even though we may not be able to estimate the unit-specific parameters consistently. This is because unit-specific parameter estimates drop out when summing over all observations of one unit in Equation 7, as shown in the proof. Second, by using estimates that fulfill the convergence condition of the theorem, we avoid the issue of obtaining trivial residuals for the treated observations. The resulting variance estimates are asymptotically conservative. From these estimates we can also obtain conservative confidence intervals (that asymptotically have coverage that is at least nominal) if the estimator is also asymptotically normal, such as under the sufficient conditions of Proposition 8.

It remains to choose the estimates . We focus on auxiliary models that impose the equality of treatment effects across large groups of treated observations: for a partition , for all . The can then be estimated by some weighted average of among . Specifically, we propose averages of the form

| (8) |

In Section A.8, we show that this choice of weights leads to minimal excess variance in the case where there is only a single group , corresponding to a conservative auxiliary model which requires all treatment effects to be the same. The choice of the partition aims to maintain a balance between avoiding overly conservative variance estimates and ensuring consistency. If the sample is large enough, one may want to partition into multiple groups of observations such that treatment effect heterogeneity is expected to be smaller within them than across. For instance, with many units, a group may consist of observations corresponding to the same horizon relative to treatment onset. If cohorts are large, one can further partition observations into groups defined by cohort and period, which we use as the default in our Stata command.

While sufficiently large groups in Equation 8 avoid overfitting asymptotically (under appropriate conditions), in finite samples these still use and thus partially overfit to . In Section A.9 we therefore also consider leave-out versions of these .

We make four final remarks on Theorem 3. First, our strategy for estimating the variance extends directly to conservative estimation of variance-covariance matrices for vector-valued estimands, e.g. for average treatment effects at multiple horizons . Second, the result applies in short panels under the low-level conditions of Section A.7 (see Proposition A7). Third, while we have focused here on the case of unrestricted heterogeneity (), Theorem 3 can be extended to the case with a non-trivial treatment-effect model imposed in Assumption 3.252525By Proposition A2, the general efficient estimator can be represented as an imputation estimator for a modified estimand, i.e. by changing to some . Theorem 3 then yields a conservative variance estimate for it. We note that under sufficiently strong restrictions on treatment effects, asymptotically exact inference may be possible, as the residuals in Equation 4 may be estimated consistently even for treated observations (except for the inconsequential noise in ), alleviating the need for an additional auxiliary model. Finally, computation of for the estimator from Theorem 1 involves the implied weights , which becomes computationally challenging with multiple sets of high-dimensional FEs. In Section A.10 we develop a computationally efficient algorithm for computing based on the iterative least squares algorithm for conventional regression coefficients [54].

4.4 Testing for Parallel Trends

In this section, we discuss testing the (generalized) parallel-trend and no-anticipation assumptions Assumptions 1′ and 2. We propose a testing procedure based on OLS regressions with untreated observations only, departing from both traditional regression-based tests and more recent placebo tests. This procedure is robust to treatment effect heterogeneity and, under spherical errors, has attractive power properties and avoids the problem of inference after pre-testing explained by [37]. We propose:

Test 1.

(Robust OLS-based pre-trend test)

-

1.

Choose an alternative model for for untreated observations that is richer than that imposed by Assumptions 1′ and 2: for an observable vector (which we consider non-stochastic, like and ),

(9) -

2.

Estimate by in Equation 9 using OLS on untreated observations only;

-

3.

Test using the heteroskedasticity- and cluster-robust Wald test.

This test is valid because equation Equation 9 is implied by Assumptions 1′ and 2 if the null holds.262626There is a natural alternative test of the null in the model Equation 9, namely the Hausman test based on the difference between the imputation estimator based on the model in Equation 9 and the efficient imputation estimator that is only valid when . Like our test, this test only uses untreated observations and avoids the [37] pre-testing problem for spherical errors. The Hausman approach has the advantage of quantifying the magnitude of bias from omitting , while Test 1 has the advantage that it is also informative about violations that cancel out in the Hausman test. The two tests are equivalent for scalar .

The test requires choosing to parametrize the possible violation of Assumptions 1′ and 2. A natural choice for , which parallels conventional pre-trend tests, is a set of indicators for observations periods before the onset of treatment for some , with periods before serving as the reference group.272727The optimal choice of is a challenging question. As usual with Wald tests, choosing a that is too large can lead to low power against many alternatives, in particular those that generate large biases in treatment effect estimates that impose invalid Assumption 1′. This choice is appropriate, for instance, if the researcher’s main worry is the possible effects of treatment anticipation, i.e. violations of Assumption 2. This choice of also lends itself to making “event study plots,” which combine the ATT estimates by horizon with a series of pre-trend coefficients; we supply the event_plot Stata command for this goal. Alternatively, the researcher may focus on possible violations of Assumption 1′. For instance, with data spanning many years one could test for the presence of a structural break in unit FEs.

Test 1 can be contrasted with two existing strategies to test parallel trends. Traditionally, researchers estimated a dynamic specification including lags and leads of treatment onset, and tested — visually or statistically — that the coefficients on leads are equal to zero. More recent papers [[, e.g.]]DeChaisemartin2018,Liu2020a replace it with a placebo strategy: pretend that treatment happened periods earlier for all eventually treated units, and estimate the average effects periods after the placebo treatment using the same estimator as for actual estimation.

Both of these alternatives strategies have drawbacks. Because the traditional regression-based test uses the full sample, including treated observations, and imposes restrictions on treatment effects (which are assumed homogeneous within each horizon), it is not a test for Assumptions 1′ and 2 only. Rather, it is a joint test that is sensitive to violations of the implicit Assumption 3 [60]. Even if a researcher has reasons to impose a non-trivial Assumption 3 in estimation, a robust test for parallel trends and no anticipation per se should avoid those restrictions on treatment effect heterogeneity. With a null Assumption 3, treated observations are not useful for testing, and our test only uses the untreated ones.282828[62] shows that as long as treatment effects are allowed to vary flexibly, tests based on specifications estimated on the full sample do not use treated observations. Therefore, such tests are also not contaminated by treatment effect heterogeneity.

