A class of dependent Dirichlet processes via latent multinomial processes

Abstract

We describe a procedure to introduce general dependence structures on a set of Dirichlet processes. Dependence can be in one direction to define a time series or in two directions to define spatial dependencies. More directions can also be considered. Dependence is induced via a set of latent processes and exploit the conjugacy property between the Dirichlet and the multinomial processes to ensure that the marginal law for each element of the set is a Dirichlet process. Dependence is characterised through the correlation between any two elements. Posterior distributions are obtained when we use the set of Dirichlet processes as prior distributions in a Bayesian nonparametric context. Posterior predictive distributions induce partially exchangeable sequences defined by generalised Pólya urns. A numerical example to illustrate is also included.

Keywords: Bayesian nonparametrics, generalised Pólya urn, moving average process, spatio-temporal process, stationary process.

1 Introduction

The Dirichlet process (DP), introduced by Ferguson, (1973), is the most important process prior in Bayesian nonparametric statistics. It is flexible enough to approximate (in the sense of weak convergence) any probability law, although the paths of the process are almost surely discrete (Blackwell and MacQueen,, 1973). A DP measure is characterised by a precision parameter and a centring measure defined on , in notation . In general, for any and any partition of , the random vector , that is, has a Dirichlet distribution.

Sethuraman, (1994) characterised the DP as an infinite sum of random jumps with probabilities at random locations , i.e., , where and is the dirac measure at . This characterisation is also known as stick-breaking since with , that is a beta distribution.

There have been several proposals to construct dependent measures in Bayesian nonparametrics. They can be classified into three categories: stick breaking, random measures and predictive schemes. We briefly describe them here.

MacEachern, (1999) introduced a general idea to define dependent Dirichlet processes (DDP) as a way of extending the DP model to multiple random measures . His idea relies on the stick-breaking representation of the DP and introduces dependence by making the probabilities and/or the locations to be a function of , say and , where is an indexing covariate and is a suitable space. There have been many proposals in the literature to achieve this and most of them have been summarised in Quintana et al., (2020). For example, Rodríguez et al., (2010) rely on latent gaussian copula models to introduce dependence in the locations, and Camerlenghi et al., 2019a define the locations as Dirichlet processes or normalised random measures (Regazzini et al.,, 2003).

A Dirichlet process can also be seen as a normalisation of a gamma process (Ferguson,, 1974). The more general class of normalised random measures relies on normalising increasing additive processes, where the gamma process is a particular case. A way of introducing dependence, not necessarily in Dirichlet processes, is by making the underlying (unnormalised) random measures to be dependent (e.g. Griffin et al.,, 2013; Lijoi et al., 2014a, ). Clustering performance of a specific class of dependent normalised random measures in mixture models is studied in Lijoi et al., 2014b .

In a different perspective, Walker and Muliere, (2003) defined a DDP via predictive schemes for only two random measures . Their approach relies on a latent Dirichlet-multinomial process . Other approaches are those of Müller et al., (2004) who introduced dependence by considering convex linear combinations of a common measure and idiosyncratic measures for different studies, and Teh et al., (2006) who introduced the so called hierarchical Dirichlet process by taking conditionally independent for a set of ’s and . Distribution properties of this and more general hierarchical processes is studied in Camerlenghi et al., 2019b .

Posterior predictive distributions of a DP induce exchageable sequences of variables whose law is characterised by a Pólya urn (Blackwell and MacQueen,, 1973). A DDP can also be defined via generalisations of the Pólya urn to induce partially exchangeable sequences. For instance, Caron et al., (2007) induce dependence in time via a deletion strategy of past urns, whereas Papaspiliopoulos, (2016) and Ascolani et al., (2021) use a Fleming-Viot process to induce dependence among random measures by sharing a common pool of atoms that depend on a latent death process.

In this article we construct a class of DDP by considering a predictive scheme, as in Walker and Muliere, (2003), for multiple random measures that have DP marginal distributions and can be temporal and/or spatial dependent. Predictive distributions of our construction induce partial exchangeable sequences defined by a generalised Pólya urn.

The content of the rest of the paper is as follows: In Section 2 we define our generalisation and characterise the dependence induced. In Section 3 we use our model as a Bayesian nonparametric prior distribution, characterise its posterior laws and define a generalised Pólya urn to define partially exchangeable sequences. We illustrate the use of the model in Section 4 and conclude in Section 5.

2 Model construction

Let us start by defining a multinomial process . This is characterised by an integer parameter and a measure defined on , in notation , such that for any and for any partition of , the random vector , that is, a multinomial distribution with number of trials and probabilities , . Moreover, if we sample independently and identically distributed from , then the multinomial process is defined as . Moreover, if and conditionally on , , then marginally , that is, a Dirichlet-multinomial process with parameters .

We now recall the bivariate Dirichlet process of Walker and Muliere, (2003). Their construction takes , and . Then, after marginalising the latent process , the pair is a DDP with marginal distributions for and correlation given by for any set .

We note that Walker and Muliere, (2003)’s construction is reversible, so we can start by taking

| (1) |

for to obtain the same bivariate model such that marginally. Therefore the key aspect to obtain a Dirichlet process marginal distribution is to condition on a latent whose law is a Dirichlet-multinomial process.

We extend this idea to multiple processes with a finite index set, say with . For that we require a set of latent processes , one for each , plus a single latent process that will play the role of anchor. Let be a set of “neighbours”, in the broad sense, for each . For instance, if denotes time, we can define dependencies among the ’s of order as in time series moving average models. In this case . We show in Figure 1 a graphical model with temporal dependence of order . Moreover, if denotes a spatial location, then , where “” denotes actual spatial neighbour. More general definitions of can be taken to define seasonal or spatio-temporal models (see Nieto-Barajas,, 2020). In any case for all .

Then, the law of the dependent set is characterised by a three level hierarchical model with the following specifications:

| (2) | ||||

for , where the set is such that , for , and take and with probability one (w.p.1) for . In notation we say that .

Properties of construction (2) are given in Proposition 1. In particular, the correlation induced and the marginal distributions can be obtained in closed form.

Proposition 1

Let be a set of dependent measures , defined by (2).

-

(i)

The marginal distribution of is for all .

-

(ii)

The correlation between any pair of measures for is given by

for , and

for such that .

-

(iii)

If for all then the ’s become independent.

Proof

- (i)

-

(ii)

We note that for a single set , , and in (2) simplify to beta, binomial and beta distributions, respectively. We rely on conditional independence properties and the iterative covariance formula. Then for the first part, . The first term in the sum becomes zero since ’s are conditionally independent given , for . The second term, after removing the additive constants of the expected values, is rewritten as divided by . Concentrating in the numerator, and using the iterative covariance formula for a second time, we get . The first term, after separating the sums in the common part, reduces to which becomes . After computing the expected value, this can be re-written as . The second term, after computing the expectations becomes . Finally, using , we note that , so dividing the covariance between the product of the standard deviations we obtain the result. For the second part, we proceed analogously, the covariance is the same as before but is replaced by . Dividing by the product of standard deviations we get the result.

-

(iii)

We note that if then w.p.1. If we do this for all then it is straightforward to see that the measures ’s become independent.

Many things can be concluded from Proposition 1. Parameter and are the precision and centring measure parameters, respectively, of all Dirichlet process marginal distributions. Parameters for control the strength of the correlation between any two elements and , together with the definition of the neighbours . The correlation is stronger, if the two elements share more parameters. Some locations can be more influential than others if their corresponding parameter is larger. Moreover, the set becomes strictly stationary if the parameters for , which implies that the correlation for simplifies to

where denotes the number of elements in the set .

Let us consider a set with only two elements, . There are several ways of defining dependencies between and . For instance, an order 1 moving average time series model would have and . Then, for a set , , which is the same correlation induced by the bivariate DDP of Walker and Muliere, (2003). Alternatively, nothing constrains us to define circular dependencies, say . In this case the correlation induced becomes .

3 Posterior characterisation and Pólya urn

Let us assume that we observe a partially exchangeable sequence in the sense of de Finetti, (1972). That is, for each , we observe a sample of size , say such that for . Moreover, the prior distribution for the set is defined by the given in (2).

Since ’s are independent Dirichlet processes, the conditional posterior distribution for each given , does not depend on , and can be straightforwardly derived (Ferguson,, 1973)

| (3) |

where is the empirical distribution function of sample , for .

To produce posterior inferences we also need to provide the full conditional distributions for the processes and . For an arbitrary partition , the posterior conditional distribution of given , does not depend on , and is given by

| (4) |

where is the reversed set of neighbours of , that is, .

Finally, the posterior conditional law for the process given , does not depend on , is another DP of the form

| (5) |

With conditional posterior laws , and , given in (3), (4) and (5), respectively, we can implement a Gibbs sampler (Smith and Roberts,, 1993) to obtain posterior summaries. In practice, we choose an arbitrary partition of size to approximate the paths of the processes. The larger the , the more precise the approximation is. However, for a larger computational time increases drastically and the mixing of the chain, specially for ’s, is slower since w.p.1.