Tests based on placebo estimates appropriately use untreated observations only and may have intuitive appeal. However, mimicking the estimator does not generally correspond to an efficient test of a class of plausible alternatives. In contrast, Test 1 possesses well-known asymptotic efficiency properties when is correctly specified. For example, when are spherical and normal, it is asymptotically equivalent to the homoskedastic -test, which is a uniformly most powerful invariant test [30, ch. 7.6].

Finally, we show an additional advantage of Test 1: if the researcher conditions on the test passing (i.e. does not report the results otherwise), inference on is still asymptotically valid under the null of no violations of Assumptions 1′ and 2 and under spherical errors. This avoids the issue pointed out by [37, Proposition 4] in the context of restrictive dynamic event study regressions: that variance estimates which do not take pre-testing into account are inflated, leading to unnecessarily conservative inference.292929[37] points out another issue, which we also avoid under the assumptions of Proposition 9: when pre-trend and treatment effect estimators are correlated, the bias arising from violations of Assumptions 1′ and 2 is affected by pre-testing; it is exacerbated in specific cases [37, Proposition 2].

Proposition 9 (Pre-test robustness).

Suppose the model in Equation 9 and Assumption 4 hold. Then constructed as in Theorem 1 is uncorrelated with any vector constructed as in Test 1. If the error terms are also normally distributed,303030The normality assumption is not essential; in the proof, we show that a similar, asymptotic result holds generally under regularity conditions. then and are independent, and inference on based on is unaffected by pre-tests based on .313131An early version of [37] shows how to construct an adjustment that removes the dependence when it exists, provided the covariance matrix between and can be estimated. By Proposition 9, this adjustment is not needed for the Theorem 1 estimator under spherical errors.