Posterior predictive distribution of can be easily obtained from (3), conditionally on the latent processes . If we re-express the latent processes in terms of random variables , where , such that then

| (6) |

Expression (6) provides an interesting interpretation of the updated mechanism of our construction. Posterior predictive distribution for is a weighted average of distributions and two sets of empirical distributions: coming from latent data for ; and coming from actual observed data . The weights are the precision , the sample sizes for , and . So, as in the posterior distribution of a DP, parameter is also interpreted as prior sample size.

Similarly to Blackwell and MacQueen, (1973) and Walker and Muliere, (2003), we can define the partially exchangeable sequence of observable variables with Pólya urns. The dependence mechanism induced by (2) assumes that each urn starts with a composition of balls , for and . Some of these starting balls are shared among urns and , according to whether is empty or not. Then the first draw is either a new ball coming from with probability or one of the balls in the urn with probability . In other words

The structure of the urn now changes adding the first ball . The second ball is either a new ball coming from , one of the starting balls or the first ball , that is

We add the already extracted balls to the urn. In general, for the ball we have

4 Illustration

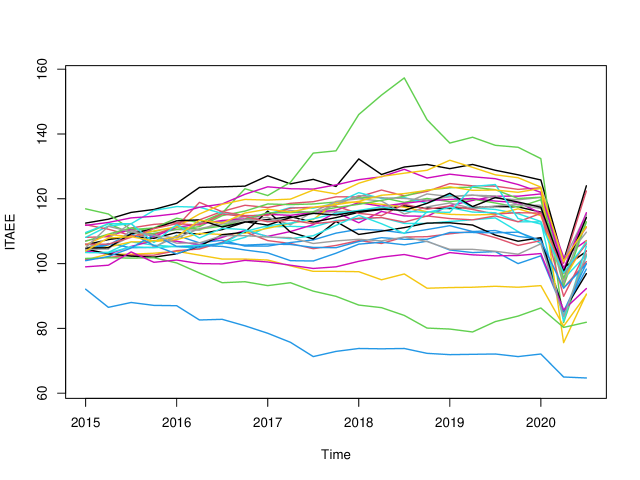

The Official Statistics Institute of Mexico constructs an economic activity index (ITAEE) for each of the 32 states of the country and it is reported every three months. The last report of this index (https://www.inegi.org.mx/temas/itaee/) consists in destationalized values, where seasonal peaks have been removed, of constant prices of the year 2013. For the purpose of our analysis we consider the indexes of the last six years available, that is, from the first trimester of year 2015 to the third trimester of year 2020. In total we have samples for of sizes , for with trimesters.

The data is reported in Figure 2. We can clearly see that in the second trimester of 2020 there is a drop for all states due to the Covid-19 pandemic. Previous to year 2020, the state of Baja California Sur (top green) showed its highest value in the third trimester of 2018. On the other hand, states like Campeche (bottom blue) and Tabasco (bottom green) showed a decreasing trend in its economy.

The objective of our analysis is to characterise the variability of the economy in the whole country. For that we use our model with order temporal dependencies such that the neighbouring sets are defined as . We took and with the standard normal cumulative distribution function. If we denote by and the sample minimum and maximum, respectively, then we took and . We defined a partition of size with and and . The dependence parameters were assumed constant across time. For and for the order of dependence we consider a range of different values to compare. In particular we took and .

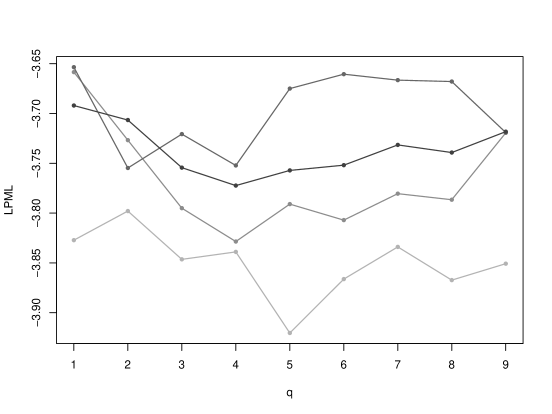

To choose among the different model specifications, we considered two statistics. The logarithm of the pseudo marginal likelihood (Geisser and Eddy,, 1979) defined as

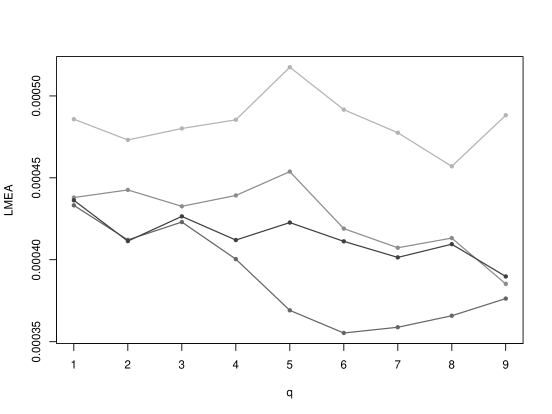

where is the Monte Carlo approximation of the conditional predictive ordinate and denotes the iteration. The second statistic is the L-measure (Ibrahim and Laud,, 1994) which is a summary between variance and bias of the predictive distribution. This is defined as

with .

We implemented a Gibbs sampler with the full conditional distributions described in Section 3. Sampling from (3) and (5) is straightforward since the finite dimensional distributions for and , conditionally on the other processes, become Dirichlet distributions. However, sampling from (4) requires the implementation of a Metropolis-Hastings step (Tierney,, 1994) and sampling each of the , one at a time, for and . This procedure induces highly autocorrelated chains. To overcome this effect we ran large chains with thinning. In particular we took 100,000 iterations with a burn-in of 5,000 and a thinning of one of every 25th iteration.

The goodness of fit statistics, LPML and LMEA for , for the different combinations of and are reported in Figure 3. We recall that higher LPML and smaller LMEA denote a better model. Considering LPML statistic, we note that for , the best model is obtained with , however, for , models with between 5 and 8 also obtain a high LPML. Considering now LMEA statistic, for a fixed the best model is obtained for . In particular, for the best model is that with , so combining both goodness of fit measures, we take this latter as our best model. Since the data are observations every three months, having a temporal dependence of order 6 means that the distribution of the economy in a given time depends on the economy of up to around one year and a half ago.

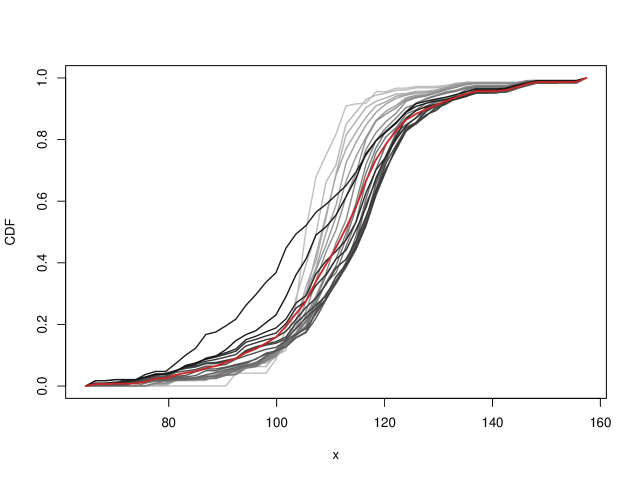

For the best fitting model we characterise posterior predictive distributions and report the posterior mean as point estimates for each of the ’s. These are included in Figure 4. In this graph we use darker colours to indicate larger (more recent) times. For early times (small ’s) the cumulative distribution functions (CDF) are more concentrated around the values of 110, whereas for more recent times (large ’s) the CDFs show more variability. In particular, there are two times that show a distinctive behaviour and assign larger probabilities to smaller values. These two correspond to the second and third trimester of 2020 where the Mexican economy was shaken by the Covid-19 pandemic.

Finally, we also show in Figure 4 in red colour, the posterior mean of the anchoring process . It can be interpreted as the overall mean behaviour of the Mexican economy in the period of study.

5 Discussion

We have introduced a collection of dependent Dirichlet processes via a hierarchical model. Three levels were needed to ensure that the marginal distribution for each element is a Dirichlet process. Temporal, spatial or temporal-spatial dependencies are possible. Other types of dependencies, like circular dependencies mentioned at the end of Section 2, are also possible.

Posterior inference of the collection of processes is possible when used as Bayesian nonparametric prior distributions. This requires an easy to implement Gibbs sampler.

One of the common uses of Dirichlet processes is to define mixtures for model based clustering, exploiting the discreteness of the Dirichlet process. We can also use our for that purpose. Say , with a probability density, then and for and . Clusters obtained for each time will be dependent, according to the chosen definition of the neighbouring sets . Studying the performance of this mixture model is worthy, but it is left for future work.

Acknowledgements

The author acknowledges support from Asociación Mexicana de Cultura, A.C.

References

- Ascolani et al., (2021) Ascolani, F., Lijoi, A. and Ruggiero, M. (2021). Predictive inference with Fleming-Viot-driven dependent Dirichlet processes. Bayesian Analysis 16, 371-395.