5 Application

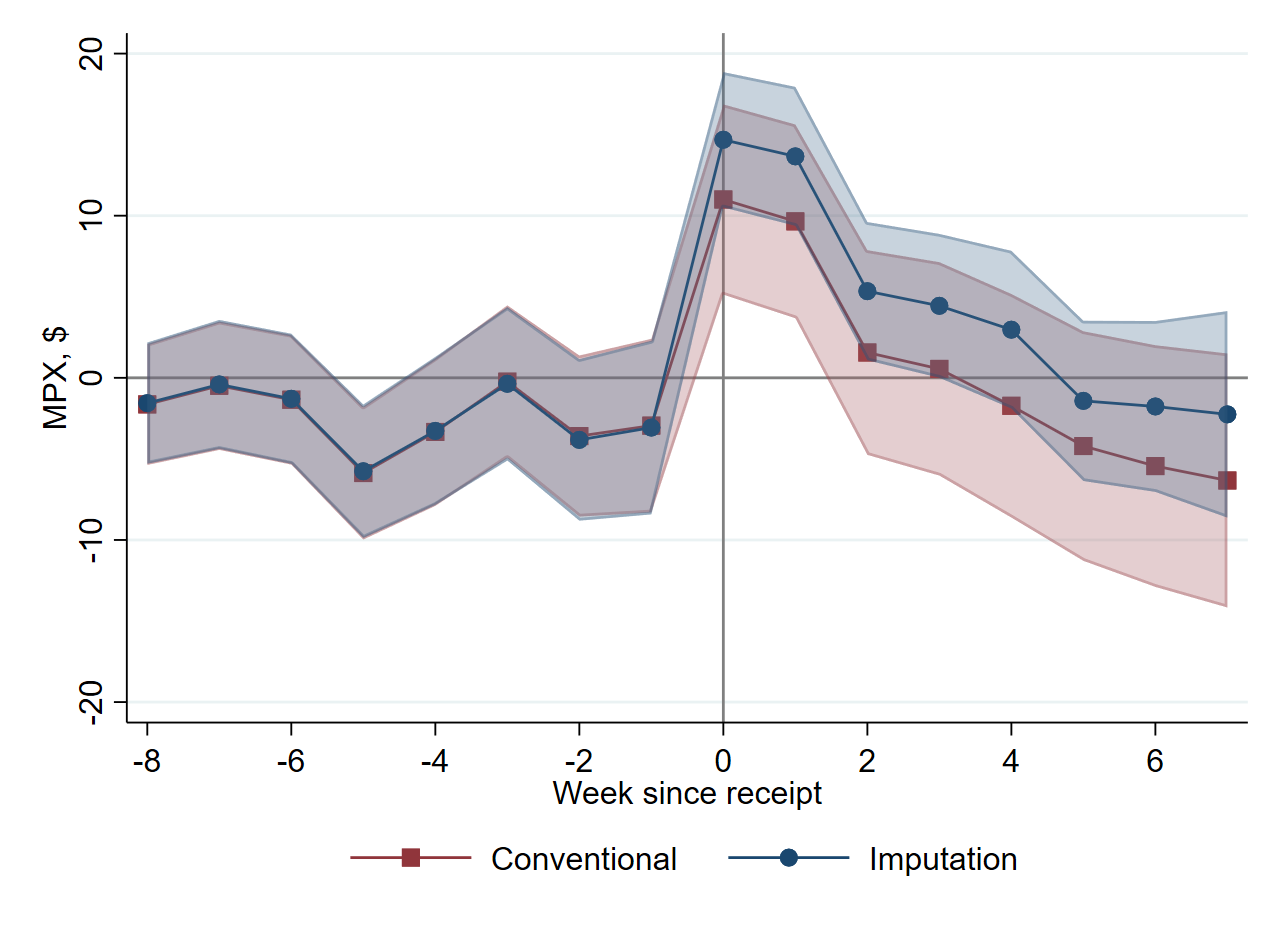

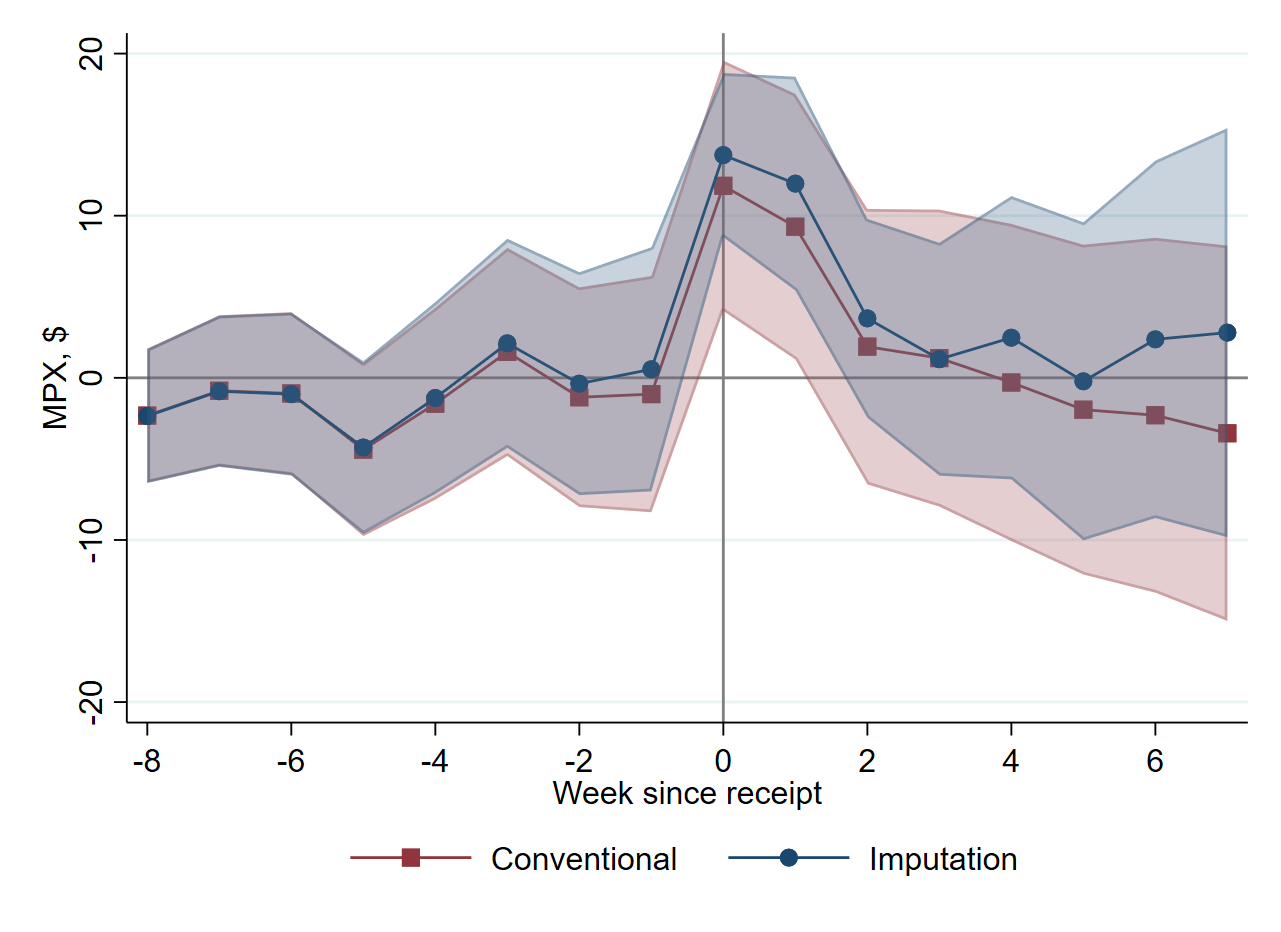

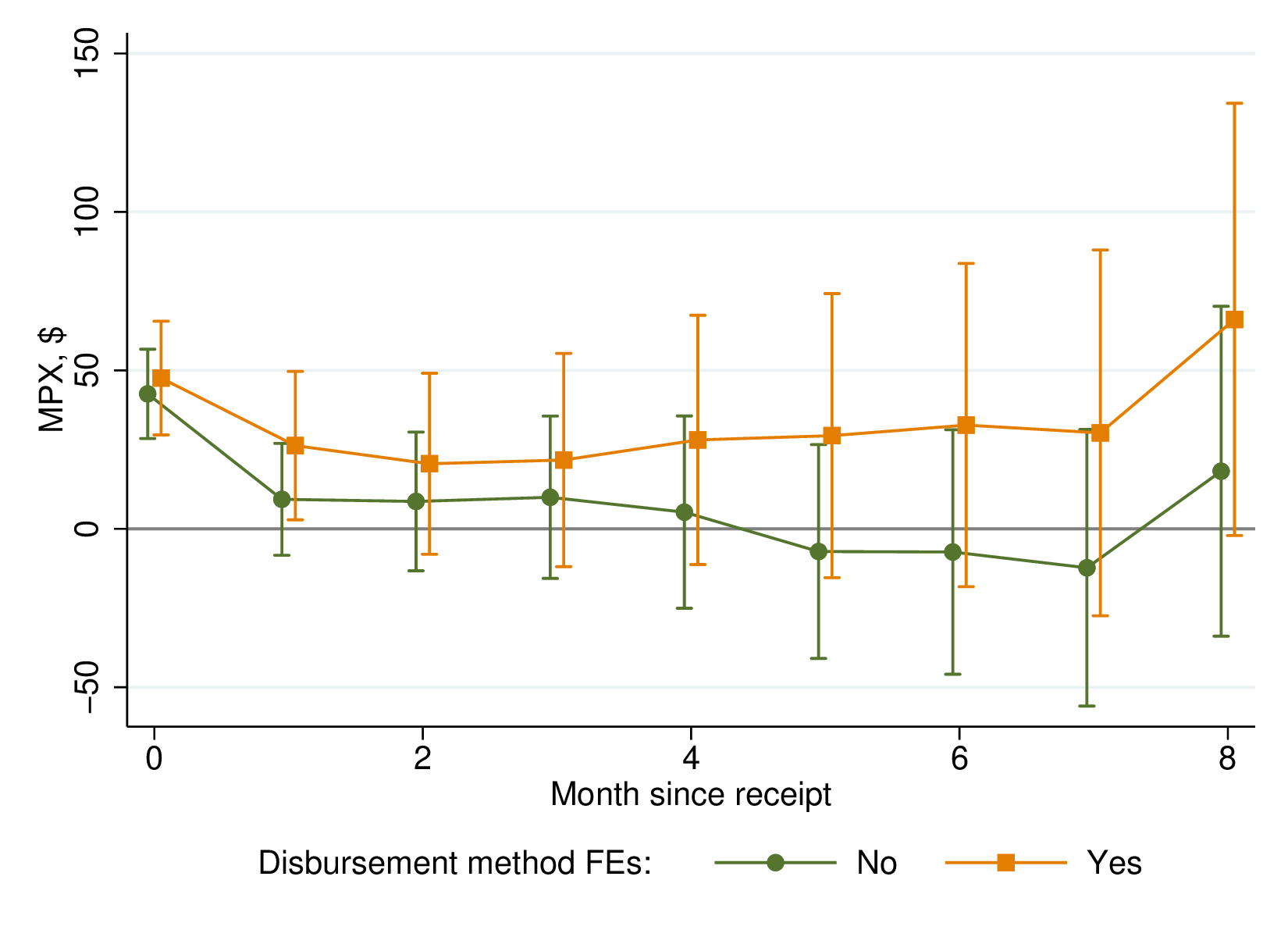