- Blackwell and MacQueen, (1973) Blackwell, D. and MacQueen, J.B. (1973). Ferguson distributions via pólya urn schemes. Annals of Statistics 1, 353-355.

- (3) Camerlenghi, F., Dunson, D.B., Lijoi, A., Prünster, I. and Rodriguez, A. (2019a) Latent nested nonparametric priors (with discussion). Bayesian Analysis 14, 1303–1356.

- (4) Camerlenghi, F., Lijoi, A., Orbanz, P. and Prünster, I. (2019b). Distribution theory for hierarchical processes. Annals of Statistics 47, 67–92.

- Caron et al., (2007) Caron, F., Davy, M. and Doucet, A. (2007). generalized Pólya urn for time-varying Dirichlet process mixtures. Proceedings of the 23rd Conference on Uncertainty in Artificial Intelligence, Vancouver.

- de Finetti, (1972) de Finetti, B. (1972). Probability, induction and statistics. Wiley, New York.

- Ferguson, (1973) Ferguson, T.S. (1973). A Bayesian analysis of some nonparametric problems. Annals of Statistics 1, 209–230.

- Ferguson, (1974) Ferguson, T.S. (1974). Prior distributions on spaces of probability measures. Annals of Statistics 2, 615–629.

- Geisser and Eddy, (1979) Geisser, S. and Eddy, W.F. (1979). A predictive approach to model selection. Journal of the American Statistical Association 74, 153–160.

- Griffin et al., (2013) Griffin, J.E., Kolossiatis, M. and Steel M.F.J. (2013). Comparing distributions by using dependent normalized random-measure mixtures. Journal of the Royal Statistical Society, Series B 75, 499–529.

- Ibrahim and Laud, (1994) Ibrahim, J. and Laud, P. (1994). A predictive approach to the analysis of designed experiments. Journal of the American Statistical Association 89, 309–319.

- (12) Lijoi, A., Nipoti, B. and Prünster, I. (2014a). Bayesian inference with dependent normalized completely random measures. Bernoulli 20, 1260–1291.

- (13) Lijoi, A., Nipoti, B. and Prünster, I. (2014b). Dependent mixture models: clustering and borrowing information. Computational Statistics and Data Analysis 71, 417–433.

- MacEachern, (1999) MacEachern, S. (1999). Dependent nonparametric processes. Technical Report. Department of Statistics, The Ohio State University, Ohio.

- Müller et al., (2004) Müller, P., Quintana, F. and Rosner, G. (2004). A method for combining inference across related nonparametric Bayesian models. Journal of the Royal Statistical Society, Series B 66, 735–749.

- Nieto-Barajas, (2020) Nieto-Barajas, L.E. (2020). Bayesian regression with spatiotemporal varying coefficients. Biometrical Journal 62, 1245–1263.

- Papaspiliopoulos, (2016) Papaspiliopoulos, O., Ruggiero, M. and Spanó, D. (2016). Conjugacy properties of time-evolving Dirichlet and gamma random measures. Electronic Journal of Statistics 10, 3452–3489.

- Quintana et al., (2020) Quintana, F., Müller, P., Jara, A. and MacEachern, S.N. (2020). The dependent Dirichlet process and related models. arXiv: 2007.06129.

- Regazzini et al., (2003) Regazzini, E., Lijoi, A. and Prünster, I. (2003). Distributional results for means of normalized random measures with independent increments. Annals of Statistics 31, 560–585.

- Rodríguez et al., (2010) Rodríguez, A., Dunson, D.B. and Gelfand, A.E. (2010). Latent stick-breaking processes. Journal of the American Statistical Association 105, 647–659.

- Sethuraman, (1994) Sethuraman, J. (1994). A constructive definition of Dirichlet prior. Statistica Sinica 2, 639–650.

- Smith and Roberts, (1993) Smith, A. and Roberts, G. (1993). Bayesian computations via the Gibbs sampler and related Markov chain Monte Carlo methods. Journal of the Royal Statistical Society, Series B 55, 3–23.

- Teh et al., (2006) Teh, Y.W., Jordan, M.I., Beal, M.J. and Blei, D.M. (2006). Hierarchical Dirichlet processes. Journal of the American Statistical Association 101, 1566–1581.

- Tierney, (1994) Tierney, L. (1994). Markov chains for exploring posterior distributions. Annals of Statistics 22, 1701–1762.

- Walker and Muliere, (2003) Walker, S. and Muliere, P. (2003). Bivariate Dirichlet process. Statistics and Probability Letters 64, 1–7.