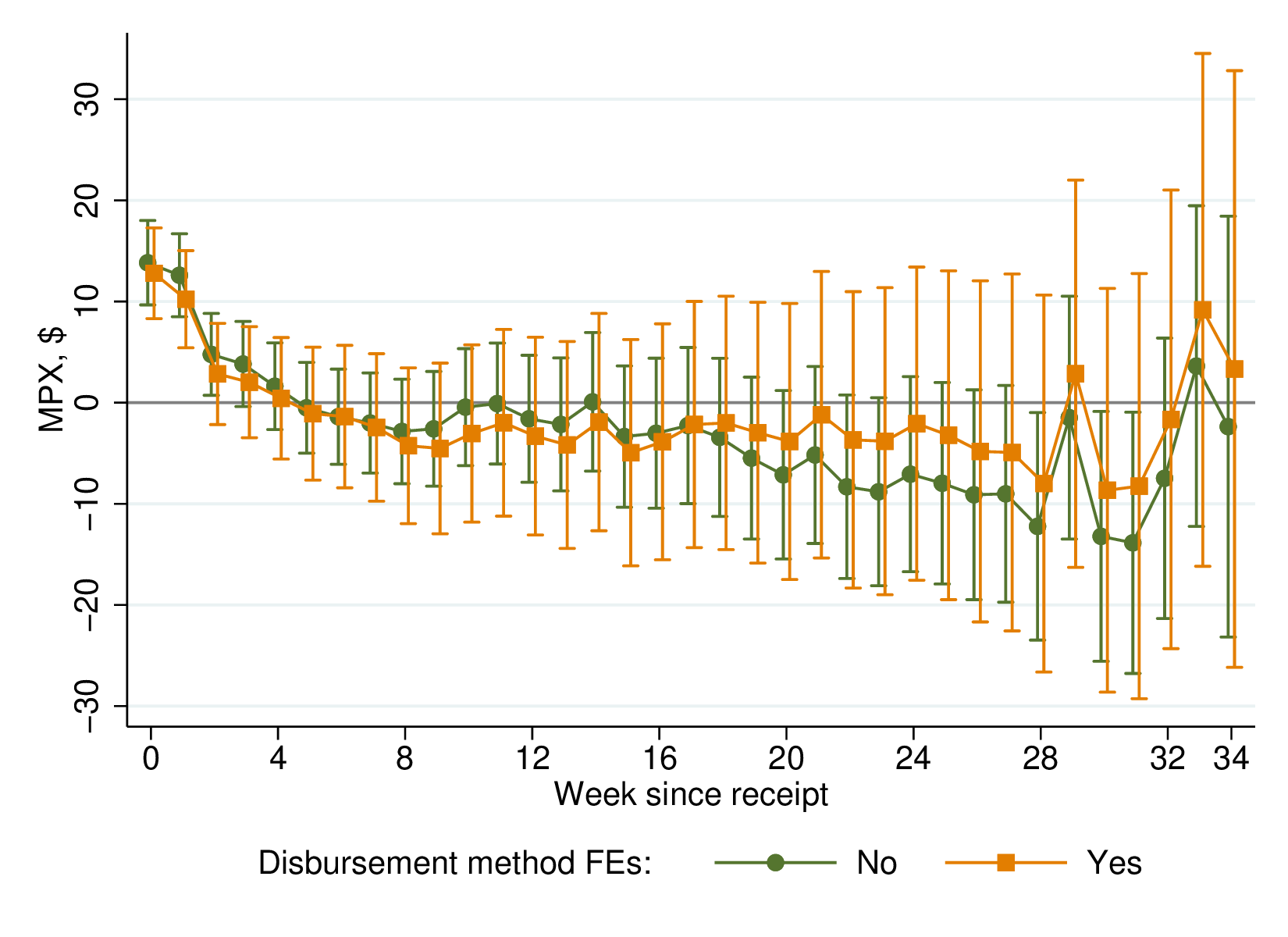

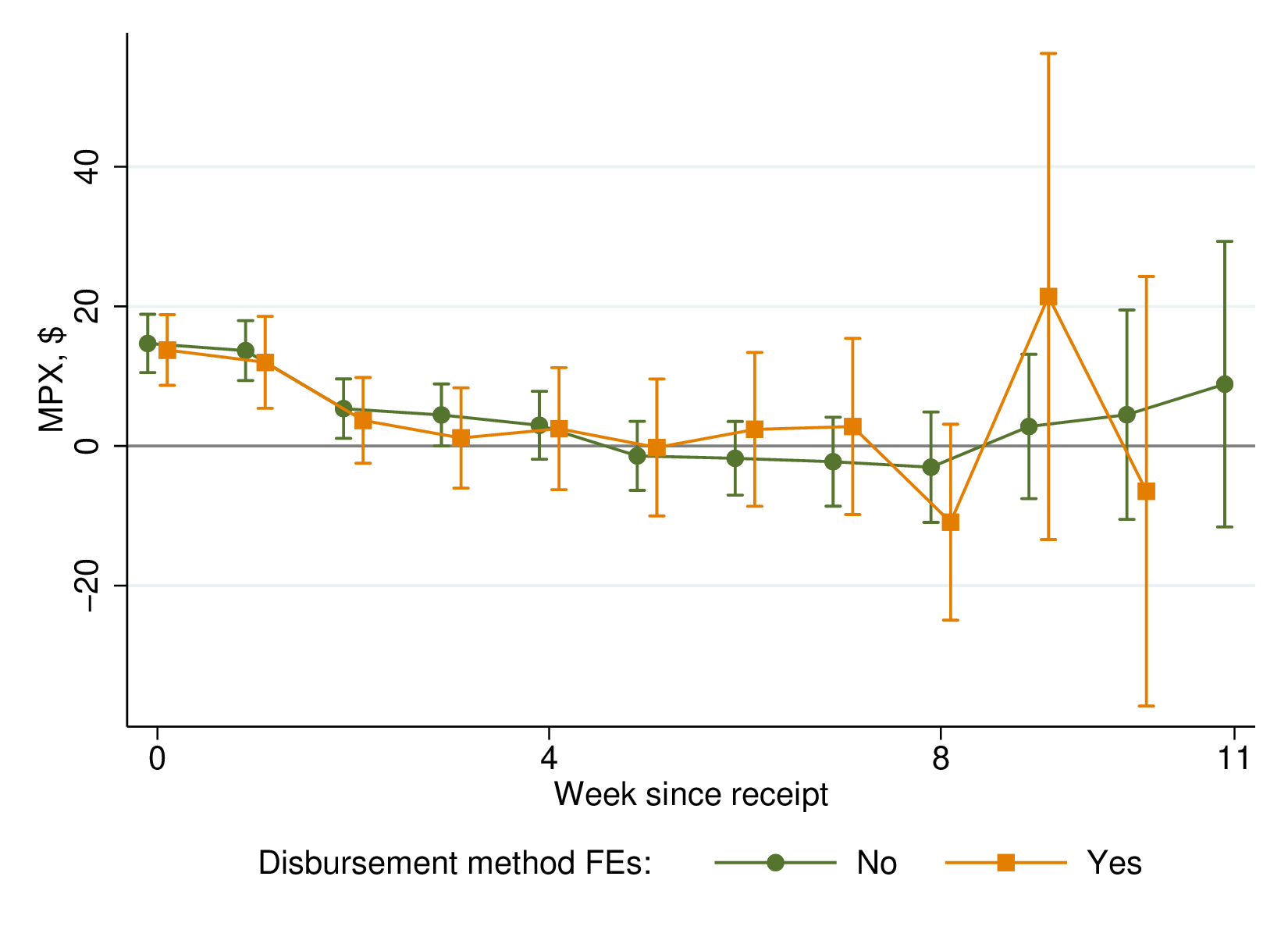

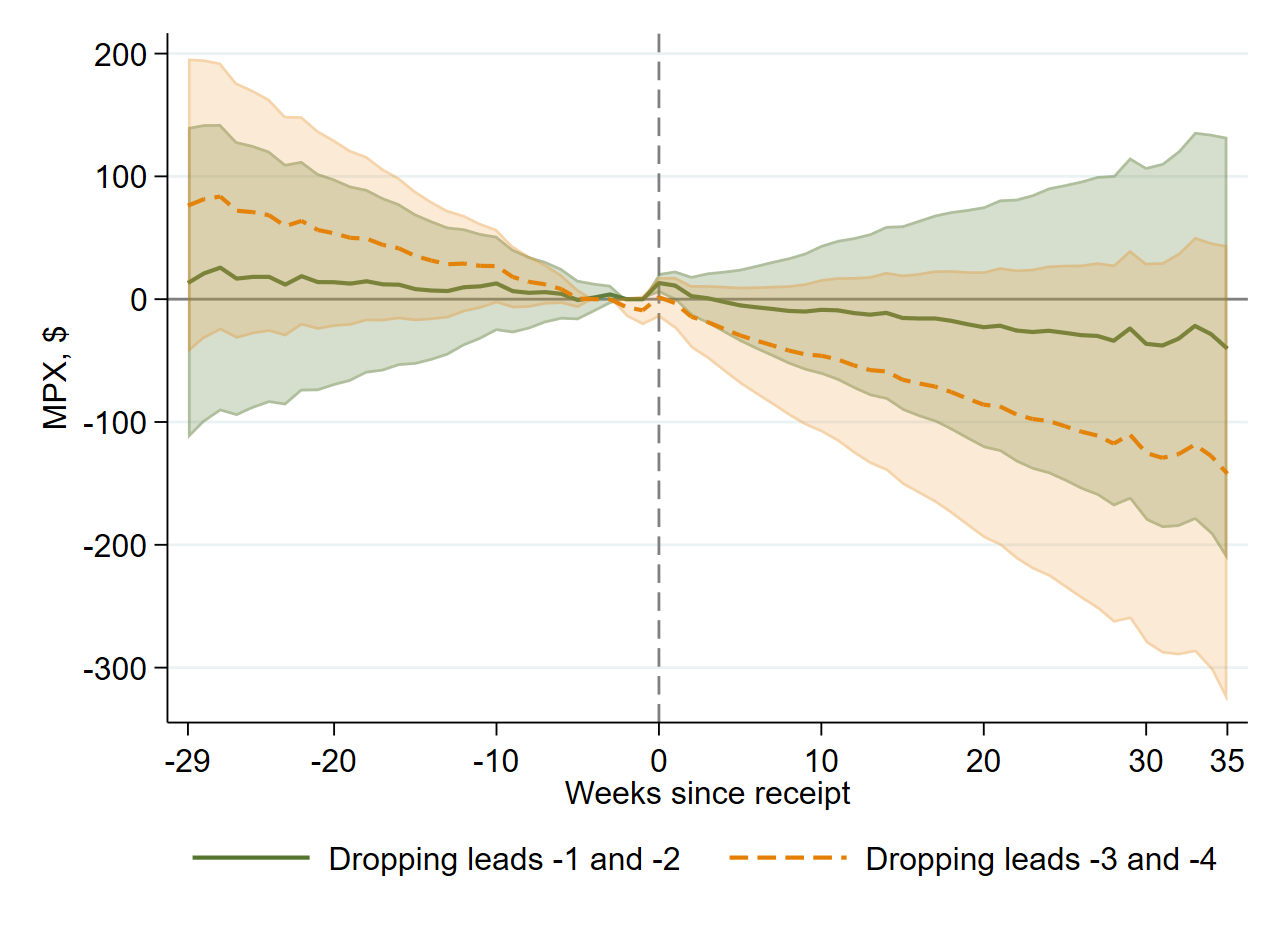

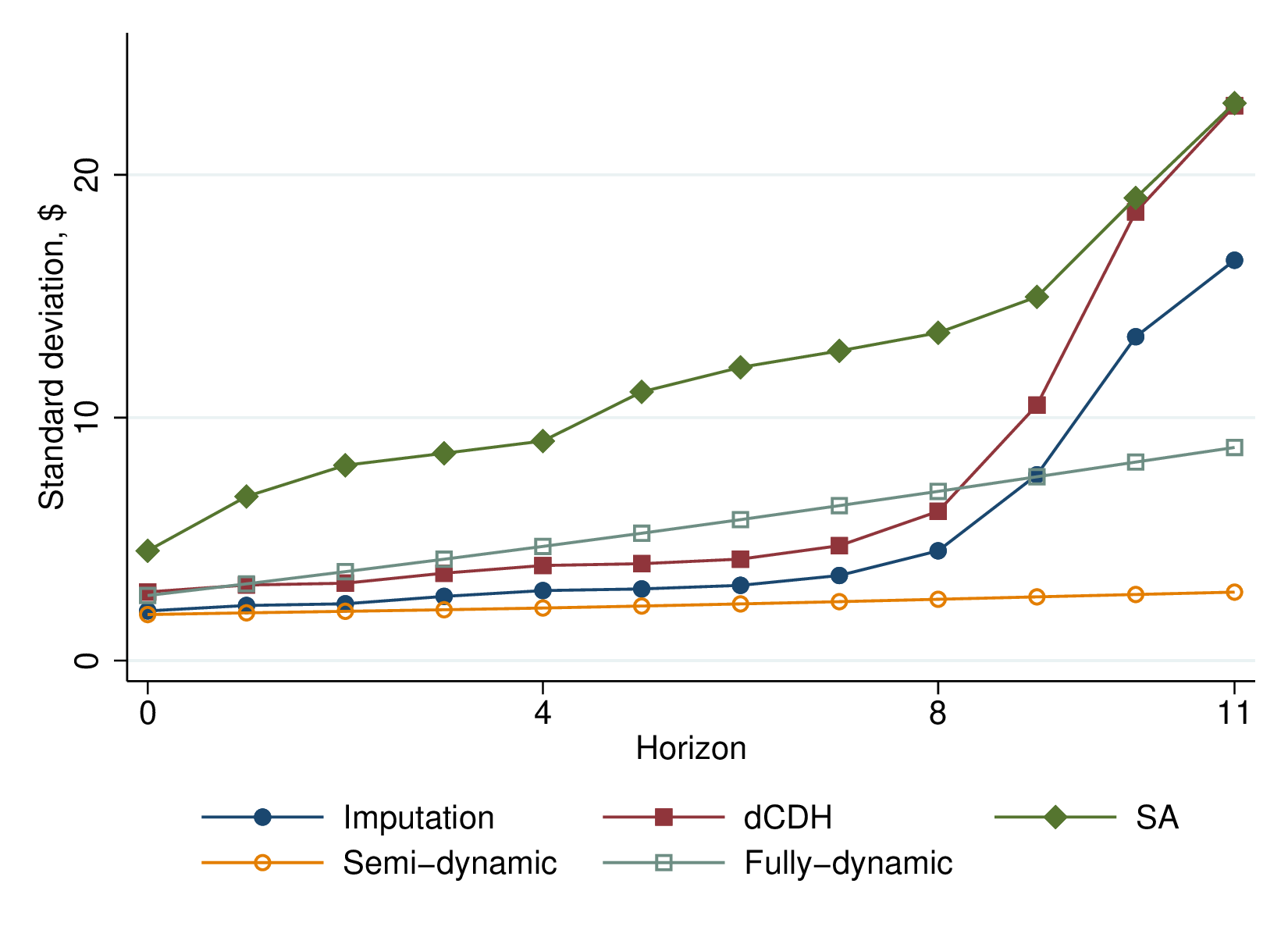

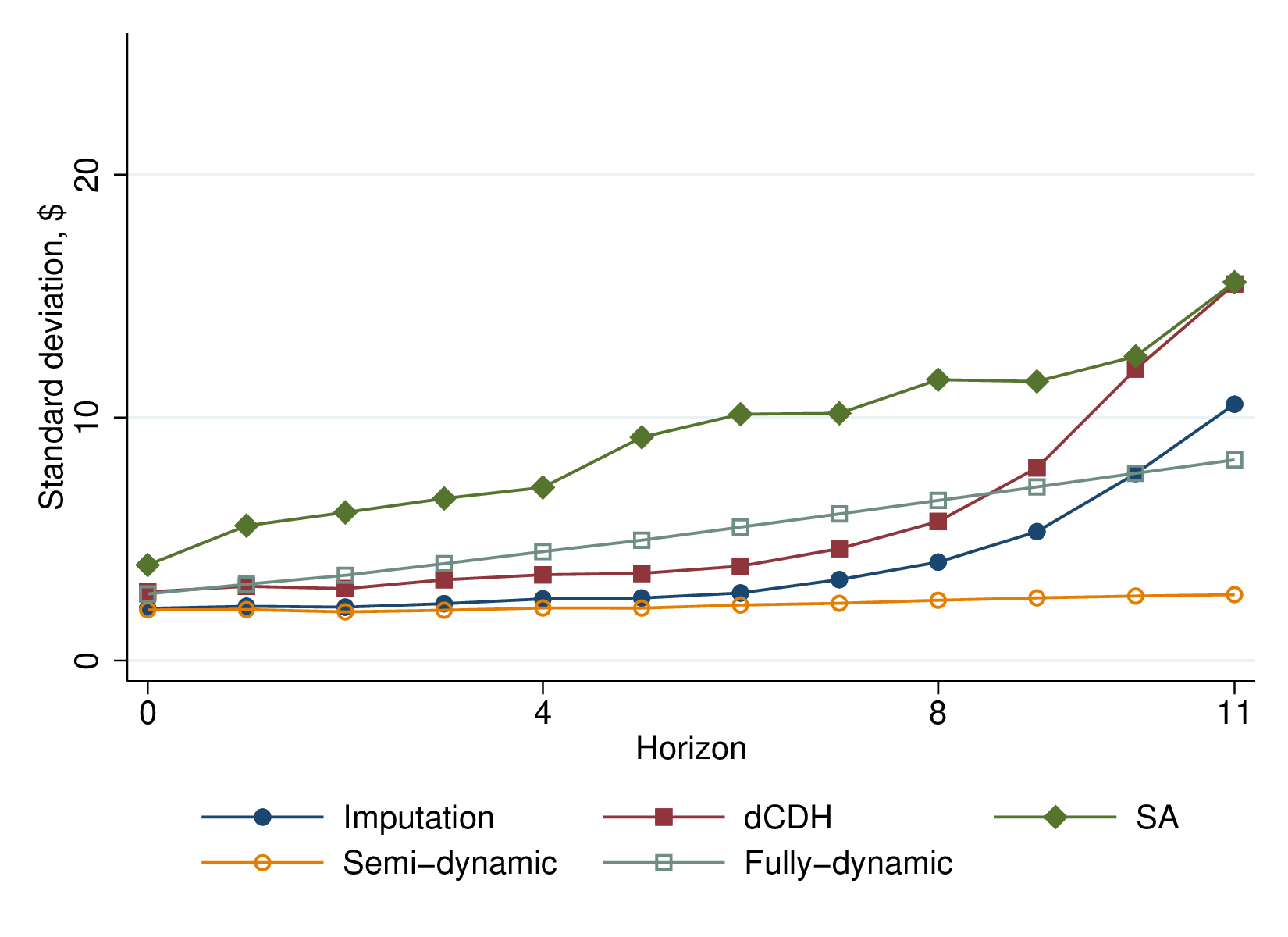

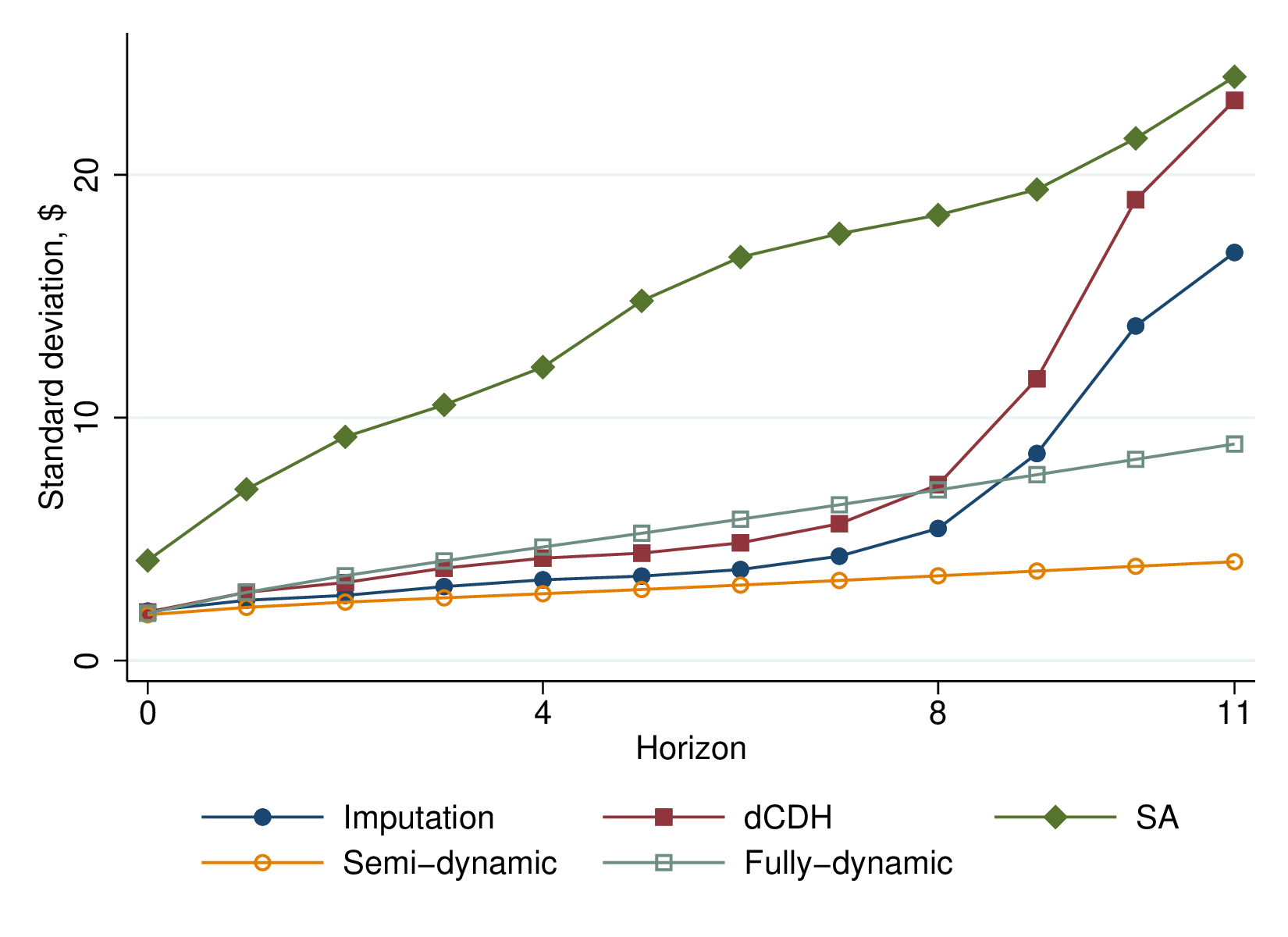

Having derived the attractive theoretical properties of the imputation estimator, we now illustrate their practical relevance by revisiting the estimation of the marginal propensity to spend in the event study of [7]. We also use this empirical setting to verify the properties of the imputation estimator in a simulation study.

5.1 Setting

The marginal propensity to spend out of tax rebates is a crucial parameter for economic policy. In the US, the Economic Stimulus Act of 2008 consisted primarily of a 100 billion dollar program that sent tax rebates to approximately 130 million tax filers. [35] and [7] estimate the marginal propensity to spend (MPX) out of the 2008 tax rebates. The rebate was disbursed using two methods: either via direct deposit to a bank account, if known by the IRS, or with a mailed paper check. For each method, the week in which the funds were disbursed depended on the second-to-last digit of the taxpayer’s Social Security number (SSN). This number provides a source of quasi-experimental variation because the last four digits of a SSN are assigned sequentially to applicants within geographic areas.

[7, henceforth BP] use an event study design to examine the response of nondurable spending to tax rebate receipt, leveraging the quasi-experimental variation in the timing of the receipt. The quasi-random assignment of the last digits of the SSN makes the parallel-trends assumption for expenditures a priori plausible.323232[45] point out that for the paper check group pre-rebate household characteristics (in levels) are not balanced with respect to the timing of the receipt. While this is problematic for randomization-based approaches to DiD (e.g. [3] and [38]), parallel trends in expenditures may still hold. Indeed, we fail to reject them with pre-trend tests below. The no-anticipation assumption may also be expected to hold: although the disbursement schedule was known in advance, households were directly notified by mail only several days before disbursement.

We estimate the performance of various estimators at estimating the impulse response function of nondurable spending to tax rebate receipt using the same data as BP. While earlier work by [35] estimates the impulse responses using quarterly spending data from the Consumer Expenditure Survey, BP leverage more detailed data from the Nielsen Homescan Consumer Panel. The Nielsen dataset tracks transactions at a much higher (in principle, daily) frequency, which is why we choose it for our analysis. The Nielsen data cover expenditures on consumer packaged goods (food, beverages, beauty and health products, household supplies, and general merchandise), representing around 15% of total household expenditures. Our dataset, identical to that of BP, is a complete panel of 21,760 households (including 21,690 with non-missing disbursement method information) observed over 52 weeks of year 2008.

5.2 Comparison between Robust and Conventional Estimates

We show how BP’s estimates of the MPX suffer from an upward bias in the short-run due to the choice of a binned specification (Section 5.2.1) and how they may be spurious in the long-run (Section 5.2.2). In Section 5.2.3 we present our preferred robust estimates and discuss implications for the macroeconomics literature.

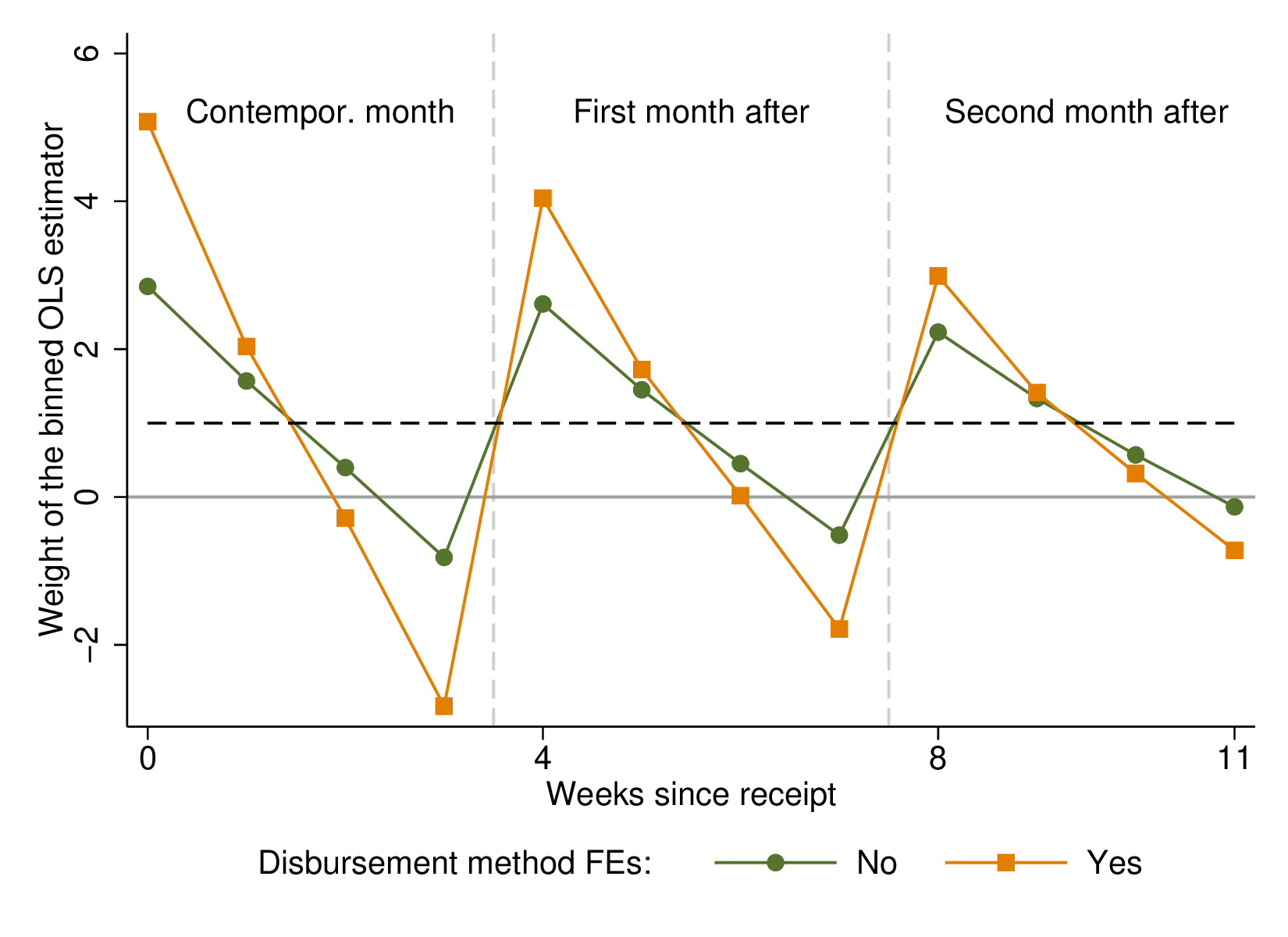

5.2.1 Negative Weighting and Upward Bias with Binning

We replicate BP’s estimates, focusing on the first three months since the receipt, while leaving longer-run effects to Section 5.2.2. BP estimate conventional dynamic specifications of the form:

| (10) |